Abstract

Local governments across Europe are increasingly engaging in ‘local government financialisation’, involving the use of bonds, derivatives and financial assets in their governance. However, the extent to which local governments use financial instruments varies across countries. Moreover, local governments engage in financialisation in the context of ‘structuring conditions’ that are largely beyond their control. This paper systematically investigates these political-economic conditions and provides a high-level comparative analysis of their relevance for financialisation in local governments. The study examines data from 22 European countries between 2000 and 2019, finding that economic, financial and institutional conditions, along with financial subordination, are critical in shaping local government financialisation. Specifically, greater decentralisation, a more developed financial sector, and, to some extent, more intense austerity are associated with higher levels of financialisation. In contrast, financialisation tends to be lower in the Southern and Eastern European peripheries. Through its country-comparative approach, the paper contributes a new perspective to recent debates on the role of the local state in financialisation.

Keywords

Introduction

Recently, both academic literature and the media have drawn attention to what can be termed ‘local government financialisation’. This can be understood as local governments using and re-purposing financial instruments and markets to manage their assets and debt (Hasenberger, 2024; Santos, 2023; Whiteside, 2023). A growing body of research offers rich empirical insights into the diverse ways in which local governance in European cities and countries has become financialised (e.g. Beswick and Penny, 2018; Dagdeviren and Karwowski, 2022; Deruytter and Bassens, 2021; Hendrikse and Sidaway, 2014). Although financialisation may appear beneficial from the perspective of individual local governments, it has the potential to reconfigure local decision-making processes and outcomes, raising questions about who gets to have a say, and whose interests are prioritised.

The literature is sometimes criticised for lacking a systematic understanding of the broader drivers of this financialisation, or what Peck (2017: 10) calls its ‘structuring conditions’. These conditions shape the environment in which local governments operate and against which their financialisation unfolds, but over which they have no direct control. Exploring these conditions helps us develop a deeper understanding of local government financialisation, its occurrence and its varying forms across different locations (Christophers, 2019).

The paper makes two main contributions to our understanding of local government financialisation. It presents the first systematic overview of the structuring conditions that shape local government financialisation across countries. Building on and integrating a diverse scholarship across economic geography and political economy, the paper highlights economic and financial conditions, such as national-level austerity and financial sector development; institutional conditions, namely the level of decentralisation in a country; and dynamics related to financial subordination. Second, the paper proposes quantitative measures for these structuring conditions and empirically investigates their relationship with three measures of local government financialisation. To the best of my knowledge, this is the first study of the structuring conditions of local government financialisation taking a country-comparative approach.

The study analyses annual data from 22 European countries over the period from 2000 to 2019 to examine the empirical relevance of different structuring conditions in shaping local government financialisation. The primary focus is on local governments’ use of financial instruments in debt management and financial investment, which is measured at the country level using the following variables: (1) borrowing through bonds (‘marketable debt’), (2) use of derivative instruments and (3) investment in debt securities. Using a panel regression approach, specifically, pooled Generalised Least Squares (GLS) with a correction for autocorrelation, the study provides an analysis of local government financialisation across European countries. While these correlations do not establish causation, they offer useful insights into the empirical relevance of different structuring conditions emphasised in the existing literature.

Since the 2007/8 financial crisis, local governments have increasingly turned to marketable debt and derivatives, a trend facilitated by historically low interest rates. Yet, the adoption of these financial tools varies significantly across countries. The panel econometric analysis indicates that local government financialisation is shaped by economic, financial and institutional conditions, as well as financial subordination. Specifically, financialisation tends to be higher in more decentralised countries, with a more developed financial sector. The study also finds limited support for the relevance of austerity, with higher austerity being correlated with lower use of marketable debt. However, this association is not statistically significant at conventional levels, and I find no relationship between austerity and the other indicators of local government financialisation. Finally, financialisation is consistently lower in local governments in Southern and Eastern Europe, reflecting their peripheral status in the global economy and financial system. The main findings are largely robust to a series of tests, presented in Tables A1 to A3 in the Supplemental Appendix.

The article is structured as follows: Section ‘Embedding local government financialisation in its structuring conditions’ reviews the literature on various aspects of local government financialisation and provides a systematic overview of the structuring conditions that shape it. Section ‘An empirical strategy to explore the structuring conditions of local government financialisation’ details the data and methodology used, while Section ‘Empirical evidence of the structuring conditions of local government financialisation’ presents and discusses the empirical findings. The conclusion cautions against overly optimistic views on local government financialisation, highlighting its potential to alter social provision and promote uneven development at different geographical scales. The article underscores the need for more in-depth and comparative research to understand the causal processes at play. Ultimately, this understanding is crucial for efforts to avert and mitigate the adverse effects of local government financialisation.

Embedding local government financialisation in its structuring conditions

What is local government financialisation?

A growing body of literature in urban and economic geography highlights the financialisation of local governance as a continuation of entrepreneurial strategies, with these strategies increasingly using ‘financially mediated means’ (Peck and Whiteside, 2016: 239) and unfolding within a financialised environment. This trend has been documented in Europe (Beswick and Penny, 2018; Dagdeviren and Karwowski, 2022; Hendrikse and Sidaway, 2014) and beyond (Pan et al., 2017; Weber, 2010). This paper focusses on the ‘internal’ financialisation of local government, which Whiteside (2023: 327) defines as ‘orchestrated through the state’s own property, purchases, and debt offerings, or where state institutions are reconfigured along financialized lines’. It is in the instances of internal financialisation that the engineering and re-purposing of ‘financial tools and markets as instruments of statecraft’ is clearest, which Santos (2023: 142) puts at the core of (local) state financialisation. The paper highlights three such instances; first, local governments increasingly mobilise financial markets to borrow at better rates and from a broader range of investors; second, they use financial tools, especially derivatives, to manage the costs and risks associated with their debt; third, some local governments purchase financial assets to generate additional revenue, thereby introducing or reinforcing a financial motive in their investment activities (see also Hasenberger, 2024).

