Abstract

Unlike historical and biological topics, economic topics are seldom dealt with in documentations on television. They are to be found in consumer advice programmes or recently in so-called help formats. Advice programmes of this kind which are based on the life story of a family or an individual person have meanwhile become an integral part of all television programmes. They are responding to the need for advice in society, which also includes economic issues and offensively resort to entertainment in order to achieve their goal (section 1). However, it remains unclear what the audience actually learns. Hill poses this question and formulates an ‘idea of learning’ that lies in store for the audience with these formats. With the help of a multistage test design, the television format ‘Out of Debt’ (section 3) shall be examined for a potential learning contribution among adolescent consumers (section 4).

Informal learning via television

In the Anglo-Saxon discussion, Annette Hill’s ‘idea of learning’ dominates the media education debate on informal learning via television. Hill (2005) provocatively poses the question ‘What can we learn from watching reality TV?’(p. 79). She discusses the education processes evoked by reality TV formats. First and foremost, these programmes serve voyeuristic needs. However, do people really learn something by watching Supernanny, Animal Hospital or Children’s Hospital? Do they receive information on education and a healthy life style in these formats? And does it encourage the audience to change their way of raising their children?

In one of her studies, Hill (2000, 2005) reports that on the part of the audience of such programmes, an ‘idea of learning’ was developed: Although the tabloid news connection is often used as evidence of the ‘dumbing down’ of factual television, the connection can also be used as evidence of the way reality TV attempts to present information to audience who want to be entertained and informed at the same time. (p. 80)

This corresponds to Corner’s (1995) arguments who writes ‘that television is a “message system” that is received “in private,” but has a strong “public” character’ (p. 11). The public character is linked to news and information (Corner, 1996, 2000). However, ‘television invites viewers into empathy and understanding. It creates a virtual community of the commonly concerned, of vicarious witness; to cut through accommodating abstraction with the force and surprise of “things themselves”’ (Corner, 1995: 31).

Since reality TV in fact does not aim at this public character it is capable of binding the aforementioned virtual community. The viewing figures prove this impressively. In order to achieve this, the traditional counselling programmes as they have been broadcasted since the 1980s and that rather remind of a formal educational process had to be redefined. While until the end of the 1990s only two format types were known – the so-called infospot and the monothematic magazine – the variety of formats is significantly higher today: Servotainment magazines such as, for instance, the German ARD-Buffet, coaching shows such as the internationally marketed format Supernanny as well as call-in programmes and especially makeover formats are not only very popular in Germany. 1 Yet they thematically cover similar fields such as programmes in previous times. Some people also believe (Renner, 2008) that the variety has even decreased. 2

The journalistic role, however, has changed significantly. The coaching formats are no longer limited to mere advice in the sense of knowledge transfer in an almost formal setting, but they want to offer practical help as well to those seeking advice and help (Bondebjerk, 1996). The protagonists of the formats are coaches and troubleshooters who do not only solve people’s problems but also fulfil their unfulfilled wishes. In the coaching programme Raus aus den Schulden considered here the journalist is to be found behind the camera and the moderator and presenter function is delegated to the expert.

The informal character of learning becomes apparent since Formal learning (‘the Learning Programme’) is clearly associated with primary features of a programme, whereas informal learning is more associated with secondary features. What comes first is entertainment, and any secondary pleasure may include the possibility of learning, but are optional extras.

3

The popular help formats therefore also fulfil a counselling function attributed to them by Corner 4 and incorporate this into their concept of the programme. They are aware of the fact that they are ‘imparting’ knowledge that is not or hardly ever imparted in school. They close a gap in education with their counselling that would otherwise be closed by learning by experience which is however all too often linked to a loss of money in the financial sphere which then soon leads to further problems in other areas of life.

