Abstract

The article analyses the dynamics of start-up growth in Brazil highlighting the role of government, companies, venture capital and the innovation system in start-up policy. The most significant recent change in the Brazilian start-up ecosystem was the rise of growth-oriented entrepreneurship and start-ups. The 2021 Brazilian Legal Framework of Start-ups and Innovative Entrepreneurship is a milestone as it establishes mechanisms for the acquisition of products/services by the government provided by start-ups.

Introduction

Several studies have strived to explain the feedback among start-ups creation, the generation of innovations, opening new jobs and economic development resulting from these activities. Despite the COVID-19 pandemic of 2020 and 2021, start-ups expanded in Brazil. From 2015 to 2019, start-up creation jumped from an average of 4,100 to 12,700, an increase of 207%. By the end of 2021, the country had 14,065 start-ups distributed in 78 communities and 710 Brazilian cities, 1 led by São Paulo (4,027), followed by Minas Gerais (1,240), Rio Grande do Sul (976) and Rio de Janeiro (880).

Their activity areas are operated: 9% in education, 7% in other services, 6% in finance and 5% in health and well-being. Of the total, 47% target B2B; 29% B2B2C and 19% B2C. According to CB Insights data, start-ups in Latin America raised a whopping $9.3 billion during the first half of 2021—double the investment in all of 2020, with Brazilian start-ups capturing the lion’s share.

Then, in June 2021, Brazil passed the Complementary Law No. 182 dated 10 June 2021, the Legal Framework of Start-ups and Innovative Entrepreneurship (LFSIE) came into force aiming to create a favourable regulatory environment for innovative companies.

The article analyses the dynamics of start-up ecosystem in the context of Brazilian Science, Technology and Innovation (STI) evolution highlighting the role of the State, companies and venture capital in this movement. It is divided in three sections, besides this introduction. The second section presents a brief review of the literature on start-ups and the methodology. The third section provides an overview of Brazilian STI evolution. The fourth section highlights the role of the State, industry and venture capital in the expansion of start-ups, including start-up policies. The final section offers concluding remarks and directions for future research.

Theoretical Framework and Methodology

There is growing interest in policies to support entrepreneurship for economic growth, increased competitiveness and jobs, as they define the institutional environment in which business decisions occur and influence business growth (Minniti, 2008). Entrepreneurship policy pursued by countries to promote the establishment, growth and impact of innovative start-ups (Lerner, 2010; OECD, 2020b) are more effective when associated with an innovation policy due to the synergy created (Minniti, 2008).

The Concept of Start-up

The genGlobal ‘Start-up Nations Atlas of Policies,’ a major study of relevant policies in twenty-nine countries in Europe, North America and South America, covering a total of thirty-nine initiatives (Audretsch et al., 2020) identified a great heterogeneity of start-up concepts and diverse approaches in policies. It identified six approaches to define start-up: The Legal Framework of Start-ups and Innovative Entrepreneurship defines a regulatory and development environment for small technology-based companies in which only new or recently founded firms (up to 10 years) are considered start-ups, whose performance is characterised by innovation applied to the business model or to products or services offered. Additionally, limits are set for gross revenue. According Audretsch et al. (2020), Brazil adopted the ‘Self-declaration’ approach, as the proof of the innovativeness is given by the firm. That is, statement contained in the company’s foundation by law, that innovative business models are used to generate radical or incremental innovations in products and services.

Policies to support entrepreneurship have been the object of analysis by different authors in view of aspects focused on certain specific situations or objectives. The design of such policies to support often observe regional aspects, such as demographics, industrial structure and occupation, socio-economic conditions, as well as cultural aspects, access to finance, skills, network, among others. The main types of intervention are: (a) policies for institutional conditions; (b) direct support for entrepreneurs; (c) support to the development of entrepreneurial ecosystems (OECD, 2020b).

Audretsch et al. (2020) proposes a classification framework of entrepreneurship policy based on: (a) the antecedents of the creation of innovative start-ups; (b) their founding characteristics; (c) their behaviour; and (d) the outputs and impacts generated by them.

They generally adopt a range of instruments such as direct subsidies, tax cuts, capital grants, business training and counselling services (Autio et al., 2007), grants and subsidised loans (Hottenrott & Richstein, 2020), contracts through agencies, or government-run venture capitalist funds.

Several countries have promulgated ‘start-up acts’. Examples can be cited; the Italian Start-up Act (2012), encompasses different instruments for the subsidisation of both debt and equity of the innovative start-ups, highlights the complementarity of these two types of instruments that flow to different types of young innovative companies (Giraudo et al., 2019). Other developed countries have also established specific policies, such as Spain and Portugal (Fernández et al., 2022), USA (Buffart et al., 2020), Australia, Finland and Israel (OECD, 2013).

A normative view according to Shane (2009) and Colombelli et al. (2016) suggested that public policies supporting entrepreneurship should focus on programmes that support companies with high growth potential, that is, a small set of start-ups, which are responsible for creating most jobs and economic growth.

Considering this framework, this article analyses the dynamics of start-up ecosystem in the context of the Brazilian National Innovation System (NIS), highlighting the role played by state, companies and venture capital, as well as other private initiatives, in the growth of start-ups in the country. To achieve this goal, one needs to assess the Brazilian ST&I evolution, the design of public policies targeted at start-ups, as well as the main challenges for this set of companies. Thus, the next section analyses the role of innovation policies and instruments covering all phases of innovative firm creation, development and expansion, including financing, business services and entrepreneurial training. It further discusses main trends to develop policy implementation.

Brazil ST&I Evolution

In Brazil, historically, two sets of interrelated public policies are observed: science development policy and technology and innovation and industrialisation policy. The scope of each is differentiated and their interaction remains limited.

The emergence of the university was quite late, as it was only in 1920 that the Federal University of Rio de Janeiro was established followed by the University of São Paulo (USP) in 1934. The introduction of research in Brazilian universities and the institutionalisation of research began to take hold in 1948 with the creation of the Aeronautics Technological Institute (Botelho, 1999) and the founding of the Brazilian Society for the Advancement of Science (Botelho, 1990), respectively. Yet, the official sanctioning of research universities by the government did not take place until 1968 (Schwartzman, 2010).

