Abstract

Studies reveal that the financial well-being of employees has a direct bearing on their productivity and overall well-being. The wellness initiatives organized by the information technology (IT) companies operating in India have also started focusing on the contributing aspects of financial well-being. In this context, the article explores the determinants of financial well-being of IT professionals in India. The article utilizes confirmatory factor analysis (CFA) for the analysis. The study employs a survey questionnaire covering financial literacy, financial behavior, and financial fragility. It also attempts to recognize the influence of gender and job roles (technical or managerial) in ascertaining financial well-being. The sample data used in the study include 237 professionals employed in the IT sector. The study uses partial least squared structured equation modelling (PLS-SEM) to understand the connection between the determining factors. The results indicate that financial well-being is positively influenced by financial literacy and financial behavior while financial fragility has a substantial negative impact. The financial literacy and financial fragility are significantly different between technical and managerial roles. Gender appears to have a sizeable impact on the financial behavior and financial fragility levels—women employees performed better in both the factors. Interestingly, financial literacy levels of the two genders are not significantly different. The results show that there is a need to focus on literacy, behavior, and fragility in financial wellness programs organized by the IT industry. Further, the study recommends offering tailored financial wellness training modules created based on the job levels and gender instead of following “one program, fits all” standardized approach.

Introduction

Financial well-being is a crucial component of the financial health of an individual. In the wake of COVID-19 and the related job losses, the financial health has become a decisive issue confronting people from all walks of life. The rising commodity prices and living costs during the prolonged lockdowns have only exacerbated the concerns. With companies shutting operations for both short- and long-periods depending of their operations, the job-losses and pay-cuts have become the norm across industries. The expensive medical costs, rising inflation, and threat of loss of income post-pandemic have forced employees to take a hard look at their financial health. In addition to the pandemic, the emerging leanings in education, occupation, and demographics, like the diminishing job security, increased number of women in workforce, rising divorce rates, and single parenthood, are creating new-fangled tensions on financial decision-making by individuals.

Due to the complex financial markets and systems, the capability to make healthy financial decisions managing money has become more challenging. There has been support from the governments and corporates to help individuals to navigate through this maze . For instance, the security exchanges in India conduct financial literacy campaigns to introduce financial products for investment. Financially literacy is important as this allows individuals to make healthy financial decisions (financial behavior), attain the financial objectives, and protect themselves from possible economic shockwaves and related risks (financial fragility). These factors would ultimately lead to their financial well-being, which is defined as a situation wherein a person is well-equipped to meet the current requirements of life and also in the future, feel assured about the future, and equipped to deal with unpredicted crises . Therefore, an improved financial well-being implies not only poverty alleviation but also have an effect on physical health and psychological condition of an individual.

Researchers have considered various factors which adversely impact the financial well-being of an individual. These factors include undisciplined spending, inability to repay debt, absence of an emergency fund, low-income levels, and lack of knowledge of financial markets and products . One of the prominent determinants of financial well-being identified in the literature is financial literacy . Financial literacy enhances the individual’s ability to plan for future needs, both near-term (emergencies, healthcare, etc.) and long-term (retirement planning). Moreover, researchers have established a direct link between financial literacy and financial behavior . Lack of financial literacy causes overspending on credit, reliance on borrowings, lower savings, and poor financial decisions . Poor financial behavior and lack of financial knowledge raise the financial fragility of the individual . Increased financial stress further leads to detrimental impacts on the individual’s professional and personal life.

The financial well-being surveys conducted across countries indicate that an appreciable segment of the workforce is more concerned than ever about their current and future financial health. The surveys also give clear indication on how financial strain has become a distraction at work. For example, according to the 2021 PwC Employee Financial Wellness Survey, 72% of the millennials experienced enhanced financial stress due to the pandemic, of which 45% agreed it has reduced productivity. The survey also showed that 72% were attracted to companies which cared more about their financial well-being.

