Abstract

Using a framework for educational design research, this article reports and evaluates the (process of the) design of a financial education program. The program is designed for high school students in the prevocational track in the Netherlands. The aim of the program is to improve students’ financial knowledge, attitudes, self-efficacy, and (savings) behavior. The main outcome of this study is the identification of design principles that can be used by others for the design of financial education programs: setting a personal savings goal, commitment with and reflection on this goal, discussing money issues with peers and family, hands-on activities with autonomy, and explicit instruction through animated video clips. The results show that our program, called “SaveWise,” improves high school students’ financial knowledge and skills, financial awareness, attitudes towards money, self-efficacy, and financial behavior.

Introduction

Financial literacy is increasingly seen as an essential skill for participation in society (Organization for Economic Co-operation and Development (OECD), 2014). Young people grow up in a society in which the financial landscape is complex (Amagir et al., 2018a) and governments are shifting financial responsibilities (e.g. student loans) to citizens. This increases the need to improve the level of financial literacy among the population at large. National strategies for financial education are being developed to provide lifelong learning opportunities. The number of countries in which financial education is being implemented in schools is increasing (OECD, 2017). In the Netherlands, however, it is currently not a mandatory part of the curriculum (Amagir et al., 2017). In high schools, some limited attention is being paid to financial education topics, such as budgeting and purchasing goods and services, depending on priorities set by schools or individual teachers (Money Wise, 2014). Fifty-eight percent of the lowest track high school students in the Netherlands find it important that school teaches them how to manage money (Money Wise, 2016).

Financial education ultimately aims to empower and motivate people to change their financial behavior, for example, for making well-considered financial decisions (Amagir et al., 2018a). Saving regularly is one of the most widely recognized money management principles. Although one in five households in the Netherlands does not have any form of savings, and one in three households indicates that it is unable to absorb unforeseen expenses (National Institute for Family Finance Information (NIBUD), 2017), the vast majority of adults recognizes the importance of saving. However, one in three young adults does not have sufficient savings to absorb unforeseen expenses (Rabobank, 2018).

Although there is evidence to suggest that school-based financial education may promote financial knowledge and attitudes toward money, studies that assess the effects of financial education on children’s and adolescent’s actual financial behavior are scarce and show hardly any effect (Amagir et al., 2018a; Kaiser and Menkhoff, 2018). Moreover, most effect studies on school-based financial education programs do not explicitly describe the teaching methods and the design principles of the program concerned, nor do they provide information on what could be improved or changed (Amagir et al., 2018a).

To fill this gap, this study addresses the following question: what are the characteristics of a financial education program that is relevant for high school students of the prevocational track in the Netherlands – that is, the lower track in secondary education – with the aim of improving students’ financial knowledge, attitudes, self-efficacy, and (savings) behavior?

Method and research questions

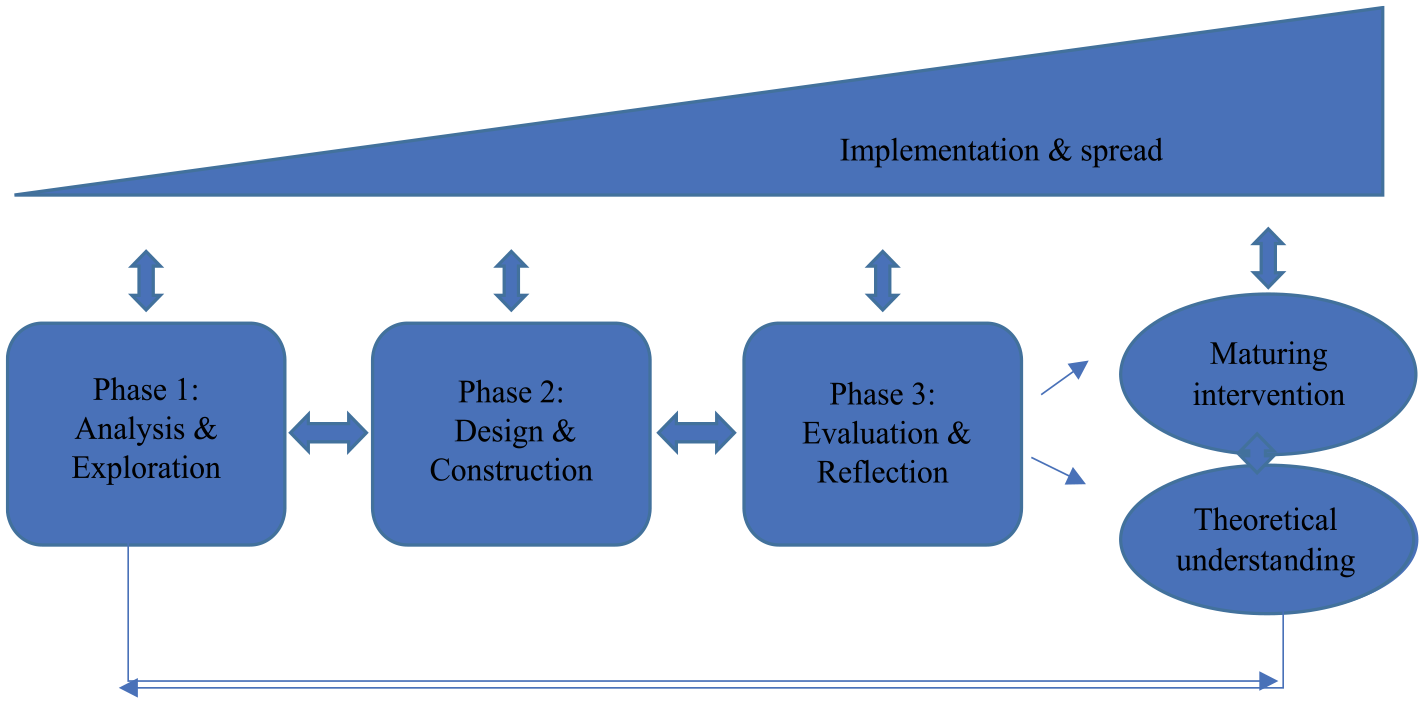

We used an adapted version of a generic model (Figure 1) for conducting educational design research (EDR) by McKenney and Reeves (2012), who describe EDR as “a genre of research in which the iterative development of solutions to practical and complex educational problems also provides the context for empirical investigation, which yields theoretical understanding that can inform the work of others” (p. 9). Barab and Squire (2004) argued that “design-based research that advances theory but does not demonstrate the value of the design in creating an impact on learning in the local context of study has not adequately justified the value of the theory” (p. 6).