From 1951, government institutions to promote the development of S&T were launched: the National Council for Scientific and Technological Development (CNPq), driven by the interest in the use of atomic energy and exploitation of national mineral resources (Burgos, 1999) and Coordination for the Development of Higher Education Personnel (CAPES), to support the training of human resources for government and companies (Martins, 2003). The import-substitution industrialisation initiatives of the federal government in the 1950s aimed at the production of durable consumer products, intermediate products and capital goods, was based on the import of technology, financed by foreign investments, associated or not with local entrepreneurs (Tavares, 2010).

Following the 1964 military coup, S&T activities expanded, driven by a goal of technological autonomy in strategic areas related to national security, focused on public companies (information technology, defence industry, aviation, nuclear power, oil and telecommunications). However, the private sector was generally excluded and did not benefit from the generation of technology (Coutinho & Ferraz, 1995).

Later on, the 1990s new initiatives were implemented to promote research. In 1998, the federal government set up the Oil and Gas Sectoral Fund, financed by mandatory taxes levied on companies, to promote research in key economic sectors. In the end, 16 sectoral funds were established.

The second ST&I conference in 2001 for the first time put innovation in the government agenda. It also for the first time discussed the role of start-ups and venture capital in innovation. In the beginning of the same decade, the Inovar project was launched by the Studies and Projects Financing Agency, later known was Brazil Innovation Agency (FINEP), in cooperation with the Inter-American Development Bank. In addition, FINEP launched pioneering calls for economic subsidy for companies in partnership with universities and a programme to establish and fostering venture capital, a fund of funds, until then non-existent.

In parallel, private initiatives towards entrepreneurship and innovation growth were taking place to shape a startup ecosystem. Among others, in November 2002, the first angel investment group in Latin America was formatted and created under the framework of the ‘New Venture Financing Project’ at the Pontifical Catholic University of Rio de Janeiro (PUC-Rio), supported by its alumni association, Gávea Angels. 2 The same university research unit behind it, Genesis Institute for Innovation, Entrepreneurship and Venture Capital Research Centre (NEP Gênesis), co-organised with the MIT Club of Brazil and the financial support of the Ministry of Science and Technology (MCTI). Finally, NEP Gênesis formatted and catalysed the foundation of the Brazilian Venture Capital Association (ABCR, later ABVCAP) in 2004 and produced a series of pioneering studies on entrepreneurship, start-up financing and venture capital in Brazil (Botelho & Pimenta-Bueno, 2002; Botelho et al., 2003; Botelho et al., 2003a; and Botelho et al., 2004).

Brazil’s Innovation Law discussion had started in 2000, shedding light on the need to develop an innovation policy with its respective mechanisms to foster innovation both in research institutions and in the Brazilian productive system. However, it was not until 2005 that its regulatory framework was issued and initial measures were not implemented until 2007–2008.

Next, between 2000 and 2014, the federal government introduced three sets of policies: Industrial, Technological and Foreign Trade Policy, Productive Development Policy (PDP), conceived by the National Bank for Economic and Social Development (BNDES), and the Great Brazil Plan, all ambitiously aimed to transform the country’s institutions with numerous initiatives. There was an expansion of financial resources made available and calls for firm innovation. Criticism of these initiatives argued for a targeted, smaller number of sectors, such as semiconductors, software, capital equipment and pharmaceuticals, to achieve greater impact, as their technologies permeate other sectors and affect the industry and the economy as a whole, besides the fact that they continuously exhibited high trade deficits (Suzigan & Furtado, 2006). In contrast, Salerno and Daher (2006) suggested that innovation directed to all economic sectors benefited the overall Brazilian industrial structure. Arbix (2019) notes that the PDP had three weaknesses: (a) abandonment of the emphasis on innovation; (b) broad goals, without taking into account the new dynamics of global innovation; and (c) use of old instruments, such as subsidies and protectionist measures. These weaknesses were still present in the PBG, which encompassed nineteen economic sectors and failed to prioritise innovation.

The economic and political crises from 2015 aborted the policies’ implementation, resulting in the reduction of the level of direct investment and the cancellation of tax incentives for R&D. After the 2016 impeachment of President Dilma Rousseff, significant cuts occurred in investments in science and education. After the election of Jair Bolsonaro in 2018, universities, research institutes and the areas of science and technology faced increasing obstacles, with attacks on science and on scientific activity, persecution of researchers and an exodus of young scientists and researchers. In 2020, the government approved a National Innovation Policy, which just amounted to a governance design, without setting targets, indicators, resources or priority sectors.