The German help format ‘Out of Debt’

The debt problem is a topic with high entertainment potential for different television formats (Brants, 1998). For a variety of reasons, people are either close to private bankruptcy or already bankrupt and no longer know how to cope with the situation or they know other people who have been in such a situation (Glynn, 2000). In the television show ‘Out of Debt’, a programme of the private TV channel RTL, people like this are helped out of their financial predicament with advice and active support. The procedure here is always the same: the expert analyses the revenues and expenditures together with the people in question, which normally leads to the discovery of a great hole in the budget. Subsequently, he points out ways of saving money in order to overcome this hole in the budget. In the process, he also often contacts creditors or financial supporters in his function as mediator. At the end of the episode, the success of his measures is examined by means of a repeated confrontation of the new revenues and expenditures. Thus, not only the extent of the indebtedness is pointed out, but the focus is on the path that leads to the discharge of one’s debts. This also goes for the episode that was used for this study. 5 It deals with the case of the Hege family. The family consists of the mother, the father and two daughters one of whom has a boyfriend who is living with the family. Both parents are employed, the daughters still attend school.

The family lives together in a house for which it went deeply into debt. The main topic from the perspective of economic education is the handling of the loan and of the monthly financial burden resulting from this (see Schuhen and Schürkmann, 2014). This poses a constantly growing challenge to the family on a regular basis since the annuity to be paid leads to a monthly deficit (budgetary gap). This episode of the series ‘Out of debt’ can be considered as a very suitable episode for adolescents since the adolescents and the parents are both affected by financial constraints that were caused by indebtedness. Furthermore, in this episode, there is no mixing of private debts and debts from self-employment. Social problems also play a subordinate role. This facilitates the learning process on the part of the audience (Buckingham, 1996).

The success in media of this format is impressive. ‘Out of debt’ registers up to 4.65 million viewers aged from 14 to 49 years in Germany. Thus, it achieved a market share of approximately 25% (Krei, 2008).

Methodologies and hypotheses

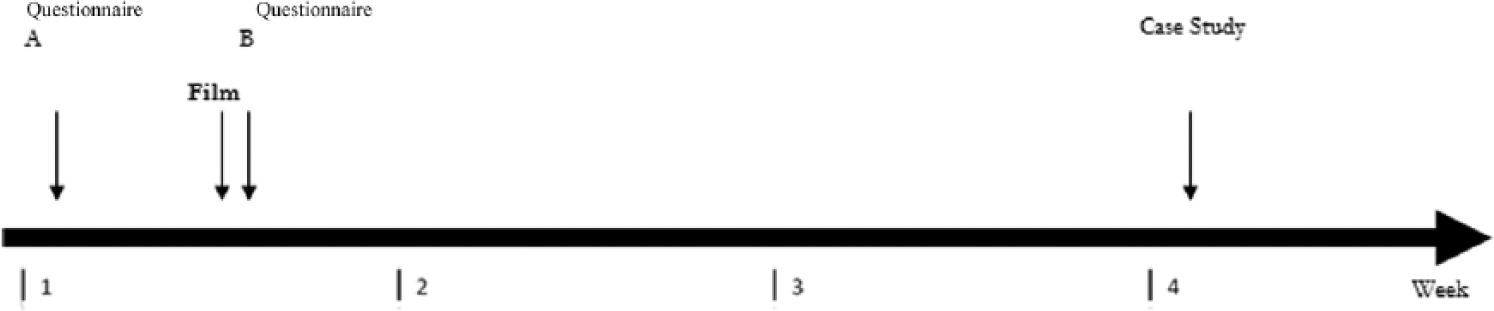

By means of an experimental design, it is examined whether or not watching an episode of ‘Out of Debt’ leads to an increase in competence in the field of economic education among pupils. Economic competence in this case is composed of two facets: of a quantitative and qualitative increase in knowledge as well as of the ability to apply this knowledge in the framework of a case study (Macha and Schuhen, 2012; Salemi, 2005; Schuhen, 2015). In the latter, economic competence manifests itself inter alia in systematic action and in decision-making. The increase in knowledge was recorded with the help of a pre-post survey (questionnaires A and B). In addition to questionnaire A, the pupils were asked to solve the Cultural Fair Intelligence Test (CFT) test as well as the vocabulary and the numerical sequence test (Weiß, 2006, 2007). Figure 1 shows the sequence of the use of the questionnaires and of the film.

Study design.

