Abstract

This article explores the important but understudied topic of authenticity in investment evaluations. Building on research in authenticity and signaling theory, we theorize how visual first impressions, such as clothing, can generate perceptions of authenticity that lead investors to overlook later quality signals, including a lack of prior experience. We found support for our theory in two field studies and a randomized experiment: investors tend to perceive entrepreneurs who are casually dressed as more authentic than those formally dressed, which is associated with higher investor evaluations. Moreover, perceptions of authenticity generated by casual clothes crowd out later signals: Casually dressed entrepreneurs are evaluated highly regardless of their entrepreneurial experience, but formally dressed entrepreneurs are penalized for perceived inexperience. We discuss the implications of our findings for authenticity research, the temporal order of signals, and early-stage investments.

Introduction

Appearing authentic was one of Sam Bankman-Fried’s greatest strengths. As the founder of the cryptocurrency exchange FTX, Bankman-Fried consistently wore T-shirts and cargo shorts, which investors and journalists viewed as a marker of personal authenticity (McHugh, 2023). His laid-back clothing became “a uniform that telegraphs to the watching world somebody who doesn’t have the time to worry about what they are wearing because they are thinking such big, world-changing thoughts” (Friedman, 2022: 1). This perceived authenticity, channeled through Bankman-Fried’s clothing, might have led investors to overlook crucial warning signs that he was misappropriating billions of dollars in customer funds to make high-risk bets (Clifford, 2023) ultimately leading to FTX’s bankruptcy (Rothenberg, 2024). Similarly, Elizabeth Holmes, the founder of Theranos, leveraged a carefully curated appearance to convey authenticity. Her black turtlenecks, which she claimed to have worn since childhood (Leive, 2015), helped portray her as “an authentic and sympathetic person” (Chozick, 2022: 1) who was praised for the “authenticity in [her] lack of polish” (Michari, 2015: 1) and the way “she deliver[ed] her message authentically” (Civiello, 2016: 1). This helped Holmes gain investors’ trust before she lost hundreds of millions of their dollars (Buhr, Funk, & Owen-Smith, 2021; Carreyrou, 2018).

These cases suggest a broader pattern—casual clothing can signal authenticity, shaping investors’ perceptions of entrepreneurs. While perceived authenticity often benefits the person being evaluated (Gill & Caza, 2018), the Bankman-Fried and Holmes cases suggest that it can also impair evaluators’ judgments by distorting their impression of the entrepreneur. From a signaling theory perspective (Spence, 1973), clothing-based impressions are, therefore, “low validity visual cues” (Mahmood, Luffarelli, & Mukesh, 2019: 1) that should lose relevance when costlier (more informative) signals emerge (Connelly, Certo, Ireland, & Reutzel, 2011; Drover, Wood, & Corbett, 2018), but often prove surprisingly sticky (Mann & Ferguson, 2015). As such, entrepreneurs’ clothing may bias investors’ judgments, crowding out more diagnostic signals, such as entrepreneurial (in)experience—a core indicator of venture quality (Kleinert, 2024; Zacharakis & Meyer, 2000). This raises two questions: Do entrepreneurs’ clothes affect venture evaluations by influencing perceived authenticity? And does that perceived authenticity obscure more reliable signals?

We investigate these research questions across three independent samples. Study 1 uses data from 774 pitches made on the TV show Shark Tank from 2009 to 2019. We find that early-stage investors evaluate entrepreneurs who are casually dressed more favorably than those who are formally dressed, and that perceived authenticity mediates this effect. Moreover, while early-stage investors evaluate casually dressed entrepreneurs positively regardless of later revelations of a lack of experience, investors downgrade their evaluations of formally dressed entrepreneurs in response to a lack of experience. In Study 2, we replicate the findings of Study 1 using field data from 101 investments made by a European angel group. In Study 3, we conduct a randomized experiment with 714 equity investors that tests the causal links and rules out alternative explanations. We also conducted six semi-structured interviews with early-stage investors to explore practitioners’ thoughts about the mechanisms underlying our findings (see Appendix A for details).

This paper makes three primary contributions. First, our findings contribute to the literature on visual impressions by demonstrating how clothing affects perceptions in entrepreneurial contexts (Clarke, 2011; Scheaf, Davis, Webb, Coombs, Borns, & Holloway, 2018). While prior research in the contexts of management, academia, and medicine suggests that formal clothes result in more favorable evaluations (Brase & Richmond, 2004; Maran, Liegl, Moder, Kraus, & Furtner, 2021; Warnick, Davis, Allison, & Anglin, 2021), we find that entrepreneurs benefit from wearing casual clothes. We explain this difference by suggesting that “traditional sectors” value formal attire as a signal of professionalism (Forsythe, Drake, & Cox, 1985; Rafaeli & Pratt, 1993), while the entrepreneurial ecosystem favors casual clothes that convey authenticity. This points to a previously unexplored way for entrepreneurs to “present an appropriate scene to stakeholders [and] create a professional identity” (Clarke, 2011: 1367).

Second, we contribute to the authenticity literature (Cha et al., 2019) by demonstrating how perceived authenticity forms in venture pitches (Bai, Ho, & Liu, 2020), which are brief, superficial, and unidirectional. When investors lack the time or information needed to carefully assess authenticity, they rely on salient visual cues—easily observed aspects of the entrepreneur (Scheaf et al., 2018)—such as the entrepreneur’s clothing. Once formed, these perceptions act as cognitive anchors, creating a sense of shared reality between the entrepreneur and the investor, which boosts confidence but clouds judgment (Rossignac-Milon, Pillemer, Bailey, Horton Jr, & Iyengar, 2024). This perceptual shortcut enables entrepreneurs to strategically curate the appearance of authenticity without offering meaningful evidence of it, decoupling authenticity perceptions from inner truth, and turning the former into a strategic signal (Pillemer, 2024). This reveals how even signals meant to convey sincerity can be used to manipulate investors’ perceptions, exposing a potential “dark side of authenticity” (Cha et al., 2019: 655).

Finally, we contribute to recent developments in signaling theory (e.g., Colombo, 2021; Connelly et al., 2011) by investigating the interplay between initial low-quality signals (i.e., clothes) and later, more valuable signals (e.g., prior entrepreneurial experience, Kleinert, 2024; Scheaf et al., 2018; Steigenberger & Wilhelm, 2018). Specifically, we move past the more common simultaneous interpretation of signals to demonstrate that the order of signals matters—early weak signals can crowd out later strong signals. Thus, our theorizing connects the signaling literature (e.g., Connelly et al., 2011; Drover et al., 2018) to the literature on first-impression biases (e.g., Antretter, Wesemann Lekkas, Djokovic, Souitaris, & Wincent, 2025; Swider, Harris, & Gong, 2022; Uleman & Kressel, 2013) to view signal attention as a “temporal process” (Drover et al., 2018: 225).

Theory and Hypotheses

We draw on signaling theory and the authenticity literature to theorize how entrepreneurs’ clothes (a low validity visual cue) affect investment evaluations. Signaling theory (Connelly et al., 2011; Spence, 1973) explains how individuals use signals to convey indications of quality, which can be particularly useful in uncertain settings, such as early-stage investing (Colombo, 2021). Authenticity research (Cha et al., 2019; Rook, Leroy, Zhu, & Anisman-Razin, 2024) provides theoretical arguments on how and why perceptions of authenticity foster a sense of connection and mutual understanding, thereby aligning the perspectives of investors and entrepreneurs (Cha et al., 2019; Gill & Caza, 2018). Collectively, these frameworks allow us to theorize how initial perceptions of authenticity shape evaluations in the challenging and uncertain context of early-stage investments.

Clothes as a Signal

Early-stage investors often make investment decisions after seeing and hearing an entrepreneur’s pitch in which the entrepreneur introduces the venture and provides additional background information (Clarke, Cornelissen, & Healey, 2019; Huang, Ivković, Jiang, & Wang, 2023). Most early-stage ventures have no prior track record, endorsements, or sales (Colombo, 2021; Huang & Pearce, 2015), which creates considerable information asymmetries between entrepreneurs and investors in an uncertain context. During venture pitches, early-stage investors try to gauge whether the entrepreneurs can deliver on their promises (Bammens & Collewaert, 2014; Huang, 2018; Maxwell & Lévesque, 2014).

However, investors’ interactions with entrepreneurs during pitches are brief (Huang et al., 2023), and the information asymmetries are difficult to overcome (Colombo, 2021). Early-stage ventures are too complex to assess accurately in a short pitch, so investors cannot consider all relevant information (Butticè, Collewaert, Stroe, Vanacker, Vismara, & Walthoff-Borm, 2022; Butticè, Croce, & Ughetto, 2021). Instead, they tend to rely on simple heuristics (i.e., rules of thumb) that accelerate decision-making (Tversky & Kahneman, 1973) and leave cognitive capacity for other tasks (Drover et al., 2018), but still produce sufficiently good results (Kahneman, 2011). These heuristics often base decisions on salient visual cues. While research has investigated visual cues such as facial characteristics (Huang et al., 2023) and attractiveness (Schreiber, Hess, Grichnik, Shepherd, Tobler, & Wincent, 2024), clothing is a visual cue that has an inherently symbolic character (Adam & Galinsky, 2012). Moreover, they are one of the easiest ways for people to express themselves (Peterson, 1997) and one of the first things an individual notices when interacting with another person. Therefore, clothes are a powerful communication tool (e.g., Forsythe et al., 1985; Pratt & Rafaeli, 1997) and an important factor in initial assessments (for a review, see Chang & Cortina, 2024).

When seeking advice on what to wear in a business context, most research recommends wearing formal attire. In almost all studies, formal wear is associated with positive traits (Chang & Cortina, 2024; Rafaeli, Dutton, Harquail, & Mackie-Lewis, 1997) like trustworthiness (Morris, Gorham, Cohen, & Huffman, 1996), credibility (O’Neal & Lapitsky, 1991), and power (Kim, Holtz, & Vogel, 2023). The dominant attitude has been summarized as follows: “We are more likely to believe, respect, and obey the man who wears a suit than the man who does not. . . . In any level of society, suits are associated with authority, with position, with power” (Molloy, 1988: 41; Sebastian & Bristow, 2008). As a result, the literature consistently recommends formal clothes to be evaluated more positively (Barry & Weiner, 2019; Chang & Cortina, 2024).

However, compared to the established sectors and businesses in which this research was conducted, the entrepreneurship sector places less emphasis on factors like perceived authority and more on perceived authenticity (Hmieleski, Cole, & Baron, 2012). Indeed, much of the halo that surrounded Bankman-Fried existed because he looked like he unapologetically dressed in a way that was true to himself, regardless of the context. This shift from perceived authority to perceived authenticity may affect the overall recommendation on what clothes are beneficial. If clothes can signal authenticity and if perceived authenticity is sufficiently important to venture investors, the wearing of casual clothes during startup pitches may conceivably be beneficial for entrepreneurs.

