Abstract

A rapidly expanding body of entrepreneurship literature draws on signaling theory. Yet as the field grows, common understanding of the theory’s underlying constructs has become increasingly fuzzy and riddled with ambiguities. To establish a common ground for entrepreneurship scholars, we take stock of 172 articles in a systematic literature review and develop a taxonomy of signal constructs. In an effort to increase the clarity of signal constructs further, we apply this taxonomy to assess the signal constructs’ boundary conditions, relationships, and interplays with complementary theories in entrepreneurship contexts. Finally, we leverage the novel insights to identify promising opportunities for further theory-based developments in the field.

Introduction

Applications of signaling theory (Spence, 1973), which suggests that high-quality ventures indicate their unobservable quality with observable activities or characteristics that are costly and difficult for low quality ventures to imitate (Ahlers et al., 2015), are growing rapidly in popularity in entrepreneurship research (Kleinert et al., 2021; Luo et al., 2020; Shafi et al., 2020). This development is unsurprising, considering how signaling theory helps resolve one of the main obstacles faced by new ventures: reducing severe information asymmetries for important audiences such as potential customers, strategic partners, and investors (Hallen et al., 2020; Reuer & Ragozzino, 2012). The foundation of entrepreneurship signaling research are the theory’s underlying constructs, defined as conceptual abstractions of categories that are not directly observable (Shepherd & Suddaby, 2017). For example, signal strength as a relevant construct describes the correlation between a signal and a new venture’s unobservable quality (Vanacker et al., 2020). Such clear constructs are fundamental for theory development (Suddaby, 2010) and for making theoretical contributions in entrepreneurship signaling research (e.g., Butticè, Collewaert et al., 2021; Plummer et al., 2016; Tumasjan et al., 2021).

Yet the proliferation of signaling theory in entrepreneurship research has created a concern: No consensus exists regarding the theory’s underlying constructs. The field thus lacks construct clarity (Post et al., 2020), which raises four critical challenges. First, the countless number of signaling constructs available tend to be ambiguous and overlapping, and researchers often use different labels to refer to signal constructs with similar meanings. Consider the terms used to refer to signals from third parties: third-party signals (Anglin et al., 2020), investor-generated signals (Wang, Mahmood et al., 2019), external signals (Colombo et al., 2019), or endorsement signals (Courtney et al., 2017). Second, entrepreneurship signaling research keeps introducing new constructs. For example, recently introduced constructs related to the effects of signals include dynamic signaling (Ko & McKelvie, 2018), signal redundancy (Steigenberger & Wilhelm, 2018), signal flexibility (Scheaf et al., 2018), and signal intensity (Calic & Shevchenko, 2020). Despite their potential importance, these constructs tend to emerge from research silos, without clear evidence of their relationships with other constructs. Third, the confusion is intensified by the lack of consideration of boundary conditions about when signal constructs apply. For example, entrepreneurship encompasses very early-stage ventures and more mature companies but insufficient research considers whether signal constructs are equally applicable across those stages (e.g., for crowdfunding and initial public offerings [IPOs]; Anglin et al., 2018). Fourth, entrepreneurship research often combines signaling with other theoretical perspectives. Doing so can add value, but it also can create ambiguities; the combination with institutional theory (DiMaggio & Powell, 1983) often confuses quality signals with legitimacy, for example. The lack of construct clarity in contemporary entrepreneurship research in turn makes it increasingly challenging to keep track of what is known, understand the contributions of prior research, or establish a common knowledge basis. The field therefore risks redundant research and non-meaningful theory development.

To address such concerns, we undertake a systematic literature review (Rauch, 2020), involving 172 entrepreneurship signaling studies, and use a “clarifying constructs” approach, which represents a recommended, theory-generating method for literature reviews (Post et al., 2020, p. 360). The analysis relies on a narrative synthesis approach (Macpherson & Jones, 2010) and produces a taxonomy of signal constructs for entrepreneurship. We then use this taxonomy as a baseline for an in-depth discussion of construct clarity in entrepreneurship signaling research, as well as to set a new theory-driven research agenda.

Therefore, our review makes three main contributions to entrepreneurship signaling research. First, we distill 18 clearly defined constructs in a taxonomy, which synthesizes the current state of knowledge about signaling theory in entrepreneurship contexts. By defining, sorting, and ordering the signaling constructs, this taxonomy reduces ambiguities and creates a common language for the field. In this role, the taxonomy can serve as a building block for further applications of signaling theory in entrepreneurship research. Second, we apply the taxonomy of signal constructs to establish meaningful boundary conditions, clarify critical relationships, and explain the influences of complementary theories. We identify contemporary who, where, and when boundaries (Welter, 2011), which reflect the scope and conditions in which signal constructs apply or not in entrepreneurship contexts (Suddaby, 2010). The relational perspective highlights relevant, logical connections among signal constructs, which contributes to resolving silo views within entrepreneurship signaling research. By accounting for the growing influence of complementary theories on signal constructs, we uncover potential sources of ambiguities and novel insights. Third, we introduce a novel research agenda to guide further, theory-driven developments of entrepreneurship signaling research.

In this sense, our study also goes beyond existing reviews. For example, with a selection of 68 articles, Colombo (2021) offers a comprehensive synthesis of which new venture signals are most effective for crowd funders, business angels, venture capitalists, and equity investors. Our more theory-centered review approach (e.g., Post et al., 2020) instead aims to establish the clarity of signal constructs in entrepreneurship contexts, which results in a distinct research agenda. For this purpose, we review the entire entrepreneurship field and draw on a larger set of journals and articles. Connelly et al. (2011) review selected signaling studies in management research; extending their effort, we use a systematic review method, applied to state-of-the-art literature (76% of studies published after 2011), and account explicitly for the distinctiveness of the entrepreneurship context. To establish these contributions, we start in the next section by introducing signaling theory and its relevance for entrepreneurship, then explain our systematic literature review method. After presenting our novel taxonomy of signaling constructs, we discuss its insights, then set an agenda for continued entrepreneurship signaling research.

Signaling Theory, Core Tenets and the Entrepreneurship Context

Originating in economics, signaling theory, as introduced by Spence (1973), offers a solution to the information gaps that arise among actors in markets characterized by uncertainty. For example, in the labor market, a job applicant knows more about his or her productivity than the employer. Because job applicants have incentives to report favorable information, employers might mistrust their accounts. Employers then struggle to identify good candidates, and the hiring process represents an investment under uncertainty. To prevent inefficient market outcomes, 1 actors with an information advantage (signalers) can transmit signals that carry credible information about their otherwise unobservable qualities, so that other actors, who lack such information (receivers), can receive and interpret the signals, in support of more informed assessments (Spence, 1974). Signaling theory has several core tenets. First, signals must be observable characteristics or activities that also are alterable. In contrast with unalterable indices (e.g., sex), signals can be adjusted (e.g., education) by the actors that send them (Spence, 1973). Second, signals must invoke costs that correlate negatively with actors’ quality. Therefore, poorer quality actors must invest more to obtain a signal and are less likely to imitate signals transmitted from high-quality actors. Receivers thus gain some confidence that the signals convey credible information (Spence, 2002). Third, in the long run, signalers outperform non-signalers (Bergh et al., 2014), and receivers gain experience and new data that enables them to learn whether the signal is confirmed.

With its intuitive nature and potency for resolving information asymmetries, signaling theory often gets applied in investigations of organizational realms in which differently informed parties interact (e.g., strategic management, human resource management, entrepreneurship). Originally based on a few clear constructs (e.g., signal cost), it has expanded significantly, reflecting its frequent application. Connelly et al. (2011) even account for progress in management disciplines according to a general classification of the key elements of signaling theory: signaler, signal, receiver, environment, and feedback. But among various management research fields, entrepreneurship represents the dominant target of applications of signaling theory (Colombo, 2021). The theory’s relevance in this context stems from its particularly severe and problematic information asymmetries (Higgins et al., 2011; Hoenig & Henkel, 2015); new ventures critically depend on signals to convince key audiences, such as resource providers or early customers, of their capabilities (Hallen et al., 2020; Wang, Mahmood et al., 2019). Because signaling has become the go-to theory for investigating how new ventures attract external parties, researchers keep advancing the theory by introducing myriad new signal constructs. As a result, the field of entrepreneurship signaling has grown fuzzy, and the theory’s underlying constructs appear ambiguous, which poses an existential threat to further theory advancements.

Method

We use a systematic review (Patriotta, 2020; Tranfield et al., 2003), a method that has proven useful to develop entrepreneurship theory (Rauch, 2020) and advance construct clarity (Post et al., 2020).

