Abstract

A global energy transition requires alternatives to fossil fuels in energy-intensive industries and transport sectors, which are particularly reliant on the unique material properties of fossil fuels as fuel and as feedstock. Renewable energy transitions, therefore, demand large-scale investments in green hydrogen to produce substitutes as a means of indirect electrification. In the context of European climate governance, a political consensus has emerged to support the establishment of such production networks to lower emissions and create renewable-based fuels and feedstock. Yet, despite seemingly strong momentum, investment decisions are far behind global net zero scenarios. Through interviews with key actors, participant observation and document analysis, we explore investments in this type of production capacity, focusing on the challenges associated with financing such investments. We argue that risk expectations and uncertainties around profitability are holding back energy companies and institutional investors from investing in hydrogen and hydrogen derivatives. While investors and creditors await public derisking, fossil fuel incumbents maintain favourable financing conditions vis-à-vis renewable energy developers. These findings suggest clear limits to derisking and highlight the relevance of disciplinary measures to compel incumbents to scale up alternatives to fossil fuels.

Introduction

‘[The hydrogen economy] is here today!’ the president of a prominent interest group enthusiastically remarked from the stage at the German-Danish Green Hydrogen Summit in November 2023. Yet, it was preempted by a noteworthy caveat: ‘I do hope the politicians will take the leap of faith with us – we just need the leap of faith’. 1 Together with 31 prominent actors in the envisioned future value chain, Green Power Denmark had just signed a declaration on a shared commitment to develop a ‘world-leading’ green hydrogen market. Signatories included the oil giant TotalEnergies, major renewables developer Ørsted, the world’s largest chemical producer BASF, and the asset manager and energy developer Copenhagen Infrastructure Partners. Signing the declaration, they officially endorsed the message that ‘national governments must help to kickstart the green hydrogen offtake market’ by advancing hydrogen infrastructure and increasing subsidies to reach stated national and international policy targets. The declaration was the industry’s answer to the question of how to finance this new Danish energy ‘fairytale’. With numerous risks and a substantial price difference between green and fossil-based alternatives, the issue at stake was how to turn grand visions into actual investments.

The focus on investments epitomizes a problem outlined by the International Energy Agency. Globally, announced projects for low-carbon hydrogen (counting both green and blue varieties) will amount to, if built, 38 Mt in 2030. However, only 4% of that potential production has reached a final investment decision (International Energy Agency [IEA], 2023). In Denmark, a similar gap exists between announced projects and committed investments. Developers have announced projects of 20 gigawatt electrolysis capacity by 2030 for green hydrogen but only made a final investment decision on one industrial-scale project of 50 MW capacity. If green hydrogen and its derivatives are missing pieces in the energy transition, how come developers are not making final investment decisions and who is best positioned to do so? In this paper, we take up these questions, exploring how risk expectations guide developments in this emerging production network, focusing on Denmark and Northern Europe. Denmark is an interesting socio-spatial setting because of its geographically specific resource endowments and institutional environment, which make it a potential hub for investments. With a concentration of renewable energy development firms, state ambitions of developing substantial green hydrogen production capacity infused with ideas of export-oriented climate pioneership, and considerable bureaucratic resources dedicated to the issue area, one would expect Denmark to be a hotspot for green hydrogen production (Collington, 2024; Dyrhauge, 2021). Yet, investments are lacking.

The relevance of our study is tied to the unique challenge of substituting fossil-based fuels and feedstock. Fossil fuels serve both as energy carriers and as feedstock to create a host of synthetic materials (Bauer et al., 2023; Tilsted et al., 2023). While renewable electricity production and electrification are the most energy-efficient ways to lower emissions, a range of sectors rely on the unique material properties and high energy density of fossil fuels and therefore seek alternative paths to reducing GHG emissions. Power-to-x is increasingly portrayed as the solution to this problem (Tooze, 2023). The term describes the use of electricity to produce various products that can substitute fossil fuels and feedstock, most prominently hydrogen, ammonia and methanol, with hydrogen being converted to the latter two (Breyer et al., 2024; Palys and Daoutidis, 2022). Power-to-x centres on the substitution of fossil-based products with non-fossil alternatives. With this agenda comes a new set of complications. McCarthy (2015: 2499) highlights dependence on fossil fuels for purposes other than thermal electricity generation as one of the main obstacles to fossil-free capitalism. Similarly, the energy historian Smil (2020, 2016)) highlights long-haul transportation as well as the use of fossil carbon in energy-intensive processing industries as an enormous challenge for energy transitions, pointing to the role of fossil gas for ammonia production and hydrocarbons for plastics. There is thus a critical need to understand what guides and shapes power-to-x investments.

This study extends the literature on the political economy of financing energy transitions and also responds to Baker’s (2023) recent call for greater scholarly engagement with renewable energy infrastructure as an emerging asset class. So far, research on the political economy of energy finance has largely focused on solar and wind energy (Baker, 2023: 23; Christophers, 2022a, 2022b; Luke and Huber, 2022). Extending this literature to so-called hard-to-abate sectors, this paper explores the (lack of) investments in power-to-x and reflects on the implications for scaling. Based on elite interviews and field observations, we analyse investment strategies related to power-to-x and the risk dynamics of financing such investments. We argue that power-to-x buildout subjected to the logic of financial capitalism is challenged by uncertainties in a range of domains that threaten to undermine investments and favour fossil fuel energy firms over renewable energy developers. Consequently, the build-out of hydrogen and hydrogen derivatives may be unduly slow, legitimize fossil fuel companies and be directed towards ineffective end-uses. On this basis, we argue for the need for compelling and reprimanding state interventions to guide investments.

The paper proceeds as follows. First, we review the literature on the role of finance and risk in renewable energy transitions, laying out the basis for our analytical approach. Second, we describe our methods of data collection and analysis, before providing a background section on policy targets and hydrogen production. We then turn to our analysis, showing that risk expectations and the pursuit of bankability in various domains are shaping investments in hydrogen and its derivatives. We end with a concluding discussion of our findings, contending that they support the relevance of alternatives to derisking in the form of more interventionist public finance and the need to rethink the role of fossil-based industries in energy transitions.

Energy and finance

With new investments needed to decarbonize the economy, the intersection between climate mitigation and finance is receiving growing scholarly attention (Bridge et al., 2020). This literature has explored the incentives and ability of energy developers and financial institutions to rapidly accelerate the deployment of wind and solar energy, as well as what form energy transitions take under financialized conditions. Work in this tradition includes Baker (2023, 2015), who argues that the increasing private equity ownership in renewable energy and its logic of short-term commercial interests may threaten the long-term stability of renewable energy build-up. Similarly, Knuth (2018) shows that the impatience of Silicon Valley’s venture capital community contributed to destabilizing the prospect of a clean-tech boom. Adding to these insights, Christophers (2022b) advances the argument that governments' recent drawdown on subsidies for solar and wind power and the lack of credible buyers in the market for power purchase agreements impair the installation of solar and wind energy as investors worry about financial returns.

The mainstream political response to scaling large-scale green investments is that of derisking (Gabor, 2023). Derisking has become the dominant approach to green industrial policy in the United States and the European Union as it serves a broad suite of purposes under financial capitalism – from preserving financial stability to actualizing large-scale infrastructure projects in the Global South (Gabor, 2021; Musthaq, 2023; Schindler et al., 2023). For example, Gabor and Sylla (2023) show how ‘derisking developmentalism’ guides the build-out of green hydrogen production in Namibia, entrenching patterns of unequal ecological exchange. Derisking includes efforts to restructure relationships between the state and private actors around investibility, that is, the question of whether equity holders consider a project to have a satisfactory risk/return profile. Derisking makes investments more attractive through ‘state interventions to steer price signals and correct market failures that generate “uninvestable” risk/return profiles’ (Gabor, 2023: 54). Contrary to what the word suggests, derisking does not remove or reduce risk as such. Rather, it transfers risk from the private to the public sector, creating asset classes that fit the risk-return preferences of developers, pension funds and asset managers (Gabor, 2023, 2021; Gabor and Braun, 2023).

