Abstract

The financial system is a highly competitive field whose applications range from as big as the strategic vision and missions of the multinational companies to as small as day-to-day household expenditure decisions or management of pocket money by students. Financial literacy is a life skill that, in theory, is highly related to the well-being of individuals and companies. In the subject of financial literacy, there is a large body of literature, but very little to no knowledge on the trend and patterns of the literature and research advances in the body of knowledge. With the help of Scientific mapping analysis (SMA) and Bibliometric analyses, this study aims to declutter the literature in the field and find the future research direction in financial literacy. The study is carried out on 1000 documents from a 20-year time horizon (2001–2021), indexed on Web of Science. The study shows the publication trends, most relevant authors, journals, countries. The most significant, developing, and trending themes in the subject and the intellectual structure were investigated using keyword analysis. To better understand the social structure in financial literacy and well-being, co-authorship analysis was used.

Introduction

The formalisation of the economy, organisation of the unorganised sector, increasing the digitisation of transactions, increasing the level of financial inclusion, poverty alleviation, the well-being of individuals, human development, and many other challenges that the modern society and the governments face are in some way or the other linked with financial literacy of the individuals. Financial literacy is considered to be a life skill, Kezar and Yang (2010) all the citizens of the modern economies must be financially literate and also showcase literate financial actions in their day-to-day financial transactions. The implications of financial literacy are strongly connected to financial inclusion, promotion of which can have significant positive consequences for the real economy, Grohmann et al. (2018).

In almost all economies of the world, over the past two decades, Access to credit has been increasing, and financial markets are becoming more digitalised. As a result, financial literacy is recommended as a policy tool to the governments to protect the individuals from the exploitation that they are prone to in the area of finance, be it daily transactions that are necessary for survival or the long-term purchases by them. The definition of financial literacy is highly debated in the literature. According to OECD (2014), Financial literacy is a mix of knowledge and comprehension of financial ideas, risks, and instruments, as well as the drive and confidence to apply that knowledge in financial decision-making. Huston (2010) similarly defines financial literacy, but some authors limit the definition to only understanding financial concepts and the ability to perform basic financial calculations, Lusardi and Mitchell (2011b). This is highly debated, as also mentioned by other studies, that mere knowledge is not enough unless applied, Atkinson and Messy (2012).

Financial literacy has become a matter of grave concern, especially after financial crises, Hussain and Sajjad (2016) of the early and late 2000s in the developing countries and the major financial inclusion drives in the emerging economies like India. Throughout the world, there is a massive issue of lack of financial literacy evidence of which has been widely documented by researchers, and policymakers, Lusardi (2011); Lusardi and Mitchell (2008), (2011b), (2014); Mottola (2013). Studies suggest that financially literate individuals tend to make better financial choices related to Credit cards, Retirement planning, Debt management, and others, Hilgert et al. (2003); Santos and Abreu (2013); van Rooij et al. (2011). Various policy tools have been recommended in the literature of which majority signals towards the inclusion of financial education and literacy programmes at the elementary and higher levels of schooling, Holzmann (2011); Lusardi (2013); Willis (2008), so that financial literacy can be learned at an earlier stage of life.

Past studies suggest a strong connection between financial literacy, showcasing financially literate behaviour, and the overall well-being of the individuals. There were very little to no studies found on scientific mapping of the field with a particular reference to well-being. Moreover, there is minimal knowledge on the emerging areas and themes in the field, without which the research cannot go in the right direction. Therefore, the study becomes necessary in this respect. From the perspective of individual and societal well-being, the prime objective of this study is to examine the scientific research advances and information developed in this sector.

Web of Science database provides metadata on Authors, Keywords, Years, References, Affiliated institutions, Countries, etc., such information when examined, becomes extremely useful. The method of analysis on such data is called bibliometric analysis, Cobo et al. (2011). The definitions of bibliometric analysis and the techniques used have been taken from the pioneering work of Pritchard (1969) and Broadus (1987).

This study contributes to expressing existing knowledge and prospective research lines on the impact of financial education and financial literacy on economic growth in individuals and societies. This study, on the other hand, is valuable for academic institution administrators, researchers, and managers with the primary goal of valuing financial education in all areas. Starting with a discussion of the data sources and methodologies utilised, this article investigates the intellectual state of financial literacy research, extracting the most recent and influential research trends. Finally, it summarises its major results, as well as its conclusions and future directions. The findings demonstrated the importance of this line of study, allowing for the identification of the primary driving factors in this sector and their future and emerging trends.

Objectives of the study

The primary goal of this study is to provide the current status of the research advances in financial literacy and well-being with the help of the research Meta-Data from the top-tier journals over the past two decades. The following questions have been put for defining the study’s scope:

RQ1. What are the publication trends from 2001 to 2021 in the discipline of financial literacy and well-being? RQ2. Who are the most relevant authors, Sources (Journals on WoS), most productive countries publishing the studies in the concerned field? RQ3. What is the intellectual structure (Co-occurrence, Co-authorship, and Co-citation) in financial literacy and Well-being? RQ4. What are the contemporary topics being researched in the discipline of financial literacy and well-being? RQ5. What is the conceptual structure in financial literacy and well-being?

Methodology

The study aims to showcase the development in the literature on financial literacy and well-being. The research advancement in the field has been studied for the past 20 years, from 2001–2021, in the top-tier journals indexed on the Web of Science (WoS) database by Clarivate analytics. The decision of taking data from WoS has been taken in accordance with other bibliometric studies on financial literacy Goyal and Kumar (2021) and on Wealth and Inequality, Korom (2019). A quantitative bibliometric analysis along with the scientific mapping analysis (SMA) has been done for this purpose. A search query based on the requirement of the study was entered into the database, and the results were filtered based on the actual requirements of the analyses.

Data inclusion

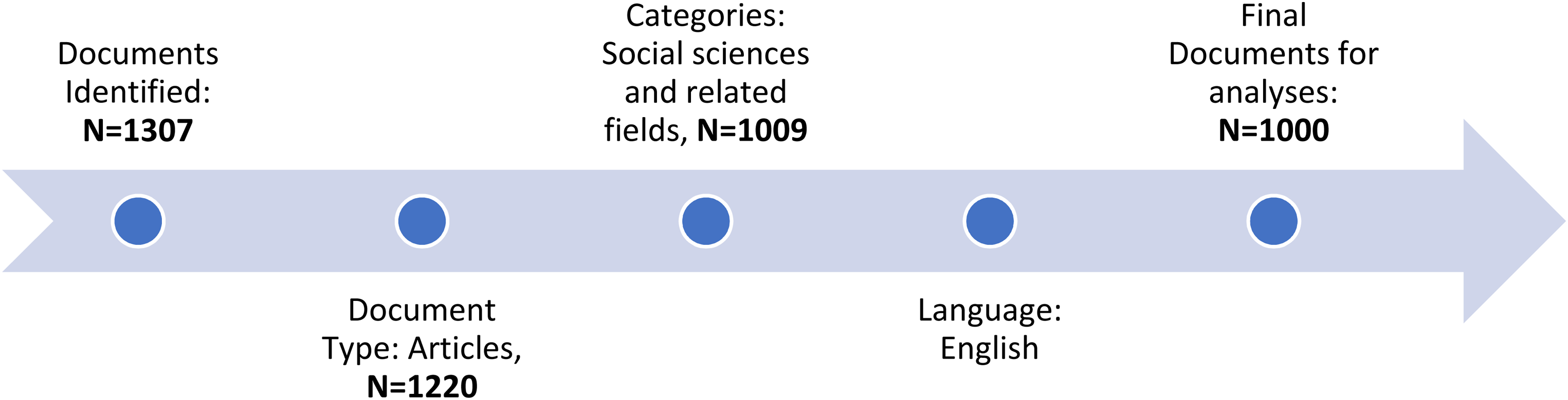

The term ‘financial literacy’ was entered in the Topic, Title, and Abstract field of the search query along with the term ‘Well-being’ in All Fields. This search entry retrieved 1307 documents of all languages and types in all years. Only research articles were required; thus, the search was further filtered to ‘Research Articles’ as the document type bringing the output down to 1220 documents. These 1220 documents belonged to all the fields in all the disciplines that were indexed on WoS, but since the areas of concern were only limited to Arts, Humanities, Economics, Business & Management and other social sciences fields, including multidisciplinary so such filtration was also done bringing the no. of documents further down to 1009. At the last step, English was selected as the language of choice for the articles, which surprisingly only cut shorted only nine more documents bringing the total down to 1000 articles, which was ultimately used for the study. The process has been depicted in the flowchart below (Figure 1):

Data filtration process.

Analysis method

The present study used bibliometric and SMA, as well as network analysis, to analyse existing work on financial literacy and well-being. The methodological flow of the study is divided into five steps which are based on the recommendations of Aria and Cuccurullo (2017); Firdaus et al. (2019).

The methodological flow ranges from designing the study to visualisation and interpretation of the finding.

Designing the study: The research questions are defined to set the foundation of the bibliometric analysis of the documents and further for the SMA. Data collection: Meta-Data from the top-tier journals have been first identified based on the search query, and subsequently, the results are narrowed down using filters of Document type, language, and categories. Data analysis: Biblioshiny application of the Bibliometrix package of the R studio is primarily used for the bibliometric analyses. Data Visualisation: Social networks among Top authors (Collaboration), Co-occurrence networks for the identification of various thematic clusters, and Citation network of various studies for creating the visual map of the clusters of citations among different documents using bibliographic coupling has been created using the VosViewer software. Interpretation: The interpretation of the research findings has been discussed in the conclusion section of the study.

This methodological flow is the most suggested methodology for synthesising current studies and is highly respected when determining the research gap.

Results and discussions

Sample statistics

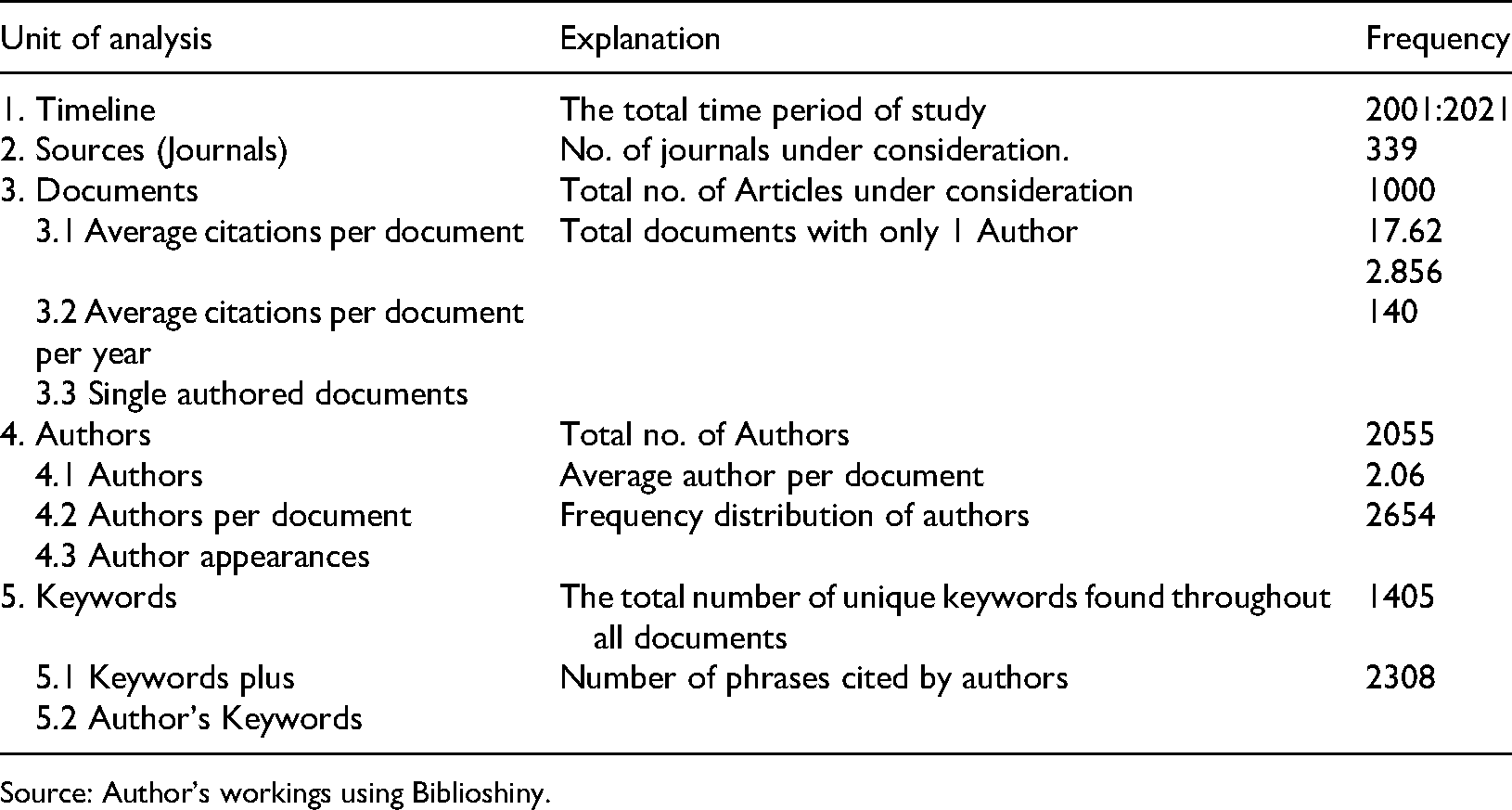

Basic sample attributes.

Source: Author’s workings using Biblioshiny.

Publication trends

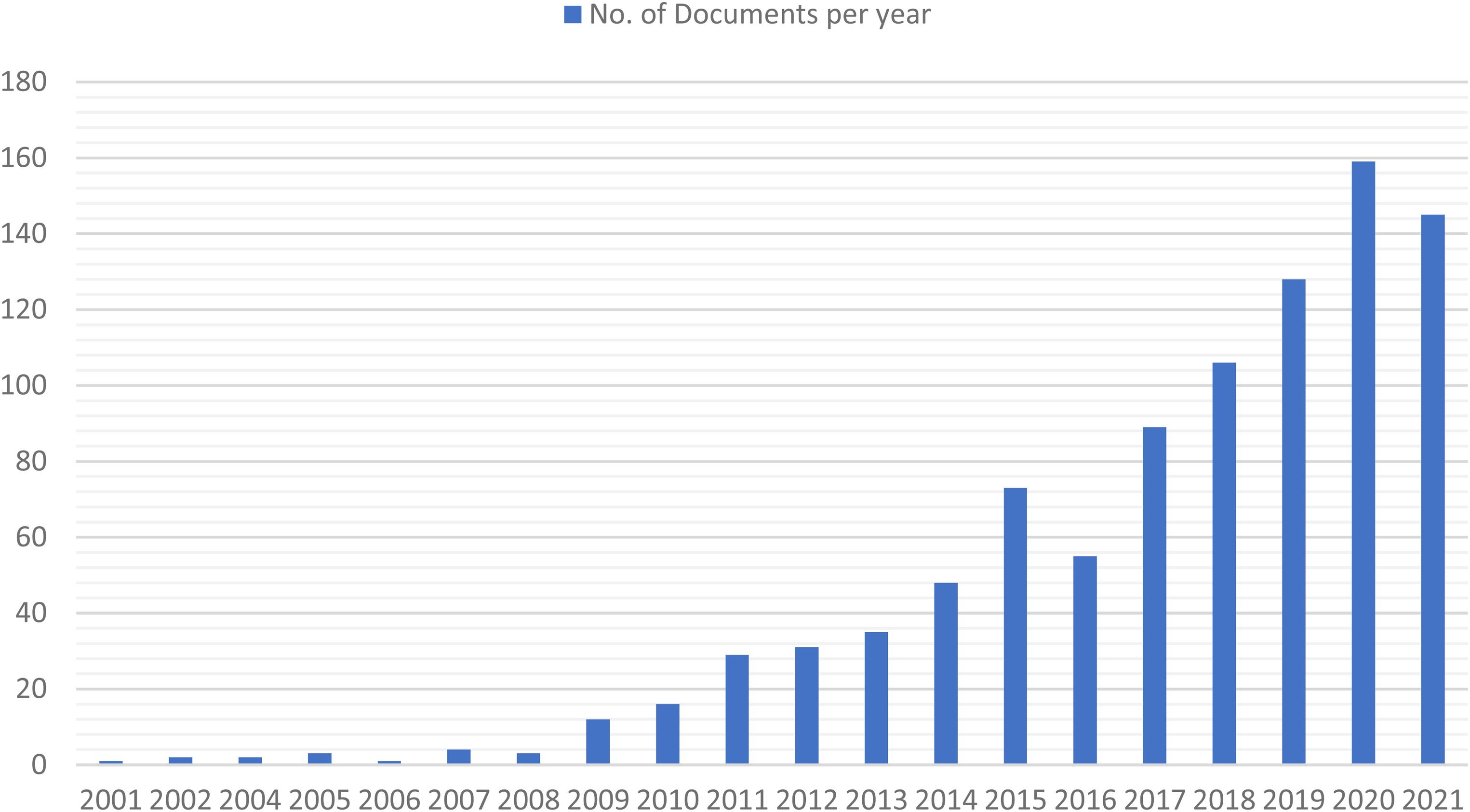

Figure 2 shows how the trend for no. of published documents have been in the past 20-year period (2001–2021) based on the WoS database. It shows the no. of papers published per year. It highlights how the area is emerging at an increasing rate, from near to zero documents at the beginning of the timespan to more than 150 documents in the recent years, with only a few exception years, the no. of studies has increased year on year. The rising no. of studies can be attributed to the financial crises, as mentioned by Goyal and Kumar (2021) and Hussain and Sajjad (2016).

