Abstract

Keywords

Introduction

In 1931, the “Macmillan gap” was proposed, referring to the phenomenon where the financing needs of specific entities cannot be effectively met. This phenomenon has been repeatedly observed and studied as economic conditions evolve. Small- and medium-sized enterprises (SMEs) are critical contributors to sustainable economic growth, 1 employment, and innovation. But SMEs face systemic obstacles in accessing traditional financial services, with information asymmetry being a primary barrier. This asymmetry results in elevated collateral requirements and risk premiums, disproportionately affecting SMEs with limited financial histories or informal operations. 2 In developing economies, these informational gaps force SMEs to rely on informal financing channels, further marginalizing them from formal systems. Structural barriers, including stringent collateral requirements and high transaction costs, exacerbate these challenges. 3

Enterprises that are specialized, refined, distinctive, and innovative are designated as SRDI enterprises. These enterprises are regarded as the most advanced within the SME sector. SRDI enterprises are concentrated in mid-to-high-end industrial sectors, such as new-generation information technology, high-end equipment manufacturing, new energy, new materials, and biopharmaceuticals. These enterprises are a vital support force for high-quality economic development. 4 Consequently, various local governments have implemented numerous policy subsidies. For instance, the city of Beijing offers a reward of up to RMB 30m for eligible enterprise projects involving intelligent, digital, and green technological transformations. Zhejiang Province has adopted a policy of encouraging enterprises to establish research and development (R&D) institutions overseas through mergers and acquisitions or self-construction, with the promise of a one-time reward of up to RMB 5m for those with a total R&D investment exceeding RMB 10m, calculated at 5% of the verified R&D investment. But SMEs often face significant financing constraints due to their size, limited collateral, and information asymmetry. 5 Therefore, the first question discussed in this study is whether SRDI enterprises still encounter financing constraints despite policy support.

Digital finance and supply chain finance have emerged as pivotal innovations in the contemporary economic landscape, particularly benefiting SRDI enterprises. By mitigating financial constraints, these innovations significantly enhance operational efficiency and stimulate innovation, especially within contexts of digital transformation and disruptive technology integration such as blockchain. As digital finance evolves, it plays a pivotal role in empowering SMEs and SRDI firms, enabling them to navigate liquidity challenges and achieve growth in increasingly complex supply chain environments.6,7 Leveraging digital platforms and advanced technologies, these financial solutions address persistent financing gaps and improve credit access, thereby fostering economic growth, innovation, and resilience. The synergy between digital finance and supply chain finance optimizes cash flow management, reduces financial risks, and elevates operational efficiency for SMEs and SRDI enterprises. 8

Technology plays an important role in supporting the business processes of supply chain finance (SCF). Following several decades of development, the field of SCF has witnessed the emergence of novel models, including the utilization of artificial intelligence (AI) for evaluation purposes and the concept of green SCF. The concept of green finance has been demonstrated to have the capacity to alleviate corporate financing constraints, improve corporate performance, and achieve sustainable development.9,10 In the context of the current digital economy wave, digital supply chain finance (DSCF) is receiving increasing attention.

11

The digital transformation of enterprises can enhance their performance.

12

The advent of SCF, driven by blockchain technology, has been instrumental in surmounting the prevailing lack of trust, giving rise to a multitiered SCF system. This development has enabled the maximization of value-added and transmission effects within the manufacturing industry chain, while concomitantly mitigating the financial constraints experienced by small and medium-sized manufacturing enterprises.

13

The utilization of blockchain technology in the construction and administration of SCF has the potential to address the prevailing issues of trust among supply chain participants, enhance the efficiency of capital and information flows, and reduce financing costs.

14

The integration of Internet of Things (IoT) and AI into SCF has also proven beneficial. AI-driven analytics improve credit risk assessments by leveraging alternative data, while digital supply chain twins enable real-time monitoring and optimization of supply chain operations. These technologies enhance decision-making and operational efficiency, paving the way for more responsive and resilient supply chain networks.

