Abstract

Objectives

This paper investigates the role of digital finance in promoting environmental sustainability within a group of 52 developing economies from 2010 to 2019. Specifically, it examines whether digital finance effectively contributes reducing CO2 emissions in these nations.

Methods

This paper is a quantitative study which employs the IV-GMM (instrumental variable generalized methods of moment) approach that tackles any potential endogeneity. Furthermore, to ensure robustness of results, this paper also utilizes different measures of financial development.

Results

Estimation results from this study reveal the presence of inverted U-shaped relationship between digital finance and CO2 emissions. This suggests that the beneficial effects of digital finance may take time to materialize. Additionally, this research also records the presence of the Environmental Kuznets Curve and a significant impact of renewable energy, trade openness, financial development, urbanization, and population on CO2 emissions.

Conclusions

It can be concluded that it may take time for digital finance to become beneficial to the environment. Therefore, in addition to digital finance, countries should also adopt other measures simultaneously (use of renewable energy, combination between digital finance and financial development).

Introduction

The fundamental importance of finance in driving growth has been well-established. It traces back to the original ideas put forth by Bagehot 1 who contended that the UK's financial system, through the mobilization of capital, plays a vital role in fostering and facilitating industrialization within the UK. However, empirical support for the beneficial effect of finance on growth remains inconclusive. Similarly, the influence of finance, as proxied by financial development, on another crucial objective, namely, CO2 emissions, has yielded mixed results. 2

While the effects of finance and financial development have been recorded and widely recognized, albeit with ongoing debates, another facet of finance has recently gained prominence – digital finance. Thanks to the rapid advancements in information and communication technology (ICT), access to finance has become more efficient. Much like traditional finance, digital finance is expected to exert significant and positive effects on economic growth. Moreover, this emerging form of finance is strongly believed to have additional impacts on various aspects of an economy, including the banking sector, financial inclusion, and financial stability. This paper attempts to contribute to the literature about the role of digital finance in promoting environmental sustainability within developing economies. Digital finance, often described as the fusion of traditional financial systems with information and digital technology, is anticipated to bring significant benefits to individuals, households, businesses, governments, and economies.3–5 While this perspective is also supported by Manyika et al., 6 there is scarcity of empirical evidence, with few studies investigating the digital finance CO2 emissions nexus. This manuscript seeks to fill this void in literature.

Regarding carbon emission, it is well-established in the literature that it can inflict serious consequences on various stakeholders. 7 Numerous studies are conducted to study the detrimental effects caused by carbon emissions. For example, Bakry et al. 8 noted severe climate change, higher sea levels, frequent natural disasters, and many others. Nghiem et al. 7 stated that the potential and realized adverse consequences associated with climate change and carbon emissions have prompted governments, scholars, scientists, and other stakeholders to explore solutions to these problems. They argue that a spate of instruments has been proposed, ranging from the use of ICT, the production and consumption of renewable energy to the combination between ICT and financial sector development. Similarly, other scholars also stress the importance of the integration of the digital and energy industries and the facilitation of financial sector,9,10 the use of green finance reform 9 and the implementation of innovation city policy.11,12

With respect to the victims of climate change, developing nations are thought to be key stakeholders in the fight against climate change. Even though developing nations bear smaller responsibility for carbon emission rather than their developed counterparts, the former is particularly vulnerable to these consequences.13,14 In addition to the severity of their direct consequences, climate change and carbon emissions may also exert other serious effects that are harder to notice but equally disastrous. For example, according to the United Nations, if left unmitigated, climate change is likely to incur higher cost of capital and debt repayment obligations by nearly 170 billion USD on developing economies over the next decade. Worse still, Suresh et al. 15 argue that climate change can lead to widespread hunger and poverty across developing economies. However, as these countries usually fall into the groups of low-income and lower-middle income levels, it would be difficult for them to adopt the solutions/approaches mentioned above as these solutions may require huge initial investments and time-consuming.

Another problem facing developing countries is their ever-higher level of (traditional) financial development which may have both advantages and disadvantages. On the one hand, the effects of traditional financial development on the environment remain inconclusive. 16 On the other hand, while expected to significantly contribute to growth, 17 traditional finance may only be beneficial for big corporations, high-income countries or developed regions. On the contrary, it may do more harm than good to less developed economies as it can lead to financial exclusion18,19 especially with respect to small- and medium-sized enterprises (SMEs), rural areas or the underdog. As SMEs account for majority of firms in developing countries, lack of access to finance may hamper the growth and development of these countries, thus making their bad situation even worse. Under this context, digital finance is expected to resolve the dilemma confronted by developing economies in general and traditional finance in particular. 20 By offering financial services for low-income people, SMEs and inaccessible areas, digital finance may fix the shortcomings of traditional finance. 19

Hence, it is natural to expect that digital finance may come as a rescue to these developing economies in their response to both economic and environmental challenges. Therefore, in this paper, the authors decide to include these countries exclusively in the sample rather than considering developed economies or a mix between these two kinds. First, the fact that digital finance may act as a ‘silver bullet’ for developing countries motivates us to include them in the sample and ignore developed economies. As developed economies have been at a higher stage of development and technological progress, their adoption/application of digital finance should have been prolonged, which in turn, leave it easy to make incorrect and misleading conclusions. Furthermore, digital finance data are only available for developing nations while remains unavailable for their developed counterparts. Consequently, this manuscript focuses on the group of developing economies and aim to figure out the role of digital finance in the fight against climate change in these nations. Another significant and practical contribution of this study lies in the fact that it may inform developing economies of the possible, affordable, and timely solutions to their environmental challenges.

