Abstract

In this paper, we analyse the recent development of green sukuk (often referred to as an Islamic green bond) since its issuance in Malaysia in 2017, and critically evaluate whether it addresses some of the existing contradictions of green finance. Using a financial ecologies approach, we examine Malaysia's configuration of green sukuk as drawing from the existing international green bond regime, partnership with the World Bank, and Malaysia's own experience and expertise in Islamic finance, with the objective of building Kuala Lumpur's competitiveness as a global Islamic financial centre. Through documents analysis and interviews with key market actors in Kuala Lumpur and other financial centres, our findings point to the emergent international adoption of green sukuk. While this achieves Malaysia's state-building objectives, specifically through expanding Malaysia's sukuk market and advancing its status as a frontier of Islamic financial innovations, the potential for improving the current green bond regime has been more doubtful. A key limitation is the incorporation of existing Green Bond Principles, which enables not only green sukuk's international acceptance but also renders it susceptible to greenwashing. By examining the intersection of different ecologies of green and Islamic finance, we reveal the contradictions and limitations of green sukuk in contributing to Malaysian state-building and climate action.

Introduction

Over the past decade, concepts of “sustainable finance” and “green finance” have become more prominent in mainstream financial discourse, generally referring to financial instruments whose proceeds are directed at sustainable development projects and initiatives, improving environmental outcomes, and promoting green economic transformation towards low-carbon and climate-resilient pathways. Globally, green bonds have gained popularity as a financing instrument for green infrastructures such as renewable energy, green buildings and low carbon transportation, with more recent and notable growth of emerging economies in green bond markets (CBI, 2018). 1 The geographical literature has been critical of using financial mechanisms to resolve environmental and climate problems as such tools often serve as facades for financial and political benefits while making limited progress on environment and climate issues (Bracking, 2015; Sullivan, 2013). Specifically, green finance has been criticised for following highly performative rituals that do not produce environmental benefits (Bracking, 2015a; Jakonvić and Bowman, 2014). More recently, Islamic green sukuk (often interpreted as an Islamic-compliant version of green bonds) has emerged as a new financial instrument that could address some of these criticisms. Discussions of the mutual compatibility between green and Islamic finance emerged in July 2017 when a Malaysian solar photovoltaic company issued the world's first green sukuk. Partly in response to the United Nations Sustainable Development Goal and the Paris Climate Agreement, some practitioners are identifying synergies between green finance and Islamic finance in contributing to sustainability and climate goals, especially in Islamic economies (Ahmed et al., 2015; Bennett and Iqbal, 2013; Obaidullah, 2017; RFI, 2018; UNPRI, 2017; White and Case, 2016). Specifically in Malaysia, the development of green Islamic finance opens an Islamic-compliant avenue for a low carbon ‘capital switch’ (Castree and Christophers, 2015), particularly for its most carbon intensive and polluting oil and gas and agroforestry industries (Begum et al., 2015).

Islamic finance is commonly known for its prohibition of certain financial practices such as the charging of interest or industries prohibited by the religion (Pollard and Samers, 2007; Rethel, 2011). These prohibitions are fundamentally driven by an overarching objective of enhancing the general welfare and justice of society (Obaidullah, 2017; Visser, 2013). Accordingly, Islamic scholars, financial practitioners and environmental think tanks have argued that Islamic finance is inherently compatible with principles of green finance that seeks to channel investments towards purposes that bring environmental benefits (Ahmed et al., 2015; Obaidullah, 2017; RFI, 2018; UNPRI, 2017). Specifically, the principle of wasatiyyah requires maintaining the balance of mizan (the natural state of the world) – which entails the avoidance of waste, extravagance and corruption. Fasad (the promotion of disorder) is prohibited under Islamic teachings, together with unethical transactions and dealings that include interest/usury (riba), uncertainty or deceptive contracts (gharar) and gambling (maysir) (RFI, 2018). According to this framework, businesses should fulfil people's needs within the boundaries of a sustainable and efficient economic system. Financial activities that induce disorder, including environmental depletion, are thus prohibited (Obaidullah, 2017; RFI, 2018). In the face of climate change, environmental degradation and subsequent humanitarian crisis, Islamic scholars argue that the injunctions between Sharia and environmental sustainability meant Islamic finance must contribute to environmental conservation and climate action (Obaidullah, 2017). Green sukuk, with its specific structural requirements and underpinning philosophy of concurrently express economic, environmental and Islamic values, has the potential of overcoming some of the issues faced by green finance.

In this paper, we examine how green sukuk has developed in Malaysia and critically evaluate the influence of green sukuk in improving the current green bond regime with better “green” credentials or guarantee, its contribution in financing Malaysia's climate transition and its role in the country's strategic aspirations as a global Islamic financial centre. To do this, we examine the knowledge networks of finance and regulatory professionals in green and Islamic finance, existing financial infrastructure in Malaysia and the political motivation to develop green sukuk to uncover how different groups of actors, knowledge communities and political motivations come together in constructing new market knowledge and structures. Does this new conception of green finance that incorporates Islamic values address some of the existing contradictions of green finance? Or does green sukuk work primarily to fulfil state-building objectives in consolidating Malaysia's Islamic financial centre growth and enhancing regional and global influence in wider Islamic financial networks? Within the geographical literature, there has been limited analysis of green finance from a market-making perspective (Bracking, 2019). A close examination of green sukuk provides important insights into how a financial instrument is conceptualised, regulated and promoted to simultaneously express economic, environmental and religious values. We do this by examining the development of green sukuk through a financial ecologies approach (Carolan, 2019; Lai, 2016; Langley and Leyshon, 2017), which analyses financial instruments and practices as embedded in diverse forms of knowledge domains and market practices instead of a neat categorisation of conventional/alternative financial markets that typically frame studies of green bonds and climate finance. An ecologies framework offers analytical flexibility in considering complementary and conflicting objectives and motivations in the process of market construction. Our focus on the case of Malaysia also contributes to current debates regarding the state-finance nexus (Lai, 2018; Töpfer and Hall, 2018) and the role of developmentalism in financial innovation (Lai and Samers, 2017; Lai et al., 2017; Rethel, 2020).

We adopt a qualitative, interpretive methodology involving two stages. First, desk-based research focuses on analysing documents such as policy documents, non-governmental organisation (NGO) publications and corporate reports in English (which is commonly used in the business sector in Malaysia) to identify key milestones in the development of green sukuk and construct the current market landscape. Second, 23 interviews were conducted between September 2018 and September 2019 with key market actors, such as green sukuk issuers, investment bankers, regulators, capital markets lawyers, environmental consultants, institutional investors, Sharia advisors, academics (including Islamic scholars) 2 and NGOs. Fifteen of these respondents are based in Kuala Lumpur, while others are in international financial centres with significant green or Islamic finance expertise, including Dubai, London, Saudi Arabia and Singapore. Fifteen interviews were conducted face-to-face and eight via telephone/video calls. Interviews ranged from 45 to 120 min and were conducted in English. All but one of the interviews were recorded with permission and transcribed afterwards for coding and analysis, alongside extensive notes taken during those interviews.

