Abstract

While immigrant entrepreneurs contribute to economies by creating employment opportunities and innovative ventures, they often represent a marginalised group facing greater challenges in access to entrepreneurial finance. Crowdfunding may help remedy some of this challenge through more democratic access to finance and investment opportunities. This study examines the effects of the presence of immigrants in entrepreneurial teams on equity crowdfunding campaigns’ success and on the ventures’ survival. To answer these questions, we build on risk-attitude, cognitive resource diversity, and social capital theories. Our analysis uses data about UK-based firms behind 1,171 equity crowdfunding offerings on three platforms (Crowdcube, Seeders and SynicateRoom). The results suggest a relation following an inverted U-shape between the share of immigrants in entrepreneurial teams and both the amount raised and number of investors. Furthermore, the campaign’s goal sum mediates these associations. Interestingly, the higher the share of immigrants among entrepreneurial team members, the lower the likelihood of an equity crowdfunded venture’s long-term survival. However, such effects may be overturned when fundraising by majority immigrant teams involve relatively high sums, while avoiding undercapitalisation.

Introduction

Immigrant entrepreneurs identify, create and exploit economic opportunities for starting new ventures in their country of destination (Dheer, 2018). Regardless of whether driven by necessity or ambition (Abada et al., 2013; Chrysostome, 2010; Clark and Drinkwater, 2000), such entrepreneurs are often seen as offering benefits to the economies in which they operate. These include the creation of employment opportunities for both immigrants and native-born individuals (Fairlie and Lofstrom, 2015; Hammarstedt and Miao, 2020; Jones et al., 2018), as well as contribution to innovation and growth through the introduction of novel business ideas and technologies (Abd Hamid et al., 2023; Hunt and Gauthier-Loiselle, 2010; Kerr and Lincoln, 2010). Despite these contributions, immigrant entrepreneurs also often represent a marginalised group facing greater challenges in accessing finance to fund their ventures. They are less likely to access loans (Bewaji et al., 2015; Lee and Black, 2017), either being denied credit or offered smaller amounts than native-born entrepreneurs (Bruder et al., 2011). Hence, they tend to resort to more informal sources (Kushnirovich and Heilbrunn, 2008), while focusing on bootstrapping (Moghaddam et al., 2017), and support from family and friends (Hulten and Ahmed, 2013). A literature review (Malki et al., 2022) identified five key barriers for immigrant entrepreneurs access to finance including: low social integration into communities, low economic integration of their businesses into local markets, lack of government support, demographic discrimination in formal financial markets and growing information asymmetry and distrust of financial institutions (Fraser, 2009; Hulten and Ahmed, 2013) that result from these barriers with respect to existing funding opportunities.

In this context, the emergence of crowdfunding as an important alternative channel for entrepreneurial fundraising, presents new possibilities for a more democratic, transparent and levelled playing field that has the potential to help overcome the exclusive control, biases and opaqueness of financing by traditional channels, as well as enlarging the circle of potential backers (Shneor and Torjesen, 2020). Specifically, crowdfunding was viewed to more broadly present opportunities for reducing social inequalities and overcoming some patterns of discrimination (Greenberg, 2019). As such, it holds potential in aiding immigrants’ engagement in what has been labelled as ‘transitional entrepreneurship’, allowing resourcefully marginalised individuals to pursue new venturing as a vehicle for positional advancement (Pidduck and Clark, 2021). While research at the intersection of immigrant entrepreneurship and crowdfunding remains limited, some interesting insights have been documented. Some found that immigrant entrepreneurs were able to overcome their ‘liability of outsidership’ when running reward crowdfunding campaigns, while raising similar amounts to those of native-born entrepreneurs thanks to greater support from international backers and the build-up of social capital throughout the campaign (Butticè and Useche, 2022).

A case analysis of an immigrant entrepreneur’s reward crowdfunding campaign however, has highlighted the critical role played by family social capital in mobilising support from social networks in both host and origin countries (Arshad and Berndt, 2023). However, immigrant entrepreneurs with limited knowledge about crowdfunding were also more hesitant in using it due to the fear of failing to reach their goals (Bernardino et al., 2022). Regardless, this research often compared immigrant entrepreneurs to native entrepreneurs but has ignored the potentialities underlying mixed teams of immigrant and native entrepreneurs, and their prospective effects on entrepreneurial fundraising efforts. Hence, it remains unclear whether mixed teams are better or worse at unlocking resources from the crowd. Such understanding may have profound implications for both practice and policy towards entrepreneurial team build-up and presentation. Moreover, earlier studies were conducted in the context of the non-investment model of reward crowdfunding, but not in investment models such as equity crowdfunding (hereafter ‘ECF’). In reward crowdfunding, backers exchange financial support for products, services or tokens of appreciation, while, in ECF, investors exchange financial contributions for ownership stakes in the fundraising venture. Accordingly, ECF involves more rigid qualification procedures for both fundraiser and investors, substantially higher amounts being raised and a longer-term binding relationship with backers as owners rather than consumers (Shneor, 2020).

Overall, ECF attracts both unaccredited and accredited investors, as well as a growing number of more professional angel investors and venture capital funds (Wang et al., 2019). It has experienced strong growth in recent years, with some research showing indications of growing sophistication among both investors and fundraisers (Lukkarinen et al., 2022). Nevertheless, the growth still presents mixed evidence of successes and failures, as it gradually achieves wider appeal and legitimacy, parallel to growing legal clarity (Schwienbacher, 2019). As such, ECF platforms seek to strike a delicate balance between financial professionalism and democratic idealism, with the latter drawing on views of ECF as a tool for reducing inequalities and improving financial access to a wider set of entrepreneurs (Lukkarinen et al., 2022), immigrants included. From an entrepreneur’s perspective, ECF represents opportunities to fundraise relatively quickly while retaining greater shares of equity and autonomy (Brown et al., 2017), as well as enhancing own commercial competencies and network connections (Meghouar et al., 2023).

The current study aims to address this gap by exploring the implications of using ECF by immigrant entrepreneurs. More specifically, we seek to examine: (1) whether the share of immigrants among an entrepreneurial founding team members is associated with the results of a venture’s ECF campaign? (2) as well as with its long-term survival? Here, we draw on three theories: risk attitude (Weber, 2010), cognitive resource diversity theory (Horwitz, 2005) and social capital (Bhandari and Yasunobu, 2009). Risk attitude is used to explain implications of the risk preferences of immigrants. Cognitive resource diversity explains implications of different degrees of team diversity, as captured by the share of immigrants in the team, and social capital explains the implications of tapping into different magnitudes of social networks. More specifically, arguments are made that immigrant entrepreneurs are more risk-averse than others, and that more diversified teams (i.e. those including a balanced mix of immigrants and non-immigrants) are more likely to succeed due to access to complimentary cognitive resources driving greater creativity and problem-solving capacities, as well as access to broader social networks driving wider reach of campaign messages. Put differently, both cognitive resource diversity and social capital are assumed to influence risk attitudes and hence, have implications for ECF campaign management choices.

To answer these questions, we use multiple regression analyses employing data about UK-based firms that were behind 1171 ECF offerings on three platforms (Crowdcube, Seeders and SynicateRoom) between 2011 and 2018. This unique database combines campaign data from platforms with data about team member citizenship and firm survival status from the national UK company registry. As such, we answer growing calls for the use of data from multiple platforms in crowdfunding research (Dushnitsky and Fitza, 2018). The focus on the United Kingdom is justified by the profound presence of immigrant entrepreneurs behind successful companies, with a recent report showing that 39% of the fastest-growing ventures in the United Kingdom have at least one immigrant co-founder (Ives et al., 2023). The United Kingdom has also been recognised as one of the largest and more sophisticated crowdfunding markets globally, second only to the USA in terms of volumes and regulatory maturity (Ziegler et al., 2021). At the same time, the United Kingdom may also represent a context of a liberal market economy with immigration levels similar to other major economies such as the USA, Spain, Netherlands, France and Germany (Sumption et al., 2024).

Overall, our findings suggest a nuanced approach to the analysis of immigrant team members and performance implications of ECF experiences. First, we identify non-linear relations that follow an inverted U-shape between the share of immigrants in entrepreneurial founding teams (hereafter ‘EFTs’) and both the amount raised during the campaign and the number of investors it attracted. Moreover, these effects are mediated by the campaign’s goal sum. Overall suggesting that more homogeneous teams, whether of majority immigrants or majority natives are both associated with lower levels of funding raised, and number of investors attracted; on the other hand, more diverse teams attract more funding and investors. We suggest that this pattern of associations can be explained through theoretical integration. Here, the main logic followed is that of risk attitude, which, when applied to our context, relates to fundraising entrepreneurs’ tendency to take risks when setting ECF goals. These tendencies are moderated by both cognitive diversity in entrepreneurial teams and their social capital. Specifically, we argue that teams with greater cognitive diversity are better at setting optimal campaign goals, by balancing differing risk attitudes, versus less-cognitive diverse teams where risk attitudes of members are more similar. Furthermore, we also argue that these tendencies are further supported by abilities to access a team’s social capital endowments, where more diverse teams can utilise wider social capital networks to gain successful completion of ECF campaigns, while less-diverse teams reach a more limited base of social capital and more limited resources embedded within it. In addition, when considering long-term survival, we find that the higher the share of immigrants among EFTs, the lower the likelihood of an equity crowdfunded venture’s long-term survival. This may be explained by possible undercapitalisation in majority immigrant teams due to their greater risk-aversion, which in our context is evident in lower ECF campaign goal setting, and its results. This receives support in further findings that when initial fundraising involves higher sums, such misfortunes are reversed.