Brazil National Innovation System

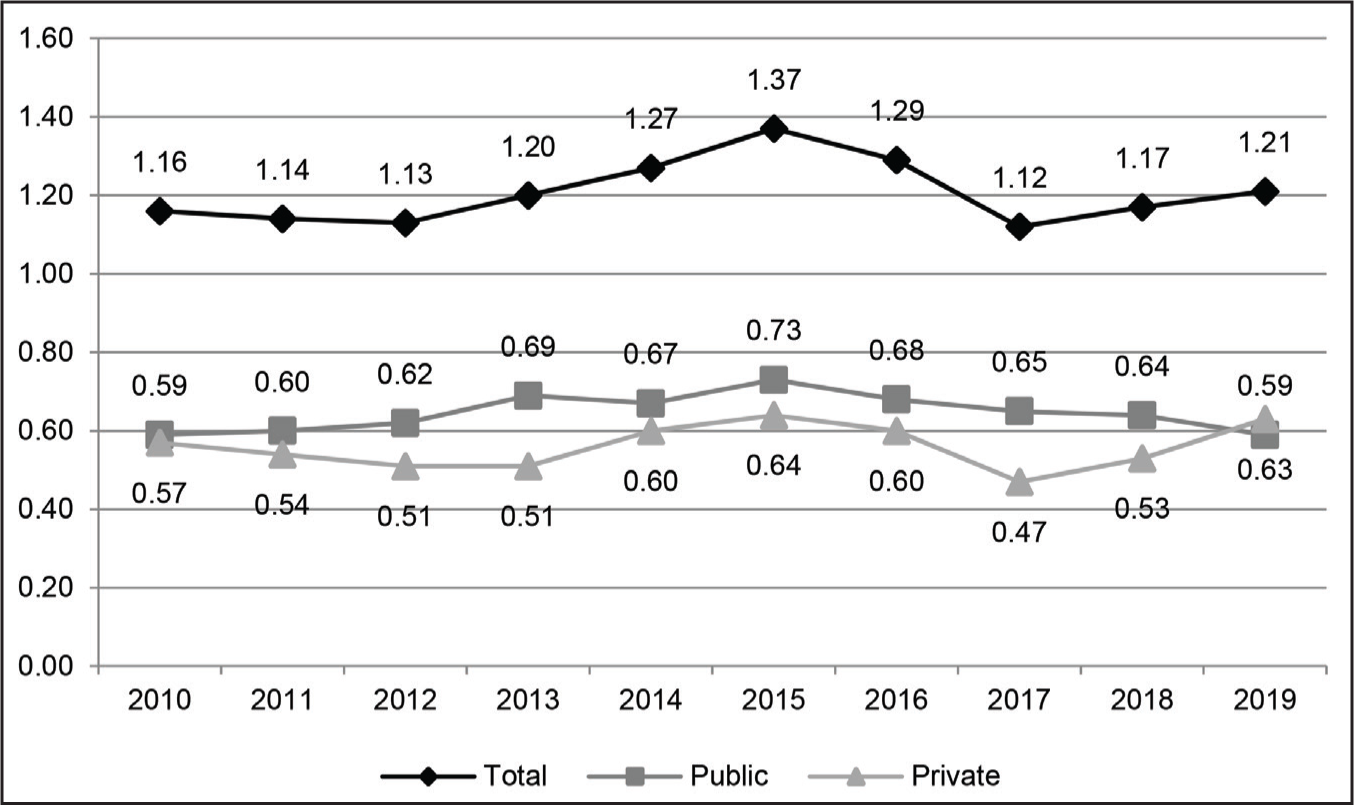

Resources for RDI as share of GDP increased from 0.96% in 2004 to 1.16% in 2010 (Figure 1), but after reaching a peak in 2015, fell abruptly and then stagnated, reaching 1.21% in 2019 (last year available) (MCTI, 2021). The strong growth in RDI in the first half of the last decade, particularly from 2012 to 2015, was due to both public and private sector expenditures. But as a recession and a fiscal crisis set in from 2015, the share fell abruptly and then experienced a moderate recovery from 2017 to 2019, when it reached 1.21%, slightly above the 2013 share of 1.20%. The growth recovery was driven by the rise in the share of the private sector, which reached 0.63% in 2019, the sector’s historic record and the first time it surpassed that of the public sector. The total of national R&D expenditures includes amounts allocated by federal/state governments and, to a lesser extent, companies to graduate programme, that correspond to 31% of total R&D.

Brazil’s entrepreneurial ecosystem ranking was 71 in the Global Competitiveness Index in 2019 (Schwab & Zahidi, 2020). In 2021, Brazil ranked 57th in the Global Innovation Index (GII) among the 132 economies (WIPO, 2021). The country’s position in the Global Entrepreneurship Index in 2019 was 117th in 136 countries (Ács et al., 2019).

The analysis of the internal context of ST&I by some authors using different methodologies has led to rather obvious conclusions that there are weaknesses and difficulties in the development of the innovation system in the country. For example, Albuquerque et al. (2008) claim that the innovation system in Brazil is ‘immature’, due to, among others: (a) a large share of specific individuals in patenting activities; (b) little firm involvement in innovation; (c) lack of continuity in patenting activity; and (d) low sophistication of inter-firm technological division.

The results of an analysis of a database of over sixteen million Brazilian companies and organisations to measure the Triple Helix Indicator through the synergy generated between geographic, technological and organisational distribution (number of employees) suggest that there is no synergy generated at the national level, which may conclude that the country’s political economy has not yet been transformed into a NIS (Almeida et al., 2022).

Innovation in Brazil

The last 2017 Innovation Survey, conducted every three years, covered a total of 116,962 firms in manufacturing, selected services, energy and gas companies, that employed ten or more people, indicates that the overall innovation rate is 33.6%. The largest innovation type share has been in internal processes (14.8%), involving mainly the replacement of machinery and equipment, followed by innovation in both products and processes (13.7%), while innovation in products alone was a mere 5.1%. The distribution of innovation by sector shows that in the manufacturing sector, 33.9% of the companies carried out innovative activity, while in services, it was 32% and energy and gas was 28.4% (IBGE, 2020).

Start-ups

Background

At the start of the 2010s, Brazil began to evolve vibrant start-up ecosystem, a product of state and civil society initiatives, which, nevertheless faltered due to the fragmentation and disconnection of policies and the continued weight of the 2008 Great Financial Crisis. The OECD 2013 assessment of Latin American countries strengthening their instruments and design of new programmes to foster start-ups claimed that ‘Brazil has the most dynamic private sector, in part due to the size of its economy’ (OECD, 2013, p. 15).. Recognising the existence of barriers to the creation and expansion of start-ups, the report assumes that policies are important for the creation of these firms and in their support through the seed and growth stages. It diagnoses that the creation and expansion of start-ups faces higher barriers in Latin America because of a ‘lack of appropriate financing mechanisms, scant dynamism of national innovation systems and a less business-friendly regulatory framework’ (p. 26).

