Abstract

This study aims to analyse the causal link in the short-run and long-run between economic growth, renewable energy, non-renewable energy and public spending in eight countries of the South Mediterranean Countries group during the 1980–2020 periods. Four steps are used: augmented Dickey-Fuller and Phillip Perron unit root tests to check the order of stationarity of variables, bound tests to verify the presence of cointegration, autoregressive distributed lag approach to check the effects of the dependent variables on the independent variable in short run and long run and finally the vector error correction model was used to detect the causal relationships among variables. The results approve the presence of cointegration between variables which confirm the existence of the long-run relationship. In addition, the Granger causality results show varied outcomes and the short-run causal relationships (unidirectional and bidirectional) exist in both countries of South Mediterranean Countries. These results remind the awareness of the South Mediterranean Countries government to revise their energy policy given the cost of energy consumption for importing countries. For the oil-exporting countries (Algeria and Egypt), the international energy market is an unstable market and highly dependent on external factors such as supply and demand and the stability of the world countries. So, it is good that the economies of these countries rely on new sources of energy such as renewable energy.

Introduction

Since the industrial revolution, the world has known a considerable evolution in population numbers and a growing and continuous development of industry. These elements have led to an increase the production activity and to develop the means of transport. As result, the global energy demand has increased steadily over time and energy self-sufficiency has become a basic need for all states of the world. Overall, South Mediterranean Countries (SMCs) group are among the countries concerned to meet their basic energy needs at a time which they are experiencing rapid population growth and low incomes. The Mediterranean Agency of National Energy Management Agencies presents a scenario based on a greater consideration of energy-efficiency actions and a sustained development of renewable energies. It could, according to the SMCs; primary energy demand will increase by 7% between 2013 and 2040. The energy transition scenario still forecasts in 2040 an increase of 55% in energy consumption in SMCs. These scenarios have various consequences on the countries studied, including their energy dependency on other countries, economic instability, the increases of public energy consumption spending which generate budgetary imbalance and even environmental pollution. In the same context, the question of the use of new energy sources such as renewable energies has become a topical and frequent issue for most countries in the world. Renewable energy can provide financial gains for governments and an opportunity to conserve environmental cleanliness and minimizes the disadvantages of intensive use of non-renewable energy such as oil and coal. According to Al-Mohannadi et al. (2018), the emissions of natural gas consumption are less intensive than emissions resultant from CO2 from coal consumption. This result confirms that it is possible to reduce CO2 emissions by the gradual adoption of natural gas consumption. Jebli and Youssef (2015) investigate the relationships between economic growth, trade, CO2 emissions, and energy consumption (renewable and non-renewable) in Tunisia during 1980–2009. The results confirm that in short term, economic growth, trade, non-energy consumption, and CO2 emissions cause renewable energy consumption. However, in long-term trade and non-renewable energy affect positively CO2 emissions, while the increase of renewable energy decreases CO2 emissions. In addition, Ben-Salha et al. (2018) have proved that in the short run, bidirectional causality between renewable energy consumption and economic growth exists. Nevertheless, a unidirectional causality has been found between the variables in long run. Thorarinsdottir et al.’s (2017) study found that renewable energy has a positive influence on gross domestic product per capita of European Union (EU) – 28 countries during 2003–2014 period. They show that an increase of renewable energy produces by 1% begets an increase of gross domestic product per capita by 0.05%, 0.06%. However, in the short and long run, a unidirectional causal relationship exists precisely from growth domestic production (GPD) per capita to renewable energy products. In another study, Ghalayini Latife (2011) has demonstrated that the economic growth of oil importer countries decreases when the oil price increases, by contrast, the increases in oil price have a positive effect on the economic growth of oil exporter countries. The results of Granger causality show that there is a unidirectional relation from oil price to GDP in Organization of the Petroleum Exporting Countries countries in addition to Russia, China and India data and G-7 group data from the beginning of 1986 to 2010.

In 2016, Chen et al. (2016) have examined the relationships between CO2 emissions, economic growth and energy consumption for 188 countries during the 1993–2010 periods. The empirical results confirm the existence of relationships between the three variables and there is unidirectional causality from energy consumption to CO2 emissions in both countries. However, the authors have found that energy consumption affects negatively only the economic growth of developing countries. The same result was founded by Karanfil and Li (2015) in order to study the long-term and short-term dynamics between economic growth and electricity use in 160 countries.

Al-Darraji and Bakir (2020) meant to identify and assess the effect of renewable energy on economic growth by using panel data and the fully modified ordinary least squares econometric technical for 18 countries from 2008 to 2015 periods. The study shows that renewable energy has a positive impact on economic growth. However, Chen et al. (2020) check the causal relationship between renewable energy exploitation and economic growth via using a threshold model for 103 country samples during the 1995–2015 periods. The authors discover that the relationship between renewable energy consumption and economic growth was dependent on the quantity of renewable energy consumption. In addition, the results reveal that the consequence of renewable energy consumption on economic growth is positive only in the condition the development exceeds a certain threshold of renewable energy utilization. On the other hand, in the case when developing states employ renewable energy lowers than a certain threshold level, the effect of renewable energy consumption on economic growth will be negative. However, the results of the study also show that renewable energy consumption has no significant consequence on economic growth in developed countries, while this effect becomes positive and significant on economic growth in the Organization for Economic Co-operation and Development countries.

On the other side, Zhang et al. (2021) analyse the relationship between public expenditure on Research and Development (R&D), green economic growth and energy efficiency during 2008–2021. The study was based on panel data of Belt and Road Initiative member countries (BRI), using the Generalized Method of Moments (GMM) method and Data Envelopment Analysis (DEA) to identify the relationship between the three variables. The results of GMM technical confirm equally composition and system impacts in the whole model. However, the result of the sub-sample demonstrates the existence of heterogeneous impact on rich countries. In addition, the study demonstrates that public expenditure on human capital and R&D of renewable energy technologies gives rise to a sustainable green economy through employment and technology-oriented fabrication behaviour and diverse effects.

Based on data collected from 25 European countries, Ntanos et al. (2018) analyse the nature of the relationship between renewable energy sources consumption, non-renewable energy consumption sources, gross fixed capital, labour and economic growth during 2007–2016, using Autoregressive Distributed Lag (ARDL) approach. The study exposes that all variables are associated in the long term. In addition, the results of the estimations show the existence of a higher correlation between renewable energy consumption and economic growth in the richest countries than in less rich countries.

In 2018, Marinaş et al. (2018) have selected 10 EU countries from Central and Eastern Europe in order to test the correlation between economic growth and renewable energy consumption in the short and long term during the 1990–2014 periods by applicant ARDL approach. The results of the short term show that in Romania and Bulgaria case, the GDP and renewable energy consumption are independent. However, in Hungary, Lithuania and Slovenia case, renewable energy consumption represents an important factor for the increases in GDP. In addition, the bidirectional causality relationship between economic growth and renewable energy was verified in the long term in both countries.

