Abstract

The authors investigate the role of employee voice in corporate governance for corporate environmental impact. This issue is important given the potentially serious employment implications for corporations seeking to transition to lower carbon economic activity and the urgency of moving toward a carbon neutral economy. Using secondary and interview data from Germany, the authors use Qualitative Comparative Analysis (fsQCA) to demonstrate that strong employee voice in corporate governance is a key factor in reducing the environmental impact of corporations. The authors also illustrate distinct strategies by which labor representatives at the company level enact institutionally granted power resources for environmental issues. This work contributes to academic debates on labor and the natural environment literature. In particular, it highlights that, alongside unions, labor representatives at the company level constitute an important source of employee voice for environmental transformation.

Keywords

Corporations are known for their devastating effects on the natural environment. Yet they differ in their corporate environmental policies and impact on the natural environment. Past research highlights corporate governance as an important determinant of corporate environmental policies, emphasizing the role of ownership patterns, board characteristics, and reporting requirements (Aguilera, Aragón-Correa, Marano, and Tashman 2021). By structuring the rights and responsibilities of those with a stake in the firm, corporate governance is central for how firms prioritize objectives within corporate decision-making and thereby impact the environment through their activities.

While research on corporate governance and the environment is growing, the role of employee voice remains underexplored. This lack of research is surprising given that employee voice has been shown to play a substantial role in diverse issues, including auditing (Cho, Chung, and Lee 2019; Chyz, Eulerich, Fligge, and Romney 2023) and CEO compensation (Huang, Jiang, Lie, and Que 2017; Boodoo 2018), or the adoption of employment-related corporate social responsibility (CSR) policies (Jackson, Doellgast, and Baccaro 2018). Furthermore, employee voice is an institutionalized feature of corporate governance in many countries, including board-level employee representation in countries such as Germany, Denmark, and the Netherlands. Here, it provides a powerful lever in employee representatives’ bargaining processes (Benassi 2023). Against this backdrop, it is important for researchers, policymakers, and employee representatives alike to understand how board-level employee representatives use voice in corporate governance regarding environmental issues because of the potentially serious employment implications for corporations seeking to transition to lower carbon economic activity as well as the urgency to reduce corporate environmental impact.

In this article, we focus on employee voice in corporate governance and ask: How does employee voice in corporate governance influence corporate environmental impact? And what strategies do board-level employee representatives use to engage with other corporate governance actors such as shareholders and managers on environmental issues?

Our investigation takes a configurational view of corporate governance, highlighting the interdependencies of different actors (Fiss 2007, 2011; Fiss, Cambré, and Marx 2013; Misangyi et al. 2017; Greckhamer, Furnari, Fiss, and Aguilera 2018). Employee representatives’ formal-legal power in corporate governance is limited, since they always constitute a minority within co-determined boards. Hence, employee voice in corporate governance requires employee representatives to enact (mobilize) various power resources (Refslund and Arnholtz 2022; Rothstein 2022) to leverage their structural power. Accordingly, our approach focuses on the joint role of corporate governance actors for corporate environmental impact, specifically configurations involving conflict, alignment, and coalitions among shareholders, managers, and employees (Aguilera and Jackson 2003). In addition, we explore the various strategies used by employee representatives to engage with other actors regarding environmental issues and thereby “doing” influence in the strategy-making process.

We study these issues in the context of Germany, an archetypal case of employee co-determination and strong role of employee voice in corporate governance. We use set theoretical methods (fsQCA) (Ragin 2008) to explore whether corporate governance configurations are necessary or sufficient conditions for achieving a relatively low (high) environmental impact compared to peer companies. Our analysis uses secondary data on German Stock Exchange–listed corporations in 2013 derived from Thomson Reuters Asset4, the Climate Disclosure Project (CDP), and the MB-ix, an index on the strength of co-determination (Scholz and Vitols 2018). In addition, we explore the mechanisms through which employee voice shapes corporate environmental impact by drawing on interviews with board-level employee representatives from the companies of our QCA results, complemented by interviews with other field experts. In total, we make use of 40 interviews conducted between 2015 and 2023.

Our empirical results show that strong employee voice is an integral factor in reducing carbon emissions. In particular, employee representatives seek to form coalitions with other actors by appealing to the business case or playing an active role as co-managers. Moreover, if employee interests are in broad alignment with both long-term shareholders and managers, employee representatives may also play an active role in corporate agenda setting or making deals that advance environmental issues. The article thereby makes two major contributions. First, we add to the literature on employment relations and the natural environment by highlighting the role of company-level employee voice (for a rare exeption, see Houeland and Jordhus-Lier 2022), which complements earlier studies on individual employees (Markey, McIvor, O'Brien, and Wright 2019) or unions (e.g., Räthzel, Uzzell, and Elliott 2010; Barca and Leonardi 2018; Stevis, Uzzell, and Räthzel 2018; Räthzel, Stevis, and Uzzell 2021). Second, we contribute to research on corporate governance and the environment by developing a configurational perspective and highlighting employee voice as important.

