Abstract

In this systematic literature review, we evaluate the effectiveness of financial-literacy education programs and interventions for children and adolescents. Furthermore, the key characteristics of the design of a successful financial-education curriculum are described. The evidence shows that school-based financial-education programs can improve children’s and adolescents’ financial knowledge and attitudes. Studies that assess the intention to practice good behavior and studies based on self-reported behavior also report positive effects. However, studies that assess the effects of financial education on children’s and adolescent’s actual financial behavior are scarce, and show hardly any effect. A promising method to teach financial literacy to children and adolescents in primary and secondary school is “experiential learning.” In college, the focus should be on specific “life events” of students. The findings may be useful for designing an effective school-based financial education program.

Background

In an increasingly complex society, financial literacy is widely seen as essential, and therefore as an indispensable part of education (Organisation for Economic Co-operation and Development (OECD), 2014). This is in line with the development of educational curricula that focus on the development of active citizenship. Citizenship implies independence, freedom and responsibility, including in financial matters. Therefore, “economic citizenship” is an important aspect of citizenship that, so far, has not received much attention in citizenship education curricula. Children and adolescents can only realize their full potential as citizens if they are financially empowered and capable; the buildings blocks in this respect are financial education, social education, and financial inclusion (CYFI, 2013).

Hastings et al. (2013) associate low financial literacy with negative credit behaviors such as debt accumulation, high-cost borrowing, poor mortgage choice, mortgage delinquency, and home foreclosure. A recent study shows that about one in six households in a developed economy like the Netherlands either have problematic debts or run a high risk of developing such debts (Kerckhaert and de Ruig, 2013). According to Van Dam et al. (2014), the economic crisis has played a role in the growth of the debt problem. However, it is increasingly recognized that irresponsible financial behavior and poor financial skills are major causes of the emergence of debts, not only among adults, but also among youngsters, who are a particularly vulnerable group. To cite another example from the Netherlands: the proportion of adolescents under 26 who are in debt and requesting debt counseling has been growing from 9 percent in 2008 to 15 percent in 2013 (Madern, 2014), while 42% of 18- to 24-year-olds have at least one form of debt, loan or payment arrears. However, only 28% of 18- to 24-year-olds with payment arrears are aware of the fact that they have a financial problem (Van der Schors and Van der Werf, 2014). Financial debts create substantial costs and loss of well-being, not only for the debtors, but also for society as a whole. Although not all debts are problematic (e.g. students loan debt create possibilities for future careers), many debts can be detrimental to society, for example, direct losses of income by banks, insurance companies or public service corporations, and increased spending on social security, as well as indirect costs caused by, for example, increased illness absence, drug addiction and child neglect in debtors households (Madern, 2014).

Financial literacy can be seen as an investment in human capital, and can be helpful in the context of decisions about pension, savings, mortgage, and other financial decisions (Lusardi and Mitchell, 2014). Today’s young people are growing up in a society in which the financial landscape is complex and the financial responsibilities of citizens are substantial. Financial education in schools may help to meet these challenges. This raises the question, “What effective educational approaches could improve the level of financial literacy?”

In the literature, the term “financial literacy” has commonly been used for knowledge of financial concepts and procedures, whereas “financial capability” has been utilized to indicate the skills to apply this knowledge, and “financial inclusion” to indicate the opportunity to do so. The OECD (2014) combines these three aspects in one unitary concept of financial literacy:

knowledge and understanding of financial concepts and risks, and the skills, motivation and confidence to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, to improve the financial well-being of individuals and society, and to enable participation in economic life. (p. 33)

Financial literacy defined in this way refers to ways in which individuals understand, manage, and plan their personal finances. The core of the domain of financial literacy is personal finances that can support financial well-being: a situation in which personal finances are a means to achieve and maintain a desired standard of living.

Financial education can be defined as teaching which is intended to lead to financial literacy in the wider sense indicated by the OECD (2014). The ultimate goal of financial education is to empower and motivate people to change their financial behavior, for example, to induce them to make well-considered financial decisions. Therefore, we distinguish three components in our definition of financial literacy:

Knowledge and understanding. To know how to behave, it is necessary to be informed adequately about the domain referring to the intended behavior. However, the effect of knowledge on changes in behavior is relatively limited (Hilgert et al., 2003; Perry and Morris, 2005). Therefore, two other aspects must be taken into account.

Skills and behavior. To be able to change one’s behavior, it is necessary to master the operational skills which refer to the domain, for example, how to deal with budgeting.

Attitudes and confidence. To be able to apply something outside the context in which it has been learnt, it is necessary to have self-efficacy (Bandura, 1997, 2006), and develop the necessary motivation in order to do so.

In sum, our definition comprises knowing what to do, the skills to be able to perform these actions, and the inclination to carry them out.

In this study, we look at interventions aimed at developing financial literacy among children and adolescents. Our review addresses the following question, “To what extent can financial education in schools improve the financial literacy of children and adolescents and enhance their capabilities as economic citizens?” The objectives of this review are as follows: (1) to describe the extent to which the empirical literature provides evidence on the effectiveness of financial education programs for children and adolescents and (2) to describe the key characteristics of the pedagogical design of successful financial education programs.

Recently, two peer-reviewed literature reviews have been published that primarily focus on promoting financial literacy of children and adolescents by means of financial education (McCormick, 2009; Totenhagen et al., 2015). Other reviews focus primarily on financial education among adults (Fox et al., 2005; Gale and Levine, 2011; Hastings et al., 2013; Hathaway and Khatiwada, 2008). A meta-analysis of the studies among adults and adolescents has been performed by Miller et al. (2014) and Fernandes et al. (2014). To date, review of the effects of programs that are exclusively aimed at children and adolescents and at all the components of our definition of financial literacy is lacking now. The current study attempts to fill this gap, as it examines the international evidence about the pedagogical design characteristics of effective financial education programs.

