Abstract

The advent of generative AI (GenAI) has caused consternation across the industrial landscape. The financial industry is no exception. The scramble to find GenAI solutions in the financial industry has led to a proliferation in the academic and practitioner literature on the subject. However, the field of knowledge remains scattered. The authors offer four deliverables. First, using a survey of the literature and interviews of managers in financial firms, they create a funnel-shaped, two-stage framework of how GenAI can empower financial businesses. The top stage comprises seven GenAI value propositions for financial firms, condensed into the EMPOWER acronym. The bottom stage includes three functions for each proposition. Second, the authors propose ten novel GenAI-based applications spanning the five verticals of financial services, thus extending the current industrial focus of GenAI applications. Third, they outline the benefits and risks of these GenAI applications, visualizing them in a benefit–risk matrix to assist financial managers in prioritizing these applications. Fourth, they propose research questions to guide academic research and policy making at the intersection of GenAI and finance.

While artificial intelligence (AI) has already changed the way businesses operate, generative AI (GenAI) promises an even more transformative leap (Chui et al. 2023). GenAI—a subvariant of AI (Banh and Strobel 2023)—refers to large language models (Vaswani et al. 2017) that self-learn from vast volumes of data to generate text, image, audio, and video in response to natural language prompts (Bommarito et al. 2023). This ability to create multimedia content through natural language instructions is what makes GenAI transformative (Kumar et al. 2025).

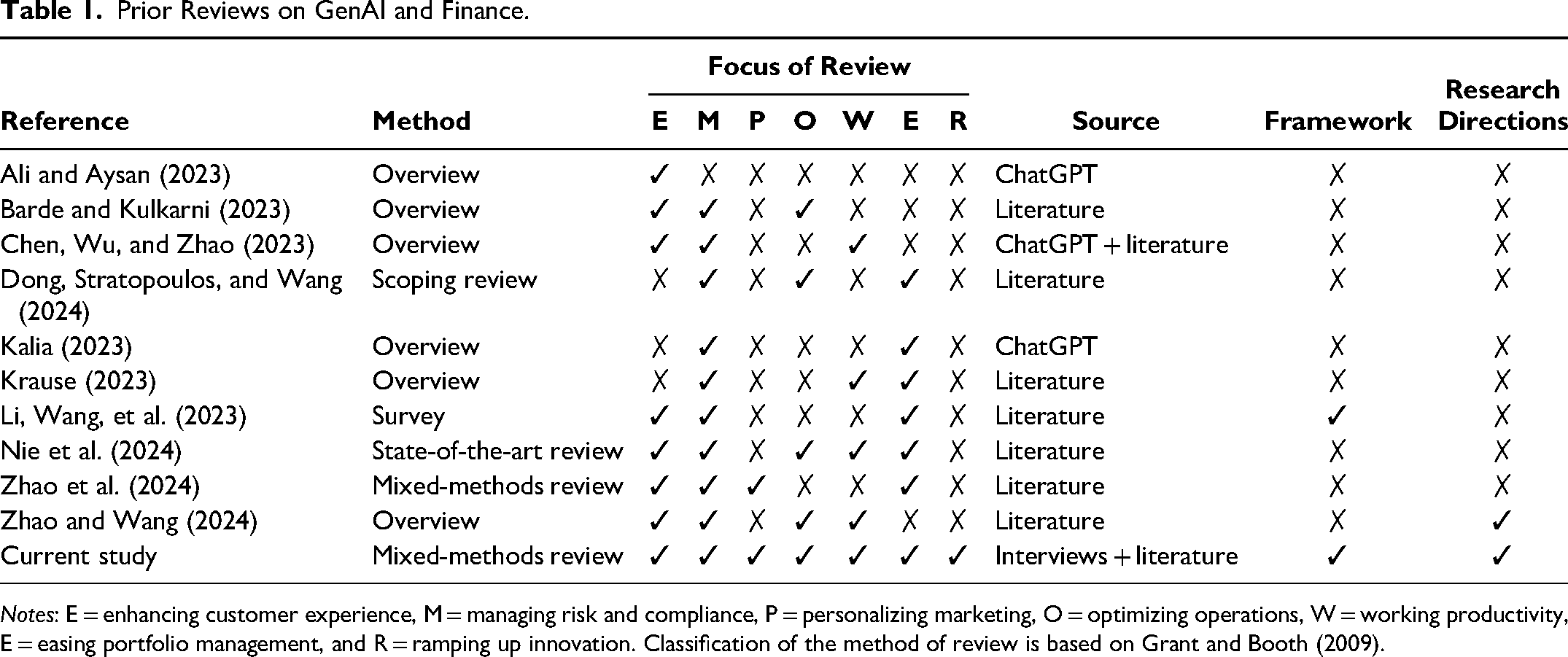

With technology embedded in the core of its business functions, the finance industry is uniquely positioned to harness the power of GenAI (Feyen et al. 2021). Indeed, McKinsey & Company estimated that adopting GenAI in banking could add an annual value ranging from $200 billion to $340 billion to the industry (Chui et al. 2023). Boston Consulting Group considered GenAI a revolution that could disrupt every industry, offering a substantial competitive advantage to industries that choose early adoption (Candelon et al. 2023). Banks have begun to make leaps toward adopting GenAI (Evident Insights 2023). The Evidence Index Report 2023 revealed a remarkable escalation in GenAI-specific roles in the financial job market, surging from just 11 active positions in March 2023 to a staggering 79 by August 2023 globally (Evident Insights 2023). Table 1 compares our article with prior research (all preprints). We analyze the GenAI functions proposed in each paper and compare them with our EMPOWER framework. The comparison helps elicit our article's contribution.

Prior Reviews on GenAI and Finance.

Notes: E = enhancing customer experience, M = managing risk and compliance, P = personalizing marketing, O = optimizing operations, W = working productivity, E = easing portfolio management, and R = ramping up innovation. Classification of the method of review is based on Grant and Booth (2009).

Considerable excitement around GenAI has spurred academic research on the topic. Our review article synthesizes the current state of knowledge and outlines the scope of GenAI solutions for financial firms (Snyder 2019). We also bind prior knowledge into a conceptual framework that helps streamline and structure GenAI solutions for financial firms (Palmatier, Houston, and Hulland 2018). This framework provides a lens through which researchers, managers, and policy makers may analyze the potential of GenAI in finance, identify critical success factors, and frame effective regulation. Further, unlike prior reviews, we adhere to a systematic survey protocol—the PRISMA guidelines (Page et al. 2020)—to ensure the transparency and replicability of our study (Palmatier, Houston, and Hulland 2018; Snyder 2019). In addition, most reviews adopt a technical perspective on GenAI solutions in finance, thus diluting the business focus of the reviews (Nie et al. 2024). We have overcome this dilution by interviewing financial managers, thus lending a strong business focus to our research (Astvansh, Antia, and Tellis 2024; Gioia 2022). Further, given the risks associated with GenAI, we highlight key policy implications and propose a research agenda to guide regulators, researchers, and practitioners.