By applying the instrumental variable generalized method of moments (IV-GMM) methodology to a panel of 52 developing countries, this study empirically examines the effect of digital finance on emissions. The reduction of CO2 emission aligns with one of the most critical objectives of the United Nations’ Sustainable Development Goals (SDGs), addressing climate change. 2 This study is expected to make several significant contributions to the current literature. To the authors’ best knowledge, this study is among the first attempts to investigate the global level relationship between digital finance and CO2 emissions. Most previous studies, to our knowledge, have primarily focused on China. Finally, the findings and conclusions of this study hold crucial implications for governments, policymakers and businesses, offering insights into the digital finance-CO2 emissions nexus. This can aid governments in formulating and implementing effective policies to achieve SDGs.

Literature review

What is digital finance and why is it important?

Digital finance gained significant attention, particularly with the onset of the 4th Industrial Revolution. 21 The current 4th Industrial Revolution, characterized by the convergence of digital technologies, the Internet of Things, and other advancements, has accelerated the transformation of financial services. Consequently, digital finance has emerged as a significant field within the financial sector in recent years. Various authors in recent literature refer to “digital finance” as the use of digital technology, like ICT, to provide and access to financial services and products. It contains a wide range of financial activities, including mobile banking, online payments, digital wallets, peer-to-peer lending, and various other financial transactions conducted through digital platforms and electronic devices. For example, Zhao et al. 5 defines digital finance as the payment, investment, financing, and other financial services jointly offered by Internet companies and traditional financial service providers. In their studies, Wang et al. 3 and Chang et al. 4 regard digital finance as the result of the integration between traditional financial system and digital-information technology. Wan et al. 21 consider digital finance as financial innovation driven and facilitated by state-of-the-art ICT with finance acting as the core and ICT providing the means. Finally, Wang et al. 3 regard digital finance and digital finance inclusion as having the same meaning. Consequently, it becomes evident that digital finance entails delivering financial services through ICT tools, simplifying access and utilization of financial services for individuals and other end users.

The significance of digital finance becomes evident when considering its potential impact. Despite ongoing debates among researchers and policymakers, the reach of digital finance is extensive. Primarily, it has the capacity to sustain and stimulate economic growth. Through the supply of financial products/services to individuals and, notably, SMEs, digital finance enhances financial accessibility, thereby contributing to gross domestic product

Furthermore, digital finance can also lead to greater financial inclusion 22 which is confirmed to bring about other significant benefits (such as facilitation of SDGs, greater financial stability and higher economic growth). Thirdly, digital finance may help alleviate financial constraints and the problem of asymmetric information in financial markets,4,21 thus boosting efficiency and improving transparency in the financial sector in general and in the banking industry in particular.3,21 Through the provision of accessible and affordable financial services and products to millions of poor customers, digital finance can greatly improve the life of these people. Digital finance may also offer certain benefits for banks.22,23 Fourthly, digital finance is expected to generate more tax revenues for governments.6,22 Finally, digital finance may prove helpful for firms as it can boost firms’ financing efficiency. 4

The positive impact of digital finance does not necessarily limit to the above-mentioned target beneficiaries. Specifically, digital finance can help farmers reduce their time and costs searching and gathering information, thus mitigating credit constraints faced by farmers as well as increasing credit availability to them. Moreover, digital finance is able to provide financial services to remote areas at lower costs. 5 Last, but not least, digital finance is believed to provide other major benefits to individuals and firms alike. These benefits, to name but a few, include greater transparency in the financial system, better control of personal finance, faster financial decision-making and more convenient financial transactions as well as lower risks of firms going bankrupt.22,24

The digital finance-CO2 emissions nexus

As the effects of digital finance have been confirmed to be significant, far-and-wide, it is not unreasonable to expect that digital finance can exercise considerable influence on environmental problems especially CO2 emissions. Usually regarded as the combination and/or integration of ICT and financial services, digital finance is inherited with properties of both ICT and traditional finance. ICT may have both increasing or dampening effects on energy consumption and therefore, CO2 emissions.25–32 On the one hand, ICT can release beneficial impacts on the environment through several mechanisms: (1) enhancement of energy efficiency and (2) reduction of energy consumption which in turn, may lower emissions and maintain economic growth.28,32 Better still, ICT can also facilitate energy conservation/preservation, develop green production and manufacturing processes, encourage renewable energy production and consumption, thus improving environmental quality and foster sustainable development. 7 On the other hand, ICT may also damage the environment as the production and usage of ICT products are environmental-unfriendly and energy-intensive which may do more harm than good to environmental protection.7,30 The empirical literature also records a significant (yet inconclusive) relationship between ICT and CO2 emissions.25–32

As the effects of ICT on carbon emissions have been confirmed in the literature, it is natural to expect that the combination/integration of ICT into other areas/industries/products should also have similar significant impact on emissions. Among these areas/products, digital finance – the provision of financial services through technological applications – is believed to exert substantial effects on CO2 emissions in particular and in the fight against climate change in general. However, as this area has only come to prominence recently, the literature on digital finance-emissions nexus has been scant and only surged recently, especially over the past 2–3 years.

