Abstract

The ecological transformation of the economy is frequently approached politically with market-based policy, in particular derisking, which attempts to steer private financial actors into ecological and climate sustainability by taking on risks. To understand the effects of such approaches, I point to the relational and concrete dynamics that unfold between states and finance. Conceptually, I propose analyzing the investment chains that surround these programs, and the conditionalities that constitute its relations, which I read as manifestations of infrastructural power. I argue that conditionalities are the qualifier of the transformative potential of market-based policy programs. The proposed “micro-financial” analysis allows to unpack the inherent limitations of derisking-based governance approaches. These approaches come with a dependence on financial intermediaries, which results in weak conditionality and enforcement. Concretely, I analyze how under BlueInvest, a pilot within the European Green Deal (EGD), the European Commission (EC) mandates the European Investment Fund (EIF) to harness venture capital (VC) funds in order to foster the blue economy. I show how, as a consequence of investors’ intermediary position in derisking-based operations and the EIF’s profitability orientation, policymakers come to depend on venture capitalists, hindering strong and effective conditionality and hardwiring limited sustainability effects into the investment chain.

Keywords

Introduction

The state is back—or rather it was never gone. But over the last decade, states have arguably taken on a more active role and, at least discursively, industrial policy is out from under the shades of history. One crucial field of state activity is the ecological transformation of the economy. Here, as in other policy arenas, it is frequently the case that states do not directly invest but instead construct partnerships with global finance; they “escort” capital to make sustainability—like development, infrastructure, or technologies—“investible” (Gabor, 2021: 430), which essentially means that they take on risks and hence guarantee returns for private investors. Importantly, this form of governance relies on financial markets for the pursuit of its policy goals (Braun et al., 2018).

Existing studies have demonstrated the new variety of state-capital interactions in general (Alami et al., 2022) and the prevalence of derisking policy more specifically (Gabor, 2021; Gabor and Sylla, 2023). They have also focused on the role of public or private financial actors in tackling the climate crisis (see, e.g., Akomea-Frimpong et al., 2021; Thiemann et al., 2022). In contrast, the aim of this article is to offer an analytical approach to market-based governance, which, instead of focusing on the mechanics and attributes of financial or public actors per se, encompasses the power dynamics emerging in this relationship along with the resulting limitations.

Therefore, I develop a notion of infrastructural power, which I define as the power to shape relations of intermediation in the investment chain. The investment chain extends the scope of the analysis beyond single actors or interaction points to the relations that together constitute market-based approaches to governance, including public, private, and “borderline” public-private actors. For instance, a guarantee program might include development banks, commercial banks, and corporations. Infrastructural power, I argue, manifests in the conditionalities of policy programs, which are an underexplored qualifier of market-based governance. Importantly, the conditions attached to public guarantees or investments represent the hardwiring of state-market relations in investment chains and determine the potentials and limitations of policy programs.

Concretely, I analyze the case of one policy program, called “BlueInvest,” under the European Union’s (EU) policy package for the green transformation, that is, the European Green Deal (EGD). This program “aims to boost innovation and investment in sustainable technologies for the blue economy,” that is, in companies “based on or related to the oceans, seas, and coasts” (European Commission, 2021c: 2). The sector contributes around 1.5% of the EU-27 GDP (European Commission, 2021c: II). Through this program, which is led by the European Commission (EC), the European Investment Fund (EIF)—the EU’s multilateral development bank for financial intermediation (Cooiman, 2023)—provides capital to venture capital firms; these firms then invest in blue economy startups.

With my analysis, I demonstrate the limitations of derisking-based policy. Via the BlueInvest investment chain, I tie my findings to the institutional landscape of the European Union. I argue that the profitability orientation of the EIF, which is a central part of the BlueInvest chain, fosters dependencies on financial actors. These dependencies result in weak conditionality and lax enforcement and thus hardwire limited sustainability into the investment chain. I therefore contend that a green transformation requires institutional transformation.

I focus on the BlueInvest program for two main reasons: First, as a field-in-the-making, the blue economy offers insights into the power dynamics surrounding market-based green transformation policy, which are harder to disentangle for fields that are already more established and that involve more actors, such as the “green economy.” The BlueInvest program is small—it has a €500 mm volume—but I argue that it speaks to the power dynamics between finance and politics more generally, because governing through financial markets—particularly via derisking—is an increasingly popular approach in the EU and beyond (Braun et al., 2018; Gabor, 2021, 2023). Second, the focus on venture capital investments makes BlueInvest particularly relevant. VCs are arguably located in the machine room of the future economy (Beckert, 2016) and—in this case—connect finance, innovation, public policy, and ecological and climate concerns. Policymakers try to harness VCs for their own goals, but the degree to which that works remains an open question that needs to be addressed.

This article makes several contributions. First, empirically, I follow calls, as made in the introduction to this special issue, to focus on the concrete dynamics surrounding green finance by analyzing one specific policy program, thereby shedding light on the notoriously vague European Green Deal (Harvey and Rankin, 2020) and the role of financial intermediaries, such as venture capital investors, in it. Second, I show how under BlueInvest the European Green Deal effectively employs the operational logic of derisking, further proving the prevalence of the derisking state. I point to the inherent limitations of this approach to governing. Finally, conceptually, with the proposed framework of infrastructural-power-as-conditionality-in-the-investment-chain—that is, if you will, “critical micro-finance”—I offer new insights on the concrete and relational workings of recent governance approaches to the green transformation. In doing so, I contribute to recent efforts that seek to grasp state-finance relations.

This paper proceeds as follows. First, I develop a conceptual framework centered in conditionality in the investment chain in order to address the power dynamics of (financial) market-based approaches to governance. This is followed by a brief presentation of the article’s methodological approach. The third section introduces the institutional setup surrounding BlueInvest, which serves as an in-depth case study for this paper. The empirical section then goes on to explore the power dynamics and conditionalities along the BlueInvest chain. The last section discusses the findings and concludes.

Conditionality and power in the investment chain

In this section, I develop my understanding of the power dynamics of (financial) market-based approaches to governance and link these conceptually to the study of conditionality.

There is a long intellectual history of attempts to understand the role and power of finance under capitalism, with debates that are still ongoing (Braun and Koddenbrock, 2022; Dafe et al., 2022). Instead of recounting this history, I briefly introduce the two most commonly used forms of financial sector power; these are intended to serve as contrasts to the notion of infrastructural power developed in this article. Typically, one distinguishes between instrumental power, that is, the power of financial actors to directly influence politics, for example, via lobbying and organized interests, and structural power, that is, the power of financial actors to indirectly shape the political process due to their privileged position in the capitalist economy (see, e.g., Lindblom, 1977).