Method

Literature search strategy

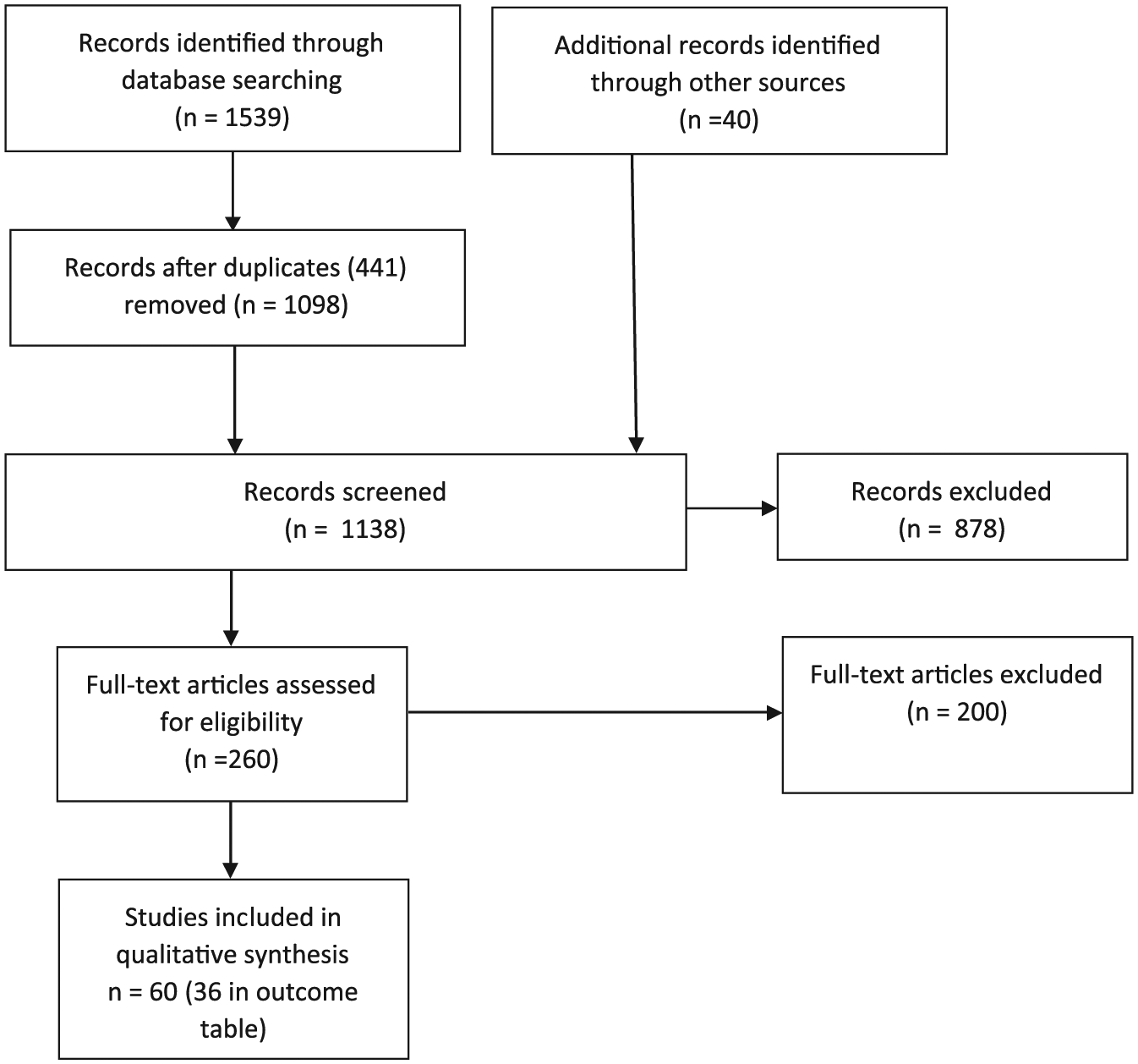

To be thorough in the reporting of our systematic review, we used the checklist and the flow chart from Prisma (Moher et al., 2009) shown in Figure 1. We undertook an exhaustive search of the literature on financial literacy and financial education programs or interventions in schools which involved children and adolescents. The first step comprised a database search in ERIC, Business Source Premier, Econlit and Web of Science, using different combinations of the following keywords: financial-literacy education, financial education in schools, financial education for youth, and personal finance at school. In the second step, to counteract the effect of inadequate choice of keywords, we searched the contents of the last five volumes of the Journal of Economic Education and the International Review of Economic Education, and searched the reference lists in McCormick (2009), Miller et al. (2014), and Totenhagen et al. (2015) for relevant studies (i.e. the snowball method). This hand search did not result into any additional studies next to the ones already identified in the database search. Finally, we consulted experts on the OECD/INFE Conference on Financial Resilience. 1

Flow chart.

Selection criteria

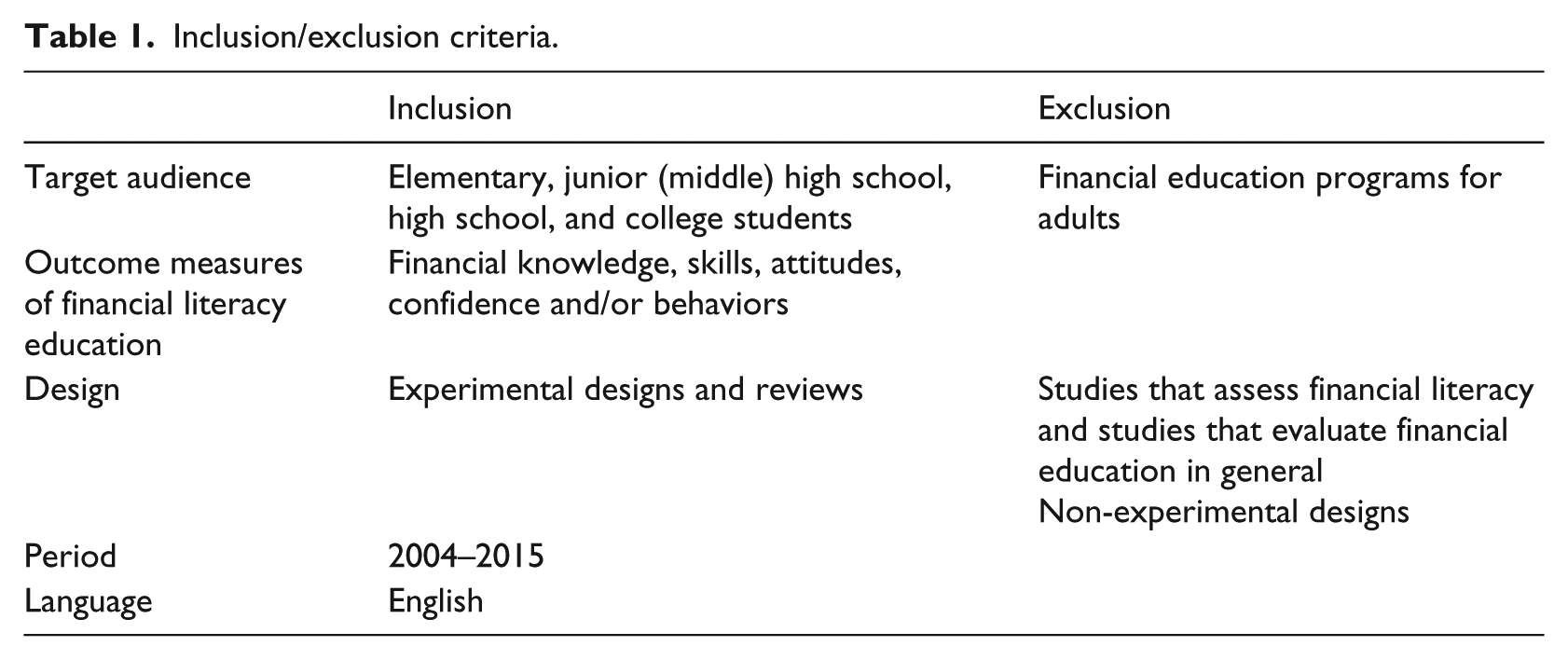

The evidence on the impact of financial education on knowledge, attitudes, confidence and behavior among children and adolescents is relatively limited and recent. The majority of the studies were published less than 10 years ago. In this review, we cover the research published between 2004 and 2015, with a special focus on studies that evaluate programs in elementary schools, junior high schools and high schools. Furthermore, we include programs which aimed to increase the financial literacy of college students during their first year of college. According to Shim et al. (2010), this period constitutes an especially important transitional stage of development because most college students are not yet financially independent but are actively learning the skills needed to develop toward independence. We only include those studies that provide information about specific financial education programs. We therefore exclude studies that evaluate the overall effectiveness of financial education in general. Furthermore, we do not include studies that only assess financial literacy without testing the effects of educational programs or interventions, because we are interested in the effectivity of financial education programs, not in the general level of financial literacy among the population. In Table 1, the inclusion/exclusion criteria are presented.

Inclusion/exclusion criteria.