Accordingly, our study presents several contributions. First, we provide empirical evidence for the role of mixed EFTs in reaching more optimal crowdfunding campaign results. This insight while important for fundraising EFTs, platform operators and policymakers has been overlooked in earlier works focusing on comparing immigrants versus native entrepreneurs. As such, it also presents a novel insight with respect to the ability of crowdfunding to democratise and improve access to finance for marginalised entrepreneurs. More specifically, it shows that teams with a balanced mix of immigrants and natives provide more optimal campaign results, than more homogenous teams of majority immigrants. Second, it suggests that such novel insight can be explained through theoretical integration arguing that effects of risk attitudes on campaign goal setting and execution are moderated by cognitive resource diversity and social capital endowments. Thus, we challenge assumptions that marginalised entrepreneurs enjoy better outcomes when using ECF simply because of its more democratic nature as an open and public internet-enabled fundraising mechanism. In addition, instead, suggest that immigrant entrepreneur preferences for risk aversion leads to lower goal setting and less optimal outcomes in immigrant majority teams using ECF, while mixed teams of immigrants and natives enhance optimal outcomes of ECF thanks to greater cognitive diversity and wider social capital reach. Third, in terms of contribution to research, the current study extends our understanding of relations between immigrant engagement in investment crowdfunding (such as ECF) and success, and not only non-investment crowdfunding and success, which was the focus in earlier works. Such a distinction is important as the context of fundraising through presales of products and services is markedly different to that of fundraising through the sale of ownership stakes, as the latter involves substantially higher amounts raised and higher risks involved.

In the remainder of the article, we first review literature on success of ECF campaigns and post-campaign success of equity crowdfunded ventures. Next, we present the unique phenomenon of immigrant entrepreneurs and suggest hypotheses about relations between the share of immigrants in entrepreneurial teams and ECF campaign success and long-term venture survival. These are followed by a presentation of our methodological choices and procedures, as well as a summary of the results of our analyses. We later discuss these results considering earlier works, and conclude by highlighting the key contributions, limitations and implications of the study.

Literature review

Success of equity crowdfunding campaigns

Research into the determinants of ECF campaign success has attracted much attention in recent years leading to the publication of several literature reviews (Mazzocchini and Lucarelli, 2023; Mochkabadi and Volkmann, 2020; Shneor and Vik, 2020), with the most recent of which identifying 32 studies examining related questions. All reviews conclude that while drawing on a broad range of theories, most studies build on the arguments of signalling theory for overcoming information asymmetries between fundraisers and prospective investors (Coakley et al., 2022; Nitani et al., 2019; Vismara, 2016). Furthermore, for the identification of potentially influential signals, researchers have often employed human capital (Barbi and Mattioli, 2019; Lim and Busenitz, 2020; Piva and Rossi-Lamastra, 2018) and social capital theories (Barbi et al., 2023; Brown et al., 2019; Graziano et al., 2023), when referring to characteristics of both fundraisers and investors. Unsurprisingly, these reviews conclude with a long list of variables that were significantly associated with campaign success indicators, roughly clustered into eleven categories (for detailed review see: Mazzocchini and Lucarelli, 2023).

When focusing specifically on issues related to the characteristics of the fundraisers, research refers to characteristics of entrepreneurial teams and individual entrepreneurs. The guiding assumption is that the EFTs’ size, qualities and composition may be relatively easy to observe and assess, and hence, serve as important criteria in investment decision-making. Here, it is worth noting that the criticality of such considerations is not specific to fundraising via ECF and has been seen to have significant effects on venture capital and business angel investment decisions (Mason and Stark, 2004; Muzyka et al., 1996; Pintado et al., 2007). Nevertheless, the more open nature of ECF, allowing the participation of less-experienced and less-sophisticated retail investors, merits investigations into the importance of similar criteria also for ECF investors.

First, when considering team size, most studies find that fundraising EFTs represent a more attractive proposition than solo entrepreneurs (Coakley et al., 2022; Lim and Busenitz, 2020), and that larger teams lead to better ECF campaign outcomes (De Crescenzo et al., 2020; Mamonov and Malaga, 2018; Ralcheva and Roosenboom, 2020). Reducing dependency on any single individual and spreading it across multiple individuals presents greater flexibility for continued operations if a lead entrepreneur is incapacitated or decides to opt out of the venture. Furthermore, EFTs imply greater availability of complementary skills and cognitive capacities to successfully address different problems that may emerge throughout the startup life, as suggested by the cognitive resource diversity theory (Horwitz, 2005). Hence, overall, such preferences are part of efforts for reducing potential execution risks (Mamonov and Malaga, 2018).

Second, when considering team member qualities, research examined potential effects with respect to different indicators of human capital. Some studies examined the role of education level finding that ventures with more highly educated team members are also more likely to run successful ECF campaigns (Barbi and Mattioli, 2019; Nitani et al., 2019; Piva and Rossi-Lamastra, 2018). However, studies that examined the role of prior entrepreneurial and professional experiences suggest inconclusive results, where some found a positive association with ECF campaign outcomes (Barbi and Mattioli, 2019; Lim and Busenitz, 2020; Nitani et al., 2019; Piva and Rossi-Lamastra, 2018), others found no such effects (Cumming et al., 2019b; Mamonov and Malaga, 2018; Vismara, 2019).

Finally, when considering team compositions, research primarily focused on issues related to gender returns inconclusive results. Some analyses find non-significant associations between the presence of women on EFTs and campaign success (Mamonov and Malaga, 2018; Piva and Rossi-Lamastra, 2018). Others find positive associations between having at least one woman on the team and average investor pledge, amount raised and the extent of overfunding (Cicchiello et al., 2021). Similarly, positive associations were also found between the number of women on the venture’s team and both the amounts raised and the number of investors attracted (Barbi and Mattioli, 2019). On the other hand, an earlier study found that women founders tend to raise significantly lower amounts (Vismara, 2016).

Despite prevailing notions of crowdfunding as a channel easing access to entrepreneurial finance for minorities who have experienced greater challenges in obtaining it through traditional sources, earlier research has not yet examined the potential role that an immigrant’s presence in EFTs may have on the success prospects of ECF efforts. Such investigation may be needed especially considering growing immigration waves affecting many countries, the efforts made towards their successful economic and social integration, as well as the harvesting of benefits from successfully launched businesses by immigrant entrepreneurs (Dheer, 2018; Malki et al., 2022).

Immigrant entrepreneurs

Entrepreneurial venturing incorporates the acceptance of a significant degree of risk in both immigrant (Batista and Umblijs, 2014) and non-immigrant communities (Stewart and Roth, 2001). Nevertheless, immigrant entrepreneurs can be deemed to accept even greater risks by pursuing entrepreneurial careers due to confounding effects of the risks inherent to both their immigration and entrepreneurial experiences. In such cases, immigrants place both the legitimacy of their business and their social-economic standing in their host country in danger. Furthermore, many immigrants may start their entrepreneurial journeys from humble socio-economic backgrounds and/or a sense of necessity, hence, risking relatively larger shares of their savings and other economic resources in their entrepreneurial venturing. As a result, when faced with economic instability, limited financial resources and language and/or market knowledge barriers immigrant entrepreneurs may become more risk-averse in order to protect the little they own (Stark, 1991).

Research documents a significant negative relation between risk aversion and income (Meissner et al., 2023). However, the greater risk aversion demonstrated by immigrants with respect to employment decisions results in significantly lower average income than natives, with payment gaps standing at 19% internationally and as high as 42% in some countries (International Labour Organisation, 2020). The same study also found that a significant portion of the migrant pay gap remains unexplained even after controlling for worker education, experience, age or location. One explanation for such a pay gap may be greater risk aversion, which has been documented (Golgeci et al., 2023; Stark, 1991). Thus, when pursuing entrepreneurial careers, immigrants are likely to carry such preferences with them while settling for lower incomes also as entrepreneurs, and especially when fundraising for their ventures where investors expect substantial commitments of ‘sweat capital’. Furthermore, taking into account the greater difficulties faced by immigrant entrepreneurs to access entrepreneurial finance (Bewaji et al., 2015; Bruder et al., 2011; Lee and Black, 2017), and their greater dependence on own resources and the support from their close social circles (Hulten and Ahmed, 2013; Kushnirovich and Heilbrunn, 2008; Moghaddam et al., 2017) may all result in setting more modest goals in their fundraising efforts. Here, ECF campaigns may further enhance tendencies of immigrant entrepreneurs for setting lower goal sum objectives in their campaigns due to fears of possible failure to raise funds, as well as its public nature.

While some ventures are started by solo entrepreneurs, many are created by teams. Entrepreneurial teams are likely to emerge under conditions of bounded structural uncertainty and perceived strong interdependence that arise from common interests shared by prospective team members, who view the likelihood of reaching their objectives increased through team efforts (Harper, 2008). Alternatively, when compared to individual entrepreneurs, an entrepreneurial team is better able to deal with the uncertainties associated with venture creation thanks to a negotiated collective cognition in such teams (West, 2007), while accessing a broader human and social capital resource base (Omri and Boujelbene, 2015). Accordingly, immigrant members of EFTs influence the negotiated collective cognition of the team in its decision-making processes (West, 2007), including those related to ECF campaign offerings, as a part of a venture’s fundraising efforts. However, immigrants may represent a minority, a majority or a balanced group within EFTs. Hence, when the majority of EFT members are immigrants, they are likely to aim for lower goal sums, as part of joint efforts to lower risks of unsuccessful fundraising and a general will to accept lower pay. However, when EFTs represent a more balanced mix of native and immigrant team members, intra-team negotiations are likely to result in setting higher sums than immigrants would have gone for independently. In such cases, members of the team may be less willing to accept lower pay, while at the same time view the ability to tap into more numerous and different social networks as an opportunity to raise more funds through a potentially wider campaign reach. Finally, when immigrants represent a minority of team members, thanks to the greater ease with which natives can access to other funding sources, financial dependence on crowdfunding may be more limited and allow for setting lower goals. This, coupled with a disposition towards more conservative expectations from the campaign, and their more modest contribution in terms of social reach to unique contacts, having an immigrant member may help convince the team to set relatively lower sum goals for their ECF campaign.

Accordingly, we hypothesise the following:

Research on drivers of ECF campaign success has highlighted the positive influence of various dimensions of social capital on campaign outcomes (Cai et al., 2021), with studies often finding a positive association between the size of an entrepreneur’s social network and successful outcomes of their campaigns (Graziano et al., 2023; Lukkarinen et al., 2022; Nitani et al., 2019). Overall, more diverse teams are likely to reach a broader network of non-overlapping contacts and hence, be endowed with a wider social capital base. Furthermore, more diverse teams are also more likely to come up with more innovative ideas for campaign distribution and promotions, thanks to enjoying greater cognitive resource diversity (Horwitz, 2005).