15

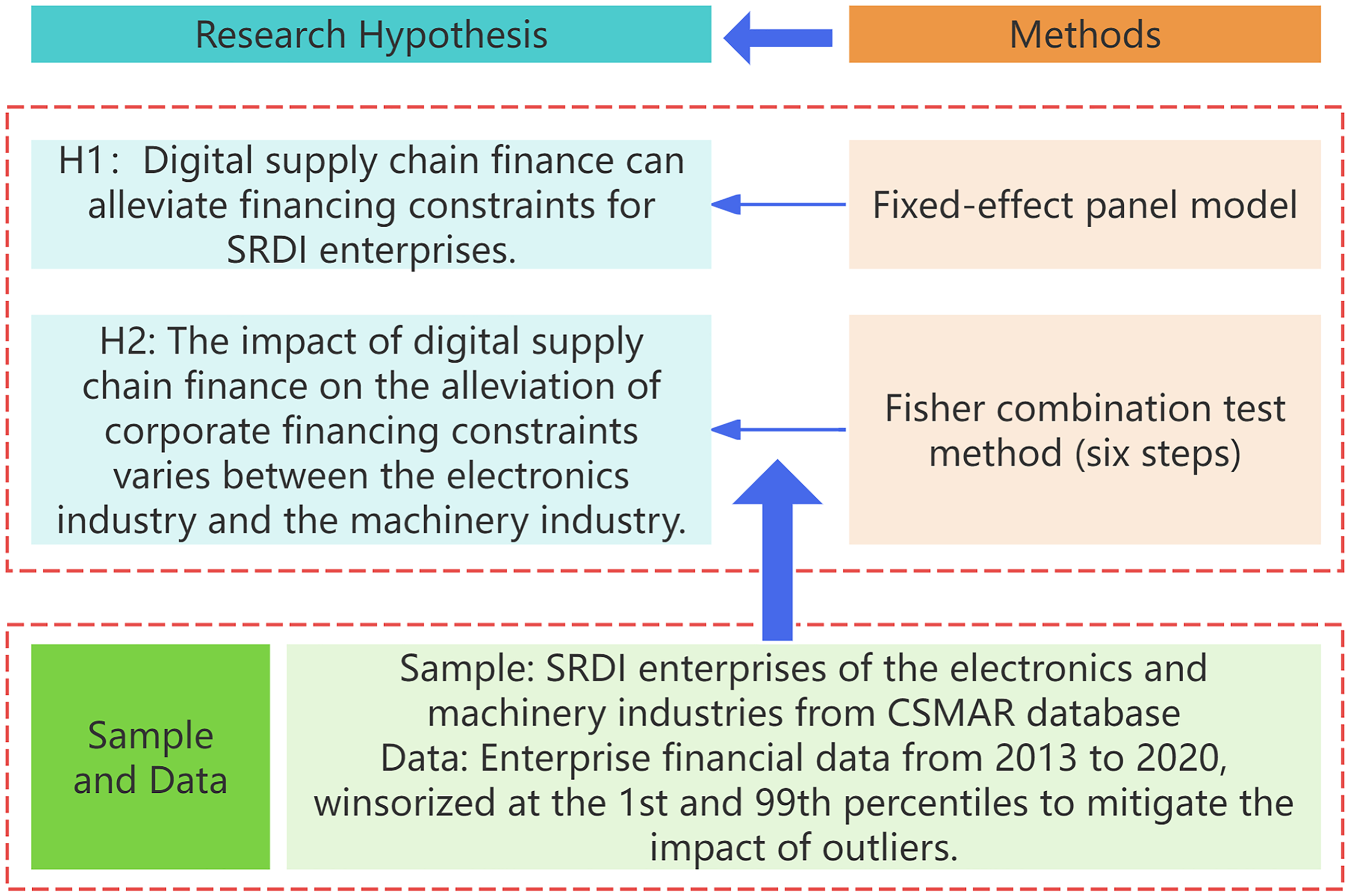

Therefore, this study proposes the following hypothesis: H1: Digital supply chain finance can alleviate financing constraints for SRDI enterprises.

SCF has been observed to manifest divergent characteristics across a range of industries.