We focus primarily on peer-reviewed studies. Discussion papers, working papers, and research reports were included only if they met our quality standards. As shown in Figure 1, we initially screened 1138 articles, of which 878 articles were excluded in view of their titles and abstracts, using the inclusion and exclusion criteria shown in Table 1. We assessed both the abstracts and the full texts of 260 articles for eligibility. This resulted in a total of 60 articles being included in the review. Of these, 36 articles describe the effects of financial education by means of empirical data. Of the papers that used the same data set, we only included the papers that presented the most complete data. We analyzed each study by using the following characteristics: sample size, target audience, research design, content of the intervention, length of the intervention, outcomes of the programs, gender differences, and pedagogical characteristics of the program. We also checked the effect sizes (Cohen’s d) in studies that used a control group. If the authors did not, or could not, provide the required statistics to calculate the effect size (in some cases, we have asked authors for extra data beyond those that were reported in their articles in order to be able to calculate effect sizes ourselves), we only registered whether there was a statistically significant effect.

Contents of school-based financial-literacy education programs

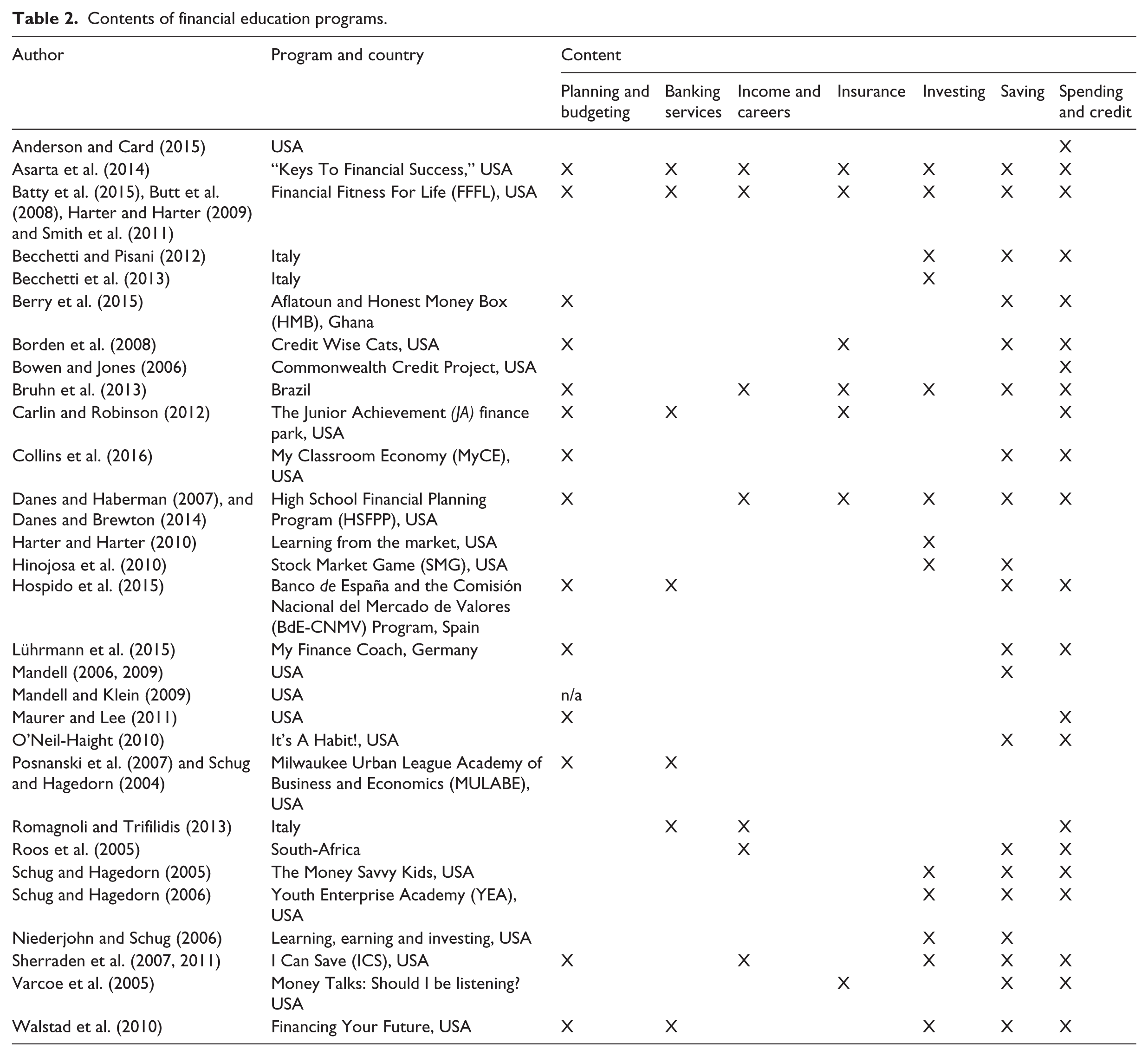

As shown in Table 2, knowledge and understanding of planning and budgeting, earning an income and careers, saving and investing, spending and credit, and insurance and banking services are the core elements of financial education programs across different educational levels. Financial education programs in elementary schools primarily focus on planning and budgeting, saving, spending, and credit concepts. A few programs look at concepts regarding investment and banking services. In secondary schools, the majority of the financial education programs aim at spending and credit, saving and investment, and budgeting concepts. A few programs look at banking services, insurance, income, and careers. Financial education programs in college focus mainly on issues regarding budgeting, credit card use, and compulsive spending decisions. The financial education programs in this review revealed no fundamental differences in concepts across countries.

Contents of financial education programs.

Skills or (meta) cognitive strategies are necessary to gain and apply financial knowledge, in order to effectively manage one’s finances. Our review of the material on different financial education programs yielded four categories. The first category is concerned with making thoughtful, well-informed financial decisions both in the long and short run (Asarta et al., 2014; Batty et al., 2015; Bruhn et al., 2013; Butt et al., 2008; Collins et al., 2016; Danes and Brewton, 2014; Danes and Haberman, 2007; Harter and Harter, 2009; Hospido et al., 2015; Lührmann et al., 2015; Smith et al., 2011). To ensure students’ financial well-being, it is necessary to build up attitudes, optimism, self-confidence, and perseverance in financial decision making (Bruhn et al., 2013; Danes et al., 2007, 2014). As an example, The Council for Economic Education’s Financial Fitness For Life (FFFL) curriculum aims at helping students make thoughtful, well-informed decisions by using the “economic way of thinking” (Batty et al., 2015; Butt et al., 2008; Harter and Harter, 2009; Smith et al., 2011). To help students be confident about their future and form positive expectations for the future, the FFFL material is oriented toward the future. The FFFL curriculum also aims at developing strategies to accomplish good habits and practical skills that pay off in both the short and long run. The content of this curriculum is based on national and state standards regarding economics, personal finance, mathematics, and language arts. The instructional materials have been adapted to different age groups ranging from Kindergarten to Grade 12. One of the strong points of the FFFL program is that valid tests have been developed to measure students’ knowledge and understanding of personal finance concepts. The FFFL test does not assess financial attitudes and behavior. Another example is a program in Brazil that aims to help students make responsible financial choices and the capacity to plan finances, which involves long-term budgeting, cost-benefit analyses, financial prudence, and spending discipline (Bruhn et al., 2013). “My Finance Coach,” a German program, aims at consumption and (intertemporal) planning, and savings and investment choices (Lührmann et al., 2015).

