Abstract

This conceptual article uses the theory of planned behaviour and the social comparison theory with an aim to propose an integrated conceptual model of individual financial well-being. The study helps to understand the process by which individuals acquire the skills required for responsible management of finance and achieve financial well-being. The present article synthesises findings from the existing literature and proposes an integrated conceptual model that incorporates financial knowledge, financial behaviours, financial attitude, financial social comparison and financial self-efficacy into a single financial well-being model. Besides this, one’s level of materialism, orientation towards future, level of conscientiousness and cultural values are identified as antecedents of financial attitude. Moreover, the gender perspective is also incorporated in the model, which provides valuable insights on the existence of wide gap in wealth accumulation as indicated by substantial research work. The study develops several propositions that may advance empirical research in financial well-being domain. The study also discusses practical implications for financial service professionals who can positively improve the ability of individuals in financial matters by emphasising the importance of psycho-social variables.

Introduction

Financial management has become one of the most important life domains in the recent past due to a shift in social and economic structures. The ability to take responsible financial decisions and manage money in a complex financial world proliferated with diverse financial products has become challenging (Salignac et al., 2019). The shift in family structures from joint to nuclear families has increased family financial obligations and demands the responsible management of finance (Sahi, 2013). Research on financial well-being (FWB) gained traction after the financial crisis of 2008 (Sorgente & Lanz, 2017). While nations recovered from the great recession, another economic havoc wreaked by the COVID-19 pandemic has spread economic instability, causing millions of people to become unemployed and increasing their financial burden. Financial turbulence around the globe necessitates prudent management of finance. The past decade has witnessed a persistent uptick in studies aiming to examine and improve individual FWB considering its significant impact on other life domains. As per a survey report of the American Psychological Association (2015), financial concern is the biggest cause of stress among US households, which further poses a threat to their mental and physical health. The issue is more striking in the context of developing economies. As per a report given by Willis Towers Watson (2016), more than half of employees in India are insecure about their present and future financial concerns and think that these insecurities about finances affect their performance at work. In another report by PricewaterhouseCoopers (PwC, 2019), it is found that one out of three employees report financial issue as a source of distraction at work. The report further states that more than 64% of millennials feel stressed about their finances. Considering, the far-reaching effects of poor FWB, the question as to what affects FWB becomes indispensable.

FWB as a research agenda is widespread across disciplines, and many perspectives are still required to be unfolded (Brüggen et al., 2017). The dynamic nature of the financial environment across the globe has challenged the financial decision-making skills of people. The responsibility to make keys decisions about saving, investment and retirement rests on the individual itself. Moreover, a consistent uptick in debt burden has been seen among youngsters due to changes in consumer patterns and easy access to credit cards or other personal debt instruments (Serido et al., 2013). These changing financial circumstances call for good financial knowledge and skills. A person with sound financial knowledge is capable of taking prudent decisions for their families, which ultimately improves their economic growth (Lee et al., 2020). Though financial knowledge is a key component to improve FWB, the literature suggests that it is of utmost importance to study the other behavioural perspectives (Consumer Financial Protection Bureau [CFPB], 2015). Most financial interventions targeted at increasing FWB cannot achieve the desired results because they focus on improving only financial knowledge. A meta-analysis by Fernandes et al. (2014) stresses on improving interpersonal skills together with content knowledge about finance to make education programmes more effective. Similarly, Drever et al. (2015) opines that some behavioural changes are essential to increase FWB, irrespective of various resources and opportunities. People should be motivated to embrace habits that promote future-oriented financial behaviours (Dholakia et al., 2016). A research agenda on FWB by Brüggen et al. (2017) also pinpoints the need to study personal factors as one of the most important antecedents of individuals’ FWB.

In view of the aforementioned suggestions, the literature provides an evidence of the important role played by multiple factors explaining FWB. These factors include financial knowledge, psychological factors (impulsiveness, materialism and time orientation), societal factors (social influence, parental socialization and relative income), economic factors (income and net worth) and behavioural factors (credit card usage, retirement planning, saving, spending and compulsive buying behaviour). However, these studies do not consider the combined and interrelated effect of these elements. The present article fulfils this gap by proposing an integrated conceptual model in which all these factors can be easily accommodated and empirically tested. Moreover, empirical studies in the past lack the support of strong theoretical background. This article draws upon two widely used behavioural theories—the theory of planned behaviour (TPB) and social comparison theory, which are explained in the following section. Apart from this, the model provides incremental contribution by identifying additional factors that build up one’s attitude toward finance—a matter rarely recognised in previous studies. A mediating role of financial behaviours is another gap identified. Hence, the proposed model extends the previous studies by capturing the holistic view of cognitive, psychological and social dimensions in the realm of FWB.

The present study is arranged into different parts. Pursuant to the introductory part in the first section, the study proceeds with defining concept of FWB in the second section. The third section discusses research methodology adopted to gather pertinent literature along with a tabular representation of these gathered studies. The fourth section comprises of propositions development and conceptual framework. The fifth section discusses theoretical and practical implications along with scope for future research. Lastly, the sixth section summarises the study in concluding paragraph.

