Abstract

This article argues that urban governance, and academic theorisations of it, have focused on the role and strategies of real estate developers at the expense of understanding how investors are shaped by regulatory environments. In contrast, using the case of institutional investment in London’s private rental housing (Build to Rent), in this article I argue that unpacking the private sector and the development process helps reveal different types of risk which necessitate variegated responses from within the real estate sector. In doing so, I demonstrate the complexities of the private sector in urban development, especially housing provision, and the limitations of a binary conceptualised around pro- and anti-development narratives when discussing planning decisions. Instead, I show the multiplicity of responses from within the private sector, and how these reflect particular approaches to risk management. Uncovering this helps theorise the complexities of governing housing systems and demonstrates the potential for risk-based urban governance analysis in the future.

Introduction

The provision of affordable, high-quality housing is a problem for cities globally (Wetzstein, 2017). Mitigating the challenges captured under the umbrella of ‘housing crises’, including alleviating poor-quality rental housing, a lack of social housing and difficulties saving for a deposit to buy a home, is deeply entrenched in and impacted by politics (Heslop and Ormerod, 2020). A recent political response globally has been to actively seek out new forms of funding and financing, often in international capital markets and from institutional investors. In this article, I analyse how the governance of housing systems, particularly new forms of housing tenure that are emerging in response to this form of investment, requires recognising the different risk priorities of real estate professionals and how these translate to different development objectives. In doing so, I push back against the idea of a state body (at any scale) being either ‘pro’ or ‘anti’ development and argue that what is anti-development for one group of actors may be beneficial or ‘pro-’ for another.

This article draws from research in London, where despite the complexity of the housing crisis, the situation is primarily framed as one of simply supply-side constraints (Gallent et al., 2017). The political response has been to govern the crisis through supply stimulation in the for-sale market, often through financialised land supply markets (Bradley, 2021). Nationally, this includes mortgage assistance schemes to stimulate housebuilding, which have primarily caused house price inflation, worsening the situation rather than addressing systematic failures (National Audit Office, 2019). At a city level, the Mayor introduced grants to encourage building, whilst on a local level, pro-development boroughs are positioned as key to meeting the target numbers for housing in the local authority, as well as in the city as a whole. To meet affordability needs, local planning authorities negotiate developer contributions through a viability assessment of projects, with ‘section 106’ agreements between developers and authorities outlining the level of affordable provision required of a site within a profitability framework largely shaped by developers (Sagoe, 2018). As such, localised politics and different geographies of viability influence the degree to which affordable housing is brought forward as part of developments (Ferm and Raco, 2020). In summary, the governance of housing in London can be understood as having centred on attracting developers, creating a ‘pro-development’ agenda and encouraging developers to bring forward high volumes of housing that includes some degree of affordable housing.

Alongside such approaches in the for-sale market, there is recognition that renters are an increasing proportion of the population (and therefore an important voting block), and that they too are distressed by the system. Similar incentive-based approaches have been used to address issues in the private rental sector (PRS) through a shift in supply: since 2012, the national government has sought to intervene in the provision of rental housing, with an emphasis on utilising institutional investment to fund new sites (Department for Communities and Local Government [DCLG], 2012). As such, there has been a surge in institutionally owned private rental housing, with an estimated 20% of new units within London forming part of the ‘Build to Rent’ (BTR) market. This form of housing investment is essential for understanding the housing system as a whole, since 40% of Londoners live in private rented accommodation (see e.g. Paccoud and Mace, 2018). Whilst the professionalised PRS has warranted academic attention internationally, less is understood about it in emerging markets such as London (Nethercote, 2020).

With the political response to London’s housing in the background, this article turns to a question posed by Le Galès: what is governed in cities (Le Galès and Vitale, 2013)? In this article, I take up the challenge of answering this question, as well as who, how and where, in relation to London’s housing market. I argue that governance and research on this has tended to focus on shaping developers’ strategies, often at the expense of understanding and therefore being able to influence investment decisions. There has been a huge growth in literature on the financialisation of housing (see Aalbers, 2019 for an overview), which has paid particular attention to certain types of investors and the governance of their processes. This has highlighted the ways in which particular regimes of governance have enabled a financialised real estate market, especially in commercial or mixed-use developments (see e.g. Anselmi and Vicari, 2020). Building on this work by focusing on institutional investors and their strategies, and specifically how these relate to the developer–investor relationship(s), I demonstrate what the division of risk between different actors throughout the development process means for local governance, particularly planning legislation, which I argue is deemed largely irrelevant by investors. In contrast, national government legislation that shapes demand for rental properties and property ownership structures is more significant.

To make this argument, I use the lens of risk to better theorise urban governance and empirically illustrate the multiplicity of actors now involved in London’s current residential investment landscape. I argue that developers in London are governed by local authorities, but that investors rarely are. This is not because investors act beyond the state, but because they are concerned with different factors. This resonates beyond a London context because institutionally owned purpose-built rental housing is growing globally, particularly in ‘newer’ markets, such as European cities. Focusing on the differentiated experiences of various private-sector actors within the wider real estate ecology helps draws out the complexities of governing these changing housing systems.

The article proceeds in the following way. The second section argues for a greater attention to risk management in urban studies, as a lens through which differentiated outcomes of governance within the private sector can be understood. The third section introduces London, demonstrating different actors’ relationship to risk. The fourth section compares the ways in which developers and investors respond to political risk. The fifth section builds on these contrasting approaches to demonstrate how the governance of housing development in London, in terms of who and what is governed, reflects the particular risk-based mitigation strategies employed. The final section offers the three main conclusions of the paper: firstly, I unpack further the ‘black box’ of the private sector in urban development (Campbell et al., 2014) to show the multiplicity of contrasting reactions to urban governance mechanisms through a comparison, within one city, of different actors. As such, I push against the binary conceptualisation of planning authorities as pro- or anti-development. Secondly, I bring into conversation the wide variety of financing and funding types that have emerged by focusing on what Nethercote (2020) highlights as an under-explored but vital part of new development in places like London: institutional investors in the PRS. Thirdly, I demonstrate the relevance of risk-based analysis for theorising urban governance.