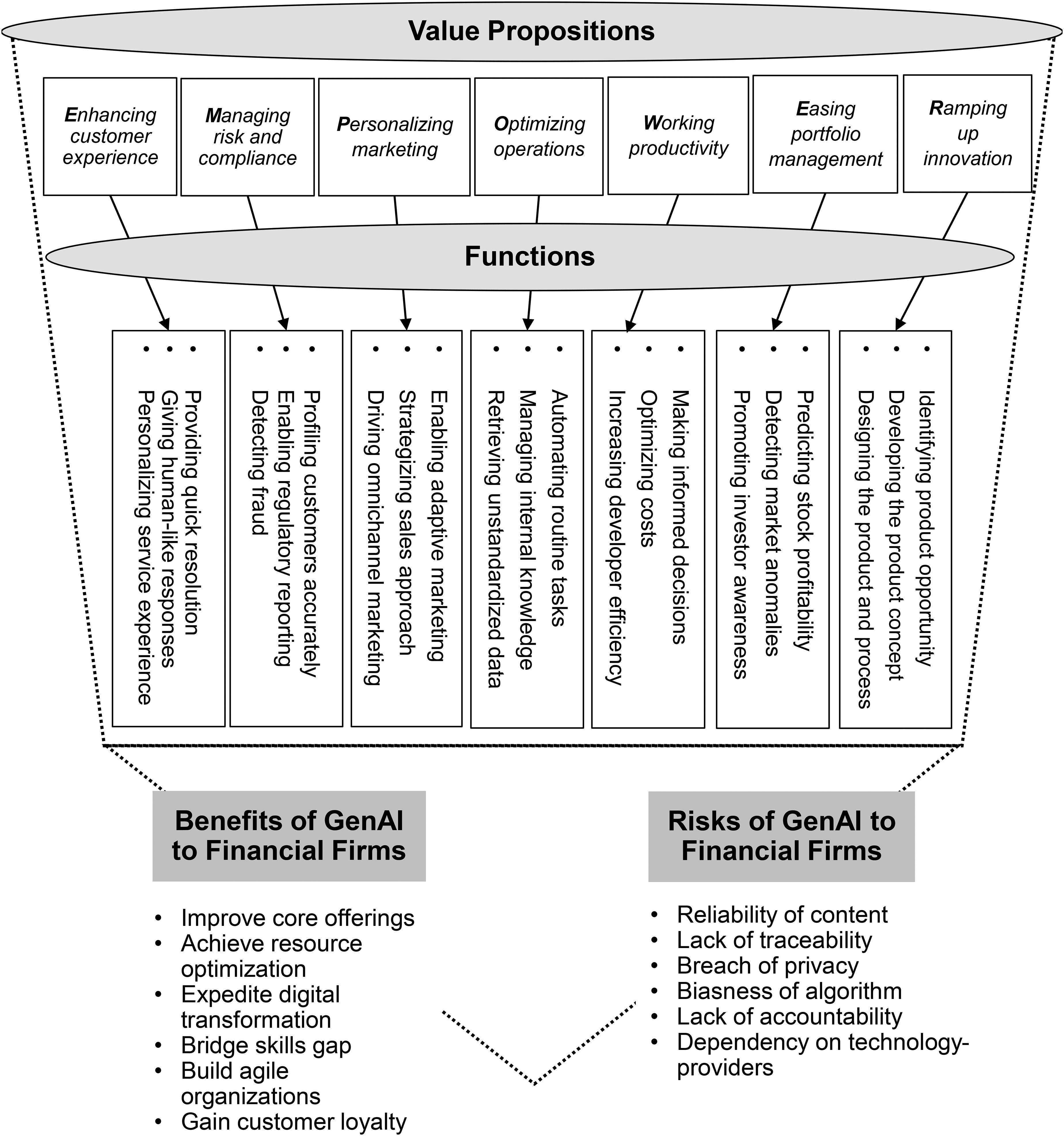

Specifically, we contribute through four deliverables. First, (1) interviews of managers in financial firms and (2) a review of the relevant literature (using the PRISMA 1 method) help us create a funnel-shaped framework of how GenAI empowers financial businesses. The framework (our first deliverable) comprises two stages. The top stage consists of seven GenAI value propositions to financial firms. The first letters of these propositions lead us to create the EMPOWER acronym. The bottom stage includes three functions for each value proposition. Second, we highlight the current applications of GenAI in financial firms and contribute by illustrating ten novel GenAI applications for these firms. We arrange these applications along five verticals of financial firms based on existing classifications. Third, we specify the benefits and risks of the applications. We arrange the applications in a 2 × 2 benefit–risk matrix, which builds on two risk-based principles and benefits accrued from core versus ancillary financial services (Ozment and Morash 1994). Positioning the applications in the matrix allows managers to trade off the benefits and risks and prioritize implementing applications that yield the greatest net benefits. Fourth, we propose three research questions for each of the seven value propositions, flagging key policy implications to guide academic researchers, regulators, and industry stakeholders.

Web Appendix A describes GenAI's evolution and its current uses in finance. More concretely, Table WA1 summarizes the current knowledge at the intersection of GenAI and finance.

Method

We utilize the theories-in-use approach (Zeithaml et al. 2020) that blends qualitative insights from practitioner interviews with the literature to conceptualize emergent themes (Challagalla et al. 2014; Strauss and Corbin 1990). We further enrich the analysis by using secondary sources,—such as corporate reports, magazine articles, and blogs—published by professional firms engaged in or associated with financial business (Astvansh, Antia, and Tellis 2024).

Practitioner Interviews

Sampling and interviews

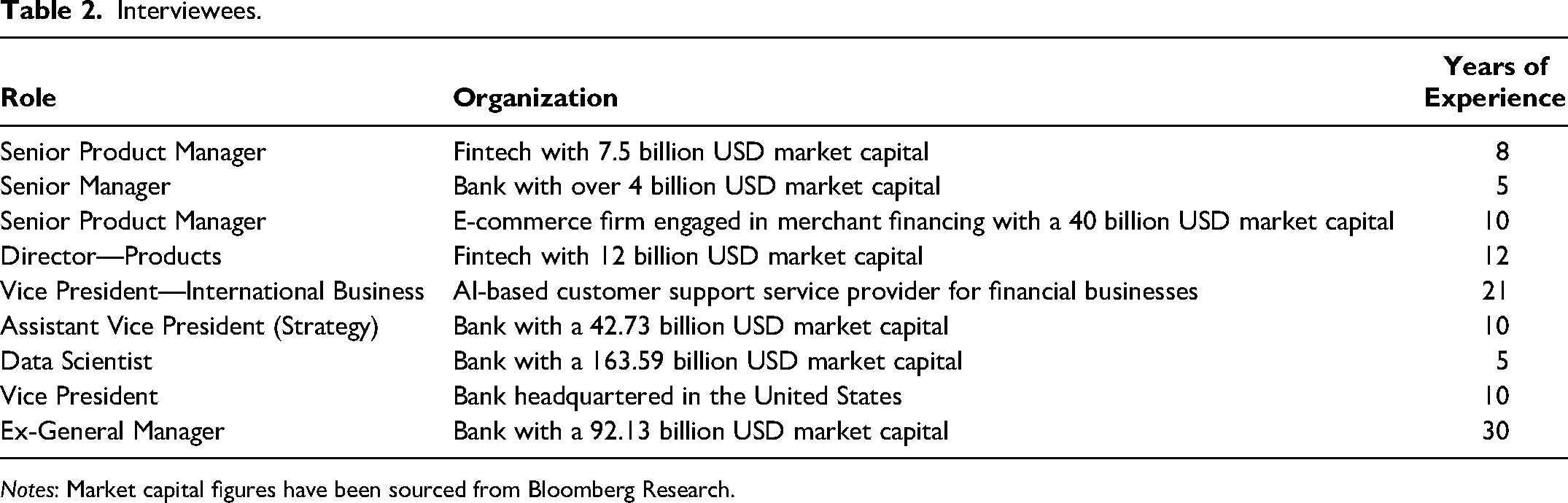

Given the novelty of the research at the intersection of GenAI and finance, we explored the knowledge at this intersection by interviewing managers from the financial industry. The interviews aim to assess the current adoption and prospects of GenAI in financial businesses. We followed an interview approach adopted in prior marketing and public policy research (Astvansh, Antia, and Tellis 2024; Morgan and Zane 2022). Specifically, we used our industry connections to employ purposive sampling in identifying prospective interviewees (Challagalla et al. 2014). We contacted 20 prospects, out of which 10 accepted our invitations, and ended up with nine transcripts, as one remained incomplete. Each participant held a management job title in a prominent financial firm (see Table 2 for sample characteristics). Participants’ industry tenure had a mean of 17.5 years and a range of 5 to 30 years. The participants’ functional backgrounds included finance, economics, and data science, thus offering us broader perspectives (Creswell and Creswell 2018). The first author corresponded with the interviewees between March 2024 and April 2024. The interview protocol was designed to explore GenAI functionalities currently in use, expected to be used, and the benefits and risks that managers see in its adoption by financial firms. The interview included an open-ended, predefined set of questions (see Web Appendix B for questions). The first author followed up on the interviewees' answers to seek clarification.

Interviewees.

Notes: Market capital figures have been sourced from Bloomberg Research.

Data analysis

We followed Strauss and Corbin’s (1990) coding procedure to ensure analytical rigor and transparency in our analysis. The first author coded interviewees’ answers to (1) Gen AI tools their organization is using or may use and (2) business functions these Gen AI tools may serve. Following Gioia, Corley, and Hamilton (2013), we elicited 40 tasks that GenAI can perform for financial firms. Next, we grouped these tasks into GenAI functions. Last, we combined the functions into Gen AI's value propositions for financial firms (see Table WC1 in Web Appendix C for our detailed coding scheme). We ensure the reliability and accuracy of our coding procedure by enlisting two external reviewers who independently coded the transcripts. Codes had an interjudge reliability of over .80, well over the .70 threshold for exploratory research (Rust and Cooil 1994).