Concept of FWB

FWB as a research area has attracted the interest of scholars and scientists from several fields including psychology, sociology, consumer behaviour, personality differences and family economics. But the term still lacks consensus in its definition and measurement. This concept has been given many labels such as financial wellness, financial satisfaction, financial stress or financial strain (Prawitz et al., 2006). The literature highlights that FWB is a construct that can be measured using both objective and subjective indicators (Brüggen et al., 2017; Xiao et al., 2009). Objective FWB is measured with observable variables such as income and wealth whereas subjective well-being involves asking consumers how they perceive their financial status (Xiao & Porto, 2017). Accordingly, the existing literature in terms of FWB measures can be broadly classified into three groups: those using both objective and subjective measures, those using only objective measures and those using only subjective measures to examine FWB. The first category treats FWB as a composite concept, and it evaluates both objective and subjective dimensions (Porter & Garman, 1992; Sehrawat et al., 2021; Shim et al., 2009). For instance, Shim et al. (2009) measures it as both the assessment of financial status (credit scores) and also by perceived satisfaction with standard of living. The second category involves measuring FWB using only objective measures. While some researchers include pure financial information such as housing expenses, savings, assets and liabilities (Greninger et al., 1996), some others use measures such as household’s ability to absorb shocks, diversification of portfolio, unpaid loans and ability to manage liquidity (Aggarwal, 2014; Sehrawat et al., 2021). The third category includes more of a subjective approach, and recent conceptualisations of the term FWB identify and embrace this subjective aspect. This approach rests on an important fact that greater levels of income do not always lead to higher FWB, and it emphasizes the role of personality and individual’s nature in predicting FWB. Though a handful of studies in the past have measured subjective aspect using a single self-reported question of ‘how satisfied you are with your financial position?’, the recent evolution of the concept has emerged with comprehensive scales capturing subjective financial position. According to the CFPB (2015), it refers to the situation wherein a person is capable of meeting their financial obligation, have secured financial future and can make choices that allow enjoyment of life. A recent study conceptualizing the term FWB states it ‘as the perception of being able to sustain current and anticipated desired living standards and financial freedom’ (Brüggen et al., 2017, p. 4). Netemeyer et al. (2017) proposes two distinct dimensions: current money management stress and future financial security. D’Agostino et al. (2020) explain FWB as consisting of five dimensions, which include inner well-being, relative assessment, time dimension, financial security and financial freedom. Therefore, recent studies emphasize a subjective approach and provide a more comprehensive explanation of FWB.

Methodology

With an aim to capture a holistic and synthesized overview of the research in the field of individual FWB, this research article begins with a review of the literature to develop our conceptual model. Some influential studies in the past indicate that conceptual models are proposed by integrating the existing literature (Chaudhary et al., 2021; Rana, Raut, Prashar, & Hamid, 2020). To achieve this objective, this conceptual article first identifies top journals publishing research on individual FWB, such as Journal of Consumer Affairs, Journal of Financial Counselling and Planning, Social indicators research, International Journal of Bank Marketing, Journal of Economic Psychology, International Journal of Consumer Studies and Journal of Family and Economic Issues. These journals fall into the top ten journals publishing research in the FWB domain (Kaur et al., 2021). To identify and review the seminal work on FWB, various keywords suggested in past studies (Sorgente & Lanz, 2017) such as ‘financial well-being’, ‘financial satisfaction’, ‘financial wellness’ and ‘financial health’ are searched in these journals. The oldest studies that met the selection criteria of the current paper were conducted by Wilhelm et al. (1993) and Parrotta and Johnson (1998). However, this area became widespread after the economic crisis of 2008. The specific criteria followed for selecting the articles are as follows:

The articles that explore personal factors influencing financial behaviours or FWB. The articles should have financial behaviours or FWB as variable of focus. The articles should be available in full text in English.

The study is executed through a threefold synthesis of FWB literature following the research methodology steps in previous conceptual studies (Rana, Raut, Prashar, & Quttainah, 2020). First, the study tracked the evolution of the concept of FWB. This exercise helped us to gather different definitions and measures used to study FWB. Second, the study proceeded to synthesize the literature on FWB using measures such as model/theory applied, variables selected and significant findings of the study. The details are displayed in tabular form (Table 1). Third, this pertinent information gathered from step two was used to identify the disintegrated but important antecedents of FWB. This part of the study helped us to conduct a thorough review of the selected antecedents and to develop an integrated conceptual model. From the analysis of the existing literature, it can be inferred that FWB is an end result of the multiple factors given in Table 1.

