Abstract

Recent literature at the nexus of geography and political economy notes that local governments are becoming financialised. But it is not always clear what this means. Specifically, what is being financialised? And what is the role of local governments in this process? Building on Whiteside’s definition of local state-led financialisation as enabled and internal, this article combines a systematic literature review with the comparative analysis of country-level statistics to clarify this process further. It identifies four channels through which local government financialisation unfolds empirically. First, local governments enable the financialisation of public assets and services through privatisation and outsourcing and by applying financial principles to land use planning. Second, they borrow against their own assets. Third, local governments use bonds and derivatives to manage the risks and costs of their borrowing. Fourth, they invest to generate financial income. Focusing on high-income countries in Western Europe, the article extends the geographical remit of the US- and UK-centric literature. Building on its findings, the article highlights two avenues for further research. First, internationally comparative research can explore how the structural context in which local governments operate shapes their financialisation. Second, critical research into the tension between the objectives and risks of local government financialisation adds nuance to current debates.

Introduction

It is increasingly acknowledged that essential local public assets and services, such as housing, infrastructure or social care, are becoming financialised (Aalbers, 2019; Lindgren, 2011; O’Neill, 2019). Yet it would be hard to imagine such a development without a ‘change in policy and behaviour of public institutions reflecting this financialisation’ (Karwowski, 2019: 1002). Specifically, we would expect a change at the local state level. Indeed, changes in local governance have sparked a debate about how local governments use ‘financially mediated means’ (Peck and Whiteside, 2016: 239) to manage their assets and services (Beswick and Penny, 2018; Guironnet, 2019) and the ways that they borrow and invest (Dagdeviren and Karwowski, 2022; Mertens et al., 2021; Weber, 2010). Local government provides vital services to many people, but especially the most vulnerable. It is crucial to understand how service provision and governance change with financialisation.

We can summarise this debate under the label of ‘local government financialisation’. But while a growing number of academic studies highlight cases of local government financialisation, it is not always clear what that means. Authors focus on different objects of financialisation and diverge in the role they attribute to local governments in this process. The reason could be a disciplinary divide: while geographers tend to focus on the financialisation of urban development, political economists often research changes in local governments’ financial management practices.

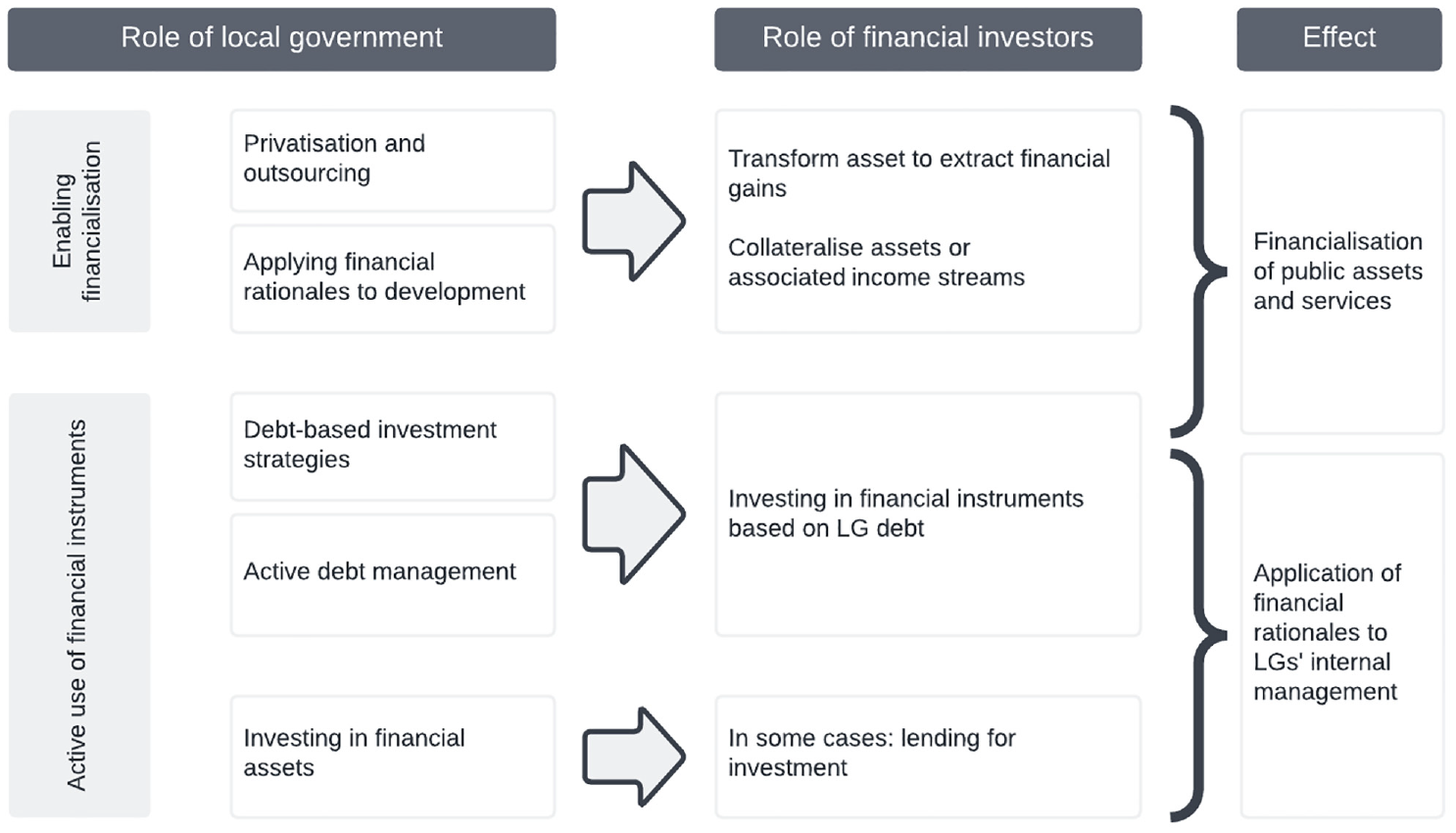

This article integrates research in geography and political economy to enable a comprehensive understanding of local government financialisation. Starting from Whiteside’s (2023) definition of local state-led financialisation as both internal and enabled, I systematically survey the literature and analyse country-level statistics to further clarify the process in Western Europe. I identify four channels through which local government financialisation unfolds empirically. First, local governments enable the financialisation of public assets and services through privatisation, outsourcing and applying financial principles to land use planning. Second, they actively use financial instruments to borrow against assets, transforming public assets into financial ones. Third, local governments use bonds and derivatives to manage the risks and costs of their borrowing. Fourth, they seek to generate income from financial investment. Where local governments actively use financial instruments, they reconfigure internal processes ‘along financialised lines’ (Whiteside, 2023: 237).

