Abstract

Financial systems reveal complex and nonlinear behavior in the presence of various macroeconomic drivers. In the present study, we investigate the nonlinear financial system behavior through the formulation of an ordinary differential equation model using interest rate, investment demand, and price index as the state variables. The model involves government debt and investment time delay as the most influential parameters of system dynamics. Firstly, we examined the elementary characteristics of the system’s solutions, identified equilibria, and analyzed local stability. Our findings show that, within a certain range of government debt, the system maintains stability until it reaches a critical point, at which it becomes unstable due to a Hopf bifurcation. We illustrated how raising the investment delay can drive the system towards instability after passing a critical delay magnitude. To counteract the emergence of erratic behavior caused by unregulated debt and time delay, we introduced a synchronization control strategy. Numerical simulations are presented to validate the theoretical results, demonstrating the efficacy of the introduced control mechanism in stabilizing the financial system.

Introduction

A financial dynamical system is a dynamic representation of the interactions within financial markets. Studying nonlinear financial systems is essential for managing high risk, predicting market movements, and formulating policy. Financial variables, such as gross domestic product (GDP) fluctuations, depreciation, banking panic, and stock market collapse, can have substantial and disproportionate consequences. Lorenz et al.1,2 studied the chaotic attractor, chaotic saddles, and fractal basin boundaries of Goodwin’s nonlinear accelerator model. Chian 3 explored complex economic dynamics in a forced oscillator business cycle model. Unstable periodic orbits, chaotic saddles, intermittency in periodic windows, and their relation with stock and foreign exchange markets were analyzed by Chian et al.4,5 Achitouv 6 studied the stock return correlation and identified some dynamical properties of the network that were relevant to market returns. Benhabib and Nishimura 7 explored the stability in the presence of closed orbits in an economic growth model.

Numerous economic models have been used to investigate the existence of Hopf bifurcation in economics. According to Ma and Chen,8,9 Liao et al., 10 stability and bifurcation with regard to several economic parameters for a few basic financial models were examined. Gao and Ma 11 studied the Ruelle–Takens route to chaos and strange nonchaotic attractors (SNA) of a three-dimensional (3D) financial system. Zhang et al.12,13 studied the qualitative behaviors of four-dimensional (4D) financial systems. Ma and Wang 14 observed the horseshoe chaos in the financial system based on the topological horseshoe theory. Szuminski 15 explored the concept of differential Galois theory and its application to the analysis of the intrinsic property of the finance system. A more thorough explanation of Galois theory and its implementation can be found by Ruiz, 16 Put and Singer, 17 and Maciejewski and Przybylska. 18 Research indicates that the behavior of financial systems is influenced by production, currency, and interest rates. Yu et al. 19 proposed an economic model with four dynamic factors: interest rate, investment demand, price index, and profit margin, and they used speed feedback control and linear feedback control to suppress the chaotic behavior of the system. Some other 3D chaotic finance systems have been widely studied by Wu and Chen, 20 Tusset et al., 21 Dousseh et al., 22 and Vaidyanathan et al. 23

The generalization of classical calculus to derivatives and integrals of non-integer orders, known as fractional calculus, has been widely utilized in financial systems given that it captures memory and hereditary features of economic activities. Instead of instant responses to changes in the market as assumed in classical models, fractional-order models describe the long-range dependencies and temporal correlations present in asset returns, volatility, and risk dynamics. Farman et al. 24 established a nonlinear fractional-order model to investigate the behavior and prediction of economic diversification under the effect of stochastic engineering variables. They investigated the stability, boundedness, and persistence of the model by means of fixed-point theorems and verified the theoretical results by numerical simulations so that tourism, green finance, and foreign direct investment are crucial catalysts of sustainable economic growth. Olayiwola et al. 25 considered an optimal problem of embedding minimum interest rates and maximum investment demands to study long memory effects on the financial soundness, disclosing a positive association between investment demand and interest rates for enhanced prediction and financial market stability. Through the Caputo and Atangana–Baleanu formulations, the nonlinear dynamics of a financial system that includes a minimum interest rate parameter and exhibits stability, uniqueness, and realistic macroeconomic behavior can be observed by Farman et al. 26

Time delay systems can capture the influence of past states on the current state of the system. Such a delay typically gives rise to non-trivial dynamics, oscillations, bifurcation, and instability. Time delay is widely observed in different fields such as population dynamics, engineering, and neural networks. Understanding time delay systems and being able to analyze them with designing control strategies as well as predicting system behavior is an important investigation in nonlinear dynamics.27,28 Similarly, time delay plays a vital role in nonlinear economic dynamical systems. For example, changes in the interest rate do not cause immediate changes in the economy, and there is always a time lag. Delays in fiscal policy make the dynamic problem realistic, as the decisions made by the government for public purchases take time to implement. The investment-saving and liquidity preference-money supply (IS-LM) model is a simplified representation of the dynamic adjustments of the goods and services market and the money market. Fanti and Manfredi 29 investigated dynamical properties through an IS-LM model with tax collection lags. Rajpal et al. 30 introduced a 4D IS-LM model consisting of gross domestic product, interest rate, capital stock, and money supply as a state variable with two-time delays. Çalıs et al. 31 investigated the stability and Hopf bifurcation of the financial system with investment delay. They introduced profit margin as a new state variable in a 3D financial system. Kai et al. 32 studied the impacts of two-delay feedback on dynamics characteristic of the nonlinear financial system. Thus, time delays increase the realism of the financial system. Other important research of the financial time delay system was found by Liu et al., 33 Zhao et al., 34 and Zhang and Zhu. 35

