Abstract

In 2022, Malaysia was ranked 28th worldwide in terms of its energy oil consumption. Energy consumption in Malaysia has been predominantly reliant on natural gas and coal in both the past and present. Oil and gas in Malaysia are predicted to be depleted in 14 years due to the high energy consumption, especially from petroleum sources. Thus, the Malaysian government aims to expand renewable energy (RE) in the country's energy mix as an alternative source of energy. As of 2022, Malaysia has generated roughly 2% of its electricity from various renewable sources, which is still far from the initial target of reaching 20% RE penetration by 2030. However, since 2017, RE has started to contribute to energy mix generation. Several policies, including an act, have been implemented in Malaysia to achieve the target in RE, but many challenges and difficulties have hindered the progress. Thus, the present study explored the current status and challenges for RE in Malaysia and discussed the effectiveness of the available energy policies and programs. The outcomes are potentially valuable to Malaysian policymakers, industries and researchers to improve their current practices for achieving the initial national RE target by 2030 as well as to move forward towards net zero emissions by 2050. This study provides a crucial roadmap for Malaysia to achieve its RE objectives and contribute significantly to the international transition towards a more environmentally friendly and sustainable future.

Introduction

Two decades ago, there was a shift in energy demand towards alternative sources as a result of the consistent increase in oil prices. Numerous countries worldwide have voiced apprehension regarding this issue, as a surge in oil prices might potentially endanger their respective countries’ energy security. Between 1973 and 1979, the Arab-dominated Organization of Petroleum Exporting Countries oil embargo demonstrated a high level of concern for energy stability, which continued to intensify after 2004's dramatic increase in oil prices (Razek and Michieka, 2019). Oil prices have varied dramatically during the previous 10–15 years, from record highs in 2012 and 2013 to record lows in 2015 and 2016 (Brown and Huntington, 2017). When oil prices reach an all-time high and spark demonstrations, they have a knock-on impact on the economy and energy security (Espinola-arredondo, 2019). Other low-cost and more sustainable sources must be identified for continuous access to energy (Menegaki, 2008). Renewable energy (RE) sources are identified as new candidates for power generation sources instead of oil and gas (Aleixandre-Tudó et al., 2019).

Malaysia is blessed with conventional energy sources, such as crude oil, natural gas and coal, as well as alternative energy sources, such as hydro, biomass and solar (Kardooni et al., 2018). Malaysia is the second-largest oil and natural gas (O&G) producer in Southeast Asia and fifth in the world, given its abundant O&G reservoir. However, these resources will be depleted in the near future. As of January 2021, according to statistics reported by the Oil and Gas Journal, the country's crude oil and condensate reserves totalled 3.60 billion barrels, or 14 years of supply (Conglin Xu, 2021). Meanwhile, Malaysia's natural gas reserves totalled 87.76 trillion standard cubic feet (Tscf), which is sufficient to finance 37 years of gas demand at current rates (Basri et al., 2015). The rapid decrease was observed in January 2020, when the natural gas reserves totalled 41.8 Tscf (Conglin Xu, 2021). Natural gas reserves on Peninsular Malaysia's east coast are set aside for domestic use, whereas those in Sarawak are set aside for revenue generation by LNG exports.

In addition, Malaysia has been reported as one of the fastest-growing countries in terms of greenhouse gas (GHG) emissions. The compounded annual growth rate of 7.9% from 1990 to 2006 (Wan Mansor et al., 2020). Malaysia's GHG emissions are forecast to increase by 74% between 2005 and 2020, from 189 million tons of CO2e to 328 million tons of CO2e (Shamsuddin, 2012). Therefore, Malaysia committed to a voluntary cut of up to 40% in terms of emission intensity of GDP by 2020, relative to 2005 levels, at the United Nations Climate Change Conference's 15th Conference of the Parties (COP) (WO, 2009). Malaysia took this action to significantly reduce GHG emissions and support the environment.

In 1997, the Kyoto Protocol was introduced, requiring further intervention in the post-2000 period to reduce GHG emissions (Bujang et al., 2016; Manolopoulos et al., 2016). The protocol requires developing countries to make a legally binding pledge to reduce their cumulative emissions of six GHGs by at least 5% from 1990 levels between 2008 and 2012 (Gupta, 2016). In addition, the protocol defines a carbon trade system, which includes a clean development mechanism (CDM), to assist countries in satisfying their commitments (Oh and Chua, 2010; Streimikiene and Girdzijauskas, 2009).

The Paris Agreement was implemented at the United Nations Framework Convention on Climate Change (UNFCCC)'s 21st COP (COP21) in December 2015 in Paris (Lau et al., 2012). The Paris Agreement is a landmark international climate agreement that aims to maintain the global average temperature increase well below 2 °C (Gao et al., 2017). In addition, it sought to advance attempts to maintain the increase to 1.5 °C and reach net-zero pollution in the second half of this century (Rahman and Wahid, 2021; Bauer and Menrad, 2019). To comply with the agreement signed by Malaysia at the international level, several policies have been enacted to ensure the objective could be achieved as agreed (Rasiah et al., 2017). The program intended to reduce carbon dioxide (CO2) could only be achieved using renewable sources to create energy (Saidi and Omri, 2020). Continuously using O&G and coal cannot reduce CO2 because the process generates a high volume of CO2 (Razmjoo et al., 2021; Babatunde et al., 2021). Therefore, Malaysia emphasizes the utilization of renewable sources in its policies (Mekhilef et al., 2014).

Renewable energy provides a vast advantage. In terms of environmental impact, it decreases GHG pollution, thereby reducing the effects of global change (Vares et al., 2019). In terms of sustainable development, it reduces dependence on finite fossil fuels (Kuik et al., 2019). In terms of energy security, RE ensures the sustainability of Malaysia's energy supply by reducing dependence on imported fuel (Hannan et al., 2018). Moreover, in terms of economic development, it uses Malaysia's enormous capacity and establishes a competitive, sustainable energy sector.

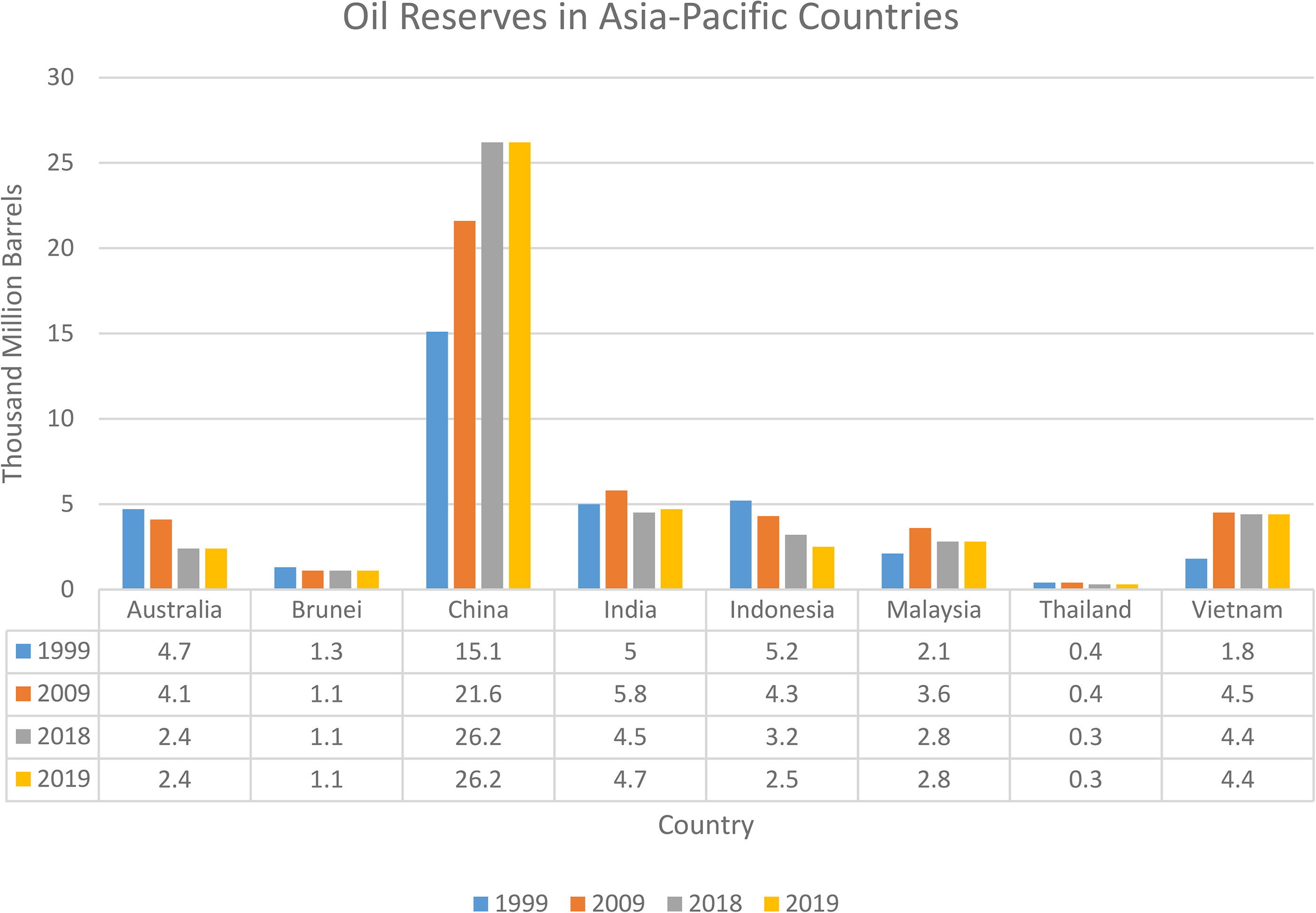

Figure 1 shows the oil reserves in Asia-Pacific countries in a 10-year gap. All Asia-Pacific countries show a decrease in oil reserves, with China being the only country with an increase in oil reserves. The extensive implementation and utilization of RE in China have effectively preserved existing oil and gas reservoirs and facilitated the exploration of new reservoirs. Vietnam showed an increase in 2009 and maintained a stable value after 2009 after it changed from oil and coal usage to a reserved reservoir and utilized RE. Vietnam actively utilizes RE as a primary energy supply; RE has been proven to preserve its non-RE sources. China and Vietnam have proven that RE utilization enhances their energy sources while preserving their unrenewable energy sources safely for future usage. In this situation, Malaysia needs to move fast on RE to ensure the sustainability of its economic income as an energy exporter. To remain in the top 30 energy exporters, RE will help maintain the country's income from this sector.

Oil reserves in Asia-pacific countries.

The RE policy and Renewable Act in Malaysia are evaluated after 10 years of implementation. The details of RE sources and agencies that contribute to RE and RE progress in Malaysia were listed in more information. The current situation of RE in Malaysia was thoroughly analyzed, and the effect of this policy and act after implementation was evaluated. A critical review of the current situation in Malaysia is highlighted in the final section. This finding could help the Malaysian government analyze the effectiveness of the policy and act after 10 years.

Energy demand in Malaysia

Malaysia is a Southeast Asian nation with an average daily temperature ranging between 21 and 32 °C. It covers an area of approximately 330,323 square kilometers (km2). Malaysia's population was 32.7 million in 2020, an increase of 0.4% over the previous year's population. The slower pace of population increase is due to the decrease in the number of non-citizens from 3.1 million in 2019 to 3.0 million in 2020. The citizen population's development rate remained stable at 1.1%, increasing from 29.4 million in 2019 to 29.7 million in 2020 (DOSM, 2020). Malaysia's population statistics are crucial because the energy demand in the country is obtained from its population, especially in electricity usage and fuel for transportation.

Historically, Malaysia has primarily exported crude O&G through pipelines in liquid form. In 2015, 46,035 kilotons of energy (ktoe) were exported, an expansion of 11% over 2014 (41,414 ktoe). The majority of the increase in energy exports was due to an unexpected increase in crude oil exports from 2051 ktoe in 2014 to 7696 ktoe in 2015, an amount not observed since 2007. Total energy imports decreased by 0.4% between 2014 and 2015, from 38,080 ktoe to 37,927 ktoe (Energy Comission of Malaysia, 2018). The majority of the downturn occurred in petroleum goods, given the decrease in overall energy imports from 16,009 thousand tons in 2014 to 14,218 thousand tons in 2017. In the year 2020, the decrease of −14.3% in export petroleum oil products was compared with that in 2019, with a value of $12,784,896,000. At the same time, crude oil exports recorded a decrease of −32.9% with a value of $4,717,198,000 in 2020 compared with 2019 (Workman, 2021).

