Abstract

This study compares the financial knowledge of Korean (N = 1006) and German (N = 1346) university students. The country-specific adaptations of the US-American Test of Financial Literacy was used to assess financial knowledge. Financial knowledge can be divided into three areas (everyday money management; banking; insurance). German students show a slightly higher knowledge of everyday money management and insurance. Korean students tend to be stronger in the area banking. The paper examines the impact of gender on financial knowledge and the role of financial information gathering. A gender difference is determined in Germany, but not in Korea. Male students in Germany score higher than female students. An analysis of variance shows that Korean as well as German students who inform themselves more frequently about financial topics achieve a higher financial knowledge score. The article shows that it is possible to validly measure financial knowledge in Germany and Korea, which have different economic systems.

Keywords

Relevance

Financial knowledge is becoming increasingly important in today’s global world – not just for professionals in the sector of investment and banking, but for every person responsible for managing his or her financial affairs in everyday life around the world. A high level of knowledge enables people to make appropriate financial decisions as consumers, savers or investors. 1 Such individual decisions strengthen the economy as a whole and promote growth. Not only in economic powers such as Germany and Korea is the demand for stronger promotion of financial knowledge becoming increasingly relevant (Aprea, 2016; Atkinson and Messy, 2012; Erner et al., 2016; Lusardi and Mitchell, 2011; Sohn et al., 2012). Even though Korea was a latecomer, it has now also begun to emphasize public financial knowledge in the country (Jang et al., 2014). The East Asian economic crisis of 1997 and the global economic crisis in 2008 have shown how important the population’s financial knowledge is to understand the complexity of global economic processes and to master financial challenges (Ali et al., 2016).

Other reasons for concern about the level of financial knowledge, especially among young people, is increasing distress due to a decreasing welfare system and demographic changes (Organization for Economic Co-Operation and Development (OECD), 2020a, Organization for Economic Co-Operation and Development (OECD), 2020b). Financial knowledge 2 is a central (and sometimes the only) component of financial literacy. According to Aprea and Wuttke (2016, p. 402), ‘financial literacy enables a person to effectively plan, execute, and control financial decisions’. Although the importance of financial knowledge has increased significantly in recent years, this topic is not firmly anchored in the school curriculum in Germany and Korea. In Germany, financial knowledge is part of other school subjects like economics education (Erner et al., 2016; Frühauf and Retzmann, 2016). Financial education as a separate subject is missing in the curriculum. Instead, due to the federal system in Germany, a varying proportion of financial or economic topics are taught in other subjects in each federal state. The status of financial education in Korea is similar. In Korea, the Ministry of Education revised the national curriculum in 2009 and included financial knowledge in high school economics as a new independent unit (Jang et al., 2014). However, there has been a decrease in enrolment in economics courses in Korean schools since those courses are not mandatory (Hahn and Jang, 2010). Korean high school students across the nation participated in a financial knowledge test created by the Financial Supervisory Service. In total, 63% of the students said that financial knowledge is not taught adequately in school (OECD, 2013).

Therefore, it is not surprising that young people’s basic financial understanding is unsatisfactory. High school research in Germany was conducted to investigate students financial knowledge and found weak performances (Brandlmaier et al., 2006; Erner et al., 2016; Lüdecke-Plümer and Sczesny, 1998). Studies performed with students from the higher education sector also see a need for improving financial knowledge (Förster et al., 2019; Riebe, 2018). Similar results are found in Korean research studies. Korean high school and higher education studies identify deficits in financial knowledge (Lee, 2019; Oh and Do, 2005). These deficits call for improvements to financial knowledge. Aprea (2016) therefore states: ‘Given the complexity of the underlying economic, political and social trends, it is an issue that cannot be solely left to the family and peer socialization but should be a concern for political and educational actions throughout all countries in the world’. This global need is considered by the Council for Economic Education (CEE) in the USA. The CEE developed the National Standards for Financial Literacy to include financial topics not only in the curricula (Walstad and Rebeck, 2016). These standards refer to international finance issues which are well known in the world. In this article, we will show that these standards are also applicable in an adapted version for the two countries Germany and Korea, which both exhibit differences in their economic systems.

Korea and Germany are two of the world’s bigger industrial nations (Federal Statistical Office, 2020). An international comparison in financial knowledge between countries reveal differences and similarities and foster awareness and encourage further advocacy in all nations (Happ and Zlatkin-Troitschanskaia, 2021). Both Korea and Germany have recognized the importance of financial education. As a result, there have been curricular changes in both countries in the last years, which is why focusing on these two countries makes sense. In addition, both countries have been affected by economic crises. There was a major financial crisis in the Asian region and there were such challenges in the European region as well. Therefore, both countries lend themselves to being included. To the best of our knowledge, there is no study so far that has compared the financial knowledge of young adults between these two countries. So far there has been only a lot of research within the western world (Behrman et al., 2012; Brown et al., 2018; Chambers et al., 2019; Lusardi et al., 2010; Riebe, 2018). 3

The main goal of this paper is the comparison of financial knowledge and understanding between German and Korean higher education students. Especially for first-year students in higher education, financial knowledge is of major importance. First-year students start a new phase of life in which they make first major financial decisions, run their own household and sign own contracts (Förster and Happ, 2018). Some of the students need to take out student loans. Consequently, they incur large debts at an early age (Lusardi et al., 2010). Therefore, financial knowledge is highly relevant for university students in Germany and Korea. Due to the lack of curricular anchoring of financial knowledge in the school sector in Germany and Korea, it is particularly exciting to look at university students who have just completed school.

This paper investigates students’ financial knowledge using the Test of Financial Literacy (TFL). The TFL was developed to measure individuals’ financial knowledge and understanding (Walstad and Rebeck, 2016). In addition to a total score indicating overall financial understanding, certain sub-scores are examined. Different areas examine everyday money management, banking and insuring (Förster et al., 2018; Huston, 2010). Based on these different sub-categories, the first research question (RQ)

4

can be formulated as follows: RQ1: Are there differences in the specific sub-categories of financial knowledge across Germany and Korea?

Due to an inadequate anchoring of financial education in the school system, other factors come to the fore, resulting in differences in financial knowledge among individuals. The use of a comparable test instrument also allows us to comparatively analyse these indicators in both countries. In Germany, differences in financial knowledge according to gender are currently being discussed (Bucher-Koenen and Lusardi, 2011; Erner et al., 2016; Förster et al., 2018; Riebe, 2018). A gender gap has been determined in favour of male individuals. These results can also be seen in other western countries (Atkinson and Messy, 2012; Chambers et al., 2019; Lusardi and Mitchell, 2011). By contrast, Korean studies do not exhibit any gender gap (Hahn, 2021; Hahn et al., 2014). On the basis of current research in both countries, we assume different results according to gender in Korea and Germany. Therefore, we state the following research question: RQ2: Does gender have a different effect on financial knowledge in both countries?

A second potential influencing factor is information gathering, that is, informing oneself about financial topics outside university. Recent studies in Germany and Korea show similar effects of this characteristic on financial knowledge. Young adults who actively inform themselves about financial aspects are more financially literate (Förster et al., 2019; Hahn et al., 2014). Similar results from Korea and Germany regarding information gathering lead to the following research question: RQ3: Does information gathering have a similar effect on financial knowledge in both countries?

This paper begins with the theoretical definition of financial knowledge and its sub-areas followed by presentations of the school systems in Germany and Korea as well as the respective anchoring of financial education. Based on the school system and on previous research, we determine which sub-categories German or Korean students are (not) well prepared for. The Correlation of gender and information gathering on financial knowledge section provides an overview of the connection between gender/information gathering and economic knowledge. Afterwards, the hypotheses are generated. In chapter 3, the test instrument and the sample are presented, leading to the empirical analyses of higher education students from Korea (N = 1006) and Germany (N = 1346). The paper concludes with limitations and implications for promoting financial knowledge in both countries.

