Abstract

This study maps the evolution of the Australian start-up and innovation ecosystem by exploring policy developments and mapping the key actors, activities, and artefacts. This study unpacks policy developments over the past two decades to show the government’s role in shaping the innovation ecosystem and the implications for start-ups. We outline the ecosystem’s key actors, including start-ups, scale-ups, support organisations, investors, research institutions, and their growth over time. We examine the artefacts of the ecosystem to understand start-up and innovation performance in a global context. We also explore the activities of the ecosystem in terms of collaboration, research, and development. The study concludes with a discussion of policy gaps.

Introduction

Ecosystems perspectives focus on dynamic interactions between actors in a given environment and how these interactions develop over time (Adner, 2017). The ecosystem lens is a popular conceptual and metaphorical tool applied to many disciplines ranging from management, entrepreneurship, and innovation (Autio, 2022; Bliemel et al., 2024; Cetindamar et al., 2020; De Jager et al., 2017). While there has been some convergence towards a conceptual understanding of innovation ecosystems, no two ecosystems are the same, as one recent study identifies fifty distinct types of innovation ecosystems (Klimas & Czakon, 2022). Given the heterogeneous nature of innovation ecosystems, place-based insights are needed to understand how ecosystems develop over time.

The ecosystem’s view has advanced beyond the research on economic geography, clusters, and regional or national innovation systems (Fernandes et al., 2021). More recently, the constructs of ecosystems were described as models comprising a specific space and place, for example, national innovation ecosystems, regional innovation ecosystems, industrial innovation ecosystems, and enterprise innovation ecosystems (Jiang et al., 2019). Ecosystems literature recognises that innovation processes in these regions involve a collective effort of various actors working within particular institutional arrangements (Gifford et al., 2021), and public policies shape such institutional arrangements. Therefore, it is no surprise that policymakers show great interest in ecosystem concepts because they offer a more holistic and integrated guide for entrepreneurial and innovation activities (Daniel et al., 2022).

Studies in entrepreneurship and innovation indicate the strong geographic effects on ecosystems (Muñoz et al., 2020). Despite all the research on road mapping and ‘stock taking’ of innovation systems and policies, the link between this and how policymakers utilise this to make decisions is unclear (de Vasconcelos Gomes et al., 2021). Hence, policymakers could conduct deliberative interventions through policies to create a supportive environment for flourishing ecosystems. Krishna (2019) shows how government policies for entrepreneurship, such as supporting incubation and science and technology parks, have changed leading Asia-Pacific universities. Similarly, Audretsch et al. (2021) point out how institutions influence entrepreneurial ecosystems at the city level by defining incentives that guide individual and firm rational choices operating in these systems. Rong et al. (2021, p. 545) also found a direct positive link between having ‘appropriate and well-informed governmental support’ and how this, in fact, ‘can significantly boost the national innovation system’. Regional governments therefore play a role in closing the gaps and supporting access to opportunities with underdeveloped institutional infrastructure and systems (Rong et al., 2021).

Despite an inherent relationship between ecosystem dynamics and policy, studies attempting to link policies with ecosystems are at their early stage (Borrás & Edlerm, 2014), and the gap between innovation policymakers and researchers contributes to delays in progress (Recke & Bliemel, 2018). Simultaneously, there are increasing calls for more research to shift the focus from individual entrepreneurs or specific innovations towards the orchestration of ecosystems (Autio, 2022; Han et al., 2022; Muñoz et al., 2020). Drawing from the ecosystem approach, this paper poses the following question: How could we explore the dynamics of a national start-up and innovation ecosystem through an analysis of policy developments?

The remainder of this paper is structured as follows. The section ‘Literature Review’ introduces the key concepts from the literature, followed by an introduction to the background of the Australian Innovation Ecosystem. The section ‘Analysing the Australian Start-up and Innovation Ecosystem’ presents the elements of the Australian Innovation Ecosystem. The presentation relies on the innovation ecosystem framework and ‘zooms in’ at the micro level on cases that exemplify specific policies and their impact. The section ‘Policy Gaps, Challenges, and Enablers’ points the overall challenges, while the section ‘Conclusions’ summarises observations from the Australian case.

Literature Review

The ecosystem construct is inspired by a natural lifecycle where species organise through mutual adjustment of their parts to survive or fail, are heavily influenced by conditions of the local environment (Moore, 2006). Each subsequent application of the ecosystem concept shares common attributes of actor agency, the actor’s capacity to envision an unrealised state and mobilise action towards an end goal (Han et al., 2022).

The characteristics of the ecosystem are evident in recent definitions of the various ecosystems, including business, innovation, entrepreneurship, knowledge, service, and platform ecosystems (Beaudry et al., 2021; de Vasconcelos Gomes et al., 2021; Hou & Shi, 2021). After analysing 120 publications on ecosystem approaches, Granstrand & Holgersson (2020, p. 3) define the innovation ecosystem as an ‘evolving set of actors, activities, and artefacts, and the institutions and relations’ that determine the innovative performance of actors.

In the context of an innovation ecosystem, actors are individuals or organisations such as firms and banks, activities include innovation processes and research & development activities, and artefacts consist of inputs and outputs (such as products and services) and resources (such as technological and non-technological resources). Relations refer to the interchange of cooperation or competition among actors. Institutions constitute the context in which entrepreneurs, firms, and organisations operate activities and influence artefacts and relations within the context. Institutions are synonymous with rules, policies, and regulations (Gifford et al., 2021).

This paper considers the extent to which policy as ‘rules of the game’ (North, 1990) influences the innovation ecosystem in Australia. Key characteristics of the innovation ecosystem include (1) a focus on value creation and value capture and (2) the co-evolution of actors through competitive (substitutive) and cooperative (complementary) relations (Granstrand & Holgersson, 2020). Compared to a more static systems perspective, Beaudry et al. (2021) highlight the ecosystem’s emphasis on dynamic movement and a geographic focus. The dynamic and place-based features of the innovation ecosystem make it a desired tool for policymakers in achieving resilience and competitiveness through adaptation capacity (Boyer, 2020). A policy’s role is to realise the ecosystem’s ideal-state condition (Zheng & Cai, 2022). Hence, our study aims to increase knowledge on policies as institutions affect actors, activities, and artefacts in an innovation ecosystem. By doing so, policymakers might focus on how to co-evolve with the ecosystem and effectively respond to changes by adapting their policies.