While there is a rich empirical literature on the financialisation of local assets and services, such as housing and urban development (Beswick and Penny, 2018; Guironnet, 2019; Savini and Aalbers, 2016), much less has been written about local governments’ active use of financial instruments for debt management and investment. Borrowing, including through bonds, is a longstanding practice in local government. However, this article shows that the scale of borrowing has exploded from 2007 onwards, also coinciding with an increasing uptake of derivatives to manage borrowing risks. This indicates a shift in local governance towards financialisation, which is only starting to reverse recently following the Covid-19 pandemic.

The literature on active financialisation largely focuses on the UK (Dagdeviren and Karwowski, 2022; Mertens et al., 2021; Pike, 2023), with some attention to continental Europe, especially Germany (Hendrikse and Sidaway, 2014; Trampusch and Spies, 2015). Outside of Europe, the literature has mostly focused on North America, particularly the USA, where local government financialisation is more continuous and long-standing (Jenkins, 2021; Weber, 2010). Recent literature has also explored the phenomenon in emerging market economies, notably China (Wu, 2023). This article broadens the geographical focus of research on local government financialisation by analysing data on the financial investment and debt management of local governments in high-income countries in Western Europe. I find substantial variation over time and between countries in the use of financial instruments for local governance. Moreover, in an international comparison, active financialisation is surprisingly low in British local governments, in contrast to the UK’s prominence in the literature. Instead, the article highlights the relatively higher financialisation of local governments in places like Scandinavia, the Netherlands or Austria, which have received far less attention.

Methodologically, the literature I survey, and hence the empirical channels I derive from it, is biased towards extreme cases of financialisation (Ward, 2022). However, research in England and elsewhere shows that the extent of financialisation varies significantly across local governments (Dagdeviren and Karwowski, 2022; Pérignon and Vallée, 2017; Trampusch and Spies, 2015). For example, Pike (2023) identifies a minority of ‘vanguards’ and a ‘long tail’ of local authorities that do not use financial instruments. This means that the conclusions of this article are likely only reflective of some but not all local governments. Despite this caveat, the focus on extreme cases helps us draw out and ‘emphasise the main features’ (Savini and Aalbers, 2016: 890) to develop a better understanding of local government financialisation. The use of country-level statistics, while further obscuring variegation within countries, enables us to consider institutional and macro-level contexts of local government financialisation. For example, the article indicates that the degree of decentralisation, or structural differences in financial market access between countries, may be important in shaping financialisation, despite having been neglected in the existing literature.

The next section develops the conceptual framework for this article. The following two sections discuss how local governments have enabled financialisation and actively used financial instruments in their debt management and financial investment activities. The last section summarises and discusses the findings and highlights two pathways for further research. First, internationally comparative research is needed to explore the macro-level drivers of variegated financialisation. Second, the article draws attention to the tension between the objectives and risks of local government financialisation. A critical evaluation of this inherent contradiction can add nuance to debates on the scope and limitations of local government financialisation.

Conceptualising local government financialisation

Over the last decade, financialisation has gained traction across academic disciplines, including various strands of political economy and heterodox economics. Geographers add that financialisation has a ‘profoundly spatial’ character, as it is often underpinned by spatially fixed assets (French et al., 2011). Indeed, a prolific literature demonstrates how local assets, such as housing and infrastructure, have been engineered into financial assets (Allen and Pryke, 2013; Beswick and Penny, 2018). Despite the diversity of approaches, a common thread in the scholarship on financialisation is the assertion that finance has become more prevalent across various spheres of life, facilitated and propelled by the financialisation of the state (Karwowski, 2019).

Research in political economy highlights two roles that states, at large, play concerning financialisation: an enabling and a more active role (Karwowski, 2019; Schwan et al., 2021). First, states enable financialisation of the economy through policy and regulation, such as financial liberalisation. In this case, some authors argue that financialisation is the unintended result of governments’ reactions to challenging structural circumstances and global competitive pressures – for example, capital control liberalisation in Britain may have been intended to boost export competitiveness but ended up facilitating the current financialised housing crisis (Copley, 2022). This idea of government strategies responding to globalised capitalism’s competitive pressures is reflected in economic geography literature on ‘urban entrepreneurialism’ (Peck, 2012) and, more recently, ‘financialised urban entrepreneurialism’ (Beswick and Penny, 2018; Peck and Whiteside, 2016).

In addition to enabling financialisation of the economy, the state financialisation literature notes that governments have actively invested in financial markets (Schwan et al., 2021; Wang, 2015) and borrowed by issuing bonds (Fastenrath et al., 2017; Preunkert, 2017). Babic et al. (2020) argue that states pursue two broad motives through their investments: control and returns. States invest in strategic sectors, such as transport or energy infrastructure, to strengthen their control over key industries. Additionally, states make portfolio investments, where they are more interested in receiving financial returns than acquiring control of a company or sector (Babic et al., 2020). States use financial instruments in their debt management, for example to create markets for their bonds, hoping to reduce interest rates by selling their debt to a larger pool of investors (Fastenrath et al., 2017; Vetter et al., 2014).

This literature tends to focus on the national state. While important, this obscures nuance relating to processes in the subnational state, and tensions between state actors at different scales. Despite following similar motives of generating additional revenue and increasing control over development in the face of structural constraints, these constraints may play out differently locally. For example, austerity is often highlighted as a pivotal driver of financialisation of the local state (Beswick and Penny, 2018; Dagdeviren and Karwowski, 2022; Deruytter and Bassens, 2021). Yet, local strategies to navigate austerity, such as through innovative tactics to increase their borrowing, are at odds with national objectives of reducing government debt (Lagna, 2015). A rich empirical literature, discussed in detail in the sections below, highlights financialisation in various areas of urban governance, for example land and housing (Guironnet, 2019), infrastructure (Strickland, 2013), social provision (Lindgren, 2011) and financial management (Mertens et al., 2021). Varied methodologies include examining individual regeneration projects (Savini and Aalbers, 2016) and strategies (Beswick and Penny, 2018; Hendrikse and Sidaway, 2014) in specific contexts and timeframes, or comparing financialised practices within countries (Dagdeviren and Karwowski, 2022; Pérignon and Vallée, 2017; Pike, 2023).

Although both address local government financialisation, the literatures on urban development financialisation and local government financial management remain notably disconnected. This fragmentation may result from disciplinary differences; geographers predominantly explore urban development financialisation, while political and heterodox economists tend to focus on financial management practices. That these literatures do not always speak to each other complicates our understanding of the nature of local government financialisation. Specifically, they present different views on what exactly is being financialised, and the role of local governments in this process.

Whiteside (2023: 237; emphasis in original) proposes a synthesising definition of local state-led financialisation as being: (1) internal, which is to say orchestrated through the [local] state’s own property, purchases, and debt offerings, or where state institutions are reconfigured along financialized lines; and/or (2) enabled by state regulatory and budgetary changes that open fiscal space and legal possibilities for financialization broadly.

While this is an essential step towards better understanding local government financialisation, the definition remains somewhat vague.

