Abstract

Background:

We assess whether a family history of Alzheimer’s disease (AD) is associated with the odds that healthy family members’ engage in retirement planning activities.

Methods:

This is a cross-sectional study utilizing individual-level data from the Utah Population Database that have been linked to Medicare records and to responses from a retirement planning survey. Engagement in 3 retirement planning activities was estimated as a function of the number of parents and grandparents diagnosed with AD along with a set of fundamental socioeconomic and demographic covariates.

Results:

Adults who had a parent with AD were 86% more likely to have seen a professional financial advisor and 40% less likely to plan to retire before age 65.

Conclusions:

Caregiving costs and/or knowledge of the familial risk of developing AD may provide adult children with a forewarning of their own future financial needs that, in turn, motivates them to engage in retirement planning.

Introduction

An Alzheimer’s disease (AD) diagnosis has consequences that can extend beyond the individual to family members. These impacts, which are especially strong for caregivers, include worries about the health of the affected relative, changes in the caregiver’s health (eg, risk of depression), and/or distress regarding what the diagnosis portends for the caregiver’s own future health or that of other relatives. Family members may also experience distress related to changes in family and social relations, finances, and/or work patterns that are a function of an AD diagnosis. 1 –6

In recent years, concern about an AD diagnosis and what it means for the health of the affected individual’s adult children has been heightened by the growing public awareness of the disease’s heritability and clustering within families. 7 –10 Research focused on the impact of genetic testing for AD risk has found that knowledge of an elevated genetic risk is linked to changes in individuals’ health behaviors 11,12 and their likelihood of purchasing long-term care insurance. 13 In this study, we investigate the extent to which a family history of AD is associated with an additional, future-oriented behavior that has significant implications for later life well-being—planning for retirement. Specifically, does a family history of AD accelerate or attenuate retirement planning, and does this relationship vary depending on the family relationship involved?

We focus on healthy adults with a family history of AD and their retirement planning activities for several reasons. First, these individuals have an elevated risk of developing the disease themselves, 1,2,8,14 –16 and it may be that such knowledge influences their retirement planning. Second, family members are most often the informal caregivers of individuals who have AD. 1,17,18 For adult children, these caregiving responsibilities frequently come in midlife. One study found that the average age of adult children who were caregivers of a parent with AD was 51, 17 an age at which reducing paid employment or exiting the labor force may have dire consequences on lifetime earnings and retirement savings. Third, even if the individual is not the primary caregiver for a relative who has AD, distress regarding the diagnosis and/or the need to contribute financially to caregiving support 3,19 may affect her or his own long-term financial planning. Finally, there is a growing concern about the inattention that Americans more generally give to retirement planning. 20,21 Research has identified many sociodemographic correlates of inattention to retirement planning, 22 –27 but little attention has been devoted to the role that family health histories may play.

Methods

Our analyses are guided by the life course framework as applied to retirement planning. 28 This framework stresses the relationships between the multiple linked roles that an individual occupies over the course of his or her life and how events and their sequencing (eg, a parent’s AD diagnosis prior to one’s own retirement) can influence future actions. Researchers who have applied this framework to investigate questions related to the complex task of retirement planning typically focus on personal life course elements such as the age at which an individual secured his or her first job, the age at which the individual’s first/last child was born, the timing of marital status changes, and health considerations. Two recent retirement planning studies that utilize the life course framework find little evidence that own health is linked to greater probabilities of engaging in retirement planning activities and a greater likelihood of expecting to retire early. 29,30

It is not surprising that the relationship between own health and retirement planning is weak. The diagnosis of a serious disease prior to retirement is not a common event; most individuals must look elsewhere for a forecast of what their health might be in later life. Because both genes and environment play a role in chronic disease transmission and life expectancy, 31,32 an individual’s parents’ and grandparents’ disease experiences may foreshadow his or her own future health. An AD diagnosis of a parent or grandparent is a life course event for the adult child or grandchild that may have implications for the individuals’ time commitments and/or financial responsibilities. The individual may be drawn into caregiving and consequently reduce her or his paid work hours. Alternatively, the individual may need to divert funds to the care of the parent/grandparent that otherwise would have been devoted to retirement savings.

