Abstract

The last 20 years have seen the emergence and proliferation of transnational sustainable finance initiatives (hereafter: TSFI). From associations like the Principles of Responsible Investment to pledges like the Finance for Biodiversity Pledge, investors have connected with each other and with other kinds of organisations in transnational fora dedicated to sustainable finance. Taking inspiration from political economy scholarship on global corporate networks, we apply a network perspective to the transnational governance of sustainable finance, examining the overlaps between investors’ membership in TSFI. In particular, we aim to identify those investors’ that hold a large number of TSFI membership (collectors), that connect centrally located TSFI with those at the margins (mediators), and that take on active roles within TSFI (performers). Analysing membership data for 30 TSFI, totalling 10.602 observations, at three analytical levels, we identify a group of 21 investors holding core positions in the global network. The majority of these investors are active in asset management and located in Nordic or continental European political economies. The predominance of some of the world’s largest investors in our three member categories suggests that the transnational governance of sustainable finance relies in part on the activities of actors that are associated with harmful financial practices. Nevertheless, the simultaneous presence of publicly owned enterprises on our list of most connected members also indicates the importance of public leadership in the transnational governance of sustainable finance.

Introduction

In the past decades, large investors have been assigned a significant role in the transnational governance of various global sustainability challenges: from climate change to the conservation and restoration of nature to the transition towards a more sustainable economy more generally. Following the Paris Agreement (2015), redirecting financial flows has become an integral part to containing global warming and averting biodiversity loss (Art. 2.1 sub e: ‘Making financial flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development’). Governments, however, only have limited means to achieve the US$3–6 trillion needed annually to realise the Paris Agreement goals by 2050 solely through public finance (UNEP, 2022). Turning to private finance instead, governments, civil society organisations and activist movements are putting increasing pressure on large investors to adopt sustainable practices.

Within this context, the past 20 years have witnessed the emergence and proliferation of transnational sustainable finance initiatives (hereafter: TSFI). From associations like the Principles of Responsible Investment to pledges like the Finance for Biodiversity Pledge, investors have connected with each other and with other kinds of organisations in transnational fora dedicated to sustainable finance. In its broadest sense, sustainable finance is an umbrella term for investments that combine profit-seeking with non-financial goals. Some sustainable investors, for instance, have adopted the so-called ESG (environmental, social and governance) terminology, encompassing different kinds of investment: from the exclusion of harmful assets to shareholder engagement. Others restrict sustainable investments to, for instance, investment in the United Nations Sustainable Development Goals or to green finance benefiting our natural environment. For all these different conceptions of sustainable finance, dedicated initiatives have emerged at the transnational level.

Despite diversity in terms of thematic focus and organisational forms, TSFI do not exist in isolation of one another. Many TSFI are connected, because they are initiated by the same organisations or because they are part of the same global coalition of advocacy groups. Moreover, many TSFI count the same investors among their members. Larger investors in particular are members of multiple TSFI, across a range of topic areas. For this reason, we argue, TSFI can be considered a global network, consisting of the initiatives themselves and their members. As a global network, TSFI have the potential to act as an important infrastructure for the diffusion of sustainable finance principles and practices. This is particularly important for those conceptions of sustainable finance that have not yet been widely adopted, such as biodiversity finance or blue finance for ocean conservation. While TSFI constitute one of several possible avenues (e.g. legislation, social movement activism) for the diffusion of sustainable finance, a study of their network composition might generate new insights on their potential impact.

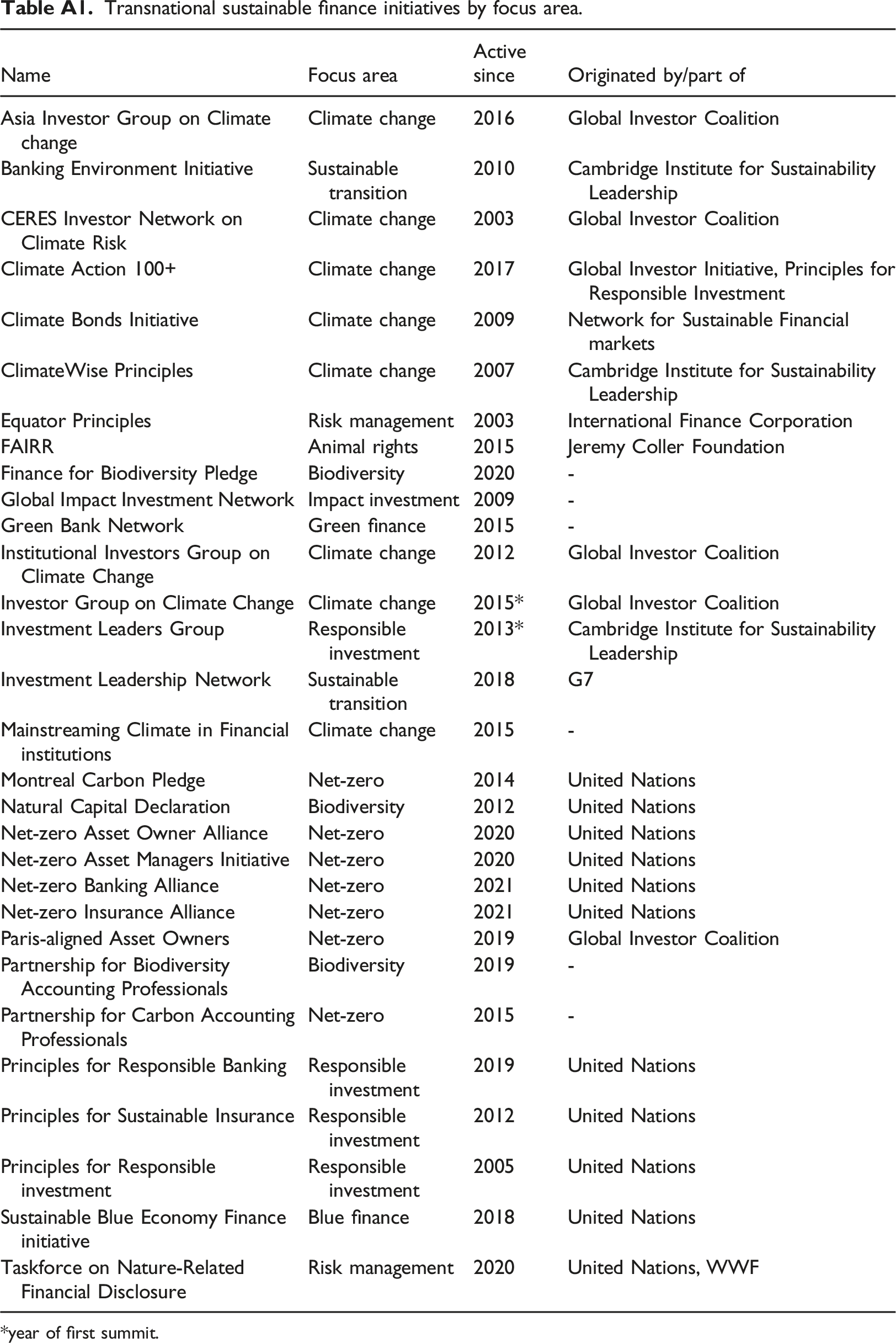

Studies of the transnational governance of sustainable finance have yet to take into account the interconnections between TSFI. Some scholars have mapped the global infrastructure of transnational financial associations and other initiatives (Kawabata, 2023; McDonnell et al., 2022; McKeen-Edwards and Porter, 2013), while others have produced single and comparative case studies on how TSFI operate (e.g. Thistlethwaite, 2012). Another strand of scholarship investigates the drivers behind investors’ uptake of sustainable finance, including their memberships of TSFI (e.g. Hoepner et al., 2021; Sievänen et al., 2013). However, to our knowledge, no study has yet applied a network perspective that examines the overlap between memberships in transnational governance initiatives as an important piece of the sustainable finance puzzle (for a network perspective on the transnational governance of sustainable finance, see Thistlethwaite and Paterson, 2016). To this end, we collected membership data for 30 TSFI, totalling 10.602 observations. We matched these observations with Standard and Poor’s Capital IQ database to retrieve information about members’ locations, ultimate parent organisations and primary industries. Taken together, this data yields a good image of the TSFI network and the most prominent members within it.

A vast scholarship on the role of networks exists in the field of International Political Economy (e.g. global production networks or value chains, transnational expert communities, offshore finance). In this paper, we take inspiration from a subset of this scholarship, namely, studies focusing on global corporate networks. Such studies have shown, for instance, how interlocking directorates have served as important coordination mechanisms within and across industries (e.g. Heemskerk, 2013; Lütz, 2005; Mizruchi, 1996). Other scholarship has interrogated the sources of power of the transnational business elite (Tsingou, 2015; Van Apeldoorn, 2000). More recently, IPE scholars have taken advantage of improved data availability to map the global ownership structures of multinational corporations (for an overview, see Babic et al., 2022). An important finding is the concentration of corporate ownership in the hands of a few large shareholders, such as the ‘Big Three’ asset management firms (Braun, 2022; Fichtner et al., 2017). Their central position within global corporate networks has rendered these investors particularly powerful, giving them great – often untapped – potential to help diffuse responsible business practices among their investee firms (Baines and Hager, 2023).