Database: Search and Screening Protocol

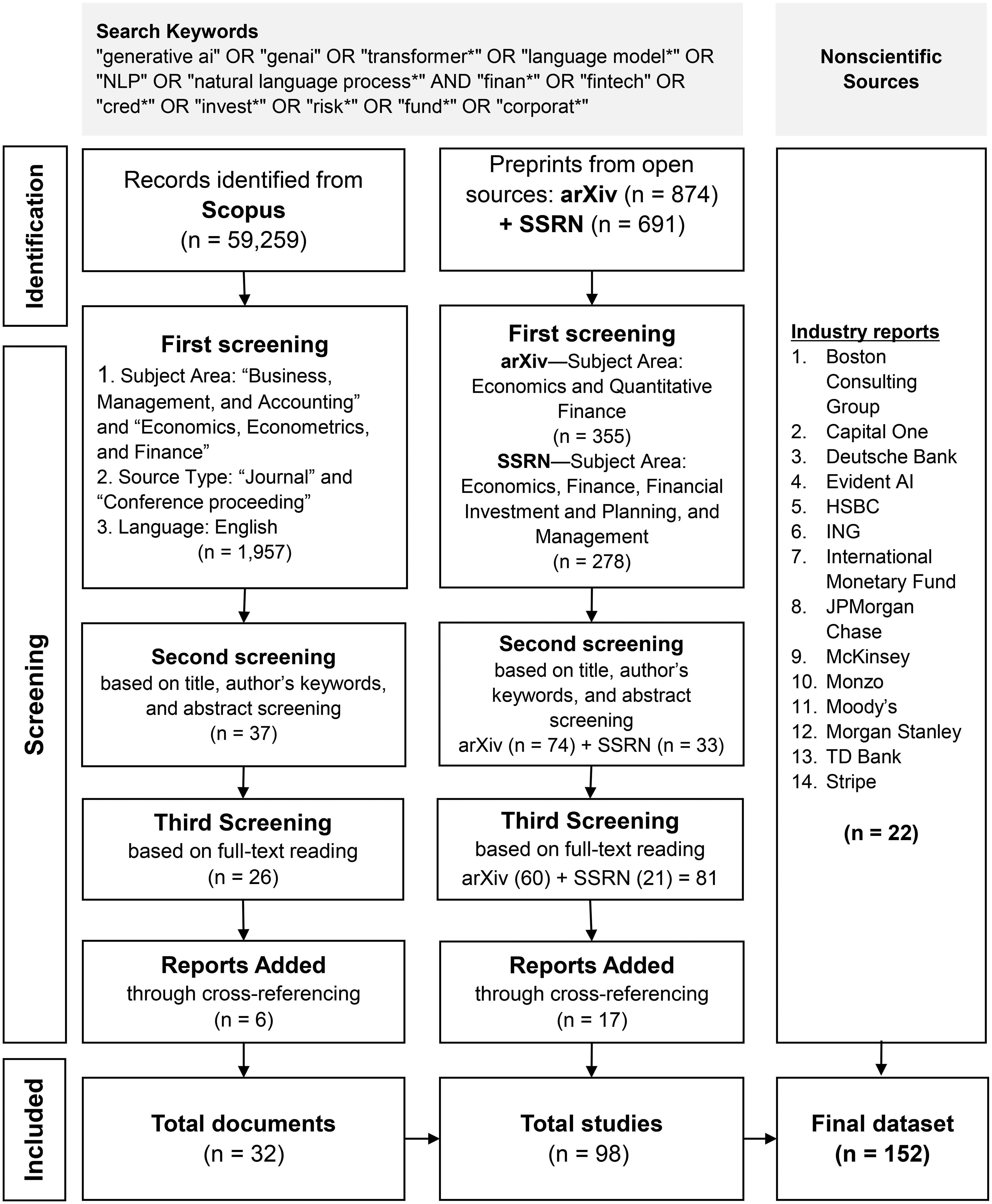

Our search and screening of manuscripts followed prior marketing studies’ quality criteria (Astvansh, Antia, and Tellis 2024; Jorzik et al. 2024). We selected Scopus because it is the largest academic research database, containing 95% of peer-reviewed articles (Donthu et al. 2021). Next, we searched the Scopus database for published manuscripts and conference proceedings with the keywords “Generative AI” and “fin*.” We read the resulting articles and included them in our search string comprising frequently appearing author-specified keywords (see Figure 1). We included journal articles from the Australian Business Dean Council-listed A* and A or rated 4*, 4, or 3 by the Chartered Association of Business Schools (Kraus et al. 2022). Further, we included papers from leading management and computing conference proceedings (Astvansh, Antia, and Tellis 2024). Following Kraus et al. (2022), we excluded (1) documents outside the domain of “Business, Management, and Accounting” and “Economics, Econometrics, and Finance,” (2) book chapters and books because they are not peer reviewed, and (3) non-English documents because English is the academic lingua franca. We read the remaining documents by reading the title, keywords, and abstracts, followed by a full-text reading.

Search Protocol and Screening Criteria Based on PRISMA.

We also searched for preprints on Social Science Research Network and arXiv—two large databases for prepublished literature (Bagchi, Malmi, and Grabowicz 2024). We screened the preprint documents based on the relevance of the subject domain, title, keywords, and abstract. For example, we excluded arXiv documents outside the subject area of “economics and quantitative finance.” We searched SSRN documents in the “economics,” “finance,” “financial investment and planning,” and “management” categories. In addition, we read forward- and backward-cited articles and included relevant documents in our data set. We included all cross-references that we found relevant to the review and that satisfied the quality criteria. We remain abreast of industry developments by supplementing the academic literature with 14 reports from consulting and financial firms and eight web pages—mostly press releases—collectively called industry reports. Subsequently, our corpus included 152 documents, which we analyze next.

GenAI's Value Propositions and Functions in Financial Firms

Practitioner interviews and our academic and practitioner literature review led us to seven value propositions (see Table WC1 in Web Appendix C). The first letters of the propositions form the EMPOWER acronym. Each proposition is implemented via three functions. In the seven subsections that follow, we introduce the value proposition, and discuss the three functions one by one, emphasizing how GenAI empowers a financial firm in implementing the function. (See Figure 2.)

A Funnel Framework of How GenAI Empowers Financial Businesses.

Enhancing Customer Experience

It (GenAI) has helped create chatbots that can curate smart responses based on millions of data points as it's sitting on a wealth of knowledge that a human cannot possibly possess. (Interviewee)

Providing quick resolution

Real-time and relevant responses to customer queries are critical in fostering customer trust in the firm (Adam, Wessel, and Benlian 2021; Huang and Rust 2018). Our interviewees were optimistic that GenAI-enabled chatbots would facilitate swift query resolution and generate intelligent responses, enabling financial firms to enhance customer service efficiency. One of the interviewees noted, GenAI-based customer-facing virtual assistants and chatbots provide instant query resolution.

Giving human-like responses

Compared with predictive AI-based chatbots, GenAI bots have more feeling capacity, enabling them to recognize, understand, and reciprocate human emotions (Huang and Rust 2023). The ability to generate more human-like responses fosters experiential value, intimate consumer–brand relationships, satisfied customers, and positive brand perceptions. In this context, one of our interviewees stated, Our GenAI-based … customer support channel solves customer issues without needing a human agent contact.

Chatbots’ empathetic responses can generate value for a firm by enriching the customer's affective and social experience and engendering loyalty and customer well-being (Liu-Thompkins, Okazaki, and Li 2022). Contextualized understanding of language enables GenAI to adapt its responses to customers (Huang and Rust 2023; Mei et al. 2024). Such responses reciprocating customer empathy could build symbiotic interactions that will be valuable to the firm, strengthening customer satisfaction and the propensity to forgive firms in cases of service dissatisfaction (Huang and Rust 2023; Liu-Thompkins, Okazaki, and Li 2022).

Personalizing service experience

Customer experience can also be enhanced by offering a personalized service experience to the customers (Lo, Ross, and Harris 2024). GenAI's ability to process information and generate responses based on past customer conversations and behavior patterns enables the personalization of the service experience (Fieberg, Hornuf, and Streich 2023). In this context, one of our interviewees responded: GenAI can provide personalized and proactive customer experiences.

Managing Risk and Compliance

Private banks can leverage Gen AI tools to strengthen their risk management processes and mitigate potential financial risks effectively. (Interviewee)

Profiling customers accurately

GenAI can extract and process multisourced unstructured data—text, image, and audio—quickly and accurately (Z. Wu et al. 2023; Zhao et al. 2023). This technological superiority enables investment firms to use GenAI to build a more accurate customer risk profile (Cao et al. 2024a; Yin et al. 2023). Higher accuracy not only ensures more effective know-your-customer (KYC) compliance but also reduces the risk of onboarding potential fraud firms (Moody’s 2024). Indeed, one interviewee quipped: GenAI can be used to manage financial risks more effectively, including credit risk, market risk, and operational risk.

Unlike predictive AI, GenAI can perform context-specific sentiment analysis. Research has shown that contextual analysis of news headlines about commodity price movements can more accurately predict industry-specific risks (Breitung, Kruthof, and Müller 2023). An accurate analysis of industry risks will allow financial firms to dynamically adjust credit provisioning, setting aside appropriate reserves to mitigate the risk of bankruptcy. Similarly, by using GenAI to evaluate semantic discrepancies in managers’ responses to earnings calls, researchers have unveiled potential hidden risks that were undisclosed in the responses (Bai et al. 2023). In related research, GenAI was used to analyze earnings call transcripts to uncover corporate risk by evaluating firm exposure to political, climate, and AI-related risks (Kim, Muhn, and Nikolaev 2023). These capabilities enable financial firms to accurately risk-profile current and prospective customers.

