Abstract

OBJECTIVES

The adverse effects of physician stress on health system performance are well documented. Financial stress is a notable cause of anxiety in medical residents; however, most residency programs lack formal, comprehensive financial education programs. Early single-center studies link financial education interventions to improved immediate fiscal well-being, but programs evaluating its long-term effects are lacking.

METHODS

Fifty (50) Emergency Medicine and Internal Medicine resident physicians from CommonSpirit Health's St. Joseph's Medical Center in Stockton, CA and Mercy One Medical Center in Des Moines, IA participated in a virtual 8-hour financial education course in April 2022. Participants completed pre-, post-, and 18-month follow-up course surveys to measure financial confidence in seven financial domains and six markers of stress of financial origin (SOFO).

RESULTS

Forty (40) of 50 residents (80%) completed the pre-and post-course surveys and 19 (38%) completed pre-, post-, and 18-month follow-up surveys. Immediately after the course, there was a statistically significant increase in financial confidence in all seven course domains (p < 0.01) and a significant reduction in SOFO markers (p < 0.01-0.02). At 18 months, financial confidence markers remained increased in most course domains, except related to debt and mortgage, passive income, and taxes. There was a strong association between financial confidence and SOFO immediately post course. Residents with low financial confidence were 15 times as likely to experience SOFO than those with higher financial confidence (p = 0.02). These associations did not persistent at 18 months.

CONCLUSION

Financial stress is a major contributor to anxiety among physician trainees. Our financial education program demonstrated a significant impact on financial confidence and markers of SOFO, especially in the short term. This offers promising results for personal finance education to serve as a feasible intervention to address physician stress but suggests the need for longitudinal education to maintain its beneficial effects.

Keywords

Introduction

Work-related stress and anxiety are more common in physicians than in the general US workforce 1 with stress and burnout reported as high as 53% in the 2023 Medscape National Physician Burnout and Depression Report. 2 Physician stress has been identified as an essential health system performance indicator as it intricately affects patient care and experience, health outcomes, and overall costs of health - the three components of the Triple Aim. 3

The Triple Aim was introduced in 2008 by Berwick and colleagues and developed by the Institute for Healthcare Improvement to optimize health system performance by pursuing three dimensions. The framework emphasizes improving health outcomes with patient experience, population health, and cost considerations. 3 In 2014, Bodenheimer and Sinsky proposed expanding the Triple Aim to a Quadruple Aim to include improving the work life of health care providers, emphasizing that “care of the patient requires care of the provider.” The authors identified the burdens on physicians and the high expectations of healthcare as disproportionate to the resources available and that the stress of work life adversely affects the ability for physicians and other staff to achieve the three aims. 4

Physician stress has many implications for the healthcare ecosystem as it leads to increased turnover rates, physicians leaving the clinical workforce, medication errors, decreased empathy, and unnecessary testing.5,6 The effects of stress on the healthcare system were prominent during the COVID-19 pandemic as its increasing rates led many physicians and other health professionals to leave clinical practice. 7 These downstream consequences of physician stress affect the optimal function of the healthcare system and adversely impact patient satisfaction and care.

Of the many causes of physician stress, financial constraints, such as medical education debt, are associated with decreased mental well-being, poor academic outcomes and choosing higher paying specialties. 8 Other factors, such as the inability to choose where to work given the algorithmic placement of residents in residency spots through the National Resident Match Program (NRMP)'s Match® process, and being unable to negotiate a salary or benefits, create financial vulnerabilities that can exacerbate financial stress. Moreover, resident compensation, which is centrally controlled by the Centers of Medicare and Medicaid Services, or CMS, has also not kept pace with inflation and cost of living in many regions of the country. 9 Many residents are severely underpaid based on the geographic area that they serve. 10

In general, financial stress has been linked to decreased psychological wellness, 11 depression, 12 and higher levels of inflammation on a biochemical level. 13 In the above mentioned 2023 physician Medscape survey, 34% of surveyed physicians stated that insufficient compensation / salary contributed most to their stress and named “increased compensation” to avoid financial stress as the most requested alleviation strategy. In physician trainees, financial worries also increased the odds for stress, in addition to work and patient care demands. 14 Financial burdens also can negatively impact resident performance including a negative correlation between debt and work satisfaction. Higher debt was associated with higher reported life dissatisfaction, career regret, stress, and burnout symptoms. 15 In 2008–2009, a national study demonstrated an association between the frequency of stress and the burnout symptoms and decreased quality of life with lower in-service examination scores in Internal Medicine trainees. Scores also decreased in residents with higher levels of debt ( > $200,000). 16

Multiple studies have shown a perceived need for financial education among residents of various specialties. A common theme among these studies is that residents report low rates of formal training and high rates of self-study of financial literacy.17,18 Notably, residents reported lack of confidence making financial decisions once they complete residency and work as attending physicians. 15 Some early study data demonstrates that cultivating a sense of financial literacy through a targeted intervention is associated with an increased sense of preparedness among radiation oncology residents 19 and general well-being in OBGYN residents. 20 Teaching financial literacy has been proposed to address stress in medical trainees, however formal studies are lacking.21‐23

Although early single-center studies have shown some link to financial wellness and stress, it remains unclear how a comprehensive, physician developed personal finance curriculum addresses stress and wellness in two of the most stressed specialties, Emergency Medicine (EM) and Internal Medicine (IM).1,2 In addition, we are unaware of existing research that has examined perceptive financial risk markers as precursors for poor well-being in a longitudinal capacity, beyond immediate post intervention evaluation. Using the Kirkpatrick model for Learning Evaluation, we conducted the current program evaluation with the following hypotheses:

Learning level: Participation in a comprehensive financial education course would improve financial confidence in each of the determined financial literacy domains both immediately and at 18-months post intervention. Results Level:

Financial confidence status correlates with markers of stress of financial origin (SOFO) and perceived financial wellness among physician trainees. A targeted training program that augments the financial confidence of physician trainees will substantially reduce markers of stress of financial origin (SOFO) and perceived financial wellness among physician trainees both immediately and at 18 months post intervention.