Synchronization in ordinary differential equation (ODE) systems is a phenomenon where two or more dynamic systems described by ODEs adjust their behavior to work in concert, often coordinating trajectories or oscillations over time.36,37 Investigating the nonlinear dynamics of chaotic systems with different synchronization strategies remains a central topic of research in physics, biology, and economics. In coupled ODE systems oscillations may attain synchronization through interactions as diffusive coupling and external forcing potentially engender identical, phase, or lag synchronization. Applications of this consequence are especially salient in secure communication, neural networks, and financial modeling, where some dynamics can be kept aligned for system stability and functioning reasons. Wei et al.

38

extended the finite-time synchronization for semi-Markov random dynamical systems by applying a new asynchronous boundary control scheme. Kumar et al.

39

established finite-time synchronization criteria for fractional-order BAM neural networks with delays using adaptive feedback control and a new Lyapunov-Krasovskii functional. Their findings, validated by numerical examples, highlight the practical significance of finite-time behavior over asymptotic synchronization. Li et al.

40

investigated the fixed-time synchronization of fuzzy stochastic cellular neural networks with mixed delays and

A significant amount of government debt can greatly impact the health and stability of an economy. High national debt can lead to a series of adverse effects on the market, affecting exchange rates, inflation levels, and unemployment rates. As interest rates go up, consumer and business borrowing becomes more expensive, and this may lead to a reduction in consumption as well as investment, ultimately causing economic growth to slow down. Excess of government debt can also lead to erosion in investor confidence, which will further put doubt into the minds of investors about making returns from their investments. This uncertainty reduces investor confidence, leading to reduced investment and hence decreased economic activity. It also reduces the value of the bonds, which leads to a loss of faith in the currency of the country. Furthermore, large public debt can hamper the government’s ability to act in response to future economic downturns, as it may not have sufficient fiscal room for maneuver to boost economic activity. This can create a vicious circle in which slow growth becomes weaker investor sentiment, greater economic fragility, and ultimately long-term challenges for the government to meet its economic aims. At the end, excessive government debt levels can lead to serious economic issues, and it is important for governments to keep appropriate levels of their debt in check so as not to exacerbate or usher in another financial crisis. In this situation, investors slow down their investments and sometimes decline to invest in the financial market due to fiscal irresponsibility. Elkhalfi et al. 47 studied a fixed-effects panel model on the effect of external debt on economic growth. They discovered a U-asymmetry where moderate debt enhances growth, while excessive debt accumulation retards it, which underlines the importance of prudent handling of debt. Das and Ghate 48 analyzed the dynamics of India’s public debt from 1951 to 2018 using a new dataset and examined both aggregate debt as well as the security level of debt. They found that inflation is an important source of financing for government debt, with nominal returns on both marketable and non-marketable debt accounting for the most substantial changes in public debt. Damrich et al. 49 studied the effect of crowding in and crowding out on GDP through various economic models. A five-dimensional debt-financed investment model with wage, employment, expected sales, and capacity implementation has been investigated by Grasselli and Huu. 50

Important insights have been gained from previous research on the nonlinear dynamics of key macroeconomic variables like interest rates, investment demand, and price indices. However, they usually fail to take into account the impact of government debt and investment delay which can heavily affect the system qualities. In addition, the destabilization result of time delay and increasing debt level has not been well studied. Also, current dynamics in the literature do not account for effective controls to stabilize the system at high debt and long investment delay. Although a number of works have investigated the dynamic states of financial systems and their change from stability into instability, very few works have studied the design of control schemes to suppress chaos. Indeed, most of the existing results concern the study of the system’s stability or the determination of the chaos onset, but do not consider a practical method to control the system if it starts to become unstable. On the other hand, if a financial system is unstable or exhibiting chaotic behaviors, the implementation of appropriate control policies is particularly useful in taming the volatility of the system and avoiding it from being too erratic. More specifically, synchronization-based methodologies appear to be far more promising from a practical perspective as they provide natural explanations for coherent behavior in linked economic factors or agents. Nevertheless, the combination of synchronization and control techniques in time delayed financial systems is still uncharted, this is the research void that is addressed by this study.