As an approach to green industrial policy, derisking entails various tools, such as favourable loans, guarantees or other forms of subsidies, to align assets with the strategic priorities of private investors. Gabor (2023) argues that the EU derisking approach is constrained by the Euro project and its political limits. Due to EU constraints on state aid, member states cannot directly engage in large-scale fiscal derisking (in contrast to the workings of the US Inflation Reduction Act (IRA)). Moreover, by focusing on attracting and mobilizing private financial capital to make investments, derisking as a climate policy strategy is attentive to phasing in and upscaling low-carbon substitutes. This orientation means that deliberate phase-out (Rosenbloom and Rinscheid, 2020) – which involves restricting the financing of carbon-intensive assets – is peripheral to derisking. On that basis, Gabor (2023) suggests that derisking is unfit to govern decarbonization.

The derisking literature is mainly concerned with macro-financial structures and state relations in the production of investibility. With this macro-orientation, the notion of derisking sheds light on general developments in green industrial policy. We therefore see a need to complement and specify the processes whereby investibility is produced, constrained and takes form in relation to the particularities of different assets. Understanding such particularities is principally relevant for hydrogen and hydrogen derivatives because of the projections and policy targets of enormous build-out and the dilemmas that come with implementation and use.

Investors, risk and bankability

The literature on economic geography has explored the role of risk in shaping production networks. This scholarship tends to distinguish between uncertainty and risk based on their calculability. Whereas uncertainty refers to threats that are not fixed and vaguely defined, risk refers to potential threats that economic actors, in principle, can calculate the probability of occurring, providing them with an indication of future costs and losses (Geenen, 2018). In contrast with this economic-centred notion of risk, Völlers et al. (2023) understand risk as ‘a matter of expectations of the future’ that arise through a dynamic process of collective interpretation (p. 1843). Such processes establish collectively shared risk expectations that structure actors’ decisions in the present. Völlers et al. (2023) highlight how risk expectations are shaped by actors’ values and the social-spatial setting they are embedded in (e.g. political, territorial and network relations). In articulating these insights, we understand perceptions of risk as expectations related to developments and future events that influence the cash flow of – in our case – power-to-x investments.

Our starting point is that risk in place-specific power-to-x projects needs to be connected to particular actors who are situated in a complex social field guided by the politico-economic context (Rodrigue et al., 2011). Because firms are embedded in a capitalist market-based economy, they are structurally compelled to mobilize their organizational resources to ‘grow [their] revenue to stabilize [their] existence’ (Cahen-Fourot, 2022: 15). To the extent that actors foresee unstable revenue streams, as implied by expectations of high risks, risk expectations discourage actors from making investments and credit decisions. This understanding mirrors the findings mapped out in the literature on the political economy of energy transitions, as highlighted in the previous section. This is not to say that investors and developers make ‘optimal’ investment decisions. Instead, we follow Green et al. (2022) in seeing firms as profit-oriented yet boundedly rational.

Actors occupying different roles in project finance approach risk from different perspectives. A crude distinction is that of credit providers (e.g. banks and credit export institutions) and equity investors (e.g. financial investors; Baker, 2022). While providers of credit lend out at a set rate, determined by their risk-return preferences, equity owners are rewarded for taking risks in the form of higher upsides. Credit providers do not receive any extra return if the project exceeds future return expectations. They simply get paid interest in accordance with pre-established contracts. Equity investors, on the other hand, own the investment. Their claims on cash flows rank lower than those of debt financiers, but they capitalize on future earnings if a project goes well and hold the right to sell the assets, carrying the potential for a high return (Baker, 2022). Because of the capital-intensive nature of power-to-x, both types are important to financing investments. Therefore, the risk-return assessments of both equity investors and creditors need to be compatible.

In their project assessments, providers of debt focus on bankability. Bankability describes the financial and non-financial risk-return criteria that projects need to meet for debt providers to extend credit (Baker, 2015; Owolabi et al., 2020). In a question, can you take the project to the bank, that is, take on debt? (Richstein and Neuhoff, 2022). At the heart of bankability is the level of confidence credit providers place in the ability of a given project to generate the returns required to repay the initial debt. The requirements for bankability therefore shape project developments, influencing, for example, choices of technology, ownership structure and issues of engineering, procurement and construction (Baker, 2022). For equity owners, the issue of bankability determines the possibility of obtaining credit and, through this mechanism, influences whether and how to move forward with a final investment decision. In the absence of credit, projects would rely solely on equity, considerably increasing the average cost of capital. Because equity investors require higher returns because of the higher risk associated with higher liabilities, such financing is much more expensive. Debt financing reduces the cost of investment and frees up capital for other purposes (Baker, 2022). Bankability is thus closely connected to what the literature on derisking refers to as investibility (i.e. satisfactory risk-return profiles; Gabor, 2023).