A risk-based approach to understanding urban governance

Planning policy and regulation, at both national and local levels, shape what and where urban development happens (Rydin, 1998). Yet, urban studies frequently highlights how governments, especially at a local level, are pro-development in a way that largely manifests as pro-private sector. As such, particularly in cities such as London, there is an acceptance that the pro-development stance of local authorities and their planning departments (driven by a variety of underlying issues) limits their capacity to govern development (Raco et al., 2016). In this regard, the governance and politics of housing has focused on the ‘what’ (planning housing delivery), rather than the ‘how’ (the aligning of interests of different types of actors) or the ‘who’ (developers, consultants, investors) (see also Raco and Kesten, 2016). Moreover, the shift from government to governance has reinforced a focus on the wider settings, neglecting the heterogeneity of actors within the sector and the multiplicity of approaches that particular firms, people and professional bodies have. As such, it has neglected clearly the dimension of ‘who’ is governed.

That said, in seeking to understand property development, urban studies has examined the roles and capacities of real estate developers. Traditionally, research highlighted developers’ strength during negotiation and planning applications, showing the ways in which developers (often used to represent the entirety of the private sector, or overly simplified; see Adams et al., 2012) are able to create coalitions, partnerships or regimes with local governments to ensure their sites are granted planning permission (Raco et al., 2016). Building on this, more recent analysis has shown how to achieve such partnerships. On the one hand, developers rely on a supportive state which views them as capable of delivering the necessary sites, often to meet housing or commercial property needs in a timely manner (Brill, 2020; Raco et al., 2018). On the other hand, developers actively shape such relationships and are able to utilise their financial and symbolic power to re-configure governance settings, as well as outcomes (Leffers, 2018; Weinstein, 2014). This includes leveraging situations beyond the individual planning applications, such as international status and links to wider geopolitical aims, in an attempt to push forward certain agendas through their projects (Ballard and Harrison, 2019; Mouton and Shatkin, 2020). Developers use curated forms of capital, including cloaking language (Herbert and Murray, 2015), to shape the institutional setting in a way that helps advance their agenda or project (Mosselson, 2020). This power imbalance is further exacerbated by the revolving door of governance, where actors involved in regulation later move to private companies (Robin, 2018). Moreover, these interactions are often very local (Robinson and Attuyer, 2021), with distinct geographies that emerge during negotiations (Ferm and Raco, 2020) such that developer–regulator interactions are fraught with local dynamics and tensions.

Adding to this governance work is a body of research that unpacks what Campbell et al. (2014) termed the ‘black box’ of the private sector, showing the multiplicity of types of developers (Ballard and Butcher, 2020; Charney, 2007) as well as broader types of professionals that surround them and aid in the development process. This work has highlighted what Henneberry and Parris (2013) term the ‘ecology’ that develops during a project, where developers work (to varying degrees of closeness) with different forms of consultants. In this set-up, developers are the co-ordinators or managers of large teams, bringing together what can be a range of expertise (Brill, 2020; Robin, 2018). Within this wide body of expertise an increasingly important set of actors is those involved in funding and financing (see Todes and Robinson, 2020).

Unpacking the role of new forms of finance, research broadly built around the concept of financialisation has sought to demonstrate the strategies of ‘new’ forms of investment in housing, revealing their power and capacity to shape development outcomes across contexts (see Beswick et al., 2016). Research has shown how investor–developer relationships are unstable and change over the course of a project (Sanfelici and Halbert, 2016), as well as the governance of financialised forms of real estate (Anselmi and Vicari, 2020). More recently, shifting the focus towards investor–developer interactions in the rental sector, research has called for a more thorough engagement with purpose-built rental housing or BTR (Nethercote, 2020). In a London context, there is a need to address how ambiguities in the emerging model of post-2008 rental-specific housing have meant policy formation has been reactive and has often lagged behind market development (Brill and Durrant, 2021). Bringing this into conversation with research on urban development and governance is necessary because the bulk of research to date, particularly in a European context, has tended to mimic market patterns: focusing on the more prolific asset class of commercial property. There are notable exceptions to this, though, and work on what has been termed ‘financialisation 2.0’ (Wijburg et al., 2018), particularly the role of real estate investment trusts and other large-scale investors, has demonstrated the changing dynamics of residential property. At the same time, others have noted that the complexity of the private sector and the multiplicity of new forms of ‘investor’ require more academic attention (Özogul and Tasan-Kok, 2020). This is particularly true when looking at how wealth chains have extracted value from urban development in London (McKenzie and Atkinson, 2020). What remains under-addressed is how the actors within these extractive financialised processes are governed in different ways, depending on their particular corporate strategies and risk profiles.

In particular, existing research on the private sector has tended to see the developer as demonstrative of the private sector as a whole, within a particular project, enabled by their co-ordinating position as the centre of development expertise (Brill, 2020; Robin, 2018). Uncovering the differences behind this united front would enable a more thorough engagement with the governance of financialised actors, and consequently enable policymakers to more effectively shape the institutional context of emergent markets (in this case, the rise of residential property as an asset class) targeted by institutional investment (see Brill and Durrant, 2021). This article analyses the city as a whole to engage with and highlight what has been termed the ‘investment landscapes’ (see Raco et al., 2018), to more broadly analyse the ‘black box’ of the real estate profession and understand the governance responses otherwise concealed.

