Abstract

Changes in the economy and society lead to a growing necessity of financial education. In this context, we investigate the approaches to financial education in secondary schools in the United States and Germany. We seek to answer the question if and how the implementation of financial education is similar and different between the two countries. We address this question for financial education by comparing the educational conditions, coursework structures, content standards, instructional resources, and assessment within each country. Additionally, we focus on differences in cognitive structure of financial knowledge and understanding among students within each country. For this exploratory analysis, we used data from the Test of Financial Literacy that was administered to students in the United States and Germany (n = 2326). The empirical results reveal differences in knowledge structures in specific content areas among students in the two countries. Possible reasons for such differences and other implications are discussed.

Introduction and conceptualization

The financial system is constantly changing in both the United States and Germany. For example, digitalization has opened access to complex financial assets, making it easier for individuals to buy goods and services and potentially mis-managing their personal finances. Furthermore, pension reforms in both countries have transferred the responsibility for retirement planning to employees and demographic changes such as increasing life-expectancies have put pressure on the finances of social welfare systems (Choi, 2015; Kilgour, 2018; Schön, 2020; Stolper and Walter, 2017; Vogt, 2017). These changes and others in the financial system require individuals to be more and more financially autonomous. Eventually, such developments also increase the necessity for people to manage personal finances in various roles as consumers, workers, savers and investors responsibly. In the US, there has always been a higher responsibility for the individual and that is probably one reason why financial education has been a longer tradition in the US.

The approaches to financial education in each country is therefore considered to be a topic worthy of further investigation as this might help to get a better understanding how each country educates its people to handle their personal finances. Our goal is to determine if different, or maybe equal, knowledge structures concerning personal finance exist in the two countries and whether such differences or equivalences can be derived from the countries' approaches in financial education. This comparative study is divided into two parts to answer the following research questions: 1) What are the similarities and differences in how the educational systems of the USA and Germany address the need for financial education? 2) How does the structure of financial knowledge and understanding differ among students within each country? By conducting a structured qualitative analysis of the countries’ approaches, curricula and underlying conditions concerning financial education, we try to answer the first question. To address the second research question, a quantitative analysis is conducted using data from the same financial literacy test that was administered to students in both countries. This exploratory analysis uses the test data to investigate differences in the structure of financial knowledge among German and U.S. students.

Our investigation, however, is limited to upper secondary education because it is at this level where substantive financial education starts to be covered in the school curriculum. After providing a brief conceptual background, the paper’s initial sections describe the different aspects of financial education in the United States and Germany such as conditions, coursework, content standards, instructional resources, and assessment. The following section features the assessment by analyzing and presenting data from a standardized test of financial literacy administered to students in both countries. In the last section, the study concludes with a discussion of the key findings concerning the approaches to financial education derived from the qualitative and quantitative analyses along with potential connections for further investigations.

Conceptual background

Prior to the analysis, there is the necessity for conceptual clarification to establish a basis for discussion. Generally, the broad field of economic education aims at fostering economic literacy and in this instance education in personal finance, which aims at fostering financial literacy, is seen as a subsection of economics (Seeber, 2012b: 261). The Organization for Economic Cooperation and Development (OCED) defines financial literacy (FL) as “the knowledge and understanding of financial concepts and risks, and the skills, motivation and confidence to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, to improve the financial well-being of individuals and society, and to enable participation in economic life.” (OECD, 2019: 128). Accordingly, FL is seen as a multidimensional construct consisting of a knowledge and understanding dimension and an application dimension. In this respect, we see knowledge and understanding as the core component necessary for the development of financial literacy. Whereas economic literacy has vocational and civic dimensions (Dubs, 2014; Eberle et al., 2016), financial literacy should primarily result in the empowerment of a person as economic citizen to successfully manage day-to-day financial issues. More broadly, financial literacy can be conceptualized in three ways as: a) management education for personal finances; b) critical consumer education for buying goods and services; and c) economic or socio-economic education (Aprea et al., 2015: 91). By following the first concept, we understand education in the core contents of financial issues (see Content standards for financial education) to be essential for personal finance management and are thus in line with the currently most circulated conceptualization of FL, which also acts as the basis for the Financial Literacy Framework of OECD’s Programme for International Student Assessment PISA (Aprea et al., 2015: 91).

Financial education in U.S. high schools

A first step for comparing financial education in high schools in the United States and Germany is to describe how financial education works in one country so it can be compared to the other. The United States serves as the basis for comparison as it has a longer history with high school economic and financial education (Walstad, 1992). To provide this context, the section focuses on five topics related to financial education in U.S. high schools: educational conditions, coursework, content standards, instructional resources, and assessment.

General conditions for financial education

The challenge of describing U.S. financial education is evident from public school data and legal conditions. According to recent statistics, public school enrollment in grades 9 through 12 was approximately 15.2 million (Digest of Education Statistics (DES), 2021, Table 203.10). These students attended 30,458 public schools in 13,452 public school districts (DES, 2021, Tables 214.10 and 214.20) which have local control over the educational curriculum. That local control, however, is subject to the curriculum and coursework requirements of the 50 states. Consequently, curriculum and instruction in a non-core subject such as personal finance will vary across states and even across school districts within a state.

These differences in the financial education requirements have been investigated as initial indicators of the condition of financial education in U.S. high schools. A bi-annual Survey of the States (CEE, 2020) assesses the inclusion of financial education into the curriculum, which is significant: (1) 45 states include personal finance in state curriculum standards; (2) 37 states require that the standards be implemented in some way; (3) 24 states require that a personal finance course be offered; (4) 15 states require that personal finance content be integrated into the coursework for another course; (5) 5 states require standardized testing of concepts in personal finance; and (6) 6 states have a mandate that a required course in personal finance be taken before high school graduation. These data also show significant improvement over time (CEE, 2020).