Bu et al. 33 also lists several channels through which digital finance may affect emissions. On the one hand, digital finance can help reduce emissions and protect the environment in the following ways. First, through its innovative approaches to financial resource allocation, digital finance may boost energy efficiency through the correction of financial distortions which in turn, lower emissions. 34 Another channel that digital finance can affect emission is through the removal of financial constraints: by lowering business costs (including financing costs, labour costs), digital finance may encourage energy conversion/saving and therefore, indirectly lead to lower emissions.35,36 The last way that digital finance can assist in mitigating emissions is through the facilitation and implementation of green finance practices/projects, thus trimming down emissions. 37 However, on the other hand, digital finance can also result in several negative consequences for the environment. The first negative mechanism may exist when corporate borrowers make use of the easier access to finance for industrial production/operations or individual consumers increase their consumption of energy-intensive products.38,39

While digital finance remains a relatively new field, the empirical literature on it has been burgeoning with various studies examining the effects of digital finance at different levels. At the international level, Hossain et al. 40 confirm that digital finance can spur green innovation. At the country level, digital finance is capable of triggering technology spillovers and diffusion which in turn, can lower emissions. 41 Better still, digital finance is also found to boost China's agricultural green total factor productivity and green total factor energy efficiency.19,42,43 At the firm-level, digital finance can help firms improve their environmental performance and green investment; boost firms’ ESG performance and trim down their financial constraints; enhance their innovation efficiency; industrial structure upgrading.44–49

Regarding the digital finance-CO2 emissions nexus, there have been few papers examining this relationship. However, the majority of studies focus on China using prefecture-level city data.21,50–53 Meanwhile, empirical studies on digital finance and CO2 emissions using country-level data are strikingly limited. To the best of the authors’ knowledge, this study is the first to examine the relationship between digital finance-CO2 emissions at a global level. There are several reasons motivating us to conduct a global level study rather than a domestic level research. First, as mentioned in the main manuscript, all of the studies on the digital finance-carbon emissions nexus focus only on China. Digital finance in these studies is measured using Peking University's Digital Financial Inclusion Index of China. While we totally trust the high quality and accuracy of this database, it only reflects the level of digital finance in China and overlooks digital finance in other countries. As a result, all current studies can only reflect the impact of digital finance on carbon emissions in China – one of world's largest carbon emitters while cannot inform us anything of the potential benefits (and costs) associated with digital finance in other developing economies. Therefore, to uncover the true impact of digital finance in developing economies, provide further insights into its advantages and disadvantages as well as create a research paper with broader impact, we decided to choose a global sample.

Second, this study employs a group of developing economies which in turn, allows us to incorporate economic integration (represented by trade openness) to see whether trade help these countries in the fight against climate change. Empirical results also confirm that trade has a significant and increasing impact on carbon emissions, implying that these developing nations are confronted with a dilemma between economic growth and environmental protection. A single country research using multi-city data (such as in the case of China) cannot reveal the true impact of economic integration.

Third, this study also utilizes the IMF's global financial development index (which provides detailed information on different aspects of financial development: financial institution access, financial institution depth and financial efficiency depth). The use of these indices offers closer insights into the role of financial institutions and digital finance in the fight against climate change which a single country research will fall short of.

Data description and model specification

Data description

This paper employs a dataset for 52 countries covering the period 2010–2019. The selection of these countries is based on the underlying reason that sufficient data for digital finance are only available for these selected countries. Moreover, these 52 nations are either developing or emerging market, implying certain similarities among them such as omitting high levels of CO2 emissions, and their financial markets are believed to be under-developed, compared with other developed nations. These characteristics signal that they are also desperately seeking for new engines of growth. These reasons further strengthen our motivations to clarify the role of digital finance in these countries. As a result, this paper aims to empirically examine the impact of digital finance on CO2 emissions in these 52 countries.

Variable selection

Digital finance and CO2 emissions

The dependent variable is carbon emissions (measured as kg per 2015 US$ of GDP) extracted from Our World in Data. While there are several types of greenhouse gas emissions, CO2 is usually employed in empirical studies owing to its potential disastrous consequences. 8 Furthermore, even though there has been a reduction in CO2 emissions due to the COVID-19 pandemic 54 and the Russia-Ukraine war, 55 the level of CO2 emissions has soared again, threatening the attainment of SDGs and human's well-being. Therefore, this paper employs CO2 emissions rather than other indicators as the dependent variable.

Regarding the main variable of interests, digital finance, as Ren et al.

56

argue, mobile payment stands at the core of digital finance. They also posit that the most important benefit of digital finance is its easy and widespread availability for people. Therefore, in this study, digital finance is measured using two indices for mobile payment: number of mobile money transactions per 1000 adults

The remaining control variables include real GDP per capita growth, population, urbanization, trade openness, consumption of renewable energy (World Bank's World Development Indicators), different proxies for financial development (IMF's Financial Assessment Survey-FAS) and electric power consumption (from Our World in Data). Table 1 provided detailed descriptions of the aforementioned variables and their respective sources. All variables are expressed in natural logarithmic form.