16

The machinery industry is chiefly concerned with the production and sale of machinery and equipment. The inherent nature of the production cycle within this sector often results in a substantial accumulation of raw materials and components. In order to reduce delivery times, some enterprises may also engage in advance stockpiling of inventory. Equipment manufacturers must provide after-sales maintenance and repair services, necessitating the preparation of spare parts inventory. The accumulation of inventory, however, has the potential to impede the efficiency of capital turnover, which can have adverse consequences for the enterprise.

17

The machinery industry, defined by long production cycles and high capital intensity, faces challenges such as delayed payments and opaque financial data. Blockchain fosters trust among stakeholders by enhancing transparency, while IoT improves operational efficiency through real-time equipment and logistics monitoring.

18

The electronics industry is distinguished by a broad spectrum of products, rapid product updates and iterations, relatively small product size but high actual value, which leads to increased storage costs. Furthermore, the demand for electronic components industry is subject to significant fluctuations, thereby constraining the inventory levels of enterprises in this sector. The disparities between the two industries in terms of inventory and accounts payable are attributable to differences in industry characteristics. DSCF, however, is a financing model that focuses on inventory and accounts receivable. In the electronics sector, high R&D costs and rapid inventory turnover create liquidity constraints. Blockchain enhances transaction security and trust, reducing fraud risks, while IoT improves resource allocation through real-time monitoring. Therefore, this study proposes the following hypothesis: H2: The impact of digital supply chain finance on the alleviation of corporate financing constraints varies between the electronics industry and the machinery industry.

The research process of the paper is shown in Figure 1.

Research process.

The remainder of this paper is organized as follows. The second section presents the model, data source, and variables. The third section depicts the empirical results. The fourth section presents some discussions. The fifth section shows the main conclusion and some policy implications.

Methods

Sample and data

In 2011, the Ministry of Industry and Information Technology (MIIT) proposed the concept of “specialized, refined, distinctive, and innovative” (SRDI) enterprises, advocating it as a pivotal strategy for the transformation and upgrading of SMEs in the “12th Five-Year Plan for SMEs.” By the close of 2018, the MIIT had initiated the inaugural SRDI Little Giant enterprise cultivation initiative, signifying the tangible phase of China's SRDI enterprise cultivation endeavors. In September 2021, the Beijing Stock Exchange was established, with its core mission to serve SRDI SMEs, providing them with more convenient financing channels. In 2024, the Ministry of Finance and the MIIT jointly issued a notice on “Further Promoting the Vigorous Development of SRDI SMEs,” clarifying that from 2024 to 2026, the country will concentrate resources to support the high-quality growth of SRDI enterprises in stages through comprehensive financial subsidies, focusing on key industrial chains, the basic areas of industry, as well as strategic emerging industries and future industries. SRDI enterprises have been identified as playing a pivotal role in driving economic transformation and upgrading, enhancing the resilience of industrial and supply chains, and improving national economic security. Their specialization in niche markets is indicative of their ambition to become leaders in their respective industries, a goal which is instrumental in promoting the development and progress of related industries.

However, SRDI enterprises may encounter more stringent financial constraints. A study utilizing European Union member states as samples reveals that high-tech enterprises encounter more significant financing constraints compared to traditional enterprises. 19 A comparative study between affluent and impoverished nations further demonstrates that high-tech enterprises in the latter face particularly pronounced financing constraints. 20

Furthermore, to compare the characteristics of technology-intensive industries and capital-intensive industries, this study selected a number of enterprises belonging to the electronics and machinery industries that are included in the listed national-level SRDI enterprises from 2013 to 2020 as the research sample for empirical analysis.

Therefore, this study set the time frame as 2013–2020 and selected listed SRDI enterprises belonging to the electronics and machinery industries as the research sample. The data were mainly obtained from the China Stock Market Accounting Research database, Wind database, and annual reports of listed enterprises disclosed on the Juchao Information Network. In order to ensure the validity of the research data and the reliability of the conclusions, this study excluded enterprises in the ST and *ST categories and excluded enterprises with missing key variables. At the same time, continuous variables were winsorized at the 1st and 99th percentiles to mitigate the impact of outliers. The data were processed and analyzed using Stata 17.0 software.