In identical questionnaires altogether 137 pupils were asked to explain the key terms concerning financial issues that were taken from the examined episode. All of the pupils were between the ages of 15 and 17 years and attended the school types: grammar school, comprehensive school or secondary school in North Rhine-Westphalia. The study was carried out, respectively, in one class of each school type and replaced one lesson there.

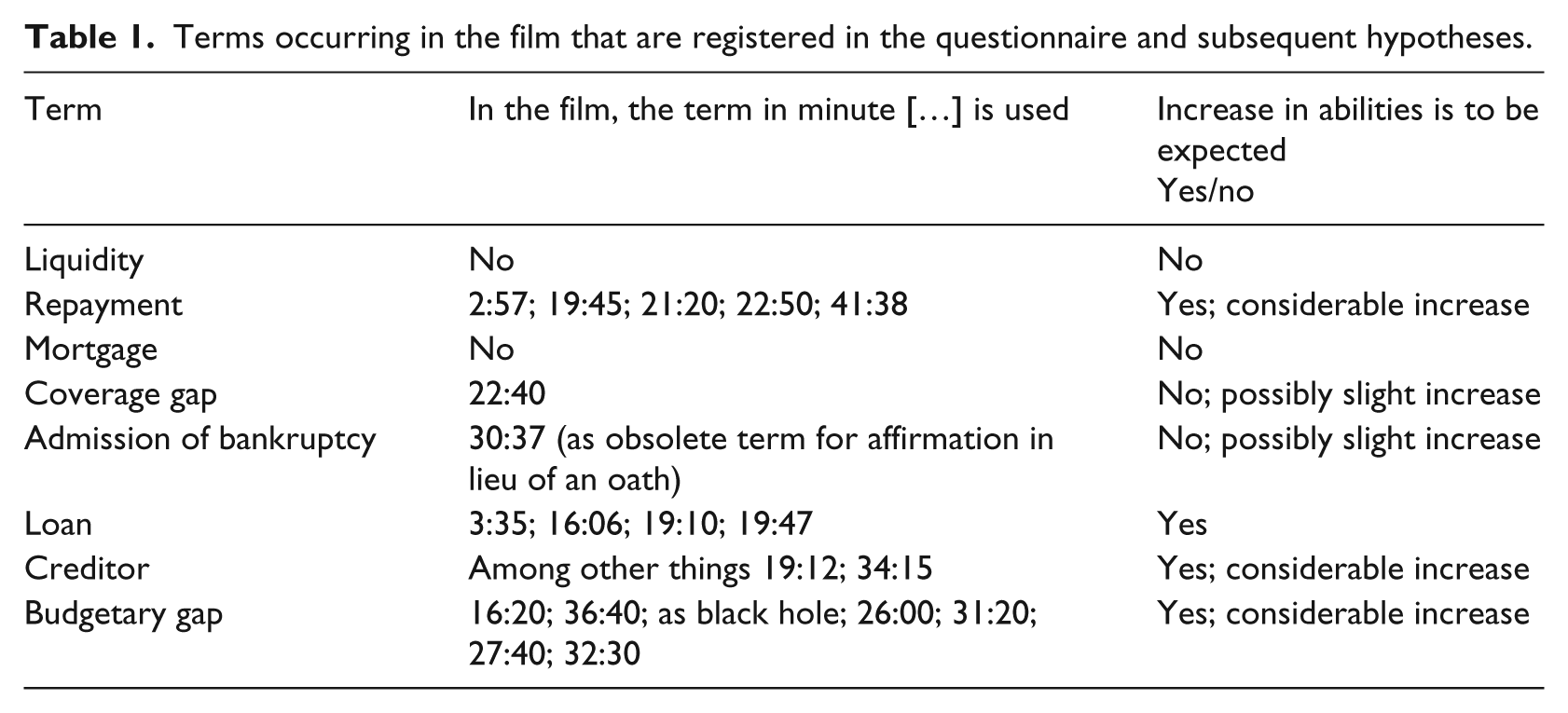

The terms concerned are designations the adolescents might at least have already heard once before. Two terms from this context (‘liquidity’ and ‘mortgage’) are not mentioned in the film but were used as control variables. The open questions require descriptions of the terms listed in Table 1. The persons questioned have to formulate their answers freely. After the recording, these answers were evaluated by two assessors by means of an assessment manual with marks from 1 (comprehensive) to 4 (unsatisfactory). In this way, the comparability of the variables could be ensured. Following the selection of the eight terms and the analysis of the film, the hypotheses concerning the increase in abilities between questionnaires A and B were formulated. They are gathered together in Table 1.