European local governments increasingly borrow through bonds, a trend that is becoming more prevalent compared to the well-established municipal bonds market in the US (Deruytter and Möller, 2020; Kovács, 2011; Padovani et al., 2018). The development and promotion of local government bonds markets in Europe was actively supported by state actors at various levels. This includes the establishment of municipal bonds agencies in countries such as France, Germany, Sweden and the United Kingdom (Vetter et al., 2014). This shift in borrowing practices has sometimes been characterised as a move to ‘marketable’ debt instruments, which can be sold and traded on secondary markets (Fastenrath et al., 2017). These expose local governments to a wider set of financial investors, potentially enabling local governments to borrow at lower interest rates (Vetter et al., 2014). This can be advantageous, especially for financing long-term projects like infrastructure development (Padovani et al., 2018). However, it has also been argued that investors in local government bonds can become a ‘second constituency’ (Peck and Whiteside, 2016: 245), with a potential influence on local policy that may contrast sharply with the interests of particularly the most vulnerable local residents (Omstedt, 2020; Petzold, 2014).

The prevalence of this practice has significantly increased in European local governments, in the period of low interest rates following the 2007/8 financial crisis, as will be discussed below. The literature indicates a rise not only in general obligation bonds but also in revenue bonds within Europe. In the latter case, local authorities are borrowing against assets like user fees (O’Brien and Pike, 2019), rental income (Beswick and Penny, 2018) and future tax revenue (Findeisen, 2022). Borrowing against income from public assets reconfigures those assets along financialised lines; besides providing the basis of a public service, they now need to generate the revenue necessary to repay debt (Hasenberger, 2024).

Another aspect of the shift towards financialisation is the use of derivatives by local governments, primarily interest rate swaps, to manage the costs and risks associated with their borrowing. In recent years, local governments have used derivatives in a bid to lower interest payments, for instance, by exchanging fixed interest rate payments for variable ones (Mertens et al., 2021; Pérignon and Vallée, 2017; Trampusch and Spies, 2015). In addition to standard interest rate swaps, some local governments have reportedly used more complex derivatives like Constant Maturity Swaps or ‘snowballs’, arguably to generate additional revenue rather than just to lower costs (Dodd, 2010; Hendrikse and Sidaway, 2014). Derivatives can help local governments smooth out cash flow volatility (Khumawala et al., 2016; Lagna, 2015) and reduce borrowing costs, including restructuring interest payments on long-term debt (Luby, 2012). However, this strategy is effective only as long as interest rates behave as local governments anticipate. When interest rate trends were disrupted by the 2007/8 financial crisis, some local governments consequently incurred substantial losses on their derivative contracts (Dodd, 2010; Hendrikse and Sidaway, 2014; Pérignon and Vallée, 2017).

In addition to mobilising financial markets and repurposing financial instruments for their debt management, it has been noted that local governments also invest in various financial assets. For example, local governments in Britain have used cash reserves and deposits to invest in higher-yielding assets such as solar farms, shopping centres and money market funds. Some of them borrow to pursue these investments (Christophers, 2019; Dagdeviren and Karwowski, 2022; Davies and Boutaud, 2020). In Belgium, local governments use inter-municipal utility companies not just for delivering public services but also to generate additional financial revenue through dividends (Deruytter and Bassens, 2021).

The structuring conditions that shape financialisation in local governments

The literature reviewed above provides detailed insights into how local governments have used and re-engineered financial instruments and markets in their governance. However, this body of work is sometimes criticised for lacking a systematic understanding of the factors that shape, enable and constrain this financialisation. Peck (2017: 10) refers to these factors as ‘structuring conditions’. These conditions, which are outside the control of local governments, play a critical role in shaping their operations. Christophers (2019) calls for a more in-depth understanding of the structuring conditions to better understand why financialisation occurs in local governments and why it takes different forms across places. This section builds on the diverse body of scholarship on local government financialisation to identify the conditions under which it takes place; economic and financial, and institutional conditions, and financial subordination.

Economic and financial conditions

Much of the literature highlights austerity as a principal driver of local government financialisation. This literature suggests that austerity policies decided on the national level have caused significant pressure on local budgets. In turn, local governments had to seek alternative sources of revenue to be able to continue providing services, maintaining public infrastructure and paying their employees. It has been argued that this often meant an increased reliance of local governments on financial markets to compensate for reduced transfers from central government (Beswick and Penny, 2018; Dagdeviren and Karwowski, 2022; Lagna, 2015; Omstedt, 2020; Peck and Whiteside, 2016).

Moreover, there is some evidence that higher financial development in a country can promote local government financialisation through two main channels. First, in countries with higher levels of financial development, there is greater potential for financial innovation, such as the availability of investment opportunities and debt instruments tailored to the needs of local governments, such as local government bonds. This may also attract a larger pool of investors interested in buying these debt instruments, especially where municipal bond markets are more highly developed and liquid (Cestau et al., 2019; Lemoine, 2017; Vetter et al., 2014). For example, in the US, the proximity of banks involved in municipal swap markets have facilitated the uptake of swaps by local governments (Janssen, 2022). Second, in countries with higher levels of financial expertise, local governments may be influenced to use financial instruments to manage their assets and liabilities by lobbying and revolving-door mechanisms, or simply through higher exposure (Mertens et al., 2021). For example, Janssen (2022) finds that local government officials who are also part of a community of finance professionals tend to use swaps more frequently for municipal finance.

Institutional conditions

It has been argued that local governments in countries with more decentralised governance structures are more likely to use financial instruments (Cox, 2009; Weber, 2010). This is because they have higher decision-making power than their counterparts in centralised countries and can thus engage in various innovative budget management techniques, including financialisation. Empirically, Mertens et al. (2021) note an increase in the use of ‘Lobo’ loans with embedded derivatives by English local governments following devolutionary reforms in the early 2000s. Similarly, municipal policymakers in the US in areas with higher ‘local control’ over factors such as the issuance of debt and local development processes found it easier to access capital markets for borrowing (Weber, 2010: 253). In Europe, this also has a regional aspect. Northern and Western European countries tend to be more decentralised than those in Southern Europe, and decentralisation is relatively recent in post-Soviet countries of Eastern Europe (Büdenbender and Aalbers, 2019).