During these turbulent times, employers are attempting to address the welfare of their employees, financial well-being including. These include various financial wellness programs to address the financial stress of their employees including online workshops and counselling sessions, financial literacy campaigns, dedicated human coaches, and digital technology platforms. Multinational firms operating in India have followed a similar approach in enhancing the financial well-being of their employees. Investing in improving the financial well-being enhances the overall well-being of employees, thereby improving their physical and mental health, increasing productivity, and engagement. Hence, understanding the factors affecting the financial well-being of their personnel becomes critical for companies so as to design and offer an appropriate solution. It also becomes important to understand how the employee groups are different from each other so that customized solutions can be provided. Hence, this study addresses this gap in literature and attempts to understand the interaction of financial literacy, financial behavior, and financial fragility on the financial well-being of professionals working in the IT sector. It further scrutinizes the impact of gender and job position on the above factors.

This study focuses on the IT industry as it is a prominent contributor to India’s GDP, exports, and employment generation. According to the industry trade association, NASSCOM, the IT sector generated US$194 billion revenue in 2020, accounting for 8% of India’s GDP. It also reported US$136 billion in exports and provided direct employment to four million+ employees during the year. IT sector was chosen for the study considering its significant contributions in economic development and job creation. As the worker productivity and retention depend on employee well-being it is essential to understand the factors impacting the well-being of IT employees before devising wellness plans. This research aims to recognize the interplay of influencers of financial well-being of IT employees in the country. It attempts to answer the following questions—what are the different factors affecting financial well-being? and does the impact depend on characteristics of the employee and their job role? The findings will be of interest to IT employers in designing customized programs to their employees to address their financial well-being.

The article is organized in five sections, namely, literature review, research methods, findings, discussion, and conclusion. The following section covers the theories and literature in financial well-being. The conceptual model and hypothesis built based on these theories and literature are also covered in this section.

Literature Review

Theoretical Framework and Recent Literature

Maslow’s theory on motivation was found relevant in setting the framework for this study. According to this theory, actions of an individual are motivated by their needs . Maslow classified these needs into five levels—psychological, safety, social, self-esteem, and self-actualization. He argued that these needs take a tiered structure—the needs in the lower tiers need to be fulfilled before progressing to a need in a higher tier. According to this theory, the individual will act only to satisfy unmet needs, that is, the need will no longer be a motivator once that need level is satisfied. The financial health of an individual belongs to the lowermost levels, that is, psychological and safety needs. The gratification of this level of need is necessary before scaling up to higher levels of needs. In addition to the income level of the individual, the ability to have a safe livelihood would also depend on the effective management of their income. The responsibility to ensure the fulfilment of these needs of an employee would extend to the employer. Hence, employers’ responsibility extends beyond offering salaries to training their employees on effective management of financial resources. It is noticed that the productivity drops and attrition rises if there is a lack of such support mechanisms.

Starting with Porter and Garman, several researchers have tested conceptual models for financial well-being. The researchers examined the impact of demographic factors (ethnic background, educational qualifications, employment, and gender) and attributes such as income level, dependents, and wealth on financial well-being. The findings indicated that demographic factor and attributes evaluated significantly influence financial well-being.

The model of financial well-being built by Sabri et al. emphasized the mediating role of financial literacy. The results show the significant impact habits facilitating saving and socialization have on financial well-being. As a broader concept, financial literacy encompasses three areas: (a) understanding of the financial markets, instruments, and regulations, (b) skills, and (c) attitudes . Studies have used two distinct approaches to measuring financial literacy. One method to measure is by using objective tests of financial concepts and the other is based on the self-assessment of the understanding of financial topics by respondents themselves . In this study the researchers have used the self-assessment method to measure financial literacy.

Many studies have demonstrated that in personal finance, financial behavior is dependent on financial literacy . The general agreement among the researchers is that knowledge about financial markets and instruments led to a significant improvement in financial behavior. The disciplined financial behavior was found in detailed retirement planning and asset accumulation . The findings can also be extended to stock market investment . It has also been affirmed that less financially literate households are more prone to have trouble in repaying their liabilities . Empirical studies have concluded that financial literacy has a significant negative impact on the probability of both payment delays and default rates in mortgage payments. Brüggen et al. reported that financial behavior influences financial well-being, and financial behavior is affected by several financial interventions, like financial education. Researchers also agree that financial skills and knowledge do have an influence on financial behavior and financial well-being . Extending the impact of financial literacy, researchers find that higher financial literacy are linked to lower financial in individuals . Based on the existing research, we expect financial literacy and financial behavior to have a positive impact of financial well-being. Financial fragility is expected to have a negative impact on financial well-being.