Terms occurring in the film that are registered in the questionnaire and subsequent hypotheses.

Four weeks later, the respondents had to work on the already mentioned case study. In the time between questionnaire B and the case study, the normal lessons that had been planned at the beginning of the school year took place. This was important for the investigation design because long-term increases in competence were to be recorded with the help of the case study. For comparison purposes, the case study was presented to 27 pupils who had not watched the film. It was assumed that pupils who had watched the episode would be better equipped for solving the case study even after a longer period of time than pupils who had not watched this episode. For organisational reasons, the case study could only be presented to those respondents who had also watched the film.

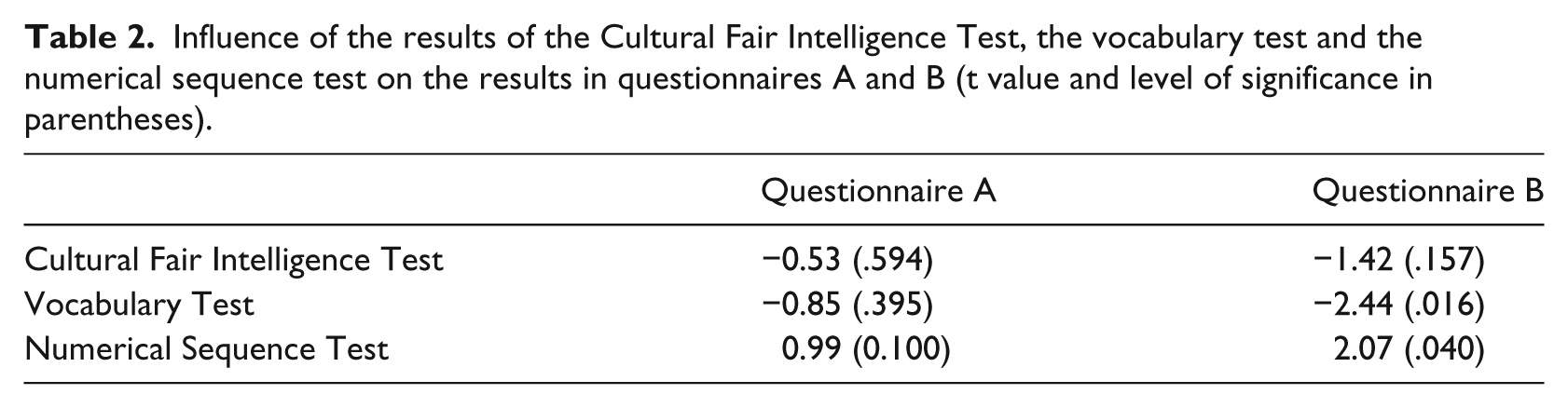

In order to ensure that general intelligence as well as numeracy and literacy skills are no essential influencing factors for the increase in economic competence, the respondents were tested regarding these variables before the investigation. The already mentioned CFT (Weiß, 2006, 2007) was used together with the vocabulary test and the numerical sequence test. The first test records general intelligence with the help of tasks in which, for example, a picture from a number of pictures is to be selected which does not fit in with the others. The vocabulary test records to what extent the respondents are able to select a term unfitting in terms of content from a series of words. The numerical sequence test records whether or not the pupils are capable of grasping the logic of a numerical sequence and of continuing it. All three are standardised (Weiß, 2006, 2007). The regression results are depicted in Table 2. As far as the questionnaires are concerned, the results of the CFT do not have a significant impact on the ability to define the terms neither in the pre- nor in the post-test. Also in the first testing period, the results from the vocabulary test and from the numerical sequence test do not have a significant influence on the ability to interpret financial terms. From this, one can draw the conclusion that neither general intelligence nor advanced mathematical or verbal skills led to better results in the initial test. As far as the results of the post-test are concerned, however, the results of the vocabulary test and of the numerical sequence test have a slight significant influence.