Financial subordination

On the national level, Santos (2023: 1) argues that states’ ability to use financial tools and markets in their governance is shaped by the ‘differentiated positions countries occupy within the world economy’. A crucial aspect of this ‘subordinate’ state financialisation is the extent to and conditions under which states have access to financial markets to pursue policy objectives. For instance, while wealthy countries in the core of the capitalist system, like the US, UK, Germany and France, usually have no problem selling their debt to private investors, this is more complicated for peripheral countries and subnational state actors (Eichacker, 2024).

Two (related) aspects shape the subordinate position of state actors. First, their position in the international currency hierarchy relates to the assumption that ‘national money can be considered an international asset class which stands in competition with other nations’ money’ (Alami et al., 2023: 8). At the top of the hierarchy sit the currencies of core countries – in particular the US dollar, and to a lesser extent, the euro – with the highest relative ability to ‘perform international money functions [. . . i.e.,] to act as a means of payment, store of value, and unit of account’ (Alami et al., 2023: 8). Currencies of smaller, peripheral countries sit at the bottom. Countries’ position in the global currency hierarchy is also reflected in the systemic importance of assets denominated in their currency in the financial system, for example, the importance of their sovereign bonds as collateral for borrowing (Eichacker, 2022, 2024). Second, and closely related, is investors’ perception of country risk. This means access to financial markets, especially for their debt management, is more costly and less predictable for subordinate state actors, as they are subject to more volatile investor demand and perceptions (Hardie, 2011; Massó, 2016).

The literature on financial subordination almost exclusively focuses on the national scale (Büdenbender and Aalbers, 2019). However, Eichacker (2024) notes that these dynamics may also apply to subnational state actors, which can be understood as subordinate based on the framework above, even in core countries. She discusses how US municipalities experienced a withdrawal of private funds during the 2007/8 crisis, as investors sought safety in the more ‘money-like’ national Treasuries. In other words, while using the same currency, bonds issued by local governments are perceived as lower down the hierarchy, and less liquid compared to national bonds. This is an important insight, but an explicit investigation of the relevance of financial subordination for local government financialisation is still missing from the literature.

An empirical strategy to explore the structuring conditions of local government financialisation

This paper aims to explore the empirical relevance of economic, institutional and financial conditions in shaping local government financialisation across European countries. By doing so, it contributes to the expanding body of literature on this phenomenon in Europe, which often focuses on a single country or city. The paper uses annual, country-level data for 22 countries across Europe over the 2000–2019 period. The sample includes countries from Northern and Western Europe (Austria, Belgium, Germany, Finland, France, Ireland, the Netherlands, Norway, Sweden and the United Kingdom) as well as from the Southern (Greece, Italy, Portugal and Spain) and Eastern European (semi-)peripheries (Bulgaria, Czech Republic, Estonia, Hungary, Latvia, Poland, Slovakia and Slovenia). Thus, the paper broadens the geographical scope of the existing literature on local government financialisation in Europe, which has predominantly focused on the UK and Germany (Hendrikse and Sidaway, 2014; Mertens et al., 2021; Trampusch and Spies, 2015). Studies examining this process in Southern or Eastern Europe are limited (Kovács, 2011; Lagna, 2015; Padovani et al., 2018). Moreover, the inclusion of peripheral countries in the sample enables an analysis of structuring conditions that have been largely overlooked in the literature, in particular financial subordination.

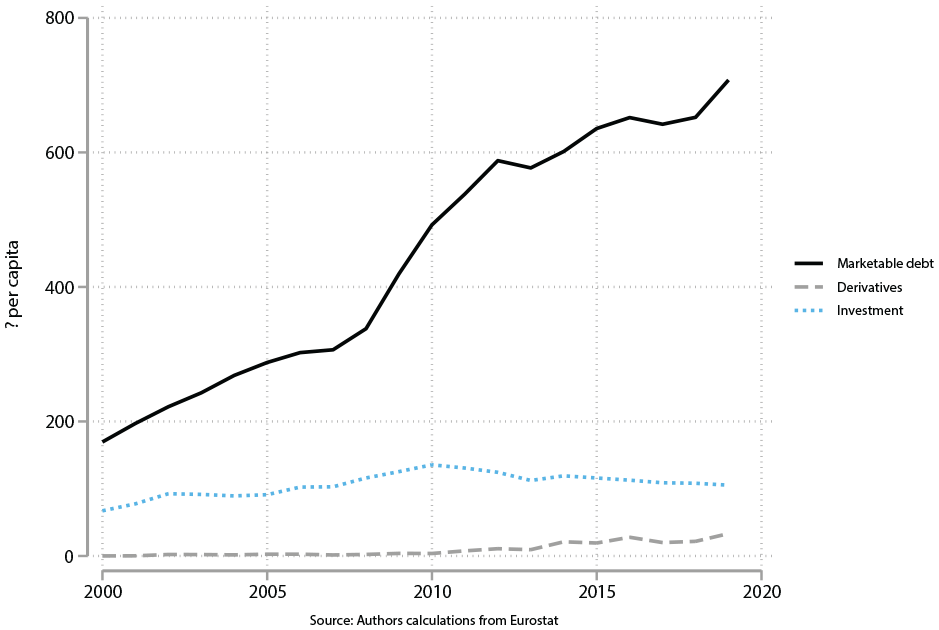

The primary variables of interest relate to local governments’ use of financial instruments, which serve as proxy measures of local government financialisation. 1 The paper uses data from Eurostat and the Office for National Statistics (ONS) to construct three measures of local government financialisation: (1) local government borrowing through debt securities (bonds), referred to as ‘marketable debt’ (Fastenrath et al., 2017; Schwan et al., 2020), (2) local governments’ use of derivatives and (3) local governments’ investment in debt securities. 2 While (1) and (3) are measured as the stock of debt securities on the liabilities and asset side of local governments in a given country and year, derivative use is measured as assets minus liabilities, in line with Eurostat (2017) guidance, taking the absolute value to capture intensity rather than success of the strategy. The variables are adjusted for inflation and to population size to make values comparable across countries. Figure 1 illustrates the average evolution of these three indicators of local government financialisation over time. It reveals a substantial increase in marketable debt, particularly accelerating after the 2007/8 financial crisis, as a period of historically low interest rates made borrowing cheaper. On average, local government investment in debt securities has remained stagnant and has even declined slightly in the last decade. In contrast, local governments’ use of derivatives has exhibited gradual growth over the past 5–10 years, presumably to manage costs and risks of higher borrowing over that period.