Accordingly, the extent to which immigrants are part of EFTs has implications for the social capital made available for the fundraising venture. Here, more homogenous teams of either majority immigrants or majority non-immigrants, may have a more limited scope of social capital the team may tap into, and hence are likely to raise lower sums overall. Furthermore, the homogeneous nature of such teams also implies a more limited access to cognitive resources diversity and hence may face greater difficulties coming up with creative ideas for campaign presentation, distribution and promotions. Conversely, more balanced teams imply the presence of greater diversity with immigrants and non-immigrants on the team, each with their own social networks, which are likely to encompass a larger pool of prospective backers overall. At the same time, the heterogenous nature of such teams implies greater cognitive resource diversity that may generate more creative ideas for campaign presentation, distribution and promotions. Such assumptions are in line with earlier findings that team diversity is a crucial condition to maintain diverse sources for information and market opportunities, when seeking resources (Martinez and Aldrich, 2011). Hence, we hypothesise the following:

In ECF, the goal sum presents the amount of money fundraisers wish to raise. It may be indicated as either a single sum or a range between a minimum and a maximum goal. In the latter case, meeting the minimum threshold represents a successful outcome of the campaign. Since unsuccessful campaigns may raise less than the indicated sum goal, and since goal ranges may indicate opportunities for overfunding beyond the minimum goal set, goal sums and amounts raised may be highly correlated but not equivalent. While inconclusive about the direction of impact, earlier research does find significant associations between goal sums and amounts raised, share of amounts raised out of target and the number of investors. Some finding a negative association (Piva and Rossi-Lamastra, 2018; Ralcheva and Roosenboom, 2020; Vulkan et al., 2016) when campaigns can be viewed as less attractive due to requirements of higher investments for a set ownership share. Others find a positive association interpreted as viewing higher goals as indicators of higher degrees of entrepreneur self-confidence and project quality (Lukkarinen et al., 2022; Vismara, 2016, 2019). Hence, when combined with earlier arguments for the effects of share of immigrants in EFTs on campaign goal setting and outcomes, we hypothesise the following:

Upon successful completion of an ECF campaign, ventures receive the funds raised and further focus their attention on firm development and growth. However, evidence suggests that most new ventures will not survive in the long term (Eisenmann, 2021; Triebel et al., 2018). Thus, we proceed to examine the likelihood of survival of ventures that used ECF. We first review the literature on survival and failure of ECF funded firms and then examine whether immigrant presence in teams may influence it.

Survival and failure of equity crowdfunded firms

While the success of ECF campaigns has received much research attention, the long-term success, survival, or failure of equity crowdfunded ventures remains limited. First, a study by Hornuf et al. (2018) exploring the survival of 413 German and UK-based equity crowdfunded ventures found that those who presented higher valuations attracted a larger number of initial VC investors and those with a larger senior management were also more likely to survive. A different study by Signori and Vismara (2018) examining 212 UK-based firms, found that those reporting positive sales at campaign period and attracting more qualified investors were also more likely to survive, while those offering shares with voting rights were more likely to fail. A later study by Coakley et al. (2022) of 1291 UK-based firms found that solo entrepreneurs were more likely to fail than entrepreneurial founding teams, and that ventures presenting higher valuations, offering a larger share of equity, and attracting more investors were less likely to fail. More recently, a study by Kivilo et al. (2023), which examined 429 US-based firms, found that ventures where entrepreneurs retained higher shares of equity (i.e. offered less equity to the crowd), set higher campaign goals, and reported higher revenues at time of campaign, were more likely to survive. Across studies, we see that three found that firm age at time of campaign, and the status of its patenting efforts were not associated with the likelihood of either survival or failure. Moreover, two of the studies also showed that the number of employees had no such effect either. Again, and despite examining contexts with relatively large share of immigrants in the population, none of the previous studies examined the potential influences of the presence of immigrants in EFTs may have on equity crowdfunded firm survival. Moreover, neither of these studies has considered potential impacts of founder team diversity more broadly either. The closest indirect insight emerged in the finding that ventures led by teams rather than solo entrepreneurs are more likely to survive (Coakley et al., 2022), and that firms with a higher number of senior team members were also more likely to survive (Hornuf et al., 2018). In addition, while larger teams do not guarantee diversity, they are at least more likely to incorporate it.

When considering immigrant entrepreneurship, research in different national contexts suggests that ventures established by immigrants exhibit even lower survival rates than those established by natives (Mata and Alves, 2018; Vinogradov and Isaksen, 2008). Such failures have been explained by a variety of reasons from the offering of novel products and the use of locations in high-cost and competitive urban environments (Vinogradov and Isaksen, 2008), as well as low levels of work experience in the destination country and over reliance on relatively small ethnic communities in these countries (Mata and Alves, 2018). In the latter case, research shows that greater dependence on co-ethnic clientele results in financial penalty of lower revenues entrepreneurs draw from their business (Shinnar et al., 2011). This means that immigrant entrepreneurs may miss out on potential benefits from partnerships with native co-founders, as it may expand their businesses’ client base. Despite the benefits that mixed immigrant and native EFTs may yield, the potential effects of the share of immigrants among EFT members on firm survival and growth is rarely explored. When viewing the presence of immigrant entrepreneurs on EFTs as a source for cognitive resource diversity and access to wider social capital, research suggests that their related contributions become even more important later in the venture’s development; a study by Abd Hamid et al. (2023) considering immigrants as ‘transnational entrepreneurs’ found that they serve as resource arbitrageurs thanks to their intercultural experiences and aptitudes, while their ‘underdog’ status in new home markets provides them with stronger abilities to generate innovative outsider insights holding advantages over purely monocultural entrepreneurs. Cross-cultural experiences involve experiences of ‘self-image shocks’ which translate to enhanced skills that are highly relevant for entrepreneurial work in sensing, seizing and transforming capabilities (Pidduck, 2022; Pidduck and Zhang, 2022). Furthermore, while not considering immigrants specifically, a study by Steffens et al. (2012) found that more homogeneous entrepreneurial teams were less likely to present strong performance in the long term whereas Martinez and Aldrich (2011) found that team diversity has greater importance in later stages of a venture’s life cycle for maintaining diverse sources of information and market opportunities. When considering immigrants specifically, evidence suggests that the presence of immigrants in EFTs substantially increases the chances of an exit via a financial harvest either involving an acquisition or initial public offering (Elitzur et al., 2023).

Thus far, the spares research on the venture survival rates of equity crowdfunded firms provides limited insights on the potential effects of EFT diversity on venture survival, while remaining silent about the prospective effects of immigrants on EFTs. Nevertheless, related studies do show that ventures that were established by EFTs exhibit higher survival rates than those started by individuals (Coakley et al., 2022), and that ventures with larger senior management teams are also more likely to survive (Hornuf et al., 2018). Furthermore, both tenure (experience) and age diversity among team members were associated with greater survival (Coakley et al., 2022). Bringing these insights together one can expect that more homogenous teams (with either majority immigrants or non-immigrants) are less likely to enjoy cognitive resource diversity and access to wider social capital resources when navigating the challenges during the venture’s life. Furthermore, the greater likelihood of failure may be amplified in ventures with majority immigrant teams due to self-reinforcement of strategic choices that lead to such failures (as presented earlier with respect to product, location, work experience and ethnic community focus choices). However, a more balanced team may have better access to both cognitive resource diversity and social capital resources and is more likely to employ them in times of need and therefore, survive. In addition, it is also possible that discussions in such teams may help reduce some of the likelihood of the strategic choices that have been associated with higher failure rates among immigrant entrepreneurs. Accordingly, we hypothesise the following:

Methods

Data and sample

Our sample is comprised of selected ECF offerings from the Crowdcube, Seedrs and SyndicateRoom platforms, compiled via the database of TAB (available on Thomson Reuters Eikon App Studio). 1 Firms had to meet several criteria to be part of our final sample. First, follow-on offerings are removed to avoid endogeneity issues that may arise from the relation between initial campaign and first follow-on success (Coakley et al., 2022). Second, we focus on UK firms only to limit other reasons for seeking crowdfunding (such as fostering internationalisation) and to reduce cross-country heterogeneity related to different reporting and regulatory frameworks (Cumming et al., 2019a). Third, we remove firms with missing information about entrepreneurial teams. TAB data are matched with those from the UK Companies House to extract information about team members. The registration number is used for venture identification. We focus on those appointed as directors. Existing research uses them as proxy for founders (Haans and van den Oever, 2021). This selection criteria results in a list of 1171 offerings in the period from April 2011 to December 2018.

Measurements

Dependent variables

The total amount (£k) of funds (Amount) raised and the number of investors (Funders) are used for capturing campaign outcomes. Furthermore, a dichotomous indicator of firm failure, and a continuous indicator of time to failure are used for capturing long-term likelihood of failure, as used in Signori and Vismara (2018).

Independent variable

The share of immigrants in EFTs is calculated as the ratio of those founders who do not hold the UK citizenship over the total number of EFT members. The dataset included only 14 observations of single entrepreneurs. In such cases, the value 0% represented a native entrepreneur, while 100% represented an immigrant entrepreneur. The exclusion of these observations did not affect the results of the analyses.

Control variables

Several factors that have been shown to affect campaign outcomes in earlier research were used as controls, including level of EFT members’ education and equity share on offer (Ahlers et al., 2015); firm age, sectoral diversification and average team age (Ralcheva and Roosenboom, 2020; Signori and Vismara, 2018); as well as year, platform and location fixed effects (Hornuf et al., 2022; Johan and Zhang, 2022).

Data analysis

Our analysis involves two steps, as it aims to shed light on the relation between share of immigrants in EFTs and both the campaign outcomes, and long term-firm likelihood of failure.

