Abstract

Among the new ventures actively seeking funds through equity crowdfunding, only a lucky few seemingly survive the rigorous selection process imposed by equity crowdfunding platforms (ECFPs). With a conjoint experiment involving decision-makers from 50 platforms in 22 countries, this study provides first quantitative evidence regarding how ECFPs actually use quality signals to select new ventures to start fundraising campaigns. The ECFPs interpret signals differently, depending on whether they impose a co-investment requirement or generate revenues from new ventures’ long-term performance. The effectiveness of the signals also is contingent on the applicant’s industry background and the signals’ accessibility in the country where the ECFP operates.

Equity crowdfunding platforms (ECFPs) connect entrepreneurs who want to raise capital and investors who want to acquire equity shares in promising new ventures (Pollack et al., 2021). Each year, thousands of entrepreneurs apply to appear on ECFPs, but to ensure that investors select from high-quality ventures, ECFPs routinely accept less than 10% of these applications from ventures, which then may start their fundraising campaigns (Löher, 2017). Information asymmetries about the new ventures’ unobservable quality bear the crucial risk that ECFPs falsely accept low-quality ventures (Belleflamme et al., 2015). Correctly assessing the quality of each of the many applicants would require costly, in-depth due diligence (Cumming et al., 2019), and ECFPs might instead evaluate the quality of applicants based on signals sent by the new ventures (Connelly et al., 2011).

We have ample knowledge on how investors react to quality signals such as patents, prominent customers, or human capital in equity crowdfunding campaigns (e.g., Ahlers et al., 2015; Bapna, 2019; Vismara, 2016) and what contextual and investor characteristics moderate the effects of these signals (Kleinert et al., 2020; Wang et al., 2019). However, research has neglected the extent to which ECFPs account for quality signals in their own screening processes and how substantial heterogeneity in ECFPs’ environments and business characteristics (Cumming et al., 2019; Rossi et al., 2019) might moderate the effects of those signals.

The quality signals that new ventures use to overcome information asymmetry with ECFPs might be the same as those used to convince investors, because both players care about venture quality. However, substantial heterogeneity already exists in the effectiveness of signals across investors (e.g., Anglin et al., 2018; Scheaf et al., 2018). As potential signal receivers, ECFPs do not act as investors; they adopt different business models, face different risks, and likely have different decision-making processes. Whereas investors generate profits from returns on equity, ECFPs earn flat fees or percentages of successful crowdfunding campaigns (Cumming et al., 2019; Rossi et al., 2019). As two-sided markets, ECFPs’ legal responsibilities also differ (Cummings et al., 2020; Hornuf & Schwienbacher, 2017), and they encounter reputation-based network externalities (Rochet & Tirole, 2003) that create reputation risks. Failing to evaluate a venture correctly might threaten the platform as a whole, because the error cannot be hedged among the pool of all listed ventures (Belleflamme et al., 2015). Furthermore, in contrast with investors who tend to develop an industry-specific focus (Amit et al., 1998; Zacharakis & Shepherd, 2007), ECFPs receive applications from multiple industries and therefore might rely on more general evaluation processes. Thus, compared with investors, ECFPs may evaluate venture quality signals differently, and different contingencies may become influential.

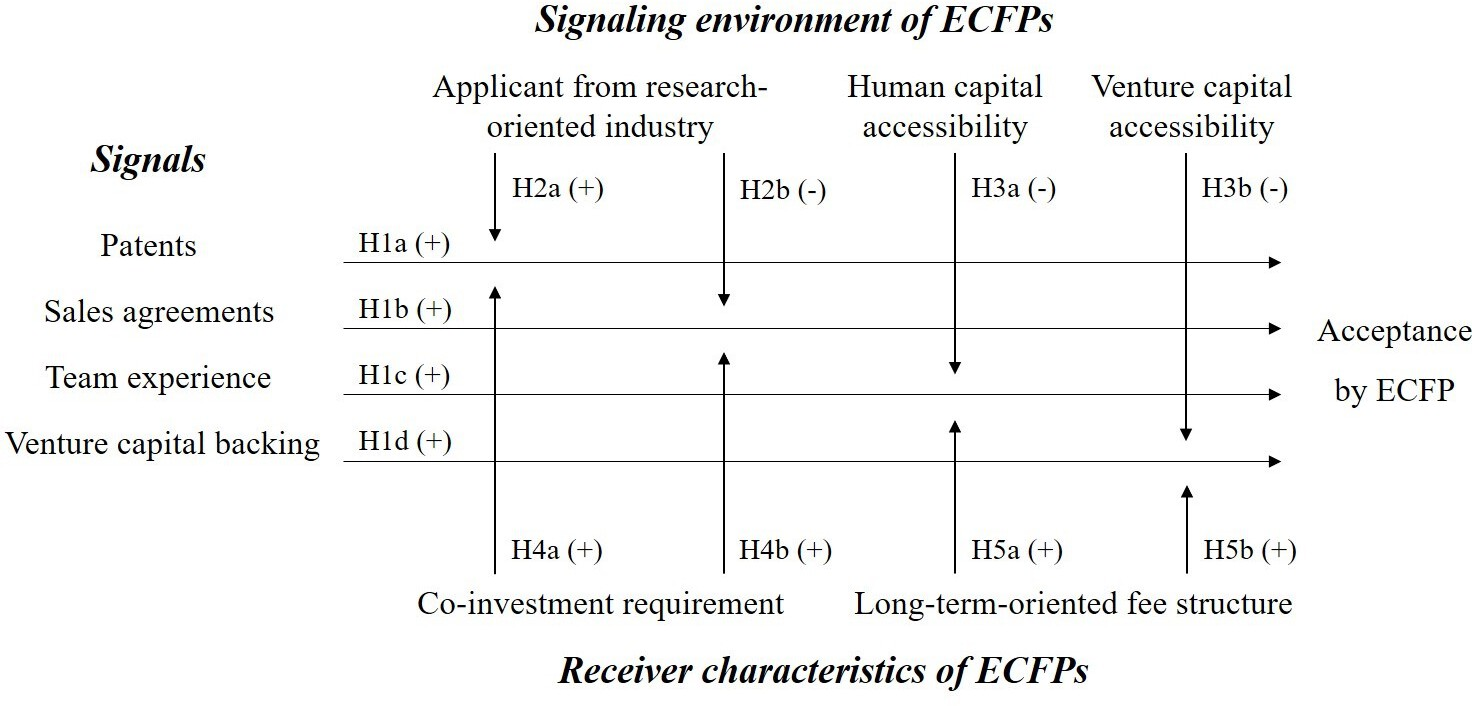

Accordingly, we draw on signaling theory to inform our analysis of how ECFPs select new ventures for funding campaigns (Spence, 1973). On the basis of practical insights gathered through websites and interviews, we apply Bapna’s (2019) framework of venture quality dimensions, as evaluated by investors, to our analysis of ECFPs. In turn, we derive four venture quality signals that are of potential relevance for ECFPs: patents, sales agreements, team experience, and venture capital backing (Baum & Silverman, 2004; Hoenig & Henkel, 2015; Ko & McKelvie, 2018; Ragozzino & Reuer, 2011). Building on Connelly and colleagues’ (2011) synthesis of key signaling concepts, we propose two sets of moderation hypotheses regarding contingencies of signal effects, related to the unique signaling environments and receiver characteristics of ECFPs.

First, we address two critical components of the signaling environment: the task environment and the institutional environment (Connelly et al., 2011). As their critical task, ECFPs evaluate ventures (Belleflamme et al., 2015) from vastly diverse industries, such as research- versus retail-oriented industries, which may evoke distinct information asymmetries (Zacharakis & Shepherd, 2007; Zacharakis et al., 2007). Even if they tend to develop generally streamlined decision rules, ECFPs may need to adjust their evaluation of new ventures to industry particularities. Furthermore, across institutional environments, ECFPs encounter varying signal accessibility (Useche, 2014), so signals might be perceived as less informative in countries in which they are easy to access. Second, we consider contingencies based on receiver characteristics that may influence ECFPs’ signal interpretation (Connelly et al., 2011). For example, ECFPs vary substantially in their co-investment requirements and fee structures (Rossi & Vismara, 2018; Rossi et al., 2019); these characteristics likely affect the importance that ECFPs attach to particular signals.

Data on real-world applications by ventures are scarce and may suffer from selection biases, so we test our predictions using a conjoint experiment (Aguinis & Bradley, 2014; Shepherd & Zacharakis, 1999). Our data include 624 venture evaluations by 78 ECFP decision-makers, representing 50 ECFPs in 22 countries. Altogether, the platforms featured in our experiment have collectively facilitated at least US$5 billion in funding for new ventures, a substantial fraction of the volume of the international ECFP market (Statista, 2019). We identify the weights that decision-makers assign to the four signals (patents, sales agreements, team experience, and venture capital backing). To test for heterogeneity in these weights, we complement the conjoint study with a randomized between-subject experiment that manipulates the industry among applicants and with data about the platforms’ business characteristics, collected from their websites, and about their country-related institutional backgrounds, collected from the World Economic Forum.

With these combined insights, this study makes two main contributions. First, we contribute to equity crowdfunding literature, with its predominant focus on campaign success (Ahlers et al., 2015; Kleinert et al., 2020; Wang et al., 2019), and provide first quantitative evidence of how new ventures can gain access to ECFPs, a precondition for any equity crowdfunding campaign. By examining the pre-campaign phase, when ventures try to secure access to ECFPs, we call attention to the multiple phases of equity crowdfunding (Pollack et al., 2021). We identify the pre-campaign phase as critical; rejection rates that average around 90% suggest that it may be even more critical to success than the campaign phase. We also advance research on ECFPs (e.g., Löher, 2017; Rossi & Vismara, 2018) by establishing that platforms differ in their screening processes in the pre-campaign phase, such that success factors may be specific to certain types of ECFPs.