There are two further gaps in the literature that this article hopes to help address. Firstly, despite a huge growth in literature engaging with the multitudes of private-sector actors involved in urban development, and recognition of the importance of taking seriously the private sector (see Campbell et al., 2014; Raco et al., 2018), urban governance literature often fails to acknowledge and respond to the differentiated experiences of actors within the private sector, especially in the context of new types of funding and financing increasingly involved in delivering housing (see e.g. Todes and Robinson, 2020). Whilst research shows how capital gravitates to particular political configurations (Weber, 2010), the type of money and investors, and what they are looking for – both in terms of the eventual asset investment and partners to work with – are less well understood (Guironnet et al., 2016). In London, as with other cities, the rise of a more financialised model of housing delivery and acquisition has led to new actors entering the market (see Beswick et al., 2016). The role of traditional, often small-scale speculative housebuilders is decreasingly relevant for understanding the governance of urban – and especially residential – development. Whilst the bulk of housing over the last 10 years has been delivered by volume housebuilders (Colenutt, 2020), the advent of the global landlord in European cities such as London warrants further attention (Nethercote, 2020). Specifically, there is a need to engage with how different degrees of and approaches to ‘pro-development’ governance structures shape private actors’ strategies in a non-linear, non-expected or differentiated way.

Secondly, this article hopes to address the ways in which entrepreneurial and otherwise pro-development governance shapes the political risk mitigation strategies of real estate professionals. Risk management and mitigation are core components of many developers’ strategies and as such, hugely shape the types of professionals hired and the sites and projects which are built out (Magalhães et al., 2018). Research has demonstrated the ways in which a broadly conceived notion of risk shapes development approaches (see Brill and Robin, 2020), yet the lens of risk has not been fully utilised to understand the politics of development. Moreover, much of this work has focused on a single type of actor – the developer or the planning consultant – without utilising the possibility of comparison within a city or a site to understand the variegated impacts of political risk as experienced and responded to. Again, this is particularly important in the context of new forms of funding and financing that lead to the creation of new asset classes (Revington and August, 2020), where investors and financiers have different time horizons than traditional build-to-sell (BTS) actors (Brill and Durrant, 2021).

Learning from critical risk studies (see Brill and Robin, 2020), it is necessary to unpack how risk is seen and understood by actors, especially within the private sector, and the resultant challenges it poses for them and for governance (see Omstedt, 2020). Urban studies research, particularly of office and commercial markets, has shown the ways in which risk is created within the market, for example how systemic risk is linked to ownership models (Lizieri et al., 2000). Yet there has been less said about how risks are responded to by various real estate professionals (Brill and Robin, 2020). 1 This is important in light of the ways in which risk mitigating and risk management have formed a core component of encouraging institutional investors into property markets (see Gyourko and Linneman, 1990). This encouragement centres on an understanding of risk from the perspective of an asset manager, in which it is argued that diversifying into property represents a key mechanism by which large funds could diversify exposure across their portfolio. Yet there has been little consideration of the other types of risk that these actors would then face; for example, the ways in which new types of actors such as planning consultants or architects are implicated in investment and development decisions (see Imrie and Street, 2009). Of particular importance within other types of risk – those heavily linked to the particularities of property as an asset – is political risk, where the politics of development at both a national and local level manifest as challenges to real estate professionals’ strategies (see e.g. Ballard and Harrison, 2019). As Waldron (2019) has noted, the politics of urban development and the risk profiles of key actors are inextricably linked. Building on this, it is necessary to understand how the particular tools frequently employed – or even the lack of regulatory mechanisms utilised – shape risk mitigation strategies and approaches. This would allow a better understanding of how the politics of development impacts the housing system through both deliberate and accidental policymaking, as understood through a risk-based analysis. This approach also enables analysis to challenge a binary between pro- and anti-development state bodies.