Inclusion Criteria and Sample Identification

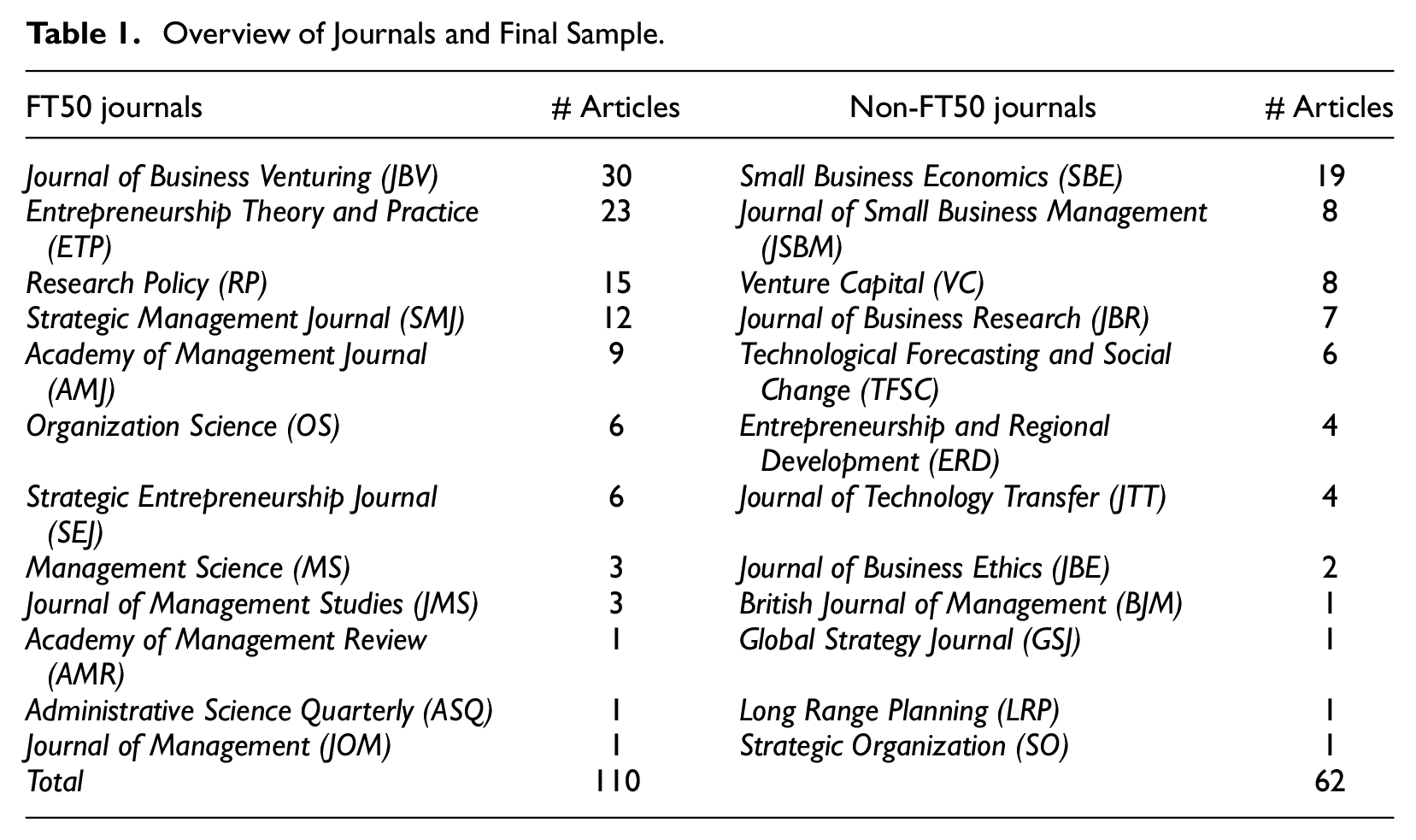

To identify suitable entrepreneurship studies to include in the review, we follow best practices for data collections in systematic reviews (e.g., Macpherson & Jones, 2010; Short, 2009; Tranfield et al., 2003); with a three-step process, we generate a relevant sample of entrepreneurship signaling studies. First, in defining relevant outlets for our study, we specify journals that appear on the most recent Financial Times Top 50 list (FT50 journals). These journals also offer the highest 5-year impact factors, according to the Journal Citation Report by Web of Science, in the categories of entrepreneurship, management, or strategy. Finally, they appear in prior reviews of entrepreneurship topics (e.g., Drover et al., 2017; Überbacher, 2014). We identified 12 journals this way. But to ensure a broad view of signaling constructs, we include other respected journals that publish entrepreneurship signaling studies, as identified from the Association of Business School’s list (e.g., Sutter et al., 2019) of “highly regarded journals” (rating ≥ 3), again in the categories of entrepreneurship, management, or strategy. This set included 14 additional journals. Next, we searched the Web of Science database for journals that received the most hits in response to the search term “signaling in entrepreneurship” (within the “Business & Economics” category). This search confirmed that our existing journal list covered the most relevant outlets but also revealed three additional journals: Technological Forecasting and Social Change, Venture Capital, and Journal of Technology Transfer. Overall, we thus include 29 outlets in our search for relevant articles.

Second, we searched the Web of Science database to identify articles in each journal, from the date of its inception until November 2021. The search targeted general article topics, so it encompassed the title, abstract, and keywords (Shepherd et al., 2019). Our search term included “signal*” and nine keywords: “entrepreneur*” OR “early-stage” OR “newness” OR “new organization*” OR “new firm*” OR “start-up*” OR “startup*” OR “Initial Public Offer*” OR “IPO*.” This search resulted in 283 potential studies for inclusion in our sample.

Third, after reading all identified studies and through mutual agreement, we excluded 121 studies that did not refer to signaling or did not deal with entrepreneurship (e.g., Shepherd et al., 2019). As a final check to confirm that we identified all relevant studies (e.g., Überbacher, 2014), we reviewed the reference lists of the remaining studies and added 10 relevant publications that did not emerge from our database search, because their text focuses on “signals” or other search terms, but those words did not appear in the title, abstract, or keywords. The final sample thus contained 172 studies, published in 12 FT50 and 12 non-FT50 journals, as listed in Table 1. Our sample size exceeds that of previous reviews of signaling theory (Colombo, 2021; Connelly et al., 2011); it is comparable to prior reviews that seek construct clarity in other domains (e.g., Massa et al., 2017; Scheaf & Wood, 2021). In this sense, our sample size reflects the purpose of our study, namely, to provide a complete account of current knowledge and applications of signaling theory to entrepreneurship.

Overview of Journals and Final Sample.

Analysis of Articles

For the data analysis, we adopted a narrative synthesis approach (Macpherson & Jones, 2010), with the goal of developing a taxonomy of signaling constructs used in entrepreneurship research (Post et al., 2020). Following best practices of previous review articles (e.g., Sutter et al., 2019), each author read each article independently and coded its characteristics, such as the research question, theoretical framework, empirical evidence, and study context. For the first categorization, we used each article’s main theoretical contribution to signaling theory, applying the existing classification system for management research by Connelly et al. (2011) as a foundation. We confirm that this classification system of key elements (signaler, signal, receiver, environment) is appropriate for categorizing the studies in our entrepreneurship sample on a higher level; only feedback does not appear in any detail in the reviewed studies.

However, these key elements do not reflect the full complexity and depth of entrepreneurship studies using signaling theory. The vast number of entrepreneurship signaling studies published in the past decade have produced new, more profound theoretical insights about the key elements and a plethora of underlying signal constructs. To go beyond a general distinction of key elements, we seek to pinpoint underlying signaling constructs and understand how they form key elements of signaling theory in entrepreneurship, as used or discussed in the articles of our sample. For this effort, we applied an iterative process in which we repeatedly read the articles, discussed emerging constructs, and linked the constructs to the key elements over several rounds, such that we deleted, merged, or adjusted constructs as needed. Overall, our analysis yielded 18 signaling constructs. The full sample and coding list is in the Appendix A.

Initial Sample Insights

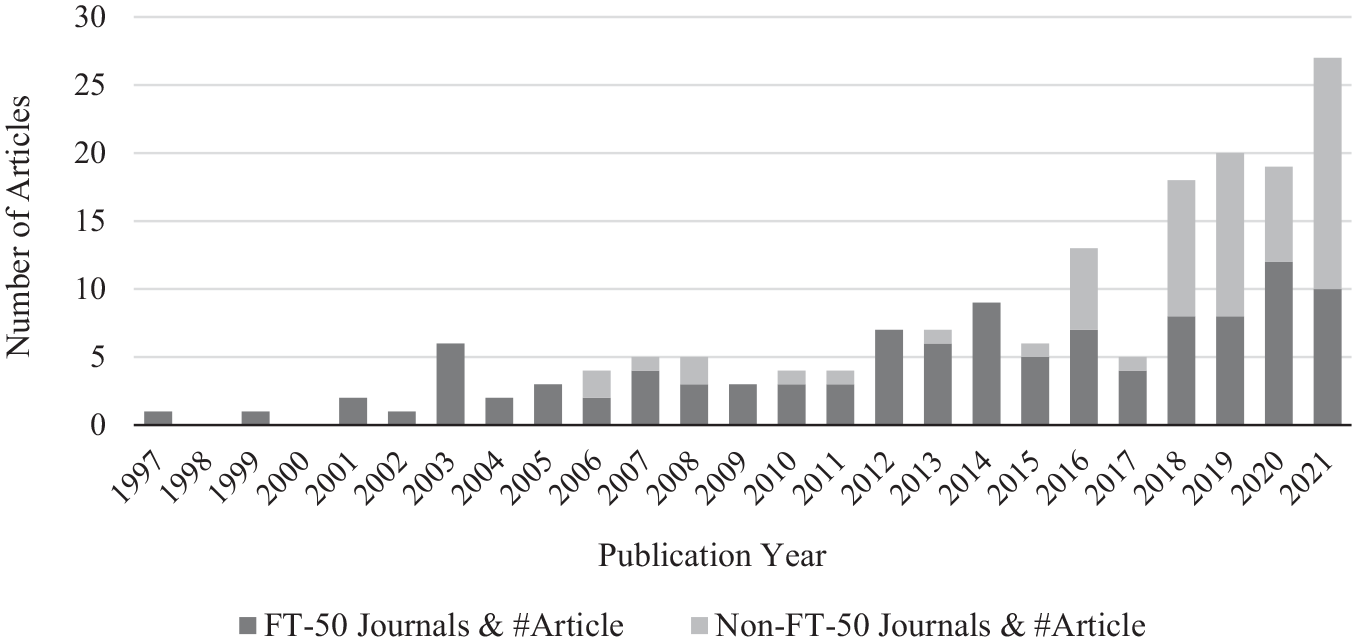

Before we present the results of our analysis, we note interesting differences across the sampled studies published in FT50 and non-FT50 journals. Figure 1 illustrates some notable publication patterns. The first entrepreneurship signaling study appeared in 1997, in a FT50 journal; non-FT50 journals started to publish entrepreneurship signaling studies in 2006. This pattern implies that the topic originated in top journals, then after some time spread to other journals. Across all journals, the number of published entrepreneurship signaling studies has increased drastically in the past decade, but since 2018, the number of published studies is greater in non-FT50 than in FT50 journals. For example, in 2021, FT50 journals published 10 studies, while non-FT50 journals published 17.