We defined SOFO as concerns linked to financial stressors measured using a questionnaire reviewed, enhanced, and approved by the curriculum development team.

Methods

EM and IM residents at CommonSpirit Health (CSH)'s St. Joseph's Medical Center (SJMC) in Stockton, California and MercyOne Medical Center in Des Moines, Iowa participated in an 8-h financial education course in April 2022. CSH delivers clinical care across a system of 140 hospitals and more than 1000 care sites in 21 states, serving as one of the nation's largest providers to Medicaid beneficiaries and one of the largest health systems in the United States. 24 The CSH academic network has approximately 2800 clinical trainees in a broad mix of primary care residencies, medical and surgical sub-specialties, and advanced fellowship training programs. Program evaluation support was also provided by Baylor College of Medicine's Center of Excellence in Health Equity, Research, and Training Program in Houston, TX.

Each resident physician participant from SJMC in Stockton belonged to the Emergency Medicine specialty group while all participants from MercyOne Medical Center in Des Moines, IA belonged to Internal Medicine. The institutional review committees at SJMC and MercyOne Medical Centers approved and deemed this study to be exempt from institutional review board (IRB) oversight. The committees approved the waiver of informed consent and consent to publish given the exempt IRB status of the study, the educational nature of the program, de-identified data collection, and minimal risk to participants. The course was developed by a team of attendings and residents at both institutions. The reporting of this study conforms to the Strengthening the Reporting of Observational Studies in Epidemiology (STROBE) statement (see Supplemental File: STROBE Statement). 25

Financial education curriculum development

The financial education course created for this program was developed by a team of academic physicians, heavily informed by an extensive literature review and needs assessment surveys completed by both resident and attending physicians in both residency programs. We developed an initial consensus list of 13 topics for residents and attendings to rank on the needs assessment survey based on our literature review, personal experiences with finances during and after residency, and several conferences with the curriculum development team. Needs assessment survey information from residents and attending physicians from each participating program was collected prior to the seminar to guide the topics to be discussed and expand on those with more traction during the survey. The surveys captured basic demographic information, baseline confidence levels on financial literacy domains, and general attitudes and beliefs around financial education in residency. Residents and attendings were also asked to rank topics of interest, which were developed into the financial education course material. Participants were invited to offer additional topics or concepts to be covered in a free response section. The one topic that came up on several occasions in the free response section and was not on the original list of topics was “who should be on your financial team?”. As such, this was added to the list of course topics. Topics that were determined to be most important to residents and attending physicians based on their rankings were given preferential time. Specifically, modules such as budgeting and savings, tackling student loans, and retirement planning were given the most time in the course based on their needs assessment rankings (Figure 1).

List of financial education topics, their instructors, and session lengths. April 2022. *This MD / DO is also a licensed real estate agent and tax specialist.”.

Sessions included a combination of lectures and panel discussions as determined by the needs assessment surveys and curated by the curriculum development team. The final list of topics, speakers, and schedule of the day was reviewed through extensive communication among curriculum team members facilitated by multiple virtual conference sessions until the group reached consensus on the course details. A comprehensive session outline for each of the speakers was developed, which included specific learning objectives and recommendations on at least interactive activity during the module (reviewing retirement account asset allocation calculating marginal tax rate, calculating closing costs on a home, etc). The team worked very closely with each speaker to create their lecture and optimize for focus on the highest yield topics for physicians in training. All lectures were reviewed, edited, and finalized by the curriculum team. Each session had a dedicated time for question and answer, and the course was held virtually and recorded on a separate day for each institution and taught by a team of financial services professionals and physicians with self-reported comfort and experience teaching financial education topics (Figure 1). We chose to have most of our educators as physicians as they are considered trusted sources of resident mentorship and can relate to residents’ financial concerns. Additionally, physicians are experts at learning and educating on new and complex topics as part of their professional roles and frequently teach topics both within and outside of their immediate expertise. We apply this principle to their ability to learn and teach introductory financial content as well.

Our non-physician financial and health administration educators were selected based on recommendation by trusted physician colleagues. They were also available to our physician presenters for any financial questions they needed answered to prepare for their presentations. The non-physician financial professionals who were invited to speak were instructed to avoid promotion of any specific products or services and had their lectures reviewed by the curriculum team for any potential biases or financial conflicts of interest.

Course participants

Financial seminar and study participants were PGY 1–3 residents in EM and IM at SJMC and MercyOne. As noted earlier, all residents at SJMC were EM and all at MercyOne were IM. Participating residents were in good academic and administrative standing. Course participation was required for all residents except those with approved exemptions (ie, off-site rotation, vacation, leave of absence). There were 27 residents at St. Joseph's who were eligible to participate and 30 at MercyOne. totaling 57 eligible participants. There were 50 total course attendees with 22 participants from SJMC, 27 from MercyOne, and one from an unspecified other specialty. The sample size was determined based on the number of available and eligible residents in our respective residency programs. The five residents at St. Joseph's and 3 at MercyOne who did not participate had approved exemptions.