Xie et al. (2020) try to calculate the green economic development level in the 27 EU governments. The analyses show that green economic development increases between 0.67 and 10.87 units when renewable energy consumption increases by one unite. Also, renewable energy consumption was positively affected by the development of new technologies. However, the improvement of presented technologies was unsuccessful to show a valuable impact on the relationship between renewable energy use and green economic development. Also, the phase of economic development force impacts the consequence of renewable energy on green economic progress.

In 2020, Venkatraja (2020) founds that the declining split of renewable energy to the total energy capacity has supplied the quick economic growth in BRIC (Brazil, Russia, India and China) region. It means that in BRIC states if the split of renewable energy to total energy augments, the economic growth will decrease.

According to the inference resulting from these studies, we can show that the preceding literature studying the cointegration and causal relationship between economic growths, public spending, renewable energy and non-renewable energy is not convincing to deliver policy approval that can be practical across states. This paper so aims at satisfying this lack and funding to the empirical literature. The objective of this study is to determine the four-way linkages between public spending, renewable energy consumption, non-renewable energy consumption and economic growth in eight countries of SMCs during 1980–2020. To the greatest of my information, there has never been an effort to examine this relation for this region. This research tries to fill this hole and gives empirical literature. We have chosen this area because of its importance throughout history. It is the meeting point of many civilizations and cultures, and it is a link between the two banks of the Mediterranean basin. It is also an important transit point for people and goods between the industrial north and the south, which is rich in natural resources. Also, some climate experts and researchers in economics history consider that this region has a role in the current climate change, as it is one of the most important regions in the world exporting oil and coal, and the main supplier of energy to European countries. We have excluded Libya and Syria from our sample due to lack of necessary data due to political and economic instability and also because of the lack of transparency and credibility of data.

However, we have to try to analyse this problem by using multi-step techniques and tests: tests of stationarity, cointegration tests, ARDL and vector error correction model (VECM). The ARDL bounds testing approach was used in order to examine the short-run and the long-run effects of exogenous variables on the endogenous variable. The rest of the paper is distributed as follows: The section ‘Materials and techniques’ defines data and empirical methodology for this study. The section ‘Unit root and Bounds tests results’ is consecrate to the empirical results and discussion. Finally, the section ‘Conclusion and Policy implication’ represents the conclusions with main results and policy implications.

