Abstract

The use of signals to overcome information asymmetries and reduce the uncertainty inherent in resource acquisition has become a prominent theme in new-venture financing literature. In particular, the assessment of a wide range of different information signals, with the aim of conveying a venture’s quality and legitimacy to prospective investors, is receiving increased scholarly attention. With contributions from a broad spectrum of diverse research foci investigating interactions with distinct types of investors, the literature on entrepreneurial signaling in new-venture financing has become fragmented, and this is harming further development of the field. This study systematically reviews the different literature streams on entrepreneurial signaling to provide a more integrative framework, which can contribute to the cumulative and evidence-based body of knowledge about the role of entrepreneurial signaling in new-venture financing. Furthermore, the authors identify critical sender-, signal-, receiver-, and environment-related boundary conditions that influence the signaling effectiveness. In this way, the authors identify gaps in the existing literature and map directions for future research.

Acquiring financial resources is one of the most vital entrepreneurial tasks during new-venture creation (Ko & McKelvie, 2018; Zhang, Soh, & Wong, 2010). Financial resources not only enable entrepreneurs to exploit identified opportunities but also contribute to the venture’s ability to realize profits (Shane, 2003). However, entrepreneurial efforts to obtain financing from external sources frequently fail due to the difficulties associated with the inherent information asymmetries between entrepreneurs and prospective investors concerning them and their venture’s quality (Amit, Glosten, & Muller, 1990). Since new ventures typically involve unproven technologies or unfinished products, as well as an unverified market demand, factual evidence regarding the venture’s quality is often unavailable (Murray & Marriott, 1998; Nagy, Pollack, Rutherford, & Lohrke, 2012). Consequently, prospective investors’ evaluations may primarily be based on subjective, nonverifiable claims made by the entrepreneur (Maxwell, Jeffrey, & Lévesque, 2011) before more reliable reputation- or market-related information becomes available (Elsbach & Kramer, 2003). Given these especially challenging circumstances, unless entrepreneurs find a way to effectively overcome the liability imposed by the novelty of their ventures, they face a high probability of failure (Baron & Markman, 2003; Shane & Cable, 2002).

One possible approach for effectively mitigating information asymmetries and attracting prospective resource providers is the use of signals to convey a venture’s qualities (Ahlers, Cumming, Günther, & Schweizer, 2015; Arthurs, Busenitz, Hoskisson, & Johnson, 2009; Connelly, Certo, Ireland, & Reutzel, 2011). Regarding the decision-making process, resource providers typically try to evaluate two hidden attributes to decide whether the addition of their financial resources would contribute to a successful investment outcome; first, prospective investors examine the quality of a venture’s economic activities, and second, they try to assess the firm’s capabilities and skills to execute these activities (Ahlers et al., 2015; Courtney, Dutta, & Li, 2017; Steigenberger & Wilhelm, 2018). Accordingly, research in this domain is primarily driven by the question of which venture features entrepreneurs need to display to prospective investors to communicate such qualities, thereby reducing uncertainty and gaining legitimacy and resources.

Despite an increasing body of literature assessing signals in the entrepreneurship context over the past three decades, little review and/or consolidation of entrepreneurial signaling has occurred. As such, there is a limited systematic understanding of what and how to signal to prospective investors to gain legitimacy and financial resources. Since the literature on entrepreneurial signaling in the context of new-venture financing has been generated across different research streams, dealing with heterogeneous target audiences ranging from crowd to initial public offering (IPO) investors, the fragmented nature of the existing research has made it difficult for scholars to draw generalizable conclusions or accumulate knowledge about the potential of the use of signals for entrepreneurs. For instance, while literature drawing on signaling theory in the context of angel investors predominantly focuses on attributes that display behavioral intentions (e.g., Maxwell & Lévesque, 2014), prospective IPO investors place greater emphasis on observable attributes, such as human capital and affiliation signals (e.g., Cohen & Dean, 2005; Colombo, Meoli, & Vismara, 2019). Given the wide variety of signals, which are assessed in diverse contexts ranging from the high-noise environments of crowdfunding to the lower- or lowest-noise stages of venture finance, the current body of knowledge lacks an integrative framework for organizing these findings.