Malaysia's oil reserves (including condensate) amounted to 5.9 billion barrels, with Peninsular Malaysia accounting for 37% of the total (the Malay basin) (Ministry of Economic Affairs Malaysia, 2017). Malaysia's economic progress and population expansion over the last decade have resulted in significantly increased power consumption. In 2018, the nation generated approximately 160 gigawatt-hours (GWh) of net power (U.S. Energy Information Administration, 2021). In response to the country's population growth, the Malaysian government has taken several steps to investigate and encourage the use of RE as a substitute fuel source.

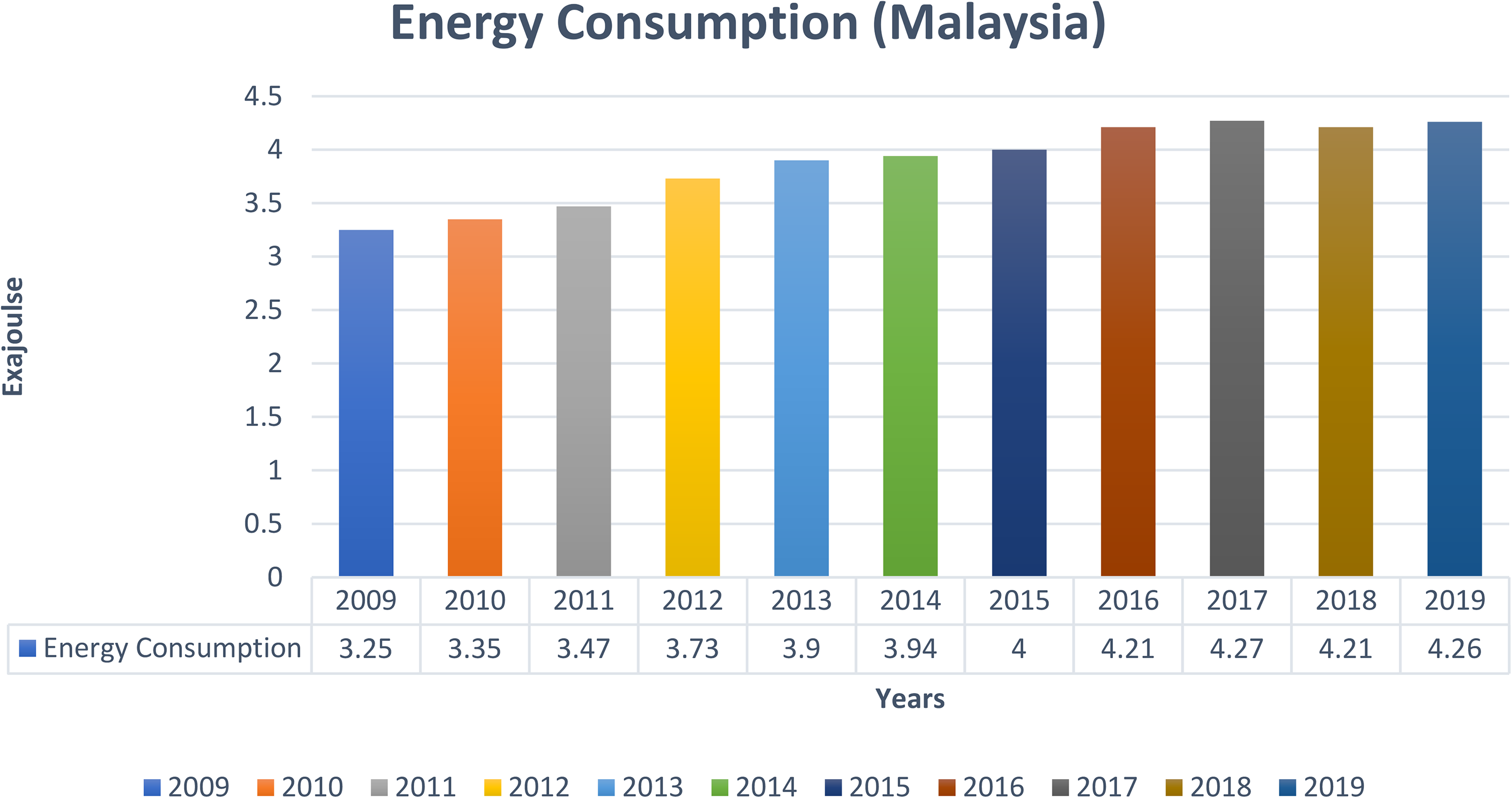

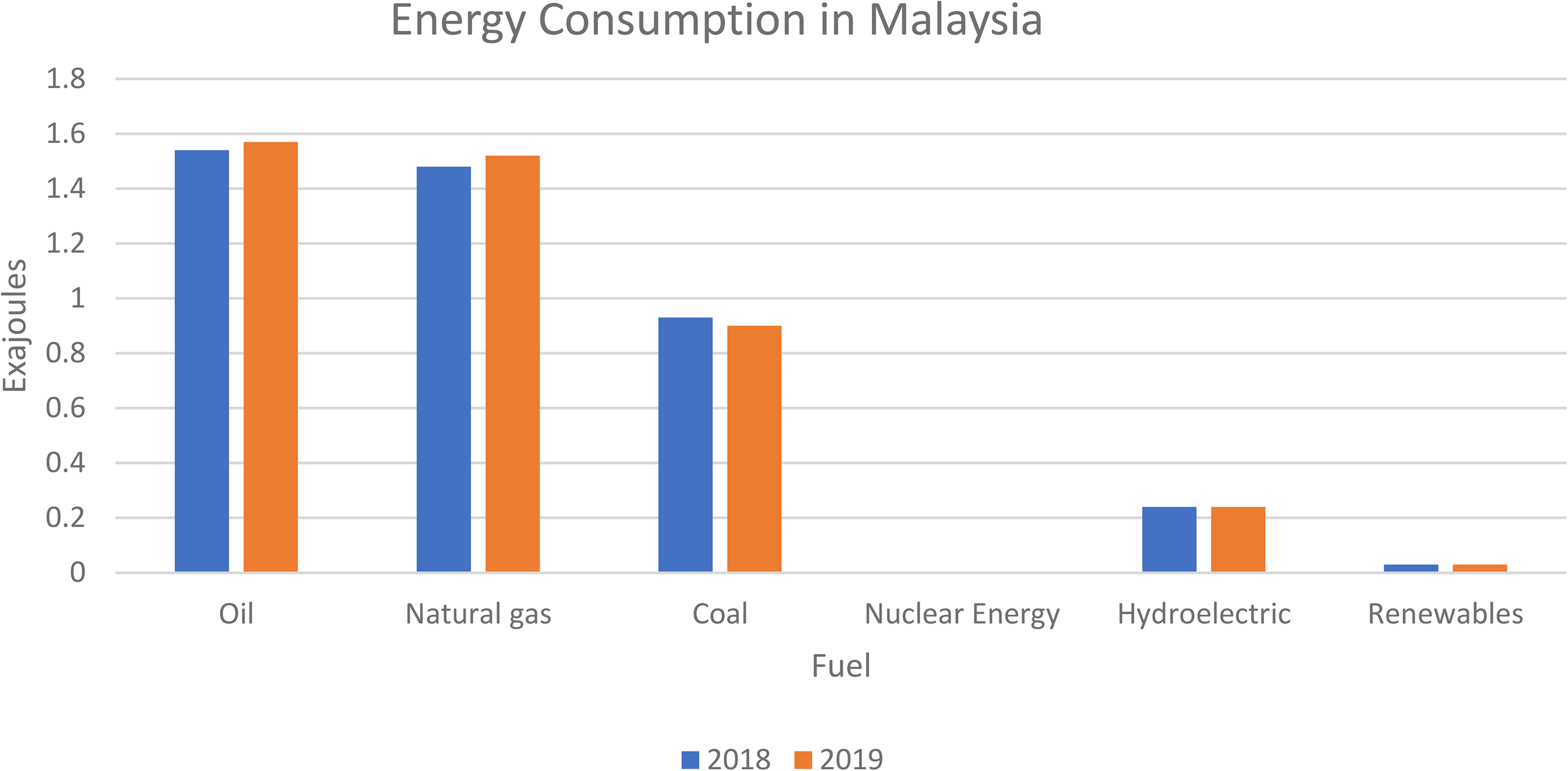

Figure 2 depicts Malaysia's energy use from 2009 to the end of 2019, indicating an increasing trend in energy consumption. The increase results from various factors, including the country's population growth and an increase in economic activity. By examining energy use, which also reflects Malaysia's energy requirements, it can be deduced that the country's O&G and coal reserves may not last much longer. As of 2020, the reported energy consumption in Malaysia is approximately 4.26 (BP, 2020). Oil reserves have been predicted to only persist for 14 years, as explained previously. Thus, energy sources must immediately shift to RE. Figure 3 shows the Malaysia's energy consumption by fuel types.

Energy consumption in Malaysia by years.

According to the country's Energy Commission (EC), between 2015 and 2020, energy demand in Malaysia increased from 16,822 MW to 18,808 MW, or 2.3% annually. In 2020, the COVID-19 pandemic significantly reduced the overall demand. However, fresh peak demand was reported on March 10, 2020, barely one week before the Movement Control Order was implemented on March 18, 2020. Demand is expected to grow at a rate of 0.9% per year between 2021 and 2030 and 1.7% per year between 2030 and 2039 (Tenaga, 2021a). As per the Generation Development Plan 2020, the net demand in Malaysia is expected to grow at a rate of 0.6% per year between 2021 and 2030 and 1.8% per year between 2031 and 2039. By 2030, 6077 MW of additional capacity will be required to satisfy demand growth, replace retiring plants and ensure system stability, with reserve margins expected to fall below 25% by 2039 (Tenaga, 2021b).