Studies on innovation systems show various types according to level of analysis lying on national, sectoral, regional, technology, or firm levels (Gu et al., 2021; Lammers et al., 2021; Muñoz et al., 2020) or even at the organisation level, such as research centres (Dolan et al., 2019). This paper’s primary unit of analysis is the national level while acknowledging the interplay with the state level.

This study presents a narrative account of policies in a national innovation ecosystem. Our contribution to the literature is introducing and examining a novel institutional context in Australia by presenting:

Policies focusing on actors of the ecosystem, such as entrepreneurs. Policies related to artefacts, such as technology. Policies affecting the activities in an ecosystem.

Two Decades of the Australian Start-up and Innovation Ecosystems

The 2000s

In 2000, Backing Australia’s Ability (BAA) package provided a national approach to fund innovation (Commonwealth of Australia, 2001; Innovation and Science Australia [ISA], 2017). The BAA supported research reform to address incentives that emphasised publications over wider, broader impact. However, the programme did not include effective institutional mechanisms to support a coherent whole-of-government approach (Gunn & Mintrom, 2018). The programme provided funding for science but was criticised for providing comparatively little for collaboration or the commercialisation of research and taking an interventionist market-failure approach over a systems approach (Conley & van Acker, 2011; Dodgson et al., 2011).

The BAA programme was extended in 2004 with Backing Australia’s Ability – Building our Future through Science national package (Australian Government, 2004). Observations on the BAA period of innovation programmes noted a preference for general tax relief rather than focused or selective support for innovation and it reflected a belief that market failures pose less long-run risks than government failure (Dodgson et al., 2011).

The 2009 strategy Powering Ideas: An Innovation Agenda for the 21st Century placed more of an emphasis on the system of innovation through ‘connections between innovation and research with industry, businesses, and government’ (Commonwealth of Australia, 2009; Dodgson et al., 2011, p. 1151).

Powering Ideas made a case for a systems approach, referencing Australia slipping from fifth to eighteenth in the World Economic Forum’s Global Competitiveness Index, a 22% decrease in Commonwealth science and innovation spending as a share of GDP over 16 years, stagnant rates of the proportion of Australian firms introducing innovations, and a ‘decade of policy neglect’ (Commonwealth of Australia, 2009, p. 2).

The report presented themes to be included in reports over the next 7 years on the National Innovation System: business innovation, entrepreneurship; science and research, networks and collaboration; and skills and capability. The report’s vision statements for 2020 outlined aims for aspects of the innovation system such as ‘researchers, businesses, and governments work collaboratively to secure value from commercial innovation and to address national and global challenges (Commonwealth of Australia, 2009, p. 9).

The Queensland Innovation Strategies.

In 2000, the Queensland Government offered innovation grants with an initial annual budget of $6.4 million and provided grants for initiatives such as a $175,000 pre-seed funding innovation start-up scheme that was cited as Australia’s first technology incubator in Toowong with a capacity for 15 companies, a time limit on participants of 2 years, and budget of $3.75M; four technology parks with a combined investment of $28 million; $1.4 million funding to the Queensland Manufacturing Institute. The Department of Innovation and Information Economy was established in 2001 to manage the portfolio, with additional priorities including the establishment of a $100 million Smart State Research Facility Fund, the Queensland Industry Development Scheme, a 4-year, $10.3 million Communication and Information Industries Development Strategy, and a 10-year, $270 million Biotechnology Strategy.

The 2010s

The next significant national innovation policy statement was the 2015 National Innovation and Science Agenda (NISA) (Australian Government, 2015). The NISA supported initiatives across four themes Culture and Capital, Collaboration, Talent and Skills, and Government. The initiative was supported by other programmes related to intellectual property, tax, education and talent development and attraction, global connections, and regional development. The suite of policies contributed to a national narrative while also being criticised for increasing activity levels without ensuring activities are successful, a lack of investing in new directions, and high knowledge creation and low translation and commercialisation that did not necessarily account for the complexity of innovation policy (Carter, 2017). Universities noted that ‘$1B of the $3B cut in research and innovation expenditure under the previous government was being restored’ (Barrett, 2016). The programme audit conducted mid-way through the project in 2017 would further identify programme delays, a lack of outcome evaluation or expected impacts, and recommendations reliant on assertions rather than evidence (Australian National Audit Office, 2017).

The Entrepreneurs Programme, 2014–2015.

The Australian Government started the programme with a $400 million fund to help small businesses become more competitive and accelerate their growth by the following four mechanisms:

Accelerating Commercialisation Business Growth Grants Incubator Support Innovation Connections.

After the bushfires in 2020, the programme was expanded to include a new service called Strengthening Business, aiming to connect companies with specialists to help them to strengthen, resiliency, and future-proof their business.

The 2020s

The current portfolio of Australian innovation policy comes from the amalgamated Department of Industry, Science, Energy, and Resources and its portfolio agencies and collaborative entities. Individual strategies are part of whole-of-economy reforms in tax, industrial relations, energy, trade, expansion and diversification, and innovation and skills (Department of Industry, Science, Energy, and Resources, 2021). The overarching portfolio strategy―Digital Economy Strategy―under the Department of the Prime Minister and Cabinet includes (Department of the Prime Minister and Cabinet, 2021) digital technologies such as Artificial Intelligence and Cyber security and climate technologies for emissions reduction and clean technologies such as Hydrogen. The last update in April 2022 reflected support for a continuation of the Digital Economy Strategy over 4 years (Department of the Prime Minister and Cabinet, 2021).

George & Tarr’s (2021) review of Australian innovation policies suggests that current policies are blurring a system approach. The study mentions that Australia introduced an innovation policy framework in early 2020 entitled Stimulating Business Investment in Innovation. Compared to the NISA policy, the new policy is based on the near-term policy focus on non-R&D innovation as the mechanism to achieve productivity growth and emphasises targeted measures. They strongly argue that placing industry in front of innovation and science for the new name of Department of Industry, Innovation and Science Australia in October 2020 signals how policies shift from innovation ecosystems to industry ecosystems.

NSW Entrepreneurship and Innovation Action Plan 2021.

The NSW Government’s action plan aims to grow jobs and new industries through commercialising R&D by calling specific projects to deal with strategic challenges. To date, three challenges have been announced to develop a product or service that could strengthen the state’s entrepreneurship capability. The first two challenges have already seen $1M invested in innovative ideas, such as an artificial intelligence diagnosis platform for lung scans that helps improve COVID-19 detection. The third challenge offers an additional $500,000 in seed funding invested in R&D solutions that address the pandemic’s long-term strategic challenges, such as strengthening NSW’s sovereign capability and local supply chains.