Casual Clothes Seem Authentic

We theorize that casual clothes increase an entrepreneur’s perceived authenticity for two reasons. First, casual clothes enable true self-expression. While formal clothes are often used to project authority, credibility, and competence (Slepian, Ferber, Gold, & Rutchick, 2015), they are usually worn to conform to external expectations (Cable, Gino, & Staats, 2013) even if they go against one’s inner self (Costas & Fleming, 2009). However, in startup ecosystems, where authenticity is highly valued, an overly polished image may lead investors to suspect that the entrepreneur is trying to create a professional image rather than engage in genuine self-expression. Therefore, formal clothes can raise suspicions about someone’s authenticity and motives (Jarvis, 2019; Waddingham, Zachary, & Walker, 2022). In the worst case, this can trigger the “self-promoter paradox” (Bolino, Long, & Turnley, 2016: 379), where those who appear to be trying hard to impress others come across as inauthentic and even incompetent (Kleinert, 2024).

Entrepreneurship abhors such conformity, and even the most accomplished and wealthiest entrepreneurs often express themselves in casual clothes. For example, consider the casually authentic styles of figures like Steve Jobs (turtlenecks; Sharma & Grant, 2011), Mark Zuckerberg (T-shirts; Roose, Kang, & Frenkel, 2018), or Jensen Huang (black leather jackets; Friedman, 2023). Jensen Huang, for instance, has consistently worn the same style of black leather jacket for more than 20 years and even referred to himself as “the guy in the leather jacket” (Friedman, 2023: 1). This mindset is not limited to “superstar” entrepreneurs whose status may afford them the right to break norms (Bellezza, Gino, & Keinan, 2014): it extends to “regular” entrepreneurs as well.

When people feel most like themselves, they wear certain casual clothes. When an entrepreneur shows up in casual clothes, it suggests that “this is how they dress.” Such displays of personal consistency across different contexts are a critical antecedent of perceived authenticity (Cha et al., 2019), as people tend to trust individuals who behave naturally rather than tailor their actions to external expectations (Hogg & Van Knippenberg, 2003). Personal consistency is associated with greater trust and perceived integrity (Gooty et al., 2023) and may translate into higher perceived authenticity (Rivera, Christy, Kim, Vess, Hicks, & Schlegel, 2019). In contrast, formal wear is typically reserved for special occasions and appears formulaic, that is, fitting a script rather than allowing others to see one’s true self (Molloy, 1988; Rafaeli & Pratt, 1993).

While this link between casual clothes and perceived authenticity has not been formally theorized, it reflects common wisdom in lived entrepreneurship, where the maxim is “just be yourself,” and entrepreneurs are advised to “keep it simple, casual, and true to personality” (Williams, 2017: 1). As Shark Tank investor Barbara Corcoran put it: “Everyone recognizes and responds well to people who act like themselves. You don’t have to be fancy, you just have to be yourself” (Corcoran, 2017: 1). Based on the above reasoning, we hypothesize:

Hypothesis 1: At a venture pitch, investors perceive entrepreneurs wearing casual clothes as more authentic than entrepreneurs wearing formal clothes.

Benefits of Perceived Authenticity

Next, we theorize that being perceived as authentic helps entrepreneurs secure more funding. While underexplored in the entrepreneurship literature, perceived authenticity has consistently been linked to positive outcomes in other fields, and recent research sees it as a strategic signal (Pillemer, 2024). Gill and Caza (2018) list four benefits of perceived authenticity: identification, trust, positive states, and positive exchange. In this section, we explore each factor and its relevance for entrepreneurs.

First, perceived authenticity fosters stronger identification with an individual’s vision (Gill & Caza, 2018). For example, authentic leaders build strong followings by maintaining transparency and staying true to their beliefs (Gardner, Cogliser, Davis, & Dickens, 2011). The same logic applies in entrepreneurship, where early-stage founders often pitch ventures that have not yet made any revenue, making their vision the primary asset for securing funding (Lee & Huang, 2018; Sine, Cordero, & Coles, 2022). Perceived authenticity helps entrepreneurs convince investors to see the world as they do (Murray & Fisher, 2023), thereby increasing the likelihood of investment (Edú Valsania, Moriano, & Molero, 2016).

Second, perceived authenticity generates trust (Gill & Caza, 2018). It reduces suspicion of opportunism (Cha et al., 2019), thereby improving decision-making in managerial contexts (Gardner, Avolio, Luthans, May, & Walumbwa, 2005; Kernis & Goldman, 2006). Overall, authenticity is seen as consistency with one’s values, which increases perceptions of trustworthiness (Wang & Hsieh, 2013). This is particularly critical in high-risk contexts, such as early-stage investing, where investors have limited post-investment control and must trust that entrepreneurs act in good faith (Hmieleski et al., 2012; Wesemann & Antretter, 2023).

Third, perceived authenticity promotes positive psychological states, such as increased optimism (Gill & Caza, 2018), which foster psychological safety and emotional well-being in teams (Guenter, Schreurs, van Emmerik, & Sun, 2017). It also leads evaluators to perceive others more positively (Markowitz, Kouchaki, Gino, Hancock, & Boyd, 2023) and become more open to risk taking (Hsiung, 2012). This is particularly relevant in venture investing, where entrepreneurs must foster optimism to help investors accept the high risk of startup failure (Soto-Simeone, Sirén, & Antretter, 2020).

Fourth, perceived authenticity fosters long-term relationships by reducing skepticism (Gill & Caza, 2018) and enhancing communication, which strengthens support and engagement (Agote, Aramburu, & Lines, 2016). As a result, individuals who seem authentic are more likely to be hired (e.g., Krumhuber, Manstead, Cosker, Marshall, & Rosin, 2009) and form more lasting professional relationships (Rossignac-Milon et al., 2024). The willingness to form long-term relationships is critical in entrepreneurship, where investments often last a decade or more (National Venture Capital Association, 2025) and where strong investor support is needed for future venture development (Sariri, 2025).

If achieved, this combination of stronger identification, trust, positive states, and positive exchanges gives rise to a sense of shared reality—perceived unity in how individuals see the world (Higgins, Rossignac-Milon, & Echterhoff, 2021). The shared-reality literature even describes perceived authenticity as the “epistemic glue” that allows individuals to construct such shared understandings (Rossignac-Milon, Bolger, Zee, Boothby, & Higgins, 2021; Rossignac-Milon et al., 2024: 4). People are drawn to others they perceive as authentic (Higgins et al., 2021), and they heavily weigh authenticity when deciding to form lasting relationships (Rossignac-Milon et al., 2024). However, creating a shared reality is not an easy task. When entrepreneurs fail to appear authentic, investors may ask themselves, “Do we actually see the world in the same way, or do they just want me to like them?” (Rossignac-Milon et al., 2024: 2). Such misalignments can prompt rejection (Koudenburg, 2018).

In the high-uncertainty context of early-stage venture investments, creating a sense of shared reality may be among the entrepreneur’s most critical challenges. Decisions are often made quickly with limited hard data and under high uncertainty (Blohm, Antretter, Sirén, Grichnik, & Wincent, 2022; McMullen & Shepherd, 2006; Wesemann Lekkas, Antretter, Shepherd, & Wincent, 2025). As a result, investors tend to seek signals offering reassurance that the entrepreneur can be trusted, will act in alignment with shared values, and is able to handle volatility (Bammens & Collewaert, 2014; Coulter & Coulter, 2003; Deutsch, 1958). Entrepreneurs who project authenticity may trigger the desired sense of alignment, prompting investors to see the world in the same way. The power of perceived authenticity to signal integrity and fit (Oo & Allison, 2024; Radoynovska & King, 2019) is essential in early-stage investing, where relationships typically last 5 to 7 years (Bammens & Collewaert, 2014). In such long-term, trust-dependent partnerships, perceived authenticity becomes more than a social virtue: it serves as the foundation for commitment. One interviewee noted: “In the end, this is a people business. If I did not trust the entrepreneurs to deliver on their promises, I would never invest”. Based on the above reasoning, we hypothesize:

Hypothesis 2: In a venture pitch, entrepreneurs perceived by investors as more authentic receive more positive evaluations than those perceived as less authentic.

The combination of Hypotheses 1 and 2 brings us to Hypothesis 3:

Hypothesis 3: Perceived authenticity mediates the relationship between an entrepreneur’s dress formality and investment evaluations. Specifically, the entrepreneur’s dress formality is negatively associated with perceived authenticity and perceived authenticity is positively associated with investment evaluations.

Entrepreneurial Experience as a Quality Signal

While the perceived authenticity of entrepreneurs is vital in shaping early investors’ impressions, clothing is, ultimately, a weak basis for inference. Dressing casually does not require much effort and does not reveal much about an entrepreneur’s underlying qualities. It is a “low validity visual cue” (Mahmood et al., 2019: 1) that tells investors little about the true potential of the person or the opportunity (Connelly et al., 2011). Moreover, like other easily mimicked signals, it is unreliable (Bergh, Connelly, Ketchen Jr., & Shannon, 2014; Kleinert, 2024).

In comparison, entrepreneurial experience is a strong signal, and one of the most robust predictors of early-stage venture quality (Kleinert, 2024; Zacharakis & Meyer, 2000), as it is difficult to obtain and imitate (Spence, 1973). Indeed, for investors, prior entrepreneurial experience offers evidence that the entrepreneur not only understands the ecosystem (Colombo, 2021) but can also pursue entrepreneurial opportunities (Ko & McKelvie, 2018; Zunino, Dushnitsky, & Van Praag, 2022), commercialize new products (Fisher, Kuratko, Bloodgood, & Hornsby, 2017), manage uncertainty (Ko & McKelvie, 2018), and organize managerial routines (Shepherd, Douglas, & Shanley, 2000). Experienced entrepreneurs are also more realistic about how ventures develop (Capelleras, Contin-Pilart, Larraza-Kintana, & Martin-Sanchez, 2019; Kleinert, 2024). As a result, they show higher chances of survival (Soto-Simeone, Sirén, & Antretter, 2021), and they tend to deliver greater success for investors (Cope, 2005; Roccapriore, Imhof, & Cardon, 2021; Souitaris, Peng, Zerbinati, & Shepherd, 2023). Conversely, a lack of experience is often considered problematic (Bottazzi, Da Rin, & Hellmann, 2016; Ucbasaran, Shepherd, Lockett, & Lyon, 2013).

However, there is one crucial caveat: the lack of entrepreneurial experience is rarely visible upfront. Unlike clothes, which are immediately visible, prior (in)experience is only revealed when the entrepreneurs mention it, usually toward the end of a pitch on the team slide. This means that investors typically form initial impressions based on early visual cues, such as clothing, and only later learn about the entrepreneur’s qualifications (Todorov, 2008; Todorov, Pakrashi, & Oosterhof, 2009; Willis & Todorov, 2006). In principle, investors should update their evaluations when more diagnostic signals—like information on prior experience—become available. Instead, first impressions are notoriously sticky (Mann & Ferguson, 2015) and tend to retain some power even after individuals obtain superior information (Hogarth & Einhorn, 1992; Swider et al., 2022). Judgments formed within 100 milliseconds of seeing a person remain surprisingly constant, even after extended periods of exposure (Willis & Todorov, 2006). As the saying goes, “you never get a second chance to make a first impression.” This dynamic causes a first-impression bias, where early visual cues shape belief systems in ways that make information revealed later less influential (Aversa, Huyghe, & Bonadio, 2021; Uleman & Kressel, 2013).