Published entrepreneurship signaling studies in the sample.

According to Web of Science, as of February 2022, the median number of citations for FT50 studies in our sample is 47.5; this value is 11.5 for non-FT50 studies. We find some outliers though, especially in the FT50 sample, such as Stuart et al. (1999) with 1,408 citations, Baum and Silverman (2004) with 610 citations, and Ahlers et al. (2015) with 606. In the non-FT50 sample, the most cited study is Vismara (2016), with 249 citations.

During the coding process, we noted differences in the use of signaling theory and constructs in the FT50 versus non-FT50 sample studies. On average, FT50 studies are more likely to feature fundamental advancements to signaling theory, such as introducing new signaling constructs or challenging core assumptions. The more incremental contributions in non-FT50 studies instead tend to involve testing well-established signal constructs or applying the theory to a new context. One-third of non-FT50 studies apply signaling theory to crowdfunding contexts, whereas the focus is more diverse in FT50 studies, and the IPO context is the most prominent application field.

Taking Stock: A Taxonomy of Signaling Constructs in the Entrepreneurship Context

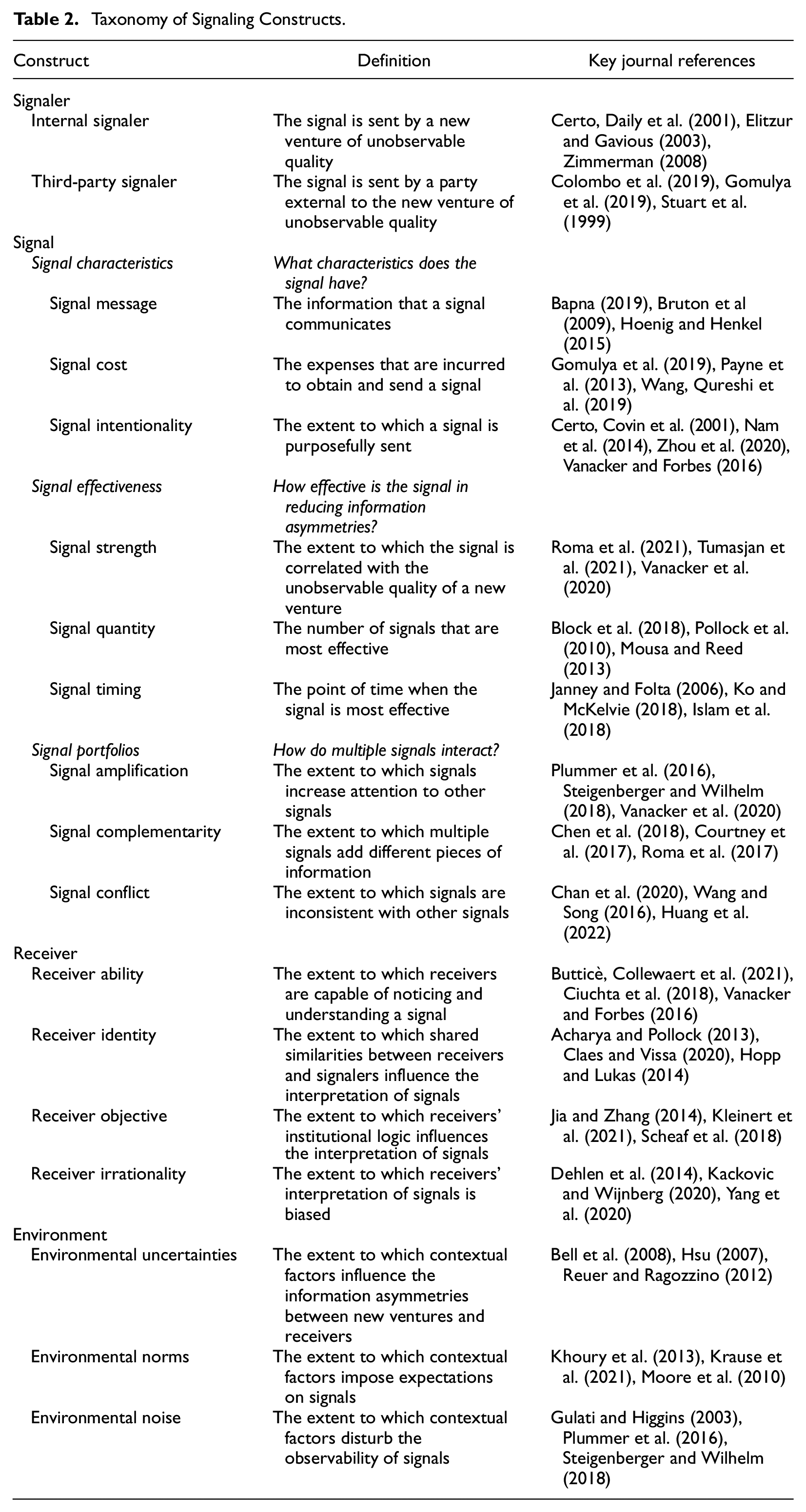

Our analysis yields a taxonomy of 18 signaling constructs that underlie the four key elements: signaler, signal, receiver, and environment. Table 2 presents the taxonomy; in the following sections, we clarify the constructs.

Taxonomy of Signaling Constructs.

Signaler

Signalers in entrepreneurship contexts hold private information about the unobservable quality of a new venture (Huynh, 2016), which they use to develop costly, informative signals for outsiders (Spence, 1973), such as potential investors or employees, who lack the information. The signaler often is the new venture itself, but other signalers are possible. Entrepreneurship signaling research tends to be ambiguous about who is sending the signal, though in our sample, we can establish a categorical distinction between internal and third-party signalers.

An internal signaler corresponds to new ventures with unobservable quality that send the signal. They bear the cost to create the signal, such as when a new venture invests time and money in research and patent application fees to establish a patent signal (e.g., Deeds et al., 1997). This internal signaler in turn might be an individual or an organization. Individuals usually are entrepreneurs or managers, who function as representatives of a new venture. They hold private information about their individual capabilities, which they can indicate to outsiders with signals such as education or experience (Ko & McKelvie, 2018). An entrepreneur also has private information about his or her commitment and might signal heightened levels of effort to increase the chances of early-stage funding (Eddleston et al., 2016; Elitzur & Gavious, 2003). As startups transition from early to growth phases, management boards often come into being, and the founders might be replaced as company leaders (Certo, Covin et al., 2001). In these transitions, individual managers and management teams gain importance as internal signalers; a management team might cite its members’ experience and heterogeneous backgrounds to send a signal about its strong human capital (e.g., Cohen & Dean, 2005; Zimmerman, 2008). However, entrepreneurship studies tend to focus on signals from the organization as a whole, rather than individual members (Daily et al., 2005; Jain et al., 2008). A nascent new venture might signal the quality of its novel product with a working prototype (Audretsch et al., 2012); a late-stage venture could signal its potential by highlighting its high employment growth to acquirers (Cotei & Farhat, 2018); and an IPO firm can emphasize its quality by spending more on R&D (Daily et al., 2005; Heeley et al., 2007).

A third-party signaler instead is external to the new venture of unobservable quality; it might represent a venture capitalist, alliance partner, or media institution (Partanen & Goel, 2017; Scheaf et al., 2018; Stuart et al., 1999). Such third-party signalers might hold private information too, such that they could function as insiders (Wang, Mahmood et al., 2019). For example, underwriters and venture capitalists conduct in-depth, due diligence to obtain private information about a new venture’s economic potential (e.g., Reuer & Ragozzino, 2012; Shafi et al., 2020). When they issue signals, third-party signalers incur signaling costs, often related to their valuable reputations, which they put at stake by affiliating with a new venture (Gomulya et al., 2019). Entrepreneurship studies frequently focus on third-party signalers, because they help compensate for new ventures’ lack of opportunity to establish a reputation yet. Thus, prestigious university partners (Colombo et al., 2019), prominent venture capitalists and underwriters (Pollock et al., 2010), or reputable strategic partners (Stuart et al., 1999) can lend their reputation resources to signal the new venture’s quality to outsiders (Hsu & Ziedonis, 2013). Beyond lending reputation resources, third parties might perform other signaling activities (Bruton et al., 2009), such as when venture capitalists convert preferred shares into common equity, which opens them to the risk of lost control and high costs (Arcot, 2014). Due to digitization trends, new forms of third-party signalers have emerged, such as when Twitter audiences retweet an IPO firm’s announcements (Mumi et al., 2019), customers share product experiences online (Courtney et al., 2017; Reuber & Fischer, 2009), or small backers support crowdfunding campaigns, which signals their confidence in the new venture (Chan et al., 2020). These digital third-party signalers seem to be growing in importance, because their signals are very observable and can shape the opinions of vast audiences.