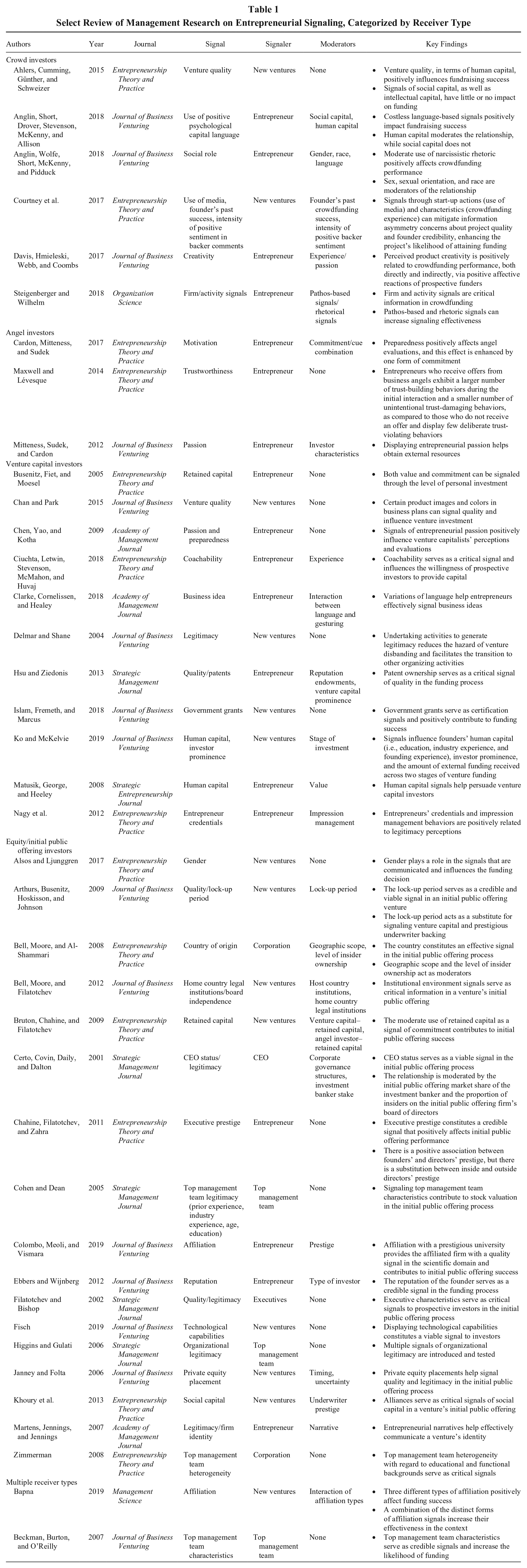

To begin to fill this gap, our systematic review contributes to the entrepreneurship literature in several ways. First, we clarify and assess the role of entrepreneurial signaling in new-venture financing. Second, we offer an integrative framework that organizes and synthesizes the entrepreneurship literature to inform scholars about the current state of research on entrepreneur–investor signaling (see Table 1). Although previous reviews have advanced our understanding of signaling in management research, such as the studies by Connelly et al. (2011) and Taj (2016), they do not provide concise and integrative syntheses of signaling in the context of new-venture financing. Third, as a result of critically analyzing entrepreneurial signaling in the context of new-venture financing at distinct stages of the venture life cycle—ranging from early-stage crowdfunding investments, which are characterized by high-noise environments, to lower-noise environments at the IPO stage—we can now map directions for future research on the role of signaling in entrepreneurial finance. Finally, this review also has implications for the broader literature on the interaction between capital market participants and corporations.

Select Review of Management Research on Entrepreneurial Signaling, Categorized by Receiver Type

Scope and Methods of the Review

Our literature review follows a multistep approach to provide an overview of the relevant studies, including an explicit statement of their research objectives, intervening variables, and methods, which is an explicit and reproducible methodology (Denyer & Tranfield, 2009). Guided by best practice (Denyer & Tranfield, 2009; Drover, Busenitz, Matusik, Townsend, Anglin, & Dushnitsky, 2017; Macpherson & Jones, 2010; Tranfield, Denyer, & Smart, 2003), we followed a multistep approach to conducting this review. First, to identify the relevant literature, we systematically searched the following electronic databases: Business Source Premier, Science Direct, and Wiley Online Library. We used the Boolean search term “signal*” in the abstracts field and “signal* AND entrepreneur*” in the full-text field of peer-reviewed and academic journals. The systematic searches returned 248 and 379 articles, respectively. To ensure that the identified research focused on the entrepreneurship context, we followed the best practices frequently applied in other literature reviews (e.g., Drover et al., 2017) and limited the scope of journals to those concerning management and entrepreneurship. Specifically, our analysis of venture financing research included an interdisciplinary set of 11 leading journals: Academy of Management Journal (AMJ), Academy of Management Review (AMR), Administrative Science Quarterly (ASQ), Entrepreneurship Theory and Practice (ETP), Journal of Business Venturing (JBV), Journal of Management (JOM), Journal of Management Studies (JMS), Management Science (MS), Organization Science (OS), Strategic Entrepreneurship Journal (SEJ), and Strategic Management Journal (SMJ).

Second, we defined content-related inclusion/exclusion criteria in line with the research objectives to determine which papers should be retained for further analysis. The inclusion criterion was that entrepreneurial signaling was a clearly identifiable and empirically studied construct in relation to resource acquisition, even if entrepreneurial signaling was not the main focus of the study. Then, we excluded all papers on entrepreneurial signaling that were unrelated to resource acquisition. This process yielded 65 papers. Next, we examined the reference lists of the selected articles to identify additional work that may have warranted inclusion in the review. This led to the inclusion of three additional articles in the review sample. Consequently, we reviewed 68 papers from 11 different journals.

Results

Crowdfunding Investors

Crowdfunding represents a rapidly growing equity funding mechanism in the entrepreneurial finance landscape and is receiving increasing scholarly interest (e.g., Drover et al., 2017). Equity crowdfunding refers to the type of early-stage funding in which a large number of investors, who are primarily approached via online platforms, each contribute a small fraction of capital for company ownership (Vulkan, Åstebro, & Sierra, 2016). While this type of financing initially faced significant legal challenges, which hampered the expansion of crowdfunding, regulatory changes reduced the barriers for crowdfunding and led to its rapid growth in various countries (Ahlers et al., 2015). However, for entrepreneurs who aim to effectively convey messages to prospective investors and attract resources, crowdfunding represents an especially noisy environment in which numerous signals vie for investors’ attention (Steigenberger & Wilhelm, 2018).

