Abstract

‘Disconnected capitalism’ is a thesis defined and developed in Work, Employment and Society. This article contributes to the sociology of work by further developing the thesis both theoretically and empirically. The article does so by specifying how accounting practices enable investor-owner managers to take money out of firms with detrimental consequences for workers. Empirically, this development of the thesis is based on four case studies where the theoretical and empirical contributions add to the thesis by highlighting a contemporary dialectic in light-touch regulation that is illustrated by these studies. The article is important because the further development of the thesis provides an analytical device that illustrates how investor-owner managers take advantage of moral hazard provisions in light-touch regulation enacted by the state to deliberately exploit and strategize these provisions through management accounting strategies.

Introduction – Taking money out of a business

As a contribution to the sociology of work, this article provides new knowledge in a theorization and empirical specification of the disconnected capitalism thesis (DCT). The article addresses the following research questions: first, how can contemporary firm-level owner-manager investors ‘take money out of a business’ disguising this in sophisticated accounting strategies at the expense of a wider group of stakeholders, principally labour? Second, to what extent are investor-owner managers and the firm-level managers they appoint a distinctive form of corporate agency? To do so, the article divides into four parts: first, in terms of theory, the DCT is developed as an analytical device where ‘taking money out of a business’ appears as a contemporary logic of control for investor-owner managers to strategize the appropriation of value from the already earned income of creditors and workers. Moreover, the focus on capital-labour social relations and structural antagonism in the employment relationship illustrates the role of the state in ‘light-touch’ regulation and the logics that condition investor-owner manager decision-making. This focus is central to the sociology of work because it examines how regulation by the state enables sophisticated patterns of labour exploitation in some contemporary workplaces. Regulatory permissiveness condones and underwrites the negative consequences that follow on from the application of secured creditor status, use of credit default swaps, refusal of and/or re-negotiation of creditor bills or debt write-offs by strategic use of administration. The second part of the article outlines the methodology that bridges the theoretical treatment in part one and the findings in part three. The empirical material in part three presents four case studies to illustrate how investor-owner manager choices appropriate value and result in a series of detrimental outcomes for labour. The cases and the theoretically informed method develop the ‘taking out’ argument to illustrate how contemporary strategies that return monies to investor-owners evolve to disconnect a business where financialization is the prime mover that informs change in mature capitalism. Last, to go beyond the ‘so what’ question, a connected discussion of these strategies informs a conclusion that highlights the limitations of light-touch regulation for workers and the autonomous strengths of light-touch regulation for disconnected investor-owners.

Theory – Disconnected capitalism – Financialization and labour outcomes

This article provides a contribution to new knowledge through a theorization and empirical specification of ‘disconnected capitalism’, a thesis defined, developed and elaborated on in this journal. The theorization focuses on ‘taking money out of a business’ as a contemporary manifestation of disconnected capitalism that is a contemporary form of financialization. To do so, the theorization reviews influential contributions in the development of the broadly defined disconnected capitalism thesis and how they connect a regime of accumulation centred on financial capitalism to the priority of short-term returns to investors.

The DCT theorizes a model of capitalism that stratifies the business system, the firm and vogue human resource strategies termed ‘high performance’ workplace systems, into separate disconnected layers (Thompson, 2003). The original contribution by Thompson is outlined at a high level of abstraction but delivered a first conceptual innovation for specialists in the sociology of work and employment – financialization. The theorization developed herein outlines how new forms of financial competition commodify contemporary labour returns, and historical labour returns, as a disconnected source of value to business owners, investors and managers effectively as a windfall. For example, investor-owner managers may choose to place employees in an associated holding company with few assets, thereby disconnecting a business brand from its employees to boost financial returns. By association, as the extant literature demonstrates, systematic demands for investor returns assume a central role in preventing operating firm managers from keeping their side of the workplace bargain. For example, Appelbaum et al. (2013) demonstrate how curtailment of investment in staff development and high-performance employee resourcing at EMI led to a flight of human capital that undermined the business.

A second contribution to the development of the DCT theorized changing patterns of business ownership and how these speed up the demands of capital. This is so because new types of institutional business investor, in particular those who developed the private equity business model, focus exclusively on short-term returns to investor-owners (Clark, 2009). These returns predominate over wider stakeholder interests including those of employees, creditors, suppliers or the community that hosts a business. Such short-termism may witness new majority investor-owners in listed businesses or those that they have taken private unilaterally change agreements with trade unions but avoid transfer of undertaking regulations because a change in majority ownership is different legally to a change of ownership. These unilateral decisions come at a cost to labour but provide a return to investors; for example, in the sale and lease back of business equipment and premises (which in the event of a business sale may leave employees with no equipment to work with) or terminations of final salary pension schemes (that undermine and reduce employee wages in retirement). For example, Georgen et al. (2014) provide an extended treatment of the DCT outlining how institutional investor-owners disconnect and break up established business practices and associated employment relations agreements with correspondingly negative effects on employee interests.