Campaign outcomes

To test hypotheses 1–3, we investigate the relationship between immigrant share and amount, as well as the role played by goal in this relation. To investigate whether the hypothesised relationship follows and inverted U-shape, we include both the share of immigrants in EFTs and its square values in the analysis. To test if goal amount mediates this effect, we use the Baron and Kenny (1986) method. This means that the share of immigrants in EFTs should affect both the goal and campaign outcomes. If the relationship between the immigrant share variable and campaign amount becomes weaker when goal is included in the analysis, this indicates mediation. We employ OLS analysis as summarised in the following equations,

Firm failure

To examine potential long-term influence of the share of immigrants on EFTs, we analyse its non-linear association with the likelihood of post-campaign firm failure. Thus, we deploy the probit and Hazard models. The latter has the advantage of taking into account time to fail. Methodology can be summarised by the following equations,

Equation (6) represents the probit model and equation (7) represents the Weibull hazard model. In the reported multivariate analysis, both successful and unsuccessful offerings are included to avoid endogeneity that may arise due to selection bias if we include successful offerings only (Coakley et al., 2022; Signori and Vismara, 2018).

Results

Univariate analysis

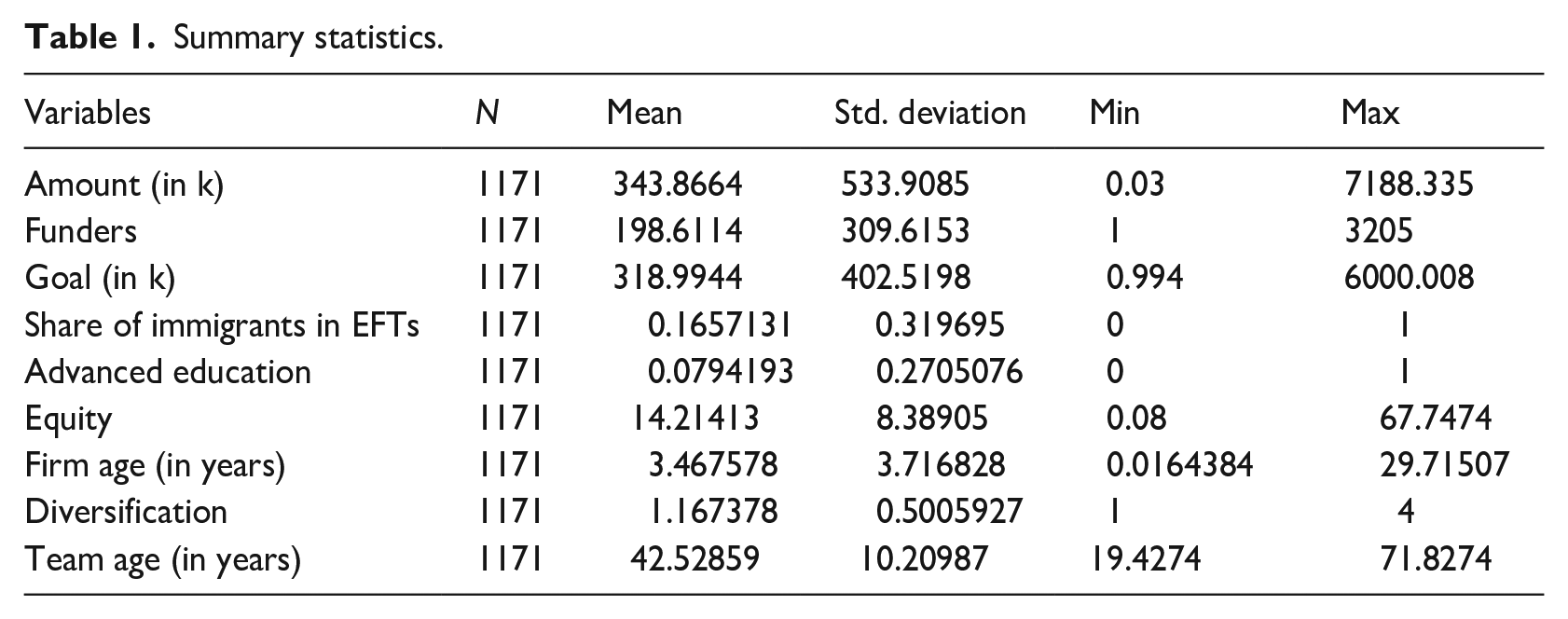

Overall characteristics of our full sample are described by descriptive statistics summarised in Table 1. The presence of immigrant founders in ECF founder teams is at 16%. The total amount raised is £344k on average when firms aim to raise around £320k. Teams are relatively small with two members on average. Around 7% of campaigns are conducted by startups with at least one member holding a doctor of philosophy. The average number of investors is 198, and the equity issued is around 14%. Team members have an average age of 42 years.

Summary statistics.

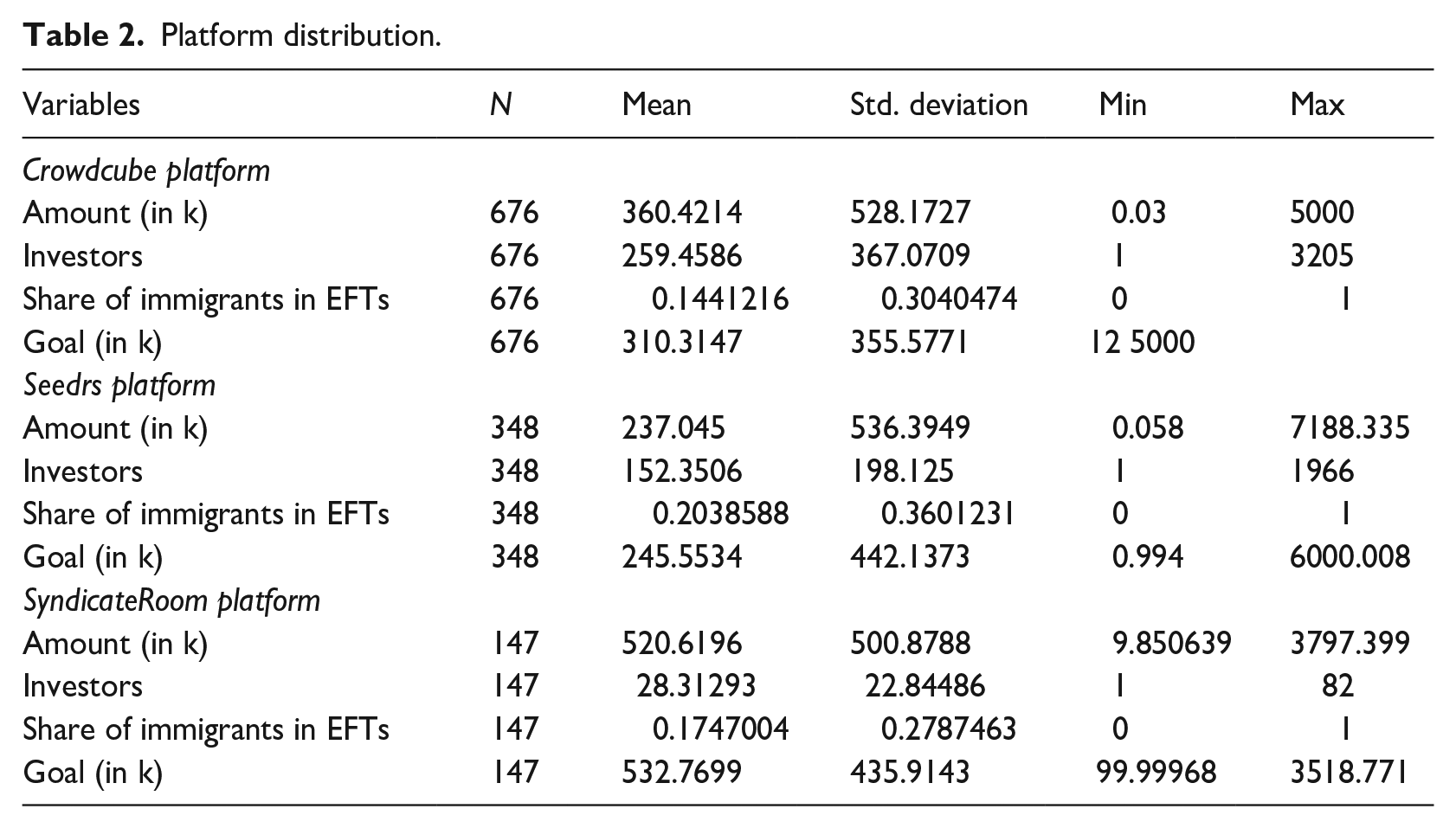

While the descriptives in Table 1 present the full sample, since our sample includes observations from three different platforms, Table 2 reports summary statistics on all the key variables of our study by platform.

Platform distribution.

