Abstract

Purpose:

This study aims to understand how knowledge, awareness, regulatory changes, and perceived risk and return influence Gen Z’s decisions to invest in cryptocurrency. It focuses on young working professionals in Bengaluru and how these factors affect their financial well-being.

Data:

The study surveyed 398 Gen Z respondents in Bengaluru using a structured questionnaire. The target group included early-employed young professionals, providing insights into how this demographic engages with cryptocurrency investments.

Methodology:

The study used a mixed-methods approach. To analyze the data, exploratory factor analysis (EFA) and confirmatory factor analysis (CFA) were conducted using SPSS and AMOS software. These methods helped examine the relationships between key factors.

Findings:

The results show that knowledge and awareness have the strongest positive impact on financial inclusion. Regulatory clarity comes next, followed by how Gen Z perceives the risks and returns of crypto investments. Gender and marital status do not significantly affect investment decisions. However, financial literacy, clear regulations, and managing risk perceptions are essential to encouraging smart and responsible investing.

Originality:

This study focuses specifically on Gen Z in India, a group often influenced by social trends and digital tools offering insights not widely explored in existing research. It also emphasizes the need to consider behavioral and psychological elements in crypto adoption.

Implications:

To support Gen Z investors, there is a need for better financial education, more transparent regulations, and improved communication about investment risks. These steps can help increase participation in cryptocurrency markets while promoting responsible investment behavior.

Keywords

Introduction

Cryptocurrency is gaining popularity among Generation Z in India, but adoption remains cautious due to regulatory uncertainties, limited financial literacy, and mixed risk-return perceptions. This study examines how regulatory ambiguity, risk-return perceptions, and behavioral elements influence Gen Z’s cryptocurrency investment behavior, aiming to foster a safer, more informed, and inclusive market for young Indian Gen Z investors, especially in the context of cryptocurrency in India. A. Kala et al. (2023) found that young Indian investors are strongly influenced by the fear of missing out (FOMO), social pressure, and ease of use when deciding to invest in crypto. Building on this, Gupta et al. (2024) used a technology adoption model to show that Gen Z values platforms that are easy to use, useful, and socially approved. Similarly, Dugar and Madhavan (2023) observed that Gen Z is beginning to lean toward more formal investment options such as stocks and mutual funds, and their families and mobile apps play a big part in these decisions.

In smaller Indian cities, Panchasara and Bharadia (2024) found that social media heavily shapes Gen Z’s investment views, although many lack basic financial knowledge. Financial literacy remains an important factor, as Arriqoh and Zoraya (2023) revealed—Gen Z investors with limited knowledge often follow the crowd, leading to riskier decisions. Islam et al. (2023) added that Gen Z investors are more likely to invest if the experience feels enjoyable and they do not perceive it as too risky. The trust factor also plays a major role, as shown by Sharma et al. (2024), who found that perceived usefulness, ease of use, and trust in technology encourage crypto adoption.

Focusing on young Indian women, Joshi et al. (2023) noted that trust, awareness of risks, and familiarity with the technology significantly impact their crypto investment behavior. Sood et al. (2023) explored how behavioral biases such as overconfidence and trend-following affect Gen Z’s investment choices. Finally, Sharma et al. (2023), while focusing on millennials, highlighted similarities with Gen Z in that trust, education, and simplicity influence their decision to invest in cryptocurrency. Together, these studies offer a well-rounded picture of Gen Z investors in India, showing that their investment decisions are shaped by a mix of psychological, social, and technological factors, all within the complex regulatory environment of cryptocurrency.

Cryptocurrency is attracting growing interest worldwide, especially among Gen Z investors, but research on its adoption by this group in India is limited. Most studies emphasize global trends and regulations but overlook India’s unique socioeconomic factors, regulatory uncertainties, and cultural attitudes that particularly influence young investors. Additionally, there is little insight into how financial literacy and behavioral finance affect Gen Z’s cryptocurrency decisions. This research gap limits our understanding of how regulatory clarity, risk-return perceptions, and behavioral factors together shape Gen Z’s adoption of cryptocurrencies in India. This study aims to address this gap by exploring these key factors, helping policymakers develop safer frameworks and enabling financial educators to create targeted programs that support informed and responsible investment among Gen Z.

Literature Review

According to Petukhina et al. (2021), cryptocurrencies have gained popularity due to their high average returns and low correlations, making them an attractive investment for portfolio and risk management. As per Jagtiani et al. (2021), cryptocurrencies, including Bitcoin and Ethereum, are rapidly transforming the financial system. As of May 2020, over 4,000 cryptocurrencies existed. The potential for cryptocurrencies to replace central bank currencies, a cashless system, and regulatory changes are discussed. The use of distributed ledger technology, blockchain, and initial coin offerings are also discussed. Robba et al.’s (2024) study of 1,153 Italian consumers revealed six psychological profiles, with high financial literacy, risk tolerance, and self-efficacy being most likely to hold cryptocurrencies, while low literacy and risk appetite are associated with past ownership. Cumming et al. (2024) examine the risk-return trade-off in international cryptocurrency market regulation from 2018 to 2023. They reveal that strong enforcement quality amplifies regulations’ intended effects, particularly for financial regulators and liquid tokens. The study also finds that cultural uncertainty avoidance amplifies regulation’s intended effects. Wang’s (2024) study reveals UK cryptocurrency investors lack diversification, prefer high-risk investments, and share similarities with gambling behaviors. It calls for tailored financial education and a holistic regulatory approach to improve understanding of cryptocurrency investments. Alganb and Alshahrani (2023) investigate trust in cryptocurrencies as investment options among investors and their relationship with knowledge management. They seek to understand current perceptions and attitudes toward cryptocurrencies and how effective knowledge management can influence these perceptions. Nuhiu et al. (2023) examine the risk-return trade-offs of cryptocurrencies based on portfolio diversification techniques. Three portfolios were created from 2016 to 2022, analyzing daily prices and trade volume. Results show that a portfolio with 10 cryptocurrencies offers better optimization, generating the same returns with lower risk. The year 2018 represents the maximum diversification benefits, indicating potential benefits for both crypto and institutional investors. Veerasingam and Teoh (2023) investigate factors affecting cryptocurrency investment decisions among potential investors in Malaysia, an Islamic country. Data from 200 individuals aged 18 and over were collected. Results showed that attitude toward risk and perceived behavioral control positively affect cryptocurrency investment decisions. Machine learning forecasting also enhanced the relationship between perceived benefits and investment decisions. Chittineni (2022) explores factors influencing retail investors’ decision to add crypto assets to their portfolios, using personality theory and innovation diffusion theory. Results show that familiarity with the asset, trust, risk and return profile, and perceived security influences purchase intentions. Innovativeness mediates these relationships but has no significant impact on familiarity or risk and return consciousness. Kaur et al. (2024) investigate the impact of herding, loss aversion, overconfidence, and FOMO biases on crypto investors’ investment decisions. Data from 473 respondents were gathered through a questionnaire survey. FOMO bias mediates the relationship between herding, loss aversion, and crypto investors’ decision-making behavior.

Knowledge and Awareness of Cryptocurrency

A significant barrier to cryptocurrency adoption is a lack of understanding among potential investors (Aya et al., 2024). Many individuals invest without adequate knowledge (Hadan et al., 2024), highlighting a critical need for effective financial education. Studies have shown a strong positive correlation between cryptocurrency knowledge and investment behavior (Aya et al., 2024), emphasizing the importance of financial literacy in fostering informed and responsible participation in cryptocurrency markets. Aya et al.’s (2024) research specifically points to the need for policies that address perceived risk factors and improve financial literacy among younger generations. This aligns with findings from other studies showing that increased knowledge positively impacts investment intention, particularly regarding specific cryptocurrencies like Axuscoin (Malik et al., 2023). However, the level of awareness and participation varies significantly across demographics and geographic locations. For instance, a study focusing on young Indians revealed that facilitating conditions, social influence, effort expectancy, and price value significantly influence cryptocurrency adoption intention (A. Kala et al., 2023), while perceived risk surprisingly does not play a significant role in this specific study. Further research is needed to understand the nuances of knowledge acquisition and its impact across different investor profiles. The study by Kamau (2022) on Kenyan youth highlights the need for both local and international regulation to boost investor confidence and improve security in the cryptocurrency market. This points to a critical gap: while knowledge is crucial, its impact is modulated by external factors such as regulatory environments and societal trust in the cryptocurrency market.