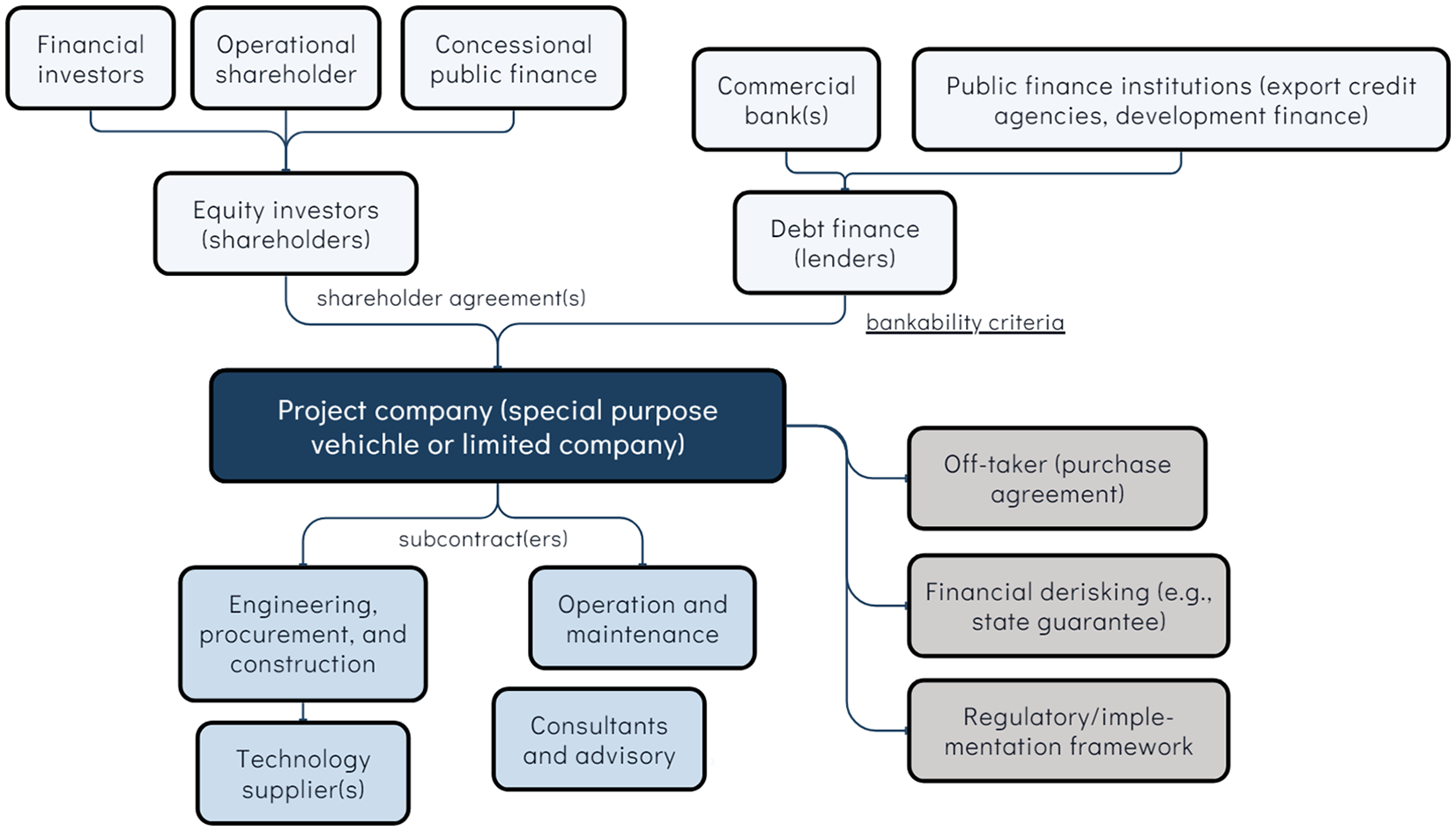

Although criteria of bankability and investibility travel across geography, they are also contextual. This is exemplified by how investments in the Global South generally face higher costs of capital as credit agencies price in so-called ‘regulatory risk’. In Figure 1, we provide a stylized overview of project finance, illustrating the roles undertaken by different types of actors. Project finance typically involves creating a separate entity (often a special-purpose vehicle) that develops, owns and operates the project. This structure limits the risk exposure of the parent company(/ies) by allocating them amongst involved parties, holding them ‘off the balance sheet’ (Baker, 2022: 1748). As also shown in the figure, there are various forms of equity and debt that finance the development of the project. In analogus terms to value chains approaches, we can think of the financial structure of infrastructural assets as an ‘investment chain’, where financial investors, operational shareholders and public financial institutions pursue diverging value capture strategies guided by their business models and governance principles (Cooiman, 2023). For instance, some financial investors (including both small venture capital funds and large institutional investors) might focus on developing greenfield renewable energy projects. Such actors take on development risk and require higher returns on capital deployed than institutional investors, who simply buy into a project once it has reached final investment decisions. The renewably-oriented asset manager Copenhagen Infrastructure Partners, for example, specializes in ‘[building and creating] greenfield premi[a]’ – a strategy typically not followed by their counterparts because it extends the investment horizon (Petersen, 2023). Copenhagen Infrastructure Partners is interesting because it claims to operate the largest dedicated ‘clean hydrogen’ fund in the world (which closed in 2022 with a total of 3 billion euros for power-to-x projects), promising equity investors a rate of return of 10%–14% (Copenhagen Infrastructure Partners, 2024: 7). In comparison, BP reports return expectations of 15%–20% on their hydrocarbon business (while the same figure is 6%–8% on renewables investments), aligning with what other oil and gas companies are reporting to their investors (BP, 2024: 32; Christophers, 2022a). From the onset, then, key actors in the energy transition infer that power-to-x offers a lower return than the fossil fuels it is supposed to replace.

Stylized overview of the structure of project finance.

To sum up, the build-up of power-to-x under existing institutional forms of financial capitalism is premised on market-aligned development where investors can make satisfactory financial returns. To understand the prospects of these investments, we, therefore, need to unpack risk expectations among project developers, investors and credit providers, why they arise and how these expectations relate to the issue of credit extension, that is, bankability. What project criteria and notions of risk are actors attentive to when making their credit decisions, and what are the implications of striving for bankability for investments in power-to-x? In a world where green industrial policy takes the form of derisking and seeks to produce investibility, bankability influences the direction, speed and form of energy transitions in specific geographies.

Methods

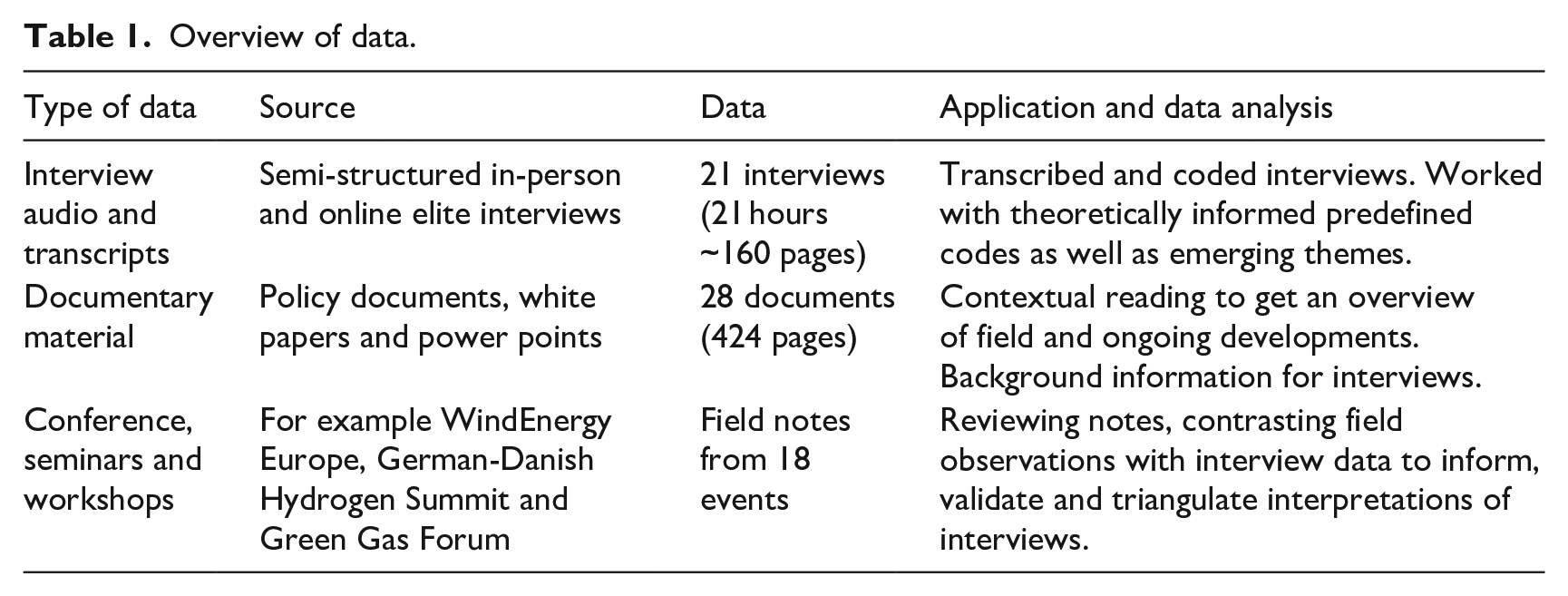

Empirically, this paper focuses on Danish actors, many of whom occupy important positions in the emerging power-to-x production network. These include energy developers from fossil and renewable enterprises, asset managers, institutional investors, gas utilities and state officials. As a social field, the Danish energy sector brings together a wide selection of actors, interests and public-private partnerships. The analysis draws on a range of data sources (see Table 1). We conducted 21 interviews in June–November 2023 with actors who play key roles in establishing power-to-x production. The interlocuters were selected on the basis of their work experience. We mainly sought to interview senior employees working directly with project development and finance. In most cases, we preceded by using publicly available project data to identify relevant companies and then used LinkedIn to find interviewees who worked on finance and investments within the respective organization. In others, we relied on referrals or found participants by participating in industry events. Although many of them were embedded in the Danish context, they also operated in other regions, and interviews also included discussions on their project portfolio as a whole and investments outside Northern Europe. To corroborate our findings, we also interviewed other actors in power-to-x value chains, including industry organizations, utilities, consultants and civil servants (for an overview of the organizational affiliations of the interviewees, see Table A1 in the Appendix A). We collected documents and reports from central actors in the field. We used these documents as background information for our interviews and analysis and continuously expanded the range of documents as new reports with direct relevance to the analysis were published.