While the effects of first-impression biases affect everyone, they might be particularly common in early-stage investment decisions for two reasons. First, while investors are boundedly rational (Maxwell, Jeffrey, & Lévesque, 2011; Tversky, 1972), the entrepreneurial context is full of noise and ambiguity, and attempts to filter through every piece of information can quickly lead to information overload (Antretter, Blohm, Sirén, Grichnik, Malmström, & Wincent, 2020a; Huang & Pearce, 2015; O’Reilly III, 1980). As a result, investors rely on shortcuts, and they may stop searching altogether when first impressions feel “right” (Drover et al., 2018; Jonas, Diehl, & Brömer, 1997). For example, in a study by Butticè et al. (2022), venture investors made their final decisions after evaluating, on average, four out of nine available pieces of information without considering the rest. When the first few signals seem consistent, they consider that “enough” and disengage from further evaluation. This decision-making process makes the temporal order of signals vitally important, as late signals might not even register (Connelly et al., 2011; Drover et al., 2018). Such reduced attention to later signals is especially likely when first impressions like high perceived authenticity create a sense of belonging, kinship, or shared reality (Rossignac-Milon et al., 2021).

Second, venture investors tend to be optimists. They tolerate ambiguity (Taeuscher, Bouncken, & Pesch, 2021), overestimate their ability to spot winners (Blohm et al., 2022; Brunnermeier, Gollier, & Parker, 2007), and believe they can find “diamonds in the rough” (Huang & Pearce, 2015: 614). This optimism can also lead to restricted variance interactions, where strong early impressions compress variability in investment decisions (Cortina, Koehler, Keeler, & Nielsen, 2019; Cortina et al., 2023). When investors perceive someone as highly authentic, they quickly shift from evaluation to envisioning future collaboration, making them less responsive to later signals, like a lack of entrepreneurial experience. In contrast, when perceived authenticity is low, investors continue to look for evidence and are more likely to be swayed by subsequent signals. As a result, experience matters more when perceived authenticity is low and less when it is high. As one of our interviewees stated: If an entrepreneur convinces me early, I find myself thinking during the pitch about how I could contribute to this investment. If I am skeptical from the outset, I continue looking for information that might help me decide. However, if I do not find that information relatively quickly, I will disregard the opportunity.

In sum, perceived authenticity is processed early and sticks. Information on a lack of experience is processed later and might be discounted if the entrepreneur appears authentic. Therefore, inexperienced entrepreneurs who are perceived as authentic may benefit from an increased sense of shared reality, as investors might pay less attention to their later-revealed lack of experience. In contrast, those who do not receive this early authenticity bonus may be judged more harshly when their lack of experience becomes known. Based on this reasoning, we hypothesize:

Hypothesis 4: At a venture pitch, the negative relationship between an entrepreneur’s lack of experience and investment evaluations is less negative for entrepreneurs perceived by investors as more authentic than those perceived as less authentic.

Methods and Analyses

We conducted three studies to investigate how entrepreneurs’ dress formality and experience influence investment evaluations of those entrepreneurs’ ventures. The use of multiple settings and research methods allowed us to triangulate the results and increase external validity (Scandura & Williams, 2000). Specifically, in Study 1, we tested our model with data from Shark Tank—a TV series in which entrepreneurs pitch their businesses to well-known early-stage investors (Blaseg & Hornuf, 2024). We initiated our study within this context, leveraging readily available data, but acknowledged the limitations of this approach. Therefore, in Study 2, we tested the same hypotheses using proprietary data from an invitation-only angel-investment group that invested more than USD 156 million in startups from 2012 to 2023. In Study 3, a randomized experiment involving 714 equity investors, we isolated the effects of dress formality and lack of experience through experimental manipulation to establish causality and rule out alternative explanations.

Given our theoretical focus and the nature of our variables, there is a risk of hierarchical dependencies based on the national context, which can bias parameter estimates if ignored (e.g., Bliese, 2000). In particular, perceived authenticity is culturally shaped and varies across national settings (Grandey & Gabriel, 2015; Markus & Kitayama, 2010), which creates constraints for generality (Cha et al., 2019) because individuals from different countries may interpret the same behavior differently (Morris & Peng, 1994; Yuki, 2003). Empirically, intraclass correlation coefficients (ICCs) support our approach: perceived authenticity exhibited substantial clustering in Study 1 (ICC = 0.32), moderate clustering in Study 2 (ICC = 0.11), and modest clustering in Study 3 (ICC = 0.06). While the effects in the perceived-authenticity models make clustering essential in Studies 1 and 2, it is also advisable in Study 3, as the ICC exceeds the common lower threshold of 0.05 (Bliese, 2000), and as recent publications recommend clustering for such values when theoretically justified (Li et al., 2024). Aligning the approach across studies also avoids producing “uninterpretable blends of variances and effects attributable to different kinds of things” (Humphrey & LeBreton, 2019: 481). Therefore, we cluster all models by national context (for more detailed discussions, refer to Aguinis, Gottfredson, & Culpepper, 2013; Bliese, Schepker, Essman, & Ployhart, 2020).

Study 1: Evidence From Shark Tank

Sample and Procedure

We analyzed 895 pitches made on the TV show Shark Tank between 2009 and 2019 in the United States (10 seasons, 246 episodes). On this show, entrepreneurs looking for equity investments of USD 10,000 to USD 500,000 pitch to a panel of prominent investors known as the “sharks” (Blaseg & Hornuf, 2024). Of the 895 ventures, 547 received financing. Shark Tank data has been used extensively in previous research, including investigations of obesity stereotypes (Antretter et al., 2025), gender penalties (Liao et al., 2024), entrepreneurs’ coachability (Cable et al., 2013), and rhetoric (Sanchez-Ruiz, Wood, & Long-Ruboyianes, 2021). The data is also particularly well-suited to our research model because the investors receive no information about the venture before the pitch (Herjavec, 2024).

We collected the required information from all pitches, Shark Tank’s website, company websites, and the entrepreneurs’ social-media profiles. We focused our data collection on the lead entrepreneur (i.e., the entrepreneur initiating the pitch). We excluded 37 observations that were non-equity deals (i.e., loans or royalty deals) and 84 cases in which the entrepreneur wore job-specific clothes (e.g., a lab coat or a firefighter uniform), leaving a final sample of 774 observations. A test of the variance inflation factors (VIFs) in regular regressions showed that the highest VIF for one of the core variables was 1.20, and the highest model VIF was 1.35, both well below the acceptable maximum of 10, suggesting that multicollinearity is not a problem (Allison, 1999).

Measures

Investment evaluation

Consistent with previous research using Shark Tank data to investigate investment evaluations (e.g., Pollack, Rutherford, & Nagy, 2012; Sanchez-Ruiz et al., 2021), we used the natural logarithm (logarithm + 1) of the amount (USD) invested in the venture (Kanze, Conley, Okimoto, Phillips, & Merluzzi, 2020).

Dress formality

Building on previous investigations of dress formality in management research (Maran et al., 2021), we measured dress formality with a three-item scale: casual, business casual, and business. To do so, we followed Huang et al. (2023) and took video stills of the entrepreneurs for each Shark Tank pitch. We classified individuals’ dress formality as casual when they primarily wore plain T-shirts, sweatshirts, jeans, and/or sneakers. The business-casual category included entrepreneurs wearing, for instance, white or blue dress shirts along with dark pants or chinos and possibly a blazer. The formal category included entrepreneurs wearing suits (men and women) or other formal outfits (women). Two researchers independently coded the lead entrepreneurs’ dress formality (α = 0.92). We settled any differences in coding through discussion.

Perceived authenticity

We measured perceived authenticity using the dictionary developed by Kovács, Carroll, and Lehman (2014), which includes terms such as authentic, real, pure, sincere, and honest (see Appendix B for the complete list). In line with current best practice (e.g., Gray, Howell, Strassman, & Yamamoto, 2024; Roccapriore & Pollock, 2023), we fed the dictionary into the language-analysis software Linguistic Enquiry and Word Count (LIWC; Boyd, Ashokkumar, Seraj, & Pennebaker, 2022; Pennebaker, Boyd, Jordan, & Blackburn, 2015) to generate a perceived authenticity score for the transcript of the angel-investor discussion that followed the startup pitch.

Experience

We measured entrepreneurial experience using a dummy variable denoting whether the entrepreneur had founded another business before the focal venture (Hsu, 2007; Ko & McKelvie, 2018). This variable took a value of 1 if the entrepreneur had previously founded at least one business and 0 otherwise. This data was coded from LinkedIn and, if unavailable, the ventures’ websites (for a similar approach, see Blohm et al., 2022).

Controls

We controlled for several factors related to the entrepreneur, venture, and pitch. First, we controlled for the entrepreneur’s education, age, and gender, obtained from LinkedIn or personal websites. We coded education as the highest educational attainment (1 = high school diploma, 2 = associate degree, 3 = bachelor’s degree, 4 = master’s degree, 5 = doctoral degree) to account for the effect of education on entrepreneurial performance (Guo, Chen, & Yu, 2016). We also controlled for the age of the entrepreneur because age affects venture success (Azoulay, Jones, Kim, & Miranda, 2018). Moreover, we included gender (0 for men; 1 for women) due to its effect on venture fundraising (Malmström, Wesemann, & Wincent, 2020; Wesemann & Wincent, 2021).

Second, in terms of the venture’s attributes, we controlled for venture quality, the venture pitch year, and the industry. To account for quality differences among the ventures, we included venture quality, operationalized as the logarithm + 1 of prior sales (Sanchez-Ruiz, Wood, Michaelis, & Suarez, 2023). We followed previous entrepreneurial-finance research in controlling for industry effects on investment evaluations (e.g., Antretter, Sirén, Grichnik, & Wincent, 2020b; Matusik & Fitza, 2012) by including the venture’s industry using venture economic industry codes (VEIC).

Finally, for the pitch attributes, we controlled for variables that affect fundraising outcomes. Specifically, we controlled for the four LIWC language variables (Boyd et al., 2022) associated with assertiveness (McSweeney, McSweeney, Webb, & Devers, 2022): certainty, power, social, and tentative. Furthermore, we include the LIWC dictionary for emotion due to its effect on pitch outcomes (Allison, Warnick, Davis, & Cardon, 2022). Pitch year accounts for the circumstances of the broader economic environment (Rossi, Vanacker, & Vismara, 2023). Moreover, to reduce the effects of Shark Tank TV show artifacts, we followed prior research using Shark Tank data to control for episode (Antretter et al., 2025; Liao et al., 2024).

