Abstract

The shift to renewable energy is at the heart of meeting worldwide climate goals and securing long-term energy security. This paper provides an in-depth overview of the integration of renewable energy sources (RES) into deregulated electricity markets with emphasis on the key roles of energy storage systems (EES), electric vehicles (EVs), and policy innovations. Since renewable energy sources like solar and wind are inherently variable, their smooth integration demands cutting-edge technologies, such as smart grids, real-time monitoring, and predictive analytics, to provide grid stability and reliability. Energy storage systems and electric vehicles have a dual function in balancing power supply-demand fluctuations and ancillary grid services support. The paper discusses market mechanisms like power purchase agreements (PPA), renewable energy auctions, and competitive bidding, which are crucial in deregulated markets for facilitating innovation and competition while ensuring energy security. In addition, an indicative financial analysis is included to show the investment feasibility of renewable projects based on parameters such as Net Present Value (NPV), Internal Rate of Return (IRR), and payback periods. These findings support the economic viability of incorporating renewables, especially when integrated with energy storage. The research also pinpoints obstacles like forecasting errors, grid congestion, and regulatory hurdles, and suggests anticipatory measures like grid modernization, dynamic pricing, and stakeholder engagement. Finally, the paper emphasizes that an integrated, technology-based, and economically viable framework for renewable energy deployment in deregulated markets is crucial to developing a sustainable, low-carbon energy future.

Introduction

The growing global concern with the reduction of greenhouse gas emissions and the fight against climate change has brought renewable energy as the basis for modern electricity production. It has several important environmental benefits since electricity can be produced without releasing carbon dioxide (CO2) or other greenhouse gases emitted when fossil fuels are burned. These technologies are inherently sustainable in that they use sufficient natural resources and provide long-term energy security while addressing crucial environmental challenges. This reduces greenhouse gas emissions, as the electrical grid expands with a share of renewables. It also diminishes dependence on finite fossil fuel reserves, thereby promoting global climate action. Apart from these environmental advantages, this shift opens the opportunity for flexible, low-carbon energy infrastructure to potentially allow a resilient and sustainable power system. However, the variability and intermittency of renewable sources are mainly because of factors like weather, diurnal cycles, and seasonal variations. Therefore, the integration of these renewable sources into the grid will need to be done unobtrusively. For this purpose, advanced technologies such as smart grids, energy storage systems, and real-time energy management solutions would be necessary (Nayak et al., 2023). The reliability of the grid would be maintained by ensuring the balance between supply and demand as excess energy will be stored during periods of high renewable generation and released when production is low.

Smart grids have embedded sensors, communication networks, and learned control systems that enable the optimization of the distribution and usage of renewable energy. Such systems allow for dynamic responses to varying generation and demand, make possible the integration of distributed energy resources (DER), and improve the stability of the entire grid. Such systems include lithium-ion batteries, pumped hydro storage, new technologies such as flow batteries, and compressed air energy storage (Kumar et. al., 2025). Energy storage is a very useful tool in the management of variability from renewable sources (Kumar et. al., 2022) (Latif et al., 2021) (Patil et al., 2022). These technologies capture excess energy and release it at peak demand or low-generation periods to keep the supply of power smooth and reduce reliance on backup fossil fuel-based generation. Apart from the above factors, real-time management systems use artificial intelligence (AI) and machine learning (ML) algorithms to predict renewable generation patterns, optimize the dispatch schedule, and further enhance grid efficiency. Renewable energy integration in the deregulated electricity market frameworks has both challenges and opportunities. Deregulated markets introduce a competitive environment wherein multiple private entities are allowed to participate in electricity generation, transmission, and distribution. It will have an open structure, innovate, cut costs, and diversify the choices available to the consumer. The introduction of renewable energy will help enhance the mix of energy in such markets and add to the diversity in competition, thus fortifying the power grid to be resilient. Key among these mechanisms include Power Purchase Agreements, renewable energy auctions, and competitive bidding processes. There could exist a direct supply between independent renewable power producers, say a solar or wind farm, and a utility or large customer. That immediately makes it a short-term market that reacts to any changes in the market conditions of supply and demand. Hence, independent system operators (ISOs) and regional transmission organizations (RTOs) are helpful to have them in the deregulated markets. ISOs and RTOs allow for coordinating real-time grid operations, energy trading, and system balance. These mechanisms also counterbalance some of the variabilities associated with renewable energy resources. They also perform demand response programs, which allow consumers to alter their energy use relative to the conditions of the grid and add sophisticated forecasting tools to forecast renewable output more effectively. Besides, these organizations are also in favor of the deployment of energy storage, therefore enabling the grid to absorb variability and maintain system reliability. It also fosters technological innovation, especially through hybrid systems that combine renewably generated power with either energy storage or complementary generation. For example, hybrid installations can integrate solar and wind along with battery storage, which yields consistent power output while extracting maximum resource utilization. Time-of-use pricing and ancillary service markets offer market-based incentives for flexibility and grid-support capabilities. In an overview, the integration of renewable energy into deregulated electricity markets presents a transformative approach to achieving sustainable low-carbon energy systems. This is ensured by the erudite grid technologies encouraging competition while promoting innovation so that this will utilize renewable sources with the reliability of the grid and with economic efficiency. This kind of integrated approach is also consistent with the global climate objectives while serving the purposes of long-term energy security and resilience from changing market dynamics and environmental concerns. The key highlights of the paper are as follows:

The paper stresses the importance of integrating renewable energy into deregulated electricity markets. It points out the transformative effects of competitive market dynamics, which are made possible by mechanisms such as PPAs, renewable energy auctions, and advanced grid technologies. Major enablers that address supply-demand balancing issues while mitigating the variation in renewable sources are said to be smart grids with advanced energy storage solutions. Lithium-ion batteries, pumped hydro storage, and compressed air energy systems have been identified as major technologies improving the stability and reliability of grids. Policies and technological innovations play an important role in the realization of renewable energy targets. The paper focuses on the importance of stakeholder cooperation in formulating policies that promote renewable energy adoption and facilitate sustainable energy transitions. The use of renewable energy decreases GHG emissions and climate impacts and hence creates a scope for improving economic development with increased employment and emerging industries related to the field of renewable energies. The addition of DERs results in better resilience and efficiency of a system. The paper addresses issues including grid integration intermittency of renewable energy sources, and regional disparity, among others. It promotes scaling up capacity, deploying advanced storage solutions, infrastructure upgrades, and policy improvements to achieve ambitious targets like India's 2030 goal of adding 500 GW of non-fossil fuel energy capacity.

These highlights collectively underscore the paper's focus on advancing renewable energy integration, leveraging technology, and driving sustainability in competitive energy systems.

Current status of energy in India

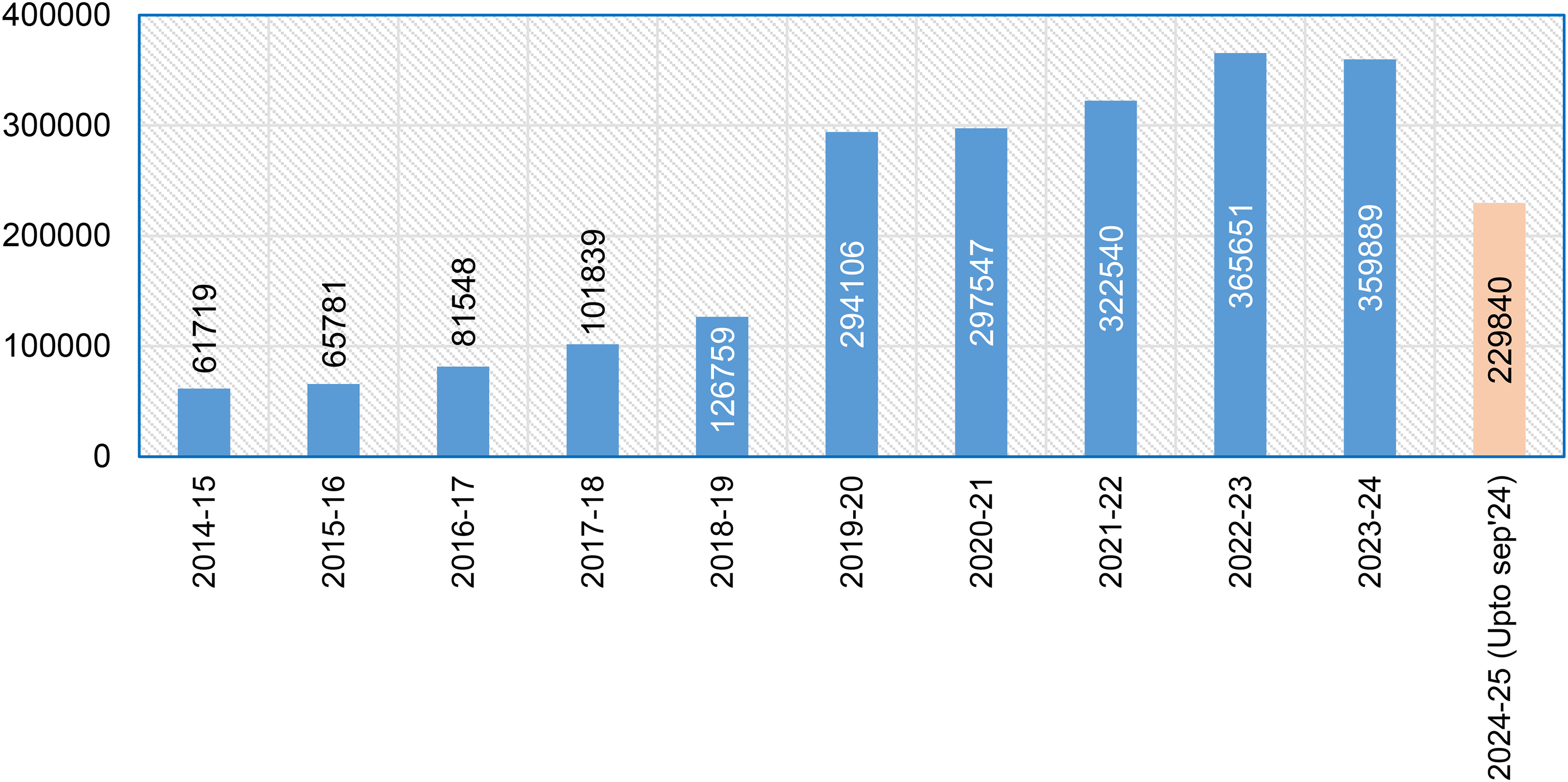

The load generation balance report (LGBR) for 2024–25 provides a detailed appraisal of the contemplated power supply scenario over India. Such comprehensive assessment consists of all possible generating stations together with the availability of their conventional or renewable sources, and all crucial factors like available fuels as well as resources of water that are indispensable for the hydroelectric mode of generation. These are the reasons for the reliability and balance of the supply of electricity throughout the year. The conventional capacity addition of 19,680 MW is scheduled for 2024–25. The planned capacity additions under the conventional sources have been split between various sources such as thermal, which will add 14,040 MW, hydel 3790 MW, and nuclear sources to contribute 1900 MW (CEA, 2020). This expansion will help strengthen and make the power sector more reliable. In addition, this capacity addition merges with the government's vision of adequately meeting growing energy needs while mitigating peak load demands. The LGBR shows an overall energy surplus in India at 2.4% during the fiscal 2024–25. However, a peak deficit of 4.3% is forecasted in the final generation plan for the same period. These projections highlight the ability of the current and new generation infrastructure to meet normal energy requirements and also provide some room for unexpected contingencies that might arise. Some of the contingencies could be brought about by changes in the weather conditions, unexpected loss of generating units, or some unexpected rise in power demand. In practical terms, the report reiterates that the actual energy available will be almost equivalent to the needed energy for the operational stability of the national grid. Total energy requirement and supply both saw huge growth in the fiscal year 2023–24. On the whole, energy requirements have risen by 7.7%, and the supply has risen by 7.9% in the last fiscal year. Likewise, the highest peak witnessed an increase of 12.7%, where the peak met rises by a remarkable 15.8% during the fiscal year 2022–23. These statistics ensure that on the supply side also, demand has been easily matched which reflects operational competence and sound management within the power fraternity.

The data indicates there is only a small degree of mismatch between demand and supply levels in both energy and peaking terms during the fiscal year of 2023–24. Nonetheless, the report asserts that the mismatch was strongly driven by factors not by the insufficiency in power availability. For instance, some of these have been ascribed to externality issues such as grid limits, inefficiencies in distributions, and localized outages. This is important for policymakers and stakeholders to address systemic issues without blaming the gap on generation shortfalls. An important takeaway from the LGBR is the difference between projected and actual figures of energy demand and peak demand during the fiscal year 2023–24. The actual energy requirement was 2.5% over the forecast, and it turned out that the actual peak demand by 6.2% of the forecast (CEA, 2020). These kinds of deviations were mainly ascribed to extreme weather incidents. For example, an extraordinary heat wave occurred which caused an unexpected increase in consumption of energy. That makes a case for the adaptation of dynamic and adaptive types of forecasting models that adjust their parameters according to different sorts of climatic variabilities. The LGBR 2024–25 results do indicate that India continues its efforts to improve the capability and deliverability of the power sector. The increase in proposed conventional capacity along with dependence on renewable energy would help resolve both short-term and medium-term energy gaps. Based on proactive action to solve the potential gaps between supply and demand with the employment of sophisticated forecast techniques, India's power sector is bound to help meet the aspirations of the economy and guarantee energy security for the country. This strong planning framework leads to resilience against predictable and unforeseen challenges, opening the door to sustainable and reliable energy.

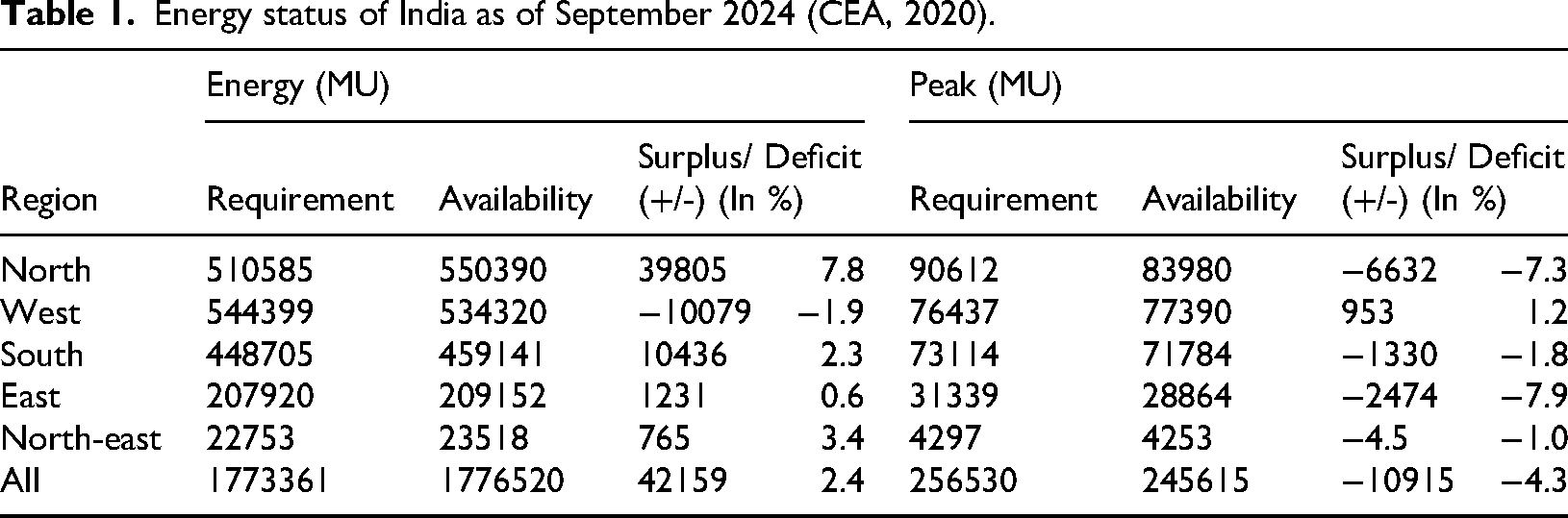

The energy status of different regions in India reflects a significant regional variation in the availability, requirement, and surplus or deficit of energy which are depicted in Table 1. The North region has a notable surplus of 39805 MU (7.8%), which means that this region has sufficient energy generation compared to its requirement of 510585 MU. However, its peak availability is short by 6632 MU (−7.3%), reflecting challenges in meeting peak demand of 90612 MU (CEA, 2020). The West region experienced an energy deficit of 10079 MU (−1.9%), though it managed a peak surplus of 953 MU (1.2%), suggesting a more balanced peak demand and supply.

Energy status of India as of September 2024 (CEA, 2020).