The next section underscores the financial ecologies approach in studying the emergence and deployment of diverse market-making knowledge and practices. We review the current green bond regime and consider how the principles of Islamic finance might overcome some of the limitations of governing “greenness” identified by existing studies. The empirical analysis in sections ‘Developing green sukuk to advance an islamic finance frontier’ and ‘Green sukuk: Climate action or state-building tool?’ begins with outlining the political economic context in which Islamic green bonds developed in Malaysia. The section ‘Developing green sukuk to advance an islamic finance frontier’ identifies three processes of green sukuk development, analysing the relations between actors and the tensions arising from conflicting objectives that have determined the current market landscape. In section ‘Green sukuk: Climate action or state-building tool?’, we critically evaluate the extent to which green sukuk have effectively expressed economic, green and Islamic principles, and argue that that green sukuk may be limited in improving the ‘green’ standards of climate finance while being more successful by other measures of Islamic financial centre development. In the conclusion, we highlight the analytical value of ecologies thinking in understanding market development, as well as the practical implications of such green sukuk configuration on climate and environmental action.

Theorising ‘greenness’ as financial ecologies

Green bonds have proved to be increasingly popular as an effective instrument in raising green finance, with US$521 billion issued since 2007 (CBI, 2018). However, concerns have been raised over their ‘green’ credentials, especially how the majority of green bonds are currently governed. Green bonds are ‘self-labelled’ by the issuers, who have the discretion to voluntarily disclose information to prove the ‘greenness’ of the green bond and enable investors’ scrutiny. To date, the most widely recognised disclosure framework is the Green Bond Principles (GBP) published by the International Capital Market Association, which provides a guideline of information disclosure at every stage of the bond's term to encourage transparency and accountability in the market. However, the requirements of the GBP are vague and best practices such as obtaining external reviews or following consistent annual reporting methodology are merely ‘recommended’, meaning alignment with the GBP does not guarantee accurate, credible and consistent information disclosure. The GBP does not give external reviewers the right to revoke the ‘green’ labelling if they found the reviewed green credential to be questionable. Instead, they could only raise the issue in a ‘second party opinion’ document, separate to the bond offering circular. Moreover, external reviewers are hired by the issuer, creating a patronage relationship that could limit the likelihood of raising doubts regarding the green credentials of the bond (Bracking, 2015). Under the GBP, there is also no legal or financial liability if the proceeds from the issuance are not deployed for green purposes as advertised. While the ease of use of the GBP has meant this voluntary governance framework has doubled as a tool to promote green bonds internationally (Perkins, 2021), the above features create a weaker accountability structure for the green credential of the bond. As such, the disclosure process has been criticised to be ‘highly performative’ without necessarily guaranteeing the ‘green’ quality of the asset funded by the project (Bracking, 2015).

Some have argued that this system of market self-regulation avoids the rigidity of formal regulations, which might limit the development of a nascent product, and that investors and wider civil society would hold green bond issuers to account (Park, 2018). However, market self-regulation requires established knowledge in green finance amongst investors and civil society, as well as resources to conduct the necessary environmental due diligence process in order to screen out any ‘greenwashers’ (Bloomberg, 2019). Furthermore, investors could only be selective with a bond's environmental credentials if there are sufficiently high-quality green bonds available on the market. Bond investors tend to look for ‘investment grade’ bonds, which are at lower risk of default according to credit rating agencies. The problem arises when credit-worthy assets with weak environmental credentials could label themselves as ‘green’ due to the lenient governance system. As demand increases for green labelled products, issuers with assets that only bring marginal environmental benefits or with poor environmental track records have begun to issue green bonds. Investors with less sophisticated environmental mandates would invest in these bonds and allow green bonds with weak environmental credentials to thrive (Bowman, 2019). As a result, the classic contradiction in neoliberal environmental governance is demonstrated in green bond investing, where environmental assets must first and foremost earn their right to survive in the financial market (McAfee, 1999).