Signals

The literature has examined multiple distinct signals used to successfully transfer information about ventures’ qualities to prospective crowd investors to generate legitimacy and, ultimately, obtain resources. Scholars drawing on arguments of identity theory underline the identity-building function of signaling and document claims that creating an entrepreneur’s identity as a lead user, pioneer, or innovator results in successful crowdfunding campaigns (Oo, Allison, Sahaym, & Juasrikul, 2019). Since prospective investors attach certain favorable attributes to such an identity, lead-user entrepreneurs are assumed to be better at opportunity recognition (Autio, Dahlander, & Frederiksen, 2013), and pioneer or innovator entrepreneurs are associated with better knowledge of the market and its needs (von Hippel, 2005). Other scholars demonstrate that the extent of an entrepreneur’s human or social capital also reflects valuable entrepreneurial attributes, such as capabilities and skills as well as resource access (Ahlers et al., 2015). Furthermore, since crowdfunding projects typically lack a proven track record, prospective investors may rely on other observable characteristics that convey the venture’s quality, such as the founder’s crowdfunding experience (Courtney et al., 2017).

Considering the signaling value of social capital, the literature documents that networks with suppliers (Ahlers et al., 2015) or high-status customers (Bapna, 2019) are also able to reduce uncertainty as these attributes represent reliable and credible sources of information for prospective investors. In addition, Scheaf, Davis, Webb, Coombs, Borns, and Holloway (2018) show that patent ownership constitutes a valuable signal to prospective investors’ evaluations in the context of equity crowdfunding. Since the ownership of patents could represent a critical source of competitive advantage, it could constitute a critical signal of differentiation. Moreover, research drawing on affective events theory, with its explanation of how certain events may engender affective reactions in individuals, finds evidence that perceived product creativity can trigger positive emotions about the venture’s potential, thus contributing to crowdfunding performance (Davis, Hmieleski, Webb, & Coombs, 2017).

Another stream of literature in the context of crowdfunding deals with language-based signals for shaping prospective investors’ assessments. Although scholars traditionally view the cost to acquire and send a signal as a key aspect that differentiates high-quality signalers from low-quality signalers (Connelly et al., 2011), research documents the ability of these costless language-based signals to transmit critical information, thus contributing to crowdfunding performance. For example, scholars report a positive effect on the evaluation of prospective investors when using positive psychological capital language (Anglin, Short, Drover, Stevenson, McKenny, & Allison, 2018) or applying a certain linguistic style (Parhankangas & Renko, 2017). However, the findings of another study in this context clearly show that such costless signals may work only up to a certain point; those researchers report an inverted U-shaped relationship for narcissistic rhetoric and crowdfunding performance (Anglin, Wolfe, Short, McKenny, & Pidduck, 2018).

Contextual factors

Beyond signaling, contextual factors play a critical role in explaining variations in signaling effectiveness. Conceptual work underlines the relevance of these aspects by arguing that the effectiveness of influencing receivers’ behaviors is contingent on the extent to which the signal is perceived and processed (Connelly et al., 2011). Compared with low-noise environments, such as one-on-one negotiations between entrepreneurs and venture capital (VC) investors, where the receiver pays attention to each signal (Spence, 1973, 1974), in the high-noise context of crowdfunding, effectively transmitting information is especially challenging because entrepreneurs need to draw prospective investors’ attention to substantive signals while multiple other signals compete for the target audience’s attention (Drover et al., 2017). Extending traditional signal theory, which assumes that receivers process signals in isolation, Steigenberger and Wilhelm (2018) found support for the claim that certain bundles of signals complement substantive signals by effectively directing the receiver’s attention to them. As such, the rhetorical signals that accompany substantive signals can increase the sender’s credibility and strengthen the effect on crowdfunding performance. Furthermore, research documents that several characteristics of the entrepreneur could affect the sender’s credibility, influencing the effectiveness of the signaling. For instance, drawing on social role theory, Anglin, Wolfe, et al. (2018) demonstrate that the entrepreneur’s race and expressed sexual orientation contribute to signaling effectiveness, while the entrepreneur’s gender does not have a significant effect, which could be explained by the general preference of crowd investors for female-led ventures (e.g., Greenberg & Mollick, 2017). In addition, the entrepreneur’s human capital (Anglin, Short, et al., 2018), past crowdfunding experience (Courtney et al., 2017; Davis et al., 2017), and perceived entrepreneurial passion (Davis et al., 2017) increase the sender’s credibility and the affective state among prospective investors about the venture, which ultimately enhances signaling effectiveness. In addition, a study by Bapna (2019) shows that social proof, evidenced by other investors investing or high-status customers, serves as another critical aspect contributing to the entrepreneur’s credibility and his or her ability to effectively transmit information.

Angel Investors

The term angel investor typically refers to an individual who independently or in collaboration with other angel investors invests his or her own capital in new ventures. Angel investors, who predominantly focus on young, high-growth-potential ventures at their extremely early stages, are playing an increasingly important role in the entrepreneurial finance landscape (Drover et al., 2017). To illustrate their importance, angel investors account for more than 70% of the capital provided to new ventures (Morrissette, 2007). However, despite their practical relevance, research assessing angel investments has attracted only limited scholarly attention compared with other investor groups, such as venture capitalists; consequently, studies on this group represent only a small fraction (about 10%) of our sample.