Theoretical background

Financial knowledge

A variety of terms for financial knowledge can be found in the research literature. Financial literacy, financial knowledge or financial understanding are similarly widespread. Yet there has been no consensus on one consistent definition. The most basic definition states a competency to manage money (Remund, 2010). Financially literate individuals can understand, manage, analyse and communicate financial issues. They have knowledge of personal finance concepts and products, and are able to apply this knowledge (Huston, 2010). Going into more detail, financial literacy is the ability to handle financial challenges and to make effective financial decisions (Ali et al., 2016; Aprea, 2012; Sohn et al., 2012). Atkinson and Messy (2012) differentiate financial literacy on three dimensions: knowledge, attitude and behaviour. This study focuses on the cognitive dimension, meaning knowledge and understanding of personal finance. We use the term financial knowledge in this paper.

There are studies based on different content areas of the construct financial knowledge. The Council for Economic Education (CEE) published the National Standards for Financial Literacy in 2021 (CEE, 2021). These standards include the following six areas: (1) earning income, (2) spending, (3) saving, (4) investing, (5) managing credit and (6) managing risk. Rudeloff et al. (2019) conducted a survey in Germany to investigate financial knowledge among secondary students. They divided their test into five areas: ‘money and payments, savings, loans, insurance, and monetary policy’. According to Huston’s (2010) study four categories emerged: ‘personal finance basics, borrowing, saving/investing and protection’. Above-mentioned areas show overlaps (Erner et al., 2016; Schuhen and Schürkmann, 2014). ‘Money and Payments’ in Rudeloff et al. (2019) is quite similar to ‘Personal finance basics’ in Huston (2010). Therefore, Förster et al. (2018) combined these in one area ‘Everyday money management’. Rudeloff et al. (2019) and Huston (2010) both use the groups borrowing/loans and saving which are summarized under ‘Banking’. Protection and insurance reflects the sixth CEE dimension which also occurs in Rudeloff’s (2019) and Huston’s (2010) classification. Therefore, Förster et al. (2018) keep that area as a third subgroup.

The analyses of the TFL results in this paper follow a three-dimensional model including the components (1) Everyday money management, (2) Banking (which comprises Huston’s categories saving and using credit), and (3) Insurance which were developed by Förster et al. (2018) but are still based on the CEE standards. 5 The analyses refer to these three sub-scores to determine whether specific individuals have greater knowledge in one or another component.

Financial education in Germany and Korea

In the following, we examine the curricular anchoring of financial knowledge in the German and Korean education systems.

Financial education in Germany

Financial education can be considered a part of economics education. Economics education includes all activities that prepare individuals for the professional domain of economics and enables them to act responsibly in a society and market economy (Holtsch and Eberle, 2016). Therefore, ‘financially shaped life situations are simply a segment of economically shaped life situations’ (Retzmann and Seeber, 2016). The demand for an increased share of economics education thus also indirectly relates to the expansion of financial education. The school’s mission is to ‘enable students to act responsibly, autonomously, and appropriately in financial situations’ (Retzmann and Seeber, 2016). Due to the federal structure in Germany, each state has a different curriculum (for a description of the education system in Germany see Oswald-Egg and Kemper, 2017; OECD, 2020). Although there are almost 40 different subjects with economic and financial content (Frühauf and Retzmann, 2016), the school curricula for general education schools do not offer sufficient personal finance content (Retzmann and Seeber, 2016). In general, there are no ‘dedicated financial education programs’ in Germany (Erner et al., 2016).

The vocational sector exhibits a different picture. Students who attend vocational schools take subjects like business administration, economics or accounting. These subjects provide students with basic financial knowledge (Frühauf and Retzmann, 2016). The scope and choice of subjects depends on the type of vocational training that individuals have chosen. The curriculum for a commercial profession provides a higher proportion of economic and financial content (e.g. banking or financial services vocational trainings) (Oswald-Egg and Kemper, 2017).

The higher education sector is characterized by a very high degree of student autonomy. Students start to deal with financial topics of everyday concern. The first rented flat and thus the first own household, first own mobile phone contract or a student loan result in students having to deal with personal finance issues out of necessity. In terms of financial literacy, students gain experiential knowledge, that is, knowledge which increases through ‘learning by doing’ (Bruce and Bloch, 2012). In university courses, students do not learn these everyday aspects. Even though students in business administration or economics programmes take subjects like controlling or financial policy, the university curriculum does not include personal finances. In Germany, Riebe (2018) conducted a test on financial knowledge among university students and detected a low level of knowledge. Informal counselling is offered, for example, by the student advisory service. However, formal courses do not exist. This implies that there is a need for financial education in higher education. We can see that the promotion of financial knowledge is not yet an educational mission in the higher education sector in Germany.

Financial education in Korea

In Korea, all schools must follow the national curriculum. Korea conducted a major revision of the national curriculum in 2009 and 2015 (for a description of the education system in Korea see Kemper and Oswald-Egg, 2017; OECD, 2019). One out of five units in the economics textbooks in high school covers personal finance. The unit covers ‘money, financial systems, interest rates, financial institutions, income, spending, credit, debt, the management of financial assets, financial investment, life cycles, and financial planning’ (Jang et al., 2014). Although this was considered a great improvement, enrolment in economics courses in high school has decreased. In total, 90% of Korean students do not take the opportunity to learn more about personal finance (Jang et al., 2014). It is noteworthy that major contents for insurance were missing in the high school economics national curriculum. In 2020, the Financial Supervisory Service introduced new standards for personal finance for every grade between first and twelfth grade that consists of five main categories: finance and decision making, income and expenditure management, saving and investing, credit and debt management, and insurance and retirement planning (Financial Supervisory Service, 2020).

Like Germany, Korean university students rarely learn about personal finance. However, there are some extracurricular training opportunities to improve financial literacy, for example, household management programmes. About 10% of all female college students complete a household management/consumer programme (Lown and Ju, 2000). The idea is to empower particularly negatively affected groups (e.g. homemakers) in terms of financial literacy with the help of financial education opportunities (Moon et al., 2014). The Financial Supervisory Service provides a special course at universities to encourage students to learn financial topics of everyday concern. But the number of students who benefit from the course is limited.