Analysing the Australian Start-up and Innovation Ecosystem

Actors of the Ecosystem

Support Organisations and Institutions

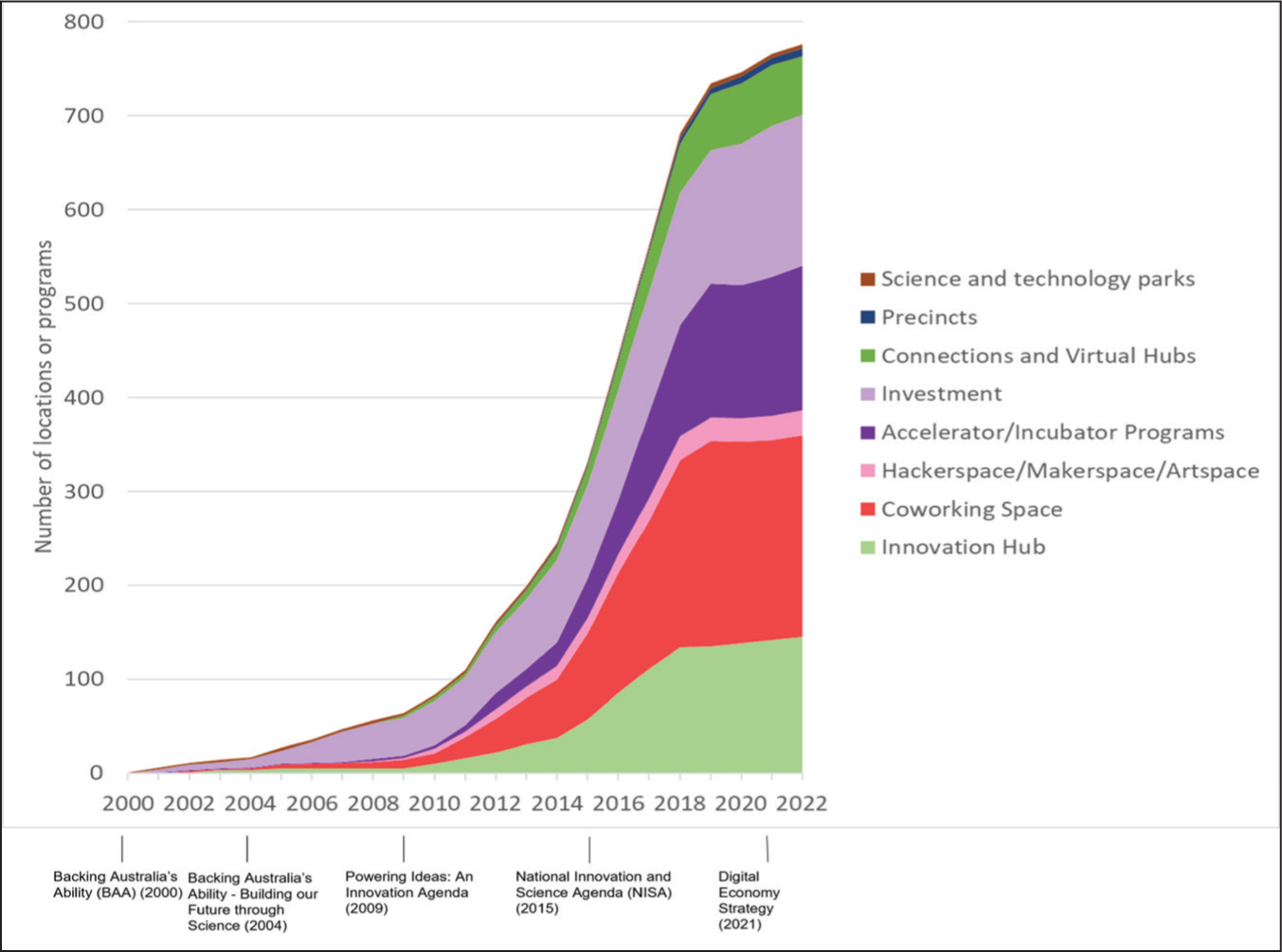

A core outcome of innovation policy is increasing actors’ capacity to support the innovation and entrepreneurial process. Two forms of this support include incubation and investment. Incubators describe ‘an overall denomination for organisations that constitute or create a supportive environment that is conducive to the hatching and development of new firms’ (Bergek & Norrman, 2008, p. 20). Hence, they include coworking spaces, precincts, science and technology parks, hubs, accelerator programmes, and hackerspaces. Investment considers the broad range of risk capital, including angel investment, venture capital (VC) funds, crowdfunding, government grants, and debt financing. Data on Australian Innovation Ecosystem actor entries and exits were captured in Renando (2020) and maintained in Renando’s Startup Status mapping platform (Figure 1). While definitions of each type of organisation remain debatable, the data reflect a significant growth period.

Innovation Policy and Start-up Support Organisations in Australia (2000–2022).

Australia experienced a significant increase in the number of entrepreneur support actors starting around 2010, with the number of actors accelerating from 2014, with much of the growth supported by NISA’s Incubator Support Program and state-level policies, peaking in 2018, the year in which over eleven incubators per month on average were established.