Second, we add to new venture signaling research (Ahlers et al., 2015; Anglin et al., 2018; Fisch, 2019) by studying two under-researched key signaling concepts: the receiver and the signaling environment (Connelly et al., 2011). On the one hand, new venture signaling research mainly focuses on investors as signal receivers (Colombo, 2021; Connelly et al., 2011). We highlight ECFPs as a distinct signal receiver. They generally do not invest themselves, and they also feature unique, not previously studied receiver characteristics, which affect how they interpret signals. We offer initial evidence that ECFPs’ business characteristics, in terms of long-term, performance-oriented fee structures and co-investment requirements, lead them to issue different evaluations of venture quality signals. On the other hand, we establish novel insights into the signaling environment and signals’ effectiveness in different countries. Previous research, which mostly compares just a few countries, suggests that signal effects vary across countries due to regulatory or cultural differences (Bell et al., 2012; Jia & Zhang, 2014; Useche, 2014). Based on a sample of ECFPs from 22 countries, we establish that the accessibility of quality signals in an institutional context, particularly of human and venture capital, influences how effectively those signals (i.e., team experience and prior venture capital backing) influence signal receivers’ decision-making.

Equity Crowdfunding Platforms

There are three main actors in equity crowdfunding: entrepreneurs who seek funding, investors who seek investment opportunities, and ECFPs that bring entrepreneurs and investors together. We define ECFPs as active, two-sided online platforms that serve as gatekeepers for new venture applicants to regulate the equity crowdfunding process. Before deriving our hypotheses, we introduce ECFPs in more detail.

ECFPs’ Business Models

As a primary service, ECFPs provide a platform for equity crowdfunding campaigns (Belleflamme et al., 2015). With their platform-based business models (Rochet & Tirole, 2003), they create value by facilitating exchanges, so ECFPs must attract one side (e.g., investors as finance suppliers) to be attractive to the other side (e.g., entrepreneurs as finance requestors) and vice versa (Belleflamme et al., 2015). On the demand side, ECFPs typically call for ventures in their seed or growth stage (Kleinert et al., 2020). On the supply side, they often seek out unaccredited small investors as an underserved investor segment (Ahlers et al., 2015).

Their specific services, pricing models, and target customers may vary. As two-sided markets (Rochet & Tirole, 2003), ECFPs may earn revenues from one or the other side. Most existing ECFPs charge the entrepreneurial venture a variable amount, based on the funding it raises, but some platforms charge a fixed administration fee for listing ventures so that they can generate returns even on failed campaigns (Cumming et al., 2019). Other platforms (e.g., OurCrowd, Seedrs) charge investors too, such as on the basis of carried interest if the invested business thrives after the campaign and increases in value. These platforms thus generate revenues even after the funding campaign has ended.

The main target of ECFPs are unaccredited investors, yet approximately 21% of ECFPs also demand at least one additional accredited co-investor in the planned fundraising campaign (Rossi et al., 2019). These co-investors are high net worth individuals or sophisticated investors, such as business angels, who invest at the same time and under the same conditions as unaccredited investors. Co-investors use their expertise to evaluate the venture and possibly support the entrepreneur with advice or network access after the campaign. In this sense, they enhance the investment opportunity’s credibility in the eyes of unaccredited investors (Agrawal et al., 2016). Typically, the value proposition of ECFPs with co-investment requirements is to offer safer investment opportunities—that is, higher quality ventures.

ECFP–Venture Interactions in the Pre-Campaign Phase

The focus of our study is on the pre-campaign phase of ECFPs, in which they select new ventures to include on their platform. The pre-campaign phase roughly consists of three subphases before final admission to the platform: deal sourcing, deal assessment, and deal structuring (Löher, 2017). During deal sourcing, entrepreneurs usually apply directly through an ECFP’s website, typically with a business pitch deck, but they also might rely on the ECFP’s network or referrals from investors. The number of applications that platforms receive varies but routinely exceeds several thousand per year (e.g., Löher, 2017; our own interviews 1 and website information support this estimate). Then, in the deal assessment phase, ECFPs screen and evaluate the applications according to formal criteria, such as completeness or overall impression, as well as in relation to specific quality dimensions, such as market potential, team, or business model (as reported by the Seedmatch and Republic platforms, as of January 2021). If the start-up achieves good fit with the platform, then ECFPs typically conduct legal due diligence, including independent research to validate statements in the applications. A positive assessment leads to deal structuring, during which platforms and entrepreneurs negotiate terms about, for example, participation rights, the type of investment, and company valuation (Löher, 2017). If they agree, the campaign commences. Relatively few applicants are approved; according to prominent ECFPs’ websites, for example, OurCrowd only selects 1% to 2% of applicants, Companisto 1%, and Republic 2.5%. Overall, the pre-campaign phase thus is critical for ECFPs, and it ultimately influences the success of new ventures’ efforts to raise capital through equity crowdfunding.

Information Asymmetries Between New Ventures and ECFPs

The presence of information asymmetries between new ventures with superior information about their industriousness, track records, and economic potential (e.g., Ko & McKelvie, 2018; Leland & Pyle, 1977; Stuart et al., 1999) and less sophisticated, unaccredited investors that lack such information is well-known (Ahlers et al., 2015). Mitigating such information asymmetries is legally required from ECFPs and a critical function to build a high reputation among potential investors (Belleflamme et al., 2015; Cumming et al., 2019). The continuously increasing success rates of equity crowdfunding campaigns suggest that ECFPs are getting better in fulfilling this function (Ralcheva & Roosenboom, 2019).

Historically, equity crowdfunding has been prohibited in many countries because of the substantial information asymmetries between unaccredited investors and securities issuers (e.g., new ventures). In the United States, equity crowdfunding became legal only with the 2012 Jobs Act (Title III) and is now regulated by the U.S. Securities and Exchange Commission. Even when allowed, ECFPs must fulfill clearly defined responsibilities (Cumming et al., 2019), such that they must perform specific investor education duties, be authorized by law (Hornuf & Schwienbacher, 2017), disclose their fee structure (Cummings et al., 2020), and provide investor discussion boards (Kleinert & Volkmann, 2019). The European Parliament also has clear regulations in place, with the primary objective of protecting investors, such that ECFPs are obligated to engage in a professional and transparent selection procedure (EC, 2020). If they fail to reduce information asymmetry for each venture they list, they put their licenses and businesses at stake.

Beyond the legal burden, ECFPs experience reputation-based network externalities (Rochet & Tirole, 2003), so a failed campaign not only lowers their financial returns but also threatens their reputation among potential investors (Bouvard & Levy, 2018), which in turn makes them less attractive to more profitable ventures (Belleflamme et al., 2015). Then, less profitable ventures with higher debt levels might become more prevalent on these ECFPs (Walthoff-Borm et al., 2018), creating a potential downward spiral into a market of lemons (Akerlof, 1970). A strong reputation for providing good, qualified investment opportunities is as vital to ECFPs as the financial returns they earn from successful campaigns (Belleflamme et al., 2015).

Despite the strong incentives to select only high-quality ventures, ECFPs cannot afford to undertake costly evaluations for every applying venture (Cumming et al., 2019; Löher, 2017). Even when ECFPs hire expert reviewers and may request further information, the vast numbers of applications (i.e., the selection rate implies that they evaluate up to 100 times as many ventures as most investors) prohibit them from conducting detailed, fully fledged due diligence on each venture. They instead select ventures based on incomplete information (Belleflamme et al., 2015), initially gathered from the pitch decks. As a deal flow manager explained, “so for us, it’s important that start-ups directly present themselves in their best way; we only have a certain amount of time designated to each application and try to streamline this process as much as we can.” Accordingly, new ventures must find ways to demonstrate their quality and overcome information asymmetries with ECFPs.

Hypotheses Development

Signaling Theory in Entrepreneurial Finance

Signaling theory (Spence, 1973) is a frequently applied theoretical lens to study how insiders can inform outsiders about their unobservable quality. For example, new ventures and entrepreneurs know more about their quality than outsiders, such as investors or ECFPs. Ventures can resolve this information asymmetry by transmitting credible signals, in the form of observable and costly activities or attributes that provide information about ventures’ unobservable qualities (Connelly et al., 2011). High-quality ventures are more likely than low-quality ventures to be able and willing to obtain costly signals. Therefore, costly signals correlate with unobservable quality and eventually facilitate a separating equilibrium in which new ventures that send signals outperform ventures that do not (Bergh et al., 2014; Spence, 1973).

Connelly et al. (2011) suggest that the effectiveness of signals can depend on the signaler, the specific signals, the signaling environment, and the receiver. The latter two have received less attention from researchers. Environment refers to the context, either within or between organizations, and it can affect the severity and firm-specific relevance of information asymmetries. Receivers are outsiders who are supposed to react to signals, and they may differ in how they interpret and eventually react to signals. Signaling theory has been applied extensively to explain how investors such as venture capitalists, initial public offering (IPO) investors, and crowdfunders react to signals such as affiliations with partners, reputation, or top management team characteristics (e.g., Colombo, 2021). For investors, as signal receivers, the effectiveness of signals is moderated by environments, such as the industry of the new venture (Hsu, 2007) or the regulations in the new venture’s country of origin (Bell et al., 2012). Furthermore, different investors interpret the same signals differently; patents are interpreted differently by backers in reward crowdfunding versus investors in equity crowdfunding (Scheaf et al., 2018), and signals about coachability evoke different interpretations by experienced versus unexperienced business angels (e.g., Ciuchta et al., 2018).