The existing research also highlights a gap in understanding how different educational approaches might influence knowledge acquisition. While using game design elements has shown promise in other educational contexts (Hadan et al., 2024), further research is necessary to evaluate their effectiveness in improving cryptocurrency literacy. Hadan et al.’s (2024) study on gamification and gaming in cryptocurrency education, for instance, suggests a need for dynamic, accessible, reliable, and community-building interventions but does not provide concrete evidence of their success. Similarly, while studies like Chittineni’s (2022) explore factors influencing retail investors’ purchase intentions, they do not directly address the effectiveness of different educational interventions. This creates a need for more studies that compare different educational methods and assess their impact on investors’ knowledge and decision-making processes. The role of social media in disseminating information also requires further investigation. While platforms like Twitter can be used to promote cryptocurrencies (Ardia & Bluteau, 2024), they also contribute to the spread of misinformation and potentially harmful investment strategies. Understanding how to leverage social media for effective education while mitigating its potential negative aspects remains a significant challenge.

Regulatory Changes and Cryptocurrency Investing

The cryptocurrency market is significantly influenced by regulatory changes (Borri & Shakhnov, 2019; Zhyvko et al., 2023). Zhyvko et al.’s (2023) research shows that global economic and military-political crises often lead to increased interest in cryptocurrencies as a safe haven for capital but also highlights the significant price fluctuations during such crises, underscoring the inherent risks. This volatility is further exacerbated by varying regulatory approaches across countries (Kondrat et al., 2020), ranging from absolute prohibition to permissive frameworks. Kondrat et al.’s (2020) analysis of the Ukrainian cryptocurrency market exemplifies this uncertainty. The absence of a clear legal status in many jurisdictions creates uncertainty for investors and hinders the development of a stable market. Furthermore, the study by Borri and Shakhnov (2019) demonstrates the significant international spillovers resulting from domestic regulatory changes, illustrating the interconnectedness of global cryptocurrency markets. Their research highlights the impact of a regulatory change in China on trading volume in other markets, indicating that regulatory actions in one jurisdiction can have profound consequences elsewhere.

The impact of regulation extends beyond trading volume and price volatility. Regulatory uncertainty can affect investor confidence (Kamau, 2022), potentially hindering investment and market development. The lack of clear regulatory frameworks also opens the door to illicit activities (Kondrat et al., 2020; Trozze et al., 2022), such as money laundering and tax evasion, creating further challenges for market stability and investor protection. Trozze et al.’s (2022) comprehensive review of cryptocurrency fraud highlights the variety of scams and the need for better collaboration between sectors to address these issues. The study emphasizes the evolving nature of cryptocurrency-related fraud and the need for proactive measures to protect investors. The development of national cryptocurrencies, as noted by Pantielieieva et al. (2019), represents another significant regulatory development, potentially reshaping the landscape of international finance. However, the long-term effects of these regulatory shifts on market dynamics and investor behavior remain largely unclear, necessitating further research. The interplay between regulatory frameworks and technological innovation also needs to be explored more comprehensively. The rapid evolution of cryptocurrency technology often outpaces regulatory efforts, creating a constant state of flux and uncertainty. Further research is needed to understand how regulatory frameworks can adapt to this dynamic environment while effectively protecting investors and maintaining market integrity.

Perceived Risk and Return in Cryptocurrency Investment

The high risk–high return characteristic of cryptocurrencies is a central driver of investment decisions (Ng et al., 2023). Ng et al.’s (2023) research, utilizing the theory of planned behavior, demonstrates that attitude, perceived behavioral control, and subjective norms are key drivers of cryptocurrency investment decisions, while perceived risk surprisingly did not significantly affect behavioral intention in their study. However, other studies have shown that perceived risk is a major barrier to cryptocurrency adoption (Aya et al., 2024; Huang et al., 2022). Huang et al.’s (2022) research, using a dilemmatic dual-factor model, highlights financial, legal, and operational risks as critical factors increasing users’ perceived risk. They also found that perceived benefit can mitigate the impact of perceived risk on discontinuance usage intention. This indicates a complex interplay between risk perception, benefit anticipation, and investment decisions. This aligns with the findings of Malik et al. (2023), who found that perceived risk positively influenced the intention to reinvest in Axuscoin, suggesting that risk tolerance may be a significant factor for some investors.

The perception of risk is not uniform across investors. Risk tolerance levels vary considerably (Aya et al., 2024), influencing how individuals assess and respond to potential losses. The role of FOMO also adds another layer of complexity (A. Kala et al., 2023). D. Kala et al.’s (2023) study on young Indian investors highlights FOMO as a mediator between adoption intention and investment behavior, suggesting that emotional factors can significantly impact investment decisions even in the face of perceived risk. Furthermore, the perceived security of the investment platform and the asset itself plays a crucial role in shaping investor confidence (Chittineni, 2022). Chittineni’s study (2022) emphasizes the importance of trust and perceived security in influencing retail investors’ purchase intentions. This underscores the need for secure platforms and transparent information disclosure to build investor confidence and mitigate risk aversion.

The interplay between perceived risk and return is further complicated by market volatility (Tanos & Badr, 2024; Ullah et al., 2022; Zhyvko et al., 2023). The high volatility of cryptocurrency prices makes it difficult to assess the true value of an asset and increases the risk of significant losses (Zhyvko et al., 2023). Abou Tanos and Badr’s (2024) study on price delay and market efficiency highlights the impact of liquidity and volatility on price delays, suggesting that increased illiquidity can lead to increased market inefficiencies (Tanos & Badr, 2024). This volatility is also influenced by external factors such as macroeconomic news, regulation and hacking incidents (Lycsa et al., 2020), and celebrity endorsements (Ullah et al., 2022). Lycsa et al.’s (2020) research indicates that positive investor sentiment regarding regulation and attacks on cryptocurrency exchanges significantly impacts bitcoin volatility, while macroeconomic announcements have less influence. Ullah et al.’s (2022) study found that positive tweets about Bitcoin are positively associated with price volatility, demonstrating the influence of social media sentiment. The dynamic interplay between these factors necessitates a nuanced understanding of risk and return in the cryptocurrency market, going beyond simple risk-return models. Further research is needed to explore the temporal dynamics of risk perception and its interaction with market sentiment and external events. This includes investigating how investors adjust their risk tolerance and investment strategies in response to market fluctuations and regulatory changes.

The cryptocurrency investment landscape is characterized by a complex interplay of knowledge, regulation, and risk perception. While increased knowledge and awareness are crucial for informed investment decisions (Aya et al., 2024; Chittineni, 2022; Malik et al., 2023), regulatory uncertainty and market volatility create significant challenges (Borri & Shakhnov, 2019; Tanos & Badr, 2024; Zhyvko et al., 2023). The perception of risk, influenced by individual risk tolerance, FOMO, and trust in the investment platform, plays a central role in shaping investment behavior (Aya et al., 2024; Huang et al., 2022; A. Kala et al., 2023; D. Kala et al., 2023; Ng, 2023). However, the existing research reveals several significant gaps. Further research is needed to explore the effectiveness of various educational interventions in enhancing cryptocurrency literacy (Hadan et al., 2024), the long-term impacts of regulatory changes on market dynamics and investor behavior, and the nuanced interplay between risk perception, market sentiment, and external events. This research should incorporate diverse methodologies, including qualitative approaches to capture the perspectives and experiences of a wide range of investors. A more complete understanding of these factors is essential for fostering a more informed, secure, and sustainable cryptocurrency market. The development of more sophisticated models that account for the complex interactions between these factors is crucial for both investors and policymakers. These models should consider not only the economic factors but also the psychological and social aspects that influence investment decisions. This multidisciplinary approach will contribute to creating a more robust and resilient cryptocurrency ecosystem.