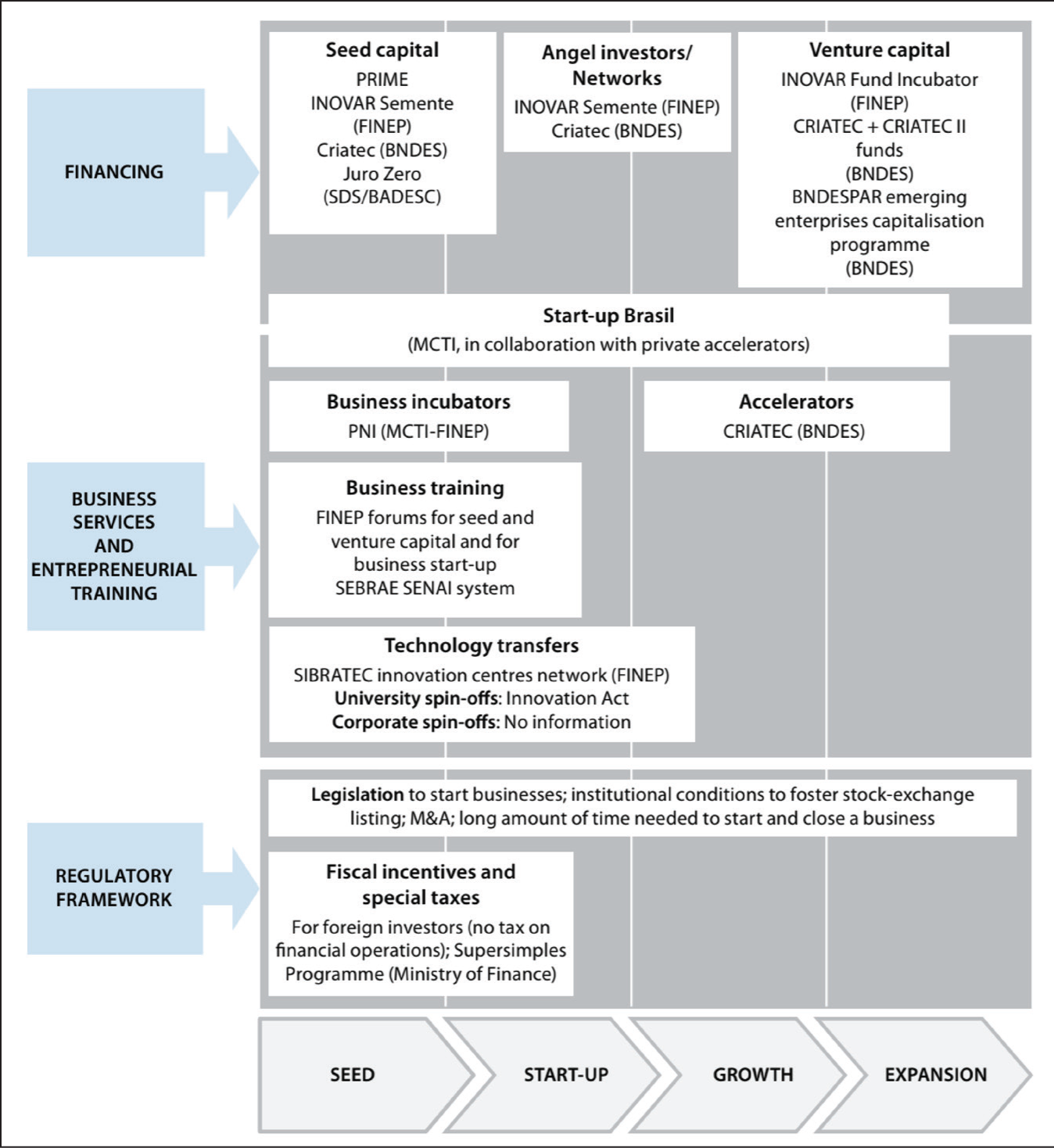

Regarding Brazil, it remarks that the country had been promoting new firm creation since the 1980s and highlighted the enhanced role of innovation policies and its expanding budget, concluding that it had a comprehensive roster of instruments (Figure 2) covering all phases of innovative firm creation, development and expansion, including financing, business services and entrepreneurial training. Further, it noted the growing start-up support role of state and local governments through technology parks. Still, it singled out the inadequate regulatory framework and lack of infrastructures as the main challenges for start-ups to play a significant role in the country’s development (OECD, 2013, p. 135).

Incubators began to be created in Brazil in 1986, mainly in universities. The first incubators were aimed at the creation of technology-based companies, but from the 1990s the scope expanded to include social and local development objectives (Etzkowitz et al., 2005). Today, in Brazil, there are a total of 363 business incubators, 43 technology parks, 3,694 incubated companies and 6,143 graduate companies, 14,457 jobs in incubated companies and 55,942 in graduated companies (Anprotec, 2019; MCTI, 2019a), as well as 270 Technology Transfer Offices (MCTI, 2019b).