Variable definition

Dependent variable

The dependent variable is enterprise financing constraints. The measurement of the variable can be divided into two main approaches: constructing indices to measure financing constraints and constructing models to measure financing constraints.

In the context of constructing an index to measure financing constraints, three primary methods are identified.

The KZ index, as pioneered by Kaplan and Zingales, 21 is a linear combination of corporate cash flow, future growth, debt-to-asset ratio, dividends, and cash holdings. The KZ index has been demonstrated to exhibit a positive correlation with the degree of corporate financing constraints.

The WW index, as outlined by Whited and Wu, 22 is a linear combination of dividend payment dummy variables, cash flow, debt ratio, firm size, firm's operating revenue growth rate, and industry operating revenue growth rate. It has been demonstrated that this index is also positively correlated with the degree of financing constraints.

The SA index, proposed by Hadlock and Pierce, 23 challenges the reliability of measures of financing constraints that rely on endogenous financial indicators, such as the debt-to-asset ratio and cash flow, contending that they can result in erroneous measurements of corporate financing constraints. Consequently, they have selected two strongly exogenous indicators, firm size and age, to construct the SA index, with a view to reducing the influence of endogenous variables. The SA index is a negative index, meaning that the smaller the value, the higher the degree of corporate financing constraints.

The model-based approach to measuring financing constraints employs the investment–cash flow sensitivity model (FHP) proposed by Fazzari et al. 24 This model posits that if a firm faces higher external financing costs, it will tend to use retained earnings and forgo external financing when investing, making its investment susceptible to its cash flow. Since the introduction of the FHP model, it has been widely used in research on corporate financing constraints. However, concerns have been raised by numerous researchers regarding the FHP model. For instance, Vogt 25 has theoretically and logically posited that a high sensitivity coefficient of investment to cash flow does not exclusively signify financing constraints; it could also be indicative of over investment by the firm. Therefore, model-based indices are excluded from our methodology.

The SA index relies exclusively on size and firm age, those exogenous variables unlikely to be directly affected by contemporaneous financial conditions. The KZ and WW indices use endogenous variables, such as cash flow, leverage, and dividends; these variables can be consequences of constraints. 23 Given that the data for this paper is sourced from listed enterprises in China; in order to mitigate endogeneity, this paper employs the SA index as an indicator to measure corporate financing constraints. The SA index's reliance on stable, exogenous factors makes it a robust, parsimonious alternative to KZ and WW indices, especially when avoiding reverse causality is critical. The SA index is generally less than zero, and the larger its absolute value, the greater the impact of financing constraints on the firm. Consequently, in the regression analysis, the absolute value of the index is utilized for the purpose of analysis.

Independent variable

The extant literature has predominantly concentrated on SCF rather than DSCF.26,27 DSCF, which leverages advanced technologies such as blockchain, big data, and AI, has emerged as a promising solution to alleviate financing constraints by increasing transparency, reducing transaction costs, and facilitating access to credit.

This paper is pioneering in its approach to measuring the level of DSCF. In the practice of DSCF, the level of a company's DSCF is determined by two key factors, the external environment of digital economy development in the region where the company is located 28 and the company's own level of SCF. The paper proposes a methodology for calculating the level of a company's DSCF. The methodology involves the multiplication of two factors: the degree of financial digitization in the company's location and the company's level of SCF. Drawing on Yao et al., 29 the level of SCF development is measured by the sum of a company's short-term loans and notes payable in the current year divided by its total assets at the end of the year. Guo et al. 30 established the digital financial inclusion index of prefecture-level cities at Peking University as a metric of financial digitization. The financial digitization level of an enterprise is obtained by matching its registration location with the corresponding regional digital finance index.

Control variables

In order to improve the accuracy of the research results, regarding the existing literature, 31 this study selected the following variables for control: debt-to-asset ratio (leverage (LEV)), expressed as the liability that is commensurate with each unit of assets; return on assets (ROA) expressed as the net profit corresponding to each unit of assets; revenue of the enterprise (REV) expressed as the income derived from an enterprise's primary business activities. Based on the construction method of this variable, a higher value is indicative of a more advanced level of development in the enterprise's DSCF.