The curriculum team developed a pre, post-course, and 18-month follow-up survey using a Likert scale (1- strongly disagree to 5- strongly agree) to assess financial confidence based on the course topics, financial stress and wellness, as well as self-reported desire and ability to participate in physician and patient advocacy initiatives (see supplemental materials). The survey questions were developed and pre-tested on a sample of six attending physicians and population health researchers (12% of the study population). A population health researcher with expertise in survey development gave extensive feedback to improve the design and content of the questionnaire before implementation. The pre-course survey data was collected using SurveyMonkey® immediately before the course, the post-course survey data immediately after the course, and follow-up survey data collected 18-months after the course. Pre-, post- and 18-month follow-up survey data was matched using self-generated participant IDs. Surveys that were incomplete or without pre-or post-match data (n = 10) for the first analysis and pre-, post-, and 18-month match data (n = 31) for the follow-up analysis were excluded.

The survey gathered basic demographic data (age, gender, residency year, race / ethnicity, training institution, clinical year, specialty, type of medical degree, years between undergraduate and medical school, and additional degrees (ie, MPH, PhD, MBA), prior careers before medical school, career plans after graduation) (see Appendix A).

Financial confidence

The financial confidence of the participants before, immediately after, and 18 months following the seminar were analyzed. Survey questions were categorized under one of three classifiers- 1) general financial knowledge, 2) financial management and 3) financial literacy. Financial literacy questions were further classified into one of five topics 1) budgeting, 2) debt and mortgage 3) investment and retirement 4) work / employment related literacy 5) asset optimization and protection.

Financial stress

Six (6) survey questions were developed through a collaborative and iterative process where the financial education team discussed, and pre-tested survey questions several times over the course of development. It was determined that we would create a survey that focused more specifically on markers of stress of financial origin (SOFO) to assess the role of financial confidence with anxiety and wellness both in and out of the workplace. The most common themes to emerge from this process and inform the survey questions included freedom to engage in physician and patient advocacy, familiarity, and comfort with finance topics to avoid stress, and concerns about exploitation from others (ie employers, administrators, financial advisors).

Statistical analysis

Univariate analysis was performed using frequencies to describe characteristics of course participants. The pre- and post-course scores and the pre- and 18-month follow up scores obtained from the administered pre, post-, and 18-month follow-up course surveys were compared using paired t-tests. Mean percent change was calculated for each pre- and post-survey or pre- and 18-month survey item to derive the magnitude of change that occurred between before, after, and 18 months following the educational workshop. For the stress measure utilized as a categorical outcome for subsequent un-conditional logistic regression, we referred to this change variable as stress of financial origin (SOFO).

The following financial confidence classifiers were included in the SOFO variable: 1) general financial knowledge; 2) financial management; 3) financial literacy-budget; 4) financial literacy-debt and mortgage; 5) financial literacy-investment / retirement; 6) financial literacy-work / employment; and 7) financial literacy-asset optimization and protection. The aggregate of all the questions in each of the seven domains was calculated during the pre- and post-intervention and 18-month follow-up period. Also, the percent mean change from the pre-, post-, and 18-month follow-up was computed and was then dichotomized as low or high yield based on the median score; values less than or equal to the median score were categorized as low financial confidence and values above the median score were characterized as high financial confidence.

To derive adjusted estimates for the association between financial confidence and SOFO, we conducted unconditional logistic regression and loaded onto the model the following variables: age categorized as 25–34 and 35–44 age; race / ethnicity re-grouped into Non-Hispanic (NH)-White and other; gender was re-grouped into male and female by eliminating the single “unknown” response category. The following variables were removed from the analysis: seminar mandated by residency program; own a car; lease a car; own a house; clinical year; degrees; additional degrees; and having any career outside of medicine for more than 2 years. The logistic regression model considered percent change in SOFO from the pre-intervention to post-intervention period and then the pre-intervention to the 18-month follow-up period as the outcome variable while financial confidence as the exposure. The model was adjusted for demographic characteristics that were statistically significant from bivariate associations. Statistical significance was defined as p-value < 0.05. All analyses were run using R (Version 4.0.4) and RStudio (Version 7.1.554).