Each form of power, I argue, fails to fully account for the dynamics that emerge in governance through financial markets. Instrumental power is concrete in so far as it is based on the specific historical efforts of financial actors, yet static in so far as it is simply exercised unilaterally. In contrast, structural power is relational in so far as it emerges from the relations of the capitalist economy, yet abstract in so far as it operates at a systemic level (Kalaitzake, 2022). These concepts thus go only so far in unpacking the fundamentally relational and concrete power dynamics that surround governance through (financial) markets.

In response to these shortcomings, Braun has suggested working with infrastructural power, which is “derived from direct entanglement at the level of policy instruments rather than the indirect dependence at the level of ultimate policy goals” (Braun, 2018: 5). Infrastructural power is a form of structural power in so far as it is based on the privileged position of capital in the political economy of capitalism. Yet, in contrast to structural power, infrastructural power is concrete. When policymakers use financial intermediaries to govern, the emerging entanglements and dependencies grant these intermediaries a form of power that is exercisable in the political process and that shapes the unfolding of these governance programs (Braun et al., 2018).

I extend the analytical purchase of infrastructural power by situating it in the investment chain that surrounds market-based governance and by qualifying the relations of the chain as conditionalities. Infrastructural power, as conceptualized in this article, describes the power to shape relations of intermediation in the investment chain of concrete, (financial) market-based governance efforts.

Incorporating the investment chain into the analysis allows one to focus on the concrete agents of (infra-)structural power—as Culpepper (2015: 406) and Marsh et al. (2015: 585), amongst others, have called for—and, importantly, their concrete structural position. The investment chain was originally proposed within the social studies of finance to describe the “sets of intermediaries that ‘sit between’ savers and companies or government” (Arjaliès et al., 2017: 4). In the field of political economy, the concept enables the systematic study of indirect governance approaches, which reach from state agencies, through financial markets, into the economy. I situate infrastructural power not in the abstract structure of the capitalist system, but rather in the concrete structure of the investment chain.

Importantly, the investment chain not only serves as quasi-structure but also comprises the relations that constitute infrastructural power. I argue that, in order to get at the power dynamics of market-based governance approaches, one must take into account these relations of the investment chain. In the case of this article, this means studying the relations between the European Commission, the European Investment Fund, VC firms, and blue economy businesses. To qualify these relations, I foreground conditionality. Conditionality describes the degree to which political programs, such as the EGD, attach conditions to state assistance. Importantly, conditionality qualifies not only the direct interface between states and markets, that is, between policymakers and financial intermediaries, but all the relations of the investment chain, including those between financial intermediaries and the businesses they invest in.

Conditionality is often negatively associated with the International Monetary Fund (IMF) and its historic “prescriptions of fiscal austerity, trade and capital account liberalization, public sector layoffs, and ‘structural reforms’” (Kentikelenis et al., 2016: 2). In development studies, the impact of state engagement—be it positive or negative—has long been tied to the setting of performance conditions (see, e.g., Maggor, 2021; Wade, 2018: 528). To be successful in terms of policy goals, a close relationship with capitalists, such as under the developmental state, requires a state’s “capacity to discipline capitalists and capital” (Wade, 2018: 526). The derisking literature has little to say about conditionality, dismissing it with comments such as: “derisking and capital discipline are fundamentally at odds because the former relies on private profitability to enlist private capital while the latter forces capital into pursuing the strategic objectives of the state” (Gabor, 2023: 4). While I acknowledge the tension between the logic of risk/profit and policy goals, which actually is at the core of market-based approaches to governance, a quick dismissal leaves little room for analysis of how policymakers move within this tension in concrete governance attempts and of the implications of such attempts.

The central question, if we are to understand the power dynamics of market-based governance, then is: Who can make the investment chain work in their interest? In other words, it is a question of who exercises infrastructural power: Is it policymakers seeking to achieve policy goals, such as ecological and climate effects, or private actors, presumably seeking profitability? Here, conditionality comes in as an analytical category: to reach policy goals, policymakers have to set performance conditions and discipline investors (see Wade, 2018). Analyzing not only conditionalities but also their enforcement is crucial to an understanding of the actual potential of such policy programs (see Bulfone et al., 2022: 7). If conditionalities and enforcement are weak, they will not change the behavior of financial actors—hence, policymakers only take on risks and increase investors’ profitability, while losing on political rewards. In the case of this article, weak conditionality would entail effectively subsidizing VC firms and their investors’ returns while having little to no positive climate and ecological impact.

Conditionality serves as empirical subject of this article and is understood here as the outcome of struggles over infrastructural power, that is, the power to shape relations of intermediation in the investment chain. I argue that proposals that understand conditionalities as an expression of structural power—“a form of power derived not from the strategic or intentional activities of business, but rather through the operation of (global) market pressures that compel states into providing policies that privilege the interests of business” (Bulfone et al., 2022: 6)—miss out on the previously discussed relational and concrete character of recent political approaches, in which power dynamics unfold. A differentiation between infrastructural and structural power is important here because, while structural power comes in an apolitical guise, infrastructural power is open to political conflict. Understanding conditionality as an expression of infrastructural power allows a direct analytical link between the setup of policy programs and their limitations.

To study actual power struggles, rather than their outcomes, one would need access to the negotiations within and between public institutions, such as the EIF and the Commission, which is nearly impossible due to the confidential nature of such negotiations. This is a pragmatic reason for my focus on the analysis of conditionalities. Another reason for this focus is that conditionalities are not only the outcome of power struggles; they also codify (Pistor, 2019) the political and financial outcomes of governance programs and thus lay the ground for future power (im)balances.