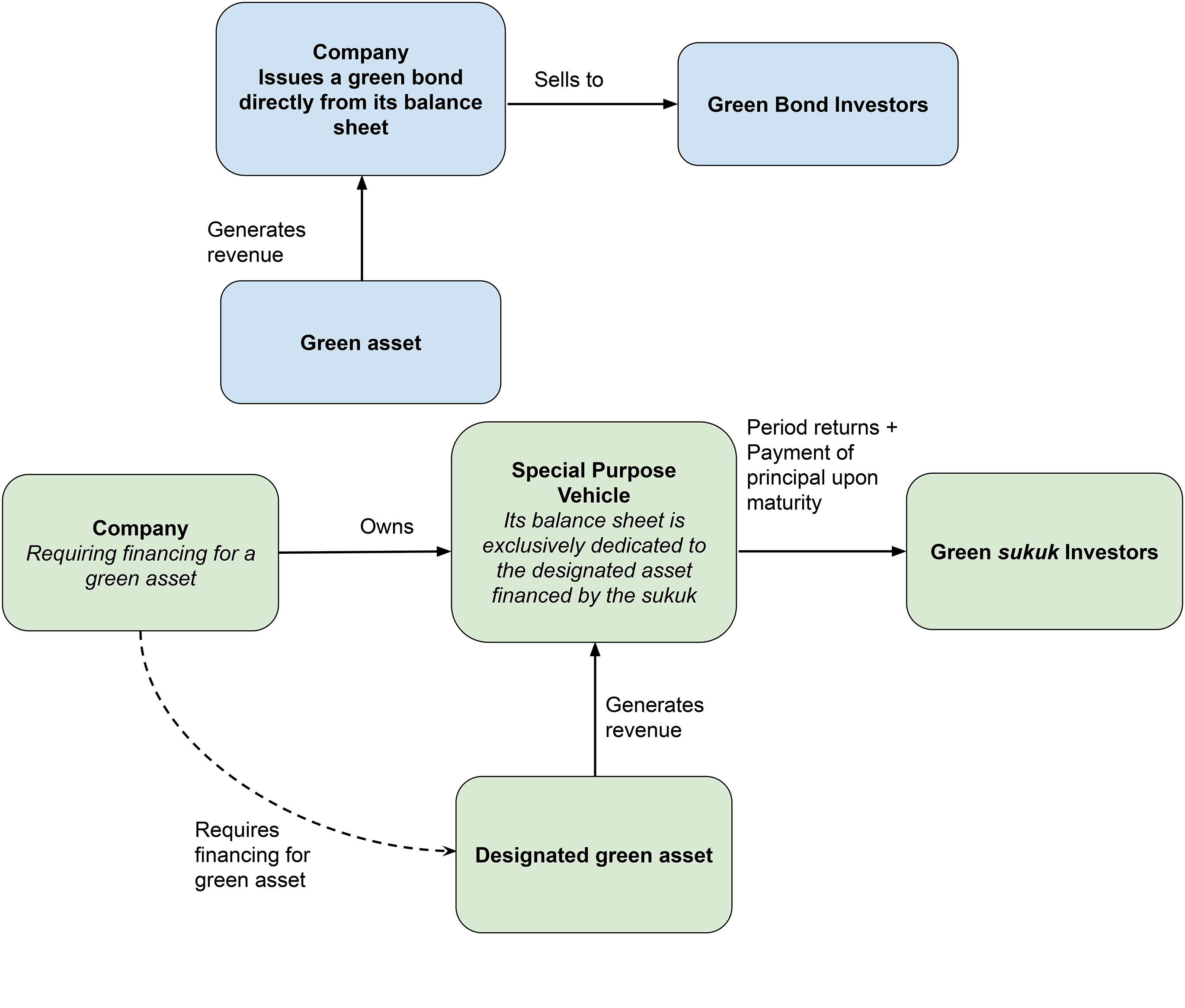

This raises the question of whether the Sharia rules governing green sukuk might address some of the limitations of the prevailing green bond regime. Sharia compliance requires funds raised through a sukuk to be dedicated to an identifiable asset, usually through a special purpose vehicle created and owned by the company that wishes to finance an asset (Figure 1). This is unlike green bonds that are usually issued from a company's balance sheet. As such, a sukuk structured to fund a specified green project is unlikely to be used for other non-green purposes, which improves legal accountability (Hussain et al., 2017). Moreover, there is potential for stricter governance of ‘greenness’ under Islamic principles. The Sharia-board, which is a committee of Islamic scholars in an Islamic bank that determines what types of transactions are Islamic-compliant (halal) and are of theological purity (tayyib), could decide on the Islamic principles that a green sukuk must fulfil. As such, Islamic principles related to the environment and sustainability (see Section 1) would be embedded into the asset rather than being merely reflecting in the structure of the sukuk. Overall, green sukuk seem to have the potential for stricter governance of ‘greenness’ and accountability framework under Islamic principles.

Comparison of ownership structures between green sukuk (indicated in the diagram below) and the ownership structure of a conventional corporate green bond (indicated in the diagram above) (developed from White and Case 2016).

In analysing the development of green sukuk and its impact on the current green bonds regime, we do not view them as competing forms of alternative green finance. Instead, we examine their roles as distinctive financial instruments, focusing on how they emerge and mobilise knowledge domains that are embedded in wider ecologies of financial markets and practices. In this approach, the financial system is not pre-defined by some conventional logic of the global circuit of capital, instead, it is framed as a coalition of smaller constitutive ecologies (Lai, 2016, Langley and Leyshon, 2017). These relational arrangements entail distinctive groupings of financial knowledge and practices, which unfold and evolve in different places with uneven connectivity and material outcomes, such that distinctive ecologies emerge and sometimes endure, or may fade in importance. Studies have made use of financial ecologies to examine socio-material practices in rural households, financial advisory and peer-to-peer lending, with particular attention to their uneven socio-spatial operations and outcomes (Carolan, 2019; Coppock, 2013; Lai, 2016). A key feature of ecologies thinking is the fuzzy boundaries between different forms of markets and knowledge domains, such that they are not framed as distinctively ‘conventional’, ‘alternative’ or ‘niche’ markets but must necessarily draw upon different domains for their functioning and legitimacy. Markets are constituted and performed through combinations of knowledge communities, institutional frameworks, political environments, social values and cultural practices. An ecologies approach helps to unpack the complex market dynamics that give rise to a variegation of market practices, whereby groups of actors with different values and motivations shape market functions and outcomes. While there is a certain resemblance to other relational concepts such as assemblage, actor network and apparatus, which all emphasise fluidity and change, we argue that an ecologies approach is more effective for considering why particular sets of relations or knowledge domains are more durable or resistant, such that ‘certain “stickiness” to relations and processes might prove more stubborn to shifting than others’ (Lai, 2016: 30). In this case, we are interested in critically examining how green sukuk might be an improvement on the current green bond regime, whether certain limitations have remained ‘sticky’, or whether its success could be viewed through the lens of other political economic goals instead.

Instead of a cohesive green bond market, we see these as smaller constitutive ecologies jostling for legitimacy and influence, even as they negotiate different motivations and objectives to achieve robust ‘green’ credentials (and what would constitute that robustness) amidst broader demands of ‘investment grade’ ratings and investor mandates. In framing green sukuk and green bonds as financial ecologies, we pay particular attention to considering different motivations, objectives and power in influencing market configurations and practices, as we analyse how green sukuk engage with the international green bond regime, and the role of Kuala Lumpur in these emerging financial networks.

Developing green sukuk to advance an Islamic finance frontier

Islamic banking and finance in Malaysia

Kuala Lumpur, the capital and financial centre of Malaysia, has been labelled as an ‘Islamic financial frontier’ for the innovative instruments and practices it champions (Poon et al., 2017). This reputation is important for understanding the financial knowledge and practices underpinning green sukuk. The development of Islamic banking and finance in Malaysia is motivated by two interconnected policy objectives. First, Islamic banking and finance is developed as a neoliberal ethnic-religious policy to promote financial inclusion and prioritisation of economic benefits for the majority Muslim Malays (termed bumiputra) 3 (Lai, 2015; Lai and Samers, 2017). Second, Islamic finance development would enable Malaysia to expand and diversify its financial sector in an Islamic-compliant manner (Poon et al., 2018; Rethel, 2018). This strategy of meeting ethnic-religious goals through the promotion of neoliberal market mechanisms has been referred to as ‘ordoliberalism’, through which Malaysia has established itself as an international Islamic financial centre (Lai and Samers, 2017). From the establishment of the country's first Islamic bank in 1983, to expanding Malaysia's influence over global Islamic finance development more recently, the state has employed classic ‘industrial policies’, such as standard setting, tax incentives, and adoption of new products by government agencies to boost the development of the sector (Lai, 2015). Notably, the Malaysian government issued the world's first sovereign sukuk and Malaysian state-owned corporates followed suit to generate publicity and build the confidence of private sector engagement (Lai, 2015). The Malaysian state has directed resources specifically to train Islamic financial professional service providers and Sharia scholars and set up Islamic banking and finance research institutes to support financial innovation and lend legitimacy to Malaysia's interpretation of Sharia law (Lai and Samers, 2017; Poon et al., 2018). The research they produced also plugged knowledge gaps for the international Islamic banking and finance community, which in turn gave Kuala Lumpur significant agenda-setting power in the sector's global development (Bassens et al., 2011). The development of Islamic financial instruments in Malaysia demonstrates how particular financial ecologies evolve and touch down in places, albeit with variegated socio-economic outcomes. For example, the concept of sukuk was initially rejected by the Middle Eastern states as interest-generating. However, the combination of Sharia expertise in Malaysian Islamic banks and proficiency in English common law of Malaysian lawyers enabled the restructuring of sukuk in the Gulf states to accommodate stricter Sharia interpretations (Poon et al., 2017). While there are established Islamic financial ecologies in the Middle East, Malaysia is able to capitalise on precisely its physical and theological distance from the Islamic centre in the Middle East to spearhead innovative Islamic financial products (Poon et al., 2017).

The emergence of green sukuk is consistent with Malaysia's strategy to expand the Islamic financial market and to be at the frontier of Islamic financial innovations. In a development plan published by the Securities Commission Malaysia (SCM) (2011), the capital market was highlighted as a platform for developing innovative environmental finance solutions. Following the plan, the Sustainable and Responsible Investment (SRI) sukuk framework (which also governs green sukuk) was launched in 2014 to expand the capital market through sustainable financing and investment (SCM, 2014). In addition to growing Malaysia's capital market and maintaining its reputation as an innovative Islamic banking and financial centre, green Islamic finance aids Malaysia's commitment to environmental sustainability, which has been outlined in various national development plans, including the 10th and 11th Malaysia plans and the New Economic Model (Economic Planning Unit, 2009, 2015). Thus, the development of green sukuk is SCM's response to ‘growing concerns over environmental and social impact of business and greater demand for stronger governance and ethics from businesses’ (SCM, 2014) within its mandate of advancing Malaysia's capital market, particularly since ‘Islamic finance has natural synergy with responsible investment. It's a solution to deal with issues such as the environment, climate and green [finance]’ (Interview with regulator, January 2019).

