Abstract

From IPCC reports to global asset managers and governments, calls for more green finance to fuel the sustainability transition are ubiquitous. Concurrently, the critiques of a benign embrace of financial techniques, products, and flows as solutions to the climate crisis are growing louder. As a field of inquiry, IPE has the right tools to address such controversies productively. Yet, we diagnose a lack of what we call a deep engagement of IPE with epistemic and practical questions of what green finance is, how it operates, and its outcomes. The ambition of this special issue is to develop a research agenda that examines the contemporary global and concrete forms of green finance and its governance in order to better understand the following dynamics: first, how political and economic power relations within global finance shape environmental governance outcomes, and second, how the climate crisis itself influences the governance of global finance. To facilitate such thinking, we propose to understand green finance as an evolving ecosystem in the broader web of global finance instead of a specific instrument, asset class or concept. We hold this to be a fruitful approach to engage questions of green finance in both a global and concrete manner across different sectors, geographies, actors, and structures. By acknowledging the global nature and implications of green financial flows, we can push forward thinking not only on climate change and environmental governance in IPE, but also turn attention to the ongoing contestations, contingencies, and crises of finance in the global political economy.

Keywords

Introduction

In recent years, there has been an explosion of green finance, comprising of a multitude of public and private financial initiatives, instruments and institutions that seek to develop environmentally oriented financial services, funds, projects, policies and commodities to support global climate adaptation and mitigation goals, as well as forms of biodiversity (Lindenberg, 2014; Sachs et al., 2019a). Despite its rising popularity, however, the latest IPCC working group III report stressed a continued global deficit of green finance, posing an ongoing obstacle to effective climate mitigation and adaptation. Not only has the IPCC found that funders have failed to meet the USD $100 billion annual global requirement in the past years – it also predicts that climate finance will need to increase beyond present-day levels by a factor of three to six (IPCC, 2022: p. 61). Amid calls for enhanced financial commitment to climate goals, the financial sector has been found to ‘overstate or misrepresent’ its de facto contribution to achieving these goals (Sachs et al., 2023, p. 4). Disturbingly, cumulative public and private financial flows to fossil fuel exploration and production continue to outpace financing for climate mitigation and adaptation (IPCC 2022: p. 15). While the 2023 United Nations Climate Change Conference (COP27) announced a novel loss and damage fund targeting vulnerable countries, finance towards environmental goals continue to be extremely spatially uneven (Robinson et al., 2023). High financial debt precluding low-carbon development investment further compounds this reality for many of these same countries in the global South (Táíwò and Bigger, 2022). Consequently, the IPCC report concludes with high confidence that ‘accelerated international financial cooperation is a critical enabler of low-GHG and just transitions, and can address inequities in access to finance and the costs of, and vulnerability to, the impacts of climate change’ (IPCC 2022: p. 62). The consensus within global environmental policy making circles is that more green finance is needed to address the climate crisis in an effective, equitable and just manner. Critical voices challenge this idea and its implications, arguing that a focus on increasing the scale of finance as a core means of climate action have been constrained to suit finance-led regimes of accumulation and subordination (Alami et al., 2023; Bracking, 2019; Newell, 2019). Questions as to whether more and greener finance is an adequate solution as well as how this greening of global finance can be done in a rapid and just manner sit at the heart of debates within the field of International Political Economy (IPE). Building on these debates, this special issue asks: what do we consider to be green finance? How does green finance emerge and how does it sit alongside other socio-ecologically-oriented forms of finance, such as sustainable, climate or inclusive finance? What actors drive imaginaries, institutional configurations and material outcomes of green finance? Who benefits from the mobilization and deployment of green finance, and why? Finally, is green finance a tool or an obstacle towards sustainability transformations? These open questions reflect a need for a deep engagement of IPE with what green finance is and how it can (or cannot) be used to accelerate green transformations. The ambition of this special issue is to develop a research agenda that examines the respective instruments, initiatives and institutions of green finance to advance such a deep engagement with the topic. This engagement should not only shed light on an understudied domain of global environmental and financial governance but also can help IPE scholars in developing critical and praxis-oriented insights and understandings of green finance for a global green transformation underway.

There have been significant shifts in the global financial industry, which has embraced more concrete and wide-ranging commitments towards climate change and the environment in the last decade (Fichtner et al., 2023). It is no longer the case that only multilateral and public institutions seek out largely voluntary and non-binding private actor engagement on environmental matters (Gabor, 2021). Private financial actors are more fulsomely engaged with a range of activities falling under the umbrella of green finance including through developing public-private partnerships on climate change governance, initiating green funds, and driving climate-related infrastructure investment (see, e.g. Akomea-Frimpong et al., 2021; Baines and Hager, 2023; Sachs et al., 2019a, 2019b). The result is that global financial actors will not only shape environmentally oriented markets but also sustainable transition policy and governance frameworks, which investments individuals become embroiled due to the financialized nature of the global economy, and the day-to-day grounded outcomes for communities that are implicated by forms of green finance (Ciplet et al., 2022). At the same time, however, the forms of continuity and change in the evolution of socially and ecologically oriented forms of finance merits investigation. Green finance is neither a rebranding of financial activities that formerly fell under labels of climate, sustainable, or development finance, nor is it a completely distinct phenomenon. There are loose boundaries and overlaps across all the above forms of finance. It is precisely the evolution as well as processes of expansion and reinvention of socially and ecologically responsible financial instruments and their governance that warrants attention. As finance is constantly reanimated in responses to crises and contestation under global capitalism – a process that Peck (2012) refers to as ‘failing forward’ – the emergence and execution of green finance is a powerful contemporary signifier of this ongoing evolution. As such, examinations of what forms of green finance emerge, what they aim to achieve and the configurations and outcomes that arise therein hold merit, in IPE and beyond.