Model setting

This study constructed the following regression model (1) to test hypothesis:

Within the domain of SCF, companies situated at disparate points along the supply chain possess divergent capabilities with regard to acquiring financing. From this standpoint, considering the characteristics of industry inventory, SCF in the machinery industry should be more effective in alleviating financing constraints than in the electronics industry. Consequently, Fisher’s combination test method is used to test H2. The empirical research steps are as follows.

Step 1: Divide the samples into two groups, electronics industry and machinery industry, and set the regression models (2) and (3) as follows:

We focus on the difference in coefficients between the two groups in the DSCF variable. Define the difference in coefficients between the two regression models of the digital supply chain as

Step 2: Combine the two sets of samples from the electronics industry and the machinery industry to obtain a total sample S consisting of

Step 3: Obtain experiential sample

Step 4: For the empirical samples

Step 5: Repeat steps 3 and 4 K = 1000 times to obtain the empirical distribution

Step 6: Calculate the empirical p-value,

Results

Descriptive statistics

Table 1 reports the results of the descriptive statistics for all the study variables. In order to maintain consistency in the order of magnitude of the data, logarithmic adjustments were made to variables DSCF and ASA.

Descriptive statistics results.

DSCF: digital supply chain finance; ROA: return on assets; LEV: leverage; REV: revenue of the enterprise.

As illustrated in Table 1, the standard deviation of the level of DSCF is 0.313, with a range of 1.672, suggesting that there are notable variations in the development level of DSCF among different enterprises. The mean value of the corporate financing constraints (SA index) is −2.171, with all values being negative, and there is a tendency for the index to increase with the length of enterprise establishment, suggesting that SRDI enterprises in the sample generally face certain financing constraints. In the following research, the paper will use the absolute value of SA index (ASA) for analysis. This paper's first finding is that, despite the benefits of preferential credit policies, some SRDI enterprises still encounter credit constraints. The mean value of ROA is 0.092, with a standard deviation of 0.07. However, it is evident that there are samples with negative values, indicating that the net profits of SRDI enterprises are unstable and may experience losses.

Regression results

Table 2 presents the main results from our analysis, which demonstrate that DSCF exerts a significant impact on the alleviation of financing constraints. In Table 2 the first column presents the result of the regression model that only contains control variables. And the second column presents the result of the regression model contains all variables. In other words, it includes independent variables and all control variables. The purpose of doing this is to compare the coefficient signs and significance of the model with only control variables and the model with all variables. The research results show that the effect directions of the control variables are consistent, indicating that the selection of the control variables is appropriate and the main results are reliable.

Regression results.

DSCF: digital supply chain finance; LEV: leverage; ROA: return on assets; REV: revenue of the enterprise.

Note: t-Statistics are shown in parentheses.

***Indicate the significance at the 1% levels.

The second column presents that F-value of the regression equation with all variables is 128.654, with corresponding p-values all less than 0.01, indicating that the model passes the F-test. The regression coefficient of level of DSCF is −0.476 and passes the 1% significance level test, indicating that DSCF can alleviate SRDI enterprises’ financing constraints. Hypothesis 1 is valid.

SCF optimizes cash flow and reduces financial risks by aligning financing solutions with supply chain operations. It provides SRDI enterprises with credit solutions, such as reverse factoring, dynamic discounting, and inventory financing, which help manage liquidity and working capital more effectively. The digitalization of SCF has revolutionized its effectiveness by leveraging technologies such as blockchain, the IoT, and AI. DSCF is a robust tool for optimizing cash flows, reducing bankruptcy risks, and fostering collaboration among supply chain participants.

The regression coefficient of the leverage ratio (LEV) is significantly positive at the 1% level, indicating that an increase in LEV exacerbates financing constraints, which aligns with the characteristics typically observed among listed enterprises in China. Lu and Ye 33 posited that there is a pronounced predilection for equity financing among listed enterprises in China, a phenomenon that may be associated with factors such as free cash flow, capital size, and financing costs. Listed enterprises are obligated to disclose financial information on a regular basis, and an excessively high debt-to-asset ratio can have a detrimental effect on stock prices. Thus, an increase in the debt-to-asset ratio has been shown to exacerbate financing constraints.