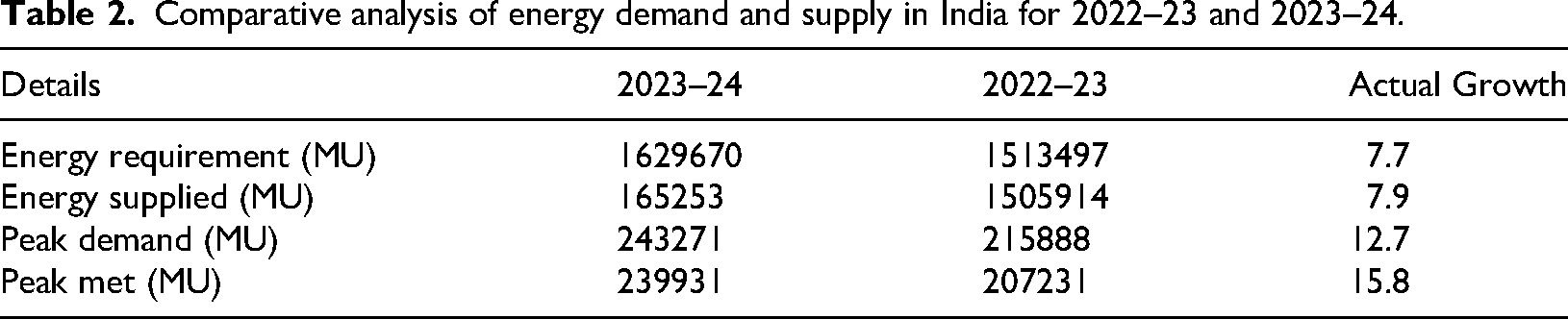

The South region recorded an energy surplus of 10436 MU (2.3%) against the requirement of 448705 MU but faced a peak deficit of 1330 MU (−1.8%) with overall supply and peak load capabilities different from each other. The East region had an energy surplus of only 1231 MU (0.6%), and its peak demand was found to be 2474 MU higher than availability (−7.9%). Whereas, the North-East region, with relatively lesser energy requirements, had surplus energy of 765 MU (3.4%) and a peak deficit of 4.5 MU (−1.0%). On a pan-India basis, India had an energy surplus of 42159 MU (2.4%) against a total requirement of 1773361 MU. However, it faces a peak deficit of 10915 MU (−4.3%), meaning while the general energy availability is more than adequate, managing peak loads is a concern. India's energy demand and supply showed a strong increase in 2023–24 as compared to 2022–23 (shown in Table 2). The total energy requirement has increased by 7.7%, which is from 1513497 MU to 1629670 MU, and energy supplied has increased by 7.9%, which is to 1652531 MU. This suggests a positive correlation between the growth in demand and supply, meaning that the growing energy needs were adequately met. Peak demand jumped up by a significant 12.7% during 2022–23 at 215888 MU and increased to 243271 MU in 2023–24. Peak met rose even more impressively by 15.8% during 2023–24 from 207231 MU to 239931 MU, indicating an improvement in peak loads management. The figures point out the enhancement of India's supply-side capacity to accommodate growing energy demand while problems in managing surplus at peaks remain.

Comparative analysis of energy demand and supply in India for 2022–23 and 2023–24.

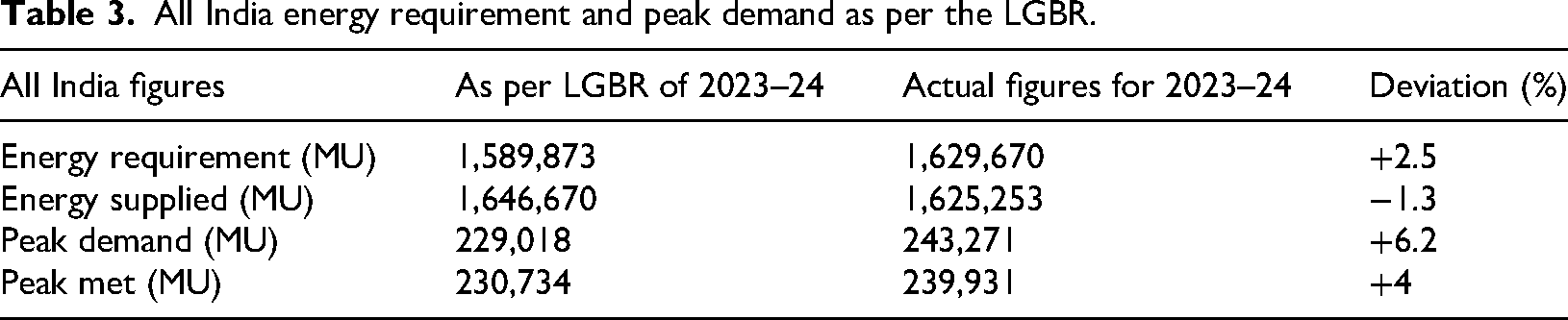

The LGBR forecast for 2023–24 was underestimating the actual energy requirements and peak demand, with the deviations pointing out the requirement for better forecasting mechanisms (depicted in Table 3). The actual energy requirements were 2.5% higher than the forecasted, at 1629670 MU against the forecasted 1589873 MU. Similarly, the actual peak demand was 6.2% higher, at 243271 MU against the forecasted 229018 MU. On the supply side, the energy supplied was 1.3% lower than forecasted at 1625253 MU against the projected 1646670 MU. Peak met was also 4% lower than forecasted, thus pointing to a need for better supply prediction and actual demand pattern alignment. The data in the following tables points out urgent trends and gaps in the Indian energy sector, focusing especially on region-specific planning along with improved peak demand management. The ability to provide correct forecasts is crucial for predicting bursts of demand, especially related to extreme weather conditions. Based on the deficits and deviations noticed, investments are required in the following areas:

Adding generation capacity at an appropriate time, especially for peak-load management. Improving the transmission and distribution infrastructure to reduce losses and accommodate variable demand. Increasing the share of renewable energy to diversify energy sources and reduce dependence on conventional fuels. Developing advanced storage technologies to balance supply during off-peak hours and meet peak demand effectively. Facilitating policy frameworks that incentivize infrastructure development and enhance operational efficiency.

All India energy requirement and peak demand as per the LGBR.

Through the fulfillment of these needs, India looks forward to a sustainable, efficient, and reliable energy future wherein ever-growing demand will be met without compromise to economic or environmental objectives.

Renewable energy growth scenario in India

India's renewable energy sector has grown exponentially during the last few years, following strong government policies, innovations in technology, and increasing awareness about sustainability. It has added 1875.26 MW new capacity in September 2024, of which about 1330.14 MW comes from the solar sector, 170.59 MW from the wind sector, 369.11 MW from biomass, small hydro 5 MW, and other sources 0.42 MW (Government of India, 2024). This is where India is heading towards a sustainable energy future.

Capacity Additions and Growth Trends

Capacity additions during September 2024 witnessed a significant growth compared to the same period last year. Interestingly, solar energy continued to lead the renewable energy mix, accounting for 70.94% of total capacity addition in the month. Wind energy, though much smaller in comparison, adds much value in terms of diversifying the energy portfolio and ensuring grid stability (Das et al., 2022). Further to the increased utilization of biomass and small hydro sources, the country focuses on harnessing diverse renewable resources.

Generation and Performance Review

Renewable energy generation in September 2024 was up by 18.60% year over year compared to September 2023, indicating improved operational efficiencies and favorable weather conditions. Key observations are as follows:

Large Hydro Contributions

Large hydro generation increased by 26.05% compared to September 2023, excluding data from Sikkim and Meghalaya. This growth shows the role of large hydro projects in meeting peak demand and providing ancillary services for grid stability.

Integrated Renewable Energy Systems

India's renewable energy policy is slowly shifting more towards integrating DERs with grid management technologies, advanced. In the USA, ISOs and RTOs implement predictive analytics and real-time monitoring, deploying dynamic dispatch systems to solve the uncertainty problem of variable renewables and ensure better resource allocation that improves system reliability.

Renewable Energy in a Deregulated Market Framework

The introduction of renewable energy in the deregulated framework of the electricity market has, in turn, enhanced competition and innovation. The PPAs, renewable energy auctions, and competitive bidding have encouraged the participation of the private sector. Direct supply of electricity to utilities and industrial consumers from the robust financial instruments of solar and wind farms is contributing to a dynamic and efficient market environment.

Future Outlook and Challenges

In the future, India will need to increase its non-fossil fuel energy capacity to 500 GW by 2030. To achieve this:

India's renewable energy growth scenario is an example of a transformative approach to energy sustainability, supported by technological innovation, policy backing, and stakeholder collaboration. India is well-placed to lead the global renewable energy transition by addressing operational challenges and leveraging advancements in grid management. In September 2024, India's RE sector witnessed considerable growth, with notable capacity additions and increased generation output compared to September 2023. The total RE capacity added 1875.26 MW in September 2024, which was more than the modest 268.77 MW addition recorded in September 2023. This marked improvement underscores India's commitment to scaling up its renewable energy infrastructure.

In September 2024, India added a remarkable 1875.26 MW of renewable energy capacity, with solar power accounting for 1330.14 MW or 70.94% of the total additions. Wind energy accounted for 170.59 MW, followed by biomass at 369.11 MW, small hydro at 5 MW, and other sources at 0.42 MW (Government of India, 2024). On the other hand, in September 2023, the capacity addition was quite minimal at 268.77 MW, mainly contributed by solar (170.74 MW), wind (94.95 MW), and waste-to-energy (3.08 MW). The comparison year on year shows that the pace of investment and deployment has increased for renewable projects, especially for solar energy, indicating the increasing attention towards renewable infrastructure development in India. All India RE generation for September 2024 witnessed an increase of 18.60% against September 2023. This is proof of better operational efficiency along with capacity utilization. Salient features are as follows:

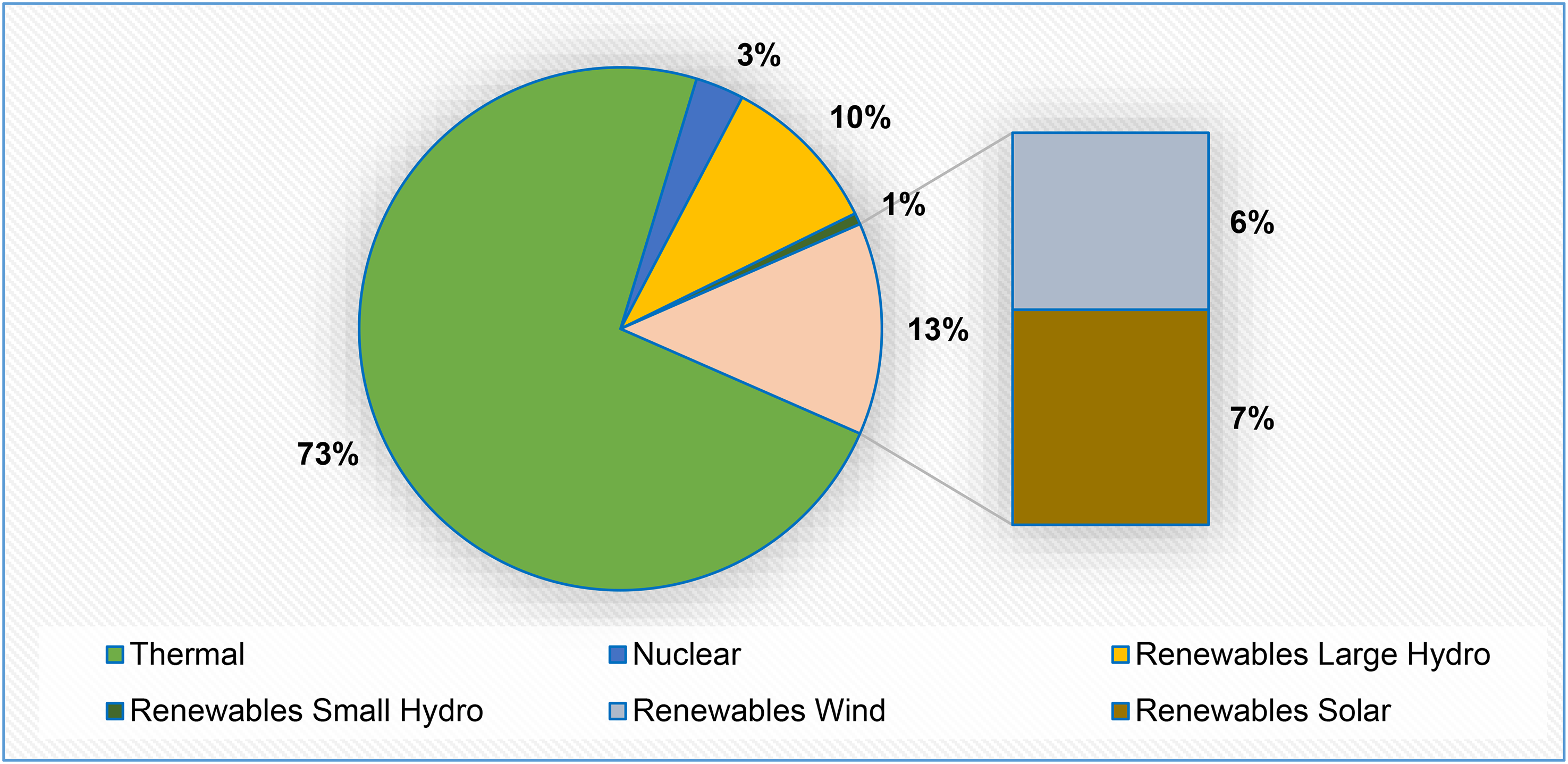

The comparative analysis reveals a large shift towards solar and large hydro contributions in 2024, with a decline in biomass and bagasse-based generation. This reflects the strategic prioritization of scalable and sustainable renewable technologies. In conclusion, the renewable energy sector in India has made tremendous progress due to focused policies, technological developments, and diversified resource usage. The year-on-year comparisons highlight the country's increased capacity to meet its aggressive renewable energy targets and handle issues of variability and optimization of resources. Figure 1 presents the share of each source to the total energy generation; how each source has been progressively replacing the other over time is also reflected. In Figure 1, the total energy generation in India as of September 2024 is detailed, with renewable energy sources contributing a substantial share.

All energy resource generation in India as of September 2024.

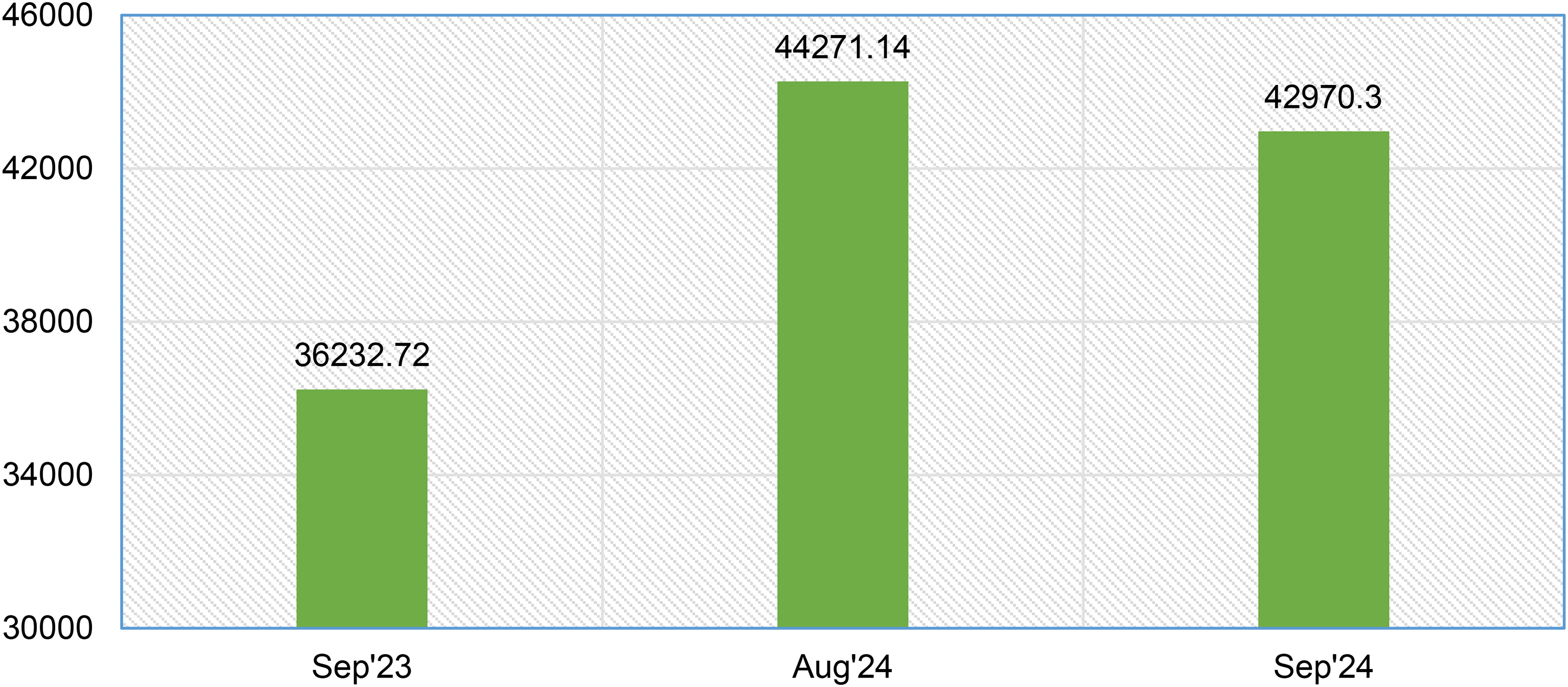

Solar energy dominated with approximately 70.94% of the total renewable capacity added in September 2024, followed by wind energy at 9.10%, biomass at 19.68%, and small hydro at 0.28%. This emphasizes the pivotal role of solar power in India's energy transition. Figure 2 shows the renewable energy production in the fiscal year 2023–24. It segregates into solar, wind, biomass, small hydro, and others, with changes year by year and share of respective sectors. Its leading production source is solar power, showing a year-over-year increase of 22.58% while, on the other hand, wind has shown a growth of a mere 0.22%. Biomass-based generation faced challenges, reflecting a 1.90% decline, whereas small hydro witnessed a robust growth of 31.97% compared to the previous year.