Enabling regulatory reporting

The financial industry is globalized, and businesses must comply with not only national regulations but also global regulatory requirements (Shabsigh and Boukherouaa 2023). Navigating international regulations can be time-consuming and error prone. GenAI's ability to retrieve and process data and generate information makes it particularly adept at the task of regulatory reporting (Cao and Feinstein 2024). Firms can use GenAI to automate report creation, ensuring accuracy and consistency in language and compliance with ever-evolving regulations (Dowling and Lucey 2024). This automation can allow people to focus on core business activities. Our interviewee notes: Gen AI tools can help private banks ensure compliance with regulatory requirements.

Detecting fraud

Financial fraud has been subcategorized into payment-related fraud, bank-related fraud, corporate fraud, insurance fraud, money laundering, and terror financing (Basel Committee on Banking Supervision 2023; West and Bhattacharya 2016). A data paradox constrains fraud detection. The sheer volume of transaction data can generate noise and false positives. Further, the scarcity of fraud-related sample data prevents effective training of predictive AI models to detect fraud (Hilal, Gadsden, and Yawney 2022). In this respect, one interviewee notes: GenAI can be used to detect fraudulent activities, identify suspicious patterns, and assess credit risks more accurately.

Personalizing Marketing

Gen AI tools can analyze users' financial data, investment preferences, and risk tolerance to offer personalized financial planning and investment advice. (Interviewee)

Enabling adaptive marketing

GenAI can transform marketing and sales activities to be more adaptive and data driven. For example, GenAI-based models can craft persuasive messages (Kapoor and Kumar 2024), incorporate customer responses (Huang and Rust 2023), and develop effective sales approaches based on real-time feedback (Sinha, Shastri, and Lorimer 2023). This approach enables GenAI-driven marketing to achieve hyperpersonalization at scale, which is not possible with predictive AI (Jansen et al. 2024). Our interviewee concurred: GenAI tools can be used to provide personalized offers to clients.

Strategizing sales approach

GenAI-powered tools can also be valuable for sales agents working in a highly dynamic, customer-facing environment (Sinha, Shastri, and Lorimer 2023). They can utilize GenAI to obtain a real-time customer feedback analysis by manually feeding responses or using voice-to-text tools (Deveau, Griffin, and Reis 2023). Such analysis could help agents adjust their interaction style and sales pitch based on these inputs, resulting in a more adaptable sales force (Marinova et al. 2017). An interviewee offered examples: Utilizing GenAI for analytics—trend analysis, lead scoring, and lead generation.

Driving omnichannel marketing

Potential customer touchpoints have grown substantially with the expansion of marketing channels. Consequently, omnichannel marketing is crucial in ensuring consistent messaging, as disjointed communication may jeopardize customer loyalty (Mainardes, Rosa, and Nossa 2020). However, data access and integration, and customized content generation have been a challenge, preventing financial firms from achieving successful omnichannel presence (Cui et al. 2021). GenAI models can revolutionize omnichannel marketing for financial firms. One of our interviewees elaborated: GenAI could be used in marketing for generating copies for ads, blogs, (and) social media posts.

Optimizing Operations

KYC verification is one important process of onboarding a business as one of the documentation requirements. Gen-AI has helped make this 10X faster and (more) efficient. (Interviewee)

Automating routine tasks

Financial firms handle volumes of customer data, often involving manual processing of application forms for account opening, KYC norms, and other verification procedures (Li and Vasarhelyi 2024). This manual approach is not only slow but also prone to errors. GenAI-based models can be trained to perform clerical and time-consuming tasks such as invoicing, writing memos, and preparing inventory (Sarmah et al. 2023). The automation of routine work, which currently takes about 60% to 70% of work time, would relieve employees of repetitive and time-consuming tasks (Chui et al. 2023). An interviewee summarized: GenAI would help in managing mundane financial tasks.

Managing internal knowledge

As per McKinsey & Company, tasks mostly involving the application of natural language occupy about 25% of the total work time at financial firms (Chui et al. 2023). These tasks consume a significant portion of employee effort in searching for existing knowledge, piecing together information from various sources, and processing this information to draw relevant knowledge. GenAI-based tools can synthesize knowledge from disparate sources, generating summaries that consolidate key insights and saving employees valuable time and intellectual effort (Zhao and Wang 2024). An interviewee offered us an example: GenAI can be used for the quality monitoring of voice calls in the form of script and summary of each voice call in contact center environment.

Retrieving unstandardized data

Banks often store customer data in siloed servers across branches, leading to the problem of unstandardized data (Berner and Judge 2019). GenAI models can solve this problem. For example, D. Wang et al. (2023) demonstrated how GenAI can decode complex spatial layouts of documents and summarize relevant information in natural language. An interviewee concurred: Gen AI tools help improve data retrieval and documentation verification process.

Working Productivity

Tools will vary by use cases. For example, for colleague productivity improvement, Microsoft Copilot is used amongst several banks—for software development, GitLab is used—several banks are also developing their own proprietary tools. (Interviewee)

Making informed decisions

GenAI-based models could substantially augment employee capabilities through quicker retrieval of information that will enable faster and more informed decision-making (Huang, Wang, and Yang 2023). Financial businesses are training GPT models on proprietary data to cater to their specific needs and offer customized support to their employees. For instance, Morgan Stanley is training GPT-4 to aid and assist its consultants in answering basic investing and financial queries (Q.AI 2023), and BloombergGPT—a 50-billion parameter language model—is equipped to generate short news headlines, answer financial queries, and retrieve financial data (S. Wu et al. 2023). An interviewee told us: GenAI enables managers to extract actionable insights from large volumes of data.

Optimizing costs

Firms are also expected to gain productivity benefits due to cost optimization, as higher workforce productivity would enable the same output level in a short time and with fewer employees (Albrecht and Aliaga 2023). This optimization is consequential because our interviewees viewed cost as a barrier to leveraging opportunities. GenAI-based tools can address this concern by streamlining knowledge management, which is a significant time and resource drain in many institutions (Bommarito et al. 2023). A manager of a private bank agreed with this perspective: GenAI will lead to increased operational efficiency and cost savings for private banks.

Increasing developer efficiency

GenAI is also a powerful tool for augmenting the efficiency of software developers (Kamalnath et al. 2023). Because financial firms depend heavily on software, several interviewees affirmed using GenAI in coding assistance and software development, like GitLab, to streamline software delivery. Other potential GenAI-driven applications could include code generation, automated testing, bug detection, and performance optimization (Banh and Strobel 2023). An interviewee stated: GenAI could serve as coding assistants and [in] software development.

Easing Portfolio Management

GenAI can be deployed in studying market dynamics and current trends in the industry, set portfolio markers and triggers based on the risk appetite of the bank. (Interviewee)

Predicting stock profitability

Several studies have reported GenAI to outperform predictive AI in sentiment classification tasks, thereby predicting stock price movements and returns with greater accuracy (Fatouros et al. 2024; Guo and Hauptmann 2024; Hu, Liang, and Yang 2023). For example, Cao et al. (2024b) demonstrated GenAI's power in analyzing earnings call transcripts—combining text classification, sentiment analysis, and audio segment analysis—to comprehensively understand stock performance drivers. An interviewee who specializes in wealth management offered us the following insight: GenAI tools [are being used] in the front office like [for] wealth management and trading.

Detecting market anomalies

Predicting market anomalies has been fraught with failures and has relied mostly on expert judgments (M. Chen et al. 2023). Signs of market failure are associated with information demand and supply over the internet (Nikkinen and Peltomäki 2020) and characterized by buildup phases leading to market crisis (M. Chen et al. 2023). Our interviewees were optimistic about the use of GenAI in flagging market anomalies. They believed that GenAI could assist in establishing portfolio triggers, thereby facilitating adjustment in investment strategies based on real-time risk assessments (Kim 2023; Liu 2024). One interviewee suggested: GenAI can be utilized to set portfolio markers and triggers, and identify good and bad segments of the portfolio.

Promoting investor awareness

Investor education is another promising application of GenAI. Financial data can be overwhelming and complex, impeding individual investors’ decision-making. GenAI can generate clear and concise summaries of large, abstract data and thus help solve the problem. For instance, GenAI can efficiently summarize complex corporate disclosures and analyze them to predict the direction of a firm's future earnings (Kim, Muhn, and Nikolaev 2024). These summaries may empower investors to draw insights into future earnings, enabling them to manage their portfolios better. An interviewee who advises investors suggested: GenAI can be utilized for providing financial advisory services.

Ramping Up Innovation

By analyzing customer behavior, market trends, and economic indicators, banks can make data-driven decisions, identify new business opportunities. (Interviewee)

Identifying product opportunity

Opportunity identification is crucial for initiating product innovation. GenAI trained on market research data can carry out a comprehensive analysis of multimodal data—text, image, audio, and video—to identify customer pain points and unmet market needs (Feng et al. 2024). An interviewee agreed: GenAI can be used to identify new business opportunities.