The second category aims to reinforce student’s transferable skills. Cormier and Hagman (1987) indicate that such transfer takes place when prior learned knowledge and skills affect the way in which new knowledge and skills are learned and performed. A competency-based curriculum (High School Financial Planning Program) for Grades 8–12 is one of the few programs that aims at building students’ confidence to make well-considered financial decisions, as well as developing their transferable skills (Danes et al., 2007, 2014).

The third category concerns investing in one’s own human capital, specifically by teaching students how to earn, manage, and save money, and build aspirations and expectations for post-secondary education and training (Berry et al., 2015; Schug and Hagedorn, 2006; Sherraden et al., 2007, 2011; Varcoe et al., 2005; Walstad et al., 2010). Programs like the “Aflatoun Program” and “Honest Money Box” (HMB) that, among other things, are concerned with investing in one’s own human capital are especially important for underdeveloped countries where children and their parents often do not have access to financial services. The “Aflatoun Program”, which bears the name of the ancient Greek philosopher Plato in Arabic, combines a savings program with social education components for children aged 3–18 years executed in 116 countries. “Aflatoun” focusses on personal exploration and children’s rights and responsibilities, while also highlighting the pitfalls of child labor, such as forgoing school to work and the risk of dangerous working conditions. The HMB curriculum strictly aims at financial education. Both “Aflatoun” and HMB continue as savings clubs after completion of the curriculum (Berry et al., 2015). Finally, the fourth category is concerned with problem-solving skills. Programs like the FFFL (Batty et al., 2015; Butt et al., 2008; Harter and Harter, 2009; Smith et al., 2011), Aflatoun (Berry et al., 2015) and the Milwaukee Urban League Academy of Business and Economics (MULABE) highlight this skill. MULABE schools offer a customized economic and personal finance curriculum (about one-third of the school curriculum) with the aim of teaching students basic skills such as banking, personal budgeting, and problem-solving, as well as more advanced business and finance skills (Posnanski et al., 2007; Schug and Hagedorn, 2004).

Effectiveness of school-based financial-literacy education programs

Studies which assess the outcomes of financial-literacy education may report effects on financial knowledge, financial behavior, attitudes, and/or confidence. The majority of studies in our review cover multiple outcomes, others concentrate on either financial knowledge or financial behavior. To our knowledge, there are no studies which exclusively assess attitudes or confidence; these outcomes are only assessed in relation to financial knowledge or financial behavior. Studies which assess financial knowledge mostly use a personal finance test about knowledge and understanding, besides self-reported-data. Studies which assess financial behavior can be split up into three categories. The first category comprises studies which assess behavior based on self-reported data. The second category investigates assessed behavior (actual), mostly savings behavior. The third category assesses the intention to deploy good financial behavior.

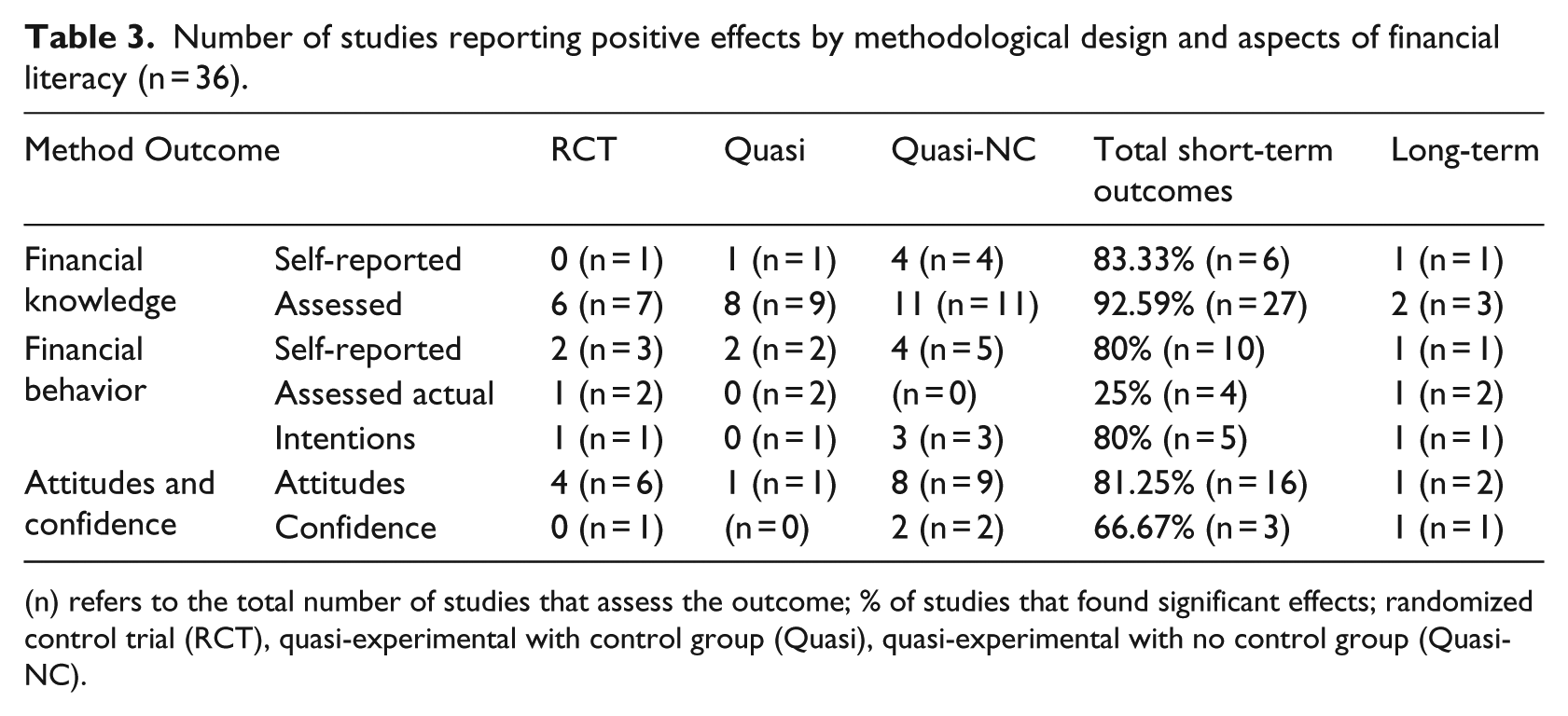

As shown in Table 3, the majority of experimental studies in primary schools, secondary schools and colleges (27 out of 36) assesses financial knowledge with the help of a personal finance test, of which 25 found short-term positive effects. From the seven studies using randomized control groups and nine using a quasi-experimental design, all but one in each category found positive knowledge effects. Five out of six studies that are based on self-reported knowledge report positive effects. Five studies assess the intention to practice sound financial behavior, of which four report positive effects. Ten studies assess self-reported behavior, of which eight found positive effects. Studies assessing behavior (mostly savings) are scarce (n = 4), and show hardly any effects (one out of four). In 16 out of 36 studies, financial attitudes are dealt with besides other outcomes, of which 13 found positive effects. Only three out of 36 studies focus on confidence in combination with other outcomes. A few studies (n = 3) assess the long-term effects (after 1 year, 1.5 years, or 5 years) of financial education programs with a specific curriculum. The effects of these programs on knowledge and behavior are mixed (Batty et al., 2015; Bruhn et al., 2013; Mandell, 2009).

Number of studies reporting positive effects by methodological design and aspects of financial literacy (n = 36).