Signals for ECFPs

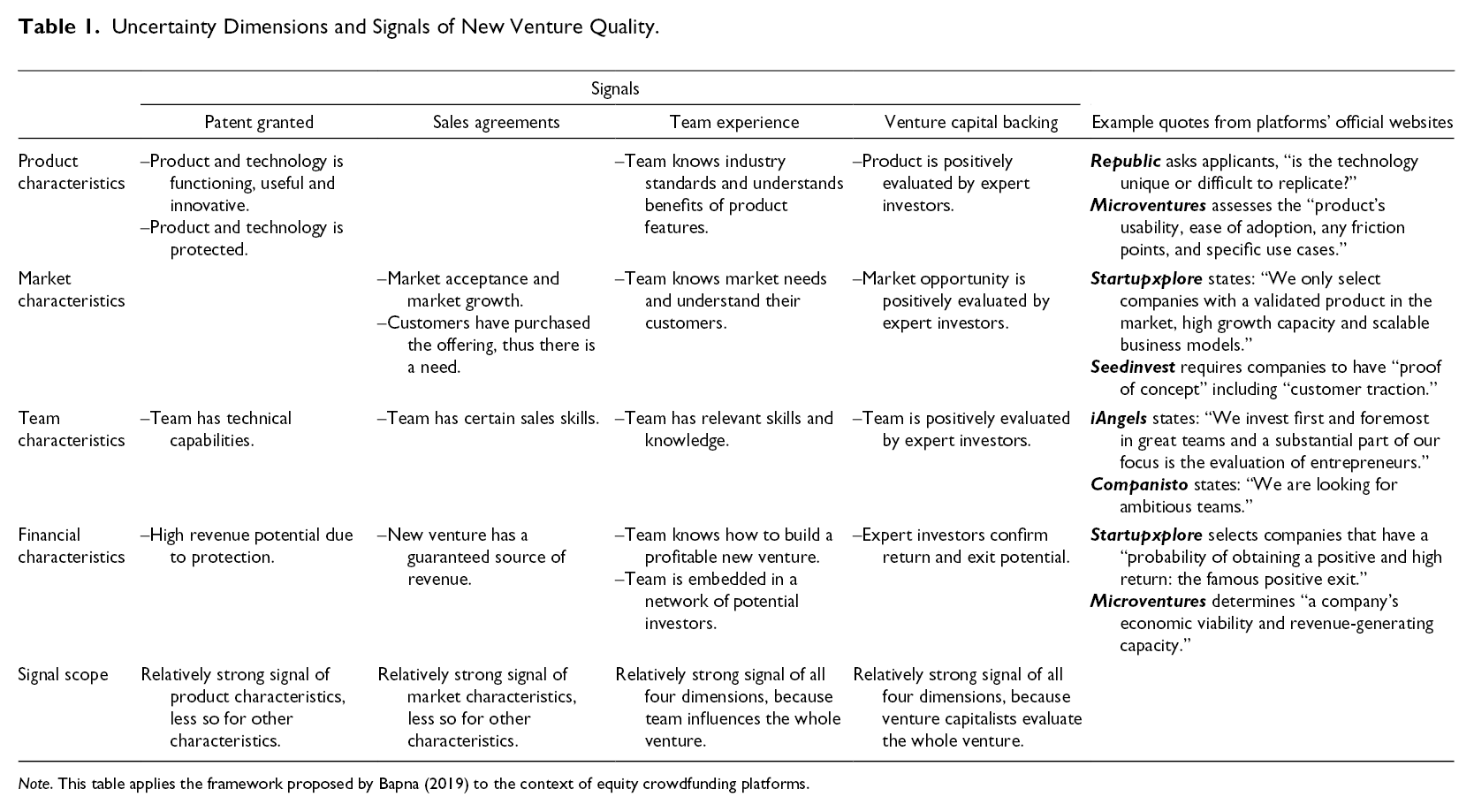

Noting the lack of research on venture signaling toward ECFPs as receivers, we first identify quality signals of potential relevance. According to new venture financing research, uncertainty about new venture quality, and thus information asymmetry, relates to four main dimensions: product, market, team, and financials (e.g., Petty & Gruber, 2011). These dimensions also appear in Bapna’s (2019) framework of signals for investors. Product characteristics refer to whether a new venture has a functioning, differentiated, protected product that meets industry quality standards. Market characteristics involve questions about sufficiently sizable market opportunities, possible entry barriers, and addressed customer needs. Team characteristics pertain to the team’s entrepreneurial skills and relevant experience. Finally, financial characteristics might include returns on investment and future exit potential for a new venture.

As confirmed by the ECFPs’ own websites, 2 qualitative evidence by Löher (2017), and our interviews, ECFPs consider these four uncertainty dimensions when selecting applicants in the pre-campaign phase. Signals sent by new ventures to ECFPs thus should attempt to address uncertainties about the product, market, team, and financials. Extending Bapna’s framework of quality signals for investors to the analysis of ECFPs, we can link the four uncertainty dimensions to four well-established signals: patents, sales agreements, team experience, and venture capital backing (Baum & Silverman, 2004; Hoenig & Henkel, 2015; Ragozzino & Reuer, 2011). Using selected quotes from ECFPs’ websites, in Table 1 we illustrate the relevance of the four dimensions for ECFPs and the respective signals.

Uncertainty Dimensions and Signals of New Venture Quality.

Note. This table applies the framework proposed by Bapna (2019) to the context of equity crowdfunding platforms.

Patents are credible because they are visible in publicly available databases, and they also involve direct (e.g., application fees) and indirect (e.g., R&D) costs (Fisch, 2019). They mainly signal the product and technological quality of new ventures and their innovativeness; by definition, a granted patent means that a patent officer regarded the new venture’s product and technology as new, useful, and non-obvious (Hoenig & Henkel, 2015). However, they are weaker signals of market quality because they do not reveal whether customers value the proposed product (Roma et al., 2017), and occasionally, patents are granted to technologies without market applications (Scheaf et al., 2018).

Sales agreements with a reputable partner also are visible (Baum & Silverman, 2004), because they likely result in some form of a written agreement that is often promoted to outsiders (Hoenig & Henkel, 2015). Sales agreements are costly (Stuart et al., 1999), in that incumbent companies are unlikely to enter into a sales agreement with insufficiently committed low-quality start-ups. Compared with patents, sales agreements provide less information about the product (e.g., differentiated, protected, well-functioning). Sales agreements may indirectly reduce information asymmetries about the venture’s future revenues, but they do not necessarily signal information about other financial characteristics, such as exit potential (Bapna, 2019). Instead, sales agreements with a reputable partner are primarily market signals (Roma et al., 2017) that provide information about current market demand and established market access.

Team experience is a costly and visible quality signal (Ko & McKelvie, 2018). It generally is included in the team description in entrepreneurs’ pitch decks. Compared with low-quality start-ups, high-quality start-ups can recruit experienced team members with less cost and effort (Hoenig & Henkel, 2015). Team experience addresses multiple information asymmetry dimensions (Bernstein et al., 2017). The existence of a team of serial founders with relevant industry experience represents information about team-related characteristics. It also reduces information asymmetries about future market potentials because experienced teams can better identify unmet customer demands and opportunities that others might not see (Westhead et al., 2005). Founding and industry experience further reduces information asymmetries related to financial characteristics, in that serial entrepreneurs know how to build a viable new business (Hsu, 2007).

Finally, venture capital backing functions as a credible signal of firms’ unobservable qualities (Ragozzino & Reuer, 2011). When raising new equity capital, ventures have to announce the composition of other shareholders publicly. It is also costly because reputable venture capitalists do not risk their reputations by affiliating with low-quality firms, and founders usually must give up some of their entrepreneurial residual rents to them (Hsu, 2004). Before investing in a start-up, a venture capitalist undertakes due diligence to assess the product, market, team, and exit potential (Petty & Gruber, 2011), so existing venture capital backing provides likely signals about every relevant dimension of new venture quality (Bapna, 2019).

The following hypothesis summarizes our discussion so far and establishes baseline relationships for examining how ECFPs’ signaling environments and receivers’ characteristics affect their relative influences.

Signaling Environment of ECFPs

The signaling environment includes the task environment and the institutional environment (Connelly et al., 2011). It affects the presence and salience of information asymmetries, which may be mitigated by signals as well as the strength of the signal, that is, the degree to which it correlates with unobservable quality and thus can mitigate information asymmetries (e.g., Useche, 2014).

Task Environment

To reach a sufficient scale as doubled-sided markets, ECFPs often allow and evaluate applications from all kinds of industries. Thereby, they differ from investors who typically specialize in single industries (Amit et al., 1998; Zacharakis & Shepherd, 2007) and use specialized knowledge to evaluate firms based on industry-specific signals (Fisch, 2019; Zacharakis & Shepherd, 2007). The ECFPs’ streamlined decision-making processes might generally not allow for the attribution of varying importance to quality signals depending on the venture’s industry background. Yet, ECFPs may deviate from such streamlined decision-making processes for ventures from fundamentally different industries to increase their appeal for investors. Research-oriented and retail-oriented industries, which both appear on equity crowdfunding platforms, 3 constitute such extreme cases (Zacharakis & Shepherd, 2007), and we expect differences with respect to the key task of ECFPs, that is, venture quality evaluations.

Information asymmetries arise in both research- and retail-oriented industries, but the specific types differ. Ventures in research-oriented industries (e.g., biotech, life sciences) encounter greater R&D risks, complex technologies, and lengthy development processes, such that information asymmetries tend to relate to their product and technological characteristics (Fisch, 2019; Urbig et al., 2013). In contrast, information about the accessibility to key markets might be more relevant for new ventures in retail-oriented industries (Kotler et al., 2016). These ventures typically do not face high-tech barriers but must attract sufficient market demand and sales early in their development (Trester, 1998). Therefore, ECFPs may assign distinct relevance to quality signals that address product versus market information asymmetries, according to the applying venture’s industry background. Among the four signals, we consider patents are the primary tool for addressing product issues (Fisch, 2019; Hoenig & Henkel, 2015), and the sales agreement mainly addresses the market dimension (Bapna, 2019; Roma et al., 2017). The remaining two signals do not align with particular dimensions of information asymmetry and may be equally relevant across diverse industries. Acknowledging the variation in the salience of particular dimensions of venture quality, we predict that patents have a more positive effect when ECFPs evaluate ventures from research-oriented industries, but sales agreements have a more positive effect for ventures from retail-oriented industries.

Institutional Environment

The institutional environment affects not only the emergence and prevalence of crowdfunding (e.g., Rau, 2020) but also related signaling processes, especially across different countries (Bell et al., 2012; Useche, 2014). Costlier signals tend to be more effective (Bergh et al., 2014; Spence, 1973), and the accessibility of signals constitutes a fundamental cost driver that may vary across institutional environments. Furthermore, ECFPs’ perceptions of how easily new ventures can access signals might affect their judgments of these signals’ credibility. 4 For our discussion, we focus on team experience and venture capital backing as heterogeneously accessible signals. In contrast, national and international patent offices make patents equally and widely accessible, and bilateral sales agreements are unlikely to be strongly influenced by country-specific institutions.

Team experience signals might be more or less accessible, depending on how difficult it is for new ventures to invite experienced team members to join them. In developing countries, access to skilled labor is limited because educated, skilled labor often emigrates to more developed countries with better job markets (Beine et al., 2008). In countries where skilled labor is abundant, new ventures can recruit experienced team members more easily, and even lower quality new ventures might have relatively easy access to a good team. Therefore, ECFPs operating in countries with less access to skilled labor may perceive team experience as a stronger signal than ECFPs from countries with better accessibility.