On one hand, a family member’s AD diagnosis may lead an individual to postpone or eschew long-range financial planning activities simply because she or he instead prioritizes activities that are more immediate. Evidence in support of this argument includes the findings that the significant time demands imposed on caregivers of patients with AD appear to precipitate higher levels of stress 33 and more physical health problems 34 than otherwise similar caregivers who were caring for an adult who did not have dementia. Such personal complications may lead these caregivers to put off activities that have consequences only for the distant future. Alternatively, having a family member diagnosed with AD could heighten an individual’s awareness of the importance of adequately preparing financially for his or her own retirement, given the risk that it could be made more expensive by a dementia diagnosis. This alternative hypothesis is consistent with research that has found individuals who received information regarding their elevated genetic risk for AD (ie, carriers of 1 or 2 copies of the Apolipoprotein E4 (APOE4) allele) were significantly more likely to purchase long-term care insurance 13 than were otherwise similar individuals who did not receive any genetic risk information.

In the current study, we test 2 hypotheses that are motivated by the life course framework. First, we posit that a family history of AD among prime age working individuals will lead these individuals to plan differently than individuals who have no such family history, but the direction of this relationship cannot be predicted, given the scarcity of previous relevant findings. Such a diagnosis is a significant family event that may place new time/money resource demands on extended family members and/or provide pause for thought about what one’s future health is likely to be.

Second, we hypothesize that the diagnosis of a parent will have a larger impact on retirement planning than the diagnosis of a grandparent. From the adult child’s perspective, the genetic link is stronger with the parent than the grandparent and this is likely to make a parent’s diagnosis more salient. The life course perspective suggests this relatively greater saliency will be reinforced by the fact that the timing of a parent’s diagnosis likely occurs during the respondent’s working years, whereas the grandparent’s diagnosis likely occurs before the respondent is old enough to be attentive to retirement planning issues. Likewise, this timing issue makes it more likely that an adult child will be called upon to contribute time and/or financial resources to the care of a parent than a grandparent.

Unique, high-quality data from 3 sources are linked to test our hypotheses. Information on retirement planning comes from the University of Utah’s Retirement Planning Survey (UURPS). The UURPS was designed to assess University of Utah employees’ retirement planning knowledge, priorities, perceptions, and behaviors. All University of Utah benefits-eligible employees with valid e-mail addresses (N = 9747) were invited to participate online in the UURPS during October 2009, and 3000 people submitted completed surveys (32.1% cooperation rate). This survey focused on retirement planning and thus, questions regarding family health histories and perceived risk of someday receiving an AD diagnosis were not included.

Detailed family health histories come from the Utah Population Database (UPDB). The UPDB is a shared research resource located at the University of Utah. Central to the current investigation, the UPDB includes family relationship information and state-wide medical information on causes of death. Utah death certificates (1904-2009) and the US Social Security Death Index are linked to the UPDB and provide the needed information on age and cause of death for relatives of the UURPS respondents.

Finally, UPDB has been linked to Medicare data that are used to identify relatives of respondents who have been diagnosed with AD but who have not yet died. Based on a separate project (NIH grant AG022095) that examines changes in the health status of older Utahns as a function of early life conditions, Medicare claims data were linked to UPDB. These data were approved to be linked to the UPDB for that study through an agreement with the Centers for Medicare and Medicaid Services (CMS). These records hold data on all Utahns who link to UPDB with respect to diagnostic codes from 1992 to 2009. The agreement with CMS also allows for reuse of the records for new projects, an approval that was obtained for the present investigation.

The linkage of the data across the 3 data sets and the analyses that follow were reviewed and approved by the University of Utah’s Institutional Review Board and the Resource for Genetic and Epidemiology Research Panel that oversees all studies utilizing the UPDB data. Record linkage of the UURPS survey data to UPDB and CMS records was done by staff at the Pedigree and Population Resource (PPR) at the University of Utah’s Huntsman Cancer Institute, the organization responsible for managing and maintaining the UPDB. A de-identified file was returned to the researchers by the PPR staff. For the current analyses, the sample is restricted to respondents who (1) link to both a biological mother and biological father in UPDB (N = 1009), (2) are of age 30 to 61 at the time of the survey (N = 740), and (3) have no missing data on variables used in the analysis, restrictions that lead to a final analysis sample of N = 720. The 30 to 61 age restriction is imposed to ensure that our sample definition is consistent with the age range of individuals who are typically encouraged to plan actively for retirement.

We estimate equations that capture 3 key activities that retirement planning educators encourage consumers to engage in and periodically revisit during their work lives. 35 –38 While these 3 activities do not constitute a complete retirement planning checklist, they are indicative of someone engaging in at least some of the most commonly recommended retirement planning activities. They are (1) calculating what one’s financial needs will be in light of retirement timing, lifestyle considerations, and life expectancy; (2) meeting with a financial advisor to ascertain how much one needs to invest (and in what type of investments) to meet her or his retirement goals; and (3) identifying one’s likely age of retirement, given past and future retirement investment plans.

