Abstract

Financial literacy is becoming increasingly important, in particular for adolescents since they are exposed to financial services earlier and earlier. At the same time, empirical studies indicate that male learners show higher financial literacy than women; however, other studies find significant or contrary differences between male and female learners. These partially contradictory results make it necessary to investigate such gender-specific effects in more detail. This article addresses two questions to contribute to the literature on financial literacy: first, in which financial content areas are there significant performance differences between female and male adolescents? Secondly, does the relationship between learning opportunities and financial education differ among pupils? The analyses are based on a sample of 530 secondary students from Germany. The results indicate that female students show higher test results for the financial literacy dimensions money and payments, and insurance, male students perform better regarding the dimensions savings and monetary policy. Furthermore, learning opportunities may contribute differently to the gender gaps. We contribute to the literature by investigating the important question of gender gap for five different dimensions of financial literacy and by showing that different learning opportunities play a role in the development of students’ financial literacy.

Introduction

In our modern service society, financial literacy is becoming increasingly important (OECD, 2017).Financial literacy “enables a person to effectively plan, execute, and control financial decisions” (Aprea and Wuttke, 2016: 402). It is of relevance for people of all ages because financial instruments and services are becoming more complex and also because financial literacy is associated with economic and social well-being (OECD, 2017). Accordingly, in recent years, the number of studies focusing on adolescents’ financial literacy has been increasing (e.g. Amagir et al., 2018; Aprea and Wuttke, 2016; OECD, 2017; Rinaldi and Todesco, 2012; Rudeloff, 2019; Schürkmann, 2017; Sohn et al., 2012). This can be attributed to the fact that adolescents are exposed to financial services earlier and earlier, for example, within the framework of mobile phone contracts or their own bank account (OECD, 2017).

When comparing the study results, performance differences between different gender can be seen for both adolescents and adults. A multitude of empirical studies provides evidence that male learners perform better than women (Atkinson and Messey, 2012; Bucher-Koenen et al., 2014; Chen and Volpe, 2002; Filipiak and Walle, 2015; Förster et al., 2018). However, no significant or contrary differences between male and female learners are also found (e.g. Hill and Asarta, 2016; Jang et al., 2014; Walstad et al., 2010). In addition to the studies mentioned earlier, the current PISA (Programme for International Student Assessment) study shows only a gender gap in Italy. In Australia, Lithuania, Poland, Slovakia, and Spain, on the contrary, girls perform significantly better (OECD, 2017). Although the research results are not unambiguous up to now, the question is also of high practical relevance since it is crucial that women have sufficient financial literacy, in particular in the area of old-age provision. There are two main reasons for this: first, women have a higher life expectancy than men, and thus, depend longer on old-age benefits. Second, women often pay less into the state pension system because they interrupt their careers in favor of raising children (or other family obligations). As a result, women are generally more often affected by poverty in old age than men (Grohmann, 2016; Lusardi and Mitchell, 2014). In light of these partially contradictory research results and due to the high practical relevance of the topic, it is necessary to investigate the gender-specific differences in financial literacy in more detail.

In this context, it should be taken into account that current studies such as PISA (OECD, 2017) acknowledge that financial literacy consists of several content areas such as money and transactions, planning and managing finances, risk and reward, and financial landscape (OECD, 2017) but the scaling and evaluation of the data are generally one-dimensional. Most studies identify a gender gap for the overall construct of financial literacy (Atkinson and Messey, 2012; Bucher-Koenen et al., 2014; Chen and Volpe, 2002; Filipiak and Walle, 2015; OECD, 2017). Consequently, these studies do not check whether this effect is equally apparent for each content dimension of financial literacy. Two recent exceptions are studies by Förster et al. (2018) and by Schürkmann (2017). In the study by Förster et al. (2018), financial literacy consists of six content areas in the field of personal finance “earning income; buying goods and services; saving; using credit; financial investing; protecting and insuring” (p.297). Using the German version of the Test of Financial Literacy (TFL-G), it was shown with a sample of 1108 17–25 -year-olds that females performed significantly worse on the three dimensions of banking, everyday money management, and insurance. 1 This gender effect, however, is not significant for everyday money management if interest and media usage are controlled for. In Schürkmann’s (2017) study, students between the ages of 14 and 17 from different German federal states were tested in a 45-minute online study to measure their financial literacy in six content areas. The results show that male students perform significantly better than female students in the content area of debt.

In summary, since there is unambiguous evidence regarding the overall gender effect and since only a few studies look at this question using a more-dimensional instrument, this article aims at contributing to this research gap by further analyzing the gender gap with a multi-dimensional measurement instrument, going beyond the Test of Financial Literacy. Accordingly, the first research question is as follows:

In which financial content areas are there significant performance differences between female and male students?

To explain the gender gap in empirical data, a number of variables were used in different studies: differences in individual characteristics between men and women, differences in socioeconomic characteristics between men and women, differences in the task format of the test instruments used, and country-specific characteristics (Bucher-Koenen et al., 2014). Furthermore, students’ interest in financial and economic topics was taken into account (Förster et al., 2018).