Venture capital accessibility also differs across institutional environments. For example, the United States is the most developed venture capital market, so it is easier for new ventures to raise venture capital there than in France for example (Milosevic, 2018). We also note considerable variation across emerging nations: good venture capital accessibility in Brazil, Poland, and Malaysia but weak accessibility in Argentina and South Africa (Chemmanur et al., 2016). More difficult access creates a stronger distinction between high-quality and low-quality ventures, such that only the very best ventures likely attract venture capital (Bergh et al., 2014). Accordingly, ECFPs’ perception of venture capital backing as a signal likely depends on the perceived accessibility of venture capital in their respective countries.

Receiver Characteristics of ECFPs

Differences among receivers constitute a central element in explaining how signals are interpreted (Connelly et al., 2011). We consider two particularly relevant receiver characteristics that are likely to influence ECFPs’ evaluations of quality signals and that are unique to ECFPs compared with investors: co-investment requirements and fee structure (Rossi & Vismara, 2018; Rossi et al., 2019).

Co-Investment Requirements

If ECFPs require the involvement of a professional investor as a condition for listing new ventures, they tend to offer a unique value proposition by providing safer and less risky investment opportunities (Agrawal et al., 2016). Supporting this perspective, the Spanish ECFP Startupxplore advertises on its website “invest in […] companies with high growth potential, in an easy and safe way,” in which “quality comes before quantity.” That is, ECFPs with co-investment requirements likely put more emphasis on quality signals such as patents, sales agreements, team experience, and venture capital backing in their selection of new ventures. The importance of these four quality signals might be further leveraged because ECFPs with co-investment requirements also need to attract accredited investors as an additional investor group to their site. These accredited investors have particularly high expectations about new venture quality because of the reputational and financial penalties of investing in poorly performing ventures (Agrawal et al., 2016).

The previous argument suggests that all four quality signals gain importance, but this gain might be particularly prominent for patents and sales agreements and less so for team experience and venture capital backing. A required co-investor may become actively involved in a new venture, which would reduce uncertainties about the venture’s future development (Agrawal et al., 2016). A co-investor contributes experience and supports the founding team with strategic advice (Colombo & Grilli, 2005; Hsu, 2006) and might thus substitute for the team experience signal. Co-investors may also provide a third-party endorsement of the new venture’s overall quality (Guerini & Quas, 2016), partly substituting for the venture capital backing signal. In this sense, the co-investor might be redundant, as a signal, with team experience and venture capital backing, which might decrease the relevance of these two signals (Steigenberger & Wilhelm, 2018) for ECFPs with co-investment requirement. However, co-investors cannot create accomplishments for the new venture ex post, such as patents or previous sales agreements. Patents and sales agreements focus on past achievements, linked to a product’s technology and market access, so they exhibit less redundancy and are more likely to complement the presence of a co-investor (Fisch, 2019; Hoenig & Henkel, 2015). In summary, ECFPs with co-investment requirements likely attach more relevance to patents and sales agreements, rather than to all four signals.

Fee Structure

Depending on their fee structures, some ECFPs generate returns primarily from short-term–oriented fees, such as from listing new ventures, but others generate revenues primarily from long-term–oriented fees, such as the performance of new ventures that have received financing (Cumming et al., 2019). 5 We argue that ECFPs with long-term–oriented fee structures attach more weight to team experience and venture capital backing as quality signals. Fees related to the long-term success of new ventures create financial incentives for such ECFPs to identify new ventures that are likely to be acquired or undergo an IPO. We accordingly expect them to pay more attention to signals that reduce uncertainties about (long-term) future success. Patents and sales agreements reduce specific uncertainties about a differentiated product and established market access at the time of the application to the ECFP, but these past accomplishments have less predictive power related to whether the product is competitive and market demand will exist in the future. In contrast, team experience and venture capital backing reduce broader forms of uncertainty (Table 1) and are more closely related to the future exit potential of a new venture and long-term performance (Bernstein et al., 2017; Guerini & Quas, 2016; Hsu, 2006). More experienced teams have better entrepreneurial judgment, make more effective strategic decisions, and use their knowledge to react to competitors’ moves (Colombo & Grilli, 2005). Venture capitalists typically provide the new venture with operational and strategic guidance, which increases its chances of an IPO or acquisition (Hsu, 2006). For instance, new ventures funded through equity crowdfunding with a more experienced management team and qualified investors, such as venture capitalists, have greater chances to raise follow-on funding or exit (Hornuf et al., 2018; Signori & Vismara, 2018). In sum, ECFPs with a more long-term–oriented fee structure are more likely to put more emphasis on team experience and venture capital backing as quality signals than do ECFPs with short-term–oriented fee structures.

Figure 1 summarizes all our hypotheses.

Overview of hypotheses. Note. ECFP = equity crowdfunding platform.

Method

To ensure the internal validity of our multilevel analysis of the influence of ventures’ signals on platforms’ decision-making, we conduct a metric conjoint analysis 6 (Aguinis & Bradley, 2014; Shepherd & Zacharakis, 1999), as recommended for multilevel entrepreneurship research (Shepherd, 2011). We employ a passive participation design in which participants are real-world decision-makers but make hypothetical decisions (Hsu et al., 2017). Conjoint analyses are widely used in entrepreneurship research (Lohrke et al., 2010), especially for studies of entrepreneurial finance providers’ decision-making (Drover et al., 2017; Warnick et al., 2018). Conjoint analysis can address introspection biases associated with post-hoc methods and problems related to the unobserved heterogeneity arising from different platforms evaluating different projects. Participants assess predefined profiles (venture applications) with varying attributes, and the systematic variation of these attributes enables the identification of the relative importance of different criteria.

We use moderation analyses to test our hypotheses about how the effects of the four signals depend on other variables. For all the moderators, we sought to reduce the influence of experimenter demand effects and common method variance associated with within-subject treatment comparisons (Gerber & Green, 2012; Williams et al., 2019). Industry, as a critical moderating variable, varies randomly and exogenously among participants. Availabilities of human and venture capital as country-level variables come from an independent secondary data source, the Global Competitiveness Report from the World Economic Forum. Finally, the moderators related to the platform business were collected directly from the platforms’ web pages. Thus, all the moderating variables are independent of participants’ responses to the conjoint analysis or other parts of the survey instrument.

Sample

To attain a globally diverse sample of ECFP decision-makers involved in their respective platforms’ selection processes, we first identified suitable platforms for investigation, using various sources. The Crunchbase database provides rich information about early-stage investments and transactions (e.g., Signori & Vismara, 2018; Yu, 2020). We searched the database with the following keywords: “equity crowdfunding,” “crowd investing,” and “investment platform,” along with the industry filters “crowdfunding” AND “finance,” and “funding platform.” We also performed web searches with the search term “platform” and one of the following keywords: “equity crowdfunding,” “crowd investing,” or “investment crowdfunding.” We searched for platforms with webpages in English only, to avoid linguistic distortion in the research process (Köhler et al., 2017). In addition to Crunchbase and the web search, we looked at registries, including all the European registries used by Rossi and Vismara (2018), such as the CONSOB registry (Italy) and the ORIAS registry (France), along with the U.S. Financial Industry Regulatory Authority, because the United States is a critical location for equity crowdfunding.

We used several filter criteria to decide whether to include each ECFP in our sample. In contrast with crowdfunding platform studies by Meoli et al. (2020), Rossi et al. (2019), and Rossi and Vismara (2018), we do not consider securities-based crowdfunding in general but equity crowdfunding in particular. To maintain the fit between our theorizing and empirical approach, we exclude debt-based crowdfunding and focus exclusively on platforms that offer equity or equivalent compensation forms (e.g., returns based on the new venture’s profit). Furthermore, in contrast with Meoli et al. (2020), we concentrate on platforms that facilitate the financing of new ventures, excluding those for real-estate projects that likely rely on different evaluation processes. To ensure the external validity of our conjoint study, we also confirmed that decision-makers, at the time of inquiry, faced daily decisions about accepting new ventures; that is, we only include active, still-operating platforms that had investment options on their websites at the time of the study (early 2019). In total, we identified 113 active ECFPs that fulfilled these identification criteria.

To identify relevant decision-makers involved in the screening processes, we leveraged insights gained from interviews with ECFPs and job descriptions on LinkedIn, which indicated people in positions that typically participate in ECFPs’ screening decisions: deal-flow managers, venture analysts, investment associates, due diligence associates, or auditors. We considered similar job titles, and both founders and C-level managers, who tend to be involved in all business processes. With these criteria, we checked the ECFPs’ webpages for email addresses, then visited their profiles on the professional social network LinkedIn. We retrieved more than 90% of all contacts used in this study from LinkedIn, including 603 people employed by the 113 focal ECFPs. From May to August 2019, we contacted all potential respondents via email or LinkedIn and invited them to participate in our study, sending two reminders to each potential participant. Overall, 94 people agreed to participate, and 83 participants from 53 different platforms completed the entire survey (individual-level response rate 14%, platform-level response rate 47%). To ensure respondents were involved in screening, we included two validation questions. All the respondents affirmed that their platforms engaged in quality assessment, but we removed five respondents (which removed three platforms) who indicated they were not personally involved. Our sample of 78 decision-makers meets the size requirements set by Shepherd and Zacharakis (1999) and is comparable with samples in other studies that use conjoint analysis to investigate decision-making by early-stage investors (Drover et al., 2017; Murnieks et al., 2011; Shepherd et al., 2003).

Among the analyzed decision-makers, 83% were men, which corresponds to prior studies in the venture capital industry (Drover et al., 2017; Murnieks et al., 2011). Respondents indicated a range of experience with start-up financing. Whereas 16% of respondents were new to it, with less than 1 year of experience, about 40% had more than 5 years’ experience. In their job positions, most participants were deal-flow managers (or similar job titles, 37%), followed by co-founders and CEOs (33%) and higher management personnel (12%). The majority of respondents were from Europe (60%), followed by North America (15%) and Australia (10%). Among the 22 countries, 7 the highest country-level representation was England (22%), followed by the United States (15%). The equity crowdfunding market is still young, with the first platforms emerging in the 2010s, and accordingly, the average age of the platforms is relatively low (5 years), with a range from 1 to 12 years. A few platforms have more than 50 employees (6%), but the majority are medium (11, 30 employees, 46%) to small (fewer than 10 employees, 40%) in size. According to the websites of 38 sampled ECFPs, they jointly accounted for US$5 billion in funding for new ventures by 2020; 12 ECFPs did not publish this information.