Entrepreneurs, Start-ups, and Scaleups

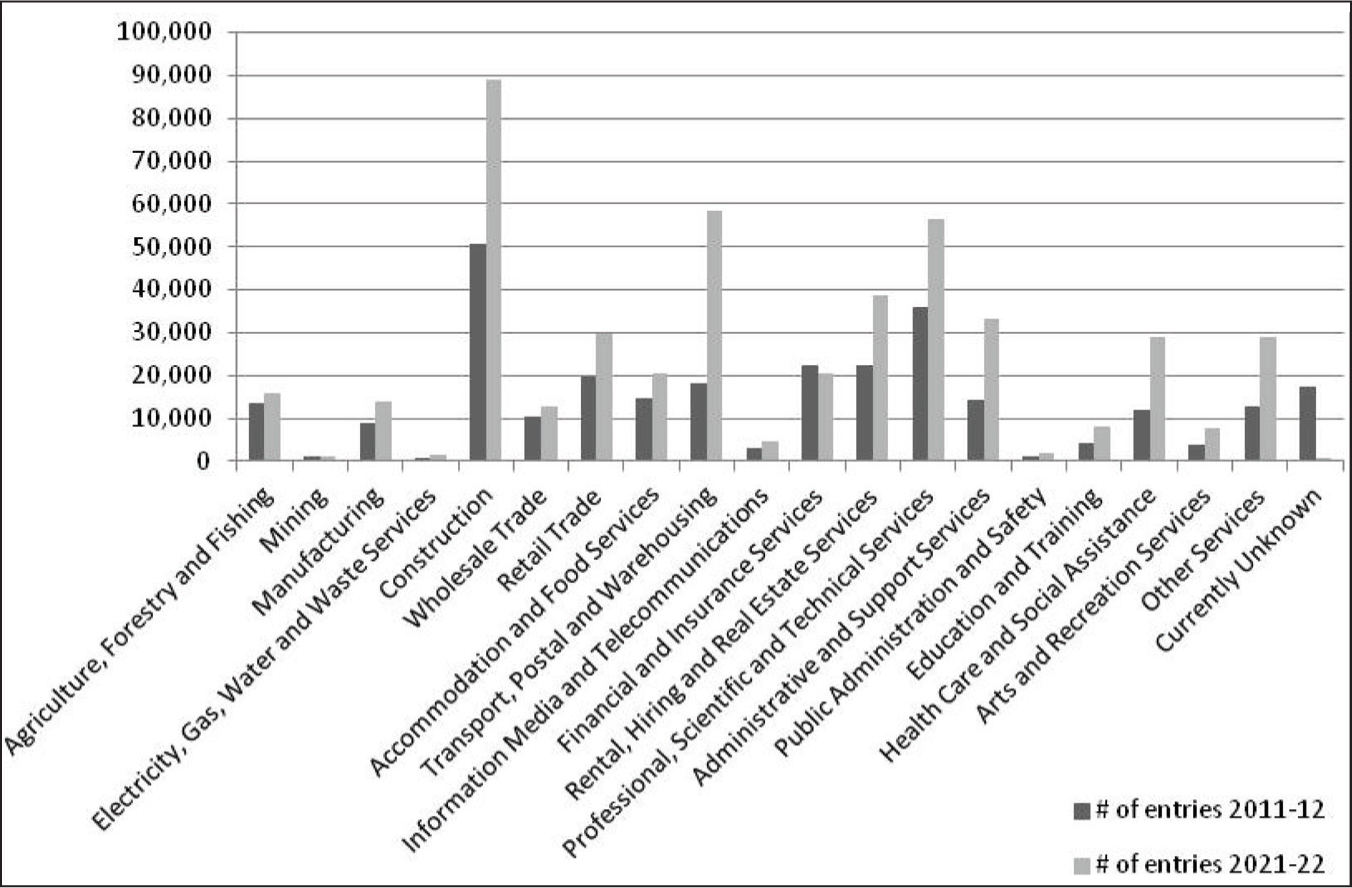

Definitions of ‘start-up’ vary significantly, as do methodologies to study them. This paper adopts the number of new establishments to measure the evolution of start-ups in Australia and finds a 39% growth between 2012 and 2022 (Australian Bureau of Statistics, 2022). While new establishments were roughly around 3% of all in 2012, they represented 6% of all businesses in 2022. The top three industries where the highest entries have been experienced were (1) Construction; (2) Transport, Postal, and Warehousing; and (3) Professional, Scientific, and Technical Services. As of 2021, these top three sectors’ contributions to the Australian GDP are 9%, 5%, and 11%, respectively (see Figure 2).

A few studies observe the growth of Australian start-ups in tech sector, which experienced a 58% growth between 2015 and 2018 (Startup Muster, 2018), a short period over which a consistent methodology was applied to study tech start-ups. The Tech Council of Australia (TAC) report (2022) argues that Australia has a similar share of global start-ups to its share of global GDP (1.7% and 1.6%, respectively). However, it finds out that the most salient start-ups seem to operate in the top five technology areas. These start-ups come from Mining Tech, where Australia has 8.2% of global start-ups, followed by Quantum Tech (3.2%), Lending Tech (3.4%), AgTech – Food Tech (2.8%), and Construction Tech (2.7%). Among these top technology areas, two are associated with Information Media and Telecommunication & Finance industries, while others are related to traditional Australian sectors: mining, agriculture, and construction.

Another measure of the growth of start-ups might be the number of ‘unicorns’, companies worth around $1.5 billion or more. In the last decade, Australia produced twenty-one unicorns, corresponding to a 2.2% share of global unicorns that exceeds Australia’s 1.6% global GDP (TCA, 2022). According to the TCA (2022), Australia has sixty-seven companies with a valuation of $100 million or greater, founded since 2010. Stock markets and VC firms have supported them. However, some of these unicorns moved their legal headquarters abroad, such as Atlassian, excluding them from the list of Australian unicorns. The most updated list indicates six companies and another potential seventeen companies (Australian Unicorn, 2022).

Another measure regarding the overall development of start-ups is funding. For example, the total market capitalisation of all Australian public technology start-ups was over $123 billion, experiencing over 320% increase from 2016 to 2021 (Cut Through and Folklore Ventures, 2021). Most of these public companies represent scale-up companies, the next phase of start-ups experiencing growth, such as Canva. However, this number shows the overall strength of entrepreneurial actors in the national market.