These variables show some explanatory power but even after they are taken into account, a large part of the performance difference between males and females remains unexplained. Consequently, further research is required. For example, Bucher-Koenen et al. (2014) provided the explanation that men and women acquire financial competence in different ways and that a different use of learning opportunities 2 can be another explanation for the gender gap.

Recent research shows that a number of learning opportunities influence the acquisition of financial literacy. Studies on financial socialization show the influence of parents, work experience, and school (Grohmann et al., 2015; Jorgensen and Savla, 2010; Shim et al., 2010; Solheim et al., 2011). The relevance of media usage is highlighted in the studies by Förster et al. (2018) as well as by Rudeloff (2019). To complement this, the influence of formal and informal learning opportunities such as the influence of the school, and different personal learning opportunities such as the peer group needs to be examined. The extent to which gender-specific use of learning opportunities can explain the gender gap has not yet been investigated, so that the second research question for the contribution is as follows:

Does the relation of learning opportunities and financial literacy differ for female and male students?

The article is structured as follows: Section “Conceptualization of financial literacy” conceptualizes the construct financial literacy. Section “The relation of different learning opportunities and financial literacy” presents the different formal and informal learning opportunities as potential predictors of financial literacy. In section “Empirical findings,” our research design, the test instrument, the sample, the available data, and the evaluation methodology are discussed. Subsequently, the findings are presented and critically examined in section “Discussion and conclusion.”

Conceptualization of financial literacy

At present, it is already possible to draw on a number of national and international studies, but some of these studies differ considerably in their conceptual design (Aprea, 2012; Kaminski and Friebel, 2012). One reason for this is that the studies refer to different constructs, such as financial knowledge, financial literacy, financial education, or financial capability, which are not uniformly defined in the literature (Aprea, 2012; Liening and Mittelstädt, 2011; Reifner, 2011). In addition, the studies differ in their conceptualization of financial literacy and, thus, use different models of financial literacy, indicating a different concept of a financially educated person (Aprea, 2014). According to Aprea (2014), the following three types of conceptualizations 3 can be identified:

Manager of personal financial issues,

Responsible consumer, and

Responsible economic citizen.

The most widespread conception in research comprises personal financial management. The focus is primarily on individual financial decisions related to private life and household management, such as the money management and loans, the insurance of life risks, the accumulation of assets, and old-age provision. Accordingly, the economic subjects in their role as consumers are in the center, reducing this conception to the consumer perspective (Aprea, 2014). This approach is the basis for a large number of studies and publications that focus on knowledge or competencies in the financial sector (Förster et al., 2018; OECD, 2017; Schlösser et al., 2011). The second concept of a responsible consumer adds the aspect of responsible consumption to personal financial management. This includes the ability to critically reflect one’s own needs and purchase decisions, with the overall objective to reduce information asymmetries existing in consulting and sales situations. Also, the rights and obligations of consumers in their relationship with other financial market players are relevant in this approach (Aprea, 2014; for a recent study see Reifner, 2011). The central idea of a responsible economic citizen (third concept) is about embedding personal financial decisions in an expanded and comprehensive context of the economy and society. Thus, this approach also includes monetary policy aspects and the relevant role of the state in this context. The regulation of financial markets and the influence of international interdependencies are also central issues. In consequence, citizens are rather regarded as co-designers of institutional conditions and should be enabled to participate in the shaping of a democratically compatible economic and financial system. This third approach is more comprehensive than the first two variants and, at the same time, systemic because, as has been shown, it also includes a political dimension that goes beyond the consumer perspective (Aprea, 2014; Aprea et al., 2015). Only recent research projects and publications increasingly follow this comprehensive concept of the responsible economic citizen (e.g. Aprea and Wuttke, 2016; Kaminski and Friebel, 2012; Retzmann and Seeber, 2016). This approach is also taken up in this article.

Against this background and the definition of competence by Weinert (2002), financial literacy is regarded as a domain-specific construct. Financial literacy is understood as the interplay of knowledge, skills, and abilities, motivational and emotional processes as well as attitudes and self-efficacy expectations. This interplay of these different constructs enables people to make well-founded decisions in financial contexts with the goal to participate in (economic) life as a responsible person. It is assumed that financially literate individuals consider institutional and macroeconomic conditions in their decision-making process, so that both individual and social well-being can be improved (OECD, 2013; Rudeloff, 2019; Weinert, 2002). In this research, financial literacy is understood as a multi-dimensional construct based on the concept of the responsible economic citizen (see above). The instrument is based on analyses by Kaminski and Friebel (2012), Schürkmann (2017), Schürkmann and Schuhen (2013), and Walstad and Rebeck (2017). 4 The instrument consists of five content dimensions including money and payments, savings, loans, insurance, and monetary policy, which were defined with as little overlap as possible (Rudeloff, 2019).