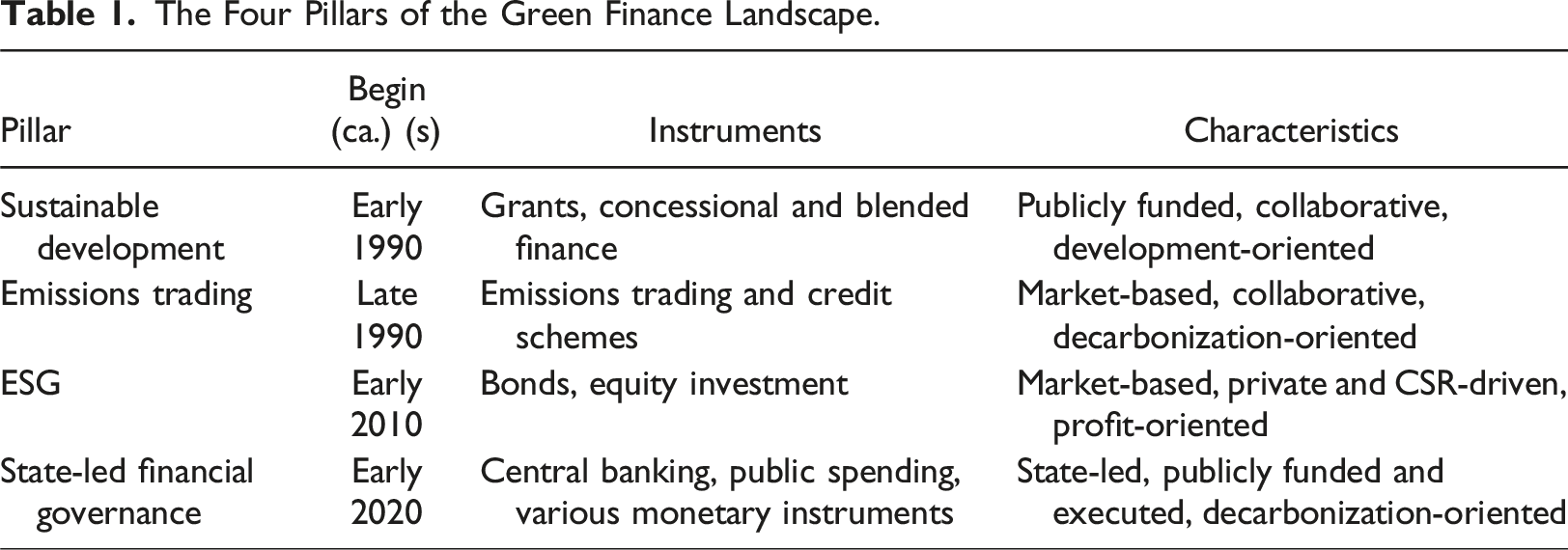

We put forth two considerations here that substantiate our call for a deep engagement with green finance and sketch a potential research agenda. First, we emphasize that green finance has emerged within the historical evolution of global finance and its contradictory governance in the global political economy. The relative novelty and ‘fashion or fad’ (Chwieroth, 2014) around financial phenomena such as green finance must be contrasted against the historical emergence of variegated relationships between global financial governance and forms of crisis and contestation (Samman, 2019). This consideration is important to locate the historical and political significance of green finance among the continuous reinventions, renegotiations and re-legitimations of global finance. We identify in total four main pillars of the current landscape of green finance that evolved historically and constitute the phenomenon today (see next section). Second, we advocate for an ecosystem view of green finance that would allow for deeper and more concrete engagement of IPE with it. By studying green finance as an ecosystem revolving around the supplier-target relationship, we emphasize that it is not just a neatly bounded financial type or instrument, but that green finance comprises various initiatives, instruments, and institutions that are embedded in a diffuse landscape of regulation, politics and power relations. By expanding the analytical approach from type towards ecosystem, we hope to stimulate a broader research agenda that takes green finance seriously as a potentially significant shift within the trajectory of global finance in the coming years. Such an approach allows us to integrate various, multidisciplinary angles in a broader research agenda and thus overcome much of the disciplinary narrowness characterizing, for example, the debate on green finance in financial economics (see, e.g. Zhang et al., 2019). In what follows, we discuss each of those two considerations closer and, in the last section, explain how the papers of this issue speak to this broader research agenda.

A brief history of green finance

The decarbonization of the global political economy is a core contemporary global governance objective. In this context, green finance is growing to shift both the financial industry and economic sectors around climate mitigation and adaptation goals, albeit in a contested and uneven manner (Baines and Hager, 2023; Bracking and Leffel, 2021; Steffen, 2021; see also Guter-Sandu et al. (2024) as well as Chamberlain and Bernards in this volume). Despite a recent and intensifying spotlight, we hold that green finance is not a novel financial type or instrument emerging out of a vacuum but is defined and contested through the evolution of the global financial system. Within this process, green finance evolved from a small and limited form of development assistance to a multi-trillion dollar industry today.

The first prototype of green finance arrangements dates to the establishment of the United Nations Framework Convention on Climate Change (UNFCCC). The first global finance mechanism – the Global Environmental Facility (GEF) – was introduced in 1991, before the 1992 Rio Earth Summit (GEF, 2022). The question of financing of green transformations played an early and often controversial role in global environmental governance (Raustiala, 1997). The GEF dealt with a core problem that still shapes green finance debates today, asking: which actors will pay for global sustainability transitions? In addition, the GEF included some key characteristics of contemporary multilateral green finance such as the attempt to de-risk, crowd in and leverage private finance due to the limited funding public climate funds and similar entities enjoy (Pearce, 1997). The establishment of the GEF followed major trends in post-Cold War global governance, attempting to include voices critical of conventional developmental institutions such as the World Bank and involving non-state actors like NGOs in green finance arrangements (Woods, 1999). As a multilateral finance body, the fund relies on financial contributions from its roughly 40 nation-state stakeholders. This focus on sustainable development finance and on market-based solutions became a key pillar of green financial governance. Later initiatives such as the World Bank’s Climate Investment Funds (CIFs), the UNFCCC Green Climate Fund (GCF) and the EU’s European Fund for Sustainable Development (EFSD) follow this sustainable development logic through grants or concessional and blended finance instruments to developing countries.