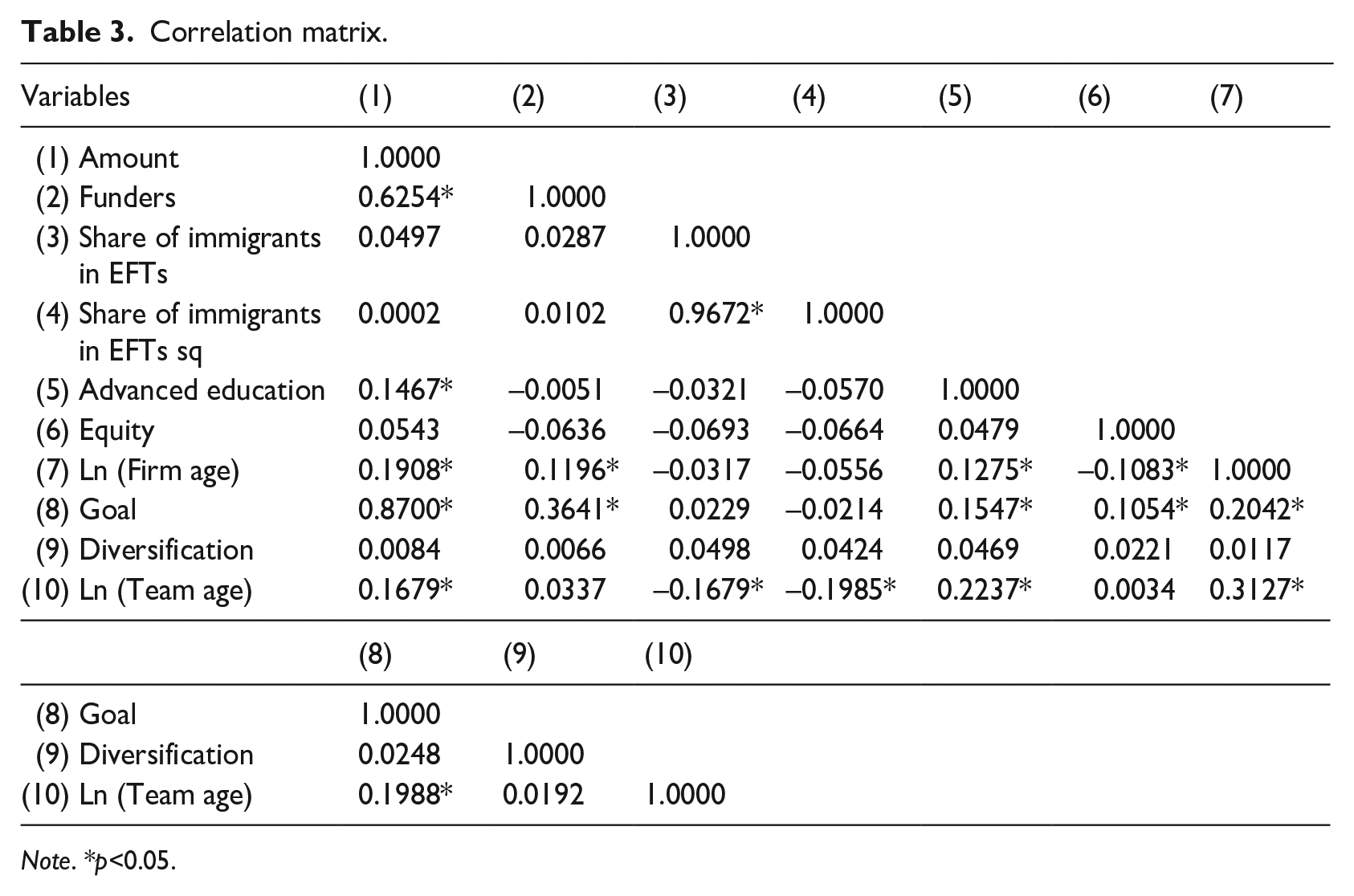

Results suggest there is heterogeneity across platforms. SyndicateRoom offerings raise more possibly due to the pronounced presence of professional investors. They also involve campaigns setting higher goals. The share of immigrants in EFTs is higher on Seedrs, representing 20% of EFT members on average. The same figures on SyndicateRoom and Crowdcube stand at 17% and 14%, respectively. Crowdcube exhibits a higher number of funders compared to the other two platforms. The next test checks for multicollinearity among the variables employed in this study. Correlation values are presented in Table 3.

Correlation matrix.

Note. *p<0.05.

There is no evidence that supports the presence of multicollinearity in this study. The highest value among control and explanatory variables is the one between firm and team age. That is the value of 0.31, which is well below the 0.7 threshold. This means that measures used are uniquely capturing different variables.

Multivariate analysis

Campaign outcomes

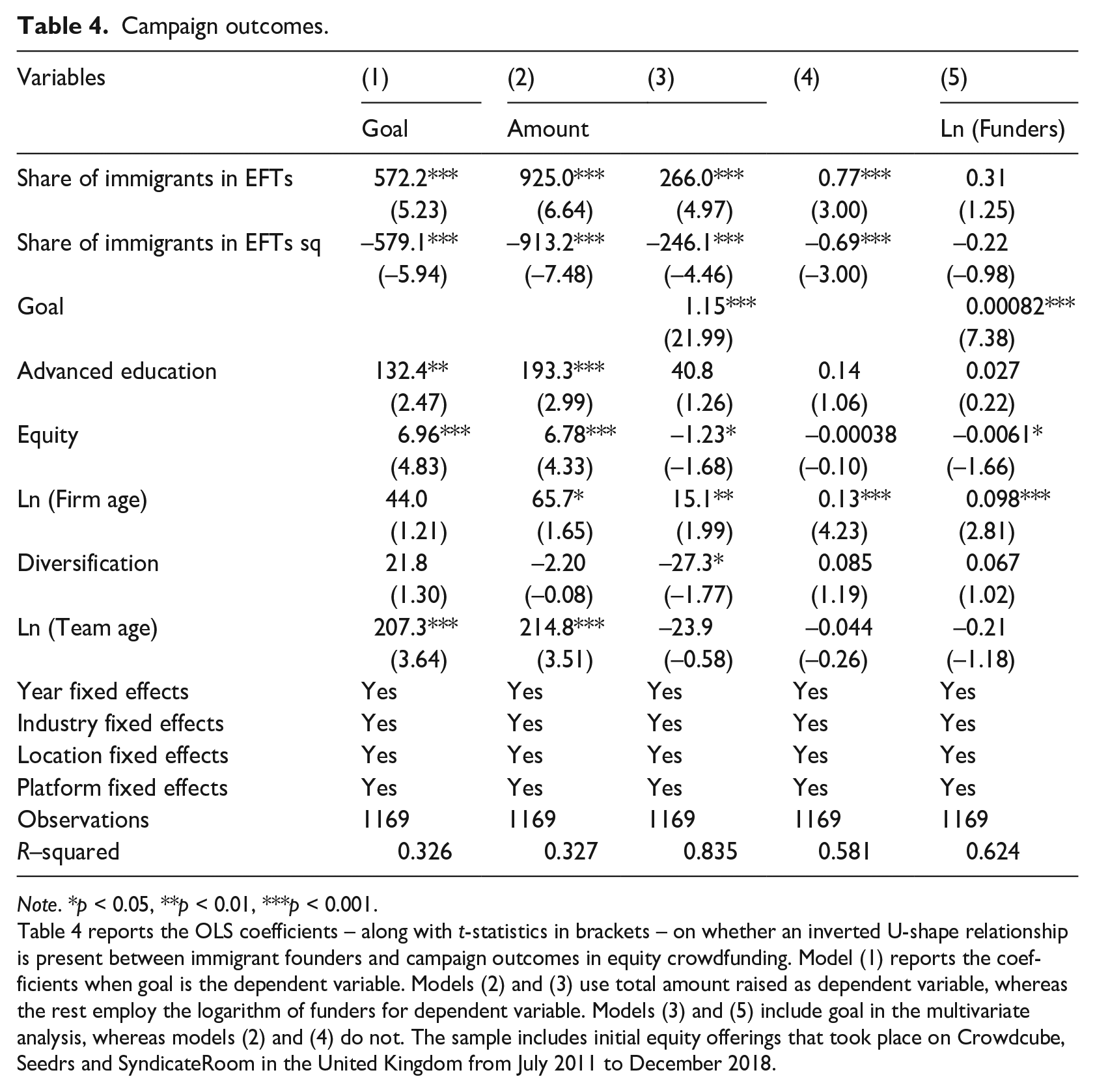

Results of the regression analysis are reported in Table 4. Model (1) uses goal sum as the dependent variable, whereas the remaining models use either the amount (models 2 and 3) or the number of funders (models 4 and 5) for dependent variables.

Campaign outcomes.

Note. *p < 0.05, **p < 0.01, ***p < 0.001.

Table 4 reports the OLS coefficients – along with t-statistics in brackets – on whether an inverted U-shape relationship is present between immigrant founders and campaign outcomes in equity crowdfunding. Model (1) reports the coefficients when goal is the dependent variable. Models (2) and (3) use total amount raised as dependent variable, whereas the rest employ the logarithm of funders for dependent variable. Models (3) and (5) include goal in the multivariate analysis, whereas models (2) and (4) do not. The sample includes initial equity offerings that took place on Crowdcube, Seedrs and SyndicateRoom in the United Kingdom from July 2011 to December 2018.

Model (1) results document an inverted U-shape relation between the share of immigrants in EFTs and the campaigns’ goal sum, lending support to Hypothesis 1. The coefficient for share of immigrants in EFTs is positive and significant at 1% level, and the square coefficient is negative and significant at 1% level. Put differently, as the share of immigrants in EFTs increases, they set higher goals for their campaigns. However, once immigrants become a majority, the larger their share in EFTs, the lower sums they seek to raise.

Model (2) findings reveal an inverted U-shape relation between immigrant presence and total capital raised, as the coefficient is positive and significant at 1% level, as well as negative and significant at the 1% level for the square coefficient. This supports Hypothesis 2. When we add the goal sum in model (3), this result suggests that goal mediates the relation between the share of immigrants in EFTs and total capital raised. This means that the effect of share of immigrants in EFTs on amount of money they raise operates through the goal sum being set for each campaign. The magnitude of the direct effect of the share of immigrants in EFTs, as captured by the relevant coefficients, is 3.5 times lower once also considering its indirect effect via the goal sum set. Furthermore, the model’s explanatory power increases significantly with r-square changes from 0.33 to 0.83. Results are similar in models (4) and (5) in which findings support the presence of an inverted U-shape relation between share of immigrants in EFTs and funders. This may serve as evidence in support of Hypothesis 3.