Local government financialisation in Europe over time (sample average).

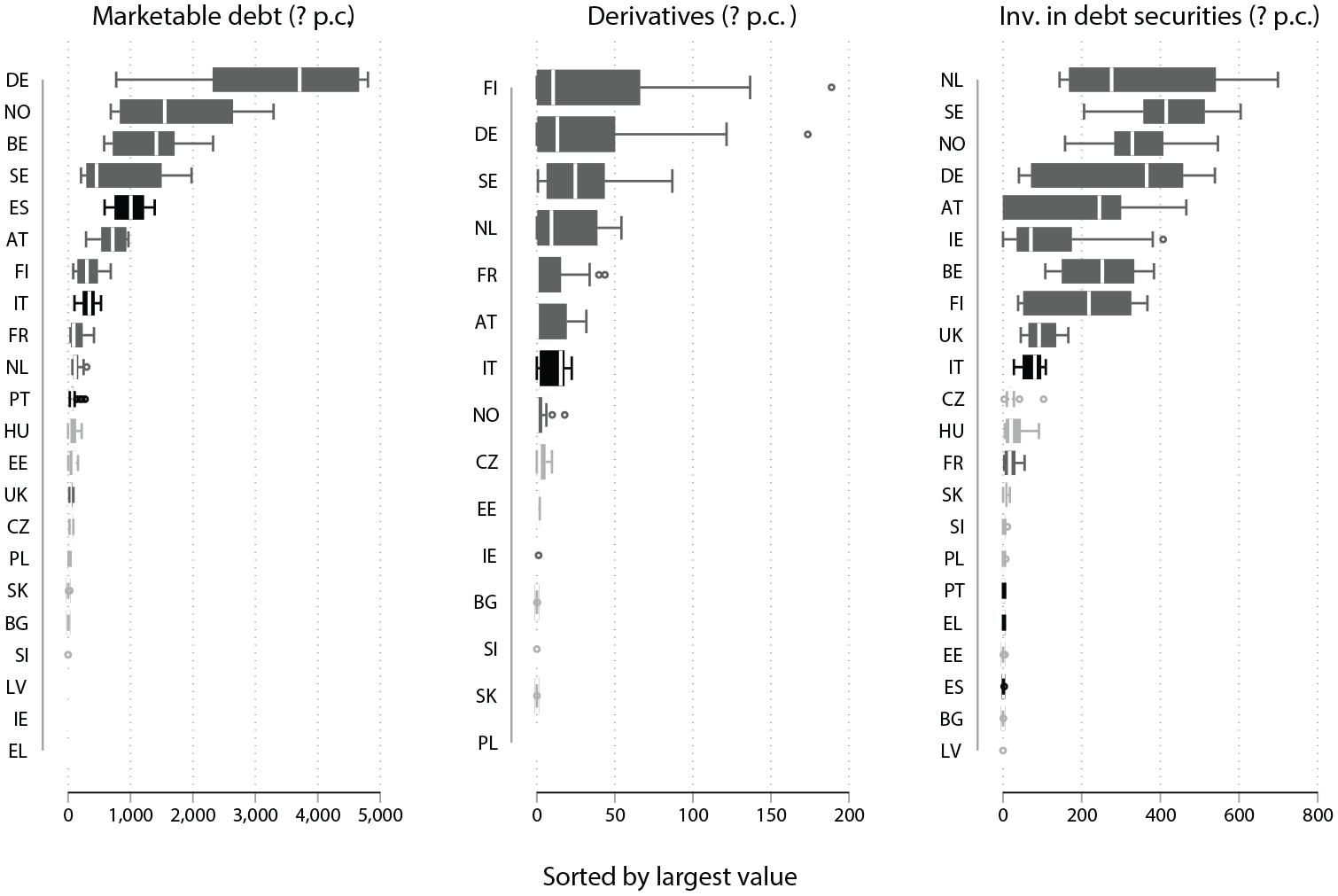

However, Figure 2 shows substantial variation in the three indicators of financialisation between countries. The figure shows that in some countries, often in Western and Northern Europe, local governments’ use of financial instruments is both higher and takes on a larger range of values.

Local government financialisation by country (2000-2019).

This study seeks to explore some of the structuring conditions that shape the variation in local government financialisation between countries. A panel regression approach is used to examine the relationship between the three indicators of local government financialisation and their structuring conditions, measured at the country level. To be sure, these correlations do not establish causality. But they can provide useful insights into the empirical relevance of different factors highlighted in the existing literature. Three separate models were estimated, one by indicator, using the following baseline specification:

The outcome variable is the natural logarithm of the financialisation indicators, to which a constant of one has been added to offset zero values in the original variable. AUST is a proxy for austerity, operationalised through the annual change in central government expenditure as a percentage of GDP, using data from Eurostat and the ONS. This measure is inspired by discussions on the significance of expenditure- versus tax-based austerity (e.g. Alesina et al., 2019). 3 FDEV is the measure of financial development in a given country and year. It is operationalised through the IMF Financial Markets index, a sub-indicator of the fund’s Financial Development index (Svirydzenka, 2016) which ranks countries based on measures of the ‘depth’ of financial markets (e.g. bonds issued by public and private borrowers), ‘access’ (e.g. the range of credit providers) and ‘efficiency’ (e.g. stock market turnover). The natural logarithm was taken to facilitate the interpretation of the results. DEC is a measure of decentralisation in a given country and year, operationalised through the share of local government expenditure in total government expenditure, using Eurostat data. GDP is a measure of GDP growth taken from Eurostat, which is included to control for differences in local government financialisation based on differences in the general economic conditions of a country. The measures of austerity and GDP growth are included as 1-year lags, considering these may not be immediately reflected in local government actions.