A second market-based green finance pillar that centers on emissions trading emerged in the same era: The Kyoto Protocol (1997), which introduced the credit scheme triad of the Clean Development Mechanism (CDM), the Joint Implementation (JI) and emissions trading schemes. Together, these instruments intended to lower the costs of decarbonization projects, also through global North-global South collaboration. Similarly to the GEF, these flexible mechanisms engaged with sustainable development through market-based mechanisms to provide green finance to specific projects. They reflect a strong contemporary bias of environmental governance toward market-based solutions that were supposed to find cost-efficient ways of mitigating climate change (Bailey and Maresh, 2009). This is not a coincidence, given that the 1990s were the golden era of neoliberal globalization and financial liberalization (Helleiner, 1994; Krippner, 2012). The rewiring of development into a sustainable and market-based project also narrowed possible questions of governance towards the mobilization of green finance as both a solution and profit opportunity (see Schoenmaker, 2017). While this approach was significantly modified in later years, it still plays an important role in how green finance functions today.

A third key pillar in the evolution of green finance are the different forms of Environmental, Social and Governance (ESG) investment that came to prominence in the early 2010s. ESG can be a form or type of investment as well as refer to sets of standards such as used for creating ESG indices. It is not only restricted to firm-investor relations but also plays a role between suppliers and lead firms, for example, in clean manufacturing. Investors that seek sustainable or green assets can theoretically pick products, assets and projects that adhere to one of the many global ESG standards and hence increase green financial flows towards these targets. In reality, however, only a few standards and indices are de facto able to channel investment toward green targets, exemplifying the still limited regulatory landscape (Fichtner et al., 2023). The introduction of the first green bond by the European Investment Bank – the ‘Climate Awareness Bond’ in 2007 – marked the beginning of the proliferation of ESG instruments (EIB, 2023). Issuers of green bonds, as other assets such as green equity, pledge to use the investment they receive towards sustainable projects in accordance with a set of standards, be it ESG or other taxonomies. The rise of such green investments expanded the landscape of green finance significantly because they do not necessarily rely on public de-risking or leveraging through international institutions such as the World Bank. This lack of public involvement also leads to loopholes in ESG governance, which make the certification of such instruments a key determinant of their de facto environmental performance (Flammer, 2020). Different from mechanisms like emissions trading or concessional finance, ESG-type investment is profit-oriented and geared towards growth. The green bond industry, for example, grew from almost zero in the early 2010 to a total issuance of over 2tn. USD just a decade later (Schmittmann and Teng, 2021). The rise of ESG marks the involvement of important aspects of the global financial system (such as large corporations or asset managers) in the landscape of green finance. While riddled with problems, we can for the first time see that global financial actors recognize both the green finance gap on a global scale but also the potential profits arising out of green assets and industries. The rise of ESG and instruments like green bonds in the early 2010s hence intensifies the contradictions and tensions between the necessity of the funding of green projects for successful global decarbonization on the one hand and the profit interests and opportunity-seeking financial capital on the other hand (see also Alami et al., 2023).

The Four Pillars of the Green Finance Landscape.

This historical overview suggests that green finance is not a static concept or set of instruments but one that evolves and transforms over time, being re-conceptualized in relation to its previous iterations as well as developments and crises in the global financial system. 1 The rise of ESG-oriented investment after the global financial crisis, for example, reflects a growing awareness of the private sector regarding the capacity of green financial assets to become profit opportunities, whereas it has been before delegated to publicly funded de-risking and development finance. The ensuing flood of green finance in the Global North and the boom of ESG instruments is a consequence of these developments (Wheatley, 2022). Likewise, the nascent turn to macrofinancial planning and state-led investment forms is a direct response to the ineffectiveness of market-based forms of green finance to reduce emissions in accordance with the Paris Agenda. Understanding the historical context of the emergence of different aspects of green finance is, however, not merely a chronological exercise. We frame the different aspects of the green finance landscape as pillars to indicate that they still play a major role today. Sustainable development and the necessary financial means, for example, are still the main issue for authoritative bodies like the IPCC (2022). The different pillars are situated alongside one another and take different roles and functions within the broader landscape of green finance. We describe this evolving and expanding landscape as green finance ecosystem to capture these developments better and to render green finance productive for IPE research. As hopefully became clear, thinking about green finance as a particular instruments or an entity with bounded characteristics and mechanisms under-appreciates its transformative and contested nature. Instead of a broad but arbitrary signifier on the one hand and a narrow description of singular instruments on the other hand, we suggest understanding green finance as an evolving ecosystem within global finance.