The analysis begins with descriptive information regarding the sample and an assessment of the interrelatedness of the 3 retirement planning indicators. Next, we estimate multivariate logistic regressions. We estimate logistic regressions because of the dichotomous nature of the 3 dependent variables. The multivariate models control for important sociodemographic and economic characteristics of the respondents that have been related to retirement planning activities in past studies. 22,25,26

Results

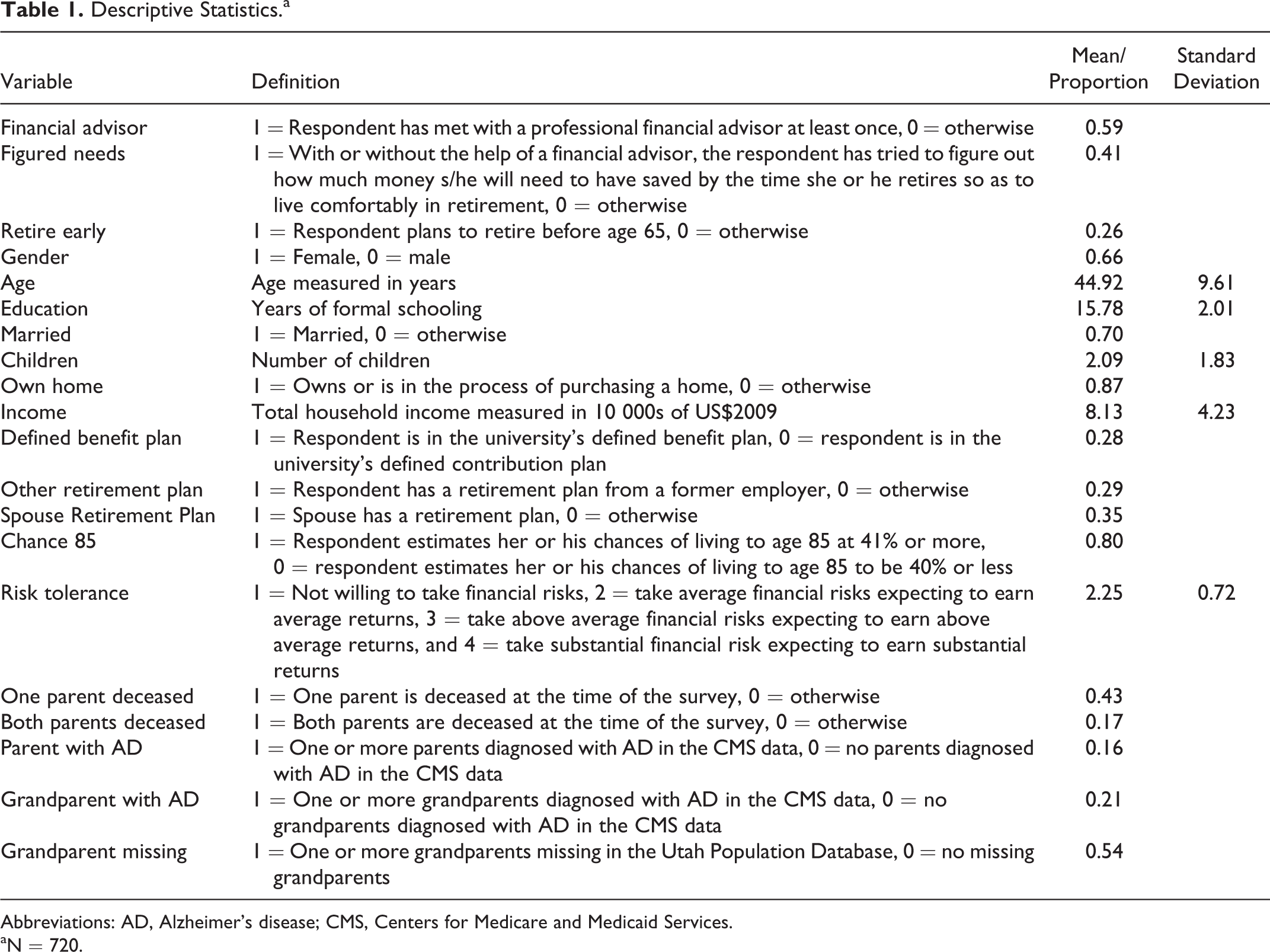

As depicted in Table 1, the typical survey respondent is female, age 45, with a college degree, married, and living in a household where the annual income in 2009 was slightly more than US$81,000. Thus, our respondents are slightly older, more highly educated, more likely to be married, and have a higher household income than the average American in 2009.