Signals

From the signaling perspective, entrepreneurs need to overcome particularly high information asymmetries to successfully attract angel investments, as their ventures are typically at an early stage (Murray & Marriot, 1998). Due to the lack of a proven track record and unverified market demand, entrepreneurial signaling in the context of angel investment primarily rests on transmitting signals based on subjective and nonverifiable claims (Maxwell et al., 2011). Therefore, the conceptual literature concludes that one of the key challenges for entrepreneurs at this stage is the development of an engaging narrative that presents the venture in a favorable light and, thus, contributes to its legitimacy (Lounsbury & Glynn, 2001). As such, due to the early stage of the venture, the entrepreneur and his or her characteristics play a central role in developing an appealing narrative to successfully transfer relevant information to prospective investors. Therefore, the empirical literature places great emphasis on messages that convey motivation, capabilities, skills, and personality when investigating entrepreneurial signaling in the context of angel investments. For example, one of the most observable cues of an entrepreneur’s motivation is his or her enthusiasm, which is typically displayed as highly positive emotions about a product, a service, or the venture itself. The communication of such positive emotions through verbal or body language expressions can evoke positive associations in the target audience about the entrepreneur’s capabilities and the venture’s prospects, and ultimately, it could increase the likelihood of obtaining funds (Chen, Yao, & Kotha, 2009). Empirical studies provide support for this perspective by showing that entrepreneurs who display greater enthusiasm are more successful in attracting resources (Cardon, Mitteness, & Sudek, 2017; Mitteness, Sudek, & Cardon, 2012). Furthermore, research on storytelling (Martens, Jennings, & Jennings, 2007) and persuasion (e.g., Rucker & Petty, 2006) suggests that individuals can shape the message they transfer to the target audience to create a certain impression and, ultimately, influence the prospective investors’ behaviors. Accordingly, signals of entrepreneurial motivation, such as preparedness and commitment, could be transferred to create the impression of a well-prepared and determined entrepreneur. The positive influence of both of these signals is supported by empirical evidence (Cardon et al., 2017). Moreover, research further underlines the relevance of the aforementioned signals, which are frequently summarized as entrepreneurial passion (e.g., Chen et al., 2009) in the context of attracting angel investment, by showing that the perception of passion significantly contributes to the evaluation of a venture’s funding potential (Mitteness et al., 2012).

A study conducted by Warnick, Murnieks, McMullen, and Brooks (2018) provides more nuanced insights into how to effectively signal passion by demonstrating the positive effect of displaying entrepreneurial and product passion on the probability of securing an investment. Since prospective investors and, especially, angel investors aim to contribute significant amounts of time and effort to their portfolio firm, which go beyond financial resources, the entrepreneur’s behavioral intentions constitute a critical factor for investment decisions. Therefore, sending signals that create a positive and trustworthy impression of the entrepreneur is especially important for reducing uncertainty about the individual’s intentions and future behavior (agency risk). Maxwell and Lévesque (2014) provide empirical support by reporting the positive influences of trust-building signals, such as displaying vulnerability, self-disclosing information, and being coachable.

Contextual influences

The literature has identified several factors that can influence the effectiveness of signaling in the angel investment context. For example, since entrepreneurial passion may come with potential drawbacks, such as resistance to investors’ advice, openness to feedback has been identified as a critical attribute in interactions with angel investors (Warnick et al., 2018). By displaying behavior that shows openness and the willingness to accept investor feedback, signals of entrepreneurial passion are complemented by suggesting that the entrepreneur can temper exuberant and irrational decision making (Cardon et al., 2009). Furthermore, since signals rooted in behavior are perceived as more credible than those based on verbal expressions (Busenitz, Fiet, & Moesel, 2005), prospective investors may be more inclined to positively evaluate a venture’s potential when signals such as preparedness and enthusiasm are accompanied by indicators of entrepreneurial commitment (Cardon et al., 2017). However, the literature demonstrates not only that the characteristics of the entrepreneur as the sender can contribute to signaling effectiveness but also that the angel investor’s characteristics as the receiver matter. For instance, in their findings, Mitteness et al. (2012) document that prospective investors place more emphasis on passion if they are older, apply a more cognitive style, display a more open personality, or are motivated to mentor others. Consequently, they are more likely to respond to stimuli that contain related cues. Moreover, research finds evidence that moderate use of certain impression management techniques, such as using positive language to promote a venture’s distinctiveness or expressing high levels of opinion conformity, contributes to signaling effectiveness (Parhankangas & Ehrlich, 2014). Furthermore, the use of specific language to create a certain impression is well supported by the literature on entrepreneurship and communication (e.g., Barry & Elmes, 1997).

VC Investors

The term venture capitalists refers to the group of financial intermediaries that raise capital from other investors to directly invest in new ventures (Busenitz et al., 2005). In doing so, this type of entrepreneurial financing is different from crowd and angel investors, who typically use their own capital for their investments. Representing a group of professional investors, VC funds take an active role in the portfolio firm with the intention of maximizing the venture’s value. Accordingly, due to the associated costs and risk of an investment, VC investors predominantly focus on new ventures at a later stage (Drover et al., 2017).