Conclusion on the educational systems and hypotheses

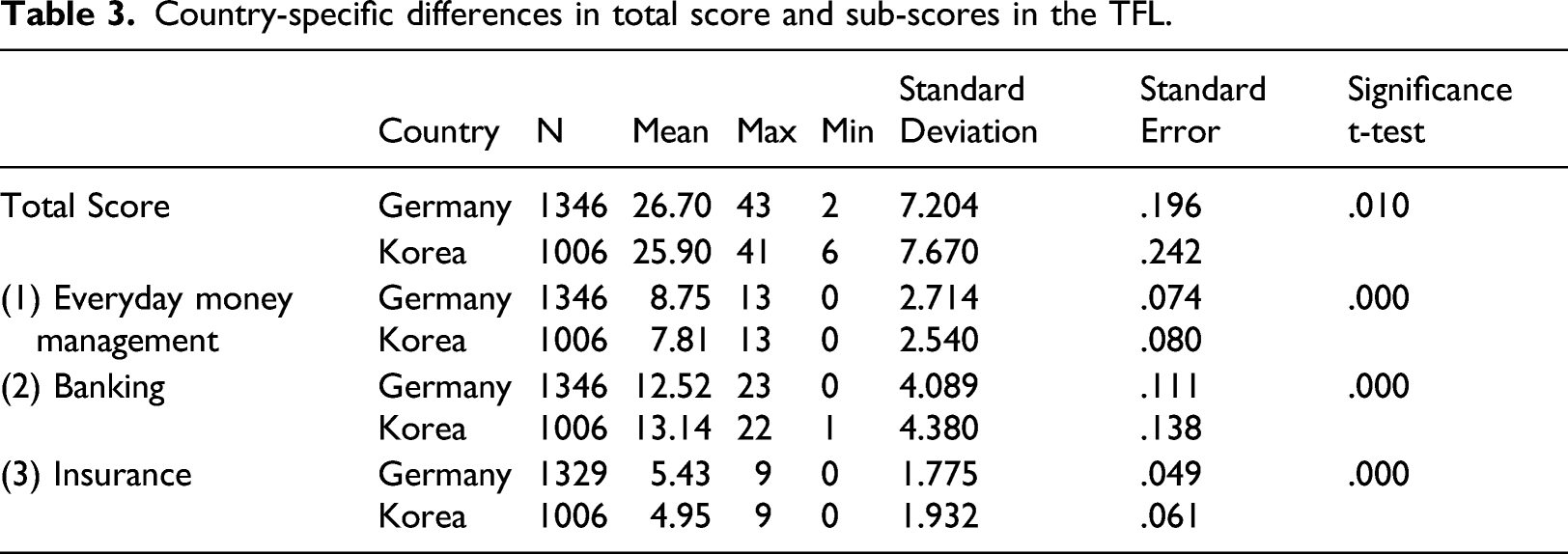

We have seen that financial education in the two countries slightly differ from each other. In economics and thus also in financial education in Germany, the emphasis lies on the individual’s self-responsibility to financially shape their life situations. Schools should therefore provide a general framework to facilitate this autonomy (Vansteenkiste et al., 2005). This could result in higher knowledge among German students in the area of (1) everyday money management. While everyday money management is and will remain of major importance, let us not forget that Germany is undergoing a demographic crisis (Sinn and Uebelmesser, 2002). Due to the growing importance of preventive care triggered by this crisis, there is the assumption that knowledge in the area of (3) insurance is high among students. Erner et al. (2016) conducted a survey with 1416 German tenth-grade students from different school types. They conclude a lack of ‘basic understanding of the long-term consequences of saving and investing’. We assume for our study that the participants have the lowest degree of knowledge in the area of banking (2) which includes saving and investing.

We assume that Korean students have the least knowledge in the area of (3) insurance not only because important standards for insurance are not included in the national economic curriculum but also because students have little experience in making financial decision related to insurance. Young Koreans have little interest in insurance. Most college students do not own a car and thus are ignorant of car insurance. Therefore, we postulate the assumption that knowledge in the area of (3) insurance is low among Korean students. Hahn (2021) reported that prospective elementary school teachers had a poor understanding of insurance. The proportion of college students living with their parents and receiving allowances is still relatively high, leading to less experience in daily money management.

Therefore, we state the following hypotheses: H1.1: In Germany, we assume that students have the most deficits in “banking” and higher knowledge in “insurance” and “everyday money management”. H1.2: In Korea, we assume that students have the most deficits in “insurance” and higher knowledge in “everyday money management” and “banking”. H1.3: German students score higher on “insurance” whereas Korean students score higher on “banking”.

Correlation of gender and information gathering on financial knowledge

Gender

Various research studies around the world have focused on differences in financial knowledge according to gender (Atkinson and Messy, 2012; Erner et al., 2016). Many show that male individuals have more financial knowledge than women (Chen and Volpe, 2002; Fonseca et al., 2012; Lusardi and Mitchell, 2011). Studies from Germany show the same result. Bucher-Koenen et al. (2017) surveyed young German adults and found lower financial knowledge among women. Förster et al. (2018) investigated the financial knowledge of German students at the beginning of their university studies and found a gender gap in knowledge as well. Riebe (2018) conducted a paper-pencil survey in different degree courses and also found a difference in financial knowledge between men and women. Women performed worse on average. Driva et al. (2016) surveyed 13–15-year-old high school students and confirm lower knowledge among females.

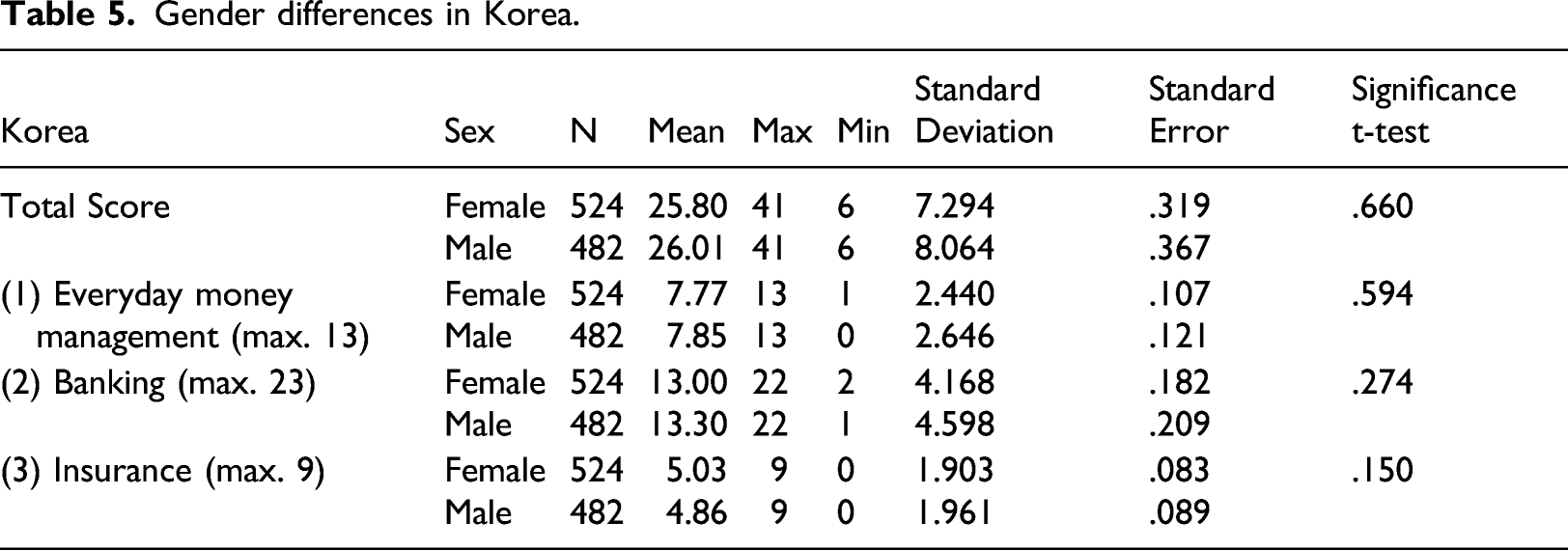

In Korea, the current state of research shows different results. Researchers found no performance differences leading to no gender gap in financial knowledge (Hahn and Abe, 2021; Hahn et al., 2014; Jang et al., 2014). So far, there has been a lot of research on financial knowledge and gender in Korea in the school sector (Cho and Park, 2008; Financial Supervisory Service, 2020; Hahn, 2013, 2018; Sohn et al., 2012).

These differing findings on gender encourage us to have a closer look at country-specific differences. The differences in gender effects between Korea and Germany can be related to cultural socialization. A survey conducted in Germany and Korea asked households which gender has more influence on financial decisions. In Germany, 21% indicated that men exert more influence over financial decisions, whereas only 14% felt that women exert more influence. In Korea, a different picture emerges. The proportions that voted for the more influential gender in each case are fairly balanced (23% for men, 24% for women). Thus, there seems to be a cultural difference here that could lead to gender differences between the two countries in terms of financial knowledge (Horowitz and Fetterolf, 2020). The equal distribution of financial tasks in Korea could be an indicator that women see making financial decisions as much a woman’s as a man’s job. Based on this we state the following hypotheses. H2.1: German female students have less financial knowledge than German male students. H2.2: In Korea, there is no gender gap in financial knowledge among students.

Information gathering

The lack of financial education in school curricula in Germany and Korea (see chapter 2.2) means that other individual factors play a role in knowledge differences. Insurance is one dimension of financial knowledge that addresses a future-oriented aspect. In order to secure a future at retirement age, sufficient knowledge about the options must be available at an early stage. Consequently, informed people have more financially literate than people who do not inform themselves about financial issues (Hahn and Abe, 2021; Lusardi and Mitchel, 2011). The other dimensions are included in individuals’ information seeking processes as well. (Atkinson et al. 2006) found a positive relationship between financial literacy and information level. Van Rooij et al. (2007) investigated a correlation between financial knowledge and information seeking related to financial products. Mimura et al. (2015) examined different financial information sources and the financial knowledge of young adults. Individuals who obtain information from their parents, other family members or college courses have a higher financial understanding and show better financial practices. Cao and Liu (2017) conducted an online survey with 18–25-year-old young adults. Their results show that young adults who use online sources to inform themselves about financial decisions have greater financial satisfaction.