Signal

A signal communicates private information from a signaler to a receiver. Entrepreneurship studies examine a plethora of signals: product certifications (Bapna, 2019), philanthropic donations (Jia & Zhang, 2014), withdrawals by affiliated venture capitalists (Shafi et al., 2020), and entrepreneurs’ rhetoric (Steigenberger & Wilhelm, 2018), to name a few. Theoretical contributions that seek to describe signal-related constructs make up the bulk of our sample, and we observe particularly blurry conceptual distinctions in this category. On the basis of our review though, we suggest classifying signals according to their characteristics, effectiveness, and interactions with other signals in a portfolio.

Signal Characteristics

The signal characteristics pertain to fundamental features of the signals themselves. We identify three sets of characteristics that distinguish signals in our sample: message, cost, and intentionality. The signal message refers to what information a signal communicates to receivers. Spence’s (1973) original model includes education as a signal that provides a message about job applicants’ unobserved productivity. According to our sample, signal messages may pertain to intentions (Busenitz et al., 2005; Vismara, 2016) or social impacts (Saluzzo & Alegre, 2021; Yang et al., 2020), but they primarily refer to the new venture’s economic quality (Baum & Silverman, 2004; Zimmerman, 2008). An important consideration is how narrow or broad the message is; according to Bruton et al. (2009, p. 911), “signals are not universal in addressing all issues.” Economic quality might refer to product, market, team, or financial qualities; some signals provide narrow information about individual dimensions while others contain broad information about several dimensions (Bapna, 2019). As examples of narrow messages, sales agreements only signal market quality (Hoenig & Henkel, 2015), and a working prototype indicates solely product quality (Audretsch et al., 2012). Broad messages instead might include venture capital backing, because investments by sophisticated investors who have conducted due diligence likely ensures high quality standards on several dimensions, such as the team and financials (Kleinert et al., 2021).

Signal costs pertain to the expenses required to obtain and send a signal. They might take the form of implementation costs incurred ex ante or penalty costs incurred ex post (Wang, Qureshi et al., 2019); both prevent low quality ventures from imitating signals and thus help receivers distinguish high from low quality firms (Bergh et al., 2014). The implementation costs of signals might be monetary, time, or psychic expenses, which signalers must invest to send the signal (Spence, 1973). For example, before new ventures can signal their quality through an ISO certification, they must invest money and time to develop reliable production facilities and processes (Bapna, 2019); before founders can obtain an educational degree, they must invest effort and psychic costs (Hsu, 2007; Ko & McKelvie, 2018). Penalty costs instead arise after the signal has been transmitted and turns out to be false. The most common form of penalty costs are reputational losses for signalers (Fitza & Dean, 2016; Momtaz, 2021b; Mousa et al., 2015). In their empirical investigation of penalty costs, Gomulya et al. (2019) find that if venture capitalists provide reputational signals to a new venture that subsequently defaults, their reputations suffer, and they cannot raise more money thereafter. Yet penalty costs also can take the form of subsequent monetary and time efforts; if the IPO firm’s rhetoric about its organizational virtue turns out to be false, investors could impose penalties, such as investing their resources elsewhere or demanding changes to the management team (Payne et al., 2013). Because receivers often can detect fabricated or untruthful signals, internal or third-party signalers that send them risk drastic penalties (Mousa et al., 2015).

Finally, signal intentionality refers to the extent to which signals are sent deliberately. Entrepreneurship studies often assume that new ventures purposefully take action to communicate their positive qualities to outsiders, such as hiring top executives for their management team (Pollock et al., 2010), obtaining and keeping a patent (Zhang et al., 2019), retaining larger ownership shares (Vismara, 2016), or strategically using an entrepreneurial rhetoric (Calic & Shevchenko, 2020). However, even Spence (1973) already had noticed that signalers might not understand what signals they are sending; that is, signals can be unintentional (Zhou et al., 2020). When entrepreneurs perform an activity that has unclear consequences for the future, the resulting signals might be serendipitous, even if unplanned. For example, starting a company that succeeds later will offer a viable signal of the entrepreneur’s skills and capabilities (Hsu, 2007). But unintentional signals can have adverse consequences too. For example, when a manager engages in earnings management, it sends an unintentional signal of the organization’s poor trustworthiness (Nam et al., 2014) or when a venture capitalist who becomes dissatisfied with a new venture withdraws a prior investment, it provides an unintended signal about the venture’s low growth prospects (Shafi et al., 2020). These unintended consequences of such actions represent an existential threat to new ventures, because the signals are “at least partially out of the control of the entrepreneur” (Saluzzo & Alegre, 2021, p. 2).

Signal Effectiveness

The effectiveness of a signal for reducing information asymmetries depends on three important mechanisms, according to prior research: strength, quantity, and timing.

Signal strength describes the extent to which a signal correlates with the quality of the new venture. If signals correlate strongly with underlying quality, they tend to be more effective for reducing information asymmetries (Vanacker et al., 2020). Entrepreneurship research theoretically distinguishes strong and weak signals (Roma et al., 2021; Tumasjan et al., 2021; Vanacker et al., 2020). For example, affiliations with prominent partners constitute strong signals that point unambiguously to the strong economic quality of a new venture, because prominent companies would not ally with poor quality firms (Baum & Silverman, 2004; Colombo et al., 2019; Stuart et al., 1999). But a complex logo (Mahmood et al., 2019), carefully designed videos for crowdfunding campaigns (Chan et al., 2020), or naming the firm after the founder (Belenzon et al., 2020) represent weak signals. They might provide some relevant information, but correlate rather weakly with the new venture’s quality. In addition, such signals are more widely available, so they generally are more ambiguous (Plummer et al., 2016). Receivers prefer strong signals; when they are not (yet) available, weak signals might be the only option. In detail, Vanacker et al. (2020) establish that investors prefer to learn about new ventures’ realized performance (strong signal) rather than unrealized performance (weak signal), but if the new ventures lack any realized performance, their unrealized performance becomes more important. 2

Signal quantity refers to the number of signals that exerts the greatest effect. A new venture might have many or few patents, many or few alliance partners, and many or few experienced managers (Mousa & Reed, 2013). Some signals exert linear effects: The more, the better when it comes to prestigious directors for IPO firms, for example. Each additional director introduces a different background and therefore contributes valuable knowledge (Pollock et al., 2010). However, most signals reach their greatest effectiveness at some intermediate level, after which their effectiveness decreases (Calic & Shevchenko, 2020; Chen et al., 2018; Thies et al., 2019), for two main reasons. First, greater quantities might be uninformative; affiliations with three venture capitalists versus four venture capitalists would provide little additional, and potentially even redundant, information about the quality of a new venture (Pollock et al., 2010). The additional informative value of more updates about a new venture’s development during a crowdfunding campaign also is decreasing, so this signal becomes less effective at higher quantities (Block et al., 2018). Second, new ventures that invest their scarce resources in more of just one signal might appear inefficient. Holding too many patents is inefficient for new ventures, due to their high application and renewal costs, as well as the time needed to monitor potential patent infringements (Mousa & Reed, 2013). Similarly, too many alliances might diminish a venture’s flexibility and lead to high costs, needed to manage the various relationships (Hoehn-Weiss & Karim, 2014).

Finally, signal timing pertains to when a signal is most effective. Entrepreneurship studies suggest sending signals immediately after their creation (Islam et al., 2018), because conditions change quickly, so their informative value likely decreases over time (Janney & Folta, 2006). The experience achieved by venture capitalists might be relevant today but obsolete tomorrow, after the market changes, so the effect of experience as a signal decreases over time (Hopp & Lukas, 2014). But some signals are effective only if longer gaps occur between them, because if substantial time has passed since the last signal, information asymmetries have increased for outsiders. Private equity placements can more effectively reduce information asymmetries between ventures and equity investors if the last one was issued long ago (Janney & Folta, 2003). Other signals achieve varying effectiveness over the life cycle of a venture, as information asymmetries decrease over time, and as firms mature (Ragozzino & Blevins, 2016). For example, entrepreneurs’ founding experiences are more effective in the first funding round of a new venture but ineffective in subsequent funding rounds (Hoenen et al., 2014; Ko & McKelvie, 2018).

Signal Portfolios

Multiple signals tend to interact, operate in concert, and influence one another, in terms of their individual effectiveness. Our review indicates that signal portfolios offer a pertinent perspective for entrepreneurship signaling research, especially in the past decade, and three prevalent mechanisms describe these interactions: signal amplification, signal complementarity, and signal conflict.

Signal amplification is the extent to which signals increase attention to other signals in the same portfolio. In entrepreneurship contexts, many startups compete for resources from a few key stakeholders, who can be overwhelmed by the vast number of signals, leading to poorly understood or unnoticed signals. Signal amplification can work in two directions. First, strong signals (e.g., affiliation with an accelerator) might unlock the value of another, weaker signal, such as a new product introduction, which otherwise would remain unnoticed in isolation (Plummer et al., 2016). Similarly, media coverage can boost attention to weaker signals, such that they even might become more effective than strong signals (Vanacker et al., 2020). Second, rhetoric and emotional language signals can boost attention to strong signals, such as prototypes, and increase their visibility (Steigenberger & Wilhelm, 2018).