A third contribution refined the financialization component of the broader DCT by providing detailed content that theorized changes in contemporary business practice for industrial capital and banks and in human resource practices (Lapavitsas, 2011). Across these behaviours, a wider articulation of the pervasive influence of financial markets describes a systematic transformation of mature capitalist economies. Both industrial capital and labour in financialized economies rely less on banks and are now directly involved in financial activities in their own right. Examples of this include auto manufacturers encouraging buyers to switch to personal finance plans for leasing cars or homeowners re-mortgaging an appreciating property asset to fund consumption expenditure. Therefore, banks and other financial institutions operate as market mediators looking to enable capital and labour to financialize their own assets. These refinements provide a more detailed theoretical framing of three tendencies in financialization under neo-liberalism: labour market de-regulation and the retreat of labour, the financialization of non-financial firms and the development of the mediation role for financial institutions and the financialization of personal revenue across classes (Lapavitsas, 2013: 36–43, 173–174).

A fourth contribution examines inter-connected domains in and around capital to outline an expansive theorization focused on institutional inter-relations (Thompson, 2013). In terms of accumulation, the focus is on how a particular pattern of financial capitalism dominates and informs the demands of capital. In turn, financialization leads to a specific model of corporate coordination and power relations dedicated to securing returns to investors and shareholders. Lastly, in terms of employment relations practice, new investors and associated business models challenge the embeddedness of national institutional structures. This contribution is influential because its empirical specification provides greater theoretical rigour; however, this remains abstract because reference to underpinning empirical material is general rather than case specific.

The mechanisms of financialization do shape business and workplace outcomes for labour, and more recent contributions to the literature demonstrate this empirically and connect contemporary accumulation regimes to these outcomes. For example, a study of Siemens shows how managers at the firm shed elements of its liberal, coordinated country of origin characteristics, its Germanness. The firm’s management did so to adopt aspects of financialization and prioritize returns to investors through a policy of externalization that witnessed some subsidiary operations re-domiciled in liberal market economies. This enabled Siemens to take advantage of business and labour market de-regulation and effectively mimic strategies associated with institutional private equity ownership beyond its base in Germany. That is, return monies to these investors rather than share them between wider groups of stakeholders (Berghoff, 2016). Moreover, advocates of firm-level financialization – institutional investors backed by hedge funds or private equity funds – further disconnect from a host of business embedded trends such as the spin-off of successful divisions. Instead, spin-off divestments appear as a global trend centred on the disintegration of conglomerate firms; for example, after the financial crisis of 2008, these investors in General Electric concentrated on the development of its financial services arm, GE capital, that remained profitable. However, the demands of institutional private equity owners that financed General Electric pushed for divestment of GE capital. This was so even though it weakened the remaining business and undermined job tenure and terms and conditions for many workers, developments that were massaged as a re-alignment of organizational resources (Smith, 2017).

A fifth contribution in the extended theorization of the DCT examines the effects of institutional investors in non-financial businesses in firm-level measures and does so empirically. This presence specifies financialization as greater than a focus on new investors associated with hedge funds and private equity funds. Across non-financial firms, it is the priority afforded to accounting strategies at firm level by these owners that provides a causal connection between abstract theorization of accounting practices and empirically informed outcomes for labour (Cushen and Thompson, 2016). It is critical to recall that the dominance of hedge funds and private equity funds in the UK flows from the extensive de-regulation of finance during the 1980s (Pendleton and Gospel, 2014: 86–111). One result of this is that less patient investment funds with a focus on short-term returns own more shares in businesses domiciled in Britain (12.8%) than more patient individual investors (12%) and traditional pension funds (1.4%) (Office for National Statistics (ONS), 2022: 4). This pattern of ownership creates two disconnecting effects at firm level: financial engineering informs investment decisions to normalize regular patterns of corporate restructuring referred to as control financialization that in turn informs profit financialization – focused on squeezing labour costs (Baud and Durrand, 2012). Both forms take money out of a business exacerbating and reinforcing the presence of work insecurity and work intensification as labour outcomes that disconnect but shape business and workplace outcomes for labour through accounting practices. The disconnection between investor-owner managers that run businesses, associated accounting practices and labour outcomes is made wider and more anonymous because 56% of shares in quoted firms in Britain are owned and managed by investors or their proxies beyond Britain in the rest of the world.