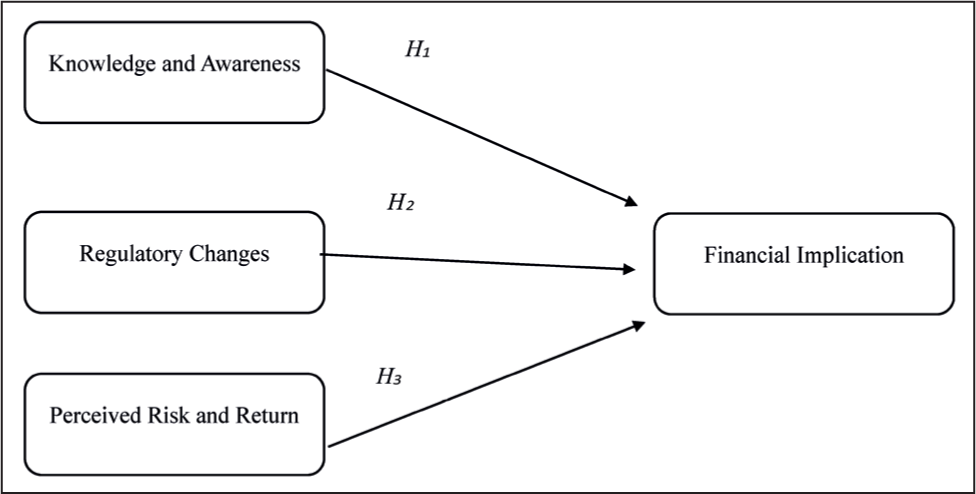

Hypotheses Developed

Nabilou (2020) explored the regulatory challenges posed by cryptocurrencies. The study emphasizes that understanding cryptocurrency’s financial implications is tied to regulatory frameworks and investor awareness, affecting the risk and opportunity perception of investments. This regulatory understanding significantly influences financial decision-making in cryptocurrency markets. Feng et al. (2023) investigated how financial literacy and risk tolerance impact cryptocurrency adoption. The study concluded that heightened awareness and knowledge enhance the ability to manage cryptocurrency investments effectively, reducing uncertainty and supporting financial growth. Bonsu and Dhital (2022) examined the role of financial education in driving cryptocurrency investment in developing markets. Findings showed that informed individuals are more likely to engage in cryptocurrency markets responsibly, utilizing knowledge to navigate volatile conditions. Kumari et al. (2023) analyzed how technology awareness and financial literacy influence cryptocurrency adoption using the UTAUT2 model. Their research highlighted the positive moderating role of awareness in shaping behavioral intentions, bridging knowledge gaps, and improving financial decision-making in crypto investments.

H1: Knowledge and awareness regarding cryptocurrency have a significant positive impact on the financial implication on investing in cryptocurrency.

Rejeb et al. (2020) examine the evolution of cryptocurrencies, emphasizing their potential for financial inclusion, lower transaction costs, and diversification benefits. They also highlight the challenges posed by regulatory uncertainty, volatility, and security concerns. The study underscores how clear regulatory frameworks could enhance the integration of crypto assets into traditional financial systems, promoting investor confidence. Giudici et al. (2020) investigate the socioeconomic impacts of cryptocurrency regulations and explore their behavioral finance perspectives. They emphasize that regulatory clarity fosters market stability and enhances investor confidence, mitigating risks associated with fraud and volatility. Hennelly’s (2022) study provides a comparative analysis of regulatory approaches in the United States., United Kingdom, and European Union. It discusses how regulations like the SEC’s guidelines and the classification of digital assets influence investor behavior, addressing the challenges posed by fragmented policies and their effects on financial stability and market growth. Auer et al. (2020) explores how central bank digital currencies (CBDCs) and regulatory frameworks affect the financial implications of cryptocurrencies. The study concludes that robust regulation can reduce systemic risks while supporting the innovative potential of cryptocurrencies in financial markets.

H2: Regulatory changes relating to crypto have a significant positive impact on the financial implication on investing in cryptocurrency.

Sukumaran et al. (2022) explored Malaysian investors’ perceptions of cryptocurrency, focusing on the roles of perceived risk and value in adoption. Using a sample of 211 respondents and structural equation modeling (PLS-SEM), it found that perceived value significantly influenced adoption, while perceived risk did not. The findings provide insights into the risk-return dynamics within a regulated cryptocurrency market. Sami and Abdallah (2022) investigated the cryptocurrency market’s impact on African firms’ market value. Findings showed that sectors with low returns (industrial, energy, financial) were negatively affected by cryptocurrency volatility, while high-return sectors (real estate and IT) showed resilience. The study highlights the financial risks linked to cryptocurrency adoption in varying economic conditions. Fischer and Sandner (2021) examined the financial stability challenges posed by cryptocurrencies. It found that while high returns attract investors, extreme price volatility increases perceived risk, leading to unstable financial implications. It underscores the necessity of regulatory measures to balance risks and returns in the crypto market. Yu et al. (2021) investigated behavioral finance principles in cryptocurrency trading, revealing that perceived risk significantly influenced investment decisions. It found that higher perceived risk dampened trading volumes, even when returns were promising. These insights emphasize the psychological aspects of financial implications in crypto investments.

H3: Perceived risk and return on cryptocurrency have a significant positive impact on the financial implication on investing in cryptocurrency.

Conceptual Framework

Methodology

A structured questionnaire was employed as the primary tool for data collection in this study. The questionnaire was divided into two sections: the first section gathered demographic details of the respondents, while the second section used a 5-point Likert scale to assess various factors such as knowledge and awareness, regulatory changes, and perceived risk and return regarding cryptocurrency investments and their financial impact. This approach allowed for a detailed exploration of the factors influencing the financial behavior of Gen Z investors. The survey targeted early-employed professionals in Bengaluru, ensuring that the findings are representative of this specific demographic group, which is particularly active in the cryptocurrency market.

Data Analysis

The data for this study were collected to examine the impact of knowledge and awareness, regulatory changes, and perceived risk and return on cryptocurrency investments and their implications on the financial well-being of Gen Z investors. The focus of the study was on early-employed professionals working in Bengaluru, who are more engaged in cryptocurrency investments compared to other financial instruments. A cross-sectional study was conducted using simple random sampling, and the final sample size consisted of 398 respondents. The data collected were entered into SPSS for reliability checks, normality tests, and the identification of any outliers. To organize and reduce the complexity of the data, exploratory factor analysis (EFA) was performed using SPSS, helping to group the indicators into distinct factors. Confirmatory factor analysis (CFA) and structural equation modeling (SEM) were then applied through AMOS to validate the relationships between the variables and construct the final model.