Influence of the results of the Cultural Fair Intelligence Test, the vocabulary test and the numerical sequence test on the results in questionnaires A and B (t value and level of significance in parentheses).

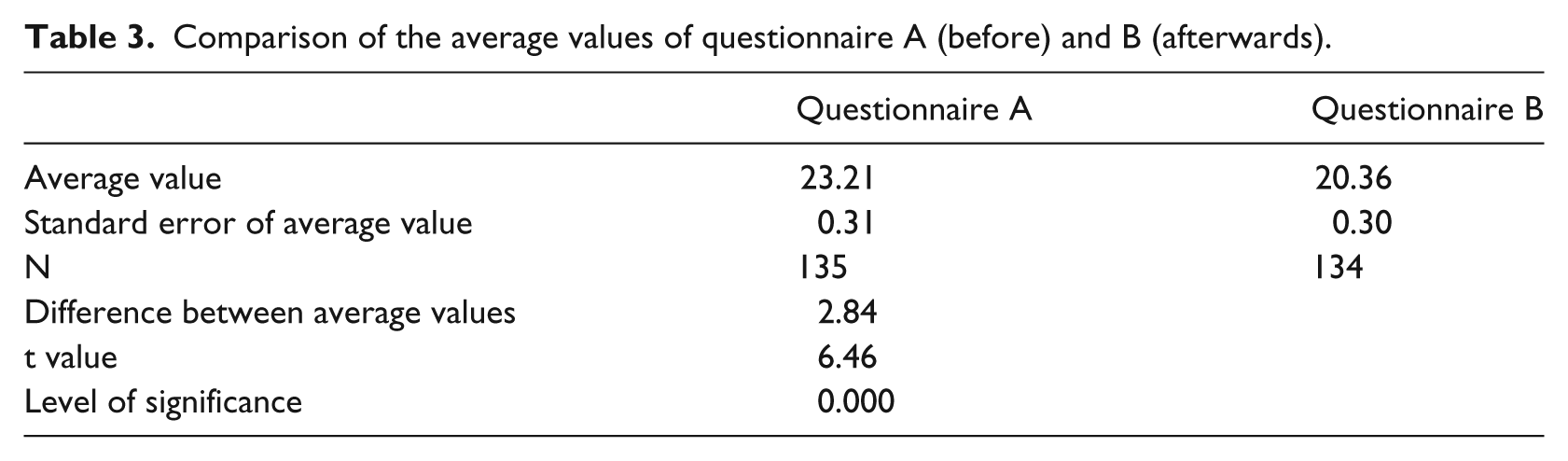

By means of a t test for connected random samples, the results of the pupils of questionnaires A and B were compared (a higher number stands for a poorer assessment/mark). A t test compares the average values between two groups in order to find significant differences. Table 3 shows the results. On average, the pupils improved by 2.84 rating points and are now on a satisfactory level.

Comparison of the average values of questionnaire A (before) and B (afterwards).