Publication trends. Source: Authors’ workings using data from WoS.

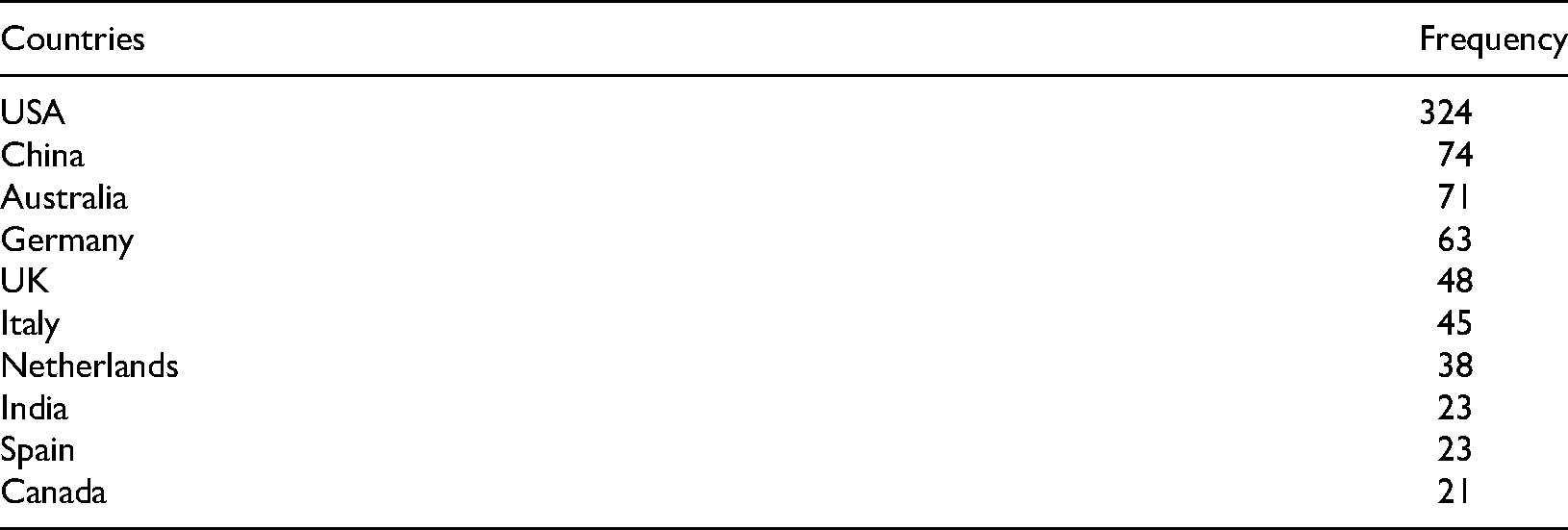

Countries

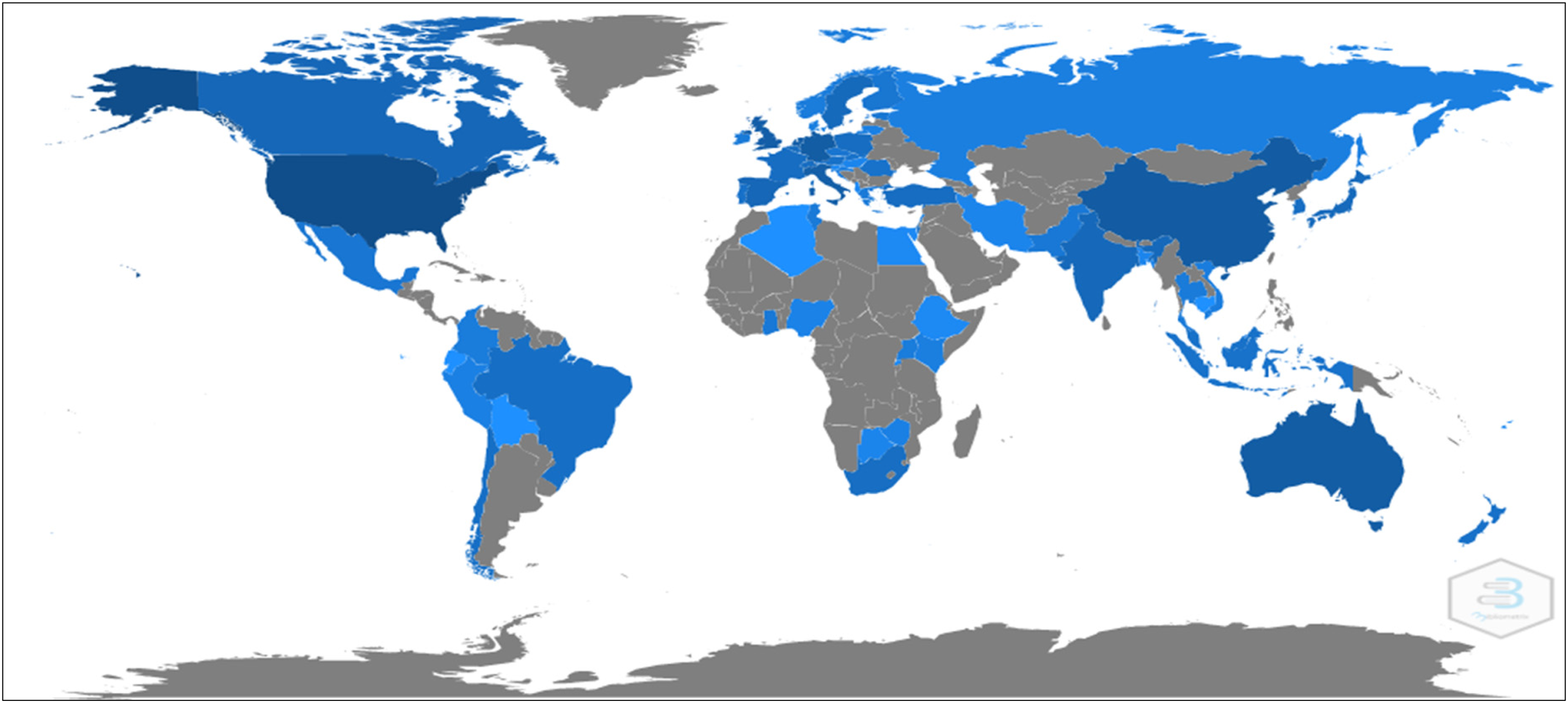

Table 2 shows the ten most productive countries in terms of the number of studies published in these countries. With the exceptions of China (74) and India (23), all top countries are from the west, either western Europe (Germany, UK, Italy, Netherlands, Spain) or the Americas (USA, Canada). The table depicts the dominance of the west in the publication on financial literacy and well-being. Figure 3 below shows the world map based on the no. of studies published in each country. The darker the shade, the higher the no. of studies published in that country. Figure 3 shows the massive lack of published research in financial literacy in the African continent, Middle-east, Central Asia, and Eastern Europe.

Country-wise production of financial literacy and well-being studies. Source: Authors’ workings using Biblioshiny.

Most productive countries.