Description of variables.

Note: All the variables are expressed in natural logarithmic form. This study covers sample from 52 countries including: Albania, Angola, Argentina, Armenia, Bangladesh, Benin, Bolivia, Botswana, Burkina Faso, Cambodia, Cameroon, Chad, Congo Rep, Cote d'Ivoire, Egypt, Eswatini, Fiji, Ghana, Guinea-Bissau, Haiti, Hungary, India, Indonesia, Jordan, Kenya, Lesotho, Liberia, Madagascar, Malaysia, Mali, Mauritius, Mozambique, Myanmar, Namibia, Niger, Nigeria, Pakistan, Paraguay, Philippines, Qatar, Romania, Rwanda, Samoa, Senegal, Seychelles, Solomon Islands, Sudan, Thailand, Togo, Tonga, Uganda, Zambia.

GDP and CO2 emissions

Unlike the digital finance-CO2 emissions nexus where the literature is scant (theoretical and empirical alike), the relationship between economic growth and carbon emissions is well-established in the literature with inconclusive empirical evidence. Lee and Brahmasrene 57 argue that there is a strong association between economic growth and specialized industry sectors. The latter, in turn, is often credited with large volume of CO2 emissions. Therefore, economic growth can be a strong driver of CO2 emissions. The relationship between economic growth and CO2 emissions is also labelled the Environmental Kuznets Curve (EKC) in which the relationship between growth and CO2 emissions resembles an inverted U-shaped curve.

Developed by Grossman and Krueger, 58 the EKC depicts that environmental degradation initially increases as income grows higher. After income reaches a certain level, the positive link between income and environmental quality would be reversed, producing an inverted U-shape of the EKC. The EKC presence is well supported in existing literature.59–62

However, the literature also records a strong association between growth and energy consumption 59 as well as between energy consumption and carbon emissions. 63 Therefore, in later studies, scholars usually employ a combination of them (together with other controls such as trade openness, population or urbanization) in a unified framework to verify the relationship among them. The current study will also adopt this approach to exploring the effect of digital finance and other important controls on carbon emissions.

Renewable energy and CO2 emissions

Similar to the GDP growth, the relationship between energy consumption and CO2 emissions is also well-documented in the literature with most studies confirming the existence of a positive relationship between energy consumption and CO2 emissions.28,29,62,64

However, thanks to technological progress and emergence of alternative energy sources, researchers have paid special attention to the role of renewable energy – a field coming to prominence over the last several decades. Renewable energy is usually described as energy produced from renewable/non-exhaustible sources such as wind, geothermal, solar, tide and wave, wood, biomass and waste which in turn, making it inherit desirable properties such as clean, green, safe and inexhaustible. 65 It has been widely agreed that the catastrophic and debilitating effects produced by climate change have caused relevant authorities to facilitate a transition from non-renewable energy towards renewable energy. 66 While being regarded as having many beneficial effects such as higher economic growth and job creations,66–69 the potential of reducing CO2 emissions makes renewable energy becomes increasingly important. 65

The beneficial impact of renewable energy on cutting CO2 emissions has been confirmed in the literature with overwhelming empirical support. Khattak et al. 70 find that renewable energy exerts a significant and negative impact on CO2 emissions in BRIC countries from 1980 to 2016. Hanif et al. 71 also document the dampening and significant influence that renewable energy has on CO2 emissions in 25 Asian economies from 1990 to 2015. Other studies reaffirming strong support to the significant role of renewable energy in mitigating CO2 emissions.72–75

To sum up, while the effects of (total/general) energy consumption on CO2 emissions are usually positive (more energy consumption leads to environmental degradation), the impact of renewable energy consumption could help reverse the situation. This study will employ both variables to empirically investigate the impact of both types of energy on CO2 emissions to make proper implications and recommendations.

Other control variables

To avoid problems caused by omission of variables, this study also makes use of several controls including financial development, trade openness, urbanization, and population.

Regarding financial development, this variable is often credited with great benefits to the environment such as large-scale and environmental-friendly investments, acceleration of research and development (R&D) activities, stronger implementation of environmental regulations or encouragement of renewable energy adoption and consumption.76,77 According to Charfeddine and Khediri, 78 financial development may release two different, contradictory effects on CO2 emissions. On the one hand, through the funding of R&D projects, the facilitation of state-of-the-art and environmental-friendly technologies, financial development can make significant contributions to lessening CO2 emissions. On the other hand, greater financial development could result in more manufacturing activities which in turn, can lead to higher CO2 emissions. Empirical evidence also gives mixed results regarding the financial development-CO2 emissions nexus. While Yuxiang and Chen, 76 Kim and Park, 79 Le et al., 80 and Usman and Hammar 81 document a significant and negative impact of financial development on CO2 emissions, Zeraibi et al. 82 and Nasreen et al. 16 record the opposite. Therefore, through the examination of the impact of financial development on CO2 emissions, this paper aims to clarify the role of financial development on CO2 emissions in developing countries and therefore, enrich the literature.

In addition to financial development, international trade is also expected to make significant contributions to ‘greening’ the economy thanks to the encouragement and facilitation of spillover effects and technology transfers, satisfying the energy demand. 45 Similarly, population and urbanization are believed to strongly affect CO2 emissions especially in developing economies. Therefore, this paper will incorporate all these variables.