The goal of our paper is to identify which investors are best positioned within the global network of TSFI to potentially act as agents of diffusion. Taking the co-occurrence of TSFI memberships as our unit of analysis, our underlying assumption is that investors need to be well-connected – or ‘interlocked’ – within the network in order to act as channels of influence, whether upstream (influencing the development of sustainable finance norms within TSFI) or downstream (diffusing sustainable finance norms from global TSFI to local contexts). Analysing membership data, we map the network of co-occurring memberships of 30 TSFI and analyse the constellation of national and transnational organisations among their memberships. We focus on those sustainable finance initiatives that are (1) transnational in membership; (2) have private financial organisations among their members, both for-profit and non-profit; and (3) whose explicit purpose is to make the financial system more sustainable, that is, reoriented towards long-term environmental and social goals. Using this broad definition allows us to include TSFI focused on different aspects of sustainable finance, including but not limited to responsible investment, net-zero investment and biodiversity investment.

We use three descriptive categories to classify investors with overlapping memberships. First, we use the term membership collectors for investors with nine or more TSFI memberships. Membership collectors occupy a central position within the global network, connecting different TSFI and by extension the investors affiliated with them. Second, we identify investors that hold overlapping memberships in centrally located TSFI and those located at the margins of the network. We call these investors mediators, because they are positioned to upload or download norms and practices to and from the centre of the network. 1 We then more closely examine those investors combining a position of membership collector with more than one fringe membership and we ask whether these investors can be considered sustainability performers. Here, our focus shifts from mere description of investors’ position within the overall TSFI network, covered by the collector and mediator categories, towards a more substantive understanding of the role these investors play. If these are the investors that are arguably best positioned to exert influence within the global landscape of TSFI, we ask, do they indeed take on leadership positions within the overall network and does this mean that they are sustainable finance frontrunners?

Our analysis of overlapping memberships shows that especially large investor firms actively engage with multiple TSFI at once and are therefore in the best position to shape the soft law of sustainable finance, controlling the flow of information and standards to and from the centre of the TSFI network. We identify a group of 21 investors, that hold memberships in nine or more TSFI. With the majority of these investors active in asset management, many of the membership collectors are publicly owned or non-profit enterprises. A closer look reveals that only a third of the membership collectors mediates the centres of the network with more than one of the fringe TSFI. Geographically, the membership collectors and mediators are concentrated in Nordic and continental European political economies with more interventionist states in the area of sustainable finance. This suggests that the private governance of sustainable finance is not completely detached from public authority.

Nevertheless, our findings also raise concerns regarding the limitations of TSFI to act as channels of norm diffusion. First, our own interrogation of well-connected investors’ performance suggests that the transnational governance of sustainable finance relies in part on the activities of actors that are simultaneously associated with harmful business practices, such as the financing of harmful industries and voting against pro-climate shareholder resolutions. Here, our findings echo existing scholarship critical of sustainable finance, addressing issues of greenwashing and window-dressing. This literature suggests that investors often engage with sustainable finance mostly from a concern for their own bottom line, limiting notions of sustainability to sustainability-related business risks (e.g. Fichtner et al., 2023). They oftentimes seek to reap reputational benefits from green branding, without adopting the concomitant practices that serve the purpose of mitigation and adaptation (e.g. Migliorelli, 2021). For this reason, our findings secondly question the importance of investors as private governance actors in the transnational governance of sustainable finance. While international organisations like the United Nations are eager to incorporate investors in transnational governance fora, our findings imply that legislation and other binding interventions by national governments might be more effective in steering financial flows towards climate goals.

The outline of this paper is as follows. The next section reviews existing literature on the transnational governance of sustainable finance, observing the relative lack of network analyses in this field of research. Drawing an analogy with scholarship on transnational corporate networks, we propose our own approach, studying the membership ‘interlocks’ held by investors in the global network of TSFI. Similar to interlocking directorates, we argue, such interlocks hold important coordinative potential and constitute a potential avenue for the diffusion of sustainable finance norms. After outlining our research design in the third section, the fourth section shows empirically which investors occupy such interlocking positions, identifying those investors holding a large number of TSFI memberships (collectors) and connecting centrally located TSFI with those at the margins (mediators). A preliminary exploration of these investors’ sustainability performance highlights their ambiguous nature: while these investors occupy leadership positions in TSFI, their business practices are simultaneously associated with environmental and social harms. The descriptive approach taken in this paper does not allow us to make observations regarding the actual diffusion of sustainability norms through TSFI. Our paper therefore concludes with an identification of areas for further research on the transnational governance of sustainable finance.

Transnational sustainable finance initiatives as corporate networks

Given the global scale of contemporary financial markets, the governance of sustainable finance requires a transnational approach. Extending beyond the regulatory reach of nation-states, global finance has increasingly become subject to transnational voluntary regulation – those ‘standards, practices, principles, and codes of conduct that are not created or enforced by states’ (Brouder, 2009: 9) – including in the area of sustainable finance. We use the term Transnational Sustainable Finance Initiative (TSFI) to describe those transnational private regulatory initiatives that aim to make the financial sector more geared towards long-term environmental and social well-being. Transnational initiatives such as TSFI may have different functions, ranging from regulatory bodies (e.g. Glasgow Financial Alliance for Net-Zero) to technical bodies (e.g. Partnership for Biodiversity Accounting Professionals) and advocacy groups (e.g. Climate Action 100+). In so doing, they may serve a range of purposes, including the signalling of sustainability goals, the setting of rules for participating organisations, fostering transparency and accountability around alignment with rules, supplying the means of implementation of practices that enable the achievement of pre-defined goals, and the fostering of knowledge sharing and learning processes (McDonnell et al., 2022).

Although TSFI can be active in different areas of sustainable finance (e.g. climate finance, responsible investment), they are each involved in the development of voluntary regulation for their affiliated members (Brouder, 2009). By setting voluntary rules and technical standards, TSFI have the potential to construct shared meanings and develop global investment norms (Hussain and Ventresca, 2010; Kawabata, 2023; MacLeod and Park, 2011). As such, TSFI may reduce perceived obstacles to sustainable finance, such as confusion over what sustainable investment actually entails (Gangi et al., 2022; Migliorelli, 2021) or uncertainty of the compatibility of sustainable investment with investors’ fiduciary duties (Sandberg, 2011). When too much heterogeneity in global TSFI networks persists, however, they may also contribute to categorical fuzziness, fostering confusion about what sustainable finance means in practice (Nath, 2021).

Existing scholarship has shown that market actors may have various motivations for joining transnational governance initiatives. From one perspective, TSFI may have a positive effect on the diffusion of sustainable finance, either by raising opportunity costs of sustaining non-compliant practices or by lowering the cost of compliance with sustainability norms (Berliner and Prakash, 2015). Voluntary commitment to transnational norms and standards, moreover, may be a way for financial actors to influence domestic regulation: by supplementing it, by pre-empting it or by providing a template for it (Bartley, 2014; Newman and Posner, 2016). In reverse, scholars have pointed out that reasons for joining transnational governance initiatives may be focused less on learning, and more on reaping reputational benefits associated with membership (Berliner and Prakash, 2015). Whether and how initiatives will have a positive impact on the social and environmental impact of economic activities will therefore depend on various factors, such as the extent to which norm compliance is monitored (ibid.), the position of participating financial actors in global value chains and the structure of these chains (Mayer and Gereffi, 2010).

Scholars have observed considerable cross-country variation in financial actors’ commitment to sustainable finance, which they attribute to differences in national institutional and cultural settings. Studying PRI membership among the top-1000 asset owners, Hoepner et al. (2021) find an increased likelihood of membership for asset owners from countries with more strongly entrenched sustainability values. Scholtens and Sievänen’s (2013) comparative study of SRI differences among the Nordic countries also reveals the importance of cultural values, in particular uncertainty avoidance and femininity. Other institutional variables positively related with sustainable investment include the size of the financial industry (Scholtens and Sievänen, 2013), the size of the pension sector and a country’s legal tradition (Sievänen et al., 2013). Together, these studies associate sustainable finance with the institutional settings of Anglo-American and Scandinavian countries rather than those of continental European countries.

Scholars have reached different conclusions on the role of the state in facilitating or inhibiting sustainable finance. Hoepner et al. (2021) find a negative correlation between PRI membership and mandatory regulation of sustainable investment. The authors suspect that reporting requirements stemming from mandatory regulation may prevent asset owners from attributing additional resources to voluntary initiatives like the PRI with their own extensive reporting requirements. Other studies, however, have shown that mandatory legislation has a positive effect on sustainable finance, for instance, by encouraging divestment from fossil fuel companies (Crifo et al., 2019; Méssonier and Nguyen, 2021). Meanwhile, the state also seems to have an indirect effect on financial actors’ commitment to sustainable finance. Studies of pension funds, for instance, have found that public pension funds in particular are more likely to adopt sustainable investment and to become members of TSFI (e.g. Egli et al., 2022; Hoepner et al., 2021; Sievänen et al., 2013). These studies echo the findings of research on sustainable finance by public financial institutions, such as public development banks (Mertens and Thiemann, 2023) and central banks (Deyris, 2023; Siderius, 2022; Thiemann et al., 2023).