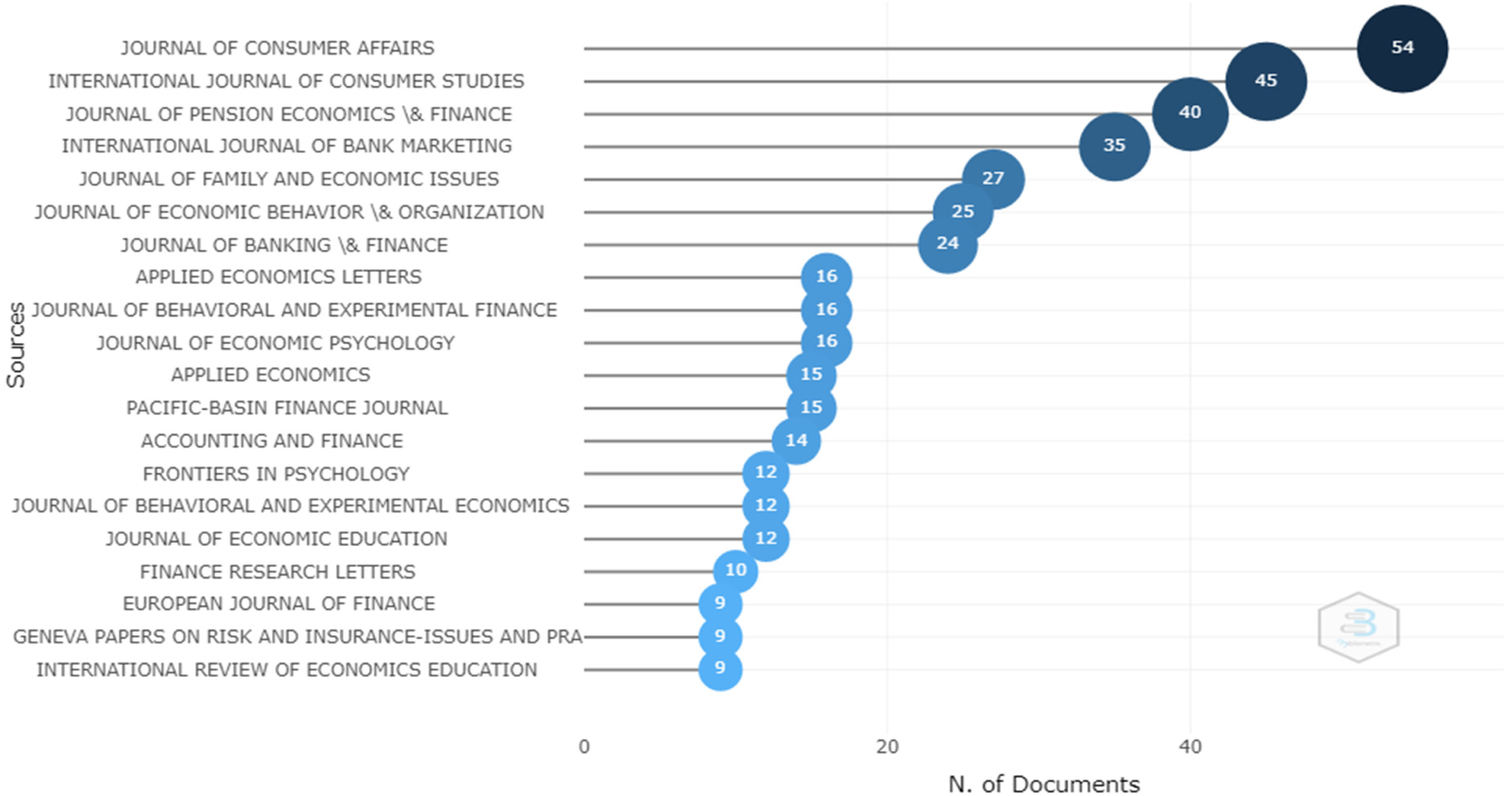

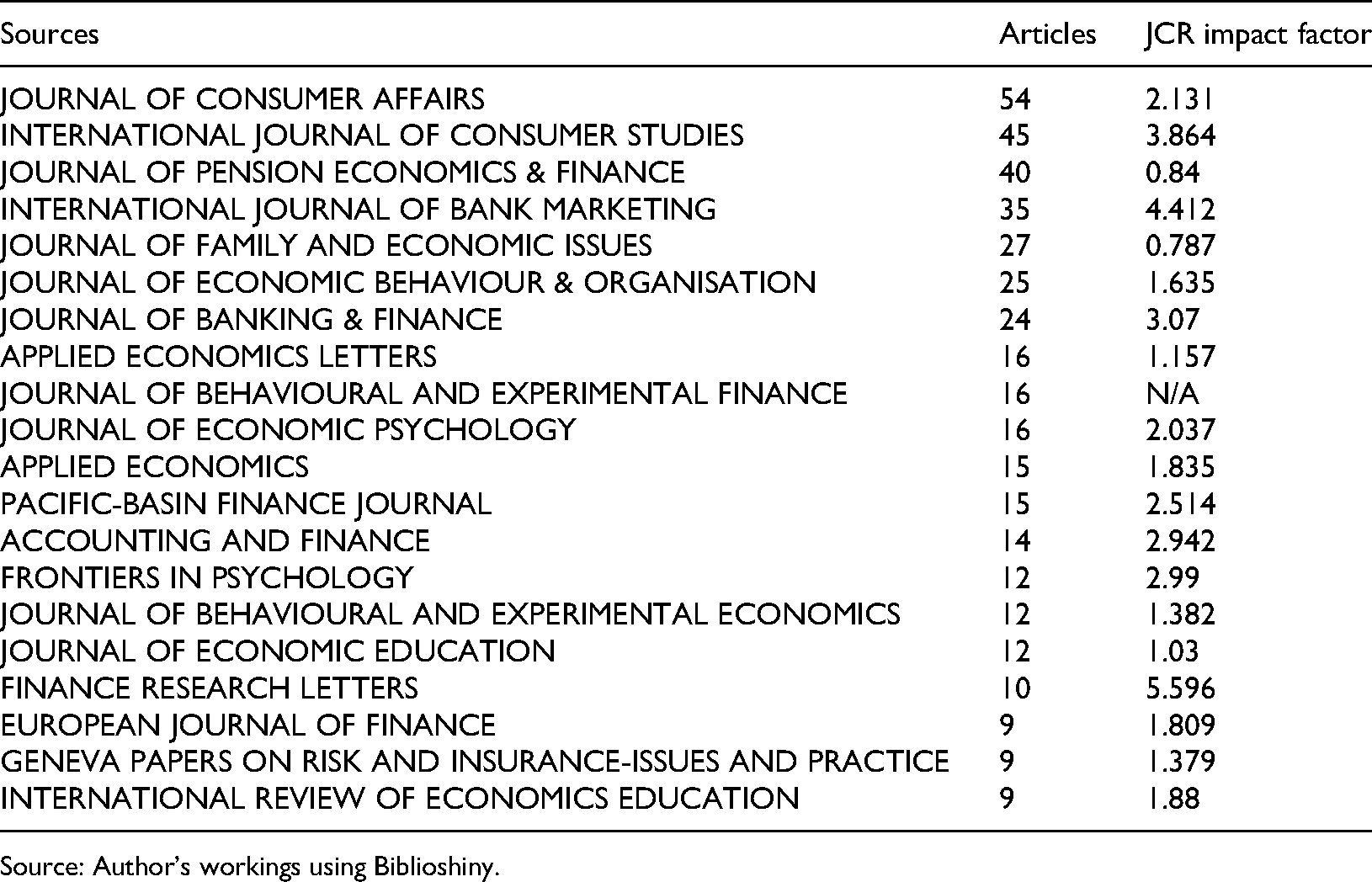

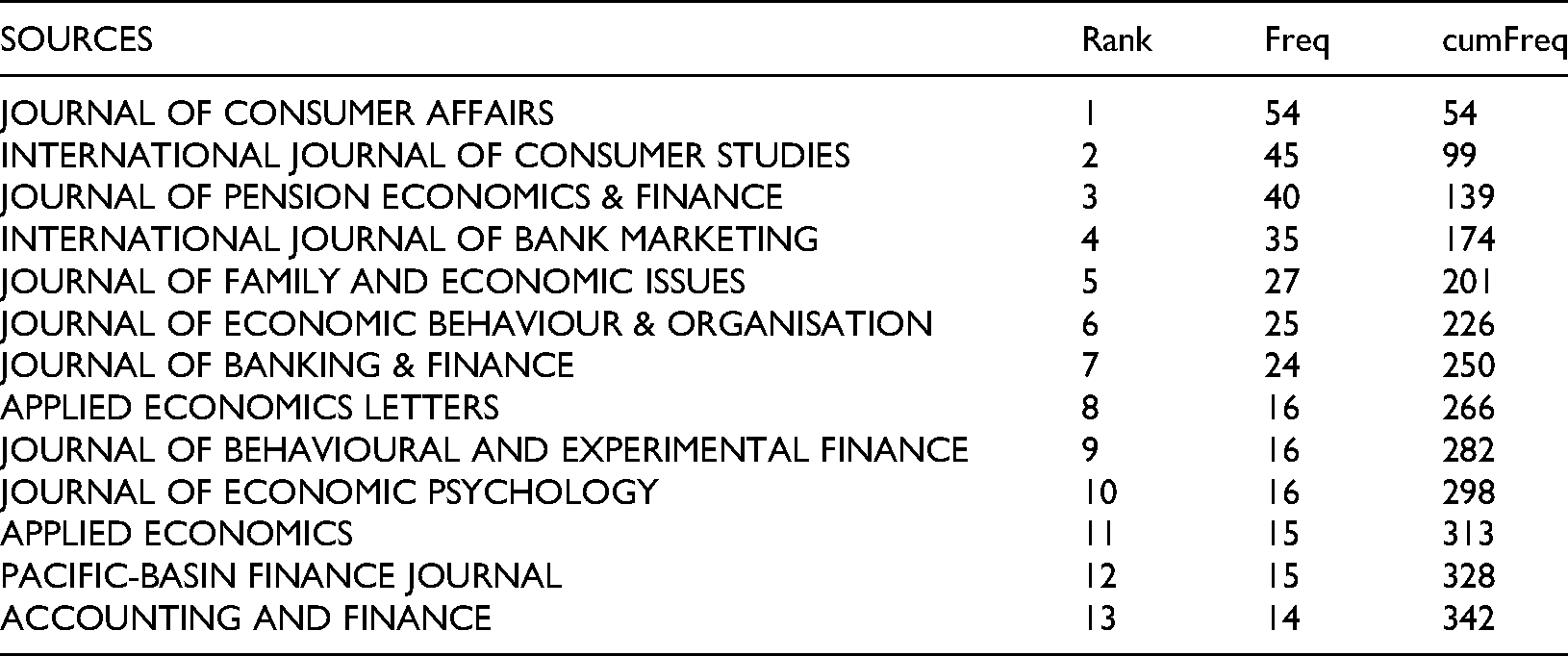

Based on the no. of documents published in the total sample, we can look at the most critical journals that must be tracked by future researchers as they have been publishing the most significant number of studies in the study time span as compared to other studies. Table 3 below lists the top publishing journals with the respective no. of articles and the impact factor. The impact factor is calculated based on the idea of how many times an article has been cited in other studies. The impact factor is calculated as No. of cites / No. of papers. Journal of Consumer Affairs (54), International Journal of Consumer Studies (45), Journal of Pension Economics & Finance (40), International Journal of Bank Marketing (35), and Journal of Family and Economic Issues (27) are the top 5 journals in terms of articles published (Figure 4).

Top sources publishing on financial literacy and well-being. Source: Authors’ workings using Biblioshiny.

Most relevant journals on financial literacy and well-being in order of no. of documents.

Source: Author’s workings using Biblioshiny.

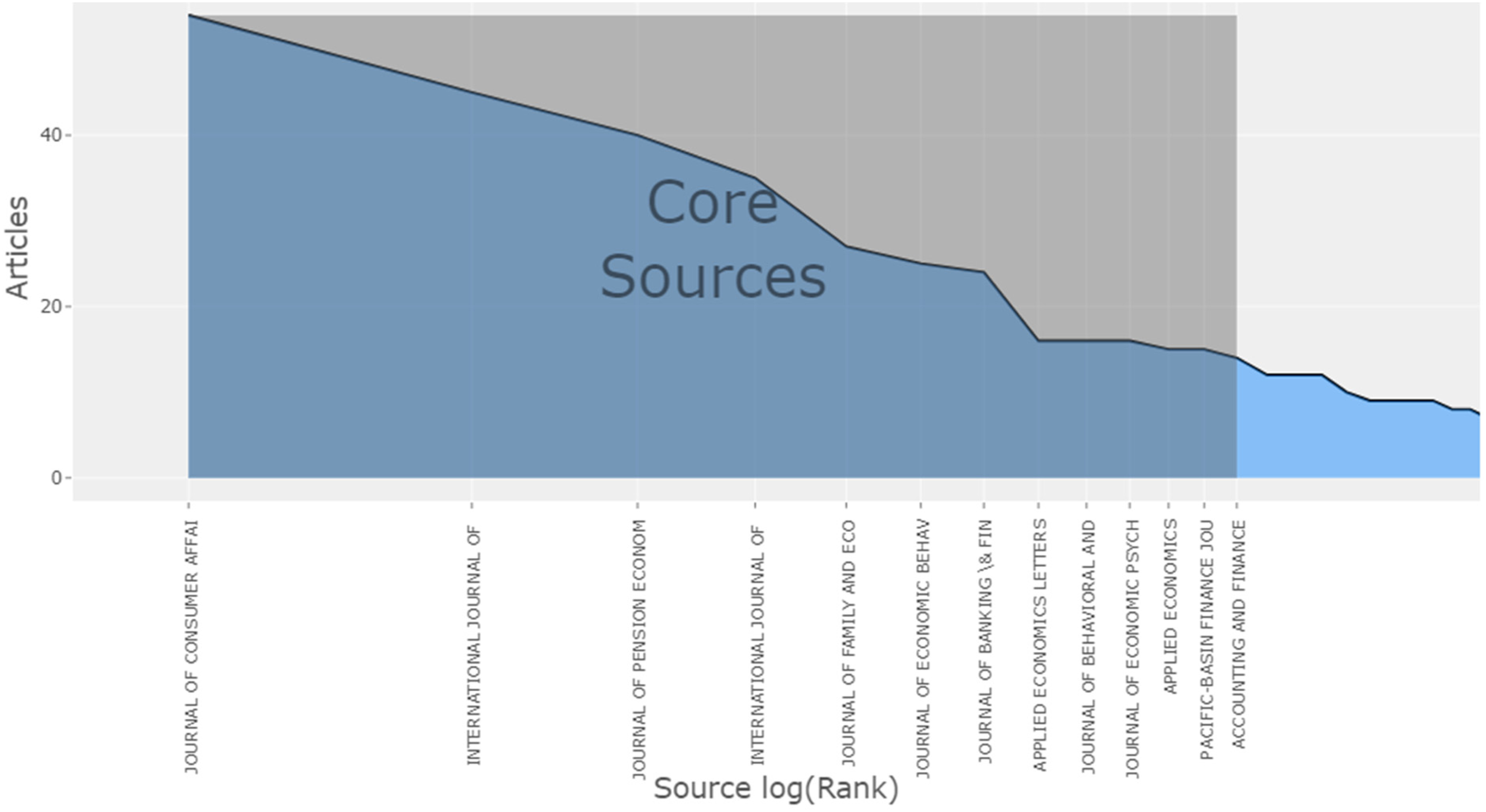

A methodology of distributing the sources (journals in this case) in a certain way so that we can know the most relevant sources was first described in the original works of S. C. Bradford. In Bradford’s law of scattering, the journals are placed in a specific order of decreasing productivity Bradford (1948); such arrangement shows that only a few sources (journals) are essential from the perspective of literature as these few sources contain the largest no. of studies. These few journals fall in the area which can be termed as ‘Core Sources’. There may be a significant no. of sources outside the core sources, but these sources contain a few number articles each. Figure 5 shows the magnified version of the distribution graph based on the methodology proposed by Bradford. According to the findings, 13 journals can be termed as Core Journals, and these 13 journals are crucial from the perspective of the research on financial literacy and well-being. Cumulatively these journals publish 342 documents out of a total of 1000 documents which is more than 1/3rd of the total studies (Table 4).

Core sources on financial literacy and well-being. Source: Authors’ workings using Biblioshiny.

Most relevant journals on financial literacy and well-being in order of no. of documents

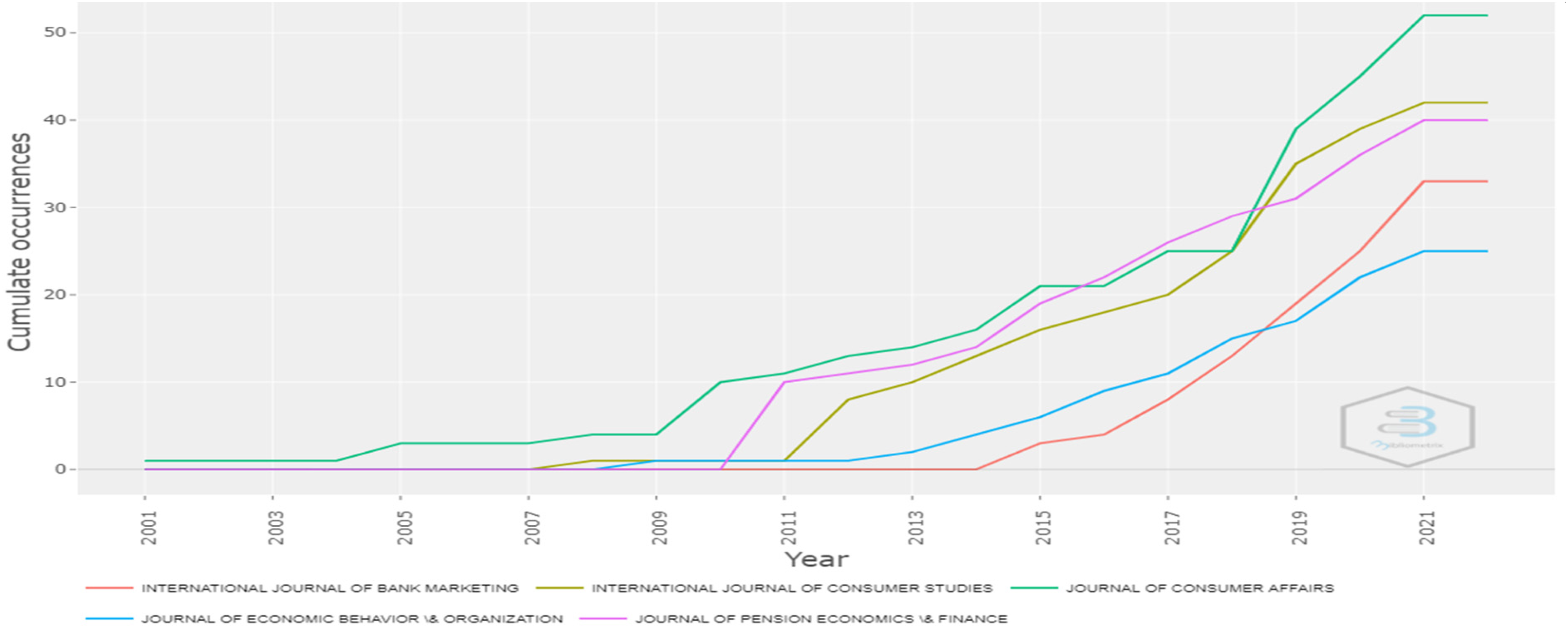

From further analysing the sources and the growth that they have shown over the past two decades, we find the top 5 sources that have demonstrated the most significant rate of growth in terms of the no. of publications on financial literacy and well-being. Figure 6 shows the International Journal of Bank Marketing, International Journal of Consumer Studies, Journal of Consumer Affairs, Journal of Economic Behaviour & Organisation, and Journal of Pension Economics & Finance to be the most rapidly growing journals. Researchers working on financial literacy and well-being should track these journals for important works.

Top sources growth over the years. Source: Authors’ workings using Biblioshiny.