Descriptive Statistics.a

Abbreviations: AD, Alzheimer’s disease; CMS, Centers for Medicare and Medicaid Services.

aN = 720.

In terms of retirement planning behaviors, our respondents are not markedly different from what is observed in nationally representative data despite their upper middle–class profile. Specifically, 59% of UURPS respondents indicate that they have met with a financial advisor at least once in their lives. By comparison, a 2010 national survey found that 33% of respondents had met with a financial advisor in the past 12 months, 39 while another study found that 24% of respondents reported regularly consulting with financial planners to make decisions about saving and investments. 40 Forty-one percent of our respondents reported having ever calculated how much money they will need to save for a comfortable retirement. This percentage is slightly less than the 46% of respondents who answered the same question in the affirmative in a national survey conducted a few months later. 39 Twenty-six percent of our sample report planning to retire prior to age 65. This figure is identical to the percentage of nonretirees who expected to retire prior to age 65 in a national Gallup poll in 2009. 41 Thus, despite the fact that the survey respondents are generally well educated, live in households with upper middle–class incomes, and have access to retirement planning services via their employer, their planning activities appear to mirror national statistics. Moreover, in subsequent years the national numbers did not increase, 42,43 suggesting that the behaviors described in this survey are likely still applicable today.

Table 1 also reveals that 16% of the respondents have at least 1 parent who has had an AD diagnosis and 21% have had at least 1 grandparent who has had an AD diagnosis. By comparison, a 2014 report estimated that approximately 11% of individuals age 65 and older had AD. 1 A further breakdown of these figures (not included in Table 1) reveals that 101 respondents have 1 parent who has been diagnosed with AD, whereas 6 have 2 parents with an AD diagnosis. There are also 104 respondents with 1 grandparent who has been diagnosed with AD, 19 who have 2 grandparents with the diagnosis, and 2 who have 3 grandparents with AD. Having multiple parents or grandparents who have been diagnosed with AD is therefore relatively rare in our sample. It should be noted, however, that in the case of grandparents, our counts may be conservative as our CMS data only date back to 1992. Thus, for some of our older respondents, a grandparent’s diagnosis may be missing. This data limitation likely makes our estimates of familial health history effects of grandparents’ diagnoses conservative.

The correlation coefficients (ie, the measures of association for 2 binary variables) between the 3 retirement planning measures are all relatively low. Specifically, the simple correlation between figuring one’s financial needs in retirement and seeing a financial advisor is .35. The correlation between figuring needs and planning to retire early is .15, and the correlation between seeing an advisor and planning to retire early is .09. Thus, as past researchers have done, we treat these 3 activities as separate elements in the retirement planning process. 22,26,29,44