Overview of data.

Over the course of 2022–2023, we also conducted field observations at 18 different conferences, seminars and workshops on power-to-x-related issues in a European context. These events included discussions with and presentations by some of the main Danish and European developers, policymakers, industry organizations and state agencies involved in establishing power-to-x production. Industry events provided insights into ongoing discussions. We attended these events at a time with heightened attention and media coverage when key decisions around hydrogen pipeline infrastructure and governance principles were made, which partly informed our decision to explore the issue. For instance, the tariffs on Danish electricity grid usage were being negotiated while we conducted our interviews, resulting in large consumers paying less, vastly improving the business case of power-to-x development in the country. Our hope was that with heightened attention, key points of contestation would have crystallized, as opposed to years prior, where visions of power-to-x had not yet come to the processes of decision-making. When analysing the data, we coded the transcribed interviews in NVivo. We did so through an iterative process, including individual and group coding, to construct themes. We triangulated the codes with our other types of data to identify patterns, which we used to outline the analysis.

Background: Policy targets and hydrogen production pathways

Hydrogen production and consumption

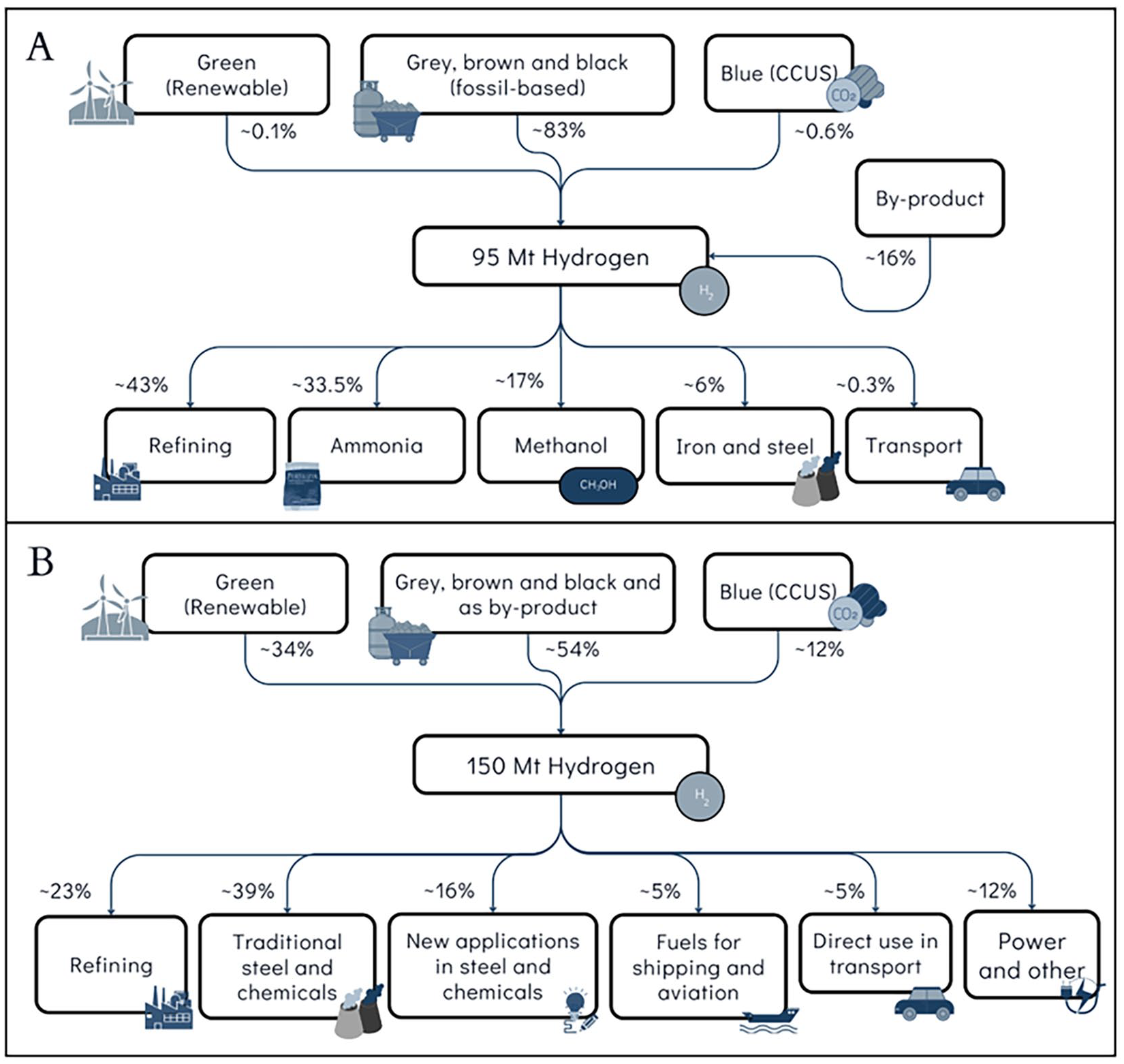

Existing hydrogen production networks are firmly entangled with fossil fuel value chains (Szabo, 2021). Of the 95 million tons (Mt) of hydrogen produced in 2022, 0.1% was green, that is, produced from water electrolysis with the help of renewable electricity (IEA, 2023: 64). Instead, natural gas (grey hydrogen) and coal (black hydrogen) account for the lion’s share of global production, while around 16% are classified as by-product hydrogen, which is produced and used at refineries and in petrochemical production. The most widespread uses of hydrogen include in refinery processes (hydrocracking and desulphurization), as feedstock for ammonia and methanol and other industrial processes (Figure 2). Unlike oil and natural gas (Bridge and Bradshaw, 2017), hydrogen is not a globally traded commodity. All of the hydrogen used at refineries today is produced either onsite or in the vicinity, with 20% of that being sourced from other companies, while essentially all hydrogen for industrial purposes is produced onsite (IEA, 2023: 22–26). The local application of hydrogen arises from its material properties – specifically its low energy density per volume and low liquefaction temperature (Zhang et al., 2023) – which create technical challenges and high transportation and shipping costs in comparison to fossil fuels (IEA, 2023).

(a) Hydrogen production in 2022 and (b) in 2030 in the International Energy Agency’s net zero scenario.

In the future, the use cases for hydrogen are set to expand considerably. Since hydrogen can potentially play a role in a range of applications in energy transitions, an often-invoked analogy is that of a Swiss army knife. Beyond existing purposes in refineries, which are set to decrease throughout an energy transition, and as feedstock for ammonia and methanol, these include synthetic jet fuels, shipping, long-distance road transport and steelmaking. Potential applications go beyond the above-mentioned purposes but are ill-advised due to the existence of more effective alternatives that are directly electrified, such as in the case of electric vehicles and heating (IEA, 2023). With expectations of continuous growth and decreasing GHG emissions, various organizations conclude that hydrogen will scale to new spheres of society, associated with notions of a ‘hydrogen economy’ or ‘hydrogen society’ (Breyer et al., 2024). This outlook requires considerable resources (land, water and energy), technologies that are largely unproven at scale and quite possibly massive geographical reconfigurations for easier access to cheap resources (Bennett and Page, 2012; Gabrielli et al., 2023; Palm et al., 2024). The belief in hydrogen as the energy carrier of the future is therefore contested. Research points to the potential for cannibalizing existing resource use (Grubert, 2023; Tonelli et al., 2023), and projections diverge significantly as a result of varying assumptions on direct electrification. The German think tank Agora Energiwende, for example, suggests that Europe only needs around one-sixth EU targets (Graf and Buck, 2023).