Materials and techniques

Model specification

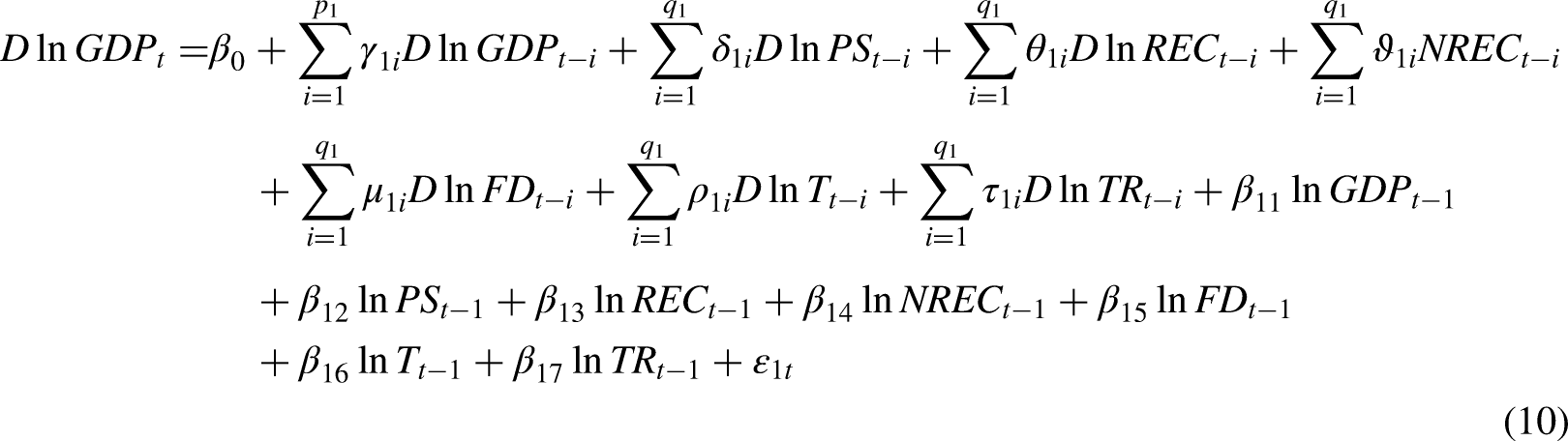

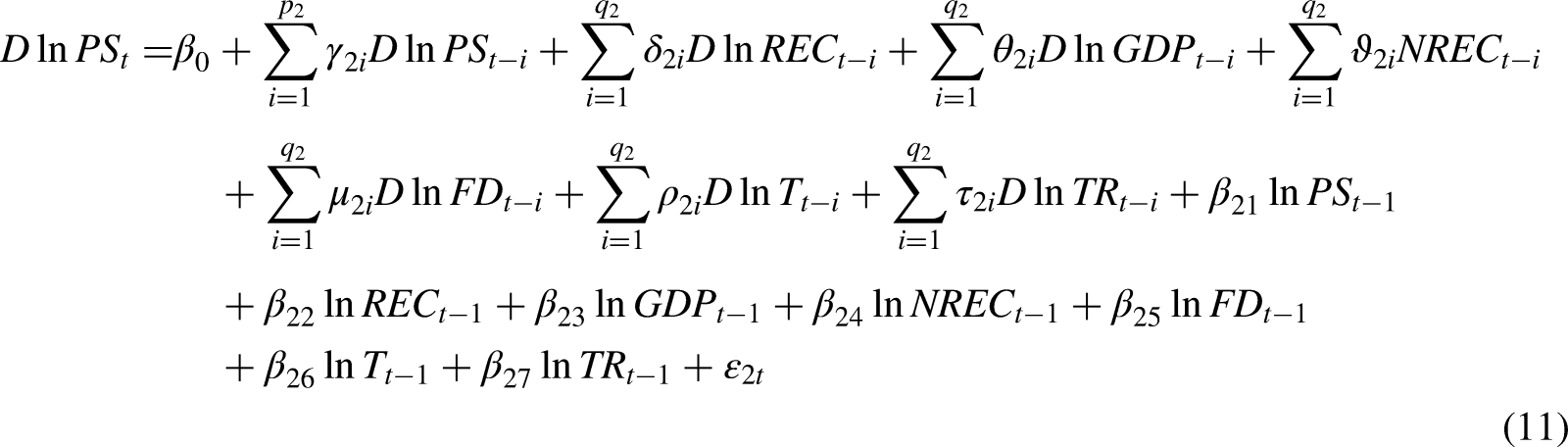

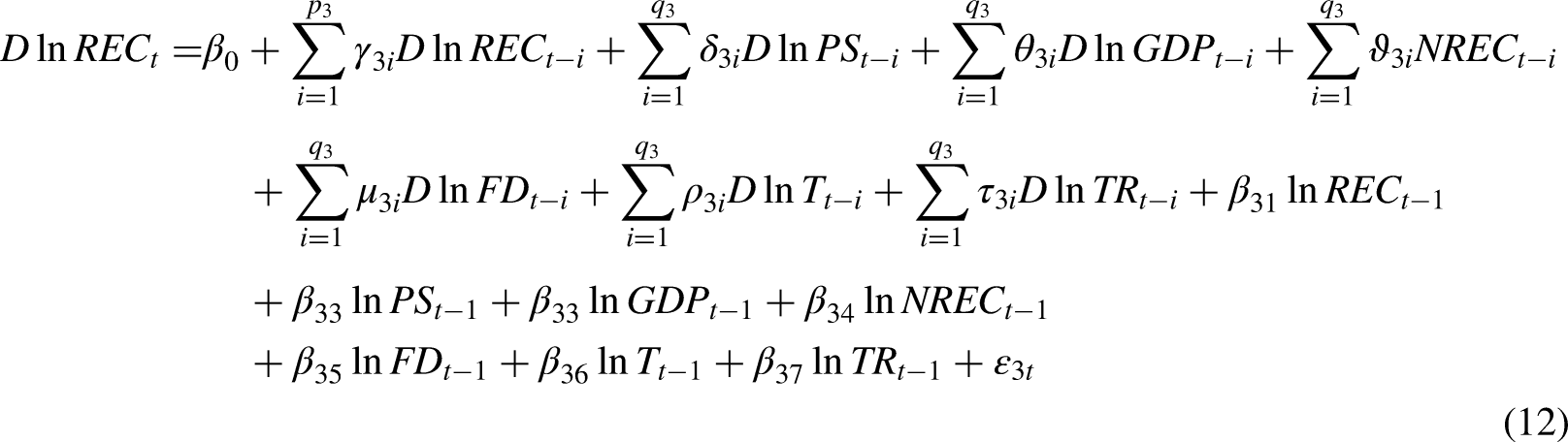

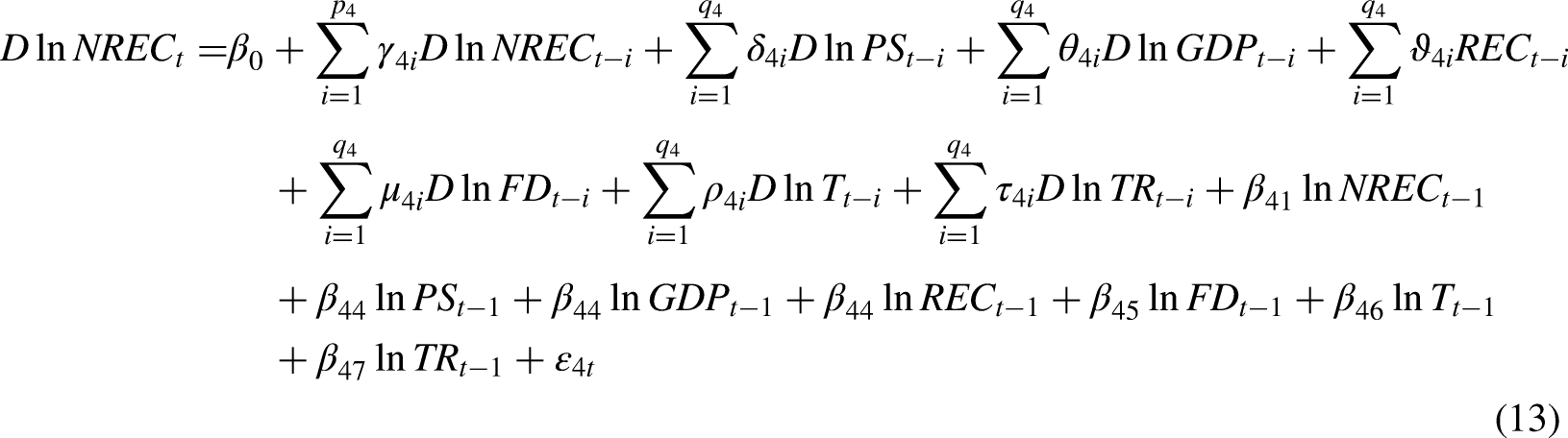

This study aims to analyse the short-run and long-run causality relationships between economic growth, public spending and renewable energy consumption and non-renewable energy consumption (REC, NREC) in eight countries of the SMCs group during the 1980–2020 periods. Basing on the work of Ben Jebli and Ben Youssef (2015), Ali et al. (2017) and Bassem Kahouli (2018) we use the standard Cobb-Douglas production function to estimate the empirical model with constant returns and time t as an aggregate output function. Our econometric model was displayed as follows:

In the second step, we integrated trade and tax rate (proxy of labour) and public spending (proxy of capital) an augmented Cobb-Douglas production function (Bassem Kahouli, 2018). Then, we consider technology factor as endogenously defined by financial development (FD) and represented by equation (2) as follows:

Unit root and bounds tests results

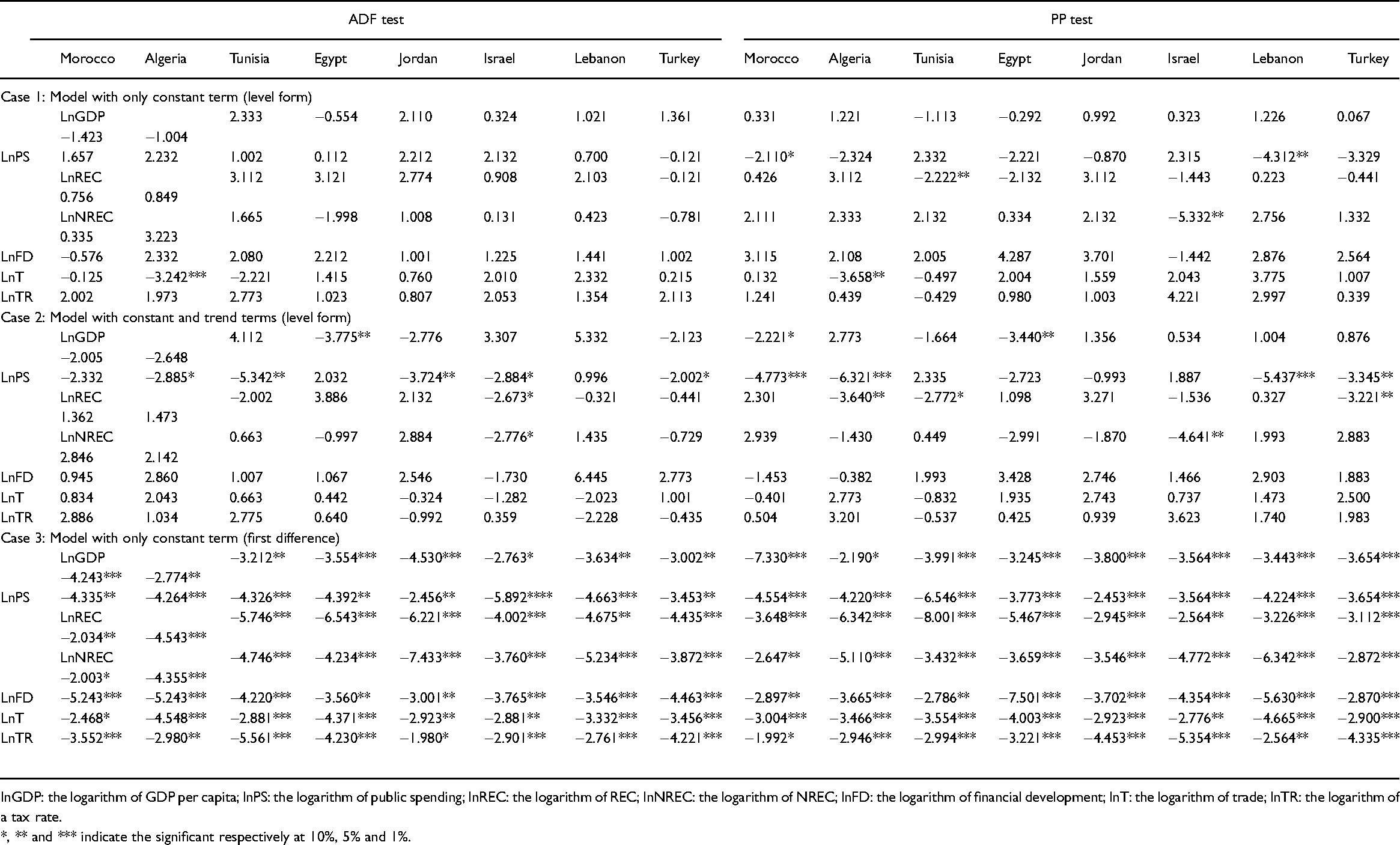

In this part of the study, we try to analyse the different relationships between variables, but before starting this investigation, we should test in the first step the stationarity of each variable in order to determine their order of integration (stationarity at level, or in first difference, or in second difference). To do it, we apply two unit root tests: augmented-Dickey–Fuller (ADF) developed by Dickey and Fuller (1981) and Phillips–Perron (PP) developed by Phillips and Perron (1988). The PP test suggests a non-parametric process to correct the existence of autocorrelation, without having to add tardy endogens as in the augmented DF process (a more robust technique in the episode of moving average (MA) model errors especially). The ADF test is employed to identify the existence of a unit root for autoregressive (AR) model type processes. It then consists in estimating the preceding models by introducing lagged variables. In addition, these two tests are very easy to use and clearly show the order of integration.

These two tests are based on the null hypothesis of non-stationarity, which indicates the presence of a unit root and the alternative hypothesis of the nonexistence of unit root, which means that the variable examined is stationary. The different results of the stationarity test are indicated in Table 1. The results show that all variables are stationary in first difference, meaning that there are integrated into order one (I1). In this case, we can reject the null hypothesis of the presence of unit root and we accept the alternative hypothesis.

Unit root test results.

lnGDP: the logarithm of GDP per capita; lnPS: the logarithm of public spending; lnREC: the logarithm of REC; lnNREC: the logarithm of NREC; lnFD: the logarithm of financial development; lnT: the logarithm of trade; lnTR: the logarithm of a tax rate.

*, ** and *** indicate the significant respectively at 10%, 5% and 1%.

We denote that emotes (*), (**) and (***) indicate the significance (variable is stationary), respectively, at 10%, 5% and 1%. While the values without (*) design that is not significant (is not stationary).

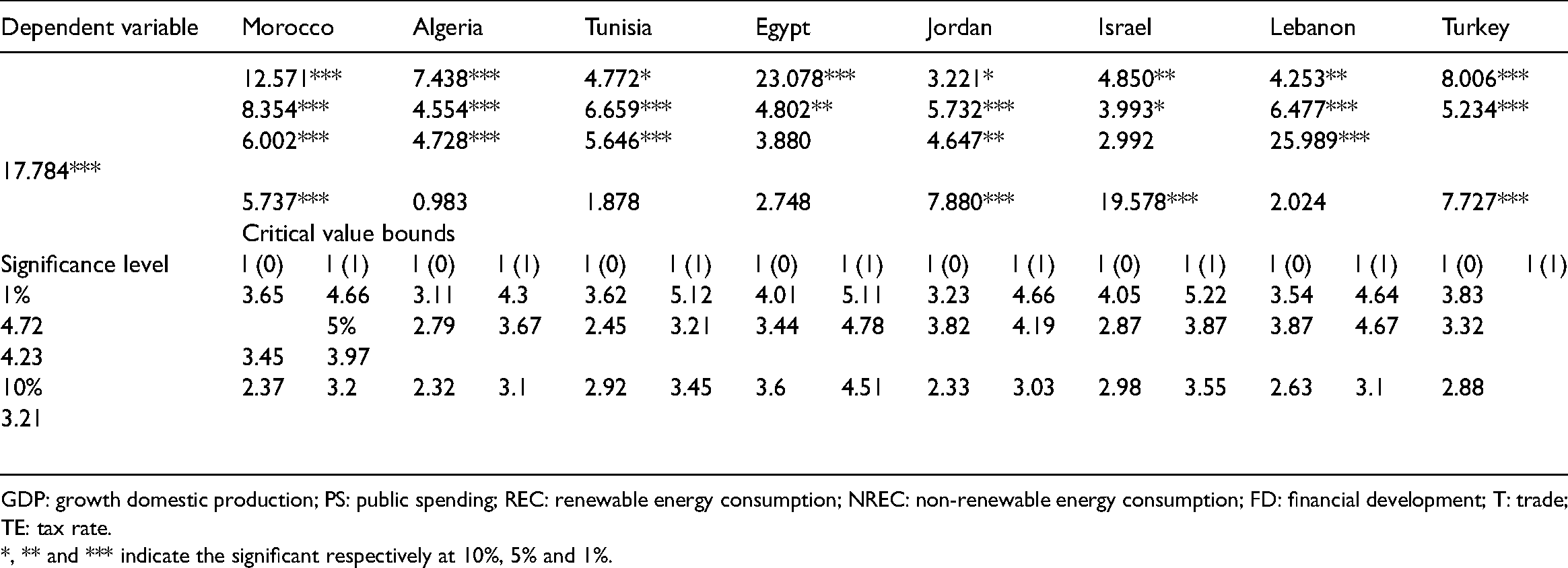

After the determination of the order of integration, we will verify the presence of long-run cointegration between variables using the bounds test. This test was used to verify that the variables of interest are bound jointly in the long term with the dependent variable. The linked stability correction was besides significant proving the presence of long-term relationships.

The Akaike information criterion and Schwarz criteria are used to determine the optimum lags for our models. Lag 3 was founded as the optimal lag for our estimation. The results in Table 2 indicate that in Moroccan and Turkish cases, the different values of F-statistic are exceeding the upper value at 10%, 5% and 1% in both models which designate the existence of long-run cointegration. For Algeria, Tunisia and Lebanon the long-run cointegration does not exist only when the NREC is a dependent variable. In Egypt, the F-statistic value at 23.078 is exceeding the upper bound value at 1%, and the F-value at 4.802 is exceeding the upper bound value at 5%. We can conclude that long-run cointegration between variables exists when economic growth and public spending as dependent variables. The alternative hypothesis was accepted in the Jordan case in both models, while in Israel, the null hypothesis was accepted only when REC was the dependent variable.