The relation of different learning opportunities and financial literacy

Overall, the acquisition of financial skills is a complex process that is determined by a variety of influences and learning opportunities (Bender, 2012). In addition to formal learning processes (such as schools), the everyday life of adolescents consists of a number of other sub-worlds such as sport, leisure, part-time work, peers, family, and political participation and commitment (Tully, 2008; Tully and Krug, 2011; Wahler et al., 2008), where young people also come into contact with financial aspects. Thus, these private areas of life can function as informal learning opportunities. According to Wiswede (2004), from a theoretical perspective, one’s own experiences or learning from a model (Bandura, 1977) are decisive for financial socialization. Models in this context can primarily be parents, peers, or media models. Gudmunson et al. (2016) defined financial socialization as a process that extends from childhood to early adulthood, in which consumer roles are developed with the help of parents, teachers, friends, work experience, and the media. Overall, literature on financial socialization focuses on three or four socialization agents through which socialization takes place: family or parents, school, experiences at work, and the media (Gudmunson and Danes, 2011). The research mainly takes into account the first three socialization agents.

The importance of the family, especially of parents, for the financial socialization has already been confirmed in a number of studies (Grohmann et al., 2015; Jorgensen and Savla, 2010; Shim et al., 2010; Solheim et al., 2011). For example, Shim et al. (2010) were able to confirm that the direct instruction of parents with regard to financial issues and decisions has a significant influence on the financial knowledge of adolescents. The same applies to the teaching of financial content at school and to work experience gained. The effect strengths of the direct parental instruction in comparison to the other learning settings mentioned are approximately twice as high. At the same time, the study shows that the financial behavior of parents is often adapted and affects not only their behavior but also the attitudes of children and adolescents toward finance.

The PISA 2015 study also highlights the relevance of parents’ financial literacy for students’ financial performance. It should be noted that in 10 countries, discussing financial matters with parents is related to higher financial literacy, controlling for socioeconomic status. This result underlines the importance of parental instructions (OECD, 2017). Parental financial literacy should therefore also become the focus of research and promotion.