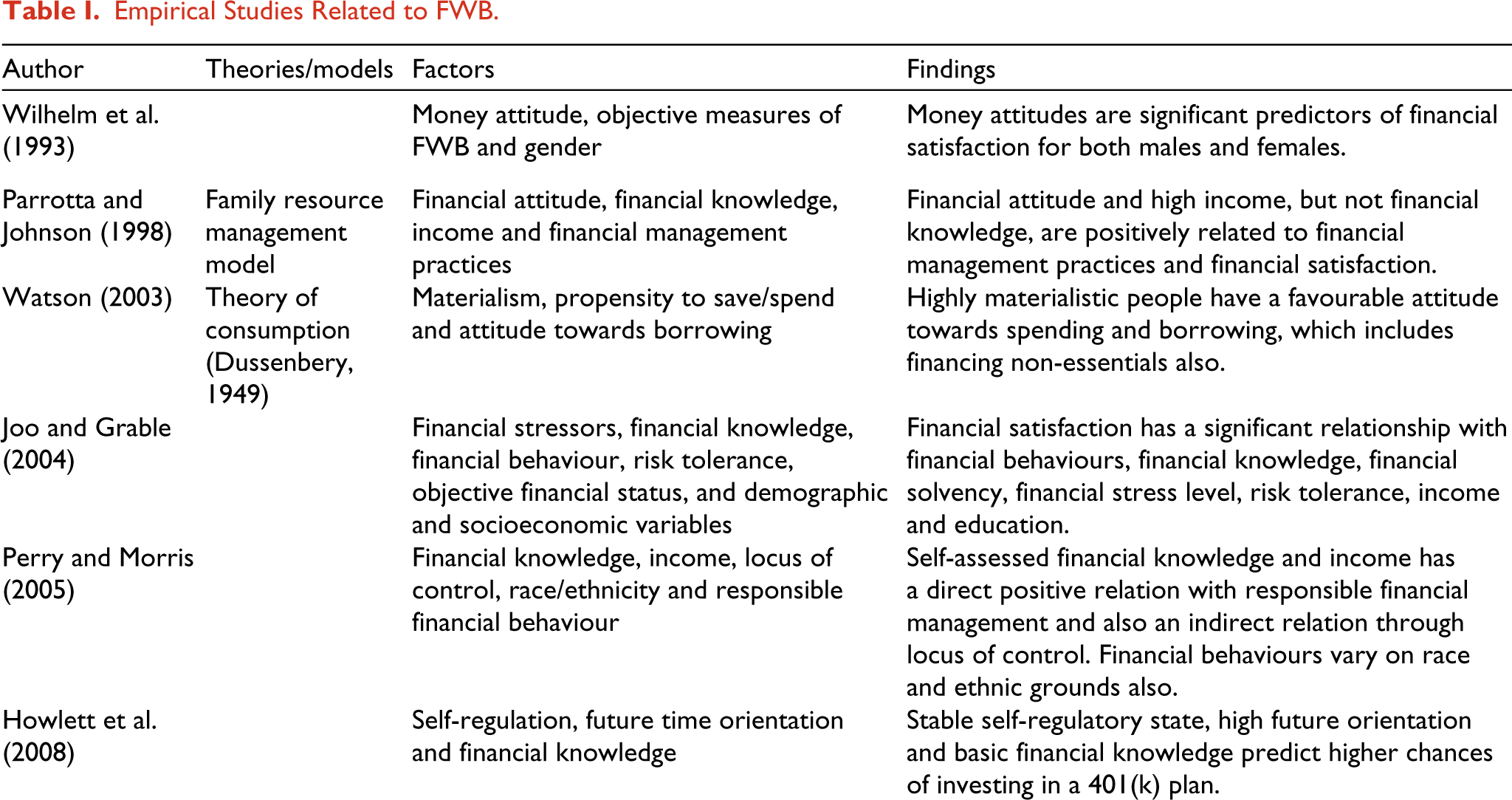

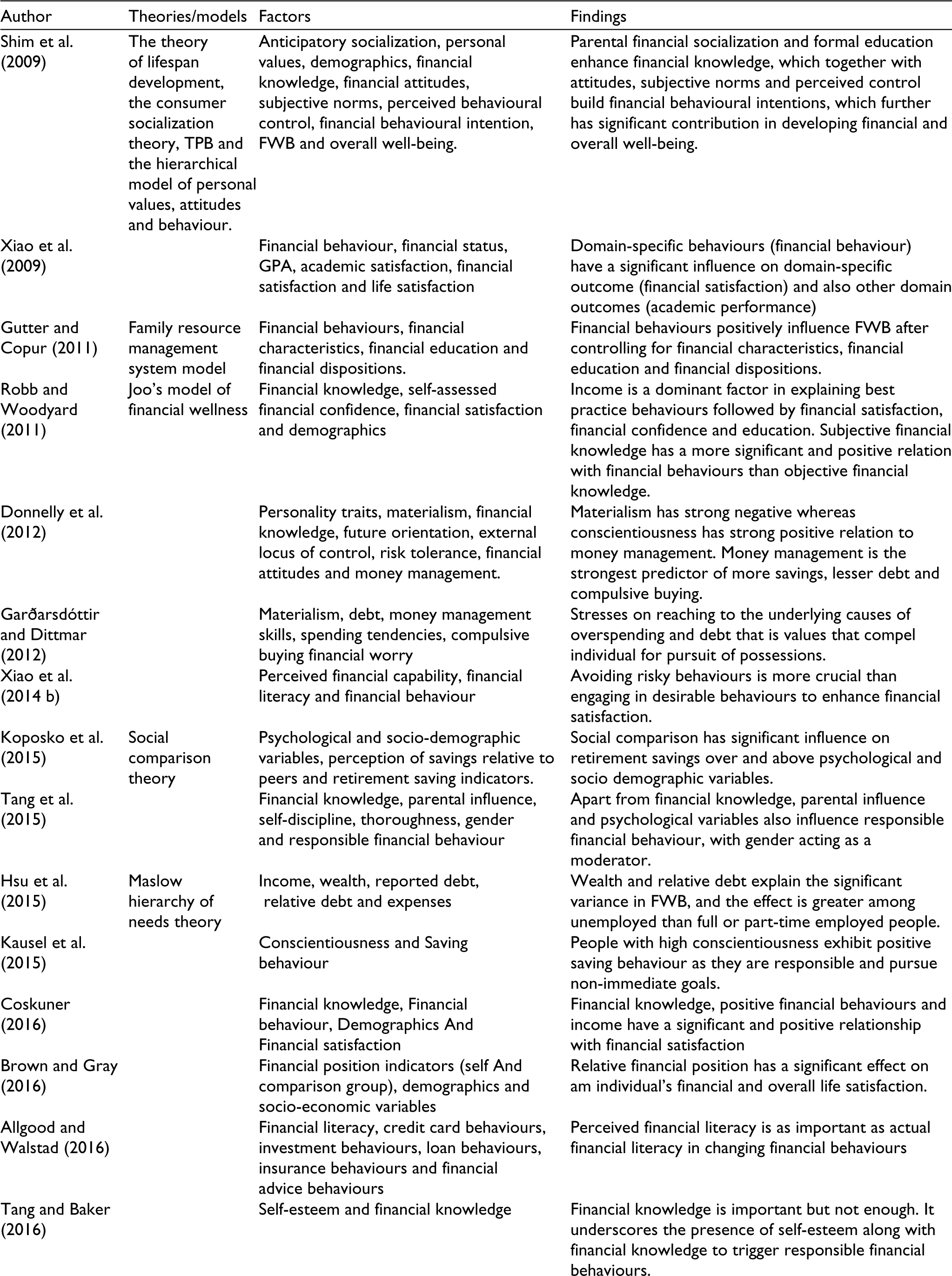

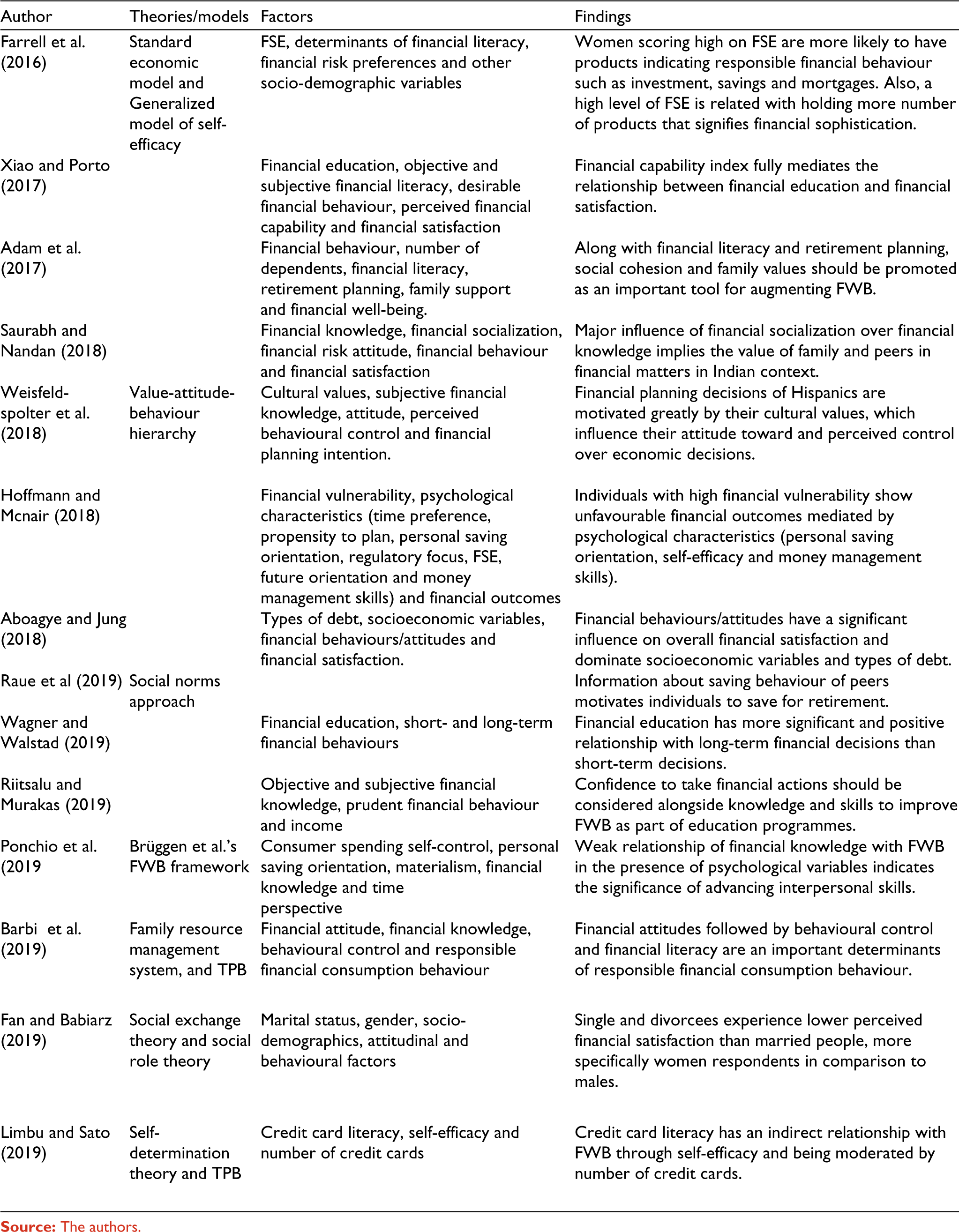

Empirical Studies Related to FWB

Proposed Integrated Conceptual Framework for Individual FWB

Theoretical Background

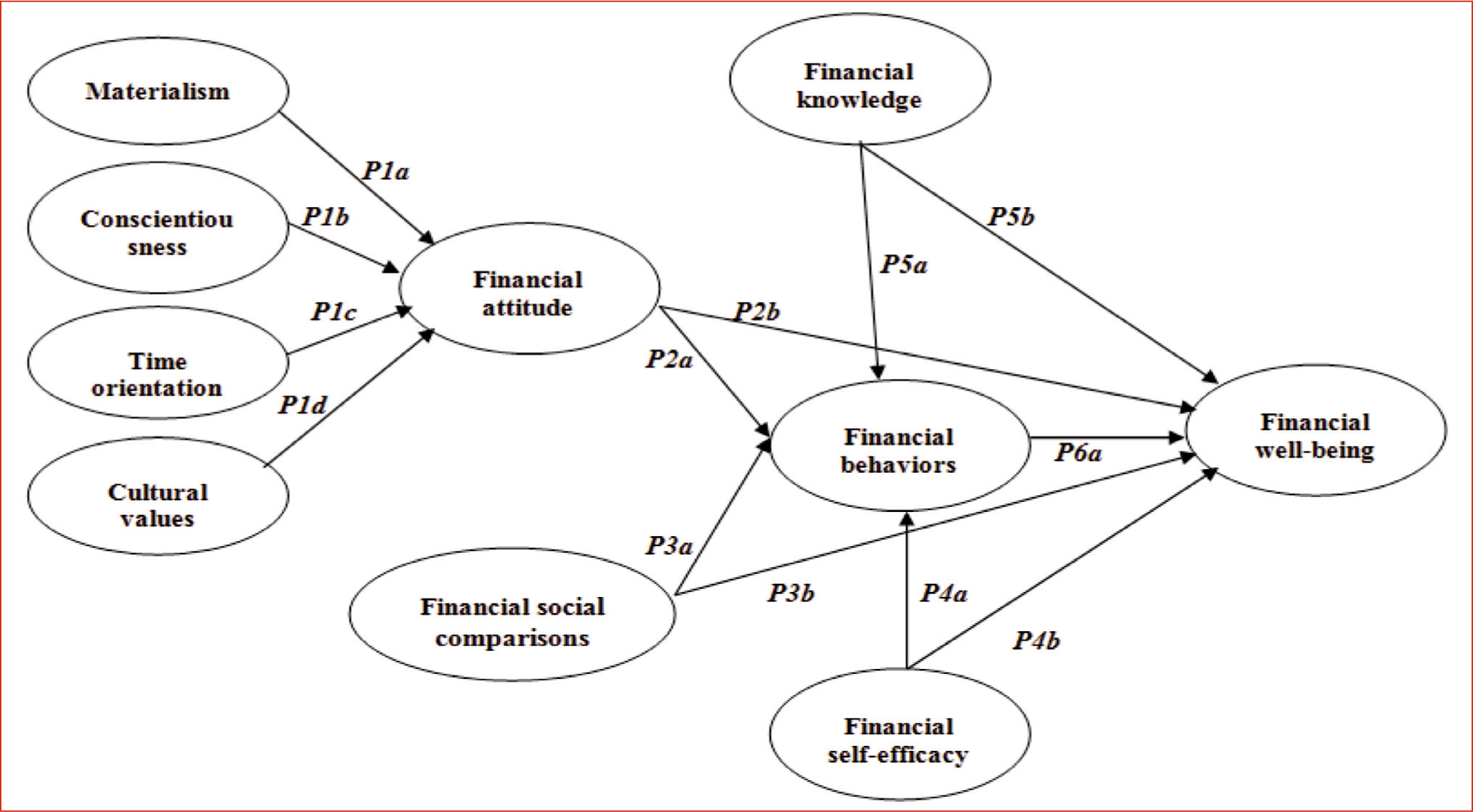

This study proposes a model based upon two fundamental theories: (a) the TPB and (b) the social comparison theory. Blend of these theories would elucidate the relationship between variables.

The TPB is the most widely used model for studying human behaviour (Ajzen, 1991). The theory comprises of three important determinants of human behaviour, which are attitudes, subjective norms and perceived behavioural control. A positive or negative attitude toward behaviour (AT), one’s perception of social pressure (SN) and own control over the circumstances (PBC) would influence individual behaviour. The use of TPB will help us to draw pathways towards responsible financial behaviours, which further leads to FWB. Moreover, the flexible nature of TPB will also allow us to include other relevant variables that are not a part of the original model (Ajzen, 1991). The social comparison theory developed by social psychologist Leon Festinger (1954) proposes that people evaluate their physical and social worth by comparing themselves with others. They have a basic drive to determine their opinions, abilities and desires with some type of reference group they feel they belong to. The inclusion of social comparison theory to study FWB lies in the importance people attach to their relative financial position than to their absolute financial position when evaluating financial satisfaction (Brown & Gray, 2016; Hsieh, 2003).