Energy policies in Malaysia

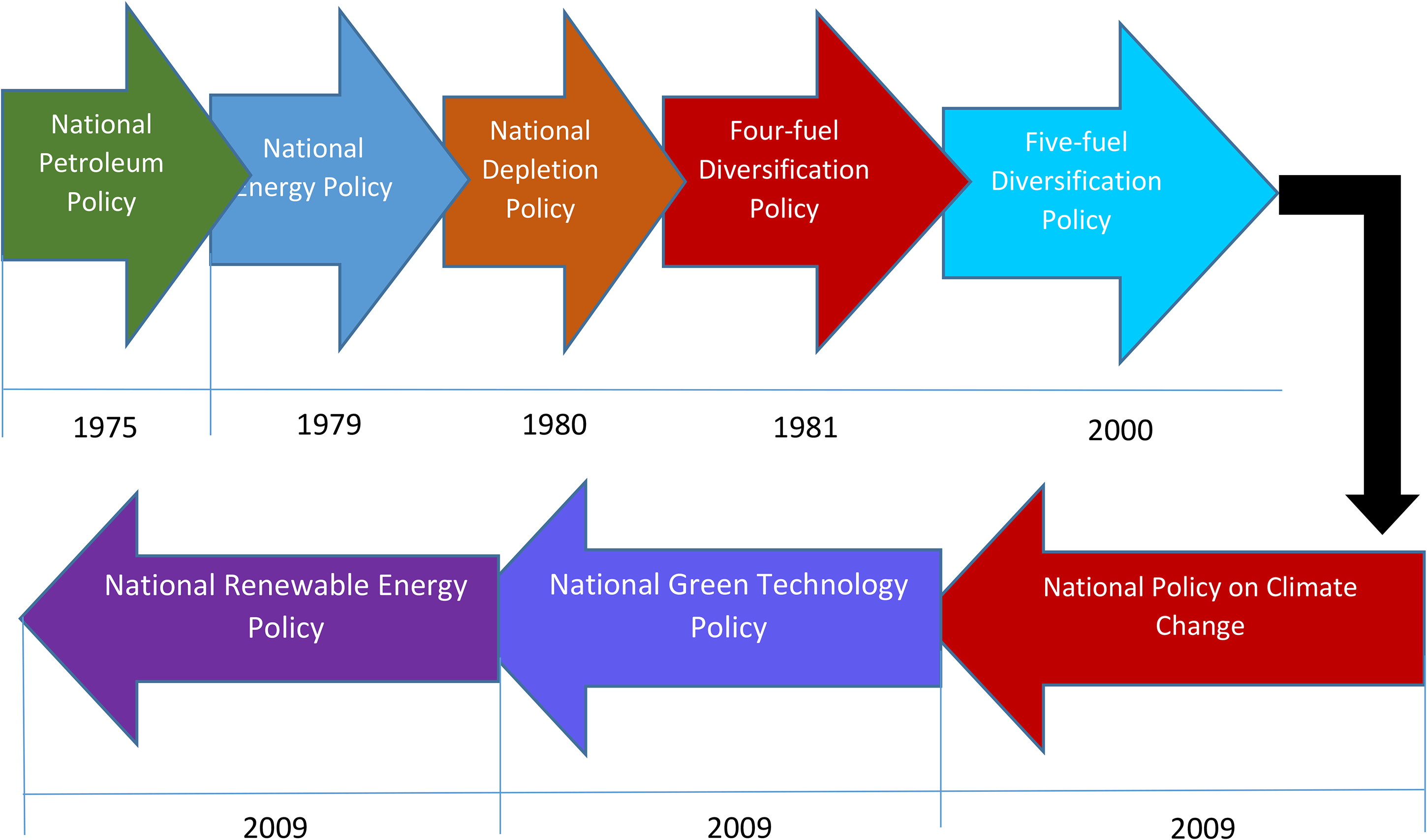

As shown in Figure 4, in 1979, the National Energy Policy was established; it is the older policy for the energy sector in Malaysia (Chua and Oh, 2010). There are three main objectives that drive this policy. The first objective is to ensure a sufficient, safe and cost-effective energy supply that makes the best use of environmental materials possible. The second objective prioritizes utilization, which calls for the implementation of productivity and recycling programs to reduce inefficient and ineffective energy use trends. The third objective emphasizes the climate goal, which specifies that environmental considerations will not be ignored in the pursuit of supply and consumption goals.

Energy consumption in Malaysia by fuel types.

Policies related to RE in Malaysia.

To complement the National Energy Policy of 1979, a five-fuel policy was implemented in 2001 as part of the 8th Malaysia Plan (Hashim and Ho, 2011). The objective was to shift the country's energy balance towards five fuels, namely, crude, gas, coal, hydroelectricity and RE. Malaysia will be fitted with a renewable model of energy production as a result of this strategy. To accomplish this aim, the Small RE Program (SREP) was launched as part of the plan to accelerate the production of RE as a fifth fuel source. The primary objective of SREP is to expedite the deployment of grid-connected small RE power plants. Later, the RE target was updated in 2006 to 300 MW of grid-connected electricity on the Peninsular and 50 MW on Sabah by 2010.

However, events did not unfold as planned during the policy's execution. At the end of 2005, under the Eighth Malaysia Plan's Fifth Fuel Policy, only 12 MW of electricity produced from renewable energies was supplied to the national grid through two projects under the SREP. The clear disparity between policy and practice clearly illustrates the obstacles to a successful transition from conventional to RE expansion. Due to the unsatisfied target, the government recommended that the Fifth Fuel Policy be carried over into the 9th Malaysia Plan, which ran from 2006 to 2010. The government reiterated its commitment to promote and accelerate the growth of a more efficient energy sector in the region. MS1525, or Energy Efficiency of Commercial Buildings, is one of the suggested guidelines that emphasizes energy consumption in commercial buildings.

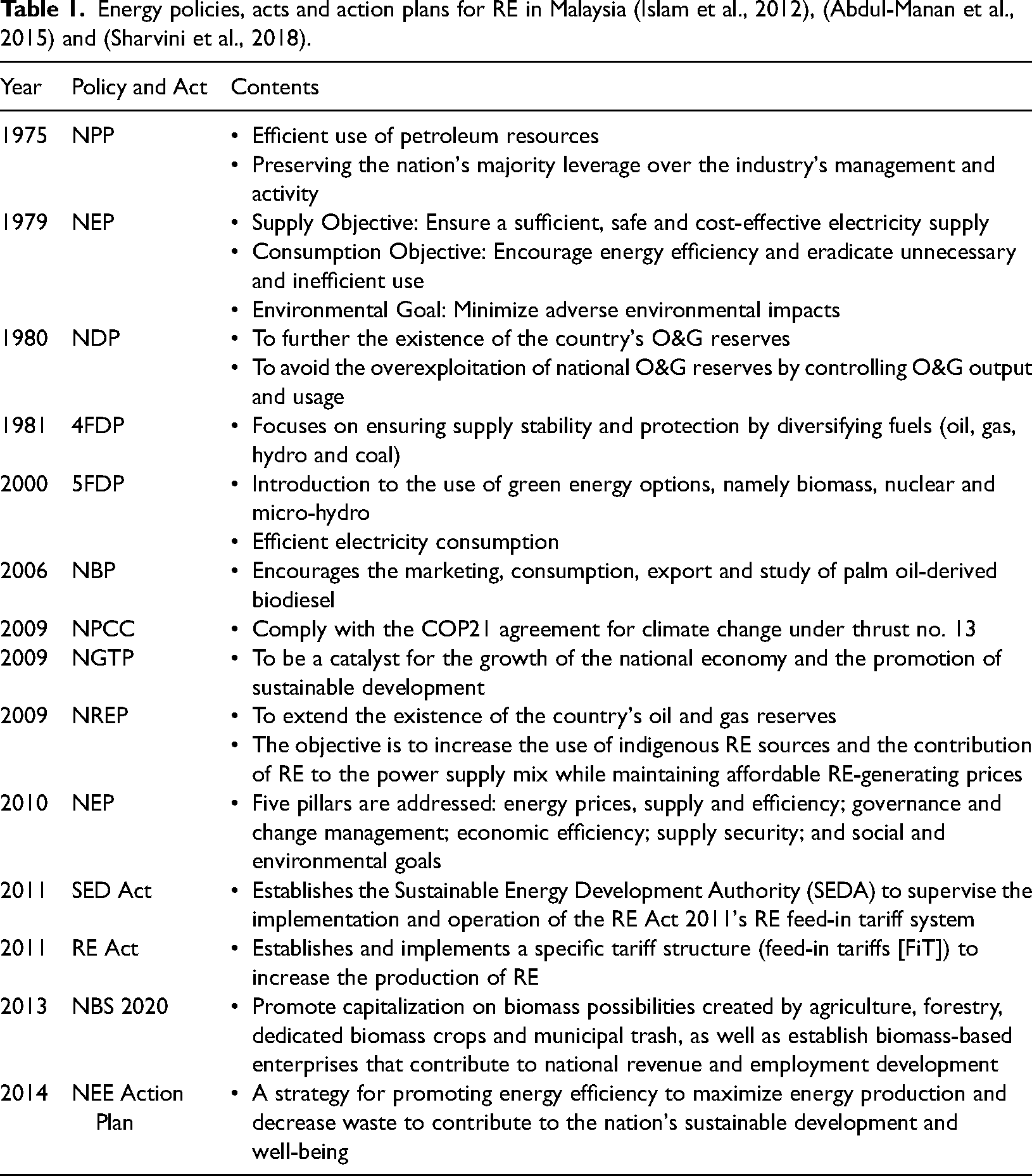

The Malaysian government initiated the National RE Policy and Action Plan (NREPAP) in 2009 with the primary goal of increasing the use of indigenous RE resources to ensure energy stability while also contributing to sustainable socio-economic growth (Hannan et al., 2018). This policy was strengthened further with the passage of the RE Act 2011, which includes provisions for the introduction of the feed-in-tariff (FiT) mechanism, the establishment of a RE fund and the establishment of the Sustainable Energy Development Authority (SEDA) to carry out the policy (Tang, 2015). Table 1 lists the mentioned policies, acts and action plans in detail.

Energy policies, acts and action plans for RE in Malaysia (Islam et al., 2012), (Abdul-Manan et al., 2015) and (Sharvini et al., 2018).

National petroleum policy

Petroliam National Berhad was the industry's first significant policy. The Third Malaysian Plan (1976–1980) was initiated in 1976 with the overarching theme of balancing growth and environmental protection (Oh et al., 2018). Within this framework, suitable steps were taken to guarantee that the energy sector develops at a rate sufficient to fulfill predicted industrial, commercial and home consumption requirements (Kardooni et al., 2018). In 1975, the National Petroleum Policy was developed to control the O&G sectors’ needs in the interest of economic growth (Bujang et al., 2016).

National depletion policy

In 1980, Malaysia enacted the National Depletion Policy to preserve and conserve the country's energy resources, especially petroleum and natural gas (Jalal and Bodger, 2009). The total annual crude oil supply must not exceed 3% of the oil initially in operation under this scheme. This condition effectively reduced the crude oil supply to 650 thousand barrels per day. The strategy was also applied to natural gas output, placing a daily limit of 2000 million standard cubic feet (Mscf) in Peninsular Malaysia (Hashim and Ho, 2011).

Fuel diversification policy

Malaysia implemented the 4-Fuel diversification policy (FDP) to diversify its energy mix. The policy's objective was to reduce the economy's reliance on oil as the primary source of electricity for power production (Hannan et al., 2018). However, the framework of this program was extended in 2001 with the introduction of the 5FDP Strategy, which included RE sources as a fifth fuel source. In support of the 5FDP Agenda, the National Biofuel Policy was initiated in 2006 and the NREPAP was launched in 2010 as part of the policy process for advancing indigenous RE production and increasing its addition to the power generation mix (Bujang et al., 2016). The NREPAP establishes long-term objectives and a holistic strategy for the strategic production of RE power capacity, which is estimated to reach 2080 MW (11 GWh) by 2020, accounting for 7.8% of the overall electricity generation.

National Green Technology Policy

The National green technology policy (NGTP) was initiated in 2009 as a first step towards promoting the economy's sustainable growth. The NGTP describes green technology as the primary engine of economic growth and sustainable development in the country. The NGTP's objectives are to foster the growth of the green technology industry and increase its contribution to the national economy, to strengthen Malaysia's capabilities and potential for creativity and to boost Malaysia's global competitiveness to protect the environment and ensure sustainable development for future generations. The strategy is based on four pillars. The first pillar emphasizes energy to ensure its independence and foster sustainable usage. The second pillar prioritizes the environment, with the target of saving and minimizing adverse effects on the environment. The third pillar focuses on the economy, with the target of accelerating the country's economic growth through the use of technology. The fourth pillar highlights society with the target of ensuring a high standard of living for everyone (Chien Bong et al., 2017).

National RE and action plan

Malaysia has stepped up efforts to promote sustainable energy production since 2001, embracing the market-based approach to achieving desired outcomes for electricity generation. The preceding 8 years (until 2009) had taught Malaysia valuable lessons about the pitfalls of such an approach, the most important of which was that a ‘business-as-usual’ approach is viable, acceptable, nor profitable. Renewable energy policy must be understood to be a synthesis of energy, manufacturing and environmental policies. The rationale behind implementing a new comprehensive and future-oriented green energy policy is to address the systemic issues related to RE, establish long-term resilience by avoiding inconsistent strategies, guarantee satisfactory results and the involvement of all parties involved, create a new thriving industry in Malaysia and recognize that the environment plays a significant role in economic growth and can be utilized to stimulate innovation. In the initial NREPAP, which was released in 2010, the government set a target of RE production reaching 10% of total generation capacity by 2020 and 13% by 2030. The government has since increased the commitment to 20% of the overall installed capability by 2025.