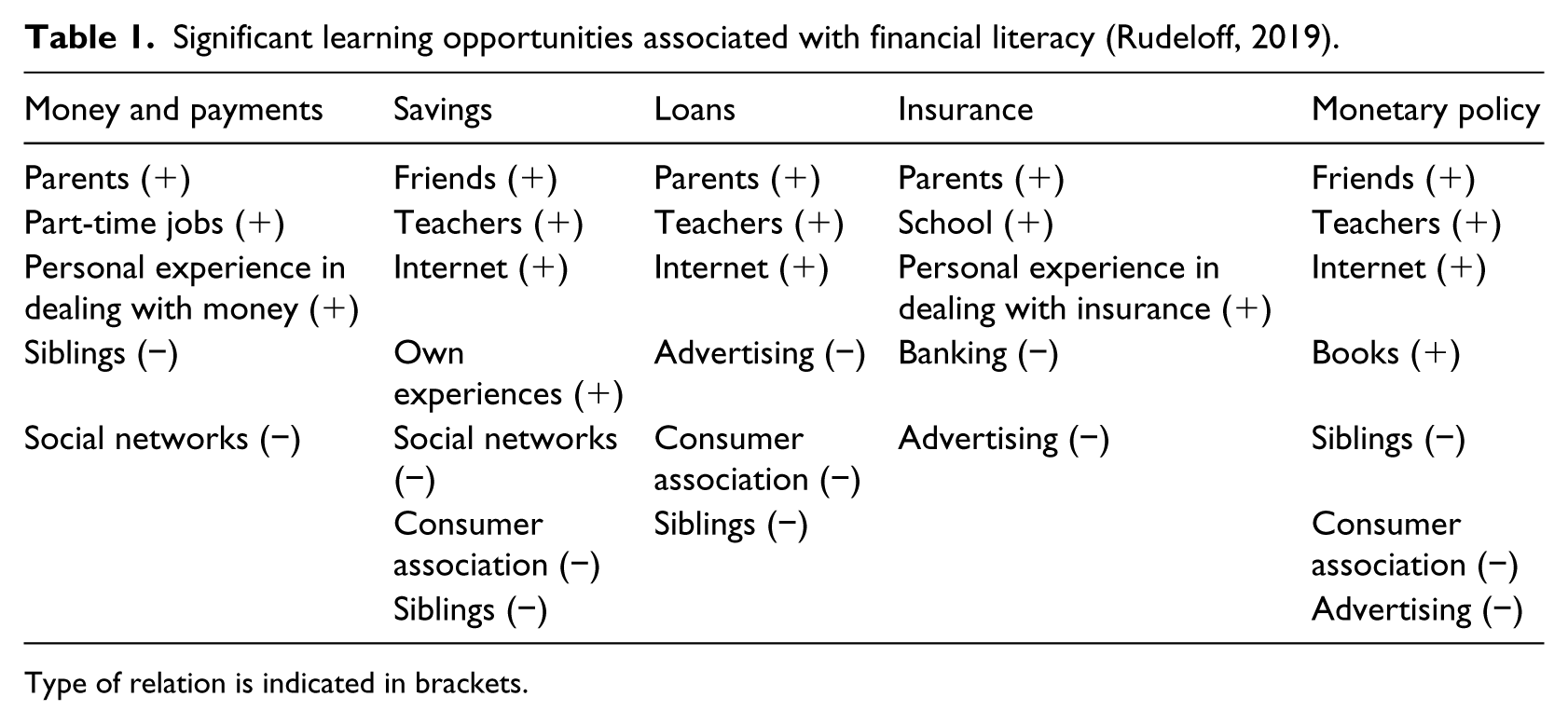

In addition to the aforementioned studies, Rudeloff (2019) recently examined the relation of a number of informal learning opportunities with the individual content facets of financial literacy (money and payments, savings, insurance, loans, and monetary policy) in contrast to the formal learning opportunity of the school or teacher in a quantitative questionnaire study with adolescents. For each dimension, items record the test performance and the use of learning opportunities. With the help of regression analyses for each content area of financial literacy, Rudeloff (2019) examined the connection between learning opportunities and test performance in the respective area. The results of the analyses show that a number of learning opportunities are significantly related to financial literacy. Table 1 provides an overview of the results.

Significant learning opportunities associated with financial literacy (Rudeloff, 2019).

Type of relation is indicated in brackets.

The negative effects of social networks and siblings are attributed to misinformation in the social networks and possible pre-concepts in comminution with siblings (Rudeloff, 2019). Rudeloff (2019) also pointed out in her study that the negative effects of the consumer association in the area of loans and monetary policy need to be interpreted with caution, as the term was not defined in the questionnaire and it is not certain whether all adolescents have a uniform understanding of the term. The learning opportunities banking and advertising are negatively associated with the test performance in the insurance sector. The negative relation is attributed to the selective presentation of information in advertising and the information asymmetries that might arise in discussions with bank employees (Rudeloff, 2019).

Whether there are differences between male and female learners in the context of financial socialization has not yet been systematically investigated. Results from other research disciplines, however, suggest that girls attribute more learning potential to high-quality media such as news or daily newspapers and in this respect reject the tabloid press more than boys (Stecher, 2005).

The previous remarks show that there are different approaches to the conceptualization of financial literacy and that this article follows the responsible economic citizen approach. It also highlights that different learning opportunities can have an impact on financial literacy. Whether there is a link between the use of learning opportunities and gender that could explain the gender gap will be the guiding question for the following results.

Empirical findings

Sample and test instrument

A paper-based questionnaire was used, which was comprehensively validated and piloted. The test is characterized by sufficient content and construct validity; the dimension-specific reliability values are between 0.70 and 0.74 (Rudeloff, 2019). According to the developed multidimensional model of financial literacy, the test contains items for the following content dimensions: money and payments, savings, loans, insurance, and monetary policy. For each dimension of financial literacy, the test included tasks of varying complexity in which the respondents – taking into account their different roles in the financial business – have to, for example, make or evaluate financial decisions. In order to systematically vary item difficulties, the test was based on items requiring different cognitive processes to solve which also differed with regard to the pre-structuring of the solution path, the number of possible solutions, and the extent of the variables to be processed for the solution (Rudeloff, 2019; Winther, 2010). The test included items using a free response format as well as multiple choice items. Assignment and selection tasks can be distinguished for tasks with a bound answer format; the latter tasks are designed as both dichotomous items and multiple-choice tasks. The instrument consists of 50 items. In addition to financial literacy, personal and socioeconomic background variables were collected (e.g. age, gender, migration, and socioeconomic status). The use of various formal and informal learning opportunities (see Table 1) was also recorded. The use of learning opportunities was measured separately for each dimension of financial literacy using a four-level Likert-type scale. Specifically, for each dimension of financial literacy, students were asked how often they had used the listed learning opportunities to learn about the relevant subject area (not at all, rare, more often, and very often). Descriptive analyses clearly show that students do not make very intensive use of the various learning opportunities to learn about finance. In the area of money and payment instruction, for example, the mean values range from 2.78 to 1.15. It can be seen that parents are the most important learning opportunity (mean = 2.78), followed by students’ own experiences in the area of money and payment (mean = 2.13). Furthermore, individual media such as the Internet (mean = 1.85) or news (mean = 1.87) are comparatively important. The same applies not only to friends (mean = 1.78) but also to schools (mean = 1.78) and information provided by teachers (mean = 1.68) and banks (mean = 1.65). On the contrary, consumer associations are very rarely used as sources of information (mean = 1.15). The relatively low use of learning opportunities is evident for every dimension of financial literacy. There are no significant differences regarding the gender of the respondents.

The following analyses are based on a sample of 530 secondary level 1 graduates drawn in Lower Saxony/Germany (Rudeloff, 2019). Overall, 9.40% of the students were aiming for a lower secondary school graduation certificate or diploma, 37.40% for a secondary modern school graduation certificate, 9.60% for a technical college entrance qualification, and 40.80% for a general higher education entrance qualification. Finally, 2.80% of the participants did not specify their intended school graduation certificate in detail. Of the participating students, 50.90% were female, 48.90% male, and 0.20% of the respondents did not report gender. If the variables country of birth, mother tongue, and nationality are considered together and combined to form a first-order migrant background, the proportion of respondents without a migrant background is 81.50%. A first-order migration background is assumed if it is only evident in one of the variables used. In addition, the migration background of the second order was considered by taking into account the countries of birth of the parents. In this case, 32.10% of the students surveyed have a migration background, 5 whereas 66.60% do not. For 1.30% of the students, the second-order migration background could not be determined due to a lack of information. The test time was 90 minutes. The students did not receive any incentives.