Under the lens of these two theories, the present study proposes an integrated conceptual framework to study individual FWB. Moreover, certain other variables indicated by previous studies are also examined and included as a part of the extended model. Therefore, FWB as the main dependent variable is measured by the combination of financial behaviours, financial knowledge, financial attitudes and subjective norms measured as financial social comparison and perceived behavioural control modelled as financial self-efficacy (FSE). Research emphasizes using self-efficacy as an important sub-construct to define the higher order construct of perceived behavioural control, and allows them to be used interchangeably (Ajzen, 1991). Ajzen (1991) explained the TPB model as being flexible enough to include more independent variables as per the requirements of the research problem. Therefore, four more variables have been included to the model for better understanding and increased application.

Proposed Constructs and Propositions Development

Perceptual Antecedents of Financial Attitude

Materialism: Materialistic values are defined as ‘set of centrally held beliefs about the importance of (material) possessions in one’s life’ (Richin & Dawson, 1992, p. 308). Richin and Dawson (1992) affirmed that materialistic people place possessions at the centre of their lives as a means to happiness and a measurement rod of success of their own and others. Several authors have documented the effect of materialism in the financial realm. Watson (2003) considered materialism as a significant variable in measuring attitude towards borrowing and saving/spending decisions of people. Materialism is found to have significant influence on individual’s attitude towards borrowing (Watson, 1998), saving and compulsive buying behavior (Dittmar, 2005) and attitude toward sound financial decisions (Vyvyan et al., 2014).

