Abstract

Financial literacy is an important but oft ignored skill that is vital for young people. This study measured financial literacy levels among high school students (N = 608) in India and found low levels of performance on standard measures of financial literacy. The percentage correct score on the basic financial literacy questions was 45% and on the sophisticated financial literacy questions the score was 44%. Financial literacy levels in India were found to be lower than those in developed countries. Gender differences were found, with females outperforming males, contrary to findings in developed countries. Students who pursued the commerce/economics stream of education were found to have higher levels of financial literacy than students pursuing the science stream. Results showed that students, despite having high levels of numeracy, were unable to transfer that knowledge to do financial computations. Parental involvement was also found to have a significant influence on financial literacy. Interviews with students highlighted the fact that understanding of societal and macroeconomic impacts of financial literacy was low. These findings lend support for high school financial education which involves parents and stresses practical hands-on application, societal and macroeconomic impact, as a means of improving financial literacy.

Keywords

Introduction

Financial literacy is a crucial topic for consumers and in particular is essential for young people (Lusardi, 2015). There are numerous definitions of financial literacy. The National Financial Educators Council (2018) defines financial literacy “as possessing the skills and knowledge on financial matters to confidently take effective action that best fulfills an individual’s personal, family and global community goals.” Financial literacy has mostly been defined from a consumer’s behavior point of view and comprises personal finance constructs, financial habits/behavior, borrowing, investment, and financial protection (Atkinson et al., 2007; Atkinson and Messy, 2012; Huston, 2010; Messy and Monticone, 2012). However, some researchers question the efficacy of this type of limited definition of financial literacy (Davies, 2015). Davies (2015) proposed a more comprehensive definition of financial literacy that included roles and responsibilities of not only the consumer but also that of other players in the economy such as banks, investment firms, and the government.

Financial illiteracy is prevalent worldwide. The 2015 Program for International Student Assessment (PISA) survey of 15-year-old students found that the financial literacy levels in the United States were below the OECD (Organisation for Economic Co-operation and Development) average. The National Financial Educators Council in the United States conducted a National Financial Literacy Test in 2016 with 3014, 15–18 year olds and the average score was 59.90%. Similar low levels of financial literacy have been found in European countries as well. The 2015 results of the OECD/INFE financial literacy survey administered in 17 European countries showed that most European high school students lacked adequate financial literacy knowledge. Erner et al. (2016) found that German high school students had relatively low levels (54%) of financial literacy.

Many researchers have investigated the impact of low financial literacy. Poor financial literacy has been shown to affect workplace efficiency and yield (Garman et al., 1996, 1999; Joo and Grable, 2000; Kim et al., 1998; Kim and Garman, 2004). The 2008 financial crisis in the United States which had a ripple effect across the world showed that bad financial decisions predominantly made due to financial illiteracy can have serious negative outcomes (International Network of Financial Education//Organization for Economic Cooperation and Development (INFE/OECD), 2009). Lusardi et al. (2017) simulated a life-cycle model and showed that financial literacy explained greater than half the wealth inequality in the United States.

The impact of financial illiteracy has been documented by researchers in European countries as well. Van Rooij et al. (2011) found that among Dutch households, higher financial knowledge correlated with higher participation in the stock market, and better financial and retirement planning. Guiso and Jappelli (2008) found similar results with Italian investors. Financial literacy, consumer debt, and financial behavior were also found to be correlated in studies conducted in the United Kingdom (Disney and Gathergood, 2013; Gathergood, 2012).

Over the recent past, governments and employers in many countries have shifted the burden of adequately saving and investing for retirement to the individual, but individuals in the United States do not seem to have the skill and knowledge needed to handle this responsibility (Lusardi and Mitchell, 2014; Volpe et al., 2006). Research has also shown that many Europeans are not adequately equipped to make financial decisions about retirement planning. A study done by the Danish National Center for Social Research showed that many adults were not aware of pension options and financial terminology (Money and Pensions Panel, 2013). Similarly, a report published by the Netherlands Pension Monitor reported that over 70% of Dutch employees were not aware of their income after retirement (Atkinson et al., 2015). Similar results were also found among adults aged 50–59 living in the United Kingdom (Banks and Oldfield, 2007).

Research has shed light on some factors that impact financial literacy. Lyons (2004) found that among American college students, females and minority students were at the highest risk of having high credit card debts. Females and younger populations in the United States have been found to have lower financial literacy levels (Lusardi and Mitchell, 2011). Financial literacy levels have been found to differ by family income, with children from higher income families having higher financial literacy (Aizcorbe et al., 2003). Those without a college degree had lower financial literacy. Even though cognitive ability is correlated with financial literacy, it did not fully explain the variations in financial literacy with education (Lusardi and Mitchell, 2007). Several studies have also reported marked differences by race and ethnicity, with African Americans and Hispanics displaying the lowest level of financial knowledge in the United States (Lusardi and Mitchell, 2007, 2011). Financial literacy was also positively correlated with parental education and whether parents held stocks and retirement accounts when the children were growing up (Lusardi et al., 2010). There is also a geographical difference in financial literacy in many countries with financial literacy being higher in urban areas than rural (Klapper and Panos, 2011).

Effective financial education, especially in high school, is important for improving financial literacy among young people. The Council for Economic Education reported in their 2018 findings of the state of financial and economic education in the schools in the United States that only 17 states required students to take a course in personal finance and 22 states required students to take a course in economics before high school graduation. They also reported that there had been very little increase in the efforts to increase financial education in the schools since their 2016 report. Walstad and Rebeck (2012) used the data from the High School Transcript Study conducted by the National Center for Education Statistics (NCES) at the US Department of Education and found that only 7.9% of students took some form of financial education courses offered in their high school. But, these low results may be due to the fact that students were getting financial literacy information from other courses, which might not be designated as a financial literacy course (Walstad et al., 2016). Thus, there is some evidence to suggest that rigorous financial education at the high school level is lacking.