Around 28% of the investigated ECFPs rely on co-investment models, slightly above the 21% that Rossi et al. (2019) find, indicating that such models might be growing in popularity (Agrawal et al., 2016). The sampled platforms are also heterogeneous in their fee structures. Beyond variable fees, around 48% of sampled ECFPs generate revenues from listing new ventures, and 24% are compensated if investors earn money. At the country level, we observe differences in human capital availability, with Romania ranking lowest and the United States ranking highest. Venture capital availability also varies across the countries. Similar to Chemmanur et al. (2016), we observe that the United States and Israel have particularly well-developed infrastructures for venture capital, whereas its accessibility is poor in Italy.

Research Instrument

The design of our conjoint study follows established practices (Murnieks et al., 2011; Shepherd et al., 2003; Wood et al., 2014). During an interactive, web-based process, we provided participants with profiles of eight hypothetical start-ups that differed on the four focal attributes, at two levels each. The chosen, well-established,

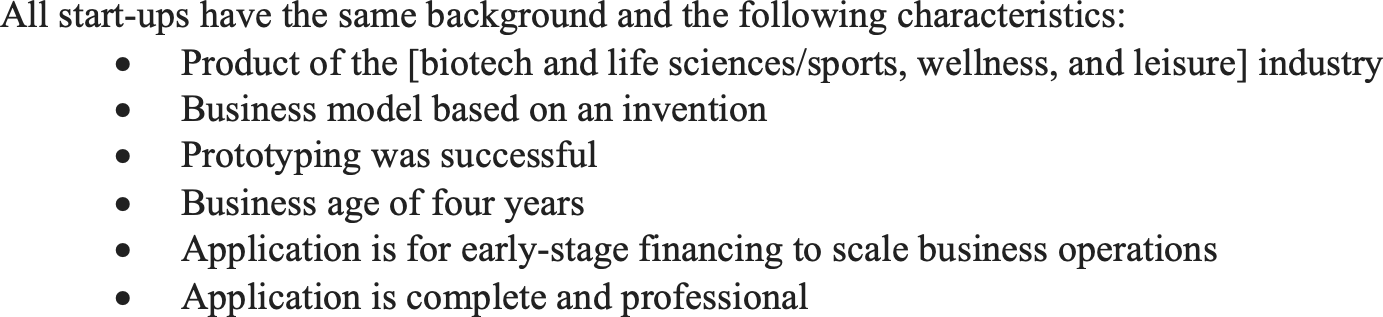

To facilitate a credible interpretation of the results, we developed a reference scenario and informed participants that the applying ventures did not differ on these general characteristics (Figure 2). In line with previous studies (Murnieks et al., 2011), we determined these general criteria through pretests and interviews with three equity crowdfunding research experts and three ECFP decision-makers from different countries. For example, based on a recommendation from the interviews, we added a statement related to the application’s completeness and professionalism, a component that is often a deal-breaker.

Reference setting. Note. This is the reference scenario presented to respondents. Only the industry differed across participants, but never for different profiles evaluated by the same participant.

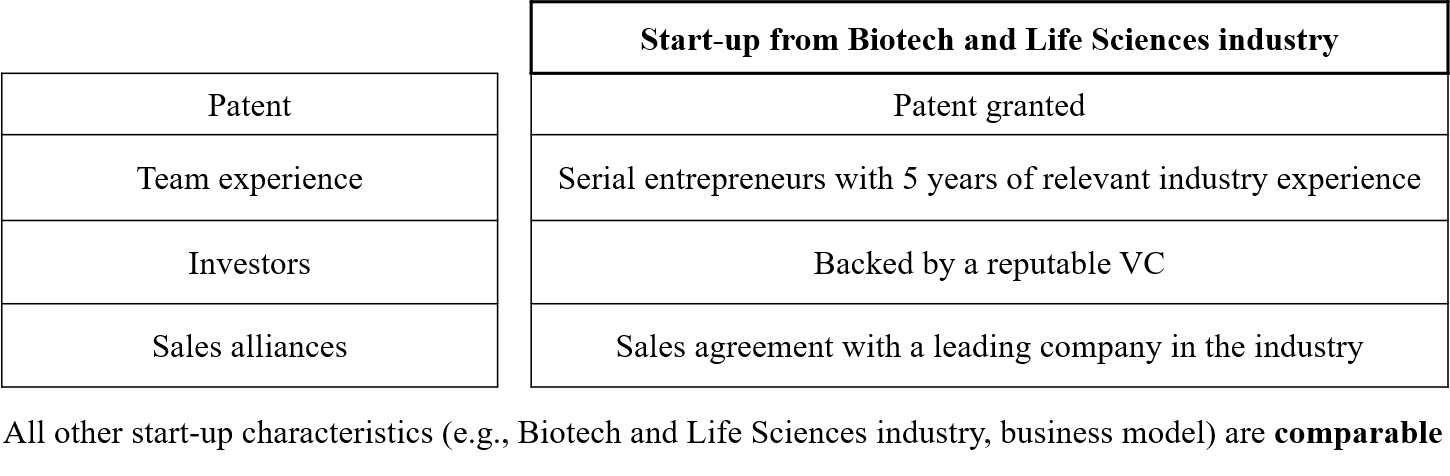

The presented profiles differed on the four attributes: patents, sales agreements, team experience, and venture capital backing. For the first two attributes, we simply manipulated the presence or absence of a patent granted (Baum & Silverman, 2004; Hoenig & Henkel, 2015) and a sales agreement with a leading company in the industry (Bapna, 2019; Hoenig & Henkel, 2015). For team experience, we manipulated entrepreneurial experience by referring to serial entrepreneurs and industry experience by citing 5 years’ experience as a threshold (Hoenig & Henkel, 2015). Finally, we operationalize venture capital backing according to whether reputable venture capitalists had previously backed the venture (Bernstein et al., 2017; Guerini & Quas, 2016). Table 2 provides an overview of the attributes and attribute levels; Figure 3 illustrates an exemplary venture profile.

Example profile. Notes. Attributes have high levels in this example. The industry description differed according to the survey version.

Attributes and Levels.

Variables

Dependent Variable

Participants evaluate the likelihood that a venture would be accepted for fundraising on their platform (Acceptance), using the following prompt: “What is the likelihood that you would allow the start-up to start a campaign on your platform?” In line with prior conjoint studies (Drover et al., 2017; Warnick et al., 2018), participants responded on a seven-point scale from “very unlikely” (1) to “very likely” (7). 9

Moderators

The industry was part of the reference scenario in the conjoint analysis. “Biotech and life sciences” represents a natural candidate for a research-oriented industry (Hoenig & Henkel, 2015). In choosing the alternative industry, we had to ensure that the signals would still make sense and that equity crowdfunding is used in this industry. We solicited input on this design choice from the experts during the pretests and selected “Sport, wellness, and leisure” as a retail-oriented business segment that meets the necessary criteria. 10 The random assignment resulted in 41 participants assigned to the sport, wellness, and leisure industry and 37 participants to the biotech and life sciences industry, which exceed the minimum of 20 participants per group recommended by Simmons et al. (2011). In our analysis, the research-oriented industry is the treatment, and the retail-oriented industry is the reference group.

Data on the availability of human and venture capital are taken from the Global Competitiveness Report from the World Economic Forum. World Economic Forum data have been used frequently in previous research, due to their credibility (Acs & Amorós, 2008; Rau, 2020). These data are particularly suitable to test our Hypotheses 3 and 4, because they present a representative picture of how business executives perceive the accessibility of different types of capital in their countries. For this study, we obtain the Global Competitive Index for 2019, the year of our data collection. Human capital availability is the country average of responses to a question about the possibility of finding skilled employees, ranging from 1 (“not at all”) to 7 (“to a great extent”). Venture capital availability is the country-level average of responses to a question about the ease of finding venture capital, from 1 (“extremely difficult”) to 7 (“extremely easy”). We center these variables so that the signals’ main effects describe the effect for average levels of human and venture capital availability (Cohen et al., 2013).

Using information collected from the platforms’ webpages or requested from the platforms’ customer support, we assign co-investment requirement a value of 1 if the platform requires a registered co-investor before a venture initiates a campaign (and 0 otherwise). Long-term fee orientation represents an index of two elements, reflecting opposing extremes on the long- versus short-term orientation continuum. Fixed fee emphasizes short-term outcomes and indicates whether (1) or not (0) a platform requires a fixed fee to list a campaign. Post-campaign fee reflects a long-term performance orientation indicating whether (1) or not (0) the platform receives a fee based on the returns that investors earn when their investment object increases in value, such as by raising another round of funding, being acquired, or undertaking an IPO. 11 We combine these two elements into an index, Long-term fee orientation, which equals the Post-campaign fee minus Fixed fee. The index ranges from −1 to +1, and more positive values reflect a more long-term performance–oriented incentive structure. In a robustness check, we also split this index into its two elements.

Control Variables

We included the platform age (collected from LinkedIn, Crunchbase, and platform webpages). Following the conjoint analysis, the survey issued questions related to additional control variables and to variables used for validity checks. We asked for the number of employees of their platform, according to the following classes: 1–5, 6–10, 11–20, 21–30, 31–40, 41–50, 51–100, or more than 100. To simplify the analysis and increase its power, we transformed the responses into metric variables, assigning each respondent the mean of the selected class (for two cases in the highest class, we assigned a value of 101). Multiple responses from participants from the same platform were averaged to form a platform-level variable. As controls at the respondent level, we asked for gender (female dummy), whether they were the founder or the CEO of the platform business (dummy), and whether they had more than 5 years’ “experience in start-up financing (e.g., through working for crowdfunding platforms, as venture capitalist, as business angel, working in private equity...).” We also included two individual-level control variables derived from the research design: whether the respondent answered after (1) or before we sent reminders (0) 12 and dummies for different orders of the presentation of profiles.