In this article, we consider government debts and investment delay as key economic parameters. These are important considerations for the kind of dynamic feedback involved in fiscal policy and investment decisions that our model attempts to study. Government debt impacts the economic environment by influencing interest rates, investor confidence, and market sentiment. Debt management is one of the most important things to foster sustainable development and reduce financial risks. In contrast, investment delay is connected with the delay in establishing concerns among viable possibilities and can potentially introduce oscillations and instability in the system. Our study provides a new understanding about how financial markets are driven and how economic variables interact along a complex spectrum. This approach extends the data that policymakers and scientists can use to anticipate interactions that might turn out to be economic shocks or instability. Through the analysis of crucial values of these parameters, we exhibit that crossing threshold values can possibly destabilize the system. Additionally, we give synchronization techniques to delayed and non-delayed systems so that the policymakers may attempt control policies on a simulated system prior to applying the control policies on the original system. This prevents worsening unpredictability because it offers a stable framework in which to stabilize financial systems. Our results provide policy-making strategies by providing a detailed account of the intricate relationship between economic variables and system stability.

The main contributions and novelties of this article are summarized as follows:

Extended model formulation: We propose an ODE model for major macroeconomic variables, interest rate, investment demand, and price index, tracing also the effects of government debt and investment delay, and study the global stability of the macroeconomic system. Determination of critical parameters: This article establishes the critical levels of government debt and investment delay at which the system becomes unstable. Synchronization of the unstable system: We design and analyze synchronization schemes in the two situations—without and with time delay—when the government debt and the investment delay surpass their critical values to guarantee system stability. Comprehensive numerical analysis: Theoretical results are supported by numerical simulations, which consist of local stability diagrams, time series plots, phase planes, and bifurcation diagrams. In addition, the proposed synchronization schemes are validated by numerical simulation examples in detail.

The structure of this article is organized as follows: the “Related literature and methodology” section explains the related literature and methodology. The basic properties of the model, such as existence, uniqueness, and boundedness, have been analyzed in the “Some basic properties” section. The stability and Hopf bifurcation at the equilibrium points of the system for different time lags and government debt are observed in the “Equilibria and stability analysis” section. In the “Numerical simulations” section, we present synchronization strategies to control the chaotic system and validate the theoretical results through numerical simulations. In the “Results and discussions” section, we discuss the key findings of our research. In the “Limitations and future work” section, we describe the limitations and future research directions. Lastly, the “Conclusion” section presents the conclusion from this investigation.

Related literature and methodology

The seminal work of Ma and Chen8,9 initially introduced the nonlinear dynamics of interest rate, investment demand, and price index with some important economic variables such as saving amount, elasticity of demand, and cost per investment. They explored how these parameters in turn affect the behavior of the financial system. On the basis of this core concept, Kachhia

51

further developed the nonlinear financial model with fractional order dynamics. This extension to the system allows us to study how the control efforts of fractional orders characterize financial relations in a more granular way. The model entails basic assumptions that can be traced to the following relationships:

Thus, we obtain the following model as given below:

Now we will discuss the impact of government debt on interest rates and price indexes. Also, we consider the impact of time delay on investment processes and their effects on the system (1).

Suppose

The feedback gain parameter k measures the degree of adaptiveness of investors’ response to the difference between their current demand for investment

The model is highly sensitive to the parameter combination

Some basic properties

In this section, we will discuss the existence, uniqueness, and boundedness of the considered model.

Define

Consider the mapping

Then, for every

If

Let

Equilibria and stability analysis

To find the equilibrium points of (2), we equate the right-hand side of each equation of the system (2) with zero and solve the system. We consider the following propositions:

If

When

Now we consider the linear transformation to shift the equilibrium point

Stability analysis

Here, we will work on the stability and Hopf bifurcation analysis for the point

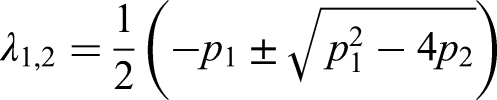

Solving (10), we obtain a three-degree exponential polynomial equation as follows:

The equilibrium point

The equilibrium point

For,

Consider

For

When Proposition 5 holds, then for all values of

Suppose that equation (14) has a root of the form

Separating both real and imaginary parts of equation (16) as follows:

If

Substituting (20) into (17), we have

Suppose

Substituting

Using equations (14) and (18) into (23), we get

In this article, we shall examine the behavior of the economic variables for the equilibrium point

For

According to the Routh-Hurwitz stability principle,

Let

Substituting

In this case,

Evaluating equation (43) at

Since the eigenvalues are

For

Separating both the real and imaginary parts of equation (45) as follows:

By squaring and adding both sides of the above equations, we obtain

Now considering the parameter values of the system (2) as

Transversality condition for the equilibrium point

Differentiating (32) with respect to

By using equations (32), (46), and (47) into (50), we obtain the following expression:

Let

By using parameters values

Numerical simulations

In this section, we will verify the theoretical results numerically and graphically by plotting the time series and parametric solutions of the system using MATLAB software. We first consider the system without time delay and investigate the critical value of government debt. We shall apply a synchronization approach in order to control the chaotic behavior due to the excessive amount of government debt. On the other hand, in the “Simulations of the system with a time delay” section, we analyze the bifurcation caused by time delay and will propose some synchronization approaches to synchronize the system with the original system. The synchronization control strategy performs well for stabilizing the federal systems despite time lapse, and it provides a potential approach to controlling complex systems with government debts and delayed times.