In this paper, we employ a network approach to the transnational governance of sustainable finance. Many studies either focus on a single TSFI (Hoepner et al., 2021; Majoch et al., 2017) or a single type of financial organisation, most often pension funds (Sievänen et al., 2013). The studies also have distinct regional foci, commonly focusing on Europe or a subset of European countries. The current paper, by contrast, takes a more encompassing view of the transnational governance of sustainable finance by (1) collecting data from multiple TSFI; on memberships held by (2) all types of financial organisations; (3) from around the world. This approach allows us to not treat memberships as discrete events, but rather place them in the context of other memberships. We thereby take the co-occurrence of memberships as our unit of analysis. In other words: rather than focusing on memberships as individual data points, our approach considers overlaps in memberships as particularly meaningful, because they tell us something about how large investors are embedded in the global TSFI network.

Our interest in co-occurring memberships is informed by political economy scholarship on corporate networks. There is a long scholarly tradition showing how interlocking corporate directorates function as a coordination mechanism among otherwise independent industrial corporations (Davis and Greve, 1997; Heemskerk, 2013; Mizruchi, 1996). In addition, scholars have studied how corporate actors wield influence through their memberships of transnational clubs and other business organisations (Tsingou, 2015; Van Apeldoorn, 2000). Finally, scholars have focused on multinational corporations’ coordinative powers within their global supply chains (e.g. Locke, 2013; May, 2015) as well as global value and wealth chains (e.g. Gereffi et al., 2005; Seabrooke and Wigan, 2017). Taken together, this scholarship indicates that the embeddedness of multinational corporations in global networks provides the foundation for large corporations’ to serve as agents of global governance (Bartley, 2018).

Yet, the same research on corporate networks also gives reasons for caution. Studies show how corporate ownership is concentrated among a very small number of very large asset owners (e.g. Fichtner et al., 2017). In theory, these asset owners are particularly well-positioned to use their ownership rights to press investee corporations to improve their sustainability track records. Nevertheless, despite outwards commitments to sustainable investment, the world’s largest asset managers are more often found to support the management of environmentally harmful corporations than to question these business practices (Baines and Hager, 2022; Braun, 2022). As Oatley et al. (2013) warn, the network structure of global finance is not necessarily benign: while it can facilitate diffusion of investment norms related to sustainability, it can also create ‘global contagion’ and create financial crisis. For this reason, investors’ centrality within global sustainable finance networks should not be taken as a proxy for their actual sustainability performance.

Methods

To perform a descriptive analysis of the global TSFI network, we collected membership data for 30 TSFI (see Appendix). Our sampling frame was based on three criteria. To be included in the sample, TSFI needed to be (1) transnational in scope. This means we excluded national sustainable finance initiatives. Selected TSFI also have (2) private financial institutions, either for-profit or non-profit, that can join as members. This means that we excluded initiatives like the Network for Greening the Financial System, whose members are public institutions. We also excluded initiatives like the Glasgow Financial Alliance for Net-Zero, which acts as an overarching framework for individual TSFI. Finally, we included TSFI (3) whose explicit purpose is to make the financial system more sustainable, that is, reoriented towards long-term environmental and social goals. Here, our approach differs from Migliorelli’s (2021) ‘finance for sustainability’ (authors’ emphasis), as we excluded initiatives exclusively aimed at financing sustainable activities within financial and non-financial organisations.

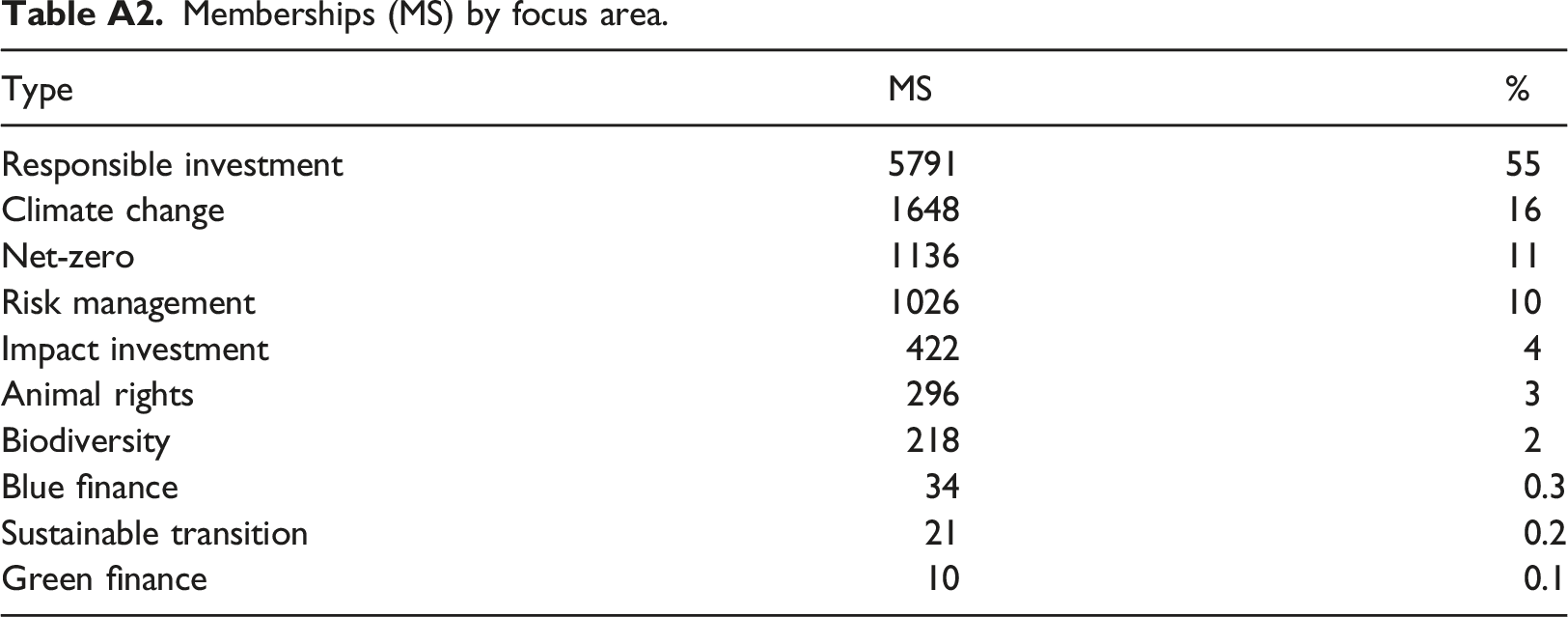

Our sampling frame generates a diverse sample of TSFI with varying governance functions and organisational forms. Nevertheless, as our analysis is meant as a starting point to study the diffusion of sustainable finance norms, we categorised the selected TSFI by their thematic foci and not by governance function or organisational form. This way we can compare membership of different thematic foci, which may tell us something about the way that different types of investors engage with TSFI more generally: do investors engage with the full range of sustainability-related themes? Or do they maintain a narrow focus on a specific sub-theme? For this categorisation, we used an inductive approach, whereby we scanned the TSFI’s mission statements available on their websites for specific codewords related to well-known principles of sustainable finance. This approach generated eight thematic foci. Each of these foci represents a subfield of the broader sustainable finance community: from more general themes like responsible investment and the sustainable transition to more specialised topics like climate change, biodiversity and ocean conservation (blue finance).