Signals

New-venture financing is conceptualized as a persuasion process whereby entrepreneurs aim to convince venture capitalists, who are seen as prospective investors, of the merits of their firm. More specifically, whether an investor invests depends on what receivers consider the basis of the judgment and what constitutes relevant evidence for consideration (Chen et al., 2009). Entrepreneurs need to convey information that fulfills both conditions to successfully attract resources. Signals that have been shown to effectively transport such valuable information have been identified and tested in several studies. Generally, the literature distinguishes between information signals, which convey the underlying viability of the venture, and interpersonal signals, which indicate the entrepreneur’s behavioral style and his or her ability to work and collaborate with others (Huang & Knight, 2017). Effective information signals in the context of VC financing constitute indicators of human capital (Beckman, Burton, & O’Reilly, 2007; Ko & McKelvie, 2018; Matusik, George, & Heeley, 2008; Nagy et al., 2012), preparedness (Chen et al., 2009), social capital (Shane & Cable, 2002), technological competency (Hsu & Ziedonis, 2013), government grants (Islam, Fremeth, & Marcus, 2018), or affiliations with third parties or other venture capitalists (Bapna, 2019; Plummer, Allison, & Connelly, 2016; Vanacker & Forbes, 2016). Examples of interpersonal signals are entrepreneurial passion (Chen et al., 2009), personal commitment to the venture (Busenitz et al., 2005), and the coachability of the entrepreneur (Ciuchta, Letwin, Stevenson, McMahon, & Huvaj, 2018). In particular, entrepreneurial coachability is an important signal, which conveys relevant information to prospective VC investors, but it is unlike other effective signals. More static signals, such as the entrepreneur’s education level and the venture’s market share, provide cues for investors on what types of returns can be expected on invested financial resources. In addition to viable cues about financial returns, coachability provides an indication of what can be expected in return for providing social resources to the venture, such as management advice or network access (Huang & Knight, 2017). In this regard, coachability constitutes an especially viable signal in the context of VC financing as this type of investor typically invests significant amounts of nonfinancial resources and, consequently, needs to evaluate the entrepreneur’s abilities to capitalize on this support in advance (Ciuchta et al., 2018).

Contextual influences

The empirical findings document the influence of a variety of different factors on signaling effectiveness in the context of VC financing. Referring to venture characteristics, the literature argues that the stage of the venture could play a critical role, as the information gap between entrepreneurs and prospective investors is assumed to narrow over time. Hsu and Ziedonis (2013) provide evidence for this assumption by demonstrating that the signaling effectiveness of patents as an indicator of a venture’s quality diminishes over time, and thus, is especially useful in the extremely early stage of a venture’s development. Meanwhile, other scholars underline the role of third-party affiliation as a critical factor that contributes to signaling effectiveness (e.g., Plummer et al., 2016). Since signals such as human capital alone may be hard for outside investors to evaluate, they often receive low levels of attention; however, through an affiliation with a credible third party, the signal is validated and increases in credibility (Connelly et al., 2011). Plummer et al. (2016) document such an effect by showing that an affiliation with a recognized venture development organization serves as a certification of the entrepreneur’s claims about his or her prior managerial experience, thereby affirming the positive attribute attached to it.

To strengthen the signaling value of a product on the market, a third-party affiliation could also lead to similar positive effects and may help outside investors distinguish between low-quality and high-quality ventures (Bergh, Connelly, Ketchen, & Shannon, 2014). Empirical evidence also lends support to this assumption and shows that the signaling effectiveness of entrepreneurial commitment benefits from a third-party affiliation (Plummer et al., 2016). The prominence of the investors is another influential factor, which has been described and verified as a type of certification that increases the credibility of signals (Hsu & Ziedonis, 2013; Ko & McKelvie, 2018). In addition, one study showed that VC investors who possess high levels of industry-specific knowledge—and are, therefore, perceived as particularly credible sources in evaluating a venture’s quality—provide an even stronger basis for prospective investors to draw inferences about sent signals than prominence (Vanacker & Forbes, 2016). However, apart from venture or investor characteristics, there are numerous factors regarding the entrepreneur as the sender of signals that contribute to communication effectiveness. Since the efficacy of signals depends on the receiver’s ability to notice them and the value placed on them (Connelly et al., 2011), experienced entrepreneurs are assumed to be more sensitive to the target audience’s needs and, thus, better able to display observable behaviors that attract attention and, ultimately, contribute to signaling effectiveness.

In regard to one especially relevant signal in the context of VC financing—experience—empirical evidence demonstrates that entrepreneurs with coaching experience are likely to be perceived as more coachable than their inexperienced counterparts (Ciuchta et al., 2018). Moreover, apart from more observable entrepreneurial characteristics, such as human capital, the literature suggests that there are factors at work at an unconscious level that may influence the effectiveness of signaling. In this regard, scholars suggest that the conformity of values between entrepreneurs and prospective investors could play a critical role. Matusik et al. (2008) document that founders whose actions display “means-to-an-end” values are better able to reduce uncertainty; as such, they are more likely to secure funding. Moreover, theoretical work suggests that the use of specific forms of language, story lines, and metaphors directly influences how investors interpret information (Cornelissen & Clarke, 2010). By including potentially equivocal signals in a more meaningful whole (Lounsbury & Glynn, 2001) or embedding the unfamiliar into a well-known or familiar structures (Cornelissen & Clarke, 2010), the signals are interpreted in a more favorable light, reducing the uncertainty inherent in the funding decision. In the context of VC financing, using specific types of speech and gestures in an entrepreneurial pitch to depict and symbolize a business idea has been shown to contribute to communication effectiveness (Clarke, Cornelissen, & Healey, 2018).