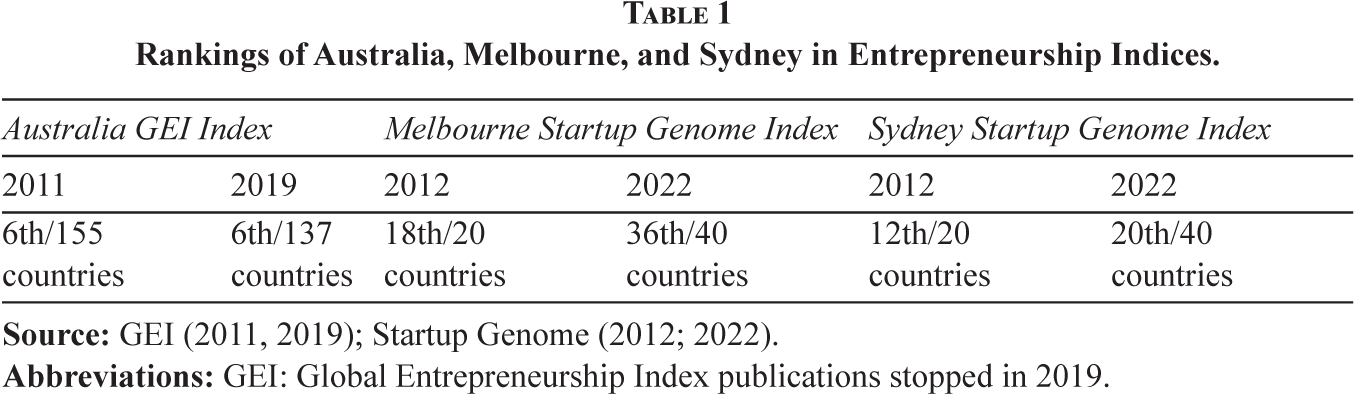

Regarding the international comparison, as shown in Table 1, the Australian start-up ecosystem is one of the top in the world, ranked number 6 globally (GEI, 2019). Australia has two cities in the top 40, where Sydney ranks 20th globally, followed by Melbourne at 36th.

Rankings of Australia, Melbourne, and Sydney in Entrepreneurship Indices.

Startup Muster (2018) data shows that New South Wales (NSW) is the start-up capital of Australia by holding half (49%) of all Australian start-up founders, followed by Queensland having 20% and Victoria hosting 13% of founders. This explains why, during the 2019–2022 period, Sydney has reached an ecosystem value equivalent to $68B (around 2.4 times the global average) and managed to raise early-stage funding of $1.3 billion (about 1.9 times of the global average) (Startup Genome, 2012; 2022). During the same period, Melbourne had an ecosystem valued at $17 billion, raising $816 million early-stage funding.

City-based regional ecosystems differ from each other. For example, Melbourne is a thriving hub for start-ups across several sub-sectors, including Life Sciences, SaaS, AI, Blockchain, Advanced Manufacturing, IoT, Big Data, and Fintech. Sydney, on the other hand, is strong in finance. According to the Startup Genome data (2012; 2022), Sydney is home to 60% of all 800 Australian Fintech start-ups, making Australia sixth in the world and second in Asia in Fintech. In addition, Sydney is a thriving innovation centre for renewable energy and Cleantech companies. With an estimated 35% annual growth rate, the renewable energy industry in NSW is expected to become the leading Australian state for clean energy production, decarbonisation, and halving emissions by 2030.

Universities

Australian universities are active stakeholders in the development of ecosystems, which adds to the inertia of creating an entrepreneurial culture and forging connections that improve start-ups’ funding and opportunities. Maritz et al. (2019) analyses forty higher education institutions in Australia concerning their entrepreneurship-related activities, ranging from offering courses to supplying accelerator services. Maritz et al. (2021) later find that ten universities represent nearly 60% of entrepreneurship education offerings and actively support student entrepreneurship through accelerators. Both studies conclude that leading entrepreneurial universities provide dynamic capabilities to regional economic development and student start-up support through active engagement in local or regional entrepreneurship ecosystems.

In Melbourne and Sydney, the role of universities has been pivotal in building city-level entrepreneurship activities that make them globally successful. For example, RMIT University has been ranked second in the world for research that has impacted the development of Blockchain technology through its Innovation Hub, the world’s first research centre focused on the social science of Blockchain (Startup Genome, 2012; 2022). This knowledge base resulted in many start-ups. Similarly, the University of Melbourne’s existence, incubator Melbourne Connect and Bio-Innovation Hub, and five of Australia’s largest medical research institutes have ranked Melbourne as one of the top 5 Life Sciences hubs in Asia-Pacific. The hub resulted in a few start-ups in the life sciences field, such as the regenerative medicine company, which raised $412.3 million in 2021.

Government agencies seem to be aware of this key role of universities; hence they include them in their policies. For example, in 2020, NSW launched the Tech Central project for technology companies and start-ups. NSW Government funds the project with an initial AU$48.2 million to facilitate collaboration among nearby institutions, namely the University of Sydney and the University of Technology Sydney, Royal Prince Alfred Hospital, and CSIRO’s Data61 research institute.

University spin-offs remain rare in Australia, with an official average of less than one start-up created by each Australian institution (Department of Industry, Science and Resources, 2020). A report (Tech Transfer Australia, 2021) concludes that between 2016 and 2021, publicly funded research organisations in Australia have achieved $1.2 billion in commercialisation deals, with 260 new companies created in Australia and 47 new companies created in New Zealand. Meanwhile alumni create hundreds of start-ups (Universities of Australia, 2019) that universities are quick to claim as ‘theirs’. This alumni pathway is why the university sector advocates for better recognition of the education link versus a spinoff link. Almost to illustrate this point, a recent newspaper article (Research Magazine, 2022) ranks universities in terms of the total number of start-ups by alumni, normalised per 100,000 students at that university in a decade. According to the list, the top 5 universities are UNSW, Bond, University of Sydney, UTS, and University of Melbourne. However, the Crunchbase database used in listing is limited to venture-backed start-ups, which are only a fraction of all start-ups. For example, it is known that both ResMed and Cochlear licensed core intellectual property from the UNSW. Nevertheless, these companies do not account as spin-offs.

Financial Institutions, Growth of Funding

Funding conditions for start-ups can be shaped by multiple policies beyond VC policy, including Tax incentives for angel investors, intangible asset depreciation, improvement of bankruptcy and insolvency laws, and alterations to the Employee Share Scheme and taxation of options issued or exercised.

As discussed in section ‘Support Organisations and Institutions’, the rapid rate of increase in incubators can be attributed partly to related policies. Examples of government incubator policies include (1) the federal NISA’s Incubator Support Program investing $22.5 million in over sixty-three accelerator programmes and $0.4 million in over 100 Entrepreneur-in-Residence programmes, (2) the South Australian Government’s $476.2 million investment over 5 years into the innovation hub Lot Fourteen, and (3) New South Wales government’s investment of $35 million into the Sydney Startup Hub and $18 million into incubator programmes at all eleven NSW-based universities through the Boosting Business Innovation Program.

Investment firms and programmes also increased in number, although the growth commenced around 2004 earlier than other actors. The Australian Government co-funded start-ups with VCs through different mechanisms, such as the Federal Government Early-Stage VC Limited Partnerships, Advanced Queensland’s $40 million Business Development Fund, and the female-founder-focused $10M Alice Anderson Fund.