Developing the product concept

GenAI can help develop creative product ideas within financial organizations. During the crucial concept development stage, GenAI can overcome the limitations of conventional thinking by analyzing vast volumes of data—including market statistics, competitor offerings, and customer reviews—to produce a holistic analysis and draw meaningful insights on product conceptualization (Bouschery, Blazevic, and Piller 2023). An interviewee who specializes in customer insights offered us the following insight: GenAI can classify product users into segments and conceptualize products accordingly.

Designing the product and process

GenAI can offer valuable assistance during the product and process design stages. GenAI-powered models can effectively assess patent value and the likelihood of patent acceptance by analyzing complex data sets through text embedding techniques, enabling the estimation of the quality and impact of a product invention (Yang 2023). An interviewee told us: GenAI can aid in brainstorming go-to-market strategy for products, writing product requirement documents, [and] understanding product user segments.

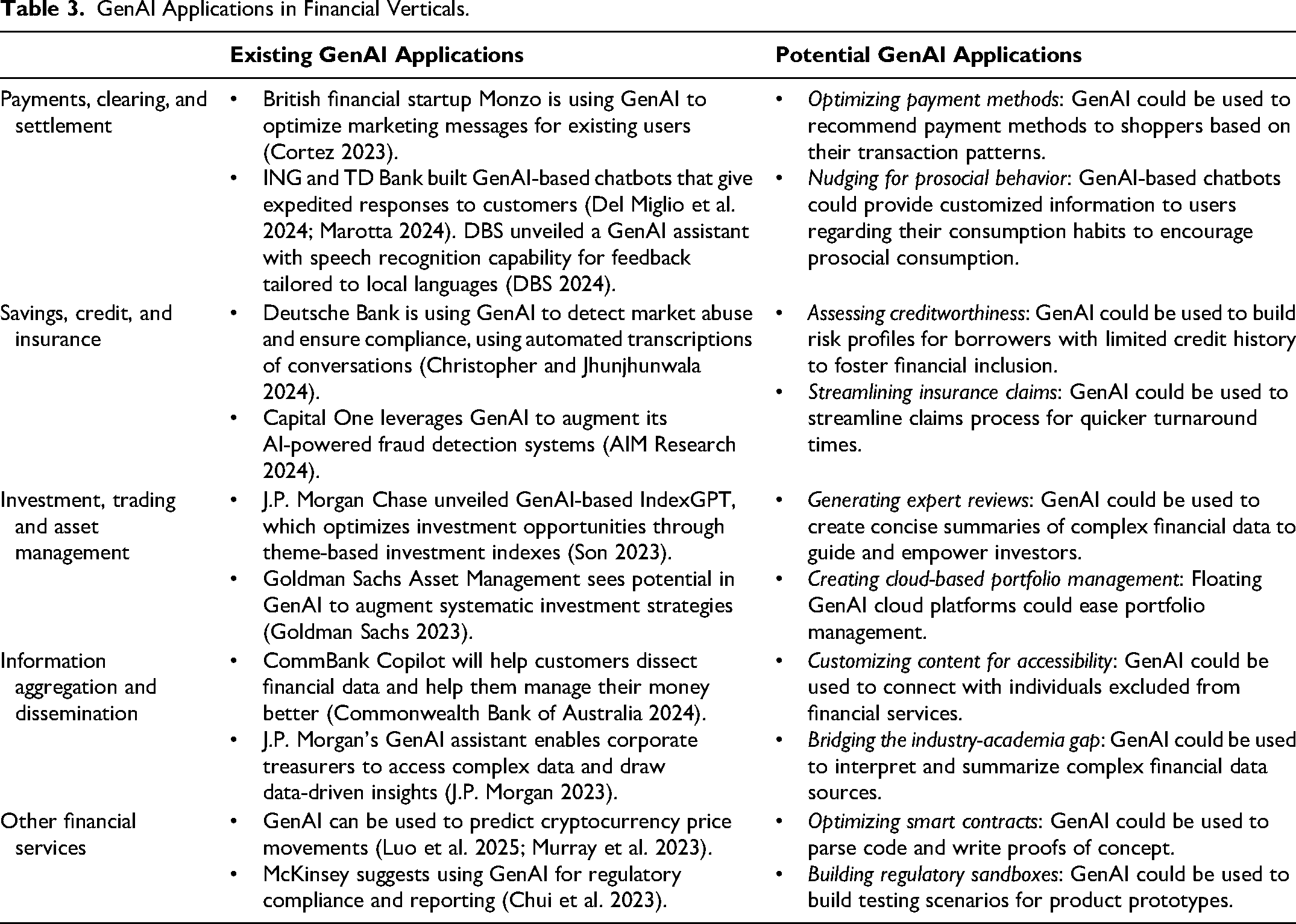

Gen AI-Based Applications in Five Financial Verticals

Next, we prescribe GenAI applications along five verticals of financial services (see Table 3). These applications are based on a current snapshot of GenAI use cases and we expect them to change as the technology evolves. The five verticals are based on industry classification (Ehrentraud et al. 2020), literature (Eickhoff, Muntermann, and Weinrich 2017; Gomber, Koch, and Siering 2017), and our manager interviews. We exercised our judgment in plotting the applications based on the interviewees’ responses and current literature. Two interviewees—each a senior financial manager—checked and approved our matrix.

GenAI Applications in Financial Verticals.

Payments, Clearing, and Settlement

Firms providing services within this vertical process payments, clear transactions, and settle funds (Eickhoff, Muntermann, and Weinrich 2017). Currently, GenAI applications provide expedited and tailored customer services. We suggest extending applications to optimize the payment cycle and promote prosocial consumption.

Optimizing payment methods

Financial firms can use GenAI to recommend a payment method to shoppers based on their purchase history, credit score, and payment preferences (Huang, Wang, and Yang 2023). More concretely, fintech apps can use the value and volume of the transaction, potential reward programs, or cashback offers tied to specific payment methods and suggest the most optimal payment method to a shopper. Shoppers would be spared the need to manually select a payment method, optimizing their payment process by reducing one step from it. This streamlined process could increase transaction volume and enhance shopper satisfaction by prioritizing convenience and maximizing potential financial benefits.

Nudging for prosocial behavior

Based on data on the spending profile of a customer across different periods, GenAI can provide detailed spending analysis to the customer within the payment application (Bommarito et al. 2023; Huang, Wang, and Yang 2023). In addition, through real-time analysis of the consumption patterns, GenAI can provide customized information to the customers regarding their consumption habits, potential benefits and risks of their consumption behavior, and suggestions for optimization of their consumption patterns (Vaghefi et al. 2023). When fed to GenAI models (Pasch and Ehnes 2022), consumption data can promote prosocial consumption patterns among customers by inducing moral nudges in the form of summaries of the environmental impact of their purchases (Vaghefi et al. 2023).

Credit, Deposit, and Insurance

The savings, credit, and insurance businesses offer services such as risk management, credit extension, and insurance provision (Thakor 2020). Current applications include detecting market fraud and ensuring regulatory compliance. We propose applications to facilitate financial inclusion and optimize insurance claims.

Assessing creditworthiness

Traditional credit-scoring models rely mostly on credit history, making it difficult for individuals new to the financial system or those from underserved communities to access loans (Feng et al. 2023). By processing information from multiple data sources—such as mobile phone usage patterns, utility bill payments, and social media activity (with user consent)—GenAI can create a holistic profile of an individual borrower (Feng et al. 2023; Z. Wu et al. 2023). For instance, Sanz-Guerrero and Arroyo (2024) demonstrated the potential of large language models in credit risk assessment by leveraging loan application data from peer-to-peer lending platforms. This demonstration enables the creation of nuanced risk profiles, even for borrowers with limited credit history. Imagine a lender using GenAI to assess a loan application based on the applicant's record of paying utility bills, even though the applicant has no credit history. Such assessment empowers financial firms to broaden their reach and offer essential financial services such as savings accounts, credit products, and insurance to underserved populations (Sanz-Guerrero and Arroyo 2024).

Streamlining insurance claims

Processing insurance claims takes time, involves much documentation, and is often subject to various types of fraud, including forgery of data and overstatement of claims (Hilal, Gadsden, and Yawney 2022). GenAI tools offer significant benefits for insurance companies. GenAI can streamline the claims process through faster document processing, leading to a shorter claim turnaround time (Telnoff et al. 2023). Multimodality enables generative models to process a variety of data—such as text, image, and audio evidence—associated with claims to detect potential fraud and mitigate its risk (Li et al. 2025). In addition, the use of GenAI tools can expedite document generation during the claims cycle, benefiting the insurance company and the claimant (D. Wang et al. 2023). The ability to retrieve information more accurately and quickly from unstructured data sets is particularly valuable because claim details often come in an unstructured format (Telnoff et al. 2023), making GenAI a powerful tool for accurate claim evaluation.