Regarding the design and promotion of green sukuk, there are two points of tension. First, the structural limitations regarding eligibility and liability in the green bond market that leads to greenwashing need to be addressed in any new configurations of the instrument, lest the problem is perpetuated. Second, Malaysia has the ambition to spearhead innovative Islamic banking and finance products, and it has succeeded in the past by deploying an array of state actors and leveraging upon the relationship between the state and the private sector. In order to develop a first mover advantage in green Islamic finance, Malaysia will have to fill the gap in knowledge and expertise in green finance, either by training local expertise or seeking external advice and legitimacy. To sustain its position as a global Islamic financial centre, Malaysia must also export green sukuk abroad, which means the design of green sukuk needs to be comprehensible and acceptable to an international audience (Rethel, 2011). Furthermore, some interviewees point out that green sukuk creates an opportunity for Islamic investors to participate in the green bond market for the first time. These investors consist of institutions that serve the bumiputra, including Islamic pension funds, banks and insurance companies. The development of green sukuk thus appears to be the latest avenue of development under ‘ordoliberalism’ that has underpinned the development of Islamic banking and finance in Malaysia (Lai and Samers, 2017): in meeting national economic and environmental objectives, the financial interest and inclusivity of the Bumiputra population must also be ensured.

Promoting green sukuk

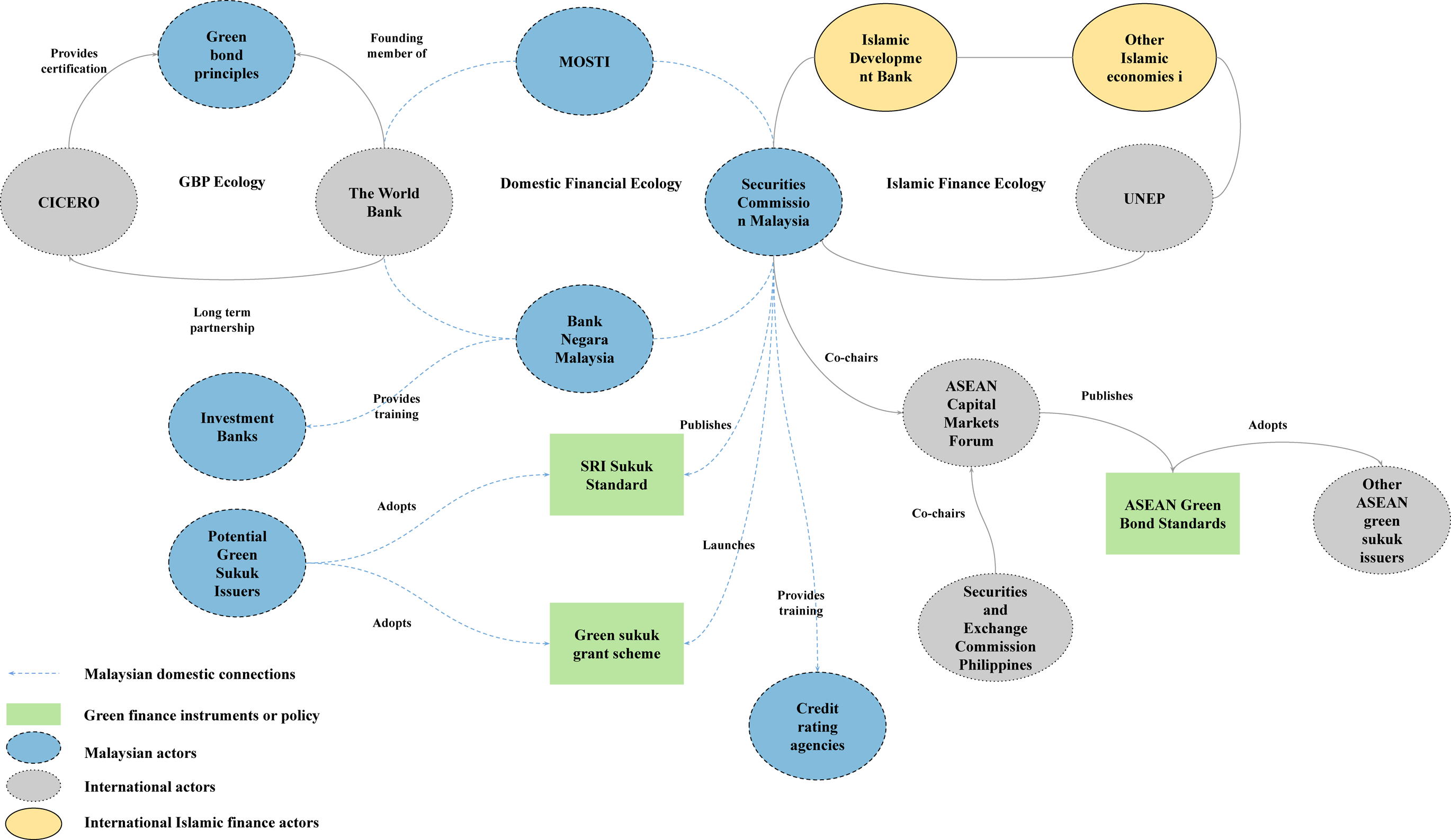

The development of green sukuk is meant to concurrently achieve economic, political and environmental objectives. We identify three processes led by the SCM to attain these goals, namely green sukuk standard setting, multi-agency promotion and growing international influence. Figure 2 depicts the ecologies of international and domestic actors contributing Islamic and green finance knowledge and expertise in these three processes.

The financial ecologies of green sukuk (source: The authors).

Green sukuk standard setting

Reporting standards is one of the ways to calculate and communicate the multitude of concerns and values in a market (Butler, 2010; Callon, 2009). They play an important role in market formation as they legitimise certain sets of practices that allow for particular values, especially non-financial, moral or ethical values, to be expressed and appraised, thus enabling the functioning of the market (Barman, 2015). In the current international green bond regime, for instance, reporting standards and practices are synonymous with governance as the environmental credentials of green bonds are solely reliant on voluntary disclosure (Perkins, 2021).