The regression coefficient of ROA is significantly positive at the 1% level, suggesting that an increase in ROA exacerbates financing constraints to a certain extent. The descriptive statistics indicate that the ROA of some SMEs is unstable. Occasionally, SRDI enterprises experience losses, and such fluctuations in earnings have the capacity to influence the financial institutions’ assessment of the enterprise's solvency. Consequently, the unpredictability of returns can intensify credit constraints.

The regression coefficient of REV is significantly negative at the 1% level, indicating that an increase in a company's operating revenue can alleviate financing constraints. This phenomenon may be attributed to the fact that an augmentation in operating revenue is indicative of a company's potential for future growth and enhanced cash flow, thereby facilitating the acquisition of credit support.

Multicollinearity test

To confirm the explanatory effect of the model, the multicollinearity test is conducted. Table 3 shows that the variance inflation factor (VIF) values of the model variables are all less than 5, indicating that the model does not have the problem of multicollinearity.

Multicollinearity test results.

DSCF: digital supply chain finance; ROA: return on assets; LEV: leverage; REV: revenue of the enterprise.

Industry heterogeneity analysis

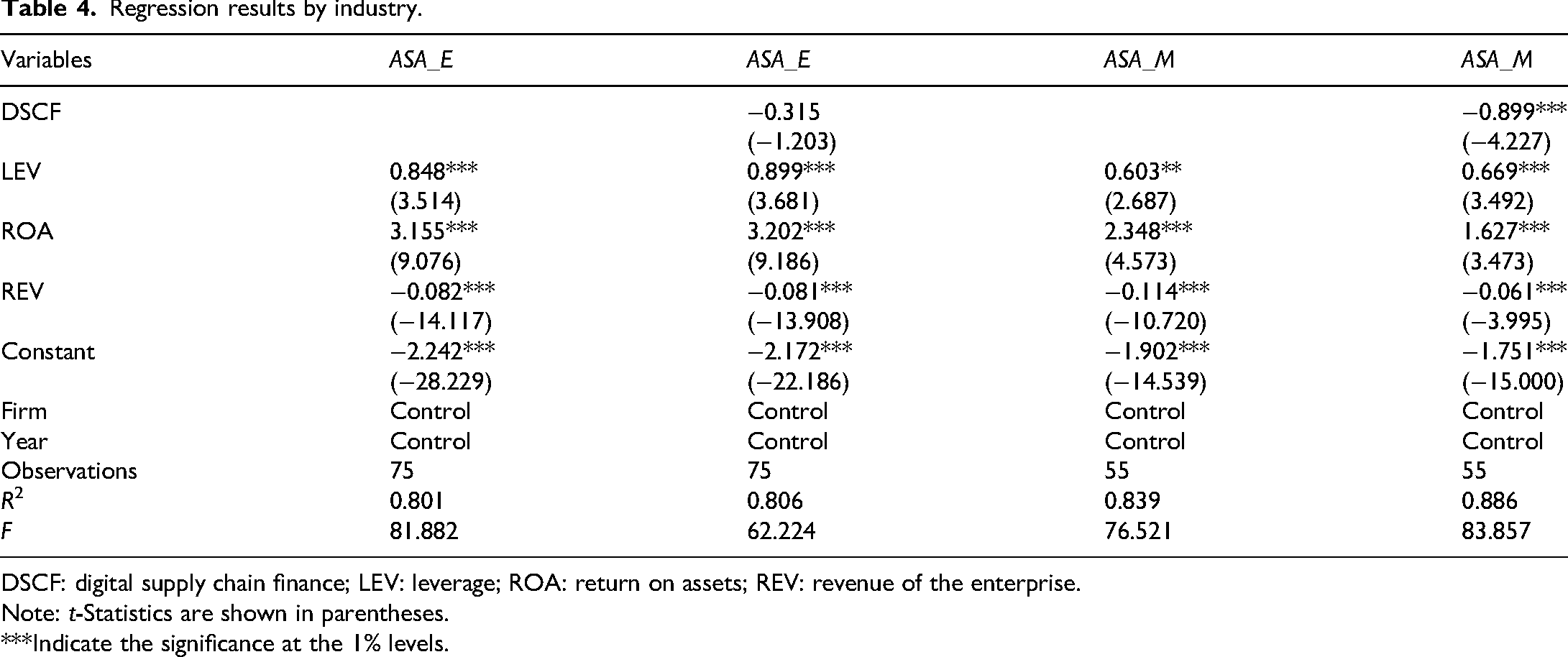

This paper selects SRDI enterprises from the electronics and machinery industries. The sample data has been grouped and regressed by industry to conduct a more in-depth investigation into the differences in the impact of DSCF on financing constraints for SRDI enterprises within specific industries. Table 4 presents the main results from industry heterogeneity analysis, ASA_E is the absolute value of the SA index of the SRDI enterprises in the electronics industry group, and ASA_M is the absolute value of the SA index of the SRDI enterprises in the machinery industry group.

Regression results by industry.

DSCF: digital supply chain finance; LEV: leverage; ROA: return on assets; REV: revenue of the enterprise.

Note: t-Statistics are shown in parentheses.

***Indicate the significance at the 1% levels.

As illustrated in Table 4, the impact of DSCF on SRDI enterprises financing constraints varies between the electronics industry and the machinery industry. Specifically, the regression coefficient of level of DSCF is −0.899 and passes the 1% significance level test in the machinery industry group. While the regression coefficient of level of DSCF is not significant in the electronics industry group, and the impact of DSCF on financing constraints is smaller than the impact in the machinery industry group.

This paper sets out to explore the reasons for the differences in the impact of DSCF on SRDI enterprises in the two industries. To this end, the paper collected and organized the following indicators for the electronics and machinery industries: inventory, inventory turnover days, and accounts receivable.