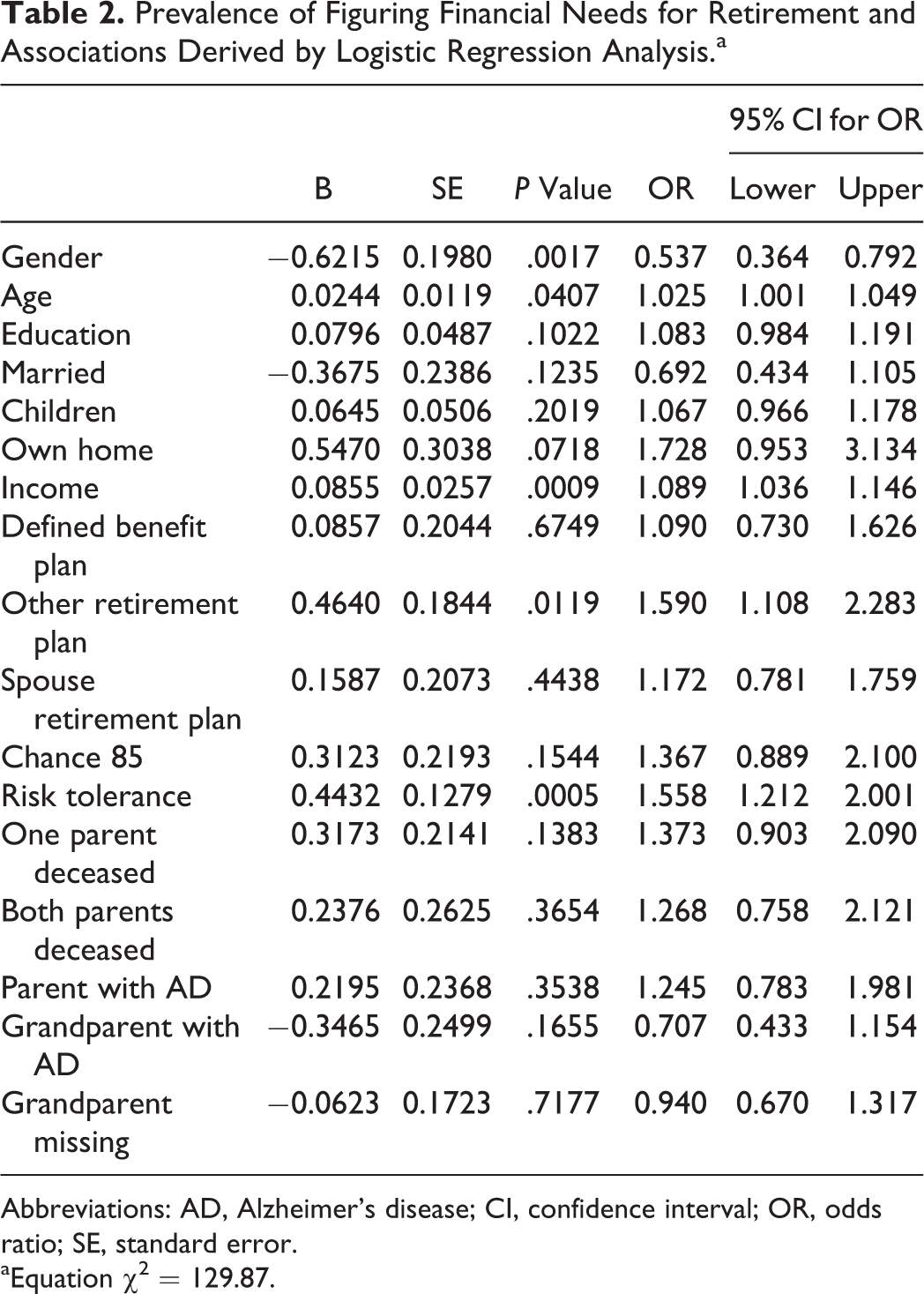

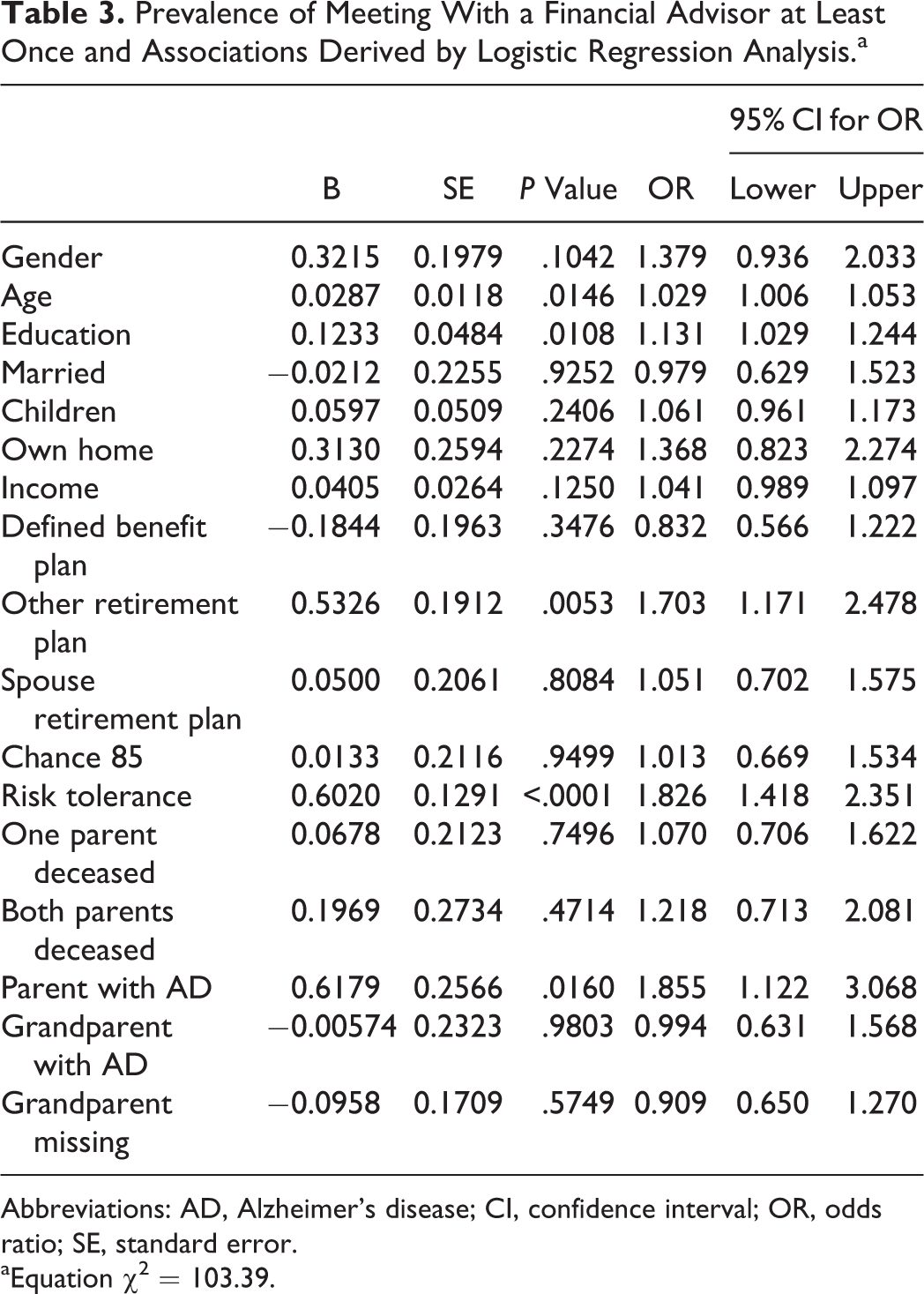

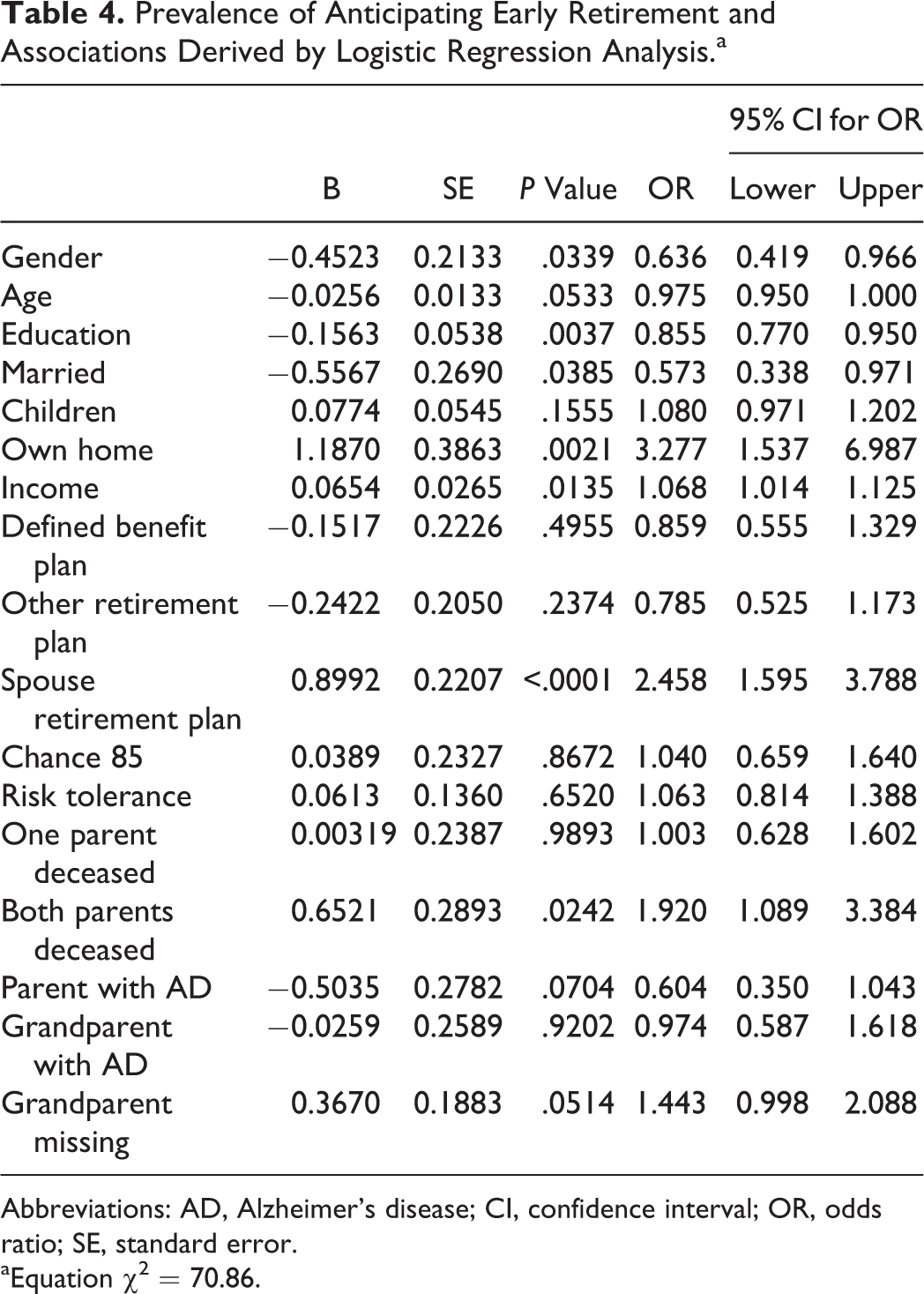

The multivariate logistic regression models are estimated with PROC LOGISTIC in SAS 9.3, and they include dummy variables that capture whether 1 or more parents and 1 or more grandparents have been diagnosed with AD while controlling for other key socioeconomic and demographic covariates. Collinearity diagnostics (available from the authors upon request) reveal no signs of problematic multicollinearity. Tables 2 to 4 show the complete set of estimated odds ratios.

Prevalence of Figuring Financial Needs for Retirement and Associations Derived by Logistic Regression Analysis.a

Abbreviations: AD, Alzheimer’s disease; CI, confidence interval; OR, odds ratio; SE, standard error.

aEquation χ2 = 129.87.

Prevalence of Meeting With a Financial Advisor at Least Once and Associations Derived by Logistic Regression Analysis.a

Abbreviations: AD, Alzheimer’s disease; CI, confidence interval; OR, odds ratio; SE, standard error.

aEquation χ2 = 103.39.

Prevalence of Anticipating Early Retirement and Associations Derived by Logistic Regression Analysis.a

Abbreviations: AD, Alzheimer’s disease; CI, confidence interval; OR, odds ratio; SE, standard error.

aEquation χ2 = 70.86.

The key findings in Tables 2 to 4 relate to the estimated odds ratios associated with a family history of AD. Although there was no relationship between grandparents’ AD diagnoses and the financial planning activities, we do observe an