Generic model for educational design research (McKenney and Reeves, 2014).

An iterative process is employed in order to make an intervention design “mature” through multiple cycles of design, development, testing, and evaluating, involving collaboration between researchers and practitioners from different disciplines (Plomp and Nieveen, 2013). The generic model distinguishes three phases; the first and second entail a literature review and context analysis, leading toward initial design principles. So the central research question during these two phases was:

1. Which design principles can be derived from theory and context and which initial design results from this?

In the third phase, the design characteristics and educational materials applied are optimized through a cycle of design, evaluation, and revision. In this context, we addressed the following research questions:

2. What is the practical feasibility of the design according to teachers and students and what changes have to be made to the initial design?

3. Were the learning objectives clear enough for students?

To assess students’ experiences with the program, we addressed the following research questions:

4. Did students find the program relevant?

5. How did students perceive the learning outcomes of the program?

Phase 1: Analysis and exploration

Context analysis

Dutch secondary education is divided into three tracks: a 4-year prevocational track (voorbereidend middelbaar beroepsonderwijs, VMBO), subdivided into a basic (VMBO-BK) and a more advanced level (VMBO-GT), a 5-year general secondary track (hoger algemeen voortgezet onderwijs, HAVO), and a 6-year pre-university track (voorbereidend wetenschappelijk onderwijs, VWO) (EP-Nuffic, 2015). This study targets at eighth- and ninth-grade VMBO students of both levels. This age group becomes increasingly independent, taking on its first financial responsibilities. New opportunities (e.g. a part-time job) allow these adolescents to develop knowledge and skills for conscious financial decision making, while also developing unconscious financial habits and heuristics that will drive their everyday financial behavior in adulthood (Drever et al., 2015: 26).

In a previous study (Amagir et al., 2017), we found that VMBO students tend to show less responsible financial behavior and find it less important to think before deciding to purchase something than students of the two higher secondary education tracks. VMBO students also have far less financial knowledge (Amagir et al., 2017). These findings are consistent with the Program for International Student Assessment (PISA) (OECD, 2017) study among 15-year-olds of OECD countries, which showed that the gaps in knowledge levels between the 90th and 10th percentiles were largest in the Netherlands and Beijing–Shanghai–Jiangsu–Guangdong (China).

Our review of financial literacy education programs for children and adolescents pointed out that most financial education programs in secondary schools focus at spending and credit, saving and investment, and budgeting, with no fundamental differences across countries (Amagir et al., 2018a).The content of the financial education program whose design is the object of this study is based on a nonmandatory Dutch framework describing learning outcomes and competencies for financial education (NIBUD, 2015). We focus on learning outcomes in the context of the competences “spending money responsibly – making choices” and “taking account of future wishes and circumstances – saving and planning.” These learning outcomes are akin to those of the PISA sub-domain “planning and managing finances” (OECD, 2013). Learning objectives describe knowledge and understanding of financial concepts, as well as skills, attitudes, and self-efficacy to apply this knowledge in daily financial decision making. For example, students can make a budget for regular spending and saving, plan ahead by setting short-, medium-, or long-term goals, save money for a large purchase, or search for options to reduce expenses and increase earnings in order to increase savings.

Input for design characteristics of financial education programs

In a previous study, we defined financial literacy as a combination of financial knowledge, attitudes towards money, financial self-efficacy, and financial behavior supporting application of financial knowledge in daily financial decision making (Amagir et al., 2018a). We define financial education as teaching encompassing all of these aspects.

A promising method to teach financial literacy to secondary school students seems to be “experiential learning” (Amagir et al., 2018a; Danes and Haberman, 2007; Harter and Harter, 2010; Hinojosa et al., 2010). Dewey (1997 [1938]) emphasizes that “there is an intimate and necessary relation between the processes of actual experience and education.” (p. 7). By focusing on content only, the teacher suppresses opportunities for students to develop their own opinions about concepts based on interaction with the information. It is, therefore, essential to reflect on what is experienced by students. Based on this idea, Kolb and Fry (1975) developed the “Experiential Learning Cycle” involving action (concrete experience), reflection (and observation), conceptualization, and new experience. A key element of experiential learning is that learners analyze their experience by reflection, evaluation, and reconstruction in order to establish meaning in the context of prior experience, which may lead to further action (Boud et al., 1993).

This experiential approach seems particularly appropriate for financial education, given the nature of financial decision making (Johnson and Sherraden, 2007). It has the potential of engaging students in topics of interest to them, as well as providing opportunities to explore how financial concepts can be applied to real-world situations (Amagir et al., 2018a). Boud et al. (1993) put forward five important assumptions about experiential learning: (1) experience is the foundation of, and the stimulus for learning; (2) learners actively construct their own experience; (3) learning is a holistic process, implying that it is an interaction between all the elements involved in learning; (4) learning is socially and culturally constructed; and (5) learning is influenced by the socio-emotional context in which it takes place. Some of these five aspects have been confirmed by our previous research. In line with the second aspect, we found that hands-on activities seem to be an effective pedagogy for financial education (Amagir et al., 2018a). We also found that financial education programs should have a holistic approach and should address not only knowledge, but also the other aspects of financial literacy, if a change in financial behavior is their aim (Amagir et al., 2018b).

Experiential learning involves students’ own appropriation of something that is personally significant or meaningful to them (Boud et al., 1993). To achieve this, students must be personally engaged with the realities being studied. Relevance of the topic by adding real-world experiences (Bruhn et al., 2016; Varcoe et al., 2005), and taking into account the students’ perceptions of goals for their future seem to be effective in improving financial literacy levels (Butt et al., 2008; Harter and Harter, 2009; Mandell and Klein, 2007; Smith et al., 2011). Evidence shows that in order to save, adolescents must be future-oriented (Otto, 2013). Focusing on the short term only, due to a lack of self-control or the need for immediate gratification, increases the risk of getting into financial problems (Madern and Van Der Schors, 2012; Webley and Nyhus, 2001). But saving seems to be pointless for adolescents lacking belief in their ability to be successful at it (self-efficacy) (Otto, 2013). Saving and budgeting also require practice, implying that children need to have sufficient money to save and make budgeting decisions, including mistakes from which they can learn (Webley and Nyhus, 2013).