Situating the ecosystem of green finance

The ecosystem view we put forward combines insights from the financial ecologies and the global financial networks literature to describe the various actors, structures, and main flows involved in the supply and provision of green finance (Appleyard et al., 2016; Liu and Lai, 2021; Oatley et al., 2013). By ecosystem we mean the sum of actors, institutions, instruments, ideas and politics (including national and international regulation and infrastructures) that govern how, where, and to what end green finance is supplied in the global political economy. The ecosystem metaphor emphasizes that green finance is not just a type or an instrument within global finance, but that it is embedded in a wider landscape of regulation, ideologies, politics, and power relations that govern green finance supply and its targets. The implications of this approach are to understand the boundaries of green finance as porous, overlapping with forms of climate, development and socio-environmental finance, and to recognize that the parameters of green finance shift over time (as described in the previous section). While in early days the landscape of green finance consisted mainly of (limited) multilateral climate funds aimed at mitigation and adaptation (Mathews and Kidney, 2012), it meanwhile developed into a broad and contested ecosystem with manifold actors, instruments, and high volumes of capital flowing through it (Cunha et al., 2021; Babic, 2024). These changes speak to the idea of financial ecosystems as ‘complex adaptive system [s]’ (Leyshon 2020: p. 131). Green finance, as any other part or sub-system of the global political economy, adapts to and in turn shapes new political realities. Today, the decarbonization of the global political economy and climate adaptation are becoming overarching global political objectives. The mobilization and proliferation of green finance as one major tool of crisis fighting is both real as it is politically contested and uneven in its consequences (Baines and Hager 2023; see also Chamberlain and Bernards in this volume). As an example, the increasing global issuance of green bonds and their financial and political consequences expanded the ecosystem of green finance as well as its weight within the wider global financial system significantly over the last decade. An ecosystem view incorporating these and other structural changes allows us to go beyond static notions of what constitutes green finance; and to integrate its study into IPE research on global finance.

The financial ecologies perspective ‘recasts the [global] financial system as a coalition of smaller constitutive ecologies’ (Lai 2016: p. 30) and draws our attention to the unevenness and inequalities of financial systems (Leyshon 2020: p. 128). This perspective suggests analysing global ‘finance’ as a number of concrete and empirically traceable elements instead of an abstract realm of the global political economy. This speaks to the call for more deep engagement with green finance in this special issue. A network perspective on global finance complements this conceptualization by bringing in the systemic aspects of green finance (Oatley, 2019). Green finance is being supplied and channelled within global financial (infra)structures that determine the uneven outcomes theorized by the financial ecologies literature (Bernards and Campbell-Verduyn, 2019; De Goede, 2021). These structures as well as the actors and instruments within the global financial system can be understood as networks governing, among others, green financial flows (Bauerle Danzman et al., 2017). This focus on global financial networks and how they govern the proliferation of green finance is more useful for an IPE perspective that seeks to extend beyond the focus of the financial ecologies perspective on everyday practices (see e.g. Coppock 2013).