Results

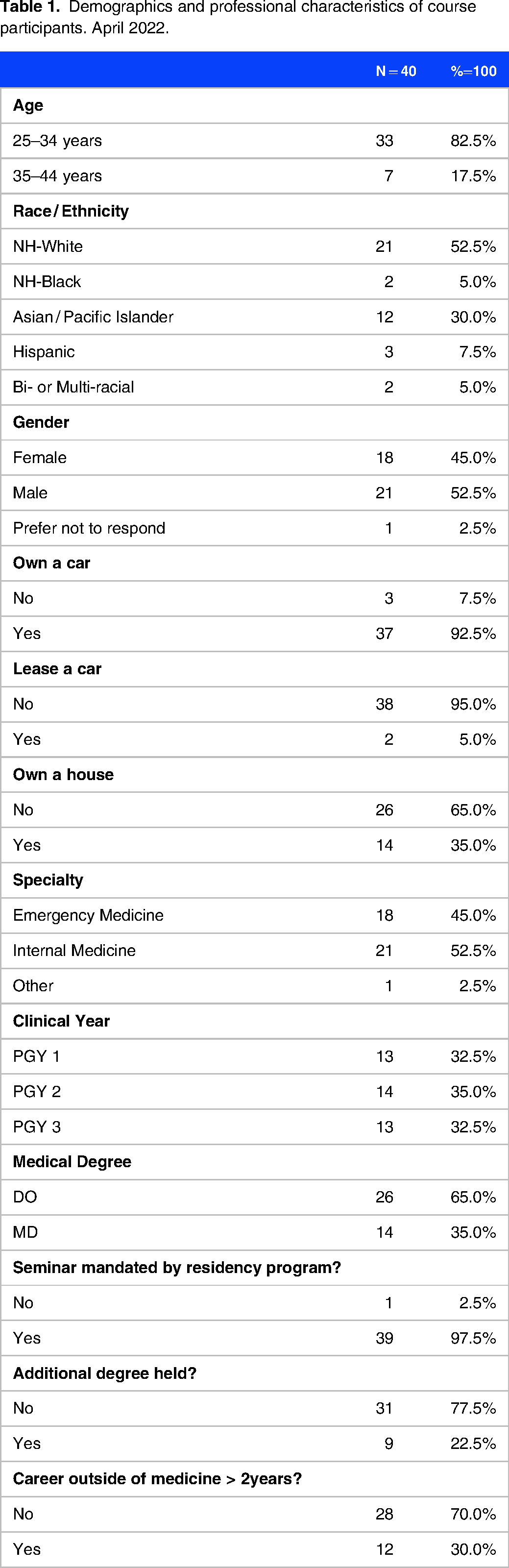

A total of 50 medical residents were enrolled in the course and 40 participants completed both pre- and post-course evaluation and were included in the pre- / post-analysis. Nineteen (19) residents completed the pre-, post-, and 18-month surveys. An additional eight residents completed the 18-month follow-up survey, but only completed either the pre- or post-survey and not all three surveys (pre-, post-, and 18-month follow-up) and were excluded from the analysis. In the pre-post-analysis, of the 40 analyzed participants, thirteen (13) or 32.5% of participants were PGY1, fourteen (14) or 35.0% were PGY2, and thirteen (13) or 32.5% were PGY3 residents. An overwhelming majority were under 35 years of age (n = 33 or 82.5%) and over 80% were non-Hispanic White (NH-White) or Asian / Pacific Islanders. There was a slight over-representation of males at 52.5% (compared to 45.0% of females) and a strong majority (over 90%) owned a car although only about a third owned a home. Both institutions were about equally represented and nearly all course participants were medical residents from either EM or IM (over 97%). Most possessed the MD medical degree variant compared to the DO medical degree with about 22% holding an additional advanced degree (above the bachelor's level), and overall, less than a third had experienced a career outside the medical profession (Table 1). Only part of the demographic information data was collected for the 18-month follow-up to aid in survey matching, if required.

Demographics and professional characteristics of course participants. April 2022.

The level of self-reported financial literacy before, after, and 18-months following the seminar expressed as mean (± SD or standard deviation) and seven financial confidence domains were assessed as follows: General financial knowledge; Financial management; Financial literacy-budgeting; Financial literacy-debt and mortgage; Financial literacy-work/employment; Financial literacy- investment and retirement; Financial literacy- asset optimization and protection. (Table 2 and Figure 2). The maximum score attainable for each item was five (5) points and the minimum was one (1). Pre-, post-, and 18-month follow-up scores were highest for the financial literacy-budgeting domain that evaluated confidence about budgeting. As a result of this narrow variance between the pre- and the post-score and the pre- and 18-month follow up score, the budgeting domain also registered the least impact of the course with 9.6% mean change between pre- and post-and 14.6% between pre- and 18-month follow-up. On the other hand, the impact immediately after the seminar was most remarkable on three subdomains all residing in the financial literacy-work / employment domain. The greatest impact (mean change) in the pre- to post-evaluation was found for the subdomain that assessed physician confidence in work benefits available to physicians with over 80% mean change. This was closely followed by confidence about variance in taxes related to forms of employment entities (79.8%) and confidence about legal business entities that could be used in medical entrepreneurship (79.1%). In the 18-month follow-up, participants report the most confidence in knowing who should be on their financial team, under the financial management domain (68.09%). This is followed by persistent confidence increase in the work / employment domain, where the mean change for all subdomains in this category was at least 50%. Most domains between pre- and 18-month follow up reported a statistically significant increase in confidence levels, except for subdomains in the general financial knowledge section around knowing how to make good financial decisions in the future (p = 0.48) and how to manage their own finances in general (p = 0.56). There was also no difference between pre- and 18 month follow up confidence levels in the financial literacy- debt and mortgage category, specifically feeling comfortable finding a home and securing a mortgage (p = 0.26) and deciding when to buy a home (p = 0.43). Finally, at 18 months, there was also no difference in the course improving the resident's understanding of how to get passive income (p = 0.11) and familiarity with taxes they are supposed to pay.

Graphic representation of seven financial confidence domains of resident participants pre, post, and 18-months following the course. St Joseph's-Stockton, CA and Mercy One-Des Moines, IA Medical Centers.

Financial confidence of the participants pre, post, and 18-months following the course. St Joseph's-Stockton, CA and Mercy One-Des Moines, IA Medical Centers.

Note: (1) the higher the score the lower the level of burnout. (2) a percent mean change = ((post mean-pre mean) / (pre-mean))*100