Researchers have found mixed results on the impact of educational interventions aimed at improving financial literacy. Some researchers have shown that financial literacy interventions for high school students have had some positive impacts in improving financial knowledge and application of the knowledge (Carlin and Robinson, 2012; Danes, 2006; Danes et al., 2013; Gellman and Laux, 2011; Morton and Schug, 2001; Walstad et al., 2010). However, Mandell (2008a) in his study of high school seniors reported that high school classes in money management and personal finance did not necessarily increase financial literacy. Other researchers also question the efficacy of the effectiveness of financial literacy intervention in changing financial behaviors and have found no correlation between interventions and changes in financial choices and behaviors (Adams and Rau, 2011; Collins and O’Rourke, 2010; Hastings et al., 2013; Willis, 2008, 2011). These researchers recommended that educators must take into account various factors such as cognitive and emotional status, personality factors, attitudes, and age when developing educational interventions.

Researchers have suggested different techniques for improving financial education. Jarvis (2002) and Tosey (2002) highlighted the importance of experiential learning in financial literacy education. They proposed the use of role-playing, practice-based learning, simulation exercises, hands-on encounters, and group work. Johnson and Sherraden (2007) proposed a more robust approach to financial education that was integrated with financial institutions so that the students can practice what they are learning in the classroom. They called this skill financial capability. Atkinson et al. (2006) and Dixon (2006) have also suggested similar experiential approaches to financial education.

Research has shown that culture played an important role in affecting the financial literacy and behavior of consumers (Asaad, 2013; Brown et al., 2017; Petersen et al., 2015; Pirouz, 2009). Petersen et al. (2015) in their study about marketing strategies and its impact on consumer spending found that countries such as China, and those in Southeast Asia, were more restrained in making risky financial decisions in spending, saving, and borrowing. While countries such as Japan, the United States, and Middle Eastern countries were more goal oriented and aspirational in their financial choices. Brown et al. (2017) studied the financial literacy of high school students in the German-French speaking areas in Switzerland and found that students in the German-speaking side had higher financial literacy than the French-speaking students. The researchers attributed the differences to family-based financial education and socialization of the German-speaking students, which enabled them to have more independent experiences with saving, spending, and maintaining a bank account.

Financial literacy and behavior is integrated with the sociological issues our youth face; hence, cultural influences and social impacts are important factors to consider when researchers and educators are developing appropriate curriculum for teaching financial literacy to our children (Johnson and Sherraden, 2007). Warner and Agnello (2012) advocated for an integrated approach to teaching financial literacy. They argued that financial literacy must be taught in the context of the society, culture, environment, and ethics. This integrated approach would help our students to think of financial decisions as a global, civic minded, and engaged citizen, versus making decisions to benefit only themselves. The researchers argued that the financial decisions one made today not only impacted the present generation but also that of future generations. Hence, they were advocating for financial literacy education integrated with responsible citizenship education. Other researchers also argued that the didactic approach to financial literacy education limited awareness to the mechanics of financial decision making but does not address the more important issue of preparing our youth to be engaged and global citizens of the world (Arthur, 2011; Remmele and Seeber, 2012).

While many studies have been conducted in the United States and other developed countries to assess the level of financial literacy among children and adults, very few studies have been conducted in developing countries in Asia and Africa. Cole et al. (2011) studied the impact of a program that taught Indonesian households who did not have bank accounts about savings accounts and found a small increase in demand for savings accounts from people who had low financial literacy to begin with. Carpena et al. (2011) studied the impact of a video-based financial training program for low-income urban households in India. They measured numeracy skills, basic financial knowledge, and attitude toward financial decisions and found no effect on increasing financial numeracy, but did find an increase in awareness of financial products and financial planning tools. Agarwal et al. (2015) used the three basic financial literacy questions in Lusardi and Mitchell (2009) to measure financial literacy among a sample of adults in India who used an online investment service. They found high levels of financial literacy in their sample with close to 80% answering all three questions correctly. The World Bank initiated FinScope surveys which mainly focused on financial access and behavior among adults have been conducted in several African and Asian countries and found low levels of financial access in general (Xu and Zia, 2012).

India as a country ranked poorly in economic/financial literacy, coming in below Asian countries like Thailand and the Philippines (Jappelli, 2010). According to the results of the global survey conducted by Standard & Poor’s Financial Services LLC (S&P) released in 2015, 76% of Indian adults surveyed lacked financial literacy. Similarly, VISA conducted a survey on Global Financial Literacy in 2012 and India was the least financially literate country. Agarwala et al. (2012) administered a financial literacy survey in partnership with Citibank to students, young employees, and the retired in India, and the results showed that less than 25% had some financial literacy. Kiliyanni and Sivaraman (2016) measured financial literacy among educated young adults in the Indian state of Kerala and found that they were able to answer only 44% of the questions on the survey correctly. The study also found that gender, age, occupation, religion, education, marital status, the discipline of study, work experience, parents’ education and their occupation, and income influenced financial literacy. Singh and Kumar (2017) studied financial literacy among women in India and they posited that the reasons for poor financial literacy among women in India were lower literacy rate, social and cultural expectations of a woman’s role, underlying fear of failure, and financial and infrastructural barriers. They also highlighted the importance of financial literacy among women to increase life expectancy, creating innovations in financial products and services, and enabling individuals to make educated financial decisions in changing family structures. These statistics demonstrate a need to improve financial education among all age groups in India. Some financial literacy programs, such as the credit counseling centers run by the Reserve Bank of India and their interactive financial literacy website, have been set up in the recent past in recognition of the need to improve financial literacy, but the focus has been only on adults. There are not many financial literacy programs focused on high school students. There is also not much research on financial literacy among high school students in India.

Thus, evidence from research and surveys suggest that financial illiteracy is widespread among the Indian population. Raghuram Rajan, the ex-governor of Reserve Bank of India, advocated for financial literacy to be incorporated into the school curriculum at all levels. 1 He proposed that by doing so, the younger generation will have better understanding of finances and will enable them to make educated financial decisions. Thus, it is important to conduct research to get a better understanding of what high school students know about financial literacy and to get a better understanding of their level of knowledge on various aspects of financial literacy.

The first step in improving financial literacy among young people in developing countries is to measure the levels of financial literacy across various dimensions so that it can inform the design of effective intervention programs and policy. There is substantial variation in how financial literacy is measured (Hung et al., 2009; Huston, 2010). Most studies employed either a performance test or a self-report test or both. Performance tests assessed knowledge in the savings, investments, and debt domains, while self-report tests assess perceived knowledge in these domains. This study contributes to the financial literacy literature and policy making by taking this first step of measuring financial literacy among high school students in India.