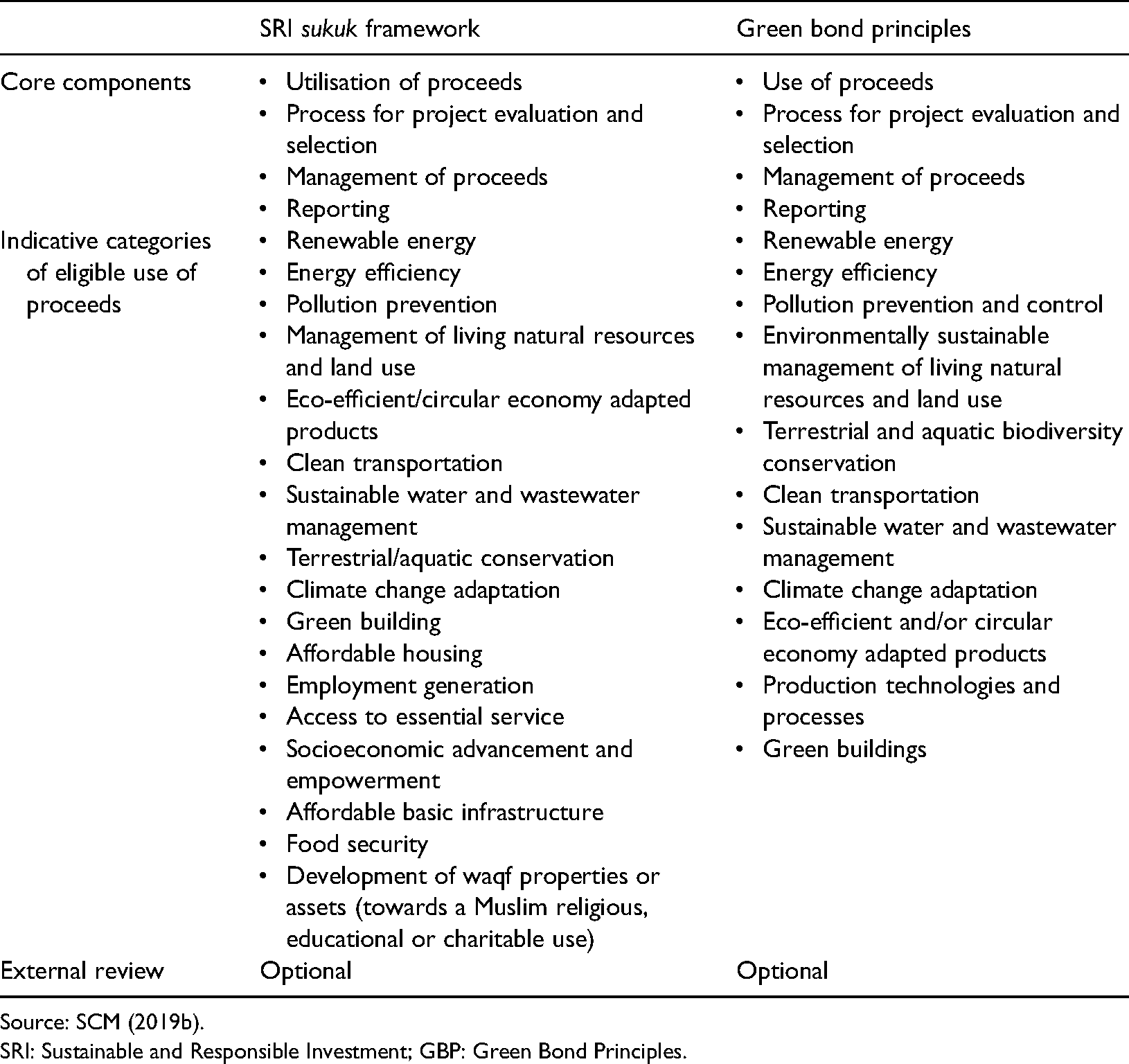

The SRI sukuk framework published by the SCM in July 2014 was the world's first set of standards codifying the requirements for a financial product to concurrently meet the requirements of social and environmental sustainability and Islamic values. This establishes green sukuk as a unique asset class and signifies ‘the beginning of green financing in Malaysia’ (Interview with investment bank, March 2019). However, green sukuk as a financial instrument did not debut until 2017, after a partnership with the World Bank was established to promote green sukuk (see Figure 2). The World Bank played a significant role in terms of standard setting by ‘identif[ying] complementarity between Malaysia's SRI sukuk guidelines and GBP to enable potential issuers to issue green sukuk in the absence of national green bond guidelines’ and ‘provid[ing] guidance on eligible green projects’ (World Bank, 2017: 2). A comparison of the original and current SRI sukuk framework reveals that the list of eligible projects (e.g. natural resources, renewable energy and energy efficiency, community and economic development) have evolved from being compatible with the GBP to being identical to the GBP indicative categories of eligible environmental projects, in addition to eligible social projects that included Islamic charitable projects (ICMA, 2018; SCM, 2014, 2019a) (see Table 1). Likewise, the qualifying procedures of information disclosure and external review come to resemble the recommendations provided by the GBP (ICMA, 2018; SCM, 2014, 2019a).

A comparison between the SRI framework and the GBP.

Source: SCM (2019b).

SRI: Sustainable and Responsible Investment; GBP: Green Bond Principles.

By framing green bonds and green sukuk as financial ecologies, we place particular emphasis on constitutive clusters or coalitions of market practices, the various actors and motivations in pursuing strategic goals, and how they matter in nuanced configurations of power and political economic outcomes. Here, the alignment of the SRI sukuk framework with the GBP follows from the institutional decision-making of the SCM. To achieve its state-building objectives, the Malaysian regulator took pragmatic steps towards wider adoption and recognition of green sukuk, while tapping upon existing networks and resources in order to achieve those goals. The choice of partnering with the World Bank, instead of other actors in the international green bond regime, is shaped by the long-standing influence of the World Bank in Malaysia since its independence in 1958 4 . As one of the earliest green bond issuers, the World Bank has played a significant role in devising the GBP (Monk and Perkins, 2020) and is an attractive resource of green finance knowledge and experience for Malaysian regulators. This points to the significance of ‘stickiness’ to particular practices (GBP) and relationships (the World Bank in Malaysia) in analysing the development of a new financial instrument like green sukuk (Lai, 2016). Even though green sukuk appears to have the potential for introducing an improved framework for green bonds, some relationships and knowledge domains endure and work themselves into the new reporting standard.

User-friendliness was another important consideration for Malaysian regulators. Following similar procedures and language as non-Islamic counterparts based on the GBP (see Table 1) lowers the cost of operation while increasing the perceived legitimacy of green sukuk. This is vital if green sukuk is to eventually engage an international audience. As such, it was deemed necessary to design the green sukuk framework in line with international practice, rather than developing a green Islamic finance framework from scratch. One might view this alignment with the GBP as conceding to a flawed system instead of creating a more effective framework with Islamic principles of environmental conservation that would better guarantee the environmental credentials of the product. However, such a judgement forecloses an analysis of the heterogeneous drivers of developing green finance, how ecologies of different market knowledge and practices emerge and evolve, and the multiplicity and variegation of financial forms that make up the broader financial system.

This melding of financial ecologies has been observed in other studies (Bassens et al., 2013; Lai and Samers, 2017) in tracing the development of Islamic banking and financial products and their acceptance by international, non-Muslim actors, which is crucial to meeting the objective of securitisation – that is, to generate more capital. Similarly, the alignment of green sukuk with GBP facilitates their adoption by international investors who might be interested in diversifying their green bond portfolio. Indeed, as previously mentioned, playing the role of bridging international conventional financial products with Islamic values to facilitate trading between the two markets is crucial to Malaysia's role as a leading Islamic banking and finance centre (Poon et al., 2017).