Results

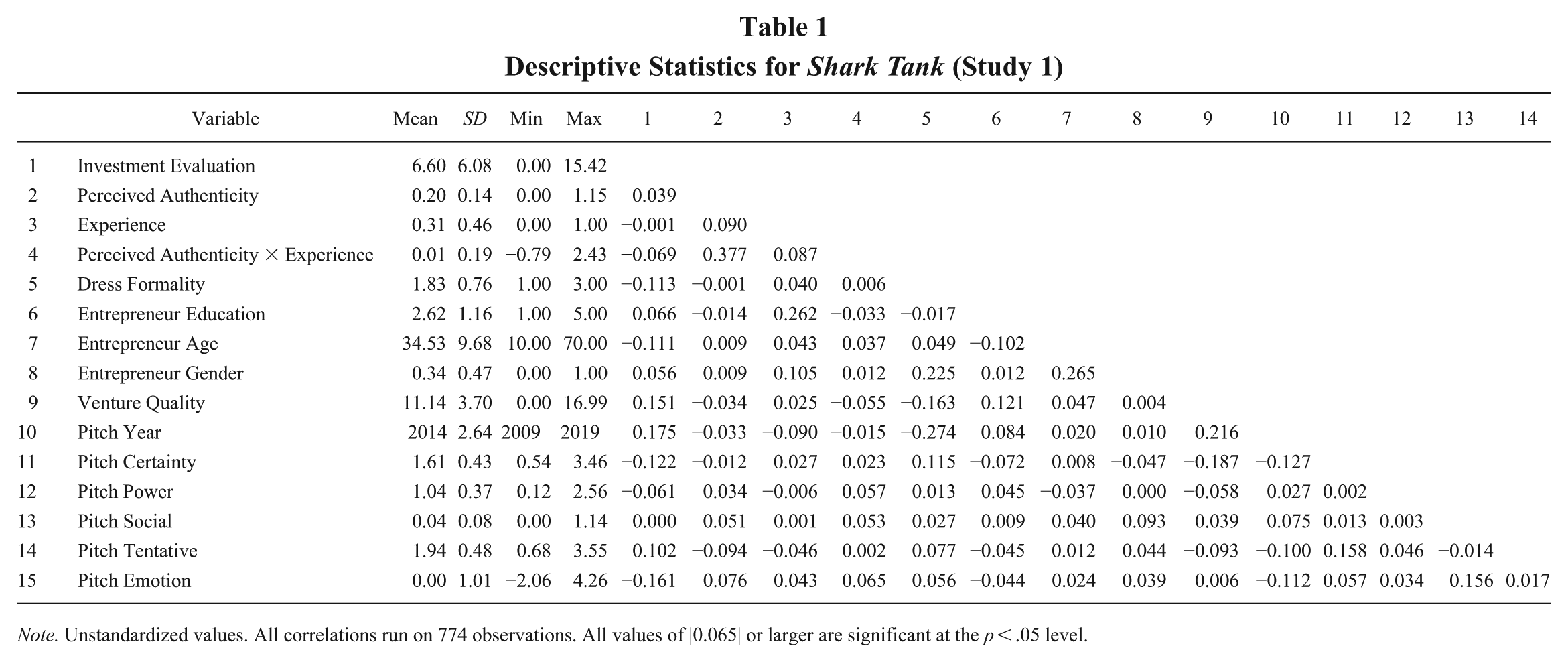

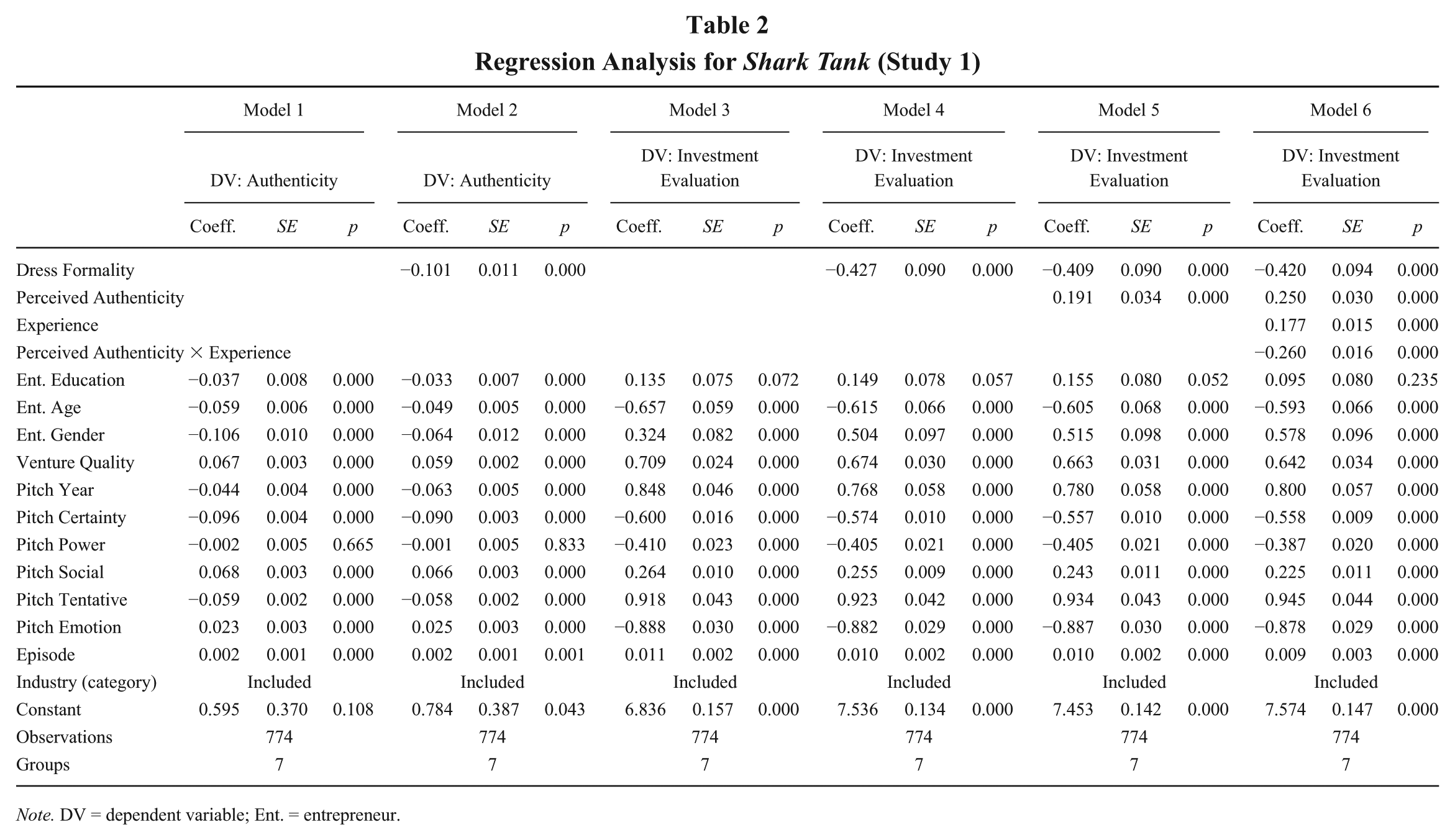

Table 1 reports the descriptive statistics and the correlations between the variables. We standardized continuous variables to reduce possible multicollinearity. Table 2 presents the results of the mixed-effects model. Models 1 and 2 have perceived authenticity as the dependent variable. Model 1 includes only the controls. Model 2 introduces dress formality and finds a significant negative effect on perceived authenticity (β = −0.101; p < .001), suggesting that investors perceive entrepreneurs wearing casual clothes during a venture pitch as more authentic than entrepreneurs wearing formal clothes. This finding provides support for Hypothesis 1.

Descriptive Statistics for Shark Tank (Study 1)

Note. Unstandardized values. All correlations run on 774 observations. All values of |0.065| or larger are significant at the p < .05 level.

Regression Analysis for Shark Tank (Study 1)

Note. DV = dependent variable; Ent. = entrepreneur.

Models 3 to 6 have investment amount (ln$ + 1) as the dependent variable. Model 3 includes only the controls. Model 4, which includes dress formality, shows that formal clothes are associated with significantly lower investor evaluations (β = −0.427; p < .001). Model 5 introduces perceived authenticity and indicates an association with significantly higher fundraising outcomes (β = 0.191; p < .001). These findings support Hypothesis 2: At a venture pitch, entrepreneurs perceived by investors as more authentic are evaluated more positively than those perceived as less authentic.

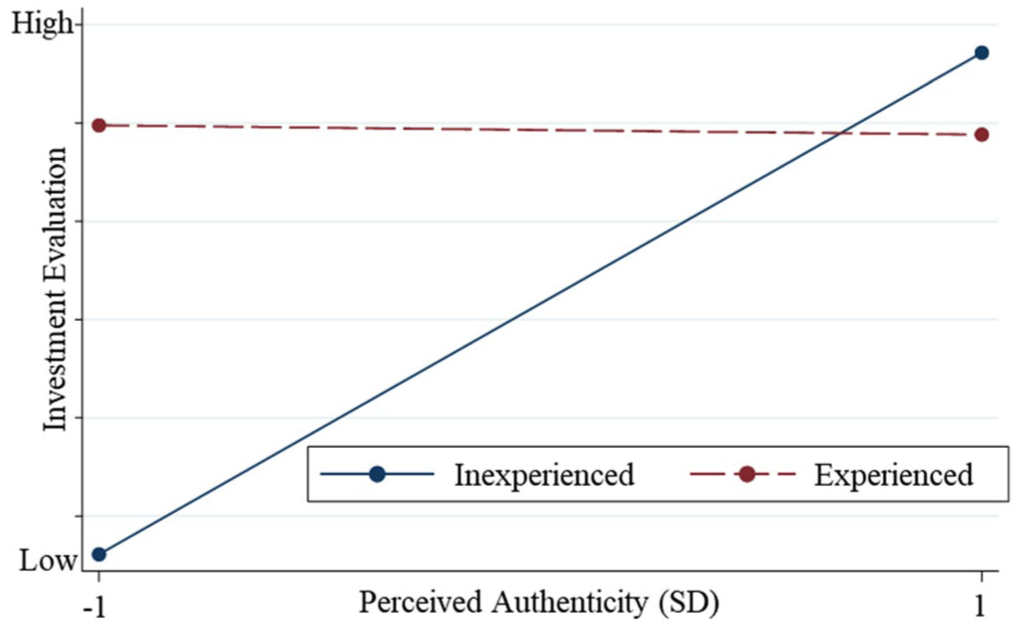

Model 6 includes the interaction effect of perceived authenticity and entrepreneurial experience, which is also significant (β = −0.260; p < .001). This suggests that the relationship between an entrepreneur’s inexperience and an investment evaluation is less negative for entrepreneurs perceived by investors as more authentic than those perceived as less authentic. Figure 1 depicts the moderated relationship. It shows that, at a venture pitch, the negative relationship between an entrepreneur’s lack of experience and investment evaluations is less negative for entrepreneurs perceived by investors as more authentic than for those perceived as less authentic. These findings support Hypothesis 4.

Impact of Perceived Authenticity × Prior Entrepreneurial Experience on Investment Evaluation (Study 1)

To assess the significance of the indirect effect, we transitioned from regression modeling to bootstrapping, which provides a more robust test for mediated relationships (Preacher & Hayes, 2008; Preacher, Zyphur, & Zhang, 2010). The analysis, which used 5,000 bootstrapped samples, revealed a significant indirect effect of dress formality on evaluation, mediated by perceived authenticity (indirect effect = −0.014, p = .002). This finding suggests that the entrepreneur’s dress formality is negatively associated with perceived authenticity and that perceived authenticity is positively associated with investment evaluations, providing support for Hypothesis 3. The index of moderated mediation (IMM; Hayes, 2015) was also significant (IMM = 0.027, SE = 0.004, p < .001), indicating that the indirect effect of dress formality on evaluation through perceived authenticity is moderated by entrepreneurial experience.