Asset Management and Trading

Financial firms offering this basket of services engage in investment advisory, portfolio management, trading platforms, and asset allocation strategies (Ehrentraud et al. 2020). We look beyond the existing focus on efficiency to emphasize democratizing financial information and scaling GenAI applications through cloud integration.

Generating expert reviews

Expert stock and trading reviews are invaluable resources for individual investors, informing their investment strategies. However, time constraints and resource limitations often hinder financial experts’ ability to produce timely reviews. Carlson et al. (2023) presented a potential solution, where they trained a transformer-based model on review data to generate human-like, unbiased expert reviews for the wine and beer industry. Financial firms can adopt this approach. GenAI models can be trained on a rich data set encompassing industry reports, regulatory filings, and online data (Lu, Huang, and Li 2024). By processing this information, these models can generate concise summaries to empower investors and guide their decision-making (Carlson et al. 2023; Li, Chang, and Wang 2023).

Cloud-based portfolio management

Portfolio management is a data-intensive exercise requiring machines to access and process vast data sets in real time (Kim 2023). However, financial firms must host the data on localized servers, which adds to infrastructure costs (Cheng et al. 2022). We propose integrating cloud platforms with GenAI (George 2024). Based on a serverless architecture, cloud-based platforms offer financial firms a cost-effective and scalable solution by providing them with the necessary infrastructure to store and process vast datasets (Cheng et al. 2022). A firm can host its training data set on the cloud server, train the GenAI model on the server, and run the model on an as-needed basis, thus incurring lower fixed costs and controlling variable costs. This control empowers financial institutions to overcome current limitations and enable real-time analysis, faster modeling, and, ultimately, more accurate investment decision-making (George 2024).

Information Aggregation and Dissemination

Firms under the information aggregation and dissemination vertical gather, analyze, and distribute financial data and insights to clients (Eickhoff, Muntermann, and Weinrich 2017; Gomber, Koch, and Siering 2017). We extend the current focus to facilitate the cross-sharing of knowledge across stakeholders.

Customizing content for accessibility

Firms can harness GenAI to connect with individuals who may be excluded from financial services. Low financial literacy is often a barrier to accessing financial services. GenAI can create customized content for readers with low financial literacy (Niszczota and Abbas 2023). Individuals can personalize financial news by prompting their sociodemographic characteristics, such as language proficiency, education, age, location, and occupation. GenAI-based chatbots can tailor the content's complexity and language to resonate with the individual's background and financial literacy (Dong, Stratopoulos, and Wang 2024). GenAI can also create interactive visuals for younger audiences, build custom layouts for accessibility, and incorporate locally relevant contexts in much shorter times, helping achieve scale (Hatamizadeh et al. 2023; Nie et al. 2024). Thus, GenAI can help create a more inclusive financial system by breaking down language barriers and adapting content to different learner levels.

Bridging the industry–academia gap

The chasm between industry needs and academic deliverables has been a long-standing concern. The gap prevents the cross-sharing of knowledge and stops academic research from reaching the industry. We propose that GenAI can bridge this gap (Li, Chang, and Wang 2023). GenAI's ability to understand context enables it to dissect complex linguistic formations in financial data sources, such as journal articles (Niszczota and Abbas 2023). Further, GenAI's ability to generate summary text in natural language allows complex information to be available to practitioners (Li, Chang, and Wang 2023). Financial analysts can access this information through prompts based on their specific needs. Therefore, GenAI can deliver deeper yet simplified insights that facilitate the exchange of knowledge between academia and industry (Kim, Muhn, and Nikolaev 2023).

Emerging Financial Services

Emerging financial services include innovations such as platforms and tools for cryptocurrency management, price forecasting, and risk compliance (Ehrentraud et al. 2020). We propose innovative uses of GenAI for optimizing smart contracts and building regulatory sandboxes.

Optimizing smart contracts

Blockchain is a decentralized distributed ledger that enables trustless transactions through cryptocurrencies (Nakamoto 2008). Transactions on the ledger occur through a consensus mechanism. Smart contracts, which are predefined codes on the blockchain, automate these transactions when specific conditions are met (Buterin 2014). They enable transactions between nodes on a blockchain through a secure and transparent process (Buterin 2014). Currently, high-quality code comments are mostly unavailable for smart contracts, constraining the comprehensibility of the code among developers (Yang et al. 2021). GenAI can help generate quality code comments through effective code interpretation. A related use of GenAI is in auditing smart contracts to test their security and reliability (Du and Tang 2024). Given the volume of blockchain transactions, manual auditing of smart contracts is time-consuming and error prone. GenAI can audit smart contracts by parsing code and writing a proof of concept (Du and Tang 2024). This use case becomes more critical as research has found nearly a quarter of cryptocurrency trades are routed for illegal activities (Foley, Karlsen, and Putnins 2019).

Building regulatory sandboxes

The rapid growth of fintech innovations calls for a critical assessment of their benefits and risks. The concept of a “regulatory sandbox” has been proposed to help this assessment. A regulatory sandbox is a safe space where businesses can test their product prototypes before introducing them to the market. The sandbox prevents the firm from incurring legal costs if the product violates regulatory norms (Financial Conduct Authority 2015). GenAI can help build regulatory sandboxes. These models trained on historical data, prevailing regulations, and contemporary events can generate a diverse range of scenarios for testing new financial products and services (Moody’s 2024). The sandbox allows regulators to assess potential benefits and risks within a controlled environment before real-world implementation. Further, GenAI can analyze vast amounts of regulatory text, highlighting relevant regulations and potential compliance hurdles for the proposed innovation (Cao and Feinstein 2024), streamlining the commercialization process.

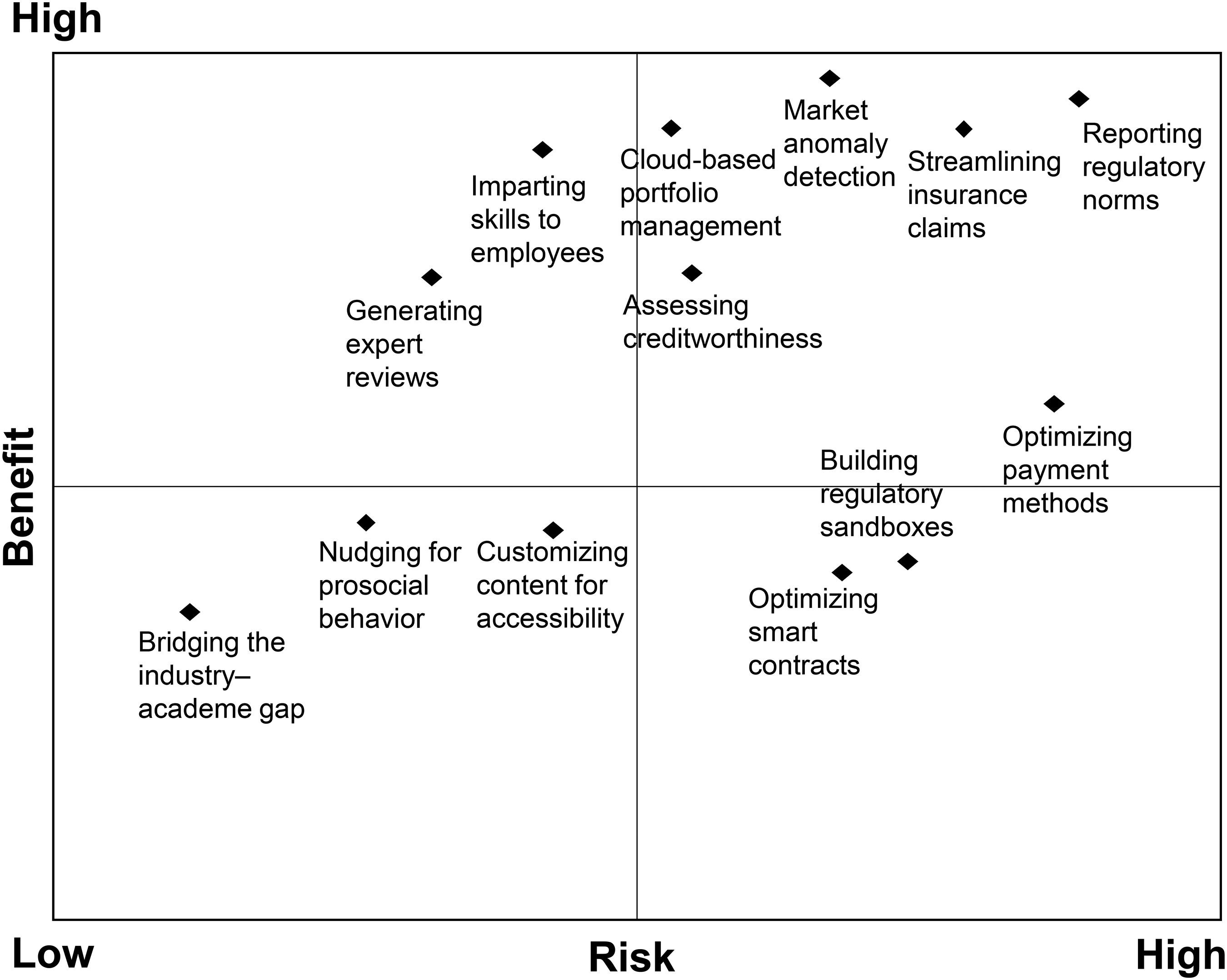

GenAI in Financial Firms: Benefits and Risks

We have thus far focused on the value propositions, functions, and applications GenAI can create for financial firms. We also explicitly asked our interviewees to list the benefits and risks they expect from GenAI-based solutions. While specific benefits and risks may vary based on a firm's core business and target market, some broad themes emerge from our interviews and literature review.