Introducing London’s institutional-driven residential rental (sub-)market

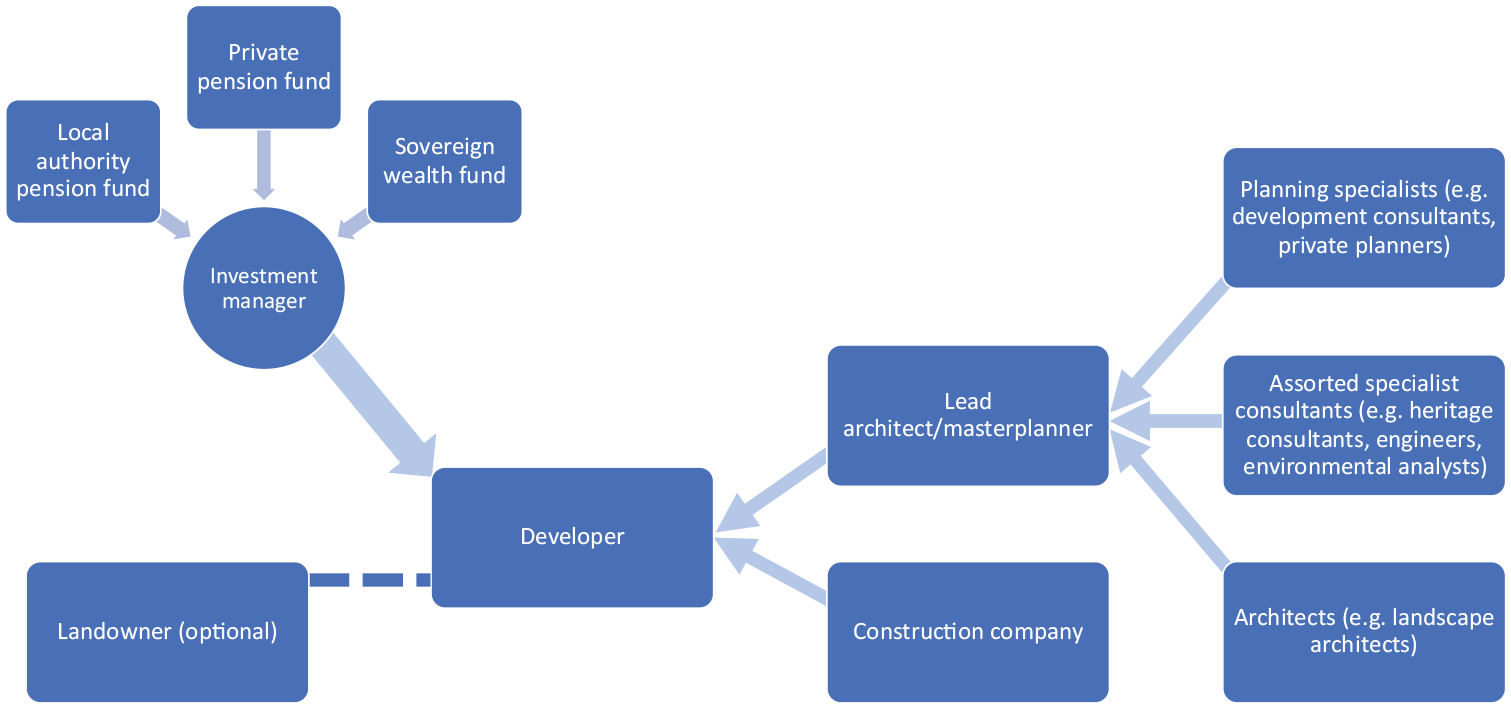

London’s housing production system is dominated by large built-to-sell (BTS) developments. Some of these properties are sold for owner occupation, whilst others, particularly flats, are sold to buy-to-let owners who cater for the growing private rental sector (PRS). The PRS constitutes over 40% of housing provision across the city, but the bulk of this market is provided by small-scale landlords: historically, over 98% of property has been owned by those with fewer than 10 properties (DCLG, 2012). Over the last eight years, there has been a shift, with an increasingly professionalised rental market where over 100,000 corporately managed properties are in the pipeline across the city. This model of development mimics many of the features of America’s multi-family housing, but in the UK it is commonly referred to as Build to Rent (BTR). Much of this property is funded by institutional investors: large asset managers, whose own investors include local authority pension funds, international state funds and some private pensions. This includes key funds such as L&G and M&G, although not all the British headquartered funds have moved into residential, with substantial actors such as Aviva remaining unattracted. These actors are primarily concerned with generating long-term stable income streams that match their liabilities to the pension funds. Residential properties in a market relatively under-supplied such as London are therefore seen as ideal assets because there is a perceived unrelenting demand for such property. However, because they can only invest in assets which are immediately income-generating, they have to use specific funding structures, that is, forward funding, to ensure that as soon as they have made a payment to a developer to bring forward a site, they receive income from the developer, irrespective of how far through construction the site is. During construction, investors therefore receive a ‘coupon’, much like a bond payment, which is typically a pre-defined amount. To summarise the coupon structure, the agent will typically use the land value, construction costs and estimates of developer profit requirements to model expected returns. The investor will have specific requirements on returns, and much of these are met through regular coupon payments. This mimics the commercial property model, such that typically ‘investor coupons run through a project and every draw down of money releases 4% to 4.5% and this is rolled off their balance’ at the end of a development (Appraisal advisor, 2021). In practice, this means if a development is late, developers have absorbed more of the risk because they still have to pay out a coupon to investors; in contrast, investors’ returns are protected.

The corporate structure of such developments is therefore relatively complicated; a simplified typical structure is depicted in Figure 1. As is evident, in a similar way to the orchestration of the development process in BTS (Brill, 2020; Robin, 2018), developers are at the heart of the decision-making process and are charged with bringing the various forms of urban expertise together. However, unlike BTS, the financing and funding are pooled funding upfront to advance a site. In order to question ‘what is governed’ in the part of the housing system captured within BTR sites, it is therefore necessary to understand how these actors and the processes which link them are shaped by regulatory tools, and how the particular firm strategies have been influenced by governance structures, beyond traditional planning literature.

Model of development actors and relationships.