Coursework and course types for financial education

For most students, course instruction in personal finance in U.S. high schools is of two types. The first one is a standalone course in personal finance that is the equivalent of about a half-year of school instruction, in which case the course will contain a substantial amount of personal finance content. The second one is a cross-curricular course in another subject, in which personal finance content is included, but coverage is limited. These cross-curricular courses can be offered in many areas of the curriculum such social studies (particularly economics), education (business, vocational, technical, or career) and mathematics.

What adds complexity to the course types is that they either can be mandated (required) or elective courses for high school graduation. Most mandates for instruction in personal finance come from state legislations. Six U.S. states have a mandate for a standalone course and these states enroll 11% of high school students in grades 9 through 12. Another 15 states have a mandate for a cross-curricular course and these states enroll 38% of high school students. The combined percentage (49) for the state mandates indicates that coursework in personal finance is far from universal in U.S. high schools.

In states without course mandates school districts may independently require students to complete a standalone or cross-curricular course or student can take the course as elective if offered by a school. The percentage of students receiving instruction in these ways, however, is likely to be relatively limited for two reasons: (1) intense demands on the school curriculum for required instruction in many different subjects that may “crowd-out” personal finance; and (2) a general lack interest in taking personal finance as an elective (Walstad and Rebeck, 2012).

Content standards for financial education

Although content in core areas of high school curricula (e.g., mathematics) is usually commonly agreed on, there is less agreement about what specific content should be covered in high school courses in personal finance. Accordingly, each state department of education has its own standards that specify what should be taught about personal finance (compare further: interactive map of the AFSA Education Foundation: afsaef.org/state-interactive-map/), and each school district within a state may provide further standards that complement or extend the state standards.

Although the U.S. federal government does not issue national standards, some non-profit educational organizations fill that void by issuing voluntary national standards. One prime example is the National Standards for Financial Literacy (CEE, 2013) (hereafter FL-Standards) that divides personal finance content into six standards: (1) earning income; (2) buying goods and services; (3) saving; (4) using credit; (5) financial investing; and (6) protecting and insuring. Each standard contains a general statement describing its rationale and content that is followed by benchmarks that explain what students should know about that standard by the end of at three grade levels (4, 8, and 12). 1 Associated with each benchmark are examples of what teachers might do to help their students demonstrate understanding. The descriptions also include a decision-making section with three parts: planning and goal setting; making a decision; and assessing the outcome.

The FL Standards have several features that make them unique and potentially more useful to state departments of education, school districts, curriculum developers and teachers (Bosshardt and Walstad, 2014). First, they integrate financial decision-making into each standard instead of treating decision-making as a separate topic. This inclusion emphasizes weighing costs and benefits in decision-making and rather a normative perspective that tells students what they should or ought to do to manage personal finances. Second, they describe the economics foundation for each of the six standards because economic concepts are an essential part of personal finance. They recognize, for example, that a choice about spending or investing has an opportunity cost. Third, they provide insights from behavioral economics when appropriate for a standard.

Instructional resources and teaching materials for financial education

Teacher preparation and training can influence how well a subject is taught to students. In most core subjects in the high school curriculum, such as mathematics or the sciences, a university education prepares students for their future teaching responsibilities through academic coursework and training in pedagogy. In contrast, future financial educators receive minimal preparation in their undergraduate education through academic content in such subjects as economics (Bosshardt and Walstad, 2019) or training pedagogical skills. Consequently, many teachers of personal finance reported in a national survey that they were ill-prepared to teach the subject and desired more content and pedagogical training (Way and Holden, 2009).

Further help for teachers, however, beyond published content guidelines, comes from the extensive instructional resources in personal finance that are available from many different organizations. The available instructional resources are evident from browsing the websites of for notable non-profit educational organizations: Council for Economic Education (www.councilforeconed.org); Jump$tart (www.jumpstart.org); Next Gen Personal Finance (www.ngpf.org); and Junior Achievement (jausa.ja.org). In addition, state departments of education at their websites sometimes include instructional resources or links to resources related to their personal finance standards (e.g., Nebraska: www.education.ne.gov/nce/bmit/curriculum/personal-finance/). Instructional resources also are available at the national or Federal level such as at government agencies as the U.S. Department of Treasury (www.mymoney.gov) or at the regional banks of the Federal Reserve System (e.g., St. Louis: www.stlouisfed.org/education).

Assessment of financial education

A final concern with financial education is with assessment of what high school students know and understand about the subject. A national answer to this question requires the development of a reliable and valid assessment instrument and administration to a nationally representative sample of U.S. high school students. This approach is what the National Center for Education Statistics (NCES) does when it conducts a National Assessment of Educational Progress (NAEP) in high school subjects (nces.ed.gov/nationsreportcard/). The closest NAEP subject to personal finance would be NAEP economics, which was first administered in 2006 and again in 2012 (NCES, 2013), but no further assessment in economics has been conducted.

At the international level, the Programme for International Student Assessment (PISA) on financial literacy was conducted in 2012, 2015, and 2018. The four main content areas for the PISA test were money and transactions, planning and managing finances, risk and reward, and the financial landscape. Test questions were aligned with four process categories: identify financial information, analyze information in a financial context, evaluate financial issues, and apply financial knowledge and understanding. The context for the financial literacy questions included education and work, home and family, individual and society. In 2018, about 117,000 students around the age of 15 took the financial literacy test in 20 countries including the United States. The U.S. score of 506 put it about average among the member states (OECD, 2020).