Analysis and Results

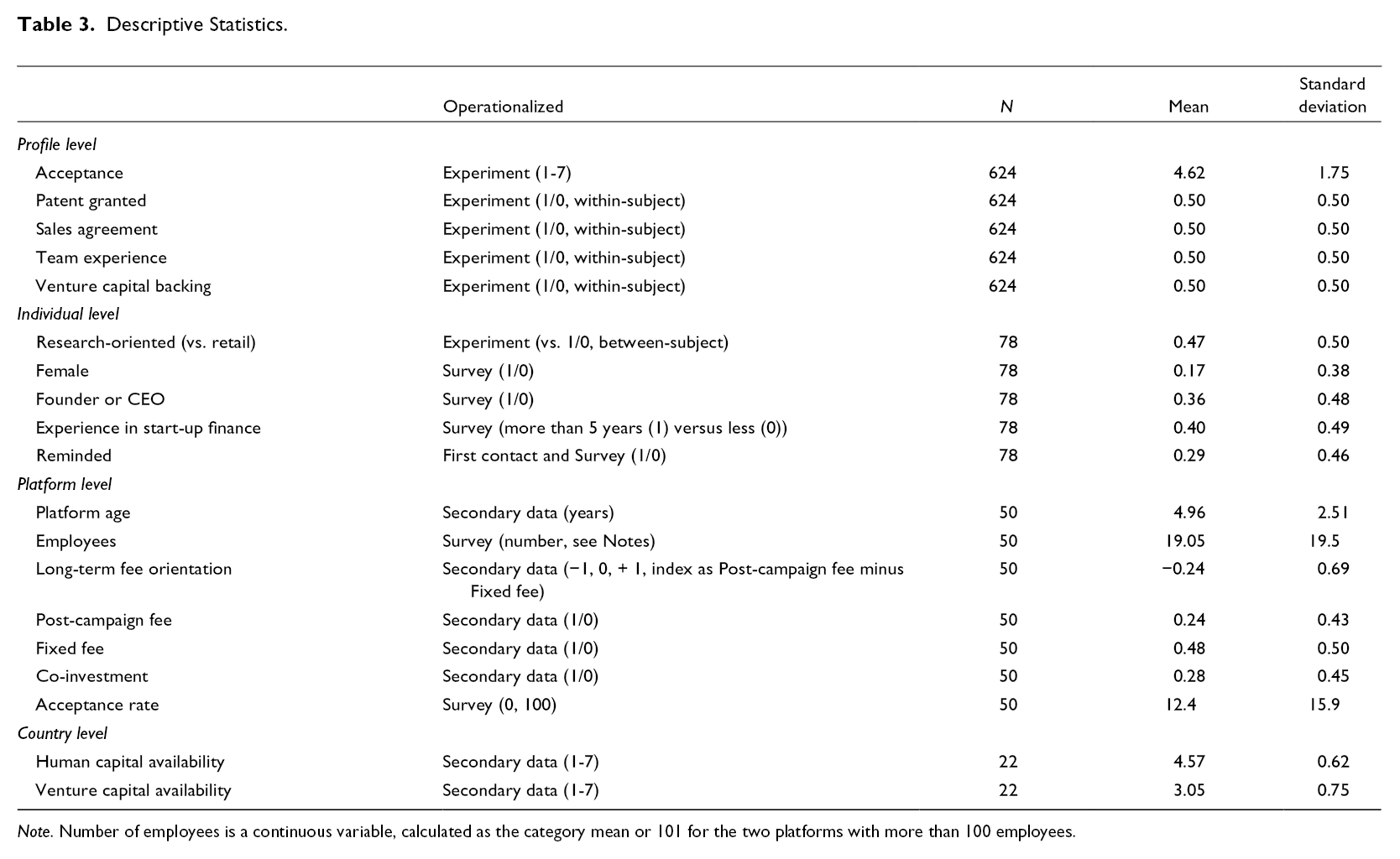

The data obtained from our conjoint experiment are multilevel in nature (descriptive statistics on the four levels reported in Table 3). Multiple profiles were evaluated (Level 1, profile level) by each individual (Level 2, individual level), multiple individuals may work for the same platform (Level 3, platform level), and multiple platforms can be located in the same country (Level 4, country level). To account for the multilevel nature of the data, we employed hierarchical linear modeling. Noting that only 12% of platforms have more than two respondents and only 12% of the sampled countries have more than two, and 23% have more than one platform, we include only random intercepts at the platform and country levels. To be more robust to small-sample biases, we used restricted maximum likelihood methods combined with the Kenward–Roger degrees of freedom method (McNeish, 2017).

Descriptive Statistics.

Note. Number of employees is a continuous variable, calculated as the category mean or 101 for the two platforms with more than 100 employees.

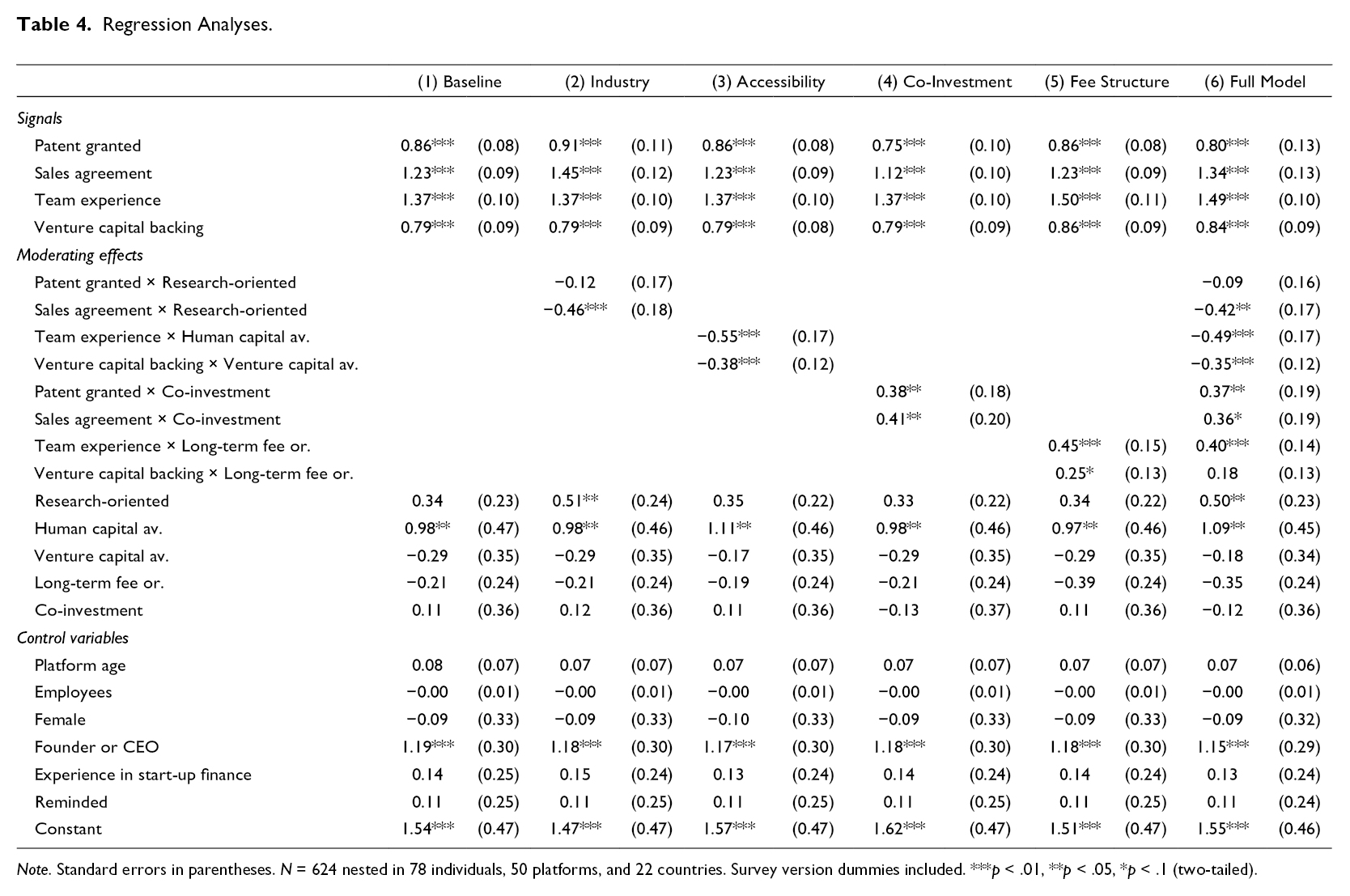

Table 4 reports the regression results. The estimated coefficients for signals reflect the change in the dependent variable in response to a one-unit increase in the independent variable (e.g., from low to high level of the signal). Because signals only have two levels and vary exogenously, such that their variance is equal, and all regressions refer to the same dependent variable, the effect sizes reflected by coefficients can be compared across signals. Model 1 includes the linear effects of the signals, which we use to test Hypothesis 1, along with the control variables. Models 2 to 5 include the moderation effects used to test our hypotheses related to the industry background (H2), the country-level availability of human capital and venture capital (H3), the co-investment requirement (H4), and the long-term fee orientation (H5).

Regression Analyses.

Note. Standard errors in parentheses. N = 624 nested in 78 individuals, 50 platforms, and 22 countries. Survey version dummies included. ***p < .01, **p < .05, *p < .1 (two-tailed).

Baseline Analyses of Signal Effects (H1)

Considering the raw data and calculating the standardized size (Cohen’s d) of the effects of signals on participants’ decisions, we observe substantial positive effects, which clearly aligns with Hypothesis 1. Team experience is on average the most important signal (d = .85), followed by sales agreements (d = .75) and, with greater distances, patents (d = .50) and venture capital backing (d = .46). The regression analyses (Model 1) replicate this order; strongly influential signals (sales agreements and team experience) increase acceptance by more than one point (about 70% to 75% of the overall standard deviation of the acceptance variable). Even the less influential signals’ effects still reach effect sizes of 45% to 50% of the dependent variable’s standard deviation. The estimated effect sizes compare favorably with those reported, for example, in related studies of screening decisions by venture capitalists using comparable Likert scales as dependent variables (Drover et al., 2017; Murnieks et al., 2011; Warnick et al., 2018).