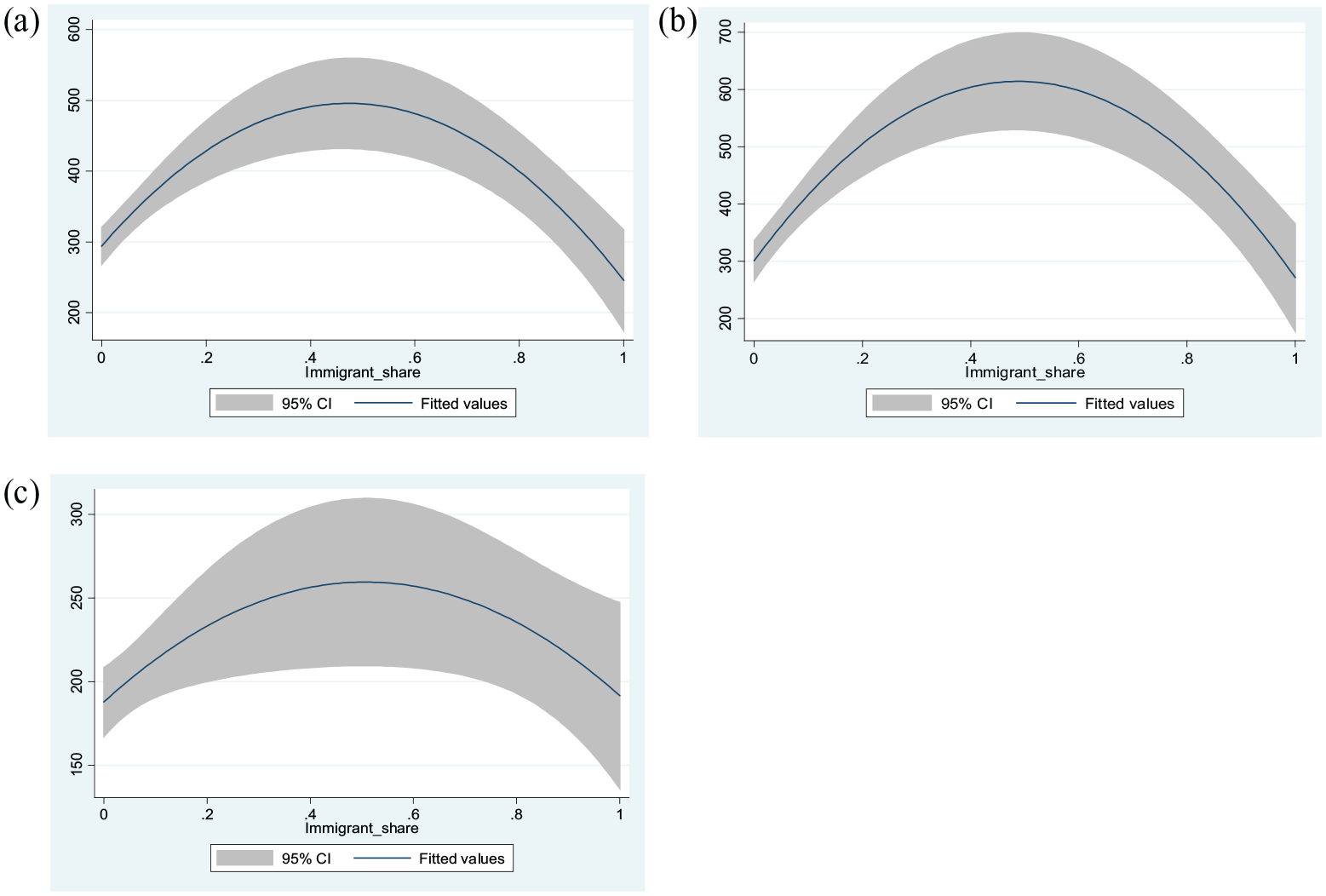

To enusre we document an inverted U-shape relationship, we follow a similar procedure as in Haans et al. (2016). For a relation to be quadratic, two requirements must be met. First, the share of immigrants in EFTs’ coefficient must be positive and significant which holds in our case. Second the slope must be negative (positive) at high (low) end. A way to test this is to plot the relation. Figure 1 plots the relations between the share of immigrants in EFTs, and the campaign’s goal sum, the amount raised and the number of funders.

Immigrants and campaign outcomes.

The graph in Figure 1 supports the presence of an inverted U-shape relation between immigrant presence in EFTs and both the goal sum and the total amount of money raised and funders. It suggests that slope is upward (downward) at the low (high) end. The final requirement is for the turning point to lie in the middle. First, Figure 1 suggests that turning point lies in the middle. Using the formula −β/2δ, the turning point is 0.5. It lies exactly in the middle of the share of immigrants in EFTs which range between zero and one. Hence, all criteria are met, while supporting the presence of an inverted U-shape relation.

Firm failure

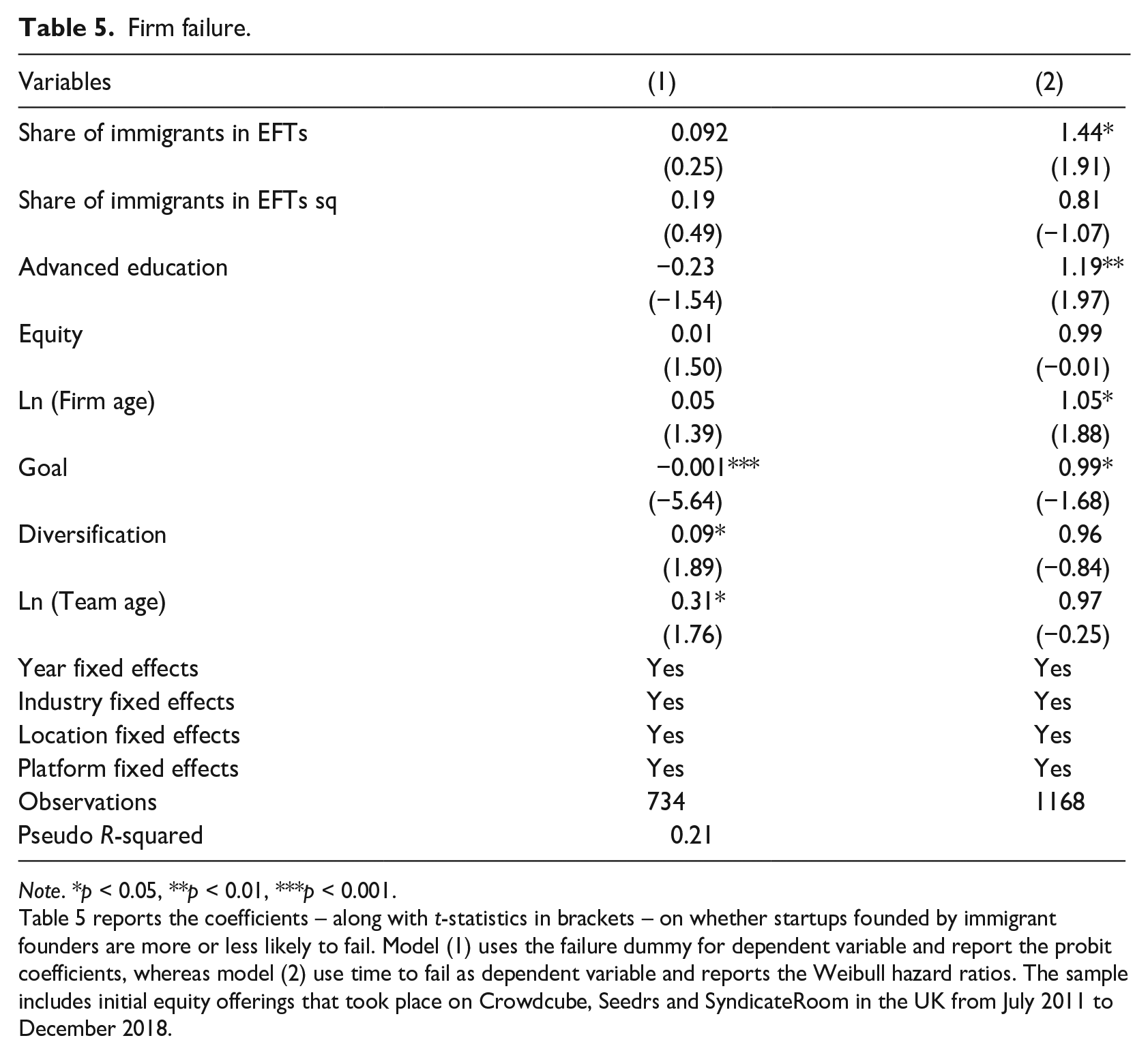

Table 5 summarises the results for firm likelihood of failure. Model (1) reports probit coefficients when the failure dummy is used as the dependent variable (receiving value ‘0’ in case of survival and ‘1’ in case of failure), whereas model (2) reports hazard ratios from the Weibull model when using time to fail as the dependent variable.

Firm failure.

Note. *p < 0.05, **p < 0.01, ***p < 0.001.

Table 5 reports the coefficients – along with t-statistics in brackets – on whether startups founded by immigrant founders are more or less likely to fail. Model (1) uses the failure dummy for dependent variable and report the probit coefficients, whereas model (2) use time to fail as dependent variable and reports the Weibull hazard ratios. The sample includes initial equity offerings that took place on Crowdcube, Seedrs and SyndicateRoom in the UK from July 2011 to December 2018.

The findings do not provide evidence in support of hypothesis 4. The share of immigrants in EFTs – along with its square – coefficients are not significant. In other words, our results suggest that the relation between firm failure and immigrant presence in ECF teams may not follow an inverted U-shape pattern. However, there is some weak evidence that majority immigrant EFTs may underperform natives and mixed teams in the long run. The coefficient for the share of immigrants in EFTs in model (2) is positive and significant at 10% level.