(n) refers to the total number of studies that assess the outcome; % of studies that found significant effects; randomized control trial (RCT), quasi-experimental with control group (Quasi), quasi-experimental with no control group (Quasi-NC).

Describing the extent to which the literature provides evidence on the effectiveness of financial education programs is challenging because programs differ in many ways making a comparison almost impossible. We tried to overcome this problem by focusing on whether the participants achieved the intended learning outcomes (knowledge, behavior, and attitude). In the next section, we present a further elaboration of the effects of school-based financial education interventions and programs for children and adolescents at different educational levels. In each section, we distinguish studies using the three components of our definition of financial literacy: financial knowledge, financial behavior, and financial attitudes or confidence.

Effectiveness of school-based financial-literacy education programs in primary schools

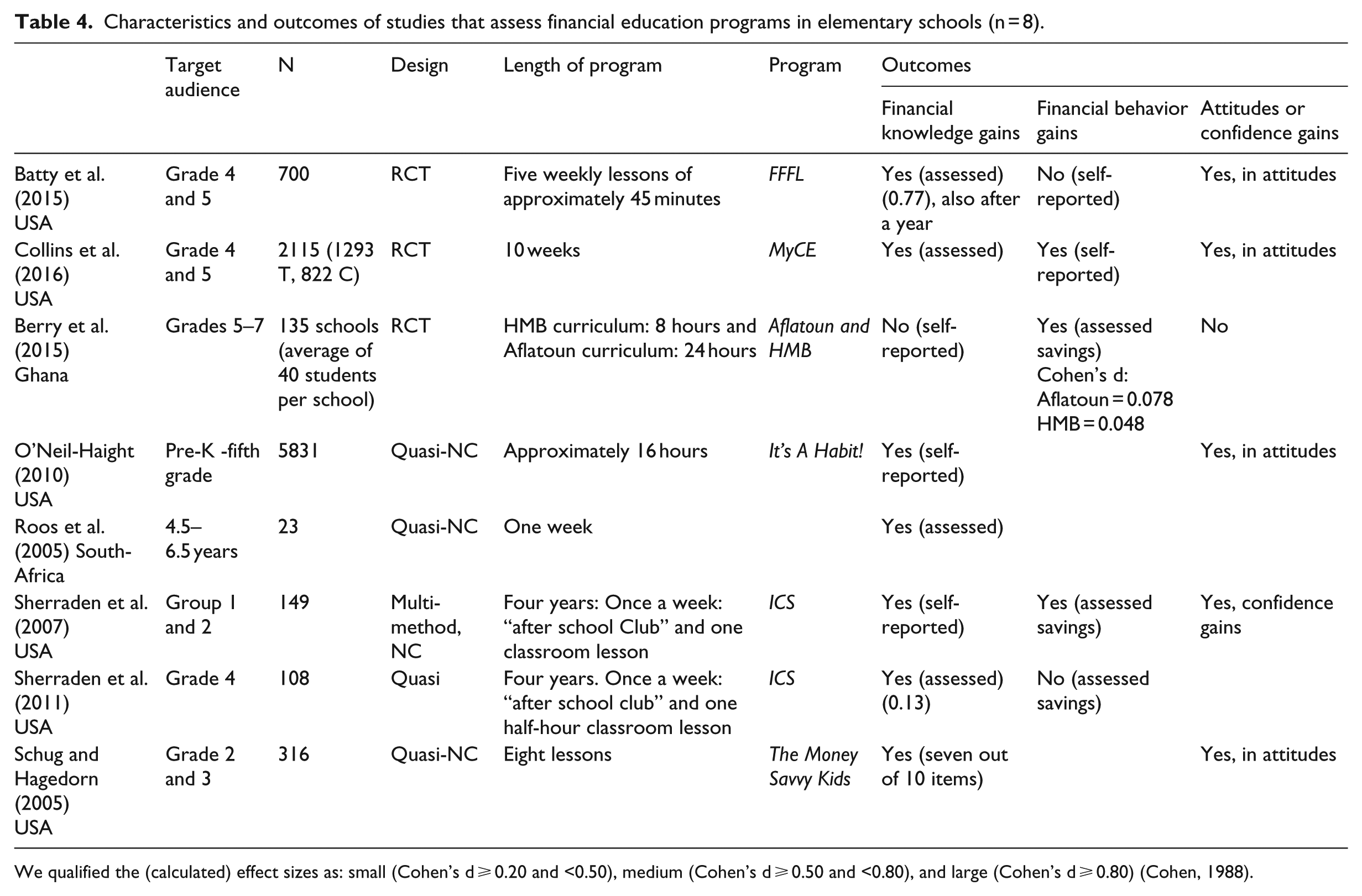

In Table 4, we present a summary of the effects of eight financial education programs in primary schools. These programs mainly found positive effects on financial knowledge and attitudes. The length of the intervention varies from 1 week to 4 years. With the data available, we cannot conclude that longer intervention periods result in better performances in children’s financial knowledge and attitudes. Furthermore, we see no major differences between programs that are integrated into existing curricula (Batty et al., 2015; Collins et al., 2016; O’Neil-Haight, 2010; Roos et al., 2005) and stand-alone classes (Schug and Hagedorn, 2005; Sherraden et al., 2007, 2011), with the exception of Berry et al. (2015), who found no gains in financial knowledge and attitudes. If we look at the four studies which have a control group, three reported a significant effect in financial knowledge and attitudes. The two effect sizes reported vary between no effect (0.13) and large effect (0.77). Conclusions about the effects of financial education on savings behavior are difficult to make, because the results are diverse in this respect. This may be due to the differences in how savings behavior is measured. For example, Berry et al. (2015) measured actual savings behavior through a locked savings box and Sherraden et al. (2007, 2011) measured savings behavior through data that is collected during the ICS club. Self-reported savings behavior is measured by general questions like “If you have a savings account, about how much money do you think is currently in the account?” (Batty et al., 2015).

Characteristics and outcomes of studies that assess financial education programs in elementary schools (n = 8).

We qualified the (calculated) effect sizes as: small (Cohen’s d ⩾ 0.20 and <0.50), medium (Cohen’s d ⩾ 0.50 and <0.80), and large (Cohen’s d ⩾ 0.80) (Cohen, 1988).

Effectiveness of school-based financial-literacy education programs in secondary schools

As shown in Table 5, the majority of experimental studies (20 out of 24) used a personal finance test to assess the impact of financial education programs in secondary schools on students’ knowledge and understanding of concepts. With the exception of Lührmann et al. (2015) and Becchetti et al. (2013), all of the studies found positive effects in assessed financial knowledge. The effects are similar in those studies that used a comparison group; 11 out of 13 found positive effects. All of the studies in this literature review that assessed self-reported financial knowledge found positive effects (Danes and Brewton, 2014; Danes and Haberman, 2007; Lührmann et al., 2015; Varcoe et al., 2005).

Characteristics and outcomes of studies that assess financial education programs in secondary schools (n = 24).