Methodology

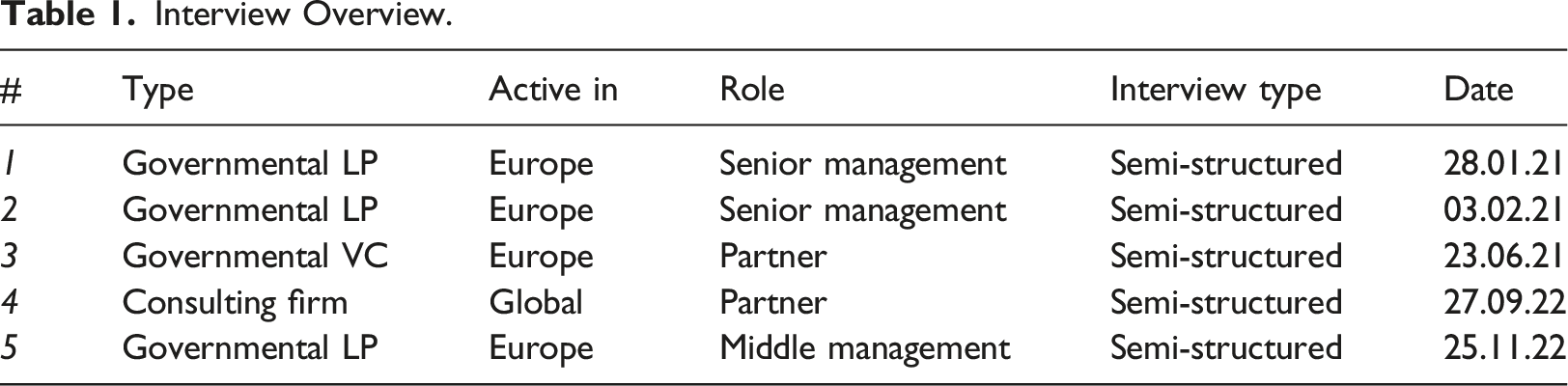

Empirically, this article is based on a content analysis of 18 documents published by the EC, EIF, and BlueInvest, triangulated by five semi-structured interviews with European policymakers and BlueInvest officials and by transcripts from the yearly BlueInvest conference (see Appendix).

The main documents I analyze are the EIF’s “Open call for expression of interest,” which targets potential venture capital funds under the program, and its seven appendices (European Investment Fund, 2022a, 2022b, 2022c, 2022d, 2022e, 2022f, 2022g, 2022k). The call “aims at selecting eligible financial intermediaries under the framework of InvestEU for providing equity investments in support of innovation, growth and social impact” (European Investment Fund, 2022k: 1). Together with the appendices, the call states the conditionalities applied to EIF funding under InvestEU, that is, the conditions for public money to be invested in private funds. In my analysis, I am particularly interested in conditionalities regarding ecological and climate effects. In addition, I analyze documentation published by the EC on the sustainability requirements of InvestEU, on the blue economy, and on the European Green Deal (European Commission, 2021a, 2021b, 2021c, 2022a, 2022b, 2022c).

The document analysis points me to the hardwiring of the BlueInvest chain, that is, the conditions that constitute its relations. To unpack the actual operations behind the program and the disciplinary potential behind the conditionalities, I have conducted expert interviews with EIF and BlueInvest officials. In addition, I have watched and analyzed recordings of the BlueInvest conference in order to shed light on the relationship between investors, policymakers, and EIF officials and to indicate the dynamics of infrastructural power at work. Overall, this combination of documents, interviews, and other ethnographic material has allowed me to provide a granular account of the BlueInvest investment chain.

European political economy around BlueInvest

As a foundation for the analysis of infrastructural power in the BlueInvest investment chain, the following section introduces the institutional context surrounding the program in the polity of the EU and the program itself.

Institutional context

BlueInvest runs under the EGD, which is the EU’s policy bundle announced in 2019 that aims to reduce EU carbon emissions to net zero by 2050. Its investment pillar, the EGD Investment Plan (“Sustainable Europe Investment Plan” (SEIP)), directs capital to sustainable investments, combining funding from the EU budget, member states, and private actors. The main driver of SEIP is InvestEU, the EU’s multiannual investment program (2021–28), which works through an EU budget-based guarantee of €26.2 billion and plans to enable—via a multiplier effect, whereby public actors leverage private capital—€372bn of public and private investment. Overall, the EGD is based on a strong belief in market-based governing, which is in line with previous programs, such as the Juncker plan (Braun et al., 2018; Mertens and Thiemann, 2018). Whether we will meet the Green Deal goals will not just depend on us, policy makers. It will mostly depend on the private sector, on businesses, scientists and consumers. Politicians and policy makers can set the scene, provide support, and eliminate the barriers. (EU Commissioner for Environment, Oceans and Fisheries, in: European Commission, 2021c: III)