European targets and Danish power to-x ambitions

The EU is positioning green hydrogen as critical to energy security and decarbonization. Following Russia’s invasion of Ukraine, the EU established high targets to expand its initial 2020 hydrogen strategy. The ambition by 2030 is to produce 10 Mt of green hydrogen domestically and import the same amount from countries outside Europe (European Commission, 2022). Europe’s hydrogen strategy is increasingly underpinned by regulatory frameworks that set out governance principles for a new hydrogen market. In 2023, the EU adopted the Delegate Acts, setting out rules and standards for green hydrogen production. It also kick-started the European Hydrogen Bank, which awards subsidies for new hydrogen projects through tenders. By setting ambitious targets, combined with governance standards and subsidies, the European Commission incentivizes energy developers and institutional investors to invest in new power-to-x capacity.

Together with Spain, Portugal and Sweden, Denmark is believed to occupy a strong position in a future green hydrogen value chain, owing to good conditions for offshore wind production and proximity to the large German offtake market (Martin, 2023a). To tap into this value chain, Denmark has a designated hydrogen strategy, aligning with government claims of climate leadership (Dyrhauge, 2021). The government set a production target of 4–6 GW electrolysis capacity by 2030 and provided 1.25 billion DKK subsidies for capital investments, with additional subsidies for research and development. The bulk of hydrogen is intended for export to Germany, as there is currently limited demand for pure hydrogen in Denmark (KPMG et al., 2022). As part of enabling trade, Denmark and Germany signed an agreement in the spring of 2023 on the maturation of a pipeline between the two countries (Danish Ministry of Climate, Energy and Utilities, 2023). The hydrogen interconnector was subsequently adopted on the EU’s list of projects of common interest, making it eligible for EU subsidies and fast-track permit processes (Martin, 2023b). Announced green hydrogen projects in Denmark by 2030 have a cummulative capacity of 20 GW electrolysis, far outstripping politically set national targets. Despite this outlook, final investment decisions have been most prominent in their absence – only one industrial scale project (60 MW of electrolysis capacity) has made final investment decision. In the next section, we delve more into these dynamics, starting by considering why firms would want to engage in power-to-x projects.

Understanding power-to-x investments

Chain upgrading via power-to-x

Investments in hydrogen bring together firms that seem worlds apart. Developers and investors involved in these projects have different legacy assets, company specializations and investment strategies. Ørsted, a global lead firm by market share in the development of offshore wind, recently made final investment decision on its power-to-x (e-methanol) project in Sweden and is developing projects in Denmark, Germany and the Netherlands (Ørsted, 2022). Japanese conglomerate Mitsui, whose subsidiaries are big in steel manufacturing and chemicals, recently acquired a minority stake in European Energy’s e-methanol project in Kassøe (European Energy, 2023). Ørsted and Mitsui exemplify the two main types of potential operators of power-to-x facilities. One specializes in the renewables sector, and the other predominantly owns and operates assets linked to chemicals and fossil fuels. In short, power-to-x brings together renewable energy giants and fossil-based incumbents.

The process whereby firms specializing in wind energy develop power-to-x facilities is an example of what Barrientos et al. (2011) refer to as chain upgrading, where producers shift to new or more profitable value chains. Firms tend to invest in value-added activities to improve technology, knowledge and skills and bolster competitiveness and profitability deriving from participation in new production networks (Gereffi et al., 2005). From a commercial point of view, firms specializing in offshore wind have at least three main incentives for chain upgrading via the power-to-x value chain.

First, converting electrons to molecules is a way for wind developers to move into potentially higher-value markets. These markets have been inaccessible because of fossil fuels' dominance as feedstock and fuel in a range of sectors. Firms tend to engage in economic upgrading in areas that align with their key competencies and available resources (Barrientos et al., 2011; Yeung and Coe, 2015). In offshore and onshore wind, value is captured through expertise in procurement contracts, electricity trade and project zoning. Therefore, they are specialists in sourcing and optimizing the most important input (by operating expenditure) in the production of green hydrogen. In combination with legacy assets (e.g. an offshore wind park), this expertise grants Danish renewable energy companies a potential competitive edge in green hydrogen production.

Second, power-to-x facilities are potential long-term electricity buyers. To develop wind and solar projects in a policy environment less inclined to subsidize such projects as costs have declined, developers operating in liberalized power sectors are looking for long-term power purchase agreements (Christophers, 2022a). This instrument emerged as a means of derisking renewable energy projects by ensuring price stability through contractual agreements where off-takers commit to buying electricity at pre-specified prices. The mechanism assures developers of the profitability of their initial investments and is vital for securing project finance (Christophers, 2022b). However, as also outlined by Christophers (2022b), a key challenge of the market for power purchase agreements is that developers struggle to find limited, credible and large buyers. This predicament makes power-to-x attractive as a means of securing long-term offtake agreements for renewable projects.

Third, and connected to the advantages of sourcing cheap electricity and the need for long-term offtake agreements, power-to-x may enhance the value of renewable energy firms' legacy markets. In Northern Europe, renewable energy developers worry about facing diminishing electricity prices in the market when building out offshore wind. Consequently, the market for offshore wind is steering towards a point where developers’ expected returns on future projects are in jeopardy because the number of profitable operating hours decline – a tendency that further renewable expansion will amplify: There will be periods when there is simply too much electricity production capacity. And there, of course, is an obvious opportunity for us to explore—can’t we somehow make use of it when it has very, very low value? Power-to-x is a natural step for a renewable energy company like ours. (Interview 6)

Hence, value-added activities via hydrogen enable renewable energy developers to hedge against low prices in the electricity market, in principle enabling them to sell electricity to the main grid when the price is high or produce hydrogen when electricity is not attractive as a commodity in its own right.

The seeming compatibility between renewables and power-to-x is no guarantee that renewable developers will invest. Across interviews, we found that developers experienced significant challenges in ensuring the economic viability of their projects, notwithstanding the location of production. A senior employee in the power-to-x team of a renewable energy developer insisted that investors struggle to make green hydrogen commercially attractive on a large scale under existing conditions. He explained that his firm’s power-to-x projects were a form of hedging: There are many paradoxes in this. The cynical one is that you can’t afford not to be involved, because if it’s a big success, you simply must be involved. At the same time, it’s not something you [as a developer] invest in, so the company is about to go bankrupt. (Interview 5)

Thus, renewable energy developers might not be the obvious investors they are cut out to be.

Fossil energy firms have announced a range of large-scale projects in green and blue hydrogen (Palmer, 2023). Potential investments in hydrogen serve a dual function. They serve as a hedge against energy transition policies by diversifying their asset portfolios to include green sectors. The needed structural shift away from fossil fuels, towards energy efficiency and renewable energy, leaves company business models and business portfolios exposed to severe financial risks and asset devaluation (Green et al., 2022). Diversifying their portfolios to include green sectors reduces that risk. In a Danish context, this is illustrated by the oil refining company Crossbridge Energy’s partnership with Everfuel over its HySynergy project. Another example is Trafigura, one of the world’s largest commodity traders and shippers of oil, who recently became the majority share owner of H2Energy and its flagship project in Esbjerg (aiming for 1 GW electrolysis capacity). But potential investments may also signal that fossil fuel companies are setting themselves up for new growth opportunities, positioning themselves to emerge as lead firms if demand for low-carbon gases accelerates.

The capacity of fossil chemical firms to develop and operate power-to-x emerged as a central theme in our data. Consultants and creditors explained that firms in the oil, gas and chemical value chain(s) could be considered ideal owners of power-to-x projects. These projects require the handling and transportation of explosive and toxic gases (with an associated permitting process), which renewable energy companies have limited experience with. Moreover, the resources associated with the material power of fossil fuel companies benefit them: Power-to-x requires more resources, both in terms of personnel and competencies. But also economically, it requires some bigger muscles. And that’s why companies like Equinor in Norway and the big ones like BP, Shell, and all those are setting up projects. They have completely different experiences and muscles they can play with. They may not necessarily have experience with solar and wind, but they have chemical industry experience. (Interview 7)

The advantages of oil, gas and chemical firms in power-to-x value chains amount to a form of ‘semi-incumbency’; they can utilize existing skills and assets – especially in the case of blue hydrogen (Halttunen et al., 2023). But how does this influence the prospects of financing investments?