Multi-agency promotional effort

The publication of the SRI sukuk standards provided the groundwork for a multi-pronged promotional campaign by Malaysian regulators. Alongside financial incentives (such as tax deduction of the issuance fee and a RM 6 million grant [roughly US$ 1.5 million] to reimburse cost of external verification), the SCM formed partnerships with BNM and the Ministry of Energy, Science, Technology, Environment and Climate Change (MOSTI) to promote green sukuk, drawing upon the knowledge and connections of different partners (see Figure 2, blue-coloured, dashed oval connections). The SCM is privy to deals that are about to enter the capital market and would approach sukuk issuers whose projects are eligible under the SRI standard. An investment bank interviewee disclosed that regulators have exerted pressure informally on financial institutions to ensure that their clients are engaging in green sukuk whenever possible: SCM, they even have a dedicated team, a special unit to actually work on the ESG [environmental, social and governance] financing. And these are the units that have been actively looking into market participation, not just the banks, they also talk to investors, and also to potential issuers… For example, if we are the arranger and we are the advisor for that financing and we did not do it under green financing when it is actually qualified, they will come and say why will you not advise your client to do this [green finance]? (Interview, March 2019)

As more local companies issued green sukuk, SCM also reached out to local credit rating agencies to initiate collaboration and provide training on providing green finance rating and second party assessment (Interviews with regulator and credit rating agencies, January and April 2019). Likewise, BNM leveraged upon its relationship with Malaysian banks to organise training on the specificities of arranging and managing green sukuk. These training sessions were organised by SCM and BNM but led by the World Bank, as part of its role to ‘share international experience of green bond issuance’ (World Bank, 2017; Interview with regulator, January 2019; see Figure 2, connections labelled ‘GBP Ecology’ on the far left). The World Bank's involvement in promoting green sukuk brought about a further partnership between early green sukuk issuers and the Centre for International Climate and Environmental Research (CICERO) – a Norwegian environmental NGO that has collaborated with the World Bank on green finance since it provided the external review for the latter's first green bond in 2009. CICERO provided external verification for the first three green sukuk issuances. These partnerships demonstrate the dynamic and variegated nature of financial ecologies in green bonds markets. While the adoption of international practice of green bond issuance beyond standard-setting appears to reinforce existing ‘performative’ practice of information disclosure and external review (Bracking, 2015), the prominent role and strategic action of the Malaysian state in promoting green Islamic finance has been crucial in enabling those forms of development and policy outcomes.

Increasing scales of influence

Malaysia's ambition in promoting green sukuk extends beyond the domestic market. Together with the Securities and Exchange Commission of the Philippines, SCM co-chaired the Association of Southeast Asian Nations (ASEAN) Capital Markets Forum in 2017 and took a leadership role in designing the ASEAN Green Bond Standards (see Figure 2, connections on the bottom right). This new standard serves similar purposes as the domestic SRI sukuk framework of legitimising the asset class and consensus-building on the scale of the regional trade bloc. Upon the standard's establishment in 2018, PNB Merdeka Ventures, a Malaysian government-linked company, took the lead in issuing a 2 billion Ringgit ASEAN green sukuk to fund a green building. The issuance resembles the historic strategy of state-owned corporations issuing the first sukuk with the view of promoting the asset class (Lai, 2015). SCM's efforts to internationalise green sukuk has seen early signs of fruition with the Indonesian government issuing the first sovereign green sukuk that complies with the framework in February 2019. This recognition by Indonesia, a neighbouring Muslim-majority country with significant Islamic financial market potential, sends a strong signal regarding the acceptance of green sukuk as an appropriate asset class in achieving Islamic finance and in environmental sustainability goals (Jakarta Post, 2019).

Efforts to promote green Islamic finance also extend beyond ASEAN. In September 2018, SCM entered into a partnership with United Nations Development Programme and the Islamic Development Bank based in Saudi Arabia to promote green Islamic finance in Muslim-majority countries (see Figure 2, connections labelled ‘Islamic finance ecology’ on the top right). The SCM brings into this partnership its valuable experience of regulating and promoting green sukuk. Beyond facilitating international adoption of Malaysia's green sukuk framework, this partnership carries deeper significance for Malaysia's international standing as an Islamic financial centre. In contrast with earlier contestation between Malaysia and the Gulf states over the development of sukuk (Poon et al., 2017), actors in the Gulf state have generally been supportive of aligning Islamic finance with green finance and the concept of green sukuk (Interview with multilateral development bank, March 2019; Interview with Islamic scholar, April 2019; Obaidullah, 2017). Having the Islamic Development Bank in Saudi Arabia as one of the partners increases the theological legitimacy of green sukuk, as Saudi Arabia is often perceived as having the most stringent reading of Islamic laws. There have been disagreements in the past between Malaysia and the Middle East over whether certain products or financial transactions are Islamic-compliant (Bassens et al., 2013). However, in this case, Gulf State actors endorsed the issuance of green sukuk for climate and sustainability purposes, as explained by an Islamic finance scholar from the Middle East: ‘climate finance, climate protection, green financing, all these are part of that specific lineage component of Maqāṣid al-Sharī’ah [Islamic legal doctrine]. So I would say that it is an inbuilt feature of Islamic finance’ (Interview with multilateral development bank, March 2019).

However, while there have been discussions in both Malaysia and the Gulf States regarding the alignment of green and Islamic financial principles, the compatibility between socially and environmentally responsible financing and Islamic principles have not been formally interpreted or codified by Sharia councils. As green finance is an evolving concept (Berrou et al., 2019; Bridge et al., 2020), 5 having a broad interpretation of the alignment between Islamic and green finance enables a greater degree of flexibility in future developments. An interviewee from the Middle East further conceded that there is limited knowledge in green finance amongst Islamic financial actors internationally to create detailed green Islamic finance guidelines or standards.

Figure 2 shows the coalition of knowledge pathways and relationships that Malaysia has pulled together from the World Bank, as well as Malaysian and Middle Eastern Sharia expertise. While Malaysian authorities have deployed a range of formal policies and informal pressure (outlined in blue) in developing green sukuk, these have also strategically drawn upon wider ecologies (outlined in grey), which have all contributed to the legitimacy and growing influence of its green sukuk framework. Notably, the engagement with the World Bank and its collaborators, who were key proponents of the GBP, reconciles the lack of specialist green finance knowledge and expertise in Malaysia. At the same time, the adoption of the GBP model maximises the strategic attractiveness of green sukuk by retaining an internationally familiar model. The engagement with Middle Eastern Islamic expertise (see Figure 2, outlined in yellow) is particularly important for instilling confidence in other Islamic financial markets regarding the legitimacy and desirability of green sukuk and increase willingness to develop and invest in Malaysia's particular configuration of green Islamic finance.

The financial sector in Malaysia also benefits from providing financial services to other Islamic markets as they embark on developing green finance. As a pioneer, advanced business services in Malaysia have unmatched knowledge and experience in green Islamic finance. A Kuala Lumpur-based researcher of Islamic finance highlights the opportunity for Malaysia to play a pivotal role in green Islamic finance service internationally by providing talent and expertise support to market developments abroad (Interview with think tank, April 2019). Another interviewee based in the Middle East concurs that: ‘In Malaysia the resources are there, the Sharia scholars, the finance people, everything is there’. (Interview with multilateral development bank, March 2019). Financial geography research has established the importance of advanced business services (such as law and accounting) to market formation and financial centre capacity (Faulconbridge, 2019; Wójcik, 2013). The growing concentration of Islamic banking and financial expertise, and the emergence of green Islamic finance continues to foster Malaysia's reputation as an Islamic financial centre: the more recognition Malaysia receives, the more demand there is for its Islamic financial services and thereby contributes to its growing reputation as an innovative Islamic finance frontier.