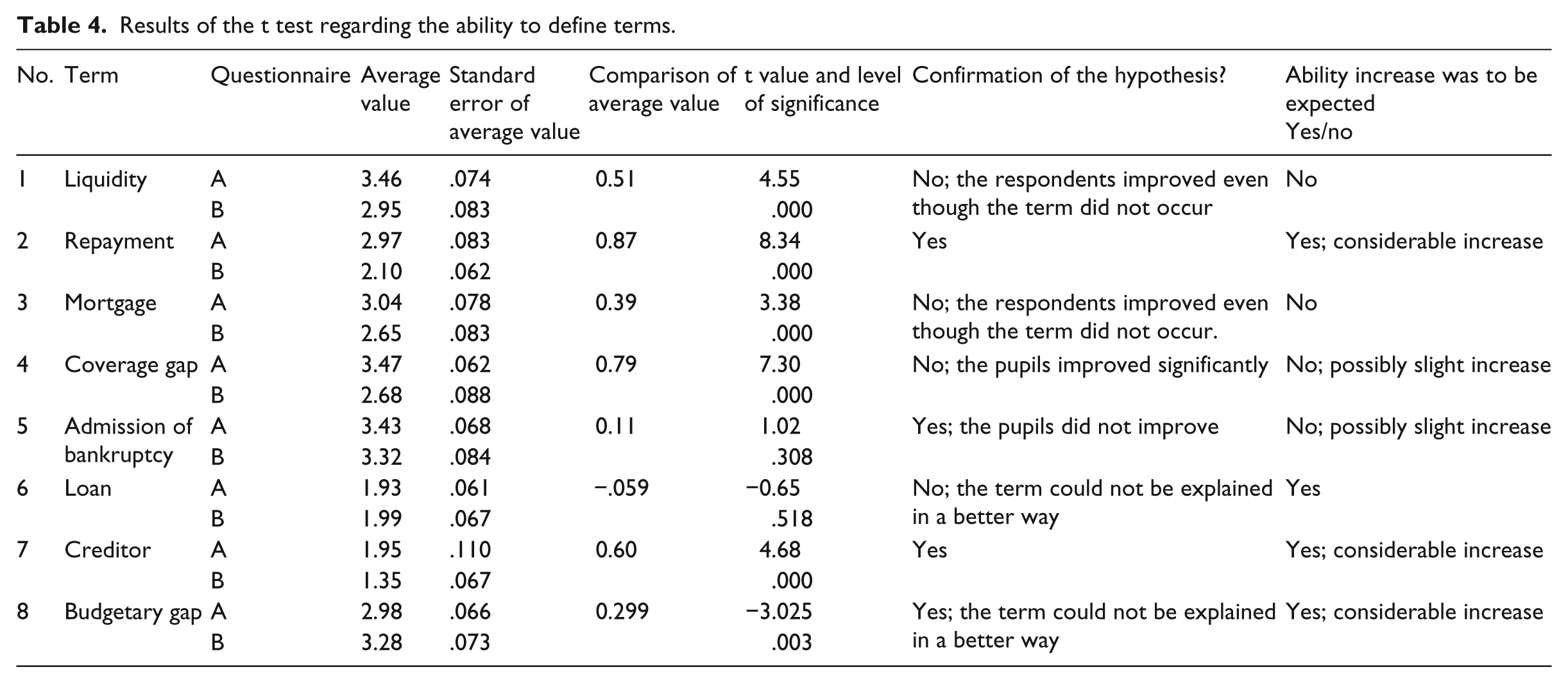

For the detailed interpretation of the results, t tests were conducted for all eight terms. Table 4 contains the results of the comparisons of the average values for each of the eight terms from questionnaires A and B. In column 8, Table 4 moreover contains the hypotheses already presented in Table 1 concerning each term. Column 9 informs whether or not the hypotheses developed at the beginning could be confirmed.

Results of the t test regarding the ability to define terms.

Results

The results show that the pupils were able to describe many of the terms that occurred in the film in a better way. They were also more able to explain terms related to the topic (liquidity and mortgage) that were not explicitly discussed. With regard to the term ‘liquidity’, this might be explained by the priming effect. Priming is the influencing of the processing of a stimulus by means of the activation of implicit memory contents by a preceding stimulus. There was no introduction to the topic before the carrying out of questionnaire A. The pupils had not been mentally stimulated for the topic. The priming stimulus that normally activates contextual information and then determines top-down how fast the subsequent stimulus (solve the task concerning the topic liquidity) is processed or if it is recognised correctly, or – in the case of ambiguous stimuli – in which way it is interpreted, was missing. The pupils also missed the target stimulus (target) that they were used to from school contexts. Nevertheless, the film might have had a priming effect which led to the fact that significantly better results could be achieved concerning the topic liquidity as well as concerning the designation mortgage because the knowledge of the pupils was contextually activated.