For completeness, a further point should be noted about comparative studies. Assessments of financial literacy are also conducted with just three brief items that have come to be known as the “Big Three” and as such covering the topics of interest rates and compounding, inflation and risk diversification (Lusardi, 2019; Lusardi and Mitchell, 2014). The Big Three were used in a series of international comparative studies like the Health and Retirement Study (HRS) in the United States and the SAVE study (Sparen und Altersvorsorge) in Germany (Hastings et al., 2013: 353–354). Additionally, variations of the Big Three exist as they were sometimes expanded to five (“basic”) or eight (“sophisticated”) items (Lusardi and Mitchell, 2009). From a measurement perspective, however, they are not the same as a standardized achievement test for high school students such as NAEP or PISA as there are few items and they are of mixed type (multiple-choice and true-false). They serve as “indicators” of the level of financial literacy among adults and are designed for inclusion within the limits for surveys on many topics such as the National Financial Capability Study NFCS (www.usfinancialcapability.org/about.php) and other ones conducted in the United States and other countries.

Although NAEP or PISA are useful for national or international comparisons of high school student achievement, they are not useful for classroom assessment with students given their complex design features and test items that are unique to a test or may not be available for widespread use. One assessment measure in the United States that has been developed for classroom use by teachers and school administrators is the Test of Financial Literacy (TFL) (Walstad and Rebeck, 2017). The test items are a representative sample of the content described in the standards and benchmarks of the FL Standards (CEE, 2013).

Financial education in German high schools

The following section mirrors the analytic approach to the situation of financial education in Germany. For our analyses, we focus on grades 10–13 and as such, on the highest level of secondary education in Germany.

General conditions for financial education

In Germany, like in the U.S., there is no uniform curriculum for each type or level of school. Nor is there a common national strategy 2 for financial education (Kaiser and Menkhoff, 2021). Due to the German federal system, each of the 16 states is responsible for the education system and its contents in its jurisdiction (Erner et al., 2016: 97). Consequently, educational coverage of economic and financial contents is quite heterogeneous and not systematically embedded in every state’s curriculum (Happ and Förster, 2019). Furthermore, the country’s federal structure is said to be one of the reasons why a common national strategy for financial education has not yet been implemented in Germany (Grifony and Messy, 2012: 14). A recent study conducted by the Institut für Ökonomische Bildung (IÖB, Institute for Economic Education) on behalf of the Flossbach von Storch Foundation stated that eleven out of 16 German states do not meet even half the prerequisites necessary (e.g., contingents of lesson hours) to establish Economics as a subsidiary subject (IOEB, 2021). According to IÖB’s OeBiX 3 (Index für ökonomische Bildung, Index for Economic Education), the states of Lower Saxony, Baden-Wuerttemberg, and Bavaria perform best on the subindex “Economics in School,” 4 while Hamburg, Saxony, and Rhineland-Palatinate perform worst (OeBiX, 2021). The curricular analyses will further focus on the states of Baden-Wuerttemberg, Bavaria, and Rhineland-Palatinate to provide three different examples in more detail. However, it must be added that the differences in the scope of economic topics between the school forms also vary greatly within the individual states. Generally, for most of the states, it can be said that the higher the school type the less economic content is taught.

Coursework and course types for financial education

One initial finding confirms the close connection between economic and financial education (Seeber, 2012b: 261) as it sometimes was difficult to draw a clear distinctive line between economic content and financial content within the curricula of the German states we investigated. Results further illustrate that economic education is quite heterogeneous when it comes to structure and coverage on a course level. Table B1 (Supplementary Appendix B) gives an overview of how the contents of personal finance and economics are spread across subjects within each of the analyzed states. Like in the U.S., economic and financial contents are taught either in separate, standalone courses (Bavaria, Baden-Wuerttemberg) or integrated in other subjects as part of a broader cross-curricular or inter-disciplinary education (Rhineland-Palatinate). Depending on the state and the chosen course of study, most of the courses seem to be mandatory. Occasionally, basic courses can be combined with cross-curricular elective courses (e.g., business ethics 5 ).

Concerning the school types, vocational and general education schools (Grammar Schools) were of particular interest for our investigation as these schools should prepare learners directly either for a subsequent career start or a university study program, both of which require a solid financial preparation. However, a comprehensive discussion about the respective curricula cannot be part of this contribution and the overview displayed in Table B1 can only act as a starting point for further comparison, but we will point out some of the most noticeable findings. The state of Baden-Wuerttemberg clearly shows the most thorough coverage of economic contents. It is worth mentioning that the Vocational high school (Berufliches Gymnasium) as the highest institution for vocational education can be further differentiated according to special interest profiles within this institution (e.g., schools with special focus on financial management, commercial training, social services and the like). According to this differentiation, the depth and the extent of economic education varies, but on a very sophisticated level. The Bavarian FOS (Technical high school)/BOS (Vocational high school) as an upper secondary education institution in Bavaria offers a course of International Business Studies in grade 12. It must be mentioned, however, that due to the heavy focus of the FOS/BOS on vocational education, course content is more about future job qualification, vocational preparation and the structure and prerequisites of labor markets than on general economic and financial content. In Rhineland-Palatinate, economic education is much capable of development. According to the OeBiX study, the state is clearly at the end of the country comparison which can be traced back to the fact that economic content is taught only very limited in cross-curricular—but mandatory—subjects.