Data analysis

To determine whether there is a significant difference between male and female learner, a t-test is used. Basis for calculations is the test performance of adolescents in the five areas of financial literacy. In order to interpret and compare the results, a scale normalization based on PISA is carried out. Thus, the mean value of the scale of the Financial Literacy Test is standardized to 500 and the standard deviation to 100 (OECD, 2017). R (R Core Team, 2019) is used for the analyses.

The present analyses build on the results of Rudeloff (2019) concerning the learning opportunities and their relations to test performance in the areas of money and payments, savings, loans, insurance, and monetary policy (see chapter 3, Table 1). In particular, it is investigated whether gender acts as a moderator for the use of learning opportunities. For this purpose, multiple linear regression analyses are conducted. While the item response theory (IRT)-scale test performance for each area of financial literacy is used as a dependent variable, gender, each learning opportunity and one interaction term (each learning opportunity × gender) are included as independent variables. To complement these analyses, personal and socioeconomic background variables are used as controls. In order to improve the interpretability of the results, in particular of the main effects, all continuous independent variables (Likert-type-scale variables treated as such) have been mean centered for the regression analyses.

Results

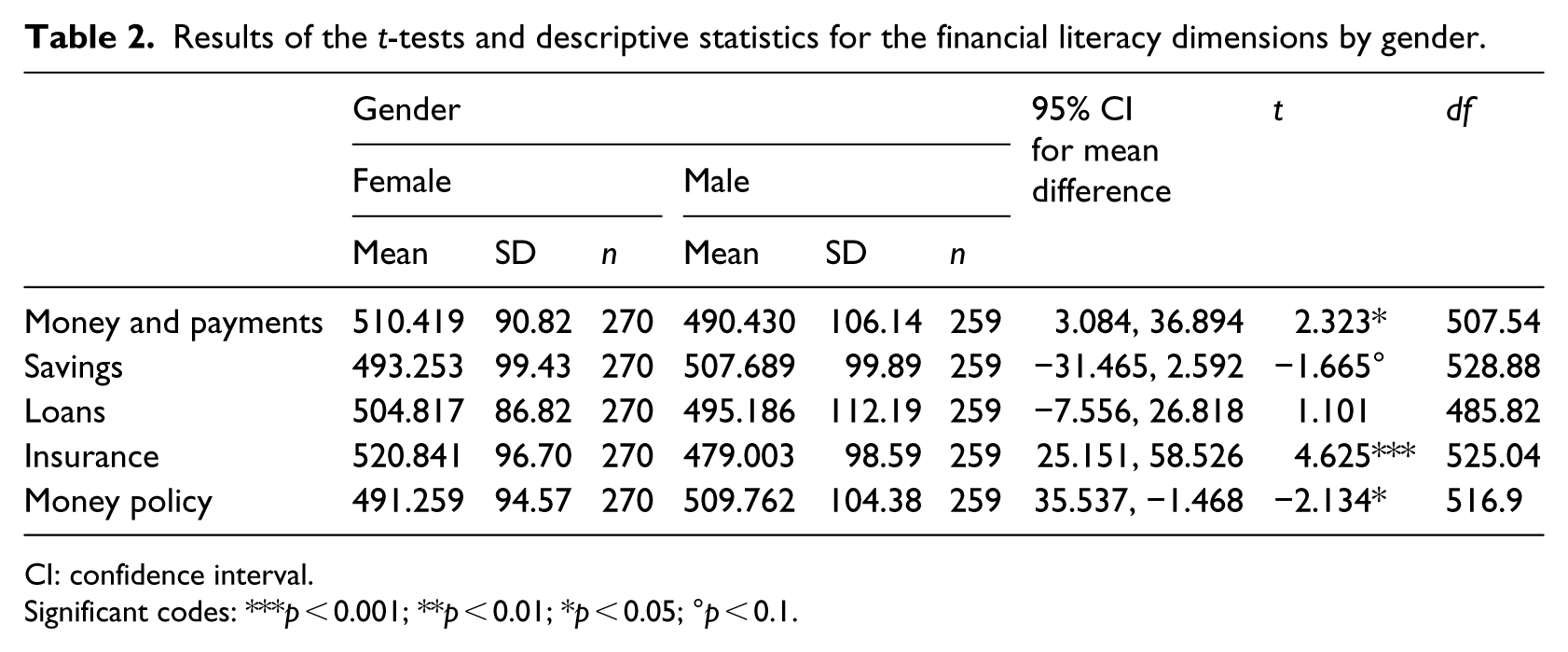

Initially, it is investigated whether performance differences can be found for the five content areas of financial literacy, using a t-test. Results are shown in Table 2. Whereas female students show higher test results for the dimensions money and payments and insurance, male students perform better regarding the dimensions savings and monetary policy. No significant gender differences could be found for the financial literacy dimension loans (p < 0.10). As the second aim of this study is to explain gender differences in the financial literacy dimensions via differing effects of learning opportunities, gender-moderated effects are only analyzed for those dimensions that showed significant differences in the t-test (Table 2). As a result, the dimensions money and payments, savings, insurance, and monetary policy are considered in the following multiple regression analyses.