This article seeks to clarify further the role of local governments in financialisation. Building on Whiteside’s (2023) definition, I systematically survey and integrate geography and political economy-inspired research with the comparative analysis of country-level statistics to identify four channels through which local government financialisation unfolds empirically. First, local governments (unintentionally) enable the financialisation of public assets and services by privatising and outsourcing them and by applying financial rationales to land use planning and development. While this does not have to result in financialisation, it enables private investors to restructure public assets to extract capital and other financial gains and use them as collateral for borrowing. Second, local governments actively use financial instruments when they borrow against their own assets. They do this to strengthen their control over local development but transform public into financial assets in the process. Third, local governments use financial instruments in their debt management, such as bonds and derivatives, to better manage the risks and costs of their borrowing. Fourth, local governments invest in financial assets to generate additional revenue. Thus, in addition to enabling the financialisation of public assets and services, some local governments apply financial rationales to their internal management, thereby reconfiguring local state institutions ‘along financialised lines’ (Whiteside, 2023: 237). Figure 1 summarises this argument, which is discussed in more detail in the following two sections.

Conceptualising local government financialisation.

Local governments as enablers of financialisation

This section argues that local governments enable the financialisation of public assets and services when they privatise or outsource them, or when they adapt planning systems to encourage private investment in local development, thereby adopting financialised logics of urban planning. In these cases, financialisation is enabled by local government strategies but done by the actors in the private sector. Financialisation unfolds through two channels: when privatised assets and outsourced services are restructured to extract financial gains, or when they are used as collateral for borrowing.

Drawing from Copley (2022), financialisation can be seen as an unintended consequence of local governments navigating structural constraints. Existing research emphasises two key influences that shape and constrain the local government operations. First, neoliberal reforms from the 1970s onwards transferred public assets and services to the private sector. National-level cutbacks were often pushed onto subnational governments, impacting social provision at the local level (Gray and Barford, 2018). This ‘devolved austerity’ (Peck, 2012) intensifies fiscal pressure for local governments. The second factor involves the financialisation of the global economy, specifically, growing interest in profitable yet safe investment opportunities in real estate and critical public services (Beswick et al., 2016; Peck, 2012). These dynamics create an environment where financial investors seek local assets. At the same time, local governments grow increasingly dependent on investment, for which they compete with their peers (Savini and Aalbers, 2016).

One response to fiscal and competitive pressure is for local governments to privatise formerly public assets and outsource services. This is often mandated by national governments (Adisson and Artioli, 2020; Christophers and Whiteside, 2021). But local governments have also been more proactive and taken the initiative to market public assets to investors. These strategies at both the national and local level have sought to increase private sector participation in the provision and management of local public services. But how can those strategies result in financialisation?

Outsourced and privatised local public services and assets, including social and physical infrastructure and housing, can be financialised through two main channels. Privatisation does not inevitably lead to financialisation. But when assets are transferred to financial investors like private equity or hedge funds, alterations often occur to raise shareholder value or realise capital gains upon resale (Aalbers, 2019; O’Neill, 2019). Such changes often prioritise dividends or ‘asset stripping’, undermining investment in maintenance and service quality. This diverges from other privatisation forms such as procurement or non-financial public–private partnerships, which tend to emphasise long-term operation and public sector control (Froud et al., 2017). Where privatisation occurs to financial investors, the focus is often on shorter-term financial gains, leading the asset to become ‘as much a financial asset as a physical asset for the production of urban services’ (O’Neill, 2019: 1311).

Throughout Europe, outsourced local public services are undergoing reconfiguration to extract financial gains. Initial outsourcing of education, social care (Lindgren, 2011), childcare (Hall and Stephens, 2020) and care homes (Horton, 2021) involved small local businesses. However, consolidation emerged as a trend, with major financial investors like private equity funds and real estate investment trusts (REITs) entering the social care sector, acquiring smaller entities. These investors tend to prioritise profit generation over the long-term viability of social care services (Horton, 2021). For instance, REITs reshaped care homes for higher shareholder pay-outs by cutting labour and maintenance costs or increasing fees (Horton, 2021). Private equity firms often acquire public service providers with a view to later selling them at a profit, potentially compromising social provision (Lindgren, 2011). Similarly, ‘global corporate landlords’ like Blackstone replicate this approach in the housing sector, capitalising on public and social rented housing privatisation (Beswick et al., 2016; Fields and Uffer, 2016).

However, Wijburg et al. (2018) highlight a shift in the financialisation of housing, which they refer to as ‘financialisation 2.0’. Focusing on Germany’s privatised rental housing, they note changes in actors and practices post the 2007/2008 great financial crisis (GFC). Listed real estate companies like REITs now play a crucial role instead of private equity and hedge funds. The shift is from speculative practices to more long-term investment strategies, prioritising stable cash-flows. On the surface, ‘financialisation 2.0’ may seem less predatory than ‘financialisation 1.0’. But the authors caution that it may still lead to negative consequences like gentrification and further housing commodification, arguing that listed companies are driven to boost the market value of their portfolios to maximise shareholder value, and this objective remains their primary concern.

The second mechanism involves leveraging spatially fixed assets like land or housing as collateral for borrowing. Physical asset value and revenue streams tied to privatised assets and outsourcing contracts can be borrowed against. For example, rental streams or user fees can be used to raise funds on capital markets (O’Brien and Pike, 2019; O’Neill, 2019). Similarly, outsourced service providers can borrow against their goodwill, an accounting technique based on anticipated income streams, such as in the case of the now defunct construction company Carillion (Leaver, 2018). The state’s backstopping of outsourcing contracts supports those practices by effectively guaranteeing revenues to private service providers (Froud et al., 2017). A widely researched example is the Australian investor Macquarie Group, which has conducted a range of leveraged buyouts of infrastructure in Europe, such as Brussels Airport (Deruytter and Derudder, 2019) and Thames Water in the UK (Allen and Pryke, 2013). Macquarie used assets of those companies for further borrowing while elevating dividends and curtailing infrastructure upkeep (Allen and Pryke, 2013).

In addition to the top-down pressure for privatisation and outsourcing, local governments have embraced financial rationales, particularly in the realm of urban planning (Ward, 2022). To attract investment into urban development, planning reforms have been implemented to ‘de-risk’ projects (Gabor, 2021). For instance, local governments have streamlined planning regulations, aiming to make context-heavy projects more standardised and attractive to international investors (Rutland, 2010), and have institutionalised developers’ rights to profits through the ‘viability assessment’ (Bradley, 2021). In England, these reforms unintentionally led to the creation of a market in which planning permissions are traded and used as collateral, but without increasing the number of homes being built. The privatisation of urban development, land and housing – which in turn enables its financialisation – is also promoted by local governments’ proactive efforts to market development projects to private investors, for example by exhibiting at international property fairs (Guironnet, 2019).

In summary, amidst ‘devolved austerity’ (Peck, 2012) and increasingly mobile global investment, local governments privatise assets, outsource services and seek private finance for urban development. What these strategies have in common is that financialisation is enabled by local government but done by private companies at the other end of the equation. Although not deterministically financialising, these strategies enable investors to restructure and leverage assets for profit and use them as collateral. From the perspective of local governments, this is a pragmatic way of navigating a constrained operating environment and continuing to provide critical services. But it transforms the nature of these services, as they become more exposed to financial markets and rationales.