Malaysia plan: a five-year development program

The Malaysia Plan is a five-year growth strategy that complements the long-term (20-year) strategy. The First Malaysia Plan started in 1966, while the Eleventh Malaysia Plan replaced it in 2016. The government initiated the Eleventh Malaysia Plan 2016–2020 in May 2015 as the final step in realizing Vision 2020, a long-term growth plan launched in 1991 that envisioned Malaysia as a fully integrated economy across all dimensions by 2020. The Eleventh Malaysia Plan contains six tactics. They include promoting green development for mitigation and resilience, as well as strengthening infrastructure to facilitate economic growth, all of which have ramifications for energy initiatives. The Eleventh Malaysia Plan emphasized the importance of addressing climate change issues by establishing a blueprint for resilient economic development that incorporates adaptation and mitigation strategies. To help the economy minimize its carbon footprint, growth efforts focus on green markets, increasing the share of RE in the energy mix, improving demand-side management (DSM), promoting low-carbon mobility and holistic waste management.

Climate change policy

Malaysia is a signatory and has ratified the UNFCCC. Thereafter, in 1995, the National Climate Committee was created, comprised of representatives from government bodies and business and civil society organizations. It aims to lead climate change mitigation and adaptation efforts. Malaysia vowed at the 2015 United Nations Climate Change Conference in Paris to cut the GHG emission rate of its GDP by 45% by 2030, compared to the GDP's emission intensity in 2005. The 45% included a mandatory 35% and a discretionary 10% contingent on receiving climate capital, technology transfer and capacity building from developing economies.

Energy efficiency policy

Malaysia's only energy conservation (ENCON) agenda is contained in the National Energy Policy, specifically under the following utilization objective: to encourage energy production and prevent unsustainable and inefficient energy use habits. The government finally enacted the National Energy Efficiency Action Plan for the period 2016–2025, which places a greater emphasis on energy efficiency. To develop a comprehensive energy efficiency strategy, the DSM initiated and completed a preliminary study in July 2017 with the intention of developing a policy and action plan covering the entire energy market, including electrical, thermal and transportation.

Energy consumption in Malaysia

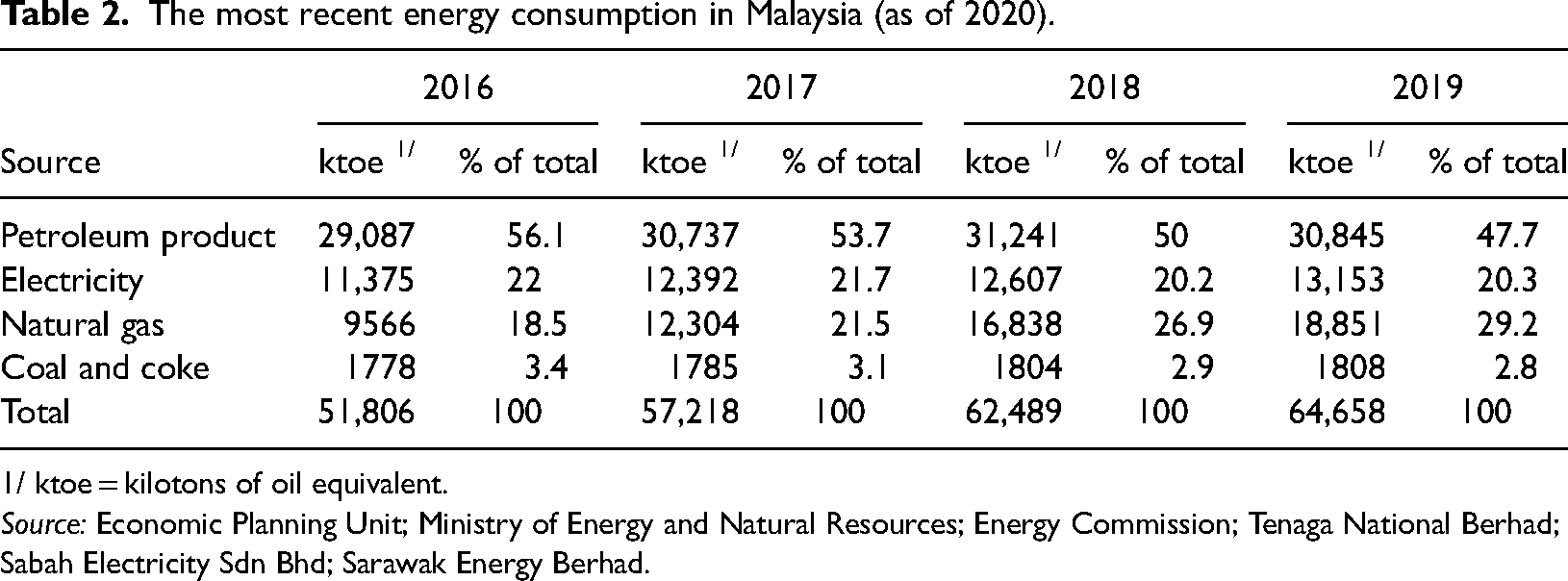

The energy consumption in Malaysia is documented in Table 2, encompassing data up until the end of 2019, which is the most recent report for Malaysia. Petroleum products continued to be the main source of energy in recent years (2019), coming in at 47.7%, with electricity and natural gas coming in at 20.3% and 29.2%, respectively (Planning, 2020). Thus, there has been a significant rise in the demand for energy in Malaysia, with substantial annual growth.

The most recent energy consumption in Malaysia (as of 2020).

1/ ktoe = kilotons of oil equivalent.

Source: Economic Planning Unit; Ministry of Energy and Natural Resources; Energy Commission; Tenaga National Berhad; Sabah Electricity Sdn Bhd; Sarawak Energy Berhad.

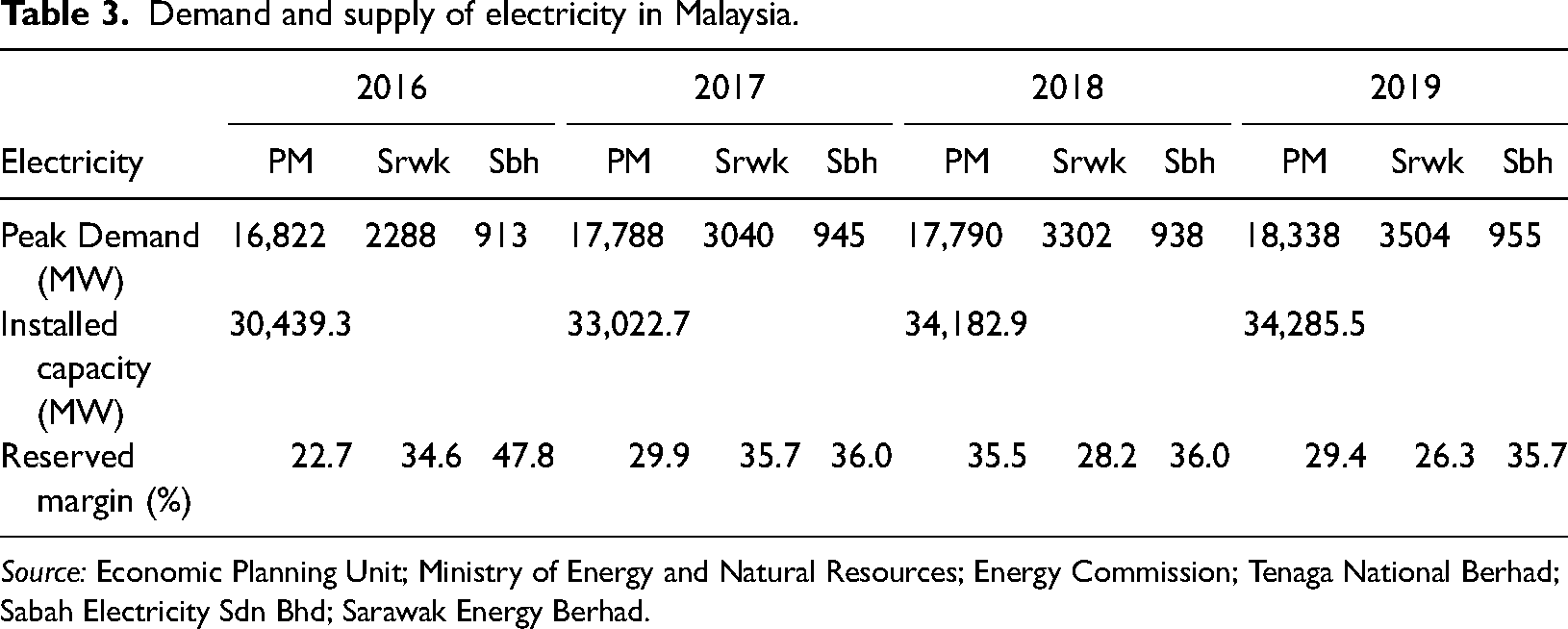

Table 3 presents specific information regarding the electricity demand and supply in Malaysia, covering the period from 2016 to the most recent data available in 2019 (Unit, 2020). An annual increase in demand was observed; however, the installed capacity surpassed the demand. Therefore, there is room to be set for reserved margins. It can be concluded that the energy demand in Malaysia is high and increasing annually. Consequently, the dependence on oil, gas and coal, which are finite and deplete rapidly, must be replaced with greener and more renewable resources.

Demand and supply of electricity in Malaysia.

Source: Economic Planning Unit; Ministry of Energy and Natural Resources; Energy Commission; Tenaga National Berhad; Sabah Electricity Sdn Bhd; Sarawak Energy Berhad.

Renewable energy in Malaysia

Malaysia emphasized the value of RE in its Tenth Malaysia Plan (2010–2015), which put a premium on adopting GHG mitigation steps. As of 1 May 2020, the gross installed capacity (excluding hydropower with a capacity greater than 30 MW and comprising only Peninsular Malaysia and Sabah) that achieved commercial service was 532.3 MW, comprised of 87.9 MW of biomass, 56.2 MW of biogas, 30.3 MW of small hydro and 357.9 MW of solar photovoltaic (PV; SEDA, 2021).

Biomass

Malaysia is the world's second-largest producer of palm oil, with 5.6 million hectares under cultivation (Malaysia Palm Oil Board (MPOB), 2016; Ng et al., 2012). As a result of these operations, Malaysia generates a large amount of biomass waste (Hansen and Nygaard, 2014). Malaysia was predicted to create 100 million dry tons of solid biomass in 2020, with approximately 91% of this biomass being wasted after processing (Mun, 2012). Apart from palm biomass, paddy, rubber and sago biomass had potentially been integrated into the value chain (How et al., 2019). FGV Holdings Berhad's largest RE power generator is a 2.4 MW biogas power plant located at its Triang palm oil mill in Bera, Pahang (The Star, 2020; Salleh et al., 2020). FGV secures a quota for 2.0 MW of export energy to Tenaga National Berhad's (TNB) national grid by SEDA Malaysia to provide electricity to 15,000 homes in Felda Triang, Felda Sebertak, Felda Purun, Felda Bukit Kepayang and Felda Tementi, all of which are situated within a 30-kilometer radius of the biogas power plant (SEDA Vol4Issue10, 2020; Ridzuan et al., 2020).

Biogas

Biogas is frequently produced in Malaysia under anaerobic conditions at waste treatment facilities. Municipal landfills, anaerobic ponds for Palm Oil Mill Effluent (POME), industrial anaerobic ponds and agricultural anaerobic ponds are the primary suppliers (Chin et al., 2013). According to a study on the potential for the CDM in the waste sector, the largest potential exists when anaerobic degradation occurs within municipal landfills and POME ponds (Ashnani et al., 2014). Malaysia and Indonesia account for 85% of global palm oil production (Dey et al., 2021). Interestingly, the advantages and competitive fuel qualities of palm oil biodiesel are comparable to those of petroleum diesel. Thus, palm oil biodiesel has established itself as a highly promising and conveniently available form of sustainable energy (Bazmi et al., 2011; Toklu, 2017).