Renewable energy generation in 2023–24 (in MU) in India.

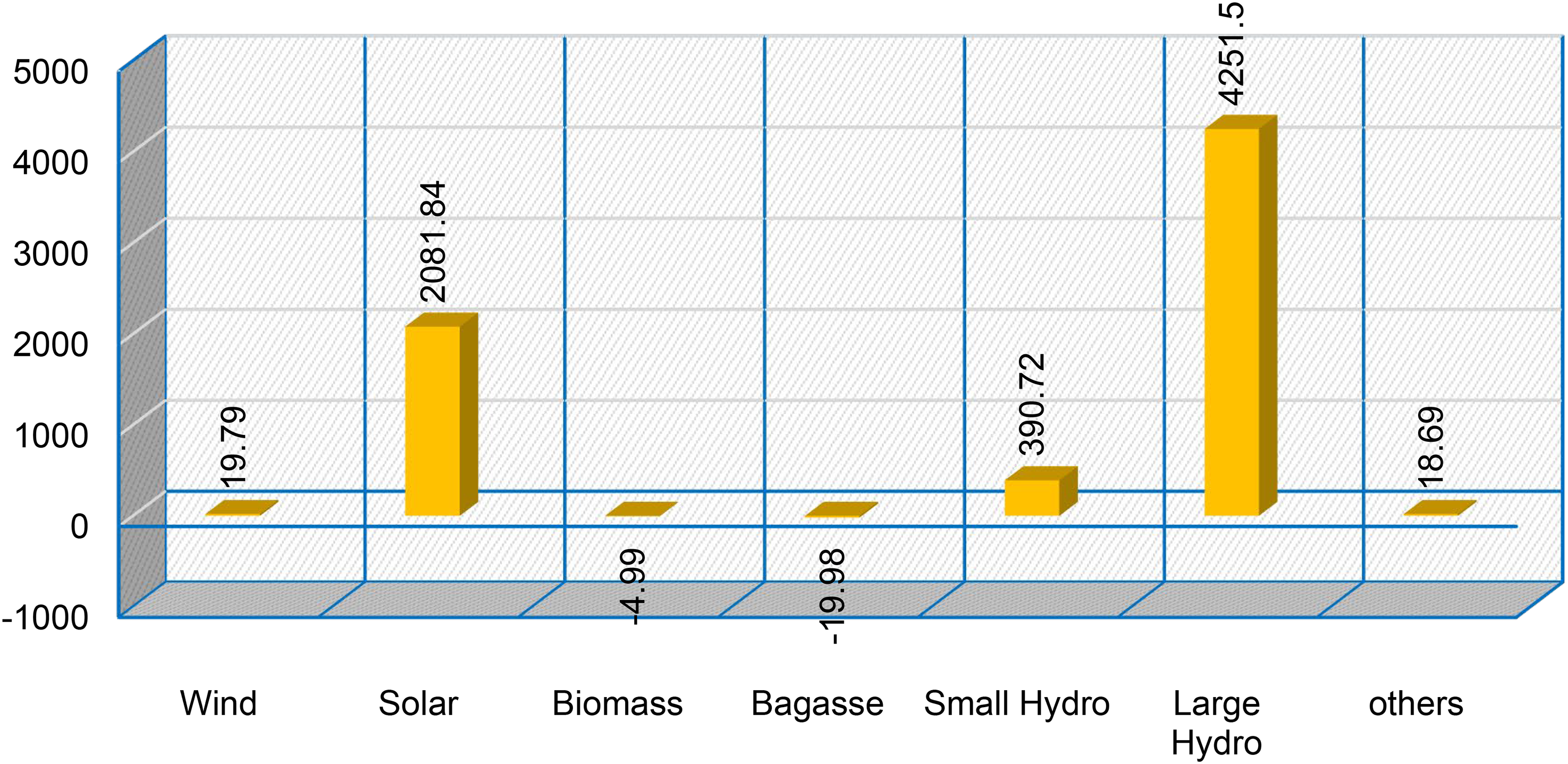

Figure 3 focuses on the rise of renewable energy generation from September 2023 to September 2024. Capacity additions and performance enhancements have been shown using month-to-month data comparisons between the two years. In Figure 3, 18.60% growth in additional renewable energy generated in September 2024 as compared to that in September 2023 reflects better operational efficiency and propitious climatic conditions. The main contributor was solar power due to the reasons of new capacity additions and technological advancements.

Additional RE generation (MUs) in Sept'24 compared to Sept'23.

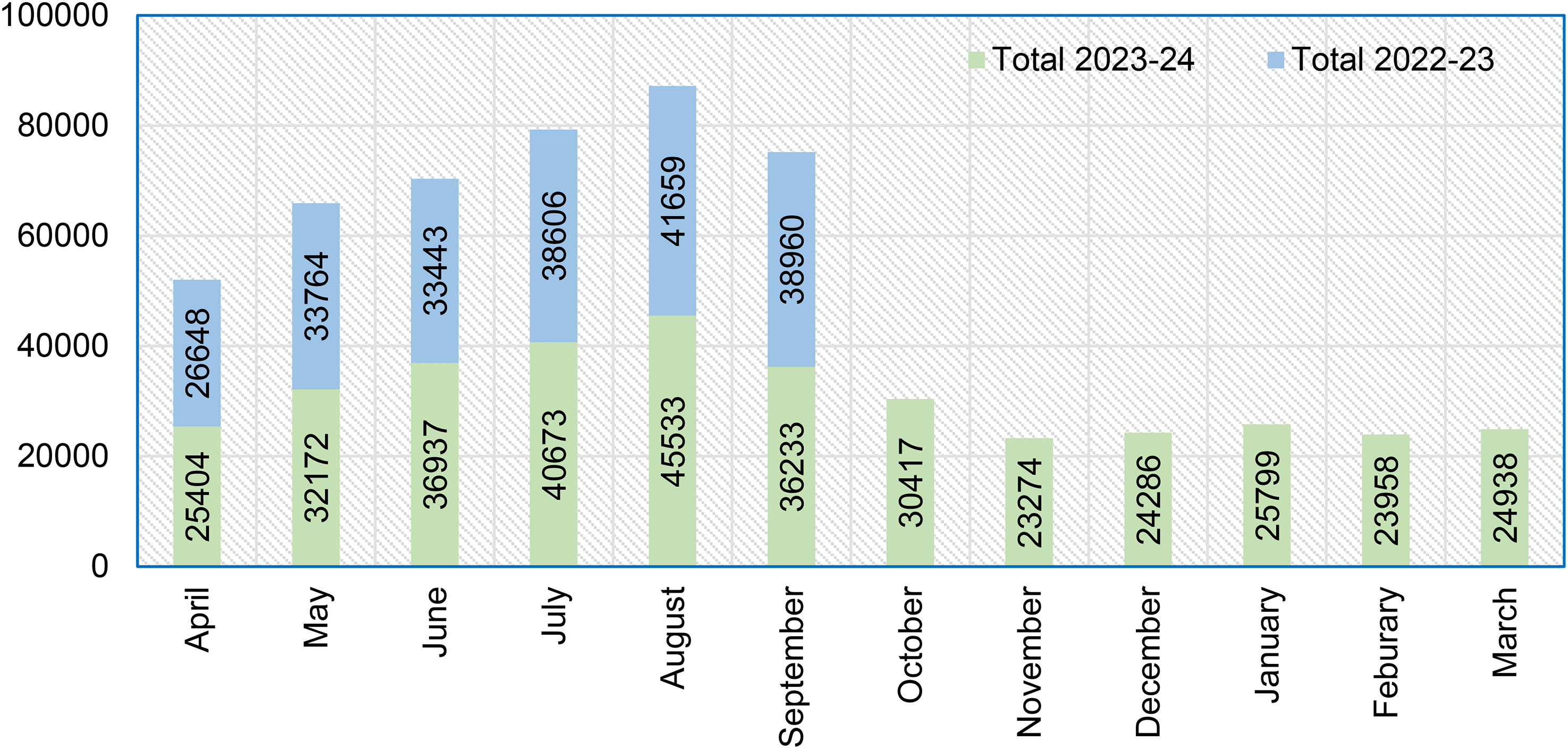

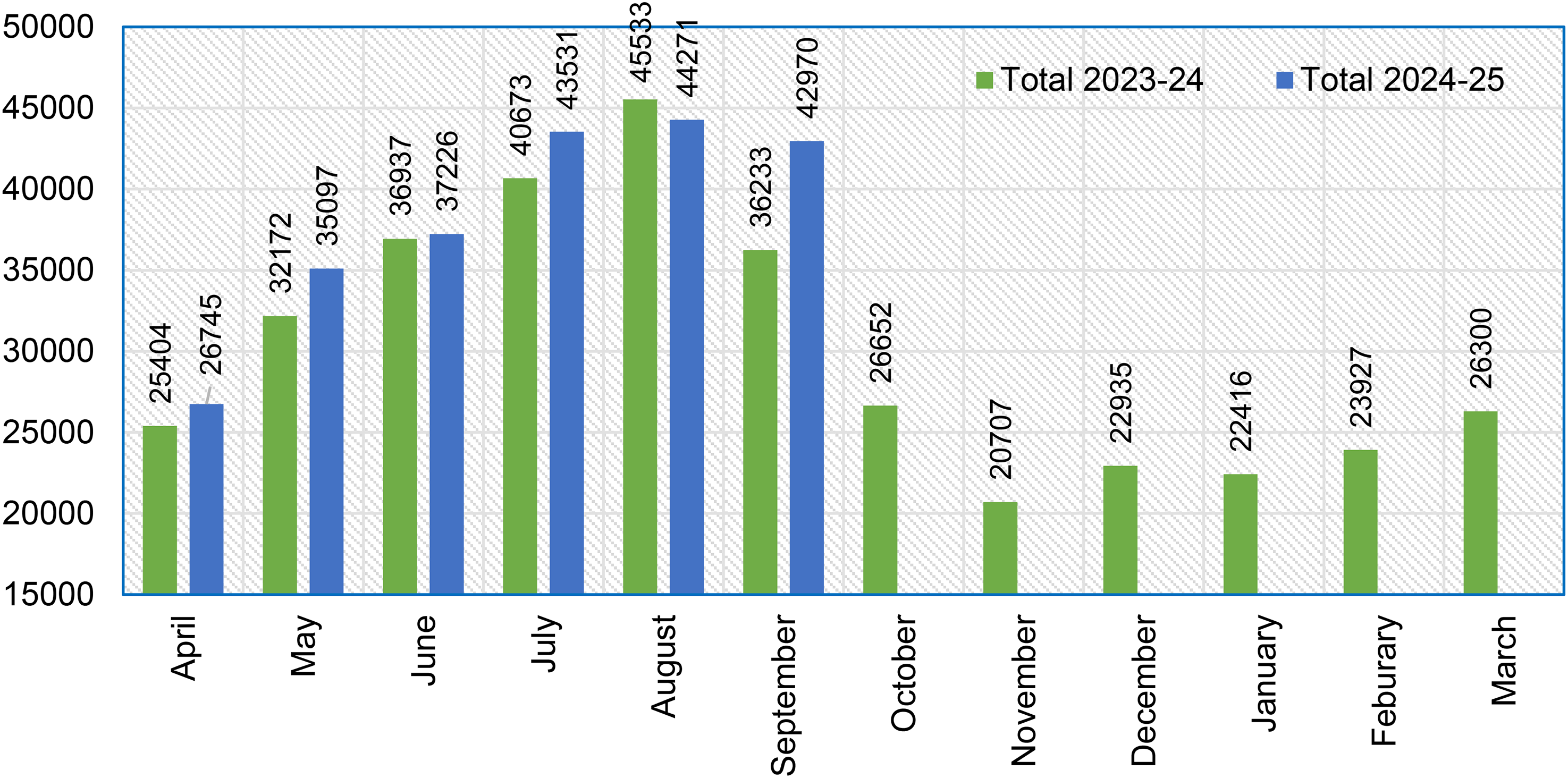

Figure 4 plots monthly renewable energy generation for two consecutive fiscal years. This graph indicates seasonal trends, fluctuations in energy production with climatic conditions, and process improvements that have led to capacity utilization (Government of India, 2023). Figure 5 extends the comparison to the fiscal years 2023–24 and 2024–25. It displays growth trends that are constantly increasing, supported by policy, new projects, and operation improvements. Figures 4 and 5 illustrate comparative month-wise renewable energy generations during 2022–23, 2023–24, and 2024–25. Figures illustrate the steady positive trend wherein peaks in production periods are largely better than preceding years owing to enhanced utilization of resources along with advancement in forecast mechanisms.

Month-wise RE generation in MU for 2022–23 and 2023–24.

Month-wise RE generation in MU for 2023–24 and 2024–25.

Figure 6 Summarizes yearly renewable energy generations for two fiscal years. It emphasizes the accretive impact of additions in capacities, operational efficiencies, and policy initiatives that push up the renewable energy output of India. The figures have depicted a cumulative growth in renewable energy generation of over 20%, thus signifying the success of the policy measures such as providing subsidies for solar and wind installations and support to distributed energy systems. India's renewable energy growth is crucial to meet its rising energy demand and sustainability objectives.

Year-wise renewable energy generation in MU for 2023–24 and 2024–25.

Renewable energy, especially solar and wind power, has become the bedrock of India's energy transition with an ambitious target of 500 GW of non-fossil fuel energy capacity by 2030. The challenges, such as grid integration, intermittency, and regional disparities, remain but are being addressed through policy measures, technological innovation, and infrastructure upgrades.

India's future in terms of energy is renewable energy for several reasons, which include:

Global status of renewable energy

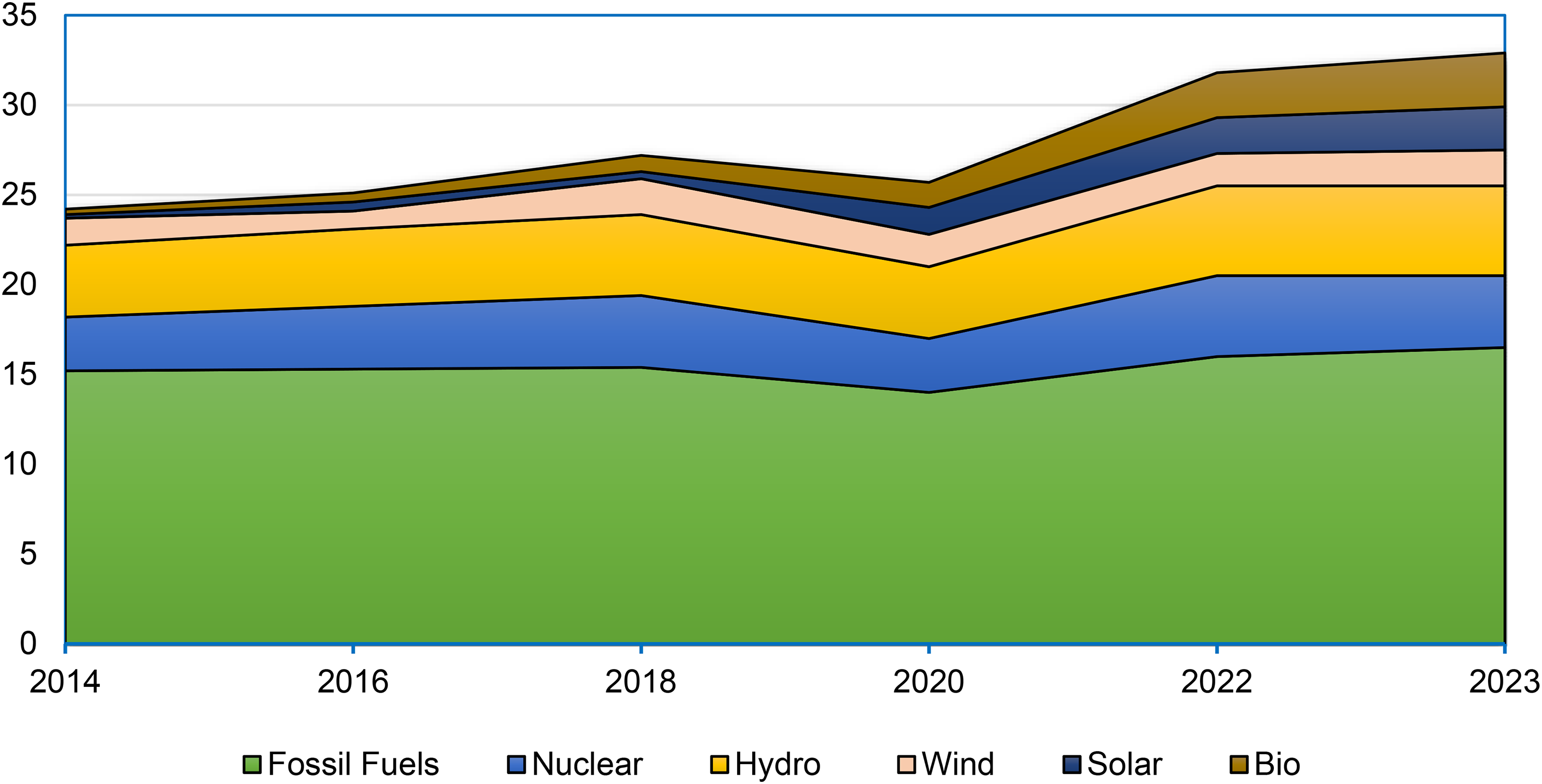

The global status of renewable energy reflects significant progress and the challenges in transitioning to a sustainable energy future. Between 2014 and 2023, renewable energy's share in global electricity generation increased from 21.7% to 30.3%, showing a steady move toward cleaner energy sources. However, fossil fuels remain dominant, contributing 60.6% of the global electricity supply in 2023, although their share is gradually declining. Among renewables, hydropower was at 14.3%, followed by wind power at 7.8%, and solar power at 5.5%. Bioenergy and geothermal power are also gaining ground as developing renewable sources, although much smaller in contribution.