A brief description of the education system in India is provided below to give context for this study. Historically, education in India was privy only to students who belonged to the upper caste (Cheney et al., 2005). However, with legislative changes, equal educational opportunities for all students have become a reality now. Schools in India are either government funded or privately funded. The medium of instruction is either English or the local language. The curriculum in the schools is influenced by the exams students take at the end of 10th and 12th standards (i.e. Central Board of Secondary Education (CBSE), the Council for the Indian School Certificate Examinations (CISCE), the National Open School (NOS) for distance education or the State curriculum). Higher secondary level students in India can choose to pursue one of three streams – business studies, science, or arts. The business study stream includes subjects such as economics, accounting, business, and mathematics. The science stream focuses on subjects such as physics, chemistry, biology (botany and zoology), and mathematics. The arts stream includes subjects such as history, geography, political science, philosophy, psychology, languages, arts, and music.

Conceptual framework

As discussed in the “Introduction” section, the concept of financial literacy can be viewed from different perspectives. The most common approach has been to view financial literacy from a personal financial responsibility perspective. This approach tended to place all of the responsibility for financial problems on the individual and failed to acknowledge the role and responsibility of financial institutions and the government. The 2008 financial crisis was a revealing example of the role of financial institutions and governments in financial problems. Thus, researchers such as Davies (2015) proposed viewing the concept of financial literacy from the perspective of a citizen’s role in a democracy. Along with personal financial responsibility and behavior, financial literacy should also extend to one’s knowledge of the financial sector (Davies, 2015). This study adopted the personal financial responsibility perspective and defined financial literacy as knowledge of saving (compound interest/inflation), borrowing, investing, and insurance/risk management. Our definition is similar to other personal consumer responsibility–based definitions in the literature (Atkinson et al., 2007; Atkinson and Messy, 2012; Huston, 2010; Messy and Monticone, 2012). Based on the above definition of financial literacy, this study attempted to measure financial literacy levels among high school students in India.

Research question

The literature review above highlighted the paucity of literature measuring financial literacy in Asian countries. In particular, there were very few financial literacy studies in Southeast Asian countries such as India. Moreover, further research is needed to better understand the factors that impact financial literacy among different populations. This knowledge is vital to informing the creation of effective educational policies and curriculum aimed at improving financial literacy among young people. This study attempted to measure financial literacy levels among high school students in India. The impact of various factors (gender, education stream, grade, medium of education, parent’s level of education, student’s future education plans, financial knowledge self-assessment, family income, amount of financial education, parental involvement) on financial literacy levels was investigated. Based on prior research reviewed above, this study hypothesized that financial literacy levels among high school students in India will be low and below that of other developed countries. This study also hypothesized that significant differences in financial literacy will be found for all the factors listed above.

Methods

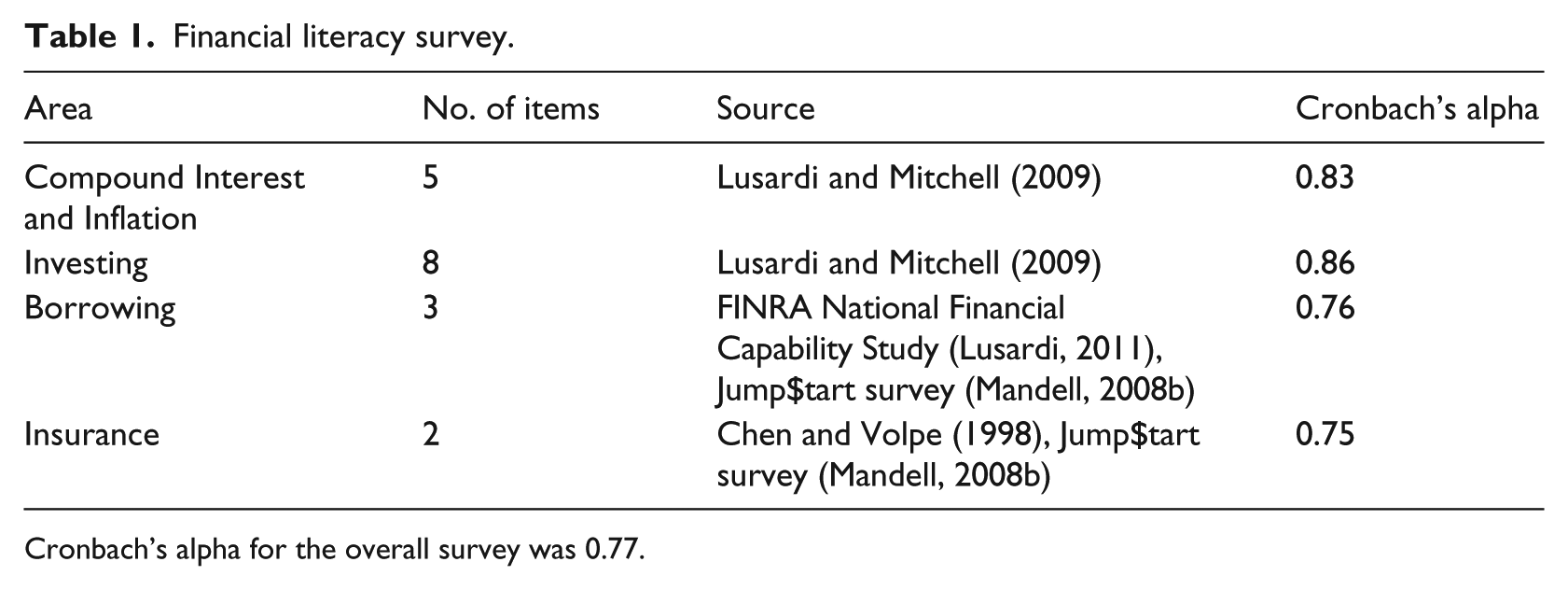

This study used a survey research design. A survey was used to measure financial literacy. The survey attempted to test performance in four domains of financial literacy – saving (compound interest/inflation), investing, borrowing, and insurance. The survey was designed by adapting different surveys from extant literature on measuring financial literacy. The survey consisted of 28 questions including questions on demographics. The survey details are summarized in Table 1.

Financial literacy survey.

Cronbach’s alpha for the overall survey was 0.77.