Signal complementarity pertains to whether multiple signals provide different information. If signals in a portfolio complement one another, they likely interact positively; if they provide overlapping, redundant information, they might interact negatively (Chen et al., 2018). For example, granted patents and successful crowdfunding campaigns provide different relevant information. These complementary signals thus reduce dual uncertainties about a new venture’s product and market risks (Roma et al., 2017). Different information also might come from internal versus third-party signalers (Ozmel et al., 2013). Entrepreneurs’ experience can signal credibility, and it also can be complemented by third-party signals, such as positive consumer comments on discussion boards (Courtney et al., 2017). A signal might compensate for the lack of another signal too, if they both provide similar information, such that government grants might compensate for a lack of patents for example (Islam et al., 2018). However, a portfolio with multiple signals that provides overlapping information might produce adverse effects. If they encounter two signals that provide information about the same product characteristics, receivers might react negatively to being forced to exert unnecessary effort to process redundant information (Steigenberger & Wilhelm, 2018).

Signal conflict arises when one signal is inconsistent with others, which typically reduces the signaling value of the portfolio (Chan et al., 2020). A founder CEO is a signal; a higher ratio of founders on the board is another. In combination, these signals are inconsistent, implying the risk that the founder might disagree with non-founder directors and exert more pronounced influences, such that group consensus may suffer (Wang & Song, 2016). Other conflicting signals include combinations of a new venture’s entrepreneurial orientation and managers’ external board activities, which signal that the venture’s resource dependency and lack of attention likely conflict with the high resource and attention needs of new ventures with strong entrepreneurial orientations (Mousa et al., 2015). However, some research predicts that conflicting signals could be beneficial, such as when entrepreneurs’ combined failure and success experiences indicate the founder has had opportunities to learn from failures and gain credibility (Huang et al., 2022).

Receiver

Receivers lack private information about the quality of a venture and seek it to be able to make informed assessments. Entrepreneurship studies identify various receivers, including investors (Ahlers et al., 2015), employees (Söderblom et al., 2015), directors (Acharya & Pollock, 2013), banks (Eddleston et al., 2016), suppliers and buyers (Luo et al., 2020), governments (Zhou et al., 2020), partners (Ozmel et al., 2013), and acquirers (Ragozzino & Reuer, 2011). Different receivers attend to and interpret signals in various ways (Connelly et al., 2011). The considerable ambiguities in entrepreneurship research regarding the underlying constructs make it difficult to explain such differences though. We note four relevant constructs: ability, identity, objective, and irrationality.

Receiver ability is the extent to which receivers are capable of noticing and understanding signals. They can react only if they notice and understand the signal, but receivers vary in this ability, due to their unique knowledge, backgrounds, and experiences. First, receivers differ in their ability to collect and process available signals. Such differences might reflect the receivers’ cognitive resources (Edelman et al., 2021), such that investors’ education and experience determine the number of signals they attend to, because less knowledgeable investors lack the capacity to process a wide range of signals (Butticè, Collewaert et al., 2021). Similarly, investors without prior coaching experience may fail to notice signals that suggest the coachability of entrepreneurs (Ciuchta et al., 2018). Second, receivers may notice a signal but fail to understand its intended meaning. With their finance backgrounds, debt and equity investors likely understand the signaling value of industry-specific experience attained by venture capitalists; employees might lack the specialized knowledge needed to understand this signal (Vanacker & Forbes, 2016). But even within a group of investors, heterogeneity exists in their comprehension ability. As Piva and Rossi-Lamastra (2018) explain, equity crowdfunders who lack knowledge in a certain industry may fail to grasp important signals about entrepreneurs’ industry-specific work experience.

Receiver identity refers to receivers’ similarities with signalers and the effects on their interpretations of signals. Similarities tend to be favorable and yield more positive interpretations. In particular, receivers perceive signals sent by similar others as more credible, because they regard members of the same group more favorably and as more trustworthy (Claes & Vissa, 2020). Thus, business angels tend to regard signals from other angels as more useful and informative than signals from crowd investors (Wang, Mahmood et al., 2019); venture capitalists perceive signals as more credible if they come from venture capitalists with whom they have conducted joint deals before (Hopp & Lukas, 2014). Moreover, receivers might actively look for signalers who seem similar, to accelerate trust formation and a productive working relationship (Claes & Vissa, 2020). A prestigious board looks for prestigious new directors (Acharya & Pollock, 2013), and prestigious investors in turn look for firms with prestigious boards (Certo, 2003).

With regard to receiver objectives, we note the extent to which receivers’ institutional logic influences their interpretation of signals. Distinct institutional logics produce diverse needs, desires, values, motives, and expectations (Kleinert et al., 2021; Scheaf et al., 2018). Receivers thus form different objectives that influence their interpretation of signals. First, they might react only to those signals that match their own institutional logic. If receivers embrace an economic return logic, they prefer signals that indicate return potential, such as financial forecasts or patents, but if other receivers adopt a community logic, they might ignore such signals (Goethner, Luettig et al., 2021; Scheaf et al., 2018). A social impact logic tends to mark impact accelerators and microfinance investors, so these receivers interpret signals about entrepreneurs’ social credentials as more critical than signals about their economic quality (Anglin et al., 2020; Yang et al., 2020). Second, receivers with different institutional logics might draw different conclusions from the same signal (Luo et al., 2020). The diverse institutional logics of underwriters, venture capitalists, institutional investors, and retail investors lead them to draw different conclusions about corporate philanthropy signals. Receivers with long-term expectations interpret corporate philanthropy positively; receivers who care about short-term returns regard it as a signal of inefficient resource usage (Jia & Zhang, 2014).

Finally, receiver irrationality relates to how much receivers’ cognitive biases affect their interpretations of signals. Biased interpretations often arise from receivers’ prejudices or stereotypical thinking about a signaler, which diminishes the effect of signals generated by certain groups (Fischer & Reuber, 2007). Particularly problematic in entrepreneurship contexts, gender-based stereotypes often mislead receivers into perceiving economic signals sent by women or social signals sent by men as less credible (Yang et al., 2020). Similarly, receivers interpret management experience as beneficial for male founders of technology ventures but not so for female entrepreneurs (Kleinert & Mochkabadi, 2021). Receivers also frequently rely on heuristics to process information more efficiently, which can lead to less rational interpretations (Kackovic & Wijnberg, 2020). Consumers usually take cognitive shortcuts to assess product features, such as adopting other consumers’ purchasing decisions (Wehnert et al., 2019). Other biases result from emotions and non-economic rationales; firm owners who have owned a company for decades likely become emotionally attached to it, so they discount credible quality signals about potential successors (Dehlen et al., 2014).

Environment

The signaling environment is the context in which signalers send signals, and receivers receive and interpret them. It can pertain to industries (e.g., Epure & Guasch, 2020), regulations (e.g., Bell et al., 2008), or cultures (e.g., Jia & Zhang, 2014), as well as other environmental factors that influence signaling processes (Connelly et al., 2011). Although entrepreneurship research generally agrees on the importance of the signaling environment, we find few constructs that clearly categorize different environmental influences. Based on our review, we productively distinguish environmental uncertainties, environmental norms, and environmental noise.

Environmental uncertainties reflect contextual factors that influence information asymmetries between new ventures and receivers. New ventures often operate in highly dynamic, unpredictable, complex environments (Huang et al., 2022; Lester et al., 2006), which affect the level of information asymmetry. In newer industries, such as the emerging clean-tech industry (Doblinger et al., 2019) or the Internet market in the 2000s (Hsu, 2007), entrepreneurs confront extreme operational and commercial uncertainties and thus benefit more from prior founding experience or license agreement signals than do firms competing in mature industries. Furthermore, country-related differences can be relevant, such that in some countries, such as those with less developed markets, for example, Brazil (Lanchimba et al., 2021), information asymmetries may be more severe, and quality signals thus are more relevant. Such country-related environmental uncertainties are especially problematic when new ventures opt for an IPO in a foreign country. They likely encounter unique home country-related uncertainties; for example, the level of economic freedom in a new venture’s country of origin strongly determines information asymmetries and renders insider ownership signals more important (Bell et al., 2008). Finally, environmental uncertainties depend on the proximity between signalers and receivers. If acquirers, exchange partners, or IPO investors also function in industries relevant to the new venture or in close geographic proximity to it, environmental uncertainty should be lower, which can make quality signals less important (Berns et al., 2021; Ragozzino & Reuer, 2011; Reuer & Ragozzino, 2012).

Environmental norms are expectations, created by environments and imposed on signals. In general, conformity with industry, regulatory, or cultural norms increases signal effectiveness. As Khoury et al. (2013) show, social capital signals from a new venture should conform with precedents set by other companies in the same industry, because exhibiting much less social capital than industry peers tends to be penalized by IPO investors. Regulatory norms can create different expectations about investor protections too; due to the lower transparency and listing standards in the United Kingdom compared with the United States, U.K. investors expect signals of investor protections (e.g., board independence), while U.S. investors do not (Moore et al., 2010). Relatedly, cultural norms can produce completely different interpretations of signals (Zhou et al., 2020). Jia and Zhang (2014) identify a stigma in China against philanthropic donations, which instead tend to be perceived as positive signals in other countries. Even if CEO power may unintentionally signal risks of managerial opportunism, it can have positive effects in cultures in which unequal power distributions are well accepted (Krause et al., 2021).

Environmental noise constitutes all the various contextual factors that might disturb signal observability. Such noise often occurs for receivers confronted with information overload from the many startups simultaneously providing signals (Plummer et al., 2016; Steigenberger & Wilhelm, 2018), such as on crowdfunding platforms (Huang et al., 2022), which leaves them unable to process or interpret available signals accurately. Sometimes even strong signals might remain unnoticed, so entrepreneurs need strategies to make signals more noticeable (Plummer et al., 2016). Similarly, in hot IPO markets, investors may be overwhelmed by the vast information associated with the large number of new ventures that go public at the same time, so new ventures need highly observable signals in these environments to be noticed (Gulati & Higgins, 2003).