The normalized forward sensitivity index of a variable X that depends differently on a parameter, p is defined as follows:

Now we define the component of the coexistent equilibrium point

Sensitivity indices of the point of equilibrium.

Simulations of the system without a time delay

First we consider the parameters’ values from Table 2 and investigate local stability of the system (2). A locally asymptotic stability ensures that trajectories corresponding to all five sets of initial points

Local stability diagram of the system (2) with respect to a set of five different initial conditions.

Parameter values taken into consideration for numerical simulations.

GDP: gross domestic product.

Now, we will explore the effect of government debt

The critical value of

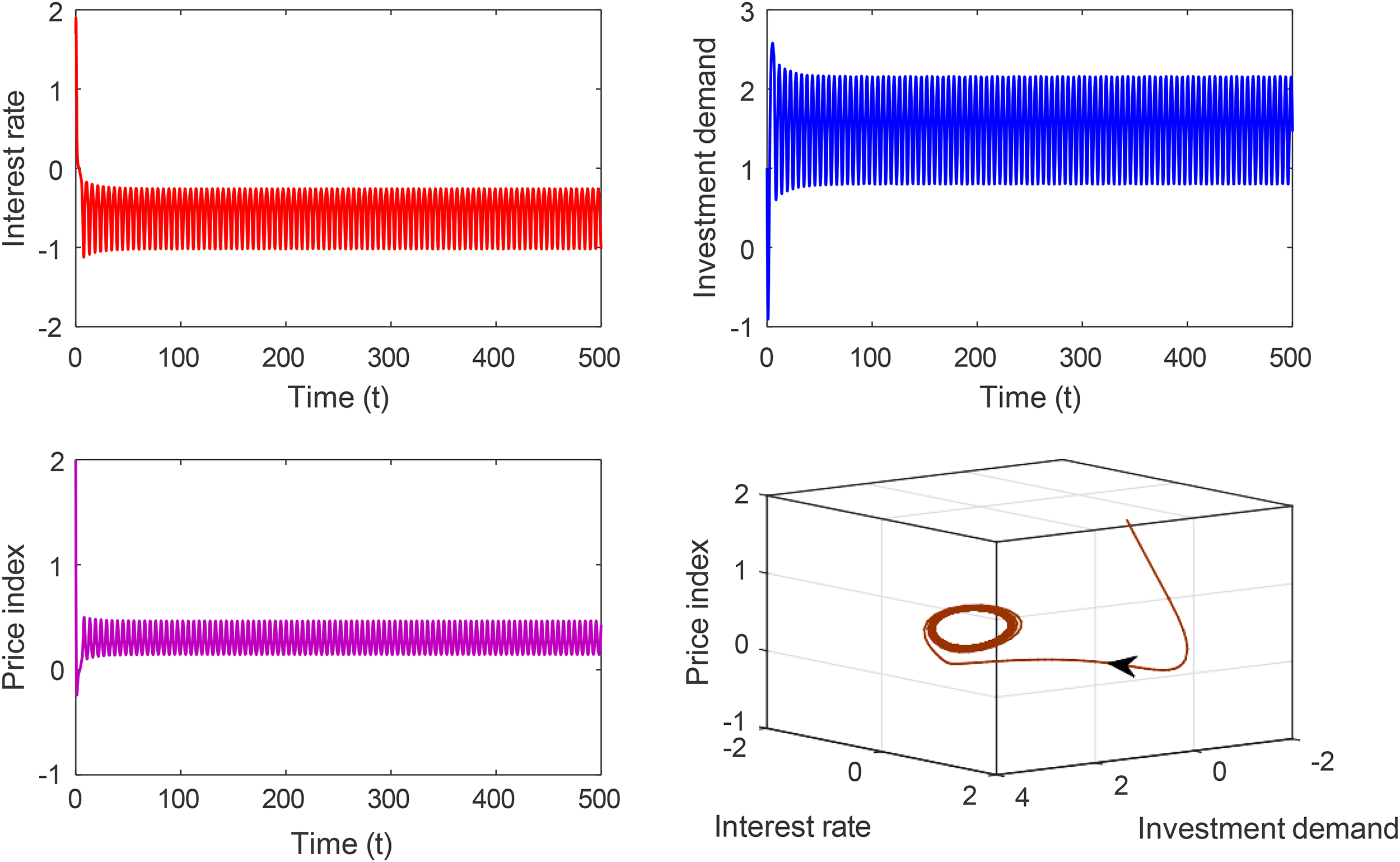

Time series and parametric representation of the solution of the system (2) for

Time series and parametric representation of the solution of the system (2) for

Time series and parametric representation of the solution of the system (2) for

Bifurcation diagram and maximum Lyapunov exponents of the system (2) for the parameter