Bounds test results.

GDP: growth domestic production; PS: public spending; REC: renewable energy consumption; NREC: non-renewable energy consumption; FD: financial development; T: trade; TE: tax rate.

*, ** and *** indicate the significant respectively at 10%, 5% and 1%.

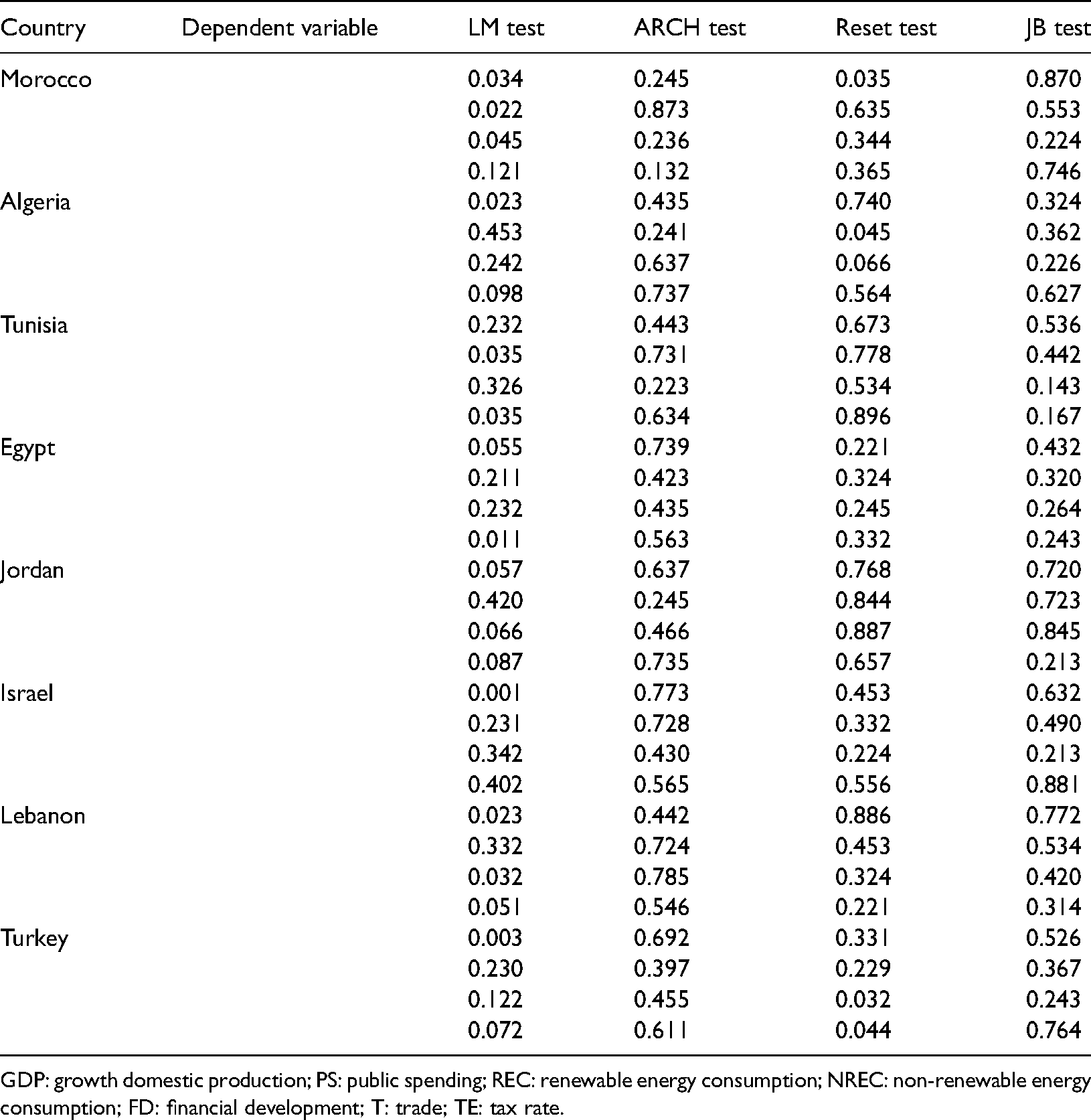

In most cases, the results of the bounds test indicate that the long-run cointegration relationships exist between variables. In the next step, we will use LM (Breusch–Godfrey serial correlation) test in order to detect the serial correlation for residuals, and the results in Table 3 indicate that there is no serial correlation for residuals. The results of the ARCH (autoregressive conditional heteroscedasticity) test show the absence of heteroscedasticity in both models. The JB (Jarque–Bera) normality test indicates that the error terms are normally distributed. The values of the reset test are greater than 1%; it means that the estimation models are free from specification errors.

Diagnostic test.

GDP: growth domestic production; PS: public spending; REC: renewable energy consumption; NREC: non-renewable energy consumption; FD: financial development; T: trade; TE: tax rate.