Model specification

Based on previous studies,21,30,83,84 the following linear model to be estimated is specified as follows:

While equation (1) specifies a model with common variables in the literature, it ignores the issue of nonlinearities associated with CO2 emissions model. Therefore, equations (2) and (3) below include not only the square of real GDP per capita but also the square of digital finance to see the shape of the relationship between digital finance and carbon emissions.

Additionally, this paper investigates the impact of the financial institutions’ accessibility, depth, and efficiency on carbon emissions. In doing so, equation (3) is re-estimated by replacing the financial development

As it could be difficult to figure out an appropriate instrument, 89 this paper uses lags of digital finance as instruments for digital finance. The validity of instruments is verified by the Cragg-Donald/Kleibergen-Paap F-statistics and the Hansen J tests.

For robustness checking, this study examines the sensitivity of the regression results to variable measurement. In achieving this, all models are re-estimated where the proxy for the digital finance variable, that is, the number of mobile money transactions per 1000 adults

Results and discussions

Descriptive statistics

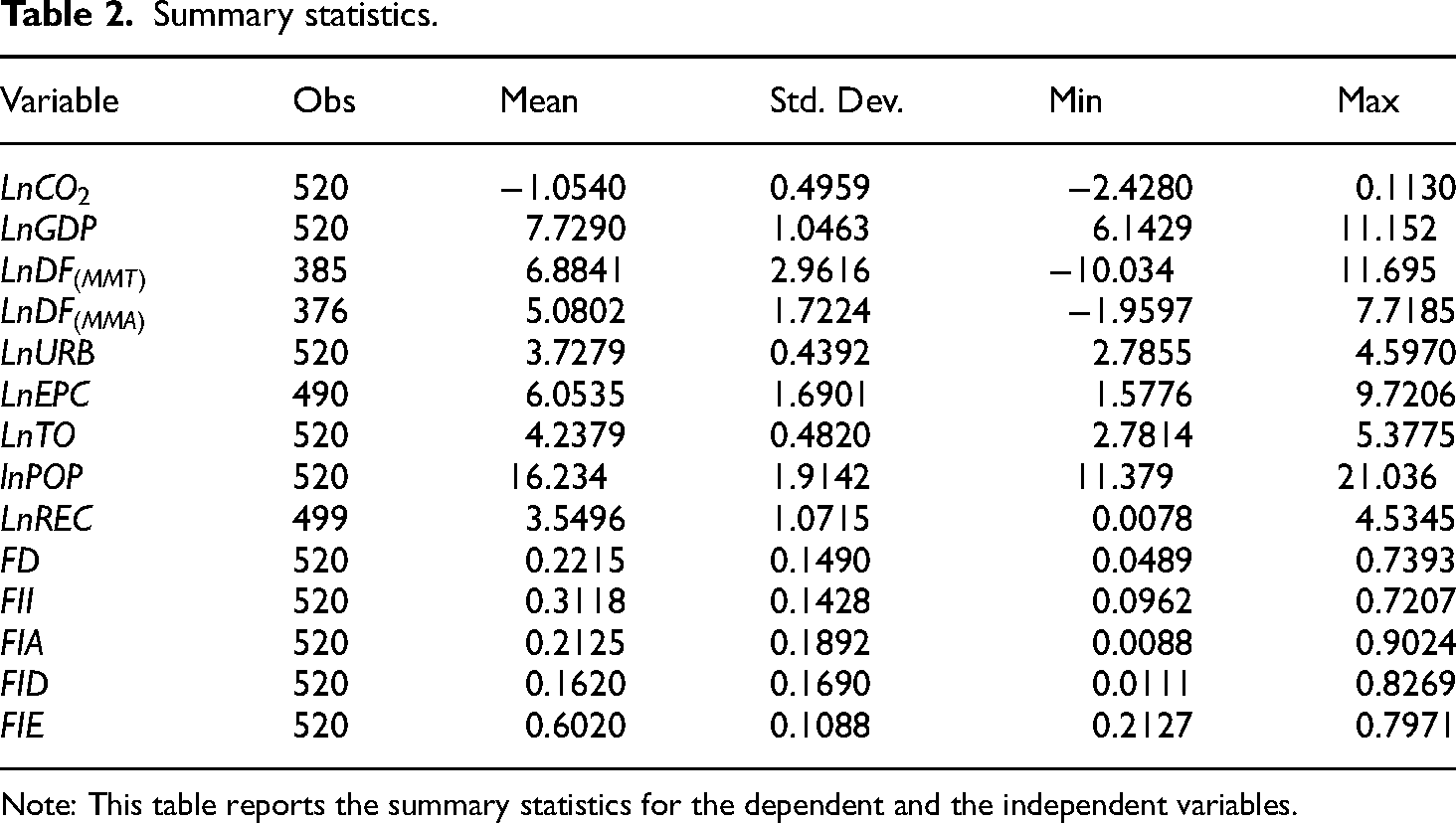

Descriptive statistics of variables used in in this paper are presented in Table 2. Based on results from Table 2, the dependent variable, CO2 emissions (measured as kg per 2015 US$ of GDP), has the mean value of −1.05 and standard deviation of nearly 0.5, indicating a small variation among the 52 countries in our sample. Similarly, independent variables such as digital finance (measured as the number of mobile money transactions per 1000 adults or the log of registered mobile money account per 1000 adults), economic growth (real GDP per capita), renewable energy (Renewable Energy consumption per capita (% of total energy consumption) also display relatively narrow variations among countries.