This raises concerns about the distributional consequences of financialisation and democratic accountability in local public service provision. Firstly, investors’ profit motives may affect outsourced public services’ affordability, quality and availability, as seen in education, childcare and water infrastructure cases (Allen and Pryke, 2013; Hall and Stephens, 2020; Lindgren, 2011). Housing being treated as financial investment rather than a social good profoundly affects affordability (Fields and Uffer, 2016). Financialisation also changes the quality of outsourced services, evident in cost-cutting designs for elder care (Horton, 2021). Investors tend to prioritise profitability, and target projects at more affluent populations (Guironnet, 2019), potentially side-lining socially beneficial but less profitable projects like affordable housing (Adisson and Artioli, 2020). Finally, financialised accounting techniques, such as in the outsourced construction company Carillion, whose borrowing against goodwill led to collapse, may affect jobs and services (Leaver, 2018).

Secondly, financialisation also raises questions about whom local governments are accountable to – citizens or investors. When it comes to development planning, local governments may bend over backwards to accommodate – even anticipate – investors’ needs (Guironnet, 2019; Rutland, 2010), possibly disadvantaging more vulnerable populations. In England, the ‘presumption in favour of sustainable development’ in planning regulation offers a way for developers to bypass local planning regulations and aims (Bradley, 2021, quoting MHCLG, 2019: 11).

Local governments’ active use of financial instruments

Besides enabling private investors to use financial instruments, local governments also use these instruments themselves: in debt-based investment strategies, the active management of risks and costs of their borrowing and when they seek to generate income from financial investment.

Debt-based investment strategies

In order to raise funds for urban development, some local governments have borrowed against their assets and associated revenue streams through mechanisms like Special Purpose Vehicles (SPVs) and Tax Increment Financing (TIF). As above, public assets are exposed to developments on financial markets when they are used as collateral. Except here, local governments actively initiate this process rather than merely enabling it. It also signals a shift in local governance towards consideration of financial rationales, in addition to public provision.

Local governments in Europe have used SPVs to achieve development objectives by circumventing borrowing restrictions. SPVs are arms-length entities with a specific and narrow purpose, such as building or renovating housing, providing and managing utilities and health or telecommunication services (Christophers, 2019; Deruytter and Bassens, 2021). While owned by local governments, SPVs’ debts do not show up on local balance sheets. In the mid-2010s, up to a third of local governments in Britain were using SPVs (Barnes, 2016, cited in Beswick and Penny, 2018), including to borrow against their assets or (anticipated) rental revenue and user fees from road tolls (O’Brien and Pike, 2019). SPVs also allow local governments to take a more ‘interventionist’ (Beswick and Penny, 2018) role and strengthen their control over local development processes.

An example is Lambeth Council in London, which uses an SPV to borrow against anticipated rental revenue from council-led housing development. This structure allows the council to access the necessary funds to start the project’s construction without bringing in a private development partner. Not only does this give the local government more control over the shape of the project – such as the inclusion of social housing – but it also allows them to recoup revenue from development projects which would otherwise have gone to a private company (Beswick and Penny, 2018).

Tax Increment Financing (TIF) is another way local governments can borrow against their assets to pursue developmental objectives. It gives local governments access to the increase in taxes resulting from development in a designated area. Local governments can use the ‘tax increment’ to pay for crucial infrastructure in the TIF area, such as to provide or upgrade transport or broadband infrastructure to make the area viable for investment. In addition, they can use TIF to borrow against (future) tax revenue streams. This means that local governments can use the tax increment to make initial investments in the TIF area, designed to attract further private investment, using credit secured against increases in property values in that same area (Strickland, 2013; Weber, 2010).

While TIF is well-established in the USA, where local governments have used it since the 1960s, it is only just being introduced in the European context, and rather sparsely. It is in the UK that the policy was most enthusiastically received (Baker et al., 2016), although its implementation remains limited. Over the last decade, a form of TIF based on commercial property taxes has been used in a handful of areas across the UK to raise money for infrastructure and urban development (Findeisen, 2022; O’Brien and Pike, 2019).

Using SPVs and TIF allows local governments to (re)gain control over development processes and take a more active role in driving local development after decades of neoliberal restructuring. But when local governments develop (debt-based) financial instruments based on public assets, they actively promote the latter’s financialisation. This also entails some financial risks and can have the unintended side effect of uneven development.

Firstly, borrowing against future revenue using mechanisms like TIF and SPVs is a gamble on an uncertain future. However, future revenue may not materialise to the extent anticipated or hoped for (Strickland, 2013; Weber, 2010). In such a case, local governments ‘might have to use [their] general funds to pay down the debts incurred in making the initial investment’ (Baker et al., 2016: 463). They also risk losing public assets, such as land and housing, which often serve as the ultimate collateral for borrowing (Beswick and Penny, 2018). Arguably, this risk is magnified in the case of TIF, where it is the local government itself which borrows, and this activity remains on their own balance sheets rather than in the books of a separate company.

Secondly, local governments’ engagement with finance can intensify structural inequalities between and within localities, as not all local governments are equally able to use innovative financial instruments to their benefit. Strickland (2013) highlights that wealthier cities will find it easier than poorer ones to attract investment into their TIF areas. This is problematic because private investment is needed to enable property values to appreciate and realise the tax increment on which the strategy is predicated. Additionally, authors have argued that gentrification is built into the design of TIF, as the tax increment is realised through increases in land and property values (Baker et al., 2016; Weber, 2010).

Active debt management

In addition to debt-based investment strategies, local governments are using new instruments for debt management. European local governments traditionally accessed loans from public lenders or local banks (Petzold, 2014), but now increasingly issue bonds which can be traded on secondary markets (including in relation to investment strategies, as discussed above). They have also used a variety of derivative instruments. This indicates a shift in local government finances from the mere administration to a more active form of public debt management, whereby local governments seek to optimise borrowing costs and risks (Deruytter and Möller, 2020; Petzold, 2014; Vetter et al., 2014).