If a term occurs several times throughout the film, as is the case concerning the term ‘repayment’, this does lead not only to a decrease in unanswered questions in questionnaire B but also to a significant improvement in the quality of the answers given. Thus, the pupils improved by 0.87 on average regarding the term ‘repayment’.

It also becomes evident that a visualisation in the film leads to better results. Accordingly, the expert uses a flip chart as a combining element that has a dramatising effect in the story board, and this does not only go for this episode. On the flip chart he visualises the family’s revenues and expenditures and gathers data and facts which he resorts to again and again in order to justify the measures suggested by him. While in questionnaire A only few pupils understood the meaning of the term ‘coverage gap’, in the post-survey significantly more pupils were able to relate the revenues and expenditures noted on the flip chart to the term that had only been mentioned once in the episode and to calculate the coverage gap. Closely connected to the term ‘coverage gap’ is the term ‘budgetary gap’ which, however, could not be better explained in the post-survey either, even though the term had been visualised and discussed several times. This could be due to the fact that the description of this term was not selective and constantly alternating. For instance, the expert questions a married couple concerning potential budgetary gaps, hence expenditures that they forgot or withheld in their list since the balance of account does not correspond to reality on the flip chart. He talks about ‘black holes’ which leads to the fact that in questionnaire B the word ‘disappear’ is now used 20 times, whereas it does not appear in questionnaire A. Even pupils who previously argued in terms of revenues and expenditures now in questionnaire B use the word ‘forget’ for their description. Here, it becomes clear that terms can also be ‘reinterpreted’ by such consumer advice programmes.

If, however, terms are only seldom used within the story board and without visualisation or specific emphasis, there is no increase in knowledge or only a slight one. Accordingly, the term ‘admission of bankruptcy’ was introduced that was superseded by the affirmation in lieu of an oath in Germany. Even though many pupils linked the term in questionnaire B to a disclosure of ‘finances’ or to the ‘court’, only very few pupils referred to the fact that it implies the admission of not being able to repay one’s debts. This described effect can be traced back to the priming effect that has already been dealt with.

If the knowledge concerning a term was already significantly high in questionnaire A, no significant improvements could be achieved. The pupils were not able to add further features to their definitions or to identify wrong elements they had named in questionnaire A. As far as the term ‘loan’ is concerned that was mentioned altogether four times in the film, it could rather be observed that the answers in the post-test were rather shortened and therefore inferior. Only the observation regarding the term ‘creditor’ contradicts this trend statement. Especially those pupils who had still explained ‘creditor’ with ‘to authenticate’ in questionnaire A were able to describe this term better. The film showed them that a creditor is ‘the person one owes money to’. In the film, a creditor (a bank) was even visited by the protagonists. The bank fulfilled the role of a ‘friendly’ creditor since it was willing to postpone the payment of the debts in time. The protagonists even visited the creditor (a bank). The bank took over the role of a ‘nice’ creditor because it was willing to postpone the repayment. Another pupil, however, was confused by this depiction of the term creditor. In questionnaire A, he still gives the correct answer: ‘A creditor lends money to someone else and gets paid back later by instalments’. After the film, he strongly adjusts his definition according to the film: ‘A creditor is a bank employee who grants a loan to the family’. In general, several pupils (13) explained the term with the help of the term bank in questionnaire B. This was not the case in questionnaire A. The film probably led to an increase in knowledge by means of personalisation (bank) and visualisation (entering the bank building). It is however alarming when correct answers in questionnaire A lead to reduced representations (creditor = bank) due to the film.