Authors

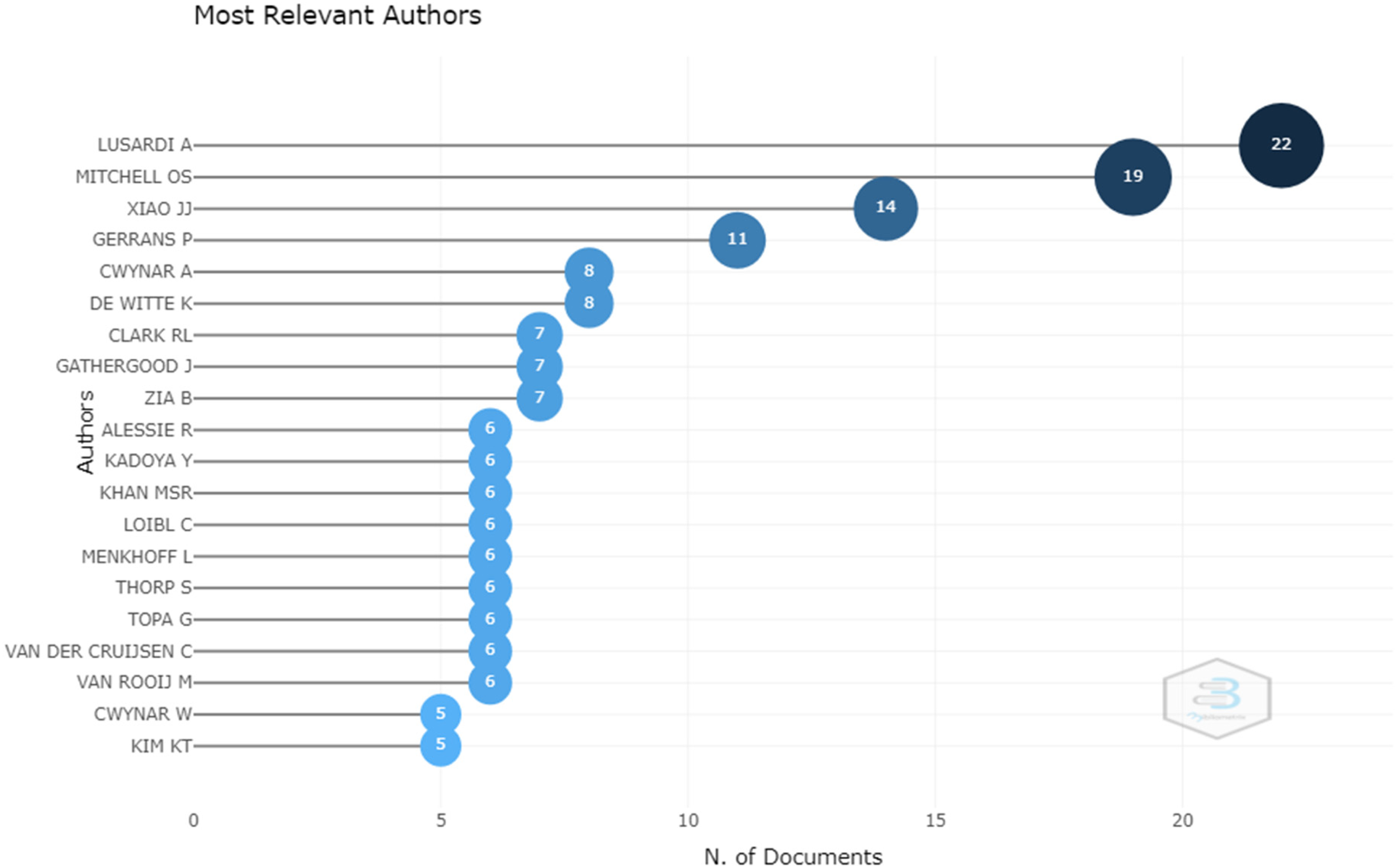

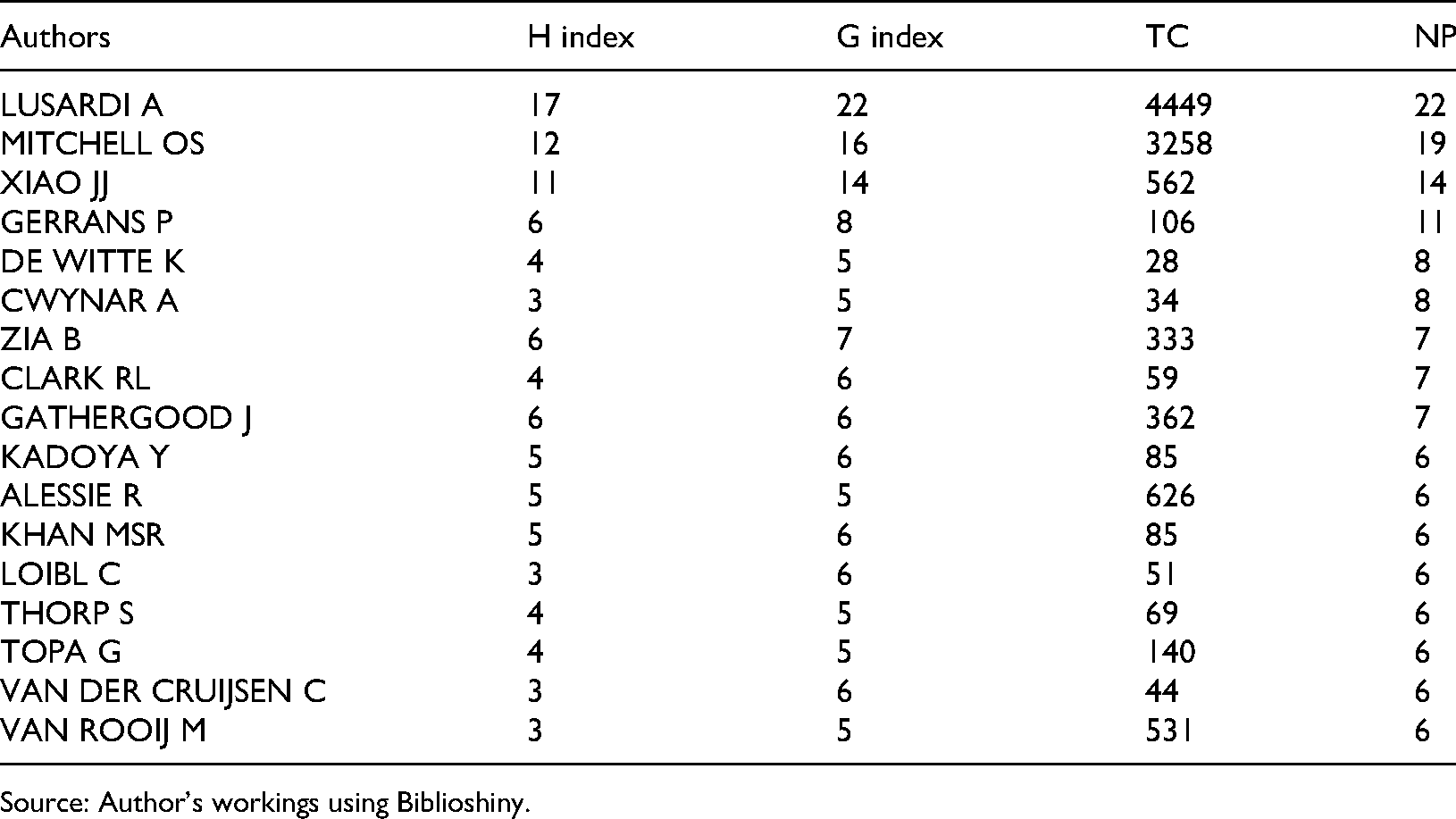

Another critical unit of analysis is the Authors. Important authors in any field can be ranked on the basis of the no. of studies they have produced over the years, the total no. of citations that their work has got, or the H index, which is defined as the highest number of documents of a researcher that received N (in this case H) or more citations each, Schreiber (2008). Table 5 below shows the list of top authors mentioned in order of total no. of productions (NP). Their respective total citations (TC), H index, and G index (another measure of author productivity) are also mentioned adjacent to their names. The data shows Lusardi A. has produced the most no. of studies (22) from 2001–2021, making her the most productive in terms of size of production. She also tops the list as per the H index. Followed by Lusardi, Mitchell OS. (19), Xiao JJ. (14), Gerrans P. (11), and DE Witte K. (8), stands at 2nd, 3rd, 4th, and 5th respectively (Figure 7).

Most relevant authors on financial literacy and well-being. Source: Authors’ elaboration using Biblioshiny.

Top authors in financial literacy in order of production

Source: Author’s workings using Biblioshiny.

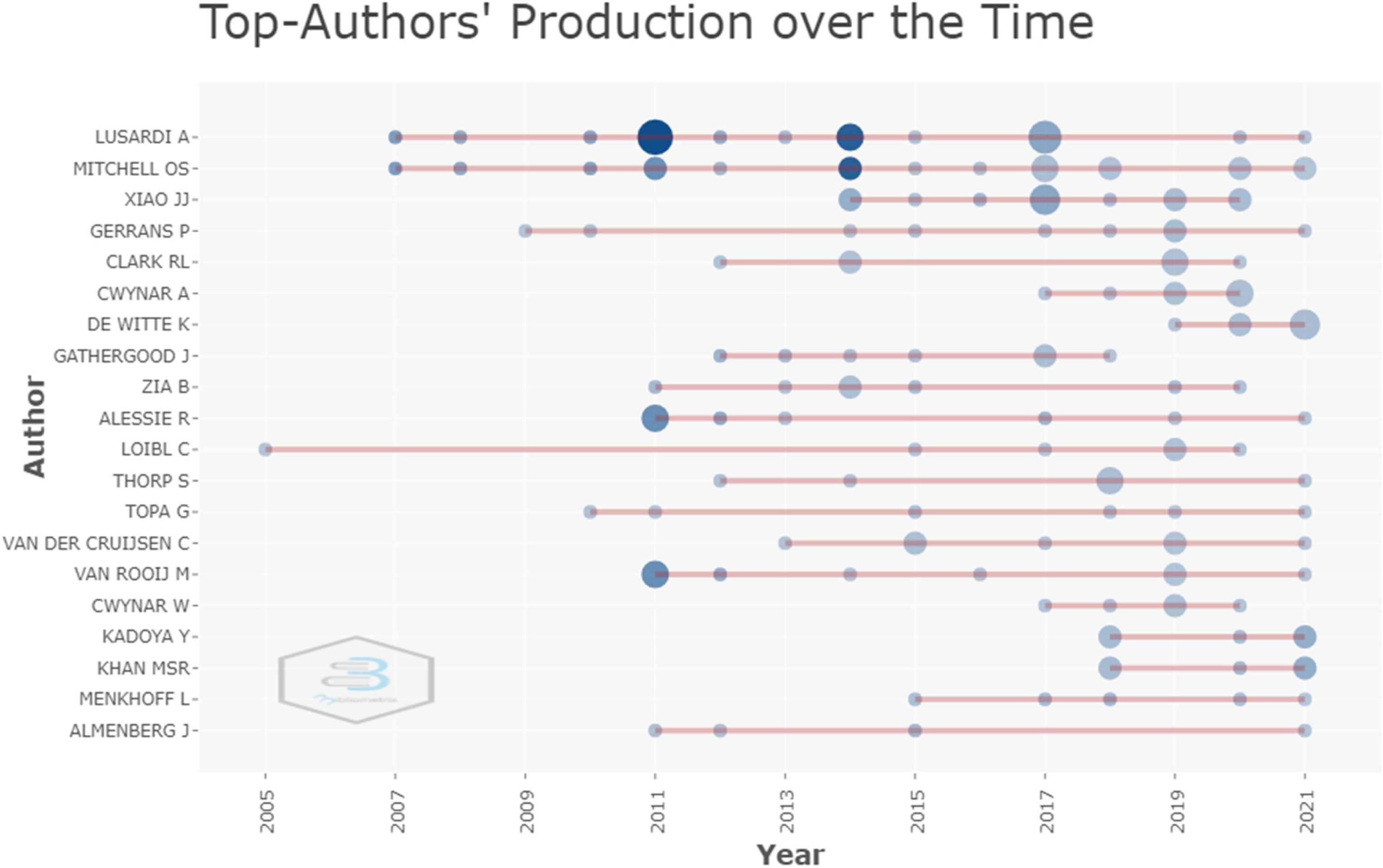

Digging deep into data on author production, we find that not all authors are regular authors. Some can be termed as regular authors, and others can be called occasional authors. Regular authors are the ones that we, as researchers in the field, are interested in. Researchers must track the works of regular authors as they are continuously committed to a particular area.

Figure 8 below shows the author’s production over time; according to the figure, some authors have been producing articles on financial literacy and well-being regularly while others are not. For example, the distribution of production by Lusardi A. is distributed across the years 2007, 2008, 2010, 2011, 2012, 2013, 2014, 2015, 2017, 2020, 2021. Compare this to Loibl C.; there is a gap of 10 years from 2005 to 2015 between the works of this author. One more insight out of Figure 8 is that not all authors that have published in 2021 or recent years have been publishing research work regularly.

Author production over time. Source: Authors’ workings using Biblioshiny.