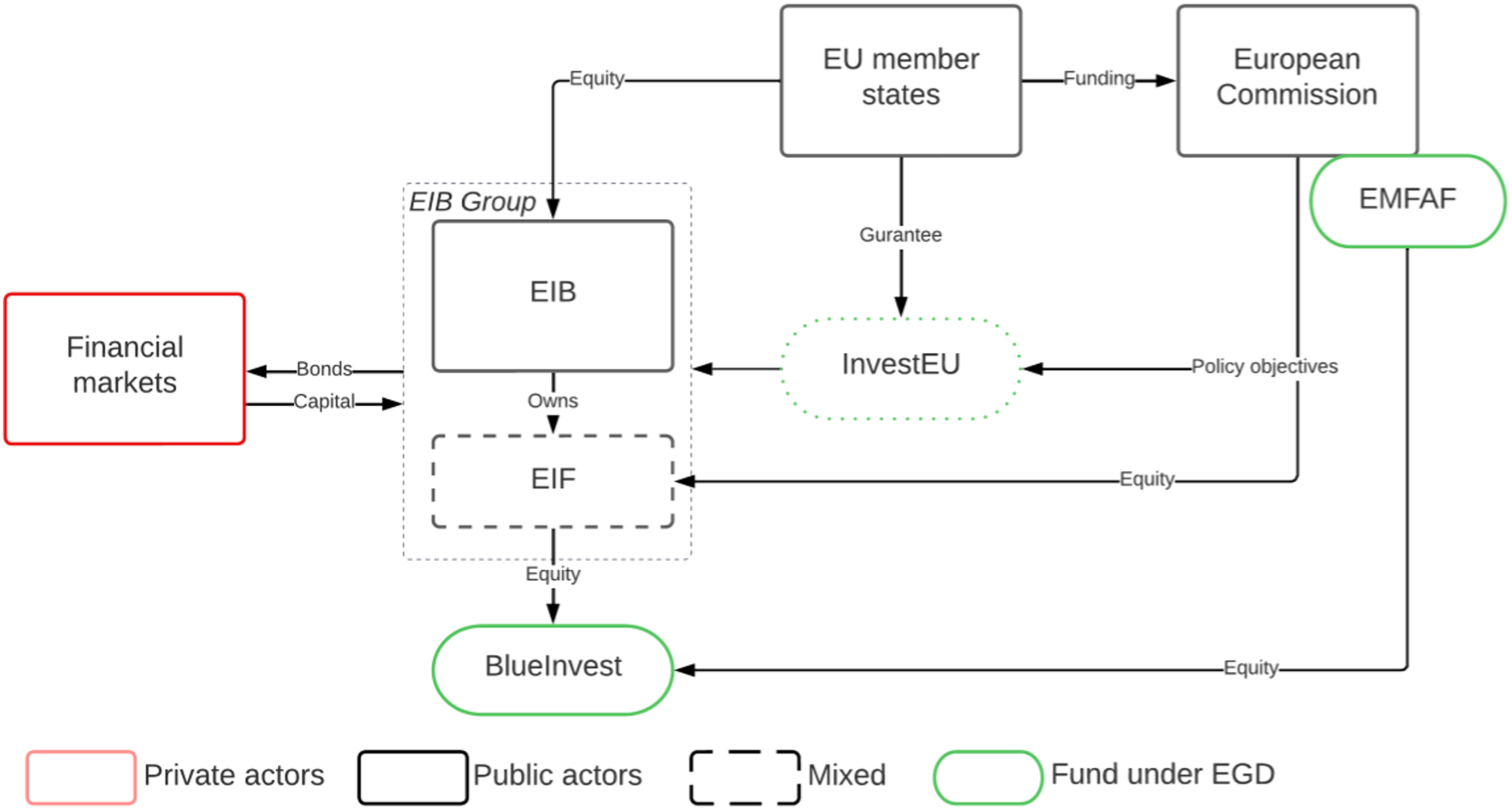

Under the EGD, 30% of InvestEU funding will be allocated to “green investments” (European Commission, 2022b). Three quarters of the InvestEU program are executed by the European Investment Bank (EIB) Group; the EIF manages €11bn of these funds, with €6.5bn dedicated to equity investments in small and medium-sized enterprises (SMEs) (European Investment Fund, 2022i), most of which—including BlueInvest—are venture capital investments. Figure 1 depicts the European institutional context surrounding BlueInvest. The polity of the European Green Deal surrounding BlueInvest.

Within this context, the EIF takes on a special role. It formally belongs to the EIB group, with the EIB being its largest shareholder, but it also caters to a range of other private and public actors. The EIF specializes in all intermediary financial operations and resembles a “semi-public asset manager” (Cooiman, 2023). Importantly, its statutory objectives are twofold: to achieve an “appropriate return”; but also to support policy objectives set by the Commission, such as those of the EGD (EIF, 2015). This speaks to the complicated history of the EIF’s emergence within the institutional constraints of the EU. The Commission sought institutional innovation in order to govern “off-balance-sheet” (Mertens and Thiemann, 2018: 6) and promised profitability in order to gain the necessary support of member states (Cooiman, 2023). As discussed in the empirical section below, this profitability criterion constitutes a key constraint on the EIF’s present political possibilities.

The EIB refinances via the issuance of bonds on financial markets. The EIF, on the other hand, mostly executes mandates given by the Commission, the EIB, or other public institutions. This is also the case with BlueInvest: the InvestEU guarantee allows the EIB to refinance on financial markets and, with that money, to provide funding to the EIF for BlueInvest. Another source of funding for BlueInvest is the Commission’s European Maritime, Fisheries and Aquaculture Fund (EMFAF), a €6bn fund that uses various financial instruments to strengthen the blue economy. What already becomes evident here is the vast net of state-market relations surrounding one relatively small EGD project.

BlueInvest

The Commission started the first BlueInvest program in order to provide financing to “underlying equity funds that strategically target and support the innovative Blue Economy” (European Commission, 2021c: 8). At its financial core, BlueInvest operates as fund of funds, providing equity to VC funds, which acquire shares in startup companies. The Commission explains that the use of venture capital in governing is grounded in the capacity of investors to strengthen sustainability and innovation. Venture Capital and Private Equity funds will play a critical role in the years to come in backing sustainable technologies and innovation that will contribute to the preservation of our oceans, seas and coastlines, precious shared resources that constitute the backbone and mainstay of the Blue Economy, a strategic high value economic sector. (European Commission, 2021c: 8)

According to the Commission, the blue economy needs to be built with policymakers’ help. To guide financial actors into the blue economy, the EC derisks investments and makes them easy for investors—an operational logic in line with the derisking state (Gabor, 2021, 2023). Many of the projects in the area of sustainability and Blue Economy are risky or require risk-bearing capacity from investors, as the returns on investments are long for many sectors. (European Commission, 2021c: 7)

In other words, under BlueInvest, the Commission mandates the EIF to invest in venture capital funds and these funds are then supposed to invest in blue economy businesses. The EIF thus takes on the investment risks of the private sector, hoping to reach a policy goal—namely, “to boost innovation and investment in sustainable technologies for the blue economy” (European Commission, 2023).

Under BlueInvest I, which operated from 2020 to 22, the EIF has invested around €100 mm in five funds, which themselves have invested into blue economy startups, such as SyAqua, a “global leader in shrimp breeding,” or Green Power Hub, a trading platform for sustainable energy. Next to the fund, BlueInvest includes a “platform” that brings together investors and companies. The EC commissioned the consulting agency PricewaterhouseCoopers (PwC) to create the platform. The pilot was regarded as a success—in terms of investments made, platform memberships, and events—and hence was expanded under the successor BlueInvest II, which was announced in 2022. The volume was increased to €500 mm. Next to the fund and platform, BlueInvest now also includes advisory services to the targeted SMEs and the investors, again provided by PwC.