Mini-Hydro

Malaysia has a total land area of 330,000 km2, of which 42% consists of highlands. The country is blessed with an abundance of streams and rivers coming from highland areas, providing potential sites for various hydropower projects (Yah et al., 2017). In 2009, 12 large-scale hydropower facilities and 50 small-scale hydropower units were operational. Malaysia has a total hydroelectric capacity of approximately 18,500 MW. In July 2009, a total of 30.3 MW of mini-hydro was under construction, with a projected capacity of 490 MW by 2020 (Ahmad et al., 2011). Apart from mini-hydro, micro-hydro with capacities ranging from 5 kW to 100 kW has significant potential for energy generation in Malaysia but is currently underutilized (Hossain et al., 2018). In Malaysia, hydrokinetic turbine technology is still in its infancy and has not yet reached commercialization (Behrouzi et al., 2016).

Solar

Due to its advantageous location near the equator, Malaysia has one of the highest solar absorption potentials in the world. Every month, Malaysia receives between 400 and 600 MJ/m2 of solar radiation. Solar irradiation is at its peak during the North-East monsoon, which occurs between November and March and occurs when the wind direction changes from central Asia to the South China Sea to Malaysia and then to Australia. There is an irradiation reduction between May and September as the wind direction shifts and flows from Australia to Sumatera Island, finally reaching the Straits of Malacca. Due to its year-round hot and sunny climate, Malaysia has a huge potential for solar energy generation. Solar power generation capacity could reach 6500 MW. Therefore, both large-scale and rooftop solar panels are viable solar deployment options in Malaysia.

New future, hydrogen

Sustainable Energy Development Authority Malaysia has offered to host a webinar on the subject of Shaping the Future of the Green Hydrogen Economy on 23 July 2020. Hydrogen started to receive attention from the government as a new potential of RE in Malaysia (Mah et al., 2019). With regards to the long-term approach, SEDA is nearing completion of the RE Transition Roadmap (RETR) 2035. Malaysia has built a roadmap for a green hydrogen economy by 2025 (Ahmad et al., 2021). The Green Hydrogen initiative should be carried out by 2035 in conjunction with the other RE policies and action plans described in the roadmap (Ahmad et al., 2021; SEDA, 2020). Under this source approach, fuel cell systems are the most promising and resilient RE technology for satisfying Malaysian consumers’ energy demand and security for the long term (Zakaria et al., 2021; Baharuddin et al., 2021).

Bintawa, in Kuching, Sarawak, is home to Southeast Asia's first hydrogen processing facility (SEDC, 2019). Sarawak Energy Berhad, a fully integrated facility, is developing and operating in partnership with Linde Fox Sdn Bhd, a subsidiary of the Linde Fox Group, a world pioneer in renewable hydrogen solutions. The Integrated Hydrogen Production and Refueling Station supports the state government's goal of establishing an emission-free transportation infrastructure. Earlier in 2021, the state of Sarawak conducted the world's first hydrogen bus trial in Kuching, the state capital (Antunes et al., 2003).

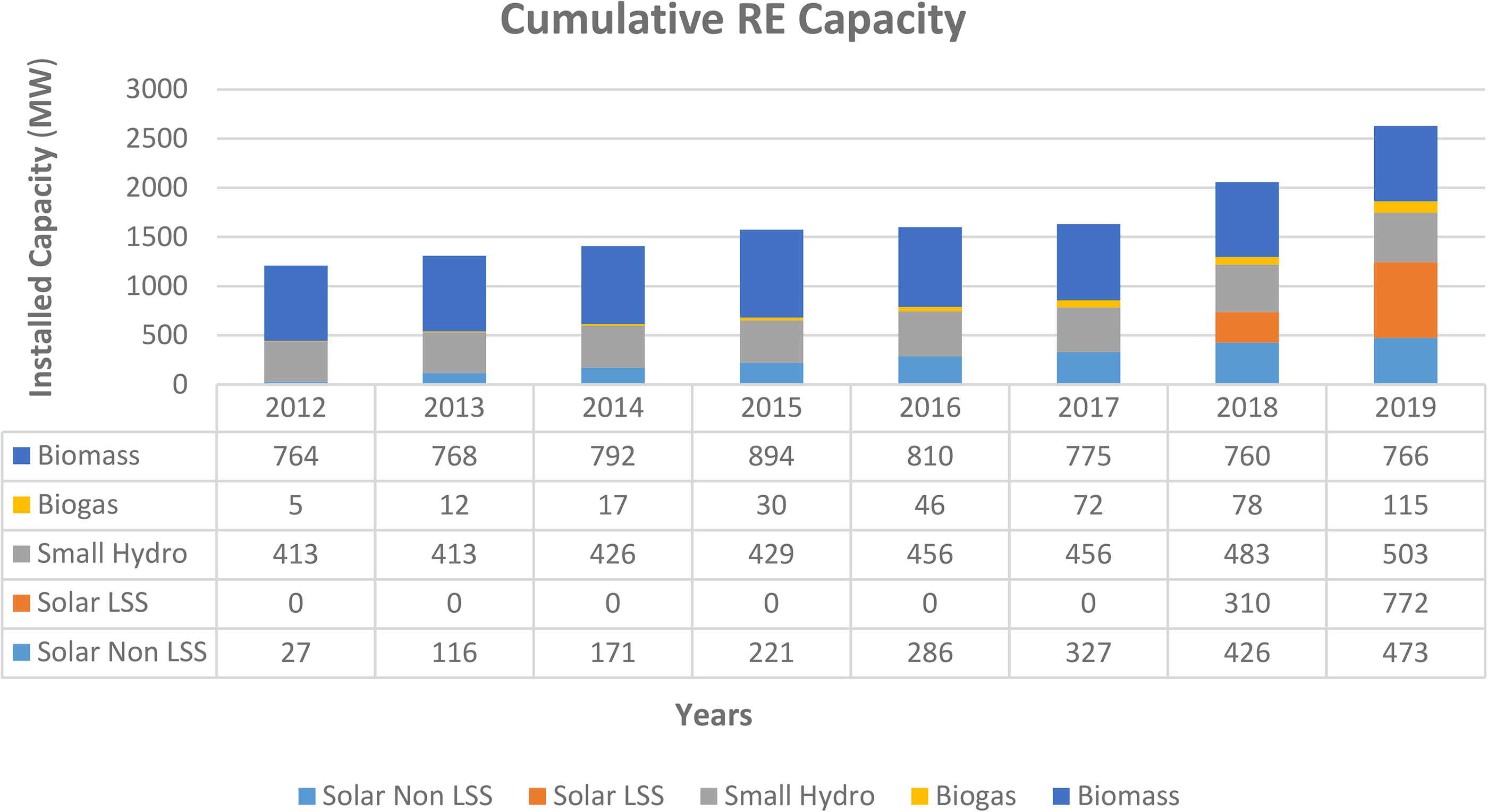

Figure 5 shows the cumulative RE capacity in Malaysia since the RE Policy and RE Act commenced. The data is presented in MW for installed capacity. The data source is from the 12th Malaysia Kick-off Conference on 2 July 2020 (Velautham and Officer, 2019).

Cumulative RE capacity.

Program for RE

Small RE Program

The SREP, implemented in 2001, permitted RE producers (REPPs) with a generation capacity of less than 10 MW to export electricity to the service provider via the distribution grid system. Biogas, biomass, small hydro and solid waste were particularly popular RE technologies under this initiative. Energy rates would be negotiated between REPPs and the applicable distribution licensee (DL), with payments made on a ‘take-and-pay’ basis. By 2009, this program had connected 53 MW of RE-producing capacity to the power grid. This statistic accounted for 0.2% of Peninsular Malaysia's total installed capacity of 21,817 MW in the same year. In 2013, post-harvest palm oil wastes, such as empty fruit bunches, fronds and trunks, fibre and palm kernels, were used directly as fuel for mill boilers. A total of 25 of the 63 projects approved under the SREP program are generators of trash derived from palm oil (Gomesh et al., 2013).

Feed-In-Tariff

Consumers may apply for a license to produce electricity from RE and sell it to the utility under the FiT program (Gomesh et al., 2013). Though this approach involves biogas, biomass and small hydro, the most realistic option for individuals and businesses is solar PV because it is the most easily accepted (Wong et al., 2015). Thus far, the overall installed capacity of solar PV projects eligible for the FiT is 310.45 MW (SEDA, 2020). The FiT program has progressed over time to ensure a favourable environment for industries, such as the switch from fixed prices to electronic bidding (Muhammad-Sukki et al., 2014). Through 2020, SEDA has conducted three successful biogas e-biddings, two small independent hydro e-biddings and biomass e-biddings in the future (Malik and Ayop, 2020).

NEM

Following the expiration of the solar PV quota under the FiT plan, the government advocated net energy metering (NEM) as a feasible remedy for the expanding sector. Under the NEM 1.0 plan (2016–2018), it was based on current displaced costs, which are much lower than the regulated power retail tariff. The take-up rate amongst electricity consumers has been extremely low, with only 27.8 MW approved as of the end of 2018. Following a review of the NEM 1.0 in 2019, the mechanism was improved to a ‘one-to-one’ energy offset mechanism, which indicates that each 1 kWh of energy generated can be used to offset 1 kWh of energy consumed. Between 2019 and 2020, there was a massive absorption of the NEM quota on authorized NEM applications. Numerous initiatives spearheaded by SEDA Malaysia to promote NEM 2.0 have resulted in the 2020 quota being filled well ahead of schedule 47.

As with FiT, NEM enables private individuals and organizations to produce electricity by using solar PV panels. This time, however, rather than selling the energy to the utility, NEM licensees use it and then sell any surplus to the grid (Hughes, 2017).

The NEM 2.0 reserve distribution is 500 MW until 2020. This quota distribution is split into two categories: domestic and non-domestic. The NEM is divided into four categories: residential, commercial, industrial and agricultural. The NEM 2.0 scheme is only available in Peninsular Malaysia, and applicants must be licensed customers of TNB. The solar PV sector is also a beneficiary of the government's Economic Stimulus Package, which included the award of 1400 MW of solar PV. Of the 1400 MW, 400 MW will be used for rooftop installations under the NEM, while 1000 MW will be used for the Malaysian EC. Notably, 300 MW is reserved for TNB's users in the home, commercial, industrial and agricultural sectors, while 100 MW is reserved for government buildings.