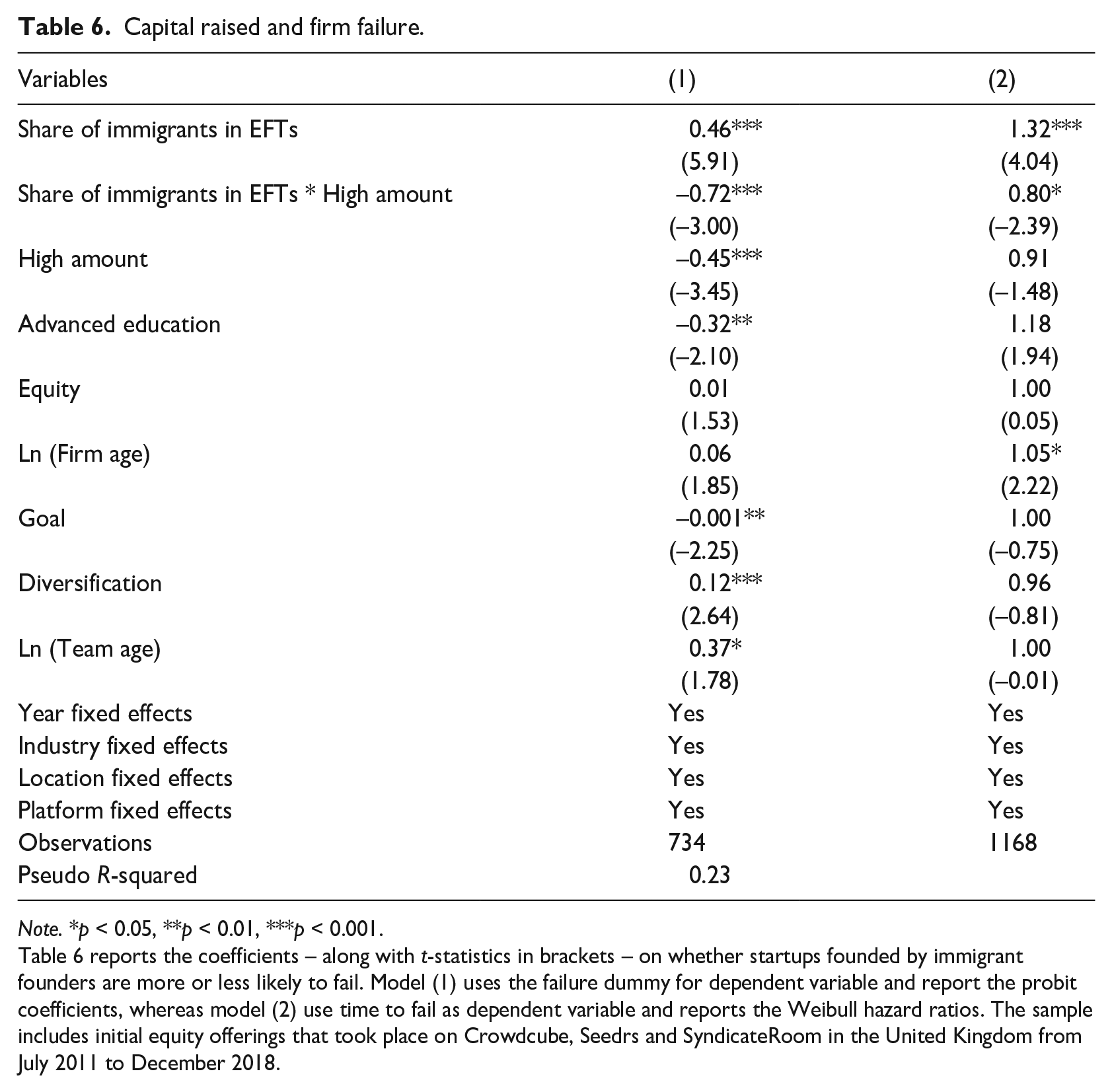

The next test aims to check whether the relative amount of capital raised in an ECF campaign is beneficial for the survival of ventures in which immigrant presence is pronounced. To do this, we add the interaction term between the share of immigrants in EFTs and high amount. The latter takes value 1 if the offering exhibits total amount higher than the median that is £160k, and zero otherwise. Table 6 summarises the results. Model (1) reports probit coefficients whereas model (2) reports Weibull hazard ratios.

Capital raised and firm failure.

Note. *p < 0.05, **p < 0.01, ***p < 0.001.

Table 6 reports the coefficients – along with t-statistics in brackets – on whether startups founded by immigrant founders are more or less likely to fail. Model (1) uses the failure dummy for dependent variable and report the probit coefficients, whereas model (2) use time to fail as dependent variable and reports the Weibull hazard ratios. The sample includes initial equity offerings that took place on Crowdcube, Seedrs and SyndicateRoom in the United Kingdom from July 2011 to December 2018.

The results suggest that ECF may help reduce failure rate for those teams with a pronounced presence of immigrants. Interaction term coefficient in model (1) is negative and significant at 1% level, whereas model (2) results report a hazard ratio less than 1 and significant at 1% level. More importantly, the magnitude of the interaction term’s coefficient is higher than the one for share of immigrants in EFTs. In other words, a high amount raised in an ECF campaign may significantly reduce the failure rate of ventures founded by EFTs in which there is a significant presence of immigrants.

Discussion

This study presents several interesting findings with respect to the roles played by the share of immigrants in EFTs in terms of determining a venture’s ECF campaign success, and long-term likelihood of survival. As such, it presents contributions to literature on predictors of ECF campaign success (Mazzocchini and Lucarelli, 2023), ECF long-term impact on venture survival (Coakley et al., 2022; Hornuf et al., 2018; Kivilo et al., 2023), and to the understanding of conditions under which crowdfunding can improve access to finance for members of marginalised groups (Butticè and Useche, 2022; Greenberg, 2019).

First, we find evidence for an inverted U-shape relation between the share of immigrants in EFTs and the total amount of capital raised, as well as the number funders investing in their venture. As such, we provide new insight to earlier literature that primarily focused on effects of team size (De Crescenzo et al., 2020; Mamonov and Malaga, 2018; Ralcheva and Roosenboom, 2020) and member’s qualifications in terms of education and professional experience (Barbi and Mattioli, 2019; Nitani et al., 2019; Piva and Rossi-Lamastra, 2018). The current study adds insight into the inclusion of immigrants in EFTs as a potential force negotiating for risk reduction on the one hand and boosting innovativeness and problem-solving capacities through cognitive diversity on the other. Furthermore, the non-linear nature of the relationship implies that homogeneity in EFTs may be less conducive for successful ECF efforts, while greater diversity enhanced likelihood of their success. These notions receive support in earlier studies about positive effects through the inclusion of females in EFTs, which represent a different resource-marginalised social group of prospective entrepreneurs and campaign success (Barbi and Mattioli, 2019; Cicchiello et al., 2021).

Second, we find that this relation is mediated by the goal sum set by the team. Here, the positive association between goal sum and funds raised finds support in earlier studies (Lukkarinen et al., 2022; Vismara, 2016, 2019), while contradicting others (Piva and Rossi-Lamastra, 2018; Ralcheva and Roosenboom, 2020; Vulkan et al., 2016). Such inconsistencies may be attributed to different samples, market contexts, and timing of data collection in a relatively young though gradually maturing industry (Lukkarinen et al., 2022). Regardless, our findings support the explanation suggesting that setting higher goals signals higher degrees of entrepreneurial confidence and project quality, and hence also tend to raise higher sums overall. Nevertheless, the relationship between the share of immigrants in EFTs and goal sums represents a new insight, unexplored in earlier work. It suggests a potential influence by immigrants in calibrating campaign ambitions and associated risks in EFTs. Furthermore, the non-linear nature of this relation, suggests that more heterogenous teams may aim for higher goals, while homogeneous teams may aim for lower goals. A possible explanation for lower goals in majority immigrant EFTs may be a result of internal pressures to reduce risks and willingness to work for lower pay (Golgeci et al., 2023; Stark, 1991). Converely, a possible explanation for lower goals set by majority native entrepreneurs may be due to a combination of lower levels of need on average (when compared to immigrants), thanks to either available or more easily accessible finance from non-ECF channels, as well as a more limited resource network due to higher overlap in contacts of different team members (when compared to international networks of immigrants).

Third, we do not find evidence for an inverted U-shape relation between the share of immigrants and likelihood of venture failure. Instead, we find a weak negative association between higher shares of majority immigrant in EFTs and the venture’s likelihood of survival. This corresponds with earlier findings about higher likelihood of failure of immigrant-founded ventures (Mata and Alves, 2018; Vinogradov and Isaksen, 2008). However, we also find that in ventures founded by EFTs with high shares of immigrants when higher amounts are raised in ECF campaigns the rate of long-term firm failure is reduced. These combined findings suggest that greater failure of immigrant-led entrepreneurial ventures may be related to undercapitalisation.

Finally, the above findings contribute to literature at the intersection of both immigrant entrepreneurship as well as crowdfunding research. From the perspective of immigrant entrepreneurship literature, we identify conditions for more successful fundraising efforts when immigrants use ECF. Here, we both highlight the need to avoid temptations of undercapitalisation, as well as the need to tap into wider cognitive diversity and social capital in EFT formation thanks to its beneficial effects on fundraising performance. From the perspective of crowdfunding literature, we show that one of the predictors of ECF campaign success is the presence of mixed ETFs including both immigrants and natives. This enhances understanding of the role played by fundraiser characteristics on campaign outcomes and performance. In this sense, the same finding contributes to both literatures.

Implications for theory

Our findings present implications for theory. First, we highlight the role of cognitive diversity and social capital as moderators of risk attitude. Specifically, we suggest that an inverted U-shape pattern of associations between share of immigrants in EFTs and ECF campaign outcomes can be explained through such theoretical integration. Here, a theoretical argument is made that a fundraising entrepreneur’s tendency to take risks when setting ECF campaign goals is moderated by both EFTs cognitive diversity and their social capital. This manifests in evidence showing that teams with greater cognitive diversity are better at setting optimal campaign goals, by balancing differing risk attitudes, versus less-cognitive diverse teams where risk attitudes of members are more similar. Furthermore, we also argue that these tendencies are further supported by abilities to tap into team members’ social capital endowments, where more diverse teams can tap into wider social capital networks towards successful completion of ECF campaigns, while less-diverse teams reach a more limited base of social capital and more limited resources embedded within it. Furthermore, we challenge the theoretical assumption that marginalised entrepreneurs enjoy better outcomes when using ECF simply because of its more democratic nature as an open, public, and easily accessible internet-enabled fundraising mechanism. Instead, we suggest that the degree of their fundraising success when utilising ECF depends on EFTs’ composition. Immigrant entrepreneurs’ preferences for risk aversion led to lower goal setting and less-optimal outcomes in immigrant majority teams, while mixed teams of immigrants and natives better facilitates optimal campaign outcomes thanks to greater cognitive diversity and wider social capital reach.

Implications for practice

Our findings also present several implications for practice. First, ECF crowdfunding platforms may use the findings to further improve site functionalities, advice provided to fundraisers, as well as their filtration and due diligence processes. In terms of site functionalities, platforms can enhance visualisation of team diversity and backgrounds, as well as related intra-team communications and information-sharing in decision flows. In terms of advice provided, platform managers can encourage mixed EFT fundraisers to create better on-site representations of the team members while highlighting team diversity, including immigrant background, for the purpose of enhancing success of their campaign efforts. Besides in terms of due-diligence, platform managers reviewing fundraising applications prior to their onsite publication, can be more sensitive towards identifying potential risks of undercapitalisation in EFTs with a majority of members with immigrant background, and provide advice on how to avoid it.