Corporate Governance and Corporate Environmental Impact

Corporate governance describes the rights and responsibilities of those with a stake in the company and plays a central role in shaping the environmental impact of corporations (for an overview, see Aguilera et al. 2021). Corporate governance matters by shaping the time horizons of corporate decision-making and prioritizing stakeholder objectives (Slawinski and Bansal 2012, 2015; Slawinski, Pinkse, Busch, and Banerjee 2017; Nyberg, Wright, and Kirk 2020). Whereas long-term orientation may not guarantee lower environmental impact, short-termism is a likely cause of under-investment in the environment (Cox, Brammer, and Millington 2004; Marginson and McAulay 2008; Calza, Profumo, and Tutore 2014). Reducing environmental impact often requires substantial long-term investment. For example, Slawinski et al. (2017) argued that investors’ attention to the daily share price is responsible for corporations not investing in carbon reduction measures. By contrast, pension funds or socially responsible investment funds provide a more long-term approach to profitability and consider environment-related risk factors (Aguilera, Rupp, Williams, and Ganapathi 2007). Short-termism may also impact managers. Myopic managerial compensation increases environmental concerns (Walls, Phan, and Berrone 2011), whereas long-term oriented CEO compensation increases pollution prevention strategies (Berrone and Gomez-Mejia 2009). Corporate boards can act to broaden the consideration of long-term issues such as the environment in corporate decision-making (for a review, see Jain and Jamali 2016).

Employee Voice in Corporate Governance

Corporate governance involves not only managers and shareholders as key actors but also employees (Aguilera and Jackson 2003). Despite the institutionalized role of employee representatives in corporate governance in many countries, employee voice has received scant but growing attention among corporate governance scholars (Gospel and Pendleton 2003; Black, Gospel, and Pendleton 2007). Employee voice plays a significant role in corporate governance issues, including auditing (Cho et al. 2019; Chyz et al. 2023) and CEO compensation (Huang et al. 2017; Boodoo 2018), as well as the adoption of employment-related CSR policies (Jackson et al. 2018) and other substantive CSR policies, including targets for reducing pollution (Scholz and Vitols 2019).

The stance of employee representatives toward reducing corporate environmental impact may depend on the potential for using employee voice to enable inclusive ecological transitions (Obach 1999, 2002; Hyde and Vachon 2019; Boodoo 2020). Most studies on employee voice and the natural environment focus on unions as actors within wider social movements pushing for ecological transformation (Räthzel et al. 2021; Flanagan and Goods 2022; Wright, Irwin, Nyberg, and Bowden 2022), framing ecological improvements as a contribution to social justice (Barca and Leonardi 2018). On a company level, however, reducing ecological impact can have ambivalent consequences for employees, whose jobs may be subject to work reorganization, re-skilling or upskilling, or geographic shifts—or may be at risk through divestment from environmentally harmful activities. Hence, while ecologically sustainable forms of work are beneficial in the long-term, employees may face substantial costs and risks of transition in the short-term. As a consequence, employee representatives may come to identify more strongly with the company’s business interests, thereby creating “a mixed legacy on the possibility of climate change-inspired revisioning” (Flanagan and Goods 2022: 491), preferring incremental rather than radical change. Consequently, the role of board-level employee representation warrants greater attention (Aguilera et al. 2021).

Board-Level Employee Representation, Power, and Corporate Environmental Impact

Board-level employee representation gives voice to employees on matters of corporate strategy, as well as specific governance issues such as executive compensation. In this context, employee voice derives its power from the formal-legal rights of employee representation on the board. However, even where employee representatives have 50% of the seats on the board, employees do not have sufficient power to impose decisions unilaterally (e.g., in Germany, a tie-breaking vote always goes to the shareholder bench of the board). Likewise, majority shareholders may have sufficient formal decision-making rights to exercise corporate control, yet most shareholders do not hold such large stakes. As a consequence, corporate governance tends to involve building coalitions around a diversity of issues (Aguilera and Jackson 2003) and exercising corporate control jointly.

Our analysis of board-level employee representation within corporate governance thereby seeks to go beyond the consideration of power as manifest as overt decision-making power based within the formal-legal (e.g., by means of voting rights or ownership share), but considers what Lukes (1974) referred to as “the second and third dimensions of power,” in which actors exercise power through mechanisms of agenda setting or hegemonic power based on the subtle or sometimes invisible influence of perceptions, beliefs, and desires in a way that aligns with their interests (see also Carstensen, Ibsen, and Schmidt 2022). In particular, we turn to recent literature on the power resource approach that explores how workers mobilize and enact power through varied resources that go beyond the institutional power of board-level employee representation (Schmalz, Ludwig, and Webster 2018).