Signaling Environment (H2 and H3)

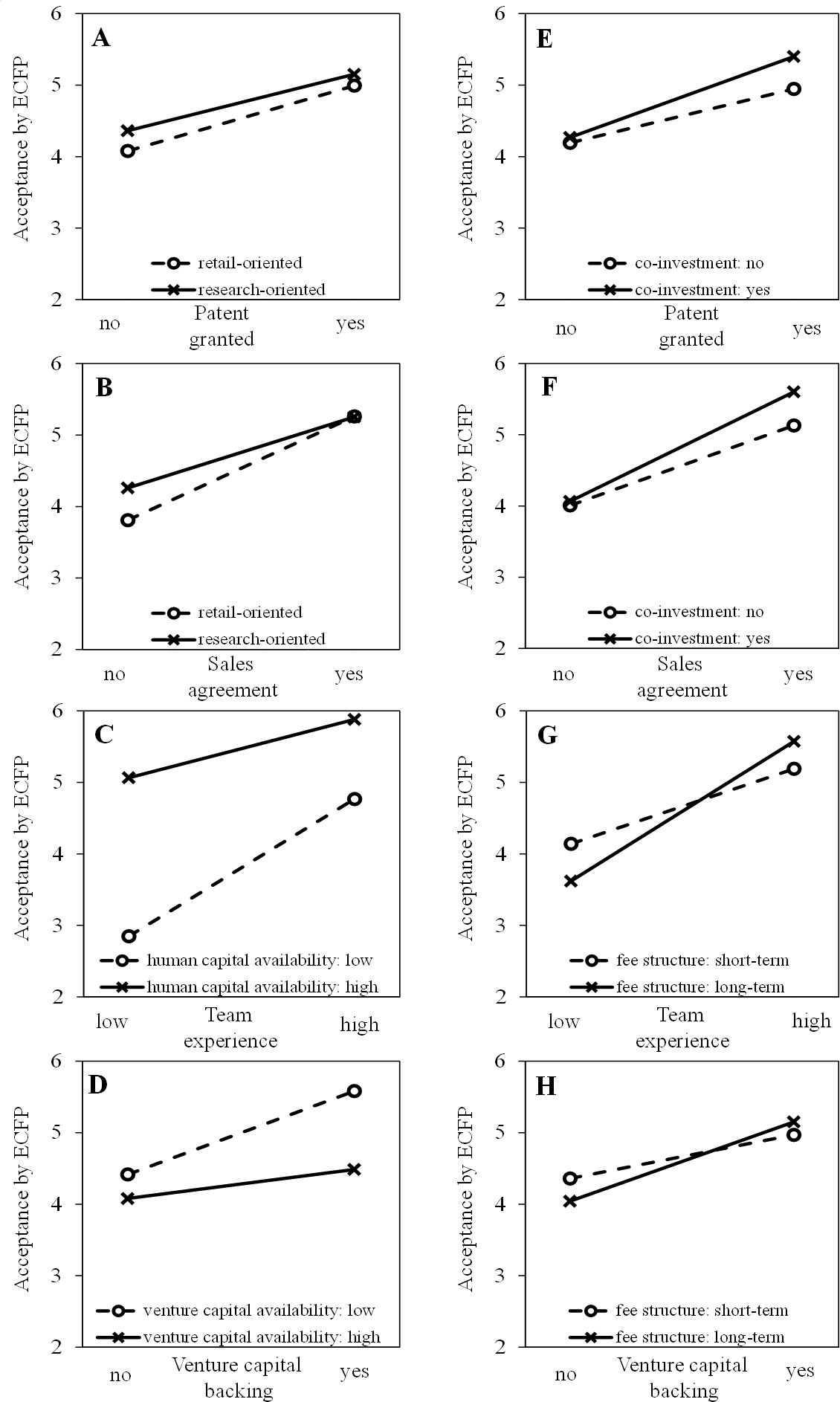

Testing the influence of the task environment, Model 2 includes interaction effects with the industry environment; graphical illustrations are provided in Figure 4 (Panels A and B). The analyses reveal that sales agreements interact negatively with research-oriented industries, which implies a positive interaction with retail-oriented industries, in support of H2b. The influence of sales agreements on ECFPs’ acceptance is about 32% greater for retail than research industries. However, we cannot support H2a, and the sign even is opposite our prediction; that is, ECFPs do not assign more weight to patents as signals for ventures from research- compared with retail-oriented industries. Either the information asymmetries regarding product characteristics do not differ that much between research- and retail-oriented companies, or ECFPs—due to their streamlined processes—do not develop industry-specific evaluations of the patent signal.

Signal effects moderated by signaling environment and receiver characteristics.

Regarding the institutional environment of ECFPs, related to the accessibility of human capital and venture capital, Model 3 (in combination with Figure 4, Panels C and D) reveals that when human capital and venture capital are more easily accessible, the related signals become less influential. Supporting Hypotheses 3a and 3b, both interaction terms are negative and statistically significant. The influence of corresponding signals decreases by more than 40% if the respective form of capital is easily accessible in a country.

Receiver Characteristics (H4 and H5)

Hypotheses 4 and 5 refer to the co-investment requirement and long-term fee orientation as important receiver characteristics of ECFPs. Model 4 includes the corresponding interaction terms to test H4 (Figure 4, Panels E and F). In support of H4a and H4b, we observe significantly positive moderating effects of the co-investment model on the influence of patents and sales agreements on acceptance by an ECFP. Furthermore, referring to the ECFP’s fee structure, when the ECFP prioritizes long-term performance, the influence of both team experience (H5a) and venture capital backing (H5b) on acceptance by an ECFP is more substantial (Model 5 and Figure 4, Panels G and H). However, the moderating effect is stronger for team experience than for venture capital backing; the latter even becomes statistically insignificant when we include all the moderating effects (Model 6).

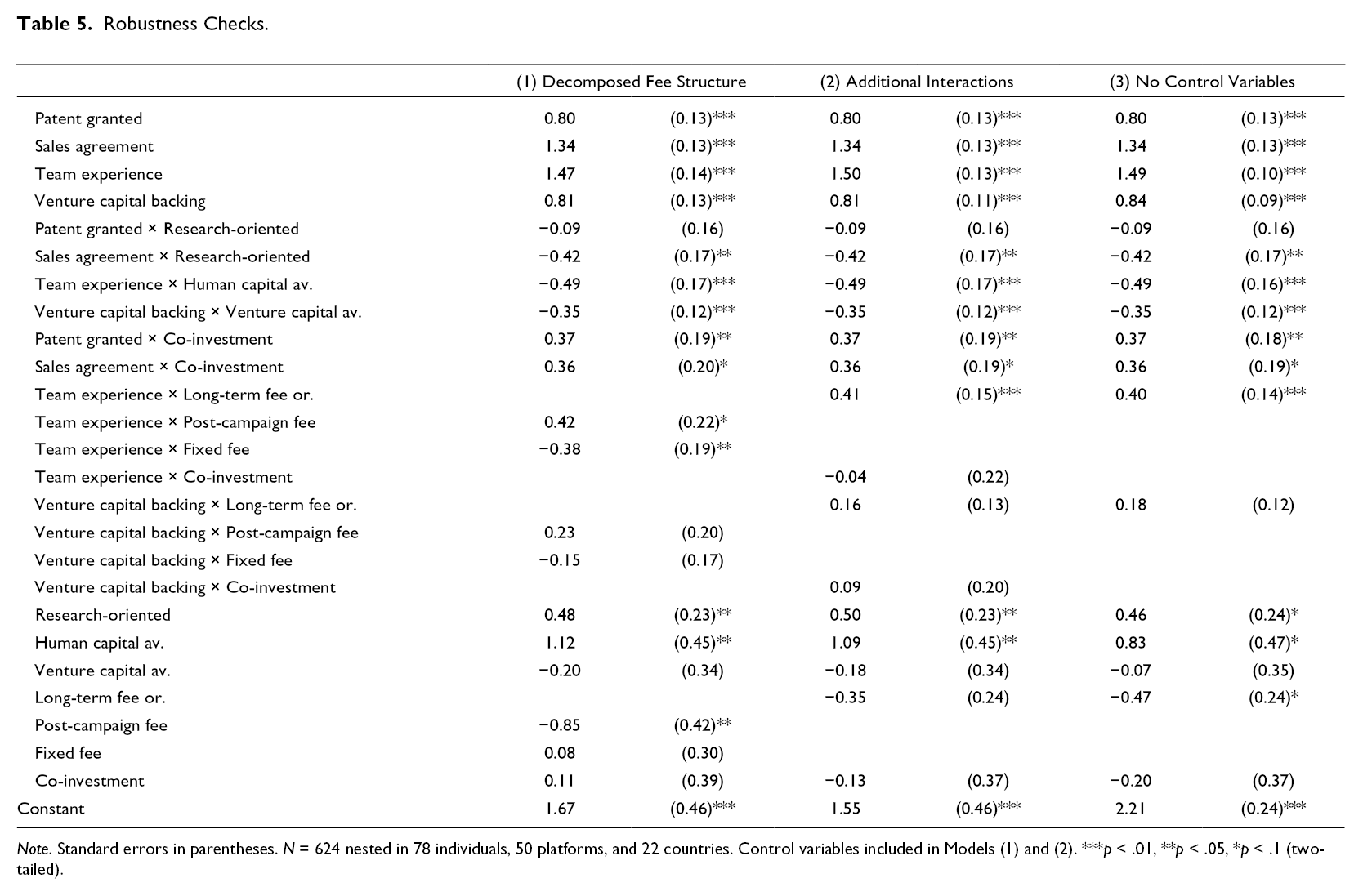

Robustness Checks

We report three robustness checks. First, we replace the long-term fee orientation variable with the two underlying dummy variables, each focusing on an extreme value of the fee structure (Table 5, Model 1). The moderation effects of both components on the effects of team experience are statistically significant and in the expected (opposing) directions. Their moderating effect on the influence of venture capital backing, which was already weak according to our long-term fee orientation variable, grew even weaker and is statistically not significant, even though their directions remain consistent with our expectations.

Robustness Checks.

Note. Standard errors in parentheses. N = 624 nested in 78 individuals, 50 platforms, and 22 countries. Control variables included in Models (1) and (2). ***p < .01, **p < .05, *p < .1 (two-tailed).

Second, we acknowledge that as part of our development of Hypothesis 4, we referred to a potential moderating effect of a co-investment requirement on the effects of team experience and venture capital backing, which could not be hypothesized due to the presence of two opposing mechanisms. To explore the aggregate effects, we include related interaction effects (Table 5, Model 2). Neither interaction is statistically significant, and the effect sizes are close to zero and much smaller than the other interaction effects. Thus, as expected, only patents and sales agreements increase in importance for ECFPs that require a co-investor.

Third, as the effects derived from the conjoint analysis are independent of control variables, we also estimate the full model excluding control variables (Table 5, Model 3). Results remain robust, also for moderation effects not derived from the experiment.