Taking power-to-x to the bank

Scaling green hydrogen and power-to-x is predicated on investment decisions. But to commit to such investments in conditions of uncertainty requires, ironically, a sense of certainty. The relevant decision-makers need to believe in the expected return of a given project to the point where project rewards are deemed credible. In other words, they need to be bankable. As put by a senior project manager in a financial institution when describing the power-to-x landscape: The overarching topic here for us is bankability, meaning that you can make your final investment decision as an investor, and you can make your credit decision as a lender. These two things are connected by actualizing bankability. So, everyone in this industry talks about bankability. Bankability, bankability, bankability. These projects must be bankable. (Interview 2)

Establishing bankability in a non-established and, from an energy perspective, structurally disadvantaged market position is no easy task. One interviewee working on financing projects outside of Denmark described power-to-x as ‘risk on steroids’ (interview 17). While political targets and global scenarios for hydrogen-based fuels and feedstock signal vast opportunities, and while renewable energy companies might consider hydrogen production crucial to their future business models, bankability puts such prospects to the test. Political attention might encourage ‘an industry of PowerPoints’ (interviews 2 and 10) and a multitude of project proposals, but investments are driven by profit expectations (Christophers, 2022a).

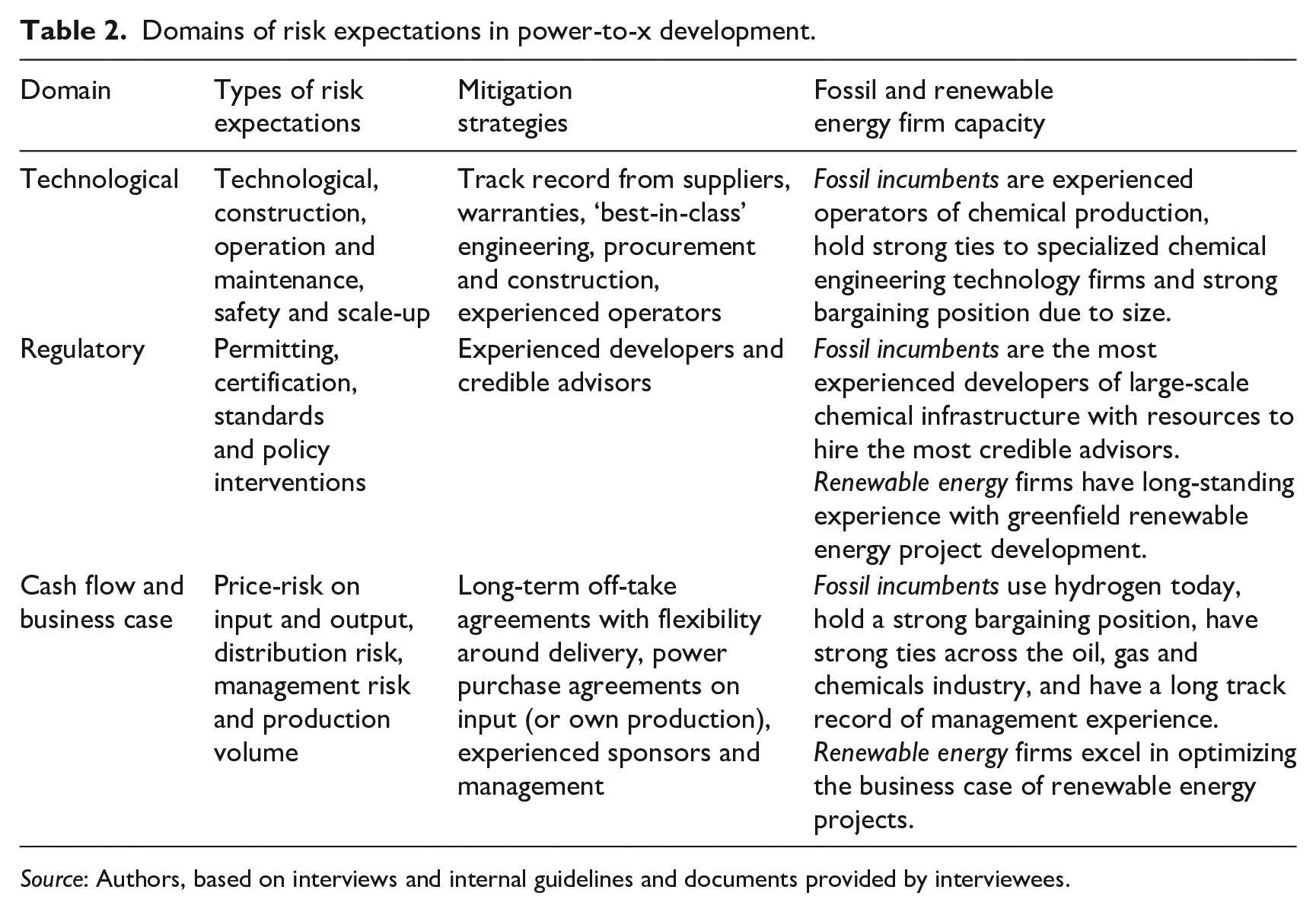

Actors reference issues that influence the ability to make final investment and credit decisions in three central domains, namely (i) technology, (ii) regulation and (iii) project cash flow (see Table 2). To deal with these and establish bankability, ‘a sufficient amount of uncertainty needs to be closed down’ (interview 3). Projects are thus evaluated based on financial and non-financial criteria that affect bankability and the extent to which actors can establish credibility around projected rates of return.

Domains of risk expectations in power-to-x development.

Source: Authors, based on interviews and internal guidelines and documents provided by interviewees.

In terms of the technological domain, risk expectations are related to the fact that running electrolysis at an industrial scale requires significant resources and is a hitherto largely untested practice. Renewable energy developers that seek to enter this market have not previously been producing hydrogen or running electrolysis facilities – and so is the case for other actors in these production networks. Several interviewees note an extensive lack of experience with operating at scale, referencing that electrolysis suppliers operate on new terrain when seeking to provide the necessary equipment to go beyond 5–10 MW projects (interviews 2, 4, 5, 6, 7, 10 and 11). Moreover, electrolysis has historically operated with constant output and stable energy provisioning. Actors do not have experience operating an electrolysis facility on intermittent electricity and report uncertainties related to performance and thereby profitability. Connecting hydrogen production to ammonia or methanol, in turn, adds to these difficulties of coordinating the power-to-x-production interface. Despite widespread hopes that institutional learning and increasing scale of production will drive down prices of electrolysis and optimize production, the lack of experience and know-how constitutes a central barrier to bankability: There is a scale-up risk that all banks are afraid of; there is no one sitting there saying this is super cool. (. . .). And there are two things. One is building electrolysis that is bigger than five megawatts. It's simply new. (. . .). To go from one to two megawatts and up to something bigger than a gigawatt. That is a crazy assumption, is it not? The other thing is the factories that will produce electrolysis plants. [They make] investment decision[s] about (. . .) megawatt plant[s] (. . .). So going up to 1 gigawatt is something else. (Interview 2)

Another set of risk expectations relates to the domain of regulation. In a technologically locked-in fossil energy order with significant direct and indirect subsidies for hydrocarbons and global competition (cf. Newell, 2019), interviewees emphasized the need for certainty around regulation that changes the fundamentals of investment decisions. In Denmark, for example, developers and industry organizations lobbied for changing the costs of using the electricity grid, substantially improving the commercial viability of power-to-x-production (interview 4, 9, 10 and 11). In the EU, decision-making bodies have agreed on frameworks for green hydrogen classification and production subsidies (which are to be handed out through auctions), as well as mandates for green hydrogen usage and hydrogen-derived fuels (Martin, 2023a). As all these forms of regulation improve the economics of power-to-x projects, their form and extensiveness are decisive for credit and investment decisions.