In particular, we highlight what Rothstein (2022) discussed as organizational power resources rooted in the organizational capacity of employee representatives, as well as the ideational power rooted in discourse and ideas. First, formal institutional power at the organizational level also has a strong relation to micro-level bargaining processes (Benassi 2023). In Germany, employee voice through board-level employee representation interacts with workplace-level co-determination rights through works councils (Bamber, Lansbury, Wailes, and Wright 2020; Keller and Kirsch 2021), who have developed strong organizational capacities as co-managers based on their knowledge, expertise, and access to information about shop-floor processes. Such workplace-level engagement may be an important impulse for environmental transformation (Goods 2017; Farnhill 2018; Galgóczi 2020) and support for effective “on the ground implementation” (Flanagan and Goods 2022: 487). Second, the influence of employee voice on CSR issues is shaped by the effective use of ideas and justifications for businesses to adopt socially responsible policies. For example, German labor unions have widely adopted the discourse of the “business case” as a primary means of justifying their social and environmental agenda (Lohmeyer and Jackson 2024).

In sum, we conceptualize employee voice in corporate governance by focusing on both formal decision-making structures, as well as the specific strategies of engagement around the environment. First, we adopt a configurational perspective (Fiss 2007, 2011; Fiss et al. 2013; Misangyi et al. 2017; Greckhamer et al. 2018) to study corporate governance. This perspective stresses the structural interdependencies and potential interactions between varied actors (Kern and Gospel 2023). Here the role of board-level employee representatives depends not only on the extent of formal institutional rights of employees but also on the broader configuration of decision power and time horizons by other corporate governance actors, specifically shareholders and managers. For example, the pro-environmental potential of employee voice depends on a long-term orientation to “just” solutions to climate issues and developing a sense of “working class environmentalism” (Barca and Leonardi 2018; Markey et al. 2019; Bell 2021). Yet the growing influence of institutional investors and focus on shareholder value orientation by managers (Beyer and Hoppner 2003; Fiss and Zajac 2004) may create resistance to environmental policies that conflict with short-term interests of shareholders or managers. Second, and within diverse configurations of corporate governance, we argue that employee voice depends on employee representatives actively “doing” influence through what we call strategies of engagement, where employee representatives mobilize formal, institutionally granted power resources, alongside other ideational or organizational resources (Carstensen et al. 2022; Refslund and Arnholtz 2022; Rothstein 2022).

Research Methods

Our empirical analysis aims to understand how board-level employee representation influences corporate environmental impact. We study this question by using set theoretical methods (fsQCA) (Ragin 2008) to investigate the corporate governance configurations of companies with relatively low environmental impact compared to their peers (for high environmental impact, please see the Online Appendix). We are doing so with a sample of large-scale (>500 employees), stock market–listed (DAX, MDAX, SDAX) corporations headquartered in Germany. In addition, we explore the mechanisms through which employee representatives shape corporate environmental impact, applying qualitative research methods. We analyze interviews with employee representatives on the supervisory boards of the companies in our QCA, complemented by interviews with other field experts.

The case of Germany offers an excellent context to study employee voice in corporate governance given its very strong institutions of board-level co-determination and works councils (Keller and Kirsch 2021). Nonetheless, German corporations vary in the strength of institutionalized employee voice (Scholz and Vitols 2018) and in the extent of pressure focused on shareholder value (Beyer and Hoppner 2003; Meyer and Hoellerer 2010; Giovanazzi 2024). We utilize this variation in corporate governance arrangements within Germany to study the role of corporate governance configurations for environmental outcomes.

Fuzzy-Set QCA: Data and Calibration

QCA methodology is well-suited to the causal complexity of organizational configurations, for which multiple factors combine at the level of cases (conjunctural causation) and multiple pathways may exist to the same outcome (equifinality) (Ragin 2000, 2008). We constructed a data set on large corporations with headquarters in Germany from several sources. Data on corporate ownership and boards came from Asset4, which represents approximately 90% of German stock market capitalization. Data on corporate-level employee rights came from the MB-ix data set (Scholz and Vitols 2018). We obtained corporate financial and operations data from Thomson Reuters DataStream. Any missing values were added manually by checking annual reports and company websites. Finally, we used Climate Disclosure Project (CDP) data on greenhouse gas emissions. 1 Since not all companies report emissions data, we focused on the year with the largest amount of data available: In 2013 about two-thirds of large German companies reported their environmental impact, leading to a final sample of 56 companies. While carbon disclosure is voluntary, the company characteristics of our sample do not suggest any significant bias (see Appendix Table A and Table B).