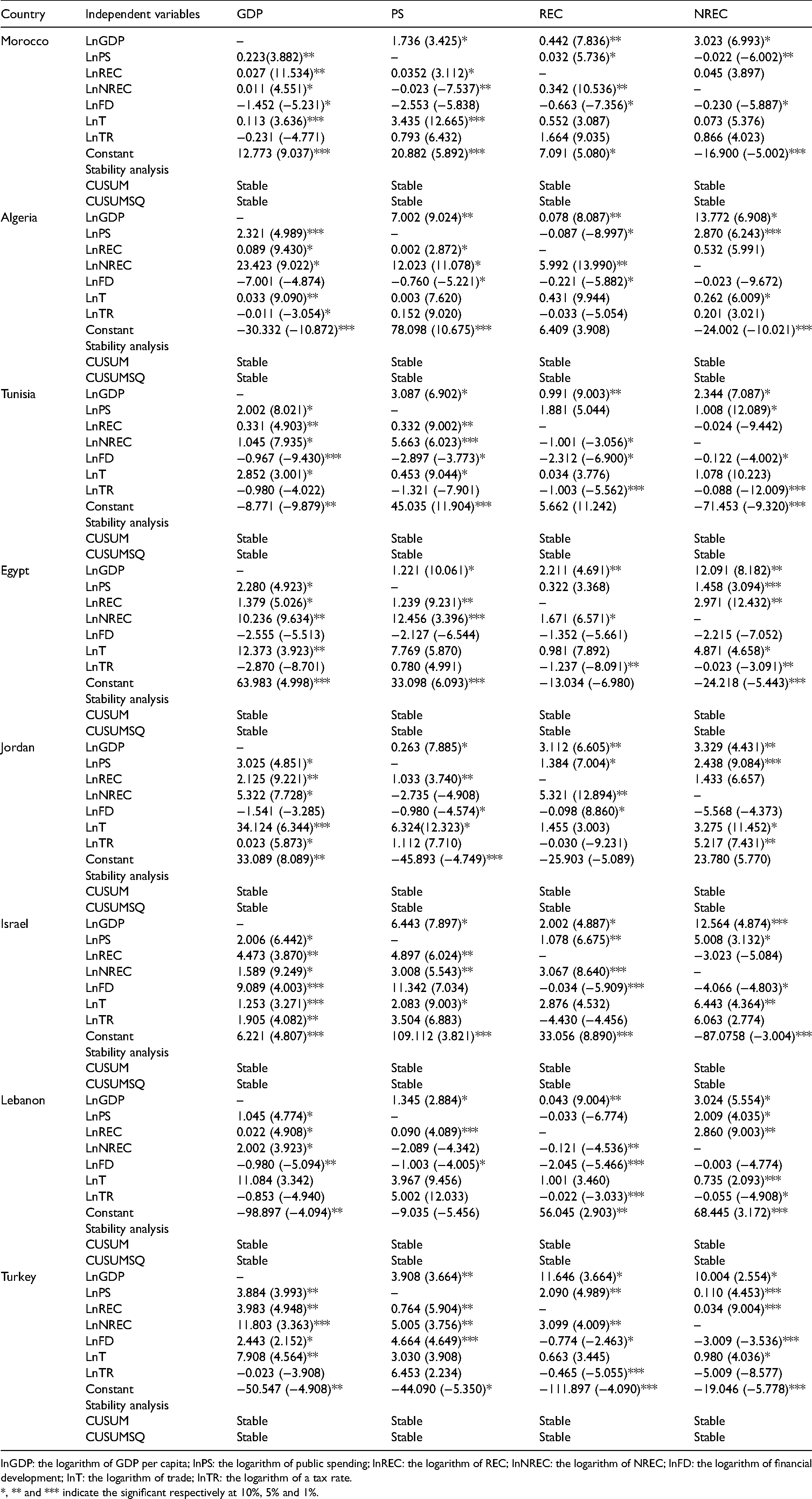

One, we have confirmed the existence of long-run cointegration relationships between variables by using the bounds test; we can investigate and estimate our four models by the ARDL approach. The different results of long-run ARDL estimations are indicated in Table 4. Starting with CUSUM and CUSUMSQ, we can observe that our econometrical model was stable during the study period for all SMCs.

Long run ARDL coefficients.

lnGDP: the logarithm of GDP per capita; lnPS: the logarithm of public spending; lnREC: the logarithm of REC; lnNREC: the logarithm of NREC; lnFD: the logarithm of financial development; lnT: the logarithm of trade; lnTR: the logarithm of a tax rate.

*, ** and *** indicate the significant respectively at 10%, 5% and 1%.

ARDL approach specification and results

After writing the different equations of our different relationships, we practice multiple steps and methods. Essentially, our study was based on the ARDL bounds testing approach (Pesaran and Shin, 1999; Pesaran et al., 2001) and the approach of Granger Causality. The ARDL approach was used in this study for many reasons. First able, we can apply the ARDL approach when variables are integrated in order of zero (I0), in order of one (I1) or similarly integrated. Secondly, the ARDL procedure can resolve the endogeneity problems and it can detect a suitable number of lags in the data series. Thirdly, the ARDL approach uses a single abridged form equation. Fourthly, the ARDL approach was used in our study because it gives us the opportunity to detect the impacts of explicative variables on endogenous variables at the same time in the short run and in long run. For these reasons, we find that the ARDL technique can resolve the problem of our study more precisely than other techniques.

After checking the integration order of different variables, it is possible to practice the ARDL approach in order to verify the cointegration relationships of long term between economic growth, PS, REC, NREC, FD, T and TR. The ARDL model can be defined as follows:

To check the existence of long-run cointegration between variables, we need to verify the null hypothesis (H0) of no cointegration and the alternative hypothesis (H1) of the presence of long-run cointegration. Wald test gives as the opportunity to check these two hypotheses, while H0: βj1 = βj2 = βj3 = βj4 = 0 (non-existence of long-run cointegration). H1:βj1 = βj2 = βj3 = βj4≠0 (existence of long-run cointegration).

After verifying the existence of long-run cointegration, we go to the next step where we use the bounds test (Pesaran et al., 2001; Narayan, 2005; Turner, 2006). The bounds test is based on two critical bounds: lower critical bound and upper critical bound. If the value of F-statistic was greater than the upper bound, so we can confirm that long-run relationships exist between variables, and no long-run relationships exist among variables if the F-statistic value was less than the lower critical bound.

For the first model (GDP as dependent variable); we observe that PS, REC and NREC have significant and positive long-term impacts on economic growth in the eight countries of the SMCs group. An increase in PS by 1%, on average economic growth will increase by 0.223%, 2.321%, 2.002%, 2.28%, 3.025%, 2.006%, 1.045% and 3.983%, respectively, in Morocco, Algeria, Tunisia, Egypt, Jordan, Israel, Lebanon and Turkey. The Algerian, Egyptian and Turkish economics are intensively affected by NREC. The FD variable has a negative impact on GDP in six countries; only in Israel and Turkey, it has a positive influence. In addition, TR affects negatively SMC’s economic growth, only in Jordan and Israel; it has a positive effect on GDP.

For the second model (PS as dependent variable), the result indicates that GDP has a positive long-term impact on PS in all countries of SCMs. We find that REC has a significant and positive impact on PS in all of our study countries, but more intensively in Israel than others. An increase in REC by 1% on average PS in Israel will increase by 6.443%. NREC has a mixed effect on PS in SCMs. An increase on NREC by 1% on average PS in Morocco, Jordan and Lebanon will decrease, respectively, by 0.023%, 2.735% and 1.003%. However, for the rest of the country, NREC has an essential role in the increase of PS. In Morocco, Algeria, Tunisia, Egypt, Jordan and Lebanon FD can reduce the PS; only in Israel and Turkey, an increase in FD will increase PS. Moreover for TR, the results indicate that in all countries TR has an insignificant and positive long-run impact on PS except Tunisia. In addition, PS was positively influenced by T in SCMs, which means that the tourism sector is an essential factor in SCMs economics.

For the third model (REC as dependent variable), we observe that GDP has a significant and positive impact on REC. This impact was more intensively in Turkey, where an increase of Turkish GDP by 1% will increase REC by 11.646%. In Algeria and Lebanon, an increase in PS by 1% will decrease REC, respectively, by 0.087% and 0.033%. Only in Tunisia and Lebanon, NREC has a negative effect on REC. The results indicate that FD has a negative long-run impact on REC in all countries of SMCs. We observe that TR has a significant and negative effect on REC in Tunisia, Egypt, Jordan, Israel, Lebanon and Turkey.

For the final model (NREC as dependent variable), NREC has been significantly and positively affected by GDP in SCMs. For example, an increase in GDP by 1% will increase NREC, respectively, by 13.772%, 12.091%, 12.564% and 10.009% in Algeria, Egypt, Israel and Turkey. Only in Morocco PS has a negative impact on NREC, where an increase on PS by 1% will decrease NREC by 0.022%. In Egypt, Lebanon and Turkey REC effect significantly and positively NREC. The result shows that FD has a negative impression of NREC in all studied countries. By contrast, T touches positively NREC in the eight countries of SCMs. Finally, TR effect negatively NREC in Tunisia, Egypt and Lebanon. In the same context, the long-run results show that TR has an insignificant effect on NREC in Morocco, Algeria, Israel and Turkey.