Green sukuk: Climate action or state-building tool?

Green sukuk has achieved important economic, and regional and international policy goals for Malaysia. When examined within broader ecologies of green finance, however, its potential in addressing the limitations of the GBP framework in delivering meaningful climate and environmental action is less certain. How has it performed as a financial instrument that simultaneously reflects economic, environmental and Islamic values?

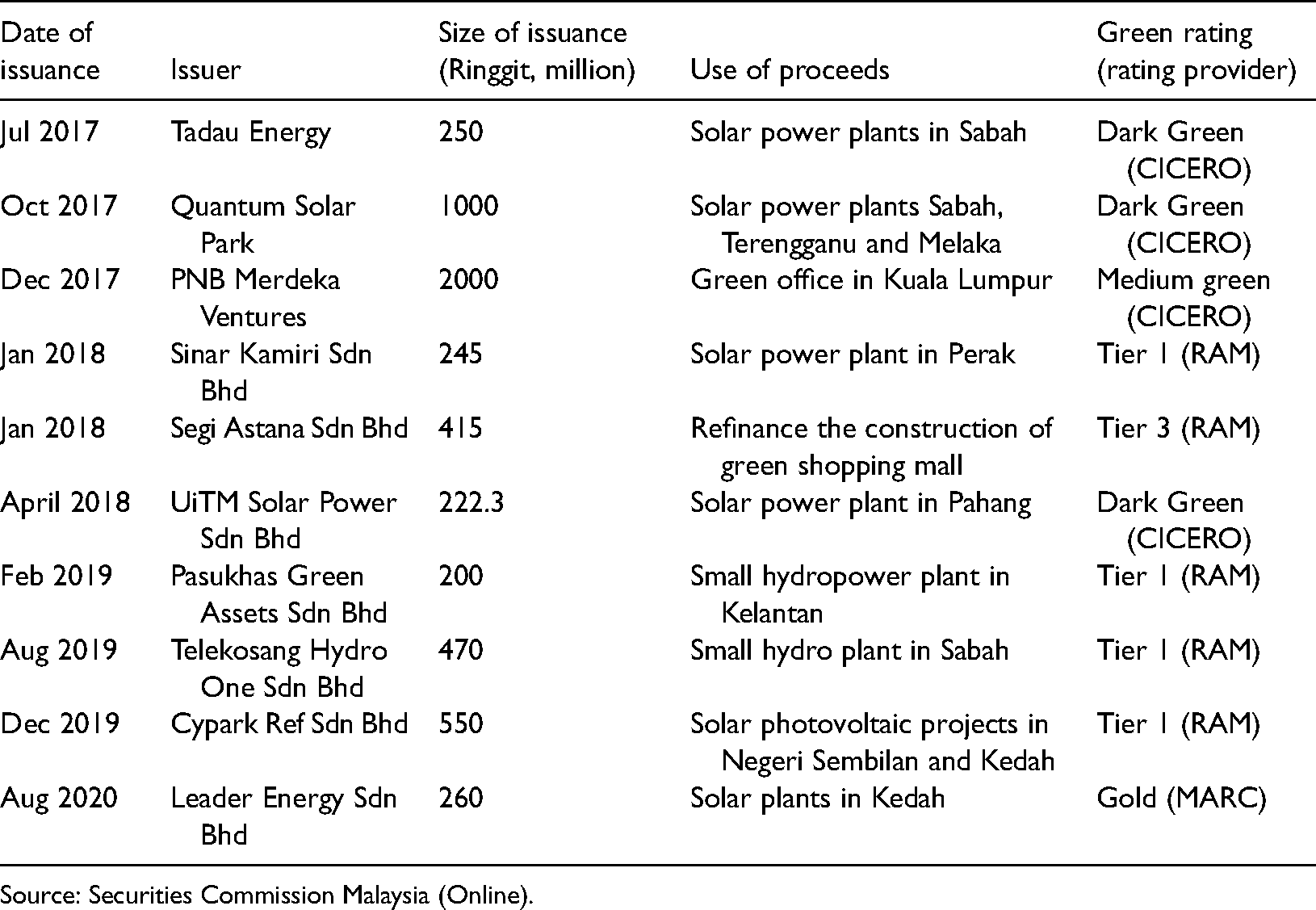

The private sector has responded to the green sukuk with reasonable enthusiasm. As of December, 10 green sukuk have been issued under the SRI sukuk framework in Malaysia, totalling 5.8 billion Ringgit (∼US$1.4 billion). Of the 10 issuers, nine are privately owned companies and one is a state-owned company (Table 2). All green sukuk issued are denominated in Ringgit with the proceeds deployed domestically. In addition to making promising progress in the number of issuances and diversity of assets funded, there is also evidence of capacity-building domestically in green Islamic finance. Notably, the two most prominent domestic credit rating agencies have independently published their own sustainable finance accreditation criteria. When the fourth green sukuk was issued in January 2018, it was verified by one of these local agencies, which points to a growing demand for green financial services as rating agencies would not have invested resources into designing such criteria otherwise. This also signifies that the partnership with the World Bank in disseminating capacity and knowledge in green finance has embedded international green bond practice by professionalising these services in Malaysia. Overall, these point to robust domestic demand and effectiveness of the SCM-led partnership, and the development of green sukuk has seen early successes in expanding and diversifying the domestic Islamic financial market.

Green sukuk issued in Malaysia, issuance sizes, use of proceeds and environmental qualifications.

On the environmental front, however, the extent to which green sukuk effectively reflects ‘green’ values remains questionable. As discussed in Section 3, the blending of the new green sukuk framework with the existing GBP governance structure has helped to legitimise green sukuk and increased its international appeal. However, this also results in similar limitations in materialising environmental benefits. As shown in Table 2, two out of the 10 green sukuk have failed to obtain the highest level of environmental certification, with one of them only achieving a ‘Tier 3’ rating. According to the external verifier that gave this rating, it means the project ‘has minimal contribution towards a low carbon future and has minimal demonstrable environmental benefits’ (RAM, 2017: 2). The three-tiered rating system published by two Malaysian credit rating agencies (RAM and MARC; see Table 2) closely resembles that of CICERO's three-tier rating system. The highest rating is allocated to projects that contribute to a long-term vision of low-carbon and climate resilient futures, middle rating allocation represent projects that are ‘not quite there yet’, and the lowest rating representing climate-friendly projects that lack a long term vision (CICERO Online: 2). This, again, reflects the tendency of ‘borrow off the shelf’ in plugging a knowledge gap and in ensuring the ease of use in Malaysia's green sukuk development.