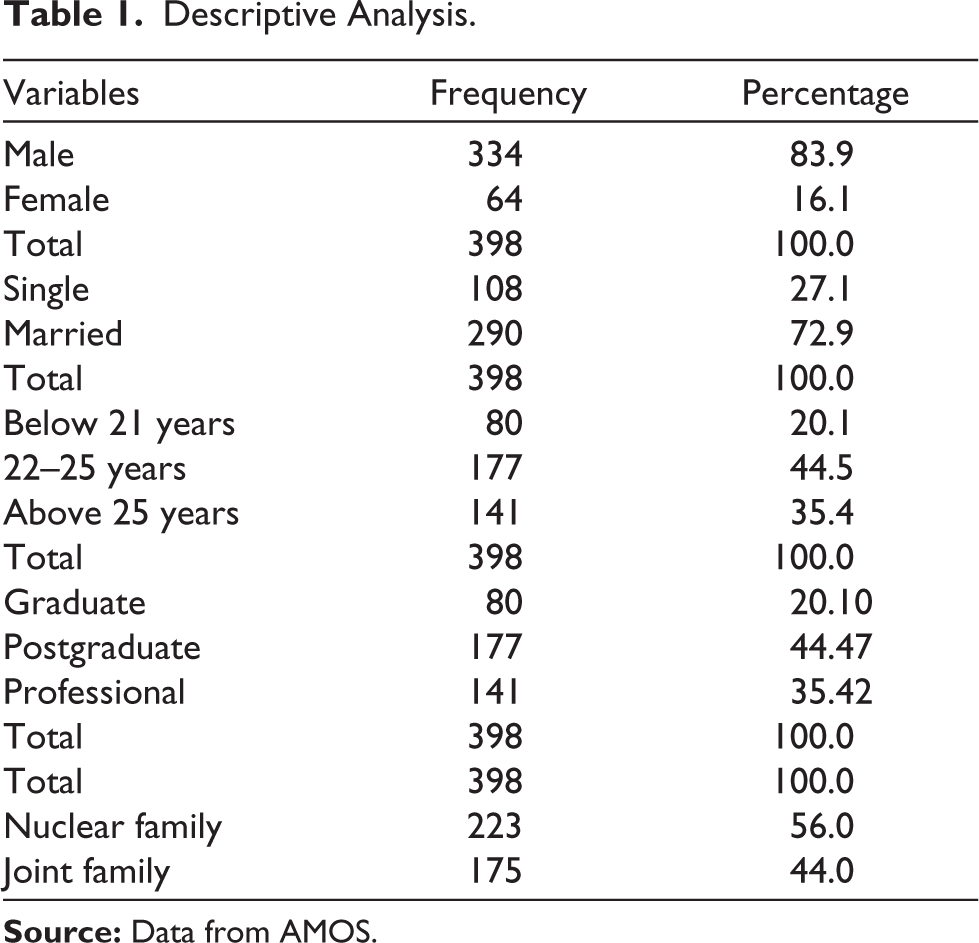

In Table 1, demographic characteristics of the respondents are highlighted by the data. Among 398 participants, 83.9% are male and 16.1% female, and their result shows that males are more dominant in this study. In terms of marital status, 72.9% are married, while 27.1% are single, thus indicating the majority who are family bound. The age distribution shows that the highest proportion is 44.5% aged between 22 and 25 years, followed by 35.4% above 25 years and 20.1% below 21 years, which suggests that young adults make up the largest proportion of the sample. The educational qualifications also show that 44.47% are postgraduates, 35.42% have professional qualifications, and 20.1% are graduates, which makes the sample very highly educated. Furthermore, 56% of the respondents have nuclear families, and 44% live in a joint family setting, which indicates balanced representation of family structures with a slight preference toward nuclear setups. In all, the statistics depict an active, basically male-dominated, married population, which is well-educated and predominantly young adults, revealing their demographic and socio-educational background.

Descriptive Analysis.

Chi-square Analysis

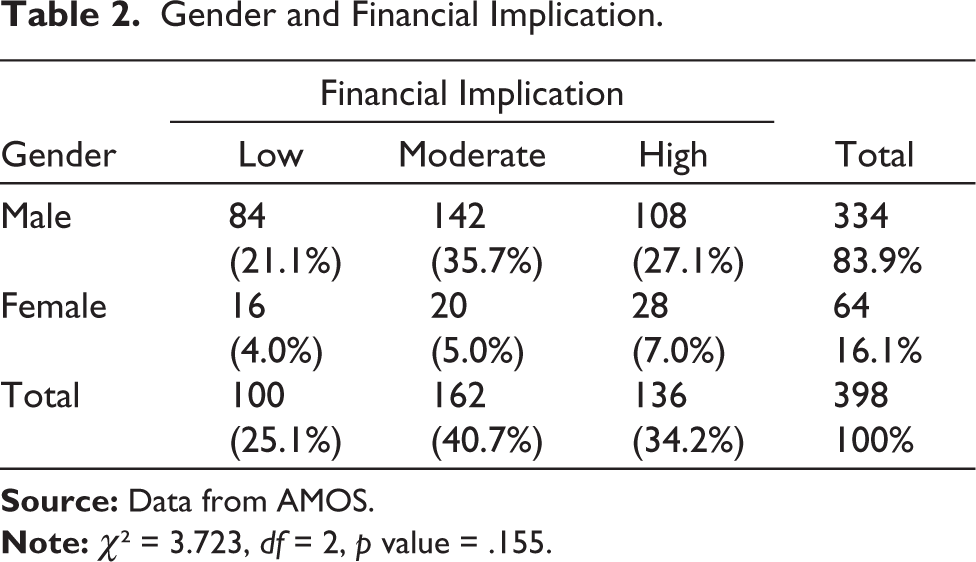

H4: There is no significant association between gender and financial implication.

Table 2 displays the counts of the distribution of the financial importance levels according to gender.

Gender and Financial Implication.

Table 2 shows that chi-square test result for Pearson chi-square is .155, which is more than .05. This means there is no relationship at the 5% significant level between gender and financial importance. Thus, H4 is supported, and a conclusion can be made that there is no statistically significant relationship between gender and the level of financial importance among the respondents.

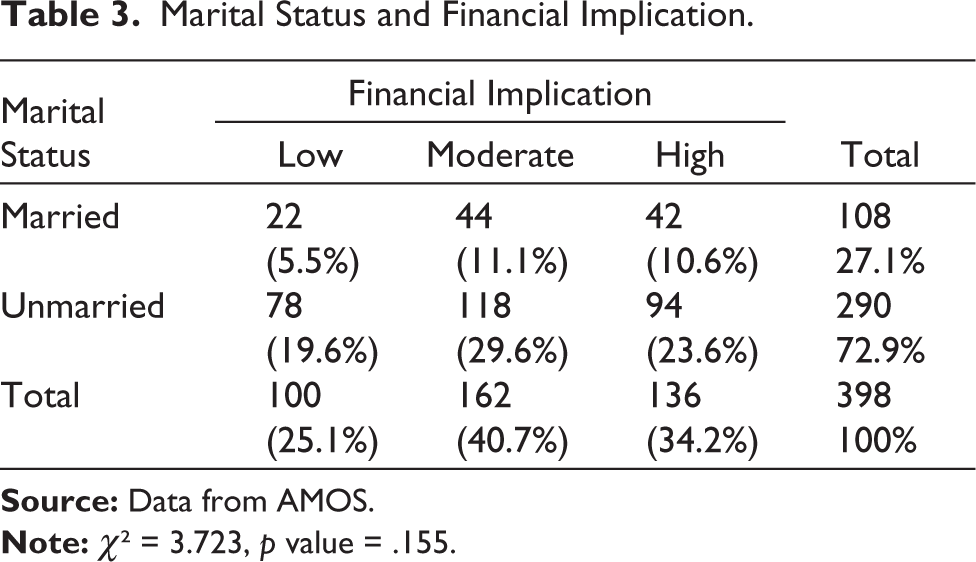

H5: There is no significant association between marital status and financial implication (FINIMP).

Table 3 provides the distribution of financial importance levels based on marital status.

Marital Status and Financial Implication.

In Table 3, the chi-square test shows that the marital status and the financial importance were not significantly related at the 5% level of significance (p = .155 for Pearson chi-square). Therefore, H5 was supported, meaning that marital status does not play a significant role in financial importance among the respondents.