Method

To take money out of a business has the potential to undermine a business as a going concern, with extended detrimental consequences for labour. The method proceeds through four theoretical and two empirical developments that locate these as a contemporary component of the DCT. First, the management of labour as a commodity is now one of several sources of value to business owners, investors and managers. Second, the commodity status of labour as a source of value is particularly so where innovative investor-owners disconnect, and break up established business practices and associated employment relations agreements. Third, a theoretical framing of non-financial firm and household activity in finance informs a systematic transformation of mature capitalism where these firms too focus operations on finance rather than on production or supply of services.

Practices that take money out of a business require specific empirical illumination to provide explanatory power that explicitly connects financialization to the shape of workplace outcomes for labour. Therefore, fourth, these processes flow from the value logics of accumulation regimes, for example, under financial capitalism the priority of returning money to investor-owner managers; in turn, accumulation regimes inform new corporate structures that disconnect established institutional structures. Fifth, by empirical association, it is accounting practices that connect and ground the theoretical abstraction of financialization to observable outcomes for labour at firm level. However, labour remains a central value producer whose role is not always recognized in productive capital – in corporate re-structuring in and beyond the workplace. The light-touch regulatory framework fostered by the state enables anonymous investor-owner managers to remove monies from a business with the knowledge that such removals can undermine the viability of a business but disconnect this from negative outcomes for workers.

The conceptual refinements described above are derived from the review of significant contributions to the DCT to enable a theorization that connects or disconnects financialization detrimental empirical outcomes for labour at the workplace. The latter flow from a strategic choice to take money out of a business. These strategies are connected because the discourse that describes them abstracts the practices from and gentrifies what they really mean as accounting practices. A dividend recapitalization, for example, loads debt onto a firm via borrowing some of which investor-owners and managers receive as either fees or a special dividend. Similarly, an employer pension holiday borrows against a pension scheme, passing these funds to investor-owners and managers instead of a pension scheme. However, these strategies require specific empirical analysis if financialization is to provide explanatory power that explicitly connects an accumulation regime to detrimental outcomes for labour. To provide this, the empirical method draws on original research provided by the author to the Department for Work & Pensions inquiry into the collapse of British Home Stores (BHS), the Parliamentary inquiry into the collapse of Carillion and formal evidence submitted to the National Audit Office (NAO) report on the collapse of Thomas Cook. This material included additional archival research using open access secondary source materials such as House of Commons (HC) inquiry reports (2016, 2018), reports from The Pension Regulator (2014, 2018) and the National Audit Office (2020), and also included primary source empirical material from interviews with workers at each of the four case study firms and with financial journalists. In each case, the arguments presented have an evidence base that is clear and beyond inference. There is also public interest in each case because taxpayer money had at some stage protected the incomes of workers and some of the monies owed to creditors. Therefore, as each firm is subject to official scrutiny it is appropriate, fair and reasonable to name them in an academic and scholarly treatment such as this one.

Findings: The appropriation of value and labour outcomes at BHS, Carillion, Flybe and Thomas Cook

The cases illustrate how financialization enabled investor-owner managers to appropriate monies and disconnect value already generated in the production or supply process, taking it out of a business. Investor-owners divert these monies to themselves where the distinction between extraction and appropriation is significant. Extraction refers to the re-allocation of contemporary resources (e.g. profits to buy back shares) where some stakeholders – usually investors and shareholders – gain disproportionately from trading their investments. Alternatively, investor-owner managers may secure windfalls following on from share buy-backs that raise the value of existing investments. In contrast to these situations, the appropriation of value refers to the theft of resources already historically allocated to and earned by some stakeholders – usually labour – and the diversion of these revenues – for example, employer contributions into a final salary pension scheme – to investor-owners. Management accounting strategies applied by investor-owners after the creation of value by labour appropriate a portion of this already-created value. The use of dividend re-capitalizations, interim dividend payments to investors, employer pension scheme payment holidays, secured creditor status and credit default swaps enables financial appropriation where the implication of each is significant if the investors are the owners and managers. The following sub-sections outline findings on each case study.

British Home Stores (BHS)

In 2000, Philip Green acquired BHS for £200 million and immediately sold it to an opaque offshore nominee-holding vehicle, Taveta 2 investments, owned by the Green family, thereby disconnecting BHS’s ownership structure from its British operations. Over the next four years, investor-owner managers at Taveta 2 pursued a policy of control financialization that saw £307 million taken out of the business and returned to the Green family in dividends, dividend re-capitalizations and lease-back deals for property (HC, 2016: 5). In terms of profit financialization, Green appropriated value from BHS by an aggressive and creative use of limited liability and debt that returned employee income monies nominally allocated to employer pension contributions to investor-owners instead (Shah, 2018: 150). At acquisition, BHS pension funds had a £43 million surplus, but by 2009 the deficit was £166 million and in 2012, when Green began looking for a buyer, the deficit was £233 million. Green was unable to sell because the Pension Regulator stated that a proposed business re-structure contained significant moral hazards; if the re-structure failed or BHS went into administration its pension liabilities would be transferred to the Pension Protection Fund (PPF), which Green and his colleagues knew to be the case. Therefore, they had no incentive to make the plan work by reducing control and profit financialization, or the debt they owed to the pension schemes (HC, 2016: 14: paragraph 31). However, while the regulator identified the potential problem, they were unable to prevent the course of action set in train by the investor-owner managers. To avoid these difficulties, in January 2015, Green shelved the re-structure and sold BHS as a going concern to Retail Acquisitions for £1.