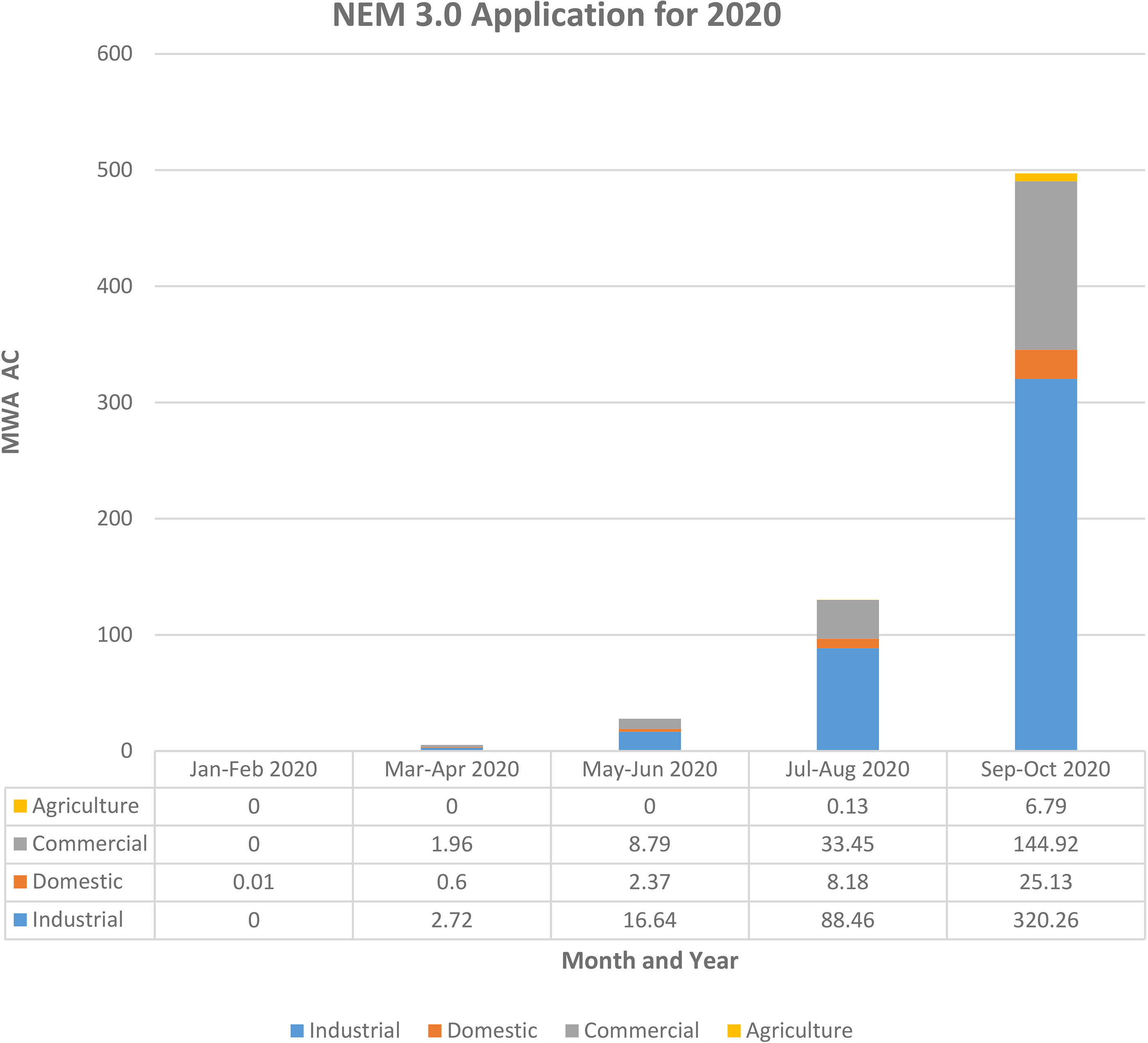

By the time, it was due to expire in late 2020, the NEM 2.0 cap had been fully utilized. NEM has entered the third phase in 2021. Since the application was announced, the number of applications has increased by months. Figure 6 shows the trend of application for NEM 3.0. Once the quota is reached, the program is terminated, similar to the former NEM program.

NEM 3.0 application for 2020.

Green technology scheme

Green technology financial scheme

The Green Technology Financing Scheme (GTFS) was founded in 2010 with a government fund of MYR 3.5 billion (USD 813 million) to promote the growth of the green technology industry until 2017 (Elias and Lin, 2015). The fund aims to provide a special funding mechanism for soft loans to businesses that manufacture and use green technology (Goh et al., 2014).

MyHIJAU labelling program

The launch of the MyHIJAU Labelling Program aims to ensure the supply of environmentally friendly goods and services in accordance with international requirements and regulations. Currently, Malaysia has three primary agencies that provide environmentally friendly certification programs: SIRIM Eco-Labelling by SIRIM Berhad for certifying the environmental impacts of green products and services; Energy Efficiency Labelling by the EC for labelling domestic electrical appliances’ energy efficiency; and Water-efficient Product Labelling by the EC (Mohd Suki and Mohd Suki, 2019).

Green Building Index

The Green Building Index (GBI) was created as a ranking system to encourage the use of green technologies in the construction industry (Dwaikat and Ali, 2018). In addition, it aims to increase developer and building owner understanding of the importance of green and sustainable building design and development (Azis, 2021). A GBI credential is awarded to architects and building owners who satisfy six standards: ENCON, indoor environmental sustainability, efficient site design and management, material and resource management, water efficiency and creativity (Mohamad Bohari et al., 2015).

Green procurement program

Malaysia developed the Government Green Procurement (GGP) program to accomplish this. The GGP incorporates environmental issues into the public sector procurement process to safeguard the natural environment, save energy and mitigate the negative consequences of human activity (Bohari et al., 2017). By 2020, the GGP will be introduced in all government departments, requiring the public sector to buy green-labelled goods and services at a rate of 20%.

Green Technology Master Plan

To further advance green growth, as reported in the Eleventh Malaysia Plan, KeTTHA launched the Green Technology Master Plan (GTMP) in 2017 to promote green growth as one of the six game-changers reshaping the economy's growth trajectory. The GTMP establishes a structure for mainstreaming green technologies into proposed projects, thereby incorporating the NGTP's four pillars. Six priority sectors have been listed in this master plan: energy, manufacturing, transportation, construction, waste and water.

‘Biogen full-scale model’ demonstration project

The Biogen FSM project, which began in 2002, sought to help facilitate the development of RE projects via biomass and biogas grid-connected power production plants. It was a collaboration between the Malaysian government and the United Nations Development Program's Global Environmental Facility. Notwithstanding such enthusiasm, only two FSM projects were commissioned as of 2010: a 13 MW biomass power plant using EFB as a fuel source managed by MHES Asia and a 500 kW biogas power plant using POME as a fuel source managed by FELDA. Financial difficulties erupted once again with the Biogen FSM project. Many previously interested parties withdrew from the selection process due to a lack of acceptable returns on investment. MHES Asia also had various financial difficulties throughout the implementation phase, particularly delays in receiving loan approvals from local financial institutions. The focus should be greater on developing a complete financial structure for RE projects.

Agencies

Sustainable Energy Development Authority

The Ministry of Energy mandated SEDA Malaysia to create an RETR in March 2018. Sustainable Energy Development Authority Malaysia initiated this study in 2019 to develop an RETR up to the year 2035. Sustainable Energy Development Authority Malaysia engaged in the Second Malaysia Energy Roundtable on 18 August 2020, as part of the World Economic Forum's ASEAN Energy Program, to discuss the goals for Malaysia's energy transformation, including the high-level concepts guiding Malaysia's National Energy Policy.

Petroliam National Berhad

Petroleum National Berhad was subject to the Companies Act 1965, starting on 17 August 1974. It is fully owned by the Government of Malaysia, which is entrusted with complete possession and management of Malaysia's petroleum resources under the 1974 Petroleum Development Act. Being Malaysia's national oil and gas company, it is accountable for petroleum product production, growth, refining, marketing and distribution.

Tenaga National Berhad

Tenaga National Berhad is Peninsular Malaysia's national electricity corporation, established in 1990 and tasked with the responsibility of electricity production, transmission and distribution in Peninsular Malaysia (TNB, 2020). In East Malaysia, the power utilities are the Sabah Electricity Board and Sarawak Electricity Supply Corporation. In addition to these primary facilities, a number of independent power producers (IPPs), dependable power producers and co-generators generate electricity. Peninsular Malaysia currently has a combined installed generation capability of 17,623 MW, with TNB owning 8417 MW (47.8%), IPPs owning 6787 MW (38.5%) and TNB and Malakoff collectively owning another 2419 MW (13.7%).

Malaysia EC

The Malaysia EC was formed as a new regulator for Malaysia's energy industry under the Malaysian EC Act 2001. This legislation was enacted to address the growing need for regulation in the energy sector. EC was also empowered in January 2002 to control, enforce and encourage all matters relating to the electricity and gas supply industries within the framework of the Electricity Supply Act 1990, the Gas Supply Act 1993, the Electricity Supply Regulations 1994, the Gas Supply Regulations 1997 and the Licensee Supply Regulations 1990. Previously, the Department of Electricity and Gas Supply was responsible for these tasks.

Ministry of energy, green technology and water (currently Ministry of Science, Technology and Innovation)

The Ministry of Energy, Green Technology and Water, or Kementerian Tenaga, Teknologi Hijau, dan Air (KeTTHA), was developed on 9 April 2009, to replace the Ministry of Energy, Water and Communications (MEWC), which had operated since 2004. Prior to MEWC, the Ministry of Energy, Communications and Multimedia (since 1998) and the Ministry of Energy, Telecommunications and Post (since 1978) were its predecessors. The KeTTHA is charged with the responsibility of administering and managing the nation's resources, green technologies and water functions. Following the 14th general election (PRU-14), the entire component of the Ministry of Science, Technology and Innovation (MOSTI), Green Technology and Energy Components from the Ministry of Energy, Green Technology and Water (KeTTHA), and associated systems of climate change and environment from the Ministry of Natural Resources and Environment was restructured to form the Ministry of Energy, Science, Technology, Environment and Climate Change (MESTECC). The MESTECC was subsequently restructured and renamed the MOSTI in 2020, following the creation of the New Government Cabinet on 9 March 2020 (MOSTI, 2020).

Malaysia energy centre

The Malaysian government founded the Malaysia Energy Centre, or Pusat Tenaga Malaysia (PTM), in 1997 to develop and coordinate energy research. The PTM's mission is to act as a hub and catalyst for collaboration between universities, research institutions, industry and national and international energy organizations. It performs four primary functions: (i) energy policy analysis; (ii) guardian and repository of the national energy database; (iii) promoter of national energy efficiency and RE programs; and (iv) coordinator and lead manager of energy research, growth and demonstration projects.

Centre for Environment, Technology and Development Malaysia

The Centre for Environment, Technology and Development Malaysia (CETDEM) was established in 1985 as an independent, charitable organization dedicated to training, research, consulting, referral and development. It is dedicated to enhancing environmental sustainability through the prudent application of technology and the promotion of sustainable growth. The CETDEM is currently the only independent Malaysian non-governmental organization (NGO) that is actively involved in addressing a range of environmental issues, including (i) the effects of long-term climate change on Malaysian society, (ii) sustainable energy, (iii) sustainable transportation, (iv) organic farming (sustainable agriculture) and (v) sustainable growth.

Achievements

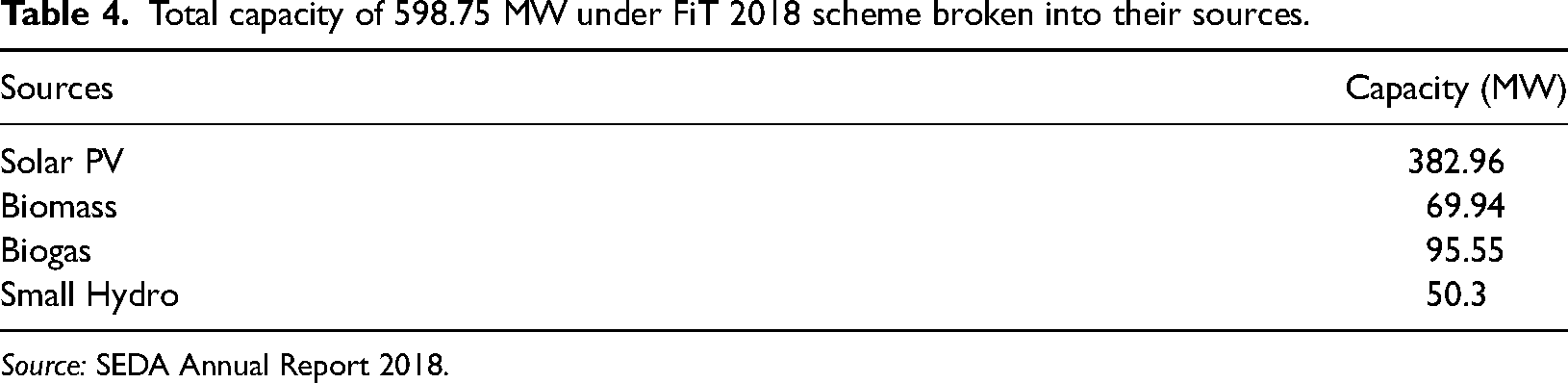

As of January 2021, Malaysia currently has a total installed capacity of approximately 34 GW of overall RE. Only 598.75 MW of installed renewable generating capacity was available under the FiT program in 2018, with the breakdown into solar PV, biomass, biogas and small hydro as reported in Table 4. Malaysia has established several initiatives aimed at maximizing the country's RE potential (LinklaterAsia, 2021).

Total capacity of 598.75 MW under FiT 2018 scheme broken into their sources.

Source: SEDA Annual Report 2018.

Hydro

Malaysia has a hydropower potential of 29,000 MW, with 85% of the six prospective sites concentrated in East Malaysia. Malaysia has mostly exploited its hydropower potential through the building of big hydropower plants, with approximately 6128.1 MW constructed. Malaysia had an RE capacity of 7.3 GW in 2017, with hydropower accounting for 82% of the capacity (Yah et al., 2017). The Malaysian government has stated a target of increasing electricity generated by small hydroelectric schemes to 490 MW by 2020. Small hydropower development (in Malaysia, small hydropower refers to run-of-river schemes with a capacity of up to 30 MW) is consistent with the Eighth Malaysia Plan's SREP and the FiT system. The small hydropower installed capacity under the FiT program was roughly 50 MW in 2018, with plants under construction up to 2023 comprising approximately 296.59 MW, constituting the largest proportion of all renewables under the FiT program. TNB aims to reach 1700 MW of RE capacity by 2025 (Tang et al., 2019).