The compound interest section in the survey was referred to as basic financial literacy and the investing section was referred to as sophisticated financial literacy in the literature. The “do not know/refuse to answer” response option was omitted from the original questions in Lusardi and Mitchell (2009) in line with other studies (Erner et al., 2016; Mandell, 2008b; PISA OECD, 2012). Minor changes, such as changing dollars to rupees (the Indian currency) and changing names to Indian names, were made to some questions in order to fit the Indian context.

The survey had a demographics section that obtained standard information such as gender, grade, race, income, and parental education. The survey also had a question that asked the student to self-assess their knowledge of finance and economics on a scale of 1–5. Parental involvement was measured with a question on what financial matters the student’s parents discuss with them.

Sample

The survey was conducted in two of the largest cities (Chennai and Madurai) in the south Indian state of Tamil Nadu. The sample was a purposive sample. The survey was administered to 620 high school students in grades 10, 11, and 12 across three schools. The three schools were selected based on the author’s prior relationship with the school. The survey was translated to Tamil in the two schools in Chennai because they were Tamil medium schools. The survey was administered in English in the school in Madurai, since the medium of instruction was English in that school. We excluded 12 participants due to incomplete data resulting in a sample of N = 608. Two schools in Chennai were girls’ schools and the one in Madurai was co-educational, so, our sample consisted of 479 females and 129 males. There were 343 students pursuing the commerce stream and 265 students pursuing the science stream. A total of 167 students were in grade 10, 269 in grade 11, and 172 in grade 12.

Procedure

The surveys were administered to the students in school, by their teachers. The researchers were available at the school to answer any questions that may arise. The teachers were asked not to help the children with answering the questions. The researchers also had informal interviews with students in the three schools to learn about their perceptions about financial education.

Analysis

In keeping with the literature, we examined percentage correct scores (PCS) defined as the number of correct answers divided by the total number of questions. A mean PCS was computed for the entire survey, to provide an overall measure of financial literacy. Mean PCSs were also computed for each of the subscales to provide a measure of basic financial literacy, sophisticated financial literacy, knowledge of borrowing, and insurance.

The reliability of the survey questions was examined by looking at the pairwise correlation between the items. All correlations except the correlations for the question on mutual fund knowledge in the investing section were statistically significant (p < 0.05). The low correlations for the mutual fund knowledge question may be due to the very low rate of correct responses for the question. Cronbach’s alpha reliability measure for the survey was 0.77. The reliability of these questions has also been shown in the literature (Erner et al., 2016). Moreover, these questions, especially the basic financial literacy questions, have been used in numerous surveys over the past several years, confirming the validity of the questions.

One-factor analyses of variance (ANOVAs) were performed in order to answer questions such as does financial literacy differ by gender and grade. ANOVAs were repeated for each of the subscales – investing, borrowing, compound interest/inflation, and insurance – to investigate differences in each of these variables by gender, grade, and so on.

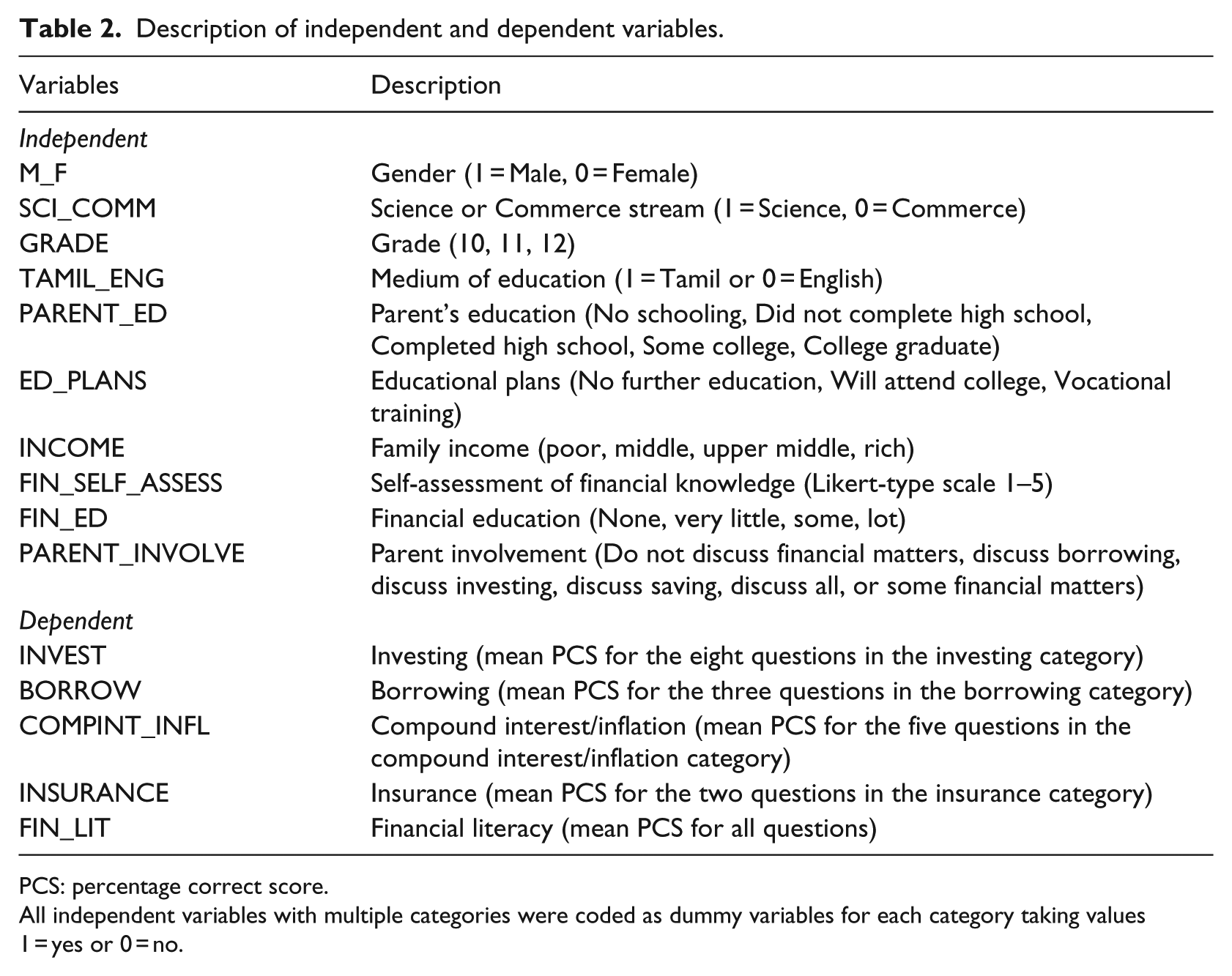

Table 2 shows the dependent and independent variables used in the analysis and their definitions.