association between a parent’s diagnosis and 2 of the 3 retirement planning activities. Adults who have a parent who has been diagnosed with AD are 86% more likely to have seen a professional financial advisor at some point in their lives than are their counterparts whose parents lack such a diagnosis. In addition, these individuals are 40% less likely than their counterparts with no parental history of AD to plan to retire before age 65, holding other factors constant. Like seeing a financial professional, planning to work beyond age 65 can be viewed as responsible retirement planning since working longer both reduces the number of years that retirement resources must last while simultaneously increasing the size of the retirement funds accumulated. Hence, in this context, a parental history of AD is again associated with greater retirement planning.

In general, the estimated odds ratios associated with the standard sociodemographic, economic, and attitudinal covariates are consistent with the findings of past studies. 22,27,45 Gender, age, and education are significantly linked to each of the 3 retirement planning activities. Economic well-being, as captured by home ownership, income, and having more than 1 retirement plan, also appear to alter the odds of engaging in these retirement-related endeavors. Finally, financial risk tolerance is associated with increased odds of figuring needs and seeing a financial advisor but is unrelated to early retirement. The risk tolerance results are consistent with previous findings. 46

Discussion

Our analyses suggest that a family history of AD is linked to differences in retirement planning as motivated by the life course framework. Moreover, our life course hypothesis that a parent’s diagnosis will have a relatively stronger link to retirement planning than a grandparent’s diagnosis is also confirmed. We view the absence of any grandparent effects with caution, however, as we may not be capturing all of the respondents’ grandparents’ AD diagnoses. That is, the left truncation of health events in the CMS data prior to 1992 may be contributing to null findings regarding grandparents’ AD diagnoses. It is also possible that the grandparents’ diagnosis may not have been known to the grandchildren in some instances. Overall, though, this methodological constraint is likely associated with the age of the respondent, a covariate that is controlled for in the models.

A family history of AD is clearly only 1 element in the larger set of considerations that impact retirement planning. In the current analyses, we were able to control for other important sociodemographic and economic covariates including age, education, income, risk tolerance, and other sources of retirement income. But, one can imagine that many other factors contribute to the likelihood of being an active retirement planner (eg, expectations for postretirement standard of living, financial literacy, expectations regarding the likelihood of an inheritance). Our analyses are the first, however, to suggest that a family history of AD may also play a role.

