Abstract

Experience with urban social protection programmes is relatively limited in the Global South. Extensions or duplicates of rural social assistance programmes do not reflect the distinct vulnerabilities of the urban poor, who face higher living costs and more precarious employment, and are not reached by social insurance schemes that are designed for formally employed workers. Neither the Sustainable Development Goals nor the New Urban Agenda reflect a specific focus on urban social protection. COVID-19 has exposed this major gap in coverage, given the disproportionate impact of lockdowns on the livelihoods of the urban poor. To ‘build back better’ post COVID-19, we propose rights-based national social protection systems with two components: categorical social assistance for non-working vulnerable groups (children, older persons, persons with disability) and universal social insurance for all working adults (formal, informal or self-employed), financed out of general revenues rather than mandatory contributions by employees and employers. These ideas are explored in the case of South Africa, which has comprehensive social assistance but inadequate social insurance for urban informal workers.

Introduction

More than half the world’s population now lives in urban areas, but most social assistance programmes in the Global South were designed for rural areas (UNDP 2019; World Bank 2020a). This apparent contradiction is the result of a historically complex interplay of colonial and post-colonial politics, path dependency, humanitarian considerations and technological change (Varshney 1993). Especially in sub-Saharan Africa and South Asia, contemporary cash transfer programmes often evolved from food aid interventions that were originally introduced to mitigate rural food insecurity (see Lavers [2020] on ‘the agrarian origins of social assistance in Ethiopia’). Substantive differences prevail in the composition of social protection between urban and rural areas. The coverage rate of social insurance and labour market interventions is more than double among the urban poor than the rural poor, but these programmes currently reach only a tiny fraction of the urban poor, typically 3–4% (Gentilini, 2015). This is because self-employed, informally employed and unprotected low-income formal sector workers are excluded from both pillars of social protection systems, namely social assistance and social insurance (as discussed in the next section).

Informality is not the only challenge to urban social protection. The complexities of urban poverty require particular attention. Satterthwaite and Mitlin (2013: 1) argue that ‘the scale and depth of urban poverty in Africa and much of Asia and Latin America is greatly under-estimated because of inappropriate definitions and measurements’ and that this ‘may be one reason why so little attention has been given to urban poverty reduction’. Urban poverty is more complex because multiple aspects of deprivation beyond low and variable incomes need to be considered, including poor quality and overcrowded housing; inadequate water supply and sanitation; inadequate access to basic services such as health care and child-care; high prices for necessities such as food; voicelessness and powerlessness within local political and bureaucratic structures; and ‘limited or no safety nets for those with inadequate incomes’ (Satterthwaite and Mitlin, 2013: 1). These challenges are becoming more pressing as urbanization accelerates globally, and a push for universal social assistance gains momentum on grounds of both efficiency (lower administrative costs than poverty-targeted programmes) and equity (social protection as a human right for all) (ILO, 2017). Furthermore, urban vulnerabilities are highly gendered. The proportion of women working in informal non-agricultural employment is often much higher than men. Women are thus less likely to be eligible for social protection, and their specific life cycle needs and risks (for example reproductive health, maternity leave, child-care) are less likely to be covered by social insurance (Holmes and Scott, 2016).

There has been much progress in the urbanization of social protection in recent decades. Only one of the five largest safety nets worldwide, India’s Mahatma Gandhi National Rural Employment Guarantee Scheme, is exclusively rural. The other four (China’s Dibao, Brazil’s Bolsa Familia, India’s Mid-Day Meal Scheme and South Africa’s Child Support Grant) extend to urban populations. Around 40% of participants in Mexico’s flagship safety net programme, Prospera, live in urban and peri-urban areas, up from 7% in the late 1990s. Yet fewer poor urban people than poor rural people have access to social protection, worldwide. In the Global South, 23% of the poorest households are covered by a safety net programme in rural areas, a low figure which nonetheless exceeds coverage of 16% in urban areas (Gentilini, 2015). The need for expanded urban coverage of social protection, without neglecting rural needs, is undeniable.

COVID-19 further exacerbated these disparities. COVID-19 lockdowns confined millions of people across the world to their homes without income for several months. Low-income urban populations were disproportionately affected, prompting interventions by governments that blended social protection and humanitarian responses. Gentilini, Almenfi, et al. (2020) estimate that 0.4% of global GDP, or $5.68 trillion, was allocated to COVID-specific social protection interventions in 2020, comparable to the global social protection response during the 2007–08 financial crisis. These aggregate numbers conceal wide variation across countries. The average per capita social protection response to COVID-19 ranged from $123 in high-income countries to a mere $1 in low-income settings (Gentilini, Almenfi et al., 2020). Just as COVID-19 lockdowns disproportionately affected the poor, so protection against the impacts of global lockdowns was lowest in countries that had the least capacity to provide effective and timely relief.

In addition to the limited experience of many low-income countries with urban social protection, COVID-19 has exposed a glaring gap in provision: the lack of social insurance for low-income workers in both the formal and informal sectors. High- and upper-middle-income countries introduced COVID-specific measures to support vulnerable workers during lockdowns, such as the Paycheck Protection Program (United States), the Self-Employment Income Support Scheme (United Kingdom), the Temporary Employee Relief Scheme or TERS (South Africa) and the Subsidy to Workers’ Payroll (Colombia). These stopgap measures highlight the limited coverage of social insurance schemes: benefits accrue only to formally employed workers who pay contributions, against which they can claim partial replacement of their lost income when they are not working.

This article advocates for a rights-based approach to social insurance, drawing on learning from COVID-19, which has the distinctive feature of delinking entitlements from workers’ contributions. Urban-sensitive social protection needs to reflect the distinct vulnerabilities of the urban poor, who face higher living costs and more precarious livelihoods. Social insurance should be universalized to all workers, with no discrimination between salaried (formal) and non-salaried (informal or self-employed), and it should be financed out of general revenues, not by taxing workers’ earnings. These ideas are explored in the case of South Africa.

The main message of this article is that social protection in urban contexts needs to be reconceptualized and redesigned, not just extended from rural villages into urban informal settlements, to better reflect the nature of urban poverty. This is even more urgent in a COVID-19 and post-COVID-19 world. Designs of urban social protection that fail to account for higher living costs, higher levels of informality and unemployment, low and variable incomes, gendered and life cycle vulnerabilities and variable access to adequate basic services would have limited success, even in a world without COVID-19.

Section 2 explores why social protection often lacks an urban lens and why this matters under COVID-19 conditions. Section 3 analyses why an urban lens is needed to protect urban residents more effectively. Section 4 describes how social protection could be redesigned to become more urban-sensitive. Section 5 applies these arguments to South Africa—whose comprehensive social assistance system nevertheless epitomizes the glaring gaps found across the world in terms of under-coverage of informal urban workers—and estimates the cost of such an overhaul. Section 6 concludes the article.

Does Social Protection Lack an Urban Focus?

In its narrowest and popularly understood sense, social protection can be defined as a range of interventions intended to provide income support to people living in poverty, either temporarily or permanently. A comprehensive social protection system guarantees income security and access to basic services to everyone throughout the life cycle—children, people of working-age and older persons (ILO, 2012). There are two basic pillars: social insurance and social assistance. Social insurance refers to contributory social security schemes for formally employed workers, such as pension funds and unemployment benefits, and is the main form of social protection for working adults. Social assistance describes non-contributory cash or in-kind transfers, usually targeted at the non-working poor, especially children, older persons and persons with disability. Broader definitions of social protection include active labour-market interventions for the working poor such as youth wage subsidies and skills training (World Bank, 2012), pro-poor or universal access to basic services like education and health care (UNICEF, 2012), and ‘transformative’ social justice measures such as anti-discrimination campaigns underpinned by legislation (Devereux and Sabates-Wheeler, 2004).

The first question this article addresses is whether these pillars adequately capture the specific needs of the urban poor, both in general terms and during COVID-19 times. Our answer is that existing social protection frameworks do not, because they have not placed urban issues as a core focus, neither historically nor currently.