Summary statistics.

Note: This table reports the summary statistics for the dependent and the independent variables.

Table 3 displays the pair-wise correlation between all variables. In general, there does not seem to be any concerns about high correlations between the independent variables. None of the correlations among explanatory variables are above 0.79 (except between overall financial development index

Correlation matrix of independent variables.

Empirical results

After examining the descriptive statistics and stationarity of variables, the next step is to estimate our models. The econometric method used in this paper is IV-GMM. Estimation results are given in Table 4. It should be noted that in Table 4, Models (1–13) are based on equations (1)–(13). The main independent variable of interests, digital finance (measured by number of mobile transactions per 1000 adults), has an overall unexpected positive impact on CO2 emissions. This variable is significant in almost all models, except models (1) and (2). However, when the square of digital finance is included, the digital finance itself still keeps its positive sign but it becomes highly significant, meaning that higher digital finance may lead to more CO2 emissions rather than lowering it. Generally, when number of mobile money transactions rises by 1%, CO2 emissions may hike by 9–24%. Meanwhile, the square of digital finance is negative and highly significant.

Digital finance (number of mobile money transactions per 1000 adults) and carbon emission.

Note: LM statistics is the Kleibergen-Paap LM statistic testing the null hypothesis that the model is under-identification. LM JP is the p-value of the Kleibergen-Paap LM statistic. Hansen J is Hansen J-statistics which tests over-identifying restrictions with a null hypothesis that the instruments used are valid instruments; Hansen JP is the p-value of Hansen J-statistics. F-statistics is the Cragg-Donald Wald F-statistics for weak instrument identification, with critical values varying between 7.25 and 19.93. The probability value for the Hansen J-statistics suggests that instruments are not over-identified while the F-statistics also suggests the instrument are not weak. The numbers in the parentheses are the heteroscedasticity robust standard errors. *, ** and *** indicate significance at the 10%, 5% and 1% levels, respectively.

The next independent variable of interest, real GDP per capita, also displays similar patterns. This variable is (highly) significant and positive, supporting the hypothesis that higher GDP growth is associated with more CO2 emissions. However, when the square of GDP is included, this new variable is highly significant and negative,

The next two variables of interests, namely total energy consumption and renewable energy consumption, display expected results. While total energy consumption has a positive effect on emissions (insignificant in majority of models), the impact of renewable energy consumption is highly significant and negative. Next, two variables closely associated with the development process, namely urbanization and population, are both positive and significant, probably suggesting that higher population and higher urbanization rate are harmful to the environment. Specifically, the urbanization rate is significant and positive across models, indicating that when this variable increases by 1%, it would result in around 0.14–0.28% more CO2 emissions. Like urbanization, population exerts a positive and significant effect on emissions across models (except in the nonlinear model (1) where it is insignificant). Results from Table 4 imply that one percentage increase in total population is associated with about 0.03–0.13% more CO2 emissions discharged into the environment.

Trade openness exerts a highly significant and positive impact on carbon emissions, implying that as these countries integrate more into the world economy, they will discharge more CO2 emissions into the environment.

The effects of financial development on emissions also reveal interesting findings. In the first three models, financial development is represented by the overall financial development index which exerts a positive and significant impact on CO2 emissions. From Table 4, when the overall financial development increases by 1%, CO2 emissions would see an increase of about 0.34%. From Model (4) to Model (7), the overall financial development index is replaced by its sub-components, namely the financial institution index, the financial institution access index, the financial institution depth index and the financial institution efficiency index. Estimated coefficients of these variables are also positive and significant, further corroborating the adverse effects of financial development on CO2 emissions. Finally, with respect to the validity of instruments used in all models, the p-value of the Hansen test indicates that the instruments used are not over-identified while results from the Cragg-Donald/Kleibergen-Paap F-statistics suggest that instruments are not weak.

Discussion of results, policy implications, limitations and future studies

Estimation results from GMM model (reported in Table 4) are note-worthy. Despite the fact that the digital finance variable (at level) exerts a significant and unexpected, undesirable positive impact on carbon emissions, its square deserves special attention here: this variable is highly significant and negative, implying that the relationship between digital finance and CO2 emissions follows an inverted U-shaped curve, lending support to the view that digital finance can reduce carbon emissions. The significance of the square of digital finance also confirms the nonlinearity in the relationship between digital finance and carbon emissions. In other words, the impact of digital finance on CO2 emissions may not always be monotonic. Therefore, the effects of digital finance on CO2 emissions resemble an inverted U-shaped curve for these developing and emerging economies. The inverted U-shape of the impact of digital finance indicates that if these developing and emerging economies want to reap environmental benefits from digital finance, the number of mobile money transactions must cross a certain threshold for digital finance to reduce CO2 emissions. Therefore, these developing countries are strongly advised to adopt, advance and accelerate their digital finance system in order to reap its full benefits. A pre-requisite for digital finance is the adoption, implementation and installation of ICT (such as the Internet, mobile phone) and other technology infrastructure. Without this pre-requisite condition, full benefits and potentials of digital finance cannot be unleased.