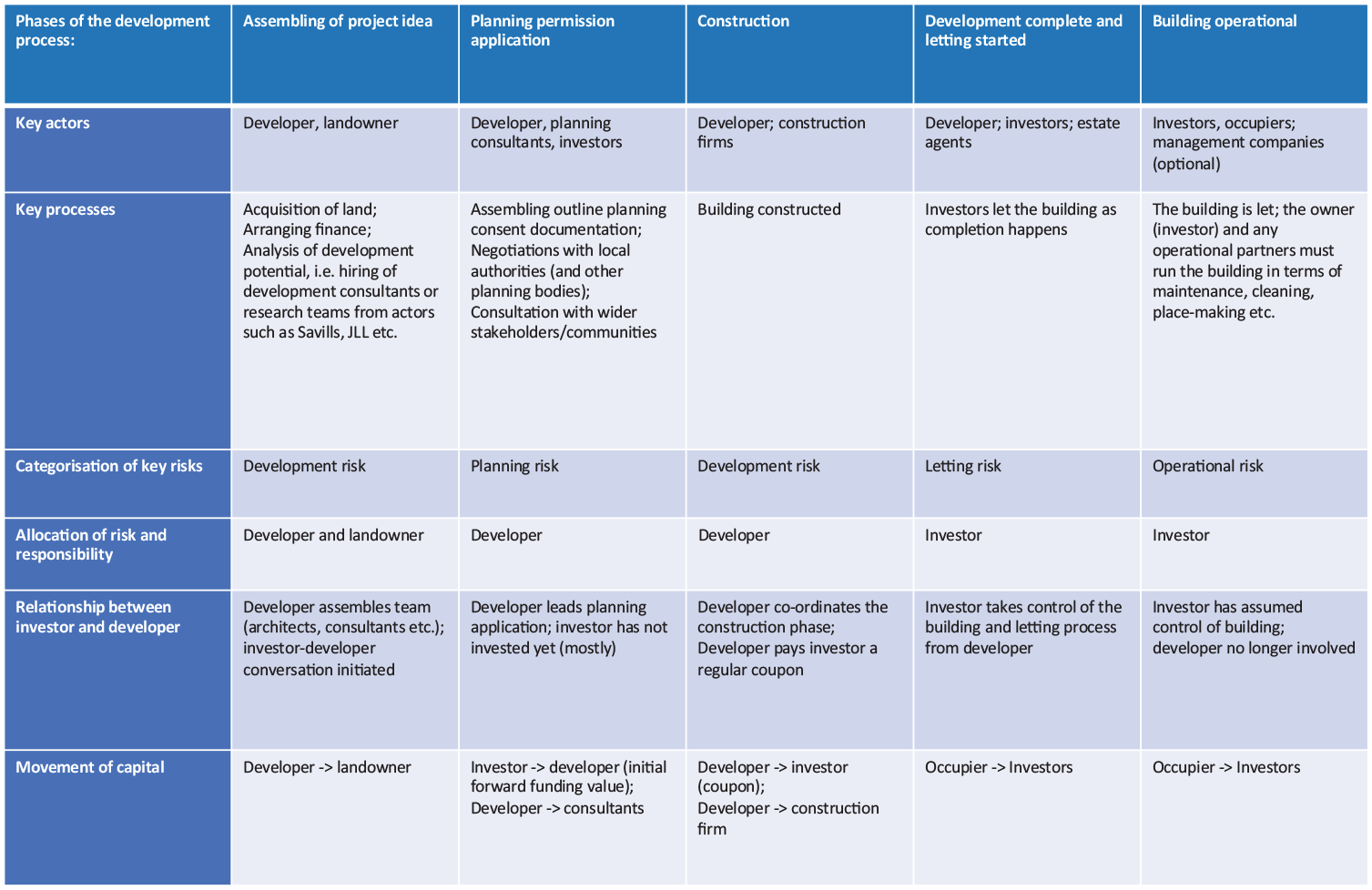

In this article, I address this question by analysing the ways in which these actors relate to the risks of development and in turn what this means for the governance of projects. The evolution of risk over time and its relationship with the actors in Figure 1 are captured in Figure 2.

Development risks during project phases.

This research is based on in-depth engagement with London’s residential investment landscape, in particular over two years (2019–2020), but also drawing on research with real estate developers since 2013. This early work included interviewing 40 real estate professionals, focusing on developers but including consultants (planning, engineering, public relations, community engagement, heritage) and architects (landscape, building, master planning). The more recent research began with early interviews with key brokerage organisations such as Savills, JLL and CBRE. I then mapped the investment landscapes using a commercial dataset from Real Capital Analytics, through which I identified key investors in London. From this dataset, I contacted and interviewed actors from firms who had invested the largest volume of capital into London’s residential market. This included large pension funds (L&G, M&G, AXA), housebuilders and a range of investors (e.g. housing specialist vehicles and mezzanine finance organisations). The interviews addressed the following key themes: (1) individual roles; (2) firm strategies including targets, strategy development and evolution over time; (3) asset investment and identification processes; (4) mechanisms by which developments were co-ordinated within the private sector; and (5) the governance of any decision-making process. In the second set of interviews, I interviewed 85 actors, primarily from the private sector and including pension fund managers, fund strategists, private-sector real estate economists, developers and BTR investors. These interviews were triangulated by interviews with lobbyists and intermediary organisations to understand how real estate professionals responded to and sought to shape particular regulations.

To understand the regulations themselves, following Lascoumes and Le Galès (2007), I identified 100 regulatory mechanisms used to shape housing delivery in the UK. These were collected from a range of sources: (1) planning applications, which indicate the relevant planning applications; (2) interviews with real estate professionals where they were asked to indicate which policies they found most impactful; (3) interviews with local authorities where they explained which policies they found most useful for governing development; (4) parliamentary debates; and (5) commercial reporting from Savills, CBRE, JLL and Knight Frank, whose research teams release frequent reports on significant policy changes. As an indication of the range, the policies most frequently addressed across these five groups were: Stamp Duty Land Value Tax (a tax paid at the point of purchase), Council Tax (an annual tax paid based on property values in 1991, paid to local authorities); Capital Gains Tax; Help to Buy (assistance for first time buyers); and section 106 mechanisms (the tool through which local authorities can dictate affordability requirements for a site). Each regulation was classified based on the scale (in terms of territorial focus); what part of the market they targeted; how they attempted to enact their aims; and their strategic process (in terms of position within the development process). To address the later point, regulations were classified based on their relationship with the market, and the ‘nature’ of the regulation according to Lascoumes and Le Galès (2007). This process did not form a significant part of the later analysis but rather helped target questions around governance in interviews, particularly around the questions of ‘what is governed (or not)’, ‘who’ is governed and ‘how’.