To capture structural inequalities in local governments’ access to financial markets, or financial subordination, a second set of regressions includes two dummy variables to indicate whether a country is located in Southern or Eastern Europe:

This study focuses on cross-country variation, using between-estimators to provide an analysis of local government financialisation across European countries. The regressions were estimated using pooled GLS with a panel-wide AR(1) correction to deal with autocorrelation, which is more efficient than the pooled Ordinary Least Squares (OLS) estimator in settings with a small sample size relative to time periods.

Additionally, the Supplemental Appendix (Tables A1–A3) includes a range of robustness tests, using different estimators (pooled OLS, year-fixed effects), estimating the relationship between financialisation and structuring conditions for the pre- and post-2008 periods separately, and using alternative measures for the main dependent and independent variables. Above, local government financialisation is measured in per capita values to allow for an intuitive interpretation of the relationships uncovered. To examine whether these hold if financialisation is measured differently, Tables A1 to A3, columns 5, estimate equation (1) with financialisation measured as a share of GDP. To capture decentralisation, the share of local government expenditure in total government expenditure is most commonly used in country-comparative studies (Rodríguez-Pose and Ezcurra, 2010; Tselios and Rodríguez-Pose, 2020). However, it is widely acknowledged that ‘no single indicator can adequately capture the real level of fiscal decentralization of a country’ (Canare et al., 2020; Rodríguez-Pose and Ezcurra, 2010: 627). Therefore, columns 6–8 in Tables A1 to A3 present results for equation (1) using three alternative measures of decentralisation: a Regional Authority Index (Hooghe et al., 2016), a Spending Autonomy Index (Kantorowicz and Jurriaan van Grieken, 2019) and a dummy for unitary versus federal governance system. Finally, the Supplemental Appendix includes a dummy variable indicating whether a country is part of the eurozone in a given year, to examine whether regional differences in local government financialisation are driven by currency hierarchies, a component of financial subordination (column 9 of Tables A1–A3).

Empirical evidence of the structuring conditions of local government financialisation

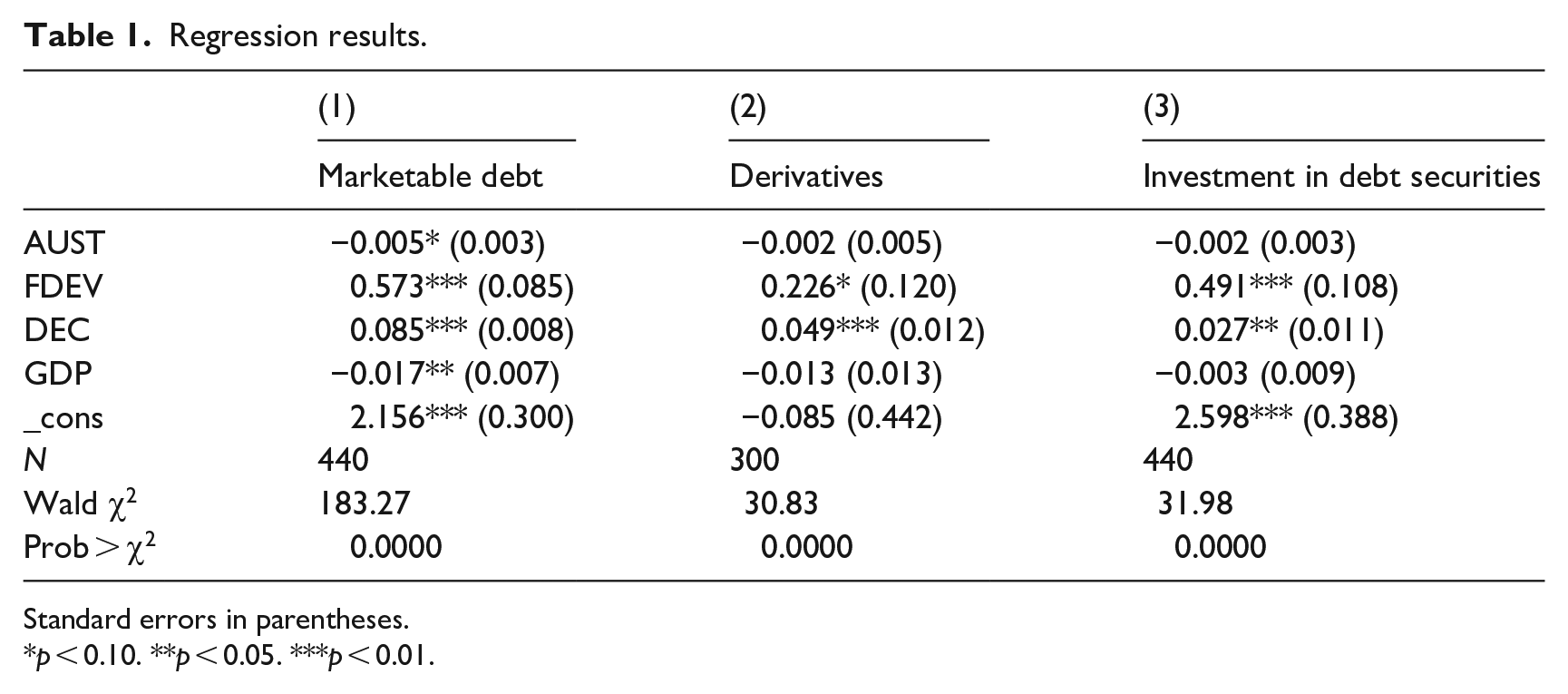

Table 1 presents the empirical results for the first set of regressions on local governments’ use of marketable debt, derivatives and local government investment in debt securities.

Regression results.

Standard errors in parentheses.

p < 0.10. **p < 0.05. ***p < 0.01.