Content standards for financial education

Although the FL-Standards were formulated for the U.S. curriculum, expert interviews have shown that these content areas also seem to be valid for young adults in Germany (Happ et al., 2018; Förster et al., 2019). Confirmatory factor analyses on the German version of the TFL indicate that the six content areas can be compiled into a three-dimensional model ((1) everyday money management; (2) banking: financial investing, saving and using credit; (3) insurance: protecting, insuring) with correlation coefficients over 0.90, thus rendering an outright separation ineffectual (Förster et al., 2018). In essence, this means that the U.S.-driven CEE-Standards can act as a potential guideline for Germany. Furthermore, Table B1 reveals that the financial contents identified in the German curricula can be assigned to the various CEE-Standards. It therefore becomes clear that in the chosen German states adequate coverage of the content standards exists, but with variations in depth and extent depending on the state and the respective school type. Again, the state of Baden-Wuerttemberg shows a very comprehensive coverage of financial topics that are consistent with the FL-Standards.

Unfortunately, a common structural model concerning explicit contents of FL has not been drafted for Germany, yet. However, a suitable connection can be found in the “Competence Model for Economic Education” (Retzmann et al., 2010a; Seeber, 2012a) formulated by the working group “Economic Education” of the Joint Committee for the German Commercial Economy. This model interlinks the roles an individual can take in an economic society (e.g., consumer, employer, earner, economic citizen) with domain-specific aspects (e.g., rational decision-making, relationship and interaction with other participants in markets and the economy) to create a three-tiered competence matrix which describes levels and characteristics of an individuals' economic behavior (Retzmann et al., 2010a: 7, Figure 3). Like the CEE-Standards, this model differentiates educational standards according to educational levels and certificates in the German School System and bears on life-like situations, that is, tasks 6 which are embedded in short situational and financially relevant prompts. The task content is most likely comparable for the U.S. and the German model as both approaches cover tasks and questions, for example, about buying decisions, investing or insurance. But while the CEE-Standards focus mainly on the core components of FL, the German conception takes on a broader perspective by additionally integrating general economic contents like micro- and macroeconomics along with a vocational- and business-oriented aspect. The common denominator for both the U.S. and the German approach is the inclusion of the individual as consumer who is part of an all-embracing economic system and should therefore be able to actively participate in the economic life. 7

Instructional resources and teaching materials for financial education

As mentioned, the basis for all educational efforts should be a pool of sophisticated and elaborated teaching materials that helps not only to give a vivid description of domain-specific relevant problems but also provides instructional resources to teachers. Like in the United States, instructional materials can be found in the schools’ official coursebooks (again, depth and extent may vary according to state and school type) as well as in pools that are provided by external organizations. In Germany, the Deutsche Bundesbank (German Federal Bank) provides a comprehensive pool of educational material for various levels of education from primary to upper secondary education (www.bundesbank.de/de/service/schule-und-bildung/unterrichtsmaterialien) along with numerous graphics, statistics and further information materials for educators. Additional material, especially on financial education for young adults, is provided by the Deutscher Bildungsserver (German Educational Server). Besides the material that is provided by public institutions, numerous private organizations, companies or NGOs share material, teaching concepts or even comprehensive educational programs to foster economic education. Programs like “SCHUFA macht Schule” by the German credit agency SCHUFA, the school project by the “Stiftung Warentest” (a charitable foundation for consumer protection), the initiative “Handelsblatt macht Schule” by the Handelsblatt (a German newspaper corporation with focus on Economics and Finance) or the program for Financial Education by the Verband der Privaten Bausparkassen (Association of private building societies) can act as evident examples. However, although the support and the promotion of economic and financial education by private institutions and organizations is often fueled by good intentions, it shout not go unmentioned that there is also a major discussion about the potential risk privately funded programs or externally provided materials can have on economic education (Engartner and Krisanthan, 2016; Hedtke, 2016). Educational materials, especially in the field of Economics and Finance, can be ideologically biased or may contain “hidden advertising” to promote specific financial products or services, which can be deliberately misleading or even potentially harmful for younger learners in particular who are impressionable more easily. It is therefore necessary to ensure that materials are free of bias and that they are provided by independent and trustworthy sources.

Assessment of financial education

Although the numbers of national FL-studies have risen in Germany over the past couple of years, research on deeper understanding in personal finance is capable of improvement and international comparison is still limited. The most prominent take on the international assessment of economic education has been done by OECD’s PISA, but Germany did not take part in its optional FL-section (Frühauf and Retzmann, 2016; Förster et al., 2018) since the Standing Conference of the Ministers of Education and Cultural Affairs (Kultusministerkonferenz) found the concept of FL to be not developed enough to be considered as part of a comprehensive national survey (Sälzer and Prenzel, 2014: 20). Thus, a direct comparison to the U.S. results is rather impossible. A series of classroom assessments, however, using the German version of the TFL has been conducted in recent years, which might be a more reliable basis for international comparisons. Using a German version of the TFL (Förster et al., 2017; Happ and Förster, 2017, 2019) found that the U.S. instruments fit very well to German students. 8

At this point as an interim conclusion, we can answer the first research question about the necessity for financial education along with the similarities and differences in the educational approaches in secondary schools in the U.S. and Germany. Over the years, financial education in secondary schools has grown in importance in the United States (CEE, 2020) and in recent years, it has also attracted more interest in Germany (Kaiser and Menkhoff, 2021). Consequently, it seems that at least an awareness for economic and financial education exists in both countries and that a certain basis is already established as a potential starting point. Although the history of financial education in secondary schools differs between the two countries, identified implementation strategies face similar problems. Both countries leave responsibility for financial education and control over its delivery to state governments within their respective federal systems. Thus, both countries have no uniform strategy for financial education—or, in the case of Germany, no national strategy at all—and federal structures result in rather heterogeneous educational approaches.