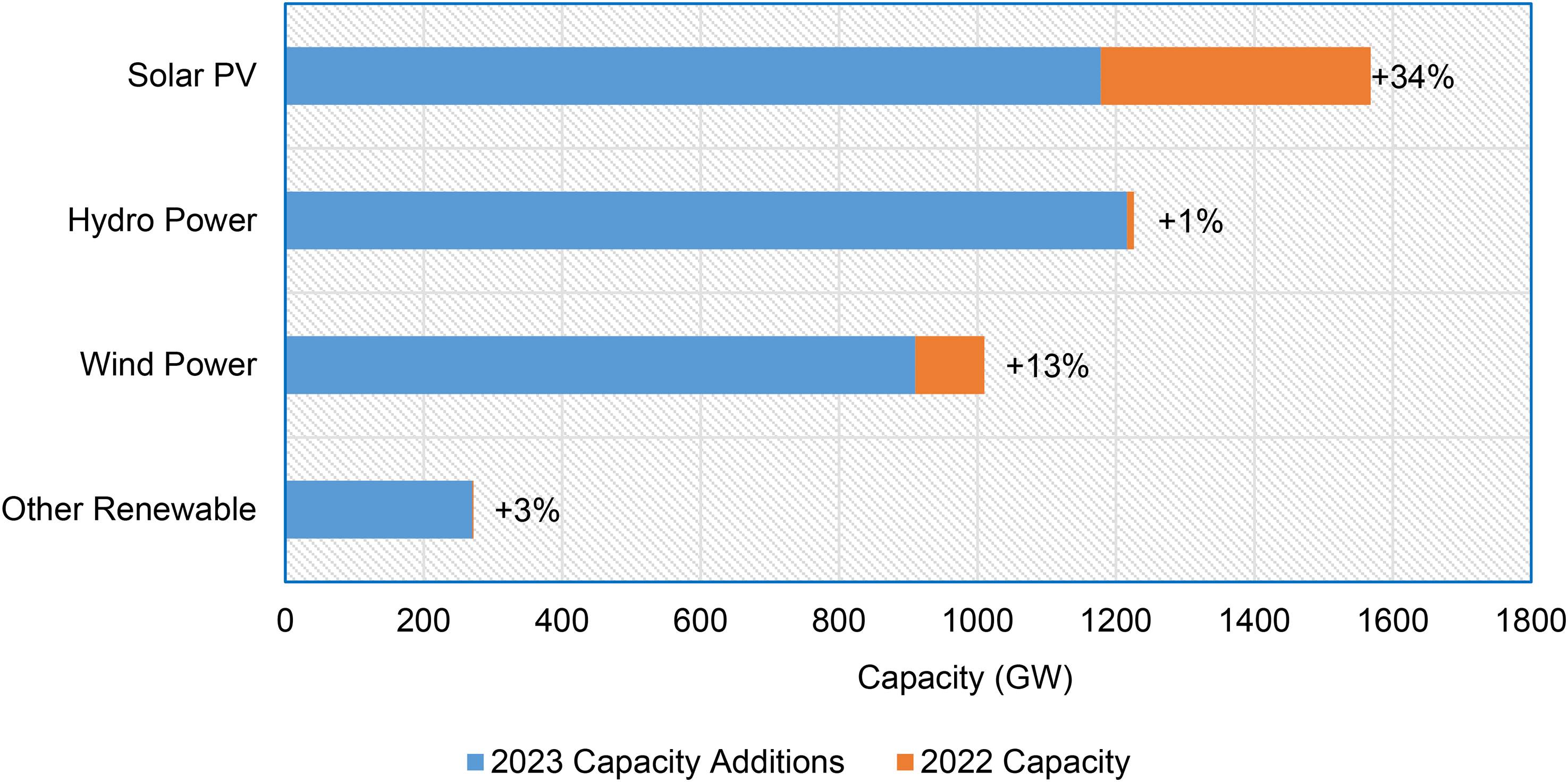

The increasing reliance on renewables thus calls for policies and investments to speed up the transition from fossil fuels even further. In 2023, renewable energy capacity was added at a record-breaking 536 GW globally. Solar PV is leading the expansion with 407 GW, up 34% year on year; wind power grew by 13%, adding 117 GW. Hydropower and other renewables, including biomass and geothermal, grew relatively marginally. The strong presence of solar PV is explained by its scalability and competitiveness, putting it at the heart of the renewable transition. The moderate growth of other renewable sources reveals constraints, which are mainly geographically and policy-related. The balancing mix of energy will depend on their rectification. The robust growth still cannot add the amount of renewable energy to bridge the annual capacity needed for meeting the International Energy Agency's (IEA) Net Zero Scenario by 2030 at 996 GW (AEE-INTEC, 2024). This shows how critically the enhancement of cooperation, innovation, and policy support are required. Deployment of solar PV and wind power needs to be accelerated while addressing bottlenecks in hydropower and emerging technologies to reach the global climate goals. Concerted efforts of governments, private entities, and international organizations will be necessary to bridge this gap and to achieve alignment with the net-zero emissions pathway. Figure 7 shows a global electricity generation mix for the period from 2014 to 2023 in TWh. During the period, renewable energy has gained significantly, rising from 21.7% in 2014 to 30.3% in 2023. This is an upward trend that speaks of a new wave of renewable energy alternatives worldwide.

Distributions of global electricity generation from 2014 to 2023 (In TWh).

However, fossil fuels continued to dominate energy production in 2023, representing 60.6% of global electricity generation, although their contribution has been gradually declining in recent years. Nuclear power remained at a stable contribution of 9.1% during the decade. Hydropower led the way in the renewables sector at 14.3% in 2023, followed by wind power at 7.8% and solar power at 5.5%. Bioenergy and geothermal power together accounted for 2.7%, an area that is emerging but not yet significant. This also represents a massive shift to renewables, which have increasingly been adopted globally to address carbon emissions and push sustainable energy solutions. Nevertheless, the preponderance of fossil fuels points out how much investment in and utilization of renewable technologies must speed up. The data shows that, though the renewable energy sector is on a promising track, huge policy and financial support is required to accelerate this transition. The leader of growth was solar photovoltaic technology at 407 GW, reflecting a 34% gain over 2022 capacity (shown in Figure 8). Wind power growth came in at 117 GW, a 13% gain. Hydropower and other sources of renewable energy saw slightly more modest growth: the former at just 1% and the latter, including biomass and geothermal, at 3%. The predominance of solar PV in capacity additions reflects its low costs, scalability, and essential role in the global transition toward renewable energy. Wind power continues to play a vital role, especially in areas with strong wind potential, as a complementary source to solar PV. Conversely, the very limited growth in hydropower is an indicator of this being a mature technology with fewer opportunities for new large-scale capacity development, primarily due to geographical, environmental, and policy-related constraints. These trends are in line with efforts to reduce fossil fuel dependence and combat climate change worldwide, but they also underpin the challenges of balancing growth more evenly across renewable technologies. The statistics point out the need for targeted policies that support emerging technologies and address sector-specific constraints toward a more diversified and resilient global energy system.

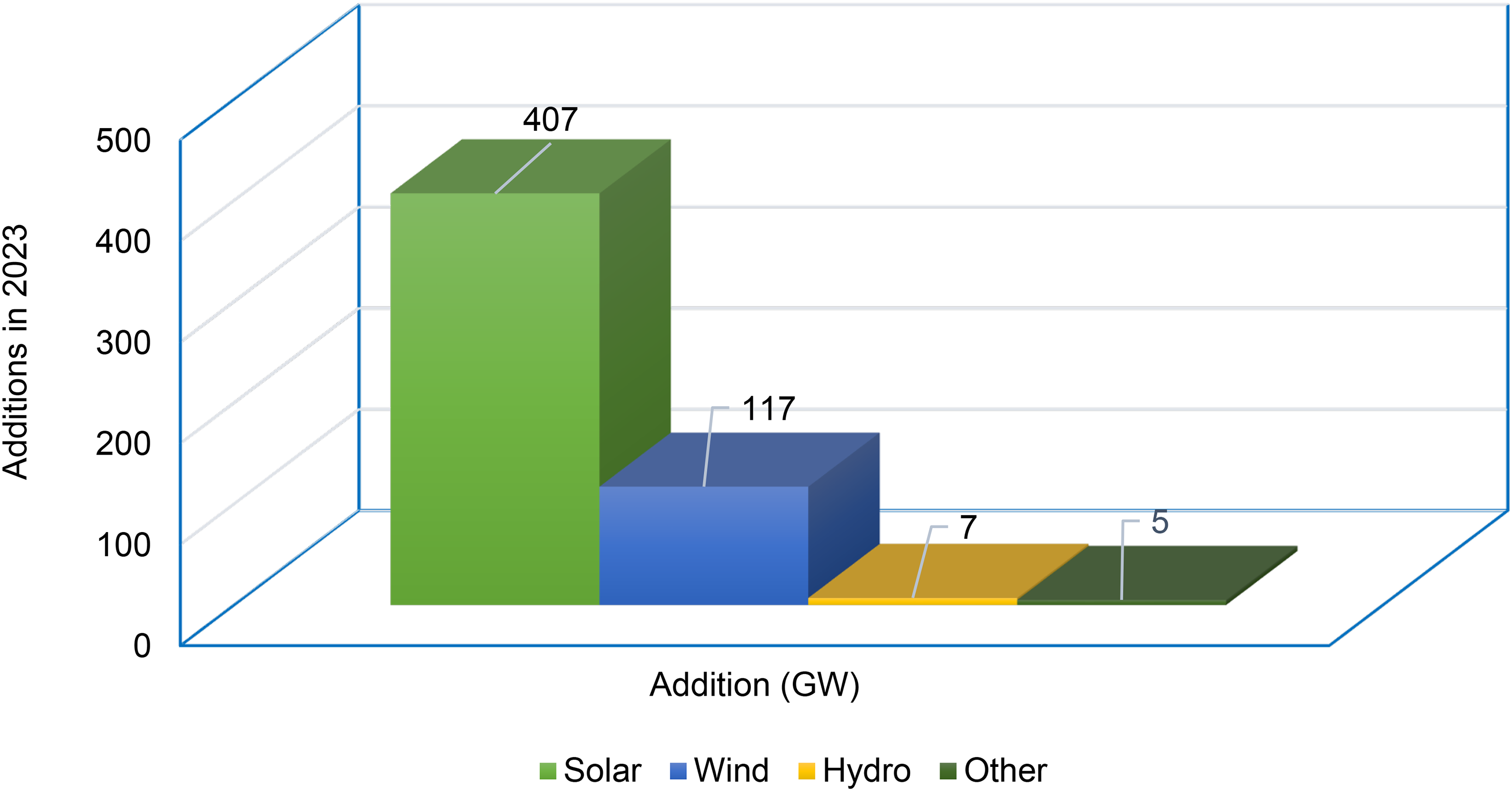

Figure 9 illustrates the annual additions of renewable power capacity from 2022 to 2023, broken down by major renewable energy sources, including solar PV, wind power, hydropower, and other technologies such as bio-power, geothermal, ocean power, and concentrated solar power (CSP). The total capacity added in 2023 reached approximately 536 GW, marking a continuation of the steady growth seen in recent years. Solar PV and wind power were the largest contributors to this growth, clearly indicating their importance in the renewable energy sector. Though renewable capacity growth is laudable, it is far from the 996 GW annual additions needed to achieve the IEA Net Zero Scenario by 2030. This scenario would bring global energy systems in line to limit global warming to 1.5°C. To reach this very ambitious goal, almost twice the current rate of capacity additions would be needed.

Annual additions of renewable power capacity from 2022 to 2023.

The figures are a strong reminder of the gap between current progress and the required pace to meet global climate targets. It calls for increased investment, innovation, and cooperation among governments, private sectors, and international organizations. Accelerating the deployment of renewable energy technologies, especially solar PV and wind, and addressing bottlenecks in sectors such as hydropower and emerging renewables, will be crucial to aligning with the net-zero pathway. This calls for robust policy interventions, enhanced financial mechanisms, and a focused effort to scale up deployment to unprecedented levels.

Global challenge for the year 2030

The entire world is facing huge challenges in the incorporation of renewable energy sources in the existing power system.

Renewable electricity

As the global energy landscape evolves, achieving ambitious renewable energy targets by 2030 presents multifaceted challenges. Forecasts indicate that global renewable electricity generation will exceed 17000 TWh (60 EJ) by 2030—a value surpassing the combined electricity demand of China and the United States for the same year. However, significant milestones are projected within the next six years that reflect transformative trends in the renewable sector:

By 2024, solar PV and wind power will together outpace hydropower generation. By 2025, renewables-based electricity will surpass coal-fired generation. By 2026, wind and solar generation will exceed nuclear energy production. By 2027, solar PV will overtake wind energy as the leading source of renewable electricity. By 2029, solar PV will surpass hydropower, becoming the largest single source of renewable energy. By 2030, wind power will also surpass hydropower in generation, making solar and wind the dominant contributors to global renewable energy.

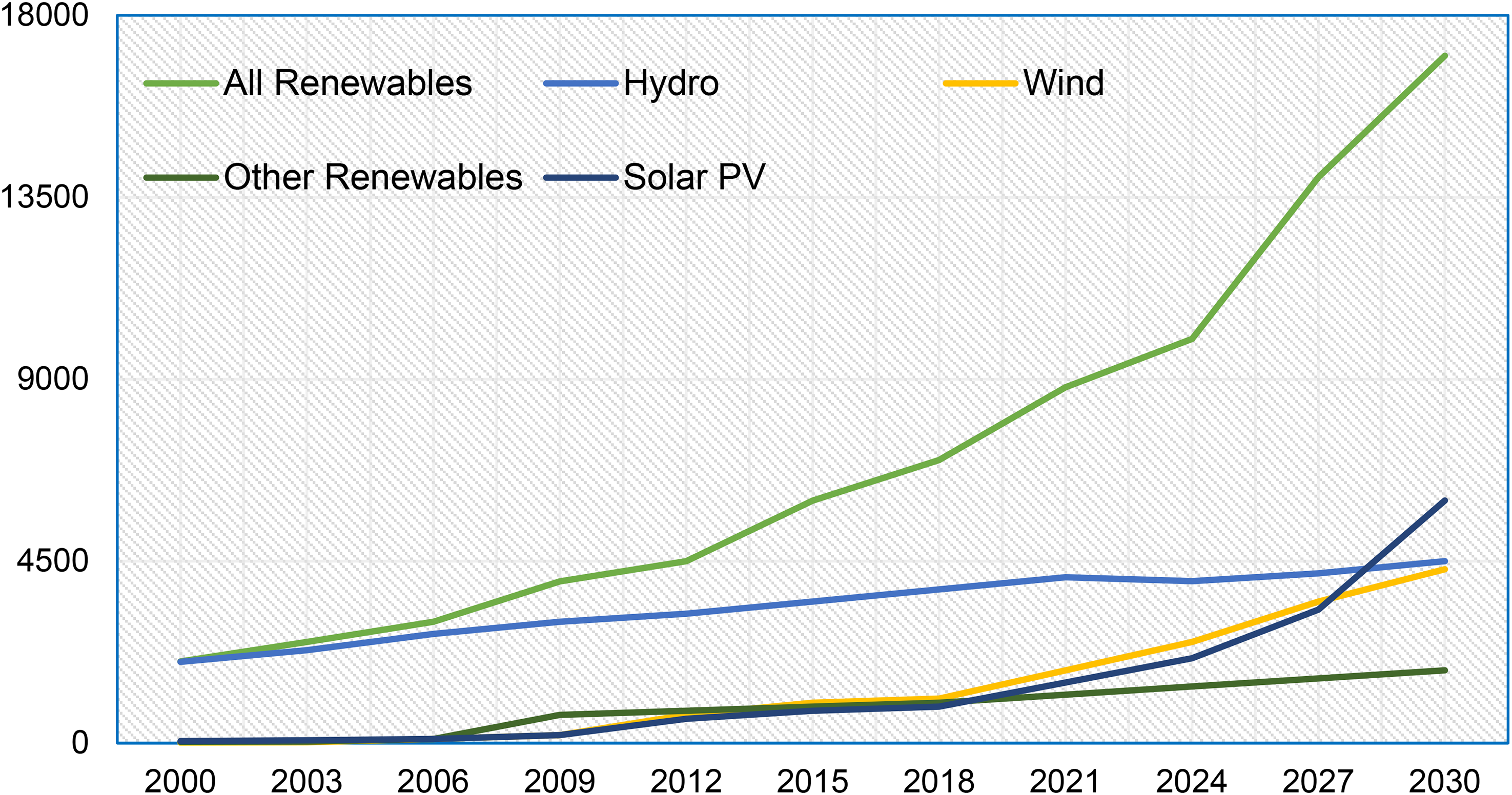

In 2030, renewable energy sources are expected to account for 46% of global electricity generation, with solar PV and wind combined contributing 30% (Bahar et al., 2024). While these figures mark significant progress, they fall short of the IEA's Net Zero by 2050 Scenario, which targets 60% renewable energy generation by 2030. This discrepancy of 14 percentage points represents approximately 5000 TWh—nearly equivalent to Europe's total electricity production in a year. Accelerating renewable energy deployment is essential to bridge this gap. Figure 10 illustrates the progression of electricity generation from 2000 to 2030. By 2030, renewables will supply 46% of global electricity, led by solar PV (16%) and wind (14%), both surpassing hydropower (12%). Fossil fuels will decline but still contribute 54%, underscoring the urgency to accelerate renewable adoption.