In addition, researchers have also studied the impact of demographic factors on financial well-being . Literature has also shown that the financial knowledge and behavior of women are significantly different from men . In this study, we consider gender and job levels (technical and managerial roles) as categorical input on which the input factors would depend on. Gender also has a major influence on financial well-being .

According to the RAND Europe report 2021, there is a higher proportion of workers having financial concerns and there is a proven and well-accepted association between financial concerns and mental health . Some of the challenges faced by workers that can lead to weak financial well-being are lower earnings and savings, credit card debt, and less affordable housing. The study underlines the urgent need to amend the financial well-being of, particularly young workers. A model place for such interventions is the workplace. Due to the difference between the requirements and characteristics of employees these interventions need to be personalized with modules specific to employee groups having similar characteristics. This is reinforced by the existing literature on the impact of corporate policies on the financial well-being of employees .

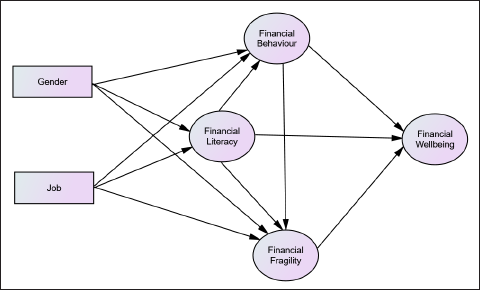

To the best of the authors’ understanding, there is no study conducted to comprehend the factors influencing the financial well-being of the IT professionals in India. As this is a prominent industry for India, both in terms of its contribution to GDP and employability, this article attempts to understand the influence of financial literacy, financial behavior, and financial fragility on the financial well-being of IT professionals in India using the conceptual model developed by Joo and Grable .

Designing the Conceptual Model

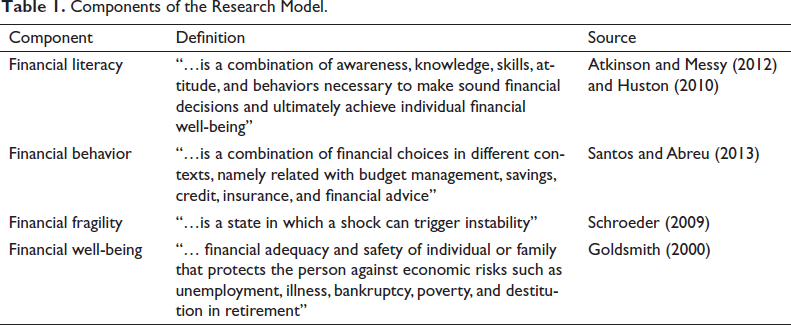

The study considers the direct impact of financial literacy, financial behavior, and financial fragility and the indirect role of gender and job levels in determining financial well-being. The definition of financial well-being and its determinants are presented in Table 1.

Components of the Research Model.

Hypotheses

On the basis on the theoretical framework and literature review, the following hypotheses were proposed.

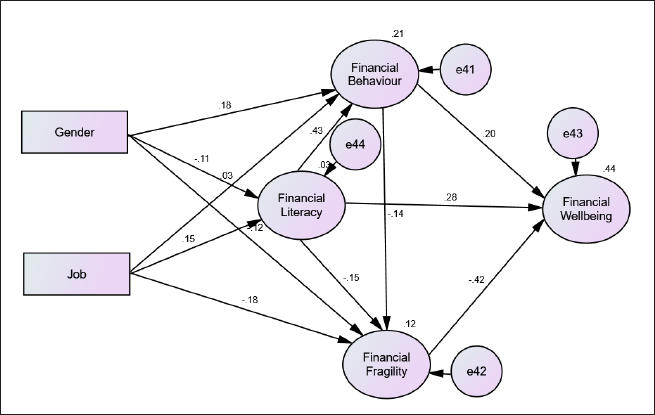

Therefore, our study applies the conceptual framework available in the literature to understand the determinants of financial well-being of IT employees in India. Our findings extend the existing literature onto one of the crucial sectors in India. We utilize the conceptual model derived from the existing literature, as shown in Figure 1. The model includes all the three key determinants of financial well-being, that is, financial literacy, financial behavior, and financial fragility. In addition, we have also included gender and job levels to the conceptual model to understand their impact on financial well-being.