For

For

For

When the value of debt is less than the threshold level (

The most interesting finding from the simulation is the critical value of debt (

Figure 6 represents the stability curve that predicts a Hopf bifurcation at point

Limit cycle diagram start at Hopf bifurcation point

Adaptive synchronization for the system without time delay

The results of the study in the previous section provided that the financial system will destabilize when debt by governments reaches a crucial level. The policymakers will seek to stabilize the system by implementing new control policies. The newly implemented policies are not always successful and may, instead, cause more unpredictable results. In a bid to correct this risk, policymakers will first work within a synchronized response system, a perfect replica of the actual financial system, to experiment with control inputs prior to implementing them in the real economy. Central banks, for instance, would typically experiment with the effects of changes in monetary policy on a coordinated model in order to forecast their likely effects and risks before implementing them in the real world. This practice offers a safer and more controlled environment for making decisions during times of economic downturns and booms.

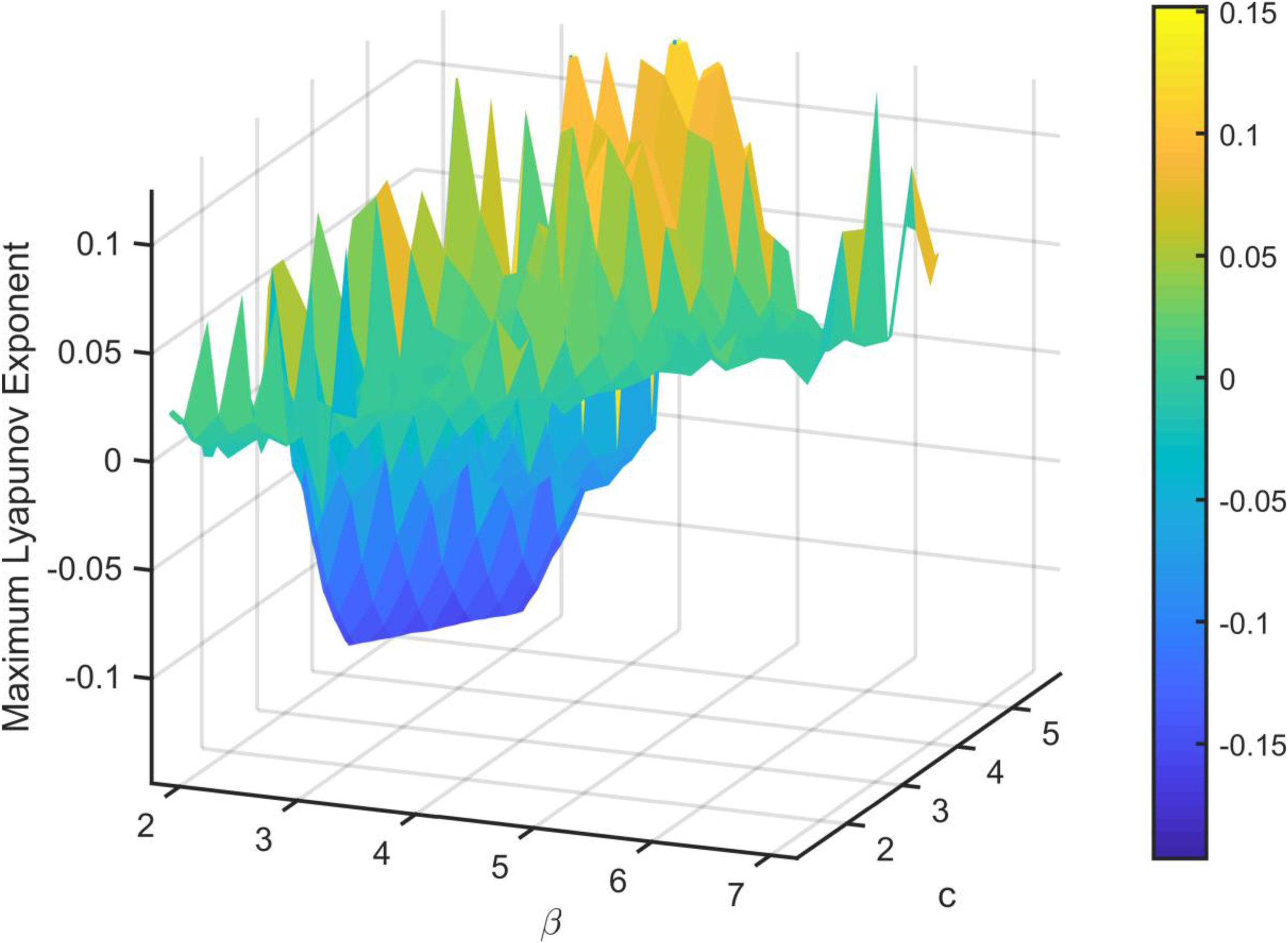

We observed that the system (2) shows chaotic behavior when the debt value is

Figure 7 shows the Lyapunov exponents diagram under the time interval [0, 10000]. Three-dimensional Lyapunov exponent diagram with respect to government debt