Global electricity generation by technology, 2000–2030 (In TWh).

Renewable transport

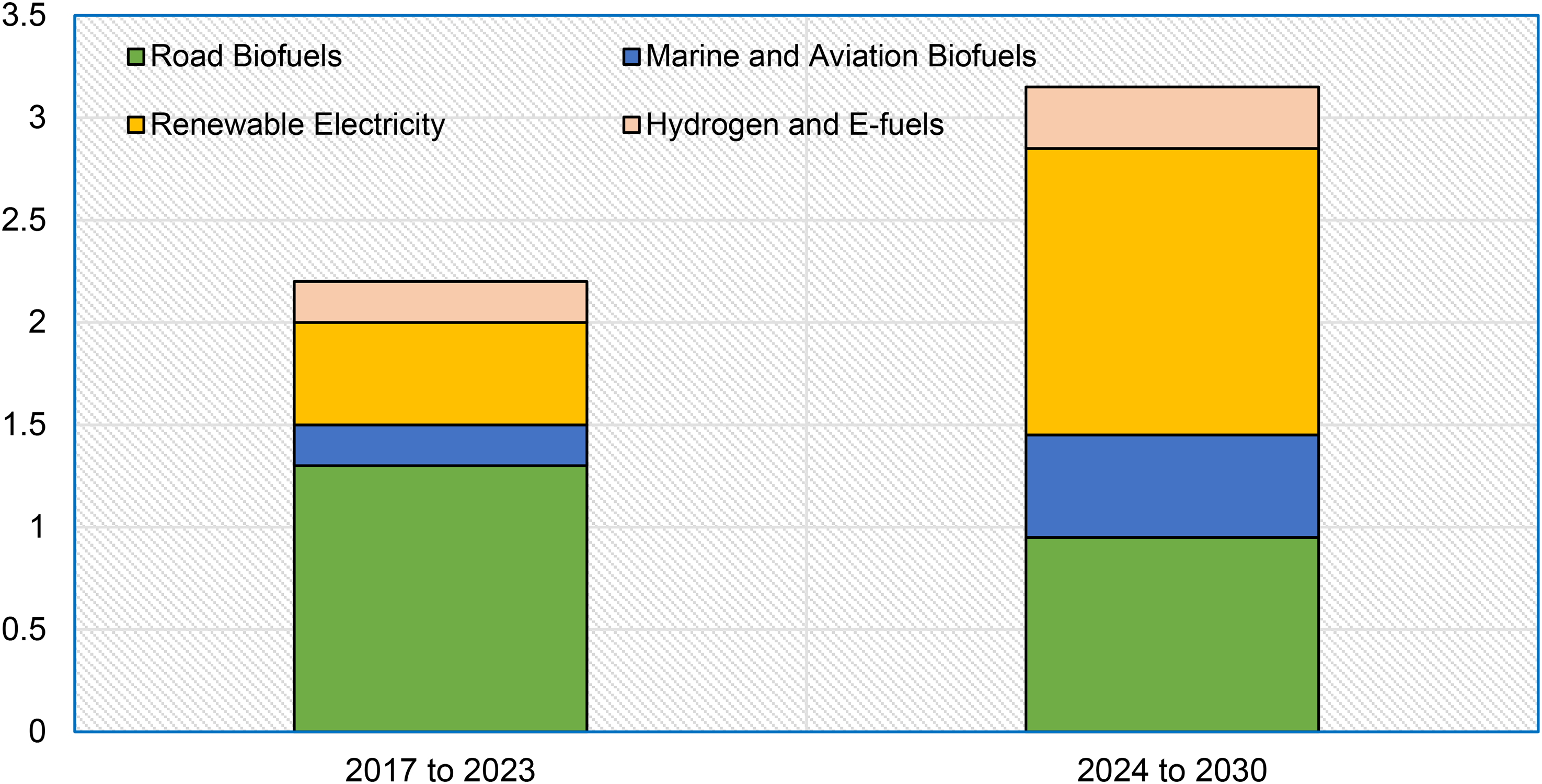

In the transport sector, renewable energy demand is forecasted to grow by 3.0 EJ between 2024 and 2030, doubling the increase observed from 2017 to 2023. This growth will diversify beyond road biofuels, which previously constituted 90% of renewable transport demand growth. By 2030, renewable electricity will represent 50% of this demand, while aviation and marine biofuels will account for 10%, and hydrogen and e-fuels will make up 7%. Despite progress, aviation and marine transport remain heavily dependent on fossil fuels, with biofuel consumption in these sectors needing to rise from 6% to 20% of global biofuel demand to align with the Net Zero by 2050 Scenario.

Global renewable shares of transport energy demand are increasing but with regional trajectories differing. In the US, Europe, and China, renewable electricity constitutes most of the new renewable transport demand since electric vehicle stocks continue expanding, which are powered by increasing shares of renewable electricity. In comparison, road biofuel demand in these regions is flattening out. Current renewable energy demand forecasts for the road, marine, and aviation subsectors fall short of the IEA Net Zero by 2050 Scenario trajectory. Among these, road transport is the closest to meeting the scenario's targets, thanks to ongoing and planned biofuel production and the growing adoption of electric vehicles, which are powered increasingly by renewable electricity. Renewable electricity will drive 50% of the sector's growth from 2024 to 2030 (shown in Figure 11). Aviation and marine biofuels will rise to 10%, while hydrogen and e-fuels reach 7%. The reliance on road biofuels will drop from 90% (2016–2023) to 33% by 2030.

Transport sector renewable fuel growth, 2017–2030 (In EJ).

Renewable heat

Renewable heating technologies like heat pumps, biomass boilers, and PV systems provide options to reduce carbon emissions and reliance on fossil fuels. Each has unique strengths, heat pumps are efficient for moderate climates, biomass boilers are ideal for larger, rural applications, and PV offers a flexible, clean energy source when paired with electric heating. Renewable heat consumption is projected to grow by over 50% (15 EJ) from 2024 to 2030. This increase is 2.4 times the growth observed in the preceding six years but will cover less than three-quarters of the expected rise in total heat demand. Consequently, fossil fuel use for heating will persist, leading to a 4% increase in heat-related CO2 emissions by 2030. Addressing this challenge requires scaling renewable heat deployment by 2.3 times current levels and implementing efficiency measures to reduce global heat demand by 3% during the same period.

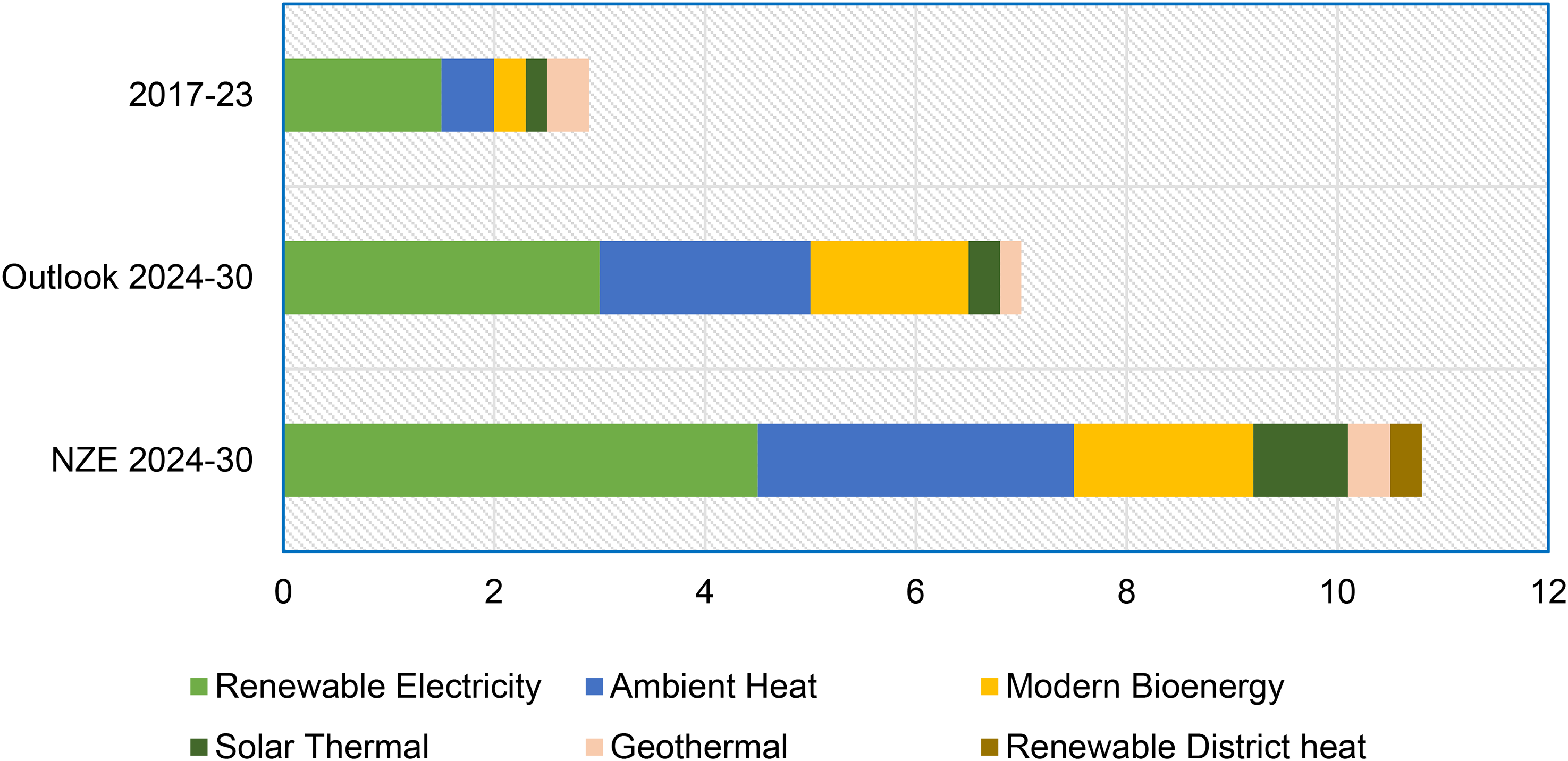

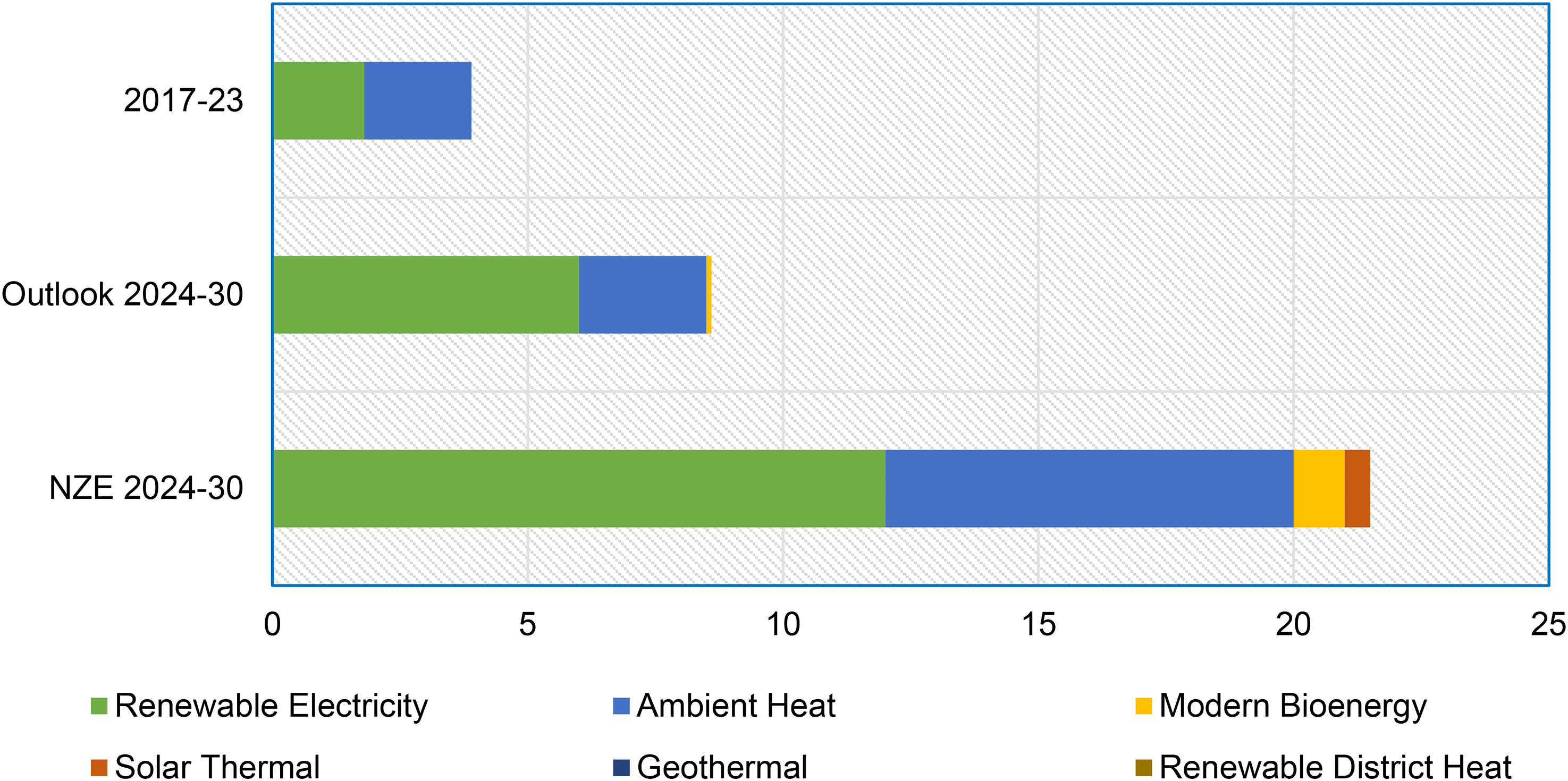

Renewable heating technologies—such as heat pumps, biomass boilers, and PV systems—are expected to contribute less than 25% of building heating by 2030 (As depicted in Figure 12). Regions with limited renewable electricity access face slower adoption, further constrained by high upfront technology costs. On the other hand, renewable electricity's contribution to industrial process heat is forecast to lag, with a 9-EJ shortfall against the Net Zero Scenario by 2030 which is deliberated in Figure 13. Biomass use in industrial heating also faces a 4-EJ gap, highlighting challenges in scaling industrial renewable heat adoption. In the industrial sector, the challenges that renewable heat has to face are considerable: it has to replace solutions that often work at high temperatures and are already integrated with existing systems. Other technologies such as green hydrogen and concentrated solar power also appear promising but are at least far from becoming economically viable at scale. Moreover, the retrofitting of older buildings in advanced economies is another bottleneck, particularly in colder climates where heating demand is more pronounced.

Heating effect in buildings from renewable sources (In EJ).

Heating effect in industry from renewable sources (In EJ).