External Validity

Conjoint experiments with hypothetical evaluations may suffer from poor external validity (Choi & Shepherd, 2004; Shepherd, 1999), so we proceed by exploring the study’s external validity. We asked participants to indicate the selectivity (i.e., acceptance rate) of their platform’s screening process (“Out of 100 applications, approximately how many start-ups are allowed to start a crowdfunding campaign on your platform?”), according to seven response categories (1, 5, 6–10, 11–20, 21–30, 31–40, 41–50, 51 or more). About three-quarters of the participants indicated acceptance rates of 10% or lower, reflecting high rejection rates across platforms. We transformed the self-reported categorical into a continuous variable by assigning category means to each respondent. We averaged this variable and the venture evaluations from the conjoint analysis (i.e., average likelihood of acceptance in the experiment for all responses from an ECFP) at the platform level. The correlation between these two platform-level variables is .57 (p < .001), which is substantial and indicates that our conjoint study robustly relates to platforms’ actual selectivity toward real-world projects.

Discussion

In this study, we leverage signaling theory to establish that, before granting listings to equity crowdfunding campaigns, ECFPs incorporate patents, sales agreements, team experience, and venture capital backing as quality signals in their acceptance decisions. However, not all ECFPs evaluate new ventures in the same way. If ECFPs require accredited co-investors and design fees to incorporate the long-term performance of applying ventures, they tend to value quality signals differently. In addition, ECFPs perceive signals as more or less relevant, depending on the applicants’ industries and the accessibility of signals in their institutional context.

Theoretical Implications

This study makes two contributions to equity crowdfunding and entrepreneurial finance research in particular, as well as entrepreneurship signaling research in general. First, previous research on equity crowdfunding success (Ahlers et al., 2015; Vismara, 2016; Wang et al., 2019) focuses on new ventures’ campaign success, but we emphasize that equity crowdfunding starts and many failures happen well before the actual campaign. New ventures first need to access strictly screening platforms (Löher, 2017). In terms of success rates, the pre-campaign phase might be even more challenging to entrepreneurs than the campaign phase; our data indicate that only around 10% of new venture applications convince ECFPs to grant them access to the platform to run their campaigns, whereas around 50% succeed once they have reached the campaign phase (Ralcheva & Roosenboom, 2019). In shifting attention from the campaign to this pre-campaign phase, in which ECFPs decide which new ventures may access their service, we respond to recent calls for more research on different phases of crowdfunding (Pollack et al., 2021) and on the activities of platforms before the actual equity crowdfunding campaign (Cummings et al., 2020).

Going beyond descriptive analyses of ECFPs (e.g., Rossi & Vismara, 2018; Rossi et al., 2019) and qualitative analyzes of ECFPs’ decision-making processes (Löher, 2017), our study provides first quantitative evidence about which signals new ventures should use to convince ECFPs to grant them access to their platforms and how the signal effects depend on unique characteristics of ECFPs. For this purpose, we propose a framework, originally developed to examine new venture quality evaluations by investors (Bapna, 2019), that covers how ECFPs evaluate new ventures. On that basis, we identify quality signals that influence whether or not new ventures get access to ECFPs. These signals affect both the likelihood of being given a chance to run a campaign (as shown herein) and campaign success, as shown in previous studies (e.g., Ahlers et al., 2015; Kleinert et al., 2020; Ralcheva & Roosenboom, 2019). This evidence implies the potential presence of selection biases for studies investigating campaign success factors based on observational data. Accordingly, equity crowdfunding research might need to account for selection biases and proactively look for either selection instruments that allow an econometric correction or analyze data emerging from field experiments.

Second, our study expands signaling research (Connelly et al., 2011), particularly in the context of entrepreneurship (Ahlers et al., 2015; Anglin et al., 2018; Ko & McKelvie, 2018). We advance the conversation about both signal receiver characteristics and the signaling environment, which both are under-researched concepts in signaling theory (Connelly et al., 2011). Entrepreneurship research on receivers of venture quality signals tends to focus on investors and how investors interpret signals, such as in relation to their specific knowledge, understanding, and attention (Ciuchta et al., 2018; Scheaf et al., 2018; Steigenberger & Wilhelm, 2018). We introduce ECFPs as (previously neglected) signal receivers that do not invest themselves but act as mediators. By considering this player, we draw attention to business characteristics as an additional moderator for how signals are processed. The ECFPs with a revenue model that focuses on new ventures’ long-term performance, rather than fixed fees, render quality signals related to the new venture’s long-term performance more critical. Whether the target market of unaccredited investors is linked to accredited investors, by requiring co-investments, also affects the signals’ relative importance. The moderation by busines model variables might even grow more important if we expand the narrow focus on equity crowdfunding to security-based (e.g., Meoli et al., 2020) or other types (Cumming et al., 2019) of crowdfunding.

Regarding the signaling environment as an under-researched concept in signaling theory (Connelly et al., 2011), we introduce perceptions about the accessibility of human and venture capital as crucial moderators for more frequently noted quality signals, such as team experience and prior venture capital backing (e.g., Guerini & Quas, 2016; Ko & McKelvie, 2018). Regulations and culture in different countries or continents (Bell et al., 2012; Jia & Zhang, 2014; Useche, 2014) influence the effectiveness of signals. Our results reveal that their effectiveness also depends on perceptions of the signals’ regional accessibility. Hiring entrepreneurial team members and raising venture capital becomes almost impossible if the local infrastructure is not yet developed, which may render interpretations of corresponding signals rather region specific. Better capital infrastructures in countries such as the United States or Israel increase access to venture capital, and the brain drain from developing to more developed countries alters the level of available human capital. By introducing signal accessibility, we extend established cost considerations (Bergh et al., 2014; Spence, 1973) and highlight how the infrastructure and resource endowments can create scarcity, which affects the credibility of signals for receivers.

Practical Implications

This study provides practical implications for platforms, investors and new ventures that engage in equity crowdfunding. Considering the relative newness of equity crowdfunding, norms for operating screening processes might not have developed and spread. By outlining the practices of about half of all identified ECFPs, we offer substantive insights into how different ECFPs evaluate the quality of start-ups, which the platforms can use as a benchmark to consider competing platforms that follow similar or different business models. For example, ECFPs might predict the consequences of their business model choice more accurately if they understand that a flat fee revenue model potentially lowers incentives for selecting high quality ventures. A better understanding of how ECFPs work also can help unaccredited investors build confidence in this new form of financing. As our study shows, ECFPs are highly selective in which new ventures they present to investors. Our findings can reassure investors that they are not investing in dubious or underperforming companies. In addition, investors might use our studies to learn about the crucial differences among ECFP designs and thereby make more informed decisions about where to invest.

For entrepreneurs who want to gain access to an ECFP to raise funds, we open a critical “black box” of the criteria that matter most in the pre-campaign phase. As we show, entrepreneurs should recognize the relevance of team experience signals, but they also need to emphasize more market-related signals, according to their industry background. They should choose the type of ECFP to which they apply carefully, according to its particular business characteristics. Convincing an ECFP that has a co-investment requirement or long-term–oriented fee structure will be more difficult and requires more profound proofs of quality.

Limitations and Future Research

In addition to the research implications of our findings, the study’s limitations may open opportunities for further research. First, a limitation pertains to our rather small sample. While our study includes data from only 50 platforms, power analyses for our study’s focal effects reveal sufficiently high power values of 70% and above 80% for most of the effects. 13 Furthermore, the platforms in our sample reflect a substantial fraction of the international ECFP market in terms of funding volume (Statista, 2019), with more than US$5 billion combined, and the 78 decision-makers from 50 platforms are comparable to numbers from other studies involving professional decision-makers (e.g., 53 in Drover et al., 2017; 60 in Murnieks et al., 2011; 62 in Wood et al., 2014). However, while using Crunchbase as a data source is a well-established procedure to identify relevant samples in entrepreneurial finance (e.g., Yu, 2020), we may have been unable to identify and collect data from smaller, more regional platforms. Larger samples of platforms might be desirable, including especially smaller ECFPs (e.g., not listed on Crunchbase). More platforms per country also may allow more reliable identifications of country-related effects and avoid possible biases resulting from a focus on more visible platforms. Additional research also could sample more decision-makers from individual platforms to approximate platform decision-making more accurately.

Second, though we engaged real decision-makers from ECFPs, the passive participation design (Hsu et al., 2017) meant that these participants evaluated hypothetical rather than real ventures. The venture descriptions provide rather general descriptions of the offered solutions and industries, which might limit external validity (Choi & Shepherd, 2004). Although hypothetical profiles can be useful for deriving real policies (Shepherd, 2011) and our additional test supports external validity, future research might enrich and expand the venture descriptions—though doing so also would increase the time demands on participants (Shepherd, 1999). Perhaps real field experiments could send randomized applications to ECFPs. Going beyond conjoint or real experiments, future research might even convince ECFPs to let their real applications be analyzed.

Third, further research might expand our study in terms of its theoretical scope. We focused on four signals, which are both theoretically (Bapna, 2019) and practically (see Löher, 2017 and Table 1 of this paper) relevant, to keep our experiment manageable and straightforward (Hoenig & Henkel, 2015). Yet a variety of additional signals also might be relevant for ECFPs. For example, entrepreneurial passion and other soft skills by entrepreneurs (e.g., Ciuchta et al., 2018), presentation quality (Scheaf et al., 2018), or language signals conveyed on the pitch decks (Anglin et al., 2018) are relevant for other entrepreneurial finance players. Continued research might expand the sets of quality signals and consider potential interaction effects among them.

Fourth, beyond particular signals, we also focused on ECFPs decision-making without studying the possible performance implications for the subsequent campaigns. Platforms’ acceptance criteria might systematically differ (e.g., due to differences in their particular business characteristics and their institutional environments), and diverse ECFPs might list different types of ventures and attract different investors, so campaign success factors likely differ across platforms too. Most equity crowdfunding research relies on campaign data related to specific ECFPs, such as Crowdcube or Seedrs (Kleinert et al., 2020; Vismara, 2016; Wang et al., 2019); further research might strive to validate the findings obtained from well-researched environments and platforms by studying platforms in other institutional environments.

Footnotes

Acknowledgements

We are incredibly grateful for the excellent feedback and support from the editor Maija Renko and the three constructive anonymous reviewers. Their comments have helped us improve the manuscript significantly. For helpful comments and suggestions on earlier versions of our manuscript, we also thank Christina Günther, Jonas Löher, and participants of the Indiana-Wuppertal Workshop 2019. Finally, we thank the interview partners and the participants from equity crowdfunding platforms for their interest and willingness to support our study.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Author Biographies