As a statement of its control financialization intentions, Retail Acquisitions appropriated – took out of the business – £7 million on its first day of ownership to pay advisers, its board, associated salary costs, transaction management fees and to buy two yachts. Retail Acquisitions also disconnected all profitable assets from BHS, transferring these to its (disconnected) ownership independent from BHS, appropriating £11 million as profit financialization in fees and salary costs in its 13-month ownership of BHS. Retail Acquisitions assumed responsibility for BHS pensions but made no payments into the schemes, so by April 2015 when BHS entered administration the deficit was £571 million. The 20,000 employees who were members of the schemes and former employees who received payments from the schemes faced an uncertain future. A resulting inquiry by the Department for Work & Pensions exposed Green’s actions but Green stated he had no responsibility for BHS pensioners in a personal capacity – which was the case precisely because of the strategies of the investment vehicle’s contractual disconnection, financial appropriation and divestment. However, on behalf of BHS’s investor-owners (mainly the Green family’s investment vehicles), in May 2016 Green made a voluntary payment of £363 million to the two insolvent pension funds. Under the payment, staff received on average 80% of full benefits. The 9000 scheme members with funds of less than £18,000 received cash settlements and the other 10,000 members received 80–88% of original entitlements in a new scheme. This represents up to 20% wage theft by the two owners of BHS, as the payment made by Green was less than the value appropriated from the business.

Carillion

Carillion was a large multinational construction and facilities management firm that entered compulsory liquidation in January 2018 owing £2.6 billion to its pension funds and £2 billion to 30,000 suppliers. Carillion’s collapse was shocking as it was in contradistinction to its 2017 accounts that auditors signed off in July as ‘fair and true’ when the firm paid a record dividend of £79 million (HC, 2018: 14–17). The theorization of disconnected capitalism outlines how non-financial businesses such as Carillion may choose alternatives to producing goods or supplying services and act more like financial market mediators. At Carillion this choice centred on returns to investor-owners and significant amounts of profit and control financialization that followed on from aggressive accounting practices, debt funding, divestment and downsizing of the business described as a ‘dash for cash’ (HC, 2018) rather than investment in expanded production. Therefore, Carillion’s business became subordinate to a management strategy of financialization. The latter disconnected the facilities management part of the firm from internal financial dealings (aggressive accounting practices) to provide a major component of profits (see Fine, 2014 who elaborates this theorization). A cross-departmental Parliamentary inquiry quantified the scale of monies taken out of the business finding clear examples of control and profit financialization; the former re-structured the business via aggressive accounting practices, including citing ‘uncertificated’ revenue as actual revenue (HC, 2018: 42, 88). Uncertificated revenues are those subject to agreement with clients and contractors that remain untraded – that is, subject to contract between them. Similarly, Carillion’s aggressive policy of 100+ days late payments to contractors and suppliers enabled the firm to over-book revenue. In contrast to this, profit financialization reduced both contemporary and historical labour costs as senior investor-owner managers declined to pay appropriate monies into final salary pension schemes in 2016, branding such payments as ‘a waste of money’ (HC, 2018: 4, 19–24). The firm financed its returns to investors via £2.6 billion of debt borrowing against the value of its pension scheme, where limited liability provisions protected investor-owners who borrowed £2.6 billion to pay a similar amount in dividends – that is, the money they choose to take out of the firm.

Carillion’s investor-owners diverted employer pension fund contributions to dividend re-capitalizations and interim dividend payments to themselves. The House of Commons report also found that senior manager investor-owners at Carillion acted purely in their own self-interest and in alignment with their personal incentives to test the checks and balances (moral hazard provisions) on corporate conduct (HC, 2018: 86): directors rewarded themselves and other shareholders by choosing to pay out more in dividends than the company generated in cash despite increasing borrowing [. . .] and a growing pension deficit.