In terms of bankability, regulatory risk pertains to more than changing a given project’s risk-return profile, namely issues of environmental permitting and safety for production, transportation and storage. Therefore, lack of experience and juridical competencies complicate project development. As explained by a developer: The process [you have to go through] to get permits for [power-to-x projects] (. . .) has, of course, created learning both for us and for the authorities, which makes it easier for the next projects. But it hasn't been easy. If you make the projects that much bigger, there are completely different environmental implications that need to be uncovered and mitigated. But the hardest part is all the safety and risk involved because these [projects] are chemical plants where there is a risk of explosion. That risk becomes that much greater when you're producing larger quantities. (Interview 10)

In this context, knowledge relatedness and resources favour fossil fuel incumbents, which already work with chemical production and have decades of demonstrated experience on a large scale (interviews 2, 4, 6 and 10). As put by the senior project manager making credit decisions on power-to-x: ‘When Total, Shell, and BP decide to look at GW projects (. . .), then banks listen’ (Interview 2).

A final set of issues is related to the uncertainty of the cash flow related to the business case itself. To ensure bankability (given that facilities work as intended under an expected set of regulations), developers and debt financiers need to believe that profitability expectations are viable. Profitability depends on costs and revenues. On the cost side, developers reference a range of practices they use to estimate future costs that take into account the geography of the specific project. Relying on in-house competencies, project partners and hired consultants, these practices include feasibility studies, projections of future electricity prices and modeling how to optimize production flows (interviews 4, 5 and 10). Such cost projections can play a pivotal role in final investment and credit decisions, with the cost of electricity amounting to around 75% of the modeled operating expenditure (interview 15). For example, a senior portfolio manager in a large asset management company explained how their modeling showed that they could not move forward unless policymakers agreed upon more favourable indirect electricity subsidies (interview 4), while a lead technology officer working for an energy developer favoured methanol production because they had a modeling ‘breakthrough’ on how to optimize methanol synthesis (interview 5). The need to establish credible cost projections in a new area creates additional challenges for developers. Several interviewees – including consultants themselves – note the dependency on hiring external personnel. Given the uncertainty around cost projections, the credibility of advisors matters in obtaining credit.

On the revenue side, long-term offtake agreements are essential for bankability and credit decisions, as developers and creditors alike emphasize the need for certainty around price and cash flow. The necessity of offtake agreements follows from the lack of market structures and prices associated with the immaturity of green hydrogen, ammonia and methanol production and trade (Dejonghe et al., 2023). Long-term offtake agreement is a risk management strategy developers employ to lower the price risk associated with upfront capital investment, exposing end-users to price fluctuations instead. The level of risk exposure is a function of contract length and pricing mechanism – whether fixed or commodity-indexed (and in that case, which commodity the end-product may be indexed to). Similar to the role power purchase agreements play in financing renewable energy (cf. Christophers, 2022b), the bankability of power-to-x projects is predicated on off-take agreements. As noted by a credit provider, ‘bankers are incredibly boring; we just want our money back’ (Interview 3).

Off-take agreements, however, face a long range of obstacles. Because green alternatives are not cost-competitive, off-take agreements require parties to settle on a sufficient ‘green premium’ (interviews 5, 6, 9 and 11). In global markets like shipping, chemicals and steel manufacturing, off-takers may be reluctant to agree to a green premium on a long-term contract as they worry about their competitiveness (Interview 16). Moreover, and for hydrogen in particular, off-take agreements require a credible form of transportation. Because the low energy density of hydrogen creates high transportation costs in liquid form, actors in the value chain posit that there are no real alternatives to hydrogen pipelines in Europe, including in the case of Danish projects meant to serve German demand. That creates what several interviewees dub a ‘chicken and egg’ problem where investment decisions require off-take agreements and off-take agreements require power-to-x infrastructure, while the commitment to building such infrastructure (including hydrogen pipelines) requires credible large-scale investments.

Taken together, the characteristics of power-to-x make investments more akin to refineries than to wind and solar farms, and the issues related to achieving bankability mean that vertically integrated oil and gas firms are favourably positioned to realize large-scale projects. In the few cases where dedicated renewable energy developers had moved forward with a final investment decision, actors pursued a strategy around minimizing perceived risk. They did so mainly by pursuing clear demand signals and building small-scale operations. In smaller projects, investors and developers might be willing to accept existing risk expectations. Small projects do not significantly impact corporations, and the prospects of showcasing proof of concept and positioning for potential upsides might thus compensate for the possibility of project failure and the uncertainty around profitability. Moreover, developers seek to maintain flexibility in their commitments. The head of power-to-x at a major renewable energy firm proclaimed at an industry conference that ‘[we] stand ready to partner with off-takers, but also ready to shut [the e-methanol project] down if we do not see the policy signals’ 2 . The firm’s plans for global production capacity ranged, accordingly, from 4 to 44 GW.

Across the three domains of bankability challenges, fossil fuel incumbents are favoured compared to renewable energy developers (see Table 2). Various interviewees emphasized the competitive edge of integrated oil, gas and chemical companies when it comes to actualizing large-scale power-to-x both inside and outside of Denmark, due to their specialized chemical engineering knowledge, proven track records of operating large chemical facilities, and the ability to absorb price fluctuations through revenue streams from fossil fuels. One interviewee explained how colleagues in large international banks that formerly worked with oil and gas now work with power-to-x and hydrogen due to the similarity in terms of financing (interview 17), while another noted that their engineering consultancy firms were hiring oil and gas professionals to grow their power-to-x-related business (interview 7). A project manager at a renewable energy developer also explained that they initially engaged with power-to-x without fully grasping that they were ‘setting up a refinery’ and not another renewable energy project (interview 10). The challenges of financing and the relevance of fossil fuel incumbents as actors in actualizing power-to-x raise an important discussion for the hope of a rapid and just energy transition.

Concluding discussion

Institutionalized targets for hydrogen production and industry actors pushing green hydrogen as the next frontier of the energy transition invite significant investments in power-to-x. However, as mapped out above, investments are far behind net zero scenarios and renewable energy companies are struggling to make projects bankable. In this section, we discuss our findings and reflect on the implications for energy transitions and the build-out of power-to-x.

Power-to-x is not a new iteration of renewable energy that simply comes on top of what already exists but is instead conditioned upon a reconfiguration of energy systems. From an energy system perspective, including the Danish, green hydrogen production makes 100% renewable energy systems possible as a means of indirect electrification, storing energy and creating flexibility (Breyer et al., 2022). The intermittency of solar and wind means that the system needs enough renewables to power the grid in unfavourable weather conditions, resulting in overcapacity at other times. This electricity can then be used for power-to-x. At the same time, power-to-x helps ensure the profitability of renewables by offsetting the downward pressure on electricity prices that results from overcapacity. As such, renewable energy developers seemingly need power-to-x when looking ahead. These prospects establish a complex interdependence, where the investibility of power-to-x is predicated on low enough electricity prices while the investibility of renewables depends on high enough energy prices, and where electricity prices themselves are partly determined by the build-out of both. Power-to-x is not simply a new asset adding to a portfolio of green investments, it changes the dynamics of renewable energy investments. Alternatives to such complex future interdependence between returns from power-to-x and renewables exist outside of the Danish context. Prominent examples include renewable energy projects in regions where oversupply is not a relevant consideration (at least at the time of investment), megaprojects that produce shippable ‘x’s’ in geographically advantageous regions for solar energy (e.g. Brazil and Australia) and locally integrated projects (e.g. green steel production in Northern Sweden). Notwithstanding the specificities of project design and geography, the attractiveness of power-to-x as an investment is predicated on its risk-return profile. Shared expectations of high risk mean that investors demand high returns to invest, requiring risk to be ‘priced correctly’ (Interview 17). In this regard, power-to-x projects are compromised in two ways. First, developers in the Danish context struggle to deliver a sufficiently high ‘risk-premium’. 3 This means that even for investors who seek upsides in high-risk, high-reward projects, power-to-x is not necessarily attractive. Second, even if projects could accommodate such risk premia, the risk-return expectations of power-to-x do not align well with the risk profiles of private equity and debt finance. Therefore, power-to-x projects lack bankability, which represents a significant barrier to the build-out of the sector. In short, financiers are not fond of ‘risk on steroids’.