Blue investment chains

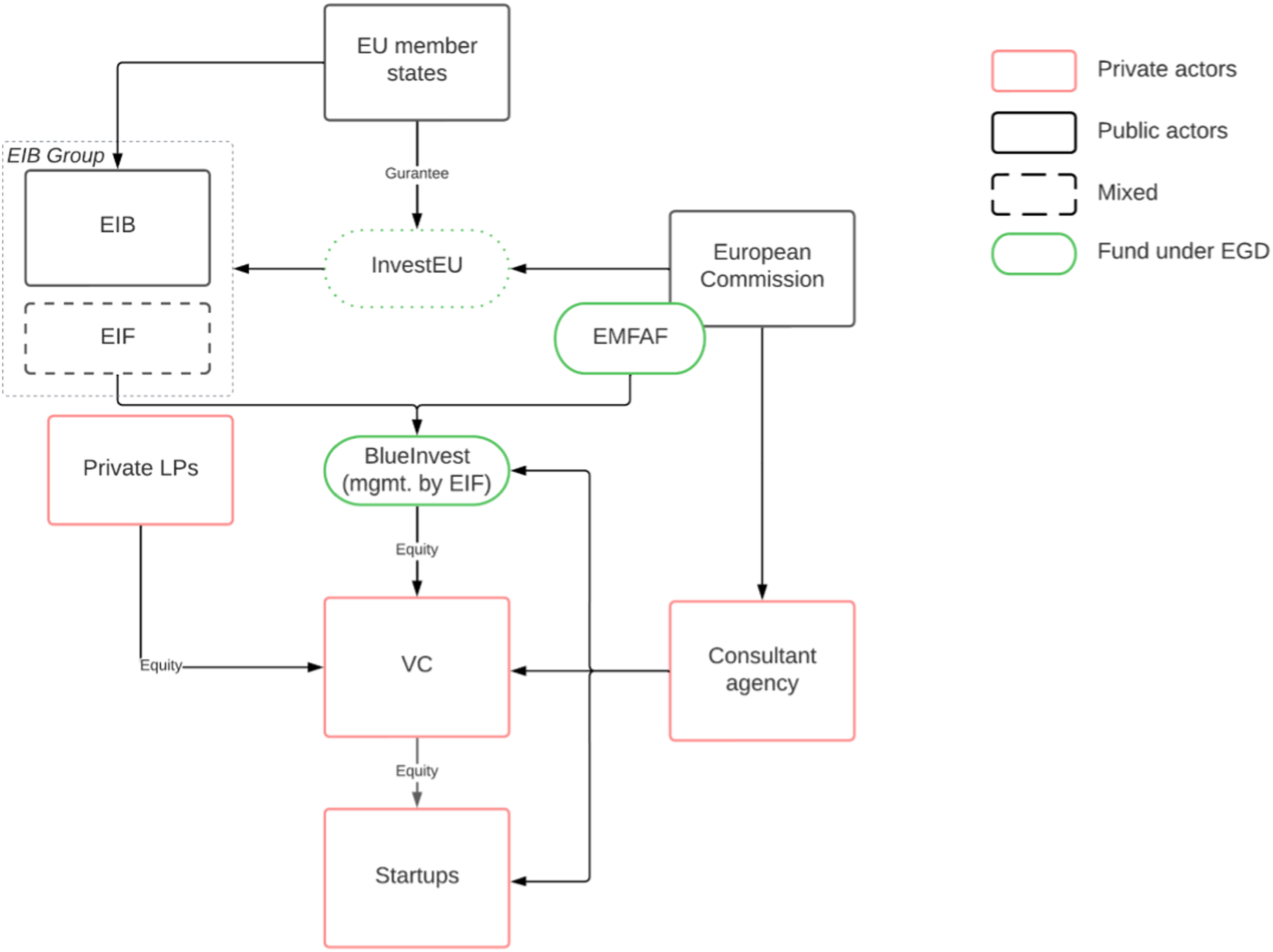

After introducing the institutional background and the BlueInvest program, this section analyzes the governance strategy surrounding BlueInvest and the attached conditions and power relations along the investment chain. Figure 2 presents an overview of the investment chain surrounding BlueInvest, which reaches from EU governance all the way to the targeted blue economy startups. To successfully harness financial actors for governance purposes, conditions have to be attached to the provision of capital. The EGD has formulated the overall policy goal of becoming carbon neutral by 2050; what is needed for this goal is much debated, and not easily quantifiable.

1

This leaves the different agents of the policy bundle themselves with the task of formulating tangible goals for smaller time horizons, which are typical for policy planning periods and their respective areas, and translating them into conditionalities. The BlueInvest investment chain.

The European Commission and InvestEU

The EC and its investment pillar InvestEU constitute the first part of the investment chain that ultimately aims to reach blue economy startups. For the 7-year investment plan InvestEU (2021–27), the EC has set the goal of a 30% share of investment volume in sustainable, green investments in order to pay into meeting the overall goal of carbon neutrality by 2050.

From the perspective of the EC, steering private finance toward sustainability via InvestEU indicates the EC’s infrastructural power. They can structure the relations of intermediation with financial actors. This is demonstrated by their calculation of a multiplier effect of 11.4, which means that for every Euro spent under InvestEU, “€11.4 of total investment—that would not have happened otherwise—is generated” (European Commission, 2022c). This logic is debatable and depends on the concrete conditionalities attached to capital, which indicate who it is that structures these relations of intermediation in their interest. In the following, I analyze the conditionalities relevant to the BlueInvest program as they are formulated at the level of the European Commission.

InvestEU is a public guarantee, and this allows it to fund a wide range of financial instruments, each of which asks for specific conditionalities as to what entails a sustainable investment. Therefore, the EU has developed a taxonomy for sustainable activities, which details a list of “environmentally sustainable economic activities” to help “shift investments where they are most needed” (European Commission, 2022a). The taxonomy—itself the subject of heated debates and criticism—is used to classify investments that pay into the EGD, and it asks financial intermediaries that use InvestEU funding to publish documentation to prove sustainability. The extent of this documentation varies. As discussed in the next subsection, financial intermediaries—particularly those focused on SMEs—are often subject to weaker requirements for proportionality purposes.

The overarching “Sustainable Finance Disclosure Regulation” (SFDR) classifies funds according to their level of sustainability engagement, namely: funds with no sustainability orientation, regulated under Article 6; “light-green” Article 8 funds, which do consider, amongst others, environmental and social criteria; and “dark-green” Article 9 funds, with sustainable investment as their objective (European Parliament and Council of the European Union, 2019). In order to qualify for funding under BlueInvest, VCs need to oblige either Article 8 or Article 9 of the SFDR, which require them to consider principal adverse sustainability impacts (PASI) in their investment decisions and, as an Article 9 fund, to align with at least one of the taxonomy criteria and to do no significant harm to the others. In practice, what is required for the fulfillment of such criteria is not defined further and can take the form of a loosely formulated paragraph on the website (see, e.g., BlueInvest fund Ocean 14 (2022)).