For balance, it is necessary to make clear that at BHS and Carillion pension fund trustees and the Pension Regulator made representation to investor-owner managers, asking them to improve the level of provision (HC, 2018: 56–58). However, the obfuscations that followed these requests demonstrated the feeble nature of the regulatory regime in the face of significant moral hazard flowing from management action (HC, 2018: 73, 80). The trustees could see what was happening but were powerless to stop it. The PPF assumed liability for Carillion’s pension fund debts to 27,000 scheme members, making the level of wage theft from workers past and present significantly greater than that at BHS. This means, first, that all appropriately funded schemes contribute to the failure of this scheme to protect the general capitalist interest and, second, because of the shortfall in the funds recovered, Carillion fund members receive lower payments than those agreed. This represents historical wage theft from already earned income similar to that imposed on BHS pensioners. Moreover, the frailty of the regulatory framework enabled investor-owner managers at Carillion to reverse the principal–agent relationship and take strategized advantage of moral hazard provisions effectively built into the regulatory framework. The state provided a subsidy to errant capital in the processes of light-touch regulation.

Flybe

Flybe was a British-based regional airline. In 2010, the firm floated on the London Stock Exchange and in 2019 was sold to Connect Airways, a private consortium supported by three dominant investor-owners whose managers oversaw the business: Cyrus Capital hedge fund, Stobart Aviation and Virgin Atlantic. In 2020, Flybe entered administration when it soon became clear that its structure enabled these investor-owners to secure both profit and control financialization by taking money out of the firm. First, the three investor-owners invested only small amounts of cash, with the majority of their stakes made up of assets. Stobart Aviation, for example, invested only £7 million in cash, with the rest of its 30% stake in the firm made up of £43 million of leases levied on Flybe for airport equipment and aircraft leasing operations – that is, paid by Flybe to Stobart Aviation. More significantly than this, both Cyrus Capital and Virgin Atlantic protected their more sizeable assets through ‘secured creditor status’, enabling them to protect and secure the majority of the £135 million of assets they provided to Flybe. Secured creditors are often banks, but in this case, Cyrus Capital and Virgin Atlantic are asset-based lenders to the business and held a fixed charge on business assets that they manage. By registering these charges at Companies House, Cyrus Capital and Virgin Atlantic appear as both investor-owners and (secured) creditors, effectively separating these assets from the business. This dual status inverts the notion of limited liability wherein investors can lose all their investment, enabling them instead to protect their investment more fully than unsecured creditors. Unsecured creditors such as employees and sub-contractors must apply for protection in government-backed support schemes or via the administrator.

A second way in which Flybe’s current and more particularly its previous investor-owners appropriated value from the firm was in the disconnection from the business and re-domiciliation of its final salary pension scheme. The scheme has 1300 members, some of them retired and some of them employees made redundant when the firm entered liquidation. The scheme though is beyond the jurisdiction of the United Kingdom and Great Britain PPF because of its registration and domicile in the Isle of Man. The Connect Airways consortium of investor-owners knew this and the extent of the pension fund deficit when they acquired the business. As this is a recent case, it remains unclear, although unlikely, that Connect Airways sought to make up the deficit even if they did start to make regular employer payments into the scheme. The potential exclusion of the Flybe scheme from the PPF means that Flybe pensioners may lose all their pensions, a clear example of historical wage theft from labour and a further demonstration of the frailties of the regulatory framework. As in the previous two cases, this potential is so because of the deferred pay status of employee and employer contributions to final salary pension schemes (TPR, 2014).

Thomas Cook

The Thomas Cook Group was a British global travel company formed in 2007 by a merger of Thomas Cook, a German-based business and the MyTravel Group. The firm was a tour operator and an airline and operated travel agencies in Europe. In 2019, the Thomas Cook Group and all its British-based entities (e.g. travel agents) went into compulsory liquidation, leaving 9000 workers redundant.

As the NAO report (2020: 25–26) outlines, at the date of its collapse into liquidation Thomas Cook was subject to numerous personal injury claims from customers. However, managers made a strategic choice not to secure insurance provision against these claims even though the firm’s residual assets were insufficient to cover these claims. Because of this decision, the British Government established a scheme to make ex gratia payments to customers facing the most serious hardship following on from their injuries or illness. In terms of pension provision, the firm’s scheme is unlikely to enter the PPF as it appears to have sufficient assets to provide benefits to its members in excess of protection fund levels – that is, greater than 80% of agreed benefits. However, the impact of liquidation on pension provision remains unclear in 2022.