The origins of contemporary social protection systems can be traced back to the Poor Laws of 16th-century England. However, the foundations of the modern welfare state were laid in 19th-century Europe (Polanyi, 1944). During the Industrial Revolution, livelihoods shifted away from agriculture and towards manufacturing and services, accelerating rural-to-urban migration. Urban workers increasingly depended on wages and markets to feed their families. Rural communities generally supported their vulnerable members and developed risk-pooling and community-based redistribution mechanisms. But these social networks and informal forms of social assistance and insurance unravelled in towns and cities. State-run social protection emerged to fill this gap (Midgley, 1997).

Over time, modern social welfare systems evolved that are characterized by regular cash transfers given to citizens identified as poor by the state, financed through taxation. Social welfare or social assistance is complemented by social security or social insurance, which protects workers who have formal public or private sector contracts against disrupted income caused by breaks in employment. Social insurance typically draws on tripartite funding, with contributions from employers, employees and government. Crucially, social insurance does not reach the informal sector and non-contributing self-employed workers. In most low-income countries, formal employment and hence social protection coverage are limited (ILO, 2017). Most people depend on limited informal support mechanisms, which are inadequate against major shocks such as COVID-19 lockdowns.

In the early 1990s, when first-generation cash transfer flagship programmes were being designed, 57% of the global population and 80% of the global extreme poor lived in rural areas (Castañeda et al., 2018). As a result, the evolving social protection agenda in the Global South is not yet sufficiently urban-sensitive. First, social protection is rarely specifically highlighted in urban policy statements and programming. Second, national programmes usually fail to recognize the specificities of urban poverty and vulnerability. One reason for this is the lack of such commitments globally. No mention of city dwellers or urban contexts is associated with social protection in the Sustainable Development Goals (SDGs). Conversely, the SDG dedicated to urban wellbeing (SDG 11: ‘make cities and human settlements inclusive, safe, resilient and sustainable’) makes no mention of social protection. Neither did the New Urban Agenda (NUA) focus on social protection (UN-Habitat, 2016). Yet poverty and inequality within urban areas are often extremely high (Glaeser et al., 2009), and access to public services in cities and towns is a critical determinant of wellbeing. A rights-based approach to social protection would be well-aligned with the NUA and the ‘right to the city’ agenda (Mayer, 2009). The right to social protection often does not extend to informal workers, who make up more than half the urban workforce in the Global South, rising to over 80% in south Asia (Vanek et al., 2014).

Interestingly, the design of social protection in the Global South has converged towards European-style social welfare (Devereux, 2013). One driver of the recent surge in popularity of social protection programmes was growing disillusionment with the delivery of food aid to sub-Saharan Africa and South Asia. Recognizing that humanitarian relief is inadequate against recurrent shocks, that projectized food aid (for example, food-for-work projects and school feeding schemes that use imported food) undermines local food producers and traders, and that social insurance does not reach the rural poor, agencies such as the World Food Programme (WFP) shifted to ‘food assistance’ programming, which includes cash-based transfers (WFP, 2010).

Following protracted debate (see Gentilini, 2016; Tappis and Doocy, 2018), cash transfers are now preferred almost universally to food transfers, even during food crises (Hoddinott et al., 2014; Office for the Coordination of Humanitarian Affairs [OCHA], 2018). However, working-age adults are generally overlooked in targeting of social cash transfers, and the needs of the urban poor remain relatively neglected (Asian Development Bank, 2016; Gentilini, 2015). Frameworks like the ILO’s social protection floor (ILO, 2012) do acknowledge, on paper, the importance of urban specificities. UNICEF’s Social Protection Strategic Framework outlines urban-specific poverty and vulnerabilities and key issues for urban programming, such as targeting and transfer size (UNICEF, 2012). The World Bank’s Social Protection and Labour Strategy emphasizes the need to protect informal workers from shocks that manifest differently in urban areas (World Bank, 2012). But these good intentions have not yet been adequately operationalized.

This operational gap has become more salient in the context of COVID-19. The economic impact of the pandemic is far-reaching, with an estimated contraction in the global economy of 4.9 percentage points (IMF, 2020) and a projected increase in extreme poverty of 71–100 million people (Mahler et al., 2020). The new poor are more likely to live in urban areas because high-density communities experienced rapid spread of the virus and have higher concentrations of essential services that were severely affected by closures and of workers affected by layoffs and declining economic activity.

COVID-19 does not affect everyone equally (Cuesta and Pico, 2020). This is particularly true with respect to the nature and composition of jobs. In low- and lower-middle-income countries, informal workers represent 85–88% of total employment (ILO, 2020). Low-income countries have fewer jobs that can be done from home (Dingel and Neiman, 2020). Small- and medium-sized businesses are expected to fail first from lack of revenue, capacity to quickly adapt business or eligibility of recovery programmes, such as payroll subsidies or credit lines, that are strongly geared to formal firms (Dutta et al., 2020; Cuesta and Pico, 2020).

Globally, three-quarters of informal workers—about 1.6 billion people—lived in countries with partial or full lockdowns in 2020, with youth and women over-represented in the most hard-hit sectors (ILO Monitor, 2020). Initial estimates suggested a 60% drop in the income of informal workers (ILO, 2020). A survey in Bangladesh found that between March and April 2020, the average income of respondents fell by 75% in urban slums and by 62% in rural areas (Bangladesh Rural Advancement Committee, 2020). Simulations in Colombia for the year 2020 suggest that 78% of the new poor attributed to COVID-19 were informal workers and 82% resided in urban areas (Cuesta and Pico, 2020).

In addition, COVID-19 has had gendered effects, both within and outside labour markets. Women make up over 70% of the global health and social workforces (Boniol et al., 2019), frontline jobs that increase their likelihood of contracting COVID-19 (CARE, 2020a, 2020b). Women are disproportionally employed in sectors hit hardest by the pandemic, including entertainment, retail, tourism, travel and smallholder farming, as well as in the informal economy and as migrant workers. Women entrepreneurs face uneven adversity in rebuilding their livelihoods as they may face more unfavourable conditions, such as decreasing access to financial services.