Results of the t-tests and descriptive statistics for the financial literacy dimensions by gender.

CI: confidence interval.

Significant codes: ***p

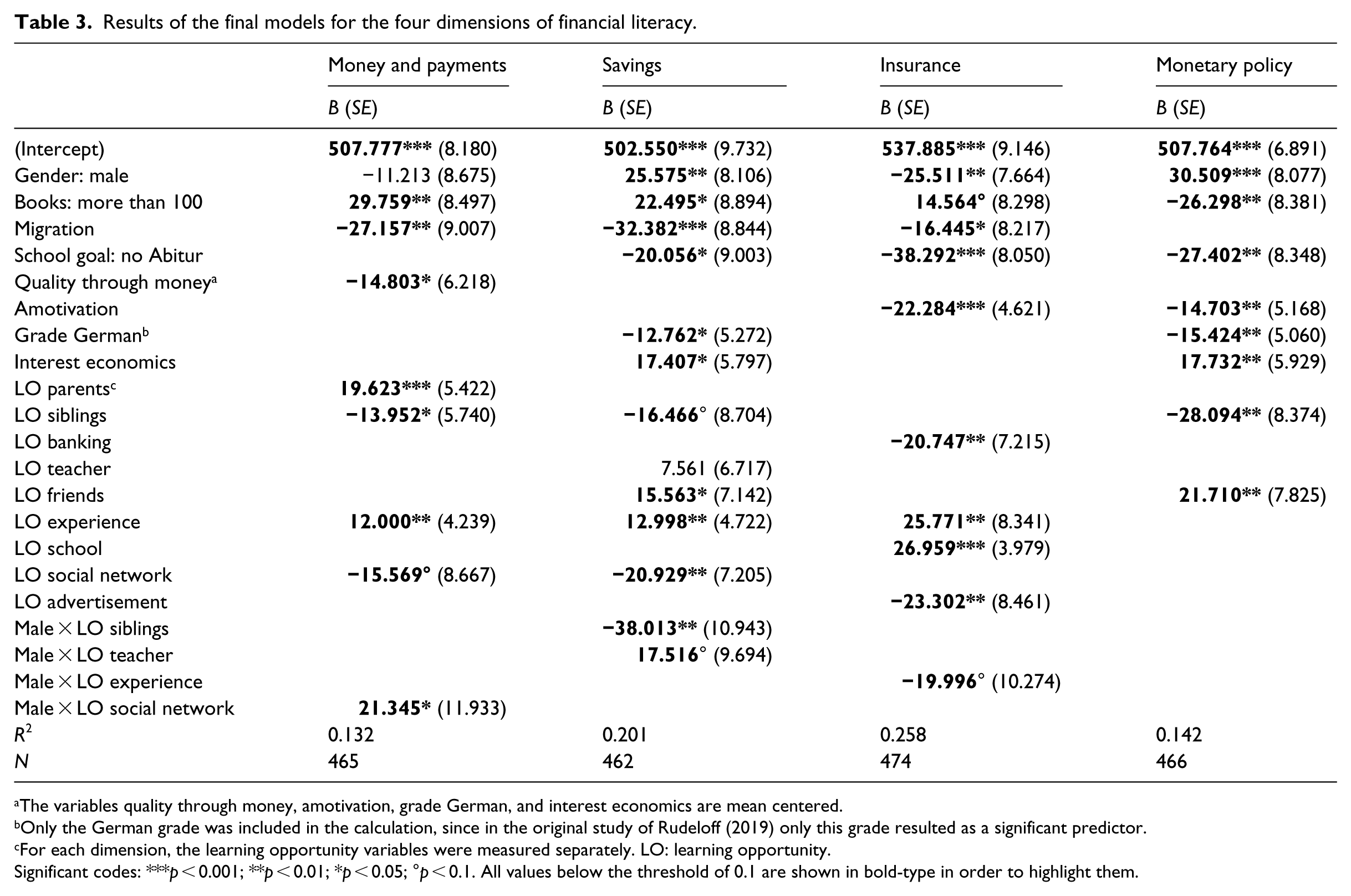

For each dimension, the previously found related learning opportunities (see above; Rudeloff, 2019) are tested in terms of a significant interaction effect with the variable for gender, while controlling for personal and socioeconomic background. Listwise deletion was used in the case of missing values. The model was build stepwise, including only the direct effects for each learning opportunity in one step and both the main and the interaction effects in another step. Only the significant effects remain in the final models shown in Table 3. Due to the mean-centering, the intercept can be interpreted as the average test result of a non-migrant, female student with average values on the continuous variables.

Results of the final models for the four dimensions of financial literacy.

The variables quality through money, amotivation, grade German, and interest economics are mean centered.