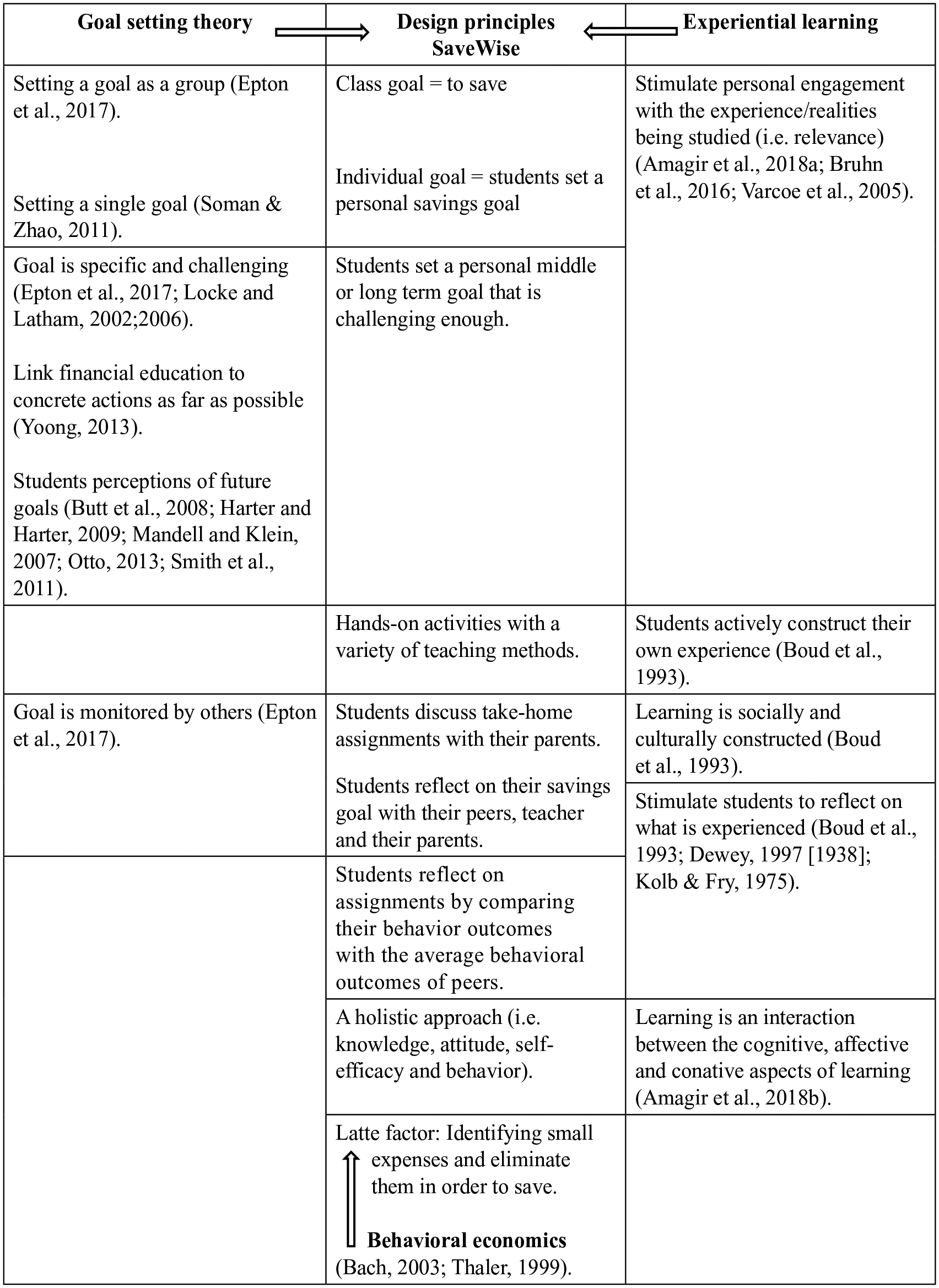

To increase the likelihood of behavioral change, financial education should be linked to concrete actions as much as possible (Yoong, 2013). This is in line with the goal setting theory entailing that behavioral change is being promoted if there is a conscious and specific, sufficiently difficult goal towards which behavior should be directed (Locke and Latham, 2002, 2006). This theory is supported by a meta-analysis by Epton et al. (2017), who add that goal setting is most effective if the goal is set face-to-face and publicly as a group goal, and combined with monitoring of behaviors by others without feedback. Carpena et al. (2017) have shown positive effects on (low-income) individuals’ savings behavior of a financial education program incorporating short-term noncompulsory financial goals. No long-term effects were found in this study. Setting a single savings goal seems to be more effective than setting multiple goals (Soman and Zhao, 2011). Riitsalu (2018) showed in a case study that a combination of goal setting, commitment through regular reminders of sub-goals with advice from peers, may be effective in improving the financial behavior of college students. Furthermore, setting promotional goals (e.g. saving for a certain purchase) seems to be more motivating than prevention-oriented goals (e.g. falling into debt) (Riitsalu, 2018).

Embedding behavioral economics into the design of financial literacy education programs may also foster behavioral change (Yoong, 2013). Shefrin and Thaler (1988), in their behavioral life cycle theory, state that people tend to categorize income hierarchically into three mental accounts: current assets, current wealth, and future income. The current assets account (cash or the balance of one’s bank account) has the largest influence on the propensity to consume, while the future income account (e.g. retirement savings accounts) has the smallest influence, with the current wealth account (e.g. savings account and home equity) in between. Small expenses, such as for a coffee or a bottle of water, are often overlooked and not booked in the appropriate mental account (Thaler, 1999). Identifying these small expenses and avoiding them in order to save, also known as the Latte Factor (Bach, 2003), is a tool to make people understand how small savings could generate a substantial amount through compound interest.

Involving parents in the financial literacy education of their children also seems to be effective (Amagir et al., 2018a; Bruhn et al., 2016; Butt et al., 2008; Harter and Harter, 2009; Smith et al., 2011), particularly in the formation of attitudes (Lusardi et al., 2010; Money Wise, 2014). Finally, it is important to train teachers in working with a financial education program (Bruhn et al., 2016; Compen et al., 2018; De Beckker et al., 2019).