The Case for Universalized Social Insurance

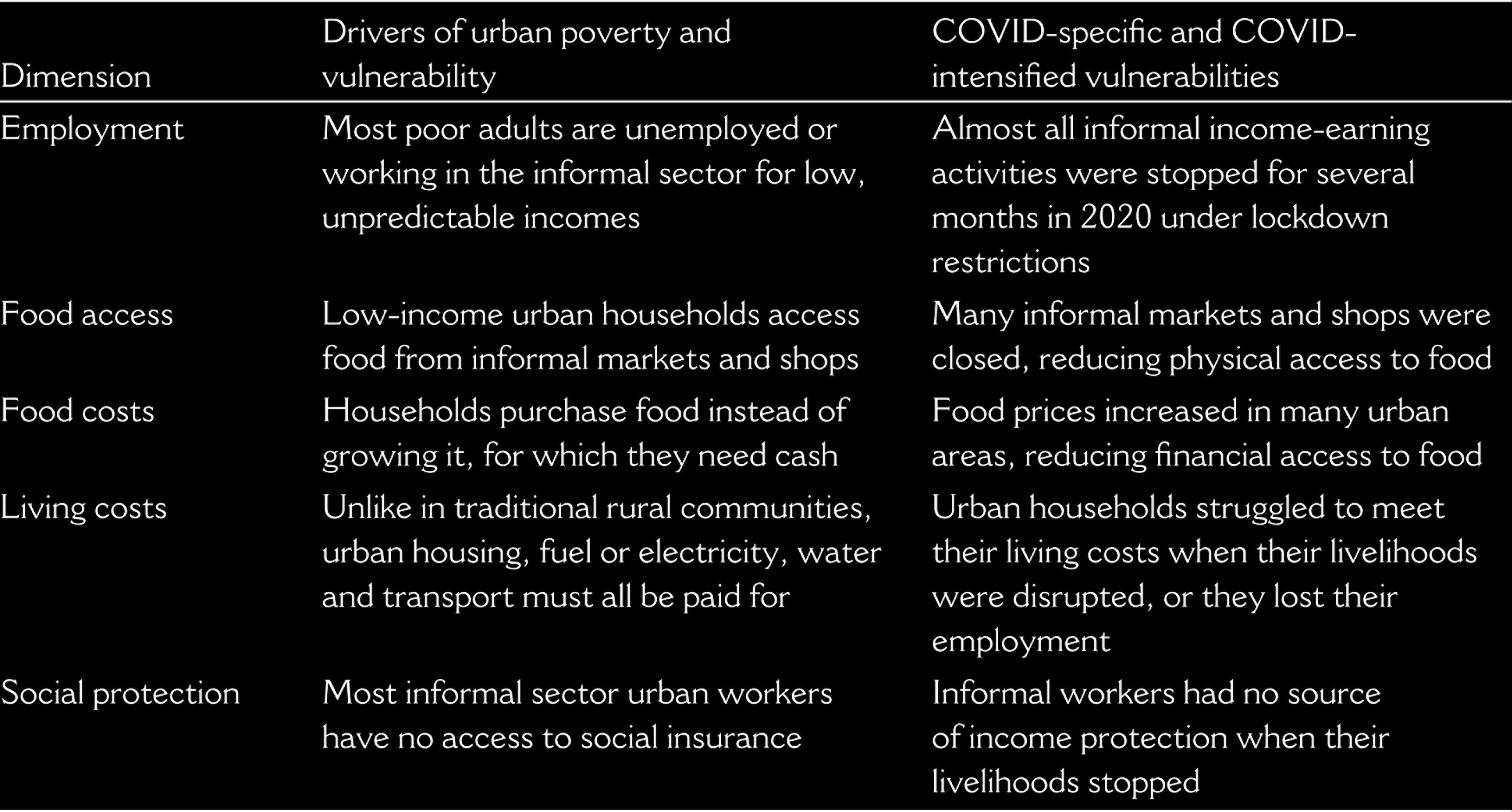

A critical starting point for designing urban social protection differently is the recognition that urban poverty and vulnerability differ from rural contexts (see Table 1, ‘drivers’ column). For instance, while the rural poor in Africa work mostly in agriculture, the urban poor are either unemployed or work in the informal sector, whether self-employed or employed by others in micro-enterprises. Across African countries rural residents have higher poverty rates, but the gap between urban and rural areas is declining—from 35 percentage points to 28 percentage points between 1996 and 2012 (Beegle et al., 2016).

COVID-Specific and COVID-Intensified Urban Poverty and Vulnerabilities

COVID-Specific and COVID-Intensified Urban Poverty and Vulnerabilities

Food security is precarious in urban areas for people who do not grow their own food but depend on markets. For this, they need to earn income, but incomes in the informal sector are low, irregular and unpredictable. Food prices also rise, sometimes rapidly. During the global food price crisis of 2007–08 prices of staple cereals doubled in some places and the number of food insecure people increased by more than 100 million globally, a high proportion of whom lived in urban areas (ACF, 2009; Ivanic and Martin, 2008). Cuesta et al., (2010) reported that food price increases led to dramatically higher increases in poverty among urban households across the Andean region. The poverty impact in 2008 was significantly higher in urban than rural households, by up to 9.5 percentage points in Bolivia.

Urban costs of living are generally higher than in rural areas because many expenditure items that are free or cheap in rural areas, such as fuelwood, water and housing, and must be paid for in urban areas. Other basic living costs are incurred more often in urban areas, such as electricity, transport and rent, as are business-related expenses like permits, bribes and facilitation fees. Additionally, urban household members may eat more food away from home, and households may decrease in size or change in composition, for example, becoming mono-parental families (Guven and Leite, 2016). In several countries, including China, India and Indonesia, poverty estimates differentiate between rural and urban populations and different price indices are applied to estimate poverty headcounts (World Bank, 2017). Ravallion et al. (2007) report that, on average, the urban poverty line is 5% higher than the rural poverty line in Eastern Europe and Central Asia, 29% higher in Sub-Saharan Africa, and 44% higher in Latin America and the Caribbean.

Against this backdrop, we argue that a rights-based universalized social insurance covering all workers is an effective response both generally and against covariate shocks such as COVID-19. We argue that urban-sensitive social protection is needed to address the specific vulnerabilities of poor urban residents. Table 1 (COVID vulnerabilities column) substantiates this argument. During the pandemic and consequent lockdowns, urban informal workers were more vulnerable to disruption of economic activities, they had limited ability to cope with the socioeconomic consequences of the pandemic as they enjoyed less social protection, and they were particularly affected by rising food prices in non-food producing urban areas. Those arguments are supported by emerging literature on the effects of COVID-19 across the world (Adams-Prassl et al., 2020; Chetty et al., 2020; Furceri et al., 2020). This evidence mostly refers to vulnerabilities and impacts during previous pandemics and severe global shocks (Barro et al., 2020); as well as real-time evidence from phone surveys or administrative data on unemployment claims (Adams-Prassl et al., 2020). A third source of evidence comes from microsimulations that project the effect of the pandemic on labour markets, across formal and informal sectors, and in urban and rural contexts (Cuesta and Pico, 2020).

While social protection has adjusted to respond to COVID-19 globally, it has not done so equally across urban settings (vs. rural) nor among informal (vs. formal) workers. During 2020, at least 195 countries introduced social protection measures in response to COVID-19 (Gentilini, Almenfi et al., 2020). Social assistance accounts for most of the social protection response. Among those, cash transfer programmes are most common (about 50% of new social assistance programmes), with a short duration and relatively generous in size (on average, an additional three months and doubling of benefits) (Gentilini, Almenfi et al., 2020). Only a small proportion of the total new social assistance interventions (21 out of over 300 in 131 countries) deliberately addressed the particular needs emerging in urban settings, with just one (in Kenya) specifically designed for slum dwellers. Most programmes (14) were cash or in-kind transfers, followed by public works (2), school feeding (2) and utility support (2) (Gentilini, Almenfi et al., 2020).

As for social insurance, Gentilini, Almenfi et al., (2020) report some 263 programmes in 125 countries, led by unemployment benefits, followed by waivers, deferment or subsidization of social security contributions and paid sick leave. Worker-related labour market programmes featured in 140 programmes in 85 countries, with wage subsidies and labour market regulations being the two interventions used most for COVID-19 response. This confirms that informal workers were mostly left out of social insurance responses to COVID-19.