On the other hand, studies that assess student’s financial knowledge differ in effect sizes. Factors that possibly influence these outcomes are the program design and gender. As an example, studies which assess the impact of the FFFL curriculum on students’ knowledge and understanding of personal finance concepts all found positive effects (Butt et al., 2008; Harter and Harter, 2009; Smith et al., 2011). The effect sizes in a study that used a shorter intervention (8 lessons) to teach the FFFL curriculum were small (d = 0.221; 0.267) (Harter and Harter, 2009) compared with a study by Butt et al. (2008) who assessed 17 lessons from the FFFL curriculum and showed a moderate positive effect in year 1 (d = 0.505) and year 2 (d = 0.561). Hospido et al. (2015), who assessed a short financial education program in Spain of 10 hours, showed a small effect size of 0.286, an improvement of one-third of a standard deviation in students’ financial knowledge. These outcomes possible indicate that a longer intervention may lead to larger effects. In contrast, an intensive program in Brazil (between 72 and 144 hours in 1.5 years) resulted into a significant but small improvement of students’ knowledge levels (d = 0.25). The MULABE program, which is also long and intensive, resulted in considerable effects on basic economic knowledge (d = 0.981) and personal finance (d = 1.020) (Schug and Hagedorn, 2004). These results show that financial education when delivered over a significant period of time can be effective. No overall conclusions can be drawn about the relationship between the length of the intervention and the effect size; the results are equivocal. Furthermore, we see no major differences in results between stand-alone programs and programs that are integrated into existing curricula. On the other hand, we do see differences in effect sizes of playing the Stock Market Game, with or without content lessons: small effects in students’ financial knowledge without lessons, ranging from 0.39 to 0.45 (Hinojosa et al., 2010), and a larger effect (d = 0.79) when combined with seven content lessons (Harter and Harter, 2010).

As shown in Table 5, in 10 out of 24 studies, financial attitudes are dealt with together with other outcomes, of which seven found significant positive effects (Bruhn et al., 2013; Danes and Haberman, 2007; Lührmann et al., 2015; Mandell, 2006, 2009; Niederjohn and Schug, 2006). Becchetti et al. (2013) reported no significant effects in investment attitudes, and Smith et al. (2011) found no effects in students’ attitudes to the future. Studies that used a control group found similar effects in financial attitudes; four out of nine studies used a control group, of which three found positive effects. Only one study reported an effect size (d = 0.166).

Studies on the impact of financial education programs on student’s financial behavior show diverse results. One out of two studies found positive effects in the intention to save, and five out of six studies found positive effects in self-reported behavior. On the contrary, no effects were found in assessed financial behavior (n = 2).

A few studies assess the long-term effects of specific financial education programs. Bruhn et al. (2013) looked at the long-term impact of the program, 18 months after the start of the program, and found small effects in knowledge (d = 0.20), behavior (self-reported and intentions) and attitudes. On the other hand, Mandell (2009), who performed a longitudinal study, found no lasting effects on students’ knowledge, savings behavior, and attitudes toward savings or “thrift” in the post-high school years. Non-experimental studies that identify the effects of state-mandated or optional personal finance programs in high school on later behavior as an adult have found mixed evidence (Bernheim et al., 2001; Cole et al., 2015; Peng et al., 2007).

A few studies report gender differences among adolescents in all three dimensions of financial literacy. Danes and Haberman (2007) showed that the scores for both genders increased after the study (HSFPP) of several concepts, but males outperformed females. Because of the program, female teens learned significantly more about finances in areas with which they were unfamiliar prior to the program than the males. Furthermore, male teens were confident about making money decisions, and their confidence scores remained higher than those of female teens after the completion of the program. By contrast, female teens increased their confidence about making financial decisions to a larger degree than males. Female teens were also more likely to believe that managing money affected their future before completing the program, and this difference continued to exist after completion. Looking at the behavior outcome, males reported achieving financial goals better than females, whereas females reported using budgets, comparing prices, and discussing money matters with family more than males. Danes and Brewton (2014) add that female students who did not grow up in a farming family business and were not employed acquired most (self-reported) knowledge from the HSFPP. Females reported that they gained in three types of financial behavior compared with males: protecting personal information from being stolen, making savings goals, and tracking spending. Lührmann et al. (2015) report that in the pre-test, girls showed lower interest in financial matters, lower self-reported knowledge, and were less likely to save. Furthermore, in the post-test, they found no evidence that girls are affected by financial education training any differently from boys, with the exception that self-reported knowledge increased less for girls than boys. Other studies of financial education programs have reported gender differences in financial knowledge. Romagnoli and Trifilidis (2013) showed that in the pre-test, boys had slightly higher levels of financial knowledge than girls in primary and junior high school. However, after the financial education training, the gender gap was significant only among junior high school students, and girls outperformed boys. Becchetti et al. (2013) found a lower level of financial knowledge among girls in the pre-test, but, after the training, girls had a greater level of progress compared with boys. Mandell (2006) however, found that females had more knowledge in the pre-test and learned more from the intervention (seeing a play about savings) than males did. Varcoe et al. (2005) showed that males significantly had a greater increase in financial knowledge after completing the financial education program. Females reported talking to their families about money matters more often than males, but the extent of talking to their families about money did not change significantly after completing the program. These gender differences in financial literacy levels between studies may be due to the context in which the study is conducted. Cultural differences between countries’ can affect the financial literacy levels.

With the exception of Mandell (2006), all of the studies reviewed above indicate that at pre-test, the financial literacy levels are low for adolescent females, and that financial education programs can reduce the gender gap.