Due to the variety of approaches it appears to be difficult to establish a common concept even for one single country, let alone general conceptions that are directly comparable across countries. Interestingly enough though, concerning actual contents of financial education there seems to be an overlap as a relatively good coverage of the U.S. content standards for financial literacy could also be identified for the school curricula in the examined German states. Additionally, in both countries, various NGOs and private organizations provide instructional materials that should further support educational endeavors in economic and financial education. Although this means that there seems to be potential for the comparison of financial content knowledge and understanding in the U.S. and Germany, the question remains how these knowledge structures are developed in students from each country.

Comparing financial knowledge and understanding

The previous explanations of financial education in the secondary school curriculum in the United States and Germany clearly show that each country conducts financial education in different ways. This heterogeneity means it is difficult to draft concrete expectations when comparing empirical test results. Therefore, in the following analysis we use an exploratory approach to investigate the differences in financial knowledge and understanding between secondary students in the two countries using a common test instrument. The purpose is to investigate whether the structure of financial knowledge and understanding differs between the two countries and whether there are country-specific advantages in certain content areas.

Instrument and sample

The Test of Financial Literacy (TFL; Walstad and Rebeck, 2016) was used for the comparative analysis. The 45 items on the TFL are multiple-choice items consisting of a short item stem, often with situational contexts, and four possible answers, one of which is the correct choice. For the U.S. version of the test, the items can be categorized in six dimensions following the six content areas described in the Content standards for financial education. The analysis from the U.S. test data using classical test theory (CTT) indicate that the TFL test is reliable and valid for use with U.S. high school students based on the content defined by the FL-Standards. Further test analysis was conducted using an item response theory (IRT) model and it shows that the measure is effective in assessing student financial literacy across a broad range of student abilities (Walstad and Rebeck, 2017). The TFL also has been adapted and validated for German use (Förster et al., 2017). Its items were adjusted to the German context over a six-month translation and adaptation process that followed the TRAPD-approach by Harkness (2003) and the Test Adaptation Guidelines (TAGs) (Hambleton, 2001). The German analysis also revealed that one item did not perform well, which was likely due to language-related difficulty in comprehension (Förster et al., 2017). Consequently, the number of items of the TFL that were used for the present country comparison was reduced to 44.

This comparative study used the U.S. TFL sample of 1218 high school students in grades 11 and 12 (ages 16–18) who were tested in 48 schools in 27 states (see Walstad and Rebeck 2016 for more details). It also used a German sample of 1108 first-year university students (ages 17–25) who were tested at the beginning of their first semester at a German university in different study programs (see Förster et al., 2017 for a detailed description). Although the two samples differ in their characteristics (ages and academic level), such differences are not central to the purposes of this study as they would be if we were interested in comparing the absolute level of financial knowledge between the two samples. Instead, this study focuses on the structure of financial knowledge and country-specific differences, so the absolute difference in the level of financial knowledge is not relevant here. We follow the approach of controlling for mean achievement differences, and then investigate task differences.

Dimension models and results

The TFL is a test of cognitive achievement that covers six different content standards. Analyzing the dimensional structure of the test allows us to obtain insights in the cognitive structure of the test takers. The research question to be answered from the empirical analysis is whether the structure of financial knowledge and understanding is comparable in both countries. Using the same instrument allows us to compare the cognitive structures using the test scores from students in each member state. The results from the analysis provide an indicator of national differences in the overall structure of financial knowledge and understanding.

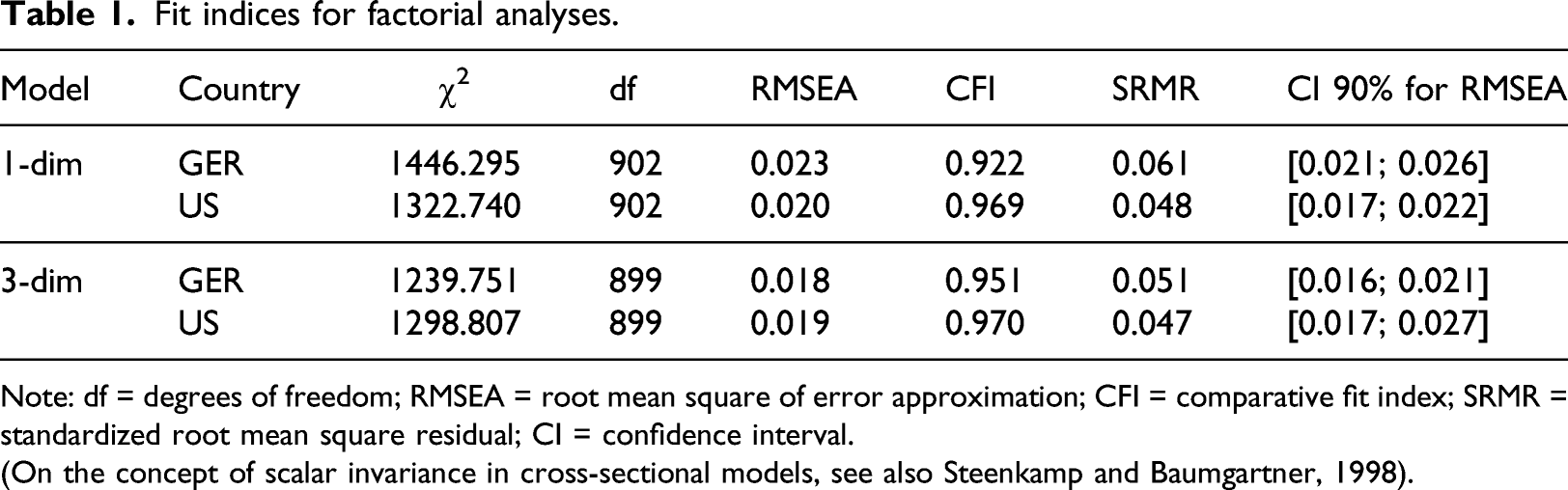

Fit indices for factorial analyses.