Description of independent and dependent variables.

PCS: percentage correct score.

All independent variables with multiple categories were coded as dummy variables for each category taking values 1 = yes or 0 = no.

Results

Financial literacy levels

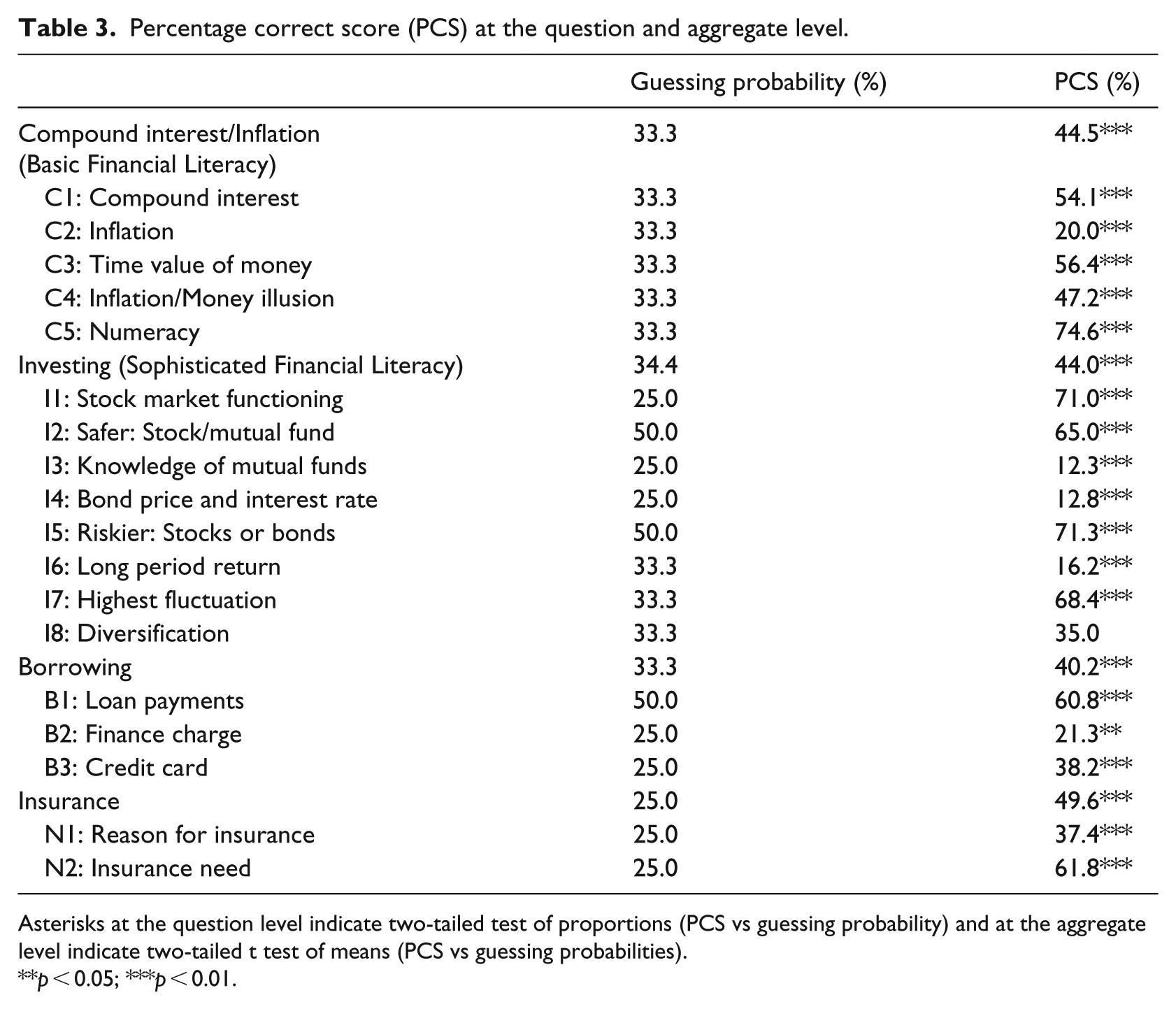

The PCS statistics for the financial literacy measures are presented in Table 3. The mean PCS across all students on the compound interest/inflation section, referred to as basic financial literacy in the literature, was 44.5%. The mean PCS for the investing section, referred to as sophisticated financial literacy in the literature, was 44%. The mean PCS for the borrowing section was 40.2% and for the insurance section was 49.6%. The mean PCS for the different sections were all significantly different from the guessing probability (p < 0.01). The PCS for all the individual questions, except for I8 dealing with diversification and B2 dealing with finance charge, were significantly different from the guessing probability at the 1% level. The fact that the PCS was statistically different from the guessing probability implies that the majority of the students did not just guess the answers to the questions.

Percentage correct score (PCS) at the question and aggregate level.

Asterisks at the question level indicate two-tailed test of proportions (PCS vs guessing probability) and at the aggregate level indicate two-tailed t test of means (PCS vs guessing probabilities).

p < 0.05; ***p < 0.01.

Students scored the lowest (12%) on questions I3, I4, and I6 which deal with knowledge of mutual funds, the relationship between bond prices and interest rates, and asset return fluctuation over long periods, respectively. The highest scores (75%) were obtained on question C5, which evaluated numeracy. This is not surprising as most high school students in India are expected to be proficient with basic math skills. What is interesting, though, is that the students seem to find it harder to apply these math skills to question C1 on compound interest calculation which is only a slight variation on the numeracy question, as only 54% are able to get the correct answer. Another interesting fact to note is that the students had a much lower PCS (20%) on question C2 on understanding of inflation as opposed to question C4 (47%) which deals with the same understanding of inflation but without using the technical term.