Start-up Policy and Initiatives, 2010–2021

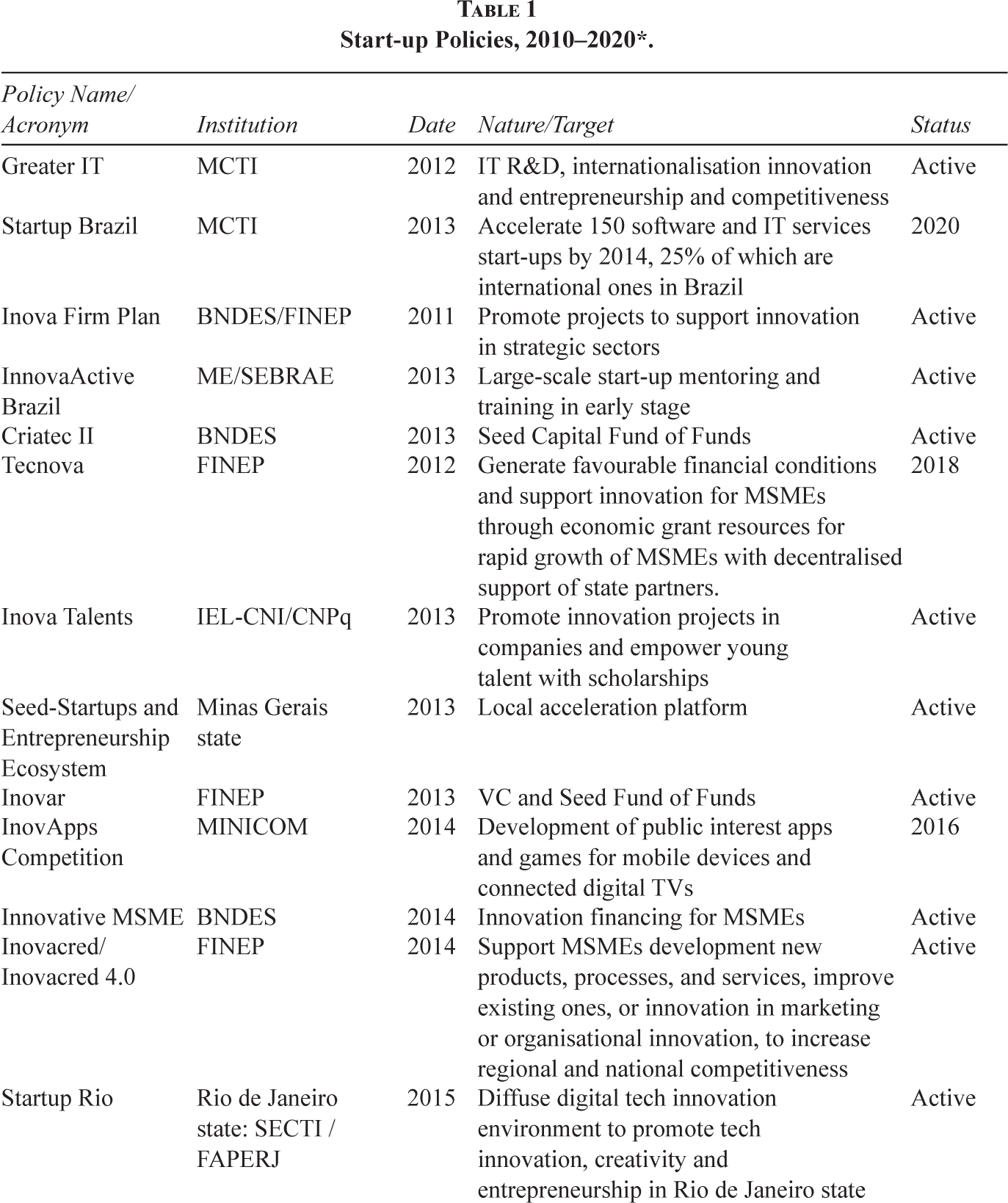

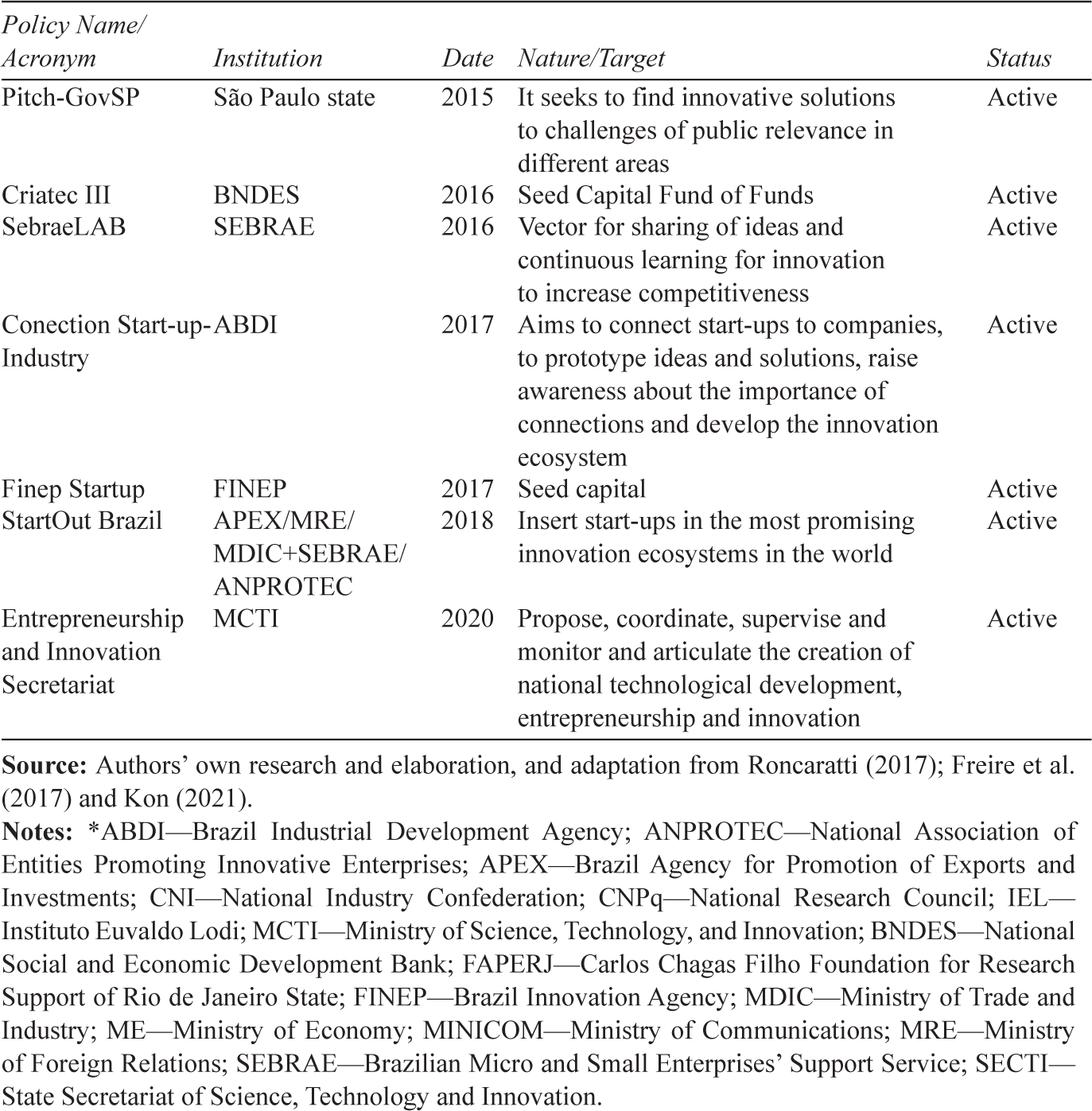

Over the past decade or so, as expected, there was a diversification of innovation support mechanisms, with a slight growth in innovative entrepreneurship and start-ups. Programmes were created (Table 1) that directly or indirectly contributed to the development of innovative start-ups and small companies, making the start-up ecosystem in Brazil more complex and diversified. Some programmes such as the Startup Brasil (2013) were further replicated in several units of the Brazilian federation like Minas Gerais, Rio de Janeiro, Santa Catarina and São Paulo states, among others. However, only at the end of the period, an Entrepreneurship and Innovation Secretariat was created at the MCTI with goal and monitoring and coordinating the wide range of policies in the Federal government.