Theoretical Model.

Methods

Data

The study utilizes a quantitative approach to test the hypotheses and conceptual model. An online survey was utilized to collect the information from professionals working in the IT sector in India. Though the online platform allowed a broader reach, majority of the survey responders were based in Bengaluru, the IT hub of India. The initial list of respondents was selected based on direct relationship with the researchers. Further participants were included via references from the initial sample. Responses were collected from professionals working in large IT companies with at least 50,000 employees. These companies included both listed domestic companies and Indian offices to multinational organizations (e.g., Oracle, IBM, etc.). Large organizations were selected for the study as these organizations have structured human resource departments which focus on employee onboarding, training, and long-term well-being. The findings of the study can be utilized to fine-tune the employee training modules within these organizations. Samples were collected from employees across different age groups and job position, covering both technical and managerial positions. The managerial positions included team lead, project lead, and higher management roles involving supervision of the job functions of another person or a group of people. Technical roles are mostly individual contributors possessing specialized skills, working in a team under the supervision of a manager. Technical roles include designations such as software developer, tester, and ERP consultant. The monthly income was also collected to understand whether the impact of FL on FW depends on the income levels. Data were collected during the period from March 2021 to June 2021. A total of 248 samples were collected, of which 11 samples were found unfit for analysis due to missing values. The researchers considered the remaining 237 samples for the final analysis.

Out of the 237 respondents, 78 were female participants and 159 were male participants. A total of 86 respondents were working in managerial positions, while 151 were working in technical role. Majority of the respondents belonged to 20–30 years; the distribution across age groups was as follows: 20–30 years (102), 31–40 years (73), 41–50 years (55), and >50 years (7). The distribution of respondents across the monthly income levels used for the study was as follows: <₹50k (56), ₹50–₹75k (48), ₹75–₹100k (36), and >₹100k (97). The income levels indicate that though managerial roles are supervisory positions, they do not necessarily pay higher than that of technical roles. The IT industry values technical professionals for their expertise in niche tools and technologies.

Instrument and Measures

A survey questionnaire was used to measure the financial well-being and its determinants. Multiple studies previously done in this area have adopted the instrument used in this study . Participants specify their agreement with the statements on a five-point scale (1-strongly disagree, 5-strongly agree). The research constructs and indicators used to collect the information are presented in the Annexure. Structural equations were built using IBM SPSS 25 and AMOS 25 software.

Results and Discussion

Validity and Reliability Analysis

To test the hypothesis and conceptual model, structural equation model based on maximum likelihood estimator was employed, using AMOS 25.