Differences in financial literacy among various groups

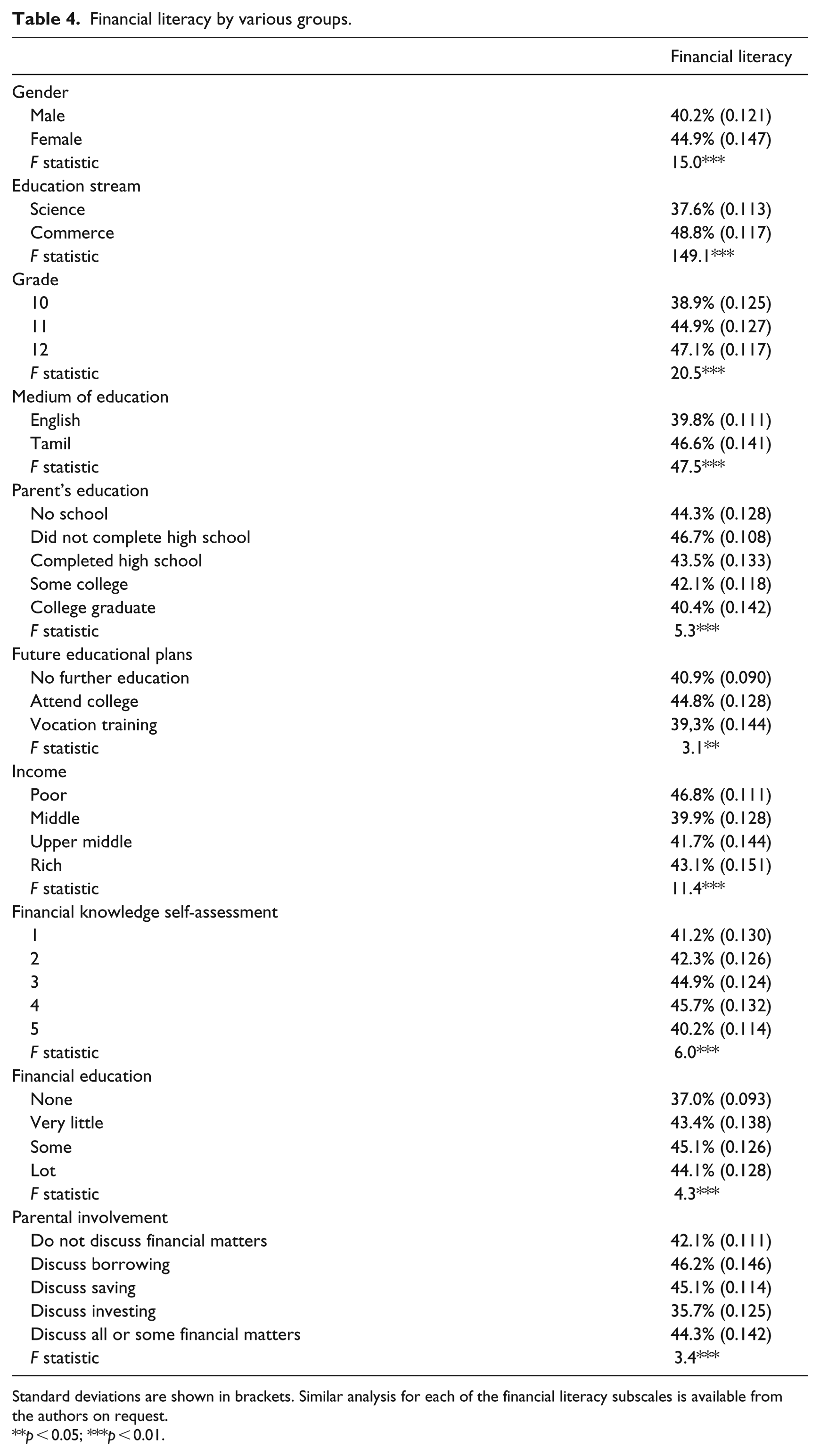

The mean PCS of various groups and the F statistic from an analysis of variance (ANOVA) to test the difference in financial literacy between the groups are presented in Table 4.

Financial literacy by various groups.

Standard deviations are shown in brackets. Similar analysis for each of the financial literacy subscales is available from the authors on request.

p < 0.05; ***p < 0.01.

There was a significant (p < 0.01) gender difference in financial literacy with females scoring higher than males. Since the proportion of females was larger than males in our sample, we wanted to check if this imbalance had any effect on the results. So, we re-ran the results by constructing a balanced sample by randomly selecting 129 female students (to equal the number of male students) from the 479 females in our sample and combining them with the males to create a gender balanced sample with N = 258. We created 100 such balanced samples with 100 such random draws. We re-ran the mean PCS on each of the 100 samples and computed the mean of the mean PCS across the 100 samples. We found that the results reported did not change significantly even when the sample was balanced between males and females (balanced sample mean male PCS was 40.26% vs an unbalanced sample mean of 40.26% and balanced sample mean female PCS was 45.31% vs an unbalanced sample mean of 45.14%). There was a significant (p < 0.01) difference in the level of financial literacy between students pursuing the commerce stream of education versus the science stream, with the commerce stream being 11% higher. The difference in financial literacy levels between Tamil (the local language) versus English as a medium of education was also significant (p < 0.01), with students in Tamil medium schools showing a 7% higher level. While this result does seem a bit surprising, we believe that this difference is mediated by the gender difference, since all the Tamil medium students were females in our sample. When controlling for gender differences, this difference indeed became insignificant.

Financial literacy differed significantly (p < 0.01) by family income; students from poor families showed a 4% higher level than students from rich families.

Difference in financial literacy based on parent’s education was significant (p < 0.01). Tukey tests indicated that the statistical significance was driven by the financial literacy of students with parents having some high school education being 7% higher than parents who are college graduates. This was a bit contrary to intuition, but we hypothesized that this result was related to the result found for family income, as people with low levels of education tended to be poorer.

Students who planned to attend college tended to have 4% higher financial literacy than those who do not plan to attend college (p < 0.01). This finding was also in line with expectations as students who planned to attend college were more motivated and were aware of their finances as they planned and saved for college.

Students who self-assessed their financial knowledge to be high seemed to have higher financial literacy (p < 0.01) indicating that students were able to self-assess their knowledge fairly accurately. Also students with parents who discussed financial matters with them had higher financial literacy (p < 0.01).