Table 5 and Figure 2 present the comparison of average inventory, inventory turnover days, and accounts receivable between the electronics industry and the machinery industry.

Comparison of average inventory, inventory turnover days, and accounts receivable between the electronics industry and the machinery industry.

Comparison of inventory, turnover days, and accounts receivable between electronics and machinery industries.

The machinery industry demonstrates a significantly higher 8-year average inventory of 86.58m yuan in comparison to the electronics industry. Furthermore, the machinery industry exhibits an inventory turnover day that is 50.9 days longer than that of the electronics industry. It is evident that both the confirmed warehouse financing model and the inventory financing model in SCF leverage corporate inventories as the core to assist enterprises in financing. The machinery industry's superior positioning in addressing its financing constraints through SCF is attributable to its comparatively higher inventory levels and longer turnover days.

In the sample, the 8-year average accounts receivable of the machinery industry is 34.33m yuan lower than that of the electronics industry. In the context of SCF, the accounts receivable financing model is predicated on the utilization of corporate accounts receivable as its fundamental element, with the objective of ameliorating financing constraints experienced by enterprises. This model is predominantly observed among upstream enterprises within the supply chain. 34 It is evident that the electronics industry is not entirely suitable for this model, and the machinery industry has stronger conditions for engaging in SCF based on its inventory characteristics compared to the electronics industry based on its accounts receivable characteristics.

In order to further test the differences in group-specific correlation coefficients, the present paper adopts the Fisher's combined probability test, as summarized by Lian and Liao. 35 By generating an empirical sample of 1000 observations through the use of bootstrap resampling, the final p-value can be determined in order to examine the differences in coefficients between the two models. Table 6 present the p-value of DSCF is 0.044, less than 0.05, which indicates that the null hypothesis (i.e. the absence of a difference between the two sets of coefficients) can be rejected at the 5% level, thereby substantiating the existence of a significant difference between the two sets of coefficients. Hypothesis 2 is valid.

Verification results of Fisher's combined test.

DSCF: digital supply chain finance; LEV: leverage; ROA: return on assets; REV: revenue of the enterprise.

Note: t-Statistics are shown in parentheses.