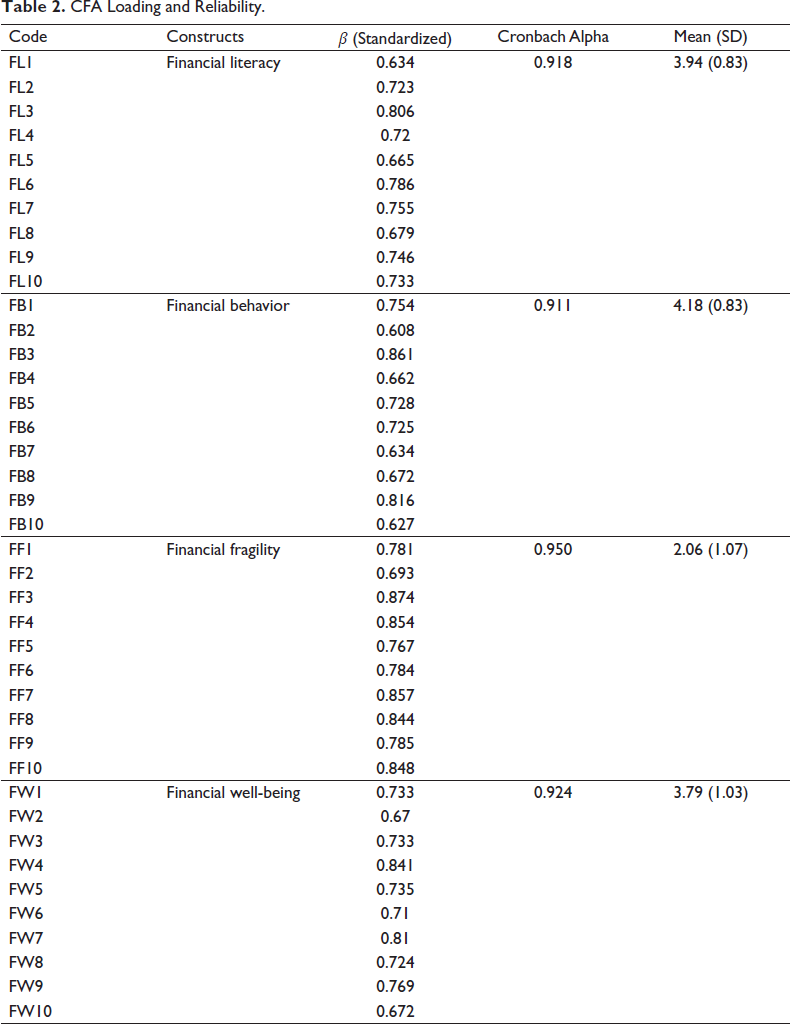

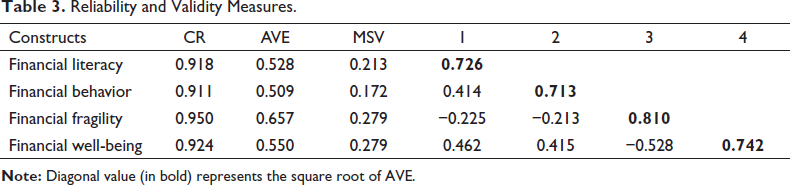

Following the literature on research methodologies for survey-based studies, confirmatory factor analysis (CFA) is used directly to confirm the factors, as there is sufficient evidence backing the scaled used . Before proceeding with CFA, the construct validity, and reliability were validated. Validity is confirmed using both convergent and divergent approaches . The correlation of the variables with the parent construct is confirmed using convergent validity while discriminant validity confirms whether the variables are sufficiently uncorrelated with unrelated constructs. The internal consistency of the instrument is measure using Cronbach’s alpha coefficient (α) . In addition, validity and reliability are confirmed using CR, AVE, and MSV . CR shows the composite reliability, AVE stands for average variance extracted and MSV is maximum shared variance.

As shown in Table 2, the standardized loading estimates (β) are above the threshold level (0.5) for majority of the variables. The composite reliability of the constructs is also confirmed as the Cronbach alpha coefficient is greater than 0.7. The measurement model is evaluated using CR and convergent validity . AVE measures used to validate the construct’s convergent validity should be greater than 0.5. As shown in Table 3, the AVE values for all constructs are higher than the required threshold of 0.5. Table 3 also supports the discriminant validity of the constructs (MSV < AVE and square root of AVE > the inter-construct correlations) . Hence, the validity of the constructs and reliability of the instrument are supported by the above results.

CFA Loading and Reliability.

Reliability and Validity Measures.

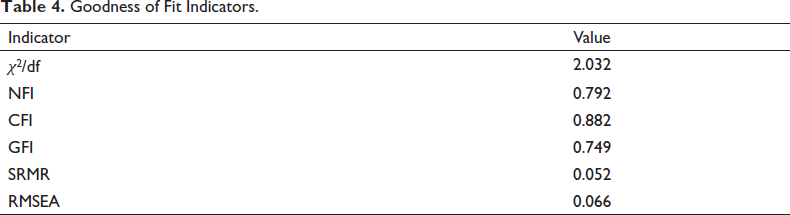

As shown in Table 4, the goodness of fit was checked using commonly accepted indicators such as χ2/df, NFI, CFI, GFI, SRMR, and RMSEA. NFI and CFI are the normed and comparative fit index, respectively. GFI stands for the goodness-of-fit index. In addition, the residual measures are also used to check the goodness of fit. The measures used include standardized RMS residual (SRMR) and RMS error or approximation (RMSEA). The values for goodness of fit measures are shown in Table 5. According to researchers, acceptable range of these indicators for a good fit are as follows: 2 < χ2/df < 3, 0.80 < NFI <0.95, 0.90 < CFI <0.97, 0.80 < GFI <0.95, 0.05 < SRMR < 0.10, and 0.05 < RMSEA < 0.08 . We conclude the measurement model has an acceptable fit.