The Australian Government provides around $2 billion annually to research agencies for R&D activities. For example, CSIRO is the largest Australian Government research agency among these research agencies, employing over 5,000 staff nationally and receiving a total funding of around $1.5 billion from the Australian Government and other sources. CSIRO is known globally for its invention of Wi-Fi (Mullin, 2012).

Final support for the financial needs of start-ups came from VC companies. When comparing a 3-year average change in VC investment amounts between 2015 and 2019 out of thirty-two OECD countries, Australia ranks 23 for the rate of increase and 19 for the per capita increase. In 2021, VC reached $10B, accounting for 0.6% of the GDP generated that year (Cut Through and Folklore Ventures, 2021). This amount has been exceptional in Australian history.

TAC report (2022) indicates that 85% of $29B of VC investment carried out during 2017–2021 was done in two technology areas: Business Software (involving B2B and B2C software) and Fintech. A smaller portion of the remaining VC within the tech sector has been invested in more specialised segments, such as Quantum Tech, Media/Design, and Energy Tech.

Artefacts of the Ecosystem

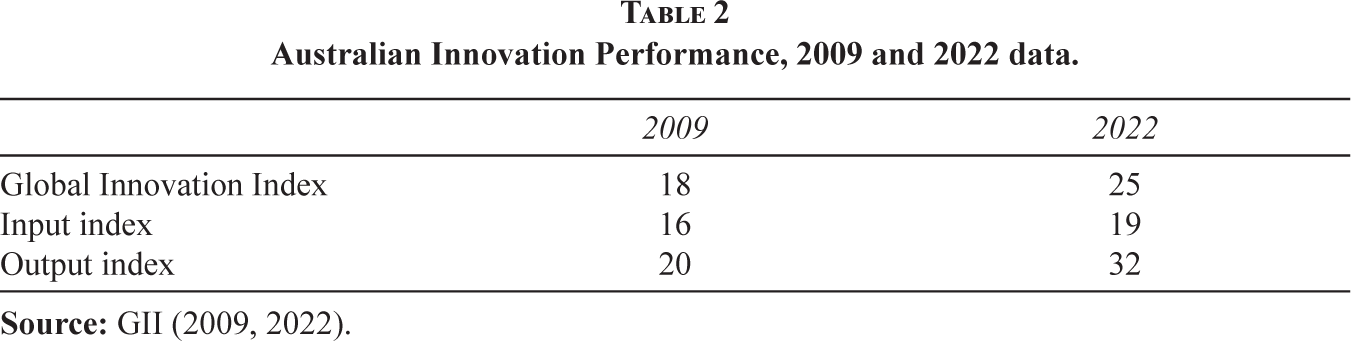

Artefacts encompass inputs and outputs (such as products and services) and resources (such as technological and non-technological resources). Regarding the input and outputs, we rely on the choice of the Australian Government, which used the Global Innovation Index’s (GII) methodology for its performance review of the Australian Innovation, Science, and Research System in 2016. Table 2 shows that Australia’ ranking has declined radically regarding its output. GII (2009 and 2022) report highlights how Australia is performing well above the average in knowledge creation, a critical output expected from an innovation system. However, it is unsuccessful in two output sub-indices: knowledge application and knowledge transfer activities.

Australian Innovation Performance, 2009 and 2022 data.

Concerning the final artefacts, namely resources, policies focused on the supply of three critical resources for innovation ecosystems: talent/skills, finance, and infrastructure. The Australian Government has been supporting talent supply through its skilled migration policies. For example, postgraduate research-qualified people with science, technology, engineering, mathematics (STEM), and IT qualifications are awarded extra points that allow them to stay in Australia after completing their studies. Australia also started the Entrepreneur Visa in 2022 to attract entrepreneurs on provisional visas. However, with skilled migrant visa paused due to the COVID-19 pandemic, the skilled labour shortage became a critical problem. Australia might consider a long-term national education programme to develop its local workforce to reduce its reliance on immigrant talent.

Regarding long-term educational needs, NISA clarified that digital literacy and STEM would be prioritised at schools. This goal is based on the estimation that 75% of future jobs will require expertise in STEM disciplines, while 90% will involve digital literacy. NISA policies increased the role of government-led organisations in innovation by contributing to the talent pool. For example, CSIRO (2015) has been positioned to be Australia’s ‘innovation catalyst’. Its ON Accelerator programme offers a range of accelerator services for researchers seeking to commercialise their research efforts, creating a more entrepreneurial culture among research staff across the publicly funded research sector.

National Innovation and Science Agenda’s support to finance is indirectly discussed in section ‘Universities’. Another strong support for resources came through the Australian Government’s infrastructure investments. The Australian Government committed to over $50B in infrastructure investment that includes: (1) increasing investment in road and rail; (2) promoting regional growth; (3) increasing economic growth; and (4) providing thousands of jobs throughout the country. The Federal Government also spent an additional $20.9 billion in equity funding on the National Broadband Network to overcome the imbalance between regional and urban access to data communications infrastructure.

The Australian Government has many industry-led initiatives to drive national innovation, strengthening infrastructures for particular products and services. For example, the Industry Growth Centres Initiative intends to drive excellence to help the country transition into high-value and export-focused industries (Department of Industry, Innovation, and Science, 2019). The initiative had a $250 million budget over the 4 years from 2016 to 2020, and it focused on Australia’s six industry sectors that are of competitive strength and strategic priority: Advanced Manufacturing; Cyber Security; Food and Agribusiness; Medical Technologies, and Pharmaceuticals; Mining Equipment, Technology, and Services; and Oil, Gas, and Energy Resources (Department of Industry, Innovation, and Science, 2019).