A German study by Förster et al. (2019) investigated individuals’ information seeking in personal finance matters. Individuals who regularly read about financial topics in the media show a higher degree of financial knowledge. Due to the low level of financial education in schools, it is assumed that informal learning opportunities are of particular importance in Germany when it comes to acquiring financial knowledge (Rudeloff, 2018; Schürkmann, 2017).

In Korea, students who inform themselves about financial issues, for example, on TV or through newspapers, achieve a higher score in the Financial Fitness for Life Test (Walstad and Rebeck, 2005) than those who do not inform themselves on a regular basis (Hahn et al., 2014). In Korea, the Financial Supervisory Service has developed websites that include financial information customized for elementary school students, middle school students, high school students and college students. Moreover, gathering information about something outside of one’s profession or studies happens on a voluntary basis and requires interest. Many studies on financial knowledge as well as on economic literacy have investigated a positive relationship between high interest in financial and economic topics and greater knowledge (for Germany see Brandlmaier et al., 2006; Förster et al., 2018; Lüdecke-Plümer and Sczesny, 1998; for Korea see Hahn, 2019; Hahn and Abe, 2021; Sohn et al., 2012). Therefore, we state the following hypotheses: H3.1: German students who have a higher information gathering level are more financially literate than German students who do not inform themselves about financial aspects. H3.2: Korean students who have a higher information gathering level are more financially literate than Korean students who do not inform themselves about financial aspects.

Measurement instrument and sample

Test of Financial Literacy

To assess the knowledge and understanding of personal finance among German and Korean higher education students, we used the Test of Financial Literacy (TFL; Walstad and Rebeck, 2017) of the US CEE. This multiple-choice test was developed according to the National Standards for Financial Literacy (CEE, 2013) and contains 45 items which cover the six areas: earning income, buying goods and services, saving, using credit, financial investing, and protecting and insuring. The items consider various everyday situations that involve financially based decision making.

The internationally established test was adapted into German and Korean to make it suitable for use in both countries. Since personal finance is a construct shaped by the culture of a certain country (Marchetti et al., 2016; Mason and Wilson, 2000), an adaptation and validation process including linguistic and cultural adjustments was necessary to create a valid instrument for measuring financial knowledge in Germany and Korea. 6

The validation process of the Test of Financial Literacy for use in Germany and Korea was based on the Standards for Educational and Psychological Testing (AERA et al., 2014). Although financial systems and practices in Germany, Korea and the US show some differences, most of the CEE standards are very similar across the three countries. However, adaptations had to be made particularly in the area of using credit and protecting and insuring. One explanation for that is the fact that in the US and Korea a lot of people use credit cards, whereas in Germany, the larger part of the population pays by debit card (Klapper et al., 2015). In Korea, credit card holders rarely use revolving services, so they are unfamiliar with the term ‘grace period’. Korea has a unique structure of residential properties called ‘jeonse’, which is a long-term rent with lump-sum deposit. The landlords make a profit from reinvesting the deposit, instead of receiving monthly rents. Therefore, landlords do not consider a tenant’s credit score when renting a house. The capital gains from stock investment are not taxed for personal investors in Korea. With regard to the other area of protecting and insuring, cultural differences play a major role, resulting in different perceptions of insurance and social security plans. For instance, Korean higher education students are not familiar with car insurance because only a few students own a car.

A standard adaptation of international assessment and surveys method is the Translation, Review, Adjudication, Pretesting and Documentation (TRAPD) approach which is in line with the Test Adaption Guidelines (TAGs) (Hambleton, 2001; Harkness, 2003). In the first step of the TRAPD process, items were translated by professional translators and any language, cultural, or content issues were highlighted. Each item was then discussed, and alternatives and adaptations were identified, as necessary. Consultations were held with various test developers and experts to check the test for factual accuracy and realism.

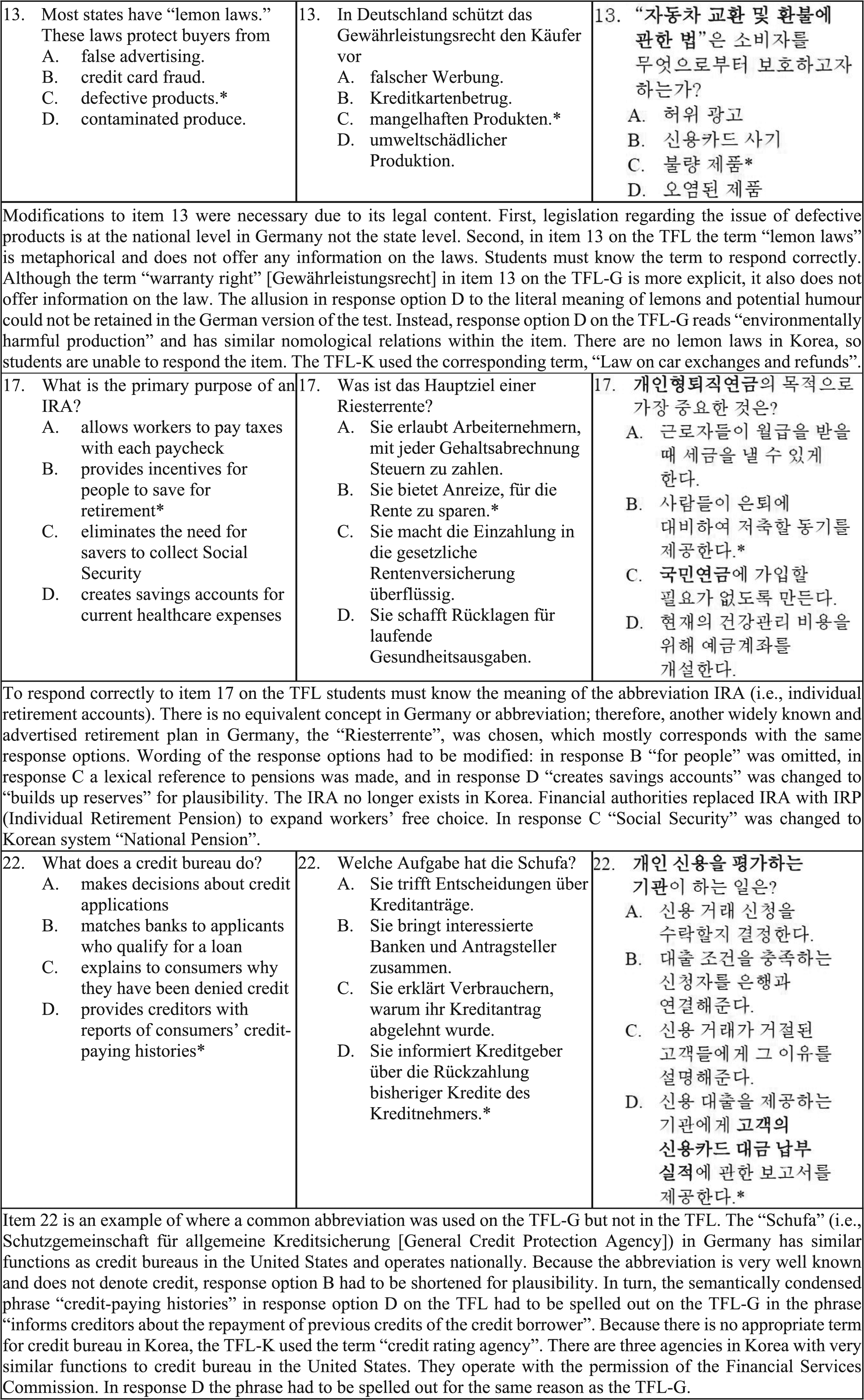

Following the TAGs, translations were closely based on the original meaning and structure of the items, sentences, phrases and terminology. Adaptations were only made if the version was inadequate for the German and Korean cultural context. Figure 1 shows sample items which needed to be modified because of different financial product terminology in the three countries. Sample items from the TFL and the adaptations.