Investor-owner managers at Thomas Cook received £19 million in pay and bonus payments during its last 10 years of operation, while some dominant investors lost the value of their investment in the firm; however, others, such as Fosun, a Chinese conglomerate investor, bought back some assets at a significant discount from the liquidator. In contrast to this, other dominant investors invested against the collapse of the firm via credit default swaps. While not as extreme as the other three cases, there is clear evidence of profit financialization at Thomas Cook – first, in the strategic choice not to secure appropriate liability insurances and, second, by some of the firm’s investor-owner managers betting on the firm’s failure and insuring against this were creating their own moral hazard. In both cases, the source of profit financialization was self-interest enabled via aggressive accounting policies. Last, the NAO report (2020) into the collapse of Thomas Cook outlines the significance of trailing the firm’s liquidation. In terms of the arguments developed in this article, this slowness enabled investor-owners and managers to either protect (or get out of the business) as much money as possible in payments to managers before the eventual collapse.

Discussion: Extending and refining (the) disconnected capitalism (thesis)?

A new logic of business control and new form of short-termism in British capitalism encourage a dialectic of management that prioritizes the creation of value but also its extraction, appropriation and removal from a firm. It is the associated adoption of new investment strategies and the realization of these as mechanisms to take money out of a firm that connect aggressive accounting practices to labour outcomes. In addition, because value flows from the costs of production, in particular labour, subsequent activity to that delivered by labour cannot create value. Therefore, unlike surplus value and valorization in Marxist political economy or factor returns in the theory of the firm, it is this vague quality of appropriation that disconnects some business failures from what they really are: investor-owner choices to take money out of a business, passing it to investor-owner managers irrespective of a firm’s performance. The practices and strategies associated with taking money out of a business can be more or less aggressive, where the aggression centres on the extent to which management strategies and accounting practices in particular exaggerate the viability of a business.

The British state is a central macro enabler of contemporary business practices centred on disconnected business acquisitions, mergers and takeovers by investment funds in the market for corporate control (Augar, 2009). By association, state intervention to promote de-regulation creates the material conditions that enable a market economy and a market society where social and regulatory relations mimic market relations (Sandel, 2010: 10). In the latter, the values of the market permeate the social relations of production to commodify labour and natural resources, removing the regulation of business from national post-war socio-economic settlements between capital and labour (Polanyi, 1944: 76–80). Rather than displaying embeddedness in actively managed stakeholder approaches, business practice is now permissive where light-touch regulation, centred on de-regulation and flexibility, operate as legal and social norms (Mayer, 2018: 131). De-regulation and liberalization followed by privatization created these norms in Britain’s financial capitalism where an unrestrained market society informs substantial relative autonomy from actively engaged regulation by the state (Miliband, 2021: 88). This is one reason why light-touch approaches utilize regulators, independent light-touch auditors of business accounts and public interest auditors such as the NAO. By operating with relative autonomy, the process of light-touch regulation disconnects the institutions of political domination that constitute the state from economic domination – the capitalist class.

The light touch of the regulatory framework does though contain built-in moral hazard provisions that reverse the principal–agent relationship in some investor-owner managed businesses. Moral hazard describes loss-increasing behaviour that arises under insurance, for example, where the behaviour of a first party changes to the detriment of a second because of a particular decision or transaction by the first party; for example, homeowners who become more relaxed about open fires and smoking in a house once they have insurance (Pauly, 1968). Moral hazards arise in employment relationships when supervisors are unable to observe all actions taken by those employees under their control. This imposes information costs on a business and because of this and the associated potential for shirking by workers, employers frequently supplement simple workplace controls with technical and bureaucratic controls sometimes referred to as surveillance or cultural controls (Alchian and Demsetz, 1972).

By providing conceptual refinement supported by empirical evidence, this article extends the DCT and does so by focusing on the agency of investor-owner managers who install self-governing incentive structures that have the potential to impose costs on a business by taking money out of a firm. The strategic choice to do so enacted by investor-owners and the managers they install not only shapes the operating environment for a business but also reverses the principal–agent relationship of self-interest to create an investor-owner manager moral hazard. Therein, investor-owners and managers take risks knowing that they may undermine a business in the knowledge of state-sponsored bailout provisions. Such behaviour may be particularly prevalent where the state via its regulators provides explicit guarantees even in the face of reckless action by investor-owners; for example, deposit insurance or payment protection schemes. Investor-owner managers can do so because dispersed minority investors are unable to observe the actions of smaller dominant groups or even individual investor-owner managers. Similarly, regulators are unable to force investor-owners or their managers into corrective action on pension fund contribution holidays or use of uncertificated payments that boost the value of a balance sheet. For example, dominant investor-owner managers can sanction considerable reward packages for themselves or associated businesses and following on from securing these returns, if necessary, default on debts. Single or dominant investor-owners can do this via the application of secured creditor status that ‘ring fences’ the value of any investment in a business to protect it from creditors or liquidators in the event of administration.