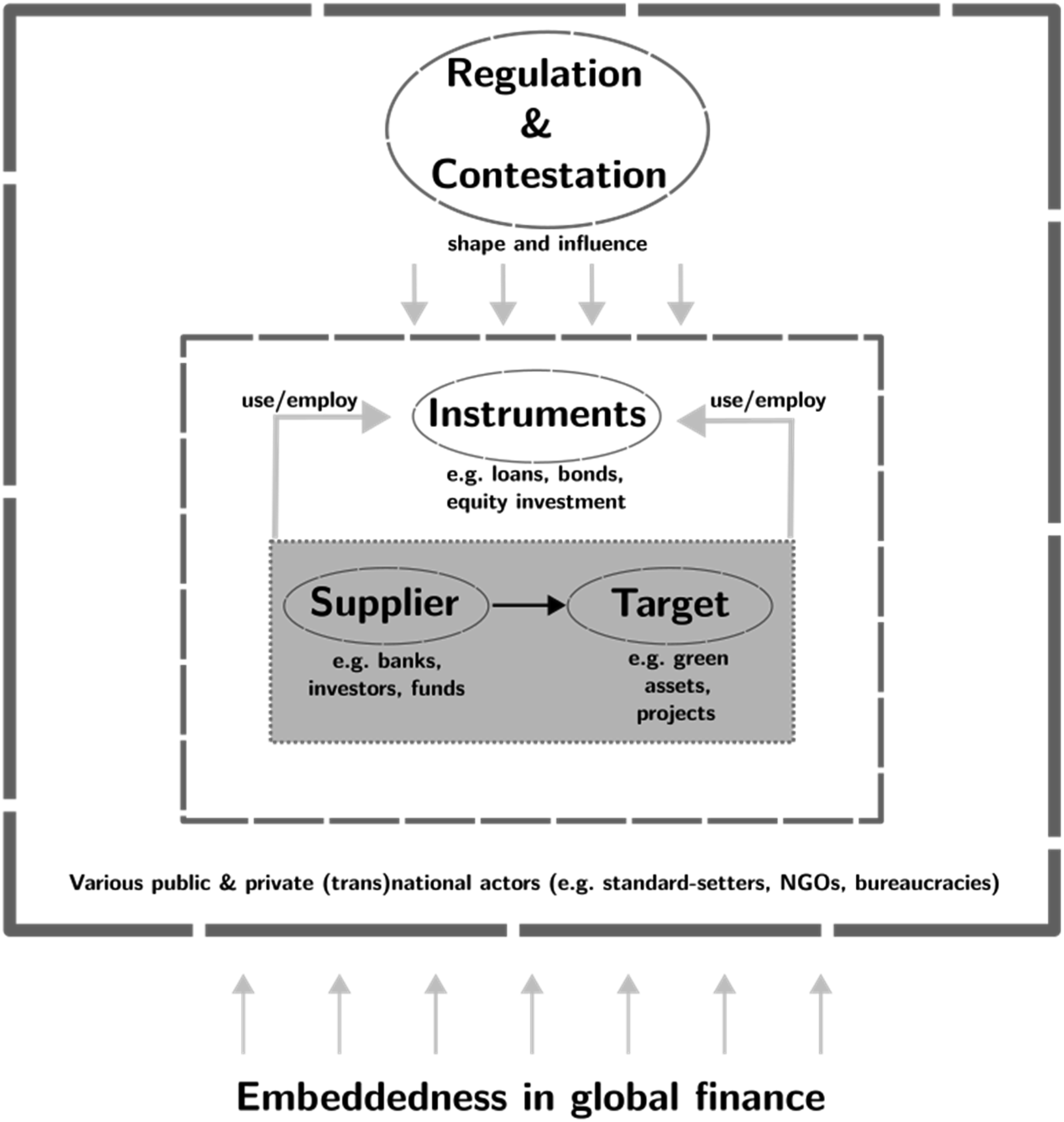

The skeleton of this green finance ecosystem consists of four different layers depicted in Figure 1. The core of this ecosystem is the relationship between suppliers and targets of green finance. Targets are usually green projects or assets that contribute to increased sustainability, mitigate or adapt to climate change. Suppliers can be any actors deciding to supply such green finance, from households to multilateral development banks and climate funds. Akomea-Frimpong et al. (2021), for example, foreground the role of private banks in supplying green finance. Other actors including central banks (Dikau and Volz, 2021), pension funds and insurance companies (Sachs et al., 2019b), institutional investors in general (Gianfrate and Lorenzato, 2019), fintech firms (Nassiry, 2019), sovereign wealth funds (Ackah, 2021) and other public actors (Marois, 2021) are involved in providing, fostering or structuring green finance. Those and other institutions are both to be found on the supplier-side of green finance, as well as involved in governing and channelling green investment through ideational, institutional and material means. These actors are not only (and not primarily) providers of green or sustainable finance; they evolve out of the global financial system and successively green their investment in contested and politicized ways, including by norm setting on what effectively constitutes a legitimate avenue for green investment (Guermond et al., 2023; Newell and Johnstone, 2018). The global ecosystem of green finance.

The next layer beyond the immediate supplier-target investment relationship are different instruments that facilitate the provision of green finance. Providing finance to green projects and assets can take place in various ways, from debt instruments to forms of concessional and blended finance. Probably best-known among those instruments are green bonds that aim to raise money for green projects (Maltais and Nykvist, 2020). The demand for green bonds has been on the rise in recent years, as has the discussion on their merits and problems, such as a global governance gap of these instruments that is being filled by decentralized private actors (Park, 2018). Another relevant instrument is green or environmental mutual funds that have been specializing in investing in green projects (Climent and Soriano, 2011). Further tools like green insurance or specialized products like green infrastructure bonds are also expected to increase their presence in global financial markets in the coming years (Akomea-Frimpong et al., 2021). According to current estimates, the totality of capital located in sustainable finance instruments, of which green finance is a major part, exceeds $35 trillion (Huang, 2021). The largest chunk of this investment, and the strongest growth across the last decade, can be found in green bonds that rose 20-fold since 2015 and now represent around 10% of global debt markets (Toole, 2022). But also other instruments such as green credit schemes, equity investment or different forms of concessional and ‘blended’ finance contribute to the expansion of the ecosystem of green finance (Naran et al., 2022; Schmittmann and Teng, 2021). The large asset managers such as the Norwegian Sovereign Wealth Fund GPF-G also administer large sums of green equity, but clear estimates of this are difficult and diverging. The global asset manager State Street, for example, self-declares 12.5% of its total assets to be green, while only 0.5% of Vanguard’s assets – another large asset manager – adheres to ESG standards (Flood et al., 2023; State Street, 2022). One major problem in quantifying the amount of global green finance is a lack of global standards that still bedevil systematic analyses of the phenomenon (Aramonte and Zabai, 2021). This is not only relevant from a purely academic perspective but obscures the actual extent and effect of green finance for investors, regulators and observers. It is unclear whether green finance instruments will displace unsustainable instruments or will drive investment away from ‘brown’ projects, which is a prerequisite for decarbonization.

Clear regulatory standards would facilitate comprehensive analyses of the effects and problems of green finance over time. However, these regulations are themselves subject to political contestation and conflict, for example, in the realm of green accounting (Thistlethwaite and Paterson, 2016). The third layer of regulation and contestation hence embeds the supplier-target relationship as well as the various instruments of green finance into the political reality of the global economy. This involves the entirety of actors, institutions, rules and regulations and the conflicts emerging out of their interplay to establish a functioning governance of green finance. Among the major standard-setting and -contesting actors in this respect are naturally governments, but also other players exercising private authority such as index providers and ESG rating agencies (Petry et al., 2021). The core task of regulatory action today is to agree on a common global taxonomy on what constitutes green finance. This missing taxonomy is especially a problem on the firm-level, where, for example, different ESG rating providers come to different evaluations of investment targets (Berg et al., 2022). Consequently, efforts on, for example, the EU-level are aimed at creating such taxonomies, but are also subject to the power and politics involved in such regulatory battles (Dumrose et al., 2022). In 2021, the EU and the People’s Bank of China began to work on a common taxonomy that so far has no legally binding powers but illustrates the difficulties of agreeing on common standards when it comes to green finance (IPSF, 2021). From research into previous rounds of cross-border regulatory efforts, we should expect rising complexity and contention going forward instead of (sorely needed) quick agreements on green standards (Farrell and Newman, 2015). Beyond these standard-setting aspects, private and public regulatory authorities also influence other realms of green finance, for example, the provision and regulation of carbon pricing as a key tool for redirecting finance into green assets and projects (Hongo, 2019). The higher carbon prices rise (through regulatory action), the more inflows into alternative assets like green finance can be expected. At the same time, the conflicts about how to define and taxonomize green assets will only increase, as larger swaths of global capital will target these new investment classes as replacement for stranding carbon assets. These are by no means technical processes and involve political contentions and controversies about the distribution of gains and losses in a heating world (Colgan et al., 2020).