VECM and Granger techniques specification and results

Subsequently testing the existence of long-run cointegration and long-run relationships between different variables of model, we try to determinate the direction of causality among them using the VECM Granger causality approach. While the VECM approach is a restriction of VAR. It is used to detect the short-run relationship and to verify the presence of the long-run relationship by means of the significance of ECT. The different equations of the VECM approach are represented as follows:

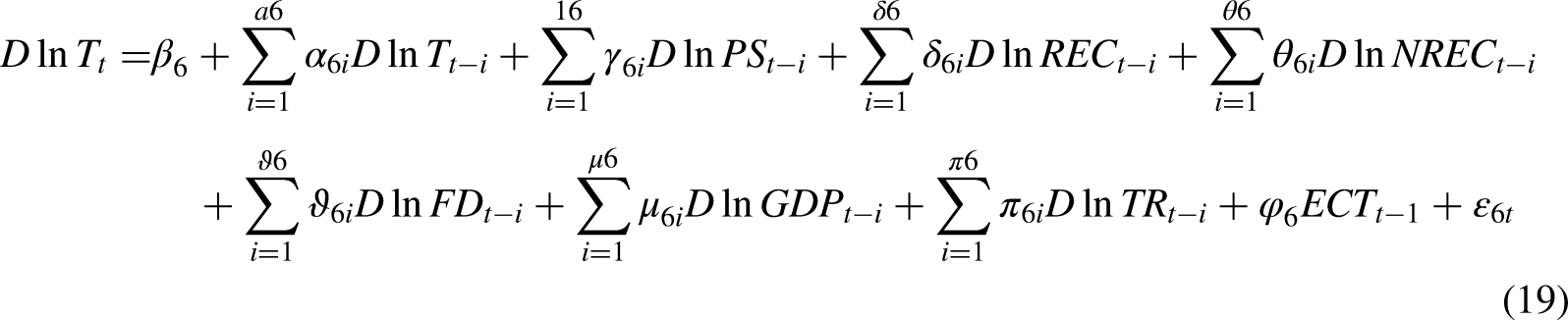

The different results of the estimates were reported in Table 5.

Granger causality test results.

lnGDP: the logarithm of GDP per capita; lnPS: the logarithm of public spending; lnREC: the logarithm of REC; lnNREC: the logarithm of NREC; lnFD: the logarithm of financial development; lnT: the logarithm of trade; lnTR: the logarithm of a tax rate.

In the case of Morocco, the results indicate the existence of two positive bidirectional causal relationships. The first relationship is between growth economic and public spending, and the second is between growth economic and NREC. In addition, there are five unidirectional relationships. More precisely, there are two positive unidirectional relationships where PS affects REC, and where trade affects GDP; and three negative unidirectional relationships where FD and TR influence GDP, and where T affects FD. In the case of Algeria, there is one positive relationship between NREC and GDP, and there are four unidirectional relationships, one positive between T and NREC and three negatives where FD and TR affect GDP, and where TR affects FD. In Tunisia there are two bidirectional relationships; one positive between GDP and trade and the other is negative between PS and REC. Three negative unidirectional relationships exist where NREC, T and FD influence TR, and there are two positive unidirectional relationships exist where trade touches GDP and PS. Also in Egypt, there are two bidirectional relationships, but all of these relationships are positive. The first is between GDP and NREC, and the second is between REC and FD. However, there two positive unidirectional relationships between PS and GDP, and between FD and TR, also there two negative unidirectional relationships where TR affects REC and T. In the case of Jordan, there are two bidirectional relationships between PS and GDP and between REC and NREC, as well there are two positive unidirectional relationships where FD and trade affect respectively PS and TR, and there three negative unidirectional relationships where REC influences NREC and T, and where TR influences GDP. Two positive bidirectional relationships exist in the case of Israel between GDP and PS and between REC and GDP. The other relationships are unidirectional; two are negative between NREC and REC and between TR and NREC, and only one is positive between FD and NREC. In Lebanon, there is only one positive relationship between GDP and PS. By contrast, there are eleven unidirectional relationships. More specifically, there are eight positive relationships where GDP affects TR, where PS affects REC and T, where REC affects GDP and NREC, where FD affects T and where GDP was affects by T and TR, and three positive relationships where REC, NREC and FD influence, respectively FD, GDP and REC. Finally, in the case of Turkey, we found three positive bidirectional relationships where GDP affects PS, REC and NREC and we found also three negative unidirectional relationships where REC, FD and trade affect respectively FD, trade and TR. The results of Granger causality show that the short-run causal relationships between GDP, PS, REC, NREC, FD, T and TR are mixed, which means that the eight countries of the SMCs group are heterogeneous.

Studying country by country, it is clear to note that in three countries among eight the alternative hypothesis is verified between growth economic and REC, more precisely in Israel, Lebanon and Turkey. These two variables are correlated. In Israel and Lebanon, REC influences GDP (unidirectional), while in Turkey GDP and REC influence each other (bidirectional). This result suggests that renewable energy and economic strategies will have to be executed jointly and the REC has an essential role in the production progression in both countries. However, the neutrality hypothesis is verified in the remaining countries, meaning that no short-run causal relationship exists between REC and GDP. For NREC and GDP, the results show that these two variables are not correlated in Tunisia, Jordan and Israel; it means that the neutrality hypothesis is verified (Chien-Chiang Lee, 2006). While in the five remaining countries, we can observe that bidirectional relationships between NREC and GDP exist (Dritsaki and Dritsaki, 2014; Bassem Kahouli, 2018), except for Lebanon where is a unidirectional causal relationship among NREC and GDP. This result shows that energy consumption has an important role in economic development in most of these countries.

The results of short-run causal relationships show that there is no causal relationship between PS and GDP in Algeria and Tunisia. On the other hand, in Morocco, Egypt, Jordan, Israel and Turkey PS and GDP positively influence each other (bidirectional). Only in Lebanon, there is a bidirectional relationship between PS and GDP where GDP affect negatively PS. We can conclude that PS is an essential element in the economic process in these six countries.

The ECT is used to detect the long-run causal relationships. To prove that there is at least a long-run relationship between variables and the endogenous variable is an adjustment factor when the econometric model diverges from equilibrium, it is necessary that the coefficient should be at the same time negative and significant. The results indicate that REC is the adjustment factor in Morocco and NREC is the adjustment factor in Algeria with a speed, respectively, of 7.4% and 5.9% per year. In Tunisia, REC, NREC, FD and T are the factors of adjustment of long-run to equilibrium with speeds, respectively, of 3.5%, 2.36%, 8.77% and 0.44%. NREC, FD and TR are the adjustment factors in Egypt with speeds, respectively, of 0.37%, 1.29% and 5.58%. In Jordan, the GDP per capita with a speed of 69.27%, the REC with a speed of 7.71% and FD with a speed of 2.65% represent the factors of adjustment of long-run to equilibrium. In Israel, the factors of adjustment are GDP, PS, REC and tax with speed, respectively, of 3.78%, 1.42%, 3.89% and 3.55%. However, there are only two adjustment factors in Lebanon REC and TR with speed, respectively, of 3.88% and 3.55%. Finally in Turkey, we can observe that GDP, PS, REC and T are the adjustment factors with speed, respectively, of 0.73%, 6.3%, 3.35% and 7.38%. We can show that the impression of the PS is neutral for Morocco, Algeria, Tunisia, Egypt, Jordan and Lebanon. However, for Israel and Turkey, a significant and long-term influence exists.