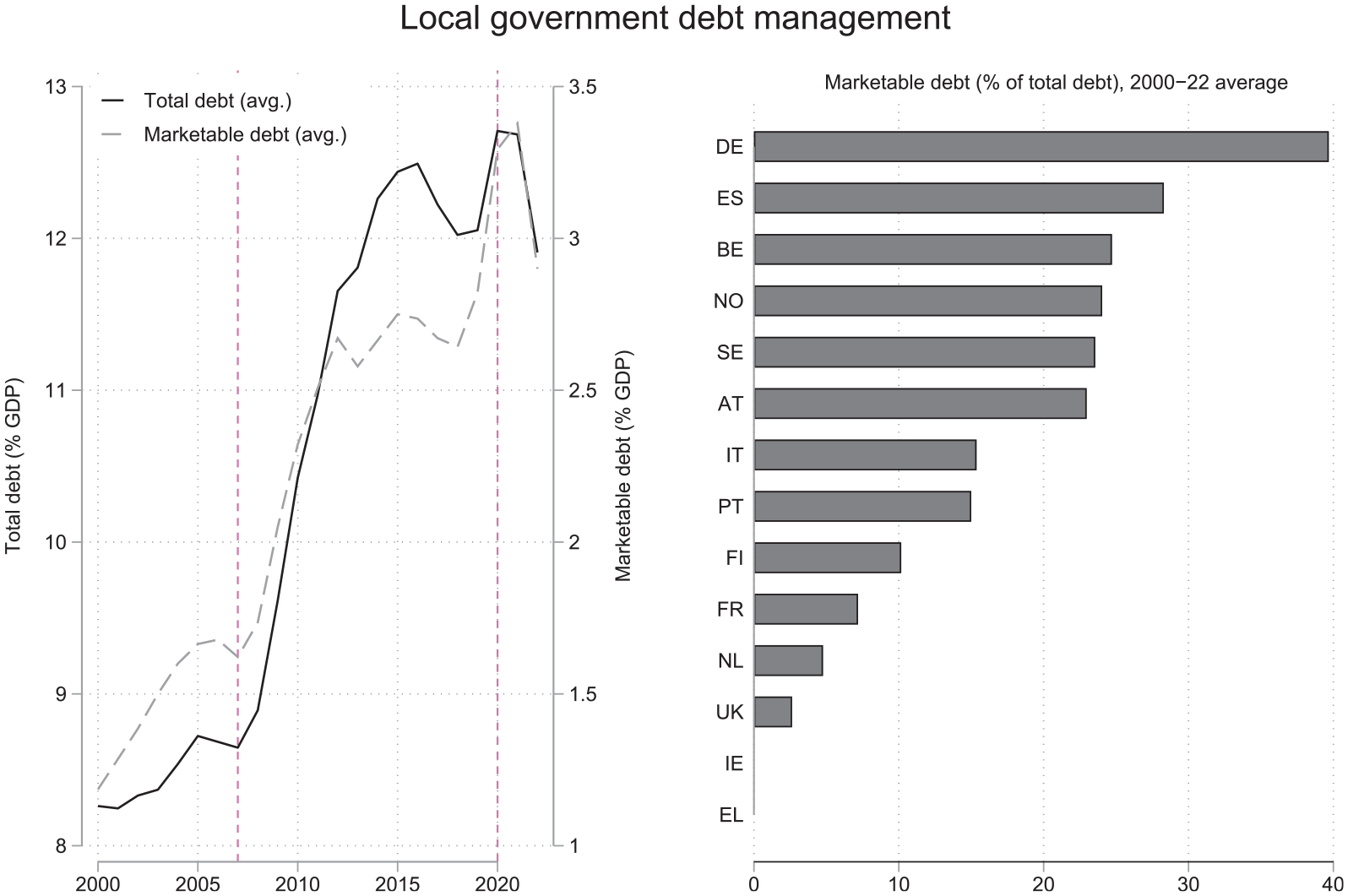

Similar to national governments, European local governments adopt marketable debt instruments, a more recent trend compared to the established US municipal bonds market (Deruytter and Möller, 2020; Jenkins, 2021; Vetter et al., 2014). The left-hand panel of Figure 2 shows the increasing use of marketable debt among European local governments, which has risen in tandem with total local government debt after the GFC, and only slowed down recently, in the wake of the Covid-19 pandemic.

Local governments’ use of marketable debt (bonds) in their debt management.

Sweden pioneered this movement in Europe; in 1986, it launched Kommuninvest, a municipal finance agency, to develop and deepen local government debt markets. France, Germany and the UK have since emulated this model, establishing similar agencies. These are expected to enhance local governments’ access to capital markets by making local government bonds more legible to investors and reducing default risk (Vetter et al., 2014). The right-hand panel of Figure 2 shows the significant role that bonds play in local government borrowing strategies, especially in more decentralised countries. Germany stands out, with about 40% of local government borrowing over the 2000–2022 period taking the form of marketable debt.