Phase 2: Design and construction

In this section, we present the design principles that were derived from the theory and context described in the previous section, thus answering research question 1. We drew up our primary design principles by combining the main aspects of the goal setting theory, experiential learning, and behavioral economics. The middle column in Figure 2 shows which principles we arrived at in this way. Based on these principles as well as the context analysis, the primary researcher drafted the first version of a financial education program (prototype I), consisting of a global description of the pedagogy, learning objectives, and contents of five lessons. During the first lesson, students set a savings goal for something they would like to do or buy. They also watch a video clip (“Stack your Money”) in order to learn about savings motives and to form positive attitudes towards saving. During the second lesson, students set up a budget to meet their goals. The third lesson is devoted to a savings plan for a particular purchase. The fourth lesson introduces students to the Latte Factor; they calculate their own Latte Factor and how they can employ it to save money. In the fifth lesson, students compose a video about ways to earn and save money, and about influences exerted on their financial behavior. All lessons are accompanied with take-home assignments that students have to discuss with their families. We decided to call the program SaveWise.

The design principles generated from theory.

Phase 3: Evaluation and reflection

Iterative (re)design process of prototypes

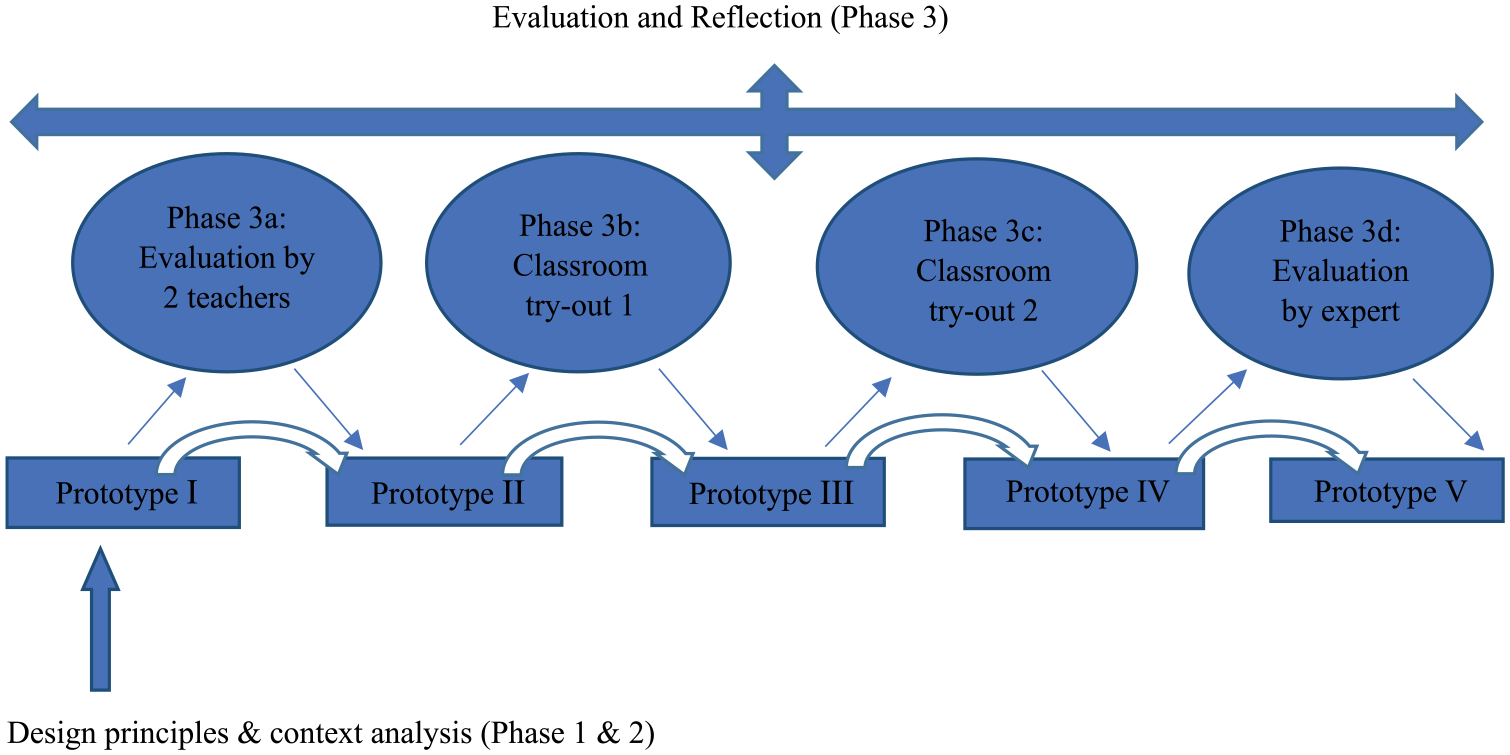

As shown in Figure 3, phase 3 involved multiple iterations of design, development, testing, and evaluating. Phase 3a comprised the revision of the first prototype based on the evaluations by two teachers, and the development of prototype II which has been used for the first classroom tryout. Lessons learnt from the first and second classroom tryout guided the development of prototypes III and IV (phases 3b and 3c). During and after each tryout, we assessed whether the program design actually worked, and which improvements had to be applied. During the last stage, prototype IV was discussed in a “walk through” with an expert of Moneywise, which resulted in prototype V. Throughout all phases, the primary researcher systematically explored how students and teachers responded to the program activities, noting what to adjust in the next stage.

The development process of prototypes (based on Mafumiko, 2006).

Data collection

The classroom tryouts were undertaken sequentially at two schools in the Netherlands. The first involved one class with 28 ninth-grade students at a large high school in Haarlem in the urban western part of the Netherlands. The school offers different educational tracks. The school population consists mainly of middle class native Dutch without a migrant background. The second involved two different classes with a total of 43 eighth and ninth graders, mainly Dutch students with a non-Western background, at a small Rotterdam school offering VMBO only. Eighty-nine percent of the students live in relatively poor neighborhoods (Gemeente Rotterdam, 2012) and have parents with low literacy skills (Gemeente Rotterdam, 2016).