The maximum Lyapunov exponents of system (2) related to the parameter

Three-dimensional (3D) maximum lyapunov exponents diagram of the system (2) that correspond to the

The positive Lyapunov exponent indicates that the system exhibits chaotic behavior, meaning that predicting the long-term evolution of this system might be difficult. Small variations in parameters or initial conditions can result in drastically different outcomes, so the dynamical behavior of the system must be taken into account before deciding on some policy or trying to predict.

Based on the model (2) with

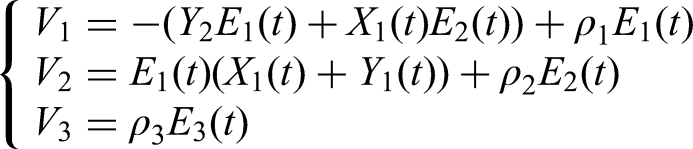

We add three nonlinear controllers:

The error system in synchronization means differences in the behavior between the master and slave systems. By solving the error system, we can develop fine-grained control strategies for the slave system to accurately track the master system, which synchronizes and stabilizes. Basically, the error system is a metric of how successfully the synchronization approach works, which helps in making better improvements and adjustments.

Define the synchronization errors:

We design nonlinear controllers to ensure the error system is asymptotically stable. Choose controllers:

By applying the control laws, we linearize the system (55) around the equilibrium

The matrix

Now, consider the Lyapunov stability function as given by the following:

The time derivative is defined as follows:

This means that for any given initial condition, the error between the systems will decrease exponentially as time progresses, ultimately leading to the synchronization of the two systems.