Activities of the Ecosystem

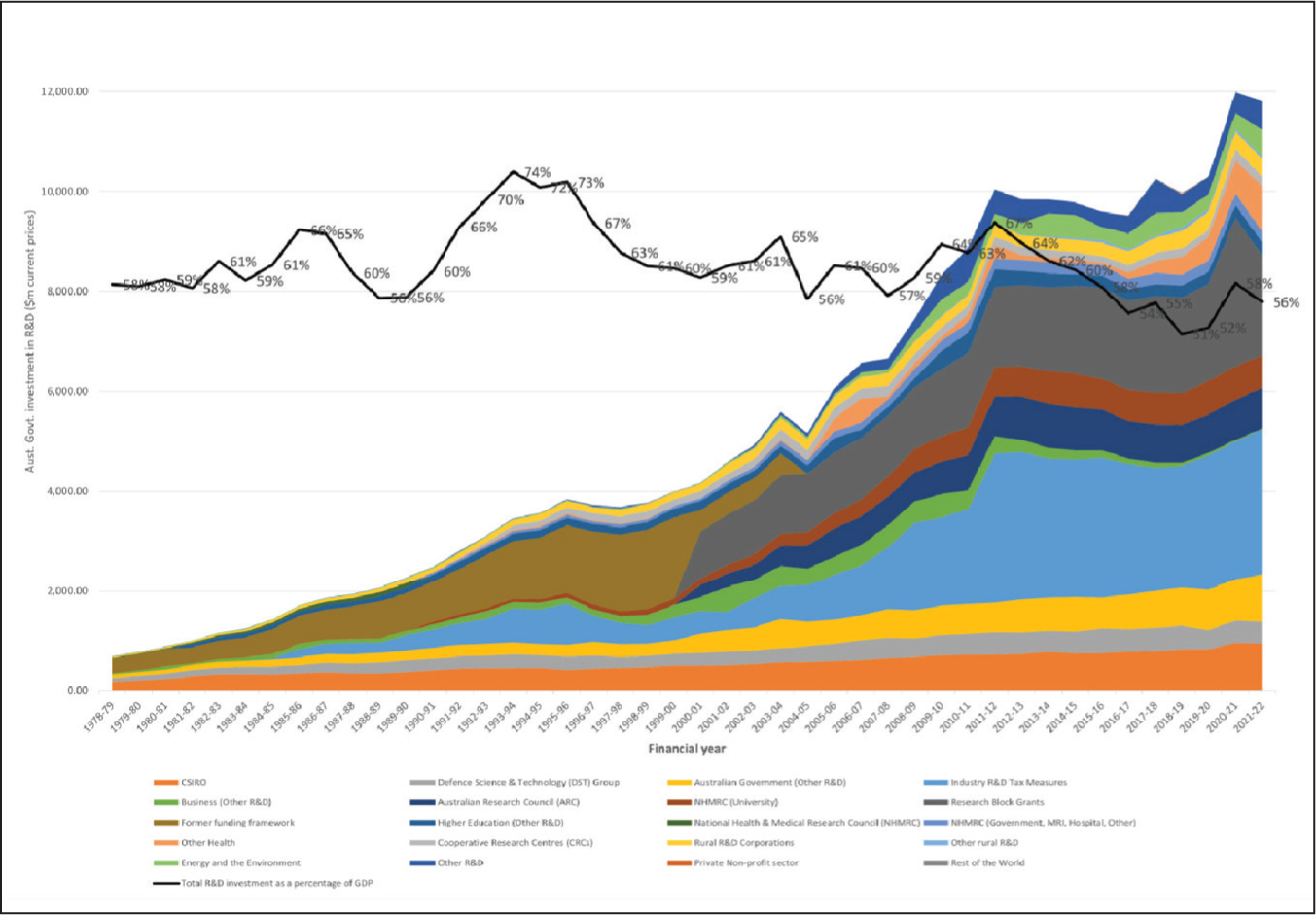

In this section, we focus mainly on R&D and collaboration activities. Australian investment in R&D as a percentage of GDP steadily decreased from 0.67% to 0.51% from 2011 to 2018 (Figure 3) (Department of Industry, Science, Energy and Resources, 2021). The trend sharply reversed in 2020 to increase to 0.58% as a result of increases across most sector categories, including a 53% increase in Research Block grants to universities amounting to an additional $1.035 billion.

Investment in R&D in Australia as a Percentage of GDP.

One effective policy for collaboration activities has been the establishment of Cooperative Research Centres (CRCs), industry-led research collaborations with universities, government, community, and other research organisations focused on a specific sector, demographic, geographic, or impact the outcome. Since the CRC programme launched in 1990, over 230 CRCs have been funded with $4.80 billion. A smaller-scale CRC Projects programme was released in 2015 for short-term collaborative projects between $100,000 and $3 million over 3 years. Many CRC research topics have place-based relevance, such as for specific sectors (i.e., agriculture) and geographic compositions (i.e., deserts). Yet, CRCs are not explicitly place-based except for the Northern territories CRC and the recurring Antarctic Climate and Ecosystems CRC.

Cooperative Research Centres provide economic, social, individual, environmental, infrastructure, and institutional benefits. For example, Australian CRCs contributed 0.3% of additional GDP growth per annum and generated a net economic benefit by a factor of 3.1 in 2012 (Dolan et al., 2019). CRCs also benefit supporting institutions, developing capacity and capability in participating universities by enhancing research quality, developing individual researchers, and brokering networks and collaborations.

For their benefit, CRCs also face sustainability and operational challenges. Factors contributing to CRC failure include unresolved internal and external competitive conflict, turnover of essential leadership, a lack of absorptive capacity in industry partners, and changing external environments impacting original agreements. Long-term sustainability without significant government funding is affected by structural friction from legal, economic, and relational mechanisms where transaction costs exceed participants’ value without subsidised government support (Sinnewe et al., 2016). The transaction cost makes the goal of a CRC over time to not only deliver on research outcomes but to develop strategies to replace or offset the government subsidy and reduce the friction inherent to the research collaboration. Moreover, while CRCs appear effective in delivering outcomes specific to the research mandate, they are perhaps not a mechanism to embed systemic and deep integration between academia and industry.

Policy Gaps, Challenges, and Enablers

Based on our analysis derived from Granstrand and Holgersson’s institutional framework, Australian policies have seemed to adopt an evolutionary national innovation system perspective with the NISA. Although these policies mention collaborations and initiate many programmes to support collaborations, it seems Australian innovation policies failed to build an integrated ecosystem of innovation and start-ups. George & Tarr (2021) points out that the ‘imbalanced’ level of single-firm R&D support increased from 66% in 2011 to around 92% of programmes encouraging business investment in innovation. Coupled with the new policies launched in the 2020s, emphasising industry ecosystems and non-R&D innovations might further weaken the establishment of a national innovation ecosystem.

Another concern is the recent shift towards targeting specific technologies and industries rather than the system. The need to intervene in market failure in these technologies and industries might not generate a healthy co-evolutionary change among all actors within an ecosystem. The ecosystem approach does not target but focuses on establishing an environment where independent actors can interact and change each other.

Based on the analysis in section ‘Analysing the Australian Start-up and Innovation Ecosystem’, our study identifies five significant policy gaps, as given below.