This leads us to the fourth and final layer of the ecosystem of green finance, namely its embedding into the broader realm of global finance. From a critical political economy perspective, this embedding requires a critical reflection on how the challenges associated with transforming power relations within global financial governance forays into ecological matters. Voices critical of green and sustainable finance argue that expanding supposedly ‘good’ forms of green finance is both contributing to increased financialization and presents an obstacle to rapid and just decarbonization and transformation (Bracking, 2021; Guermond et al., 2023; Perry, 2021). In this vein, finance acts as an obstacle cementing existing inequities and bolstering hierarchical power relations, especially when combined with supposedly ‘inclusive’ and ‘sustainable’ financial technologies (Bernards and Campbell-Verduyn, 2019; Bernards et al., 2020). Landmark studies that explicate this problematic link between finance and green transformations include Gabor’s (2021) critique of the nexus between financial firms and state guarantees in green development finance; Christophers’ (2021a, 2021b) findings that green transitions face serious obstacles due to the demise of publicly listed oil firms and the profitability of fossil fuel extraction; Bracking’s (2019) and Bracking and Leffel’s (2021) analyses of the feasibility and deficiencies of climate finance governance; Newell’s (2021) survey of financing energy transitions; and Langley et al.’s (2021) study on how the decarbonization of capital is an uncertain and incomplete process demanding critical scrutiny. Further attention has been drawn to the manner in which large financial institutions like the ‘Big Three’ asset managers Blackrock, Vanguard and State Street have been found to hinder rather than to support effective environmental governance, and hence to be rather mediocre environmental ‘stewards’ (Baines and Hager, 2023). These and other studies show how green finance is riddled by problems and contradictions that stem from the fact that it is embedded within global finance as a complex, contested and evolving system (Oatley et al., 2013). Analysing this layer is key to understanding the potentials and limitations of green finance for transforming the global political economy in the age of climate breakdown.

Taken together, such an ecosystem view on green finance allows us to highlight the political nature of its emergence, its recurrent and emerging forms of contestation and crisis in, and its relationship to the governance of global finance. It also aids in better understanding the resilience and flexibility of global finance as a socially contested set of relations in the global political economy. As material and discursive pressure mounts for transforming carbon capitalism in the present (c.f. Newell, 2021), actors within the global financial system respond by renegotiating the boundaries and power relations of what is considered to be legitimate green or sustainable financial activity over time (see also Bogner, this special issue). Harking back to the previous section, this evolving ecosystem of green finance has emerged in response to forms of climate crisis and contestation surrounding its governance. Importantly, however, the evolutions and rearticulations of socially and environmentally-oriented financial ecosystems do not arise in a natural or neutral manner in response to new crises and concerns. As Soederberg (2014) argues, finance itself is a social relation, not merely a neutral instrument for other ends. From a political economy perspective, the relations of power underpinning the ability to create, govern and consume finance capital are embedded in the dynamics of capital accumulation processes in the global political economy (Soederberg, 2014: p. 29). Narrow debates about green finance as a novel or technical instrument, however, tend to divorce the potential of forms of credit oriented towards sustainable transitions from the relations of power that inform crises in capitalism, including the climate crisis and its uneven outcomes. As such, the contestations surrounding the governance of finance considering the climate crisis also reflect a crisis of the legitimacy of liberalized global finance, particularly in its role in perpetuating unsustainable growth trajectories (Hasselbalch et al., 2023). The ecosystem of green finance entails such contestation of well-known inequities and political fault lines of the global financial system, while it also shifts some of these battles onto new terrains (such as new asset classes) (Christophers, 2021b; Langley et al., 2021).

Overview of the papers in the special issue

The contributions to this special issue look at diverse aspects of the ecosystem of green finance from a variety of standpoints and perspectives. We see these contributions as important interventions to examining this wider ecosystem, but also as being necessarily partial: there are a vast number of actors, initiatives, instruments, and politics of green finance to examine, and this ecosystem continues to grow and evolve. What this set of papers does, however, is to survey important contemporary segments of what green finance looks like and how it operates.

Bogner (2024) sketches the legal geographies of green finance by asking how law technologies and knowledge practices influence the provision of green finance. Bringing together literatures from political economy and economic geography, the paper develops further the notion of ‘asset-coding’ – the transformation of assets into capital – as a key mechanism that creates and reproduces the ecosystem of green finance. Bogner draws on original interviews and document analysis to argue that much of what counts as green finance is subject to similar asset-coding practices as conventional types of finance. Using the examples of energy infrastructures, carbon markets and offshore jurisdictions, he shows how conventional practices from mainstream finance carry on in the sphere of green finance. The author emphasizes the fact that much of what is legally and technically occuring in the global green finance ecosystem has its origin in a few powerful jurisdictions that dominate green asset-coding. This finding raises important questions and doubts about the ability of current green finance governance to fulfil the Paris pledges of annual multibillion financial flows to places where this investment is most needed.

Chamberlain and Bernards (2024) follow up on the theme of the climate-development-finance nexus, scrutinizing the African Risk Capacity (ARC) as a key green finance instrument reflecting Global North-Global South development aid dynamics. Developed in partnership between the UK’s Department for International Development and the African Union, the AR’C’s insurance mechanism was crafted to protect climate-vulnerable populations and address loss and damage costs arising from climate-related hazards including flooding and drought. Chamberlain and Bernards analyse and interpret this scheme as the expansion of the frontiers of green finance into the realm of development aid. Critically, they argue that projects like the ARC involve major contradictions that can teach us a lot about the political contestations surrounding green finance. While the core idea of such insurance-based instruments is to divert climate risk from (financially) vulnerable populations, the involved actors also see it as means of unlocking new frontiers for finance capital. This contradiction – increasing population resilience while promising a profit to capital markets – speaks directly to the core tension between profit and transformation our special issues seeks to problematize. Drawing on insights from the literature on financial subordination, the paper concludes that mechanisms like the ARC are rather detrimental for re-routing economic resources towards places where they are most needed and hence a burden for realizing climate justice. Importantly, their paper testifies to the deep entanglement of green finance with the global financial system (and its consequences for governing green finance), which we pointed to earlier.