As mentioned in the theoretical background (chapter 2.1), Förster et al. (2018) performed a factor analysis and combined these areas in three dimensions: everyday money management which contains the areas earning income and buying goods and services; banking which contains the subgroup of saving, using credit and financial investing; and insurance which simply reflects the last area of protecting and insuring. The first subgroup includes the items 1–13 (maximum of 13 points), the second group includes items 14–36 (maximum of 23 points), and the third group includes items 37–45 (maximum of 9 points). These sub-scores were also calculated for the Korean sample.

Sample in Germany and Korea

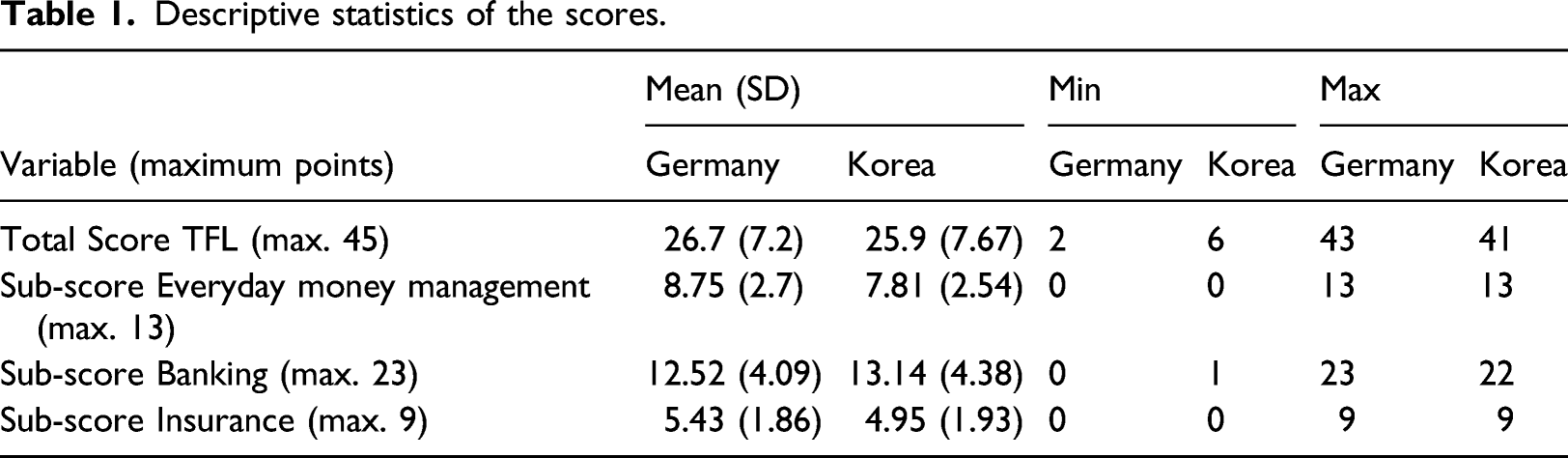

Descriptive statistics of the scores.

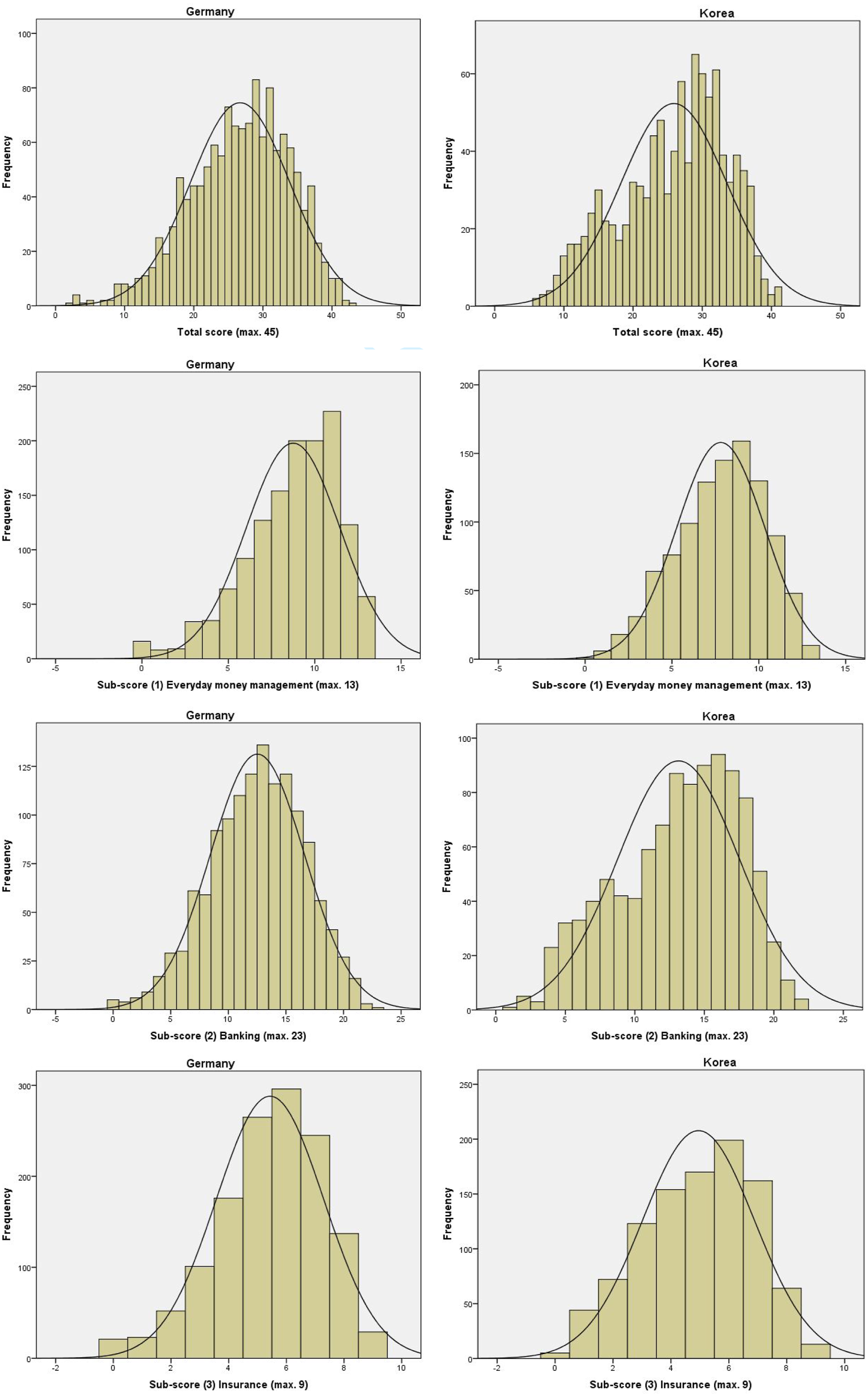

To see the distribution of scores, histograms for the German (left side) and the Korean (right side) were created in Figure 2. The histograms show that an approximate normal distribution can be assumed for all scores (Nadarajah, 2005). Distribution of TFL scores and sub-scores in Germany and Korea.

Descriptive statistics of the variables investigated.