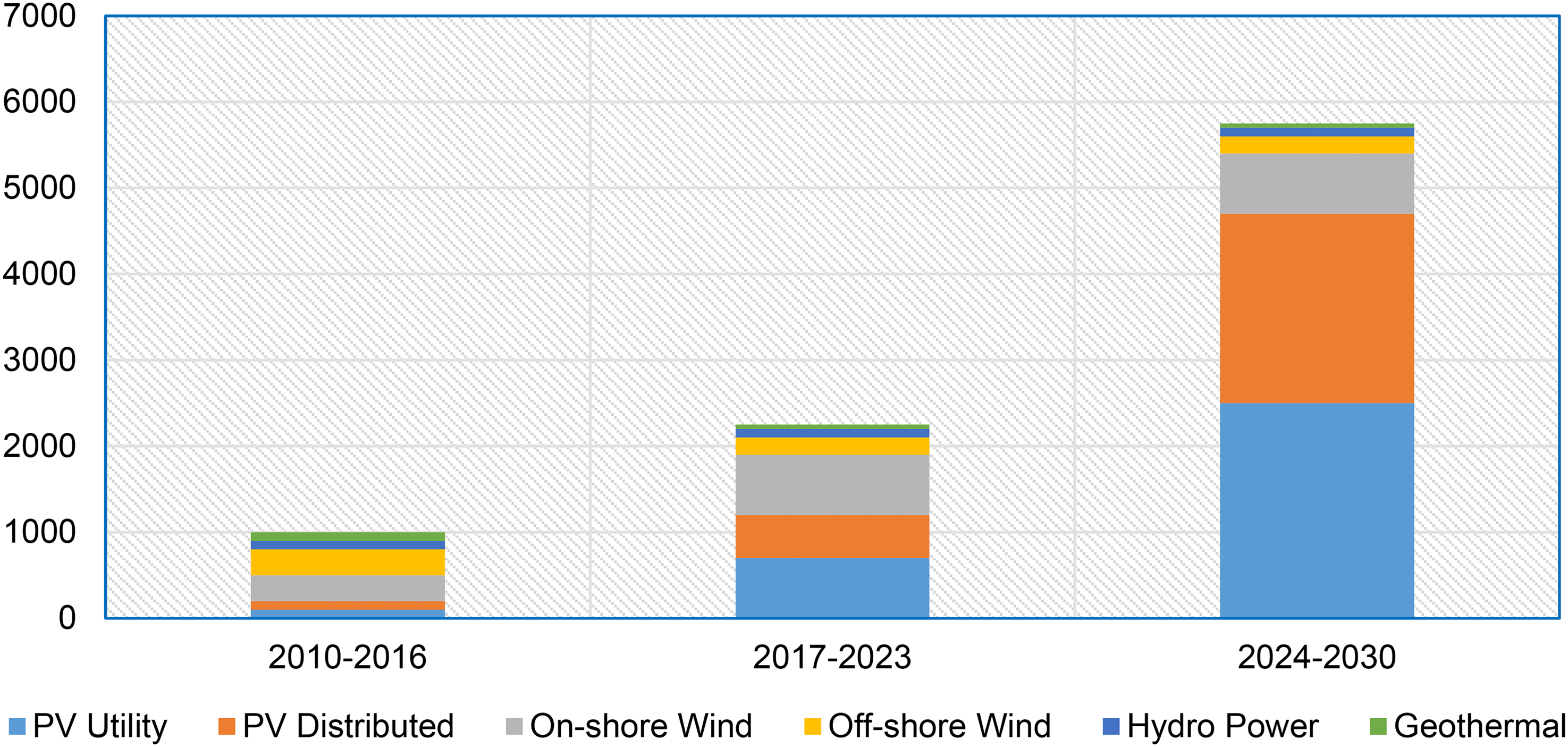

Figure 14 depicts that the global renewable electricity capacity will grow by 5520 GW from 2024 to 2030—2.6 times the deployment during 2017–2023. Solar PV will dominate, accounting for nearly 80% of new capacity, driven by declining costs, rapid permitting, and scalability. Moreover, whereas improved efficiencies in developed economies would negate growth in heat demand, there are difficulties associated with the retrofitting of older structures in those regions and higher energy demand areas, such as cold regions. Lastly, there's the issue of reliability by a grid, vulnerable also to fluctuations in renewable electricity supply should renewable electricity become dependent and where a stable renewable grid is not available. Global renewable capacity will rise to more than 5520 GW between 2024 and 2030, 2.6 times as much as deployed in the last six years (2017–2023). Utility-scale and distributed solar PV add more than triples, accounting for nearly 80% of renewed electricity growth. Solar PV adoption speeds up with lowering equipment costs, relatively rapid permitting, and wide social acceptance. PV project size can vary between a few watts and multi-gigawatt-scale utility plants, thus ensuring low-cost zero-emission electricity is available to individuals, small companies, large industries, and utilities.

Renewable electricity capacity growth, 2010–30 (In GW).

India's challenge for the year 2030

India has the ambitious task of transforming its energy landscape to meet its 2030 climate and energy goals. The four main targets include achieving 500 GW of non-fossil energy capacity, satisfying 50% of energy requirements from renewable sources, reducing carbon emissions by one billion tonnes, and lowering the carbon intensity of its economy by at least 45%. These objectives require massive expansion of renewable energy infrastructure, significant policy reforms, and technological advancements. India will have to add an estimated 340 GW of non-fossil energy capacity by the end of the decade to achieve the 500 GW target. This would mean adding an average of 40–43 GW every year, which would call for a consistent and rapid expansion in capacity. Projections from the Central Electricity Authority (CEA) present a detailed split: about 435 GW from wind, solar, and other renewable sources supplemented by 61 GW from large hydro and 19 GW from nuclear energy. The diversified mix fits into the Indian approach of integrating all forms of renewable sources for better stability and reliability in the grid (Shankar et al., 2022).

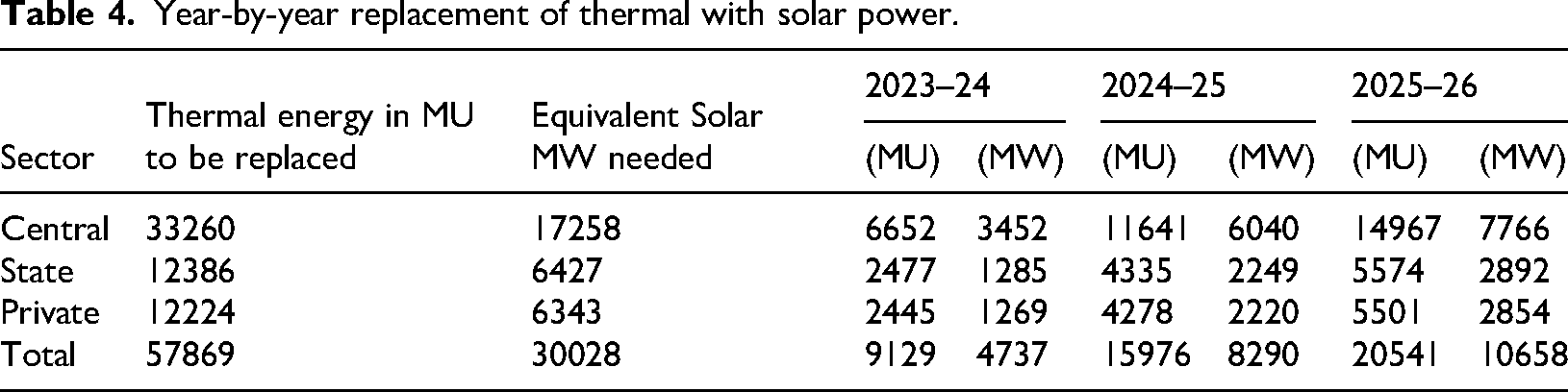

Table 4 represents a phased replacement of thermal energy with solar energy. In the fiscal year 2023–24, 20% of thermal energy would be substituted, which is 9129 MU, and would need an equivalent amount of solar capacity of 4737 MW. By 2024–25, this share has increased to 35% of 15976 MU, requiring 8290 MW of solar capacity. The substitution will increase up to 45% of 20541 MU by 2025–26, which is equivalent to 10658 MW of solar capacity. Central sector contributions lead this transition; state and private sectors also contribute significantly. This phased approach emphasizes the scalable integration of solar power to progressively displace thermal energy, reflecting a robust strategy for decarbonizing the energy mix. Table 5 projects India's installed capacity by 2030 under different scenarios. The CEA predicts a total installed capacity of 817 GW, with 64.26% from non-fossil sources. Alternate projections from TERI-BCS and TERI-HRES estimate a slightly lower total of 785 GW and 705 GW, respectively, with non-fossil shares ranging between 62.61% and 66.50%. Solar energy is likely to dominate, contributing between 189 GW and 280 GW, while wind capacity is expected to range from 129 GW to 169 GW. Hydro and nuclear sources add considerable capacity, ensuring a balanced and diversified energy portfolio. The inclusion of battery energy storage ranging from 27 GW/108 GWh to 60 GW/120 GWh emphasizes the importance of storage systems in addressing renewable sources’ intermittency.

Year-by-year replacement of thermal with solar power.

Installed capacity projections of India by 2030.

The planned replacement of 58000 MU of thermal energy with renewables by 2025–26 has made scaling renewable capacity the most urgent. This transition represents a renewable capacity equivalent of approximately 30000 MW, demonstrating India's commitment to reducing its reliance on fossil fuels. Additionally, the regional disaggregation of electricity demand ensures that growth is aligned with specific regional needs, considering historical trends and future projections. It presents granular planning through spatial demand allocation and the development of regional load profiles based on data from Power System Operation Corporation Limited (POSOCO). Reaching these goals will involve issues of infrastructure modernization, policy support, and finance. The peak demand projected by 2050 at 750 GW (700 GW in a low-carbon scenario) will require many folds of installed capacity compared with the current situation from ∼1828 GW to 2291 GW. VRE capacity will emerge to be dominant, as indicated by ∼20% of the installed capacity in 2020 and ∼79% to ∼96% of the installed capacity by 2050. This path puts tremendous potential for transformational impacts of renewables in the energy system of India. India's pathway to its 2030 energy goals is ambitious but achievable. Prioritizing renewable energy expansion, integrating advanced energy storage, and implementing supportive policies can place India at the helm of the global transition toward a sustainable energy future. The outlined strategies and projections present a clear roadmap for overcoming challenges and achieving a resilient, low-carbon energy system.

Deregulated system

A strong deregulatory framework is needed to integrate renewable energy and mitigate challenges in the traditional, regulated energy markets that tend to favor fossil fuels. Deregulation can further spur the transition to sustainable energy systems by encouraging competition, removing bureaucratic barriers, and promoting fair access for renewable developers. Key aspects include revising regulations to allow flexible grid operations, streamlining permitting processes, and implementing transparent auctions for renewable projects. Reforming tariffs to reflect the true cost of carbon emissions can further incentivize green energy adoption. PPAs, which provide long-term financial security to renewable developers, are vital tools. Mandating utilities to procure a percentage of energy from renewables and encouraging competitive bidding for PPAs can drive costs down and enhance market efficiency. ISOs play a key role in managing grids and balancing supply and demand while ensuring the reliability of the grid through competitive bidding processes. ISOs coordinate energy dispatch, encourage renewable integration, and make transparent pricing mechanisms such as Market Clearing Prices (MCP) and Locational Marginal Pricing (LMP). Advanced technologies such as resource forecasting, load demand prediction, and energy storage systems improve the stability and efficiency of the grid. Smart inverters and automated fault detection enhance power quality and system reliability. The smart grid framework, supported by deregulation, encourages private sector participation in generation, transmission, and distribution, leading to innovation and better consumer services. In the end, deregulation opens the door to a competitive, efficient, and sustainable energy system that aligns with national and global decarbonization goals while stimulating economic growth through renewable energy investments and job creation. In a deregulated grid system, generation, transmission, and distribution of electricity are distinct businesses, allowing private sector participation and encouraging competition. Such segmentation ensures efficiency, increases the quality of the power supply, and provides energy at a competitive cost to consumers. The smart grid structure encompasses some modern technologies, such as forecasting of resources, prediction of demand load, energy storage devices, power quality enhancement, and automated fault detection, in which the grids operate very seamlessly and efficiently. The central role in this system is the ISO, which manages all transactions between generators, distributors, and retailers. The transparent, fair market dynamics are allowed by ISOs to flow through the process of bidding, renewable energy integration, and calculating unit charges. It ensures that the supply equation of energy and demand balance will be optimized while enhancing the reliability of the grid. MCP is derived through the intersection of supply as well as demand curves, exhibiting market equilibrium, whereas LMP takes into account transmission loss and location-based delivery expense. These methods ensure costs are accurately allocated and the smooth operation of the grid. In India, the generation and consumption activities are properly coordinated by the various bus systems forming the grid. Such reports enable the ISOs to make data-driven decisions regarding energy distribution by generation plants and distribution companies about the optimum need of capacity and load. Consumers are allowed to select energy producers, and the transparent mode of operation by ISOs leads to this. This model encourages renewable energy use by imbalances, which give rewards for surplus generation and charges for shortfalls. Advanced systems of energy storage, such as batteries, pumped hydro storage, and compressed air energy storage, also make grid stability possible by overcoming issues of intermittency of the source.

Summary of the Model

Profit Calculation: Profit is calculated as revenue from electricity sales, adjusted by imbalance costs—positive for surplus generation and negative for deficits—and reduced by total generation costs. Imbalance Cost: Rewards generators exceeding demand and penalizes underperformance, driving operational efficiency. Scenarios: Evaluate financial performance across varying supply-demand relationships. Model Applications

a. Incentives for Excess Generation: Reward the generators for surplus energy, hence motivating more integration of renewable and ensuring grid reliability. b. Renewable Energy Support: Encourage investments through incentives for surplus generation. c. Energy Storage Utilization: Use surplus energy for storage solutions, which ensures optimum use of resources and stabilizes supply. d. Consumer Benefits: Reliability improvement and cost savings through dynamic pricing. Solution Methodology

a. System Objectives: Renewable integration, reliability, cost efficiency, and incentives for excess power. b. Data Infrastructure: Utilize historic data and real-time communication networks to enable informed decision-making. c. Role of ISO: Centralized management of bidding, pricing, and renewable integration. d. Profit Model: Calculate profits based on real-time supply-demand conditions and imbalance adjustments. e. Energy Storage Management: Use storage systems to balance supply in the event of variability. f. Dynamic Pricing: Establish pricing models that reflect the current conditions of the grid. g. Contractual Frameworks: Determine terms of energy production and consumption agreements. h. Performance Monitoring: Use KPIs on reliability, efficiency, and profitability. i. Stakeholder Engagement: Create a platform for cooperation between consumers, producers, and regulators.

India's energy mix faces the challenge of rising demand being coupled with sustainable supply alternatives. The future advanced energy storage systems are lithium-ion batteries, pumped hydro storage, and compressed air energy storage systems that can handle intermittency in renewable energy. These technologies enhance resilience in a grid by releasing surplus at low-demand periods but releasing surplus energy during peak demand, thus stabilizing and ensuring such stability. They can support India in scaling up on renewable energy adoption over infrastructure build-out and create a strong, sustainable foundation for their energy future through integration into efficient methodologies.

Electrical energy storage systems

EES is an essential cornerstone of modern power systems as it addresses several critical issues, including the variability of renewable energy sources, ensuring grid reliability, and managing peak demand (Denholm and Hand, 2011). These systems enable the efficient integration of renewable energy, optimize electricity usage, and provide ancillary services for the stabilization of the grid. The technical capabilities of EES involve various technologies designed for specific applications and operation conditions (Zakeri and Syri, 2014).

Role of EES

The inherent nature of electricity makes it challenging and underlines the need for EES. One major challenge is that electricity has to be consumed immediately after it is produced. The delivery process also needs constant balance in response to changes in demand. It is also complicated by the distance between power plants and users. Power transmission relies on the constant use of power lines. Any disruption, such as congestion, can stop the supply of energy (Divya and Østergaard, 2008). This also makes it hard to provide power to mobile applications. In addition, power flow imbalances due to variations in supply and demand may cause a concentration of load on certain transmission lines, causing congestion problems (Ibrahim, Ilinca and Perron, 2007).

Optimization: High generation cost during peak hours

Generation costs are high at peak hours. The suppliers of power are bound to use costly flexible options like oil and gas turbines.

EES helps by storing surplus energy during cheaper, off-peak hours and releasing it during peak demand, thereby lowering the overall generation costs.

Utilities benefit from the reduction of total generation expenses through strategic energy storage and release.

Consumers save money through the use of stored, low-cost electricity during peak hours instead of buying expensive power.

Consumers can recharge their batteries during off-peak times and even sell surplus energy during peak periods for profit (Luo et al., 2014).

Continuous and flexible supply: The need of the hour

A utility must ensure a continuous and flexible supply of power to maintain energy quality and avoid service interruptions. Power generation should be adequate and demand-based, with accurate forecasts of consumer demand. Two important functions of a power plant are the generation of adequate electricity in kW and a frequency control system to vary the output for minute-by-minute changes (Akhil et al., 2015). EES helps to answer these needs by making energy available to meet fluctuations. For instance, pumped hydro storage is mainly used to supply high power when electricity production is low, thus supporting grid stability and flexibility (Chen et al., 2009).

Distance between generation and consumer: A deciding factor

Distance between consumers and power generation sites heightens the risk of disruptions in electricity supply. Power outages resulting from natural events or human mistakes can cause major service disruptions in wide geographical areas (Barton and Infield, 2004). EES reduces these impacts as it provides power in times of such failures. Data centers and hospitals, which have to continuously receive power for their most critical operations, rely on EES to prevent system downtime as well as the loss of sensitive equipment. This provides reliability and minimizes the possible impact of power discontinuity (Schoenung and Jim Eyer, 2008).

Power grid congestion: A cause for concern

Power grid congestion is an imbalance between electricity supply and demand, which causes transmission networks to overload. It leads to inefficiencies and disruptions in power delivery. Utility companies may move generation closer to high-demand areas or expand the transmission infrastructure to address this. However, these solutions are costly and time-consuming (Hussain et al., 2020a). EES provides a more efficient alternative by storing excess power during low-demand periods and releasing it during peak times (Farooq et al., 2022; Singh et al., 2021). Installing EES at strategic locations, such as substations on heavily loaded lines, helps reduce congestion by smoothing out demand spikes. This also enables utilities to delay or avoid costly grid reinforcement projects, ultimately improving the grid's efficiency and reliability (Electric Power Research Institute, Inc. et al., 2016).

Transmission by cable: Point of difficulty

The power transmission via cables is very limited and not possible at all in some cases. This makes electricity supply impossible to remote or mobile applications. This technology is problematic for locations not have access to a reliable power grid. EES is a solution to this because it offers portable energy storage and charging capabilities. EVs can be charged in isolated areas using EES, eliminating the need for a direct grid connection (Brenna et al., 2020). This allows for the creation of a sustainable transportation system dependent on clean energy and minimizing reliance on conventional internal combustion engines. This further contributes to off-grid environmental benefits and makes energy accessible in off-grid regions (IRENA et al., 2017).