We also found considerable effect sizes. A shift from casual to formal clothes reduces average perceived authenticity by 3.88%. In addition, a one-standard-deviation increase in perceived authenticity leads to a 21.4% increase in the investment amount. Furthermore, perceived authenticity affects the degree to which experience matters (perceived authenticity × experience). More specifically, for inauthentic-seeming entrepreneurs (1 SD below the mean), prior experience increases investment evaluations by 14.75%. For entrepreneurs with average authenticity, the effect of experience is only 5.00%.

Robustness Tests

We conducted several robustness tests by excluding control variables and altering the clustering level in our mixed-effects models. First, we excluded all controls and found that dress formality remained a significant negative predictor of perceived authenticity (β = −0.125, p < .001). Perceived authenticity, in turn, positively influenced investment evaluations (β = 0.177, p = .003), while dress formality had a substantial negative effect on those evaluations (β = −0.881, p < .001). The moderation model confirmed a significant interaction between perceived authenticity and experience (β = −0.363, p < .001).

Second, we re-estimated all models using a revised perceived authenticity dictionary that we developed with the help of external experts (i.e., entrepreneurship professors) and practitioners (i.e., angel investors). These experts adapted the original dictionary by removing all words that they considered irrelevant to the venture-pitch context and adding other words that they considered appropriate. The resulting dictionary consists of: Blunt, Credible, Candor, Candid*, Earnest, Grounded, Natural, Original*, Raw, Really, Transparent*, and Trustworthy. After repeating our analyses with this dictionary, we found that the results remained consistent with our main findings. Dress formality is associated with significantly lower perceived authenticity (Model 2: β = −0.015, p = .007). It also significantly reduces the likelihood of investment (Model 5: β = −0.422, p < .001), while perceived authenticity positively predicts investment (β = 0.258, p < .001). Moreover, perceived authenticity moderates the effect of inexperience on investment evaluations (β = −0.299, p < .001). Overall, the pattern and strength of effects found when using the revised dictionary closely mirrored those from the original analysis, underscoring the robustness of our results.

Finally, we tested for restricted variance interactions (Cortina et al., 2019). Levene’s test showed marginal variance differences across perceived authenticity levels (p = .049). The difference in standard deviations was small—6.04 for high-perceived authenticity cases versus 6.12 for low-perceived authenticity cases—reflecting a variance decrease of 2.6%. This suggests that restricted variance may be present, meaning the observed moderation effect of experience could be somewhat conservative in its size.

Although recent studies have argued that TV-show data is an “ecologically valid environment for capturing salient effects that otherwise would be unobservable” (Sanchez-Ruiz et al., 2021: 10), we remain cautious when interpreting the results because the televised context of Shark Tank might make it less reliable as a research setting. We address these limitations by replicating Study 1 in Study 2 with field data from a more representative context: an angel group, which invested USD 156 million in startups from 2012 to 2024.

Study 2: Angel Group

Sample and Procedure

We collected data on 101 angel investments made between 2012 and 2024 through a large European angel-investment platform. Investors in this group primarily invested in early-stage ventures in computer-related industries (45.1%) and consumer products and services (14.71%). The average round size was EUR 1.26 million, and the average standard deviation was EUR 1.20 million (USD mean: 1.33 million, SD: USD 1.27 million), which is comparable to angel-group investments in other studies (e.g., Becker–Blease & Sohl, 2011; Wesemann Lekkas et al., 2025).

Entrepreneurs uploaded various information and a pitch video to the group’s deal platform. Based on this information, early-stage investors individually pursued investment opportunities. We had full access to investment details on 102 deals, and we collected additional data on these ventures and their entrepreneurs from PitchBook and LinkedIn. We dropped one observation where the entrepreneur wore job-specific clothes (i.e., a chef’s jacket in a food-delivery startup), reducing the final sample to 101 observations. No model VIF exceeded 1.75, and the highest VIF for one of the core variables was 1.45, indicating that multicollinearity is not a problem (Allison, 1999).

Measures

We operationalized our core variables in the same way as in Study 1. The dependent variable, investment evaluation, was the natural logarithm of the funds invested in EUR (Kanze et al., 2020). We operationalized dress formality with a three-item scale covering casual, business casual, and business clothes (Maran et al., 2021), and we operationalized perceived authenticity by applying the dictionary from Kovács et al. (2014) to the investor-assessment reports created for every venture after the pitch. These investor reports were typically 10 to 15 pages and contained sections on the business model, financials, market positioning, and the entrepreneur’s background. While much of the content was analytical rather than personal (e.g., product descriptions, finances, and product-market fit), certain sections—especially those covering the entrepreneur’s background and motivations—offered glimpses into the entrepreneur’s perceived authenticity. For example, one report said: “[The entrepreneur] not only takes on the role of a dedicated driver at [the venture], but he is also the authentic face of the startup externally and internally. He … uses all his experience and the network of impact entrepreneurs, reporters, and investors he has built up over the years to help [the venture] grow.” Another common feature was a discussion of why the entrepreneur started the business. These sections sometimes included direct quotes or paraphrased motivations, reflecting personal commitment.

We coded experience as 1 if the entrepreneur had founded a business before and 0 otherwise, as stated on LinkedIn or in the pitch deck (Ko & McKelvie, 2018). The control variables were the same as in Study 1, with three exceptions. First, we operationalized venture quality as the number of patents instead of prior sales, as the ventures in this angel network were largely pre-sales. Second, we included the variable video length (as the natural logarithm of length in seconds), as the entrepreneurs also shared a pre-recorded video with the investors. Third, we omitted the context-specific Shark Tank control episode, as it did not apply in this context.