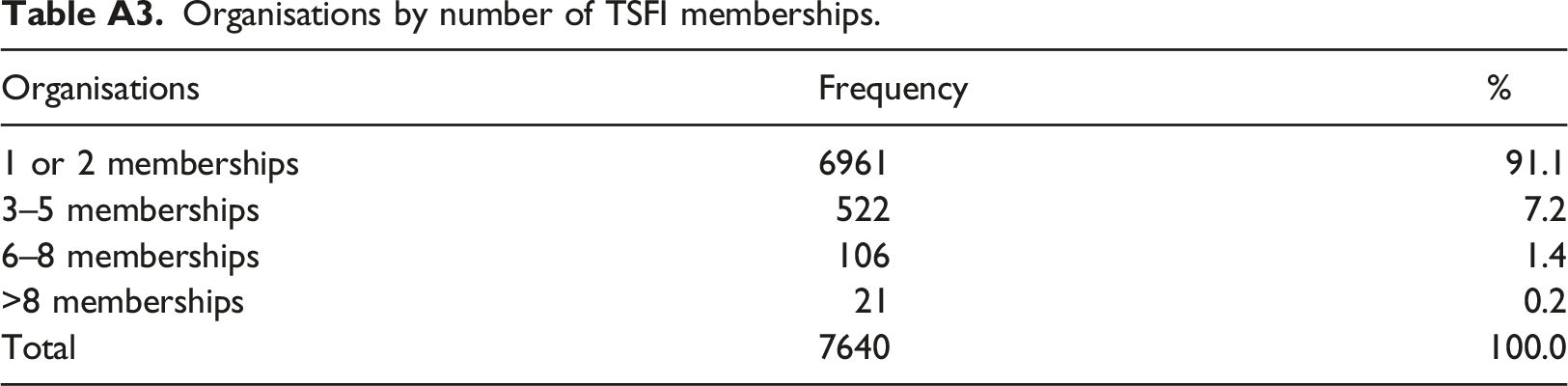

Where available, we derived membership data for 2022 from the initiatives’ websites. For some organisations, membership information was not publicly available (e.g. Climate Action 100+). In those cases, we contacted the organisation and were able to retrieve the information via correspondence. In total, we collected data on 10.602 memberships. We then tried to identify each investor in Standard & Poor’s Capital IQ (CIQ) database, yielding a unique ID. This ID allowed us to match organisations that appeared under slightly different names in the raw data. We also retrieved information about the location of headquarters, the ultimate parent company of the investor firm, and the location of the ultimate parent. When available, we cross-checked companies’ HQ locations as listed in the CIQ database with the location as listed on the website of the initiative. These did not always correspond. In case of doubt, we opted for the location as listed in the CIQ database, which allowed us to treat all initiatives the same way. We identified 7.639 corporate entities and 6931 ultimate parents, accounting for 10.602 membership relations. For 974 entities (accounting for 1.010 memberships), we failed to identify a corresponding entity in the CIQ database.

Using this data, we constructed an image of the global TSFI network based on the overlapping memberships of individual investors. This image allowed us to identify the investors that take up prominent positions in the global TSFI network. To identify these actors, we distinguish between three aspects of investors’ TSFI memberships. Collectors are investors with the highest number of overall memberships in the network. A small minority of investors thus covers a relatively large proportion of the TSFI network and therefore potentially serves as a conduit for knowledge, information and norm setting in the network as a whole. We consider investors membership collectors, when they hold nine or more TSFI memberships. Mediators are investors that link relatively sparsely connected TSFI to the more central TSFI. Mediators have the potential to either mainstream peripheral norms, or inhibit institutional change by frustrating the development of peripheral norms and practices and their diffusion. To establish which initiatives are located at the network fringes, we consider (1) those TSFI with 100 members or less, whose (2) members hold fewer than four memberships on average. 2

We then identify investors that combine a high number of memberships (>8) with multiple mediator positions (>1). We use the term ‘performer’ to describe the leadership role these investors might potentially take, although we subject this question to further empirical scrutiny below. The term ‘performance’ has an ambiguous meaning, as sustainability performance of financial corporations is often measured by metrics that do not necessarily tell us something about whether finance practices are actually aligned with the requirements of a sustainable economy. The fuzzy meaning of sustainable finance, moreover, means that corporations may be scored differently depending on which set of metrics is used (Gangi et al., 2022). Investors may perform well on sustainability performance lists, but still act in ways that are hard to reconcile with international climate and biodiversity agreements. We therefore end our analysis with a reflection on the performance of the most prominent actors in the TSFI network, combining evidence on sustainability performance from global rankings with documentary evidence on investment projects, drawn from the investors’ websites and various media outlets.

The global TSFI landscape: Collectors, mediators and performers

In contrast to their organisational diversity, many TSFI share similar origins. The United Nations Environment Programme Finance Initiative (UNEP FI) in particular has been instrumental in the creation of new TSFI over the past 20 years. UNEP FI was founded in 1992 with the explicit aim of mobilising financial organisations for environmental protection. Since then, UNEP FI has initiated several TSFI around principles for responsible finance (Principles for Responsible Banking, Principles for Sustainable Insurance, Principles for Responsible Investment) and net-zero investment (Net-Zero Asset Owner Alliance, Net-Zero Banking Alliance, Net-Zero Insurance Alliance). In turn, these TSFI have also been involved in the creation of new TSFI: PRI, for instance, is one of the founding organisations of Climate Action 100+ and oversees the Montreal Carbon Pledge. Additionally, a substantial number of TSFIs emerged from the periodic United Nations Climate Change conferences (e.g. Natural Capital Declaration). The COP21 climate conference in Paris, for instance, kickstarted several new TSFIs (e.g. Climate Action 100+; Green Bank Network; Mainstreaming Climate in Financial Institutions), while COP26 launched the various net-zero initiatives under the Glasgow Financial Alliance for Net-Zero (GFANZ).

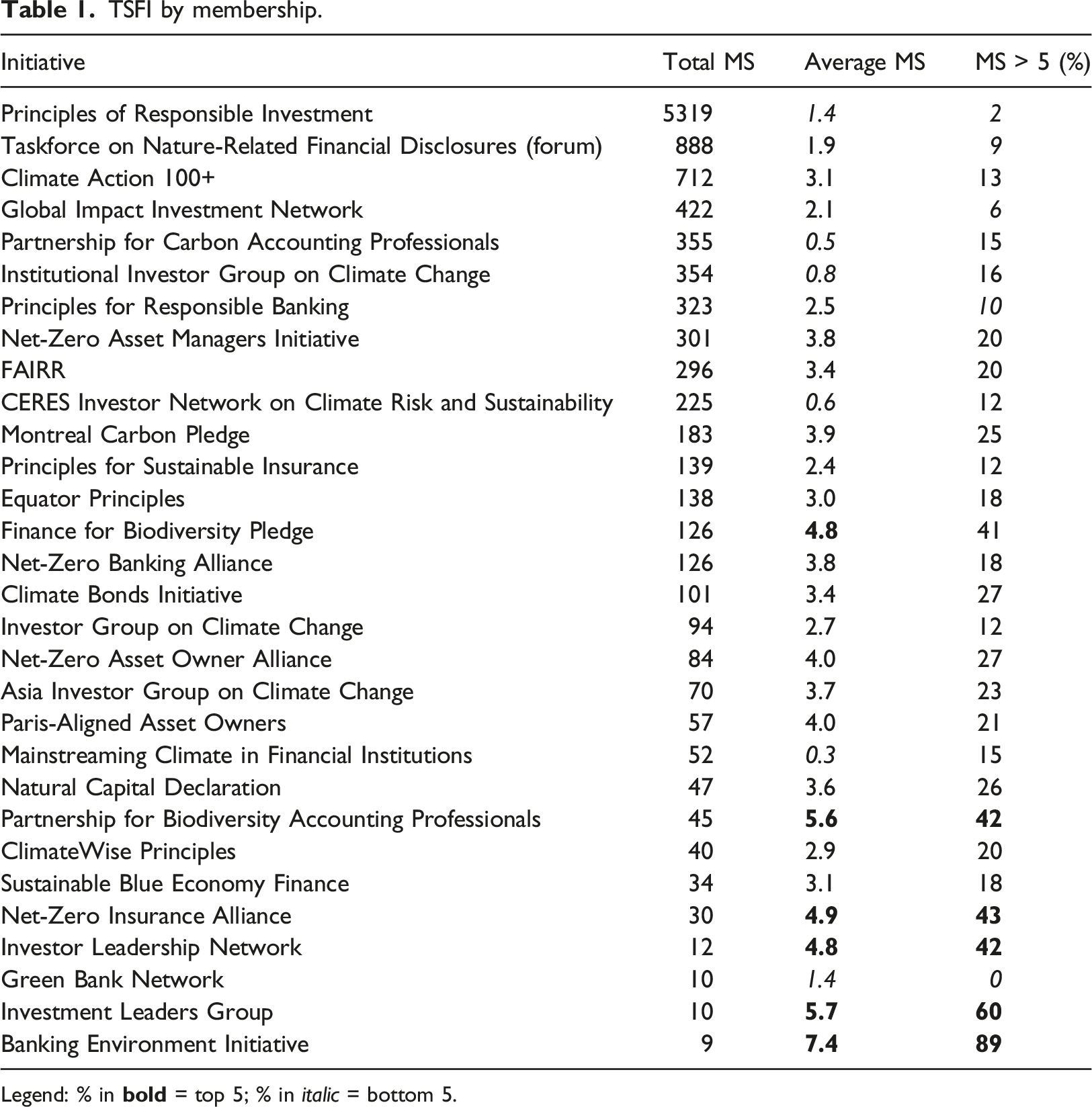

TSFI by membership.

Legend: % in

Nevertheless, while the smaller TSFI hold fewer members in total, their members do more often hold a large number of memberships than those of the largest TSFI: as Table 1 shows, only 2% of the PRI’s members are members of more than five TSFI, while 60% of the Investment Leaders Group are members with more than five TSFI memberships. In other words, whilst the largest TSFI have a broader membership base, the smaller initiatives tend to count more ‘membership accumulators’ among their members. The Banking Environment Initiative stands out in this regard: of its nine members, eight have more than five memberships to TSFI. A possible explanation could be that these membership accumulators are companies that specialise more in sustainable finance, including niche themes.