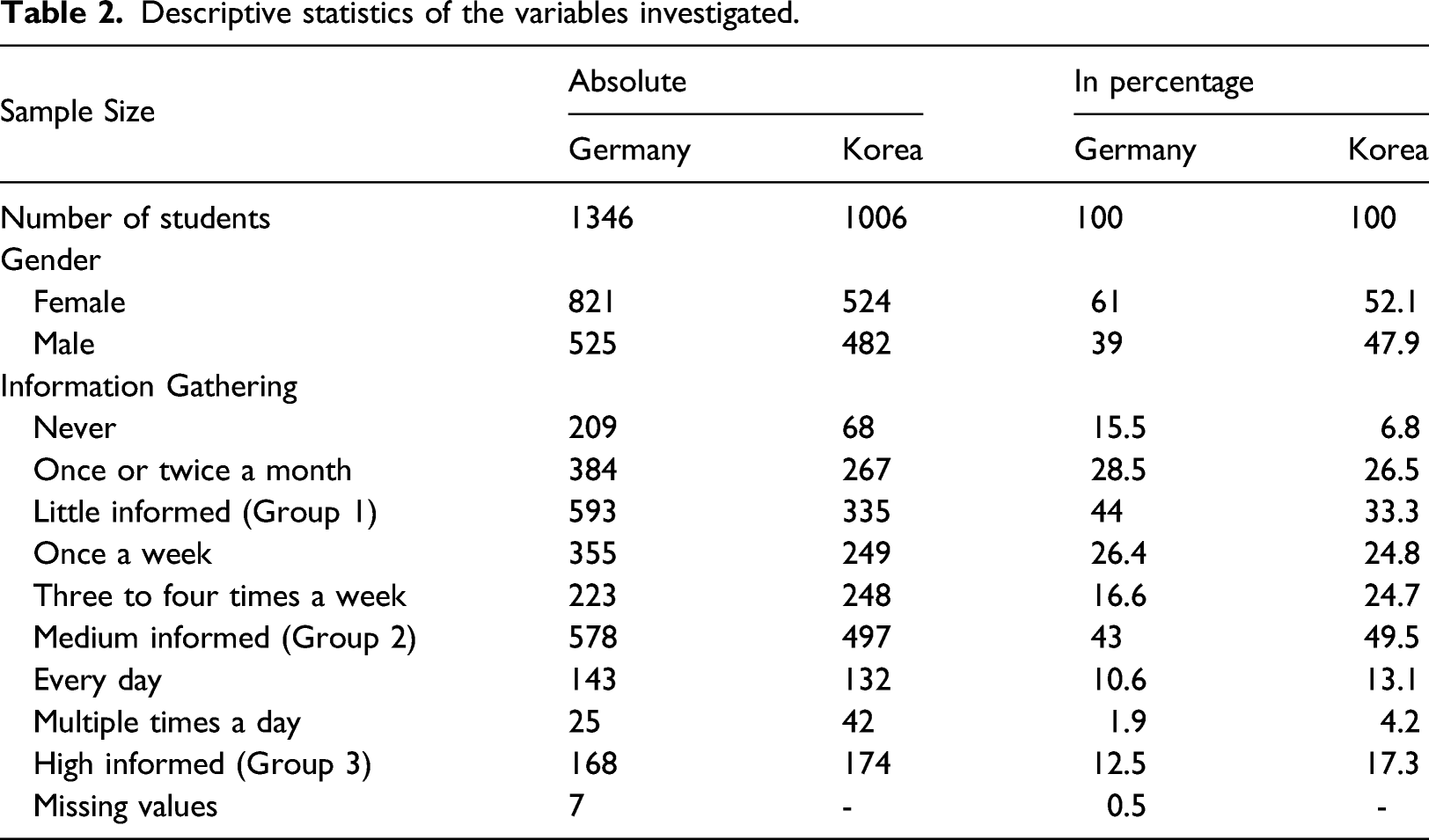

Last, the variable information gathering process is described. Students could choose one out of six options when asked how often they learn about financial issues. The German and Korean sample differ slightly here with 15.5% of the German students never informing themselves about financial topics, whereas in Korea, only 6.8% belong to this group. The groups that inform themselves more often are larger in the Korean sample than in the German sample. Only 1.9% of German students show the highest information gathering level, whereas in the Korean sample, 4.2% indicate this information gathering level. However, the largest proportion indicates a level in the medium range in both samples. To investigate differences in TFL results between students who inform themselves with varying frequency, an analysis of variance is carried out. Therefore, the number of ‘information gathering’ groups is reduced from six to three. Group 1 includes students who never inform themselves, once or twice a month. Group 2 includes those who inform themselves once a week or three to four times a week. Group 3 includes individuals who inform themselves at least once a day. Table 2 presents the number of group members in Germany and Korea.

Results

In the following, we present the results. The focus is on comparing the two countries. First, the total score and the three sub-scores are analysed using t-tests (Wilcox, 2017). Second, the countries are compared in terms of gender differences on the total score as well as on the sub-scores. Third, information gathering as an influencing factor is taken into account, analysing the differences between the countries with the help of a variance analysis (Backhaus, 2016).

Total TFL score and sub-scores in Germany and Korea

Country-specific differences in total score and sub-scores in the TFL.

Gender differences in Germany and Korea

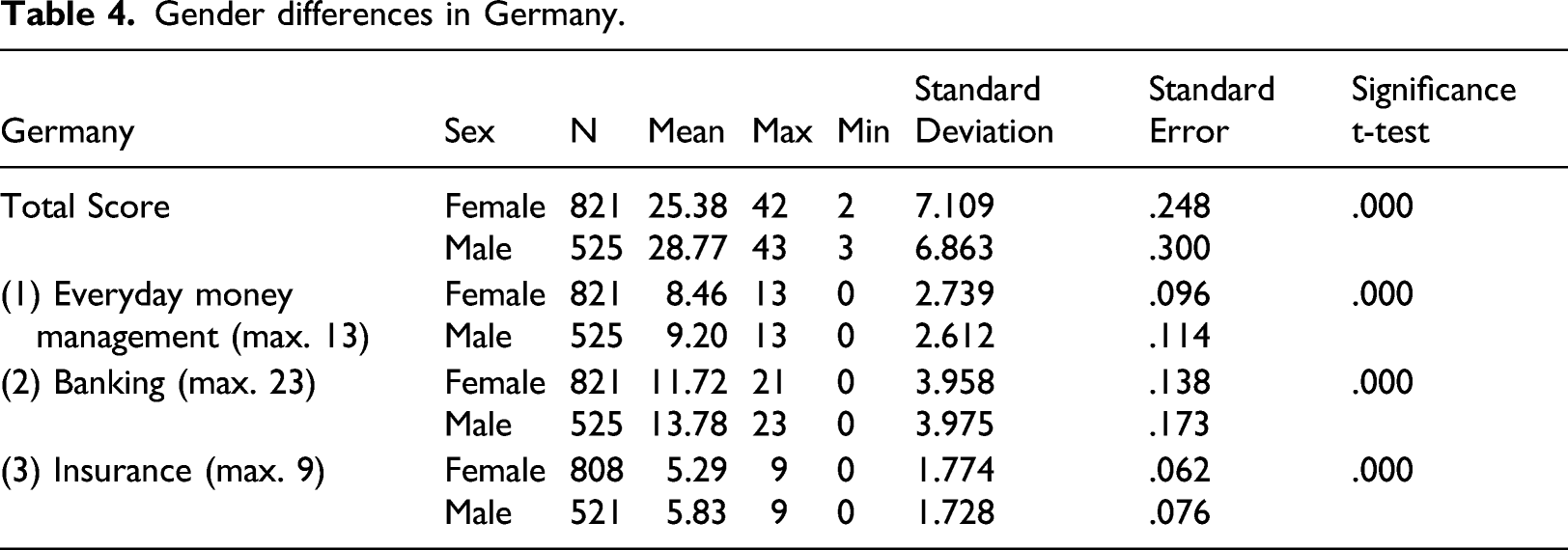

Gender differences in Germany.

The main score as well as the three sub-scores show the same results. In each case, male test takers have a higher number of correct items. Especially in the second sub-score ‘Banking’, male test takers achieve on average two more correct items than females. The differences in each category between female and male test takers are significant on a 1% level.

Gender differences in Korea.