GAP 1: Lack of Data

While policy evaluations show the success of such programmes, there is a need for improved data in this area to ensure the efficiency and effectiveness of all Australian Government interventions. Data consistency has been a significant issue for policymakers, and a proposal for a detailed set of innovation metrics was published in 2019 (Department of Industry, Innovation, and Science, 2019). The ideal case is for a constant and reliable data source, rather than each evaluation study having to generate its primary data.

GAP 2: Lack of Overall Aggressive Goals

ISR System Review has painted a picture of Australia as an incremental innovator with generally low levels of new-to-market innovation. However, in 2020, IISA suggested a policy ‘rebalance’ towards non-R&D innovation. There seems to be uncertainty about whether Australia will focus more on disruptive innovation and move closer to the technological frontier. Besides, the total size of support for innovations seems not so impressive compared with some other aggressive innovating companies such as Singapore. A study compares NISA with the corresponding policy carried out by the Singaporean Government in 2016, nearly twenty times more than what the Australian Government intended to invest in innovation and research (Suseno & Standing, 2018).

Interestingly, a private think-tank initiative, the Tech Council of Australia, puts forward aggressive targets for the future and calls the government to change its policies. The Tech Council, established in 2021, consists of all sizes of companies in the tech sector, including financial supporters such as venture capitalists. For example, the Tech Council of Australia published a report in 2022 titled ‘Turning Australia into a regional tech hub’. The report sets goals of increasing the tech sector’s contribution of $250B to GDP by 2030 from its $167B in 2020.

GAP 3: Narrow Views of Growth Versus Inclusion of Sustainable Development Goal-based and Climate Change-oriented Goals

Many policy agendas are highly limiting due to their growth-based targets at all costs (Ben-Hafaïedh & Hamelin, 2022; Brown et al., 2017). Hence, numerous articles recommend that policymakers consider multiple dimensions of the value of ecosystems to develop balanced economic growth rather than focusing on growth alone (Autio & Rannikko, 2016; Hart et al., 2021). Drawing from the UN Sustainable Development Goals, we argue that the following five key themes that could help policymakers support a diverse portfolio of innovation ecosystems: (1) sustainable/social goals, (2) rural and regional goals, (3) indigenous-oriented goals, (4) women-oriented goals, and (5) refugee/migrant-oriented goals.

GAP 4: Lack of Integration Between National and State-level Innovation Policies

This paper focused mainly on national innovation policies; however, regional and state-level policies are introduced in parallel. As the reports of the Department of Innovation, Industry, Science, and Research (2011–2017) claim, these multilevel policies are not aligned across individual levels. Hence, they remain limited in taking advantage of opportunities at a large scale.

GAP 5: Lack of Collaboration and Interdisciplinary Approach

Although policies encourage collaboration among firms, the mechanisms for doing this are vague, as are the connections between features of the plan. As indicated in ecosystem activities, most resources dedicated to R&D seem to end up in individual firm efforts rather than multi-stakeholder collaborations. Further, the lack of an interdisciplinary approach might be a problem in the long term (Bliemel et al., forthcoming). Collaboration efforts such as CRCs do not prioritise a multidisciplinary approach. Further, policies focus mainly on STEM education instead of considering the holistic consideration of STEM and the humanities and creative subjects at school, thereby wholly overlooking the future-of-work reports that call for entrepreneurial and transversal capabilities.

Conclusion

This paper observes the evolution of national innovation ecosystems through the development of innovation policies. Based on Australian data, our observations highlight how the ecosystem approach could help policymakers to observe their impact on actors, activities, and artefacts.

As argued in the literature and our observations, the ecosystem approach could benefit policymakers to co-develop new, adapted, and targeted public policies that can improve their innovation performance. Thus, policymakers might start changing their mindset of making policies towards an ecosystem form of an organisation rather than relying on markets or hierarchies as indicated in the classical economics mindset. Our paper makes one of the early attempts to analyse policies adopted in a country that aims to tackle the innovation ecosystem comprehensively.

Empirically, our observations reveal five major gaps that need to be overcome for an ecosystem approach to flourish, such that the web of policies matches and supports the needs of the Australian ecosystem: (1) lack of data, (2) lack of aggressive or internationally competitive goals, (3) narrow views of growth, (4) lack of integration across levels in the system, and (5) a lack of collaboration beyond dyadic relationships.

Further, our paper reveals the difficulties of building an innovation ecosystem from an innovation system (Zheng & Cai, 2022). Even though a policy shift from a system approach towards an ecosystem approach in Australia since the 1990s, recent policy documents in the 2020s dilute the system approach with some interventionist policies targeting specific technologies and industries. But more importantly, current policies focusing on non-R&D innovations might jeopardise the Australian start-up ecosystem driven by R&D-based innovations, threatening the TCA’s vision of making Australia the tech hub.

Overall, the observations from the actors, artefacts, and activities of the Australian Innovation Ecosystem help to demonstrate its policy strengths and weaknesses. The major strengths of the policies are their help generating diverse actors such as CRCs and strengthening artefacts such as collaborative VC funds. The main weaknesses are in the activities segment of its innovation ecosystem. Even though policies are set for generating collaborative R&D projects other than individual company-based R&D efforts, they could not deliver a high level of collaborative results and failed to have innovation performance equivalent to Australian counterparts.

Considering that start-ups and entrepreneurial cities such as Sydney are competitive globally, policymakers need to strengthen weaknesses in the start-up and innovation ecosystem rather than changing the orientation of their policies from R&D to non-R&D innovations or abandoning their innovation ecosystems for the sake of industry ecosystems. The successes of Melbourne and Sydney as vivid entrepreneurial ecosystems at the city level underline how their state government’s investment in R&D and collaborations paid off. It is essential to learn from the experience of Cicada Innovations, the leading Australian incubator of deep tech founded by the UNSW, the UTS, and the University of Sydney, with the Australian National University joining soon after. The incubator’s CEO points out at its twentieth anniversary that success in creating economic and social value takes time in deep tech by giving the example of companies Cochlear, ResMed, and CSL Limited. These companies have transformed millions of lives through their products and have reached a valuation of $12 billion, $35 billion, and $127 billion, respectively, in 2020. Australian policymakers should remember that the deep tech giants are ‘30-year overnight successes’ (Alpha Beta, 2020). Hence, they need to be patient and support start-up and innovation activities in Australia.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.