I find a slight correlation between the proxy for austerity and local government borrowing through marketable debt; however, this correlation did not extend to other financialisation indicators. Specifically, borrowing through bonds tends to be higher in countries with lower central government spending. In the sample, a one percentage point decrease in central government spending (measured as a share of GDP) is associated with an average increase in outstanding marketable debt per capita of 0.5%. Although the relationship is not statistically significant at conventional levels, the direction of the coefficient aligns with prior studies. These studies suggest that austerity prompts local governments to seek alternative revenue sources, a trend evidenced by detailed analyses in various cities or countries (Beswick and Penny, 2018; Dagdeviren and Karwowski, 2022; Lagna, 2015; Peck and Whiteside, 2016). This result highlights the limitations of the panel econometric design. In the cross-country analysis, other structuring factors emerge as more influential in shaping local government financialisation. However, the intensity of austerity often differs across local governments (Gray and Barford, 2018), and pre-existing differences, such as debt levels before austerity, influence local governments’ responses to fiscal tightening (Dagdeviren, 2024). Hence, austerity may still play an important role in promoting borrowing through marketable debt within individual countries and local governments, but the correlation disappears in the average. Conversely, the use of derivatives and investment in debt securities are less conventional activities within local governments (Hasenberger, 2024) requiring teams with specialised knowledge. Local governments affected by austerity might cut back on ‘non-essential’ teams, thereby losing capabilities required for engaging in such activities, which could explain the absence of a statistically significant correlation in the sample.

The study reveals a clear association between the sophistication of a country’s financial markets and local government financialisation. Specifically, in countries with more highly developed financial markets (based on factors like public and private borrowing through bonds, stock market turnover and the range of credit providers), we generally see that local governments are more involved in borrowing through and investing in debt securities. In the sample, a 1% increase in the measure of financial development – the natural logarithm of the IMF Financial Markets Index – is associated with a 0.57% and 0.49% increase in marketable debt and investment in debt securities respectively. The relationship is positive but not statistically significant at conventional levels for local governments’ use of derivatives. This finding aligns with previous literature, from which we can identify two channels through which a more developed financial sector can support greater financialisation in local governments. First, local governments may be subjected to lobbying efforts in countries with a larger financial sector (Janssen, 2022; Mertens et al., 2021). Second, a more developed financial sector may offer greater opportunities for innovation and the development of financial products tailored to the needs of local governments. This finding could, therefore, also indicate that local governments actively make use of the greater availability of financial instruments and investors (Lemoine, 2017; Vetter et al., 2014).

Regarding institutional conditions, the study finds a consistent pattern whereby local government financialisation is higher in more decentralised contexts. Specifically, a one percentage point increase in subnational government expenditure (measured as a share of total government expenditure) is associated with an average increase of approximately 8.5% in local governments’ use of marketable debt, a 4.9% increase in their use of derivatives and a 2.7% increase in their investment in debt securities. This trend holds statistically significant at the 1% level for marketable debt and derivatives, and at the 5% level for investment in debt securities. In other words, when comparing two otherwise similar countries, local government financialisation will typically be higher in more decentralised countries. This finding has two implications. On the one hand, it suggests that local governments are constrained in their ability to use financial instruments by the centralisation of governance systems in a country. On the other hand, this indicates that local governments use financial instruments more when they have higher autonomy in their decision-making. In line with previous literature, this suggests that local governments use their power (Lagna, 2015) to seize opportunities to repurpose financial instruments to navigate the often challenging conditions under which they operate (Findeisen, 2022).