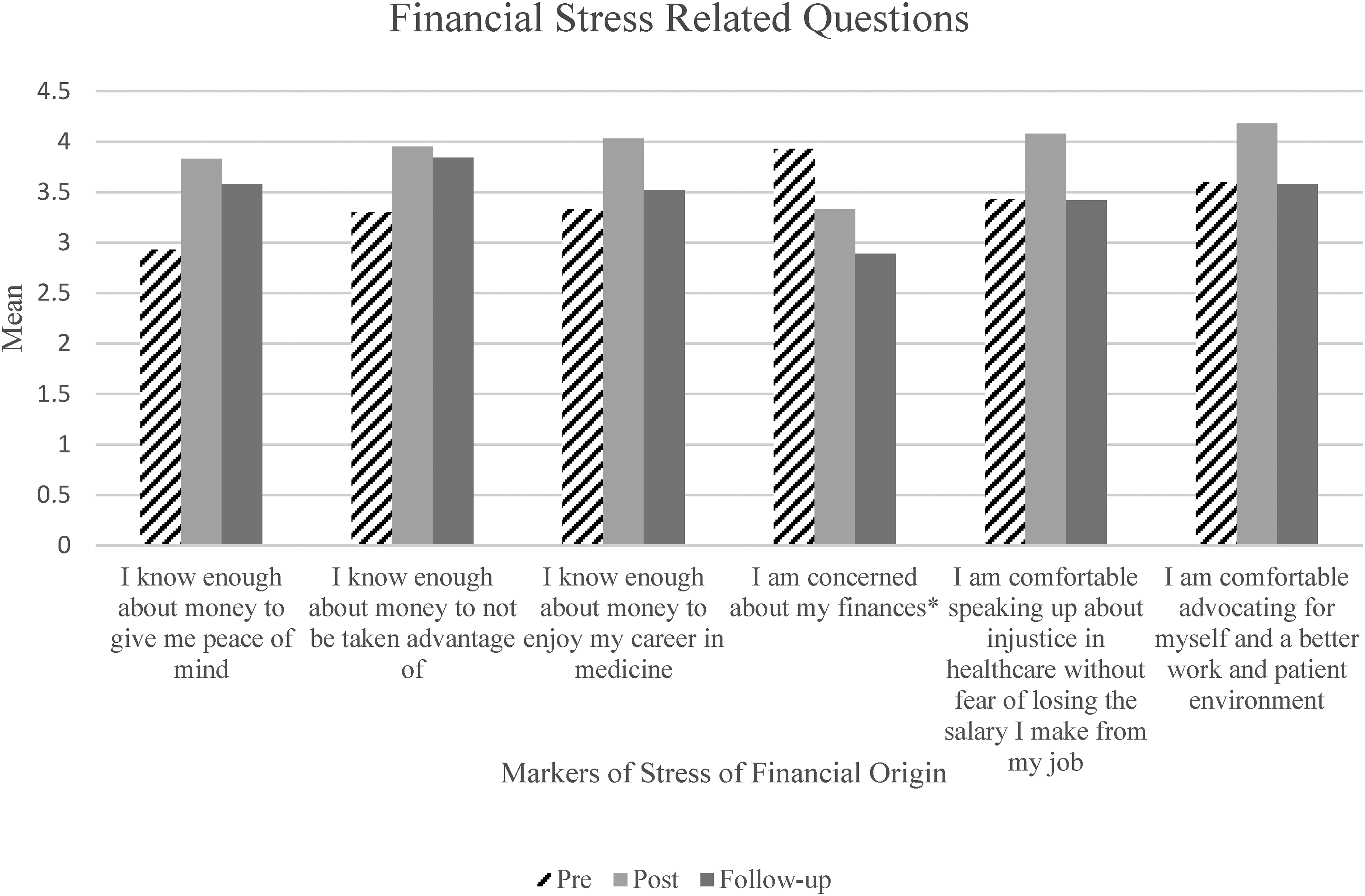

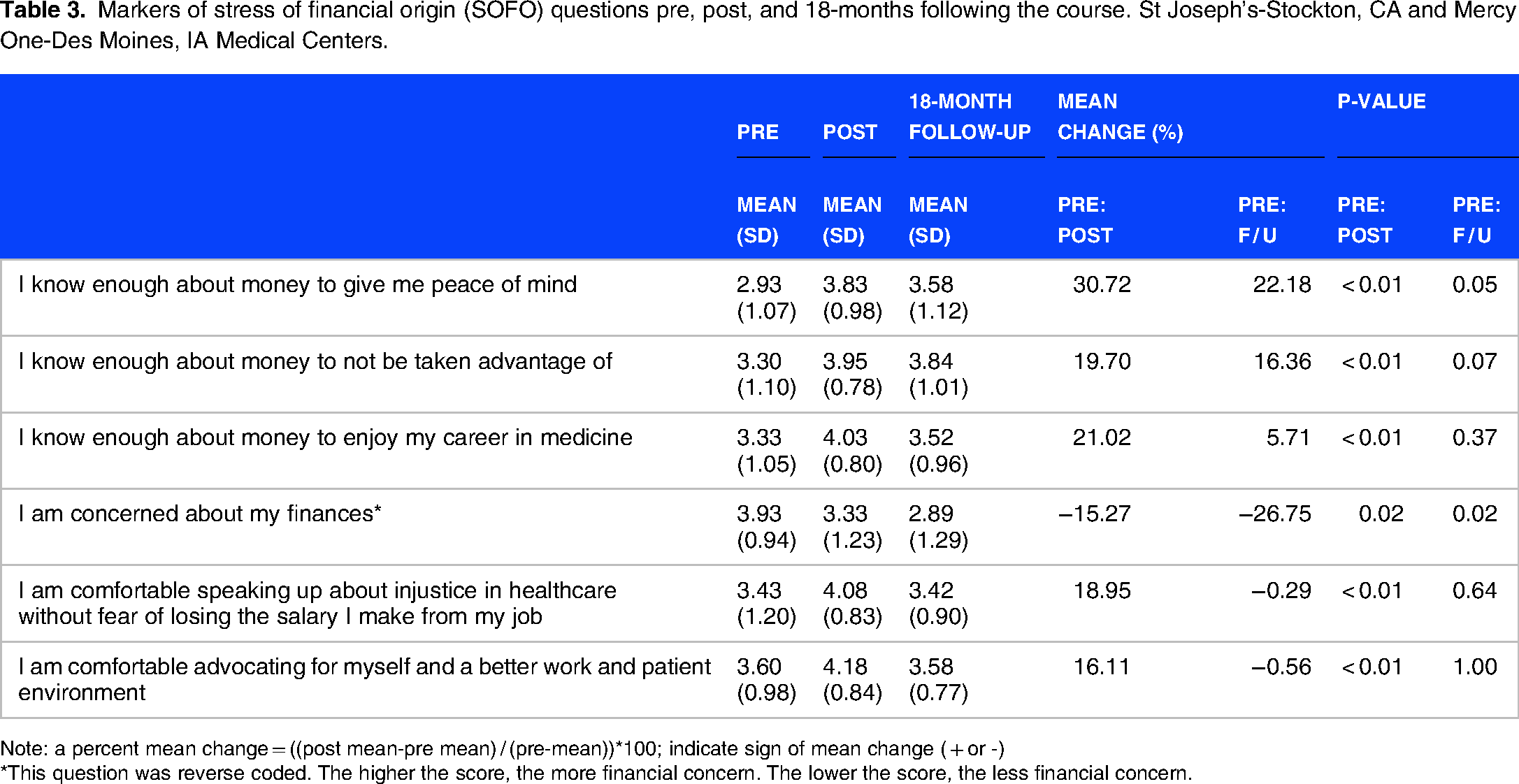

We present findings of stress related to finances before, after, and 18-months following the course (Table 3 and Figure 3). The lower the stress scores, the greater the level of stress. The mean change column captured the magnitude and direction of the impact of the financial literacy intervention on stress. The lowest mean stress pre-score (and therefore, the highest level of stress at baseline) was 2.93, which was related to the item “I know enough about money to give me peace of mind” while the lowest immediate post-intervention stress score (ie, the highest level of stress post-intervention) was 3.33 in relation to concerns about current finances. It is notable that this stress domain was recorded as having the highest level of stress pre-score (3.93) as well. Post-intervention stress score was highest at 4.18, which was observed for the domain that assessed “self-advocacy and a better work and patient environment”. Immediately post the course, the seminar had a positive impact in all domains (from lower to higher scores) (p < 0.01-0.02). The domain related to the item “I am concerned about my finances” was reverse coded and decreased significantly and substantially after the intervention from a score of 3.93 at baseline down to 3.33 post-intervention (p = 0.02).

Graphic representation of six markers of stress of financial origin (SOFO) questions pre-, post-, and 18-months following the course. St Joseph's-Stockton, CA and Mercy One-Des Moines, IA Medical Centers. *This question was reverse coded. The higher the value, the more financial concern. The lower the value, the less financial concern.

Markers of stress of financial origin (SOFO) questions pre, post, and 18-months following the course. St Joseph's-Stockton, CA and Mercy One-Des Moines, IA Medical Centers.

Note: a percent mean change = ((post mean-pre mean) / (pre-mean))*100; indicate sign of mean change ( + or -)

*This question was reverse coded. The higher the score, the more financial concern. The lower the score, the less financial concern.

At 18 months, participants reported statistically less concern about their finances (p = 0.02). The domains of knowing enough about money to give peace of mind (p = 0.05) and not be taken advantage of (p = 0.07), showed persistent improvement, but did not reach statistical significance. The increased scores immediately post the course were not maintained at 18-months for knowing enough about money to enjoy a career in medicine (p = 0.37), speaking up about healthcare injustice (p = 0.64), and advocating for a better work and patient environment (p = 1.00).