Note: df = degrees of freedom; RMSEA = root mean square of error approximation; CFI = comparative fit index; SRMR = standardized root mean square residual; CI = confidence interval.

(On the concept of scalar invariance in cross-sectional models, see also Steenkamp and Baumgartner, 1998).

Analysis of the test data was further conducted with a three-dimensional model based on the work from a prior study in Germany (Förster et al., 2018) as described in the section above. For the German sample, results show a significantly improved fit for the three-dimensional model compared to the one-dimensional structure. We also investigated whether this three-dimensional structure applies to the U.S. students. Results also show improvement in the fit values (Table 1), but to a much smaller extent compared to the German sample. 9

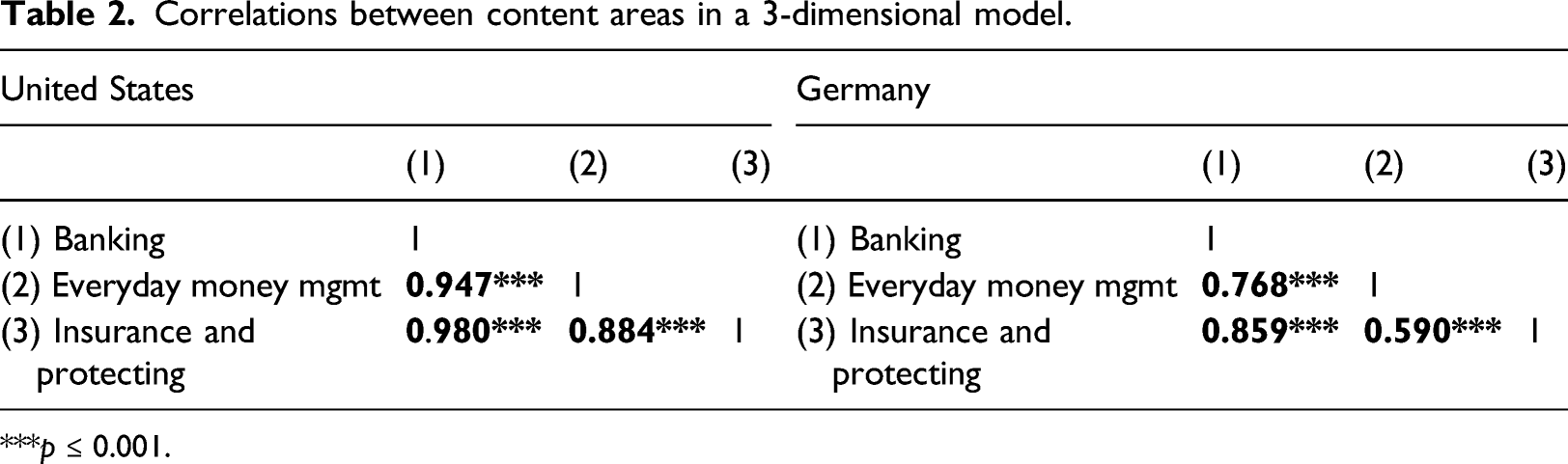

Correlations between content areas in a 3-dimensional model.

***p ≤ 0.001.

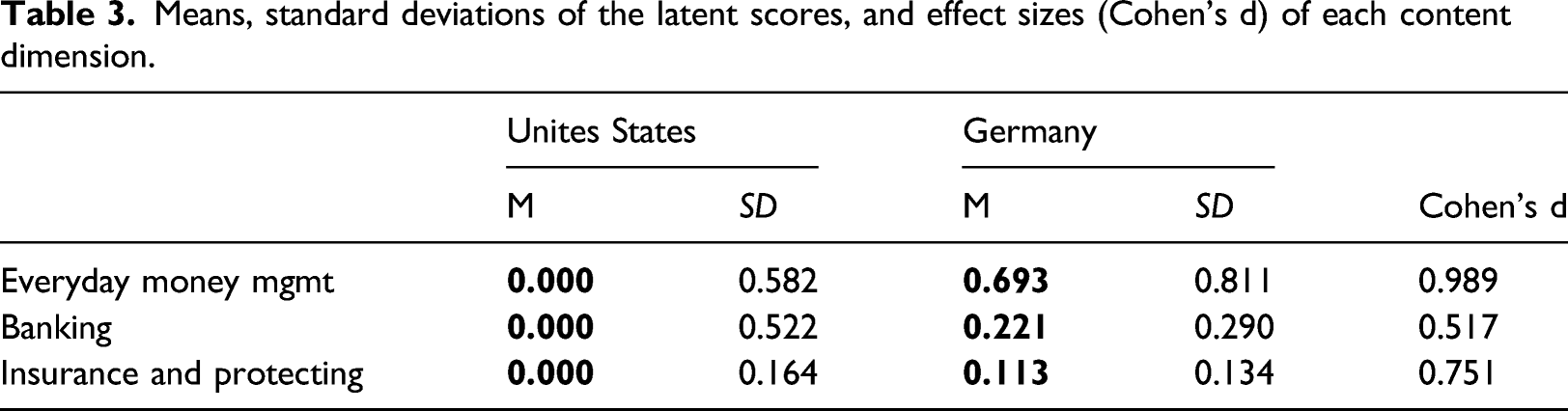

Means, standard deviations of the latent scores, and effect sizes (Cohen’s d) of each content dimension.