Garðarsdóttir and Dittmar (2012) proposed a negative relation between materialism and self-reported money management skills. Nepomuceno and Laroche (2015) reported that people who considered possessions as a source of happiness had more debt levels and less account balances, which might put them into hard financial circumstances. Ahamed and Limbu (2018) modelled the materialism construct in TPB and concluded that success dimension of materialism is positively related to attitudes towards credit card usage. This implies that a higher level of materialism is associated negatively with financial attitude toward sound financial behaviours. Hence, the following proposition is proposed:

P1a: Materialism will negatively influence financial attitudes.

Conscientiousness: Conscientiousness represents the predisposition to work hard, regulate one’s impulses/temptations, stay organized and follow obligations. Conscientiousness reflects traits of planning, controlling impulses and showing consistency, which are conceptually related to financial management behaviours.

Donnelly et al. (2012) advocated that individuals’ rich in conscientiousness develop positive financial attitudes and are good money managers. Such an attitude would be reflected in a proper mix of assets yielding ample income and satisfactory capital, making a person financially secure. Xu et al. (2015) study concluded that conscientiousness is statistically most significant and has negative correlation with financial distress. Tang et al. (2015) explored the relationship of two psychological factors—self-discipline and thoroughness—with responsible financial behaviour among young adults. Self-discipline and thoroughness have been characterized as a part of conscientiousness in big five personality traits. Self-discipline requires diligence in following financial plans, and thoroughness represents detail oriented and organized behaviour required to pursue financial goals. Therefore, conscientiousness represents a more positive financial standing, and most of the previous studies unfold this consistent pattern. Hence, the following proposition is proposed:

P1b: Conscientiousness will positively influence financial attitude.