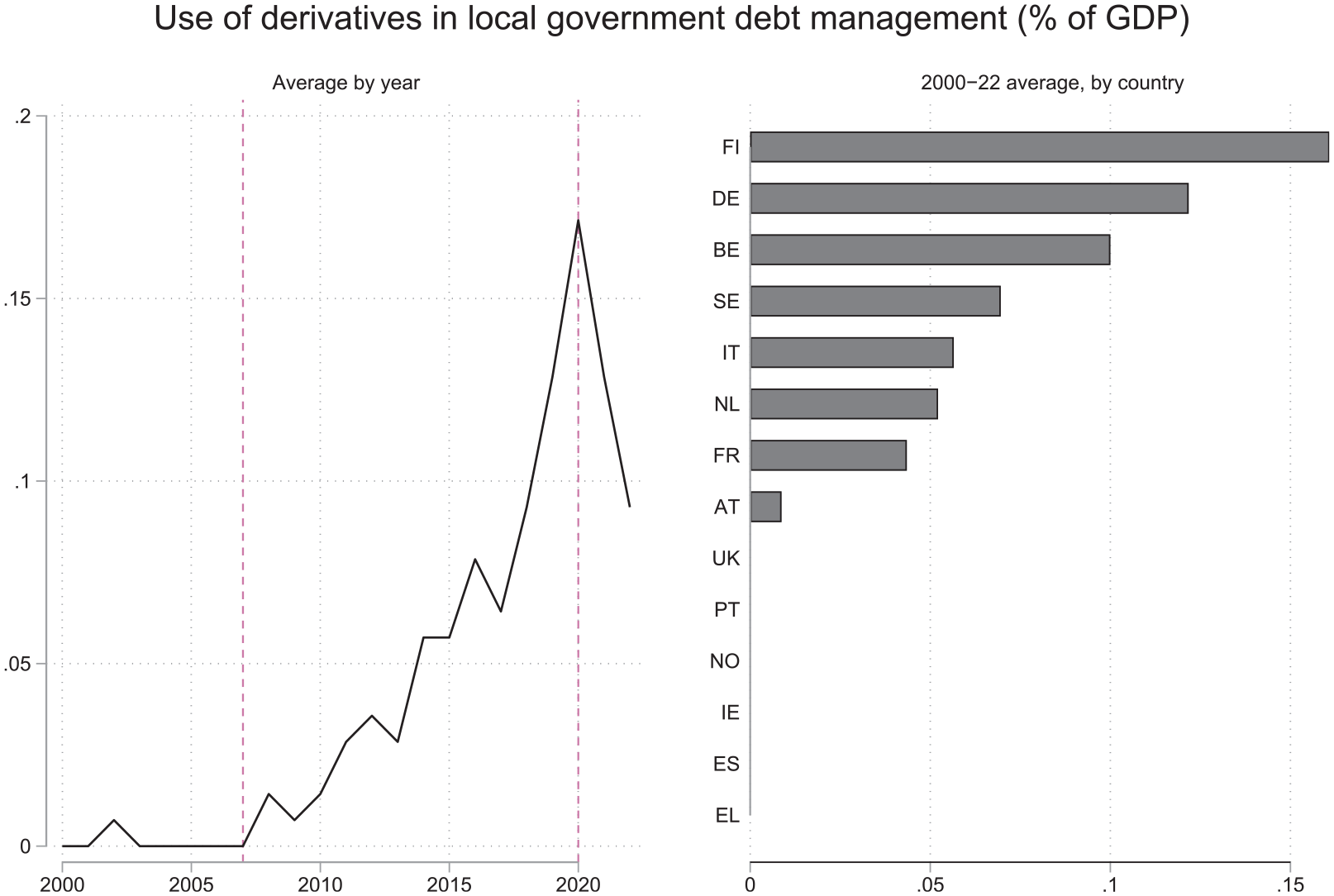

In addition, local governments across Europe have used derivatives, particularly interest rate swaps, to hedge against risks and lower the cost of their borrowing. This was often done prudently, by exchanging variable rates on loans for fixed rates. However, in the low-interest rate environment in the early 2000s, and after the GFC, derivatives were sometimes used to swap fixed with variable interest rate payments. This involved local governments contracting banks to pay fixed rates, while they paid variable rates tied to indices such as the London interbank offered rate (LIBOR). Assumptions about future rate movements guided these swaps, lowering costs when variables remained below fixed rates (Dodd, 2010; Trampusch and Spies, 2015). In the UK (Mertens et al., 2021) and France (Pérignon and Vallée, 2017), this often occurred via structured loans embedding derivatives into long-term loan contracts.

Besides standard interest rate swaps, local governments have used more complex and speculative derivative instruments. Examples are Constant Maturity Swaps, where the interest rate paid by local governments is calculated based on the spread between a long-term and a short-term index (Hendrikse and Sidaway, 2014); and ‘snowballs’, where interest rate payments in one period cannot be lower than the payment in the preceding period (Dodd, 2010). In contrast to standard swaps, it was argued that these more adventurous derivative instruments were often used ‘not to hedge risk but to generate higher income by taking on more risk’ (Dodd, 2010: 34).

Despite post-GFC concerns (Dodd, 2010; Hendrikse and Sidaway, 2014), Figure 3 shows that derivatives are increasingly used in European local governments only after the crisis. While local governments in Finland and Germany seem particularly active in this respect, about half of the sample report limited or no derivative use over 2000–2022, though this might hide derivatives within structured loans.

Local governments’ use of derivatives in their debt management.

Local governments, arguably driven by fiscal pressure, turned to marketable debt and derivatives to manage their finances (Mertens et al., 2021; Trampusch and Spies, 2015). This shift was bolstered by financial investors’ interest in local government debt (Deruytter and Möller, 2020). While derivatives helped lower borrowing risks and costs, some high-profile cases highlighted the risks of this strategy. Firstly, post-GFC turbulence disrupted trends that underpinned contracts, causing unexpected high borrowing costs for some local governments (Dodd, 2010; Hendrikse and Sidaway, 2014). For some local governments in France, these were in the order of one year of tax revenue (Pérignon and Vallée, 2017). Reacting to losses from derivative contracts, Pforzheim, Germany, implemented severe local austerity measures, such as spending cuts to services, investment programmes and public pensions (Hendrikse and Sidaway, 2014). Ultimately, it may be citizens who get to bear the brunt of financialisation gone awry (Peck and Whiteside, 2016).

Secondly, the complexity of financial instruments complicates the democratic oversight and accountability of local governments, exemplified by public outrage over derivative-related losses of taxpayer money (Mertens et al., 2021). Arguably, this issue is particularly salient in local governments’ debt management. Peck and Whiteside (2016: 245) contend that ‘creditors have effectively become a second constituency’ of local governments, potentially conflicting with citizens’ interests. This conflict of interest plays out as local governments seek to align their policy explicitly with the interests of investors (Petzold, 2014). To increase the success of their bond issuance, local governments may signal openness to markets across policy areas including housing and infrastructure planning (Omstedt, 2020), with evidence of markets penalising sovereign borrowers for things like higher welfare spending (Johnston and Barta, 2023). Clearly, this is not always in the population’s best interest, who might prioritise affordable housing, transport and other public goods and services. The conflict magnifies when investors’ interest in being reimbursed takes precedence over local spending needs (Hendrikse and Sidaway, 2014; Jenkins, 2021).

Finally, authors note that local governments’ engagement with finance can intensify structural inequalities between and within localities. Not all local governments are equally able to use innovative financial instruments to their benefit. When it comes to debt management, stronger local economies have preferential access to municipal credit markets, due to higher perceived creditworthiness (Peck and Whiteside, 2016; Vetter et al., 2014). Local governments in ‘core’ capitalist countries may find it easier to use marketable debt instruments to lower their borrowing cost than local governments in peripheral countries, whose bonds are perceived as riskier (Massó, 2016).