The student interviews mostly corroborated the results found in the survey. For example, students had the least awareness and knowledge of sophisticated investing, such as stocks and bonds. Most of them mentioned that they would just invest their money in a savings account in a bank. Another theme that emerged out of the interviews was how little the children understood the macroeconomic social impact of their individual financial decisions. Almost everyone thought that their spending and saving habits had no impact on another person’s financial well-being and the society as a whole. One student said, “My parents always said that it was bad to borrow money and that you needed to pay off your debts as soon as possible,” but did not realize that someone could borrow money to start a business and thereby contribute to the society and economy. This “borrowing is bad” theme was also echoed by almost every student. Similarly, most students mentioned that their parents constantly mentioned the need to save money for a rainy day (corroborating survey finding), but again failed to make the connection between individual savings and the greater good of the economy and the society. Hearing these surprising themes emerge from the interviews, the researchers pressed on to see if the students were aware that their choice to attend college could affect the society and economy in the future. Here, a few students acknowledged that it was good for the society if they got educated, but a vast majority did not think that there would be a significant impact in terms of the betterment of society and the country as a whole. The relationship between education and macroeconomics was not adequately recognized by most students. When told about the macroeconomic impact of their financial choices, they were surprised to learn about the influence of their spending, borrowing, and education on the broader society. They said that teaching such type of macrolevel information would help them see the relationship between their own financial habits and the impact it has on the society and encourage them to make appropriate financial decisions.

Discussion

The above results highlighted the low levels of financial literacy among high school students in India and demonstrated the need for increasing the financial knowledge of students. The overall financial literacy (44%) was quite low when compared to other developed countries and some developing countries. The basic financial literacy and sophisticated financial literacy levels among high school students in India were lower than financial literacy among high school students in the United States (47.5% as reported by the 2008 Jump$tart survey) and lower than other developed countries such as Germany (64% basic financial literacy and 54% sophisticated financial literacy as reported by Erner et al. (2016)). In this study, the students scored in the medium range in the areas of compound interest, investing, borrowing, and insurance. However, their performance in the areas of mutual funds, relationship between bonds prices and interest rates, and asset return fluctuations were low. This was understandable as the questions in these areas were among the most difficult questions in the survey and needed specialized knowledge to answer. Similar results have been found with high school students in Germany (Erner et al., 2016).

Results also showed that students did well on numeracy questions but were unable to transfer that knowledge to do financial computations in other questions. Lusardi and Mitchell (2009) found similar results when they surveyed 18 year olds and older adults in the United States about their financial knowledge. Cameron et al. (2013) also found similar results in their study of personal financial literacy among high school students in New Zealand, the United States, and Japan. Even though all the students had low financial literacy, the Japanese students demonstrated a disconnect between theory and application like the Indian students in our sample. Another interesting result was that students scored low on the question about inflation (C2) but scored much higher on a similar question (C4) that dealt with the same concept of inflation but without using the technical term. This seemed to indicate that students understood the concept of inflation in an intuitive way, but were not aware of the technical term, as they had not been exposed to the term. These findings suggest the need to have a robust financial literacy curriculum that is integrated across a variety of content areas.

The significant gender differences in financial literacy levels with the girls scoring higher was an interesting finding. This is in contrast to the literature which has shown that females have lower financial literacy levels in developed countries (Erner et al., 2016; Lusardi and Mitchell, 2009; Lyons, 2004; Van Rooij et al., 2011). One possible reason for females outperforming males in this study could be that in the Indian culture young women in the family are quite involved in the day-to-day running of the family and are aware of the management of the family finances and hence could be more financially literate. However, Singh and Kumar (2017) pointed out that even though Indian women are adept at managing the day-to-day finances, they still deferred to their husbands, fathers, or brothers to make decisions about investments. Further research needs to be done to investigate various ways to improve the financial literacy of girls to help them become more sophisticated in their financial decision making and empower them to become contributing members of the society.

Results showed that the commerce stream students did better than the science stream students. This was as expected since the students in the commerce stream received education in economics and finance as part of their curriculum. This difference also pointed to the fact that economics/finance education could be effective in increasing financial literacy. Moreover, students who reported having had some financial education fared better on our survey, further lending support for financial education as a means of increasing financial literacy. This finding also suggests that the science stream students could benefit from additional financial literacy education. A policy implication of this finding could be to add some parts of the commerce curriculum to the science curriculum, in order to increase the financial literacy of the science stream students as well. These findings lend support to the proposal put forth by the ex-governor of the Reserve Bank of India, Raghuram Rajan, to incorporate financial education classes as a part of the curriculum in all schools. The government of India has created the National Center for Financial Education, which comprised financial regulatory bodies and educational partners to make India more financially literate. This center offers a variety of financial educational programs and materials for all age groups. They also offer the NFLAT (National Financial Literacy Assessment Test) for 6th–8th grades and 9th–10th grade students. However, attention should be paid to incorporating aspects of societal, environmental, and ethical engagement in such programs. Arthur (2011) advocated for financial literacy education integrated with civic engagement education, which might perhaps provide opportunities for the students to understand about finance and economics in a larger context.

Results showed that students from lower income families had a higher financial literacy compared to their peers from high-income families. This was contradictory to previous research that showed that children from families with adequate and plenty of financial resources were more financially literate than those that came from families that had less financial resources (Aizcorbe et al., 2003; Mandell, 2008). A possible explanation for this difference could be that poor families focus more on saving, budgeting, and planning in order to run their families on a meager income and hence show greater financial literacy. Most likely, the low income students were aware of the financial status of their families and the strategies their parents used to manage their budgets. This exposure to real-life experiences helped them have a better understanding of financial issues. Again, further research needs to be done to validate this theory.

Students who self-assessed their financial knowledge to be high had higher financial literacy (p < 0.01) indicating that students were able to self-assess their knowledge fairly accurately. This is in line with the work by Lusardi and Mitchell (2009) that demonstrated that self-assessment is consistent with actual knowledge.

Results showed that students whose parents discussed financial matters with them have higher financial literacy (p < 0.01). This finding lends credence to involving the family and the community in the financial education of school students. A policy implication could be to encourage schools to implement curriculum (projects, etc.) that involve the student’s family and community in order to encourage parents to discuss financial matters with their children. Singh and Kumar (2017) also validated the importance of family discussion and participation in financial matters as a means to empower women to become financially literate.