Item analysis and results

In the next step, two methods are used to further examine the existing differences at item level in more detail. First, the data are compared across countries via classical item difficulty analysis as this is a more intuitive approach and the numbers are easier to interpret. Second, we estimated a one-dimensional scalar invariance model where all factor loadings have the same value, which corresponds to the typical assumption that all indicators are equally weighted in the respective construct. An example of such a loading is the classical sum score, where each item is equally weighted in the respective score. In the TFL, this corresponds to the usual scoring. This model additionally allows to control for a basic mean difference in the knowledge of the two samples. Additionally, it allows controlling for this mean difference to identify items in which both groups of subjects perform disproportionately well or poorly. A one-dimensional approach seems appropriate here so that the differences in the individual items can be detected well and differences in the subdimensions become more apparent.

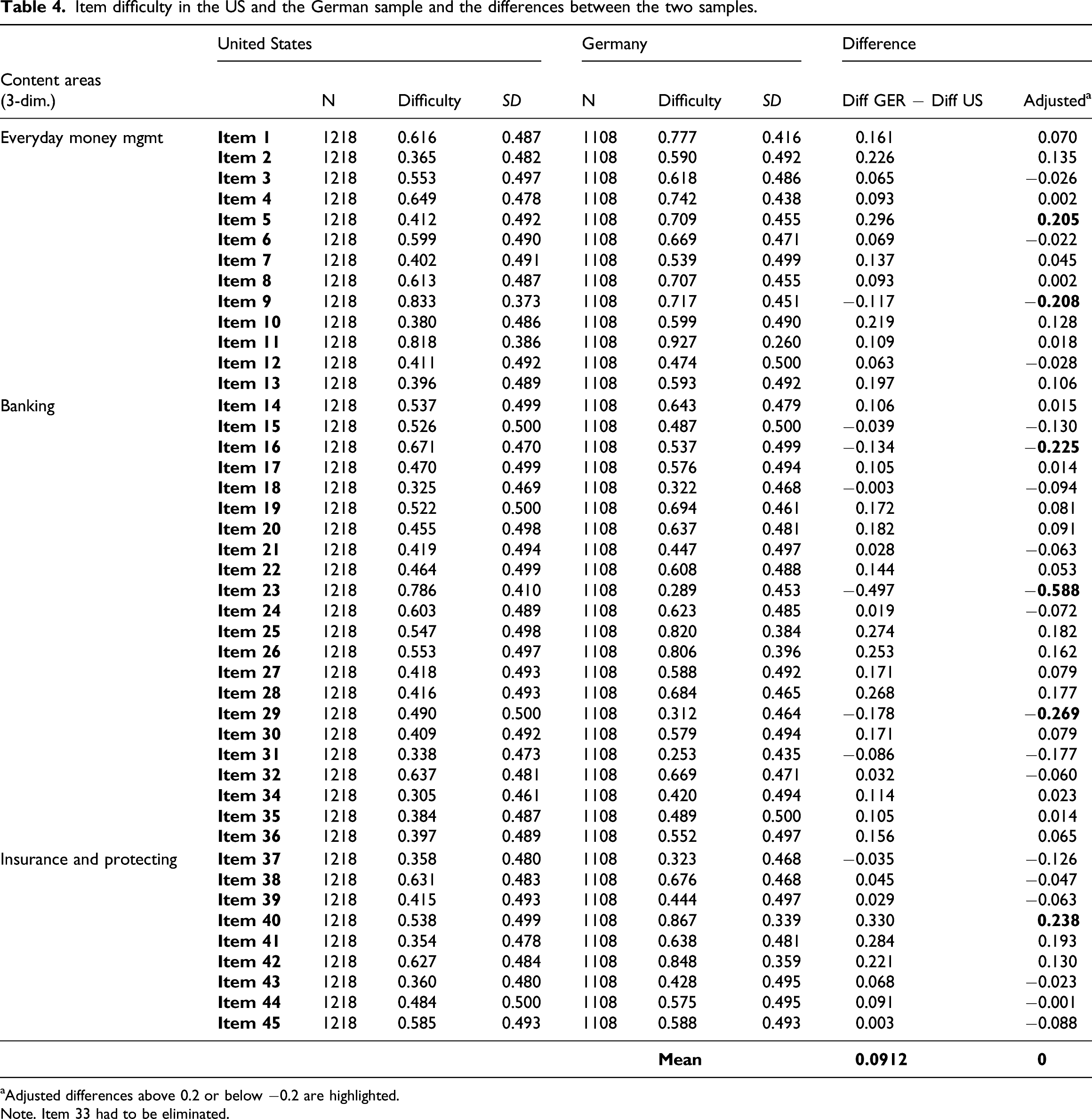

Item difficulty in the US and the German sample and the differences between the two samples.

aAdjusted differences above 0.2 or below −0.2 are highlighted. Note. Item 33 had to be eliminated.

The adjusted differences between the two countries can be summarized as follows: for the 44 items, the solution frequencies differ by less than 10% for 27 items, between 10% and 20% for 11 items, and more than 20% for 6 items (see: Supplementary Appendix A). At the same time, it can be noted that items with greater than 20% differences are distributed across all three content dimensions.

The results from items 9, 16, 23 and 29 are particularly noticeable as they favor U.S. students. An especially large difference can be found in question 23, which the U.S. students solve with a 49.6% higher frequency (58.8% adjusted). This result clearly indicates that U.S. students know that the payment history has a significant influence on the credit score, while a large number of German students are not aware of this. In Germany, the belief prevails among students that it is primarily income that determines a credit score. In comparison, German respondents show a disproportionately large advantage in car insurance and understanding the labor market. German respondents are significantly more aware that increased home mortgages are the most likely of the above-mentioned events to increase wages in the construction industry. There was also a country-specific adjustment in the correct answer to question 40. The item describes that in Germany purchase of automobile insurance is mandatory by law, whereas in the U.S. purchase of automobile insurance can be required by the state or the lender. The German participants were much more aware of the legal regulation.