Only the German grade was included in the calculation, since in the original study of Rudeloff (2019) only this grade resulted as a significant predictor.

For each dimension, the learning opportunity variables were measured separately. LO: learning opportunity.

Significant codes: ***p < 0.001; **p < 0.01; *p < 0.05; °p < 0.1. All values below the threshold of 0.1 are shown in bold-type in order to highlight them.

With regard to the dimension money and payments, the learning opportunities parents, siblings, social networks, part-time jobs, and personal experience in dealing with money are tested. In contrast to the results of Rudeloff (2019), there is no significant overall effect of part-time jobs in this model, also there is no interaction effect for this learning opportunity. However, the results may deviate from Rudeloff (2019) because a smaller number of control variables were taken into account for the present analyses and no latent modeling of scales took place. The effects of the learning opportunities parents, siblings, part-time jobs, and personal experience do not differ significantly for male and female students. Though female students (reference category) on average show higher test results concerning the dimension money and payments than male students (B = −11.213), this difference is not significant either. However, the relation of social networks is negative for female students’ financial literacy regarding money and payments (B = −15.569), but it is positive for male students (−15.569 + 21.345 = 5.776). By this model, 13.2% of the variance in the money and payments dimension of financial literacy can be explained. The results for this final model are shown in Table 3.

The financial literacy dimension savings is analyzed with regard to the predictor siblings, friends, teachers, consumer associations, Internet, social networks, and experience. For the learning opportunities consumer associations and Internet, no significant main or gender-moderate effect could be found. In the case of the other five predictors, they are significantly associated with the test results regarding savings. The overall gender difference is in favor of male students (B = 25.575), as shown in Table 3. Also, the effect of the learning opportunity teacher differs significantly for male and female students, with a stronger effect for male students (7.561 + 17.516 = 25.077) than for female students (B = 7.561). The same applies to the effect of siblings, which is negative for female and male students but is much stronger for boys (−16.466 − 38.013 = −54.479) than girls (B = −16.446). The total explained variability in test results for savings, by this model, is 20.1%.

The financial literacy dimension insurance is tested for significant gender interaction effects regarding the following learning opportunities: advertising, banking, personal experience in dealing with insurances, parents, and school. Again, in this model, not each of the results of Rudeloff (2019) could be replicated. With regard to parents, no significant direct or moderated effect could be found, based on a 10% significance level. Nevertheless, there are significant main effects for banking, school, advertisement, and personal experience and a significant average difference in the test performance in favor of female students, as again shown in Table 3. In terms of the effect of personal experience, the positive effect for female students (B = 25,771) is significantly lower for male students (25.771–19.996 = 5.775). The final model allows to explain 25.8% of the variability of the test results regarding insurance.

In the case of the last dimension of financial literacy monetary policy, the learning opportunities advertising, books, consumer association, friends, Internet, siblings, and teachers are analyzed for interaction effects with gender. Only two of the presumed significant main effects could be found, that is, the learning opportunities siblings and friends. However, there was no gender difference in the effect of these learning opportunities. In this case, the overall gender effect on test results is in favor of male students (B = 30.509). The final model, again containing only the significant regressors after a stepwise model-building, is shown in Table 3. The total explained variability in test results for monetary policy is 14.2%.

Discussion and conclusion

In this article, we first examined in detail whether there are significant performance differences between female and male students. We contribute to the literature by investigating this question for five different dimensions of financial literacy. Thus, this study is able to shed more light on the phenomenon of gender gaps in financial literacy. We extend other research which operationalizes financial literacy in one dimension (Atkinson and Messey, 2012; Bucher-Koenen et al., 2014; Chen and Volpe, 2002; Filipiak and Walle, 2015; OECD, 2017) by showing that the performance differences between male and female students vary in the different dimensions of financial literacy. Thus, our results are in line with previous studies emphasizing differential effects between male and female learners (e.g. Hill and Asarta, 2016; Jang et al., 2014; Walstad et al., 2010). In this study, we found significant gender gaps for the areas of money and payments, savings, insurance, and money policy. It is noteworthy that the gender difference is in favor of female students for the dimensions of money and payments, and insurance (in contrast to Förster et al., 2018), while male students outperform female students in the dimensions of savings (only marginally significant) and money policy. This is also a partial confirmation of the results of the PISA study (OECD, 2017), where it was also shown for some countries that female students outperform males in the overall construct of financial literacy (as mentioned earlier, only an overarching construct was measured in PISA, see above). In this context, it needs to be asked whether the usually assumed gender gap is developing only over time and as a result of different socialization processes during adulthood. This is particularly interesting since financial socialization, in which consumer roles are developed, is seen as an extended development lasting from childhood to early adulthood (Gudmunson et al., 2016). Thus, at the time of the survey, this process has not yet been completed and not all consumer roles can be fully experienced as adolescent. Other studies indicate that men more often decide upon investment and credits in households and that they specialize both in private and in job situations on financial decisions (e.g. Hsu, 2016). Accordingly, the number of women in leadership positions in the financial sector is also very low, for instance, in Germany (Holst and Friedrich, 2016). Future studies could further investigate such socialization processes during adulthood.