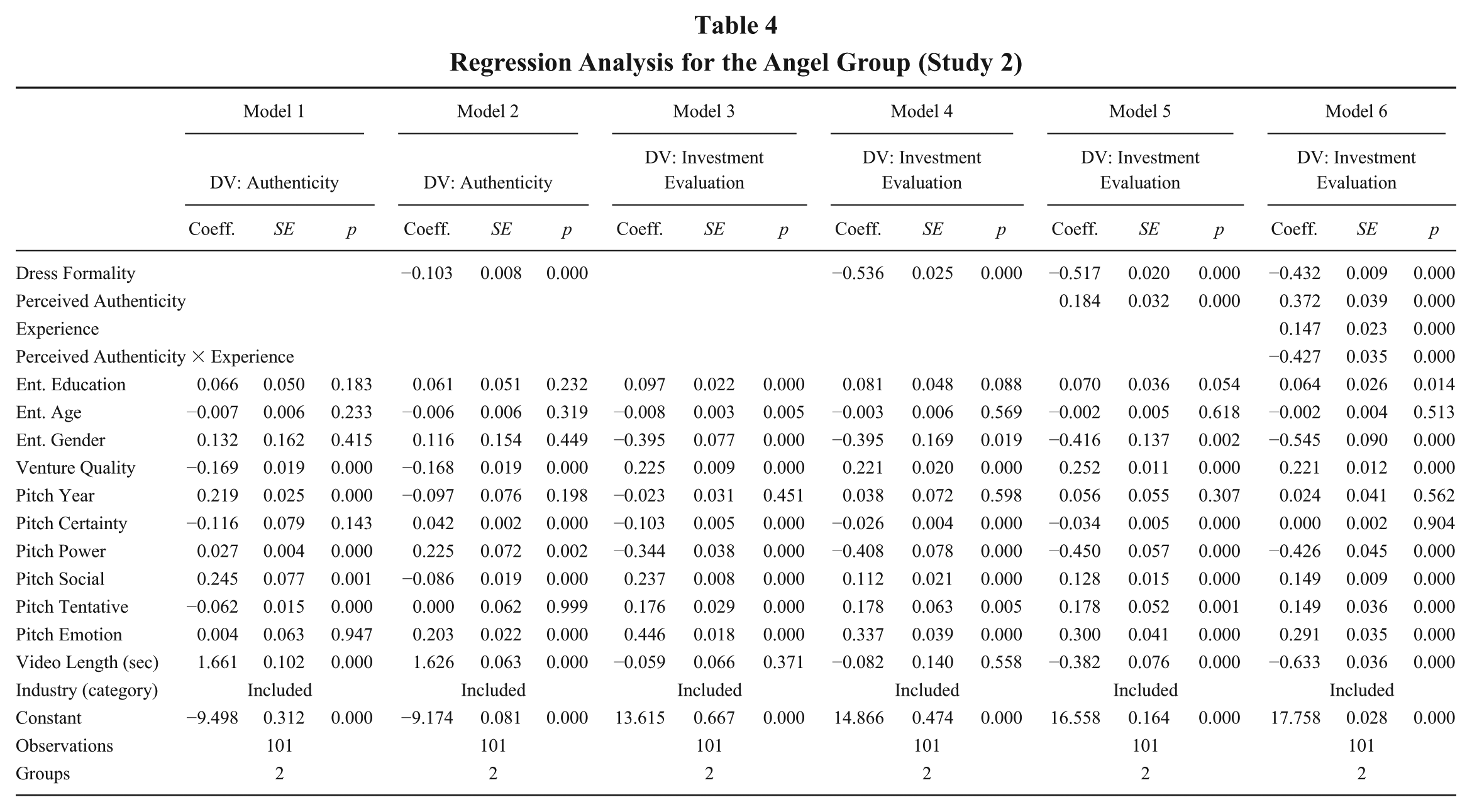

Results

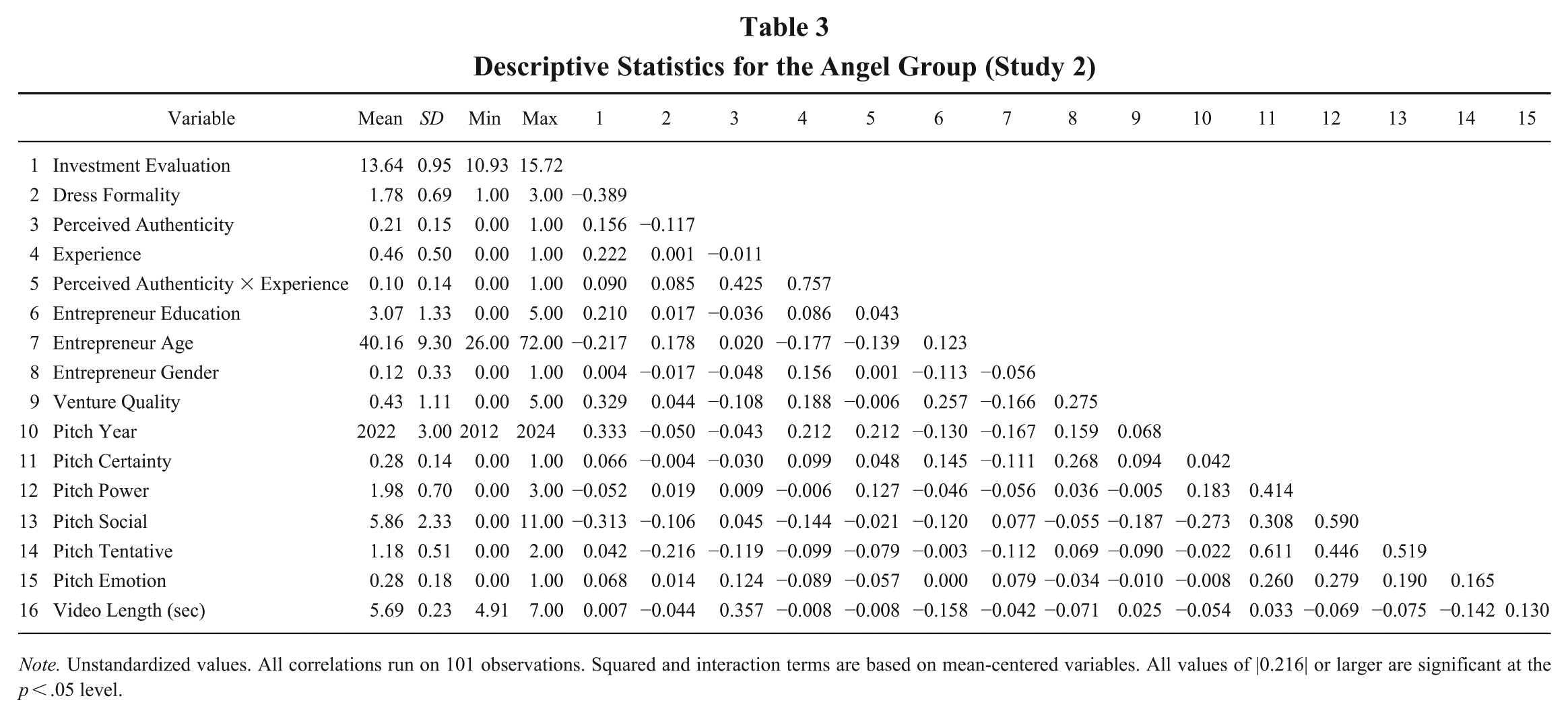

Table 3 provides the descriptive statistics and correlation matrix. We standardized continuous variables to account for possible multicollinearity concerns. Table 4 reports the regression results. Models 1 and 2 have perceived authenticity as their dependent variable. Model 1 contains only the control variables. Model 2 introduces the direct effect of dress formality on perceived authenticity and reveals a significant negative relationship (β = −0.103; p < .001). This finding indicates that investors perceive entrepreneurs wearing casual clothes during venture pitches as more authentic than entrepreneurs wearing formal clothes, supporting Hypothesis 1.

Descriptive Statistics for the Angel Group (Study 2)

Note. Unstandardized values. All correlations run on 101 observations. Squared and interaction terms are based on mean-centered variables. All values of |0.216| or larger are significant at the p < .05 level.

Regression Analysis for the Angel Group (Study 2)

Models 3 to 6 have investment evaluations (ln$ + 1) as the dependent variable. Model 3 contains only the controls in a model explaining investment evaluations. Model 4 introduces dress formality and finds a significant negative coefficient (β = −0.536; p < .001). Model 5 adds perceived authenticity and finds a significant positive coefficient (β = 0.184; p < .001), indicating that, at a venture pitch, the entrepreneurs who investors perceive as more authentic are evaluated more positively than entrepreneurs perceived as less authentic. This finding provides support for Hypothesis 2.

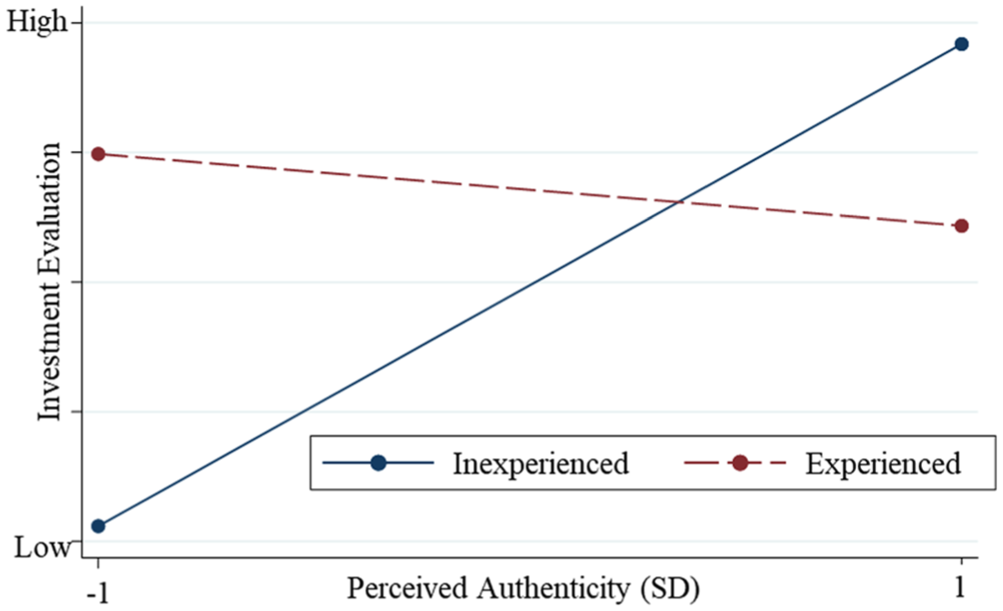

Model 6 introduces the interaction between perceived authenticity and entrepreneurial experience, and shows a significant negative coefficient (β = −0.427; p < .001). We plotted this interaction in Figure 2. These findings indicate that in venture pitches, the relationship between an entrepreneur’s lack of experience and investment evaluations is less negative for those entrepreneurs who investors perceive as more authentic than for those they perceive as less authentic, supporting Hypothesis 4.

Impact of Perceived Authenticity × Prior Entrepreneurial Experience on Investment Evaluation (Study 2)

To assess the significance of the indirect effect, we again transitioned from regression modeling to bootstrapping to provide a more robust test for mediated relationships (Preacher & Hayes, 2008; Preacher et al., 2010). The analysis used 5,000 bootstrapped samples to reveal a significant, indirect effect of dress formality on evaluation, mediated by perceived authenticity (indirect effect = −0.018, p < .001). The IMM was significant (IMM = 0.074, SE = 0.011, p < .001), indicating that the indirect effect of dress formality on investment evaluations through perceived authenticity is moderated by entrepreneurial experience.

We also calculated the effect sizes to better understand our findings. A shift from casual to formal clothes decreases perceived authenticity by approximately 48.2%. In addition, a 1 standard deviation increase in perceived authenticity leads to a 21.0% increase in investment evaluations. Furthermore, for inauthentic-seeming entrepreneurs (1 SD below the mean), experience increases investment evaluations by 77.5%. For entrepreneurs with average authenticity, the effect of experience is much smaller, at only 15.8%.

Robustness Tests

To confirm the robustness of our findings, we conducted several robustness tests. First, we excluded the control variables from our models. Even without controls, dress formality was a significant negative predictor of perceived authenticity (β = −0.169, p = .001), perceived authenticity continued to positively influence investment evaluations (β = 0.107, p < .001), and dress formality had a substantial negative effect on investment evaluations (β = −0.520, p < .001). The moderation model confirmed a significant interaction between perceived authenticity and experience (β = −0.383, p < .001).

Second, we conducted a parallel robustness test using the revised perceived authenticity dictionary described in Study 1. The results again aligned with our main findings. Dress formality was significantly associated with reduced perceived authenticity (Model 2: β = −0.169, p = .007). It also had a strong negative effect on investment (Model 5: β = −0.520, p < .001), while perceived authenticity positively predicted investment (β = 0.107, p < .001). Furthermore, perceived authenticity moderated the effect of inexperience on investment evaluations (β = −0.383, p < .001). These findings further reinforce the robustness and generalizability of our results.

Third, we tested for restricted variance interactions (Cortina et al., 2023). Levene’s test showed no significant differences in investment variance across authenticity levels (p = .11). This suggests that variance remains stable, and the observed moderation effect of experience is unlikely to be affected by variance suppression.

Study 3: Online Experiment

We followed best practices by testing our hypotheses using an experiment (Kleinert, 2024). Our experiment validated the findings of Studies 1 and 2 and established causality by ruling out alternative explanations through experimental manipulation. We pre-registered this experiment on aspredicted.org (https://aspredicted.org/6kxp-8bkc.pdf).

Sample and Procedure

Participants

We recruited participants with equity-investment experience using the online survey tool Prolific in October 2024 (for a similar approach, see Kleinert, 2024; Liao et al., 2024; Zunino et al., 2022). We restricted our sample to participants with investment experience in angel investments, venture capital, or crowdfunding; a home base in the United States; at least 10 previous submissions on Prolific; and at least a 98% approval rating for prior submissions. We invited 800 individuals to participate in our survey, and dropped individuals who failed our attention checks or did not complete the survey, which reduced our final sample to 714 observations. All model VIFs were 1.3 or lower, and the highest VIF for a core variable is 1.01, indicating that multicollinearity was unlikely to be a concern (Allison, 1999).

Design and procedure

We first informed participants that they would be shown a written summary of an early-stage investment opportunity with a photo of the entrepreneur and that they would have to evaluate the investment opportunity. We then showed them a randomly assigned picture of a professional model wearing casual clothes (jeans and a T-shirt) or formal clothes (suit and tie). The professional model in both pictures was the same person (a white man in his 20s), with the same pose and facial expression (a slight smile). The photograph frame, lighting, and background were also identical. After we showed the participants the picture, they received a short executive summary of the startup that ended with one of two prompts about the entrepreneur: (1) “John is a serial entrepreneur. He has founded and scaled multiple startups, including one that was acquired by an industry leader,” or (2) “John is an inexperienced entrepreneur. He has worked for several companies but has never founded or scaled a startup before.” The executive summary of the business was otherwise identical and pre-tested to avoid bias, as outlined by Lee and Huang (2018). We manipulated dress formality (0/1) and entrepreneurial experience (0/1) and combined them into a 2 × 2 between-subjects design.

Measures

Investment evaluations

To capture investment evaluations of the proposed opportunity, we followed Murnieks, Haynie, Wiltbank, and Harting (2011). We used three investment items measured on a 5-point Likert scale: (1) the probability of the participant investing in the opportunity (Riquelme & Rickards, 1992), (2) the amount of money the participant would be likely to invest (Elitzur & Gavious, 2003), and (3) how successful the participant expected the opportunity to be (Muzyka, Birley, & Leleux, 1996; Shepherd, Ettenson, & Crouch, 2000). The three items converged with a Cronbach’s alpha of 0.90.

Dress formality

We experimentally manipulated dress formality by showing participants pictures of the entrepreneur in casual clothes (coded as 0) or business clothes (coded as 1).

Perceived authenticity

We used the commonly used perceived authenticity scale from Barasch, Levine, Berman, and Small (2014). It includes four items, and asks participants whether the entrepreneur seems genuine, authentic, true to themselves, and real, on a 5-point Likert scale from strongly disagree to strongly agree. The four items converged with a Cronbach’s alpha of 0.93. We chose this measure because recent research has used it to investigate similar phenomena, like how describing one’s business ideas to other networking-event participants affects perceived authenticity (Gershon & Smith, 2020), how perceived authenticity affects later business-relationship formation (Rossignac-Milon et al., 2024), and how perceived authenticity judgments can deviate from reality (Bailey & Levy, 2022).