Discussion: Signaling Constructs in Entrepreneurship Contexts

By taking stock of prior entrepreneurship signaling research, we create a taxonomy of clearly defined signal constructs. In this section, we leverage that taxonomy to increase construct clarity even further, by delineating boundary conditions, relationships among constructs (Suddaby, 2010), and complementary theories that frequently get integrated with signaling theory.

Boundaries of Signaling Constructs

Theory development requires specification of boundary conditions (Shepherd & Suddaby, 2017), which refer to the contextual circumstances in which constructs are more or less applicable (Suddaby, 2010). The delineation of boundaries is particularly relevant when theories from other fields apply to entrepreneurship (Zahra, 2007). To establish them, it is pertinent to ask questions about who, where, and when dimensions (Busse et al., 2017; Welter, 2011; Whetten, 1989); accordingly, we address these questions for signaling constructs in entrepreneurship contexts.

Who Dimension

The “who” dimension refers to the signalers and receivers as key actors involved in the signaling process. For example, the liability of newness—such that new ventures typically lack a developed reputation (Certo, 2003; Stuart et al., 1999), unlike incumbent firms that can leverage their established reputation to signal quality to outsiders (Coff, 2002; Deephouse, 2000)—represents a boundary condition that drives new ventures to turn to third-party signalers such as venture capitalists (Lee, Pollock et al., 2011), accelerators (Plummer et al., 2016), underwriters (Williams et al., 2010), or external partners (Stuart et al., 1999) to indicate the credibility of the affiliated new venture and compensate for its lack of reputation (Colombo et al., 2019). Accordingly, liability of newness may render third-party signalers particularly important in the entrepreneurship context, as is evident by the vast number of studies examining third-party signalers (around 48% of studies in our sample).

Another who-related boundary condition pertains to the entrepreneurial background of receivers. Some receivers are closely integrated into entrepreneurship contexts, such as accelerators, venture capitalists, or business angels, so they are accustomed to assessing uncertain new ventures. Their entrepreneurial backgrounds set a boundary condition for constructs such as signal messages, receiver ability, and environmental noise. Because these receivers understand the critical relevance of the entrepreneurial team, they demand credible signals of the founders’ experience (e.g., Hsu, 2007; Ko & McKelvie, 2018). An entrepreneurial background also might increase a receiver’s ability to notice specific signals, such as an entrepreneur’s coachability (Ciuchta et al., 2018) or a venture capitalist’s industry experience (Vanacker & Forbes, 2016), whereas receivers without such an entrepreneurial background are likely to miss this information. Finally, receivers with an entrepreneurial background might be less disturbed by environmental noise, because they have learned how to navigate in noisy entrepreneurial environments.

Where Dimension

The “where” dimension refers to the manifold locations in which signals can be sent and received in entrepreneurship contexts (Welter, 2011). First, the entrepreneurial ecosystem may be a location-related boundary condition for signal costs, signal strength, and receiver ability constructs. In well-developed entrepreneurial ecosystems, new ventures benefit from a comparatively easy access to resources, such as human and financial capital. As a result, these new ventures can obtain human and venture capital-related signals at lower costs, so the strength of those signals diminishes (Kleinert et al., 2021). In contrast, in less developed entrepreneurial ecosystems, the strong competition for scarce resources limits accessibility to signals and makes it more difficult for receivers to understand the meaning of certain signals. For example, knowledge deficits experienced by debt financiers in Ghana prevent them from understanding new ventures’ investments in innovations as a quality signal (Robson et al., 2013). Strict regulations also can hamper the accessibility of important signals; access to patents is particularly difficult in European ecosystems, so patents become more costly, stronger signals there than in other ecosystems (Useche, 2014).

Second, exchanges on platforms have followed from developments in digitalization, so new ventures often interact on online platforms with heterogeneous, geographically dispersed, and anonymous groups of signal receivers, such as donors, lenders, or investors (e.g., Ahlers et al., 2015; Anglin et al., 2020). Unlike targeting, say, a single selected venture capitalist, it is not possible for entrepreneurs on digital platforms to establish dedicated signals that will resonate with all of the many, diverse receivers on online platforms. Instead, messages that appeal to a broad audience, such as credible narratives about entrepreneurial behaviors or identities, may emerge as more important in these digital entrepreneurial settings (Calic & Shevchenko, 2020; Moss et al., 2015). Furthermore, exchanges on online platforms are subject to different regulations that inform environmental uncertainty (Huang et al., 2022). For example, equity crowdfunding platforms verify information and even select new ventures on the basis of their quality signals, so the information asymmetries for investors are greatly reduced (Kleinert et al., 2021). But platforms for token offerings are largely unregulated (Fisch, 2019), which can create not only heightened uncertainty but also a risk that low quality ventures imitate the signals of higher quality ventures without incurring penalty costs, which implies inefficient signaling (Momtaz, 2021b).

When Dimension

The “when” or temporal dimension is manifest in the venture stage, which may be a critical boundary condition for several signal constructs. When entrepreneurship studies use signaling theory to investigate a range of companies with widely varying ages, key implications arise for signal cost, signal timing, and receiver objectives. When new ventures transmit rhetoric-based signals, they risk penalty costs such as reputational damages (Anglin et al., 2018; Moss et al., 2015; Steigenberger & Wilhelm, 2018). Those penalty costs should vary with the venture stage though. Late-stage ventures engaged in IPOs rely critically on their reputations and are liable for the accuracy of the information in their IPO prospectus (Payne et al., 2013). Thus, they may be especially reluctant to risk false signaling, whereas earlier stage ventures have comparatively less to lose. The effectiveness of signals varies between early- and late-stage ventures too, not just because information asymmetries diminish over time (Kleinert et al., 2020) but also because late-stage receivers, such as IPO investors, seek different signals than early-stage receivers, such as crowdfunders (Anglin et al., 2018).

The venture stage also might alter the impacts of internal signaler, signal message, and signal intentionality constructs. Every construct is tied to a certain level of analysis (Klein et al., 1994). In an entrepreneurship context, internal signalers are typically analyzed at the individual level (e.g., entrepreneur) or organizational level (e.g., new venture). At a very nascent stage, the signaler tends to be an individual entrepreneur or team of founders (Lim & Busenitz, 2020); a formal organization might not have been established yet. Therefore, the entrepreneurs represent figureheads, more closely linked to venture success than at any other stage. Unique signal messages thus are highly relevant, such as entrepreneurs’ intentions (Elitzur & Gavious, 2003), commitment (Vismara, 2016), or other credibility-linked traits (Huang et al., 2022). Conceivably, at this early stage, entrepreneurs may be less purposeful in their signaling strategy, and the signals are unintentional, such as entrepreneurs’ characteristics or activities performed in the past.

Relational Perspective on Signaling Constructs

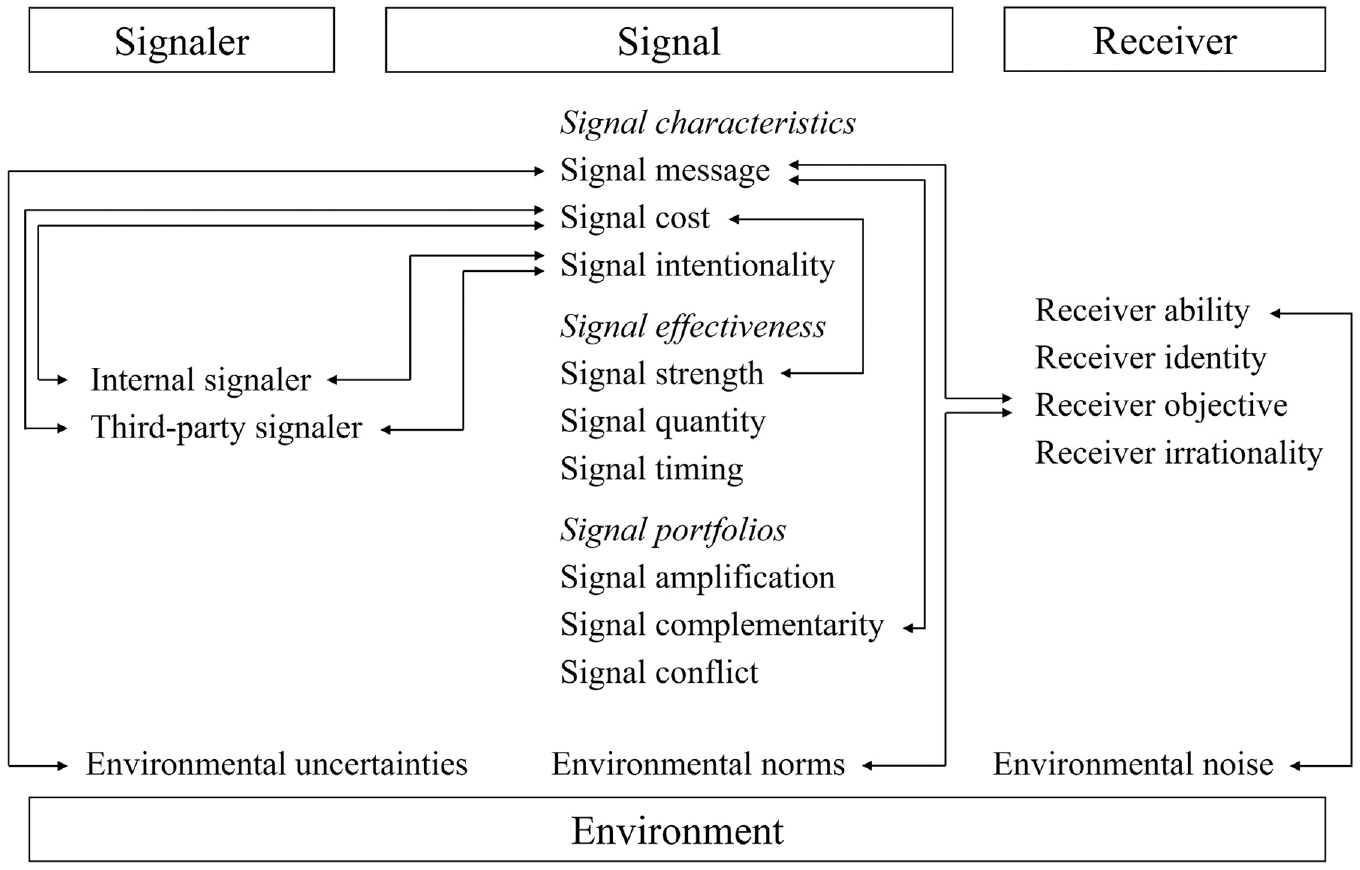

In signaling theory, constructs are always part of the signaling process in which the signaler sends a signal to the receiver, within the signaling environment (Connelly et al., 2011). Thus, signal constructs do not exist in isolation and instead relate to other constructs. To develop construct clarity, we must explore the relationships among constructs (Suddaby, 2010), some of which appear particularly important, as depicted in Figure 2.