***Indicate the significance at the 1% levels.

Discussion

Our results highlight the important role of DSCF in alleviating financing constraints for SMEs, particularly those SRDI enterprises in high-tech industries. By leveraging digital technologies, DSCF enhances transparency and trust in the supply chain, making it easier for SMEs to access credit and reduce financing costs. This, in turn, supports innovation and growth, contributing to economic development. A further analysis of the electronics and machinery industries has been conducted, which is expected to provide references for SME financing decisions and the development of SCF in different industry subsectors, and offer a basis for research on policy support for various industry segments.

These findings align with previous studies. By leveraging technologies such as mobile banking, blockchain, and AI, digital finance reduces barriers to credit access and facilitates seamless financial transactions. This is especially critical for SRDI enterprises and SMEs, which often face challenges in accessing traditional credit due to limited collateral, high-risk perceptions, and information asymmetry. 36 The effectiveness of DSCF in overcoming financing barriers is amplified by technologies like blockchain, IoT, AI, and big data analytics.

This study has important implications for DSCF and SRDI enterprises, suggesting that DSCF leverages advanced technologies to address financing constraints and optimize resource allocation. Due to the modest sample size and specific focus on listed SRDI firms, caution is warranted in generalizing these findings beyond similar contexts.

A major limitation is the study's exclusive focus on electronics and manufacturing sectors, omitting unlisted SRDI firms and enterprises in other industries. DSCF adoption varies by industry due to operational complexities and financial constraints. Future research could expand on this study by examining the impact of DSCF in other industries or countries. In addition, effective data management is critical for DSCF implementation, yet industries face challenges such as incorrect data, lack of standardization, and integration of diverse data sources. Thus, standardization across industries is another pressing issue, as the absence of unified frameworks complicates data sharing and interoperability

Conclusions

This study provides empirical evidence of the positive impact of DSCF on the financing conditions of SMEs with specialized expertise and new technologies.

Despite the implementation of a series of policies and measures by the Chinese government to support the development of the private economy, the issue of difficulty in obtaining loans for SMEs remains salient, particularly with regard to medium- and long-term loans. The constraints imposed by risk assessment and guarantee conditions frequently impede SMEs in accessing adequate financial support, thereby hindering their investment, equipment renovation, and technological upgrading. Consequently, there is an imperative for enhanced policy support and the promotion of private investment. From a policy perspective, government interventions, such as expanding tax incentives and facilitating digital finance adoption via blockchain, could further enhance SMEs’ access to credit.

The government has the capacity to introduce relevant policies, provide financial subsidies, tax incentives, and other incentive measures with a view to encouraging enterprises to establish and apply digital supply chain platforms. The utilization of technologies such as blockchain can enhance information transparency and establish a data sharing mechanism, thereby encouraging enterprises to share data and promote openness, thus disrupting information silos and enhancing the transparency and efficiency of the supply chain. This, in turn, will enhance the financing efficiency of DSCF and provide strong support for the digital transformation of SMEs, enabling sustainable development.

Financing constraints in the electronics and machinery industries stem from varying operational complexities, market dynamics, and technological adoption levels. DSCF addresses these challenges by leveraging advanced technologies to optimize financial flows, enhance transparency, and mitigate risks. The electronics sector faces liquidity challenges from high R&D costs and frequent inventory turnover. Collaborative efforts among academia, industry, and government can enhance blockchain implementation and address resource limitations, particularly for SMEs. In the machinery industry, long production cycles and capital intensity create barriers to financing. Blockchain and IoT integration can improve transparency and trust, but practical validation is needed to ensure reliability. Policy interventions and interdisciplinary approaches can optimize financial ecosystems and improve data quality, enabling better adoption of AI and big data analytics.

Footnotes

Ethical considerations

There are no human participants in this article and informed consent is not required.

Author contributions

Dr Shanshan He conceived the study, participated in its design and coordination, and contributed to manuscript drafting and revision. Zhengyang Liu participated in study design, performed statistical analysis, and drafted the manuscript. All authors read and approved the final manuscript.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Hubei Province Small and Medium-sized Enterprise Research Centre (grant number HBSME2023C06).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.