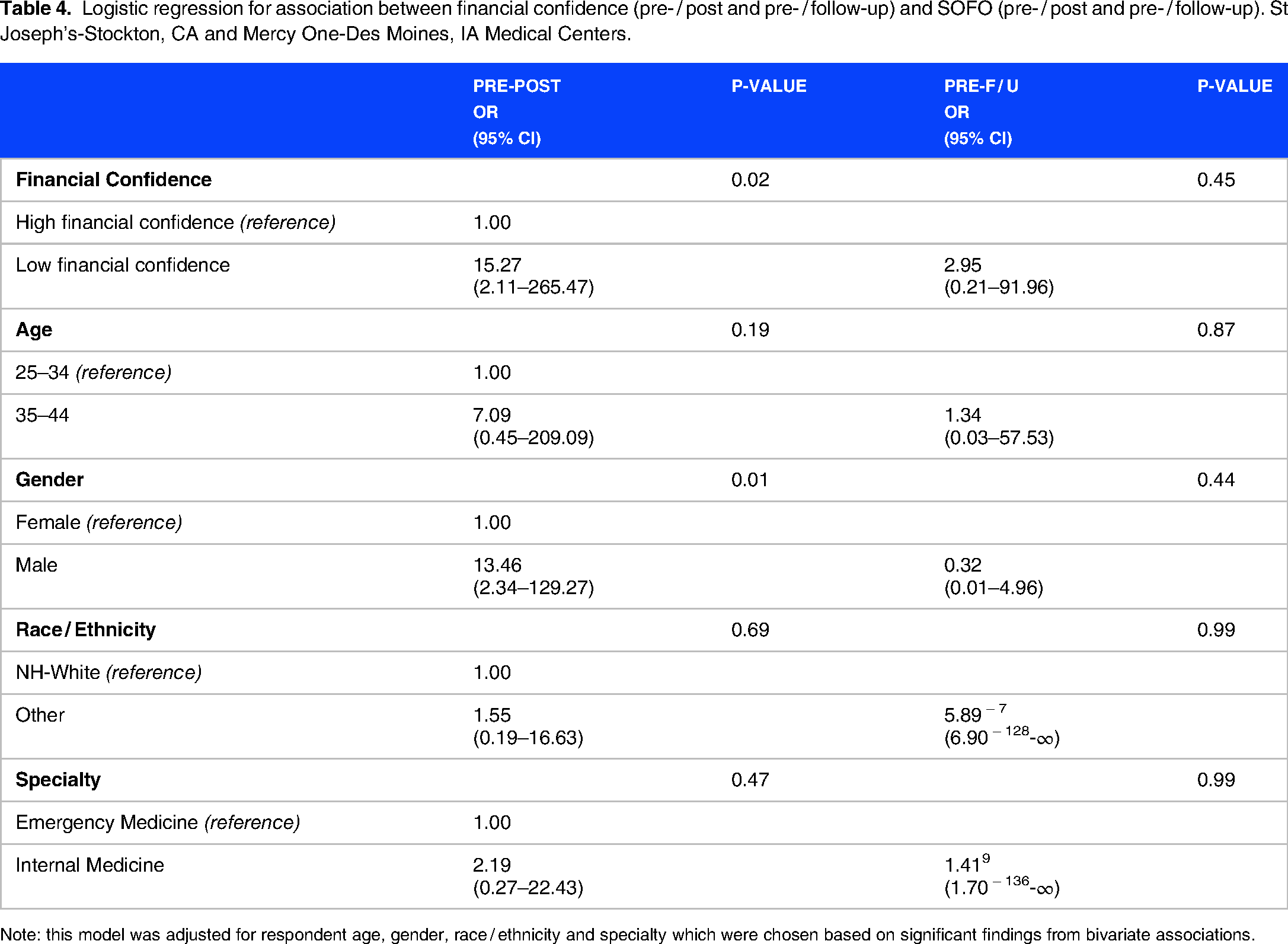

The percent change in SOFO from pre-, post-, and 18-months following the intervention as the outcome variable was also analyzed (Table 4). This table shows the results of the unconditional logistic regression analysis for the association between financial confidence and other selected socio-demographic characteristics with SOFO. We noted a strong association between financial literacy in general and SOFO in the immediate post-analysis. Medical residents with low financial confidence were more than fifteen times as likely to experience SOFO compared to their counterparts with higher financial confidence (p = 0.02). Another strong predictor of SOFO was gender with males having a significantly greater likelihood of SOFO than females (p = 0.01). Although we found a trend of higher risk level for SOFO among older medical residents and NH-Whites, the results were not statistically significant (older medical residents: p = 0.19; NH-Whites: p = 0.69).

Logistic regression for association between financial confidence (pre- / post and pre- / follow-up) and SOFO (pre- / post and pre- / follow-up). St Joseph's-Stockton, CA and Mercy One-Des Moines, IA Medical Centers.

Note: this model was adjusted for respondent age, gender, race / ethnicity and specialty which were chosen based on significant findings from bivariate associations.

At 18 months, the relationship between financial confidence and all socio-demographic domains showed no statistically significant change compared to before the intervention.

Discussion

Physician stress is recognized as a factor conditioning the performance of the health system given its effect on optimal patient care, patient experience, health outcomes and the overall costs of health.

Among the multiple causes of stress in medical trainees, financial stress is associated with decreased mental well-being and can measurably impact medical residents’ performance and work satisfaction. Most medical residents face financial stress, often resulting from accumulated educational debts and the economic costs of life decisions such as starting a family, choosing post-residency fellowship or employment, buying a home and costs of relocation, licensure exams, and preparation materials. This pilot program emphasizes the positive effects of introducing financial education to medical residents as a potential stress mitigation strategy, especially immediately post intervention. By reducing concerns about finances, our findings suggest that shortly after our financial course, residents may be able to function in and out of the workplace with more peace of mind, less concern about being taken advantage of in their jobs and by financial professionals, feel more empowered to speak about injustices in healthcare, and encouraged to advocate for a better work and patient environment without fear of financial repercussion. The positive findings immediately post course coincide with the positive results from previous qualitative studies where participants commented that managing debt and retirement can aid in stress mitigation.26,27

At 18 months, financial confidence levels in many of the domains significantly improved from pre-intervention, but less than immediately post-intervention, suggesting the need for continued educational engagement over time. The stress mitigating effects of the course waned significantly by the 18-month follow up, suggesting the need for more consistent, longitudinal educational interventions to maintain the positive impact on SOFO as seen immediately post the course.

The course was created by physicians, for physicians with the input of attending and resident physicians from two different specialties in two different regions of the country. The entire course was useful for resident learners and was extensively researched and carefully developed. By exploring the degree of self-reported confidence gained in each literacy domain, this course structure may offer helpful guidance for residency leadership and financial curriculum developers as to what content may be most useful for medical residents. Moreover, though most content demonstrated notable financial confidence benefit to the residents in the post-intervention and 18-month follow up periods, with limited educational time in residency, this program offers insight into what areas can be offered in an abbreviated curriculum given what residents are more comfortable with, such as budgeting, compared to areas of unfamiliarity and discomfort such as working with financial professionals, exploring work and employment related benefits and business entities, and optimizing assets with the tax code and insurance protection.