Experience

We manipulated entrepreneurial experience by showing participants two different prompts regarding the entrepreneur’s experience (see above). The variable was coded 0 for first-time founders and 1 for experienced founders.

Controls

We controlled for several factors related to the experiment participants: age, gender, education, and nationality. Age was included because participants’ perceptions and decision making can vary significantly across age groups (Seigner, McKenny, & Reetz, 2024). We controlled for gender (0 for men and 1 for women) due to documented differences in how male and female participants evaluate entrepreneurial pitches (Ding, Murray, & Stuart, 2013). We accounted for education due to the associated differences in judgment accuracy (Botelho et al., 2023). Lastly, we controlled for the participants’ nationality to account for cultural differences in how authenticity is perceived (Markus & Kitayama, 2010). However, due to the randomization, the inclusion of control variables is not strictly necessary, so we also ran all models without them. All significant results remained significant.

Results

We included two manipulation checks to test whether our experimental conditions affected participants’ perceptions. To avoid priming participants, we included these checks at the end of the survey, where we asked participants to rate the formality of the entrepreneurs’ clothes on a continuum from 1 = very casual to 5 = very formal. As expected, an ANOVA revealed that assessments of dress formality were significantly affected by our treatment condition, with entrepreneurs in the casual condition rated as less formal—F(4, 712) = 1709.93, p < .001—than entrepreneurs in the formal condition. Similarly, our experience manipulation showed that investors in the experienced condition scored higher than those in the inexperienced condition: F(4, 712) = 81.10, p < .001.

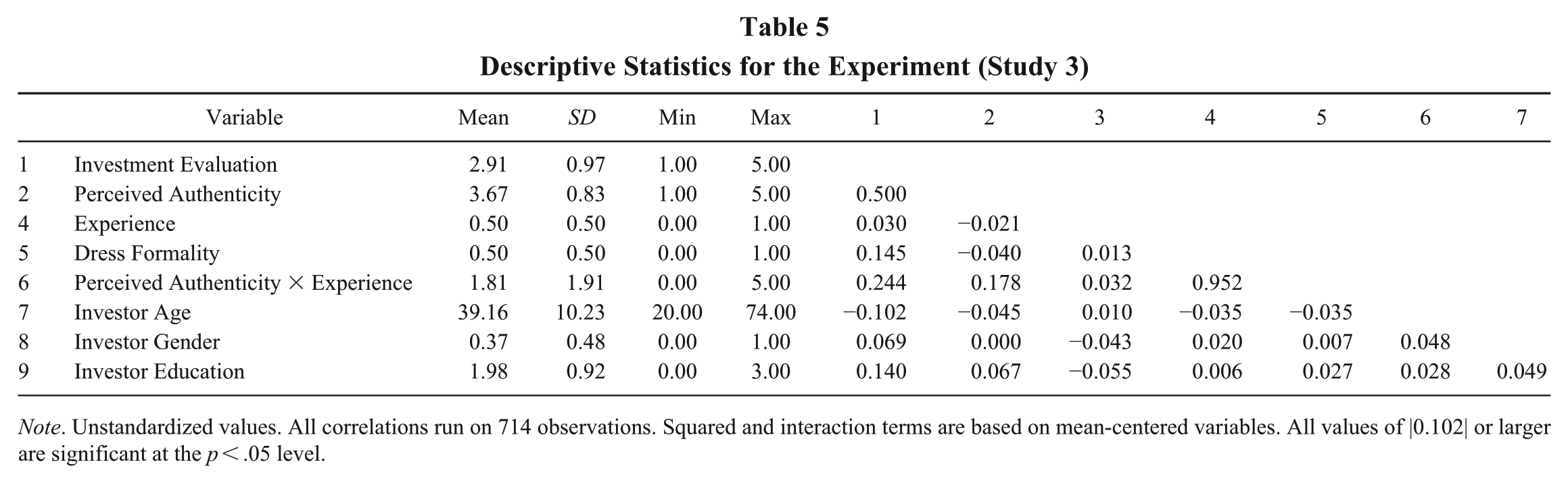

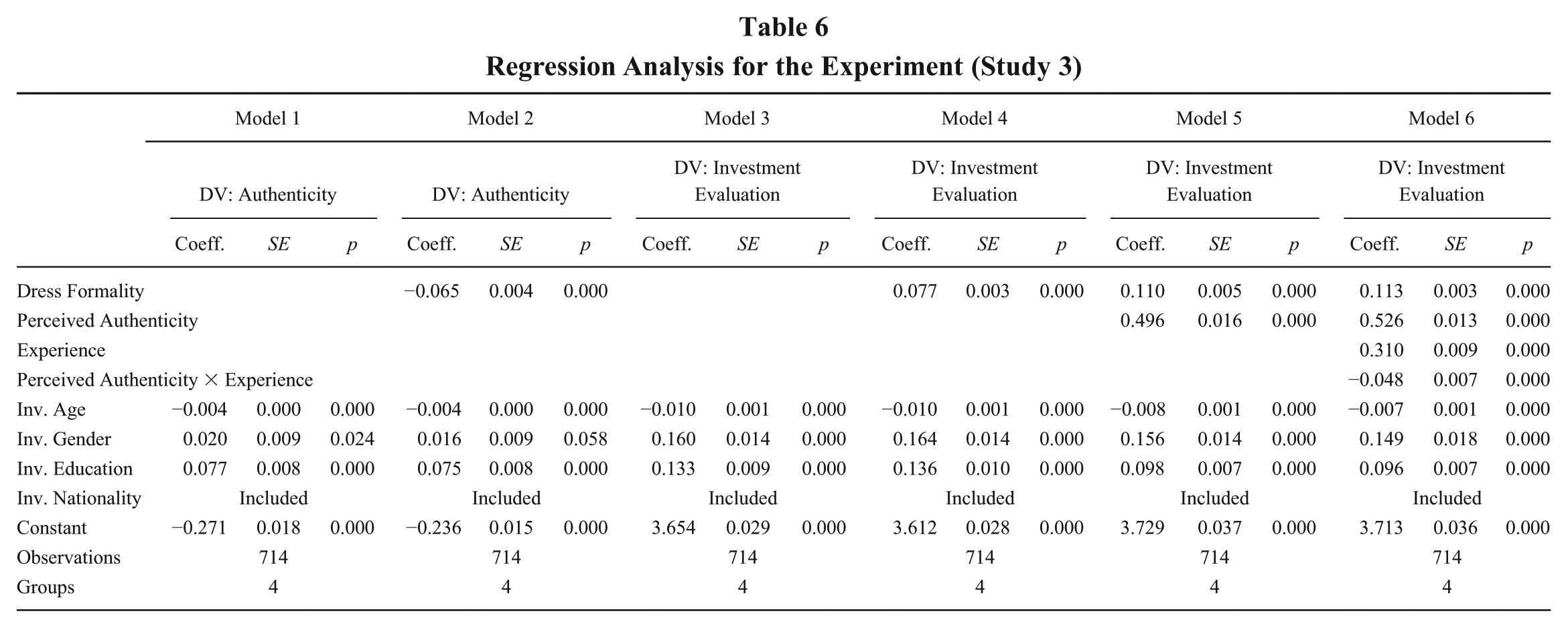

Table 5 shows the descriptive statistics, and Table 6 reports the regression results. Again, Models 1 and 2 use perceived authenticity as the dependent variable, while Models 3 to 6 use investment evaluation as the dependent variable. Model 1 only includes controls. In line with Studies 1 and 2, Model 2 shows that investors perceive entrepreneurs in casual clothes as more authentic than entrepreneurs in formal clothes (β = −0.065, p < .001), supporting Hypothesis 1.

Descriptive Statistics for the Experiment (Study 3)

Note. Unstandardized values. All correlations run on 714 observations. Squared and interaction terms are based on mean-centered variables. All values of |0.102| or larger are significant at the p < .05 level.

Regression Analysis for the Experiment (Study 3)

Model 3 includes the controls in the first investor-evaluation model, and Model 4 includes dress formality. Model 5 shows that entrepreneurs perceived as more authentic receive higher evaluations than those perceived as less authentic (β = 0.496, p < .001), which provides additional support for Hypothesis 2. Finally, Model 6 shows a significant interaction between perceived authenticity and experience (β = −0.048, p < .001). This suggests that perceived authenticity mitigates the negative effect of inexperience on investment evaluations. This finding supports Hypothesis 4.

We again tested our mediation and moderated mediation hypotheses with 5,000 bootstrapped samples. The analysis revealed only a marginally significant indirect effect of dress formality on investment evaluations through perceived authenticity (indirect effect = −0.017, p = .058). This suggests that dress formality influences evaluations through perceived authenticity, especially when experience is considered. This was the first time one of our results was only marginally significant and only partially supported Hypothesis 3. However, our moderated mediation analysis shows that the IMM was also significant (IMM = 0.002, SE = 0.001, p = .008), indicating that the indirect effect of dress formality on investment evaluations through perceived authenticity is moderated by entrepreneurial experience.

The effect sizes were also substantial. A move from casual to formal attire reduced perceived authenticity by 8.75%. In addition, a 1 standard deviation increase in perceived authenticity led to a 55.7% increase in investor-evaluation scores. Notably, the effect was approximately 22.3% greater for less experienced entrepreneurs than for their more experienced counterparts. In terms of the overall moderation (dress formality × experience), experience increased investment evaluations by 77.5% for inauthentic-seeming entrepreneurs (−1 SD). For entrepreneurs with average perceived authenticity, the effect of experience was much smaller, at only 15.8%.

Robustness tests show that our results also hold without control variables: Formal clothes are associated with lower perceived authenticity (β = 0.044, p = .002), perceived authenticity is associated with higher investment evaluations (β = 0.494 p < .001), and the link between prior experience and investment evaluation is moderated by perceived authenticity (β = 0.048, p = .013). Finally, we tested for restricted variance interactions (Cortina et al., 2023). Levene’s test showed marginal variance differences across authenticity levels (p = .050). The standard deviation in evaluations was slightly lower for high-perceived authenticity cases (SD = 0.88) than for low-perceived authenticity cases (SD = 0.90), reflecting a variance decrease of 3.4%. This provides limited evidence of variance restriction, suggesting that the observed moderation effect of experience may be slightly conservative in magnitude.

Discussion

Using three studies, we found that the initial impressions on investors that entrepreneurs generate by wearing casual clothes increase perceived authenticity, thereby improving investment outcomes. Moreover, we found that perceived authenticity makes investors less sensitive to other information that is revealed later. These findings support the view that early visual impressions serve as a powerful lens through which investors interpret subsequent information (Connelly et al., 2011; Drover et al., 2018). The perceived authenticity derived from something as simple as casual clothes can anchor investors’ perceptions, leading them to overlook or discount critical signals that would otherwise influence their decisions. This influence of dress raises important questions about the role of heuristics and biases in investment evaluations, especially when decisions are made quickly and under uncertainty. Bounded rationality limits early-stage investors’ capacity to process information, so they often rely too much on initial impressions and too little on subsequent signals (Butticè et al., 2022). This bounded rationality makes initial perceptions of entrepreneurs impactful and long-lasting (Aversa et al., 2021).