Cooiman (2023) connects to this critical view on green finance by zooming in on a particular case of green finance derisking. She analyses how the European Investment Fund, mandated by the European Commission, tries to draw in venture capital to propel the so-called blue economy of ocean ecosystems. Cooiman develops an investment chain perspective that allows her to map the actor-constellations and capital flows between the various parties involved in this investment program. For this, the author draws on qualitative interviews and fieldwork with finance and government actors and official document analysis. Cooiman shows how the attempt by policymakers to make green and blue assets attractive to investors requires the introduction of financial intermediaries that follow the profit-motive. A major consequence of this enmeshing is that conditionalities are weakened (or not present to begin with), diluting the actual sustainability goals that motivate such green finance mechanisms in the first place. The paper proposes to view the power financial intermediaries exert in these constellations as infrastructural power through conditionalities within investment chains. This new theoretical perspective opens up a broader research agenda on the entirety of such investment chains as well as the political economy of de-risking and the role of green finance in it. Cooiman impressively shows why ‘following the investment chain’ through the global ecosystem of green finance is key for determining the sustainability effects of such investments.

van der Zwan and van der Heide (2024) shed light on another important group of actors within the global green finance ecosystem, namely, transnational sustainable finance initiatives (TSFI). TSFIs do not only seek to shape the rules and discourse on green finance globally, but are also important socialization fora for transnational actors in this space. The authors argue that analysing the overlap of memberships of large-scale investors in such initiatives can inform us about power relations and the network centrality of specific global green finance actors. Van der Zwan and Van der Heide use data on 30 TSFI and over 10,000 datapoints to construct these overlapping networks. In their findings, the authors differentiate between three main groups: membership ‘collectors’ (investors with a high number of ties), ‘mediators’ that connect peripheral and central network actors and more activist ‘performers’ within these initiatives. At the core, 21 investors – mostly from the Global North – represent the core of this TSFI network and hence hold power in this transnational structure. The results of this analysis are sobering: the key players in these important networks are well-known and often-criticized corporate financial actors that are unlikely to push for real, transformative action when it comes to the diffusion of green finance. From the perspective of the special issue, this raises – similar to Cooiman’s findings – important questions about the role of and balance between private and public financiers in the governance of the sustainability transformation and whether the dominance of large financial investors in the global (green) finance ecosystem is not rather an obstacle for this endeavour.

Guter-Sandu, Haas and Murau (2024) take a step back from the messy politics of green finance to reflect on the essential question of how to actually green the financial system as a whole and hence expand the boundaries of the global green finance ecosystem. Their paper focuses on Europe and argues that a piecemeal approach to the green transition – for example, by relying on central banks or other key actors – quickly runs out of steam when it comes to the massive financial challenges of the next decades. Instead, they propose a Monetary Architecture perspective that sees monetary and fiscal systems as a set of dynamic networks of interlocking balance sheets. Doing so enables the authors to propose a concrete four-step process that first expands and finally contracts the green macro-financial regime necessary for the green transition. Guter-Sandu et al. thereby find that there is enough European elasticity space for such a large-scale financial undertaking, but that not all steps of their framework are equally feasible. They conclude that more research into the mechanisms of green monetary expansion is necessary to fill these gaps and enable a realistic shot at greening the financial system. In taking a systemic perspective, the paper speaks to the special issue’s emphasis of the global (and hence systemic) character of the green finance ecosystem, its main actors and political contestations.

The set of research papers in this special issue are complemented by two reflections by Helleiner and Clapp and by Newell and Bray. These pieces undertake a ‘stocktaking’ on the state of green finance research in IPE and critically reflect on the contributions of the papers in this issue. Importantly, both pieces also point to relevant research avenues for future contributions that will further develop understandings how green finance is deployed, the relations of power shaping its outcomes, and the academic and praxis-oriented approaches needed to confront challenges at the environment-finance nexus over the coming years. These valuable reflections, alongside the collection of research papers in the issue, will serve as a reference point for further stimulating conversation and debate on this subject.

Helleiner and Clapp push for an even broader ‘open-ended’ conceptualization of green finance than we point to in this introduction on multiple fronts, including by extending its historical lineage and regarding what subject matters should be considered to sit within the scope of green finance. The latter point of scope includes considerations that financial regulatory initiatives not themselves designed to address environmental issues have, in practice, both positive and negative consequential environmental outcomes. Helleiner and Clapp also advocate for broader theoretical engagement with the politics of green finance beyond what they frame as predominantly neo-Marxist approaches, particularly to better understand what ideas and institutions shape green finance and how contemporary geopolitical power struggles are key drivers of change in environmental governance.

Newell and Bray focus their intervention on ‘the explanatory traction of “infrastructural power,”’ which they define as forms of influence and control over hard (i.e. roads, powerplants and digital infrastructures) and soft (i.e. models, professional networks and statistics) forms of infrastructure in the political economy. Infrastructural power, the environment and global finance intersect at the heart of sustainability transitions, as those wielding power over infrastructures (and their financing) influence the shape and the scale of collective responses to multidimensional ecological crises. Critically, Newell and Bray note that despite our position that private entities are increasingly motivated to engage with environmentally oriented finance, they are continuously unwilling to take on the risks and liabilities of engaging in environmental policies, which fall to the public sector. The outcome of the above dynamic results in ‘transformismo’ over ‘transformation’, where powerful actors seek to consolidate power through ecological opportunities while minimizing green infrastructure investment and power shifts that threaten their interests (Newell, 2019).