Because of the explorative character of this study, we relied on a qualitative approach. Data collection methods included teachers’ evaluations, teachers’ log books, observations of classroom tryouts by the primary researcher, in-depth interviews with students, and student evaluations (learner reports). The main purpose of the teachers’ evaluations and teachers’ log books was generating feedback about the practical feasibility of the program in a classroom setting. Teachers were asked to note difficulties with the implementation of the program, suggestions for improvement, and observations on the strengths of the program in a logbook. Observations of these classroom tryouts were intended to track down problems teachers and students experienced while working with the material. The primary researcher conducted eight semi-structured interviews (40–60 minutes each) with students to gauge their experiences with the program and their perspectives about what and how they learned. The students volunteering to participate were representative of the school populations with a representative distribution by gender and ethnicity.

Each lesson was concluded by filling in learner reports by students. This research method enables students to report their impressions about what they have and have not learned in a particular educational situation (Van Kesteren, 1993). We asked students to describe what they learned by finishing the following sentences: “I have learned that/how . . . ” and “I have learned that/how I . . .” (Wagenaar et al., 2003). In addition, we asked students whether they had discovered a misconception about themselves and whether they were surprised about anything they learned by finishing the following sentences: “I have learned that/how it is not true that I . . . ” and “after this lesson I am surprised that . . .” Finally, we asked the students which assignments they found unnecessary or unclear.

Data analysis

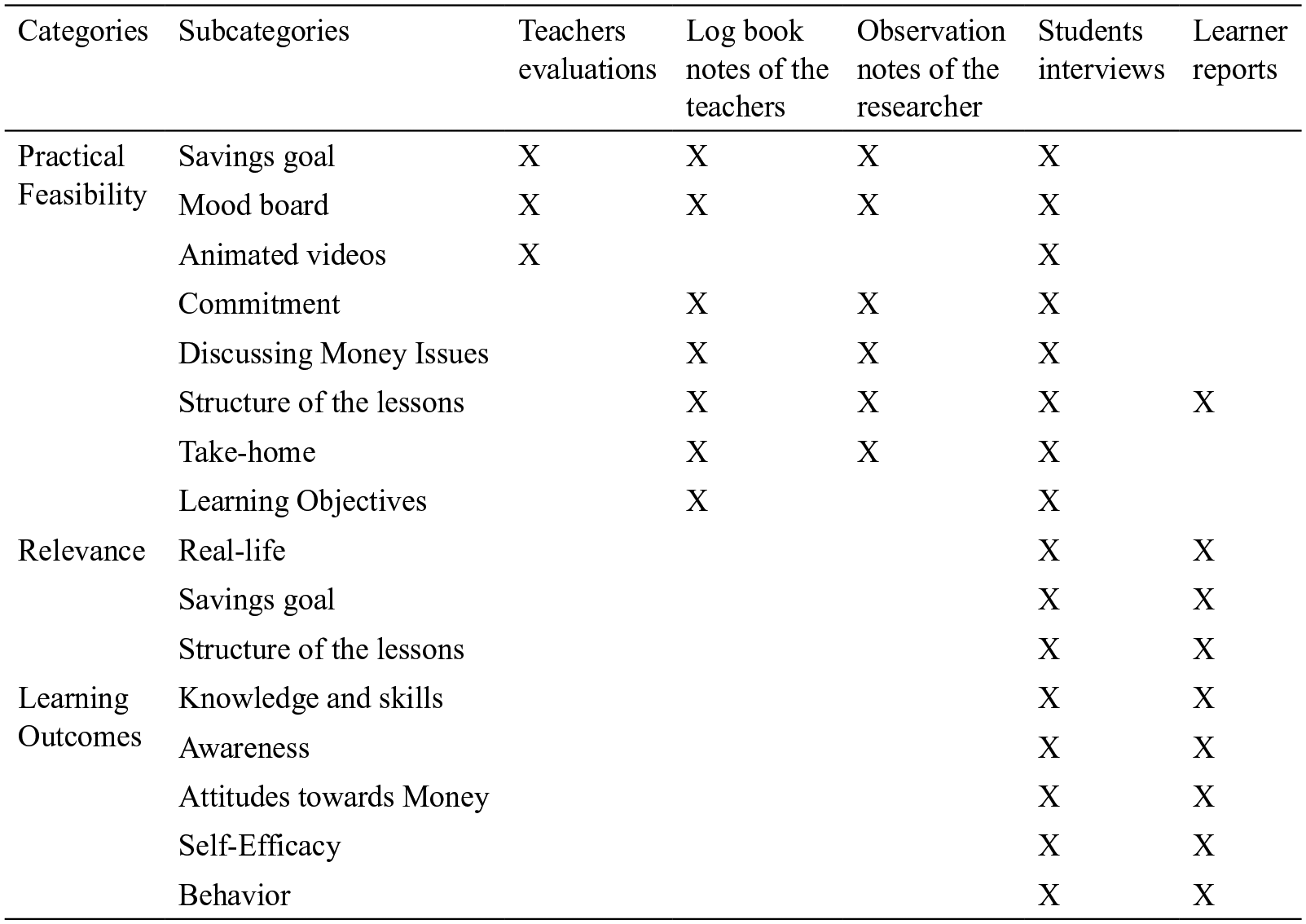

Student interviews and evaluations by teachers were recorded and transcribed literally. Deductive and inductive analyses of the transcripts, teachers’ logs, observation reports, and learner reports have been applied iteratively, utilizing thematic analysis, a “method for identifying, analyzing, and reporting patterns (themes) within data” (Braun and Clarke, 2008: 79). We first analyzed the data by means of the concepts derived from our research questions (Miles and Huberman, 1984). This resulted into the main categories. Second, we applied inductive analysis because the contents of the data suggested elaboration of subcategories which could explicate the dominant themes on a more detailed level. In order to identify the changes that should be applied in various phases of the design process, we categorized themes in a SWOT format (Bosschaart et al., 2016). Figure 4 shows how the resulting categories and subcategories were used in connection with our five data sources.

Categories and subcategories of the data.

Results

The results are presented in two sections. First, we present the results of the four phases of the iterative (re)design process of prototypes (Figure 3). We explain the changes that have been made to the initial design, based on the practical feasibility of the program (research questions 2 and 3). Second, we discuss students’ perceptions of the relevance and learning outcomes of the program (research questions 4 and 5).

The (re)design process of prototypes

Phase 3a: Evaluation by teachers

Savings goal and mood board

Teachers’ general impressions of the first prototype were very useful to fine-tune the program. Both teachers indicated that while working with a savings goal could be relevant for students, there was a risk that students might not be able to think of a suitable savings goal. One teacher suggested the use of dreams: How much fun is there in fantasizing about what you want to buy or do? You have to emphasize that students can make their dreams come true once they have any savings. Maybe you should have students visualize their dreams, by means of picturing them or possibly using a mood board.