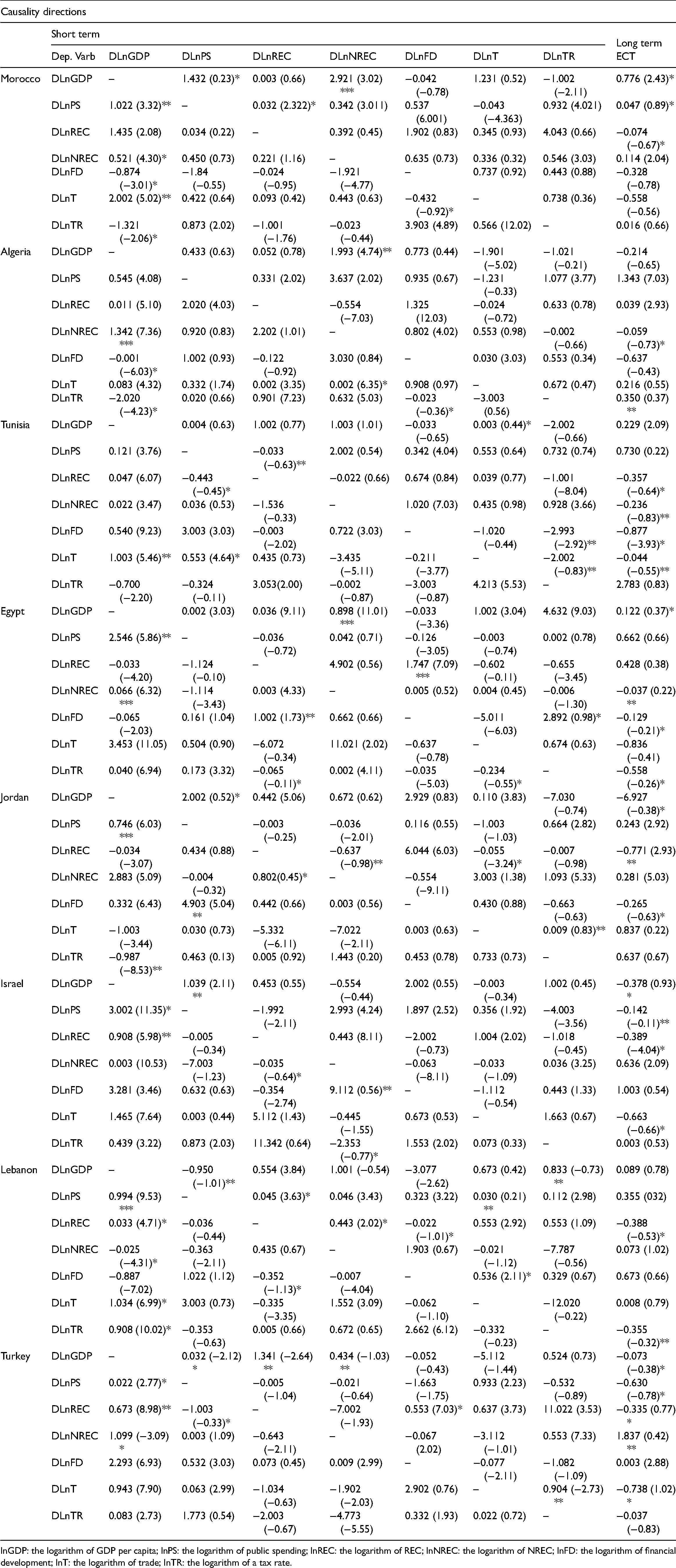

To summarize, we can confirm that the eight countries of the SMCs group are heterogeneous according to the mixed VECM outcomes for singular countries and the factor of adjustment varies from one country to another. In Figure 1, we recapitulate the different bidirectional relationships between GDP, PS, REC and NREC.

Squares of bidirectional and unidirectional causality relationships between GDP, PS, REC and NREC. Note: (+) design a positive unidirectional causal and (−) design a negative unidirectional causal. The double arrows design a bidirectional causal relationship.

We define by one arrow a unidirectional causal relationship and the direction of the arrow indicates how to cause the other, while the design of the double arrow a bidirectional causal relationship means the two variables cause each other.

Conclusion and policy implication

The principal objective of this investigation study is to exanimate the causal relationships among economic growth, PS, REC and NREC in eight countries of SMCs during the 1980–2020 period. FD, trade and TR are used as control variables. We apply different tests and technics starting with stationarity tests, diagnostic tests, bounds test and ARDL approach and finally VECM technic. The ADF and PP unit root tests in the first difference indicate that all of the series of GDP, PS, REC, NREC, FD, T and TR are stationary. The results of the bounds test approve the presence of cointegration relations between our variables, meaning that there is at least one long-run relationship between variables. The ARDL estimations show that PS, REC and NREC have positive effects on economic growth in all countries of SMCs in long term. These results indicate that PS, REC and NREC are essential factors in the economic development in both countries of SMCs in long term. While the VECM results designate that there is one bidirectional causal relationship in Morocco between GDP and PS and REC is positively affected by PS, meaning that PS increases REC. This result seems logical, indeed in the last years, the Moroccan government has devoted a very important part of their expenditure to the development of renewable energies mainly in the solar energy installed in the south of the country (the desert). For Algeria, we observe that there is a bidirectional causal relationship between GDP and NREC. This result is expected since the Algerian economy is essentially based on oil production. In Tunisia, there is a bidirectional causal relationship between PS and REC. A bidirectional relationship between GDP and NREC and a positive unidirectional from PS to GDP exist in Egypt. However, in Jordan, there is one bidirectional causal relationship where PS and GDP influence each other. Two bidirectional relationships are presented in Israel between PS and GDP and between REC and GDP, while NREC negatively affects REC in a negative unidirectional causal relationship. In Lebanon, there is one bidirectional relationship between PS and GDP, and there are three positive unidirectional relationships where REC influences GDP and NREC and where PS impacts REC and one negative unidirectional causal where GDP is influenced by NREC. Finally, in Turkey GDP have three bidirectional causal relationships with PS, REC and NREC.

To summarize, the results indicate that the majority of SMCs economies depend heavily on non-renewable energies.

At the end of this research, we find that is necessary to remember that the absence of sufficient data for both Libya and Syria due to the political and security turmoil as a result of civil wars constitutes a challenge for us to present a study that is more accurate and reflects the general situation of the region as a whole. However, the general situation in these countries and the social demands they witness, open the door to question about the fate of investment in renewable energies and in scientific research. This problem we seek to be the subject of future research and development, which deals with the study of the situation of alternative energy in SMCs countries with high consumer public expenditures and budget deficit.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.