These regulations set the scene for the blue economy investment chains, but the specified conditionalities remain broad and vague. In a FAQ document, the EC argues that “the financial partners in InvestEU will be responsible for the financing and investment operations under the InvestEU Fund since their governing bodies take the final decision on the financing” (European Commission, 2022c). In other words, the EC delegates responsibility down the investment chain to its partners, which in the case of this article means to the EIF.

To sum up, the Commission has set the high-level goal of 30% sustainable investments under InvestEU. The taxonomy and SFDR are wide-meshed, and provide general direction for reporting and governance, but do not specify concrete conditionalities. The responsibility for structuring the relations of intermediations via conditionalities is delegated down the chain, in this article’s case to the EIF.

The European Investment Fund and PricewaterhouseCoopers

The EIF, together with the consulting firm PwC, constitutes the second node of the investment chain analyzed here. The EIF manages the BlueInvest mandate and selects the VC firms that receive financing. PwC was mandated by the EC to consult VCs and startups and to support the execution of the BlueInvest program. As discussed in the previous subsection, the EC delegates the responsibility and specifics ensuring sustainable investment down the investment chain toward the EIF. To unpack the role of the EIF, I analyze the conditionalities relevant to the BlueInvest program formulated by the EIF. Weak conditionalities indicate that VC firms can structure the relations of intermediation in the interest of their profitability; in contrast, strong conditionalities suggest that the EIF can shape financial intermediation to pay into its stated policy goals.

Beyond the specifics of the BlueInvest program, recipients of EIF money generally have to adhere to the Paris alignment restrictions, which inhibit investments into fossil fuels and industries with high CO2 emittances, such as those that involve the manufacture of chemicals or cement (European Investment Fund, 2022b: 6).

The foundation of my analysis of the BlueInvest program is provided by the EIF’s “Open call for expression of interest” together with the appendices and FAQ documents of this call (European Investment Fund, 2022k). Below I outline the two central conditionalities before discussing their operational implementation and key characteristics.

The first conditionality concerns the investments conducted by BlueInvest VC funds. Funds receiving capital under BlueInvest need to “invest two times the commitment from that mandate into blue economy relevant enterprises based in the EU” (Interview #5). In other words, if the EIF invests €20 million in a fund, which typically may have a total volume of €100 mm, €40 million needs to be invested in blue economy related businesses, such as a tourism business or a shrimp-breeding company.

A second conditionality concerns the structure of the financial compensation of VCs. Typically, the value model of venture capital consists of an annual management fee and the carried interest, that is, a share in the capital gains resulting from the successful exit of an investment (Cooiman, 2022). To incentivize sustainability, part of the carried interest of VC firms is linked to key performance indicators (KPIs). Only if certain sustainability KPIs, tailored to the area of investment, are achieved, will VC firms get the full carried interest, typically 20% of net capital gains.

These conditionalities in and of themselves suggest that the EIF is indeed shaping the intermediation by VCs in such a way as to ensure sustainability. However, closer scrutiny of the operations behind these conditionalities shows how, in practice, they are only loosely enforced.

First, importantly, the EIF (“the implementing partner”) does not directly assess the sustainability of businesses that receive funding through financial intermediation (“underlying transactions”). Instead, the responsibility for assessing sustainability is delegated further down the investment chain toward financial intermediaries. Financial intermediaries self-report on the sustainability of their investments without being audited. In intermediated financing, the implementing partner does not directly assess the underlying, individual projects or operations. This is because there is at least one financial intermediary between the implementing partner and the final recipient (114). […] For intermediated financing, the responsibility for ensuring the sustainability of the underlying transactions […] is delegated to the financial intermediary. (European Commission, 2021a: 61; my own emphasis)

This self-reporting stands in contrast to direct financing, which is the specialty of the EIF’s parent, the European Investment Bank (EIB). Here a detailed proofing process is conducted by the EIB (European Commission, 2021a: 14). This special treatment once more confirms the need for further scholarly attention on financial intermediation and the surrounding politics-finance nexus.

Financial intermediaries’ self-reporting is structured according to a “simplified form of sustainability proofing” provided by the EIF. The argumentation behind these lax requirements is that one should not “overburden” small actors, such as startups. For financing of SMEs, small mid-caps and other eligible enterprises, no screening or full sustainability proofing will be required (13). However, a simplified form of sustainability proofing and specific safeguards will be applicable to ensure a minimum alignment with EU commitments, while trying not to overburden small economic actors with complex requirements. (European Commission, 2021a: 7; my own emphasis)

Concretely, the simplified form asks whether the “Investment [is] supporting climate objectives” (European Investment Fund, 2022g: 5). If so, the financial intermediary is to indicate the percentage of the business’ revenue that is made by contributing to the broad targets of the taxonomy, such as “climate change mitigation,” “climate change adaptation,” “water resources,” “circular economy,” or “sustainable enterprise criteria.”

To further clarify these broad categories, the EIF developed a guideline for Climate Action and Environmental Sustainability (CAES) (European Investment Fund, 2022j). The guideline, according to an interviewee, is intended to function as a bridge between the wide-meshed taxonomy and the concrete operations of the EIF. More specifically, CAES serves as a guideline for defining the KPIs that determine parts of the financial compensation. For some of the targets, CAES specifies concrete indicators, such as “estimated energy savings (kWh/year)” for any energy saving services, while for most it only explains what business activities are included. As an example, the guideline clarifies that “investments in nontraditional crops and alternative proteins” include: “algae, proteins from insects used for fish and animal nutrition, etc.” (European Investment Fund, 2022j: 29). Crucially, specific KPIs and target levels are defined collaboratively by the EIF and venture capitalists. So, they [the KPIs] can be quite varied. If I were to take a company that is promoting a technology that is meant to improve water efficiency, maybe then the KPIs could be liters of water saved or water leakage avoided. […] an agritech company that is seeking to improve the resilience of crops, you know, against certain types of pests, but through biological solutions and so maybe their KPI will be, you know, the loss of, harvest prevented […] it's a framework that isn't meant to set crazy impossible targets, but rather make sure that the fund manager is measuring and managing impact together with its founders. (Interview #5)

This process leaves much leeway for investors. They can define and construct KPIs in their interests to make sure that they receive full compensation. The argumentation of the BlueInvest official points to the EIF’s dependence on VCs: according to the interviewee, the EIF aims not to set “crazy impossible targets”—in other words, the EIF seeks to make things easy for investors.