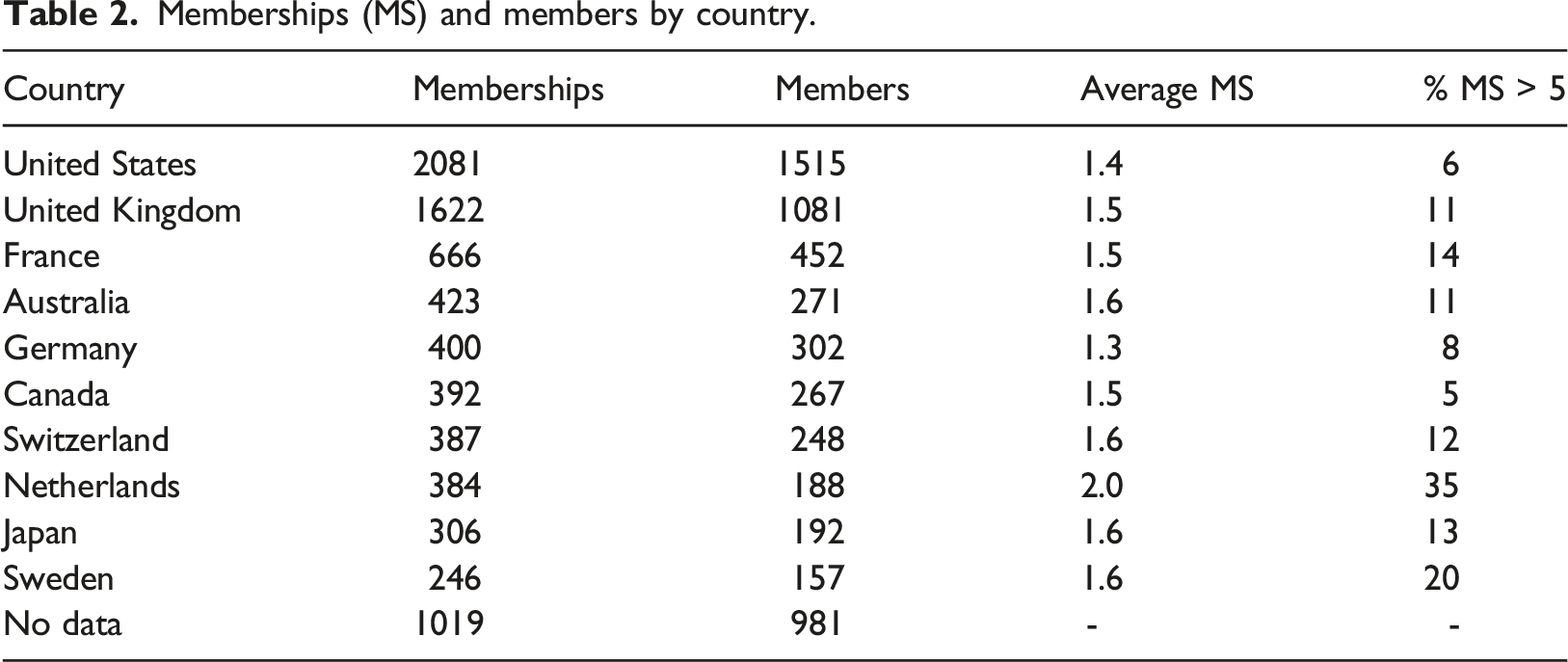

Memberships (MS) and members by country.

Our findings raise a number of questions. For instance, why do some countries produce relatively more TSFI members than others? And why do members from some countries have a relatively high average of memberships relative to members from other countries? While a vast scholarship in comparative political economy indicates the importance of national institutional settings on politico-economic outcomes, observed differences in the average number of transnational memberships seem to fall outside conventional classifications (e.g. Hall and Soskice’s (2001) liberal market economies and coordinated market economies). It may, for instance, be that meaningful differences between national financial sectors are obscured by their different compositions. In other words: it may be that the types of investors that are more likely to have multiple memberships are more often present in some national political economies than in others. To further explore this possible connection, we refocus our analysis to the level of individual members. This enables us to scrutinise the position of the most prominent investors in the overall TSFI network. To probe the importance of overlapping TSFI memberships, we consider three different dimensions of TSFI members: how many memberships they collect, whether they are members of one or more fringe TSFI, and what they actually do in the area of sustainable finance (i.e. their performance). We discuss each of the dimensions in turn.

Collectors

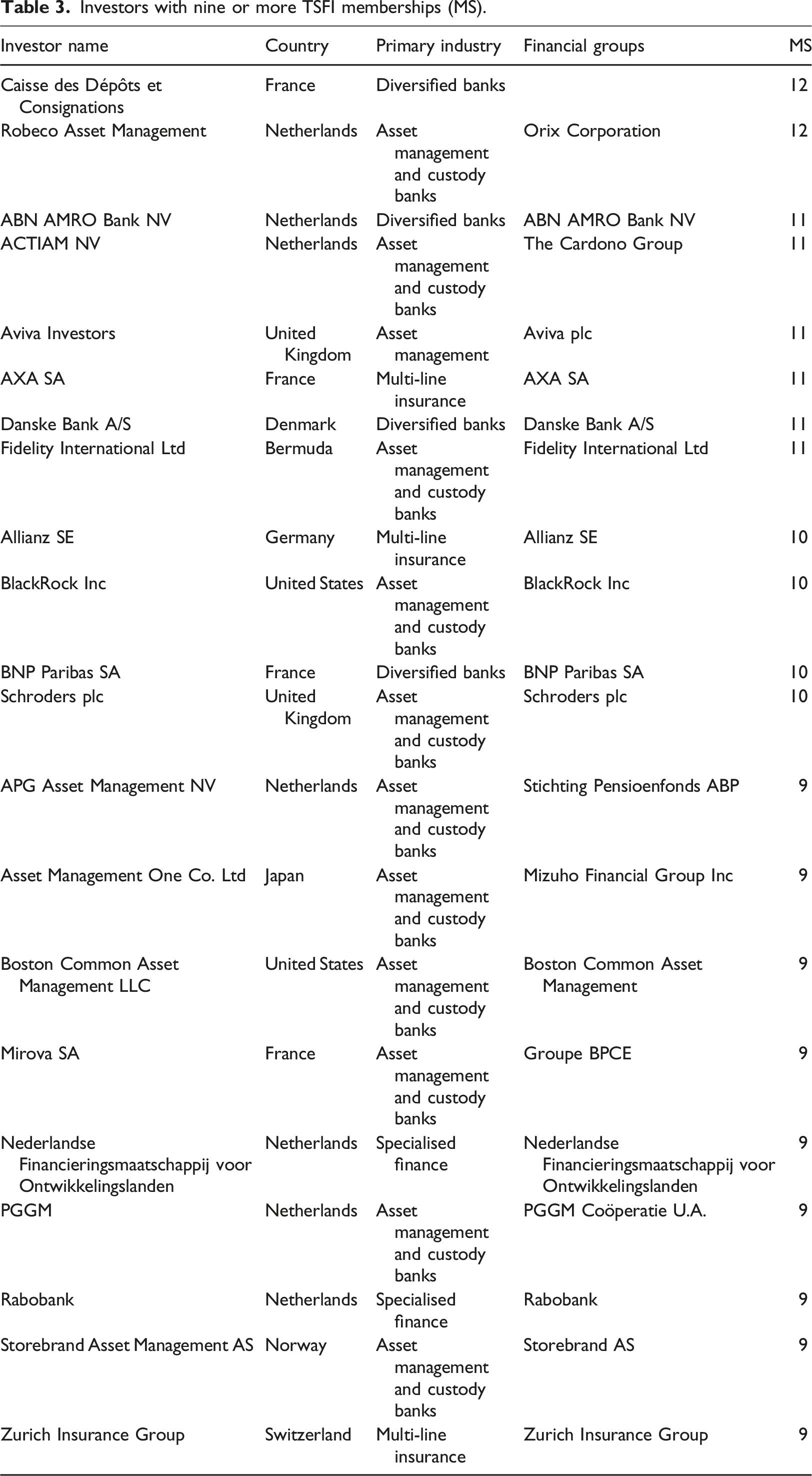

Investors with nine or more TSFI memberships (MS).

The finding for the Netherlands again stands out. Even though the Netherlands has a large pension sector, which scholars have argued is a driving force behind sustainable investment, we do not find pension funds among the Dutch membership collectors. Instead, most Dutch membership collectors are active in the asset management sector, while ABN AMRO is a bank. Nevertheless, two of the Dutch asset managers – PGGM and APG – are affiliated with two large pension funds – health care sector fund PFZW and public sector fund ABP, respectively – and provide asset management services to the Dutch pension sector. ACTIAM, meanwhile, explicitly positions itself as a sustainable asset manager, which it has in common with other membership collectors Aviva (United Kingdom), Mirova (France) and Storebrand (Norway).