The disconnecting effects of accounting practices on firm-level financialization are clear at BHS, where aggressive choices by investor-owner managers to return money to themselves undermined the business and for some time its pension scheme too. Managers at Carillion chose to financialize but disconnect the business by citing uncertificated payments and the imposition of three-month late payment agreements to boost its asset base. At Flybe, financialization of business objectives was more sophisticated as new dominant investors chose to disconnect the value of their investments in the main via secured creditor assets that appeared to boost the asset base of the firm when the reality was a very low level of real-cash investment. At Thomas Cook the business was less financialized than the other three cases but both control and profit financialization was in evidence as managers chose not to insure themselves against likely (and known to them) business risks. These measures significantly undermined each business, overstating their financial viability and demonstrating also how empirical outcomes for labour relate back to investor-owner managers chasing investor returns that load debt onto a business.

The methodology of new more aggressive investor-owner managers is also clear in three cases. At BHS, these investors used offshore investment vehicles to disguise appropriation; at Flybe, investor-owners used secured creditor status to limit their liability to less than the full value of their investment; at Thomas Cook, some investor-owners bet against the viability of their own business to reduce both interest in the firm as a going concern and reduce their liability in the case of administration. The four cases also illustrate how new business strategies transform mature capitalism at business system level and firm level. Therein, the financialization of non-financial firms creates the potential for significantly detrimental labour outcomes in three of the cases. At BHS and Carillion, this was clear in refusals to fund employee income liabilities in employer contributions to a final salary pension scheme. Investor-owners knew this course of action would undermine these schemes but chose to continue to return these monies to investors. At Flybe, the frailty of regulatory oversight by the state enabled the firm to disconnect its liability to pension scheme members, significantly cutting contemporary and historical labour costs to both themselves and the state. The re-launch of Flybe in 2021 airbrushed this position in the sale of its residual assets to new investor-owner managers who returned the brand to flying in March 2022.