Co-authorship

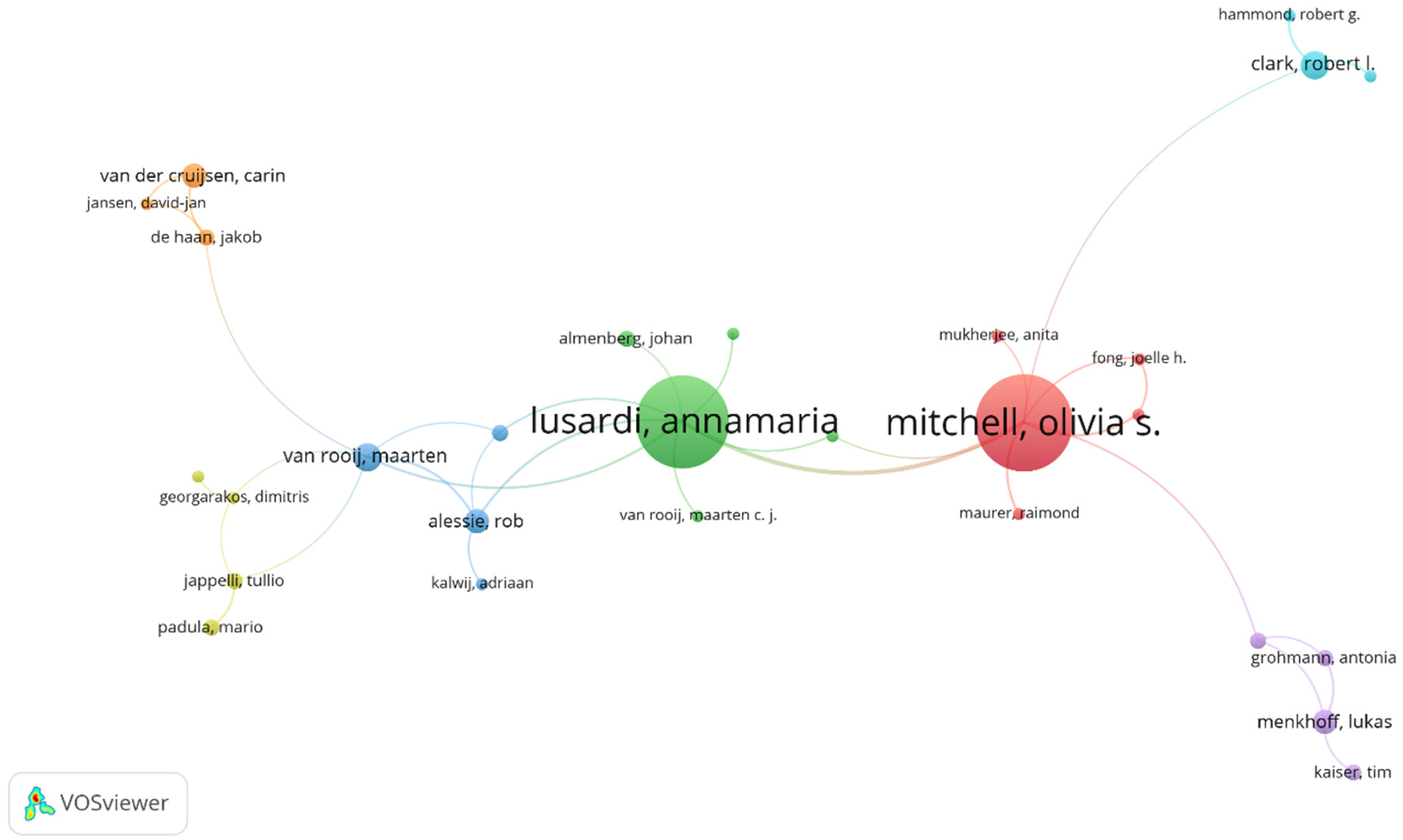

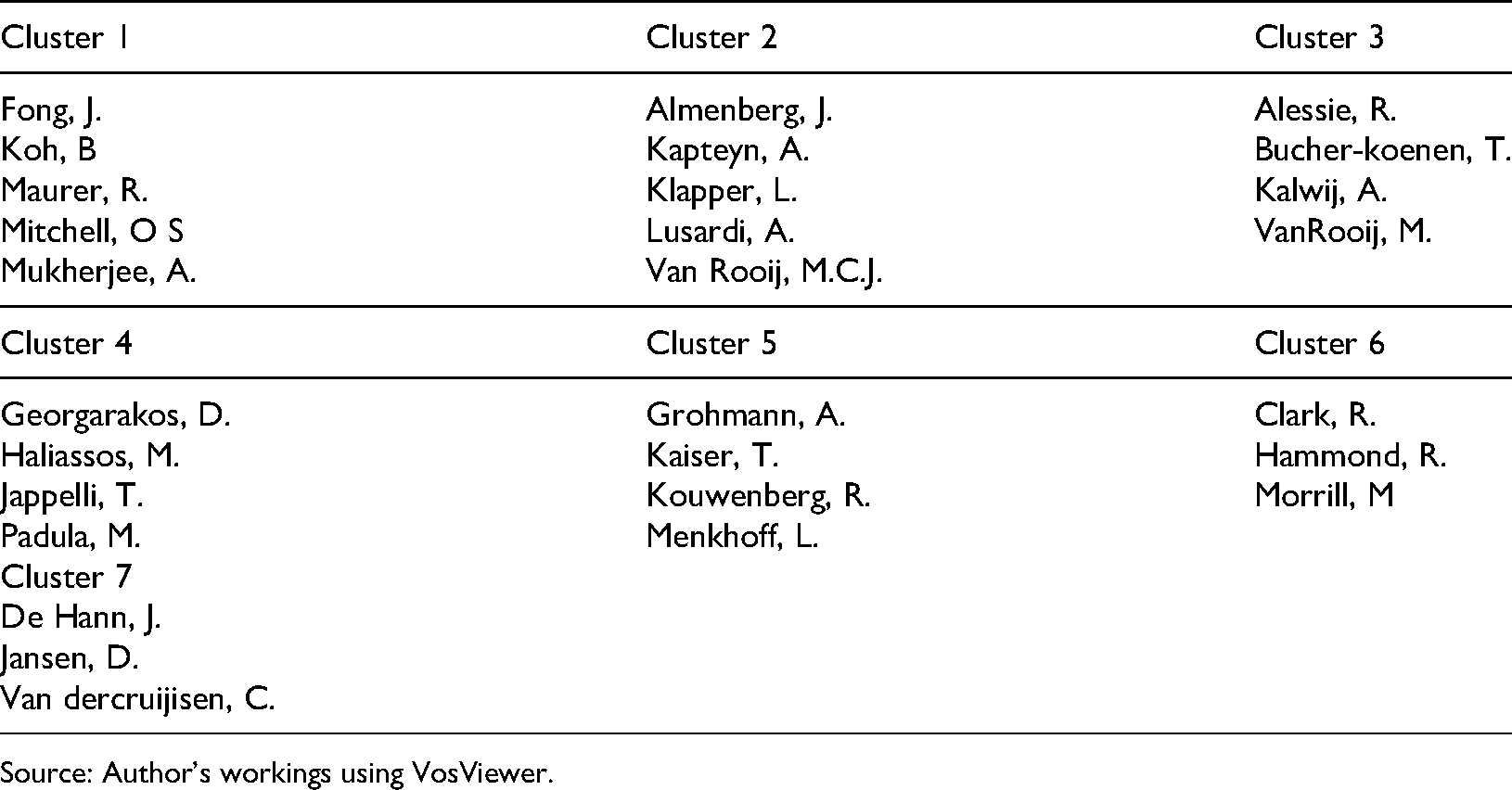

Figure 9 shows the network between different authors based on collaboration. In total, 2055 authors have been taken from the analysis point of view; out of these authors, Lusardi A. and Mitchell O.S. are authors with the highest production. Lusardi A. is connected to Almenberg, J., Klapper, L., Kapteyn, A., Van Rooij, M.C.J., Bucher-koenen, T., VanRooij, M., Alessie, R., Moreover Mitchell, O. S. is connected to Fong, J., Koh, B, Maurer, R., Mukherjee, A., Clark, R., Kouwenberg, R., Kapteyn, A. Both of these Authors are also connected with a link strength of 10 (strongest connection). The network shows 28 authors having at least three documents; of these 28 authors, a total of 7 clusters can be formed, as shown in Table 6. The total no. of links is 35, with a total link strength of 77.

Co-Authorship network. Source: Authors’ workings using VosViewer.

Co-Authorship clusters

Source: Author’s workings using VosViewer.

Themes and keyword analysis

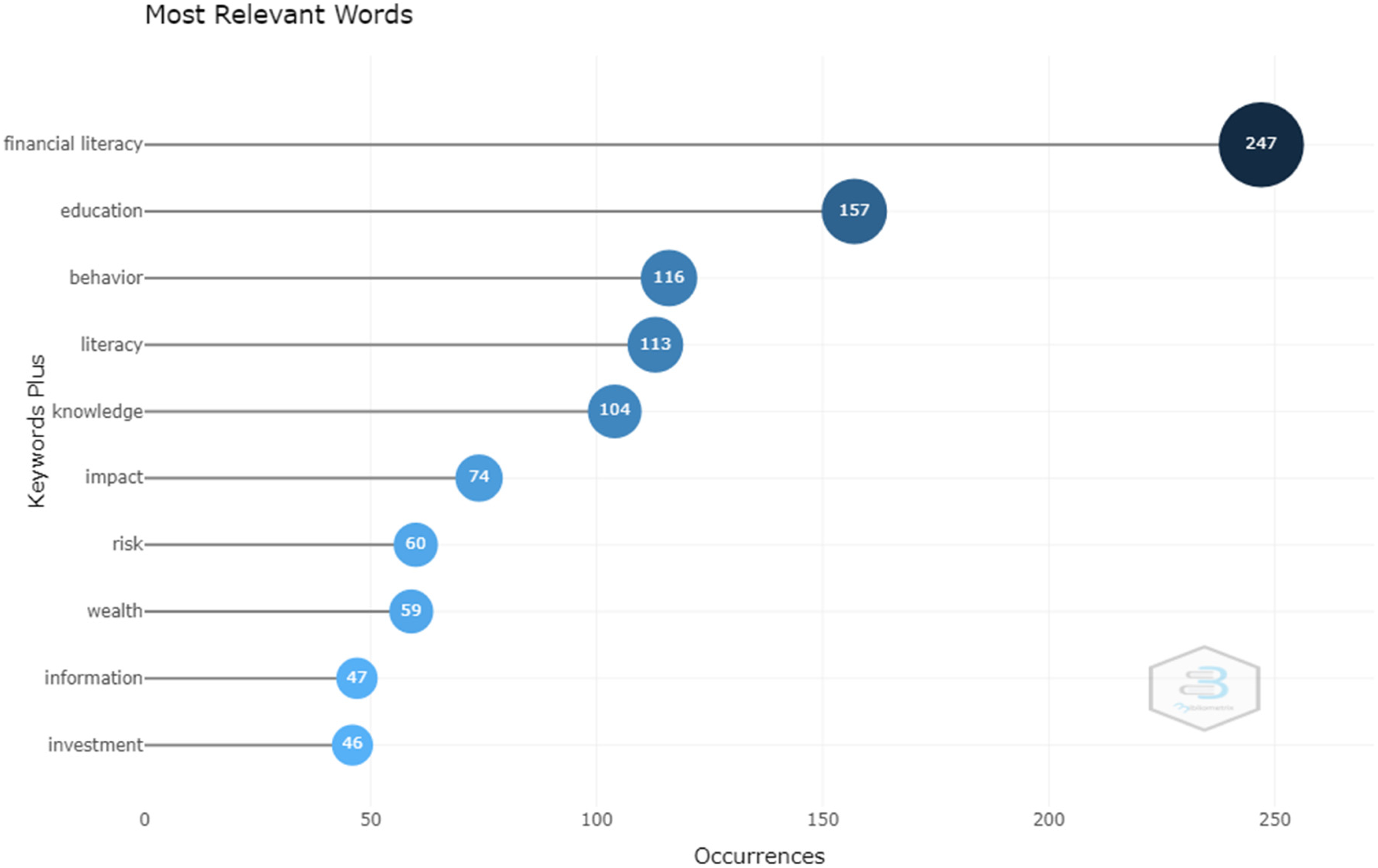

Keywords analysis can be used as a method of understanding the thematic structure of the research advances in the concerned field. To illustrate the evolution of different research areas and the trends in financial literacy and Well-being, A keyword analysis was carried out on the data. Figure 10 shows the top 10 most occurred keywords in the literature. Financial literacy is the most occurred keyword with 247 occurrences, followed by education (157), behaviour (116), literacy (113), and knowledge (104).

Most relevant keywords. Source: Authors’ workings using Biblioshiny.

Contemporary topics

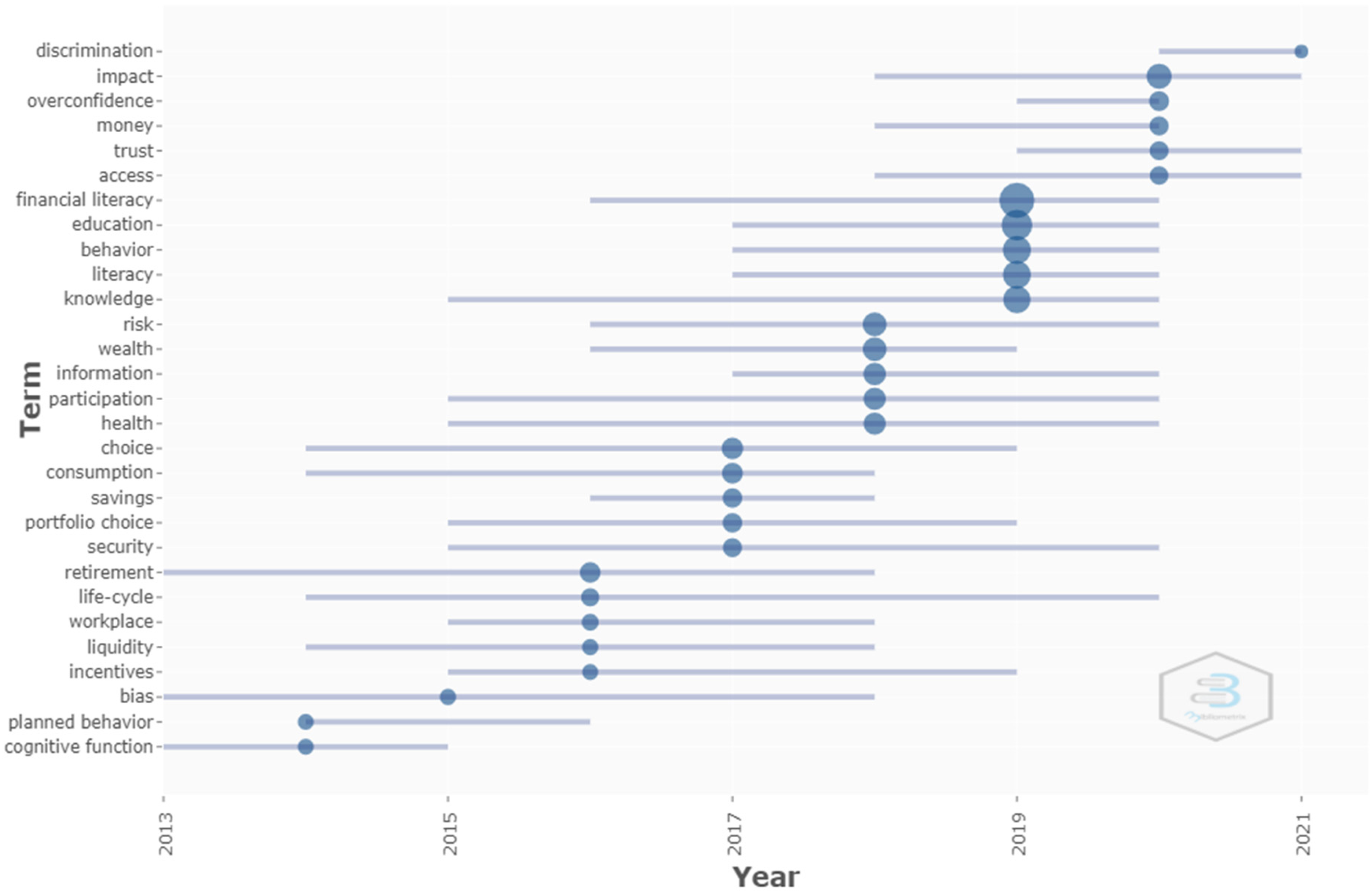

Contemporary topics are the trending topics (Subset) within the discipline (Superset) that give an understanding of the hot topics in the field. Figure 11 shows the yearly distribution of the trending topics. The lines depict the use of the respective keyword, and the circle represents the point of time when the individual keyword was in trend. The results show that in the Year 2020, ‘Impact’, ‘Overconfidence’, ‘Money’, ‘Trust’ and ‘Access’ were the trending areas. ‘Overconfidence’ and ‘Trust’ are the behavioural side of financial literacy and well-being, which also tells that the research advances in 2020 were concerned with Soft-skills. In 2019, the terms ‘Financial literacy’, ‘Education’, ‘Behaviour’, ‘Literacy’, and ‘Knowledge’ were in trend.

Contemporary topics in the field. Source: Authors’ workings using Biblioshiny.

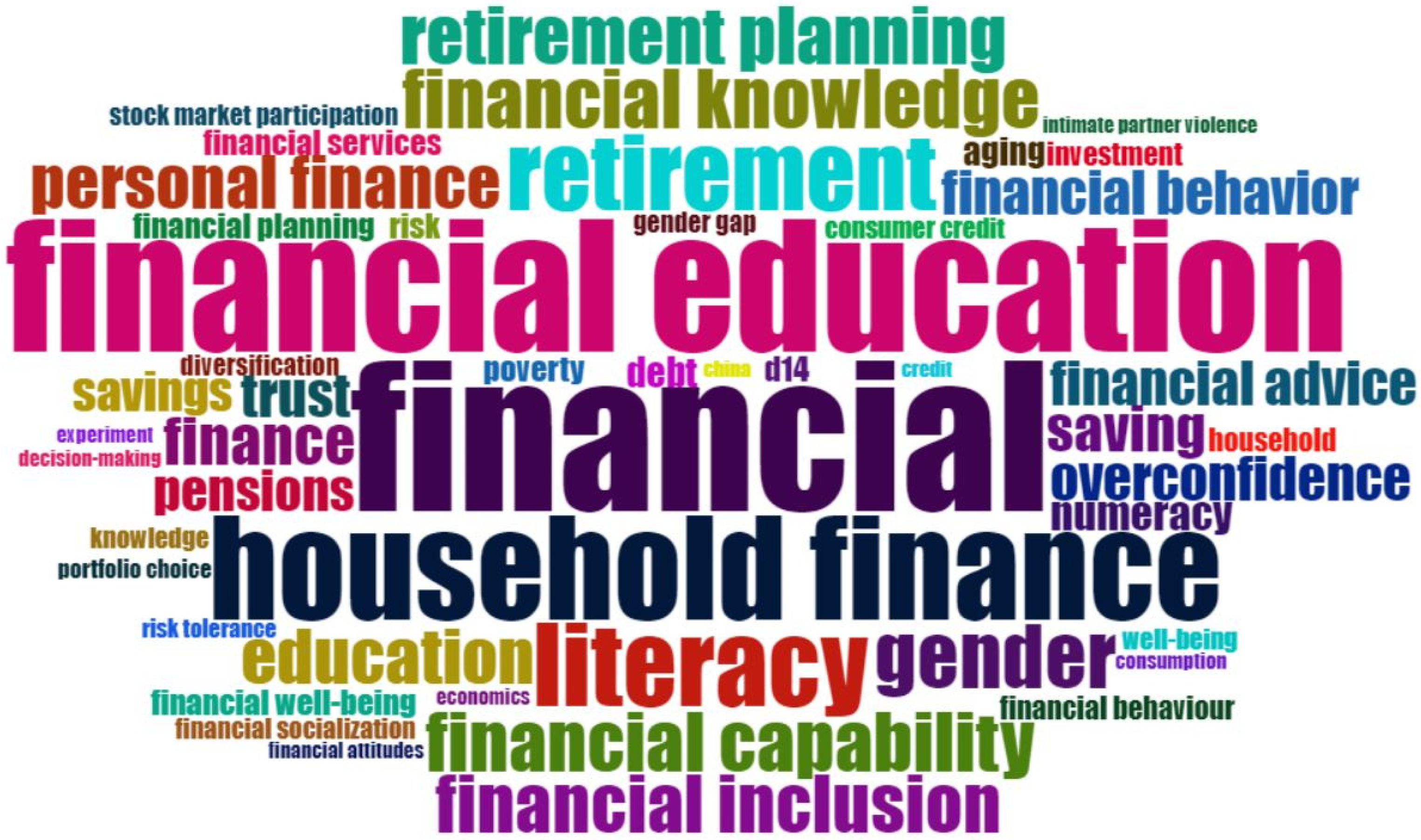

Figure 12 shows the visual depiction of the top 50 keywords framed in the form of a word cloud. ‘Financial literacy’, ‘Education’, and ‘Household Finance’ have the highest frequency in the literature. Well-being is the sub-area of human development and individual upliftment; thus, one can see the related keywords in the literature such as ‘Retirement Planning’, ‘Gender’, ‘household finance’, ‘Personal finance’ etc.