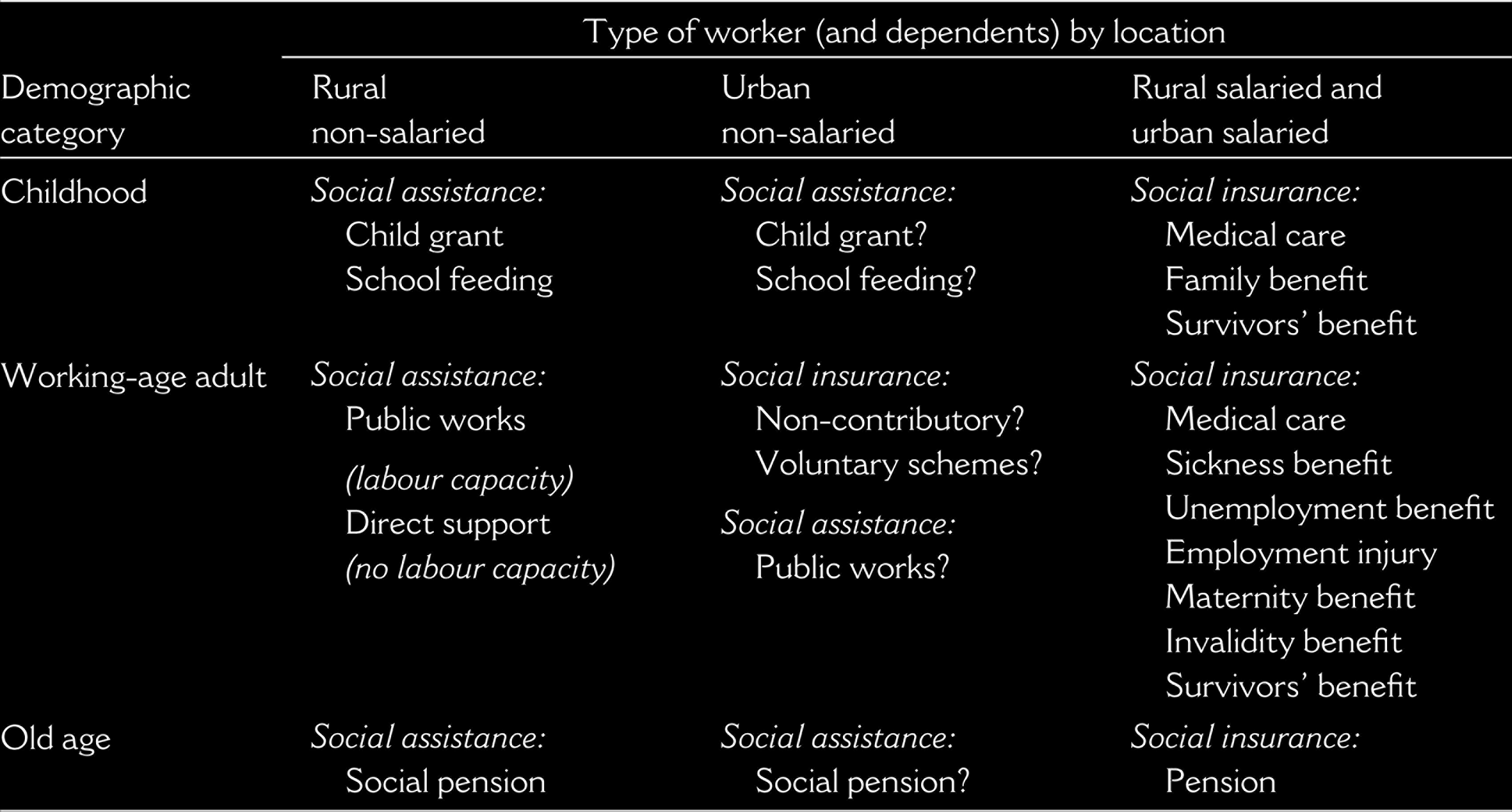

Table 2 further disaggregates beyond rural and urban. From a social protection perspective, it is appropriate to divide urban working-age populations into the salaried (who usually have access to contributory social insurance) and non-salaried (who usually do not). In Table 2, the urban salaried population is shown as potentially enjoying access to all nine branches of social security as set out in ILO’s Social Security (Minimum Standards) Convention of 1952.

Table 2 highlights that the urban salaried population is best served by social protection because of their preferential access to employment-related social insurance. Historically, the rural poor were not protected and were highly vulnerable to risks like natural disasters or health shocks, but many low-income countries have recently extended coverage to rising proportions of the rural population. Between 2014 and 2016, cash transfer programmes expanded their coverage from 2% to 16% of the population in Tanzania and from 3% to 16% in Senegal (World Bank, 2018). However, the middle group, the urban non-salaried population, and especially working-age adults in this group, have fallen between the cracks, not being eligible for contributory social security schemes nor being targeted for non-contributory social assistance. Dorfman (2015) reports that in Sub-Saharan Africa, only the social protection systems of South Africa, Mauritius and Seychelles cover at least 30% of their labour force. For most of the remaining 37 countries analysed, less than 10% are covered.

Social Protection Coverage and Gaps by Rural and Urban Populations

One reason for this oversight is a reluctance by governments to give assistance to working-age able-bodied adults. Globally, social assistance programmes tend to target demographically vulnerable groups who are either not able or not expected to work. Working adults are rarely given free food or cash in non-emergency contexts because governments fear recipients will become dependent on ‘handouts’ (Kalebe-Nyamongo and Marquette, 2014). In fact, impact evaluations of cash transfers in sub-Saharan Africa do not indicate a reduction in work effort by recipients but, instead, increased autonomy and flexibility over productive activities—recipients often choose to work on their own farms instead of doing casual agricultural wage labour (Handa et al., 2018). Similar results have been found across the Global South (Alzua et al., 2013; Banerjee et al., 2017; Surender et al., 2010). Nonetheless, this perception persists and is one of the main reasons why some governments resist extending social assistance to working-age populations.

Apart from this economic dependency argument, contemporary approaches to social protection have been criticized on the grounds that they weaken citizen voice (see Mitlin and Patel, 2005, 2014). According to this view, social protection that is targeted on the basis of personal characteristics (such as age, disability or income) essentially offers an individuated form of assistance that requires no agency or collective action, undermining the cooperative basis of social insurance efforts between workers, firms and governments. 1 While the redistributive and social justice principles of right-based approaches are not in question, a universal programme is ‘too close’ to the state, the argument runs, which might hinder the capacity of civil society to negotiate with the state, specifically around the introduction and realization of a rights-approach approach (see Mitlin and Patel, 2005; Refstie and Milstein, 2019).

As an alternative to free transfers, many governments prefer offering social assistance to working adults in the form of temporary employment on community infrastructure projects or labour-intensive public works. The work requirement acts as a self-targeting mechanism, but it also excludes working-age adults with limited or no labour capacity. Some programmes, such as the Productive Safety Net Programme (PSNP) in Ethiopia and Vision 2020 Umurenge Programme (VUP) in Rwanda, follow a two-pronged approach: Adults in poor households are offered public works employment if they can work, and direct support (free cash or food transfers) if they cannot. These programmes tend to be implemented in rural areas. India’s Mahatma Gandhi National Rural Employment Guarantee Scheme, with over 75 million participants, is exclusively rural. One of the few public works programmes with an urban component is Mexico’s Programa de Empleo Ampliado (World Bank, 2018). Also, after 10 years of operating exclusively in rural areas, where it now reaches more than 8 million people, Ethiopia’s PSNP started expanding into urban areas in 2015, and currently reaches 600,000 people in 11 cities.