We complement our analysis of overlapping memberships by individual investors with those held by their parent company groups. Many members are entities that operate as part of a larger group, which may point to meaningful connections. For instance: if an organisation is a member of both the Net-Zero Banking Alliance and the Net-Zero Insurance Alliance, a shared economic interest may exist and serve as a conduit for norms and knowledge between initiatives. Some investor firms are more closely embedded within groups than others, for instance, corporate entities that share brand names. Unfortunately, our data do not allow us to measure group integration. We identify groups simply as those corporate entities that share the same ultimate parent: the ‘highest’ corporate entity owning majority stakes in lower placed corporate entities, itself not majority-owned by another corporate entity. To what extent groups operate as loosely connected assemblies of investor firms or whether they operate as integrated corporate entities remains a question for further research

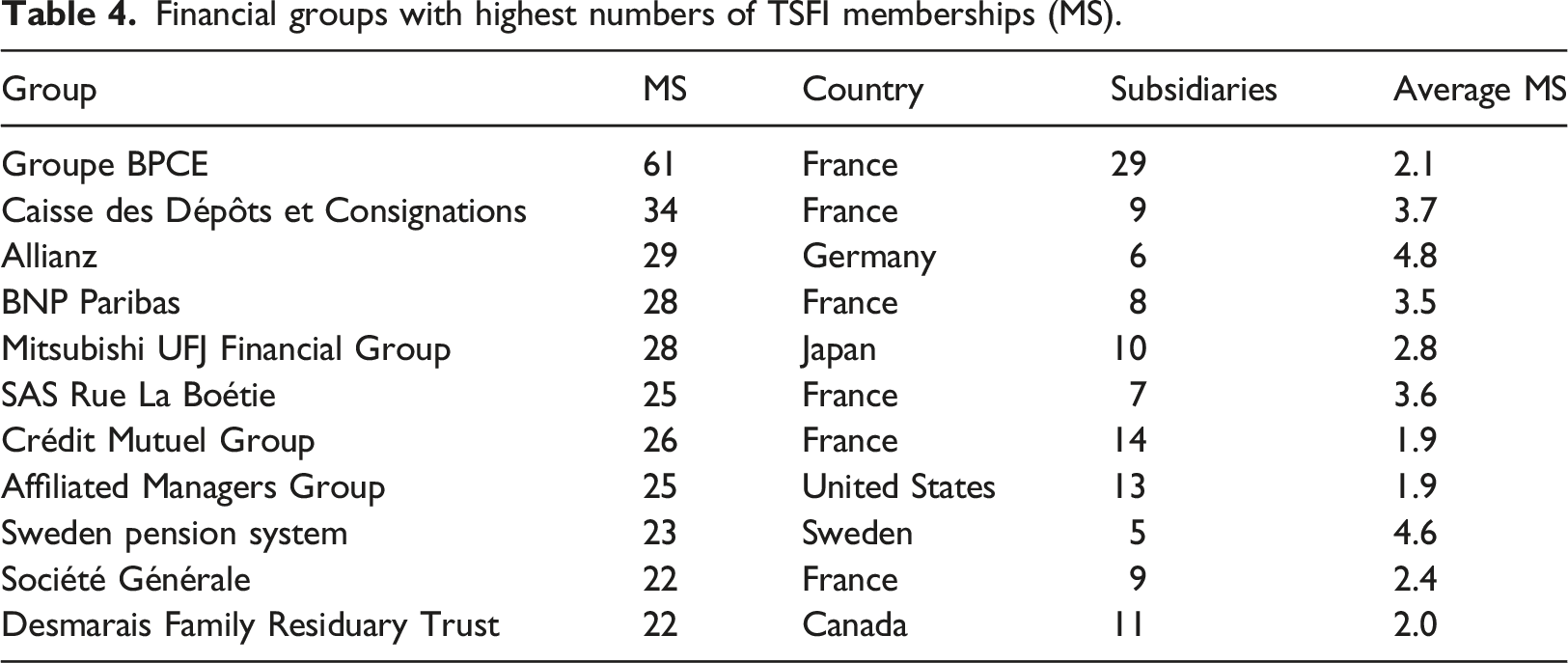

Financial groups with highest numbers of TSFI memberships (MS).

The distribution of TSFI memberships by parent groups differs considerably from those by individual members. Particularly striking about these results is the predominance of French cooperative and public banks among the top-10 of most connected TSFI. Groupe BPCE has by far the largest number of TSFI memberships. A cooperative banking group, it is parent company to Mirova, a B corporation specialising in sustainable investment, although its large number of TSFI memberships cannot be solely attributed to this affiliation. Even though we identified Mirova as one of the membership collectors, Groupe BPCE’s memberships far exceed those held by Mirova (N = 9). Other top-10 parent companies include Crédit Mutuel, a cooperative banking group, and SAS Rue la Boétie, the parent company to the Crédit Agricole cooperatives. Also noteworthy is the presence of the Caisse des Dépôts et Consignations, a state-owned financial institution with ownership stakes in – among others – public investment bank Bpifrance and the French postal services.

The predominance of French financial groups aligns with Hoepner et al. (2021)’s findings on the presence of a pro-sustainability culture as an explanation for TSFI membership. For instance, Arjaliès (2010) has shown how the Socially Responsible Investment movement – in many ways, the predecessor to sustainable finance – is strongly entrenched in the French financial sector. Nevertheless, our findings seemingly contradict Hoepner et al.’s (2021) assertion that TSFI membership substitutes for mandatory legislation. In recent years, the French state has been particularly ambitious in issuing new rules and regulations on sustainable finance. The 2021 Law on Climate and Energy, for instance, mandates financial institutions to disclose their investments’ impact on biodiversity and climate change. Our distinct focus on membership overlaps instead suggests a complementarity between mandatory legislation and TSFI memberships. TSFI members may favour mandatory legislation, because it might level the playing field between members and non-members. For the same reason, organisations facing mandatory legislation may prefer TSFI membership as a way to harmonise rules across jurisdictions. This particular hypothesis will need to be further studied in future research.

Mediators

Of the 14 TSFI with fewer than 100 members, seven qualify as fringe initiatives, whose members have an average membership below three. 3 A focus on the fringe initiatives is important, because the location of certain TSFI (and not others) at the margins may reveal pathways for inclusion present in the overall global network. For instance, the inclusion of two regional TSFI among the fringe organisations – Asia Investor Group on Climate Change and the Investor Group on Climate Change – likely indicates the presence of a geographical periphery within the global network, as its centre is dominated by investors from North America and Europe. The existence of such a periphery is problematic, because it could well mean that the local interests of geographically bounded initiatives and their members may be less well represented in the activities of TSFI more generally. Moreover, the fringe status of both the Natural Capital Declaration and the Sustainable Blue Economy Finance Initiative, both TSFI dedicated to specific investment principles, suggests that investment ideas related to natural capital and ocean conservation, respectively, are less entrenched in the global financial governance than other principles. Again, this may be problematic, because it may mean that the interest in natural capital or ocean conservation may be less important than other themes in decision-making around projects worth investing in.