Second, and in a broader context of policy, actors seeking to support transitional entrepreneurship (Pidduck and Clark, 2021) in immigrant groups should incorporate ECF training and guidance services into relevant programmes, for introducing a tool to overcome biases in traditional fundraising channels. However, these efforts should also stress the importance of avoiding temptations for undercapitalisation when seeking ECF investments towards enhancing the likelihood of long-term venture survival. Similarly, agencies seeking to support immigrant integration into the workforce through entrepreneurship may arrange networking, mingling and introduction seminars between native and immigrant entrepreneurs while presenting them with the benefits of cognitive resource diversity and wider social capital reach in mixed EFTs both for venture development and successful fundraising. Moreover, matching schemes for immigrant and native entrepreneurs may be introduced with the vision of enhancing cognitive diversity in and social capital of EFTs.

Limitations and implications for research

While presenting valuable insights, our study also has limitations that should be acknowledged and serve for directing future research efforts. First, the generalisability of our study may be constrained to the specific type of crowdfunding considered – equity crowdfunding, as well as the single country study context – the UK. Evidence suggests that results may vary across different types of crowdfunding (Cholakova and Clarysse, 2015; Troise et al., 2020), and hence, future research may re-examine the identified relations in our study in both non-investment models such as reward and donation, as well as in other investment models such as crowdlending. Similarly, national context effects may be present (Cho and Kim, 2017; Shneor et al., 2021) and so, retesting of our hypotheses in national contexts different from the United Kingdom in terms of differing institutional structures, immigration levels, as well as crowdfunding market development levels may all warrant different results.

Second, future studies may also explore the effects of immigrant presence in EFTs in a more nuanced manner, as with respect to specific national backgrounds of these immigrants, when studying whether influences of immigrants are similar regardless of country of origin. Or alternatively, when examining the role of diversity within the immigrant members of EFTs, while comparing EFTs with immigrants from one national backgrounds versus EFTs with immigrants from multiple national backgrounds. Such approach can draw on findings with respect to different venture growth strategies that are preferred by ethnically different immigrant groups (Wang and Altinay, 2012).

Third, as we present evidence for the impact of the share of immigrants in EFTs and while including various controls in our analyses, new questions may emerge with respect to other potentially influential variables not captured in the current study. One important factor may be the industry or sector which ventures operate within, both because earlier research shows that industry matters for ECF campaign results (Johan and Zhang, 2022), and that immigrant entrepreneurs tend to cluster within specific industries (Kerr and Kerr, 2020). In similar spirit, future research should examine the potential effects of team characteristics such as cohesion and collaboration-orientation, and/or other sources of diversity among EFTs such as personality, gender, socio-economic background, professional and educational experiences. Inclusion of such variables may both enhance our understanding of their potential effects on ECF campaign success and venture survival, as well as more clearly capture the distinctiveness of the effects of share of immigrants in EFTs, when testing modelling that also include the above variables.

Finally, since EFTs in our sample were relatively small with two members on average, future research may explore ways for capturing larger EFTs. Our result may be the outcome of using directors as proxy for founders, as done in earlier research. However, alternative measures for team members may be considered such as manual data collection of teams presented on the campaign sites. The challenge with such practice will be in reliably identifying them as immigrants, either through related statements in campaign texts, or through supplementary survey efforts to be sent directly to fundraisers.

Conclusion

Crowdfunding can serve as a channel to help immigrant entrepreneurs in accessing finance needed for their venturing activities. By studying 1171 ECF campaigns on three UK-based platforms, the current study shows that the share of immigrants in EFTs is significantly associated with both ECF campaign goal setting, as well as its results. This relation follows an inverted U-shape, suggesting that more mixed teams set higher goals and raise more funds than homogeneous teams of either majority entrepreneurs or majority natives. Furthermore, the study also finds weak evidence for a negative association between share of immigrants in EFTs and venture survival, which is explained by greater tendencies towards undercapitalisation. Some support for this argument can be found in the fact that raising higher sums reduces likelihood of failure of ventures established by EFTs with larger shares of immigrants.

Footnotes

Appendix 1

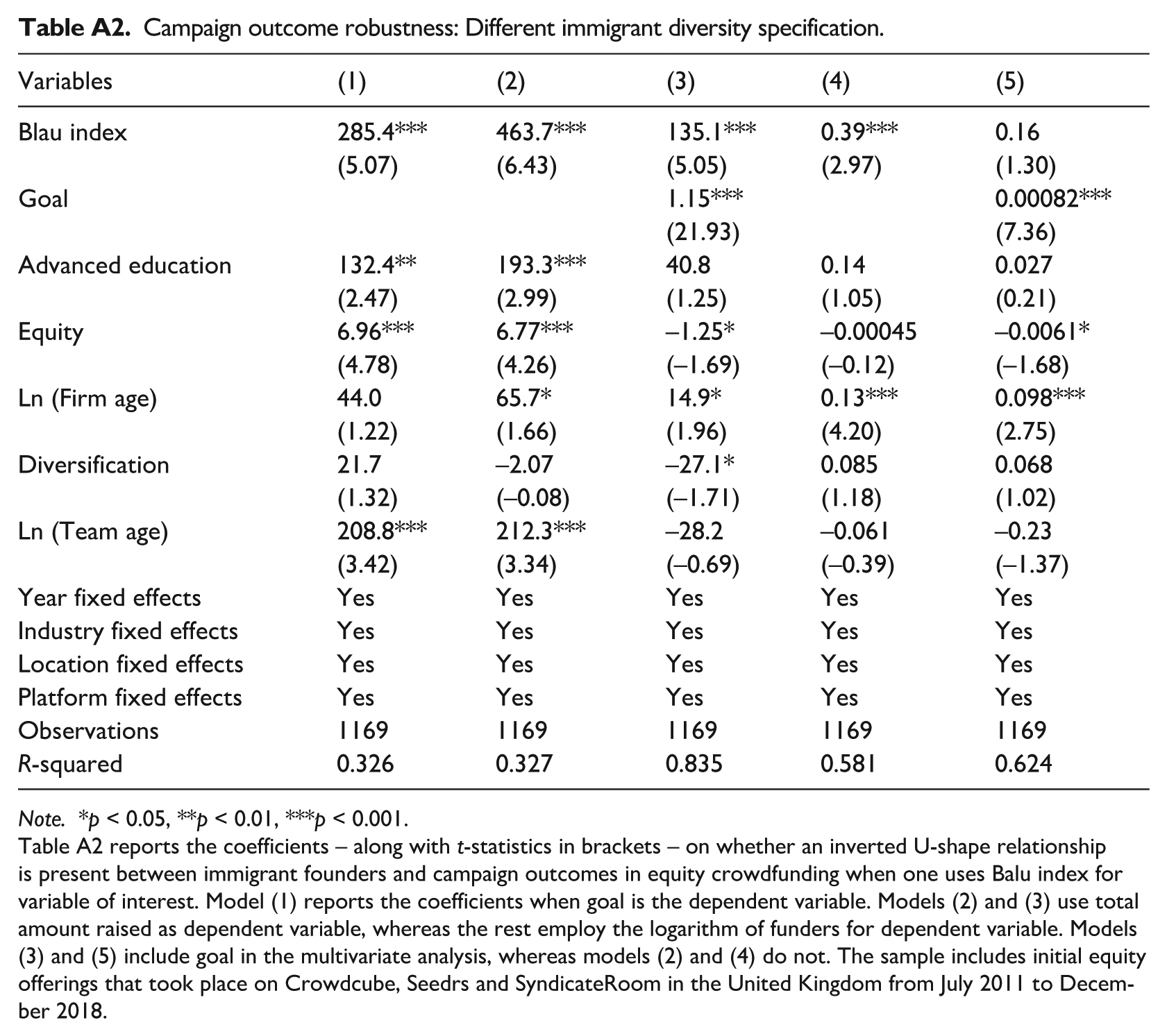

Campaign outcome robustness: Different immigrant diversity specification.

| Variables | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Blau index | 285.4*** | 463.7*** | 135.1*** | 0.39*** | 0.16 |

| (5.07) | (6.43) | (5.05) | (2.97) | (1.30) | |

| Goal | 1.15*** | 0.00082*** | |||

| (21.93) | (7.36) | ||||

| Advanced education | 132.4** | 193.3*** | 40.8 | 0.14 | 0.027 |

| (2.47) | (2.99) | (1.25) | (1.05) | (0.21) | |

| Equity | 6.96*** | 6.77*** | –1.25* | –0.00045 | –0.0061* |

| (4.78) | (4.26) | (–1.69) | (–0.12) | (–1.68) | |

| Ln (Firm age) | 44.0 | 65.7* | 14.9* | 0.13*** | 0.098*** |

| (1.22) | (1.66) | (1.96) | (4.20) | (2.75) | |

| Diversification | 21.7 | –2.07 | –27.1* | 0.085 | 0.068 |

| (1.32) | (–0.08) | (–1.71) | (1.18) | (1.02) | |

| Ln (Team age) | 208.8*** | 212.3*** | –28.2 | –0.061 | –0.23 |

| (3.42) | (3.34) | (–0.69) | (–0.39) | (–1.37) | |

| Year fixed effects | Yes | Yes | Yes | Yes | Yes |

| Industry fixed effects | Yes | Yes | Yes | Yes | Yes |

| Location fixed effects | Yes | Yes | Yes | Yes | Yes |

| Platform fixed effects | Yes | Yes | Yes | Yes | Yes |

| Observations | 1169 | 1169 | 1169 | 1169 | 1169 |

| R-squared | 0.326 | 0.327 | 0.835 | 0.581 | 0.624 |

Note. *p < 0.05, **p < 0.01, ***p < 0.001.

Table A2 reports the coefficients – along with t-statistics in brackets – on whether an inverted U-shape relationship is present between immigrant founders and campaign outcomes in equity crowdfunding when one uses Balu index for variable of interest. Model (1) reports the coefficients when goal is the dependent variable. Models (2) and (3) use total amount raised as dependent variable, whereas the rest employ the logarithm of funders for dependent variable. Models (3) and (5) include goal in the multivariate analysis, whereas models (2) and (4) do not. The sample includes initial equity offerings that took place on Crowdcube, Seedrs and SyndicateRoom in the United Kingdom from July 2011 to December 2018.

Acknowledgements

We wish to thank Prof. Armin Schwienbacher (SKEMA Business School), Dr. Simon Kleinert (Maastricht University) and Dr. Ramy Elitzur (University of Toronoto), for their feedback and suggestions helping us to develop the article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.