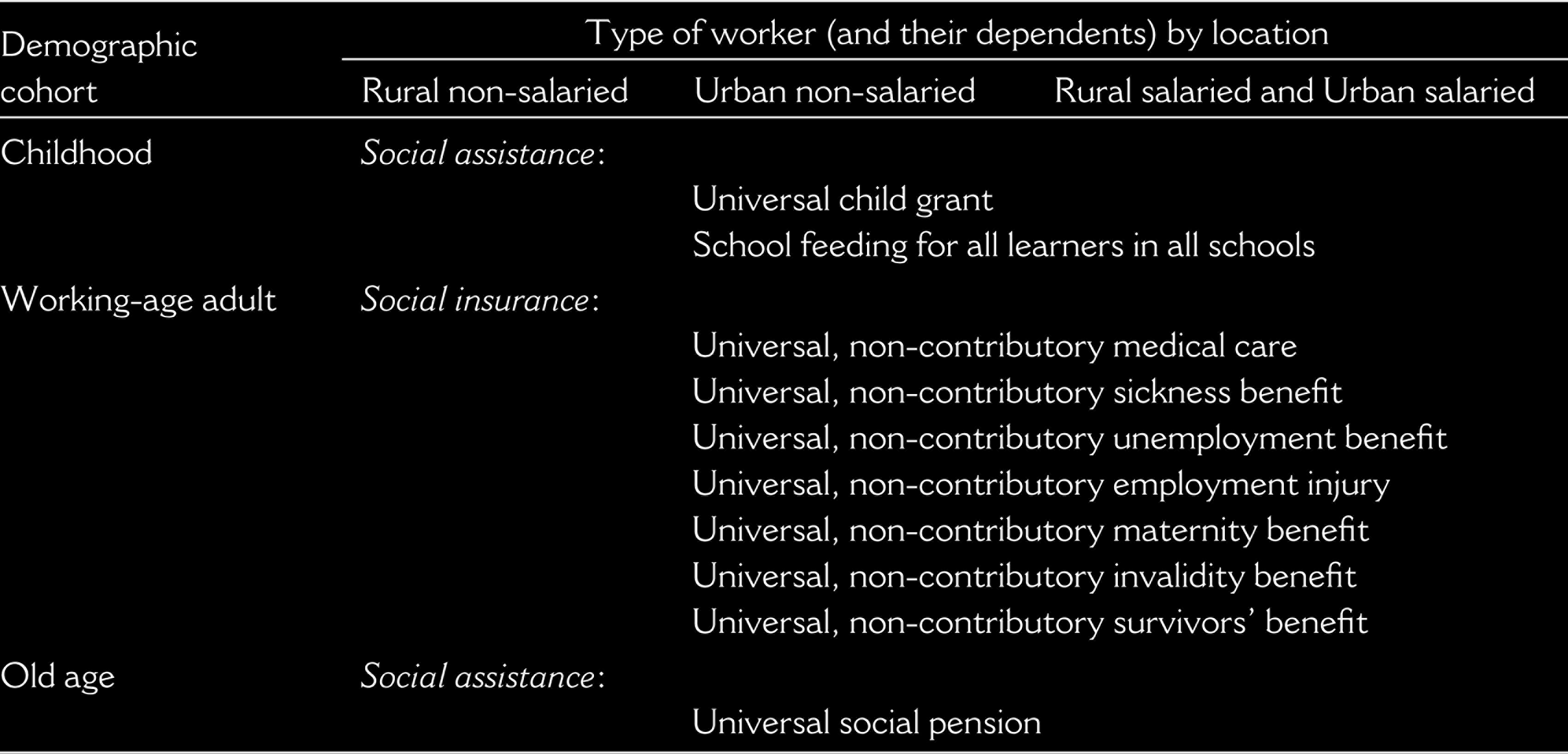

One approach to eliminating coverage gaps while recognizing the diversity of needs is to adopt a rights-based approach to social protection that follows two basic aims (Table 3). One, universalize social assistance to demographically vulnerable groups, with no discrimination between urban and rural residents: universal child benefits, social pensions, disability benefits and school feeding schemes for all learners in all schools. Two, universalize social insurance to all workers, with no discrimination between salaried (formal) workers and non-salaried (informal or self-employed) workers, financed out of general revenues, not by taxing workers’ earnings.

Implications for Social Assistance

Setting the appropriate payment level for social assistance in the urban context is crucial. The urban poor face higher living costs, produce less food, rely more on cash and are more vulnerable to unemployment and underemployment, low and erratic incomes in the informal economy and rising prices. As a result, the purchasing power of a cash grant may be much lower in urban settings. For this reason, cash transfer programmes that expanded from rural into urban areas tend to achieve lower impacts. ‘The cost of living is higher in urban areas so the transfer amounts delivered to rural beneficiaries are not sufficient’ (Satterthwaite and Mitlin, 2013: 37).

One rule of thumb is that cash transfers should be worth at least 20% of the household’s pre-transfer consumption (ILO, 2017), in each local context. Cash transfers are often set at the cost of a basic food basket, adjusted for household size. Another option is to calibrate the transfer value against the cost of a basket of food, goods and essential services. In China, the Dibao programme’s benefits are set at 65% of the local minimum wage (Zhang and Wu, 2016). To account for the higher vulnerability of urban households to inflation, the transfer should be regularly adjusted to keep pace with rising costs of living.

Alternatively, if differentiated payments between urban and rural recipients are not politically possible, urban beneficiaries could receive subsidies for payment of utilities, transport or housing, as a form of income support. In New York City, for example, low-income beneficiaries receive subsidized nutritious food (under the Supplemental Nutrition Assistance Program), heating and cooling assistance (under the Home Energy Assistance Program) and medical care, in addition to cash transfers. Benefit packages for urban families may also include access to services and livelihood opportunities such as vocational training, youth employment programmes, nurseries and early childhood development, nutritional packages, free books and school uniforms, and psychosocial support from social welfare officers.

Implications for Social Insurance

The guiding principle behind universalized social insurance is that all working-age people have a right to social protection during breaks in employment, not only those with formal contracts who contribute towards social security funds. Table 3 shows the simplicity of this proposal.

Universalized Social Protection

Universalized Social Protection

Universalizing social insurance will not inevitably lead to an equity-efficiency trade-off, as is often feared. Levy (2008) and Cuesta and Olivera (2014) argue that integrating social protection across types of participants, and financing this through general taxation rather than by increasing contributions from labour, can secure economic and equity gains simultaneously. Equity gains accrue from all workers being treated without distinction. Currently, formal workers in urban areas typically have to take life, medical and accident insurance under their mandatory social insurance package. An informal worker in a rural area may take none, all or any combination, depending on availability. More efficiency comes from the fact that contributions to social security paid by workers and their employers—as high as 76% of Colombia’s basic minimum salary (Cuesta and Oliveira, 2014)—constitute a tax on formality, while free services (of the same or similar quality) are subsidies to informality. A segmented social protection system decreases productivity by encouraging informality.

All South Africans ‘have the right … to social security, including, if they are unable to support themselves and their dependants, appropriate social assistance’ (Constitution of the Republic of South Africa, 1996, Section 27).

Current Status

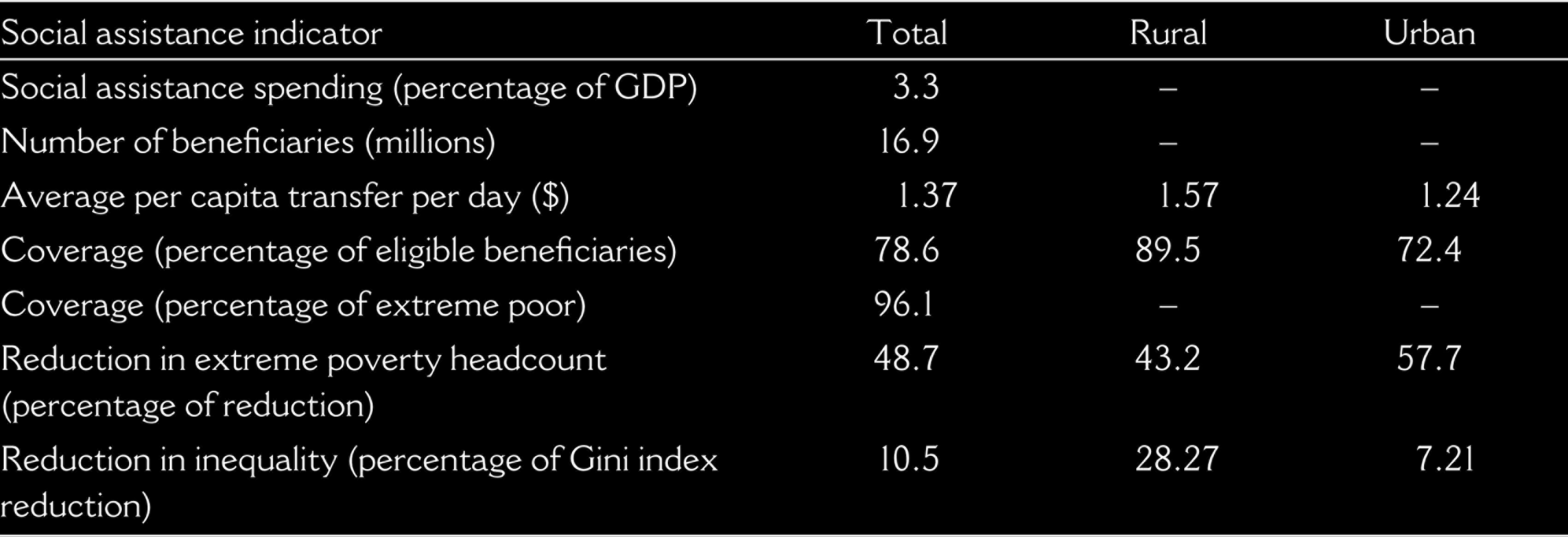

Since the transition to democracy in 1994, the ANC-led South African government has pursued neoliberal economic policies that perpetuated apartheid-era levels of poverty, inequality and unemployment. Unable to address the root causes of poverty, especially structural unemployment, the government responded by dramatically expanding the social safety net. The social protection framework seeks to ensure a decent standard of living from childhood to old age, protection against work injuries or illness, and provisions in case of unemployment or disability (ILO, 2019). The main pillar is relatively generous non-contributory social assistance. Accounting for about 3.3% of national GDP (see Table 4), this includes non-contributory pensions, child grants and free basic services (electricity, sanitation, water supply) for low-income households (ILO, 2019).