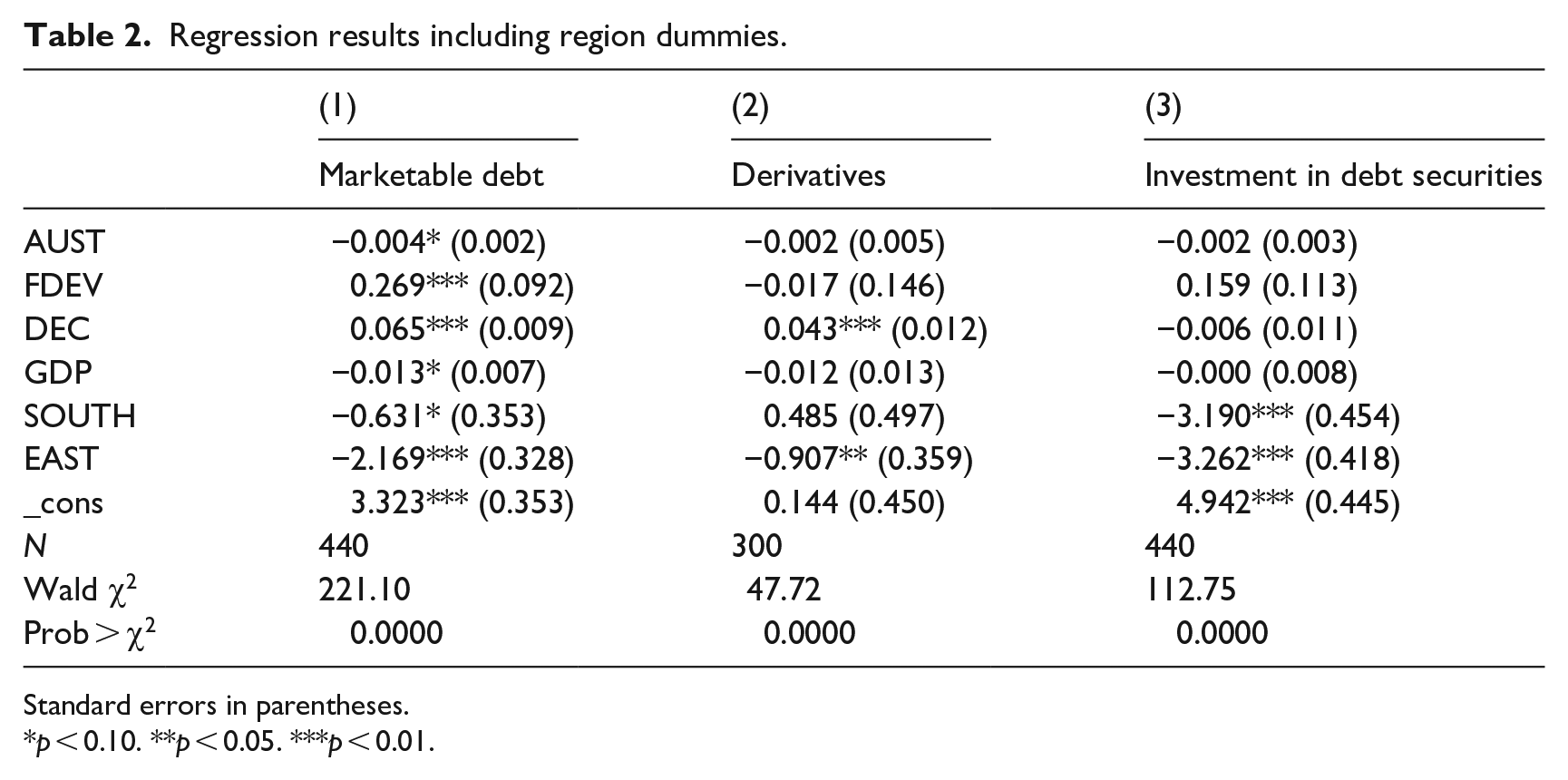

Finally, local government financialisation tends to be significantly lower in the Southern and particularly Eastern European periphery, even when accounting for the other conditions that shape financialisation (see Table 2). On average, the stock of bonds per capita in Eastern Europe is approximately 88.57% lower than in Western European countries, the stock of derivatives per capita is 59.63% lower, and the per capita stock of investment in debt securities is 96.17% lower. 4 In Southern Europe, local government investment in debt securities is 95.88% lower than in Western Europe, on average. This means when comparing two similar countries, one from Southern Europe and one from Western Europe, local government investment in debt securities in the former is typically around 4.12% of the value in the latter. These findings are also reflected in Figure 2 above.

Regression results including region dummies.

Standard errors in parentheses.

p < 0.10. **p < 0.05. ***p < 0.01.

These findings may reflect the subordinate position of state actors in the global economy and financial system. This position mediates the extent and conditions under which local governments in subordinate countries can use financial instruments in their governance (Eichacker, 2022; Santos, 2023). Specifically, local governments in peripheral countries, using currencies further from the top of the international hierarchy, typically face higher costs when they seek to use financial markets for governance purposes (Alami et al., 2023). Moreover, their access to private finance is more volatile, as investor perceptions tend to fluctuate more with business cycles and in response to changes in perceived credit risk (Hardie, 2011; Massó, 2016). Recent developments in European sovereign debt markets make clear that financial subordination is not only about currency hierarchy. In particular, Southern and Eastern European countries, both in and outside the eurozone, faced a sudden withdrawal of investor funds following the 2007/8 financial crisis (Ban and Bohle, 2021; Gabor, 2010; Massó, 2016). Bellot et al. (2017) show that the perception of national credit risk tends to be amplified at the subnational level, translating into higher borrowing costs for local governments. Taken together, higher costs and volatility exacerbate the risks of financial strategies and may therefore deter local governments in peripheral countries from engaging in financialisation, as suggested by the findings presented above.

The main findings are largely robust to a series of robustness checks, as discussed above and presented in Tables A1 to A3. A notable discrepancy is the negative and statistically significant coefficient on the Eurozone dummy (in column 9 of Tables A1–A3), to examine whether differences in local government financialisation are related to currency hierarchies rather than broader financial subordination. The finding that local government investment in debt securities tends to be higher in countries not using the euro as a national currency is possibly due to the prevalence of public investment bodies in Scandinavian countries. The coefficient is not statistically significant for marketable debt and derivative use, indicating the presence of broader dynamics of financial subordination. The Supplemental Appendix also offers evidence against the presence of multicollinearity (Table A4 presents the variance inflation factor (VIF)) and structural breaks (Table A5). The VIF test indicates a slight issue with the financial development index, which is negatively correlated with the dummy for Eastern Europe. This is particularly relevant for the model estimating the relationships for local governments’ use of derivatives. However, the other results are robust to excluding financial development from the model (see Table A2, column 10). Moreover, the Levin-Lin-Chiu test fails to reject the null hypothesis of unit roots for the measure of derivatives. When assessing stationarity for the post-2008 period, the null is rejected, and the main results hold for this sub-period (see Table A2, column 4).

Concluding discussion

This paper responds to recent calls for a deeper investigation into the structuring conditions of local government financialisation. While financialisation is understood, in this paper, as local governments’ use and repurposing of financial tools and markets to manage their debt and assets (Santos, 2023; Whiteside, 2023), its structuring conditions refer to the context in which local governments operate, but which are largely outside their control (Christophers, 2019; Peck, 2017). The paper makes two main contributions. First, building on a diverse scholarship across economic geography and political economy, this paper provides a systematic overview of the structuring conditions that shape, enable and constrain local government financialisation. Second, I propose quantitative measures for these structuring conditions and empirically test their relative importance in shaping three measures of local government financialisation across European countries: borrowing through marketable debt, use of derivatives and investment in financial assets.

Since the 2007/8 financial crisis, local governments have increasingly borrowed through marketable debt and used derivatives, a trend supported by historically low interest rates. However, the degree to which local governments use these financial tools varies widely among countries. Using panel econometric techniques, this study finds that the extent of financialisation across countries is shaped by economic, financial and institutional conditions, and financial subordination. Specifically, local government financialisation tends to be higher in countries with more decentralised governance structures and a more developed financial sector. The study also finds limited support for the thesis that austerity drives local governments towards higher use of marketable debt in their borrowing strategies (e.g. Dagdeviren and Karwowski, 2022; Peck and Whiteside, 2016), although the correlation is not statistically significant at conventional levels. This contrasts with much of the existing literature, which often highlights austerity as a primary driver of financialisation in local governments (Beswick and Penny, 2018; Dagdeviren and Karwowski, 2022; Lagna, 2015; Peck and Whiteside, 2016). This discrepancy can be attributed to the panel econometric design of the study, which presents average correlations across a sample of countries over time. Yet local governments are exposed to different extents of austerity (Gray and Barford, 2018), and they react differently based on factors such as prior debt levels (Dagdeviren, 2024). Finally, financialisation is found to be consistently lower for local governments in the Southern and particularly Eastern European periphery, which may reflect their subordinate position in the global economy and financial system.