Both Helleiner and Clapp as well as Newell and Bray speak to the need to develop further empirically contextual, geographically diverse and richer comparative studies that highlight distinctive experiences at supra-national, national and subnational scales, and pay special attention to understudied powerhouses that shape the trajectories and governance of green finance, notably China and India. Our initial set of questions framing this special issue considered the emergence and dynamics of green finance (what is green finance? what actors drive green finance? who benefits and why?), and how to best conceptualize green finance as a tool or obstacle towards sustainable transformations. While both critical reflections engage with the above set of questions, they also demonstrate the need to continue to understand the evolution of the green finance ecosystem. This speaks to the need for what we call deep engagement with how green finance is employed to accelerate or stagnate green transformations in a more developed and multi-contextual manner.

Conclusion and outlook

This special issue highlights why and how green finance deserves to be interrogated by IPE theorists as more than a fad, but rather a site of analysis as a multifaceted and evolving ecosystem with important social, economic, political and ecological consequences. We aim for the issue to constitute a platform to develop a broader set of conversations on the ecosystem of green finance. The lionshare of attention on the relationship between finance and the environment has thus far focused on how global financial governance has impacted climate change, largely in negative ways (Bracking, 2021; Bridge et al., 2020; Langley et al., 2021). We draw attention to the power and politics driving the emergence and transformation of green financial instruments and initiatives. This points to a reciprocal relationship between finance and the environment: global financial governance does not only shape environmental outcomes, but the political contestation over the climate crisis and material environmental changes importantly also shape the trajectories of global finance (Grippa et al., 2019).

An important silence in the issue concerns the reality that the critique of green finance does not only come from environmental activists and those critical of green finance continuing to perpetuate the status quo. The rise of populist and right-wing rhetoric against socially and environmentally oriented forms of finance is now also a powerful form of contestation that drives the forms and outcomes of green finance, particularly in the context of a second Trump administration. For example, the politicization of ESG standards by right-wing movements demonstrates the confluence of forces shaping the future of green finance and the role of global finance in general. These increasingly popular narratives have developed to represent contradictory messages: first, that socially and environmentally oriented forms of financial governance are low in returns and hence negatively impact profitability, affecting public investments, regular citizens’ pensions and corporate profits. Second, that ‘woke' capitalism represents tokenistic and hypocritical symbols of progressive policy that mask undemocratic forms of collusion between the private and public entities that not only do not enjoy popular support, but are also ineffective. This contestation moves beyond discourse, and has significant material outcomes, for example, in the United States, where some state-level public entities have banned considerations of ESG in pension portfolios and green municipal bonds (Gelles, 2023). The backlash against green forms of finance might herald a general scaling back of global financial relations and financialization in the context of a more protectionist and less open global economy (Babić et al., 2024). Thus, it becomes ever more important to deepen concrete understandings of how green finance consolidates in the face of social and environmental crisis and contestation; and how it affects the future of global finance as such.

As the articles in this issue show, what is considered to be a legitimate intervention to achieve shared climate goals continues to be predicated upon making financial markets work and expanding forms of finance capital. We suggest that emerging research agendas on green finance should continue to work to become both more global and concrete. By global, we refer to the fact that many of the ongoing discussions put the need of developing countries to receive, or the ability of developed countries to provide green finance central. These discussions often rely on a dyadic understanding of how green finance is reproduced in the global political economy. We seek to expand this focus toward the global interdependencies that characterize global finance as a complex ecosystem and to promote more diverse examinations globally, including the prominence and power of countries including China and India driving the shape and trajectories of green finance (Oatley et al., 2013; Helleiner and Clapp, this issue). Such a view can help to disentangle the ambiguities, contingencies, and contestations of green finance between different social forces on a global scale. It helps to highlight global power relations such as financial subordination (Alami et al., 2023) that continue to play a role in green transitions, and which remain invisible when we assume dyadic financial relations between the Global North and Global South. By concrete, we mean to foreground more contextually driven and historically informed examinations of the role of global finance in climate change and environmental governance, how (financial) actors seek to reproduce the legitimacy of markets in the face of the climate crisis, and who benefits and why from the role of green finance in global environmental governance. This includes more in-depth relational comparisons across regional, state and subnational scales of governance that seek to understand the dynamic relationship between financial power and environmental policy and outcomes.

The above approaches have the capacity to understand the multi-faceted nature of green finance in a manner that avoids getting caught up in technical and potentially unproductive delineations from other forms of socially and environmentally oriented finance. Furthermore, these perspectives can effectively facilitate research into how green finance seeks to reproduce the legitimacy of financial institutions in the face of climate crisis; how green finance is publicly and privately governed; how it is being increasingly contested from both left- and right-wing quarters on similar premises but for importantly divergently purposes; and who benefits from the proliferation of green finance in the global economy. Green finance has staying power as an object of research that should be interrogated across different sectors, geographies, actors, and structures. IPE scholarship is well placed for this endeavour, not at least because it problematizes both the historical evolution as well as the contemporary shape of the ecosystem of green finance. We hope that this special issue provides a necessary impetus to further centre climate change, and especially green finance, as a key object of political economy research for the foreseeable future.

Footnotes

Acknowledgements

We would like to sincerely thank Derek Hall for his productive comments on a previous iteration of this article, the various ‘Green Finance’ workshop members who participated in early conversations on this special issue, and the editing team at Competition & Change, particularly Hulya Dagdeviren. We also want to thank the authors of papers in this special issue, whose feedback went into the final version of this article. Special thanks go to Jeniffer Clapp, Eric Helleiner, Peter Newell and Callum Bray, who were kind enough to provide us with two reflective articles that engaged in-depth with the other papers in this special issue. We are honored to include their work in this collection.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Early Career Fellowship (to Babic) has received funding from Independent Social Research Foundation and Independent Research Fund Denmark 2102-00098B (to Babic) for research related to this publication.