Word cloud (50 keywords) on financial literacy and well-being. Source: Authors’ workings using Biblioshiny.

Co-occurrence network

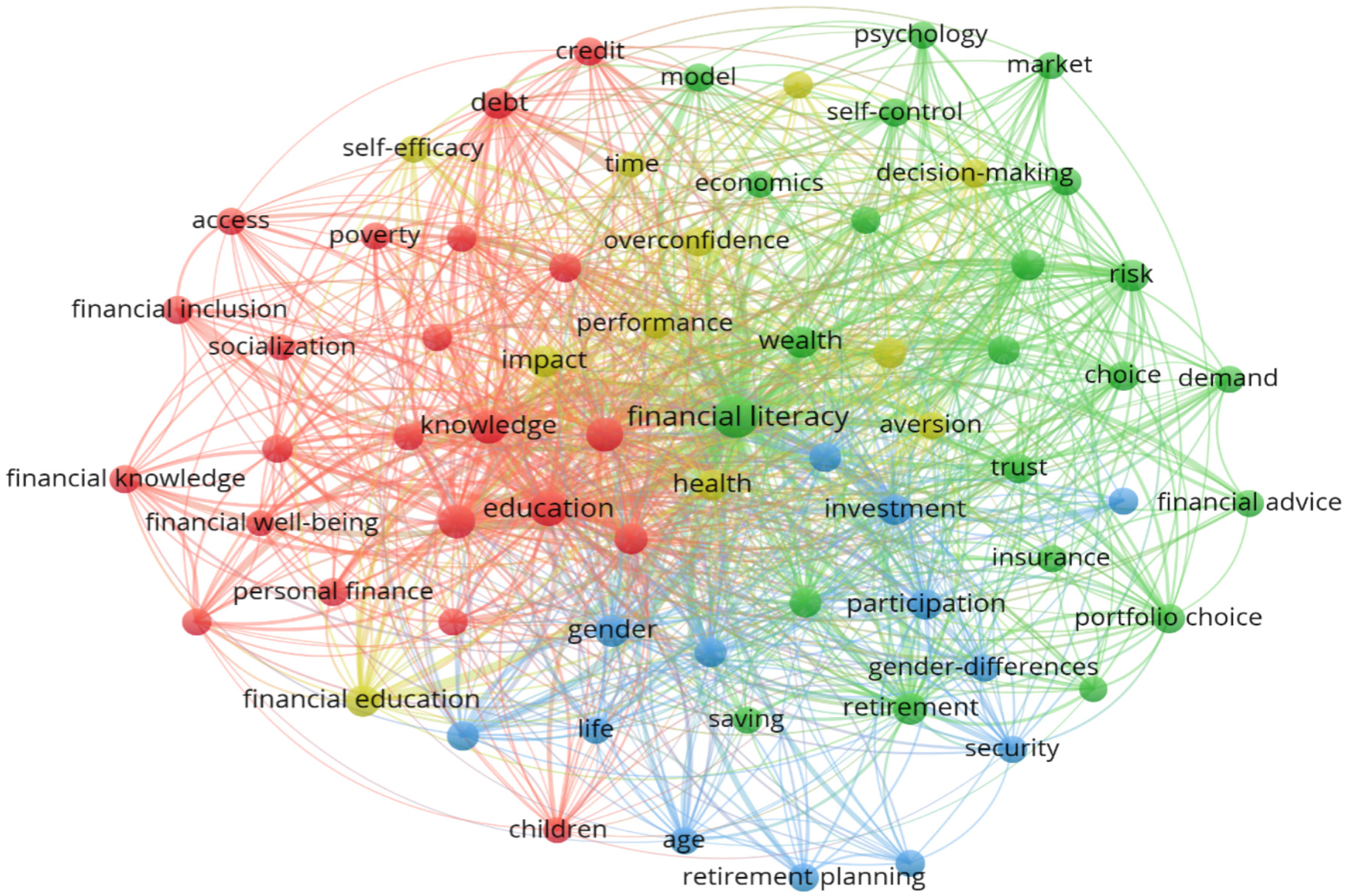

Figure 13 Illustrates the relationship between top keywords, where the keywords are shown on the basis of their co-occurrences. The colour scheme is based on various clusters. In totality, there are four major Clusters, coloured Red, Green, Blue, and Yellow. The keywords selected for the purpose of network building are based on a specific criterion where the minimum no. of occurrences of a keyword is opted as 15 for making sure that the keyword has been adequately used in the literature. 68 Keywords fulfil the criteria.

Co-Occurrence network. Source: Authors’ workings using VosViewer.

In Figure 13, among all the 4 clusters, the two most significant clusters based on no. of keywords are Red (22 keywords) mainly consists of Demographic variables, and Green (22 keywords) primarily consists of Economic variables followed by Blue (13 keywords) which consists of Welfare factors and then comes Yellow (11 keywords) which mainly talks about behavioural factors. Further discussion on the themes and conceptual framework is taken in part 4.9 of the study.

Three-field plot

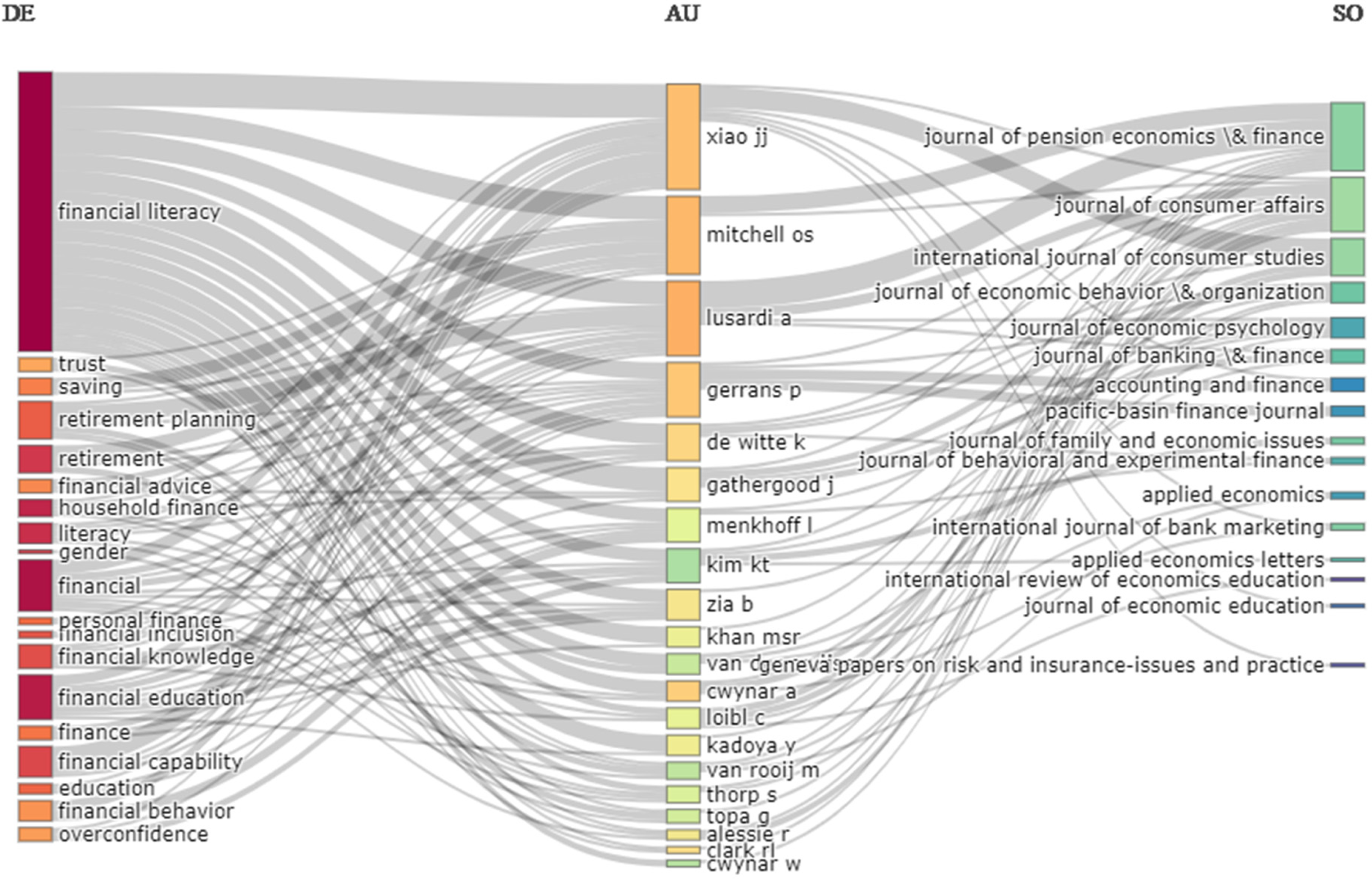

After the discussion on Keywords, Sources, and Authors, it was essential to bridge the gap of linkages among these heads. For the purpose of understanding the connection between top keywords (approximated as themes), Top authors, and Top sources (Journals), a three-field plot has been created. Figure 14 shows the linkages mentioned above. In the left-most column, top keywords have been put; it consists of ‘Financial literacy’, ‘Financial Education’, ‘Retirement planning’, ‘Financial behaviour’, among others. The middle column shows Top authors, and the rightmost column shows Sources (Journals). For every column, the left column (except for Keyword) is the incoming variable, and the right column (except for Sources) is the outgoing variable. The width of the connecting lines between columns shows the strength of the connection among variables. For the purpose of interpretation, let say, if one wants to know that who has in the past worked on ‘Trust’ in the domain of financial literacy and well-being, then looking at the three-field plot, one sees that it is connected to Mitchell O. Further one intends to know where that work is majorly being published so that the work can be tracked, using the plot it can be seen that such work is published in the Journal if pension economics & finance.

Keyword-Author-Source connection plot. Source: Authors’ workings using Biblioshiny.

Citation analysis

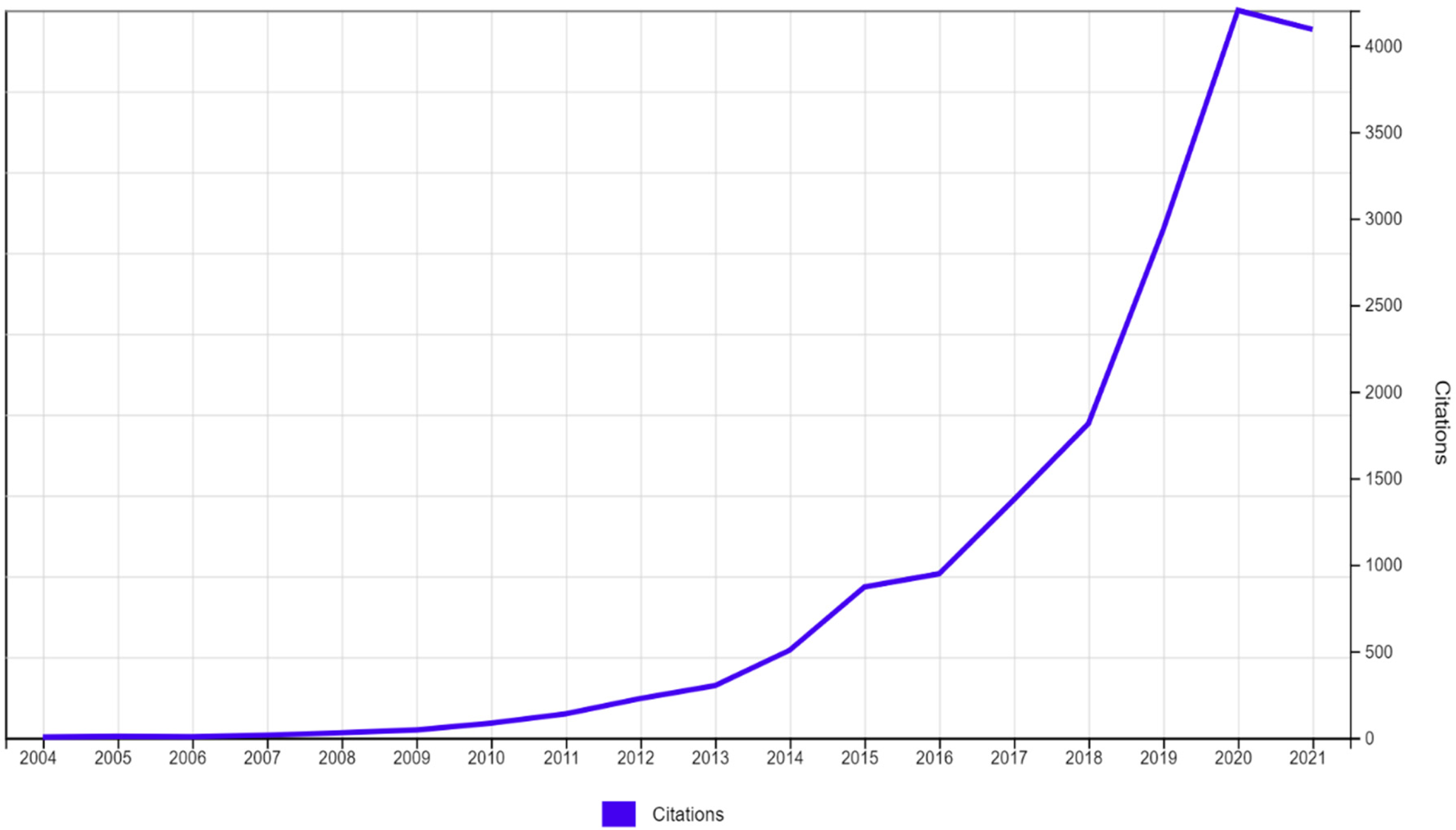

Goyal and Kumar (2021) mentions that the frequency of the citations of a document indicated the influence and productivity of that document over others. The best way to map the impact of a research paper is to use citation analysis Tsay (2009). How many times a document is cited in other research work indicated the citation count of that document. The trend of the citations in a field can suggest the movement in the influence of the area. Figure 15 shows the immense rise in the citations in the concerned field, which indicates the rising influence of the field. The TC rise from near zero in the early 2000s to more than 4000 in recent years.

Citation growth over the years. Source: Web of Science analyses.

Co-citation network

When a single unit of a document (Articles in this case) is cited in the reference section of two papers, then those two documents are said to be bibliographically coupled, Kessler (1963). The purpose of bibliographic coupling, as mentioned by Glänzel and Czerwon (1996), is finding insights on the structure of research, and also it is highly recommended for scientific mapping. Vladutz and Cook (1984) argues that bibliographic coupling helps in validly associating studies that are similar in context and nature.