We decided, therefore, to add creating a mood board to the first lesson. This may serve as an introduction to the series of lessons, while also helping students to think about future goals and to be personally engaged with the content being studied.

Animated instructional videos

Another suggestion concerned the instruction for the assignments: “It could be motivating for students if the instruction for the assignments would be given through videos. Most students cannot focus on an explanation by the teacher for too long.” We, therefore, decided to accompany three of the four lessons with short animated instructional videos (PowToon), designed by three trainee economics teachers in collaboration with the primary researcher. As a result of these suggestions, we developed prototype II.

Phases 3b and 3c: Evaluations by teachers and students

Savings goal, mood board, and commitment

The teacher in charge of the first tryout (T1) noted that she really got to know her students well through the mood board and savings goals and that students were very motivated to work on the mood board. However, they needed more time and wanted to have the freedom to draw their dreams or make a digital mood board. According to the teacher in charge of the second tryout (T2), working with a savings goal worked very well as a framework for the program. The mood board provided students with the opportunity to identify their own personal goals, which was motivating. Students confirmed this during interviews. When asked what the learning objective of the mood board was, a student answered: “To visualize what your savings goals really are, and what you want to focus on as a savings goal.” Another student pointed at the motivating aspect of the mood board: “I really liked making the mood board, I think this assignment was given to motivate us to achieve our savings goals, or to fulfill our dreams, let’s put it that way.”

One of the concerns of T1 was that students could not actively participate in the lessons if they did not have a (realistic) savings goal. T2 noted that there was a risk that students would not be committed if they did not have a sufficiently challenging, yet realistic savings goal. This was confirmed by the researcher’s observation notes. Students noted in the interviews that it is difficult to make a savings plan if you do not know how much you have to save to achieve your goal.

Based on these evaluations, we revised prototype II as follows:

Students were given the freedom to draw their dreams or make a digital mood board, next to using images cut out from magazines (as was the case in the previous version).

Students were incited to include a personal short-term, medium–long, and long-term goal in their mood boards before committing themselves to a medium–long or long-term savings goal.

Mood boards were given a more prominent role at the start of the second lesson.

Two lessons and animated clips were added to the series: (1) introduction of a five-step decision-making model and (2) students apply the decision-making model in order to make a choice for a particular brand or store to achieve their goal.

We revised prototype III with the following additions:

The teacher gives an example of a personal savings goal and savings plan.

Each lesson starts with a reflection of savings goals and students are given the opportunity to note their savings amount per week on a savings ladder.

Discussing money issues

T1 noted that there was insufficient time to discuss money issues due to the number of assignments per lesson. The observation notes of the researcher confirmed this. T2 observed that the program provided opportunities to discuss the importance of savings and to make students more aware of their money management. Student interviews indicated that the lessons differed from regular lessons because of the learning objective: “Of course it differs from other lessons, because it is . . . with another . . . these lessons have a different purpose, say, to make students aware of how they deal with money.” T2 also noted that the program enabled her to identify which students had an aversion to saving.

To provide sufficient time to discuss money issues we revised prototype II as follows:

A number of assignments were integrated into one large assignment.

Addition of a game (in one lesson) to create opportunities for further discussion of topics.

The following revision was added to prototype III:

Teacher identifies students who have an aversion to saving and asks these students’ what withholds them from saving.

Lesson structure

T1 reported that the structure of the lessons was easy to follow, and that the variety of pedagogical methods motivated students to participate well in most of the assignments. The coherent line in the lessons, the variety of pedagogical methods, and the animated instruction videos were judged positively by T2. T1 noted that students were particularly excited about the “Latte-Factor.” A student commented: “Uh, I don’t remember who it was that bought a can of Red Bull every day. For young people it should actually be called the Red Bull factor, not the Latte factor.” T1’s notes as well as observation notes of the researcher revealed three main concerns: (1) students experienced difficulties in making a savings plan because of the limited instructions (confirmed by students in learner reports and interviews); (2) students struggled with categorizing their goals into short, medium, and long terms; and (3) a number of assignments were difficult to carry out by students who claimed to have no expenses or income. T2’s notes revealed that students claiming to get everything from their parents, might not be committed enough to work on certain assignments. She also noted that a few students purported to get a lot of money from their parents, which was free for them to spend. This was confirmed by students’ statements in the learner reports.

Revisions to prototype II:

Explicit instructions for most of the assignments (categorizing different types of goals, making a savings plan, and taking decisions according to a decision-making model).

Addition of the example of the “Red Bull Factor” as a suggestion possibly helping students in calculating their own Latte Factor.

Optional working in pairs for assignments that are difficult to carry out by students claiming to have no expenses or income.

Revisions to prototype III:

Students claiming to get everything from their parents, do an assignment on the amount of money they receive from their parents and what they spend it on.

Take-home assignments

T1 noted that the take-home assignments motivated students to talk at home about their savings goal while also confronting students with the many different expenses of a household. One student mentioned in the interviews that his parents did not want to share their household spending because this is confidential. According to T2, a few students found it difficult to talk about money with their parents. However, they did talk about money with their siblings. Furthermore, some students noted in the interviews that they did not discuss the take-home assignments with their parents due to a lack of time.

Revisions to prototype II:

Addition of a comment that the school is not interested in the amount of household spending, but in the different types of expenditures made to meet their everyday needs.

Revisions to prototype III:

Students may discuss the take-home assignments with their siblings or their grandparents, apart from with their parents.

Spreading of lessons over a longer period.

Learning objectives

At the end of both tryouts, we asked students in the interviews what the main objective of the program was. Most of them mentioned “managing money” and “saving and spending less,” confirming that the main objective of SaveWise was recognized. A student of the first tryout noted: “Uh, well, that young people know more about how to manage their money, that they know how to save, and well, that they find out what they spend their money on.” A student of the second tryout put it slightly differently: “Well that you know how to manage money in a smart way, and that you know how to easily save for something that you really want, and that you also start with thinking about whether you are going to save for something, or yes, that you know how you have to save.”

Students from the second tryout further indicated that the program’s objective also was to prepare young people for the future. “Uh, preparing us, students, a little bit for what is coming when you get older, as you get older.”