One recent study estimated the monetary costs of dementia to be between US$41,689 and US$56,290 per year in 2010. 47 Consistent with these expense estimates is research showing that among individuals age 65+ in 2008, those with AD or other dementias had higher rates of hospitalization, nursing home care, medical provider care, hospice care, and home health care than otherwise similarly aged individuals who did not have an AD or other dementia diagnosis. 1 The high costs of providing care for someone with AD may lead the adult children of affected individuals to make financial contributions to cover some of the care-related costs which could motivate them to take a closer look at retirement-related finances. At the same time, knowledge of the familial risk of developing AD may provide these adult children with a forewarning or “wake-up call” about their own future financial needs as most often such a diagnosis occurs when the adult child is in the life course stage where setting aside funds for retirement is most imperative. Either one or both of these event catalysts may be part of the process that leads to our finding that adults with a parent who has been diagnosed with AD have greater odds of responsibly planning for retirement than do otherwise similar adults who have no such family health history.

The number of people in the United States with AD is forecast to triple between 2010 and 2050, from 4.7 million to 13.8 million individuals. 48 Our findings suggest that the adult children of these affected individuals may be more motivated to take an active role in their retirement planning than the average American. In an era when the rise of defined contribution retirement plans make it increasingly imperative for employees to plan actively for their financial futures, our study suggests that a family history of AD may have the unintended consequence of providing an impetus for individuals to seek professional advice and more responsibly plan for retirement.

Clearly, the good news is that individuals with a family history of AD are engaging in more active retirement planning than their otherwise similar counterparts who have no such history. Yet, given the significant financial costs associated with an AD diagnosis, are they doing enough? AD risk increases with age while financial security typically declines after retirement. Taken together, this may create the “perfect financial storm” for individuals who have not prepared adequately. As such, it is incumbent on health-care providers and financial counselors/educators to advise their clients about AD risk and the likely financial costs. For genetic counselors and other health-care providers who meet with members of high-risk AD families, it is important to use this opportunity to discuss not only what the individual’s risk of AD is but also what this might imply for their financial and caregiving needs in the future. Professional financial planners should also discuss with their clients how their family health histories may affect their financial needs as they grow older. For those individuals who have an elevated risk for AD but who have not done sufficient retirement planning, long-term care insurance may be a way to reduce the financial risk associated with an AD diagnosis going forward.

It is important to acknowledge the caveats associated with extrapolating from the current study. The barriers to obtaining professional financial advice were minimal in our sample as all of the respondents worked for a single employer where the retirement vendors offered retirement planning consultations free of charge. For individuals who work for employers with fewer retirement planning supports, the barriers to seeking retirement planning financial advice may be more daunting and as such our estimates may be somewhat liberal. The data used in the analysis come from 2009—a time of heightened anxiety about retirement finances—and as such they may not reflect the current economic and retirement planning landscape that employees are encountering today. National statistics suggest, however, that retirement planning has changed very little in this country over the past decade. 43,49,50

Finally, our survey was designed to gather information primarily on retirement planning. As a consequence, we did not gather information on the extent of caregiving, concern about the heritability of AD, or the direct financial consequences of assisting a parent/grandparent who had been diagnosed with AD. Our ability to merge our general survey with UPDB family health history data provided us with a unique opportunity to establish an empirical link between a family history of AD and retirement planning. More detailed modeling of this relationship, including possible mediating factors, awaits more extensive data collection efforts.

As our understanding of how genetics and other familial factors affect the intergenerational transmission of AD grows, it is likely that the link between family AD histories and retirement planning will intensify. The results presented here are an important first step in expanding our understanding of the potential effects of an AD diagnosis beyond the immediate financial and time burdens associated with caregiving and other family supports. Future research in this domain should focus on 3 things. First, additional work should be done to identify the process that underlies the relationships between a family AD history and retirement planning that we observed. It may be that a parent’s AD diagnosis motivates adult children to seek retirement planning advice for those who are directly involved with caregiving but not those whose involvement is modest. We will only be able to assess the possibility of such mediating effects with new data that include such process measures. This research should also seek to include a broader range of individuals in terms of socioeconomic and demographic characteristics so as to maximize both internal and external validity.

Second, research should be done to ascertain if the relationships we observed are age- or birth-cohort-specific—something that our modest sample size did not allow us to investigate. The life course framework suggests that there could be differences in retirement planning actions depending on the timing of the diagnosis relative to the adult child’s work-life stage.

Finally, it is important that we examine the extent to which responses to a family history of AD are manifest in other long-run considerations such as estate planning. Research on all of the above issues will be vital if we are to target high-risk groups for education and support as they navigate the multigenerational consequences of a family member’s AD diagnosis.

Footnotes

Acknowledgments

We thank the Pedigree and Population Resource of the Huntsman Cancer Institute, University of Utah (funded in part by the Huntsman Cancer Foundation) for its role in the ongoing collection, maintenance and support of the Utah Population Database (UPDB).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by NIA grant number 1R21AG041246. Use of the CMS data was made possible by NIA grant number AG022095.