According to interviewees, all green sukuk have been oversubscribed regardless of their green ratings, suggesting that the green credentials of a sukuk are not a crucial factor for their investors. Two interviewees recalled that environmental credentials were not a decisive factor for green sukuk holders in making an investment decision (Interview with law firm, March 2019 and Investment Bank, March 2019). This indifference is attributed to the high demand for good quality sukuk and a lack of awareness of green finance: As long as they [investors] see sukuk, it doesn't matter whether they are green or not green, they will come in. If they like the name, if they like the tenor, if they like the credit rating, if they like the pricing, they will just come in. (Interview with investment bank, April 2019)

This observation of investor indifference in the ‘green’ credential of sukuk resembles a similar phenomenon in the mainstream green bond market. In a market where greenwashing is not penalised by investors, the prospects of green sukuk in bringing about positive environmental outcomes remains limited unless investors demand better green performance. Nonetheless, as indicated by interviewees, sukuk are in high demand due to the limited product offerings for Islamic investors, whether they are ‘green’ or not.

In terms of whether green sukuk effectively reflects Islamic values, the existing alignment between green and Islamic values remain on the level of principle rather than practice. The eligibility criteria of the SRI sukuk framework covers both social and environmental assets, which aligns with the objective of Islamic finance to enhance social well-being and justice, but there is no further theological explanation specifying Islamic principles that are related to environmental sustainability (Obaidullah, 2017; RFI, 2018). Thus, strictly speaking, the ownership structure of a sukuk – that is, the financial instrument – has been officially approved by Sharia councils in Malaysia and the Gulf State as Islamic compliant, but Sharia councils have not codified or instructed how green values may reflect Islamic compliance (halal) or theological purity (tayyib). This, however, has not affected the internationalisation of green sukuk as a Malaysian innovative export, with green sukuk being adopted and acknowledged by Islamic economies regionally and internationally, including the Gulf States. This seemingly contradictory situation demonstrates how certain motivations or strategic objectives may prevail or override other concerns in emergent market practices through the configuration of existing financial ecologies.

In sum, the development of green sukuk has advanced Malaysia's domestic Islamic financial market and enhanced Kuala Lumpur's reputation as an innovative Islamic banking and financial centre. Driven by a prioritisation of ease of use and international acceptance, the structure of green sukuk has combined the existing GBP framework and Malaysian sukuk practice. Owing to a lenient governance framework and a lack of investor interest in green finance, the environmental credentials of the green sukuk issue so far remain inconsistent, rather like their GBP-governed counterpart. On the other hand, the oversubscription of green sukuk and strong domestic demand point to the success in meeting other strategic political economic goals. The development of green sukuk has strengthened Kuala Lumpur position as a centre of Islamic finance and innovation as well enabled the state to fulfil its bumiputra mandate of improving the economic well-being and financial inclusivity of the Malay Muslim population. From this perspective, the development of green sukuk as an ordoliberal state-building exercise for Malaysia has shown notable success.

Conclusion

Through a financial ecologies approach, this article has explored how evolving relations between distinctive groups of market actors with unique knowledge and motivations have constituted the current green sukuk market landscape in Malaysia. The Malaysian capital market regulators introduced green sukuk as a financial instrument that seeks to concurrently deliver national political-economic objectives, as well as environmental and Islamic values. The process began with the capital markets regulator publishing a framework that is compatible with both Islamic requirements and green bond international standards with expertise advice from the World Bank. Subsequently, this partnership supported a multi-pronged promotional effort including incentive provision, formal training and informal pressure on private sector actors. These strategies of developing green sukuk to fulfil multiple policy objectives resemble the strategies Malaysia has historically deployed to develop Islamic banking and finance. Green sukuk diversifies and expands Malaysia's existing sukuk market and presents a capital-raising instrument to support Malaysia's ambition for sustainable economic development. Importantly, the instrument is Islamic-compliant, which includes bumiputra investors in the green fixed-income market who are otherwise excluded from green bond investing. Finally, by codifying and championing green sukuk in Asian and other Islamic markets through ASEAN and United Nations Development Programme partnership, Malaysia has opened up an avenue for Islamic financial players to partake in the global trend of green bonds, which in turn reinforces its reputation as an innovative Islamic financial centre (Poon et al., 2017). Green sukuk has been hailed as ‘innovative’ in the sense that it is nominally the first financial instrument in the world that takes into consideration economic, Islamic and environmental values. By this virtue, Malaysia has benefited economically and politically from spearheading this product both at home and abroad. Indeed, these development outcomes signify that the promotion of green sukuk is a continuation of Malaysia's nation-building exercise, which underpinned the development of the broader Islamic banking and financial markets.

The current configuration of green sukuk is shaped by the availability of knowledge and expertise within existing networks of green and Islamic finance, drawn upon by Malaysian regulators. Importantly, the combination of the World Bank's contribution (with particular expertise in green finance and historical presence in Malaysia) and Malaysia's ambition of internationalising green sukuk has shaped Malaysia's green sukuk framework such that it closely resembles the internationally adopted GBP. This departs from the aspiration of incorporating Islamic principles to a greater degree in determining the eligibility of assets funded by green sukuk, as some Islamic finance practitioners and scholars have envisioned. While alignment with the GBP has enhanced the acceptance by investors in interpreting the information disclosed by issuers, the green sukuk framework has failed to address existing problems of greenwashing faced by green bonds governed under the GBP. This is a missed opportunity for Malaysia to take advantage of its Islamic financial expertise to bring about more meaningful change to the carbon-intensive and polluting sectors and its economy, even though the creation of green sukuk has achieved other strategic goals in terms of financial centre development and international recognition.

In critically evaluating existing capitalist solutions to environmental conservation and climate change (Castree and Christophers, 2015), the findings in this paper expand current understanding of green finance through the coalescence of different financial ecologies, while contributing to continued scepticism of financial solutions to problems of climate change and environmental degradation. Our analysis also highlights the theoretical relevance of the financial ecologies framework in explaining the development of novel markets seeking to incorporate multiple values, such as green Islamic finance. It is particularly useful for analysing how certain market practices or financial instruments, such as green finance, materialise into different configurations as they touch down in different places and interact with underlying political objectives, knowledge networks and market practices. An ecologies framework offers the analytical flexibility to appreciate the impact of relations of different nature, such as tensions and complementarity, as well as embedded and ‘sticky’ practices, in hindering or enhancing the achievement of different market values and outcomes. While this article has focused on the emergence of green sukuk in Malaysia and its early outcomes, future research on other emergent financial frameworks and practices (such as the growing green bonds market in China and its evolving green finance taxonomies) could illuminate how and why particular configurations dominate or fade away as different ecologies interact and jostle for attention and legitimacy. This would provide a more finely grained and multi-scalar analysis in examining how regulators, supranational organisations and private sectors are dealing with environmental needs, political objectives and market practices, and their potential to achieve meaningful climate and environmental goals.

Footnotes

Acknowledgements

We would like to thank the 23 informants who have generously spared their time and shared their insights. An earlier version of this paper was presented at the Centre for Urban and Regional Development (CURDS), Newcastle University. We would like to thank participants for their helpful comments. We are also grateful to the anonymous reviewers for their insightful suggestions in improving this paper. All claims and omissions remain our responsibility.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the King’s College London Centre of Doctoral Studies (“King’s College London-National University of Singapore Joint-PhD Studentship”, supported by the King's College London Centre of Doctoral Studies).