This program has several limitations. While it is encouraging to see consistencies between our findings and previous literature, especially immediately post course, there are several factors in our pilot program that may have unforeseen consequences for our data. First, the course was required for participants and delivered on a fixed date at each participating institution. The required nature of the course was incorporated to avoid selection bias from offering this course as an elective experience, but this type of course deployment may not be optimal or feasible for other residency programs. Additionally, with the current one-day implementation design, the results were favorable immediately post intervention, but we suspect that a more longitudinal approach to the content may be more realistic for other institutions and may have yielded different and consistently favorable results, particularly at long-term follow up. Additionally, though we were able to include two programs from two specialties in different parts of the United States, we did not perform a power analysis to justify our sample size. This was primarily because we already knew the number of trainees in our participating residency programs and focused on securing their participation as part of this study. The number of program participants was relatively small and could benefit from analysis of results in a larger cohort of learners. The small population size may impact the reported SOFO odds ratios, could inappropriately result in increased odds of experiencing SOFO, and limit the generalizability of the study. Finally, we used a non-validated survey instrument for the outcomes, but in the future can assess if there is any relationship between our SOFO markers and these established well-being assessments.

Future directions for this program are to offer this course to a larger network of residents within the CommonSpirit enterprise and beyond and evaluate the reproducibility of our results on a much larger resident physician population. We plan to implement a longitudinal approach to curriculum implementation and develop course materials for residents to re-visit over time. We hope this will help with content retention and improved financial confidence over the long term. Furthermore, a program such as this could benefit from the assessment of behavior changes in financial management (ie, opening new accounts, engaging in new investment opportunities, engaging in debt reduction activities, etc) that occur post-intervention as well as evaluating if their advocacy practices have improved over time.

Conclusion

Residents are worried about their finances. They often work long hours and get paid lower salaries than their age matched peers. Despite knowing the significant increase in potential future earnings as an attending physician, the lack of confidence and knowledge on how to navigate the financial space, work with financial professionals, manage debt, and adequately evaluate their work benefits and investment possibilities, among other financial challenges, is a cause for concern for many resident physicians. The promise of making a good salary simply is not enough to manage the financial concerns of physician trainees. Our program evaluation demonstrates that a comprehensive personal finance course can help mitigate some of these concerns, especially in the short term, but to maintain persistent financial confidence and stress mitigation benefits, it may require frequent and consistent education over the long term. Residency programs should invest in education beyond the one day or few-hour seminar session to continue to reap education and well-being benefits over time.

Supplemental Material

sj-docx-1-mde-10.1177_23821205241264697 - Supplemental material for The Impact of a Personal Finance Education Course on Financial Confidence and Markers of Financial Stress among Medical Residents: A Longitudinal Pilot Study

Supplemental material, sj-docx-1-mde-10.1177_23821205241264697 for The Impact of a Personal Finance Education Course on Financial Confidence and Markers of Financial Stress among Medical Residents: A Longitudinal Pilot Study by Tiffany Chioma Anaebere, Maria Guevara Hernandez, D Brian Wood, Deepa Dongarwar, Sylvia Adu-Gyamfi, Joseph Moran, George Idehen, Ethan Luong, Angela Park, Lydia Meece and Hamisu M. Salihu in Journal of Medical Education and Curricular Development

Supplemental Material

sj-docx-2-mde-10.1177_23821205241264697 - Supplemental material for The Impact of a Personal Finance Education Course on Financial Confidence and Markers of Financial Stress among Medical Residents: A Longitudinal Pilot Study

Supplemental material, sj-docx-2-mde-10.1177_23821205241264697 for The Impact of a Personal Finance Education Course on Financial Confidence and Markers of Financial Stress among Medical Residents: A Longitudinal Pilot Study by Tiffany Chioma Anaebere, Maria Guevara Hernandez, D Brian Wood, Deepa Dongarwar, Sylvia Adu-Gyamfi, Joseph Moran, George Idehen, Ethan Luong, Angela Park, Lydia Meece and Hamisu M. Salihu in Journal of Medical Education and Curricular Development

Footnotes

List of abbreviations

Acknowledgements

The authors would like to acknowledge, Julian Mitton, MD, MPH, Brisa Urquieta Hernandez, PhD, and Alisahah Jackson, MD for supporting and reviewing this work; CommonSpirit Health for their support of this project and their commitment to innovative ways to address health equity and physician well-being; Jennifer Oakes, MD, Gabriela Macedo, and the physician and non-physician financial educators for substantial contributions to the successful implementation of our financial education course.

Availability of data and materials

The datasets used and analyzed during the current study are available from the corresponding author on reasonable request.

Authors’ contributions

TCA and MGH were responsible for project conceptualization, administration, supervision, curriculum development, data curation and preparation for formal analysis, and were major contributors in writing the manuscript. DBW was responsible for project conceptualization and administration, supervision, and writing the manuscript. DD and SAG were responsible for data curation and formal analysis, methodology, preparation of figures and tables, and were major contributors in writing the manuscript. JM was responsible for project administration, curriculum development, and writing the manuscript. GI was responsible for project conceptualization and administration, curriculum development, and writing the manuscript. EL, AP, and LM were responsible for project administration and writing the manuscript. HS was responsible for formal data analysis, methodology, providing software, project supervision, and was a major contributor in writing the manuscript. All authors read and approved the final manuscript.

Consent

Course participation was required for all residents, except for those with approved exemptions. Written consent was waived by each institutional research committee due to the study's exempt status, the educational nature of the program, the collection of de-identified data, and the minimal risk to participants. Resident participants voluntarily completed the pre-, post-, and 18-month follow-up surveys.

Ethics statement

Approval for the study was obtained by St. Joseph's Medical Center's Research and Quality Committee (Approval L2021-07-01) and Mercy One Medical Center's Institutional Review Board (Study DM2022-08; Approval L2022-03-15).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and / or publication of this article.

Funding

The authors received no financial support for the research, authorship, and / or publication of this article.

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.