Ultimately, self-reportings are also used to measure the contribution of BlueInvest to the EGD. For instance, the VC firm Ocean 14, which received funding under BlueInvest I, may report that their investee SyAqua, the shrimp-breeding company, generates 100% of its revenue by investing in nontraditional crops and alternative proteins. Hence, the €12 mm that Ocean 14, the BlueInvest VC firm, has invested in SyAqua (The Fish Site, 2022) will be counted as fully contributing to the goals of the EGD. In light of weak reporting requirements and no auditing, VC firms are incentivized to overstate the sustainability focus of their businesses, so that they are particularly attractive for the EIF and receive full compensation. Additionally, as many young firms may not yet have historical revenue figures, the assessment for startups is to be based on their business plan (European Investment Fund, 2022b: 6, 2022l). At the same time, the potential negative environmental or climate impacts that a company may have, for instance, in its production process or logistics are not considered in this calculation. There are two layers of intermediation involved in the construction of sustainability figures. VCs self-report on broad categories without assessing negative effects and startups produce business plans, which may be overly optimistic. Overall, this suggests a tendency toward overstated EGD contribution figures, driven by the structural exclusion of negative impacts and the incentive for VCs and startups to overstate positive impact.

Finally, the reporting and indicators are not mandatory—failure to report them will not lead to penalties or the withdrawing of investments. This voluntary status once more underlines the weak operational enforcement of conditionality. Green results indicators under climate mitigation criteria in the respective units shall be estimated and reported where indicated on a best effort basis. Failing to report such indicator does not give cause to excluding the loan or investment from EIF’s portfolio. (European Investment Fund, 2022j: 1)

Overall, the official argumentation behind the soft conditionality and enforcement is that the EIF balances accountability and transparency against the required efforts for investors. We, of course, know how to structure financial instruments, how to design them to ensure the best alignment of interests, to find the right tradeoff between, on the one hand, the requirements of accountability and transparency, but on the other hand, not to overload you with red tape. I know it's a constant fight. We are always in discussions to make sure that there is a balance and I think it's never the optimum. But we are committed also in the future to try to make things as simple as possible. (Additional material #1; EIF deputy head Roger Havenith)

This argumentation indicates how in harnessing financial intermediaries to reach the blue economy, the EIF depends on them, and hence adapts the implementation to be convenient (“as simple as possible”) for investors. The EIF needs the VC firms to implement their policy—a dependency, which might be less pronounced on the end of VC firms. European VC firms have collected record volumes of capital over the last 5 years, from an increasingly global and diverse pool of keen capital providers (Atomico, 2023: 340).

The EIF deputy justifies the BlueInvest program by referring to the establishment of the blue economy as an “asset class,” demonstrating how, from the EIF’s perspective, the strengthening of the sustainability aspect of the blue economy is entwined with making it work financially. It’s also about consolidating the industry, making it organically grow, ensuring that not only companies are financed, but we have very robust, robust architecture in Europe of financiers, of investors that are looking into this type of asset class. (Additional material #1; EIF deputy head Roger Havenith)

This entwinement mirrors the EIF’s dual statutory goals of working toward policy goals on the one hand and profitability on the other. In other words, to meet their own ends—that is, the policy goal of sustainability and the overall goal of profitability—the EIF depends on profitable VC investments. These institutional entanglements and dependencies form the basis of infrastructural power: Following its own institutional logic, the EIF needs VC firms to be profitable, and thus has to give in to their demands. Consequently, the EIF leaves the investors much room to shape the intermediation in their own interest by means of weak conditionality and lax enforcement. Put differently, the mechanics behind investors’ infrastructural power arise from the concrete, relational setup of the EIF and the BlueInvest program.

PwC supports the EIF with the execution of the program, in particular by consulting startups and investors and building the “platform”/network. Though not strictly part of the investment chain, as it does not manage capital flow, PwC advises investors and investees in the chain. We provide knowledge about opportunities in the blue economy or how they can set up a fund, how they can create the governance of the funds, the sustainability metrics for the fund […] they will need to put in place sustainability measures to first assess the investment targets and then show reports to their financiers. So that's what we do to provide technical assistance on as well. (Interview #4)

As part of the program, startups are trained in “investment readiness” in order to become investable for investors and investors are provided with technical assistance in order to meet the sustainability requirements of their capital providers, for example, the EIF. Interestingly, the Commission thus mandated the EIF to provide not only financing but also a consultant agency to smooth investing for all private actors involved. This once again underlines the dependency of the EIF on financial actors, which are courted to make blue economy investments as attractive as possible.

Venture capital firms

Five VC firms have thus far received capital from BlueInvest, namely, Blue Horizon Ventures, Ocean 14, Sofinnova Partners, Astanor Ventures, and Sarsia (European Investment Fund, 2022h). These firms, as described above, are tasked with developing concrete ways to measure blue economy impact. When presenting their stance toward sustainability at the yearly BlueInvest conference, VC partners stressed their ability to achieve high returns. This says something about the enormous gains that you can have if you come in early and the technologies are disruptive enough. (Additional material #1; VC fund manager)

Their ability to make other parties’ capital work in their (financial) interest thus seems unaffected by the fact that they operate as a blue economy fund under the BlueInvest program. And so today […] it's possible to drive financial returns and drive environmental returns still with the same leverage. And that's where we focus the most. (Additional material #1; VC fund manager)

While sustainability or “positive impact” is presented as a consideration, it does not change the underlying VC logic of hypergrowth, which dictates that funded companies must have the potential to become very large and valuable and be easily scalable (Cooiman, 2022). About how we select the cases, you need to have a significant net positive impact and, of course, it needs to be very potent growth companies. (Additional material #1; VC fund manager)

VC investing holds a large degree of uncertainty, as most startups will not make it. To compensate for that, and operate successfully in financial terms, VCs thus select and build companies with hypergrowth potential. Thus, the range of blue economy startups that gets funding is limited and reflects not necessarily those businesses with the most ecological potential but rather those that promise the most growth.