Emerging Needs for EES

Several emerging needs increase the demand for Electrical Energy Storage:

A Step Towards a Greener Earth: As the world shifts towards cleaner energy sources, EES plays a crucial role in integrating more renewable energy like solar and wind, reducing reliance on fossil fuels. It stores excess renewable energy for use when generation is low, contributing to a cleaner, sustainable energy system (Barbhuiya, Das and Adak, 2024), (Wu, Zhang and Khan, 2024), (Luo et al., 2014). Renewable Energy Integration: With the increased utilization of renewable energy, EES balances the intermittent nature of these sources by storing energy when there is surplus production and releasing it during periods of high demand or low generation (Hadi et al., 2024). Grid Stability: EES stabilizes the grid by ensuring a steady power supply. It can reduce grid congestion, balance supply and demand, and provide backup power during outages, making the grid more reliable and resilient (He, Shepherd and Wang, 2024). On-Grid and Off-Grid Areas: EES is indispensable for both on-grid and off-grid systems. For on-grid areas, it allows for better energy management by storing surplus power from renewable sources, whereas for off-grid areas, it guarantees access to electricity, even when the grid is not available, supporting local energy independence. Smart Grid: As power grids evolve into smart grids, EES becomes integral in optimizing grid performance. By enabling real-time monitoring and adaptive control, EES helps make the grid more efficient, responsive, and capable of handling fluctuating demand and supply (Akkara and Selvakumar, 2023). Electrification of Transport: Since electric vehicles (EVs) are rapidly becoming popular, EES supports the charging of efficient EVs, even for people who are not geographically close to the power grid, thus aiding in building green transportation networks (Caroleo, Lazzeroni and Arnone, 2024). Cost Savings: EES empowers consumers to stockpile electricity when the electricity rate is low and use or sell it when there is a peak period and the electricity is high-priced, thus decreasing the energy costs (Berg, Foslie and Farahmand, 2024). Emergency Power Backup: With natural disasters or grid collapses, EES provides emergency backup power; thus, critical infrastructure, such as hospitals, data centers, and communication networks, are maintained operational (Hussain et al., 2020b). Types of Energy Storage System (EES):

EES systems are categorized based on the nature of energy used: (i) mechanical, (ii) electrochemical, (iii) chemical, (iv) electrical, (v) thermal and (vi) superconducting magnetic categories.

Renewable energy integration into the electricity market

Renewable energy is incorporated into the electricity market through organized mechanisms that allow for its intermittent nature while promoting competition, flexibility, and sustainability in energy systems. In deregulated markets, for example, the ones that are emerging in India and most of the developed countries, the role of renewable energy sources is supported by policy instruments such as PPAs, renewable energy auctions, and dynamic pricing approaches. These measures ensure financial sustainability and predictability for investors, while market facilities such as day-ahead and real-time markets enable renewable energy generators to compete against traditional generators. ISOs and RTOs are the key entities coordinating grid operations, maintaining grid reliability, and enabling variable renewable energy sources integration using sophisticated forecasting, scheduling, and dispatch procedures. Additionally, technologies such as smart grids and Supervisory Control and Data Acquisition (SCADA) systems support real-time monitoring, decentralized control, and optimal dispatch of DERs such as rooftop solar, wind farms, and hybrid renewable systems. EES, e.g., lithium-ion batteries, pumped hydro, and compressed air energy storage, play a key role in enabling this integration by absorbing excess during off-peak generation and releasing power during high-demand periods to balance and secure the grid. Ancillary services markets have likewise been redesigned for the acceptance of renewable sources through the promotion of grid-supporting behavior like frequency regulation, voltage support, and spinning reserves.

The importance of bringing renewable energy into electricity markets goes far beyond technical or economic considerations, it touches on some of the world's most urgent challenges. First, it decreases reliance on fossil fuels, thus reducing greenhouse gas emissions and helping to mitigate climate change. Second, it decentralizes power production, enabling communities and enhancing energy access in isolated and underserved areas. Thirdly, it improves energy security by lowering geopolitical risks associated with imported fuels and cushioning price uncertainty in international energy markets. Furthermore, the integration of renewables stimulates economic growth through employment in installation, maintenance, manufacturing, and R&D industries. The interaction between renewables, EVs, and smart grids also complements the wider decarburization of transport and industrial sectors toward overall sustainability objectives. Significantly, it makes possible dynamic energy markets where end-users become ‘prosumers’, engaged actively in the production, storage, and trade of energy, making the energy system even more democratic. For countries with emerging economies such as India, whose demand for energy is growing exponentially, renewable integration supports both goals of increasing access to energy and ensuring national fulfillment under the Paris Agreement. In general, the smooth integration of renewable energy into contemporary electricity markets is not only a technological achievement but a social necessity that provides a cleaner, fairer, and economically secure future.

The complex nature of modern energy systems introduces several critical challenges that must be carefully managed to ensure reliability, sustainability, and efficiency. One major challenge stems from the variability and intermittency of renewable energy sources like solar and wind, which can cause unpredictable fluctuations in power supply and complicate grid balancing efforts. In addition, the integration of a high proportion of DERs brings about bi-directional power flows, rendering classical grid management models inadequate. The aging transmission and distribution infrastructures, which are for centralized and uni-directional flow, are not well suited to accommodate the dynamic, decentralized characteristics of contemporary energy systems. Cyber threats also grow with the increasing digitization and interconnectivity of the grid through smart grid technologies and Internet of Things (IoT) devices. Further, market and regulatory structures in most regions have not developed quickly enough to support flexible, decentralized energy engagement, and this creates mismatches between policy frameworks and technical innovations. Social challenges, including the provision of equitable access to clean energy and handling the socioeconomic effects of the transition, also contribute to the complexity. To address these issues proactively, several strategic steps may be followed.

First, spending on sophisticated forecasting equipment based on AI and ML may enhance the predictability of renewable energy output and demand trends so that more efficient planning and real-time dispatch can be made. Second, the use of scalable and diversified EES can help alleviate intermittency concerns and offer grid flexibility. Improving transmission and distribution infrastructure to accommodate smart, bi-directional energy flows is critical to high DER penetration levels. Dynamic market mechanisms like real-time pricing, demand response programs, and capacity markets can more effectively align economic incentives with grid requirements. Cybersecurity has to be assured by strong, responsive security measures that defend vital energy infrastructures against possible attacks. Regulators need to work at a faster pace to develop flexible, open, and innovation-encouraging energy markets that promote new technologies and business models. Also, effective stakeholder engagement ranging from communities, industries, and policymakers—will be crucial in making inclusive, equitable energy transitions that confront social and economic inequalities. Through the integration of technological innovation, infrastructure modernization, market restructuring, and social inclusion, countries can effectively adapt to the complications of contemporary energy systems and fulfill resilient, sustainable energy futures.

EV's status and future aspects

The transportation sector is undergoing a deep transformation due to the critical need to reduce carbon emissions, combat climate change, and mitigate the environmental impacts of conventional fossil-fuel-powered vehicles. Among the most promising solutions is the adoption of EVs, which rely on electricity rather than internal combustion engines. EVs have garnered significant attention in recent years with their potential to lower greenhouse gas emissions, improve air quality, and decrease reliance on finite fossil fuel resources (International Energy Agency, 2024). Technological development in battery efficiency, energy storage systems, and charging infrastructure has been crucial to the rapid growth of EVs. These innovations not only make electric mobility more accessible but also add to the overall sustainability of the transportation ecosystem. Meanwhile, governments across the globe are pushing the adoption of EVs through policy incentives, regulation, and investment in the charging infrastructure (Chanda et al., 2024), (Kumar, 2022). Although this is so, challenges persist; some of the main challenges facing EVs include high upfront costs, a relatively limited driving range compared to conventional vehicles, and a need for an expanded charging network. Nonetheless, research and development are overcoming the barriers to battery performance improvement, cost reduction, and expansion of the charging infrastructure.

This paper looks at the new trends in electric vehicle technology, discusses their environmental and economic benefits, and analyzes challenges and opportunities related to their full-scale adoption. By giving a comprehensive overview, it contributes to the ongoing debate on the future of transport and the critical role EVs play in achieving a sustainable, low-carbon future.

Growth in Electric Vehicle Sales

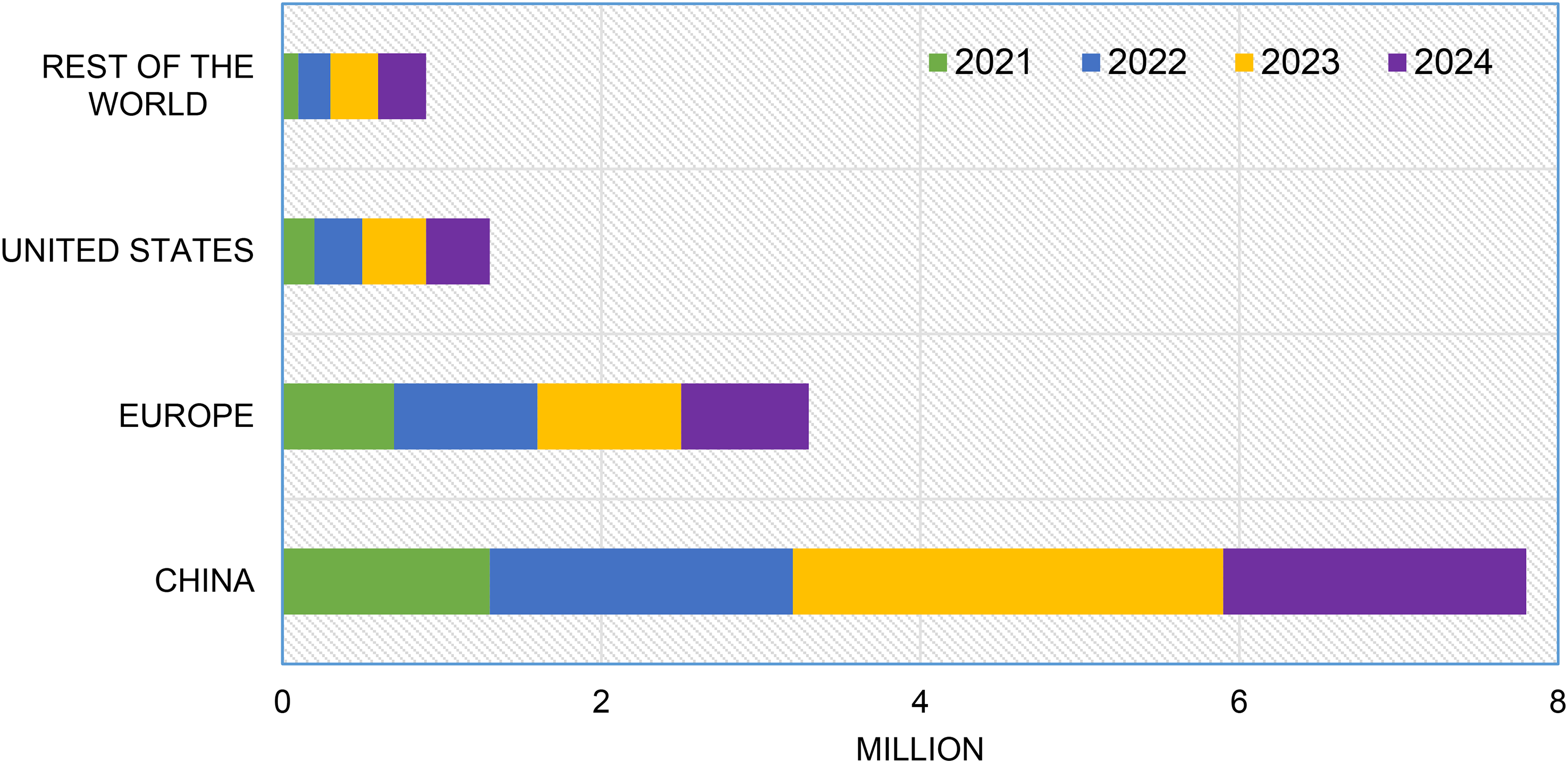

Electric vehicle sales are steadily increasing and could reach around 17 million units in 2024, accounting for more than 20% of all cars sold worldwide. This robust growth underscores the transition of EVs from niche markets to mass-market adoption in many countries. However, challenges such as tight profit margins, volatile battery material prices, high inflation, and the gradual removal of purchase incentives in some regions have raised concerns about sustaining the industry's momentum. Despite these hurdles, global sales data remain strong. In the first quarter of 2024, EV sales grew by 25% compared to the same period in 2023, maintaining a similar year-on-year growth rate observed in 2022. China, Europe, and the United States together control the EV market and, in 2023, accounted for 95% of global EV sales. The market was dominated by China at 60%, Europe at 25%, and the United States at 10% (shown in Figure 15). It is worth noting that Chinese manufacturers accounted for more than half of all EVs sold worldwide while representing only 10% of global sales for internal combustion engine vehicles.

Electric car sales by region 2021–2024.

Emerging and developing economies are slowly increasing their share of EV sales, with countries such as Vietnam and Thailand attaining EV market shares of 15% and 10%, respectively, in 2023. In larger emerging markets like India (2% share) and Brazil (3% share), government initiatives such as purchase subsidies and manufacturing incentives are playing a crucial role in promoting adoption (Gül et al., 2024). A few indicators point toward further growth in emerging economies. These include affordable EV models from Chinese manufacturers and India's PLI Scheme, a policy supporting domestic manufacturing. Mexico is one example of the rapid development of its EV supply chains, enhanced by access to subsidies under the US Inflation Reduction Act (IRA), pointing to growth opportunities in markets outside of traditional leaders (Podesta, 2023).

Indian Survey on EVs:

EVs, an innovation in the automobile industry, have emerged as a cleaner and more efficient alternative to traditional internal combustion engine (ICE) vehicles. Using electricity stored in advanced batteries and electric motors for propulsion, EVs have revolutionized the conventional understanding of mobility. Recent advances in battery technology, an increasing number of charging infrastructures around the globe, and increased consumer acceptance have placed EVs firmly in the space as a viable and sustainable option for a wide array of users worldwide. India is the world's third largest automobile market by sales volume, overtaking Germany and Japan, which is strategically shifting towards more sustainable transport. The automobile industry alone contributes 7.1% to India's GDP and offers huge employment avenues. It is indeed in the process of great transformation with immense cooperation between manufacturers and policymakers (Electric Vehicles, 2024). As per Economic Survey 2023, the domestic electric vehicle market of India is likely to grow at a compound annual growth rate of 49 percent from 2022 to 2030 and reach a projected 10 million annual sales by 2030 (NITI Aayog et al., 2022). Furthermore, by the same year, the EV sector is expected to create around 5 million direct and 30 million indirect employment opportunities (Sunita, 2025). The Indian government has set an ambitious target to achieve 30% electrification of the country's vehicle fleet by 2030. In support of this shift, various incentives and policy frameworks have been implemented.

The FY24 Union Budget has been a significant boost to the sector, with capital investments for accelerating the energy transition and achieving net-zero carbon emissions by 2070. Finance Minister Nirmala Sitharaman announced an allocation of INR 35000 crore for these critical investments, alongside support for Battery Energy Storage Systems (BESS) with a 4000 MWh capacity through viability gap funding. Further, the administration has taken various measures including the FAME-II, or Faster Adoption and Manufacturing of Hybrid and Electric Vehicles Scheme (II), and the Production Linked Incentive Scheme to boost the scale of EV manufacturing and adoption in the country. The FAME II scheme announced a budgeted allocation of INR 51.72 billion (approximately $631 million) to meet the subsidies on clean-energy vehicles, an increase of 80% from previous years (FAME II scheme, 2024). The reductions in customs duty for lithium-ion batteries, excise duty exemptions on natural gas and biogas, etc. are also expected to attract foreign investment and import EVs into India. Domestic companies such as Tata Motors and Mahindra & Mahindra have gained a lead in manufacturing EVs while international automobile companies like Volvo Cars are exploring the opportunities for establishing EV manufacturing units in India. Volvo's interest in investing is an example of the increasing importance of India as an EV manufacturing hub worldwide.