Equity Investors

Obtaining financing from the equity markets through an IPO is available only to a small fraction of entrepreneurial firms, which are typically at an established stage of their life cycle (Markova & Petkovska-Mircevska, 2009). Nevertheless, going public offers an attractive option for raising capital to foster growth and provides existing investors the opportunity to sell their stakes; ultimately, entrepreneurs could also seek to be rewarded for their efforts by reducing their holdings. As a result, the IPO stage represents a critical and high-demand step for founders as well as investors; therefore, it has received substantial scholarly attention.

Signals

From the communication perspective, the literature on IPOs offers a rich body of knowledge with extant contributions to entrepreneurial signaling. Accordingly, numerous information signals have been studied to explain variations in the funding success of ventures at the IPO stage. However, at this stage, the problem of information asymmetries between the venture and prospective investors has a particularly substantial scope, as equity investors may be exposed to opportunistic behavior and the provision of biased or misleading information (Downes & Heinkel, 1982). Accordingly, conceptual work argues that prospective investors are supposed to be particularly cautious about the validity of entrepreneurial signals at IPOs (Spence, 1976). Consequently, the credibility of signals plays a central role in obtaining funding at this stage (e.g., Cohen & Dean, 2005). A fundamental concern of scholarly efforts in the field is the investigation of signals that convey a venture’s legitimacy. For example, several scholars suggest that the human capital of the top management team (TMT) represents a credible signal in this context (Cohen & Dean, 2005; Higgins & Gulati, 2006). Another study argues that the status of the CEO as the founder provides a valuable signal to prospective equity investors (Certo, Covin, Daily, & Dalton, 2001). In addition, empirical findings underline that not only does human capital matter, but heterogeneity in the TMT regarding their educational and functional backgrounds also serves as a credible and observable signal to investors (Zimmerman, 2008). More specific signals, which have been shown to contribute to IPO performance, include top executive prestige (Certo, 2003; Chahine, Filatotchev, & Zahra, 2011), technological competency (Fisch, 2019), corporate governance characteristics (e.g., Certo et al., 2001), firm size (Daily, Certo, & Dalton, 2005), firm age (Eddleston, Ladge, Mitteness, & Balachandra, 2016), venture capitalist backing (e.g., Higgins & Gulati, 2003), affiliation with prestigious underwriters (e.g., Colombo et al., 2019), and equity retained by corporate insiders (e.g., Bruton, Chahine, & Filatotchev, 2009).

Aside from the signals just discussed, another stream of literature focuses on attributes that are rooted in the country or legal environment from which the venture comes to account for differences in the institutional setting. This research provides an institutional perspective on signaling theory and argues that prospective investors do not evaluate signals in isolation, but rather, they do so in the institutional context (e.g., Bell, Moore, & Al-Shammari, 2008). Accordingly, scholars argue that the environment contains critical cues for prospective investors, such as the development of the capital markets, to better estimate a venture’s prospects. Powerful signals in this context include the level of investor protection (Bell, Moore, & Filatotchev, 2012; Moore, Bell, & Filatotchev, 2010) and the extent of economic freedom in the country of origin (Bell et al., 2008). Compared with the other types of new-venture financing, interpersonal signals, such as passion, receive only limited attention in the literature on IPOs.

Contextual influences

Similar to that in the other types of new-venture financing, signaling effectiveness has been shown to be contingent on several sender-, firm-, and environment-related aspects. In particular, factors that could enhance the validity of a signal have received substantial scholarly interest. Considering that prospective equity investors need to make their financing decisions under uncertain conditions, the literature suggests that in the context of new-venture financing, capital providers are especially vulnerable to the influence of observable factors that enable them to draw inferences about the firm (e.g., Matusik et al., 2008). Accordingly, scholars suggest that these investors are especially prone to the influence of gender stereotypes (Alsos & Ljunggren, 2017; Gupta, Turban, Wasti, & Sikdar, 2009). In fact, research on gender-role-congruity theory suggests that receivers of communication use gender stereotypes to interpret signals from male and female entrepreneurs. As such, prospective investors associate certain expectations about the values or capabilities of the entrepreneur with his or her gender, and thus, they pay more or less attention to the information transmitted. Signaling theory describes this concept as “signal fit” and explains that when certain signals do not match with the underlying expectations associated with a specific gender, a signal is more likely to be ignored or even rejected; consequently, it will lack credibility and usefulness for investors’ funding decisions (Connelly et al., 2011). Eddleston et al. (2016) provide empirical evidence of the influence of gender on signaling effectiveness by demonstrating that information signals about venture characteristics conveyed by male entrepreneurs lead to greater amounts of funding than those conveyed by their female counterparts.