As pointed out in the preceding subsection, the EIF requires VC firms that receive BlueInvest funding to tie parts of its carried interest—that is, the variable part of their compensation, which typically equals 20% of the profits made after a successful exit—to the achievement of impact metrics. The VC firm itself is tasked with the identification and measurement of impact metrics, presumably leaving room for an advantageous interpretation of activities. The creation of the asset—the blue economy VC fund—weaves together profitability and sustainability, while at the same time constructing both. [W]e've also aligned our team incentives around this. So, 30% of our carry is tied to achieving impact metrics. So, our motivation as a team to identify, estimate, and measure impact is incredibly high. (Additional material #1; VC fund manager; my own emphasis)

This co-construction of financial value and sustainability impact is also reflected in the financial modeling that firms use as a basis for their decision-making. Ocean 14 has implemented a seemingly sophisticated impact screening tool, which calculates impact based on four dimensions with 5–6 subquestions each, such as “what is the importance of the problem the company is solving?”, which they rank on a 1–4 scale and then draw an aggregated score from. You've got here impact metrics that make a difference for the business, how we're going to measure them and against what and then at the bottom you've got the carry KPI [Key Performance Indicator]. So, this is where we're getting our flag to the most. These are the metrics that we are going to track and measure, and we've got the predicted baseline and target values against which our money is delivered. So, all of this is complicated. It's subject to a similar level of due diligence as the financial DD. We don't make assumptions, we read science papers, we anchor ourselves in facts, that's how Ocean 14 measures Impact. (Additional material #1; VC fund manager)

The resulting model systematically includes impact calculations but ultimately measures the carry, the expected returns of the funds from the perspective of the VC firms. So once this is done, we build the big financial impact model, and this is one model. There aren’t two distinct models. It's all together. (Additional material #1; VC fund manager)

This model’s structure indicates that VC firms reconcile the potential tension between financial returns and sustainability by subordinating sustainable impact to profitability.

Discussion and conclusion

Empirically, this article has demonstrated how, as part of the European Green Deal, policymakers take on the risks of sustainable investments in order to make these investments attractive for financial intermediaries. Inherent to this derisking-based approach, is the fact that to achieve their policy goals, such as sustainability, policymakers need financial intermediaries. Under BlueInvest, the case analyzed in this article, this dependency is particularly pronounced as the EIF—the institution operating the program—is bound to a profitability mandate and thus needs to “partner” with financially successful financial intermediaries. As a consequence of this dependency, the EIF supports VC firms with a consulting agency and gives them a great deal of room to construct the terms of the “partnership,” in order to get them to accept the capital-cum-policy. At the same time, policy goals, in this case ecological and climate effects, are compromised, as demonstrated by the weak conditionality, lax enforcement, and the tendency toward overstated sustainability effects under BlueInvest.

An interviewee explained that there was no conflict between sustainability and profitability; to the contrary, “the more impact that you have, the more financial value you'll create, too” (Interview #5). This logic is tempting, but it only works as long as the definition of “impact” is, to a large degree, carried out by the actors with the ultimate profit motive, as is the case under BlueInvest. Hence, VC firms can follow their logic of hypergrowth in a manner largely unaffected by the constraints of sustainability. Formally, BlueInvest attaches the strings of a “sustainable blue economy” to equity, but in practice, these strings are elastic, easily stretched by the financial firms that deal with them.

To counter the dynamics that limit the transformative potential of derisking, the institutional context of green policymaking would need to be transformed. For instance, without the profitability mandate, the EIF would no longer depend on profitable financial intermediaries and could build up its own capacities to invest directly in sustainable businesses and hold shares long-term. This way, public institutions could encourage a transformation of the economy that is uncoupled from short-term profits and at the same time partake in its long-term benefits.

Alongside these empirical contributions, the article proposes several conceptual moves to shed light on the state-finance nexus, particularly as it operates in the green transition. Overall, the proposed framework of infrastructural-power-as-conditionality-in-the-investment-chain offers an understanding of power in the state-finance nexus that is both concrete and relational. The proposed understanding of infrastructural power as the power to structure relations of intermediation in the investment chain, that manifests in (lack of) conditionality, accounts for the entangled state-finance relations of recent governance approaches. Situating such approaches within the investment chain offers a concrete basis for infrastructural power and expands the scope of the analysis by illuminating the state-finance borderlands. The analysis goes beyond direct state-market interaction points, creating analytical room for intermediation by “borderline” state-market actors, such as the EIF, or financial investors, such as VC firms. Importantly, this concrete foundation of infrastructural power in the investment chain engenders the potential for concrete political action. The infrastructural power of venture capital firms is the direct result of the institutional setup and operational logic of governance programs and, as such, can be politically challenged.

Finally, reading the conditionalities attached to capital-cum-policy as manifestations of infrastructural power gives the analysis of power, which is all too often structural, a concrete object. In the new age of industrial politics, states have announced massive state subsidy programs, such as the United States’ Inflation Reduction Act (IRA) or the European Union’s Green Industrial Plan, that are supposed to tackle the climate crisis and the problem of supply chain resilience by fostering green industries. Conditionalities are the measure of the transformative potential of such programs, which theoretically can fall anywhere between, on one hand, a reproduction of the status quo and, on the other, a true social-ecological transformation that is brought about by a strong state exercising infrastructural power. Crucially, an analysis of conditionalities must not end at the face value of conditionalities but must consider their operational implementation.

My research opens up several avenues for future research. Staying within the analytical approach proposed in this article, future research could follow the investment chain all the way to “blue” or “green” startups and analyze their business models and ways of navigating climate and environmental impact vis-à-vis profit and growth. These businesses may also hold stakes in structuring the relations of intermediation with venture capital firms. Also, the role played by private capital providers to sustainability-oriented venture capital funds deserves more attention—do these providers foster or forestall sustainability? Finally, applying this article’s approach to the field of industrial policy more generally could, for instance, result in an analysis of the United States Chips and Science Act, the resulting investment chains between public institutions, businesses, and research institutions, and the conditionalities that constitute their relations. Such an analysis would be able to evaluate the transformative potential of the program.

Footnotes

Acknowledgements

I thank Laura Horn, the organizers of the special issue Milan Babic and Sarah Sharma, and all other participants in it for helpful guidance and constructive comments.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Note

Appendix

Interview Overview.

#

Type

Active in

Role

Interview type

Date

1

Governmental LP

Europe

Senior management

Semi-structured

28.01.21

2

Governmental LP

Europe

Senior management

Semi-structured

03.02.21

3

Governmental VC

Europe

Partner

Semi-structured

23.06.21

4

Consulting firm

Global

Partner

Semi-structured

27.09.22

5

Governmental LP

Europe

Middle management

Semi-structured

25.11.22

Additional Material: Conference.

#

Title

Host

Date

Link

Last accessed

1

BlueInvest Day 2022

European Commission

28.03.2022

https://blueinvestday2021.app.swapcard.com/event/blueinvest-day-2022

03.11.2022