Information gathering in Germany and Korea

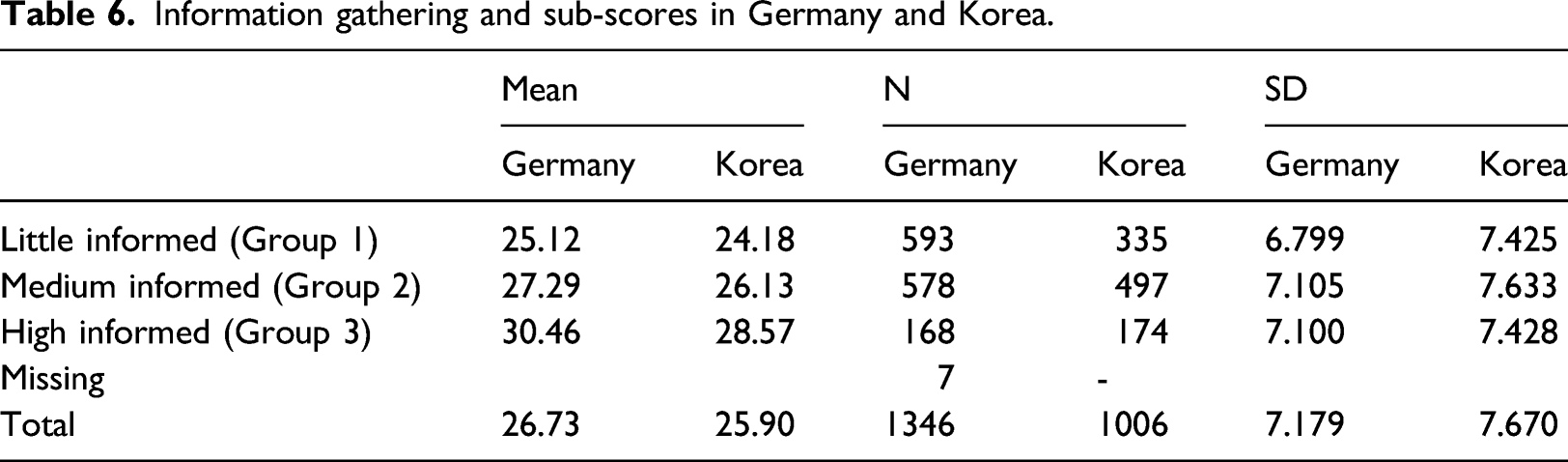

Information gathering and sub-scores in Germany and Korea.

To find out if those differences between the groups are significant, we conduct a single factor analysis of variance with post-hoc tests (Gamst et al., 2008; Weinberg and Abramowitz, 2008). These tests are conducted independently for the German and Korean sample.

Germany

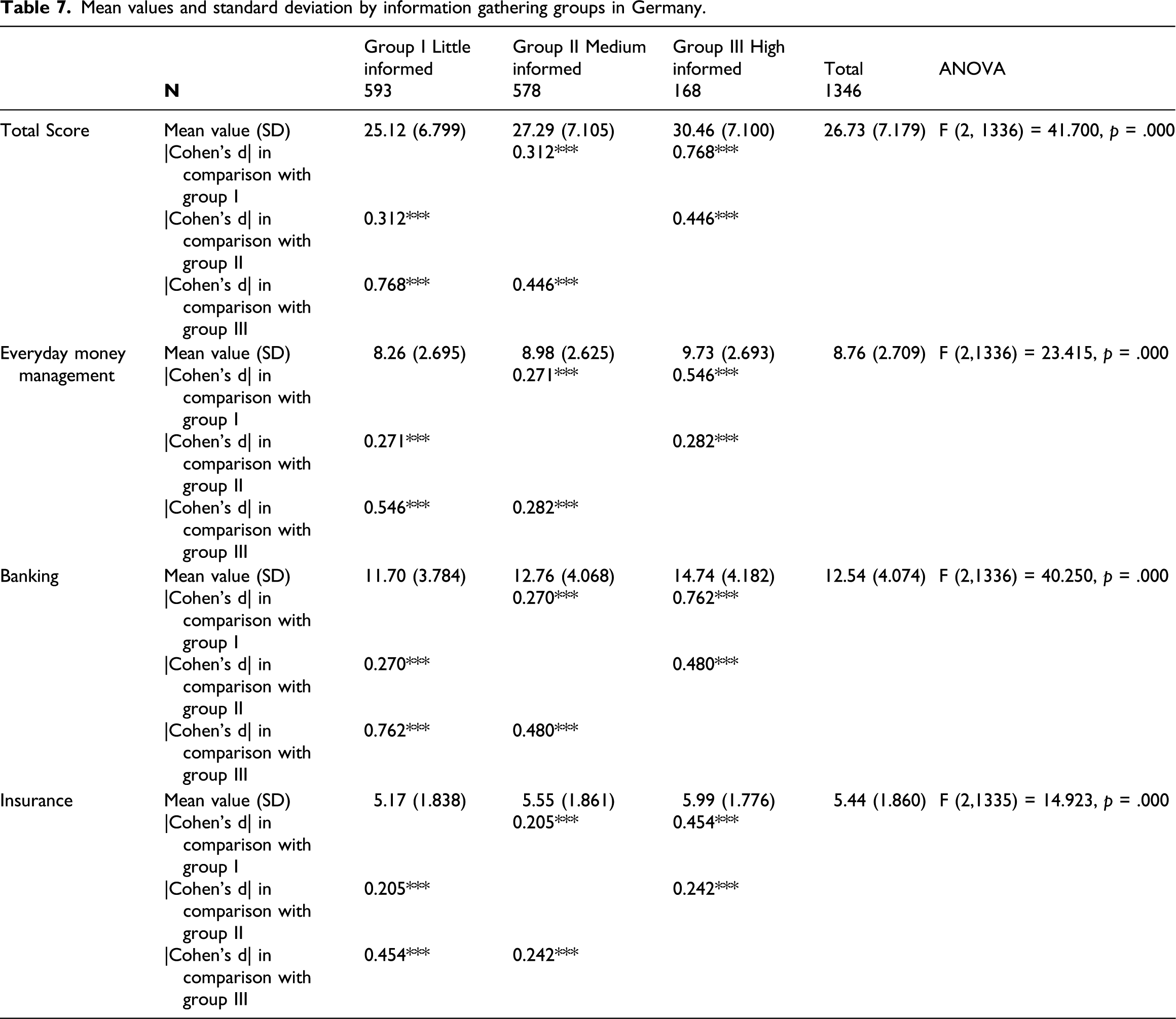

Mean values and standard deviation by information gathering groups in Germany.

The results for the German sample show that students who inform themselves about financial topics on a regular basis are more financially literate than students who do not inform themselves a lot or not at all. These findings confirm hypothesis H3.1.