Considering firm-related elements, the literature suggests that a signal’s credibility in the context of IPO financing can be substantially enhanced by referencing critical stakeholders. For example, Certo et al. (2001) demonstrate that the effectiveness of signaling a venture’s quality is enhanced when the investment bankers’ share in the IPO is small and the proportion of outside directors is high. Both factors serve as types of certification of the signal, contributing to its credibility. Furthermore, competitors’ behaviors could also contain critical cues for prospective investors’ decision-making processes, influencing the signals to which they pay attention and how they place value on them. One example is strategic conformity, which refers to the degree of similarity of a venture’s strategic investments in relation to its competitors or other firms in the industry (Deephouse, 1999). Although a certain deviation from the industry norm may be beneficial for the venture to achieve a competitive advantage in the context of signaling, such deviations may make it more difficult for prospective investors to clearly predict the future prospects of the firm based on the information signals (Coff, 2002). Consequently, the signals of the entrepreneurs under conditions of low strategic conformity levels are less likely to be perceived as clear and accurate information by prospective investors, leading to lower IPO performance (Park & Patel, 2015). In a similar vein, heterogeneity in industry valuation could serve as a critical factor, influencing the interpretation of signals (Chemmanur & Krishnan, 2012). For example, in the case of high levels of heterogeneity in industry valuation, the receivers of signals, who may need to interpret ambiguous information, will be less likely to attribute an unclear situation to the venture’s quality; instead, prospective investors are more likely to attribute it to industry risk. In doing so, the target audience will perceive the transmitted information as more credible; therefore, the signaling effectiveness will be enhanced. Park and Patel (2015) support this perspective by showing that ambiguous signals are more likely to reduce uncertainty and positively influence prospective IPO investors’ funding decisions when the heterogeneity in the industry valuation is high.

Environment-related factors that could influence signaling effectiveness in the context of IPOs are the institutional setting in the country of origin and, especially, the corporate governance practices in the capital market (Bell et al., 2012). Moreover, communication-related factors may also be critical in evaluating signaling effectiveness. O’Connor (2002) argues that the identity of a firm can be embedded in entrepreneurial narratives for especially efficient communication. Meanwhile, Shane (2003) suggests that integrating critical information into a story may help to overcome the IPO’s inherent information asymmetries as well as uncertainty, thereby contributing to funding success. Since a narrative is an appealing format that could make information more accessible, stories could facilitate the evaluation of signals for prospective investors and contribute to efficient communication. Martens et al. (2007) provide evidence on the use of entrepreneurial stories at IPOs, demonstrating that a firm’s identity can be constructed more effectively if the corresponding information is embedded in an entrepreneurial narrative. As such, this type of communication technique could significantly facilitate resource access.

Implications and Directions for Future Research

In this final section, we develop a multilevel research agenda aimed at stimulating further studies on entrepreneurial signaling as well as integrative, multitheoretical research. We present theoretical, methodological, and practical implications for signaling in the context of new-venture financing.

Theoretical Implications

Signals

Through the comprehensive assessment of signals in the context of new-venture financing, we can draw several assumptions about the effectiveness of signaling to reduce information asymmetries and uncertainty and point out promising directions for future research. First, one especially important aspect of traditional signaling theory, which is used to explain variations in the effectiveness of signals, is cost (Connelly et al., 2011). However, an emerging stream of literature on signaling in crowdfunding raises some doubts about this assumption by demonstrating that costless signals can be especially effective under certain conditions (e.g., Anglin, Short, et al., 2018). More specifically, the review of the empirical findings suggests that less costly signals may be especially effective when the target audience is less sophisticated (e.g., Loewenstein, Sunstein, & Golman, 2014), when objective or verifiable information is scarce (e.g., Lin, Prabhala, & Viswanathan, 2013), or when there are less explicit behavioral norms in a specific context (e.g., Danilov & Sliwka, 2016). In crowdfunding, all three conditions are likely met, which explains the corresponding findings. In addition, the finance literature that assesses less costly types of communication, frequently described as “cheap talk,” lends support for the assumption that such signals may also work with other types of audiences (e.g., Almazan, Banerji, & De Motta, 2008; Farrell & Rabin, 1996). Accordingly, it would represent a valuable direction for future research to advance the understanding of signaling costs and to explain variations in the effectiveness of signaling by assessing costless signals in different contexts beyond crowdfunding and their possible interactions with costly signals.

Second, despite the widespread notion of quality as the distinguishing characteristic in most signaling models in prior research, scholars have raised doubts about whether the transmitted signal (e.g., retained holdings) effectively conveys the intended message, as quality might be interpreted differently by the receiver, depending on certain boundary conditions (e.g., Connelly et al., 2011). Consequently, scholars have started to examine certain situational factors under which a signal fit between the intended message and the perceived information is more likely to occur (e.g., Chen et al., 2009). Based on the present review’s comprehensive integration of the findings on multiple boundary conditions that influence the signal fit, future research could advance the understanding of signal fit by investigating further contingencies. In particular, an assessment of the interaction between different types of signals may be a fruitful direction for future studies; as recent evidence indicates, the combination of cues could contribute to the validity of signals (e.g., Cardon et al., 2017). In doing this, future research could also advance our understanding of signaling consistency, which refers to the simultaneous agreement of multiple signals from one sender (Gao, Darroch, Mather, & MacGregor, 2008); this is important because conflicting signals are suspected to constitute a significant barrier to communication effectiveness (e.g., Fischer & Reuber, 2007).