With the second research question of this article, we analyzed whether the relation of learning opportunities and financial literacy differs for female and male students. Overall, the results show that formal learning opportunities are significantly associated with test performance in the different dimensions of financial literacy. While parents are an important learning opportunity for the dimension of money and payments which is in line with previous research (e.g. Grohmann et al., 2015; OECD, 2017; Shim et al., 2010), they are not significantly related to the other dimensions of financial literacy.

Furthermore, different learning opportunities may contribute to the gender gaps, however, to a smaller extent since there are only interaction effects for the dimensions money and payments, savings, and insurances. Accordingly, only for these dimensions, significant differences in the association between learning opportunities and financial literacy are found for male and female learners.

For the area of money and payments, the results show an interaction effect for the learning opportunity “social networks” such that using social networks is negatively associated with test performance for female students while it is positively associated for male students. Nevertheless, female students are still performing significantly better than male students in the area of money and payments. The question is how this contrary effect can be explained. A potential reason can be found in studies regarding gender differences in using social media (e.g. Windt, 2013; also Pujazon-Zazik and Park, 2010). According to Windt (2013), females show a different media behavior than males which is also named “gendered digital inequality,” indicating that women use social media less efficient and more often for private aspects.

For the dimension savings, there are different interactions which help to explain the differing test performance between male and female students. The positive association between the learning opportunity “teacher” and the test performance is higher for male students than for females which could be a possible explanation for the higher test performance of male students. On the contrary, the negative association of the learning opportunity “siblings” and the test performance is stronger for male students. Nevertheless, male students outperform girls in this dimension. Since the teacher is in this study conceptualized as a formal learning opportunity, it is worthwhile to have a closer look at the relation between learning success at school and students interest which in general is positive (Krapp, 1992). This correlation is of particular interest in the savings dimension since the contents of savings are communicated more intensively in schools than the contents from the other dimensions of financial literacy. However, studies show that female students are less interested in financial topics than their male counterparts (e.g. Lührmann et al., 2015), which could partially be an explanation for this interaction effect. The interaction effect of the learning opportunity siblings can hardly be explained based on our data since there are no further information regarding the siblings. However, Grohs-Müller and Fuhrmann (2018) also confirmed the negative effect of siblings on students’ financial literacy.

Regarding the dimension of insurances, there is a significant interaction effect with the learning opportunity “personal experiences.” The positive association of this learning opportunity and the test performance is more pronounced for female students than for male students which could partially explain the higher test results for female students in this dimension. A potential explanation for this is the higher risk aversion of women, which has been shown in other studies (e.g. Neelakantan and Chang, 2010). It is possible that this aversion already exists at a younger age, which could imply that female students reflect more upon insuring their risks than male students. However, more research is needed to confirm this assumption.

Overall, the results show that the gender gap with regard to financial literacy is a complex phenomenon, which can partially be explained by the different usage of learning opportunities. However, more research is needed to shed light on the learning opportunities and, at the same time, further potential predictors such as individual characteristics of men and women, differences in socioeconomic status of men and women, differences in the task format of the test instruments used, and country-specific characteristics (Bucher-Koenen et al., 2014). Another limitation is the way how learning opportunities were assessed in this study. Future research could aim to measure students’ usage of learning opportunities in a more differentiated way. In this study, students rated the learning opportunities on a Likert-type scale, thus, it was only asked how intensely each learning opportunity was used to acquire financial literacy in a particular dimension. However, this kind of rating does not allow for information on the kind of usage of the learning opportunities. In consequence, the analysis of gender-specific interactions is limited. At the same time, the learning opportunities were rather general which is problematic for learning opportunities such as consumer associations since adolescents might have different conceptions of consumer associations which could be a potential explanation for the negative association with students’ financial literacy. This limitation could be alleviated by defining different learning opportunities as part of the survey. Furthermore, it is not possible to explain why certain learning opportunities were used and neither whether the kind of usage differs regarding different learning opportunities. Other studies assume that informal learning processes depend more upon the students’ socioeconomic background than learning at school, that is, more formal learning processes (Aprea, 2012; Stecher, 2005). More research is needed in this regard in order to investigate the underlying mechanisms of (informal) learning opportunities and financial literacy. In this context, it is also relevant to investigate the quality of the different learning opportunities.

Although there are limitations to the results of this research, both the analysis of gender differences in a multi-dimensional model of financial literacy and the inclusion of learning opportunities and their role for students’ financial literacy are important contributions to the field. Since financial literacy is a crucial competence for adolescents to develop in today’s service society, the results provide practical implications in addition to the theoretical implications shown earlier. In particular, the results emphasize the relevance of different learning opportunities for male and female learners. In consequence, the promotion of financial literacy in school and during informal learning should take these differences into account. For instance, supporting students’ own experience in the areas of money and payments, savings, and insurance, for instance, through game-based approaches, could potentially support students’ skill development in these dimensions. Although our results are not quite conclusive yet, it should be noted that girls and boy at least partially acquire financial literacy in different ways.