Investing in financial assets

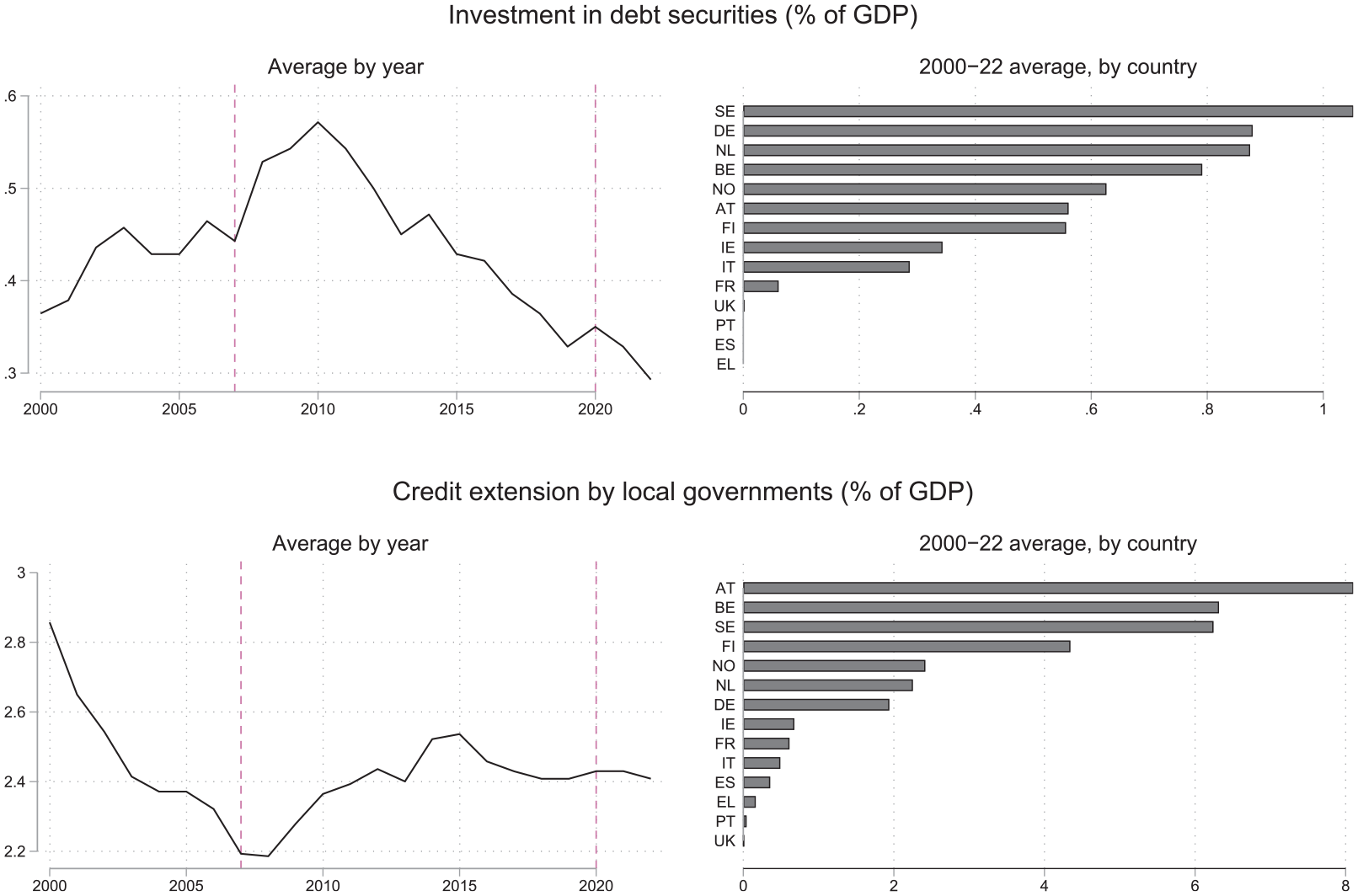

Moreover, some local governments are investing in financial assets. Mirroring processes in the national state, these local governments are turning into ‘financial market player[s], seeking returns from financial assets’ (Karwowski, 2019: 1002). For example, some local governments in Britain have sought to generate additional income by moving away from ‘traditional treasury management methods of holding liquid assets in cash and deposits’ to more high-yielding investments elsewhere (Dagdeviren and Karwowski, 2022: 702). Local governments have invested in a diverse range of assets, including solar farms, shopping centres, supermarkets and money market funds (Christophers, 2019; Dagdeviren and Karwowski, 2022; Davies and Boutaud, 2020). In Belgium, local governments have become increasingly reliant on inter-municipal utility dividends to offset budget gaps from reduced central transfers (Deruytter and Bassens, 2021).

Some local governments also lend money to private and public borrowers. To cope with budget pressure, councils in Britain have created a new market for inter-council borrowing and lending – at market rates (Dagdeviren and Karwowski, 2022). They also offer loans to private companies, including to support local development, for example to facilitate the creation of jobs for their constituency. But another goal is the generation of additional revenue, which is particularly evident when loans are extended to extra-local actors and riskier ventures (Eley, 2021).

The (limited) literature on European local government financial investments largely centres on Britain. Nevertheless, Figure 4 shows that local governments in decentralised countries in Northern Europe tend to be particularly active investors in financial instruments. On the other hand, there is not much evidence of financial investment among local governments in southern European countries, nor in the UK. Countries like Greece, Portugal and the UK not only faced the most intense budget pressure in the aftermath of the GFC and Eurocrisis, but they are also among the most centralised countries in Western Europe. This implies that the extent to which local governments can take advantage of financialisation may hinge not just on budget pressure but also on local government autonomy. Overall, though, the figure suggests that local government financial investment has stagnated or declined in the past decade.

Financial investment of local governments in Western Europe.

Especially during inflation, not investing excess cash might be seen as ‘irresponsible handling of taxpayers’ money’ (Deruytter and Möller, 2020: 406). Lending to local companies can create local jobs, though the extent to which this can be achieved likely varies with the capacity of the local government to impose and enforce conditionalities on their loans. Riskier investments could yield higher returns, but potential losses of public funds may arise if such investments fail, particularly when local governments borrow for investment (Davies and Boutaud, 2020).

Concluding discussion and further research avenues

This article integrates research in geography and political economy to develop a comprehensive understanding of local government financialisation, starting from Whiteside’s (2023) definition around its enabling and internal aspects. The article combined the systematic review of geographical and political economy-inspired research with the comparative analysis of country-level statistics to further clarify the process in Western Europe. The article identifies four channels through which local government financialisation unfolds empirically.

First, local governments enable the financialisation of public assets and services by privatising and outsourcing them. Moreover, local governments apply financial rationales to planning reforms and proactively market development projects to attract financial investors into urban development. While this does not have to result in financialisation, it enables private investors to restructure public assets to extract capital and other financial gains and use them as collateral for borrowing. In these cases, financialisation can be understood as an unintended outcome of local governments’ reactions to structural constraints on their operations, such as austerity and financialisation of the economy (Copley, 2022). Indeed, financialisation might not even be on the radar of local governments. However, second, local governments actively use financial instruments when they borrow against their assets or associated revenue streams. As above, if public assets are used as collateral for borrowing, they get exposed to financial markets and rationales, making the assets’ future contingent on the borrowers’ ability to repay their debt (O’Neill, 2019). The difference is that now the local government instigates financialisation rather than merely enabling it.

When local governments actively use financial instruments, they apply financial rationales to their internal management. The third channel relates to local governments’ active debt management. In the decade following the GFC, local government borrowing, including through bonds, exploded alongside an increasing use of derivatives to manage borrowing risks and costs. At times, derivatives were also used to make a speculative profit. Fourth, some local governments have invested in financial assets, such as debt or equity of private companies, or extended credit to private and public borrowers.

Local governments pursue debt-based investment in development, and financial investment, both to gain control over local development processes and to generate financial returns. Loans to or investments in extra-local private companies ostensibly fall on the return on investment-led end of the spectrum identified by Babic et al. (2020). Local governments’ intention for using TIF or SPVs, on the other hand, is not limited to raising additional revenue in the face of budget pressure – although, to be sure, they are also used for that (Deruytter and Bassens, 2021). But work by Beswick and Penny (2018) and Strickland (2013) makes it clear that local governments embrace the opportunity to use asset-backed debt instruments offered by SPVs and TIF to increase control over development processes and social provision.

Building on the insights developed throughout the article, the remainder of this section highlights two pathways for further research. First, comparative research is needed to explore the structural and conjunctural drivers of variegated financialisation, especially on the international scale. Second, critical investigations into the tensions between objectives and risks of local government financialisation would contribute nuance to current debates.

Comparative research to explore the drivers of variegated financialisation

Evidence presented in this article on local governments’ active use of financial instruments confirms the variegated and uneven nature of local government financialisation (e.g. Pike, 2023). Considerable variation is highlighted in instrument intensity and trends over time, as well as variation between countries.

Intensity

Overall, more conventional instruments are more popular among Western European local governments, with more innovative and exotic instruments having minor roles in local governance. On average, local governments more extensively employ marketable debt and credit extension than derivatives and investment in debt securities. In terms of debt management, marketable debt peaked at 3.4% of GDP, and the use of derivatives at 0.17% in 2020 (Figures 2 and 3). Regarding financial investment, credit extension ranged between 2.2% and 2.6% of GDP, and debt securities investment remained below 0.6% over the 2000–2022 period (Figure 4).