Third, another critical result of this review is the finding that some signals have been shown to be equally effective from the early stage to the mature stage at the IPO. One example is the effectiveness of human capital, especially the entrepreneur’s educational background and accomplishments, to signal quality and legitimacy (e.g., Cohen & Dean, 2005; Nagy et al., 2012). A possible explanation for the effectiveness of signaling through education across funding stages and investor groups may be the concept of signal honesty (Durcikova & Gray, 2009). Since entrepreneurs and prospective investors may have partially competing interests, low-quality ventures have incentives to intentionally transmit false or misleading signals to receive funding. Accordingly, due to the presence of false signals, investors are supposed to place more emphasis on claims that are frequently called universal signals, such as educational accomplishments (e.g., a specific degree); these signals could be objectively verified and could, thus, actually provide some kind of proof of underlying quality. By focusing on universal signals, future research could advance our understanding of the defining attributes of these signals, thereby contributing to the literature on signaling effectiveness.

Fourth, signaling theory in the context of entrepreneurial finance predominantly concentrates on signals intended to convey positive information about the sender or the venture. However, by actively avoiding any negatively connoted messages from the sender, conceptual work explains the failure to reduce information asymmetries and uncertainty by proposing that unfavorable information could be the result of unintended signals stemming from one-sided signaling (Connelly et al., 2011). In particular, in the context of new ventures, a more realistic description of the firm that contains both positive and negative information may be more effective than an excessively positive presentation of the venture and its defining attributes; in other words, a more realistic approach may reduce the likelihood of unintended signals. As such, not only traditional accomplishments (e.g., completion of a certain degree) but also potentially negative information, such as failure in a prior new-venture founding, may contain valuable information for prospective investors to draw a more realistic picture of the entrepreneur, thereby contributing to signal credibility and honesty. Accordingly, future research could contribute to a largely ignored area of existing research (e.g., Janney & Folta, 2003) and advance our comprehensive understanding of signals and their effectiveness by integrating positive and negative message content.

Fifth, our assessment of the signaling literature in the context of new-venture finance leads to the conclusion that a more nuanced understanding of the target audience would be beneficial for further advancements in the field. Since most existing literature emphasizes factors such as commitment (Bruton et al., 2009), age (Mitteness et al., 2012), and type of investor (Ebbers & Wijnberg, 2012), little scholarly attention has been paid to aspects that may be more directly related to the signal interpretation of prospective investors. For example, insights from cognitive science could help improve our understanding of how signals are processed (Evans, 2006) and develop a more fine-grained picture of the receiver and his or her information needs. In particular, entrepreneurs seeking funding in high-noise environments, such as the crowdfunding context, would benefit from a comprehensive understanding of the target audience to effectively convey the right message and ultimately acquire the needed resources.

Practical Implications

From a practical perspective, research on entrepreneurial signaling offers various implications for new ventures looking to improve their resource acquisition. Considering the rapidly developing landscape of entrepreneurial finance, the challenges entrepreneurs face when trying to effectively use signals in their communications with prospective investors will become even more important. Traditional VC providers, including angel investors, are becoming more professional, resulting in increased information demand and the expectation of proficient interactions with nascent ventures. At the same time, new financiers who are drawn through crowdfunding platforms confront entrepreneurs with new communication challenges. As a result of the evolution of these platforms and the emergence of new communication channels, such as Twitter, the cost of signaling with prospective investors has decreased substantially. Furthermore, due to the coverage of these new communication channels, the target audience is more widespread and no longer restricted to small groups. The opportunity to interact with prospective investors is being enhanced, but simultaneously, the question of what and how to communicate to attract prospective investors’ attention has become more difficult. Thus, regardless of whether entrepreneurs approach traditional or modern equity investors, knowing how to communicate is essential for obtaining funding.

Unfortunately, the entrepreneurial signaling literature is highly fragmented, and thus far, it has failed to offer comprehensive guidance for nascent ventures in search of funding. That said, it has produced three especially useful insights. First, for entrepreneurs to signal effectively and successfully deliver their message, it is essential to know the needs and motivations of the target audience. In this respect, the literature has indicated that pieces of information and interpersonal signals not only vary but also are interpreted differently across investor types. Second, the findings in this review underline that the stage of the venture provides an influential contingency with major implications for signaling effectiveness. Therefore, the corresponding results on entrepreneurial signaling must be judged in this context. Since scholars have already pointed out the role of changing information needs among investors throughout the financing process, entrepreneurs must be aware that these insights may not be transferable to later stages of new venture financing. Third, more recent studies (e.g., Parhankangas & Ehrlich, 2014) have emphasized that communication tactics, such as impression management behavior, must be applied carefully in interactions with prospective investors, as the extensive use of these techniques may have severely negative consequences.

Conclusion

In this work, we conducted a systematic review to identify, organize, and interpret the multiple insights provided by the different literature streams on entrepreneurial signaling in new-venture financing. In doing so, we have provided a comprehensive overview of the distinct information, as well as interpersonal signals, that have been investigated and offered a number of viable suggestions for future studies in the area of entrepreneurial signaling. While we are certain that the insights generated by our systematic study will make a valuable contribution to the signaling and entrepreneurship literature, we are also aware of their potential limitations. For example, the criteria we applied to select the relevant articles (e.g., keywords) may be different from those used by other scholars. Although we executed the literature search for relevant articles with great care, we acknowledge that alternative sampling criteria may be used, which could either enlarge or shrink our sample. Furthermore, while we are confident that the manner in which we categorized the articles in our sample was both academically sound and practically useful, we are aware of alternatives to our approach (e.g., focusing on one/other receiver group[s] or including other target journals). Notwithstanding these potential limitations, we think our review provides a new perspective on the relevance of entrepreneurial signaling in the context of new venture financing.