Benefits

Our interviewees agreed that GenAI would help financial firms improve their core offerings. As we explained in the preceding section, these offerings would vary by the firm's core business: for banks, this offering is lending (retail and wholesale); for payment platforms, online payment processing. Augmenting core offerings would help firms sustain competitive advantage. An interviewee commented: The biggest constraining factor is investment—there is always a finite amount and appropriate decisions need to be made on how to allocate limited resources to meet objectives. Building and maintaining AI capabilities requires a skilled workforce with expertise in data science, machine learning, programming, and domain knowledge. Large banks are slow in decision-making—the larger the bank, the more governance structures there are for decision-making, which makes the processes very inefficient and slow.

Risks

We describe the risks next, elaborating on quotes from our interviews. Every piece of code written with the help of GenAI is manually reviewed before deployment since we cannot afford a bug in a product in the financial services domain. So, quality of code development is a risk. (Interviewee)

Misinformation could expose a financial firm to customer lawsuits and cause strategic missteps (Dencik, Goehring, and Marshall 2023). The inherent risks associated with new technologies create resistance to their adoption. Part of this risk—specifically regarding the adoption of GenAI—also stems from the nature and complexity of the technology. Though GenAI partly addresses the issue of the lack of explainability in AI models (Nie et al. 2024), some managers are still uncertain regarding its scale deployment (Lumley 2024). Privacy is a big concern for a typical bank, since consumer data leakage through the model may lead to reputational risks. That is why many banks prefer to run pilots for colleague productivity use cases, rather than client-facing use cases. (Interviewee) I’m worried that during its [GenAI’s] interactions with customers, how can we be 100% certain that it won’t say something offensive, incorrect, or unethical—which may reflect poorly on the brand. (Interviewee) Lack of clear accountability—there may be copyright text or media used as training data for the GenAI foundation model, leading to copyright infringement. (Interviewee) Private banks may rely on third-party vendors or service providers for Gen AI tools. (Interviewee)

Benefit–Risk Matrix for GenAI Applications for Financial Firms

Next, we aim to help financial firms prioritize the GenAI applications by trading off their benefits and risks to the firms. Based on our interviews and a survey of the literature, we developed a 2 × 2 benefit–risk matrix to pursue this aim. This matrix visually depicts the net value of GenAI applications by comparing their potential benefits and risks (see Figure 3).

Benefit–Risk Matrix of GenAI Applications for Financial Firms.

Our matrix uses the following two risk-based principles. First, external-facing applications (e.g., insurance claims processing) are high risk because errors could harm the brand's reputation and expose the firm to legal liability. Compared with external-facing applications, their internal-facing counterparts (e.g., applications for employee learning) pose a lower risk as mistakes can be internally corrected. Second, the purpose of the applications (ancillary vs. core) is key. Educational applications (e.g., generating reviews, cross-sharing knowledge) have a lower risk profile because errors in a financial literacy tool might be a misjudgment in content and can be corrected quickly without affecting user finances directly. In contrast, applications involving core financial services (e.g., market anomaly detection, cloud-based portfolio management, optimization of payment methods) carry greater risk because errors might directly affect customer wealth and could invite legal consequences. Relatedly, applications at the firm–regulator interface (e.g., regulatory reporting, building regulatory sandboxes) carry high risk due to legal ramifications for compliance violations.

Benefits are assessed based on their impact on the firm. We utilize the core and peripheral service-based classification to plot these applications (Ozment and Morash 1994). GenAI applications in core services of financial firms (e.g., saving, lending, investment, trading, insurance) are associated with high benefits, as these may materialize into long-term gains in terms of customer loyalty (Walsman et al. 2014). In comparison, peripheral services (e.g., financial education, nudging), though important, might not translate into long-term benefits if financial firms fail to deliver their core services (Walsman et al. 2014). Relatedly, applications that mitigate operational risks (e.g., fraud prevention, anomaly detection, regulatory reporting) provide high benefits since failure of compliance could lead to long-term costs for firms (Moody’s 2024). Consequently, cloud-based portfolio management, market anomaly detection, streamlined insurance claims, and creditworthiness assessment are categorized as high-benefit GenAI applications due to their focus on mitigating these risks. Similarly, applications that assist financial firms with regulatory reporting provide high benefits due to their potential to ease compliance procedures. Subsequently, applications like nudging, content accessibility, and cross-sharing knowledge have been placed in the low-benefit and low-risk quadrant. Optimization of smart contracts and building regulatory sandboxes have been placed in the low-benefit and high-risk quadrant as, currently, our interviewees do not see high benefits accruing to financial firms from these applications.

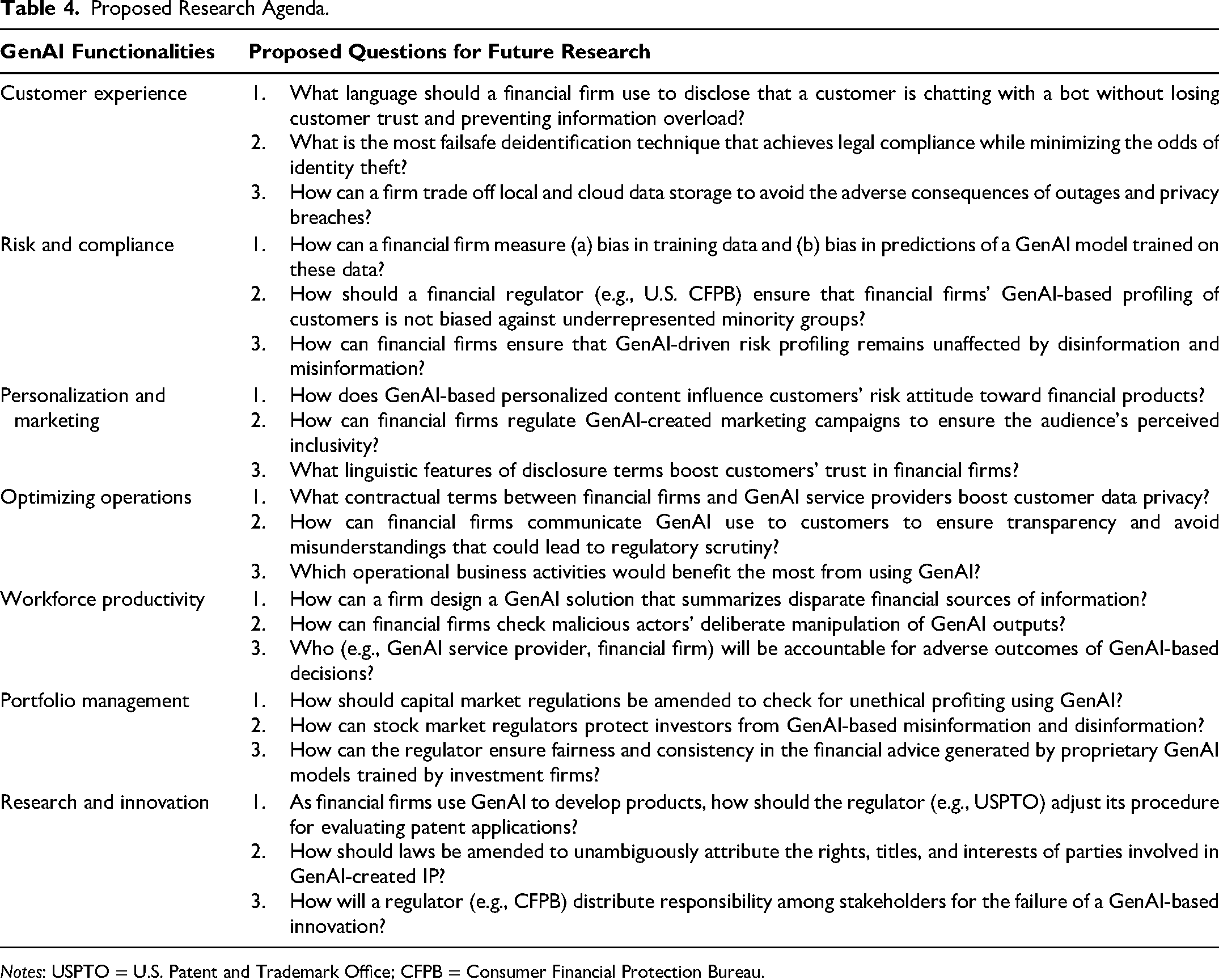

Proposed Questions for Future Research

We propose three questions for future research on each of the seven value propositions. The research questions are also listed in Table 4.