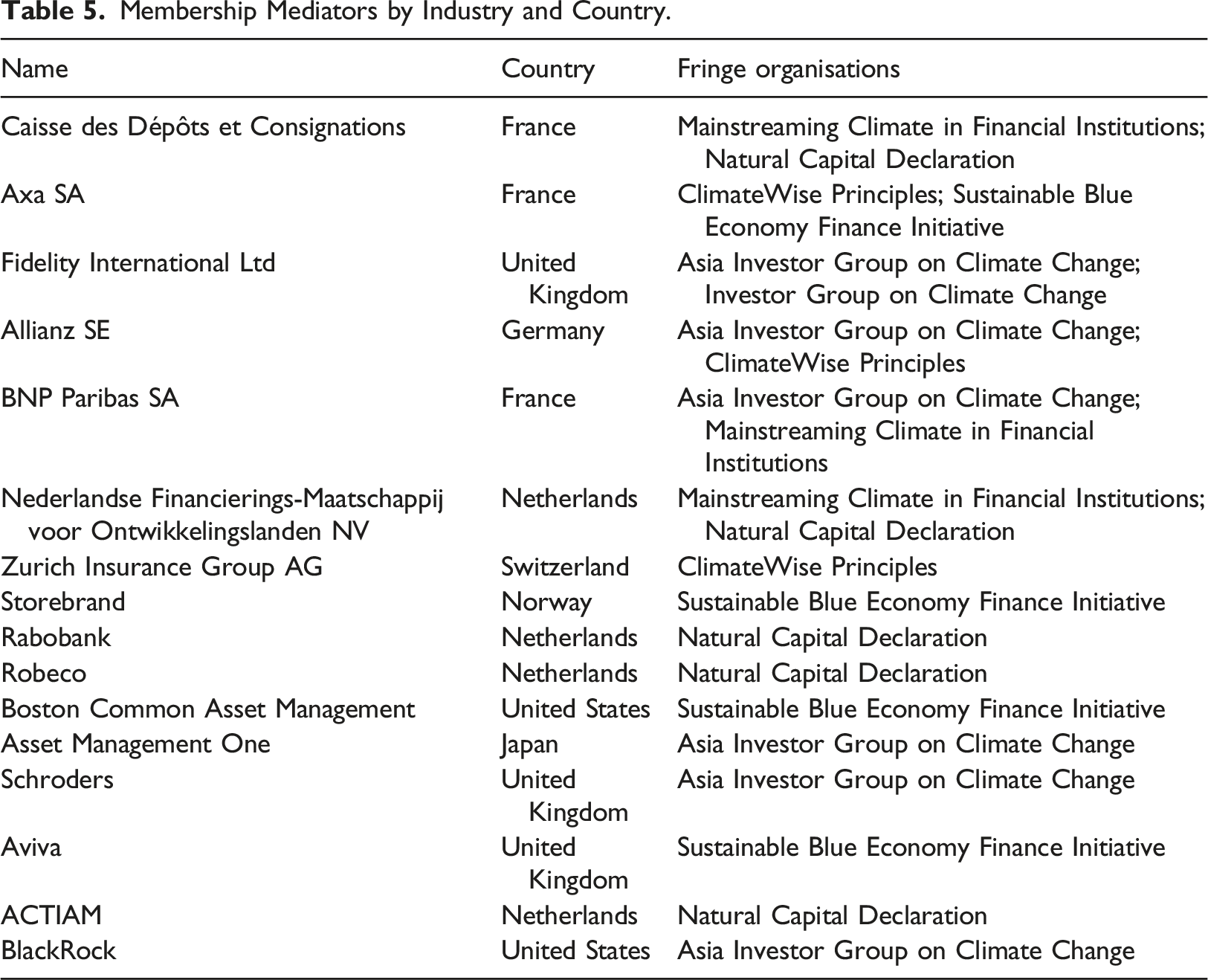

Membership Mediators by Industry and Country.

Considering the characteristics of the membership mediators, we find that they resemble the broader group of membership collectors in several respects. First, the membership mediators are a diverse group of both private commercial enterprises on the one hand and cooperative and state-owned enterprises on the other hand. Moreover, a considerable number of members offers asset management services: not only asset management firms like Schroders or Actiam, but also large financial conglomerates like Axa and BNP Paribas. We also note the geographical concentration of the membership mediators in France, the Netherlands and the United Kingdom (three mediators each). Finally, it is interesting to note which of the membership collectors are absent from our group of mediators: asset managers PGGM (Netherlands) and Mirova (France) share several characteristics with the mediators, yet do not hold memberships in any of the fringe TSFI.

Performers?

Are well-connected members of TSFI also top-performers of sustainable finance? While an in-depth analysis of the sustainability performance of investor firms with different degrees of connectivity within the overall TSFI network falls outside the scope of this paper, we present a number of observations for a subset of TSFI members: namely, those who combine a membership collector position with that of a network mediator. These are Allianz, Axa, BNP Paribas, Caisse des Dépôts et Consignations, Fidelity International and Nederlandse Financierings-Maatschappij voor Ontwikkelingslanden (FMO). Four of the six performers are large, commercial corporations that count among the largest in global finance, while the remaining two (CDC, FMO) are (majority) publicly owned and serve as de-risking vehicles for investments in sustainable development projects. Arguably, these are the investors that are best positioned to act as conduits of sustainable investment principles within the overall TSFI network. That said, do these investors also live up to their potential?

Each of the six selected investors have taken up leadership positions within the global network on sustainable finance. Insurer Allianz, for instance, is a founding member of the Net-Zero Insurance Alliance, while Axa chairs the alliance. Likewise, Allianz and Caisse des Dépôts are founding members of the Net-Zero Asset Owners Alliance. Allianz board member Günther Thallinger chairs the alliance. As prominent members of TSFI, the mediators have also been involved in developing voluntary rules and standards (IIGCC, 2020; PRI, 2022) and played active roles in public policy domains. Allianz and BNP Paribas, for instance, were represented on national sustainable finance policy committees (e.g. Germany, Singapore), while Axa, Allianz and BNP Paribas have held seats on the EU Sustainable Finance Platform and the EU’s High Level Expert Group on Sustainable Finance.

The four private corporations are also sustainable finance frontrunners through their business activities. Axa and Allianz were among the first large firms in the insurance industry to halt the sale of insurance coverage to heavy polluters in the coal industry (Ralph, 2018). BNP Paribas has stopped financing coal mining and tar sand oil producers. In 2022 and 2023, Euromoney named BNP Paribas ‘the world’s best bank for sustainable finance’. The bank also ranked #3 in the 2022 Sustainable Banking Revenues ranking thanks to its ownership of sustainable finance assets (in absolute terms; in relative terms, the bank took a more modest position at #16). Of the four financial organisations that offer asset management services (Axa, Allianz, BNP Paribas and Fidelity), BNP Paribas received a top A-rating in ShareAction’s responsible investment ranking of global asset managers, while both AXA and Allianz are listed in the top-20; Fidelity International is positioned at place 43 out of 75 (ShareAction, 2022). Finally, several mediators (Axa, Allianz and BNP Paribas) are considered industry frontrunners in disclosing their own carbon footprint (Bryan and Smith, 2023).

Sustainability criteria also apply to the investors’ voting and engagement policies. Since 2016, BNP Paribas follows a Paris-aligned voting policy, withholding approval of shareholder resolutions at corporations that are insufficiently transparent of their carbon footprint. Allianz adheres to a voting policy on executive compensation, whereby it expects remuneration to be linked to ESG performance indicators. Allianz and Fidelity International are also part of a financial sector campaign supporting so-called ‘Say on Climate’ resolutions. As part of the campaign, the corporations have urged the UK government to make climate votes mandatory for public corporations (Mooney, 2021). Finally, ShareAction (2022) has found that all four corporations offering asset management services (Axa, Allianz, BNP Paribas and Fidelity International) vote in favour of climate proposals in a majority of cases (respectively: 64%, 80%, 97% and 74%); the Big Three asset owners, by contrast, do not exceed 30%.

At the same time, the sustainability performance of the commercial enterprises has been scrutinised by NGOs and public commentators. For instance, BNP Paribas was identified by the Rain Forest Alliance as one largest financiers of fossil fuel companies and the largest in Europe, occupying the #9 position in its 2023 ranking. Reclaim Finance, moreover, has placed Allianz and Fidelity International on its ‘Dirty Thirty’ list for investing in coal, oil and gas despite promises to the contrary. A study by ClimateVotes, finally, has questioned the effectiveness of TSFI in shaping members’ sustainability practices. Singling out the voting behaviour of Allianz, AXA and BNP Paribas during Shell’s annual shareholder meeting, the authors find that members of the Net-Zero Asset Owners Alliance do not vote more often in favour of pro-climate shareholder resolutions than non-members (Cojoianu et al., 2020).

Moreover, the transnational initiatives in which these investors have taken leadership positions have faced criticism for weakening sustainability standards. Particularly, the Glasgow Financial Alliance for Net Zero, which the different sectoral net-zero alliances are part of, has been under public scrutiny. The Net-Zero Insurance Alliance has been criticised for not requiring its members to stop selling insurance cover to high polluting coal companies, (erroneously) claiming that such a restriction would break antitrust rules (Beioley and Hodgson, 2023). The Net-Zero Asset Owners Alliance has similarly faced criticism for prioritising engagement with oil and gas companies over divestment, while commentators have questioned the Partnership for Carbon Accounting Professionals’ exclusion of scope three emissions from its framework (Bryan and Smith, 2023; Flood and Mundy, 2022). Criticism has also come from the opposite corner of the financial sector. In 2022, Big Three asset manager Vanguard publicly left the Net-Zero Asset Managers Alliance, stating the investor’s need ‘to speak independently’ on issues of climate change amidst mounting political pressures from anti-ESG politicians in the United States (Masters and Temple-West, 2022).

Meanwhile, the ‘performers’ have also been associated with other kinds of unsustainable business practices. Axa, Allianz and BNP Paribas have all launched major share buybacks in recent years. Share buybacks involve the repurchasing of stocks by the issuing corporation on the open market. While widespread, share buybacks are criticised for artificially hiking up stock prices as well as compensation for corporate executives (Palladino and Lazonick, 2022). In addition, share buybacks are said to hinder innovation, as they are financed by capital that could have otherwise been used for reinvestment in the corporation (ibid.). In addition, corporations like Axa and Allianz faced criticism for their executive compensation practices, despite their own activist stance on executive compensation in investee firms. In the case of Allianz, CEO pay was raised by 24% to reach €7.9 million in 2021, even after the company had to make multi-billion dollar settlements payments following a mis-selling scandal involving the U.S. branch of its asset management division (Storbeck, 2022).