Contrasting risk calculations: Investors versus developers

Investment fund managers typically invest in the early stages of development, after planning permission has been granted, but before construction begins. As explained above, they pool pension pots, from local authorities as well as private funds and funds from abroad. They invest these in particular assets – which in the case of ‘real assets’ such as property broadly translates to ‘sites’– where a developer or housebuilder is bringing forward a development that is either completely or partially purpose-built rental accommodation, which the pension fund manager will then control once the development is complete. For those working as investment fund managers, the management of the risk curve is key to capitalising on the expected yields from a relatively struggling PRS market like London. As such, they need to make sure they are constantly monitoring various forms of risk: ‘we have to get our valuations done, I think it’s every month, they track the development to see how it’s coming along and if we can release the next tranche of payments, so we get that done’ (Investor 12, 2020). They also need to ensure that the risk they take on as a fund manager matches their investors’ risk appetite: so this is about a risk, so this is understanding what people’s investment risk appetite is and then matching it to the relevant residential investment. It’s like a language, it’s understanding what the investor [e.g. a local authority pension fund] wants or what they think they want, translating that into what that might look like from a residential investment point of view and then matching the two together to say, ‘if you want this profile of risk, if you want this type of reputation and exposure or not, this is the asset base that I would match you with,’ so putting the two together. (Investor 9, 2020)

The first stage of managing risk from an investment manager’s perspective is ensuring that they are working with reputable partners. As is well established in urban studies, relationships in real estate develop over years – sometimes decades – and key professionals within a city will repeatedly work with one another (see Brill, 2018; Henneberry and Parris, 2013). Whilst institutional investors have only recently been looking to residential markets in London, many of those involved in new residential funds have worked in new the real estate sector, before moving to a pension fund management company such as Axa, L&G or M&G. That said, investors still have to ensure that the particular site works for their fund, and this decision will largely be based on detailed, granular analysis of potential demand (demographics, job prospects, universities, sources of employment, etc.) at a local level. This is supplemented by a due diligence report on the developer: ‘I guess it’s planning risk to start with, it’s budget risk, it’s things going completely wrong. Obviously, there’s less risk as you start to work with a developer again and again; you can have more trust in them’ (Fund strategist 1, 2020). As one investor explained, sometimes developers will come to them directly with a site and at other times it will be through a broker the investor knows well, but they always have ‘to check that they [the developer] manage their balance sheet appropriately, so not too indebted, they don’t have too much risk, they’ve got a long history’ (Investor 9, 2020).

Once the investor has agreed to invest in the site, they work alongside the developer, constantly monitoring their strategy, and in some cases interviewees noted that this included fortnightly meetings. Yet throughout the early construction period, investors in PRS saw the developer as the one taking the lead because it is up to developers both to co-ordinate the various forms of expertise to bring forward the site (see Brill, 2020; Robin, 2018) and to manage the risks associated with the construction: I see the developer as being the broker, he’s a broker that takes risks, so in my view he’s finding the contractor, he or she is finding the plot of land, and they’re saying, ‘I will come to you, I will raise all the logistics of this and I need you fund it and I will take my cut for doing it, over a three-year period.’ (Investor 9, 2020)

During the construction period, the funds will receive a coupon – in this way, as explained above, the investment strategy mimics the mechanisms of income generation associated with a bond. Throughout this time, therefore, if there are any issues, the developers bear the brunt of the financial risk and the investors are protected.

However, this division of responsibility shifts once the site is built out, as investors then assume the majority of risks, which interviewees broadly categorised as letting and operational risks. Letting risk is the risk associated with renting out the properties and securing tenants. For the most part, this is considered of little concern in London because the strength of the demand for what investors perceive to be high-quality rental properties far exceeds the supply in the PRS. Instead, letting risk mainly manifests as a concern with ‘churn’– the loss of tenants over time: So one of our biggest risks is probably continuity of income, which is occupancy, because it’s very expensive for someone to leave us and to re-let it. All the advertising, the marketing, the time etc. and then the void cost is high, so when you multiply that across 3000 properties and typically people’s behaviours are to leave. (Investor 9, 2020)

Therefore investors are most concerned with maintaining long-term connections with tenants, and some explained that this was done through creating a sense of ownership for the tenants: allowing them to paint whatever they want to if they stay for at least three years (Developer 3, 2019). It is also about creating a sense of community, and many interviewees reflected on the ways in which they had attempted to bring forward sites filled with people: indeed, for established players from America, the primary concern was ensuring that as many properties as possible were tenanted and therefore that there was a ‘buzz’, rather than that the highest rent was achieved from the start (Investor 11, 2020).

In contrast with the perceived ease of letting property in London, managing property for residential tenants was acknowledged across the interviews as something investors did not necessarily have the appropriate knowledge for. In early interviews in 2019, interviewees remarked that the shift towards ‘experiential’ living forms such as BTR had caused a surge in demand for expertise from hoteliers, property management companies, and student housing and senior living specialists (Developer 4, 2013; Investor 1, 2019). For many, the ‘amenities arms race’

2

(Investor 6, 2019; Investor 7, 2019) was driving both investors and developers to provide gyms, shared workspaces and high-quality roof terraces to ensure that the operation of the buildings was attractive. However, as the market has established itself further, interviewees have shifted their language and instead focused on the more mundane parts of operationalising the properties: from the ease of cleaning to ensuring that all lifts are centrally located so they can be used interchangeably if one of them breaks (Investor 12, 2020). The bulk of this work is outsourced to a separate company that operates the property on behalf of the pension fund managers. One investor explained that for him it was about recognising that, whilst an income-generating asset for him and his teams, the property is a home and needs to be managed that way: You have to care for people in a building because it is their home and so it will be 200–300 people, perhaps, in each – maybe more, maybe 500 people in each location – and then there’s the whole operational side of it, from a risk perspective. (Investor 9, 2020)

That said, there was critique of the investment world from some within it, noting that the shift to residential had not been accompanied by the necessary scaling up of skills and in-house capacity to manage property and that this would erode the income streams and undermine the viability of assets in the long run: ‘Very few management companies are actually making money at the moment, and I think one of the things they’ve found is that it’s incredibly granular’ (Investor 11, 2020). This was seen to be particularly true of those who had moved into BTR/PRS from the dominant model of BTS: Unlike other real estate classes, it needs to be built, so there is a development side of it which needs to be done and there needs to be, probably, if you’re building city centre apartment blocks, there needs to be a greater resilience to those blocks, probably, than there is for a for-sale product and an element of economies of scale, because you’re managing the block probably more intensively than you’d manage a for-sale block which, initially, I don’t think was particularly well thought through. (Investor 11, 2020)

At the core of both forms of risk category for investors is a focus on the demand side of the property market: they want to ensure they have a reliable income stream to match their investors’ liabilities, and to guarantee this they must make sure any investment is made into a site with a robust rental market, and that the resultant property brought forward is managed in line with tenants’ expectations.