Future orientation: Time orientation insists a trade-off between outcomes of present decisions that may have implications on future outcomes (Howlett et al., 2008). The degree to which people associate future consequences of their actions represents their willingness to forego short-term pleasure from spending for long-term financial security. Rutledge and Deshpande (2015) studied the influence of time orientation on personal finance behaviours. Participants with a low future-oriented mindset were found to have higher levels of non-mortgage debt and credit card debt and have lesser levels of savings. Time perspective is widely studied in other fields also. In an effort to enrich the contribution in solving wide problem of unhealthy lives of Americans, Joireman et al. (2012) explored the role of consideration of future consequences (CFC) in adopting healthy behaviour intentions such as exercise and healthy eating. The findings concluded that concerns for future consequences or degree of importance attached to future outcomes of present actions developed positive/favourable attitudes towards health related behaviours. Therefore, orientation towards future facilitates more responsible financial behaviours and a conducive attitude toward finances. Hence, it is proposed:

P1c: Future orientation will be positively related to financial attitude.

Cultural values/Personal values: On lines of value attitude behaviour hierarchy established by Homer and Kahle (1988), consumer behaviour researches have validated the significance of personal values in stimulating financial attitudes, which ultimately steer the performance of behaviour (Shim et al., 2009). Cultural value is also considered as a precursor to attitude in the TPB (Weisfeld-Spolter et al., 2018). The cultural value of familism has a significant influence on a person’s decision-making process through its supremacy in controlling one’s psychological process (Villarreal & Peterson, 2009). People who attach greater importance to familism are influenced by their family members. Therefore, performing future-oriented and responsible financial behaviours that assure future financial security to one’s family is of great essence. In an attempt to examine how positive financial behavioural intention results into FWB of college students, Shim et al. (2009) found personal values (self-actualization) to positively influence financial attitudes and financial behavioural intentions. A study by Weisfeld-Spolter et al. (2018) also substantiated the role of cultural values as an antecedent of attitude towards purchase of financial planning services. Therefore, more research work is required to understand the cultural importance in the financial decision-making process so that the requisite educational materials and trained professionals who recognize these cultural values and diversity can be developed. From the evidence of strong influence of cultural values, the following proposition is proposed:

P1d: Cultural values will have significant influence on financial attitudes.

Financial Attitude

Financial attitude is a predisposition demonstrated with some level of agreement or disagreement while evaluating proposed finance practices or some specific financial behaviour such as credit card borrowing (Xiao et al., 2011). Ajzen and Fishbein (1980) analysed that it is the attitude (favourable/unfavourable) of an individual that affects their intention to perform a specific behaviour. A lenient financial attitude towards finances might put a person in a difficult financial situation. Financial attitudes influence the manner in which money is managed by an individual. Shim et al. (2012) advocated that attitude is the largest coefficient influencing saving and future-oriented financial behaviours of young adults. Sivaramakrishnan et al. (2017) also revealed that negative attitude towards stock market participation shunned intentions to participate in stock market and actual equity holding. Few studies also provide direct association of financial attitude and FWB (Abdullah et al., 2019; Sabri & Zakaria, 2015). This implies that an individual holding a positive financial attitude will exhibit responsible financial behaviour and will perceive high FWB. The following propositions are proposed:

P2a: An individual with a positive financial attitude will display responsible financial behaviours. P2b: Financial attitude will be positively related to FWB.

Financial Social Comparison

The idea of social comparisons can be traced back to Veblen (1899), who postulated that after a specific subsistence level, humans tend to choose that consumption plan which signals their status. So, when people try to ‘keep up with the Joneses’, they might engage in behaviours that no longer guarantee long-term maximization. The concept was then evolved from the social comparisons theory proposed by Festinger (1954).

A couple of studies have recognized the role of social comparisons in the financial context. Koposko et al. (2015) applied the social comparison theory to understand the influence of individuals’ perception of how much others save for retirement on their own savings behaviour, and the variable social comparison accounted for significant variance. Raue et al. (2019) conducted experimental studies to prompt savings behaviour by using a social norms approach. Some participants who were given social feedback (i.e. information about saving behaviour of others) and categorized as underperformers were more likely to better allocate their savings than those who were not provided social information. A study by Zhang et al. (2016) conducted on 2,700 respondents in the United States concluded that socio-economic status comparisons in neighbourhoods led to increased levels of materialism, compulsive buying and reduced savings. It is also found that individuals who make frequent social comparisons perceive lower FWB (Braun Santos et al., 2016; Hsieh, 2003). However, positive effects on FWB are also noticed if people aspire to make their lives better or foresee a better financial future by making upwards comparisons (Brown & Gray, 2016; Chatterjee et al., 2019). On the one hand, research suggests a motivational drive acquired from engaging in social comparisons which triggers self-enhancing values and behaviours among individuals. On the other hand, it has also been related to reduced savings and increased levels of stress and dissatisfaction among adults. Therefore, the following propositions are proposed:

P3a.: Financial social comparison will have significant influence on financial behaviours. P3b.: Financial social comparison will have significant relationship with FWB.

Financial Self-efficacy

Self-efficacy (or perceived competence) refers to a confidence in oneself to achieve the desirable outcomes, or it can also be referred to as a person’s judgment of their own capabilities to deal with particular situations successfully. Ryan and Deci (2000) postulated that self-efficacy is a critical factor in influencing individual well-being. A more domain-specific construct, that is, (FSE) has also been found to influence FWB (Gutter & Copur, 2011).