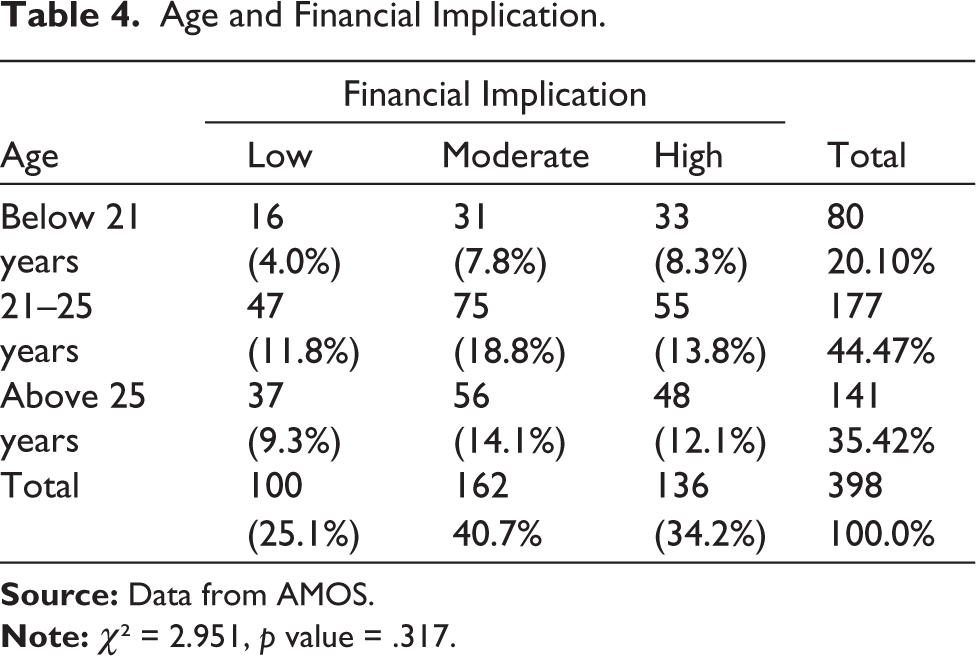

H6: There is no significant association between age and financial implication (FINIMP).

Table 4 provides the distribution of financial implication levels across different age groups.

Age and Financial Implication.

In Table 4, chi-square test results show that there is no significant association between age and financial implication at the 5% level of significance (p = .317 for Pearson chi-square).

Hence, H6 is supported, and it can be concluded that age does not significantly influence financial implication among the respondents.

Supplementary Analysis

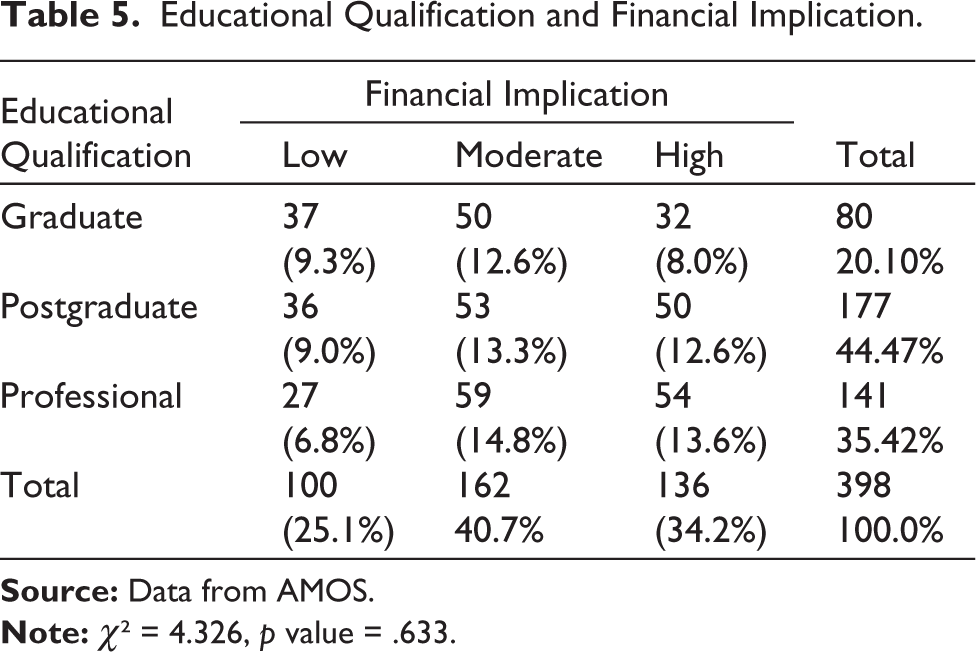

H7: There is no significant association between educational qualification and financial implication (FINIMP).

Table 5 provides the distribution of financial implication levels across different educational qualifications.

In Table 5, chi-square test results show that there is no significant association between educational status and financial implication at the 5% level of significance (p = .633 for Pearson chi-square).

Educational Qualification and Financial Implication.

Hence, H7 is supported, and it can be concluded that educational qualification does not significantly influence financial implication among the respondents.

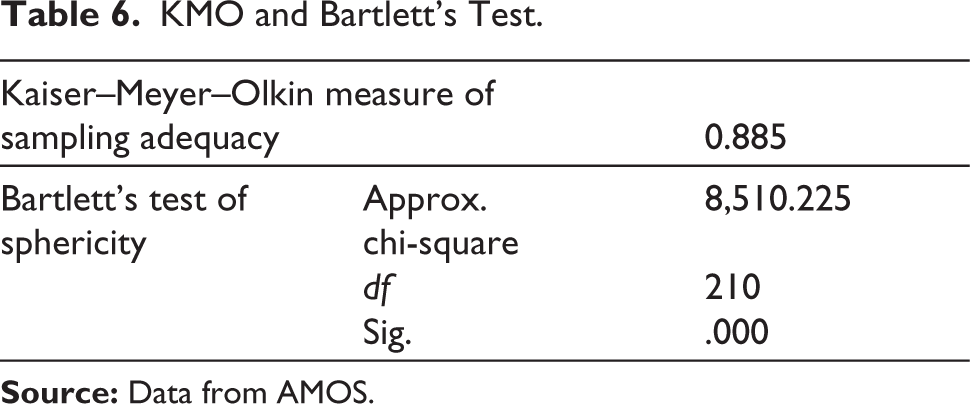

Table 6 indicates the Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy is 0.885, which further indicates that the data are adequate for further analysis. And the chi-square value of Bartlett’s test of sphericity (chi-square = 8,510.225, df = 210, sig. = .000) shows that it is not an identity matrix, and thus, the factor analysis can be carried out with the available dataset.

KMO and Bartlett’s Test.

KA, knowledge and awareness; RC, regulatory changes; PRR, perceived risk and return; FI, financial implication.