Phase 3d: Evaluation by expert

The expert found prototype IV to be very innovating. He noted that the emphasis on achieving dreams by setting a savings goal could be motivating, not only for high school students, but also for primary school children. However, he emphasized that teachers should give students enough time to discuss money issues. Furthermore, he offered some useful comments about the layout for the teacher and student guide. As a result, we developed prototype V. The financial education program SaveWise consists of eight consecutive weekly lessons, each lasting 50 minutes. Figure 1 in Appendix 1 lists the learning outcomes targeted at in each lesson.

Student experiences with SaveWise

Relevance

Students of both tryouts were personally engaged with these “real life” lessons. One student from tryout 1 (T1) stated: “Uh, I think the lessons were better than the regular lessons. Because, well, it is a bit more about daily things, more than regular lessons.” A student of tryout 2 (T2) put it slightly different: . . . especially the way we learned how to save, and make a savings plan and what also stayed with me are clever ways to save money. But also, for example, how to earn an income. These lessons are more about what happens in daily life, more than regular lessons.

This student (T2) also thought that the emphasis was more on doing than knowing: “I actually thought the lessons were quite like regular lessons, the only difference is that you learn something about the outside world, I do not think you have to know something specifically, actually you have to do it yourself.” The majority of the students indicated that working with a personal savings goal helps because it made them think about how to achieve this goal. In both the learner reports and interviews, students reported that they were very surprised to learn about the mood boards and dreams of their peers. In addition, students of T2 explicitly mentioned that the mood board was very useful for identifying savings goals: “I thought it was quite interesting to make the mood board, because you find out what your saving goals are and you also learn about the savings goals of others.”

Most students experienced a sense of autonomy in the learning process and found the lessons to be interesting because of the variety of pedagogical methods: The lessons were much more free. In other lessons, you have a book, and then you have all the theory in a book, assignments, and now you get bits of theory in the lessons, and then you have free assignments. For example, make a video or something else.

Students of T2 explicitly mentioned collaborative learning and discussing money issues as relevant: I actually have a nice experience, yes, because of the way we learned things. The lessons were not boring, because we were able to discuss money issues with other students in class. So I think that’s okay, that I could hear the opinions of others, and talk to them about it, I liked working on it together.

The majority of the students noted in the learner reports and interviews that they were very surprised about the message in the video clip “Stack your money.” One student noted, Well the clip of the rapper, rapping about money and saving, you have to keep that in the program. That is of course just funny. I thought it was funny that you could also convey a serious message in such a way. At first I thought, how did they come up with that.

Most of the students in the learner reports and interviews were surprised about the “Latte-Factor”: Uh, well, that was very interesting. And I think, I mean if you buy one thing in a day then you think, well, that’s not very much, but if you look at it on an annual basis or a monthly basis or something, you’ll see that money goes fast.

Overall students were positive about the animated instruction videos. “It was pretty clever, because kids think with animation, so, that way it’s more in line with how they think.” Students found it relevant and instructive to learn about managing money in general and about savings in particular. One student (T2), for example, stated: “I liked the lessons quite a bit, because we mainly learned how to manage money in different ways, and especially in the short and long term. We learned to save, and how to make a savings plan.”

Learning outcomes

Students reported about five types of learning outcomes: knowledge and skills, awareness, attitudes towards money, self-efficacy, and behavior. The development of knowledge and skills was mentioned less often than the other four. Students of both tryouts indicated that they learned how to set up a personal budget, construct a savings plan, and about different ways to spend less and earn an income. In the learner reports of the second tryout students mentioned that they were surprised about how easy it is to make a savings plan and that they learned more general skills, like discussing and debating. Students of the second tryout were more explicit about the process of making a savings plan compared with students of the first tryout, in both the learner reports and interviews. One student (T2) stated, Actually, we learned different ways of how you can achieve your saving goal. So imagine you save for a game you really like, then you can make a savings plan and then you can write down how much you can save per month and how much you save from your pocket money or part time job to achieve your goal.

Another student of T2 explained, I think it is that you see how much money comes in and how much you spend. And when you want to buy something, you calculate: I receive so much money, I spend so much, I could spend less to achieve my savings goal and in how much time do I have the savings to buy something.

Students of the second tryout further indicated that they learned to prioritize spending. One student stated: “Well, I always have my ATM card with me, but since the lessons, I have started to think more whether that is necessary, do I really need it or not?” Another student put it slightly differently: It is more that you have to be very careful, because in the past, I always thought you save, then you spend it, and then you save again. But now I find it better to think, do I really want it, because it’s a waste of money if you realize after a year that you don’t need it anymore.

Students of both tryouts mentioned that the lessons increased their awareness about their money management, for example: “Well, you know what surprised me a lot in the lessons? Uhm, because at first I did not know what I was actually saving for. Or rather, whether or why I save. Now I know that.” Another student mentioned that one has to be aware of small amounts: “So to really pay attention to those small amounts, so you can save more.” This student explains that she is more aware of things becoming a habit: “That you realize you’re unconsciously spending a lot on small things, which actually becomes ‘normal’.” Compared to students of the first tryout, students of the second tryout noted in the learner reports that they were more aware of the factors influencing their purchasing decisions. They also noted to be surprised about their own spending pattern and the many differences between students when it comes to managing money. One student (T2) mentioned in the interview: “Uhm, compared with others, with classmates, I learned I’m more conscious of how I manage my money. For example, I replied differently to the assignments, and so I found out that I do deal with money differently than others.”

A more positive attitude towards saving is another frequently mentioned learning outcome. In the learner reports and interviews of both tryouts, most students mentioned that they thought it was important to save, spend less, and earn an income. Students of the second tryout mentioned in the interviews that saving is important for now and the (near) future. “That saving is important and that it is very useful for later and your future and that you have to keep doing it.” This student of the second tryout noted that it is important to think before acting. “Well, I think it is important to save, because later in life you have to run your own errands. Then you can’t just spend all the money you have, you first have to think: do I need this or not.” Compared to the first tryout, students of the second tryout stated more often in the learner reports that it is important to make a savings plan and to have a savings goal to be able to succeed. They also stated that it is not true that you can achieve your dreams without a plan or goal. Furthermore, they said that it is important to keep track of your income and expenses, also later in life. They explicitly mentioned household spending. They noted that it is important to compare prices before purchasing a product and that more expensive products are not always better than cheaper products. Finally, they noted that money will not get you what you want in life and that money does not buy happiness.