In a writing to find the determinants of credit card debt among college students, Xiao et al. (2011) found that a greater ability to control own finances and perception to stick to their plans of managing finance resulted in lesser levels of credit card debt. Lown et al. (2014) also established a positive relationship of self-efficacy with the saving behaviour of low and middle income individuals. Very few studies also highlight FSE as direct predictor of individual FWB (Oquaye et al., 2020; Shim et al., 2009). Thus, studies emphasise the prominence of one’s confidence level and self-assuredness in making financial decisions, managing finance and setting financial goals. This indicates that an individual’s ability to meet present and future financial responsibilities depends upon the level of FSE. Therefore, the following propositions are developed:

P4a: FSE will have positive relationship with financial behaviours. P4b: FSE will be positively related to FWB.

Financial Knowledge

Research provides a consistent evidence of a strong relationship between knowledge and behaviour in the domain of finance (Hilgert et al., 2003; Lusardi & Mitchell, 2008; Robb & Woodyard, 2011; Shim et al., 2009). A metal analysis on financial literacy and financial behaviours has noted mixed relationships (Fernandes et al., 2014). But recent studies have shown a positive relationship to exist between financial knowledge and financial behaviours (Brown et al., 2014; Xiao & O’Neill, 2016). Further segregation of the term financial knowledge into objective knowledge and subjective knowledge enlightens up this association. Subjective knowledge means what people perceive they know rather than objective financial knowledge, which indicates that only factual knowledge about finance concepts has a greater positive and significant association with financial behaviours and FWB (Woodyard & Robb, 2016). Hence, the following propositions are stated:

P5a: Financial knowledge will have positive influence on financial behaviours, and also, subjective financial knowledge will explain greater variance in financial behaviours than objective knowledge. P5b: Financial knowledge (both objective and subjective) will have positive relationship with FWB.

Financial Behaviours

Plenty of research on FWB holds good/responsible/positive financial behaviour to be an immediate predictor of FWB (Joo & Grable, 2004; Shim et al., 2009; Xiao et al., 2009). Hilgert et al. (2003) defined financial behaviour as credit, saving and cash management. Financial behaviours include responsible sound financial behaviours and preserving behaviours during serious life circumstances, as well as destructive financial decisions (Brüggen et al., 2017).

Based upon the Happiness Study Framework by Lynbomirsky et al. (2005), which indicated that domain-specific behaviour increases one’s satisfaction in that domain (e.g., an act of kindness being performed), Xiao et al. (2009) proposed and tested a framework that performing positive financial behaviour would also increase financial satisfaction. Joo and Grable (2004) explored various direct and indirect determinants of financial satisfaction and concluded that an individual’s financial behaviour (cash, credit and money management, budgeting and financial planning) was the sole dominant factor explaining financial satisfaction. Xiao et al. (2014) classified financial behaviours as risky and desirable, revealing that the effect size of risky financial behaviour was two times that of desirable financial behaviour, which indicates that it costs twice to engage in risky financial behaviours than the benefits derived from involving in desirable financial behaviours. Therefore, the research work in area of FWB displays a consistent positive relationship between sound financial behaviours and FWB. Hence, the proposition is stated as:

P6a: Financial behaviours will have positive relationship with FWB.

Based upon the earlier discussion, it can be noticed that financial attitudes, financial knowledge, financial social comparison and FSE are significant predictors of financial behaviours and FWB. However, evidence from recent studies also calls for the examination of the mediating role of financial behaviours between these psychological beliefs and FWB (Oquaye et al., 2020; She et al., 2021). An important gap that can be identified is to investigate if the presence of these psychological beliefs directly influences FWB or if they translate into actual financial behaviours, which further leads to individual FWB. Thus, the following proposition is made to determine this relationship:

P6b: Financial behaviours will mediate the direct relationship of financial attitude, financial knowledge, financial social comparison and FSE with individual FWB.

Role of Gender

Plenty of research has shown that persistent gender differences exist in wealth accumulation, which is an important element of FWB. By keeping the income variable constant, various authors have attempted to study the underlying causes in wealth discrepancies between men and women (Danes & Haberman, 2007; Neelakantan & Chang, 2010). The extant literature shows that women are risk averse and tend to select less risky investments as compared to men (Barber & Odean, 2001; Bernasek & Shwiff, 2001). Conservative investment strategies result in low retirement income accumulation than aggressive investment strategies. So, women end up having lower retirement savings. Montford and Goldsmith (2015) suggested that it is because women have lower FSE than men do that they tend to make less risky investment decisions, which, paradoxically, yield lower returns in the long run. Men are found to hold a more positive attitude towards financial planning (Lusardi & Mitchell, 2008). Men have often been found to think more about planning for retirement (Van Rooji et al., 2011). Regarding the role of financial social comparison, no research till date has explored the issue of gender in this context. Taylor et al. (2000) suggested that women are marked by the desire to affiliate with others more than men. The desire to make social comparison arises in a state when the person lacks confidence or they are not sure of the appropriate thing to do (Guimond & Chatard, 2014). Therefore, in the context of financial decisions, if women have been found to be less knowledgeable, more risk averse and lack self confidence in choosing diverse financial products, then it can be proposed that women may have a greater need to make social comparisons than men do. So, the previous findings indicate an important place that gender itself holds and how it affects a person’s ability to take sound financial decisions. Hence, the study proposes the following for future research:

P7: To study the importance of gender role in influencing FWB through a process of multiple factors highlighted in this study and what measures can be adopted to reduce such discrepancies.

Contribution and Implications for Future Research

The major aim of any conceptual review article is to synthesize the existing findings in a particular subject or topic, identify and resolve inconsistencies, highlight major gaps in the past research that prevent the field’s ability to move ahead and present future agenda (Hulland, 2020). Following the aforementioned guidelines, the present article draws upon extant studies in the personal finance area and proposes an integrative model of FWB. Although previous studies have extensively studied the determinants of individual FWB, still, the area lacks development of analytical models. This study synthesizes the existing literature into a broader framework to understand the process by which individuals develop financial attitudes and financial behaviours and achieve FWB. The literature presents minimal evidence as to how the financial attitudes are developed, except for a few seminal works such as Shim et al. (2009) that emphasize the role of family financial socialization and financial education. However, this study recognizes the role that psychological dispositions or personal values play in the formation of financial attitudes. The present study also identifies an important mediating role of financial behaviours between different personal factors and FWB. The literature is also inconsistent and unclear about the reasons behind the gender gap in making informed or healthy financial decisions and wealth accumulation. This study reflects upon this issue and highlights the various personality traits that might cause or enhance such financial gender gaps.