Main Features of Social Assistance in South Africa (2015)

Main Features of Social Assistance in South Africa (2015)

South Africa’s total expenditure on social assistance is more than double the average spend of 1.5% of GDP across developing and transition countries (World Bank, 2018). The number of beneficiaries has more than doubled from almost 8 million in 2003 to 17.8 million in 2019 (SASSA, 2019), almost one-third of the population. This expansion mainly reflects an increase in direct cash transfers to children, two-thirds of whom receive the Child Support Grant every month (Waidler and Devereux, 2019).

Ferguson (2015) has labelled this hybrid of neoliberal economic policies and expansionist social spending a ‘neoliberal welfare state’. However, the surge in social transfers does not directly benefit the unemployed, because of government’s concerns that this would discourage job-seeking by working-age adults, but instead targets their dependents: children, (grand)parents, family members with disability. In effect, the means-tested Child Support Grant is a disguised form of unemployment insurance for millions of unemployed South Africans, the majority of whom live in informal settlements on the periphery of South Africa’s cities and towns.

Social assistance in South Africa is well targeted and progressive. Inchauste et al. (2017) report that the poorest 50% of the population receive more than 70% of total direct transfer benefits. According to the World Bank’s ASPIRE dataset (World Bank, 2020a) in 2015, social assistance programmes reached a considerable 78.6% of the eligible population and 96.1% of the extreme poor (Table 4). These programmes significantly improve poverty and inequality indicators, reducing the extreme poverty headcount by an estimated 48.7% and the Gini coefficient by over 10% (World Bank, 2020a). In other words, extreme poverty in South Africa would be double the current rate without social protection. However, although social assistance coverage is higher in rural than urban areas (89.5% vs. 72.4%) (World Bank, 2020a), its capacity to reduce extreme poverty is greater in urban than rural areas (57.7% vs. 43.2%), which is partly explained by a smaller urban poverty gap.

Social insurance, however, provides a very different picture. Coverage is a dismal 3.3% of the eligible population: 2.1% in rural areas and 4% in urban areas (World Bank, 2020a). The capacity of South Africa’s social insurance programmes to reduce poverty is very limited (an estimated 4.2%), and they may even increase inequality (World Bank, 2020a).

Social insurance, available to formally employed adults, is dominated by the Unemployment Insurance Fund (UIF). All workers with a contract and their employers pay 1% of salary to the UIF. However, less than 5% of the unemployed received unemployment benefits in 2011, for two reasons. First, South Africa’s high level of structural unemployment means that more than half of unemployed adults have never formally worked nor paid UIF contributions. Second, unemployment benefits are only paid for one year (National Planning Commission, 2011). As such, the UIF provides inadequate protection to unemployed South Africans, who in 2018 represented 27.1% of the labour force (individuals aged 15–68), or about 6.2 million people (Statistics South Africa, 2018). Annual UIF payments are less than one-tenth of social assistance payments (Devereux and Conradie, 2017), partly reflecting the fact that pension contributions by workers are not mandatory. Retired workers rely on employment-related pensions, private savings or social assistance (the Older Persons Grant).

The National Development Plan (NDP) acknowledges that the exclusion of informal workers (defined as any worker without a contract) from formal social security is the ‘most significant omission’ in South Africa’s social protection system. This group is about 30% of the non-agriculture employed, around 5 million people (ILO, 2020). The NDP recommends encouraging informal workers to contribute to formal social security schemes (National Planning Commission, 2011: 333). The majority of South Africa’s informal workers are urban residents.

Proposed Extensions

Several strategies, often drawing on the experience of other countries, have been proposed for expanding social protection among urban informal and low-income workers in South Africa (Devereux and Conradie, 2017). One such strategy is to ‘extend mandatory social insurance to selected categories of informal workers’. Examples include registering home-based workers in India with the Employees’ Provident Fund (van Ginneken, 1999) and domestic workers in Brazil with the National Social Security Institute (Malherbe, 2013). South Africa has similarly introduced ‘Sectoral Determinations’ that extend unemployment insurance coverage to domestic workers (2002) and taxi industry workers (2005) and make their employers responsible for registering them with the UIF and paying employer’s contributions (Smit and Mpedi, 2010). However, although Holmes and Scott (2016) report higher average hourly earnings and more written contracts among female domestic workers, only about a quarter of domestic workers are considered formal (that is, employers contribute to their health insurance or pension). At a broader level, the Treasury has proposed a unified National Social Security Fund (NSSF) that would cover all registered workers, who would pay 10–12% of their income in return for comprehensive social insurance (National Treasury, 2007), but this has not been implemented.

Another unimplemented proposal, put forward in 2011 by the Department of Social Development (DSD), is for an additional voluntary contribution scheme. The date and size of contributions would be flexible, rather than a fixed percentage of monthly income, and the government would also contribute (as with the UIF). To increase accessibility for informal and self-employed workers, deposits could be made into bank accounts, over the phone or deducted from earnings (DSD, 2011).

A third strategy consists of incentivizing informal workers’ savings. Savings rates in South Africa are very low. One idea that could be adapted is Kenya’s Mbao Pension Plan, a savings scheme for informal workers. Deposits can be made by cell phone, and although operated by private providers, the Plan is regulated by Kenya’s Retirement Benefits Authority (Kwena and Turner, 2013). Participation in such a voluntary savings scheme could be incentivized in South Africa if the government matched (partially or fully) deposits made by people living in poverty. Other countries currently do this, such as China’s National Rural Pension System, which is open only to the rural poor who do not pay income tax (Devereux and Conradie, 2017).

A survey of street traders in Durban, South Africa found they were willing to contribute to a voluntary savings scheme as their retirement pension or disability fund, especially if the government topped up or matched their deposits. However, many traders preferred protection against more immediate contingencies, especially unemployment and illness (Modise et al., 2011). A survey in Colombia (Fedesarrollo, 2008) found that all types of workers were unwilling to pay more than 20% of their labour incomes for full social protection (Cuesta and Oliveira, 2014).

A Bolder Overhaul

Our proposal moves away from partial improvements to the current system to a more fundamental reform that ‘guarantees universal social protection to all workers, financed through general taxes’. This would effectively delink social insurance from employee and employer contributions. This idea has yet to be implemented anywhere, so no baseline or comparison can be made in terms of arrangements or costs. However, financing out of general taxes need not create a substantial additional tax burden. This is because integrating social insurance across all types of workers would remove distortions between social security, employment, productivity and economic growth. The resulting higher economic growth and productivity would generate additional, taxable economic resources. Lower levels of informality and simpler supervision systems should also decrease administrative costs.