Important relationships among signaling constructs.

Signaler-related constructs should interlink with signal costs. When third-party signalers, such as venture capital firms, endorse new ventures (e.g., Pollock et al., 2015), they typically face penalty costs if the quality of the endorsed new venture turns out to be insufficient (Gomulya et al., 2019). But if these third-party signalers’ financial returns are tied directly to an affiliated venture’s success, they may be willing to pay some implementation costs to send a signal (Arcot, 2014). Internal signalers, such as entrepreneurs, regularly pay implementation costs for their signals, such as investing psychic energy to obtain education or develop founding experience (Ko & McKelvie, 2018; Piva & Rossi-Lamastra, 2018). Yet some studies suggest that internal signalers might also be subject to penalty costs, for example, when issuing rhetorical signals (Payne et al., 2013). Internal and third-party signaler constructs may also feature a logical connection to signal intentionality. Third-party signalers typically send unintentional signals about a venture (Milosevic, 2018); a venture capitalist does not invest in a new venture solely or even primarily to send a signal (Shafi et al., 2020). The signal is usually an unintentional outcome of the capitalist’s effort to generate a return from an investment. For internal signalers, intentionality is more ambiguous. Entrepreneurs could apply for a patent to protect their intellectual property, such that the associated signal is unintentional, or they could pursue a patent explicitly to signal their technological quality (Hoenig & Henkel, 2015).

The signal message likely relates to several constructs, including signal complementarity. It is a characteristic of the signal; in a portfolio of signals, various signals can convey distinct or overlapping messages. If they are distinct, the multiple signals can complement one another (Chan et al., 2020; Islam et al., 2018), but overlapping messages imply redundancies (Steigenberger & Wilhelm, 2018). The signal message also might relate to the receiver objective, because the signal message largely determines whether the signal conforms with receivers’ institutional logic. If the message pertains to a new venture’s social quality, it conforms with the expectations of social impact accelerators (Yang et al., 2020). Signals with broad messages, such as government subsidies, can be more flexible and address the institutional logics of multiple receivers, such as potential employees and investors (Söderblom et al., 2015). Media coverage tends to convey broad messages, such as about the validity of an entrepreneurial offering and its return potential, so it is widely effective for receivers with different objectives, such as crowdfunding backers and equity investors (Scheaf et al., 2018). Moreover, the signal message may relate to environmental uncertainties, some of which require specific messages to be effective. If technological capabilities were a major source of uncertainty, then technical white papers and high-quality source codes become necessary signals, because they offer information about technological quality (Fisch, 2019). Sales alliances, which represent a more important signal of market quality, instead may be more effective for new ventures that operate in industries dominated by greater demand uncertainty (Kleinert et al., 2021).

Another relation likely arises between signal cost and signal strength. In particular, signal cost is a characteristic that often correlates with signal strength, which relates to the signal’s effectiveness. The costlier it is to obtain a signal, the less likely it is that poor quality ventures will imitate that signal, and accordingly, higher signal costs are often associated with stronger signals. For example, business debt is a stronger signal than personal debt because it has costlier underpinnings (Epure & Guasch, 2020). However, this link depends on several factors. In noisy environments, receivers may be unable to identify the underlying cost of different signals, so less costly signals may be effective (Steigenberger & Wilhelm, 2018). In a portfolio of signals, lower-cost signals also may dominate higher-cost signals; if crowdfunding success is complemented by other signals for example, it can be more effective than venture capital backing (Roma et al., 2021), and when unrealized performance is amplified by media attention, it can become more effective than realized performance (Vanacker et al., 2020).

Environmental constructs also appear interlinked with receiver constructs. For example, receiver ability may be connected to environmental noise, because in a noisy environment, a receiver is less able to observe signals (Gulati & Higgins, 2003). This receiver’s ability depends on the noisiness of the environment (Plummer et al., 2016). Regarding the link between receiver objectives and environmental norms, we note that receivers’ interpretations of signals depend on an institutional logic, which might be shaped by geographic or industry norms. For example, a country’s legal norms largely determine the institutional logic of IPO investors; low transparency standards could leave them concerned about investor protection, such that they demand more signals pertaining to corporate governance (Bell et al., 2012).

Complementary Theoretical Lenses

Signaling theory is often combined with other theories derived in a wide range of fields (e.g., psychology, sociology, organizational behavior), which can produce unique theoretical insights but also create ambiguities (Mayer & Sparrowe, 2013). We note some important implications of frequently adopted complementary theories, for signaling theory in entrepreneurship research in general and for specific signal constructs in particular. Many studies integrate signaling theory with institutional theory (DiMaggio & Powell, 1983; Dowling & Pfeffer, 1975), which suggests that organizations gain legitimate status by conforming to the social norms, values, and beliefs that dominate an environment. Legitimacy is important for new ventures, with influences on their resource acquisition, performance, and survival (Suchman, 1995). Institutional theory thus has implications for multiple constructs, including the signal message, receiver identity, and environmental norms. Signal messages usually provide information about unobservable qualities, but studies that integrate institutional theory argue that new ventures also seek to signal their legitimacy (Lanahan et al., 2021), such as with heterogeneous management teams or prestigious boards (Zimmerman, 2008). As a theoretical lens, institutional theory informs the receiver identity construct, because it predicts that interpretations of signals constitute social judgments that depend on whether the status of the receiver and the sender match (Certo, 2003). Finally, institutional theory illuminates the environmental norms construct (Moore et al., 2010). For example, Bell et al. (2012) leverage institutional theory to explain how legal norms in different countries create normative expectations about investor protection and thus influence IPO investors’ interpretations of signals.

Another frequently used complementary theoretical perspective is the resource-based view (e.g., Daily et al., 2005; Partanen & Goel, 2017), which posits that companies develop resources that differentiate them from other companies and are sources of competitive advantage (Barney, 1991). It has notable implications for the signal message construct. That is, new ventures can signal their superior resources (Abeysekera, 2019), such as by maintaining larger boards, which thus constitute a potential source of competitive advantage (Daily et al., 2005). Following this logic, the resource-based view would shift the focus from quality to resource superiority. However, the resource-based view raises issues regarding the distinction between signals and resources. Do high-quality source codes, sales alliances, patents, and other factors studied in entrepreneurship signaling research really represent effective, costly signals, or are they simply valuable resources? Patents are both costly signals of quality and valuable resources, because they provide legal protection and competitive advantages (Hoenig & Henkel, 2015). Both arguments effectively explain why receivers may find patent-holding new ventures more attractive (Hsu & Ziedonis, 2013). Overall, few studies isolate signaling effects from resource-based explanations empirically. Those that do tend to confirm signaling effects, by identifying the stronger effects that arise when the new venture’s economic quality is more uncertain, as in the case of less developed new ventures (Colombo et al., 2019; Hoenig & Henkel, 2015; Stuart et al., 1999).

A growing body of entrepreneurship research also complements signaling theory with a cognitive view (e.g., Kackovic & Wijnberg, 2020), which suggests that people use heuristics to process information in uncertain and complex environments (Tversky & Kahneman, 1974). The cognitive view might have implications for various signal constructs, including receiver irrationality, receiver ability, signal strength, and signal amplification. Signaling theory predicts that receivers function as rational actors who always attend to observable signals (Bergh et al., 2014), but a cognitive view anticipates boundaries on receivers’ rationality, which might be relevant for the receiver irrationality construct. For example, Edelman et al. (2021) demonstrate that receivers prefer low-effort strategies, so they fail to attend to all available signals. The cognitive view also relates to the receiver ability construct, in that receivers with greater (general) human capital are more aware of their cognitive limitations, better able to overcome biases, and capable of attending to more signals (Butticè, Collewaert et al., 2021). With regard to the signal strength construct, heuristics can help explain why weak signals are effective, such as when they become highly salient and evoke processing by receivers (Mahmood et al., 2019; Tumasjan et al., 2021). Finally, the cognitive view might be relevant for signal amplification; here again, heuristics can explain the importance of attention-boosting signals that prevent other relevant signals in a portfolio from being overlooked (Steigenberger & Wilhelm, 2018; Vanacker et al., 2020).