Effectiveness of school-based financial-literacy education programs in college

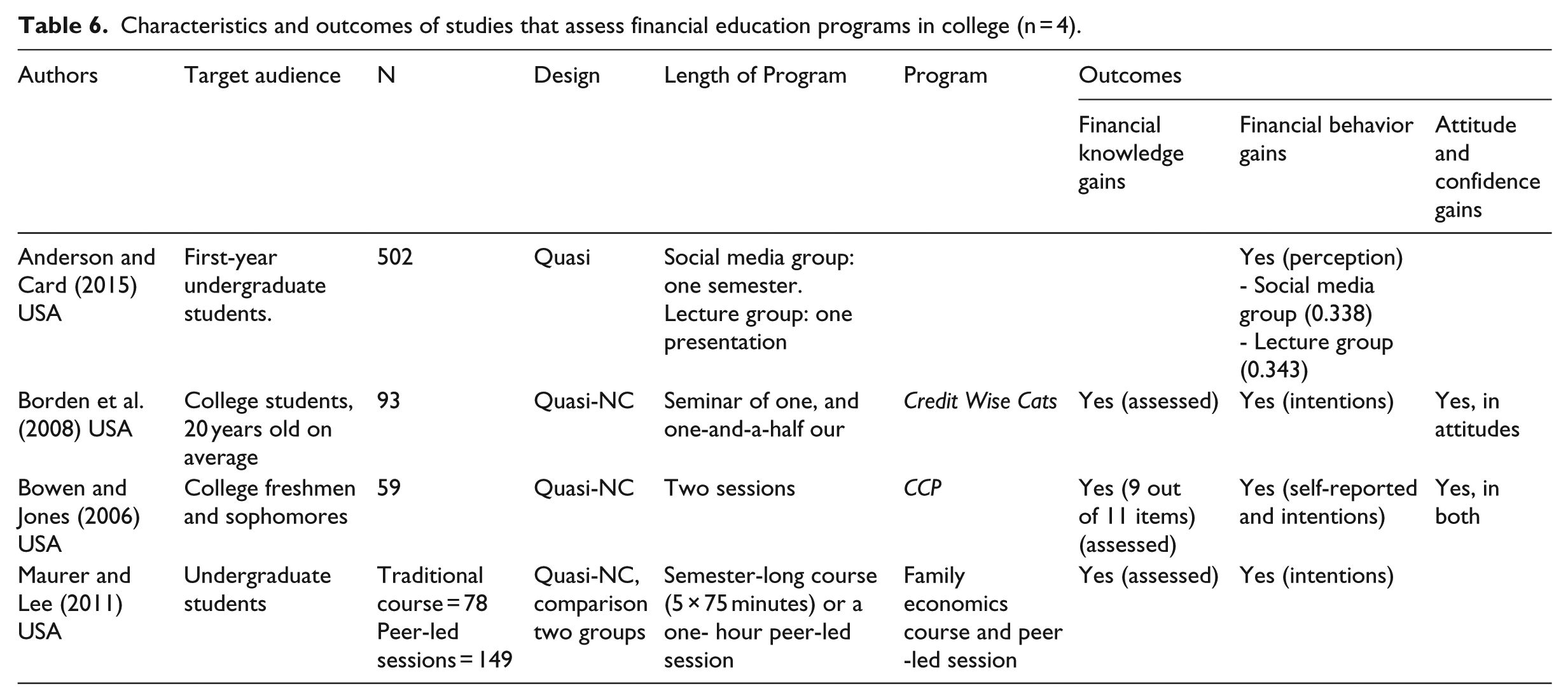

As shown in Table 6, financial education programs in college (n = 4) all showed positive effects on students’ understanding of concepts, and on their intention to engage in responsible credit card use, better budgeting, and fewer compulsive spending decisions, as well as developing more positive attitudes in these respects. If we look at the effect sizes, Anderson and Card (2015) show small effects in student’s self-perceived financial behavior (0.338; 0.343). Furthermore, conclusions about assessed actual behavior of college students must be made with caution, because the studies use only self-reported data about intention and attitudes to engage in effective financial behavior. Furthermore, the studies use mainly small non-randomized groups with no control groups.

Characteristics and outcomes of studies that assess financial education programs in college (n = 4).

In college, there also seems to be a gender gap in attitudes and spending behavior, in favor of males. In the study of Anderson and Card (2015), there is an indication that women in the pre-test may have a higher propensity to compulsively spend than men. Financial education for first-year college students has an effect on students’ perception of their financial behavior regarding compulsive spending decisions.

The design of a financial-education program: What is effective?

A variety of methods and materials are being used in different financial education programs around the world. There is a shift from a traditional subject-matter-based approach to a skills-based approach, in which the student learns the skills by doing, as opposed to the “chalk and talk” model in which the student is often passive. In this section, we describe what are the most effective pedagogical methods of teaching financial literacy in primary school, secondary school, and college. In the description, we primarily focus on programs that report the effect sizes.

In primary schools, several effective financial education programs have integrated “experiential learning” in their curriculum (Batty et al., 2015; Collins et al., 2016; Roos et al., 2005). An example of this approach is My Classroom Economy (MyCE) where students actively participate in a “simulated micro-economy” in which students earn “school dollars” that they can use to rent their own desks. In this way, students experience the impact of their decisions without their teachers teaching specific financial content. Collins et al. (2016) evaluated MyCE and found that students who participated in the MyCE had 6% higher scores in financial knowledge than the control group. Another program that uses hands-on activities to reinforce students’ understanding through application and practice, and addresses concepts in a developmental appropriate manner is the FFFL curriculum. The FFFL material uses various teaching methods like role playing, group discussions, gathering information from the Internet, reading materials, interviewing individuals, drawing pictures, and analyzing case problems. Furthermore, the FFFL materials are complemented with a parent guide for each grade level, with activities that reinforce and extend children’s understanding in personal finance. Batty et al. (2015) who assessed the FFFL curriculum found students significantly gained large positive effects (gain of 11%) in financial knowledge (d = 0.77), even after a year. This is more than the study of Collins et al. (2016), but MyCE is imbedded in other classroom activities, and therefore requires no formal instruction time. Harter and Harter (2009) who also assessed the FFFL curriculum found moderate effects of 0.555. This suggests that “experiential learning” with a variety of teaching methods yields the largest effects in the increase of students’ financial knowledge. A form of “experiential learning” that is effective in increasing students’ financial knowledge, but with a negligible effect (d = 0.13) is the school-based savings programs (Sherraden et al., 2011). In a school-based financial education and savings program, “ICS,” children have an opportunity to apply what they are learning in a real world setting. The lessons could be relevant and motivating, which in turn can lead to a better understanding of personal finance and decision making (Sherraden et al., 2007, 2011).

Financial education programs in secondary schools also have elements of “experiential learning,” with an emphasis on the “relevance of the topic” in order to motivate students. Mandell and Klein (2009) indicate that the design of a financial education program should take into account the provision of interactive teaching methods, from visual lessons to (simulation) games, in which students actively participate in the learning process. The “Stock Market Game” is an effective form of “experiential learning,” wherein students are actively learning in a simulation. Teams of students manage real-time virtual investments. They use research and program-provided news updates to invest a hypothetical $100,000 in stocks, which simulates the results of their investments as though they were being made in the real marketplace. During these sessions, students compete with teams in their classroom and teams in their states to increase the value of their portfolio (Hinojosa et al., 2010). Harter and Harter (2010) link the “Stock Market Game” with basic content about the stock market in the form of lessons from “Learning from the Market.” Each lesson pays careful attention to issues such as connection to the students’ prior learning, use of a variety of learning styles, collaboration among students, and techniques to underscore the lesson goals. A combination of playing the SMG with content lessons has proved to be effective (d = 0.79) in further deepening the financial knowledge (Harter and Harter, 2010).

“Experiential learning” can make students aware of basic financial planning concepts and illustrates how these concepts apply to everyday life (Danes and Haberman, 2007). Varcoe et al. (2005) point out that teens are naturally more interested in learning about the consumer and financial issues which they perceive as salient in their lives at that particular time. Relevance can be achieved through adding “real world experiences” to the lessons. Bruhn et al. (2013) uses interactive classroom exercises, with themes that have meaning and relevance, as they deal with everyday matters in which young people have to deal now or in the near future. The students also receive take-home exercises, such as creating household budgets with parents, and role-playing assignments. Bruhn et al. (2013) who assessed this program showed that parents were significantly more likely to report that their children discussed financial matters with them at home, and that they volunteered to help organize household budgets. The results showed a small (d = 0.25) and significant improvement of the financial knowledge of students. Furthermore, there was a significant increase of 1.4 percentage points in the intention to save for purchases, and significant improvement in the budgeting capability and skills in negotiating prices and payment methods. There is also evidence that the program affected students’ inter-temporal preferences and attitudes regarding current and future financial decisions. Mandell and Klein (2007) indicate that most financial planning starts with an analysis of goals, and therefore, it is important to take into account students’ perceptions of future goals, for example, a college degree, a professional job, or a higher salary. This is in line with the “Goal Setting Theory” of Locke and Latham (1994) which assumes that specific and challenging goals lead to better performances. Furthermore, one has to be committed to the goal, must get feedback, and must have the ability to perform the task. As an example, the FFFL material that is effective in increasing student’s financial knowledge (d = 0.221; 0.267; 0.505; 0.561) works with future-oriented thinking to help students to be confident about their future by providing tools which enable them to think about future possibilities and form positive expectations for the future. This approach seems especially important for students in urban areas and in underprivileged regions (Butt et al., 2008; Harter and Harter, 2009; Smith et al., 2011). The “Financing Your Future” curriculum uses five DVD’s, complemented with three printed lessons to reinforce the financial concepts in the video that is concerned with investing in one’s own human capital (Walstad et al., 2010). Walstad et al. (2010) found the “Financing Your Future” curriculum positively and significantly influences the financial knowledge (d = 1.021) of senior high-school students. This study is one of the few studies that describes a controlled and systematic assessment that evaluates at the fourth tier (progress-toward-objectives) and fifth tier (program impact) of Jacobs’ (1988) five-tier model of evaluation.