Besides this, the study offers the following potential research avenues for future researchers:

Operationalization of FWB: A thorough review of the existing literature indicates a lack of consensus on the definition and measurement of the construct of FWB. To achieve a more comprehensive understanding of FWB and to enable professionals to develop better policies, researchers should make efforts to come up with a more broadly accepted definition and a standardized assessment of FWB including both objective and subjective aspects (Wilmarth, 2021). Further, it has been noticed that FWB models have been developed and tested in developed economies. Therefore, testing their validity in different contexts and emerging economies is a necessary task to consolidate and generalize progress in measuring FWB.

Understanding FWB in a broader context: Although the present study is exhaustive in highlighting the concept of FWB and the role of various individual characteristics, echoes of financial troubles around the globe require that the concepts underlying the formulation of FWB frameworks require more careful consideration. It can be argued that methodologies relying exclusively on individual factors to understand FWB distort the framework that should rather incorporate other contextual domains as well such as family characteristics and societal, political, economic and cultural factors. It can be noticed that recent work in this area recognizes the importance of social and institutional environment, but only in theoretical form. The area lacks empirical research. Thus, future researchers can undertake analytical studies to examine how these contextual factors fit into the FWB framework, how they interact with each other and what is their relative importance in determining FWB.

FWB and socio-demographics: It is evident from the literature that socio-demographics have an important role in shaping an individuals’ FWB (Sahi, 2013). The model presented in this study is flexible enough to be empirically tested on different socio-demographic groups. For instance, different gender groups can be incorporated in the model to investigate how the developed propositions differ for both genders. Similarly, the effect of certain life events such as marriage or a sudden change in economic conditions can be explored in the future, which may have a significant effect on an individual’s attitude and behaviour in financial matters. Likewise, one might expect that traits such as materialism, social comparisons and self-efficacy can be influenced by income level. Therefore, valuable insights can be derived by testing the propositions of the model on different income groups. This study encourages future researchers to explore these relationships in the context of different demographic groups.

FWB and business climate: The third line of research emerging from this study is related to examining the FWB definitions, measurement and impact in the context of the business environment. Given the increased awareness among corporate employers to look after the financial health of their employees, as it affects their productivity, builds strong interrelationships and ultimately strengthen corporate image, reputation and profits, it is extremely important to advance FWB work in organisational field.

Theoretical Implications

This study offers useful implications for the theory. On the basis of the proposed conceptual framework, several directions for research can be pursued in future studies in order to have a more holistic picture of the topic. First, it can be figured from the state of research that the existing literature is disintegrated and that very few studies have investigated how the FWB of an individual is affected by cognitive, psychological, social and behavioural factors in combination. The present study proposes a conceptual model and various propositions that can be empirically tested and analysed by future researchers. Moreover, the model contributes to the understanding of the TPB with its incremental contribution as it provides antecedents to financial attitudes, that is, materialism, time orientation, conscientiousness and cultural values. Second, the model directs future researchers to study the direct and indirect effects of all personal factors on FWB with financial behaviours acting as mediator. This would provide novel insights to the FWB literature regarding how the presence of certain personal traits influences individual FWB. Third, the synthesis of pertinent information in Table 1 indicates that this research domain lacks cross-cultural research. Therefore, cross-cultural studies can be conducted to see how developed propositions interact with regional/cultural factors. For example, being materialistic and future-oriented can be influenced by individualist or collectivist form of culture.

Practical Implications

From a practical perspective, this model has got implications for consumer financial service professionals who can design tools to stimulate responsible financial behaviours among their clients. Financial advisors and counsellors can better serve their clients if they have good hold of client’s psychological and social perspective towards finance. For instance, individuals’ should be advised to avoid making social comparisons as it can result in the accumulation of large debt levels. Likewise, materialistic values should be curtailed as they can push one to postpone savings and accelerate immediate spending. Financial professionals can instil a positive financial attitude among people by showing them the future consequences of financial actions taken today. Although a large number of resources have been spent by international organizations to educate people to make more informed financial decisions, they have failed to achieve the desired results (Fernandes et al., 2014). Surprisingly, such interventions only focus on financial knowledge and do not address all factors. Therefore, this conceptual study offers an integrated approach for addressing FWB issues from a broader perspective. It recommends the significance of behavioural theories in achieving these targets. Further, gender studies reflect women being at a disadvantaged position when long-term financial security is considered. This study demonstrates factors by which such gender gaps can be captured. For instance, interventions targeting women FWB should be tailored to improve their FSE as the literature highlights the lack of this trait among women compared to their male counterparts.

Conclusion

The past decade has seen a persistent increase in studies examining individual FWB. Many of the social science scholars, scientists and financial planners have shown keen interest in investigating the important predictors. The current article extends the psychological and sociological research work in the domain of FWB. Considering that FWB is one of the most important components of overall well-being, this article aimed to provide an integrated conceptual model by extracting important factors from the set of past empirical studies. The model contributes towards the understanding of individual or personal factors responsible for executing healthy financial behaviours and the achievement of a secured financial state in the present and in future. The factors such as materialism, time orientation, conscientiousness and personal values justify the reason behind adopting positive or negative financial attitudes, which is a major determinant of individual FWB. The relationship of other factors such as financial social comparison, FSE, financial attitudes and financial behaviours shed light on the significance of these factors in building one’s financial FWB, and it draws the attention of the financial educators to adopt a more holistic approach for developing interventions to increase individual FWB instead of concentrating only on improving financial knowledge.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of his article.