Discussion

This section will now summarize the findings and the results of both the qualitative and quantitative investigations undertaken in this study. The structured qualitative comparison of financial education in the United States and Germany shows that there is great heterogeneity both between the countries and also within each country. This feature can be explained by the fact that in both countries the questions of whether and how economic and financial topics are included in the states' curricula lie in the decision-making area of the respective federal states. Consequently, the scope and the implementation of financial content in educational endeavors vary considerably as there is no shared common national framework for economic and financial education in each country. Decentralized decisions are also made as to whether the content is implemented within a separate subject (e.g., economics or business) or cross-curricular (e.g., in combination with social studies or general business courses). All these circumstances result in rather inconsistent approaches when it comes to foster financial and economic education in each country.

Nevertheless, it is possible to compare the cognitive structure among U.S. and German students who have taken the same test of financial literacy. Based on the comparative test data, the cognitive structure in the area of financial knowledge and understanding is more finely differentiated among German students, as the results show that the three content dimensions of Banking, Everyday money management (income and buying) and Insurance and protecting are less correlated with each other. Among U.S. students, the cognitive structure appears to be more one-dimensional. Furthermore, the German students perform substantially better than the U.S. students in all three content dimensions. This outcome may be explained by the slightly different target groups and the stronger selection of the German sample. As a result, the levels of knowledge and comprehension are only comparable to a limited extent, but it is noticeable that the differences are greatest in the content area of Everyday money management and smallest in the content area of Banking. Another possible explanation for these country differences may be found in the school curricula themselves. Curricular analysis for Germany (see Table B1, Supplementary Appendix B) indicates that the content areas of Buying goods and services and Earning Income are covered rather well and extensive in almost all of the analyzed schools and subjects in the three states. This means that the basics of day-to-day economics are part of the school’s economic education - even though single topics within these areas are somehow “just” embedded in cross-curricular and inter-disciplinary subjects. It is rather the special topics in the field of Banking (e.g., private accounting, financial assets, deposits) which are either completely missing or are only covered in a very shallow manner in most of the state’s curricula. This observation might explain the relatively moderate effect in this content area. This result may also act as a potential starting point when it comes to the discussion about possible improvements in curriculum content and instructions in the syllabi. Another explanation might be that the German students are a little older and are in a slightly different life situation. The start of their university studies is often accompanied by greater financial independence, as a result of which students set up their first own households and become more financially independent. It is conceivable that the cognitive structure in these areas of financial understanding differentiates more strongly in the course of life, because more and more financially relevant learning opportunities are experienced.

Finally, country-specific cultural characteristics may also contribute to differences in financial knowledge and understanding, as culture is significantly influenced by the media or financial socialization in the family (Happ and Förster, 2019; LeBaron and Kelley, 2021). Explanatory approaches can be outlined here using two exemplary items for which major country differences were found. It was noticeable that the U.S. students are clearly more aware of the rules of the financial market in the form of deposit insurance (item 16) and credit score (item 23). In Germany, it may be the case that the deposit insurance is not discussed or not perceived as important. Before the financial and economic crisis in 2008, there were hardly any cases of (German) banks going bankrupt that attracted public attention. And even during the economic and financial crisis, many banks were financially supported by the state so, again, hardly any banks went bankrupt. This situation may lead to a lack of interest in knowing about the Deposit Protection Fund, as the protection of deposits is seen as a state task. In the U.S., on the other hand, there are limits to deposit protection for each bank account and consequently, individuals’ understanding deposit insurance might be more important.

As for credit scores, our findings may also be explained by cultural differences between the countries. In Germany, the credit score is generally queried for larger and longer-term loans and this also influences the credit rate. In the U.S., on the other hand, credit rate seems to be influenced by the credit score to a much greater extent. For example, in the U.S., the percentage for a car loan can vary between 3.6% for the best credit score group and 15.24% for the worst credit score group, or between 3.9% (4.55%) and 5.5% (6.35%) for a 30-year fixed mortgage rate, respectively (as practical examples: Credit Sesame, 2019; Irby, 2021). Thus, knowledge and understanding about credit score is once again more important in the United States than in Germany. Moreover, few young people in Germany come into contact with SCHUFA (the German credit agency) because a large number of the purchases and contracts for which the credit score becomes significant are made by their parents. Due to the significantly lower debt and credit financing ratio in Germany, the issue may not be as prominent as in the USA. 10

In this respect, future research should also take cultural differences into account, as the heterogeneity in financial education within the two countries hardly provides convenient starting points for a systematic comparison of the two education systems. At the same time, our studies can be seen as an initial starting point in the area of financial knowledge and understanding. Culturally different attitudes, such as risk tolerance, may also lead to different forms of investment and financing and eventually to different financial actions and should thus also be part of future investigations. Last, at item level in multiple-choice assessments, one can look more closely at the distribution of distractors in each country so that possible country-specific misconceptions may be identified. 11

Supplemental Material

sj-pdf-1-rci-10.1177_17454999221081333 – Supplemental Material for Comparison of financial education and knowledge in the United States and Germany: Curriculum and assessment

Supplemental Material, sj-pdf-1-rci-10.1177_17454999221081333 for A Comparison of financial education and knowledge in the United States and Germany: Curriculum and assessment by Andreas Kraitzek, Manuel Förster, and William B. Walstad in Research in Comparative and International Education

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.