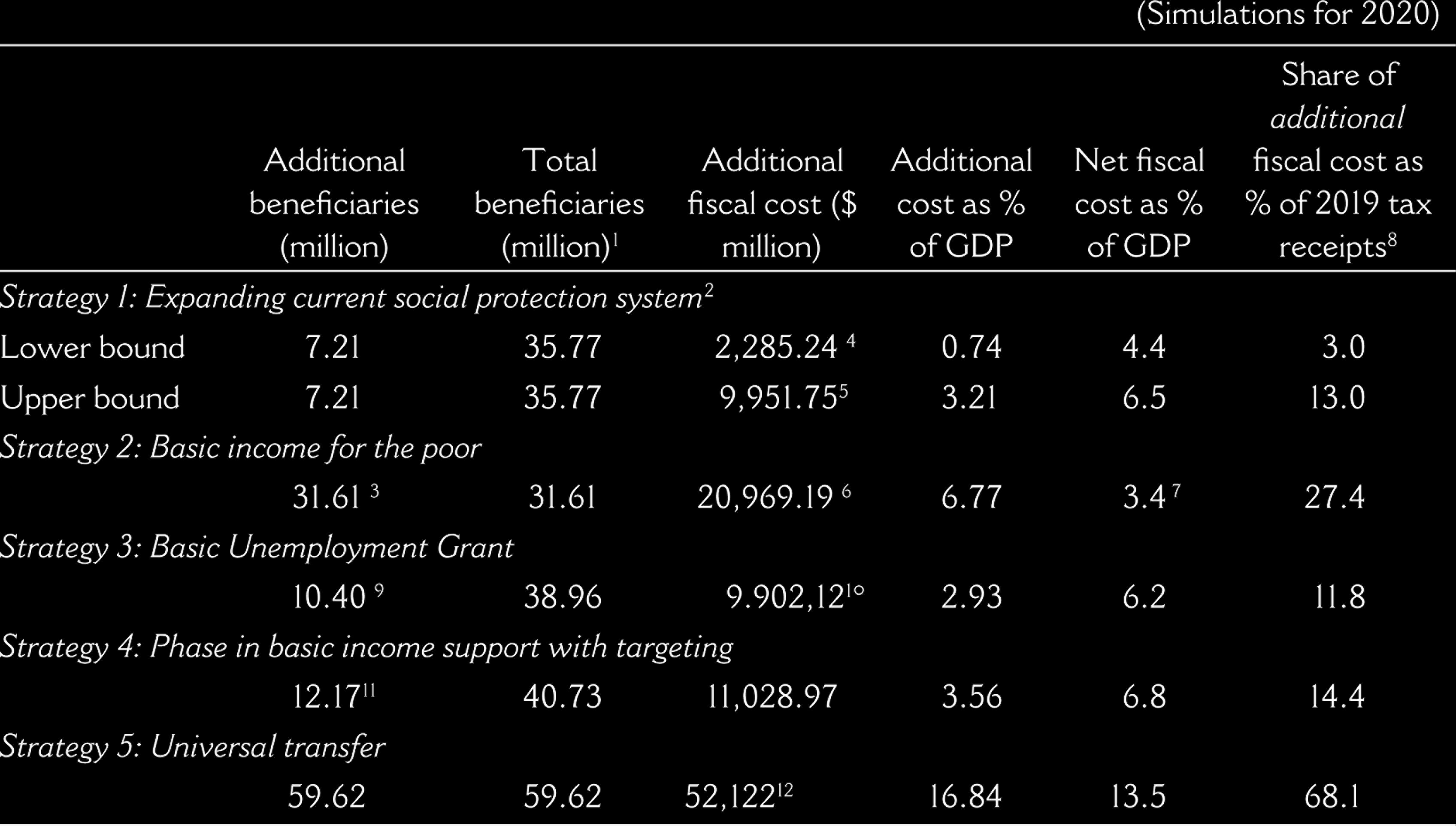

Table 5 below provides back-of-envelope calculations of the order of magnitude that such an overhaul would entail in South Africa. It compares several notional implementation strategies. The first provides a grant to any household currently not in receipt of any social protection programme: an estimated 20.1% of the population in 2015 as reported by World Bank (2020a), which we assumed to remain constant into 2020. For simplicity, we consider two scenarios, one (the lower bound expansion) where all eligible individuals without social protection are provided the lowest grant in the system, that is, R445 ($26.42) per month in 2020. A second scenario (the upper-bound expansion) provides the largest transfer, R1,880 ($110.43), prevailing in 2020.

Achieving Universal Social Protection in South Africa

Poverty rate for 2020 estimated by World Bank (2020b) MPO April 2020,

Population as reported by Statistics South Africa (2020)

Exchange rate as reported by SA Reserve Bank (2020), 28 august 2020,

Total beneficiaries add the level of beneficiaries of the current system plus the additional beneficiaries projected by the proposed reforms unless a specific population group, that is, all the poor, the unemployed is instead assumed to override previous beneficiaries.

1 Includes direct and indirect beneficiaries, i.e., individuals and household members.

2 Additional beneficiaries, 2020: 20.15% (eligible population without social protection) × 60.0% (poor population projected in 2020 by World Bank [2020a]) × 59,620,000 (population in South Africa) = 6.50 million people.

3 Total beneficiaries, 2020: 60.0% (poor population) × 59,620,000 (population) = 35.77 million people.

4 Additional fiscal cost, 2020: 20.15% (eligible population without social protection) × 59,620,000 (population) × 60.0% (poor population) × $26.42 (monthly transfer) × 12 (month) = $2,285.24 million.

5 Additional fiscal cost, 2015: 20.15% (eligible population without social protection) × 59,620,000 (population) × 60.0% (poor population) × $110.43 (monthly transfer) × 12 (month) = $9,951.75 million.

6 Additional fiscal cost, 2015: 60.0% (poverty headcount) × 59,620,000 (population) × 0.292 (average poverty gap) × $5.50 (daily poverty line) × 365 (day) = $20,969.19 million.

7 While the total cost would be 6.7% of GDP, savings of 3.3% of GDP would come from eliminating the current system of cash transfers, making net additional fiscal costs of 3.4% of GDP.

8 Total tax receipts in 2019 amounted to 24.7% of GDP, as reported by SA Revenue Service (2019)

9 Total number of unemployed, 10.4 million, as reported by Senona (2020).

10 BIG, 2020: 10.4 (million unemployed) × R1,227 (upper monthly poverty line 2019) × 12 month/12.8420 (exchange rate) = $9,092.12

11 Phase in BIS 2020: 775,000 (54–59-year-old) @ R1,227 monthly + 5.47 million (34–53) @ R 1,227 + 6 million (18–33) @ $1,227 = R185.75 billion annually, or $11.02 billion

12 Universal BIS, 59.62 million × R 1227 monthly = R877.84 billion or $52.12 billion

Next, we consider a different pathway towards comprehensive coverage: basic income support targeted to poor individuals (Strategy 2), who are given the average income necessary to surpass the international poverty line of $5.50 per person per day (that is, a 29.2% income gap over that amount).

We also consider three additional scenarios, discussed in Senona (2020). Strategy 3 is a Basic Unemployment Grant to all unemployed workers. The transfer amount is R1,227 (or $72.85) per beneficiary, which is the upper bound national poverty line in South Africa (Statistics South Africa, 2019). Strategy 4 consists of a phased Basic Income Grant (BIG) by age-group, starting with those aged 54–59 (using the current targeting formula for older persons grant), followed by the unemployed in the cohort aged 34–53, and completed by the age group 18–33, using several qualifying criteria such as unemployment and not being enrolled in any education programme. Each beneficiary is provided a uniform benefit of R1,227. Finally, Strategy 5 provides a universal transfer of R1,227 to every South African regardless of age, socioeconomic condition or labour status.

Our simulations estimate the cost of comprehensive social protection as ranging from 0.7% to 6.7% of GDP. These notional simulations do not consider administrative costs; assume perfect identification of the poor and their income gaps; and ignore possible behavioural responses and associated political considerations. Ultimately, the transitional and final costs to be financed by general taxes will depend on which parameters of social insurance are offered. However, these estimates still provide a meaningful order of magnitude and highlight several efficiencies and fiscal savings that can be made. The estimated additional financing effort is relatively modest, between 3% and 13% of tax collection (for 2019). Moreover, these efforts do not consider that comprehensive social protection might release additional incomes previously paid in labour contributions that can increase growth, consumption and, ultimately, tax collection. In any case, there are several ways to increase tax collection that are both progressive and feasible, such as raising collection from personal income and corporate taxes (which currently capture only 8.5% and 5.6% of GDP, respectively) and/or further use of luxury and inheritance taxes (Inchauste et al., 2017).