That investors’ public commitment to sustainable finance is not always met by actual sustainable finance business practices is not surprising. As Bracking (2015) notes, sustainable finance may involve some degree of performance. After all, their involvements with TSFI allow investors to reap the reputational benefits as sustainable finance leaders. TSFI membership may also offer a potential avenue for influencing the development of shared norms and standards, thereby reducing the uncertainty associated with sustainability transitions. Viewed in this light, the exposure of business models to sustainability transitions, whether positively or negatively, may be the best predictor of overlapping memberships. Finally, we should consider the potential for TSFI to increase investors’ global power. When centrally located members contribute to reports like the IIGC’s Net-Zero Standard of Oil and Gas, they exert influence not only over the financial sector but over the investee sector as well. Transnational governance of sustainable finance should therefore be seen in context of the broader position of asset owners and asset managers in contemporary financial capitalism.

Discussion and conclusion

In this paper, we set out to analyse the TSFI network, taking overlapping memberships as an indication of how well investors are positioned to shape emerging norms and standards around sustainable finance. To help identify the investors best placed to shape the flow of information within the overall network, we analysed three different dimensions: the overall number of memberships investors collect, whether investors have also become members of the more fringe initiatives, and how well investors perform in the area of sustainable finance. Our analysis indicates that there is a rather small group of large investors taking central positions within the overall TSFI network. These investors (or financial groups) potentially serve as agents of transnational private governance diffusing sustainable finance norms across jurisdictions. To assess whether and how TSFI can be helpful in bringing about the necessary institutional change enabling the global political economy to deal with climate change and related sustainability transitions thus requires paying attention to the position of these large investors within the overall TFSI network.

Based on our analysis, we want to stress three findings that could serve as starting points for future studies on the transnational governance of sustainable finance. First, our finding that by far most investors have only a relatively small number of membership relations to TSFI may obscure that TSFI are mostly a phenomenon of large investors and corporate groups. The large size of the PRI can be attributed for this paradoxical outcome. The PRI is the largest of all TSFI and almost by definition counts many investors amongst its membership base that do not have any other connection to TSFI. This raises important questions about the relation between the PRI and other initiatives, whether they are UN-led or not. For instance: can larger investors leverage their network position to set the agenda for TSFI more generally via the PRI, or is the PRI just a central node in the TSFI network enabling the transmission of norms, knowledge and best practices to and from the network’s niches? More generally, future studies could examine whether there is a functional differentiation between different types of initiatives – a question our analysis hints at, but does not unpack in more detail.

Second, our findings offer indication that the dominance of large investors among TSFI memberships limits the potential of the global network to serve as an infrastructure for the diffusion of sustainable finance. To further understand these limitations, we need network analyses explaining how different network constellations influence the actual diffusion of sustainable finance norms and by extension the sustainability performance of investors and their investee firms. For instance: what does membership collectors’ sparse connections to the network’s periphery imply for the development of non-mainstream investment principles and geographical representation? Our evidence has also shown the very mixed sustainability performance of those investors that are the most connected in the global network, indicating the limitations of these investors as ‘norm entrepreneurs’ for sustainable finance (Finnemore and Sikkink, 1998). Here our findings speak to existing studies of private governance that problematise firms’ motivations for joining transnational initiatives (e.g. Berliner and Prakash, 2015). Large investors may, for instance, stand more to gain (or to lose) in terms of reputation by virtue of TSFI membership. It may also be that their cross-border operations create a vested interest in levelling the playing field across regulatory jurisdictions. Taking our analysis as a starting point, we stress the importance of conducting in-depth case studies into how different investors relate to the norm-setting and practice-defining work performed in and by TSFI.

Third, and relatedly, our findings raise important questions about the interface between policy-making and TSFI. One set of questions pertains to the central role of the United Nations in developing the global network of sustainable finance initiatives. For instance, why and how the United Nations became a driving force behind the transnational governance of sustainable finance, why it has centred its actions around certain investment principles (e.g. net-zero) and not others (e.g. biodiversity), or how it may compete with other IOs (e.g. the World Bank) on setting the global agenda around sustainable finance. Another set of questions pertains to the importance of national financial institutions. Studies of transnational private governance have already shown (e.g. Newman and Posner, 2016) the importance of national regulation in directing the behaviour of large investors towards and within transnational private governance, for instance, when investors consider relatively stringent home country rules a threat to competitiveness. Other factors also appear important: for instance, to what extent investors operate mostly within home-country borders, the level of market concentration in financial services, the weight of different types of asset owners present in the financial system, and whether wealth is concentrated in a relatively small number of sizable asset owners or rather dispersed. An approach applying insights from comparative political economy studies on national varieties of financial systems may be particularly useful in further understanding the transnational governance of sustainable finance.

On a final note, our study points to some important limitations in studying TSFI, which are perhaps symptomatic of transnational governance more generally: namely, that it is very difficult to identify what is the appropriate unit of analysis in studying TSFI. We distinguished between individual investors and financial groups identified as the ultimate parent organisations of individual business entities. As noted, however, it is difficult to say without on-the-ground knowledge of an organisation how closely integrated the different entities within a group are. Reputational benefits and coordination capacities will likely exceed the level of individual business units in a group. At the same time, groups will rarely act in unison, and will rarely benefit from reputational benefits as a whole. TSFI memberships may be the product of group policy and branding, but it may also be the result of institutional entrepreneurship within a group organisation. Whichever of these two is the case, however, will determine whether TSFI will frustrate or benefit sustainability transitions in finance.

Footnotes

Acknowledgements

We thank Milan Babic, Sarah Sharma, three anonymous reviewers and the other contributors to this special issue for their indispensable feedback on an earlier version of this paper. We also thank Karen Anderson, Natalia Besedovsky, Théo Bourgeron, Jan Fichtner, Julius Kob and Tobias Wiß for their comments on and assistance with this paper. Special thanks goes out to Rosella Twisk for research assistance. We gratefully acknowledge the financial support of the Hans-Böckler-Stiftung for the research project. A previous version of this paper was presented at the Annual Meeting of the Society for the Advancement of Socio-Economics in Amsterdam, 9–11 July 2022.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research presented in this article was supported by a research grant provided by the Hans-Böckler-Stiftung (2020-479-4) for the research project “Nachhaltigkeit durch betriebliche Altersversorgung” (Sustainability through Occupational Pensions).

Notes

Appendix

Tables A1, A2 and A3 Transnational sustainable finance initiatives by focus area. year of first summit. Memberships (MS) by focus area. Organisations by number of TSFI memberships.

Name

Focus area

Active since

Originated by/part of

Asia Investor Group on Climate change

Climate change

2016

Global Investor Coalition

Banking Environment Initiative

Sustainable transition

2010

Cambridge Institute for Sustainability Leadership

CERES Investor Network on Climate Risk

Climate change

2003

Global Investor Coalition

Climate Action 100+

Climate change

2017

Global Investor Initiative, Principles for Responsible Investment

Climate Bonds Initiative

Climate change

2009

Network for Sustainable Financial markets

ClimateWise Principles

Climate change

2007

Cambridge Institute for Sustainability Leadership

Equator Principles

Risk management

2003

International Finance Corporation

FAIRR

Animal rights

2015

Jeremy Coller Foundation

Finance for Biodiversity Pledge

Biodiversity

2020

-

Global Impact Investment Network

Impact investment

2009

-

Green Bank Network

Green finance

2015

-

Institutional Investors Group on Climate Change

Climate change

2012

Global Investor Coalition

Investor Group on Climate Change

Climate change

2015*

Global Investor Coalition

Investment Leaders Group

Responsible investment

2013*

Cambridge Institute for Sustainability Leadership

Investment Leadership Network

Sustainable transition

2018

G7

Mainstreaming Climate in Financial institutions

Climate change

2015

-

Montreal Carbon Pledge

Net-zero

2014

United Nations

Natural Capital Declaration

Biodiversity

2012

United Nations

Net-zero Asset Owner Alliance

Net-zero

2020

United Nations

Net-zero Asset Managers Initiative

Net-zero

2020

United Nations

Net-zero Banking Alliance

Net-zero

2021

United Nations

Net-zero Insurance Alliance

Net-zero

2021

United Nations

Paris-aligned Asset Owners

Net-zero

2019

Global Investor Coalition

Partnership for Biodiversity Accounting Professionals

Biodiversity

2019

-

Partnership for Carbon Accounting Professionals

Net-zero

2015

-

Principles for Responsible Banking

Responsible investment

2019

United Nations

Principles for Sustainable Insurance

Responsible investment

2012

United Nations

Principles for Responsible investment

Responsible investment

2005

United Nations

Sustainable Blue Economy Finance initiative

Blue finance

2018

United Nations

Taskforce on Nature-Related Financial Disclosure

Risk management

2020

United Nations, WWF

Type

MS

%

Responsible investment

5791

55

Climate change

1648

16

Net-zero

1136

11

Risk management

1026

10

Impact investment

422

4

Animal rights

296

3

Biodiversity

218

2

Blue finance

34

0.3

Sustainable transition

21

0.2

Green finance

10

0.1

Organisations

Frequency

%

1 or 2 memberships

6961

91.1

3–5 memberships

522

7.2

6–8 memberships

106

1.4

>8 memberships

21

0.2

Total

7640

100.0