With regard to self-efficacy, most students of both tryouts indicated that they could save or that they wanted to save more. A few students noted that they found it difficult to save or that while having the ability to save they were not willing to do so. Students of the second tryout further noted that in order to save, it is important to have self-control and perseverance.

With regard to behavior, all but one of the interviewed students was committed to meet their savings goal, even after the program. Most of the students had a medium to long-term goal. Examples of savings goals were a cat, a camera, driving lessons, a game computer, and a scooter. One of the students noted that she did not have enough income to save, but was motivated to get a part-time job to start saving: “I was already planning on taking a job, but I’m more encouraged by these lessons.” In the learner reports, most students noted that they had to save more or had the intention to save. In general, students of both tryouts indicated to spend less because of the lessons: “Yes, that’s going better now, because I’m really saving a lot of money now, just everything I receive, I leave it on my account.”

Discussion and conclusion

In this section, we answer the following question: what are the characteristics of a financial education program relevant for high school students of the prevocational track in the Netherlands with the aim of improving students’ financial knowledge, attitudes, self-efficacy, and (savings) behavior?

Characteristics

Overall, the results of our EDR confirm that working with a personal savings goal functions well as a framework for a financial education program. Students experienced the program as relevant. The emphasis on doing rather than knowing and the real-life issues being studied were judged positively and provided for personal engagement and commitment (Amagir et al., 2018a; Boud et al., 1993; Bruhn et al., 2016; Varcoe et al., 2005). Goal commitment seems to be an important design principle resulting from our EDR. According to Locke and Latham (1990) goal commitment, defined as someone’s determination to reach a goal, is an essential moderator of the linkage between goals and behavior. Several tools eliciting a high goal commitment emerged from our EDR:

Visualizing dreams is a powerful tool to help students stay committed to their goal, also in the longer term. It also stimulates students to be future-oriented. Future orientation is important for adolescent saving (Otto, 2013), and is associated with bank saving (Webley and Nyhus, 2006).

The combination of keeping track of savings (e.g. via a savings ladder) and reflection on the savings goal with peers (Epton et al., 2017) also seems to enhance goal commitment.

Goal commitment seems to be encouraged if the particular purchase and specific savings amount needed are known.

Our findings confirm that students were encouraged to actively participate in the lessons because of the variety in hands-on activities and their autonomy in the learning process. This is in line with our previous findings suggesting that to achieve commitment and meaning in learning and to achieve intrinsic motivation, it is important to fulfill the need for autonomy in learning processes. Autonomy is also one of the three basic needs in Deci and Ryan’s (1991) self-determination theory of motivation.

Another tool resulting from our EDR is the animated instructional videos. They were designed for purposes of instruction and also promoted students’ positive attitudes towards money. The videos provided opportunities for students to interact with each other and their teachers and may have enhanced students’ motivation to actively participate in the learning process. The animated instructional videos were seen as relevant by students, because they fitted well with how students prefer to receive information. This is in line with Gurvitch and Lund (2014), who suggest that students’ attention is limited and that they prefer an interactive instructional process fitting with the way in which they typically receive information. As a result of our EDR, explicit instruction for hands-on activities was developed. Kirschner et al. (2006) suggest that unguided or minimally guided instructional approaches are less effective and efficient for novices than guided instructional approaches.

Another design principle emerging from our EDR is the importance of creating an environment in which students are stimulated to discuss money issues in order to enhance (self)-awareness and stimulate the development of positive attitudes towards money.

Discussing money issues with family through take-home assignments also seems a strong tool to foster positive attitudes and healthy financial behavior (Bruhn et al., 2016; Butt et al., 2008; Harter and Harter, 2009; Smith et al., 2011). In a previous study (Amagir et al., 2017), we found that financial socialization through peers and parents and participating in financial family decisions positively relates with attitudes towards financial planning and thinking before acting, as well as financial behavior (Jorgensen and Savla, 2010). However, the results of our EDR show that some students find it difficult to talk about money with their parents. An explanation may be that money is seen as a confidential subject and parents do not like to share private financial issues with their children (Romo, 2011).

Learning outcomes

Findings show that, in the perception of students, “SaveWise” may improve high school students’ financial knowledge and skills, awareness, attitudes, self-efficacy, and behavior. With regard to knowledge and skills, students reported to have learned skills to save and budget their money, and ways to earn an income. In addition, they reported to have learned more general skills, like discussing money issues. We found that, in the perception of students, the program increased (self)-awareness regarding managing money in general, particularly in saving, purchasing, and spending decisions. The results also show that students developed a more positive attitude towards financial planning issues, such as saving for a particular purchase and for the future, spending less, and budgeting. In addition, students learned to think before acting, for instance, by means of comparing prices before buying a product. Our own previous research indicates that responsible financial behavior is most strongly related to attitudes towards financial planning and thinking before acting (Amagir et al., 2018b).

With regard to self-efficacy, our findings show that students developed belief in their ability to be successful at saving and budgeting. According to Otto (2013), saving is pointless for adolescents lacking belief in their ability to be successful at it. However, our results also show that a few students claim to be able to save but indicate that they are not willing to do so (Otto, 2013). Our results further indicate that some students are capable of delaying gratification and displaying self-control. According to Webley and Nyhus (2006), self-control is an important determinant of individual saving and spending.

Concerning behavior, our findings show that as a result of the program, students have become more committed to meeting their savings goal, budgeting, and spending less. Saving and budgeting require practice and making mistakes from which one can learn (Webley and Nyhus, 2013). Thus, a financial education program embedded in real life may not be effective for students claiming to get everything from their parents or not to have sufficient money to save and to make budgeting decisions (Webley and Nyhus, 2001).

Our outcomes may be of interest to other researchers and practitioners involved in designing and teaching school-based financial education. Our findings have several implications for the field and for further research. The sample size of this study is small, because our goal was to design, develop, and evaluate a financial education program in collaboration with teachers and students in a more in-depth way. Future research is needed to investigate to what extent these findings are representative for a different context. An experimental study with a larger sample size should provide more evidence for the effects of “SaveWise.”

Footnotes

Appendix 1

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethical Approval

All procedures performed in studies involving human participants were in accordance with the ethical standards of the institutional and/or national research committee and with the 1964 Helsinki declaration and its later amendments or comparable ethical standards.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported in part by Money Wise Platform (In Dutch: Wijzer in geldzaken).