In contrast to the risks which preoccupy investors, developers who are bringing forward the site from idea to construction completion are most concerned with development risk (see also Magalhães et al., 2018). For the most part, development risk is defined by planning risk: whether or not the developer is able to secure planning permission for the site (Developer 1, 2014). This in turn is heavily related to the expectations of the local authority, and in the case of London the mayoral objectives. In this regard, risk functions as a key means by which the regulation of development can be better understood (Imrie and Street, 2009).

Yet this process has not been without its issues. The bulk of the BTR market has been funded through ‘forward-funding models’, and advocates of these – both developers and investors – see them as fundamentally dividing the risk and reward to reflect the ways in which most of the risk in the planning and construction, which can be long drawn-out processes, is countered by rewards for the developers. However, this was not a universal opinion: the way certain UK institutions have got into the sector, they’ve funded developments in a way that […] the developer is taking the profit and there isn’t an alignment of equity […] they’re effectively getting a coupon through the development phase and assuming that development is risk free – which is just complete nonsense. (Investor 11, 2020)

For this veteran of the PRS market, there was a sense that developers had been leveraging the increased appetite for residential investment by institutional investors to prop up valuations, and that investors were taking more risk than is broadly recognised by developers. As such, he argued that investors: need one hell of a buffer, certainly in terms of the construction phase; over the last couple of years where costs have gone through the roof and you’re then taking on letting risk, in most of these deals which is okay if you’ve factored that in in terms of the day one appraisal, but generally because the underwrite has been probably over the top in terms of what the rental is, it’s not sufficient, so you’re giving your investors increased risk. (Investor 11, 2020)

This investor highlighted how the distribution of risks, especially at moments deemed particularly vulnerable to changing market dynamics, in construction when the project has a defined timeline and costs that cannot change in response to sudden changes in the market, meant investors needed to factor in a greater degree of assurance. This quote evidences the sense of discomfort about the distribution of risks within the private sector. In the context of wider residential and mixed-use developments in London, the role of risk (particularly planning risk) has been shown to heavily impact the negotiation process (see Brill and Robin, 2020). Moreover, the co-ordinating actions of the developer within the wider ecology of a project (see Henneberry and Parris, 2013) directly shape who the community and other stakeholders see as the face of the site and therefore understand to be assuming the risks and responsibilities (see Brill, 2020). Unpacking the types of risk and their distribution demonstrates the complexities hidden behind this front, and ensures a better understanding of how risk appetite shapes individual groups’ actions within the real estate industry.

Emerging complexities in the sector and what this means for governing it

As is evident above, investors and developers have contrasting focuses for their risk calculations, as such investors argued that key in their decision-making process was acquiring a site where planning permission would be hard to get. This contributes to debates about the agency of city and local governments in relation to national legislation and real estate actors that has been revived in financialisation work (see Guironnet, 2019).

The distribution of risk has huge consequences for the governance of the housing market: the various risks which preoccupy the professions within the real estate sector are differentially governed, and therefore, to regulate the market requires ensuring that any policy will target the correct set of actors and processes. The clearest manifestation of this is the different scale of governance that most concerns actors: for developers, the planning authority is most important; whilst for investors, demand-side regulations such as rent control, and at the same time macro-level national policies on property ownership, are of more concern. In this section, I draw on the interviews and discourse analysis of regulatory tools to demonstrate that whilst developers are governed in the current system, there is less city-level governance of investment.

Of the 100 regulatory mechanisms identified, over half targeted the housing market by regulating planning processes. Indeed, throughout the interviews, investors consistently highlighted the importance of challenging planning authorities and the benefits of acquiring a site in a location where planning permission is rarely granted. For investors, who do not take on the risk of planning refusal, having a site with planning permission where supply is limited by the planning system protects their income streams: Coming back to what we’re trying to produce which is long-term, robust, growing income streams, those income streams don’t grow if it’s in an area where supply of housing is very easy to manage because you just put more housing in and therefore rents stay flat, so that’s why London is our primary location. (Investor 9, 2020)

As another investor succinctly put it when comparing different political positions of planning authorities, for areas where: It’s really hard to build, we’ve got an excellent portfolio there, we own pretty much all the best stuff […] it’s great because no one else can come and nick our tenants, it’s the same sort of thing, ‘is it hard to build in a city?’ but that’s actually a positive thing for an investor. It’s a lovely place and that’s part of the reason that we like it, NIMBYism is high. A developer might give you a different answer on that; they might get frustrated that there’s no land. (Investor 2, 2020)

As such, investors actively build this into their strategy: ‘We also try and focus on areas that are undersupplied or that have councils that are quite restrictive about new development’ (Investor 12, 2020). They seek out authorities that are known to restrict development, and in interviews reflected on the benefits of NIMBYism for the protection of their income streams. This is further compounded when the BTS market is factored into the equation: if planning risk is greater, fewer for-sale properties will come to the market too and therefore the rental market is further buoyed: if they’re [the local authority] very pro-development, you’re likely to see less rental growth, basically. If you’re anti-development, it’s probably very expensive to buy there, but the demand is very high and so you have to balance all of those in with each other. (Investor 9, 2020)

Interviewees reflected that this makes the initial process of acquiring planning consent more challenging, but the reward is greater for investors. This division of understandings of the impact of a challenging planning authority entrenches a separation of priorities between developers, who demand and desire planning authorities who are pro-development (for London, see Brill, 2020; Raco, 2012), and investors, who are looking for restrictions to protect their investments.