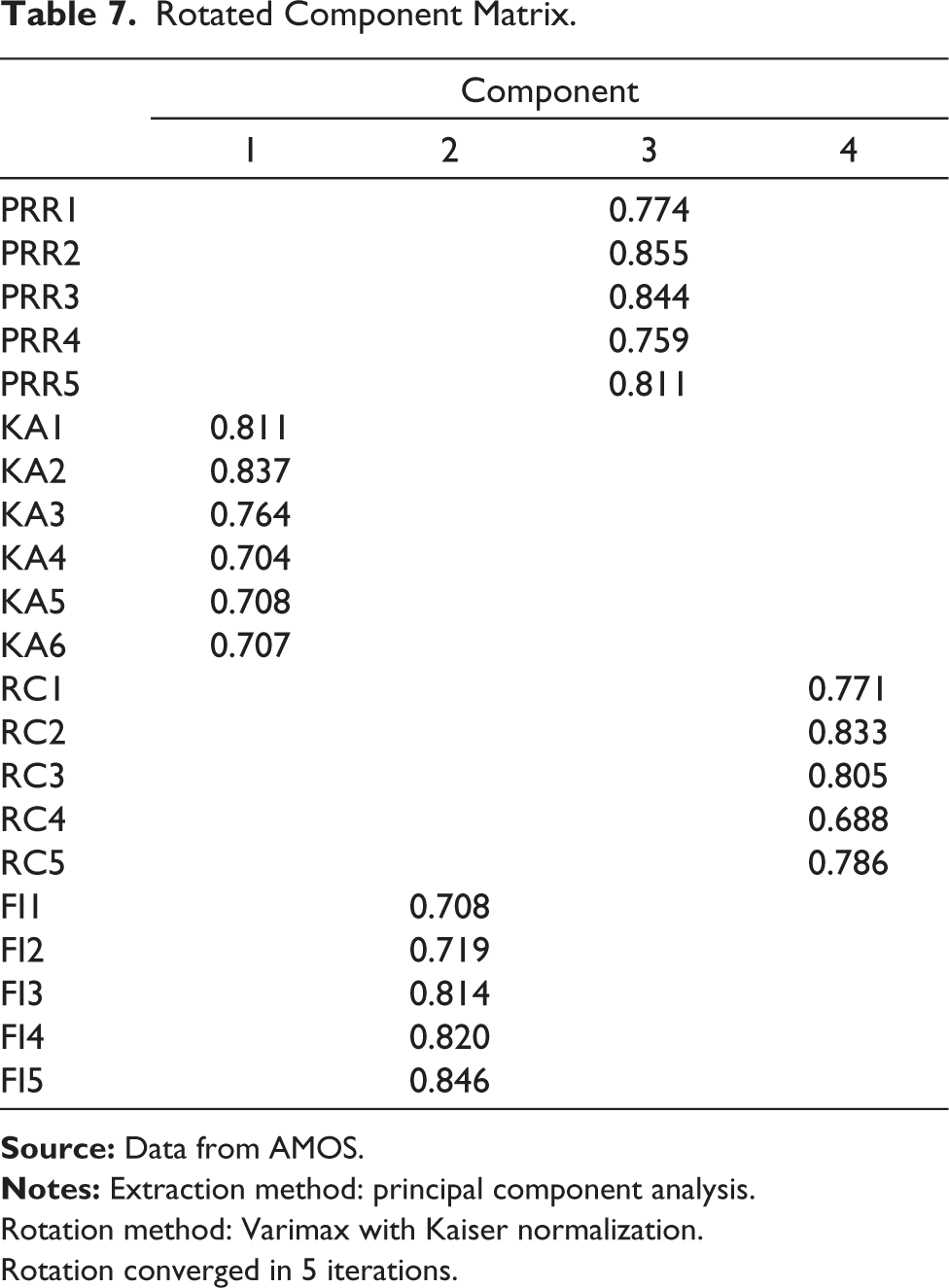

Table 7 indicates the rotated component matrix, which extracted the indicators with eigen value more than 1, with varimax rotation with Kaiser normalization that brings the different factors out of the given dataset; the first factor is perceived risk and return, with indicators including PRR1, PRR2, PRR3, PRR4, and PRR5; the second factor is knowledge and awareness, with factor loadings ranging from 0.707 to 0.837, indicating a good association of factors; the third factor that was captured is regulatory changes, with factor loadings from 0.688 to 0.833, with strong loading of factors; and the last factor is financial implication, with factor loadings from 0.702 to 0.820.

Rotated Component Matrix.

Rotation method: Varimax with Kaiser normalization.

Rotation converged in 5 iterations.

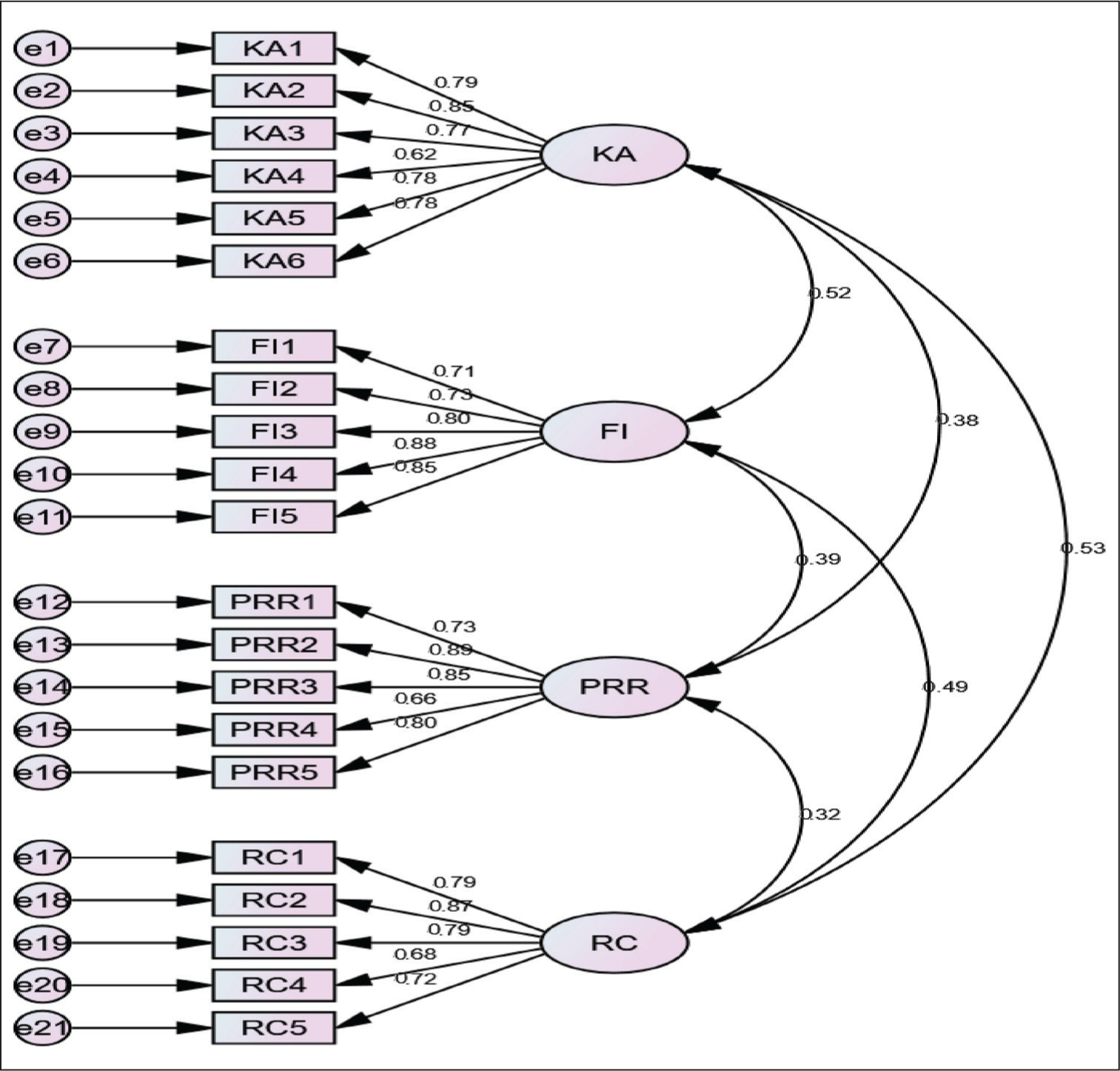

Figure 1 shows confirmatory factor analysis, which tests the relationship between the factors. SEM CFA results declared a good model fit, thus carried with SEM, which enables to study the impact and influence of a complex structure. The CFA model shows the correlation between KA and FI is 0.52, between KA and PRR is 0.38, between KA and RC is 0.53, and between FI and PRR is 0.39; the relationship between FI and RC is 0.49, and the correlation between KA and RC is 0.53.