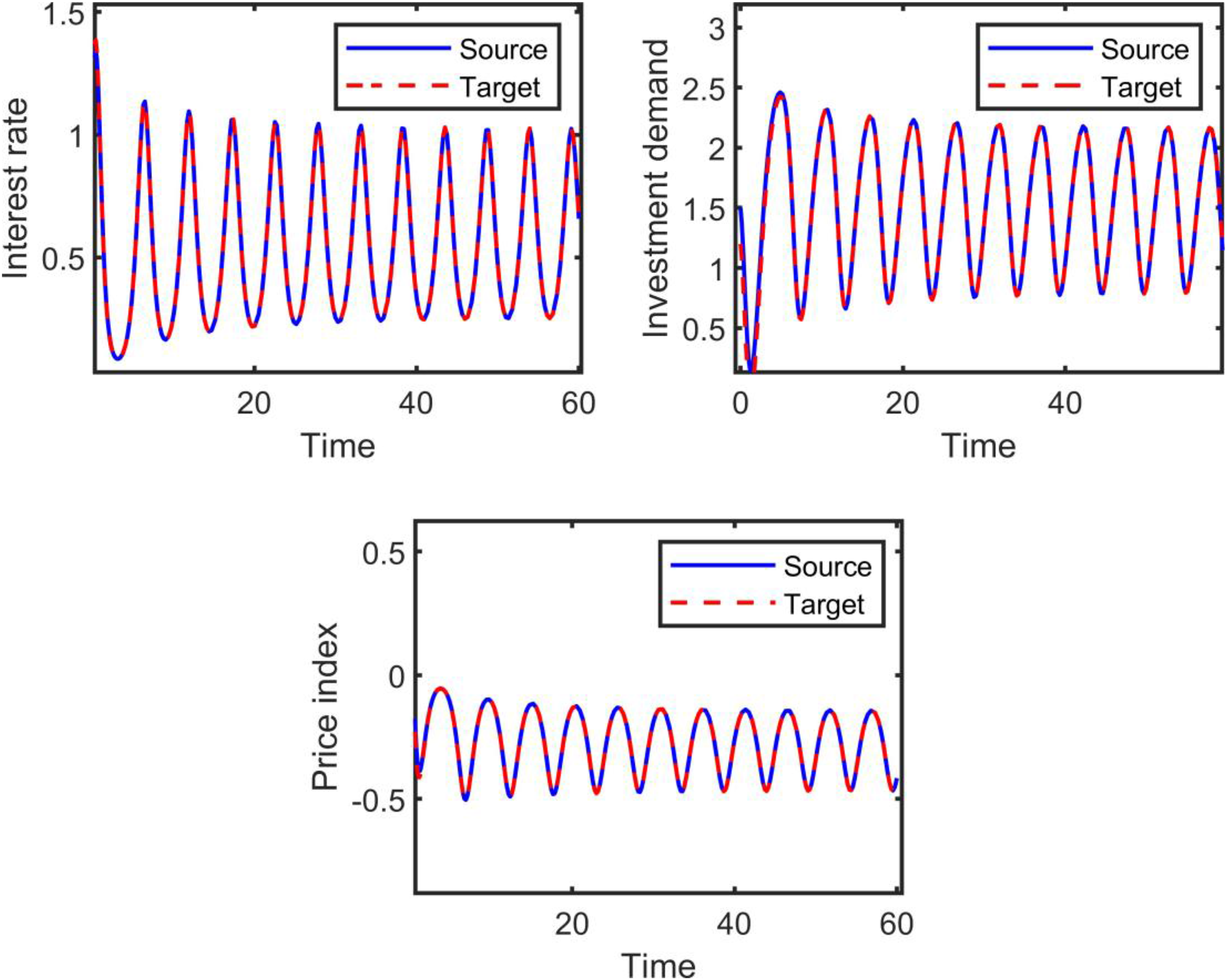

From Figure 9, we can observe that trajectories of the master and slave systems for all variables indeed show converging behavior, with both tracking each other at any given time. Synchronization is further assured by the dynamics of error between these two systems as shown in Figure 10. It is shown that as the error dynamics approach zero over time, both master and slave systems synchronize with each other. The slave system was following exactly the behavior of the master system. The convergence of the trajectories and the decaying error dynamics both validate that our synchronization scheme actually accomplishes making both the master and slave systems behave in a like manner.

Time series diagram of synchronized error signals of the system (55).

Simulations of the system with a time delay

Now we consider the parameter values of the system (2) as

Time series and parametric representation of the solution of the system (2) for

Time series and parametric representation of the solution of the system (2) for

Time series and parametric representation of the solution of the system (2) for

Time series and parametric representation of the solution of the system (2) for

Bifurcation diagram of the system (2) for the time delay parameter

When the time delay in investment demand is less than

In conclusion, the time delay threshold

Synchronization for the system with time delay

In the presence of strong investment demand lags, the financial system can also show unstable or chaotic behavior as a result of time delays in the capital investment process. Such delays also add to the system’s complexity and nonlinearity, and thus the system becomes more vulnerable to policy shocks and external disturbances. Applying new policies to the real system can yield unwanted or unexpected consequences. To do this, policymakers can avail themselves of the synchronization mechanism by building a response system that responds to the dynamics of the real financial system. The synchronized model enjoys the advantage of having a risk-free sandbox in which to experiment and assess the impact of any policy interventions prior to implementing them in the real economy. By seeing how the coordinated system responds to different control inputs, such as fiscal incentives or interest rate changes, decision-makers can tune their actions so that they are more stable and potent in the presence of lagged investment responses.

When the time delay value is

Lyapunov exponents of system (2) related to time delay

Maximum Lyapunov exponents of the system (2) that correspond to the

The master system is governed by the following delay differential equations:

We consider

The error dynamics must be stable at the origin in order to attain synchronization. Taking (60) and subtracting it from (61) yields

We design nonlinear controllers to ensure the error system is asymptotically stable. Choose controllers as follows:

Now, consider Lyapunov stability function as given by the follows:

The time derivative is as follows:

We consider,

The trajectories of the master and slave systems for all variables exhibit convergent behavior, with both systems tracking one another at any given time, as shown in Figure 18. The error dynamics between these two systems, as shown in Figure 19, further ensure synchronization. It is demonstrated that both master and slave systems synchronize with one another as the error dynamics gradually go closer to zero. The fading error dynamics and the convergence of the trajectories both confirm that our synchronization technique successfully achieves similar behavior for both the slave and master systems.

Time series diagram of synchronized error signals of the system (63).

Results and discussions

A stable equilibrium of the system can be interpreted as a stable, well-regulated economy in which macro variables such as the interest rate, the investment demand, and the price index all converge to steady states, delivering long-run sustainable real economic activities. Periodic oscillations correspond to business cycle behavior in which the economy oscillates between expansion and contraction phases, exhibiting recurring motions both in investment and price dynamics. Chaotic solutions correspond to very turbulent, unpredictable, and potentially unstable economic situations, which may be related to financial turbulence, instability, or crisis situations, where small perturbations can cause large and uncertain changes in the economic outcomes.

Our study reveals that the financial system exhibits stability for some values of government debt and investment delay. But as the government debt crosses a certain tipping point, the system undergoes a Hopf bifurcation and becomes unstable or even chaotic. The stability region of government debt is

To solve this instability and chaotic behavior, we applied the synchronization strategies by creating a response system with control variables. The given original system has complex dynamics when debt and delay value cross their critical value. We create a response system that synchronizes with the given system. By introducing control variables, we regulate the dynamics of the response system to be similar to the dynamics of the given system. Through numerical simulations, we validate the stabilization of the system using a synchronization control when government debt is above the critical level or a long-term time delay is imposed. We consider a master–slave system, and through appropriate design of the response system, we demonstrate that policymakers can construct a synchronizing slave response that stabilizes this with respect to the original one. This process of synchronization is referred to as a new policy idea for reducing the negative externalities of pro-cyclical investment demand caused by excessive government debt and time delay, thereby achieving long-term sustainable growth and stability in good policies.