Solar

Malaysia's solar PV potential is projected to be 6500 MW. Solar has consistently outperformed other green technologies in Malaysia, and the government anticipates that solar farms will account for the majority of new RE sources. To achieve this objective, the government has pushed numerous rounds of public auctions for solar projects, resulting in approximately 383 MW of solar PV installed capacity under the FiT plan in 2018. Solar PV development and implementation in Malaysia may be less challenging than with other renewable technologies, owing to the consistent supply of solar energy, the maturity of solar technology in the market and the fact that Malaysia is the world's second-largest manufacturer of PV modules and third-largest producer of PV cells (Tenaga, 2021a).

Biomass and biogas

In 2018, biomass and biogas installed capacity under the FiT plan totalled approximately 145 MW. Malaysia is ideally positioned to encourage the use of biomass as an RE source due to its status as a major agricultural commodities producer in the Southeast Asian area. Biomass resources are abundant, particularly in the palm oil plantation business. The oil palm milling business can generate electricity using solid biomass, palm shells and fruit fibres (National Biomass Strategy, 2012).

Building

Malaysia has different building ratings that are associated with different scopes and methodologies. The performance-based evaluation, known as SEDA Malaysia's Voluntary Sustainable Low-Carbon Building Performance Assessment – GreenPASS Program, is based on actual energy consumption in buildings, providing an accurate representation of the emissions contributed to the environment (environmental impacts). As of June 2020, 158 facilities in Malaysia have been registered, and 113 have been graded using the SEDA Malaysia's Voluntary Sustainable Low-Carbon Building Performance Assessment – GreenPASS Program, which assigns diamond ratings to structures ranging from one to four. The total quantity of energy saved was 89,763,232.30 kWh, which equates to a decrease of 61,882.33 tons of carbon dioxide emissions (SEDA, 2020).

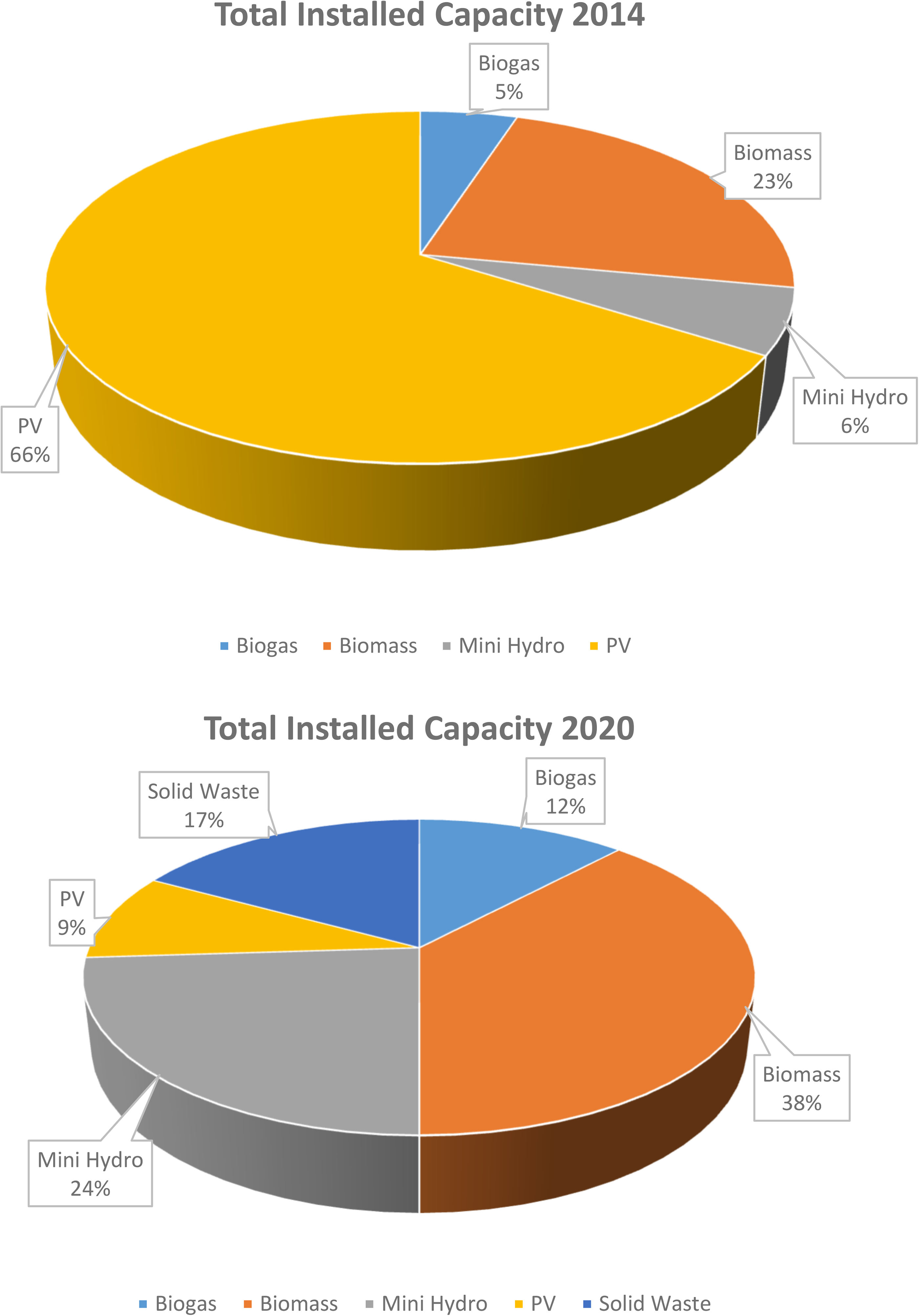

As of 2020, RE in Malaysia has successfully achieved several accomplishments. Figure 7 shows the total installed capacity of RE according to sources in 2014 and 2020. The increment was from 243 MW installed in 2014 to 2080 MW installed in 2020. PV accounted for 66% of the installed RE capacity in 2014. However, in 2020, the majority of installed RE would include biomass at 38%. Biomass has shown great potential as RE and has a bright future to expand.

Total installed capacity of RE, according to sources in 2014 and 2020.

According to the Malaysia Energy website, as of June 2021, 25 licensees have been awarded the license to commit to RE plant generation until 2034. The trend of increasing licensees to run the renewable plant is a good sign for the future of RE in Malaysi (Prestasi et al., 2018). Under the LSS project, the application and approval of projects also show an incredible number. The current license company provided 483.291 MWDC in total, whereas the LSS program provided 50 MWDC in Sabah as of 2018. Under the NEM program, 10.024025 MWDC capacity was licensed to 37 licensees to operate solar as RE in Peninsular Malaysia.

Government subsidies and tax exemptions

Feed-In-Tariff

Feed-in-tariff was established in 2011 as part of the RE Act with the goal of increasing RE output. The FiT system requires licensed enterprises to distribute power (DLs) to purchase at a predetermined FiT tariff from specific companies or individuals with a SEDA-issued feed-in permission certificate (fixed annually). For a specified period of time, the DLs will compensate for RE delivered to the electric grid (up to 21 years). To support this scheme, users who utilize more than a predetermined quantity of power are assessed a premium on their bills (300 kWh). The money is then utilized to recoup the cost of RE generated via the FiT method. This fee was increased from 1% to 1.6% in 2014, resulting in an additional MYR 325 million being added to the fund from the initial MYR 300 million (SEDA, 2021).

The FiT program applies to biogas, biomass, geothermal and small hydroelectric systems. The FiT program formerly applied to solar, but due to the high uptake of solar projects by developers, the EC is currently tendering solar projects under the large-scale solar plant. Costs have grown increasingly competitive as solar technology matures (e.g., solar PV panel prices have decreased 80% since 2009) (Chatri et al., 2018).

Green Technology Financing Scheme

The GTFS intends to increase the supply and use of green technology by providing financial assistance to producers of green technology. The initiative has been allotted MYR 2 billion until 2022 as part of the 2021 budget. As of this writing, no specifics on the current GTFS 3.0 scheme have been disclosed. Under the former GTFS 2.0, the fund was used to finance investment in green product manufacturing, green technology use and financing investments or assets associated with energy efficiency projects and/or energy performance contracts. The government covers 2% of overall interest costs (limited to the first 7 years) and guarantees 60% of the total debt financing through the Credit Guarantee Corporation Malaysia Berhad (with the remaining 40% of the total debt financing amount risk to be borne by participating financial institutions). The scheme applies to financing sums up to MYR 100 million for green technology producers (15-year tenure), MYR 50 million for green technology consumers (10-year tenure) and MYR 25 million for energy service enterprises (five-year tenure). Applicants must be amongst Malaysian-owned companies with a minimum ownership of 51%.

Tax incentives

Malaysian enterprises that are formed and engage in investing in or offering services related to green technology can seek green technology tax benefits by applying to the Malaysian Investment Development Authority. Depending on the type of green technology, such tax benefits may include the following:

Investment tax allowance

The Malaysian government provides incentives in the form of an investment tax allowance (ITA) for the acquisition of green technology and green technology assets. The ITAs provide a 100% deduction of qualifying capital expenditures incurred for 3 years from the date of the initial qualifying capital expenditure incurred against 70% of statutory income. The ITAs apply to the following:

Green Technology Projects (GTPs) Acquisition of Green Technology Assets (GTAs) Income Tax Exemption (ITE) for Green Technology Services (GTSs)

In addition, an ITE of 70% on statutory income is available for solar leasing activity for up to 10 years of assessment (depending on installed capacity), beginning on the date of the first invoice issued (Lau et al., 2020).

Comparison with other countries worldwide

The Indonesian government enacted a national energy policy in 2006. Many directives have been established for effective implementation. Indonesia has set an aim of achieving maximum RE consumption at the national level by 2025. The expansion of RE is aimed at reducing reliance on finite resources, such as oil, gas and coal. The reduction is predicted to be 20% for oil, 30% for gas and 33% for coal. Renewable energy sources, such as biofuel and geothermal, obtain a 5% gain in share, while biomass, hydropower, wind, solar and nuclear have a 5% increase in share. Moreover, liquid fuels have a 2% increase in share. At the national level, the energy policy aims to optimize the use of sustainable energy sources. Domestic energy consumption is anticipated to triple or increase by 15% in 2025, compared to 2005 levels.

The government of Brunei has developed an RE roadmap entitled ‘Brunei Vision in 2025’. Brunei Darussalam is committed to implementing sustainable energy initiatives that prioritize energy efficiency, energy security, supply diversity and ENCON. The Bruneian government proposes to diversify the energy mix by focusing on the development of RE sources for electricity generation. The government has also collaborated with NGOs, such as the Energy Efficiency Conservation Committee, the Brunei Energy Association and Brunei's National Energy Research Institute, on RE research. The policy encompasses land-based and marine RE. However, Brunei Darussalam's ocean-based RE sources are not fully utilized at the moment.

Myanmar has implemented a number of national-level energy policies aimed at preserving the country's energy reliance and increasing the usage of RE to satisfy residential household energy requirements. Myanmar has committed to assisting with ongoing development and environmental integration expenditures. The country's government established an Energy Development Committee and a National Energy Management Committee to oversee all operations related to the use and development of RE under one roof. In Myanmar, only 34% of residents have access to grid-quality power. Several organizations, including the Union of Myanmar Federation of Commerce and Industry Chamber and the Myanmar Engineering Society, are undertaking efforts connected to RE for rural power generation to ease the region's electricity crisis.