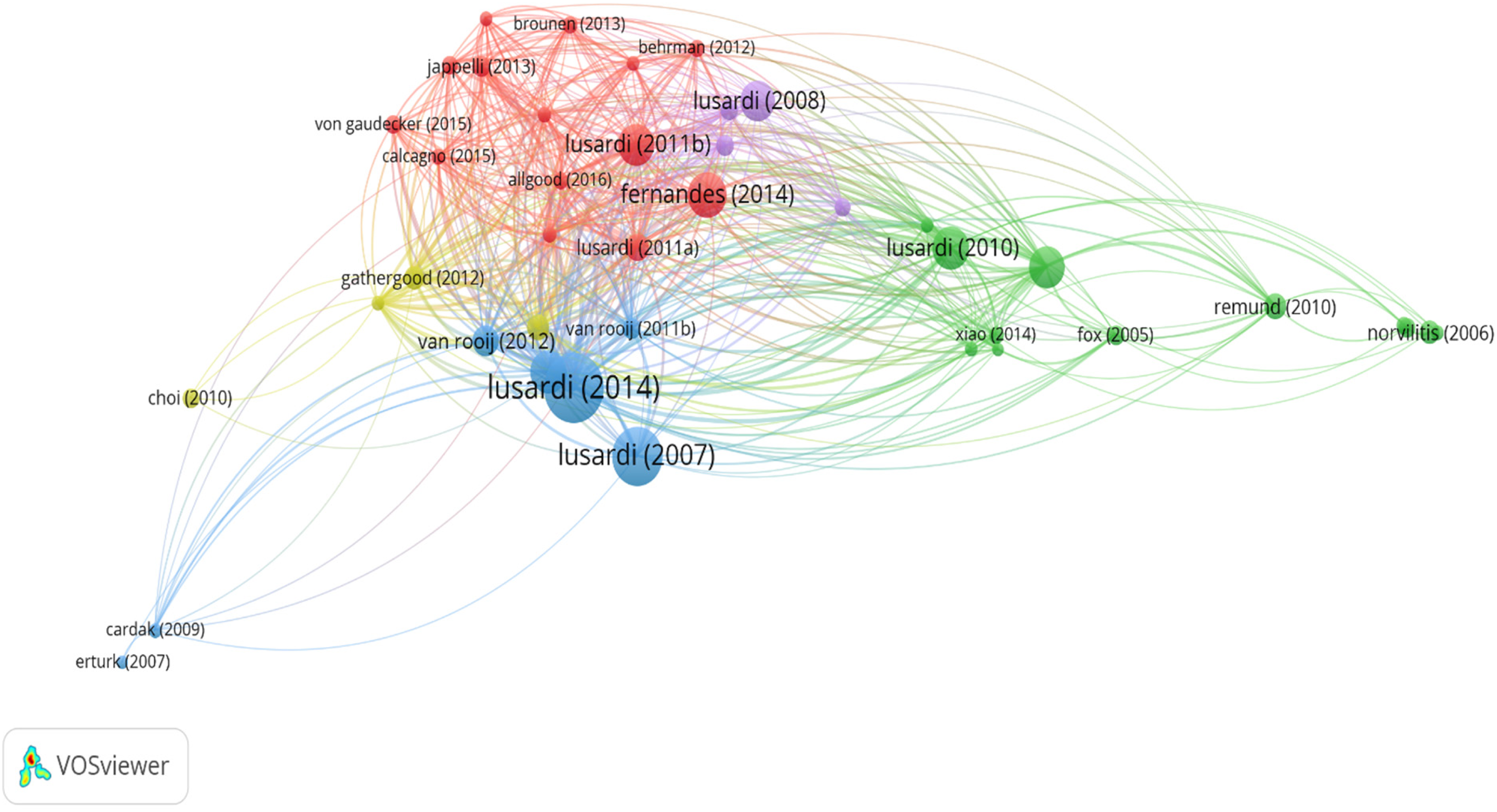

Therefore, A bibliographic coupling network has been created from the documents. Figure 16 above shows the co-citation connection map based on bibliographic coupling. Papers with a minimum of 80 citations each were selected for the purpose of network building. The criterion of 80 citations was arbitrarily chosen in order to get more relevant researches in the field and less no. of documents in the network for clarity of visuals. Five clusters can be seen in the figure, which is depicted based on five colour schemes (Red, Yellow, Green, Blue, & Purple) and also the connections between the documents.

Clusters based on Bibliographic coupling network. Source: Authors’ workings using VosViewer.