This study has important implications for financial policymakers. The above strategies can be used as a trigger for assessing the probability of instability, the critical values being those of government debt and investment delay. With a grasp of how the burrs work in combination with each other, and by introducing them to suitable synchronization regulators, policymakers can then build policies that can effectively enhance the stability of the financial system and reduce probabilities of spells of chaos.

Limitations and future work

Despite various strengths of this work in dynamics and control of a time-delayed financial system, there are some limitations that deserve to be addressed in the future. While the proposed model provides a tractable 3D ODE framework for analyzing synchronization behavior, we observed that real financial markets are highly complex, heterogeneous, and intrinsically high-dimensional. In reality, market dynamics are influenced by a broader set of interacting macroeconomic and financial variables beyond interest rate, investment demand, and price index. Important factors such as exchange rate movements, unemployment and vacancy rates, and GDP growth reflect labor market conditions, production capacity, and overall macroeconomic performance, all of which can significantly influence system stability. Moreover, sources of uncertainty—including financial shocks, policy interventions, and geopolitical risk—introduce nonlinear, stochastic, and time-varying effects that may disrupt synchronization and even generate regime shifts. These elements are not explicitly incorporated in our present low-dimensional formulation, which therefore represents a simplified and homogeneous approximation of market behavior. As a result, the current model should be interpreted primarily as a theoretical benchmark. Extending the framework to higher-dimensional systems that explicitly incorporate these additional economic factors constitutes an important direction for future research and will help enhance the realism and applicability of the proposed synchronization mechanism.

The proposed synchronization strategies, with and without time delay, demonstrate the feasibility of coordinating the considered financial dynamics within our theoretical framework. However, their applicability to real financial markets is conditional. Synchronization is most likely to generalize to situations where market interactions are sufficiently strong and coordinated, time delays in information transmission and policy response remain within manageable bounds, and the system is dominated by relatively stable macroeconomic regimes. In contrast, the control strategy may fail or become infeasible in highly turbulent or rapidly changing environments, under strong structural heterogeneity across agents and markets, or when delays become large, irregular, or state-dependent. Additionally, sudden shocks, regulatory or institutional constraints, and nonlinear amplification mechanisms may require unrealistically large control inputs to maintain synchronization. These considerations suggest that the proposed mechanisms should be viewed as theoretically informative rather than universally prescriptive, and motivate future work on more robust, heterogeneous, and stochastic control frameworks.

Besides the solutions found in the present work, it is worth noticing that the system may present other qualitative features. For instance, they can exhibit repeating or oscillating behavior in time, which is known as periodic behavior.56,57 They can also be invariant, in the sense that they are confined, or the system flows within certain regions or along certain patterns that are time independent. 58 These properties usually rely on the parameters and the initial conditions of the system. A complete in-depth study of such phenomena is outside the scope of the present; however, our preliminary analysis and exploration suggests that they could happen in certain situations. These periodic and invariant behaviors will be further analyzed in a subsequent study.

In future work the model can be generalized to higher-dimensional systems by including other relevant financial quantities such as government taxation, investor profit margins, foreign direct investment, government consumption, and so on to represent more complex market interdependence. In addition, the system can be generalized to fractional-order derivatives to take into account the presence of memory and hereditary characteristics that usually exist in real financial processes. Such generalizations would reinforce the applicability of the model and yield further insights into stability, chaos control, and synchronization in more realistic economic settings.

Conclusion

In this work, we have developed a financial model consisting of three dynamic variables: interest rates, investment demand, and price indexes, with delayed feedback on investment demand. We have also studied the basic properties of existence, uniqueness, and boundedness of the system. We have found that a higher amount of government debt makes the financial system unstable. Moreover, in the presence of an investment time delay on investment demand, the system loses its stability via a Hopf bifurcation. We examined the behaviors of the system, which are unpredictable and sensitive to the initial conditions. Subsequently, we presented synchronization techniques by taking into account one with and one without time delay. We verified theoretical results through numerical simulations.

The results of this study are important for financial policy and market stability. Analysis of the time-delayed financial system with feedback control shows that a suitable selection of system parameters—especially the feedback gain (k) and delay

Footnotes

Acknowledgements

Not applicable.

Author contributions

AP: conceptualization, methodology, formal analysis, validation, investigation, writing–original draft preparation, and writing–review. KD: conceptualization, software, formal analysis, validation, writing–original draft preparation, writing–review, and editing. HKS: investigation, and writing–review, supervision. LB: software, validation, and writing–original draft preparation.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability statement

Not applicable.