While traditional investment strategies focus on preventing poor investments, as illustrated by the adages of Warren Buffet, such as “Rule No. 1: Never lose money. Rule No. 2: Never forget rule no. 1” (Lowe, 2007: 116), early-stage investors are imaginative risk-takers willing to take a leap of faith to be part of an interesting vision (Huang & Pearce, 2015). If an entrepreneur makes a strong initial impression, investors often shift from a critical evaluation to active support and form a shared vision, for example, of how the venture might transform an industry. Our interviewees echoed this mindset: once convinced, they look for ways to support the venture, not reasons to reject it.

Theoretical Contributions

Our study contributes to the literature on appearance-based judgments, authenticity in organizations, and signaling.

Appearance-based judgments

We contribute to the literature on visual impressions and appearance-based judgments in organizational contexts (Clarke et al., 2019; Huang et al., 2023). While formal clothes benefit managers (Maran et al., 2021), physicians (Dacy & Brodsky, 1992), and professors (Morris et al., 1996), we show that the opposite holds true in entrepreneurship: casual clothes improve fundraising outcomes. We explain this difference by highlighting that “traditional” sectors tend to value formal clothes because they signal reliability and conformity (Forsythe et al., 1985; Rafaeli & Pratt, 1993), but the startup sector favors casual clothes because they seem to indicate authenticity. We argue that this is because, in entrepreneurship, a clear understanding of what makes another person tick is crucial for trusting them to navigate the volatile and uncertain venture future (Fisher, Stevenson, Neubert, Burnell, & Kuratko, 2020). Therefore, the impact of dress formality on others’ evaluations depends on the norms of the field, which are shaped by the relative prevalence and acceptance of choices (Cohen & Basu, 1987). Our findings thereby address calls to study how “entrepreneurs utilize their dress to . . . convey information about themselves to potential stakeholders” (Clarke, 2011: 1380). The effect of clothes-based, initial perceptions should not be underestimated: initial perceptions form rapidly (Mann & Ferguson, 2015), and negative perceptions have exceptionally long-lasting effects (Uleman & Kressel, 2013). Clothes can create “an appropriate scene to stakeholders” (Clarke, 2011: 1367) that provides the necessary “epistemic glue” (Rossignac-Milon et al., 2024: 4) to convince others, making them a powerful interpretive lens (Chang & Cortina, 2024).

Perceived authenticity

We challenge the foundational assumption that perceived authenticity reveals inner truth, arguing instead that perceived authenticity tends to reflect surface-level impressions shaped by context and weak signals. While authenticity is often idealized as “bring your whole self to work” (Pillemer, 2024: 1654), recent work suggests that this ideal is aspirational at best and misleading at worst (Bailey & Levy, 2022; Caza, Moss, & Vough, 2018). In fast-paced, high-uncertainty settings like venture pitches—where interactions are brief, information is sparse, and dialogue is largely unidirectional—investors lack access to substantive signals of an entrepreneur’s self-awareness, morality, and transparency (Gardner et al., 2011; Gill & Caza, 2018). Therefore, they rely on superficial but salient signals, such as how the entrepreneur dresses. This creates space for strategic authenticity signaling (Pillemer, 2024): Entrepreneurs can curate the appearance of authenticity through clothes that convey self-expression without offering deeper evidence of alignment between inner states and outer actions. Our study highlights this perceptual vulnerability and provides a concrete example of how perceived authenticity can form in the absence of meaningful verification.

However, the effects of perceived authenticity do not end with first impressions. They also matter for downstream judgments, where perceived authenticity can mask weaknesses by reducing investor sensitivity to later, negative information. Here, perceived authenticity acts as a cognitive anchor that shapes how subsequent information is interpreted or ignored. As a result, early-stage investment decisions may hinge less on the later content of a pitch than on how well entrepreneurs can create a sense of shared reality with investors (Echterhoff & Higgins, 2017; Hardin & Higgins, 1996; Higgins et al., 2021). Collectively, these findings address calls to explore the role of perceived authenticity under extreme uncertainty (Bai et al., 2020) and its role in shaping investors’ decisions (Soublière & Gehman, 2020). We decouple authenticity perceptions from inner truth, and show how even signals meant to indicate honesty can be used to manipulate impression formation. This responds to calls to study the “dark side of authenticity” (Cha et al., 2019: 655) as well as the “negative consequences of authenticity” (Gardner, Karam, Alvesson, & Einola, 2021: 5).

Signaling theory

Finally, we respond to calls to extend signaling theory in venture investments and study “how receivers meaningfully aggregate signals” (Colombo, 2021; Connelly et al., 2011: 60), thereby contributing to the cognitive view of signaling research (Drover et al., 2018). Specifically, we explore the interplay between initial visual cues and later strong (i.e., diagnostic) signals (Drover et al., 2018; Kleinert, 2024; Steigenberger & Wilhelm, 2018; Vanacker, Forbes, Knockaert, & Manigart, 2020). Much of the conversation on signaling theory concentrates on simultaneously interpreted signal sets (e.g., Connelly et al., 2011; Steigenberger & Wilhelm, 2018), where the stronger signal takes precedence in the evaluation (Drover et al., 2018). We add a caveat to this approach by highlighting the effect of the signal sequence: even low-validity visual cues (e.g., clothes) can overshadow important later information (e.g., lack of experience) when first impressions prove sticky (Mann & Ferguson, 2015). As a result, sequence, rather than valence, emerges as a critical parameter in signal interpretation and provides an alternative (or additional) assessment hierarchy for signals.

The importance of the signal sequence also represents an interesting extension of recent research by Bailey and Levy (2022), which finds that people are “intuitive psychologists” (p. 799) who assume that they can reliably judge other people’s dispositional characteristics but are rather bad at doing so. This overconfidence seems particularly problematic in venture investments, where investors often pride themselves on having a good eye for character and “investing in people, not ideas” (e.g., see Maxwell et al., 2011; Wang, Chen, Zhu, & Wang, 2020). In our empirical studies, investors quickly and superficially made authenticity judgments that led them to disregard later important information. However, based on Bailey and Levy (2022), investors may believe their authenticity judgments are accurate when, in fact, they are not—a proposition that should be tested in future research.

Boundary Conditions, Limitations, and Future Research

While our findings reveal interesting patterns, we must also consider their generalizability. First, our research focuses on specific early-stage investment contexts (i.e., Shark Tank in Study 1, an angel group in Study 2, and equity investors in Study 3) that do not fully represent all investment contexts or stages. Notably, the investors in our studies did not receive venture information before they saw the pitch. This is a defining feature of Shark Tank (Study 1; Herjavec, 2024), a function of how angel-group organizers communicate with group members (Study 2), and a feature of our experimental design (Study 3). However, in many contexts, investors review venture dossiers before hearing a pitch, which may influence their responsiveness to visual cues, such as clothing. Prior exposure could theoretically strengthen or weaken our observed effects—prior impressions may serve as an anchor that reduces sensitivity to clothes, or they may strengthen the effect because entrepreneurs are measured against more defined expectations, potentially causing disappointment. Second, we acknowledge that perceptions of authenticity might differ in professions with job-specific clothes, especially outside entrepreneurship. For example, a police officer or a doctor may have to wear “appropriate” attire to be perceived as authentic. Similarly, the context might matter—an entrepreneur asking for a loan in a bank might benefit from wearing a suit, as a bank is a more formal setting. Third, the quality and fit of clothes can vary greatly. These clothing attributes can give investors additional information about the entrepreneur, such as insights into their disposable income and their attention to detail. Lastly, our research captured investors’ reactions immediately after a pitch but did not account for potential later exchanges. While we have no reason to believe that perceptions of authenticity based on appearance are less permanent than other first impressions, there may be differences to be explored.

Our work also has limitations that offer opportunities for future research. First, perceived authenticity is not static (Hannan et al., 2019) but manifests in action (Gouvard, Goldberg, & Srivastava, 2023) and can change over time (Dobrev & Verhaal, 2024). Future research could investigate how appearance and action jointly affect perceived authenticity. Second, we focused on perceived authenticity and, thereby ignored whether the entrepreneurs also felt authentic. Therefore, we join Bolino et al. (2016) in calling for the study of the intentionality behind signals, and whether they are honest or deceptive. Third, while prior research highlights the benefits of formal clothes in mature companies, we found that casual clothes are more effective in new ventures. Future research may study the point of maturity at which this evaluation changes. Fourth, not all investors see pitches without prior preparation. As such, they may already have some background knowledge about the company and its founder when they meet the entrepreneur for the first time. We hope future research will explore how prior exposure to information affects the relationship between an individual’s clothes and the evaluator’s perception of authenticity. Fifth, future research could examine when the effects of clothing-based authenticity signals are weakened, nullified, or reversed. For example, experienced investors (especially those with negative past experiences) may resist surface-level impressions (Blohm et al., 2022). Cultural norms also shape what is seen as authentic (Wesemann & Antretter, 2022); casual dress may signal approachability in one context but seem unprofessional in another. Other moderators could include pitch format (e.g., video vs. in-person), evaluation structure (e.g., group vs. solo), or investment stage (e.g., seed vs. Series A). Identifying such boundary conditions would be helpful. Sixth, while we focused on perceived authenticity, prototypicality—representing “the clearest cases of category membership” (Rosch, 1978: 36), like a chef’s hat signaling the culinary profession—offers interesting research opportunities. For example, certain stylized clothing clichés—such as Steve Jobs’s iconic look (i.e., a black turtleneck, round, frameless glasses, jeans, and white sneakers)—have come close to becoming a visual prototype of a visionary entrepreneur. The consequences of “copying the look” remain unclear. On one hand, doing so may signal alignment with a recognizable entrepreneurial archetype (Tajfel, Billig, Bundy, & Flament, 1971). On the other hand, it may appear performative or derivative, and consequently raise concerns about inauthenticity. Given how strongly entrepreneurship values individuality, authentic self-expression may have become an entrepreneurial prototype, suggesting a paradox in which being unique is the norm.

Practical Implications

Our research shows that first impressions formed through visual cues, such as clothing, can affect perceived authenticity and bias interpretations of subsequent signals. To avoid assigning too much weight to early impressions, investors may benefit from reviewing quantitative business data before meeting entrepreneurs, thereby reducing the influence of visual cues. Entrepreneurs, in turn, should be aware of how clothing shapes impression formation and strategically use that knowledge to support their pitches. For example, inexperienced entrepreneurs might consider dressing casually to take advantage of the identified authenticity bias, potentially reducing the salience of their inexperience in investors’ eyes.

Conclusion

We draw on a cognitive perspective of signaling theory to examine whether entrepreneurs’ dress formality shapes early-stage investors’ funding decisions. Across three samples, we find that an entrepreneur’s clothing choices shape investors’ perceptions of authenticity in ways that can lead to more favorable evaluations and overshadow later signals, such as information on the entrepreneur’s inexperience. Our results demonstrate that perceived authenticity can function as a cognitive anchor in investment evaluations.

Footnotes

Appendices

Acknowledgements

We would like to thank Julio De Castro, Rachida Justo, Cristina Cruz, and Benedikt Seigner for their feedback on an earlier version of this article. Henrik Wesemann Lekkas acknowledges support from Project PID2024-155788OA-I00 funded by MICIU /AEI /10.13039/501100011033 / FEDER, UE. There are no competing interests for any of the authors.