The literature on local government financialisation generally takes a critical view. Studies emphasise that local governments’ exposure to financial markets generates financial risks, which may translate into service cuts (Hendrikse and Sidaway, 2014; Peck and Whiteside, 2016; Pérignon and Vallée, 2017). But others argue that financialisation may be a ‘problematic means’ potentially used for ‘positive socioeconomic ends’ (Christophers, 2019: 572). Specifically, financialisation may enable local governments to generate revenue for essential public services, such as pursuing housing or infrastructure development (Beswick and Penny, 2018; Peck and Whiteside, 2016), and fill budget gaps (Dagdeviren and Karwowski, 2022). Thus, financialisation might offer a way for individual local governments to navigate challenging structuring circumstances, enhancing their capacity and power, including vis-à-vis central government (Findeisen, 2022; Lagna, 2015). This means, financialisation can make sense and seem desirable from the perspective of individual local governments and their constituents, especially when it supports services that would otherwise not be provided.

But financialisation also raises questions about the democratic accountability of local governments as it reconfigures which actors have a say in decisions on public provision, and consequently, which services are provided, and to whom. Local government financialisation represents a continuation of entrepreneurial urban strategies, adapted to a financialising economy (Beswick and Penny, 2018; Peck and Whiteside, 2016). Entrepreneurial strategies, focusing on private investment, pit private-sector interests against the needs of residents, and this conflict of interest is further reinforced and modified by local government financialisation, through the introduction of financial investors’ interests and increasingly complex governance tools that complicate public oversight. As local governments increasingly rely on capital markets for their debt management and investment activities, the interests of financial investors may conflict with the needs of local residents (Jenkins, 2021; Peck and Whiteside, 2016). This conflict might manifest as local austerity measures to satisfy creditors, such as service reductions and the stopping or postponing infrastructure investments (Hendrikse and Sidaway, 2014). But it can also lead to a more sustained transformation in how local governments operate, as they are incentivised to proactively anticipate investor demands – adopting and internalising their rationales – aiming for better credit ratings to access borrowing at better conditions (Omstedt, 2020; Petzold, 2014).

Moreover, the potential benefits of financialisation – in terms of enhancing local governments’ capacity to provide public services – as well as its financial risks, are unevenly distributed across geographical scales. Locally, the adoption of financial rationales in public provision tends to prioritise market-oriented services, such as market over social housing (Beswick and Penny, 2018; Bloom, 2023). At the domestic level, wealthier local governments are typically better placed to leverage financial markets to their advantage (Dagdeviren and Karwowski, 2022; Nukpezah, 2019). Internationally, local governments in different countries have varying ability to access and repurpose financial tools for their governance (Santos, 2023). The findings of this study indicate their capability is contingent on the extent of decentralisation, the development of the national financial sector, and their position within global financial hierarchies. Consequently, a more pronounced shift towards using financial tools in local service provision could intensify uneven development at these multiple scales. During the period analysed, the data suggest such a shift, with financial tools gaining increased significance in local governance. However, it remains to be seen whether this trend will continue in the context of higher interest rates post Covid-19, which might discourage borrowing and derivatives but could render financial investments more appealing (Hasenberger, 2024; Nukpezah, 2023).

The bird’s-eye approach adopted in this paper enables the analysis of the structuring conditions shaping local government financialisation across countries. This complements the detailed empirical literature focused on specific cities or countries. While this methodological approach is a key strength of the paper, it also presents its main limitation. Specifically, the country-level analysis does not consider subnational variegation in local government financialisation. However, several studies reveal significant variation among local governments within a country (Dagdeviren and Karwowski, 2022; Pérignon and Vallée, 2017; Trampusch and Spies, 2015). For instance, Pike (2023) identifies a minority of ‘vanguard’ financially active local authorities in England, in contrast to a ‘long tail’ that do not use financial instruments. In this study’s context, the overall level of financialisation in a country and year may result from the activities of a varying proportion of, but likely not all local governments. More generally, the relationships identified in this study should not be seen as uniformly applicable to specific local governments but as average patterns across the period of analysis and sample of countries.

Moreover, and relatedly, the study’s design does not, by itself, permit a causal interpretation of the uncovered relationships. Instead, it reveals that specific structuring conditions tend to coincide with higher levels of local government financialisation – namely, greater decentralisation, a more developed financial sector, and to some extent, austerity. Conversely, being in the European periphery is associated with lower financialisation in local governments. Therefore, the paper provides empirical evidence regarding some theoretical explanations of local government financialisation noted in existing literature and adds a new one: financial subordination.

Further research could delve deeper into the causal dynamics involved. Comparative studies across and within countries would be particularly useful in examining the impact of structuring conditions on local government financialisation more closely. The conditions analysed in this paper could inform and provide the dimensions for such comparative research. Future studies might build on this paper’s initial findings to investigate the influence of financial subordination on different forms of local government financialisation, paying close attention to the similarities and differences between local governments in core and periphery. This could extend beyond the financialisation measures proposed here, for example to include initiatives to mobilise private finance for local development and involve financial sector actors more actively in the provision of local services. Ultimately, a deeper understanding of its causes is crucial for efforts to avert and mitigate the adverse effects of local government financialisation.

Supplemental Material

sj-docx-1-epn-10.1177_0308518X241256546 – Supplemental material for The structuring conditions of local government financialisation in Europe: A comparative perspective

Supplemental material, sj-docx-1-epn-10.1177_0308518X241256546 for The structuring conditions of local government financialisation in Europe: A comparative perspective by Hannah Hasenberger in Environment and Planning A: Economy and Space

Footnotes

Acknowledgements

I am grateful to Bruno Bonizzi, Hulya Dagdeviren and Aleksandra Peeroo for helpful comments on earlier versions of this paper. All remaining errors are mine.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author would like to thank the University of Hertfordshire Business School for the PhD studentship that supported the research for this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.