Proposed Research Agenda.

Notes: USPTO = U.S. Patent and Trademark Office; CFPB = Consumer Financial Protection Bureau.

Customer Experience

While interacting with GenAI chatbots, users may be exposed to several risks, amplified by the lack of clear data policies. For example, OpenAI's privacy policy doesn’t state how long the firm will store a customer's personal data (OpenAI 2024). This lack of information is contrary to the data minimization principle—under regulations like General Data Protection Regulations (GDPR) and the California Consumer Privacy Act (CCPA)—which requires firms to delete personal information after a certain period (CCPA 2018; GDPR 2016). Further, Google and OpenAI claim that they anonymize user data before using them to train their GenAI models. However, the firms do not disclose their anonymization procedure (Meta 2024; OpenAI 2024). This nondisclosure curtails customers’ ability to decide whether to use Google's and OpenAI's tools. Therefore, we propose the following questions:

What language should a financial firm use to disclose that a customer is chatting with a bot without losing customer trust and preventing information overload? What is the most fail-safe deidentification technique that achieves legal compliance while minimizing the odds of identity theft? How can a firm trade off local and cloud data storage to avoid the adverse consequences of outages and privacy breaches?

Risk and Compliance

Social media firms, such as Meta Platforms, use information posted on their platforms for training AI models (Meta 2024). This usage raises questions about embedded biases within GenAI models, because vulnerable groups are often subjected to marginalization on social media (Pearce, Gonzales, and Welles 2020)—this could lead to their financial exclusion and run counter to the principles of equity and inclusion outlined as part of the United Nations’ Sustainable Development Goals (United Nations 2023). In addition, GenAI models draw on real-time content on social media platforms. Such content may include disinformation and misinformation, which take time to verify and correct (Biancotti and Ciocca 2021). These bear three specific research questions:

How can a financial firm measure (a) bias in training data and (b) bias in predictions of a GenAI model trained on these data? How should a financial regulator (e.g., U.S. Consumer Financial Protection Bureau) ensure that financial firms’ GenAI-based profiling of customers is not biased against underrepresented minority groups? How can financial firms ensure that GenAI-driven risk profiling remains unaffected by disinformation and misinformation?

Personalization and Marketing

The Federal Trade Commission (FTC) has proposed introducing rules against the misuse of AI, including GenAI, for impersonation fraud. In this context, deepfakes have become a great concern. Deepfakes refer to a person’s artificially generated image or video in which their face or other body parts are digitally altered so that the person looks like someone else. Deepfakes use deep machine learning methods and are generated to spread misinformation about the person. The FTC fears that GenAI may not only proliferate the creation of deepfakes but also enable them to be created with greater precision (FTC 2024). The FTC has flagged the deliberate misuse of design elements in ads to trick people into making adverse selections (Atleson 2023). In addition, financial firms must disclose when an ad is made using GenAI, and customers must know if they are communicating with a human or a machine (Atleson 2023). These concerns lead us to the following questions:

How does GenAI-based personalized content influence customers’ risk attitude toward financial products? How can financial firms regulate GenAI-created marketing campaigns to ensure the audience's perceived inclusivity? What linguistic features of disclosure terms boost customers’ trust in financial firms?

Optimizing Operations

Another regulatory impasse is over the sharing of data with third-party providers. Meta and OpenAI state that they can share the collected information—both provided by a platform user and automatically collected—with their affiliates (Meta 2024; OpenAI 2024). However, regulations such as the GDPR prohibit sharing personal information without the user's explicit consent (GDPR 2016). Currently, there is opacity regarding what information is shared, with whom it is shared, and under what agreements (Ferraro et al. 2023). While GenAI is deployed to manage internal knowledge, the explainability of GenAI-based outputs remains a key concern (Shabsigh and Boukherouaa 2023). In this event, financial firms must be careful of how they use GenAI and, more so, how they effectively report and explain their decisions based on GenAI analysis (Shabsigh and Boukherouaa 2023). This point leads us to three questions:

What contractual terms between financial firms and GenAI service providers boost customer data privacy? How can financial firms communicate GenAI use to customers to ensure transparency and avoid misunderstandings that could lead to regulatory scrutiny? Which operational business activities would benefit the most from using GenAI?

Workforce Productivity

While studies show that workforce productivity improves with GenAI use, the credibility of decisions informed by GenAI remains doubtful. This doubt is due to the lack of traceability—the ability to find the correct source of information for GenAI content (Schneider et al. 2024). The risks of disinformation by malicious actors also threaten the use of GenAI despite self-check features within GenAI models (Ferraro et al. 2023; OpenAI 2024). Another problem relates to the lack of a legal framework that addresses responsibility for faulty decisions informed by GenAI outputs (Moody’s 2024).

How can a firm design a GenAI solution that summarizes disparate financial sources of information? How can financial firms check malicious actors’ deliberate manipulation of GenAI outputs? Who (e.g., GenAI service provider, financial firm) will be accountable for adverse outcomes of GenAI-based decisions?

Portfolio Management

The application of GenAI in portfolio management has significantly accelerated the pace and precision of stock selection and trading. However, this acceleration has also amplified the risk of market manipulation (Shabsigh and Boukherouaa 2023). While GenAI educates investors about stock trading, its autonomous use can potentially lead to losses, as these models are prone to errors (Ko and Lee 2024). In addition, while providing financial advice to clients, firms must disclose the use of GenAI, as FTC guidelines mandate that customers be informed of the use of nonhuman agents (Walsh 2023). This leads us to the following questions:

How should capital market regulations be amended to check for unethical profiting using GenAI? How can stock market regulators protect investors from GenAI-based misinformation and disinformation? How can the regulator ensure fairness and consistency in the financial advice generated by proprietary GenAI models trained by investment firms?

Research and Innovation

Recent lawsuits against OpenAI, GitHub, and Microsoft demonstrate the potential for GenAI models to infringe on intellectual property (IP) rights, such as copyrights and licenses (Walsh 2023). This issue arises since GenAI models utilize large amounts of data without properly attributing the data source (Schneider et al. 2024). Another issue relates to owning the rights, title, and interest of the IP created using GenAI. For example, OpenAI reserves the right to use both the user's input and the output generated (OpenAI 2024). This renders existing IP regulations ineffective at protecting rights of ownership in GenAI use (Ferraro et al. 2023). These legal and regulatory issues must be resolved to ensure responsible and sustainable innovation.

As financial firms use GenAI to develop products, how should the regulator (e.g., U.S. Patent and Trademark Office) adjust its procedure for evaluating patent applications? How should laws be amended to unambiguously attribute the rights, titles, and interests of parties involved in GenAI-created IP? How will a regulator (e.g., Consumer Financial Protection Bureau) distribute responsibility among stakeholders for the failure of a GenAI-based innovation?

Conclusion

Our research fills the knowledge gap surrounding GenAI applications in financial firms. While the enthusiasm for GenAI has led to an increase in academic literature on the topic, it remains scattered, and industry reports lack depth and coverage. Through a combination of literature review and interviews with financial managers, we identify seven key value propositions encapsulated in the EMPOWER acronym. We elucidate three functions for each proposition, demonstrating how GenAI integration can enhance their speed and efficiency. The resulting funnel-shaped framework illustrates how abstract value propositions translate into specific GenAI functions for financial firms. Further, we showcase novel GenAI applications across five financial verticals. We also enumerate the various benefits and risks associated with GenAI applications and visualize a benefit–risk matrix, aiding practitioners in prioritizing GenAI applications across business functions. Finally, we propose research questions flagging key policy implications to guide future exploration in this domain. In sum, the research lays the groundwork for further advancements in GenAI applications within financial firms.

Supplemental Material

sj-docx-1-ppo-10.1177_07439156241311300 - Supplemental material for Generative AI Solutions to Empower Financial Firms

Supplemental material, sj-docx-1-ppo-10.1177_07439156241311300 for Generative AI Solutions to Empower Financial Firms by Shashank Shaurya Dubey, Vivek Astvansh, and Praveen K. Kopalle in Journal of Public Policy & Marketing

Footnotes

Joint Editors in Chief

Jeremy Kees and Beth Vallen

Special Issue Editors

Shintaro Okazaki, Yuping Liu-Thompkins, Dhruv Grewal, and Abhijit Guha

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.