The Philippines’ RE plan established the Philippine Council for Industrial, Energy and Development as the research foundation. In 2014, the roadmap encompassed all research initiatives conducted by various institutes and academic personnel. In 2008, the Philippine government adopted a framework for RE, intended to expedite the development of state-owned RE sources; an RE management bureau was also formed to oversee implementation. This approach has worked on technological assessments of RE sources, such as wave and tidal energy, on a global scale. In 2011, the Philippine government adopted their ideas into a plan called the Green Energy Roadmap 2011. The NREP aimed to install 15,304 MW of RE capacity by 2011.

No explicit policy for RE development is available in Cambodia. However, the strategy aimed at increasing the use of RE at remote power plants is framed. In addition, the Cambodian government has implemented a more strategic policy for the electrical industry, encouraging the use of RE as a component of the region's energy mix. Rural areas are provided with a framework for planned RE development. Through the Renewable Electricity Action Plan, electricity is provided using reliable RE technology. In 2013, the Cambodian government devised and produced an RE plan for national strategy developers with a 2030 target. By 2030, 70% of all households in all villages must have access to grid electricity. The government has suggested a ‘strategic plan for green growth by 2030’, outlining a national road map.

The Laotian government, like many other nations, has formulated an extensive policy for the development of RE. However, the plans exclude ocean-based RE and instead aim to achieve a target of 30% RE and a 10% target for biofuel use. Laos has also developed a community electrification initiative to address the country's growing demand for electrical energy.

The Singaporean government set a target of a 16% reduction in GHG emissions by 2020 through a worldwide accord. Nonetheless, Singapore has considered various strategic and effective actions to achieve efficient RE, providing impetus for emissions reductions of between 7% and 11% at the BAU level by 2020. Although no policy on RE regulation has been formed at the national level, research institutes and academics continue to investigate and undertake research on the RE potential. Singapore is making great progress in terms of RE development. In 2013, the Singapore government met with representatives from several energy market authorities as part of a worldwide energy week focused on RE. Recently, signatories have come to an agreement on international cooperation with the energy research institute at Nanyang Technological University. Subsequently, the National Research Foundation published a call for competitive research grants to fund the Energy Innovation Research program, which is focused on the development of electrical energy systems using RE sources other than solar.

The proposed legislation by the Thai government is to promote ENCON through the implementation of renewable portfolio standards. The objective is to establish a goal of utilizing 3–5% of RE in all new power production capacity projects. Geothermal energy and electricity from the sea's tidal wave have been classified as RE sources by Alternative Energy Development Planning. The combined wave and tidal energy is expected to generate up to 2 MW of electricity. However, at present, it cannot be used to generate power. Since the transportation sector in Southeast Asia is the largest consumer of RE, biofuels have a greater demand-driven potential for urban transportation and long-term energy supply. The primary objective of the transportation policy is to boost the use of biofuel, despite the inclusion of electric vehicles and public transportation in the policy.

Challenges for RE in Malaysia

The five FDP implemented in 2000 did not have the desired effect of expanding the usage of RE. Even though Malaysia is endowed with a plethora of natural and renewable resources, ranging from solar to hydro and biomass, two decades have passed without any significant development. By the end of 2020, Malaysia had insufficiently diversified its energy base following the National Energy Policy's supply plan and remained primarily dependent on petroleum sources. Malaysia must immediately conduct a review of its present RE development processes to identify gaps and impediments to the execution of these projects.

The adoption of the NREPAP in 2009 has the potential to be a game-changer, particularly with the approval of the RE Act, which would permit the implementation of FiTs for RE. The FiT mechanism enables investors in RE to recuperate their investment expenses throughout the life of their contracts, but it falls short of assisting people and small businesses throughout the installation process. This phase is often the most expensive for commissioning new power facilities. If RE deployment accelerates and becomes more sustainable, then appropriate finance models must be created and implemented in the future.

Additional efforts should be made to build a ‘green financial framework’, which should include provisions for green bonds, green loans and green Sukuk, amongst other financing options. This approach will be critical in mitigating the significant budgetary difficulties of potential REPPs. Sustainable Energy Development Authority is uniquely qualified to aid in the creation of such a framework because it has a first-hand understanding of the challenges experienced by program participants. The KeTTHA should initiate dialogue with local financial institutions, private equity funds and angel investors to identify comprehensive solutions for bridging financing gaps in RE project development.

The performance targets set forth in the NREPAP to enhance the deployment of RE resources in Malaysia have not been fulfilled. This setback is significant, especially considering the demonstrated awareness of the actions required to increase the percentage of RE in Malaysia's electrical generating mix. Since SEDA's inception, key policy measures, including the FiT and net energy metering, have been successfully implemented in several nations worldwide. Nonetheless, they slightly impact the mix of energy production in Malaysia.

This inadequacy is partly attributable to the exact characteristics of these policies when implemented in Malaysia. Remarkable emphasis has been placed on safeguarding DLs’ market shares and profit rather than openly and unilaterally supporting the wider adoption of RE via these regulatory systems. An inordinate amount of attention has been provided to mitigating the disruptive effects of this progressive regulatory framework on DLs. For example, the enforcement of restrictions on RE-generating capacity under the FiT mechanism was always destined to constrain the RE industry's expansion, while the poor rates of return given to RE investors contributed significantly to the NEM scheme's failure to date. Tenaga National Berhad has benefited the most from these constraints, limiting the expansion of independently produced RE power. Several contract awards have been made using a biased or obscure procedure. Many examples of subordination have been provided towards special or entrenched interests throughout the FiT program. This finding is likely to have undermined the confidence of numerous potential investors in SEDA's RE policy. This challenge presents a significant threat to the adoption of solar energy on a large scale in Malaysia.

Sustainable Energy Development Authority and the EC have had open-ballot sessions for certain contract awards, which should become the rule for all future policy processes, starting with LSS. In addition, the NEM framework is restructured in a way that boosts the monetary incentives for individuals and energy suppliers to participate in the program and eliminates the need for expiring electricity credits, which has stifled interest in the scheme. Therefore, SEDA may need to stand up for itself, its beliefs and its objectives rather than being subordinate to KeTTHA, the EC and TNB. Simultaneously, attempts have been undertaken to expand into large-scale solar energy provision. However, it is essential to abandon previous patterns of behaviour. Undistinguished beginnings of large-scale solar occurred in March 2014 and January 2016, when KeTTHA announced contracts totalling 650 MW via direct negotiation, only to award a large contract to a single company. Thus, the benefits of open tenders are self-evident and must be enforced.

Two open-ballot events occurred in March 2016 and March 2017. The allocated installed capacity of 450 MW, which surpassed the initial 250 MW, began commercial operations in 2017. The second event garnered bids totalling 632 MW, out of which 562 MW were approved, surpassing the target of 460 MW. The commercial operations of this event commenced either in 2019 or 2020. By the end of 2020, a total of 1012 megawatts of LSS would be in operation. Hence, it is imperative to firmly adhere to project timelines in order to comply with the company that has been granted the contract, and these timelines should be closely monitored by the government.

In order to promote the growth of the industry, policies related to RE and green technology need to address a range of societal issues. The potential benefits of promoting understanding and adoption of sustainable technology in communities are significant. The primary cause of this discovery can be attributed to inadequate awareness initiatives, namely targeting individuals residing in rural areas (Yatim et al., 2016). Hence, it is imperative to evaluate and improve the effectiveness of existing public awareness initiatives, which are crucial for the advancement of renewable energies and green policies, in order to garner greater public support for sustainable development.

No adequate agenda has been found for sustainable development policies. These policies simply express the government's objectives and various approaches to green and sustainable technologies (Hossain et al., 2015). Another obstruction in Malaysia is the high import tariffs. The power sector's instruments are subject to import charges of up to 45% and a 10% sales tax. In addition, several instruments are subject to import licensing requirements.

In 2018, ASEAN conducted a peer-to-peer review of Malaysia's energy by experts from various ASEAN members. The committee of 13 members reviewed the country's energy policy and the steps taken for compliance. A full report of 78 pages with 41 recommendations was provided (Asia Pacific Energy Research Centre (APERC), 2018). Mr Takato Ojimi from APERC, Japan, led the panel of experts from various countries. The recommendations and feedback presented in this peer-to-peer review concerning Malaysia should be stressed and followed strictly to ensure the fulfillment of RE objectives in the country. Malaysia should rigorously oversee this review to verify the efficacy of its renewable plan. It was a privilege for Malaysia to have the effectiveness of the country's RE programs assessed by a specialized body.

Another obstacle is the absence of sophisticated technology for RE generation and a widespread lack of information regarding the advantages of RE. The Malaysian Centre for Education and Training in RE and Energy Efficiency should address these issues by enhancing the level of knowledge and awareness within the country's education system. Secondary school and university curricula should incorporate concepts from both RE and EE (energy efficiency). The main constraints facing RE generation include a lack of expertise in efficient processes and equipment operation, ineffective energy management and limited availability of technologies. Some technologies, considered undesirable, have inherent inconsistencies (Petinrin and Shaaban, 2015).

Overall, micro-hydro is the most efficient RE source in Malaysia, whereas wind energy has the lowest efficiency when it comes to research and development (R&D) activities. Nevertheless, the scope of R&D endeavours pertaining to small hydroelectric plants is restricted, and the generated capacity of installed systems is directly correlated with the level of investment in R&D in comparison to other RE sources. Wind energy is the least efficient RE resource since it requires substantial R&D investments compared to other sources, and it has the smallest amount of installed capacity (Mohd Chachuli et al., 2021).

Conclusion and policy implications

Conclusion

In conclusion, Malaysia's pursuit of sustainable energy strategies, climate change mitigation and economic growth underscores its evolving role on the global stage. As a developing nation, Malaysia has devoted significant efforts to shaping its energy landscape, employing diverse policy instruments ranging from fossil fuel management to the integration of RE sources.

This article thoroughly examines Malaysia's energy transformation, offering a comprehensive analysis of its historical, current and prospective developments. In contrast to earlier evaluations, the present inquiry illuminates the distinctive dynamics of operation. The findings of this study highlight the importance of the moment. Malaysia's past role as a country that exports more oil and gas than it imports has led to a situation where it depends more and more on fossil fuels for its economy, despite being protected against energy shocks from outside and within the country since the late 1980s. The untapped potential of several RE sources heightens this complexity.

Recommendation

The novel aspect of the present study is its capacity to reveal the complexities of Malaysia's energy transformation. Although the nation possesses ample resources, various factors have been examined to demonstrate why it continues to pursue the integration of fossil fuels. This study addresses a significant research gap by highlighting the obstacles and possibilities for the adoption of RE. The urgency of the shift becomes much more apparent in this environment.

Despite the implementation of the Five FDP for 20 years and the RE Policy for 10 years, there has been minimal advancement. The novelty of the present study lies in the researchers’ capacity to clearly identify the distinctive obstacles that Malaysia encounters in its pursuit of sustainable energy. Recognizing the significance of RE sources is crucial for Malaysia's energy future.

The convergence of economic, political, social and technical aspects emphasizes the increasing significance of sustainable energy in the future. The novelty of this study also arises from its capacity to offer precise recommendations and policy implications. The responsibility lies with the government to seize this opportunity and achieve a reduction of GHG emissions by up to 45% by 2030, ultimately attaining carbon neutrality by 2050.

This vision is fully in accordance with Sustainable Development Goal 7, as defined by the United Nations, emphasizing the importance of affordable and clean energy availability. This study emphasizes the need for a proactive approach in attaining these objectives and influencing Malaysia's position in the worldwide shift towards sustainable energy solutions.

In conclusion, this study represents pioneering research into the Malaysian energy landscape. This demonstrates the distinctive difficulties that the country encounters and offers a detailed plan for its long-term energy sustainability. The pressing nature of the findings requires a decisive reaction from policymakers, industry players and researchers. Malaysia's energy trajectory must be immediately redefined.

Footnotes

Acknowledgements

The authors acknowledge the Fundamental Research Grant Scheme (FRGS), grant No. FRGS/1/2021/TK0/UKM/01/5 funded by the Ministry of Higher Education (MOHE), Malaysia and Universiti Kebangsaan Malaysia for providing facilities and expertise that greatly assisted this research.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Fundamental Research Grant Scheme (FRGS), grant No. FRGS/1/2021/TK0/UKM/01/5 funded by the Ministry of Higher Education (MOHE), Malaysia.