The variables real GDP and real GDP squared also follow similar patterns: the positive impact of GDP and negative impact of squared GDP on CO2 emissions implies that GDP may help mitigate carbon emissions when the level of GDP crosses a certain threshold. These results also verify the existence of the EKC and indicate that for these 52 developing and emerging economies, things may get worse before getting better. Therefore, these countries must not be discouraged by the seemingly initial adverse effects on CO2 emissions. The nonlinear, inverted U-shaped relationship between GDP and carbon emissions also implies that developing economies may need more money to invest in their science and technology especially digital finance and its infrastructure to reduce carbon emissions.

The expected positive impact of total energy consumption (insignificant in majority of models) and expected negative (dampening) effect of renewable energy consumption on carbon emissions further strengthens the role of the former in combatting climate change and reducing carbon emissions. The positive but insignificant role of total energy consumption on CO2 emissions may also signal that in these 52 emerging and developing economies in the sample, there is a transition from fossil fuel to renewable sources. As (the transition towards) renewable energy may provide numerous additional benefits, this result calls on policymakers, businesses, banks to encourage renewable energy production and consumption. The expected, contradictory effects of total energy consumption and renewable energy consumption once again emphasize the indispensable nature of the energy transition process. Therefore, governments in these 52 countries are strongly advised to adopt measures to encourage local governments, firms and individuals to take responsible actions.

Variables representing the development process, namely urbanization and population, display expected results. Specifically, urbanization releases a significant and positive impact on emissions. When this variable increases by 1%, it would result in around 0.14–0.28% more CO2 emissions. The positive sign and significance of urbanization is also confirmed by previous studies.90–92 In their study, Acheampong et al. 92 posit that greater pace of urbanization may result in higher demand for transportation, more urban infrastructure, increased traffic congestion, thus making urban areas resource-intensive and therefore, increase CO2 emissions. Therefore, results from the effects of urbanization and population on CO2 emissions point out that these 52 economies should carry out appropriate policies to contain any substantial increase in population and urbanization. As an unplanned urbanization process (urban sprawl) may do more harm than good to the environment and people's well-being, 12 relevant authorities are recommended to perform urban planning and urbanization process in a very careful, meticulous manner.

The fact that trade openness exerts a significant and positive (increasing) impact on carbon emissions does not come as a surprise. While this effect seems counter-intuitive, it is in line with previous studies.92,93 A possible explanation to this result lies in the fact that trade is likely to boost economic growth which in turn, induce higher CO2 emissions, reflecting the scale effect of trade. 92 On top of that, the authors also propose the hypothesis that as 52 countries included in the sample are all developing countries, they may inherit outdated technologies from other countries which may hurt rather than heal the environment. Furthermore, as these countries mostly come from lower-middle income group, high income nations may export dirty technologies as well as discard their e-waste to these countries, resulting in higher CO2 emissions. These potential reasons indicate that these developing economies must be vigilant especially in their international trade activities to avoid importing ‘brown’ technologies.

The effects of financial development on CO2 emissions also reveal interesting findings. In the first three models, financial development is represented by the overall financial development index which exerts a positive and significant impact on CO2 emissions. From Table 4, when the overall financial development increases by 1%, CO2 emissions would see an increase of about 0.34%. From Model (4) to Model (7), the overall financial development index is replaced by its sub-components, namely the financial institution index, the financial institution access index, the financial institution depth index and the financial institution efficiency index. Estimated coefficients of these variables are also positive and significant, further corroborating the adverse effects of financial development on CO2 emissions. The positive and significant impact of financial development (no matter how it is measured) also signal that in these developing and emerging countries, financial institutions may either be reluctant or unable to encourage firms to adopt environmental projects. Consequently, authorities are encouraged to take actions to suggest or even request financial institutions to impose stricter rules on these financial institutions.

As financial development in general and financial institutions in particular, in developing economies, prove counter-productive in reducing CO2 emissions, it may also be interesting to see whether the introduction of digital finance can help mitigate the effects. To verify this hypothesis, the authors include the interaction term between digital finance and financial development (Model (8)) as well as between digital finance and financial institutions (Models (10–13)). Results confirm the moderating role of digital finance towards financial development in general and financial institutions in particular. In other words, digital finance will moderate financial development and financial institutions to mitigate CO2 emissions. A possible explanation for this phenomenon is that the integration/combination between ICT and traditional finance may help reduce transportation demand, thus reducing CO2 emissions.

The above-mentioned findings offer several importance policy implications. The numerous effects of digital finance imply that this new form of finance could be a potential solution to the environmental problems facing people. Therefore, it is imperative that governments implement policies aimed at facilitating and accelerating the adoption and usage of digital finance as well as providing adequate infrastructure for its development. The fact that the interaction between financial development and digital finance has a significant and dampening impact on CO2 emissions also suggest that policymakers should carry out measures to advance the integration of/interaction between these areas to compensate for the detrimental effects of financial development as well as the long-awaited fruits of digital finance in mitigating CO2 emissions. Furthermore, the benefit of renewable energy also suggests that governments should speed up the transition towards renewable energy which in turn, may play an essential role in mitigating CO2 emissions and bring about additional benefits. Finally, the positive and significant impact of urbanization and population indicates that governments in these countries should adopt appropriate measures to slow down the pace of urbanization and growth rate of population.