Goodness of Fit Indicators.

Hypothesis Testing.

Structural Model

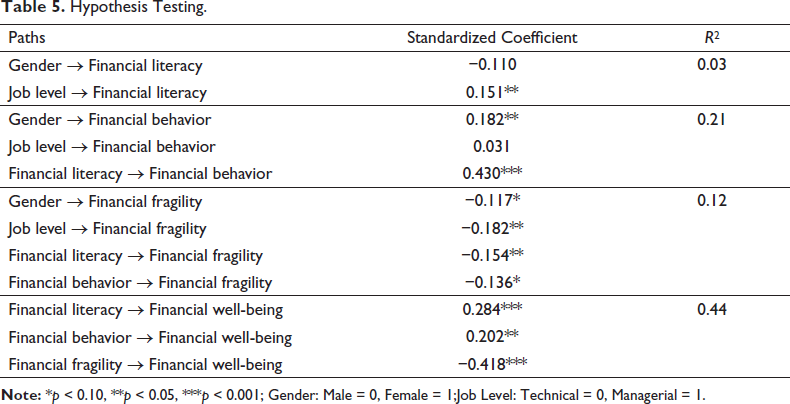

The goodness of fit of the model was examined before testing the hypothesis. The model reported moderate goodness of fit with GFI = 0.746, NFI=0.779, CFI = 0.875, RMSEA = 0.065, SRMR = 0.051, and CMIN/df = 2.001. Figure 2 and Table 5 show the standardized path coefficients (β), error of prediction (e1, e2, e3), and the coefficient of determination (R2). The standardized path coefficient indicates the extent of effect the input factors have on the dependent variable.

Hypothesized Model.

Discussion of Results

As shown in Table 5, gender and job level together explain 3% of the variations in financial literacy levels. The low R2 shows that there are variables beyond gender and job level which could have an impact on financial literacy of IT employees. However, as the objective of this study is to understand the impact of gender and job levels on the financial literacy of IT employees and not to build a predictive model, we accept the low R2. The input variables of financial behavior, that is, gender, job level, and financial literacy, together explain 21% of its variations (R2 = 0.21). Financial fragility depends on other factors in addition to gender, job level, financial literacy, and financial behavior as the R2 is just 0.12. These factors could include personality traits, cultural background, financial stability, and so on. The results show that financial literacy, financial behavior, and financial fragility can together explain 44% of the variations in financial well-being. This provides motivation to further understand the impact of these variables on financial well-being.

From Table 5, we can also conclude that gender has a significant impact on the financial behavior (β = 0.182) and financial fragility (−0.117) levels of IT employees in India. Whereas, the gender variable has no significant impact on the financial literacy levels of these employees. The standardized regression coefficients need to be interpreted keeping in mind that male gender has been used as the base variable. The positive coefficient of gender on financial behavior indicates that female IT employees have significantly better financial behavior than male counterparts. This augurs well with the existing literature which shows that women being comparatively more risk averse exhibit better financial behavior than men . Further, Indian women have also been shown to more particular in making budget and keeping track of household finances . Though there is no significant difference between the two genders on financial literacy, the financial fragility of women IT employees is significantly lower than male counterparts. This has been explained in the literature using psychological models and social norms . India being a conservative country, men are expected to shoulder financial responsibilities and this might be enhancing their financial fragility.