The unattractive risk-return profile and the lack of bankability explain the lack of final investment decisions. From a derisking perspective, the answer appears obvious. Derisking increases the bankability of projects by changing the risk-return profile of a given project and bolstering profitability through subsidies. Using various tools, derisking transfers risk on investments from the private sector to the state, mitigating risks for financial capital. In the context of Danish power-to-x development, suggestions for derisking include subsidies that address the ‘chicken and egg problem’. For example, industry actors call for a guarantee from the Danish state to cover hydrogen grid owners’ deficits if utilization is below expectations, lowering tariffs for users of hydrogen infrastructure and over-dimensioning pipelines. In this form, derisking hedges private investments against scenarios where production is lower than stipulated while allowing developers to cash in on potential upsides. Taking alternative forms, derisking can also entail direct subsidies for capital expenditures to reduce the price gap between green and fossil molecules. But not all derisking is equal. Derisking can be specified for certain uses, subject to various conditions and some forms of derisking do not require the same degree of spending but can still help achieve bankability (see, e.g. Richstein and Neuhoff, 2022).

While derisking enables bankability and increases the prospects of final investment decisions, this approach to decarbonization also entails supporting financial capital (Gabor, 2023, 2021). Our findings add another element to this discussion. Because fossil energy firms are in a favourable position in terms of securing debt financing, derisking might not only support financial actors. Derisking might also indirectly subsidize fossil fuel companies over renewable ones and thereby increase the financial viability of hedging strategies, making the existential question of whether to transition or to retire less pertinent (Green et al., 2022: 4). Thus, to the extent that derisking enables (green) hydrogen production in the hands of fossil incumbents with clear interests in prolonging the lifespan of fossil assets, state subsidies may end up serving the purpose of legitimizing and prolonging oil and gas companies’ operations.

Although our findings point to the possibility of subsidizing fossil companies, they also highlight the importance of vertically integrated petrochemical companies in building and operating decarbonized chemical plants. In this perspective, we should hesitate to outright dispel the role of oil and gas majors in energy transitions. Instead, their expertise and resources need to be channeled to areas where they are most desirable. Such areas include not only direct air capture, as argued by Buck (2022), but also power-to-x, possibly in collaboration with renewable energy developers. Because we cannot expect integrated fossil and chemical companies to transform their business models and investment patterns on the necessary scale by themselves, they must be compelled to do so. Without disciplinary measures and state interventions that force these actors to mobilize their resources differently, power-to-x will remain a form of hedging.

Investing in power-to-x is ultimately vindicated as a crucial means of lowering emissions and by the idea of hydrogen as a multi-purpose energy carrier. However, critics warn that the aspirations of a hydrogen economy are overplayed, calling the climate benefits of enabling bankability by derisking into question. Denouncing the Swiss army knife analogy, the counter-analogy of a hydrogen ladder – as associated with and popularized by Michael Liebreich (the founder of what is now Bloomberg New Energy Finance) – has gained traction. The hydrogen ladder ranks prospective use cases of hydrogen from ‘unavoidable’ to ‘uncompetitive’, prioritizing sharply between different purposes and retaining hydrogen and hydrogen derivatives for a limited number of applications (Liebreich, 2023). This hierarchical way of approaching hydrogen and power-to-x foregrounds the material properties of hydrogen and the energy efficiency losses at each stage of the production process, which makes both fossil-based equivalents and direct electrification more economical (Liebreich, 2022). Potentially fueling risk expectations, such hierarchy-thinking adds further weight to the argument that power-to-x development serves as hedging for fossil incumbents – as a means of showcasing green transition credentials while retaining fossil-based revenue streams. If a ‘power-to-x economy’ is uncompetitive, a complete transition would not be profitable.

The hierarchical approach to power-to-x development raises further doubts about the benefits of derisking as a means of crowding in financial capital in the context of decarbonization. When guided by bankability and fueled by non-targeted derisking, power-to-x is not necessarily scaled according to climate-literate use cases. Focusing on willingness to pay and options for immediate uptake rather than deterring the lock-in of inefficient use cases jeopardizes the prospects of global net zero when building out power-to-x at the required scale while disregarding questions of energy justice. Similar to Gabor’s (2023) argument that derisking is unfit to govern decarbonization due to the lack of policies facilitating phase-out, derisking is arguably unfit to govern power-to-x insofar as it does not reprimand wasteful use. But whereas fossil fuels remain profitable also in the absence of state-sponsored derisking (although subsidies are the norm), scaling power-to-x for climate illiterate purposes is not. Broad-based, unspecified derisking thus comes with limitations not only in terms of lack of phase-out but also questions around what is phased in.

To conclude, despite political momentum, investment in green hydrogen production and power-to-x fall far behind global scenarios. Financing private-led power-to-x suffers from a lack of bankability in three domains, namely technology, regulation and the business case itself, which constrain scaling and learning. On this basis, we argue that private investors will not deliver the investments required for a transformative energy transition. To expand the lines of inquiry pursued in this paper, we see a need for further research that broadens perspectives on (the lack of) investments in power-to-x by analysing a wider set of explanatory factors than pursued in this paper. Such research could foreground the importance of narratives, discourses, ideology and practices in rendering power-to-x investable (Li, 2014).

This paper also shows that the challenges to bankability and the associated forms of risk mitigation imply that fossil fuel incumbents enjoy advantages in terms of scaling power-to-x. Changing the business case of producing both fossil fuels and their renewable-based equivalents is therefore needed if climate-literate power-to-x is to be a viable investment. To go beyond a world where the prospects of scaling power-to-x are conditioned upon bankability and investibility, however, requires actively undoing the fossil energy order and dispelling the allure of green finance. Such an alternative entails active planning and interventionist public finance in the form of a ‘Big Green State’, as suggested by Gabor (2023), to deliver the needed investments and ensure that fossil fuel incumbents put their expertise to good use. As it stands, however, the possibility remains that power-to-x developments will be too little, too late, going to the wrong places, mainly benefitting a limited set of private actors.

Footnotes

Appendix A

Overview of interviewees and their organizational affiliation.

| Type of actor | Number of interviews |

|---|---|

| Industry organizations | 2 |

| Developers | 6 |

| Goverment bodies | 5 |

| (Equity) investor | 5 |

| Consultant advising on power-to-x | 6 |

| Asset manager | 3 |

| Off-taker | 1 |

| Credit provider | 4 |

The sum of interviews does not add up to the number of interviewees as some of the interviewees have multiple roles or work at the intersection of multiple organizational affiliations (e.g. doing consultancy work as state employee).

Acknowledgements

The authors would like to thank Mattias Borg Rasmussen, Fredric Bauer, Christian Lund, Kirstine Lund and Jacob Hasselbalch for their helpful and insightful comments on previous versions of this paper. The authors would also like to extend this gratitude to the participants at the organisation, markets and governance seminar at Copenhagen Business School and the global development seminar at University of Copenhagen for their helpful comments and engaged discussions.

Author contributions

Because the two authors contributed equally to this work and share first authorship, the authorship order is alphabetical.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Joachim Peter Tilsted received funding from the Swedish Foundation for Strategic Environmental Research supported the research through the programme Mistra STEPS – Sustainable Plastics and Transition Pathways (F2019/1822).