While the analysis in this study is performed with great care, it still suffers from certain drawbacks. For example, at the time of data collection, the authors can only cover the period from 2010 to 2019 – which could be relatively outdated. Therefore, future studies may employ a more up-to-date dataset to further confirm or reject the impact of digital finance on the environment. Furthermore, as digital finance data are only available for these 52 developing economies, the impact of digital finance on other economies (developed and developing alike) remains unclear. Therefore, scholars may want to examine the impact of digital finance on carbon emissions in other economies when more data for more countries are available. In addition to expanding the scope of country and time range, future studies may also employ other estimation methods such as vector error correction model or autoregressive distributed lags models to confirm whether digital finance has long-run and/or short-run impacts on carbon emissions (and whether the impact is symmetric or asymmetric). Scholars may also want to see whether the impact of digital finance on the environment is subject to the income threshold. Finally, it should be noted that the mediating variables establish relationship and adoption of green technologies and practices. Digital finance acts as a tool for individuals and businesses to invest in environmentally friendly solutions. For example, digital finance platforms can provide financing for energy-efficient appliances, electric vehicles, and renewable energy projects. This mediation effect shows that while digital finance itself does not directly reduce emissions, it creates a favourable environment for sustainable investments. Thus, digital finance reduces CO2 emissions by enhancing financial inclusion and efficiency, thereby enabling greater adoption of green technologies and practices. The mediating variable of green technology adoption is crucial in understanding the full impact of digital finance on emissions reduction requires detailed study which is work in progress for future research. All these potential studies may provide policymakers with adequate information so they can make well-informed decisions.

Robustness check

To test for the robustness of results, this study also re-estimates equations (1)–(13) where digital finance is represented by the number of registered mobile money accounts per 1000 adults. Results are presented in Table 5 and display similar patterns when digital finance is proxied by the number of mobile money transactions per 1000 adults. Therefore, it can be concluded that in developing countries, digital finance may help mitigate carbon emissions, thus corroborating other measures (such as the use of renewable energy) and accelerating the transition towards net-zero emissions. Hence, the use of digital finance should be encouraged and facilitated in the fight against climate change.

Robustness check – digital finance (number of registered mobile money accounts per 1000 adults) and carbon emission.

Note: LM statistics is the Kleibergen-Paap LM statistic testing the null hypothesis that the model is under-identification. LM JP is the p-value of the Kleibergen-Paap LM statistic. Hansen J is Hansen J-statistics which tests over-identifying restrictions with a null hypothesis that the instruments used are valid instruments; Hansen JP is the p-value of Hansen J-statistics. F-statistics is the Cragg-Donald Wald F-statistics for weak instrument identification, with critical values varying between 7.25 and 19.93. The probability value for the Hansen J-statistics suggests that instruments are not over-identified while the F-statistics also suggests the instruments are not weak. The numbers in the parentheses are the heteroscedasticity robust standard errors. *, **, and *** indicate significance at the 10%, 5% and 1% levels, respectively.

Conclusions

This paper investigates the impact of digital finance on CO2 emissions – a major culprit of climate change in 52 developing countries from 2010 to 2018. Estimation results confirm the significant and nonlinear relationship between digital finance and emissions. In addition to the direct, inhibitory effects on emissions, digital finance may also exert indirect effects. The interaction between digital finance and financial development indices confirms that digital finance can moderate the adverse effects of financial development on CO2 emissions.

Findings from this study also confirm the existence of the EKC, suggesting that these countries may need to reach a certain level of income before their income can help reduce CO2 emissions. This study asserts the critical role of renewable energy in mitigating CO2 emissions. Finally, trade is confirmed to be detrimental to environmental quality, implying that these 52 countries may run the risk of becoming the disposal site of advanced economies.

Footnotes

Acknowledgements

The authors would like to sincerely thank participants in the International Conference on Business and Finance 2023 (ICBF) for their valuable comments and feedback.

Author contributions

Walid Bakry: conceptualization, data curation, methodology, software, formal analysis, roles/writing – original draft; writing – review & editing. Xuan-Hoa Nghiem: conceptualization, data curation, methodology, software, formal analysis, roles/writing – original draft; writing – review & editing. Muhammad Ishaq Bhatti: conceptualization, data curation, methodology, software, formal analysis, roles/Writing – original draft; writing – review & editing. Somar Al-Mohamad: conceptualization, data curation, methodology, software, formal analysis, roles/writing – original draft; writing – review & editing. Lianbiao Cui conceptualization, data curation, methodology, software, formal analysis, roles/writing – original draft; writing – review & editing.

Availability of data and materials

The datasets generated during, and/or analyzed, the current study are available in the World Bank (https://databank.worldbank.org/source/world-development-indicators), Our World in Data (https://ourworldindata.org/grapher/per-capita-energy-use), and International Monetary Fund (https://data.imf.org/?sk=F8032E80-B36C-43B1-AC26-493C5B1CD33B&sId=1481126573525&ref=mondato-insight) repositories.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by International School, Vietnam National University, Hanoi (VNU-IS).