A Rightful Share, COVID-19 and the Revitalized ‘BIG’ Debate

Our proposal for universalized social insurance for working-age adults is apposite, because it would put in place a rights-based safety net for those directly affected by South Africa’s unemployment crisis, the unemployed, rather than those indirectly affected, their children and other relatives. This proposal also resonates with the long-running debate about BIG for all South Africans, which was first proposed in the early 2000s by the Committee of Inquiry into a Comprehensive System of Social Security for South Africa (Taylor Committee, 2002), but was dismissed as unaffordable by then Minister of Finance, Trevor Manuel.

As the social safety net expanded in coverage and generosity, so the campaign for BIG receded and ultimately failed (Barchiesi, 2007; Seekings and Nattrass, 2015). Civil society mobilized instead around more achievable demands, like raising the age threshold of eligibility for the Child Support Grant from 7 to 18 years, which was successfully realized by 2012 (Proudlock, 2011).

A more radical framing of basic income for all is the notion of a ‘rightful share’. Invoking the Freedom Charter’s rallying cry, ‘The people shall share in the country’s wealth!’ (African National Congress, 1955). Ferguson (2015) argues that redistributive transfers from rich to poor in highly unequal countries like South Africa and Namibia should be seen not as charity or social assistance, but as citizens claiming their rightful share of national wealth. ‘No one is giving anyone anything. One is simply receiving one’s own share of one’s own property’ (Ferguson, 2015: 178).

Unlike BIG or a rightful share, universal social insurance would be restricted to unemployed working-age adults, rather than the entire national population, but it would be complemented by the existing social assistance schemes. On the other hand, some of the costs of universalized social insurance would be recovered from reductions in social assistance, as the primary recipients of state support in low-income households would shift from children to their parents.

COVID-19 exposed the critical gap in South Africa’s social protection system. A high proportion of low-income workers with no access to social insurance was severely affected by the lockdown announced by President Ramaphosa from 26 March 2020, because they were unable to work from home and had no direct access to either social assistance or social insurance. Largely for this reason, official unemployment reached 32.5% by the end of 2020, the highest since 2008 (Statistics South Africa, 2021).

Recognizing the urgent need for income support to this group, especially (mainly urban) informal sector workers who account for about 3 million people and 20% of the workforce (Devereux, 2020), the government introduced two new cash transfer programmes, the TERS and the Special COVID-19 Social Relief of Distress (SRD) grant. Eligibility was restricted to unemployed adults who were not receiving any income, social grant or unemployment insurance. While TERS was calculated as a proportion of salaries and paid out several thousand rand a month to many temporarily unemployed workers, the SRD paid only R350 per month, less than the Child Support Grant amount of R440, which was also increased by R500 per month. All these schemes were introduced for a six-month period from May until October 2020 (Seekings, 2020).

By June 2020, it was already apparent that the economic impacts of the COVID-19 lockdown would be deeper and long-lasting than initially anticipated, and a debate started about what should be done to provide continued support to those who would remain unemployed but had no access to either social assistance or the UIF, after the special relief measures end in October. In July, the Minister of Social Development announced that BIG for unemployed working-age South Africans with no access to UIF was under consideration by the government, as a permanent addition to the social protection system (Shoba, 2020). This announcement reignited the public debate around the BIG.

In August, the activist NGO Black Sash published Basic Income Support: A case for South Africa (Senona, 2020), which included costings to demonstrate that, under simulated variations in numbers of eligible beneficiaries and payment levels, a basic income could be provided to low-income 18–59-year-olds that would be fiscally affordable. The report also identifies several options for creating the necessary fiscal space to finance the Basic Income Support scheme, including increasing tax revenues, reallocating public expenditure, reducing illicit financial flows and drawing on the UIF surplus (Senona, 2020). Our proposal is closely aligned to this idea of Basic Income Support.

Notwithstanding the relatively modest fiscal effort required and the viability of alternatives discussed for South Africa, support for expanded social protection is far from unanimous, despite the historical and political considerations favouring such an expansion. As argued by Hickey et al. (2020), the welfare system in South Africa predates others in the continent and has been influential in shaping those of neighbouring countries. Politically, social assistance constitutes a widely accepted post-apartheid social contract and a major pillar of legitimacy for democratic governance. However, the widespread support for social assistance might have delayed discussion on the introduction of mandatory social insurance (Taylor Committee, 2002). Persistent levels of poverty coupled with limited effectiveness of labour market regulations, due to high informality, may strengthen the support for social assistance while delaying the extension of social insurance instruments (Niño-Zarazúa et al., 2012). In other words, the politics behind the support for social assistance might differ from social insurance.

At the ideological level, powerful factions within the government have always been hostile to any policy direction that appears to prioritize ‘welfare’ rather than ‘development’. One counter-proposal to BIG was to massively expand public works, to offer unemployed South Africans ‘the dignity of work’ instead of ‘handouts’ (Seekings and Nattrass, 2015: 162–3). Barchiesi (2007: 561) argued that ‘the extremely cautious approach to a basic income grant in South Africa reflects a government approach that continuously praises work ethics and wage labour discipline while stigmatizing welfare “dependency”’. More recently and at the pragmatic level, even though COVID-19 created an urgent demand for a more comprehensive, rather than narrowly targeted, social protection system; it also created additional fiscal pressure following the sharp economic contraction and increased public sector borrowing that the pandemic precipitated. The Minister of Social Development’s endorsement of a Basic Unemployment Grant did not resonate with her Cabinet colleagues and appears to have no political traction. Influential economists even reacted against the government’s COVID-19 stimulus package by publishing opinion pieces with titles like: ‘SA Needs More Jobs – Not Social Grant Beneficiaries’ (van Heerden, 2020).

Global strategies such as the SDGs and the NUA have not given urban social protection sufficient attention. National development strategies have similarly failed to provide a sense of urgency, despite the rapid pace of urbanization and the range and depth of urban-specific poverty drivers. Expanding coverage of social protection from rural to urban areas is not simply a matter of applying the same design and implementation modalities. Higher living costs, high levels of informality or unemployment, low and variable incomes, and variable access to and quality of basic services all call for a tailored urban social protection strategy.

We have proposed a rights-based approach that (a) universalizes social assistance to demographically vulnerable groups, with no urban/rural discrimination and (b) universalizes social insurance to all workers, with no discrimination between salaried (formal) workers and non-salaried (informal or self-employed) workers. For social assistance, we argue that cash or in-kind transfers for urban residents should, if politically feasible, be adjusted for higher urban living costs (food, water) as well as for urban-specific costs (transport, rent, electricity). For social insurance, universal tax-financed social insurance is the ideal, because a segmented system that fails to cover the needs of all workers taxes formality and incentivizes informality. However, until this idea gets traction, since few urban informal workers currently have access to employment-related social security, voluntary participation must be incentivized, and/or specific schemes must be designed for all excluded non-salaried workers.

We also argue that general taxes could finance such a universalization and integration of programmes. We illustrate these options specifically in South Africa, a country that epitomizes a glaring gap in protection of poor informal workers in urban areas. We show that universal social protection might not inevitably involve unaffordable costs; in fact, some efficiencies are possible. Several realistic financing options are available that combine progressive increases in income, corporate and inheritance taxes. However, in order to design and implement such tax and related fiscal reforms there must be a requisite level of institutional capacity, economic prosperity conducive to the expansion of the tax base and sufficient political commitment to overcome the opposition of interest groups and elites towards a universal agenda. While the proposal is relevant for all countries that are failing to adequately cover informal workers and urban residents more generally, successful advocacy is more likely in upper middle-income countries, countries experiencing sustained economic growth or countries with growing demands for social security as part of upgraded social contracts (for example, countries where poverty reductions have meant a thickening middle class). Conversely, countries with stagnant growth, low fiscal capacity, widespread chronic poverty or fragility are not obvious candidates for transitioning towards universal programmes. Favourable economic, social and political conditions are prerequisites for comprehensive, rights-based social protection in a post-COVID-19 world.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.