The results also indicate that the job level also has a significant impact on some of the variables considered. The job level has a positive impact on financial literacy (β = 0.151) and a negative impact on fragility (β = −0.182). Interesting, there is no significant difference in the financial behavior of the two categories. The study classifies IT employees working in technical profiles as the base variable, while those working in a managerial capacity are coded 1. Using this coding criterion, we can interpret the positive relationship between the job level and financial literacy as follows: the IT employees working at managerial levels have significantly higher financial literacy levels than those working in technical levels. Considering organic progression from technical to managerial roles, the employees working in managerial levels are expected to have higher experience in handling finances. This experience could have exposed them to financial products, markets, and instruments which could explain the difference in financial literacy levels between the two job categories. Similarly, the managerial level employees have significantly lower financial fragility levels than the technical staff. The relationship could be explained using the significant negative relationship between financial literacy and financial fragility (β = −0.154). The better knowledge of financial products and markets equips the managerial professionals to be better prepared for handling financial issues. This preparedness improved their financial fragility. This result is largely in consensus with the existing literature which rejects the hypothesis that higher awareness of financial products and markets has no impact on the fragility levels among working people.

The significant, negative impact of financial literacy on financial fragility is shown by the regression coefficient of financial literacy (β = −0.154) on financial fragility. Financial literacy has a significant positive impact on financial behavior (β = 0.430) and financial well-being (β = 0.284). The results indicate that better awareness of financial products, systems, and markets improves the financial behavior and financial well-being of IT employees. As the literature indicates that financial well-being is a significant determinant of employee well-being, these results provide support to incorporating financial literacy within the broader employee welfare campaigns. Such campaigns could also support in enhancing the financial behavior of their employees since as per the findings of the study, financial behavior has a substantial negative influence on financial fragility and a considerable positive influence on financial well-being. To put it in simpler terms, improving the financial behavior of an IT employee reduces the financial stress while enhancing their financial well-being. This finding is again in consensus with the existing literature on working employees . The steps to improve the financial stress levels, that is, lower financial fragility, is important as it has a significant, negative impact on financial well-being of IT professionals in India.

To conclude, the financial well-being of IT employees in India is significantly impacted by all the variables considered in the study. Financial literacy and financial behavior have a substantial positive effect on financial well-being whereas financial fragility has a substantial negative impact. Hence, the IT companies based in India would need to design welfare campaigns targeting all the three significant determinants of financial well-being. Further, we understand that gender and job levels also play a significant role in determining the levels of the three base variables, that is, financial literacy, financial behavior, and financial fragility. Hence, there is a need to differentiate the campaigns based on gender and job levels. The practical and theoretical implications of the study are discussed in the following section.

Conclusion

This study attempted to understand the factors contributing to the financial well-being of professionals in the IT sector, one of the largest job providers, in India. The findings of the study indicate a close dependence of financial well-being on financial literacy, financial behavior, and financial fragility. Financially literate individuals demonstrate healthier financial behavior resulting in lower financial fragility and superior financial well-being. Furthermore, gender and job level have a significant influence on the factors affecting financial well-being.

Financial well-being is shown to be a critical factor leading to overall well-being of employees. The results of this study have significant policy implications while devising programs, campaigns, and strategies intended at advancing financial well-being of IT professionals, which could lead to long-term productivity enhancements and lower attrition levels. To the best of the authors’ knowledge, this study is the first attempt to understand the factors contributing to the financial well-being of IT professionals in India. However, the authors are aware of the limitations of the study. The primary limitation of the study is that the sample used for the study is dominated by responses from the IT hub of India, Bengaluru. IT sector has started extending to Tier-2 cities such as Ahmedabad, Mysore, Thiruvananthapuram, Pune, Coimbatore, and Vizag. Post COVID-19 IT employees are also preferring to work in locations closer to their home town. The factors leading to the financial well-being of employees working out of the Tier-2 cities could be quite different from that of employees located in cities. Hence, the findings of this study cannot be extended to Tier-2 locations. Another limitation of the study is that it covers employees from large IT companies with at least 50,000 employees in India. These organizations have structured human resource departments which focus on employee onboarding, training, and long-term well-being. IT industry in India also includes companies employing less than 10,000 professionals and start-up organizations working on niche sectors. However, these sub-sectors are not included in the current study. With start-up IT and fintech enterprises mushrooming in India, the financial well-being of their employees will be an interesting area of future research. Future research can also extend the limited number of demographic variables used in the study to include age, income levels, educational qualifications, and number of dependents.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.