Start-up Policies, 2010–2020*.

Throughout the same decade, diverse initiatives, often with corporate and government support, multiplied, strengthening and linking the various networks, and consolidating the start-up ecosystem, thus repeating their leading role in shaping the start-up ecosystem in the previous one.

In 2011, start-ups were still new in Brazil, but gradually start-ups from various regions were connecting to expand this movement. The Brazilian Start-ups Association (ABS), a national network with volunteers in the states, emerged from the union of several entrepreneurs to establish a cohesive front to act for Brazilian start-ups with the goal of creating a network of connections for learning, fostering start-ups and generating opportunities for associates. In 2012, it launched a database, regional managers, event support and organisation of Pitch Digital; in 2013 it professionalised and adopted a business model and created a Pitch Corporate Model and Open-Source events. Finally, in 2014, it celebrated an agreement with Apex-Brasil, organised the first CASE event, the Pitch Corporate, and launched a new Start-up Base and conducted international missions.

Large corporations, domestic and international, began to invest in the ecosystem. For example, in 2016, the Google for Startups opened the Google for Startups Campus, a physical space that offers programmes, workspace and different resources for start-ups, 3 supporting companies at various stages of growth through programmes that provide access to Google products, technologies, best practices and experts, as well as partnerships with accelerators, incubators and other start-up support organisations in more than 120 countries. More than 250 start-ups have participated in Google for Startups’ long-running programmes in the country, more than 1,500 events have been held, between the virtual and those that took place on campus, in which over 30,000 people were trained in topics related to entrepreneurship, technology and innovation. 4 In 2020, seeking to address the racial inequality in the ecosystem, Google for Startups launched the Black Founders Fund, which invests financial resources, without any counterpart or corporate participation, in start-ups founded and led by male and female black entrepreneurs in Brazil. 5

Unicorns

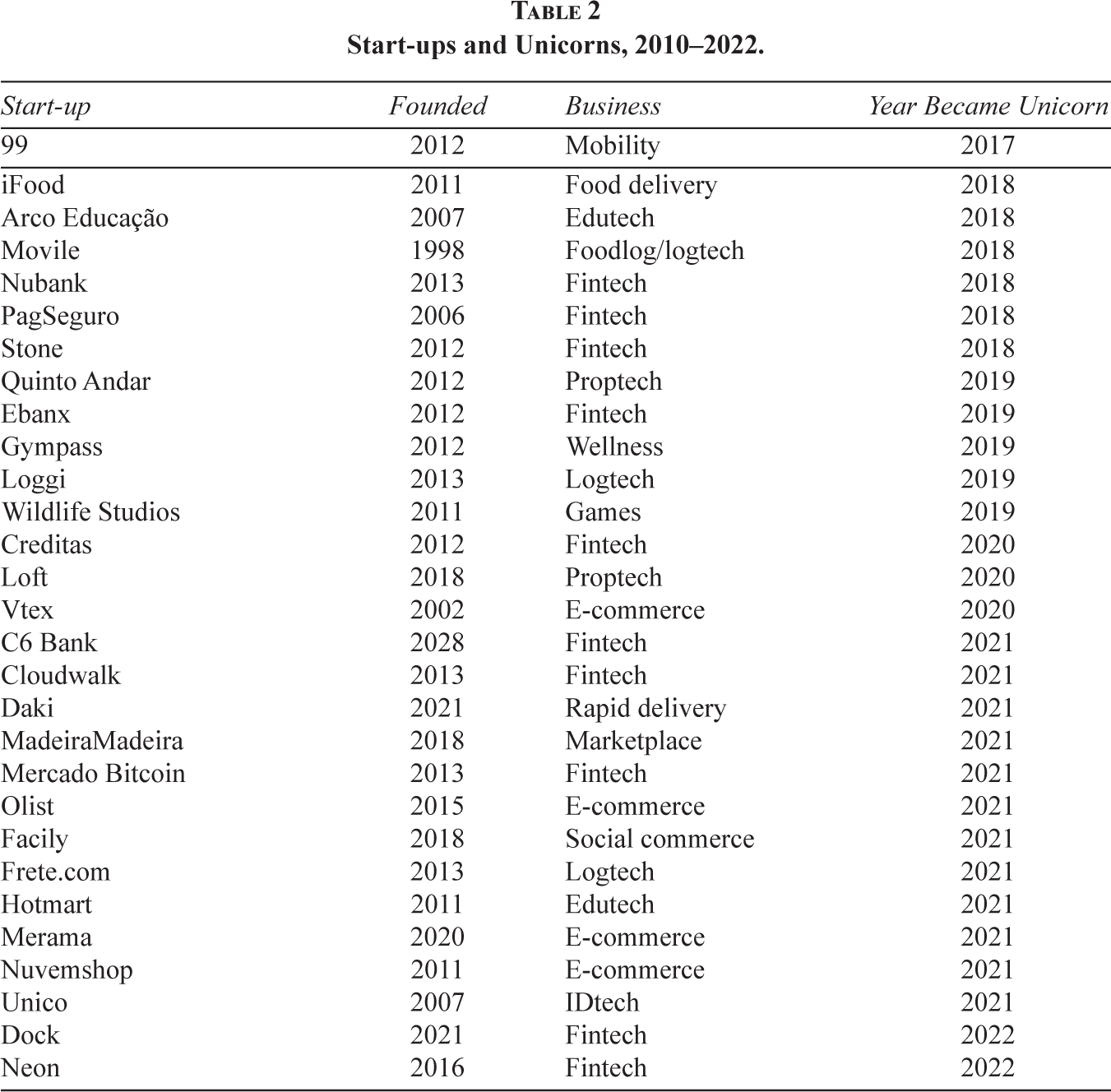

According to the tech platform Distrito, at the end of 2021, following record investment in technology (US$ 9.4 billion, over twice as much as 2020, US$ 3,659 billion), Brazil had eleven new unicorns, the highest addition since 2019, when five were added, with fintech leading. By April 2022, Brazil had twenty-nine unicorns, with an estimated total value of US$ 50 billion, in a universe of 13,712 start-ups, according to the Brazilian Start-ups Association (ABS). It was the country with the largest number of unicorns in Latin America, the third in the Americas (after the United States and Canada) and the second largest among emerging economies (behind India). However, the global economic crisis and high domestic interest rates led to massive layoffs among them.