Financial education programs in college use mainly stand-alone sessions in the form of short courses, seminars or presentations. As an example, programs that work with traditional lectures or social media, have proven to be effective (d = 0.343; 0.338) in increasing the awareness of college student’s perception regarding compulsive spending decisions (Anderson and Card, 2015). Traditional lectures, but with a clear message and perspective with respect to techniques which help to make responsible choices regarding credit card use (1), and to recognize and control compulsive spending (2) increase awareness of college student’s perception regarding compulsive spending decisions. This can also be achieved by a website where students can choose education topics that are of interest to their current lifestyle including the exploration of financial implications when making a decision, as well as methods to cope with consequences of poor financial choices. There is also a (Money Management) Facebook page where messages and discussion items are posted to encourage students to control compulsive spending, and to make responsible financial decisions (Anderson and Card, 2015). Specifically for college students, these goals are important because of the many challenges they could be experiencing. It seems that a narrowly defined financial education program that teaches the appropriate content can contribute to making better financial decisions in specific “life events.” Furthermore, short and narrowly defined programs are appropriate to reach and motivate college students and affordable for college educators. As college students experience more challenges with finances as they pay bills, use credit cards, work more, consider savings, and manage student debt, these events could work as the fuel in the learning process (Peng et al., 2007). Attitudes to and preferences concerning money are considered an important element of financial literacy education. Atkinson and Messy (2012) argue that, if people have a rather negative attitude, for example, toward saving for their future, they will be less inclined to undertake such behavior. Similarly, if they prefer to prioritize short-term wants over long-term security, then they are unlikely to provide themselves with emergency savings or to make longer-term financial plans.

Theories of “Experiential Learning”

All of this is in line with theories of “Experiential Learning.” Dewey (1997 [1938]: 7) emphasizes, “there is an intimate and necessary relation between the processes of actual experience and education.” Dewey (1997 [1938]) further notes that, by focusing only on content, the teacher eliminates the opportunity for students to develop their own opinions of concepts based on interaction with the information. In this context, it is essential to reflect on what is experienced. Following this idea, Kolb and Fry (1975) developed the “Experiential Learning Cycle” which involves a cycle of action (concrete experience), reflection (and observation), conceptualization, and new experience (Johnson and Sherraden, 2007). This approach seems particularly appropriate for financial education, given the nature of financial decision making (Johnson and Sherraden, 2007). “Experiential Learning” has the potential to engage students in topics of interest to them, and it provides opportunities to explore how financial concepts can be applied to real-world situations. To achieve commitment and meaning in learning and achieve intrinsic motivation, it is important to fulfill the need for “relatedness” (the need to have a close and friendly relationship with others), “autonomy,” and “competence.” These three basic needs are part of the “Self-Determination Theory” (Deci and Ryan, 1991). The “Self-Determination Theory,” as applied to financial-literacy education, is primarily concerned with promoting students autonomy (or self-determination) and competence. “Autonomy” implies having control of one’s own learning process. “Competence” is about the feeling of being effective in the ongoing interaction with the social environment, and experiencing the ability to exploit one’s own capabilities (self-efficacy). “Self-efficacy” is defined as: “a person’s judgment of their capabilities to organize and execute courses of action required to attain a specified level of performance” (Bandura, 1993). Walstad et al. (2010) emphasizes that the focus should not only be on the teaching of financial concepts but also on improving self-confidence.Adding this leads to healthy financial behavior.

Conclusion and discussion

This study has provided a systematic literature review on the extent to which financial education in schools can improve the financial literacy of children and adolescents, and enhance their capabilities as economic citizens. There are indications that, with regard to the three components of our definition of financial literacy, school-based financial education programs may improve children’s and adolescents’ financial knowledge and attitudes. The retention results prove to be small, and the studies measure mainly short-term effects. Studies that assess the intention to practice good behavior and studies based on self-reported behavior also report positive effects. Furthermore, little is known about the effects of financial education on children’s and adolescent’s actual financial behavior. Evidence is relatively limited because it is methodologically difficult to assess the actual behavior of children and adolescents. Also, longitudinal experimental research is needed to investigate the long-term effects of specific financial education programs on financial knowledge, behavior and attitudes. The available evidence also suggests that financial education programs in secondary schools and colleges may be effective in reducing the gender gap. These findings support the notion that financial-literacy education must start as early as in elementary school, and ought to be repeated in secondary school and college. To ensure continuous learning, financial-literacy education should be a compulsory part of the school curriculum. Furthermore, the few financial education programs that involve parents in the education of their children seem to be effective in increasing the financial literacy of children and adolescents (Batty et al., 2015; Bruhn et al., 2013; Butt et al., 2008; Harter and Harter, 2009; Smith et al., 2011). This is in line with van Campenhout (2015) and Shim et al. (2009) who report that the effectiveness of financial-literacy education could be improved if parental involvement were higher.

In the literature, there seems to be some consensus about the pedagogical characteristics of effective financial education programs (Collins and Odders-White, 2015; Johnson and Sherraden, 2007; Totenhagen et al., 2015). This study provides a number of key characteristics that should be taken into account when designing an effective school-based financial education program. A promising method to teach financial literacy in primary school and secondary school seems to be “Experiential Learning” with a variety of teaching methods. In elementary school, the focus should be on “hands-on pedagogy,” whereby a key characteristic is “learning by doing.” In secondary school, a key characteristic is “relevance of the topic” by adding real-world experiences to the lessons, and take into account the students’ perceptions of future goals. In both primary school and secondary school, a key characteristic of effective financial education programs seems to be that students experience the impact of their decisions by actively participating in the learning process. In college, an essential key characteristic of the financial education program appears to be that the content of the lessons aligns with students’ specific “life events.” Overall, “financial-literacy education” should not only be concerned with acquiring new skills, but also with knowing how to apply these skills, and, based on this, help students to gain experiences that makes them stronger.

A limitation in the design of financial-literacy education programs is that little or no attention is paid to transferable knowledge. In order to make well-considered financial decisions, children and adolescents must have the ability to make the transfer to new contexts. One way to achieve this is by embedding behavioral economics in the design of financial-literacy education programs (Yoong, 2013). Future research must investigate the effectiveness of this approach. Another limitation is that the design principles of programs do not receive sufficient attention. Specifically, several studies do not explicitly describe the teaching methods. Furthermore, they give little or no information about what in the program was effective, and how large the effects were. Moreover, they do not provide information about what can be improved or changed. Other issues concern how the effectiveness of financial education programs is measured. A self-reported increase of financial knowledge may be measuring self-confidence more than actual knowledge. The same issue exists measuring self-reported behavior that could be “intention to change” more than actual behavior change. Various studies (Asarta et al., 2014; Fox et al., 2005; McCormick, 2009; Walstad et al., 2010) highlight the importance of Jacob’s (1988) five-tier framework when evaluating the effectiveness of a financial education program for high school youth. This framework, based on program evaluation for adults, can easily be adapted for children and adolescents’ school-based financial education.

Footnotes

Compliance with ethical standards

For this type of study formal consent is not required. This article does not contain any studies with human participants or animals performed by any of the authors.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported in part by Money Wise Platform (Wijzer in geldzaken).