Temporal variation

The GFC marks a pivotal moment, impacting debt management and financial investment differently. Debt securities investment dropped post GFC, while credit extension stagnated. Conversely, active debt management surged post GFC, as marketable debt use increased from 1.4% of GDP in 2007 to 3.4% in 2020. Derivatives usage also grew rapidly during this period (Figures 2 and 3). However, the onset of the Covid-19 crisis abruptly reversed the upward trend in active debt management, possibly due to higher uncertainty and a brief period of increased government spending. Although active financialisation declines at the onset of Covid-19, enabling financialisation might become more prevalent, as the perceived contraction of fiscal space is used to justify greater reliance on private finance for development ambitions (Gabor, 2021). Moreover, inflation increases the urgency of prudent cash management for those with resources, emphasising the need for investment rather than retaining reserves (Deruytter and Möller, 2020). While this is not yet reflected in the data, concern for inflation-related losses could prompt a resurgence in local government financial investment.

Spatial variation

Characteristics of individual local governments clearly impact variegation in their financialisation within countries, including differing risk appetites and expertise (Pike, 2023), indebtedness (Pérignon and Vallée, 2017; Trampusch and Spies, 2015) and the strength of local budgets (Dagdeviren and Karwowski, 2022; Pike, 2023). However, the evidence presented in this article underscores the significance of macro-level and institutional aspects in shaping the extent of financialisation in local governments. Decentralisation and potential structural constraints in accessing financial markets across countries emerge as crucial factors, largely overlooked in existing literature on local government financialisation. Notably, local governments in decentralised Northern European countries exhibit greater use of financial instruments. This contrasts with local governments in Southern Europe (Spain, Italy, Portugal, Greece), which experienced severe austerity following the GFC and Eurocrisis but show lower financialisation, especially in financial investment. However, more decentralised Spain and Italy actively use marketable debt. These findings add nuance to the austerity-driven financialisation thesis, often based on research in Britain (Beswick and Penny, 2018; Dagdeviren and Karwowski, 2022). The evidence presented indicates that the effect of austerity may be mediated through the extent of centralisation and differential access to financial markets of local governments across countries (Massó, 2016). Moreover, the UK’s prominence in the literature contrasts British local governments’ modest financial instrument usage compared to other European countries.

Comparative and conjunctural research is needed to understand how the structural context within which local governments operate influences their financialisation. This would shed light on the reasons behind its occurrence – and, crucially, where it does not occur – and the specific forms it takes (Christophers, 2019). While a substantial literature explores the relation between financialisation and post-GFC austerity, this article highlighted other aspects warranting exploration; notably, the degree of decentralisation and country-level or regional hierarchies in financial market access. Although analyses of financialisation in specific local governments and points in time are helpful (Pike, 2023), a deeper understanding necessitates comparisons across diverse locations and over time. International comparisons of local governments, scarce in current literature (with notable exceptions being Fields and Uffer, 2016; Whiteside, 2023), may be particularly fruitful to explore the role of macro-level factors in shaping local government financialisation.

Exploring the dynamic tensions between objectives and risks of financialisation

Financially active strategies can help local governments under pressure to provide public services and even hold the promise of increasing local state capacity. However, while financialisation may look like an attractive strategy from the perspective of individual local governments, it generates new risks with potential implications for public provision which local governments now have to consider and manage (Bloom, 2023; Farmer, 2014). Risks may be further amplified through interactions between the channels of financialisation.

Risks tied to local government financialisation encompass distributional concerns, financial risks and democratic deficits (Bloom, 2023; Pike, 2023). The extent of these risks varies by financialisation channel. Distributional concerns arise when local governments enable the financialisation of public assets and services and investors reorientate them towards more affluent populations, raise prices (Allen and Pryke, 2013; Fields and Uffer, 2016; Guironnet, 2019) or prioritise profit extraction at the expense of social needs (Horton, 2021). Local governments’ active use of financial instruments may exacerbate inequalities between places, as the ability ‘to utilise financial innovation to their benefit will be uneven’, leaving some places behind (Karwowski, 2019: 1013). The risk of financial losses heightens with debt-based investment strategies, especially based on anticipated income streams (Baker et al., 2016), and with the speculative use of derivatives to generate financial income (Hendrikse and Sidaway, 2014). Enabling financialisation through privatisation and outsourcing involves lower financial risks for local governments, as debt sits on the balance sheets of private actors. State financialisation generally raises concerns about democratic accountability and legitimacy (Karwowski, 2019). For example, local governments may adapt their planning processes and governance to the need of investors, potentially at the expense of local populations (Bradley, 2021; Guironnet, 2019). This risk is magnified in active debt management strategies. When creditors become a ‘second constituency’, repayment priorities may override public service funding (Peck and Whiteside, 2016: 245).

Interactions and feedbacks between the different channels of local government financialisation potentially amplify associated risks. For instance, losses from debt-based investment or speculative derivatives might lead to further local austerity measures (Bloom, 2023; Hendrikse and Sidaway, 2014). These measures could trigger privatisation and outsourcing, enabling further financialisation and new distributional (and democratic) risks. Ultimately, while local governments resort to financialisation to navigate challenging structural conditions, financialised strategies perpetuate those conditions and may even undermine service provision and state capacity. Aligning local policy with creditor interests to increase the success of their debt issuance, local governments not only participate in financial markets but contribute to making a market for their debt. When local governments de-risk private investment in public service delivery, they solidify a system whereby local development becomes contingent on financial investors.

Further research is needed to investigate the tensions between potential state capacity gains and the risks of local government financialisation. With some exceptions (Beswick and Penny, 2018; Pike, 2023), the existing literature tends to either portray financialisation as innovative governance or, more often, to strongly criticise it. Additionally, a focus on processes of local government financialisation has meant that problematic implications are often assumed, rather than actively investigated (a notable exception is Farmer, 2014). Critically assessing the contradictions inherent to the process would contribute to a more nuanced debate around what local government financialisation can and cannot be, and what trade-offs it may entail. For example, future research could examine whether and how structural or conjunctural factors interact with risks of financialisation. Prior research often examines extreme instances (Pike, 2023; Ward, 2022), potentially contributing to the UK-centrism in literature on local government financialisation in Europe. However, limited research exists on other countries, like Scandinavia or the Netherlands, where local governments exhibit much higher financial instrument use. This raises several questions: are financialisation risks heightened by austerity? Conversely, are they attenuated in less austerity-constrained contexts, for example in more decentralised countries where local governments may be less dependent on central transfers? How have risks evolved over time?

Footnotes

Acknowledgements

I am grateful to Bruno Bonizzi, Ian Bruff, Hulya Dagdeviren, Ewa Karwowski, Aleksandra Peeroo, Nils Peters and participants at the 2022 CPERN Early Career Workshop of the Critical Political Economy Research Network, and three anonymous reviewers, for helpful comments on earlier versions of this article. All remaining errors are mine.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author would like to thank the University of Hertfordshire Business School for the PhD studentship that supported the research for this article.