As shown in Table 2, between 2010 and 2022, twenty-nine Brazilian start-ups became unicorns. Although fintech start-ups represented over one-third of this number (ten), they were distributed over a broad range of areas, evidence of the ecosystem vitality. In 2022, with worldwide rise interest rates and drastic reduction in liquidity, start-ups overall faced a challenging environment and therefore the number of unicorns in Brazil dropped dramatically to two (both in fintech and still half of the unicorns in Latin America), following all time high of eleven in 2021.

Start-ups and Unicorns, 2010–2022.

Recent Trends

According to McKinsey’s 2019 Brazil Digital Report, 63% of Brazilian start-ups have up to five people on their staff and for 69% revenue is below than R$ 50,000 reais per year. Angel investment has been growing at an annual average of 14%, according to data presented in the McKinsey report. According to data from LAVCA, the Latin American Association of Private Equity & Venture Capital, Brazil is responsible for 70% of the movement generated by this type of investment fund in Latin America. The volume of investments has also been growing and, since 2016, has increased by about 64% every year.

The ThoughtWorks’ survey Who Codes in Brazil provides an overview of diversity in technology careers in the country: the presence of women in technology positions is only 32%, the participation of black people is at a similar level, which stands at 37% and the representation of people in the LGBTQIA+ community is around 21%.

Roughly, a decade later of the issuance of its 2013 report, a new OECD (2020a) report with a broader scope on ‘SME and Entrepreneurship Policy in Brazil’ argues for the critical role of SMEs in economic growth and social inclusion in Brazil, observes the much wider gap in labour productivity between Brazilian SMEs and large companies compared to OECD countries, and calls attention to widespread business in contrast to less developed growth-oriented entrepreneurship. Some general challenges for SME noted, also valid for start-ups include the credit market, business regulations and taxation, although significant reforms have recently been introduced in each of these areas. 6 It further remarked the lack of growth-oriented entrepreneurship, both in the form of young high-growth firms and business scale-up 7 and the challenges posed by the business environment for SMEs, which are also to start-ups: limited integration in global trade; hindering their participation into global supply chains; complex business regulations; and tight credit market conditions given high interest rates and short loan maturities (p. 15). More importantly it stated that ‘Brazil has a well-functioning innovative start-up ecosystem’. 8 Some of the recommendations made, which may be important for improving the start-up ecosystem, are summarised in Box 1.

OECD (2020a) SME and Entrepreneurship Policy Recommendations.

•

•

•

•

•

Indeed, in the last few years, there has been an increase in corporate support for start-ups, either through in-house programmes, often assisted or managed by specialised providers, or as part of existing public programmes. There appear to be three main drivers behind this trend. First, firms market pressure to innovate or to appear innovative to the market. Second, evolving sectoral concessions regulatory frameworks for R&D which opened possibilities for expenditures on start-up development in view of advancing in the innovation chain. Third, technological developments in areas such as 5G create new market opportunities.

Further, corporate venture has experienced a surge in the first years of the new century in Brazil. Both large domestic and multinational companies in various sectors, across services and manufacturing, are establishing programmes, such as Boticário and Natura, the country’s leading cosmetics companies and Centre for Advanced Systems and Studies in Recife, in the northeastern state of Pernambuco, through Natura Start-up 2016. 9 Alongside, existing innovation and start-up business service providers have ramped up their hiring of corporate venture professionals to expand their activities in this domain, such as ACE Aceleratech and FCJ Venture Builder, the acceleration of start-ups in partnership with Telefônica Open Future and the Technology Park of the Federal University of Rio de Janeiro, through a project called CrowdRio, 10 the Ocean New Business Programme, between Samsung and the University of São Paulo, for the selecting of projects, 11 or the agreement between the University of Passo Fundo, in the municipality of Passo Fundo, Rio Grande do Sul state and Ambev, the country’s largest beverage company, signed in 2021. 12

In 2021, total VC investments reached US$9.43 billion distributed in a total of 779 transactions, according to the latest Inside Venture Capital report, a value 2.5× higher than 2020. 2021 also broke the record in the number of new unicorns of ten companies— MadeiraMadeira, Hotmart, C6, Bitcoin Market, Unico, Frete.com, CloudWalk, Merama, Facily and Olist—raising the country’s total to twenty-one. Fintech topped the list with US$ 3.7 billion last year in 176 rounds, followed by retailtechs, with US$ 1.3 billion in eighty-seven transactions, and real estate, which captured $1.07 billion in thirty-two rounds, health start-ups raised $530 million over sixty-nine negotiations, and mobility raised US$ 411 million in twenty transactions. Early-stage start-ups concentrated the largest amount, with the Seed phase, posting 279 transactions, totalling US$ 320 million, and 200 transactions in Pre-Seed, which raised US$ 47 million. The most advanced rounds responded for the higher volumes of investments. The twenty-seven Series C transactions for the year raised $2.04 billion, and the fifty-one series B rounds raised $1.92 billion. Finally, the number of mergers and acquisitions hit a record, with 247 start-ups bought or merged by other companies and most of the transactions were carried out by other start-ups, which, for the third consecutive time, outperformed incumbent companies in acquisitions: fintechs (forty-four), martechs (twenty-seven), retailtechs (twenty-six), edtechs (nineteen) and healthtechs (nineteen). 13