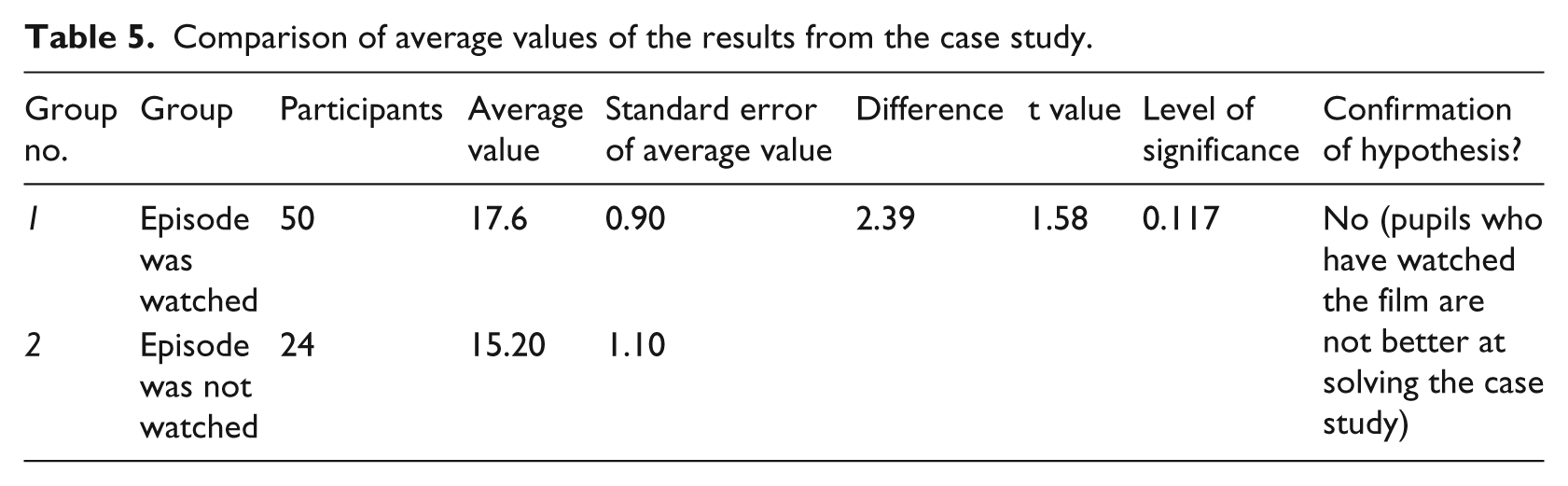

In order to check whether not only short-term increases in knowledge in the declarative field can be recorded, but whether economic competences in the sense of ‘analysing situations’, ‘applying solution strategies’ and ‘decision-making’ are also acquired by watching an episode of ‘Out of debt’, the case study already introduced in Chapter 3 was presented to the pupils for task solving after 4 weeks. In this case, we are dealing with a deliberately chosen further episode from the season ‘Out of debt’ the similar content of which was revised into a case study and provided with respective tasks by a teacher. The focus here was also on private debts that occurred due to the renovation of a house. The pupils were asked to record revenues and expenditures and to calculate a potential hole in the budget also after the additional unemployment of one of the protagonists.

Table 5 illustrates the results of the t test between group 1 that watched the episode and group 2 that did not watch the episode. Higher scores stand for a higher number of points. Group 1 reaches the average value of 17.6 rating points, which is 2.39 points more than group 2. This difference, however, is not significant. Even though the pupils learn a certain terminology by watching an episode, they are not able to apply the problem-solving strategies of the coach to a new case and to develop support strategies for the protagonists of the case study.

Comparison of average values of the results from the case study.

Conclusion

The ‘idea of learning’ in reality TV shows introduced by Hill can be partly confirmed. Declarative components of knowledge are conveyed and an increase in knowledge results among the pupils. It becomes apparent that the setting has a great influence on the learning success. Dramatic framings and visualisations have proved to be useful for learning. However, the study shows that such formats can also lead to the fact that pupils memorise terms and possibly ‘overwrite’ correct definitions when they are shortened or used in a certain context or simply used in a wrong way in the programme. Contexts that are easy to remember contribute to this. In these contexts, it can be suggested that the term used in this context is applied correctly. Correspondingly, the entertaining representation of obliviousness, for example, in combination with the reciprocal accusation of the married couple led to the fact that the term ‘budgetary gap’ was defined with obliviousness.

The statements are limited by the fact that the study was carried out during the school lessons. Here, priming effects occur as well because everything that is presented in class is relevant to learning. To what extent the measured learning effects can be reproduced in free time remains open as well.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.