Korea

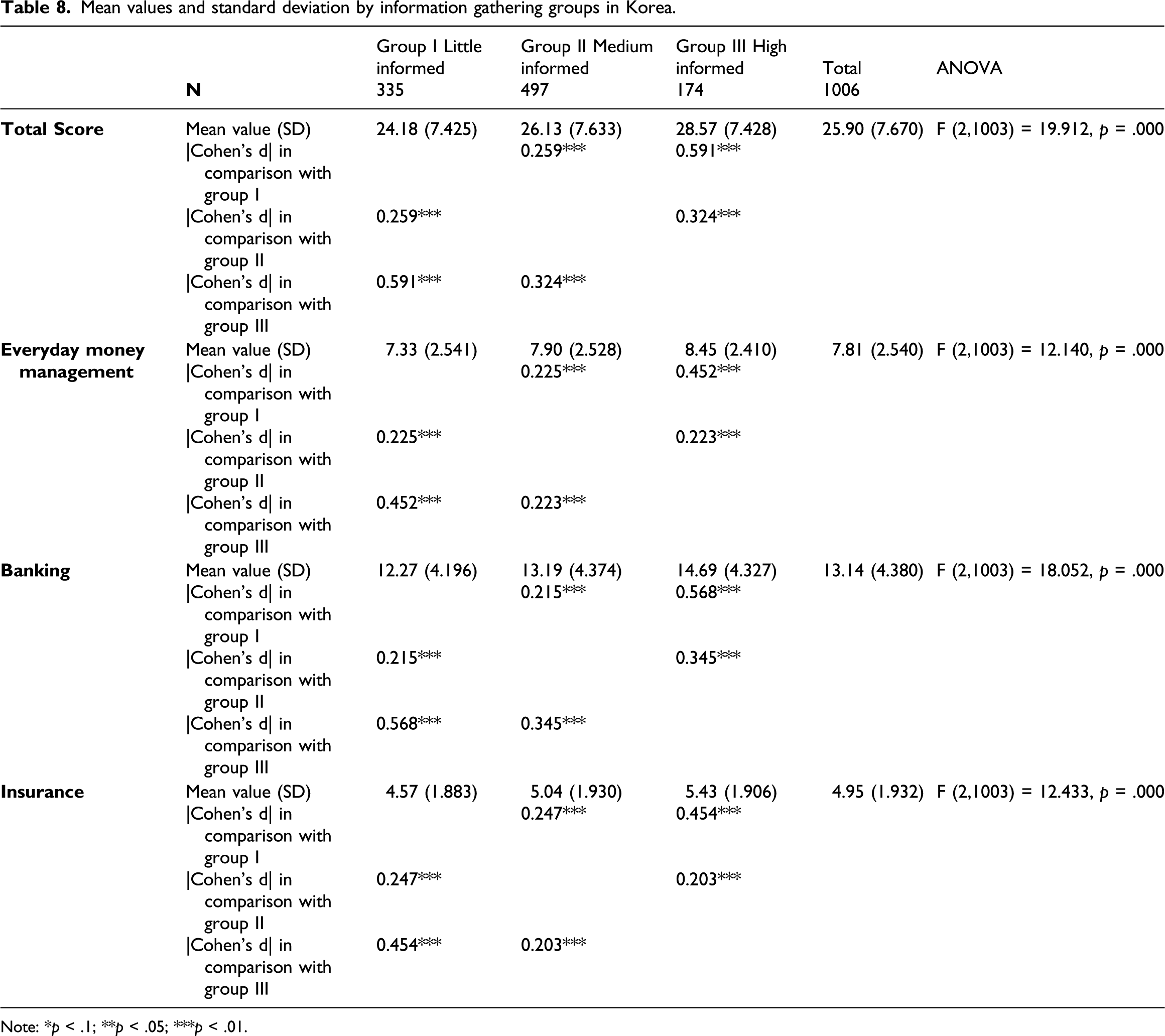

Mean values and standard deviation by information gathering groups in Korea.

Note: *p < .1; **p < .05; ***p < .01.

Within the Korean sample, it was also determined that a higher information gathering level is related to higher financial knowledge. Consequently, our last hypothesis 3.2 can be confirmed as well.

Discussion

This study comprises a comparative analysis of financial knowledge of German and Korean higher education students. German and Korean students achieve a similar score on the TFL, however, German students have a slightly higher financial knowledge and understanding. Larger differences could be detected between the two countries when analysing the sub-scores. The comparative analyses confirmed that German students outperform the Korean students in ‘Insurance’, whereas the Korean students perform better in ‘Banking’ (see H1.1-H1.3). Further mean value comparisons and t-tests could confirm the hypotheses related to the gender effect of knowledge in both countries. We could not find any gender specific differences in Korea. Male and female students perform similarly, whereas the gender difference in Germany is, as was expected, in favour of male test takers (see H2.1 and H2.2). In contrast, the information gathering comparison showed similarities in both countries whereby our last hypotheses could be corroborated (see H3.1 and H3.2). In Germany as well as in Korea, students who inform themselves about financial topics more frequently show higher levels of financial knowledge and understanding.

Limitations

The results in this paper have to be considered under certain limitations. First, this study measures knowledge and understanding of personal finance on a cognitive dimension. In order to support students in their financial decisions and provide them with the most important financial basics, other factors influencing financial decisions, such as motivation, attitude or beliefs, need to be investigated. Non-cognitive dimensions might show country-specific differences as well. Unfortunately, we do not have other personal variables of the students that were used together in both countries. This study is the starting point for further surveys we will conduct in Germany and Korea. In further studies, we will need to include more personal variables of the students in the questionnaire in both countries. Since we have a very limited number of variables, we only report mean differences in this paper.

Second, we focus on the personal characteristics gender and information gathering. Therefore, many other aspects are left out. Korean studies point for example to the importance of individualistic and collectivist approaches on financial knowledge which play a predominant role in other studies (Grable et al., 2009). In the questionnaire of our study, we did not include items on these aspects in either country. Further limitations concern the sample size. In this study only, students from a few universities were assessed. The proportion of women and men in the German sample is not balanced. Due to the small sample size, the study cannot claim to be a representative sample in either country. Next, the information gathering level was queried through self-assessment. This means that this subjective indication is distorted due to perceived social desirability in society to inform oneself about financial topics and be interested. Lastly, the theoretical explanations are limited in some places due to the scope of the article.

Interpretation and implications

In our study we did not assess cultural differences for example regarding attitudes towards financial topics. But cultural differences between German and Korean young adults may provide explanations for our results. Grable et al. (2009) investigated the relationship between financial understanding and locus of control in Korea and the US. On average, Koreans have a higher external locus of control beliefs. Those with an external locus of control exhibit less financial knowledge. Further studies between Germany and Korea may benefit from the inclusion of such constructs like the locus of control.

We also found a difference in the gender effect between German and Korean young adults concerning their financial knowledge. This leads to interpretations in terms of role distribution. The two nations show different distribution of roles in their culture regarding financial issues (Horowitz and Fetterolf, 2020). In Korea, women and men are equally responsible for financial matters in the household, whereas in Germany it is men who are seen as being more responsible for this task. This strict division of roles among parents leads to differences in behavioural support among the two genders resulting in higher financial knowledge and understanding among male students. Here, financial education in Germany can clearly benefit from Korea by taking action against such a system of role models. Behrens et al. (2014) studied German individual’s information gathering via media. Their results show that 18% of men use the internet for finance topics, whereas only 9% of women said they obtained information about financial topics via media. This study shows that it is precisely female young adults in Germany who need to be made more aware of the enormous importance of dealing with financial matters.

Information gathering was also investigated in our study leading to the result that German as well as Korean informed students show more financial knowledge. In both countries, getting information outside of school/university is important and effective due to the inadequate teaching of financial topics at school (see chapter 2.2). The question arises which kind of information sources are referred to and which possibilities are used to get specific information about the certain sub-scores. With the help of more information on this through further studies, implications for financial education in schools could be developed. Familiar and fun information-gathering channels for students could be combined with targeted content delivery in school. Media use in the context of informing oneself about financial topics is a current field of research (Sabri and Aw, 2019). Varcoe et al. (2010) have already found that young people primarily use the internet as a financial information source. For the education system, this means that young people should be empowered to inform themselves about financial topics since it goes hand in hand with higher knowledge.

In addition to supporting young people in dealing with financial issues, the education system in Korea and Germany should actively teach financial content before they have to make financial decisions as young adults. At the same time, however, this also means that trained teachers must be available who can deal with financial content in the classroom. We have seen that differences between males and females in knowledge might arise due to different perceptions of role allocation. Furthermore, the sub-scores in the TFL showed that Koreans performed better in ‘Banking’, whereas Germans perform better in ‘Insurance’. This is also due to the private environment and everyday life of Koreans and Germans. Thus, the education system has a responsibility not only to include financial education in order to promote young people’s knowledge but also to eliminate differences between subgroups. The school acts as an equalizer here (Downey et al., 2004). Consequently, different role perceptions should not arise in the first place, and students in both Korea and Germany should learn the same content in finance regardless of what they have already experienced in their private environment.

This study emphasizes the importance of financial knowledge and understanding among young adults. In cooperation with the Russian G20 President and the OECD, an appeal was made to the nation with a focus on the promotion of financial knowledge. Korea also participated in this conference and developed a Financial Education Activation Plan (OECD, 2013). This initiative provides universal training sessions for interested individuals. In addition, socially vulnerable groups are to receive customized training units. However, this raises the question of the extent to which such offers are accepted. Instead, the implication focus should be on the public education system, giving all students the opportunity to learn financial content in a timely manner.

Financial knowledge is a construct that is perceived differently depending on the country. There are cultural differences, such as the use of credit cards, which must be taken into account when constructing test instruments. Therefore, it can be stated as an important finding from this paper that it is possible to create country-specific adaptations for a knowledge test for the USA, Germany and Korea. This is an important finding and prerequisite for further international comparative studies.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.