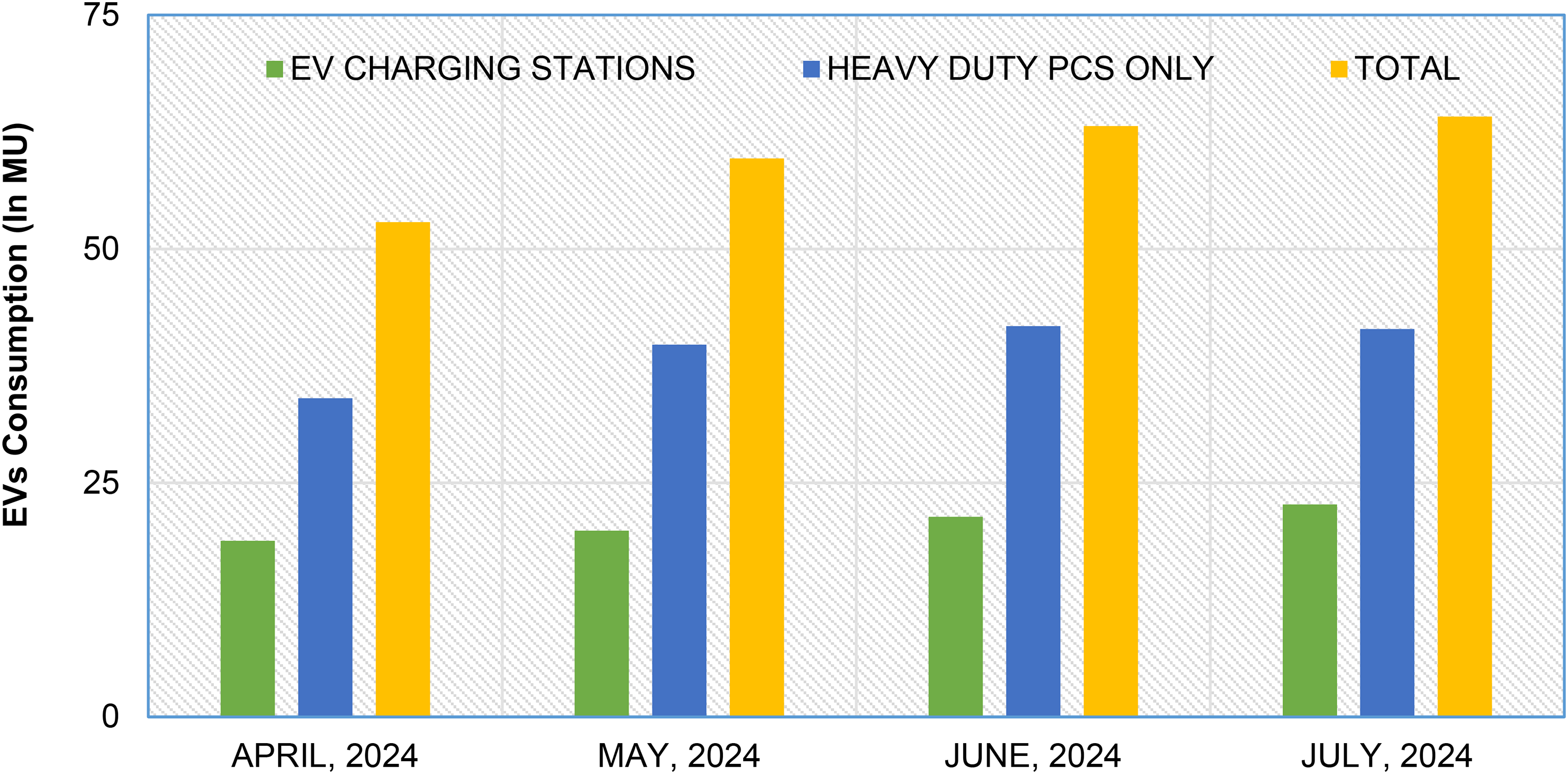

Investment in EV charging infrastructure has been another focus, where public and private partnerships have been encouraged. The establishment of India's first EV charging plaza by Energy Efficiency Services Limited (EESL) in July 2020 was a landmark moment. Charging stations multiplied fivefold within the first year. The success of such state-level initiatives, such as the Delhi EV Policy initiated in 2020, has been evident in the national capital, where EVs have accounted for 16.8% of total vehicle sales in December 2022, reflecting year-on-year growth of 86%. India's electric vehicle market is on the verge of a transformation. The robust policies of the government, technological advancements, and increased awareness among consumers are likely to drive this change (shown in Table 6 and Figure 16). This new ecosystem holds great opportunities for domestic and international investors who can invest in and contribute toward the development of a sustainable and eco-friendly transportation framework in the country.

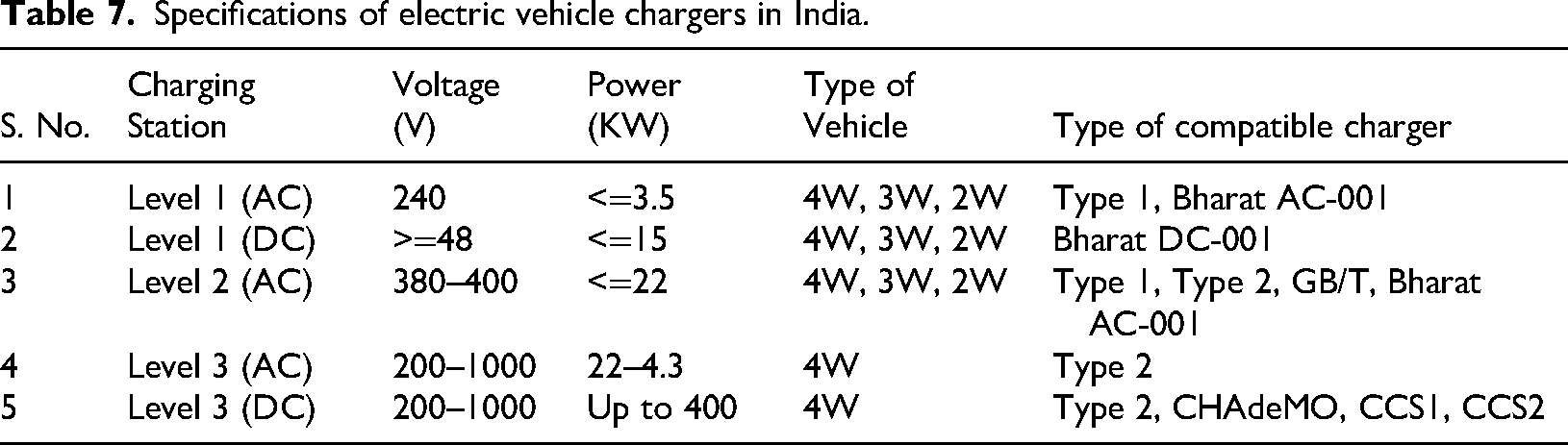

Electricity consumption details of EV charging stations in India.

Electricity consumption details of EV charging stations in India (in mu).

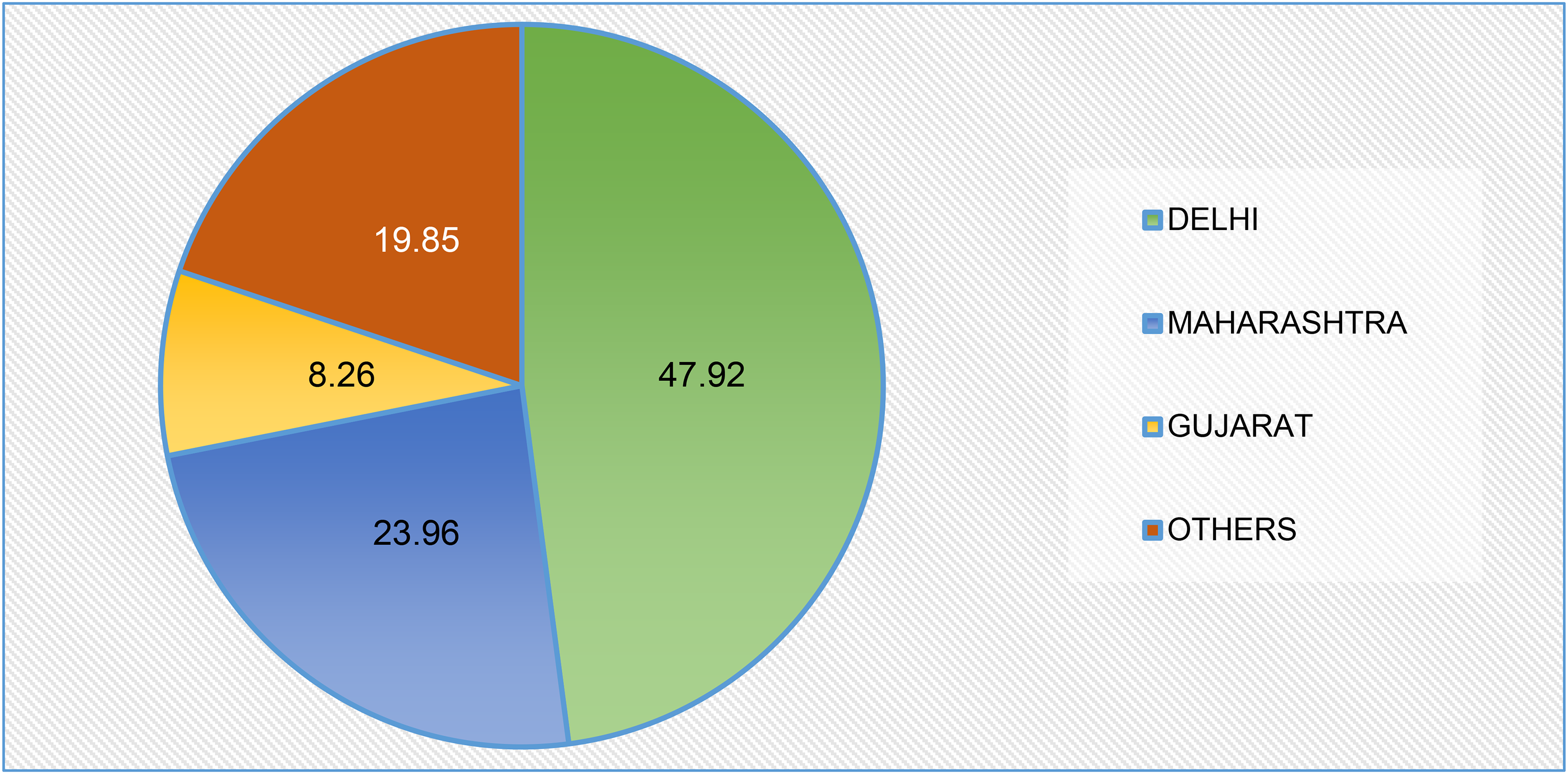

As is evident from Figure 17, from 2024–25 till July month, Delhi has consumed the maximum electricity by electric-vehicles that is 114.92 MU, 47.92% followed by Maharashtra at 57.45 MU, 23.96%, and Gujarat at 19.82 MU, 8.26%. The graph shows the electricity consumption by EV charging stations along with Heavy-duty charging stations during the period from April 2024 to July 2024. Total electricity consumption in July 2024 was 64.14 MU.

Integrating EVs with the Grid: The Role of V2G Technology

Total EV-PCS electricity consumption in 2024–25 (till July 2024) (in MU, %).

V2G technology enables two-way energy flow between EVs and the power grid, converting EVs into dynamic energy storage units. In this process, there are several critical components and steps to be considered:

Balancing the Grid with V2G Technology

To keep the electrical grid in real-time balance and frequency stability, energy generation must be balanced with consumption. This is done using two types of energy sources:

b. The solution: V2G and V2H

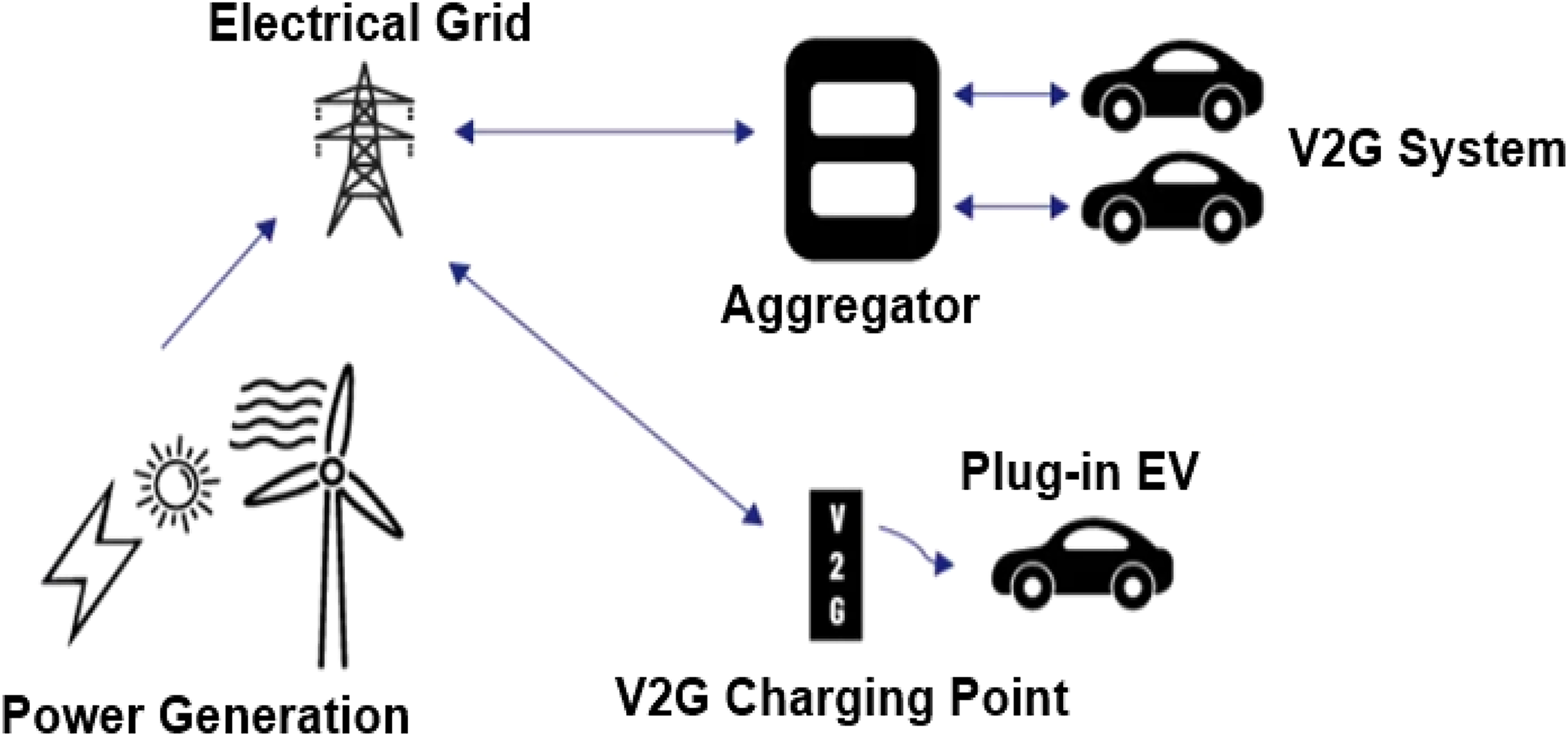

V2G technology leverages EV batteries to provide electricity back to the grid during peak demand periods. This bidirectional flow transforms EV batteries into decentralized energy reserves, helping stabilize grid operations locally and globally (Mishra et al., 2024). On the other side, V2H technology makes the batteries of an EV act as mobile energy storage for households. EVs can recharge during off-peak hours, while energy can be utilized in peak hours to power homes and cut electricity costs. In turn, it would support the grid (depicted in Figure 18). Users can then power their homes for an hour or two with the energy stored in their EV battery. They can charge their EVs when the cost of electricity is lowest and feed some of the stored energy back into the grid when the cost of electricity is at its highest. This implies that the user will pay off-peak rates to recharge his EV rather than peak rates, and he will enjoy the benefit of reduced household consumption during peak hours, which would bring down the demand in that window also (Chatuanramtharnghaka et al., 2024), (Chung and Ryu, 2024), (Ghatikar and Alam, 2023).

Block diagram of V2G system.

The technology of V2G and V2H also has an added benefit for balancing generation and demand, regulating non-controllable energy sources, and reducing the electricity bill of the end-user. While the idea behind V2G charging is fairly straightforward, the actual implementation is highly complex with a comprehensive smart technology set-up. The charging station will require software to interact with the central grid for estimating system demand at any time point.

EVs with V2G functions are connected to a charger that supports the two-way flow of power. The chargers are called bi-directional chargers since they allow the electricity to flow between the vehicle and the grid. When an owner of an EV plugs it into a charger to recharge, the charger supplies the electricity to the EV's battery. This is unidirectional since electricity flows from the grid to the car. In a V2G system, the EV also can supply electricity back from its battery to the grid when needed. It can do this through the bi-directional flow whenever it is not in an operational state and is charged with the grid. The role of communication protocols and control systems in V2G technology is important. The smart charging infrastructure and onboard systems of the vehicle talk to each other to find out when it is necessary to charge the vehicle when it should supply back to the grid with extra energy, and what quantity of power needs to be exchanged (Aftab et al., 2018).

Depending on the grid operator's needs, V2G-enabled electric vehicles can supply the following grid services (Ustun et al., 2021):

Peak Shaving: Supplying the extra power during peak hours. Load Balancing: Assisting in balancing the electricity load on the grid. Frequency Regulation: Adjusting the frequency of the electrical grid to stabilize it. Voltage Support: Supplying voltage support during fluctuations. Exploring the Underlying Benefits of V2G Technology

V2G technology is the most revolutionary approach to energy management. It enables EVs to function as part of a distributed energy network. The system maximizes power flow by draining energy from EVs during peak electricity demand and recharging them when the demand is low, which in turn helps maintain grid stability. A key component of this innovation is the concept of a Virtual Power Plant (VPP), which utilizes cloud-based platforms to manage and coordinate various battery storage units, effectively simulating a large-scale generator or storage facility. Unlike traditional power plants, VPPs combine diverse energy assets like solar panels, batteries, and EVs, providing unmatched adaptability and enhancing grid resilience (Nadeem et al., 2019). V2G systems, with their two-way energy flow, stabilize the grid by balancing the fluctuations in supply and demand, especially during peak usage or emergency conditions.

The EVs that support V2G can also be used to regulate voltage to maintain grid consistency. Additionally, bidirectional chargers with power inverters provide backup power during blackouts, demonstrating their dual functionality (Bibak and Tekiner-Mogulkoc, 2021). V2G enables better utilization of renewable energy as it will allow EVs to store extra energy from sources such as solar or wind and return it to the grid when necessary, thereby significantly contributing to sustainability and reducing greenhouse gas emissions.

India's Readiness for V2G