A growing number of studies also cite gender role congruity theory (Alsos & Ljunggren, 2017; Kleinert & Mochkabadi, 2021; Yang et al., 2020), which cautions that people evoke more favorable judgments when they behave congruently with their gender roles (Eagly & Karau, 2002). This theory is especially relevant for the receiver irrationality construct. Entrepreneurship signaling research thus integrates gender role congruity theory to account for gender stereotypes and cognitive biases in receivers’ interpretation of signals (Eddleston et al., 2016; Liao, 2021), such as when receivers perceive signals that convey a particular message as more relevant, depending on the signaler’s gender.

Moving Forward: Research Avenues

In this section, we outline a novel theory-based research agenda that our taxonomy and discussion offer for further research.

Underresearched Construct-Related Research Opportunities

According to our taxonomy, some signal constructs require further clarification and research attention. In particular, we recommend further exploration of signal strength. Prior research tends to distinguish strong and weak signals theoretically (Tumasjan et al., 2021), but the true correlation between a signal and a new venture’s unobservable quality can be confirmed only over the long run (Bergh et al., 2014). We need to determine the extent to which different strong and weak signals persuade a receiver, but also the extent to which they correlate with new ventures’ long-term performance. Some initial research indicates that new ventures with strong signals, such as managerial experience or affiliations with prestigious university partners, outperform non-signaling firms over time (Colombo et al., 2019; Gimmon & Levie, 2010), but empirical evidence of this correlation is scarce for weak signals. Only Tumasjan et al. (2021) offer initial evidence that Twitter sentiments (weak signal) appear uncorrelated with the long-term investment success of a firm.

We also recommend clarification of the signal quantity construct, with the recognition that signals often vary in quantity, even for a single venture, such as one with more than one alliance partner (Hoehn-Weiss & Karim, 2014). A dominant view in entrepreneurship research is that effectiveness decreases with the number of signals (Mousa & Reed, 2013), but it is questionable if this trend always holds good (e.g., Pollock et al., 2010). Research efforts might seek to uncover patterns across multiple signals that increase or decrease in value. Another crucial consideration pertains to how signal quantity is measured. Some studies measure the number of signals from multiple market participants (e.g., Mousa & Reed, 2013), but others only count signals from the venture (e.g., Hoehn-Weiss & Karim, 2014). A better understanding of this construct requires analyses of potential U-shaped relationships to determine “optimal quantities” of signals. Few studies in our sample feature such analyses (cf. Anglin et al., 2020), so it is difficult to compare the results for signal quantity across studies.

We also call for further clarification of signal conflict. Most considerations of how signals interact center on their complementary or substitutive relationships (e.g., Courtney et al., 2017; Steigenberger & Wilhelm, 2018), but conflicting signals represent a relevant and potentially frequent concern for new ventures. The sources of such conflicting signals represent a pertinent question, such as when signals from internal versus third-party signalers come in conflict. Other considerations might address signal messages that contain conflicting signals, such that one indicates the superior quality of a new venture (Bapna, 2019) but another points to the poor trustworthiness of its founders (Calic et al., 2021). Contemporary entrepreneurship research disagrees about whether signal conflicts are necessarily negative (Wang & Song, 2016) and if conflicting signals even might be positive (Huang et al., 2022). This pivotal question also raises a related question: How might new ventures leverage conflicting signals to their advantage?

Receiver-related constructs are generally less understood than other constructs; receiver identity especially requires further clarification. Entrepreneurship signaling research has established that similarities between receivers and signalers influence the interpretation of signals, but it has not specified precisely which similarities are important. Group membership is a frequently cited identity characteristic (Acharya & Pollock, 2013; Wang, Mahmood et al., 2019); softer characteristics likely are relevant too, such as shared interests, attitudes, or appearances (Momtaz, 2021a). In our review, we note a key ambiguity, related to the question of why similarity might affect interpretations of quality signals. Some studies support a rational perspective, suggesting that receivers can better assess the quality of similar peers (Certo, 2003), and others propose that homophily encourages trust formation and easier communication, while also evoking inherent preferences for an in-group (Claes & Vissa, 2020; Wang, Mahmood et al., 2019). Continued research should disentangle these varied explanations to clarify the receiver identity construct.

Environmental noise is another emerging, relatively poorly understood construct. The new venture context is generally a noisy one (Huang et al., 2022; Plummer et al., 2016), but a clearer idea of what constitutes noise in this environment could help scholars identify and distinguish settings with more and less noise. For example, noise might be a greater concern on crowdfunding platforms (Steigenberger & Wilhelm, 2018) than for venture capital. This construct has remained theoretical thus far, and it clearly requires empirical validation. Researchers could derive concrete measures of entrepreneurship-related noise, perhaps based on the number of competing firms or available signals. We also lack a clear understanding of how new ventures should maneuver in noisy environments. Although signal amplification appears to offer a solution (e.g., Plummer et al., 2016), we need more research to uncover alternative strategies that new ventures can leverage to succeed in noisy environments.

Boundary-Related Research Opportunities

Some constructs in our taxonomy have universal relevance for signaling research (e.g., signal costs). The applicability of other constructs instead depends on the maturity of the firm. As ventures mature, they suffer less from the liability of newness and develop their own reputations. Do these mature companies also depend less on the reputations evoked by third-party signalers? Signal quantity considerations may differ depending on the maturity of a venture too. Early-stage ventures in particular lack track records and must depend on signals (Kleinert et al., 2020), but they experience the strongest resource constraints, and these two factors may demand different optimal signal quantities than are required by more mature companies. Thus, research should explore how optimal signal quantities differ across a firm’s lifespan. Other constructs may be of less importance in later venture stages too, such as environmental noise, which diminishes as some members of the initially large population of startups fail to maintain their operations (Plummer et al., 2016). Our understanding of these signal constructs would benefit from a clarification of when (i.e., at which venture stage) specific signal constructs such as environmental noise lose their applicability or become less important. One option would be to follow the method proposed by Anglin et al. (2018) and compare the applicability of signal constructs across venture stages. These authors show that rhetorical signals that share messages about psychological capital are effective in early stages (crowdfunding) but do not affect more mature companies undergoing their IPO. Comparative research into applications of signal constructs to newer versus more developed ventures could help determine their boundary conditions more definitively.

We also need tests of the extent to which certain signal constructs apply across different geographic contexts; the generalizability of signal cost, signal strength, and receiver ability across different entrepreneurial ecosystems seems particularly questionable. Rather than studies of specific geographic regions, such as the developed U.S. market (Bruton et al., 2009) or the emerging Chinese market (Chen et al., 2018), we recommend direct comparisons of the applicability of different signaling constructs across heterogeneous locations and entrepreneurial ecosystems (Useche, 2014). In general, we note that studies rarely consider the conditions in which signal constructs apply, though as an exception, Huang et al. (2022) study signals on different crowdfunding platforms and identify the uncertainty of the platform’s business model as a boundary condition for signals of entrepreneurs’ credibility. Signaling theory in entrepreneurship contexts could be enhanced by research that accounts more explicitly for boundary conditions.

Relational Research Opportunities

There exist ample research opportunities to shed further light on the relationships between different signaling constructs. First, we need a better understanding of the link between internal signalers and penalty costs. A central assumption involving penalty costs is that signalers get penalized for false signals, but this assumption has not been sufficiently examined; to our knowledge, only Gomulya et al. (2019) address it, for third-party signalers. Emerging entrepreneurship research examines rhetoric signals issued by internal signalers (e.g., Anglin et al., 2018; Steigenberger & Wilhelm, 2018) that may incur penalty costs too (e.g., Payne et al., 2013), but we lack a clear view of the consequences of such false signaling or the conditions in which penalty costs likely arise. The approach offered by Gomulya et al. (2019) might help clarify this link between internal signaler and penalty costs. Such considerations could be combined with signal timing constructs too, because conceivably, signals based on penalty costs are more effective in later versus earlier stages, when new ventures have gained some reputation that they must put at risk. A related research effort could address penalty costs and signal strength, such as by testing the correlation of penalty cost-based signals issued by internal signalers with new ventures’ long-term performance (e.g., Colombo et al., 2019; Gimmon & Levie, 2010).

Second, illuminating other logical connections should advance understanding of signaling theory in the entrepreneurship context, such as the one between signal timing and signal complementarity. We know that certain signals are more effective when they complement each other, such as crowdfunding success and patents (Roma et al., 2017), prototypes and patents (Audretsch et al., 2012), or product certification and prominent customers (Bapna, 2019), but these benefits might vary depending on when a signal gets introduced into the portfolio. For example, are complementary signals stronger when both appear at the same time or sequentially, and does it matter which signal is introduced first? Another link worth investigating is the one between signal strength and receiver ability. Logically, strong signals have a stronger effect than weak signals; however, weak signals can generate more attention and be more visible, as in the example of Twitter sentiments (Tumasjan et al., 2021). Perhaps less experienced receivers (e.g., potential employees) are even more sensitive to weak signals than experienced receivers (e.g., venture capitalists) (Vanacker & Forbes, 2016). Relatedly, future research may further contribute to our understanding of the relationship between signal strength and environmental noise. While the effectiveness of weak signals is rather unexplored, the noisiness of signal environments offers an initial explanation for why such signals work.

Third, we hope researchers apply our taxonomy to identify additional relevant relationships that can advance signaling theory in entrepreneurship contexts. In any signaling process, there must be a signaler, signal, receiver, and environment, each of which comprises multiple signal constructs. However, studies frequently focus on one specific aspect of the signaling process. We encourage continued research that takes a more holistic perspective, includes multiple signal constructs, and accounts for how they relate. For example, combining signaler and receiver considerations in specific environmental settings or signal characteristics with different types of signalers could be deeply informative.

Combinations of Theories as Research Opportunities