Interviews with students revealed that there was a lack of understanding of the link between individual’s financial choices and its impact on the society and economy. This definitely warrants further research about changes in the curriculum and teaching strategies that would enable the students to learn about financial literacy in a social context. Many researchers have advocated for such an approach to teaching financial literacy (e.g. Amagir et al., 2017; Arthur, 2011; Remmele and Seeber, 2012; Warner and Agnello, 2012). The borrowing is bad and savings is good theme that we encountered in our interviews has a distinct cultural root. The Indian culture (and many eastern cultures) attaches a negative connotation to borrowing and borrowing is generally frowned upon, while the western culture does not attach such a negative connotation to borrowing, which is the reason that household debt levels are much higher in the west (OECD, 2017). Similarly, the Indian culture (and many eastern cultures) places a great deal of importance on saving money to tide over economic hardships, and this is borne out by the fact that India has one of the highest savings as a percentage of GDP in the world, in the 32% range, while the United States has one of the lowest savings rate in the 18% range (The World Bank, 2017).

All of the above results showed that the financial literacy levels of high school students in India were low and there is a need to develop policies, educational curriculum, and strategies to increase the financial knowledge of students. These results have to be interpreted in light of the fact that the jury is still out on whether increased financial knowledge translates to better financial behavior and decision making. The seminal work of Bernheim et al. (2001) found that middle age individuals who took a personal finance course in high school tended to save a higher proportion of their income than others who did not. Several other studies since then have also found positive correlations between financial literacy and day-to-day financial management skills, participation in financial markets, retirement planning, accumulation of wealth, and protecting one’s wealth (Almenberg and Dreber, 2011; Ameriks et al., 2003; Arrondel et al., 2012; Christelis et al., 2010; Hilgert et al., 2003; Hung et al., 2009; Lusardi and Mitchell, 2007; Stango and Zinman, 2008; Van Rooij et al., 2011; Yoong, 2011). Most of these studies were correlational and not causational. Research on causality between financial literacy and appropriate financial behaviors is very limited. Mandell and Klein (2009) investigated a more direct impact of financial education on high school students and found that those who took a financial education course did not rate themselves as more savings oriented and did not seem to have better financial behavior than those who did not take the course. This study had a small sample size and caution should be exercised in generalizing the findings. However, Mandell (2009) using the much larger sample of biennial Jump$tart surveys came to a similar conclusion that a high school class in personal finance did not have much impact on financial behavior. Another drawback with these studies is that they measured financial behavior when the students were young adults who are not yet financially stable. Perhaps the financial knowledge is more useful to decision making later in life when one is more financially stable. Thus, there is inconclusive evidence on the relationship between financial education and financial decision making later in life.

Another cause for caution when interpreting our results is the question of whether the tested financial knowledge is relevant for the actual day-to-day life of the young adult. Certain aspects of the knowledge tested, mainly the investing section, may not be immediately relevant to a young adult as most young adults are just starting to earn and thus are less likely to participate in financial markets. Mandell and Klein (2009) allude to this fact, but do concede in their conclusion that it is possible that this financial knowledge may be useful later in life as they become more financially stable. Bernheim et al.’s (2001) study with middle-aged people also seems to suggest that sophisticated financial knowledge that is gained in high school can be useful much later in life.

This ambivalence in the literature regarding the efficacy of financial education makes it even more important to focus on the content and the educational methods used to deliver financial education to students. It is essential to incorporate teaching methods that will engage the students in applying what they are learning in the classrooms. Many researchers have advocated for the use of experiential learning techniques in financial education (Jarvis, 2002; Johnson and Sherraden, 2007; Tosey, 2002). Thus, teachers should infuse their curriculum with hands-on activities such as stock market simulations that provide the student with practical financial experiences and teach the student the impact of making financial decisions.

Educators and policy makers should also strive to get a holistic understanding of financial literacy so that they can facilitate more effective financial education. As Davies (2015) suggested, financial literacy should not be looked at as a unidimensional concept related to a consumer’s knowledge and behavior, but as a multidimensional concept comprising the intertwined roles of the consumer, financial entities, and the government. Hence, financial education should integrate experiential teaching strategies that involve various financial entities and governmental agencies. Doing so will enable the students to understand not only the microeconomic impacts of their financial practices but also that of the macroeconomic impacts as well. The interviews with students, as mentioned in the results section, highlighted the disconnect between personal financial behavior and macroeconomic impact. Thus, it is important that financial literacy curricula incorporate teaching of the impact of personal financial decisions on the economy as a whole.

Financial literacy education should also have concepts such as culture, ethics, environment, and well-being of the society embedded in it, in order to create awareness among our youth that the decisions they make can affect others around them and future generations as well (Warner and Agnello, 2012). Also one should not underestimate the power of parental/community involvement and technology in improving financial literacy. As evidenced in this study, parents play a powerful role in educating their children about financial choices and financial well-being. Hence, it is important to involve the parents as partners in the financial education of children. Finally, it is of utmost importance to adequately train the teachers to teach financial literacy in an integrated manner that will enable the students to become active users of their financial knowledge. Teachers should also be trained in appropriately using technology to teach the content and actively engage the students.

Conclusion

The results from this study give educators, policy makers, curriculum designers, and finance professionals an awareness of the level of financial literacy among high school students in India. This information will be useful for them to engage with each other to develop strategies and design effective policies to improve financial literacy among young people. While there are some laudable efforts by programs like Money-Wizards and Pocket Money to bring hands-on financial literacy education to school children in India, there is still much to be done to integrate experiential learning into the financial literacy curriculum at schools.

Further research needs to be done to replicate our findings in other parts of India and in other developing countries. Research studies using an experimental design should investigate the causal link between financial education and financial decision making. More research needs to be done to identify effective methods of delivering financial education. Designing holistic and effective financial literacy curricula is another area for further research. Use of cutting edge learning technologies to deliver effective financial education is yet another direction for future research.

India has a long way to go in increasing the financial literacy of its people. Studies such as this one add to the much needed knowledge base about the financial literacy of Indians. It is our hope that the results of this study contribute to raising awareness of financial literacy in India and help in policy making that brings financial literacy programs to the masses. This will prevent people from making bad decisions that will impact the economy, environment, and social well-being of the community in a rapidly growing country like India. The results from this study, despite being from an Indian sample, also provide valuable information for policy makers and educators in similar developing countries around the world.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.