In the first quarter of 2022, Brazilian start-ups received $2.04 billion in investment, according to consulting firm Distrito, an amount 4% larger than that of the same period of 2021, which had then set a record. The first quarter of this year presented 167 rounds of investment; in the same period of 2021, there were more: 200. The start-ups of 2022 received a higher average value in the contributions; Series A received about US$18 million on average, and series F, US$260 million. In 2021, it was US$ 11.5 million and US$ 206 million (R$ 53 million and R$ 949 million), respectively. In return, the money is going to fewer start-ups. The five main target sectors received $1.555 billion in the first quarter of 2022, up from $1.496 billion in 2021. The top five consist of fintechs (finance, 67.8%), retailtechs (retail, 13.6%), HRTechs (human resources, 12.7%), real estate (real estate, 3.1%) and agtechs (agricultural, 3%). At the beginning of the previous year, real estate was at third, and human resources at fourth position. 14 In April alone, Brazilian start-ups received US$ 437 million over fifty rounds of investments that took place in April, a number about 5% lower compared to March this year, when start-ups raised $462 million. 15

According to the 100 Open Start-ups organisation, Brazil leads in the open innovation model. Between July 2021 and June 2022, the number of companies that hired start-ups grew by 30%. The business amounted to 2 billion and 700 million. The global beverage behemoth Ambev is at the head of this investment—it now has a partnership with 340 start-ups, including Lemon Energia, a start-up that helps bars and restaurants reduce the electricity bill and consume renewable energy, and Zé Delivery, an application with four million active users per month, has reached 300 cities and made almost 100 million deliveries. Also, Suzano, the world’s largest pulp producer, has partnerships with 275 start-ups in many ongoing projects.

Considering the start-up scenario, the LFSIE is a milestone in the period of 2010–2022. It establishes mechanisms for the acquisition of products/services by the government provided by start-ups. Regarding investors, it legally defined angel investors and set mechanisms to protect investors, so that those who are not a partner or manager, or have the right to vote in the management of the company, are held responsible for any kind of obligation or infringement practiced by the company. The investment made in the start-up is not considered as a member of the share capital until its option for the conversion performed by the investor. Thus, the equity risks are delimited to the amount of the contribution made, until it is included as a partner or shareholder (Málaga, 2022).

Concluding Remarks

Recently, the most significant change in the Brazilian start-up ecosystem over was the emergence of growth-oriented entrepreneurship and start-ups, fuelled by the rise of a social consciousness about the importance of start-ups for the country’s socio-economic development. Thus, at the start of the polarised 2022 presidential campaign, Guilherme Benchimol, one of the country’s most successful and celebrated entrepreneurs, founder and CEO of the fintech investment start-up XP Investimentos, when asked why he talked to with the strongest challenger of the left Lula da Silva, stated on his Instagram: ‘The agenda is how we can have a stable economy, low interest rates, inflation in check, and make our twenty million entrepreneurs, who employ more than fifty million Brazilians, increase in quantity, and can be better and better, generating even more prosperity for our country’ (Valor Econômico, 2022).

In the GII 2022, Brazil (in second place, between Chile in first and Mexico in third) joined the top three ranked innovation economies in Latin America. Although it advanced three positions from 2021 to reach fifty-four in the GII index and placed ninth in the upper middle-income economies’ subgroup (total thirty-six), it outperformed in innovation relative to its development level and had for the first time one global top 100 S&T cluster (São Paulo). Brazil retained its achiever status for a second consecutive year and moved forward in the overall rank since 2019, having experienced an accelerated ranking increase over the previous five years. In 2022, Brazil showed major improvements in innovation outputs, namely in Creative outputs, including in Intangible assets and Online creativity, as well as in the indicators Trademarks (19th) and Mobile app creation (34th). The country is top of the region for business sophistication (35th). Curiously, as noted above, the rise of Brazil in the GII occurred while government RDI expenditures stagnated and then declined, whereas private RDI expenditures to surpass those of government for the first time ever.

Further, in 2021, VC deals showed strong growth in all regions of the world with Latin America and the Caribbean (+98.7%) leading with around 300 deals, albeit from a low starting point. Financial services dominate Latin America’s start-up scene, and this is clearly reflected in the top ten most valued VC deals in the region (which received USD 4 billion of the USD 15.7 billion). Five of the top ten deals were sealed by fintech companies, such as Nubank of Brazil, which now has more customers than any other standalone digital bank in the world. Another four were start-ups in online platforms. Kavak (Mexico’s first unicorn), for example, provides digital solutions to the often-hazardous experience of buying a used car and Brazil-based Quinto Andar is making it simpler to rent a flat by eliminating the need for brokers and offering its own insurance.

However, there’s a hidden ceiling to this emerging growth ramp. All Brazilian unicorns’ business model were based on market opportunities, and none was built upon intellectual property produced in the Brazilian NIS, although a few of them were at the start incubated in a few top research universities. An OECD study, based on profiles of startups registered on Crunchbase, shows that entrepreneurship among university students and recent graduates is highest in countries such as Canada, Australia, India and Brazil, where students account for more than 10% of all entrepreneurs starting new technology companies—a rate higher than the United States, Israel, the United Kingdom and France. Out of 447,000 innovative companies from 199 countries, only 290 startups were identified in Brazil, of which 12% were started by undergraduate students or recent graduates, mainly in the gaming, transport, education and e-commerce spaces, generally linked to software applications and low-investment ideas. In fact, in Brazil, most student entrepreneurs are undergraduates or only have a bachelor’s degree, what negatively influences the level of technological innovation and the prospects of sustainable high growth. The OECD survey showed a much higher proportion of tech-based start-ups founded by people with a doctorate in Switzerland, Denmark, Germany and the United States than in Brazil. General entrepreneurship training is still absent in Brazilian undergraduate university courses and is virtually non-existent at the graduate level, and even more absent are technological entrepreneurship ones. This is due to a higher education regulatory framework which curtail efforts in this direction and continues to almost reward scientific publications solely. Integrating the stodgy Brazilian NIS with the vibrant startup ecosystem remains a slippery challenge ahead.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.