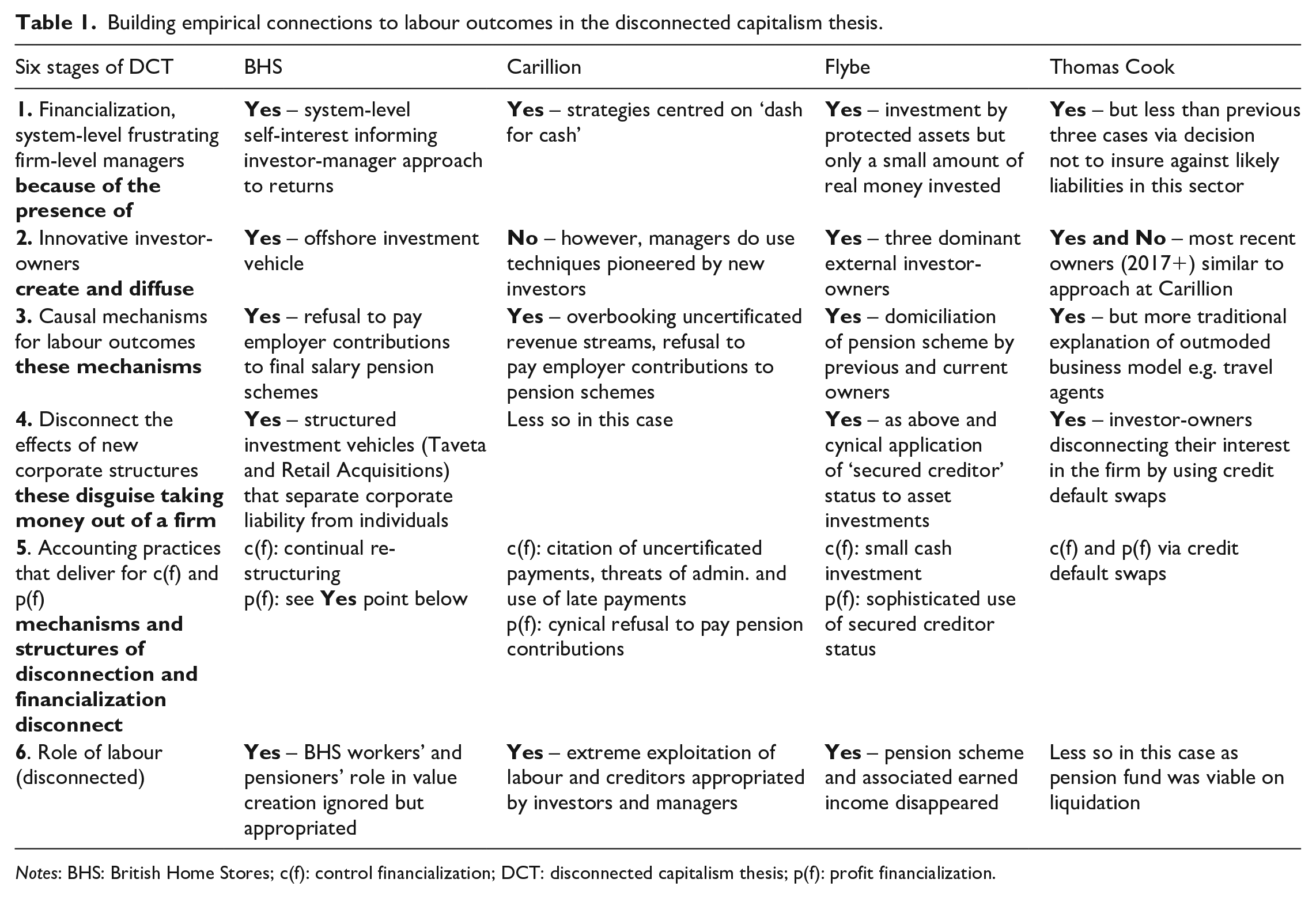

The disconnecting effects of new corporate structures on established practices is clear: at BHS the offshoring of ownership vehicles, at Flybe the offshoring of the pension scheme and at Thomas Cook in moral hazards created by investor-owners betting against the success of their own business. More significantly, though, the theoretically informed empirical material demonstrates how accounting practices led directly to negative dis-connected outcomes for labour and have the potential to undermine the viability of a business. At BHS and Carillion, financialized re-structuring techniques undermined the operation of the business, pension funds and property portfolios. At Flybe, aggressive accounting techniques enabled investor-owners to both overstate the worth of their financial investment and protect, that is contractually disconnect their assets from the business. At Thomas Cook, the use of credit default swaps created a moral hazard wherein investor-owners did not need to consider the business as a going concern. At BHS, Carillion and Flybe investor-owner managers appropriated the role of labour in the success of each business and sought to reduce current and historical labour costs to the business. In each case, moral hazard-bound strategies sought to transfer the liabilities for this already earned income and those of other creditors to taxpayers and other protection schemes. These points of discussion are summarized in Table 1.

Building empirical connections to labour outcomes in the disconnected capitalism thesis.

Notes: BHS: British Home Stores; c(f): control financialization; DCT: disconnected capitalism thesis; p(f): profit financialization.

Theoretically, this article extends and refines each stage in the development of the DCT. For example, whereas Thompson (2003) outlines how financialization frustrates firm-level managers, this contribution identifies how investor-owners either enable or act as firm-level managers to take advantage of financialization. In terms of Clark (2009), they do so because the presence of innovative investor-owner managers appears as a distinctive form of corporate agency that is not necessarily backed by private equity funds or hedge funds. The refinement here centres on the general application and diffusion of accounting strategies pioneered by these investors. Therefore, the causal mechanisms for (detrimental) labour outcomes identified by Lapavitsas (2011, 2013) are potentially in place and as this article establishes can enable favourable outcomes for investor-owners and managers. As Thompson (2013) argues, these mechanisms disconnect the effects of corporate structures that are designed to appropriate value from a business – here the extension and refinement to the DCT focuses on how corporate strategies disguise taking money out of a firm. Cushen and Thompson (2016) identify novel accounting practices as the key mechanism in financialization where the extension and refinement made by this contribution centres on how accounting practices deliver financialization in mechanisms and structures that detrimentally disconnect the role of, returns to and presence and voice of labour in the creation of value.

Conclusion

There is a caveat to this research. Any firm owner can take advantage of debt and limited liability provisions; but the evidence demonstrates that the majority who do so do not divert or securitize employer pension fund contributions to themselves and then enter administration (Department for Work & Pensions, 2018: 12; TPR, 2014: 11; TPR, 2018: 4). However, as the theorization in this article and its empirical underpinning demonstrate, some investor-owners do strategize taking money out of a business and do so by disguising this in sophisticated accounting practices. These under play or disguise the debt component before redistributing appropriated monies to investor-owners.

This article set out to answer two research questions: first, how can contemporary firm-level owner-manager investors ‘take money out of a business’ disguising this in sophisticated accounting strategies at the expense of a wider group of stakeholders, principally labour?

Second, to what extent are investor-owner managers and the firm-level managers they appoint a distinctive form of corporate agency?

On the first question, it is clear that autonomous light-touch regulation by the state enables investor-owner managers to strategize and enact the removal of money from a business rather than invest in the long-term development of a business. This is indicative of the changing scale and nature of short-termism in mature capitalism in Britain. On the second question, a contemporary dialectic in light-touch regulation underpins investor-owner managers who take advantage of moral hazard provisions enacted by the state, connecting these to incentive structures that deliberately exploit these provisions through management accounting strategies.

Footnotes

Acknowledgements

Sincere thanks to three anonymous referees and WES editors Ian Roper and Knut Laaser for their collegial support and comments on drafts of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.