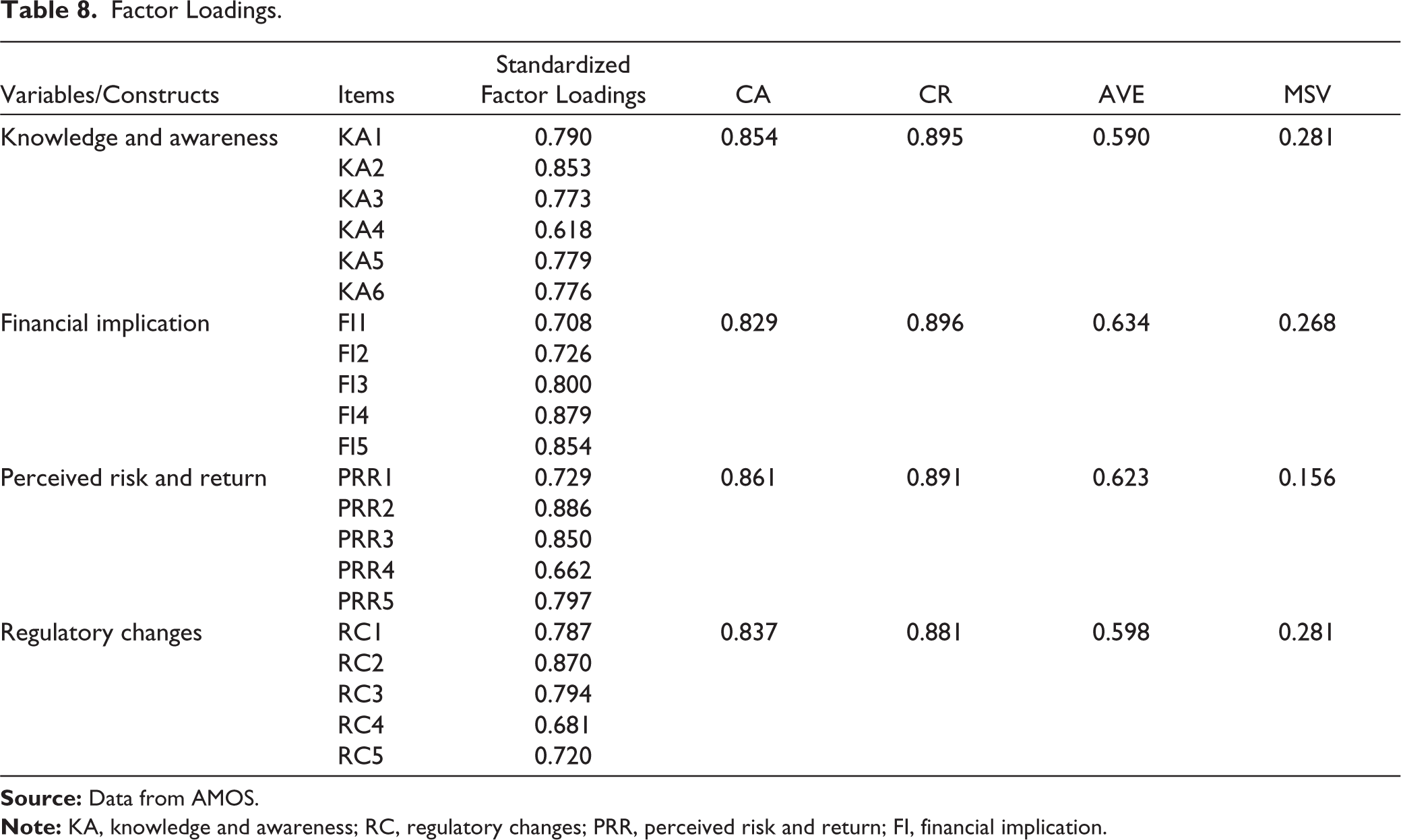

Table 8 shows that the knowledge and awareness construct with factor loadings 0.618–0.853, financial implication with factor loadings 0.708–0.879, the factor perceived risk and return with factor loadings 0.662–0.886, and regulatory changes with factor loadings 0.681–0.870, while the internal reliability is measured with Cronbach’s alpha value for each constructs measured, as knowledge and awareness is 0.895, financial implication is 0.829, perceived risk and return is 0.861, regulatory changes is 0.837, and the composite reliability is above 0.8; thus, the internal consistency and validity are established.

Factor Loadings.

KA, knowledge and awareness; RC, regulatory changes; PRR, perceived risk and return; FI, financial implication.

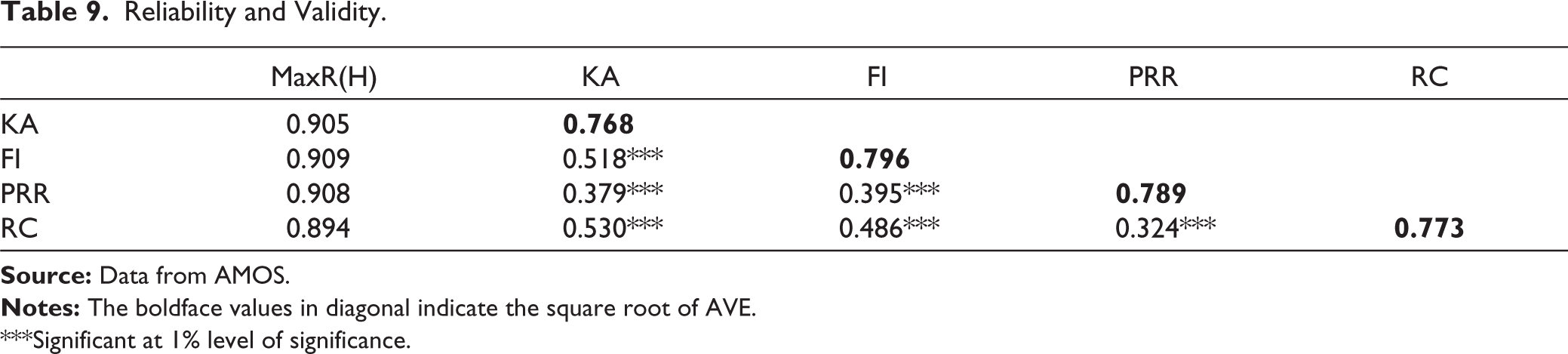

In Table 9, discriminant validity is measured with Fornell and Larcker (1981) criteria, where the values in diagonal indicate the square root of AVE, while the correlation values are less than the square root of AVE; thus, the variables have good discriminant validity.

Reliability and Validity.

***Significant at 1% level of significance.

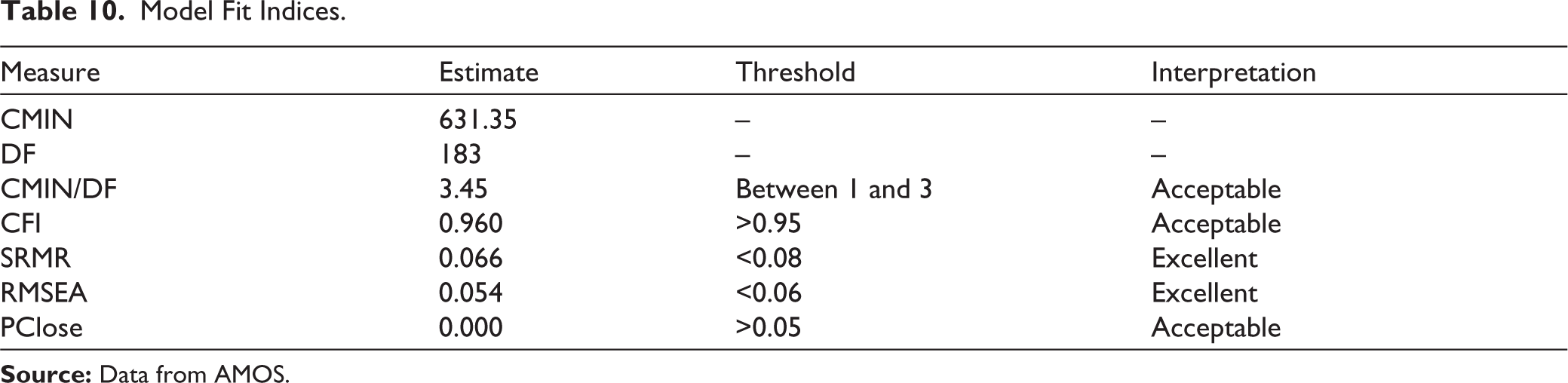

Table 10 shows model fit measures of the SEM analysis, where the CMIN value is 631.35 and the degree of freedom is 183, indicating CMIN/DF is 3.45; the CFI value is 0.960 with SRMR value less than 0.08 and RMSEA value at 0.054, which is less than 0.06, showing a good model fit.