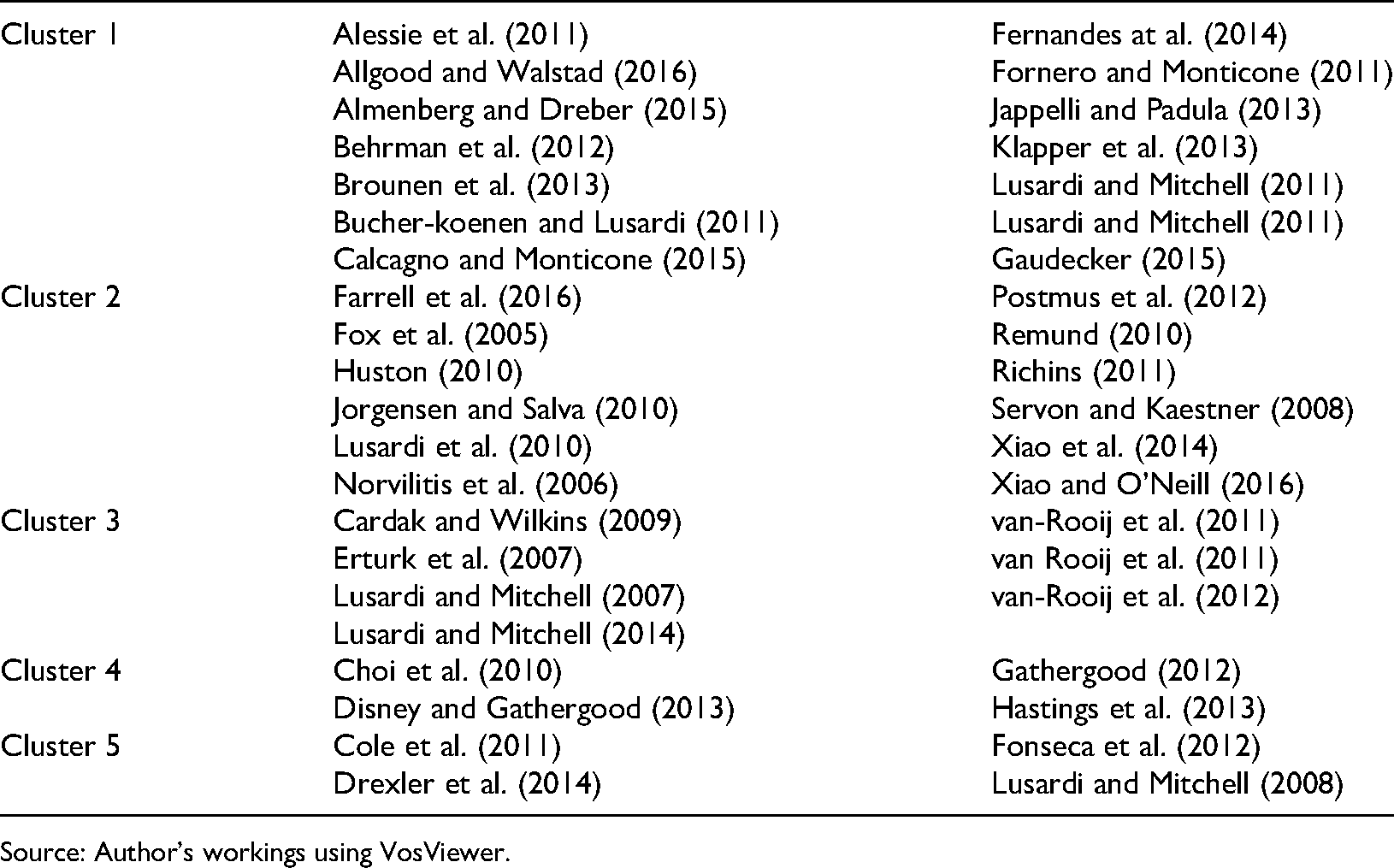

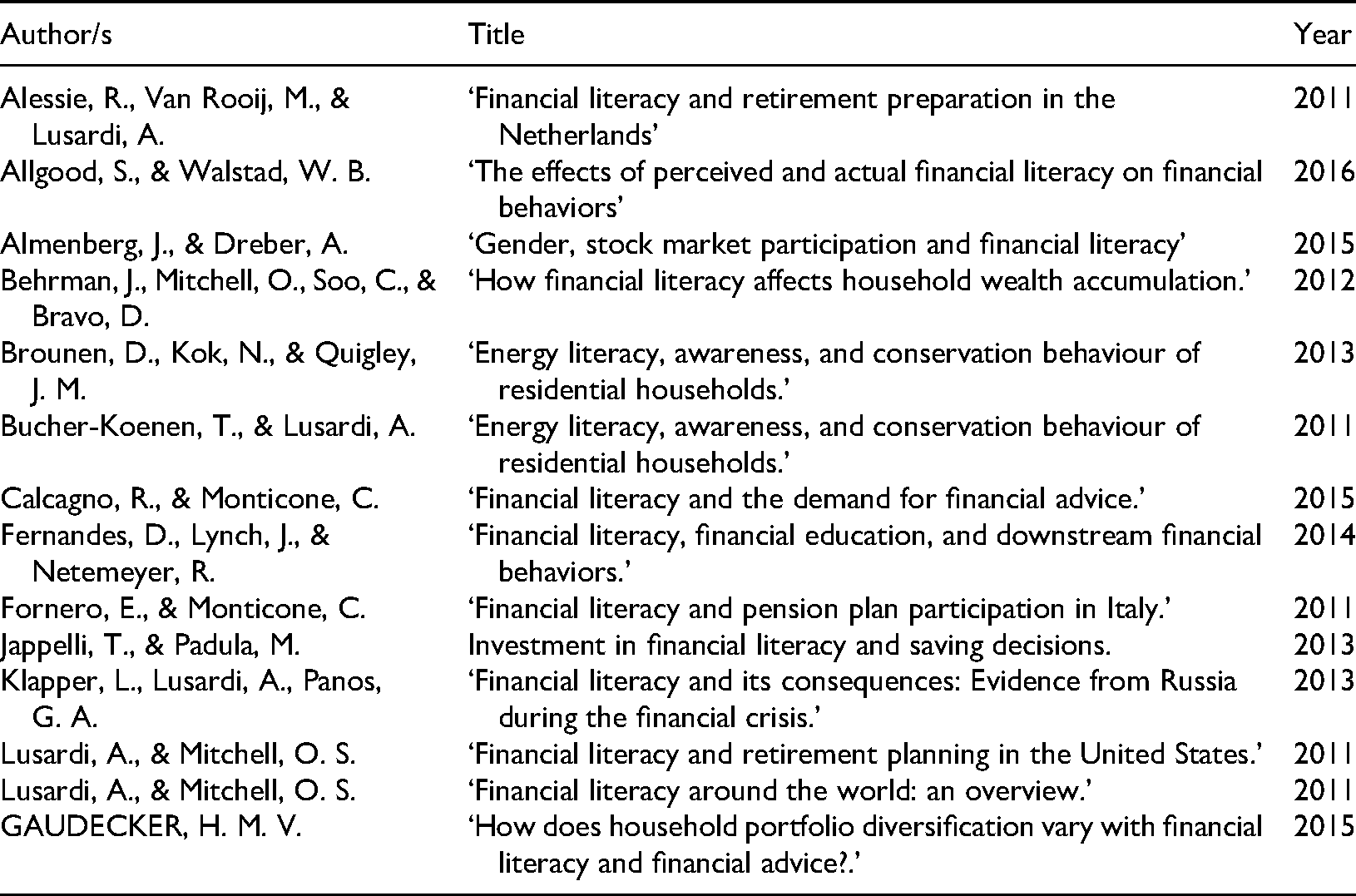

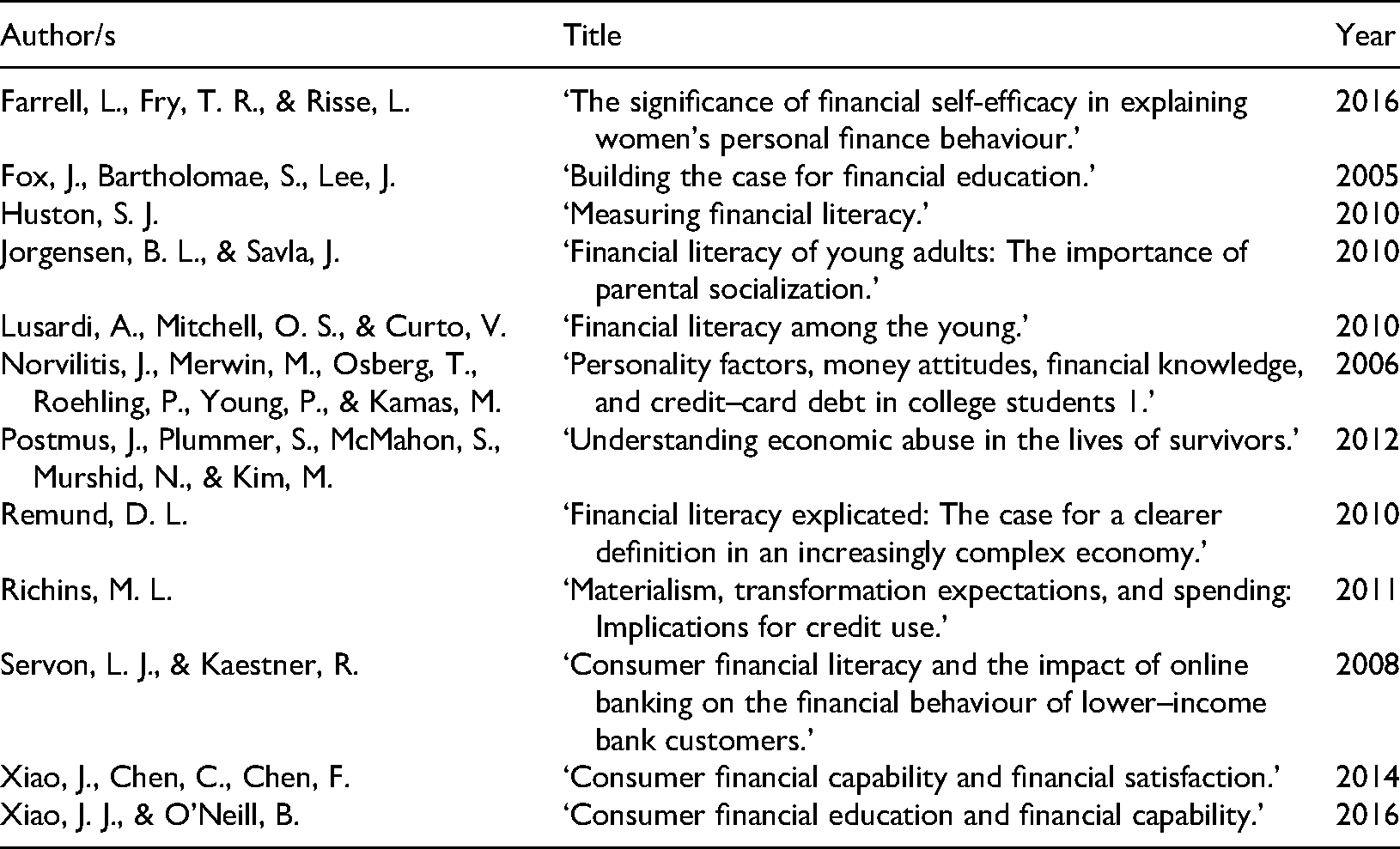

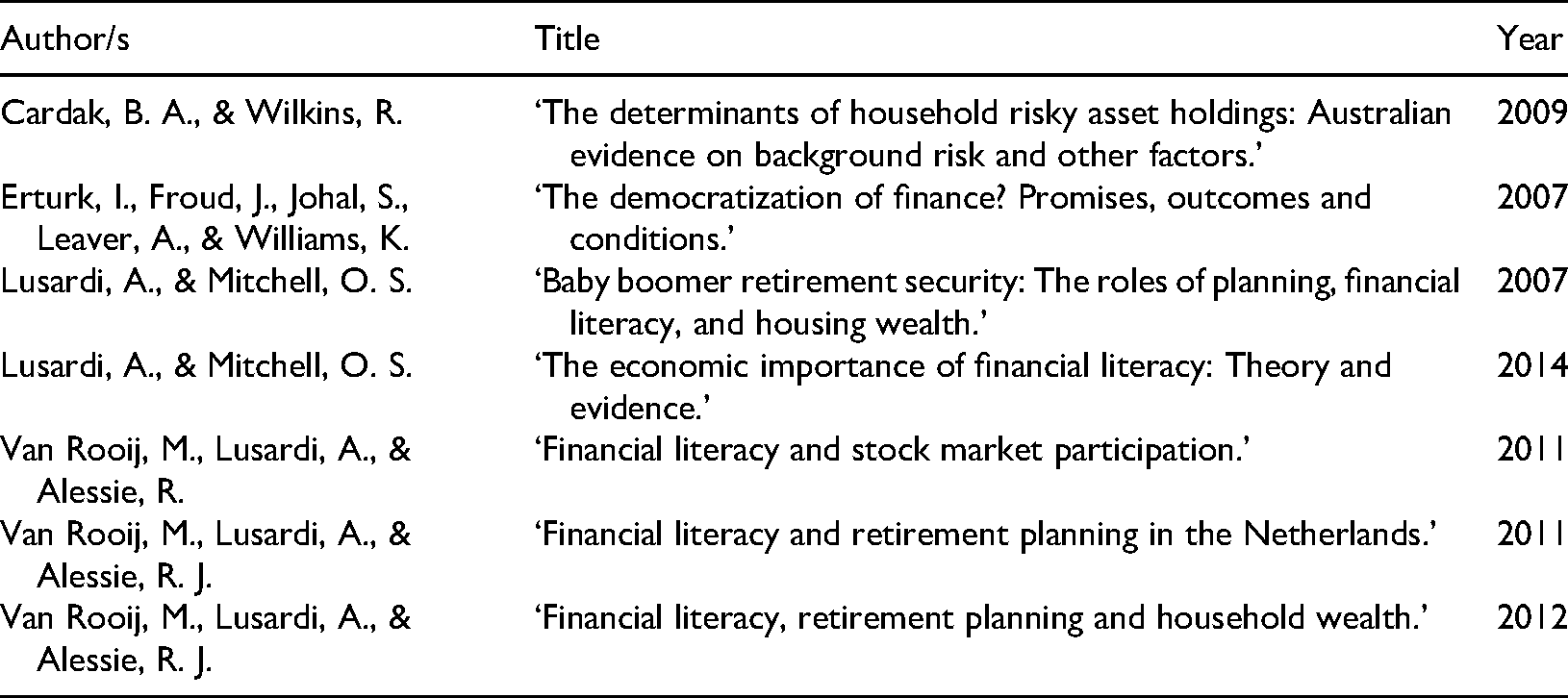

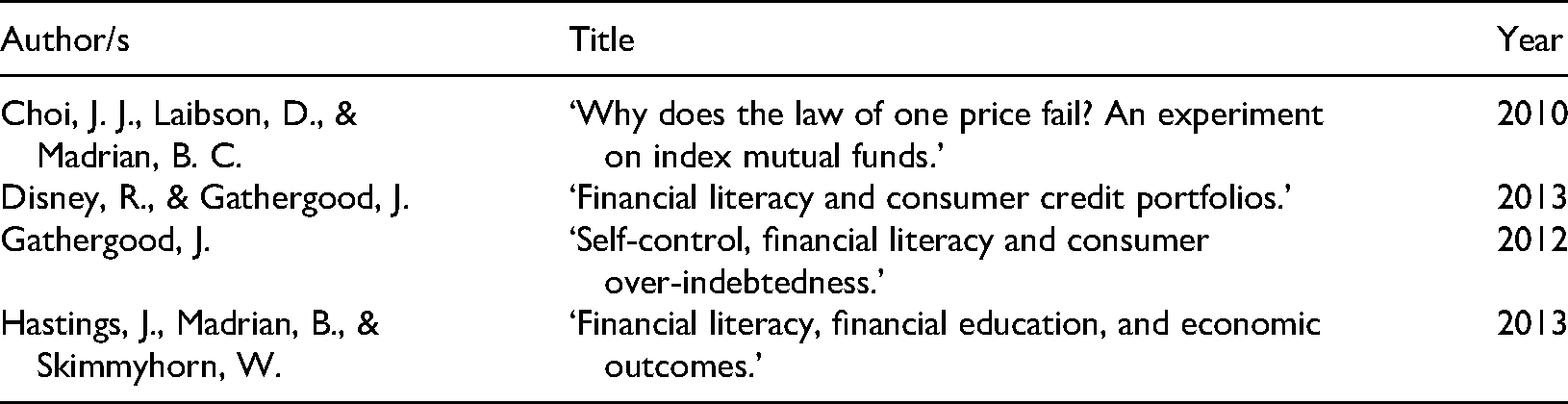

The Five clusters and their contents are summarised in Table 7 below:

Co-Citation clusters based on bibliographic coupling.

Source: Author’s workings using VosViewer.

Conceptual framework

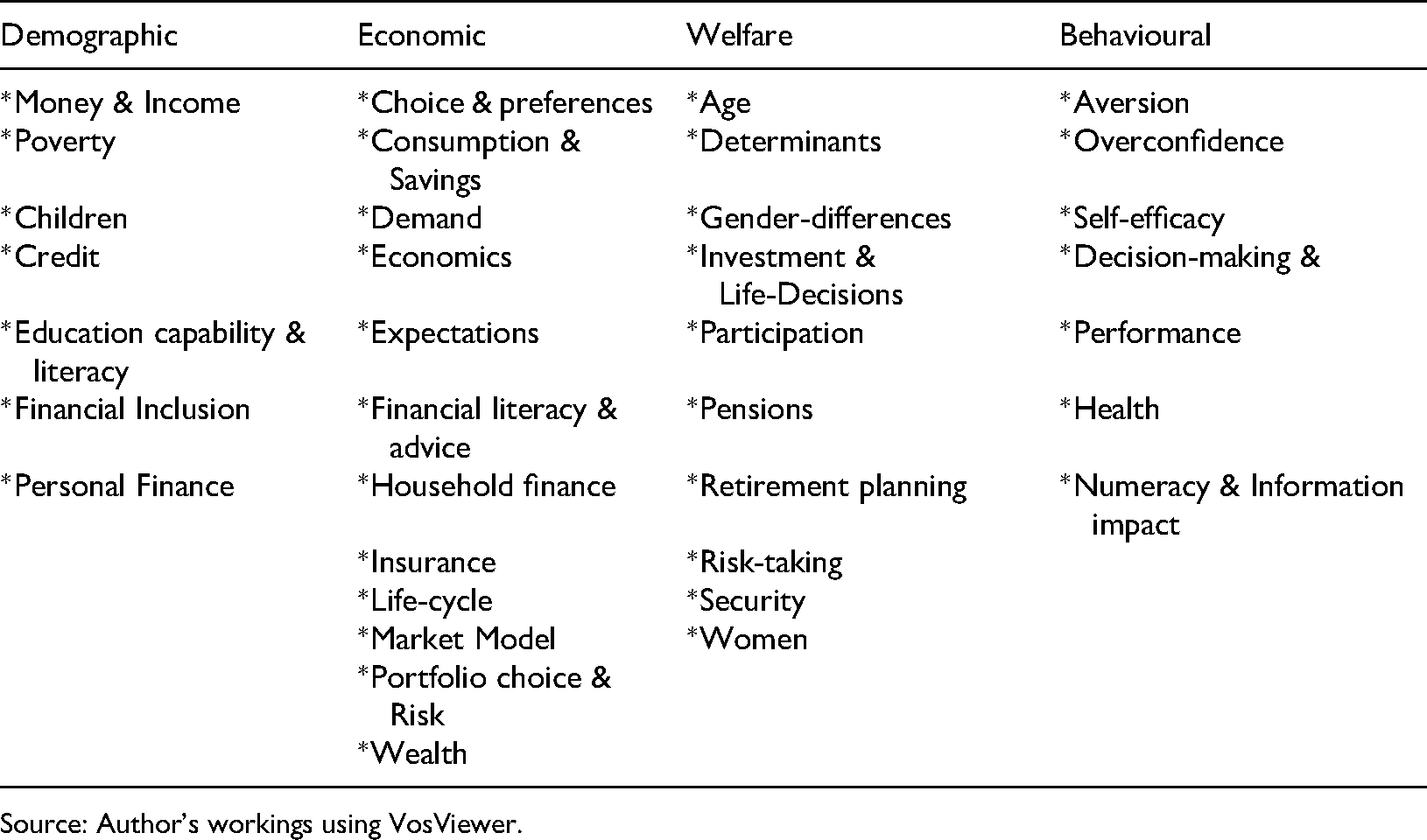

The papers reviewed can be divided into two bases. Firstly, the clusters can be made based on themes identified in the Co-occurrence network. 4 themes are identified on that basis that is earlier mentioned in section 4.6.2 of the paper, the Four themes (Demographic, Economic, Welfare, Behavioural) and the contents (Keywords) are summarised in Table 8 below:

Clusters based on co-occurrences

Source: Author’s workings using VosViewer.

The second way to create clusters and themes is on the basis of content analysis of the Co-citation network mentioned in section 4.8 of the study. The papers can be divided into 5 clusters as per the bibliographic coupling technique (Tables 9–13).

Cluster 1 based on bibliometric coupling

Cluster 2 based on bibliometric coupling

Cluster 3 based on bibliometric coupling

Cluster 4 based on bibliometric coupling

Cluster 5 based on bibliometric coupling

Key findings

The study highlights major research gaps in the literature of the past two decades, despite the fact that the literature has seen tremendous growth, the growth has been highly asymmetric. Causality-based studies have been given more attention rather than theoretical advancements. It was found that ‘financial literacy’ as an area of research is majorly studied using quantitative analysis; qualitative studies are lacking in the field. In the present study, we categorised the literature into four categories and subsequently sub-categories. Based on the co-occurrence analysis, the literature falls in the following categories:

Demographic

Studies that examine the demographics of the financial literacy phenomenon make up the demographic cluster on financial literacy and well-being. The studies are based on assessments of the financial literacy levels in various demographic groups. This entails implications for the policymakers in designing programmes that caters specific needs of each demographic group. Numerous research shows a link between financial literacy and demographic factors, Garg and Singh (2018); Lusardi et al. (2010). According to Shusha (2017), gender, income, educational achievement, and age all have an effect on one of the most important components of financial literacy – the degree of financial risk tolerance. According to Baker et al. (2018), demographics have an impact on a variety of behavioural biases in addition to financial literacy.

Economic

Economic literacy is frequently considered as a replacement for financial literacy. The heart of this cluster consists of research and causality analyses that describe theoretical connections between financial literacy and economic variables including saving and consumption patterns, economic expectations, choice and preference of insurance and wealth management products, demand, etc. According to empirical evidence presented by Murendo and Mutsonziwa (2017), financial literacy has a considerable impact on both formal and informal savers’ behaviour. In fact, according to Deuflhard et al. (2019), financial literacy also affects how much people make from their small, medium, and large-scale investments and forecasts the demand for a variety of financial goods, such as insurance (Lin et al., 2017)

Welfare

Studies that explain this connection are included in this cluster because financial literacy is a prerequisite for welfare. The patriarchal nature of society as a whole and its impact on wellbeing are signalled by the gender gap in financial literacy. Men are more likely to make financial decisions and to be financially skilled as a result (Fonseca et al., 2012). This is considered in a number of studies. Also addressed in the literature is the relationship between financial literacy and other types of welfare, such as retirement planning. Financially literate people are more likely to plan for retirement, according to Lusardi and Mitchell (2011a).

Behavioural

Financial literacy is a construct in which behaviour plays a significant impact, as stated in the OECD (2014). Based on the co-occurrence in this cluster, studies that discuss the relationship between different elements of behaviour (overconfidence, self-efficacy, aversion, etc.) and financial literacy are grouped together. Financial market activity is predicted by a high level of financial confidence (Xia et al., 2014). Numerous research have shown that the behavioural component of financial literacy, which includes self-efficacy, is a key component of the financial literacy score and it has also been used in creating an Index for the same (Remund, 2010; Warmath and Zimmerman, 2019).

Limitations

Only papers that have been published in the Web of Science database are considered in the current analysis. Although Web of Science (WoS), as was already said, effectively serves the aim of bibliometric analysis, Korom (2019), future research may still make use of other databases, such as EBSCO, Scopus, etc. Studies that measure the degree of financial literacy among different population groups employ a variety of methodology; these methodologies vary in their methods, models, and survey questions. Similar questionnaires and procedures must be utilised in order to produce valid comparisons, as stated in Yoshino et al. (2015). Future studies may conduct reviews based on the thematic analysis of methodology.

Studies that are in the character of working papers and that are sponsored by international multilateral institutions such as the World Bank, Organisation of Economic Cooperation and Development, IMF etc. and Central Banks including the Reserve Bank of India, Federal Reserve, and European Central Bank among others can be specifically focussed in the future researches on the topic.

Conclusion

Bibliometric analysis is crucial from the perspective of understanding the research advances in depth. The direction in which the research is going can only be understood with the help of a bibliometric study. The study used the meta-data to get insights out of the available literature on ‘Financial literacy and Well-being’ for the past two decades, Top authors, Journals, major themes, the connection between the three, top countries in the field, the conceptual frameworks of study along with co-citation and co-occurrence network analysis are the techniques that were undertaken throughout the study. The growth in the literature has been remarkable in the past years, but still, the discipline has new horizons that are still untapped. The majority of the studies that were included in the conceptual structure of the paper were causality-based, meaning thereby that they were trying to find causal linkages among financial literacy and other variables like Retirement Planning and Wellness, Alessie et al. (2011); Bucher-Koenen and Lusardi (2011); Fornero and Monticone (2011); Lusardi and Mitchell (2011a), Stock market participation, Almenberg and Dreber (2015), Wealth accumulation, Behrman et al. (2012). Studies in the area of behaviour concerning financial decision-making have been flourishing in recent times. In Financial literacy and Well-being, financial behaviour, Trust, Overconfidence, Self-efficacy, Preferences came out to be the crucial keywords in the analysis. Allgood and Walstad (2016) studied perceived and actual financial literacy; they concluded that perception of financial literacy is essential, in fact, almost as crucial as the level of basic financial literacy. Fernandes et al. (2014) argue for the importance of financial behaviour as a variable to be considered by the policymakers while building the financial education programmes. Therefore, it can be said that financial behaviour is an important field of the discipline. But there were little to no qualitative studies available in the areas. There were no grounded theory-based studies; although the interview method was highly used in the literature, the purpose it served was empirical and not qualitative. The literature can be divided into four major thematic categories (Demographic, Economic, Welfare, Behavioural), which further consists of minor categories. Gender, Gender-differences, and Women’s welfare is a niche area within financial literacy and Well-being which requires a lot of work specially in the emerging countries like India. Women’s participation in financial decision-making ensures the holistic development of society. Other welfare topics seen in the Co-Occurrence analysis were Pension, Retirement, Life, and Security. But there was a massive asymmetry observed in favour of western countries for all the categories combined. Therefore, even though these topics showed up in the Top keyword list, but the distribution was unequal, which again suggests a huge cope for middle, lower-middle- and low-income countries.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article