Within London, this translates to particular boroughs being seen as more desirable, and so the creation of sub-markets: because the planning policies are different, so it’s very hard to build in Southwark, Ealing are much friendlier, for example, so it’s much easier to get permissions for the developer who are, effectively, my counter party, so I’m buying with planning permission, so I’ll buy more stock in Ealing than I will in Southwark and again, that has a knock on, a pro and a negative impact. (Investor 9, 2020)

This in turn impacts the geography of the housing system beyond a simple ‘some boroughs will have more housing brought forward’, because those boroughs where developers are most regulated will be deemed more desirable for professionals looking to hold property and ensure rental yields: institutional investment will not be evenly experienced across the city.

Whilst this knock-on impact of local governance on the geography of housing tenure reflects that the local authorities’ politics are important for investors, the governance they are more concerned with is the national-level regulation. Coding highlighted the emphasis on national-level regulations, as evidenced in one investor’s explanation of which changes have impacted them the most: They’ve just introduced a new stamp duty regime for people who are domiciled overseas, so if you’re a landlord and you have more than one property, you pay an extra 3%. If you’re domiciled overseas, you pay an extra 2% on top of the 3% and each of our buildings average about £75 million and so 2% of that is quite a lot of money and the fund is now £1 billion, as of next quarter, so 2% is a big number, you can knock that all off our bottom line, straightaway, like that [clicks fingers]. (Investor 9, 2020)

As is evident in the quote above, for many investors the concern was the national level of regulations identified in the discourse analysis, and primarily those which were market shaping and economic and fiscal focused.

The governance of the housing system, and any attempt to shape the market, must take account of the diversity within the private sector. Research on the governance of the UK’s housing market, especially London’s, has highlighted the ways in which housing has been used as a macroeconomic tool to prop up the post-2008 recovery (Gallent et al., 2018; Stirling, 2019). Moreover, urban governance literature has highlighted how a viability-led planning system and ‘governance by numbers’ have created distinct geographies in where and what property is brought forward (Ferm and Raco, 2020). By focusing on the risk and unpacking the differential experiences, this article highlights how the heterogeneity within ‘the private sector’ means investors and developers, in a financialised housing market such as BTR, are looking for different sites. Here, analysing the city as a whole also proved to be particularly productive for unpacking the nuances within the sector, to show how investors are actively seeking out those areas where the anti-development authority’s approach to planning permission will protect their revenue stream by limiting competition.

Conclusions

This article offers three main conclusions. Firstly, it demonstrates the importance of opening the black box of the private sector (see Campbell et al., 2014) to reveal not just the multiplicity of developers captured within narratives of ‘the private sector’ (see Ballard and Butcher, 2020), but how these categories of developer relate to other types of professionals in the built environment. In this regard, it adds to existing understandings of the project ecology approach (see Henneberry and Parris, 2013) employed by researchers to show the wide range of expertise required to bring forward a site (Robin, 2018). However, it departs from this body of work by analysing across the city, rather than being site specific or about only one project. In doing so, it shows the contrasting ways that professionals understand and respond to governance mechanisms. This erodes the binary between pro- and anti-development governance bodies because it forces a reconsideration of how regulations at a local level are not universally embraced within the sector and points attention towards other forms of governance.

Building on this, secondly, this article contributes to a greater understanding of the differences within the new forms of funding and financing which have emerged, particularly in the rental sector globally (see Todes and Robinson, 2020). In doing so, it highlights the need to revise the breadth of actors captured within classic governance understandings. Whilst the model in the third section does not seek to be comprehensive, it points to the broadening of professions within the sector. This is essential if we are to understand the ways in which new forms of finance relate to established patterns and actors, and ultimately govern them effectively.

Finally, the empirics demonstrate the application of and potential for theorising urban politics through an analysis of the relationship between risk and governance as a way of understanding what – and who – is governed in the housing system. Recent academic research on financialisation has drawn attention to the role of risk in shaping the strategies of various forms of finance (see Ascher, 2016), and this is true in an urban context too. Indeed, research shows that risk is heavily influential, in terms of what development comes forward and in what way (Brill and Robin, 2020; Magalhães et al., 2018). This article contributes to the theorisation of risk in urban development by showing the relationship between risk and governance, and how that varies by actor and therefore over the course of a development. As projects evolve, different types of professionals become those with the most responsibility and risk, where in the case of BTR developments in London the vast majority of the risk pre-completion is assumed by the developer. That said, in contrast to the idea that planning risk is the most important and that, building on the first conclusion, pro-development planning locations are deemed most attractive for the real estate sector, this article shows how a risk-focused analysis draws attention to the variegated ways in which governance mechanisms are experienced across the sector based on at which points actors become involved in a site. The focus of this article, and applying the analysis across the whole city’s housing system and the development process, highlights the necessity of recognising the subjective way that risk is understood by different actors and the importance of actor-centred governance analysis. Future research is needed to further unpack the notion of political risk, particularly in terms of how it is generated by different state bodies.

Footnotes

Acknowledgements

As with all academic outputs, this paper benefited from conversations with many colleagues. In particular, I would like to thank Jenny Robinson and Ludovic Halbert for helping me think through the relationship between finance and developers at the early stage of this research, and the WHIG team, especially Danielle Sanderson and Mike Raco, for their thoughts on an earlier draft. I would also like to thank Antoine Guironnet for his always insightful views on how to develop my ideas and Sarah Hughes-McLure for her thoughts on risk through the years. I would also like to thank the reviewers for their feedback and the editor for guidance. All mistakes, of course, remain my own.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

This paper is financially supported by the ESRC ORA project ES/S015078/1.