Model Fit Indices.

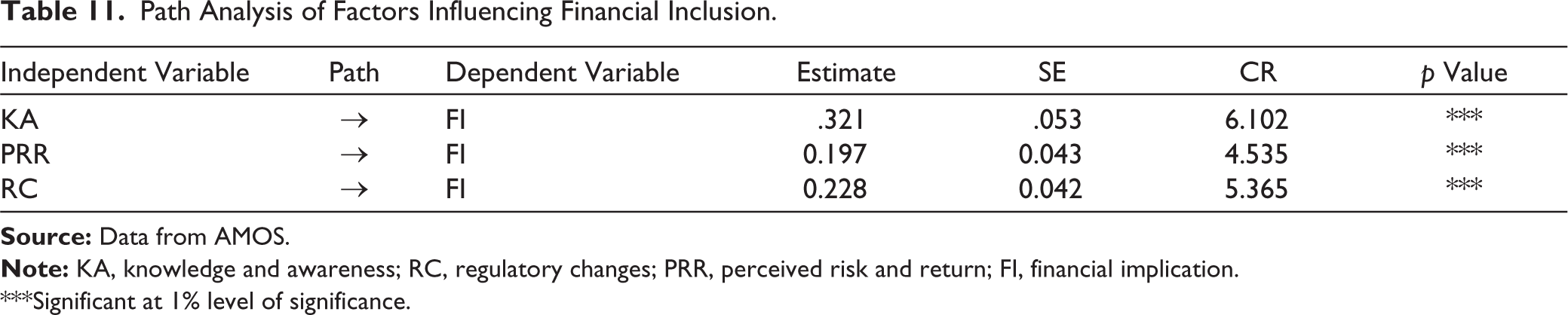

Table 11 reveals that knowledge and awareness has the strongest positive impact on financial inclusion (estimate: 0.321), followed by regulatory clarity (estimate: 0.228) and perceived risk return (PRR) (estimate: 0.197). All relationships are statistically significant (p < .001). The findings highlight the importance of enhancing financial literacy, regulatory transparency, and favorable perceptions of risk-return dynamics to promote financial inclusion.

Path Analysis of Factors Influencing Financial Inclusion.

***Significant at 1% level of significance.

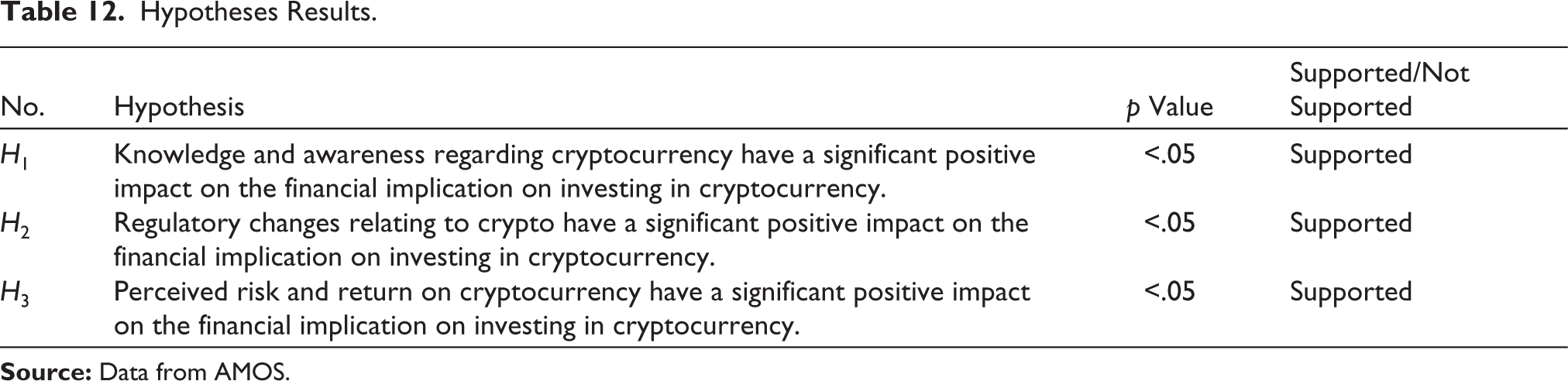

Table 12 confirms that knowledge and awareness, regulatory changes, and perceived risk and return significantly impact the financial implications of cryptocurrency investments. These results highlight the importance of informed decision-making, clear regulations, and favorable risk-return perceptions in promoting cryptocurrency adoption. The findings stress the need for enhanced education, regulatory transparency, and perception management to encourage responsible investment practices.

Hypotheses Results.

Figure 2 is used to find the implication of independent variables on dependent variables. As the independent variables knowledge and awareness (β = 0.321, p < .001), perceived risk and return (β = 0.197, p < .001), and regulatory changes (β = 0.228, p < .001) have a significant positive impact on financial implication, thus supporting the hypotheses H4, H5, and H6, this indicates that investment in cryptocurrency has implications from creating awareness in the crypto, and investors also analyse and consider risk and return factor before investing, while the changes in rules and regulations and bringing regulatory challenges also have a positive impact by investing in cryptocurrency; the R-square value is 0.546, representing 54.6% of the variation in financial implication of individuals investing in cryptocurrencies.

Discussion and Implications

The study found that the sample mainly included young, educated men, with many being married. However, gender and marital status did not significantly affect how important cryptocurrency investments were to them financially. Instead, the main factors shaping their investment behavior were knowledge and awareness, understanding of risks and returns, and the clarity of regulations. These factors—perceived risk and return (PRR), knowledge and awareness (KA), regulatory changes (RC), and financial implications (FI)—together explain what influences Gen Z investors’ decisions the most. Among these, knowledge and awareness had the strongest positive effect on financial inclusion, followed by clearer regulations and perceptions of risk and return.

This means that improving financial literacy, offering clear rules, and managing how young investors perceive risk and rewards are key to getting more Gen Z individuals involved in cryptocurrency investing. When Gen Z understands the risks and benefits better, they make smarter choices and feel more confident participating in the market. Since many worry about market ups and downs, fraud, and security, investment platforms that clearly explain risks and provide tools to reduce them are more likely to attract young investors. Clear and fair regulations are also important because cryptocurrencies are often seen as risky without official guidelines.

The study suggests that financial literacy programs, policymakers, marketing strategies, fintech companies, and social behavior changes all play important roles in helping Gen Z invest responsibly. Together, these efforts can make cryptocurrency a safer and more popular option for young investors across India.

Theoretical Implications

Financial education programs need to target young adults, especially those with higher education, to break down complex ideas and clear up myths about cryptocurrencies. Transparent regulations can protect investors and encourage innovation. Companies should work on building trust by showing realistic risks and rewards and providing secure platforms. Marketing efforts should focus on young investors aged 22–25, using incentives and educational content. Policymakers and crypto companies should work together to create rules that build confidence while supporting market growth.

Conclusion

This study shows that for Gen Z investors in India, knowledge and awareness are the biggest influences on how they view cryptocurrency investments, followed by clear regulations and their perception of risks and returns. Gender and marital status do not make much difference. To encourage safe and informed investments, there is a clear need for better financial education and clearer regulatory frameworks tailored to the needs of young investors.

Limitations and Future Research

The study’s sample was mostly young men from limited locations, and the study relied on self-reported data. It did not explore other factors like income or past investment experience. Still, it provides useful insights into how Gen Z makes cryptocurrency investment decisions and offers a base for future research. Future studies should look at a larger, more diverse group, including people from different countries, and consider psychological, social, and emotional influences. It would also be helpful to study how education, ethics, technology changes, and regulation affect young investors over time.

Footnotes

Acknowledgements

School of Science & Computer Science, CMR University, Bengaluru, Karnataka, India

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.