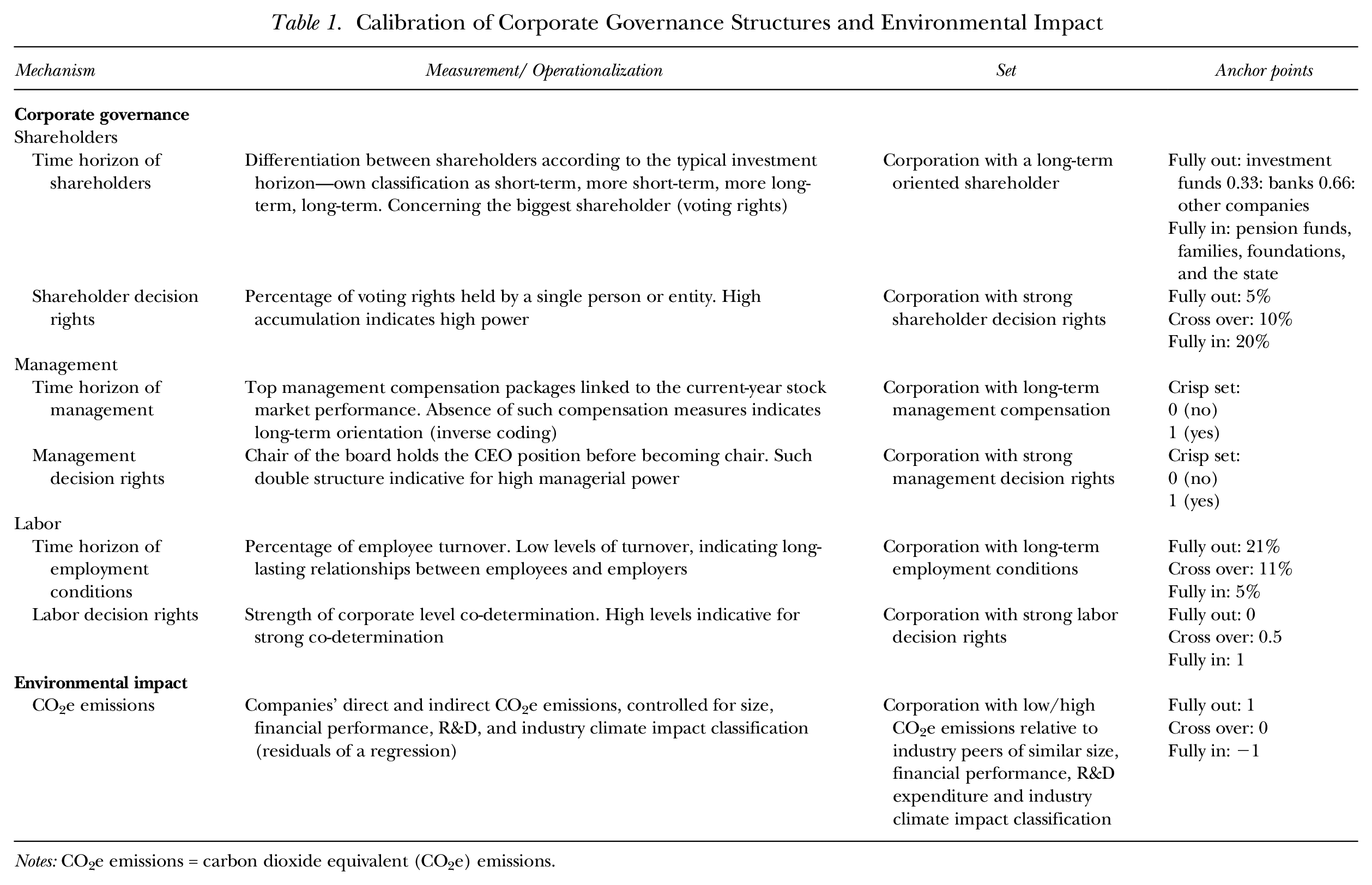

We calibrated the company-level data for fuzzy-set QCA (see Appendix Table D for the calibrated data), by assigning degrees of membership for each causal condition. Following the direct method of calibration (Ragin 2008; Fiss 2011), Table 1 summarizes each condition, the measurement, the set definition, and the anchor points for calibrating set membership.

Calibration of Corporate Governance Structures and Environmental Impact

Notes: CO2e emissions = carbon dioxide equivalent (CO2e) emissions.

We measured the outcome of corporate environmental impact through annual CO2 emissions. Our data include corporations’ direct emissions and resource use (scope 1), as well as emissions from using externally produced energy (scope 2). Unfortunately, we could not measure emissions made through the products they buy and sell (scope 3). In calibrating data on scope 1 and 2 emissions, we consider its relationship to company size, financial performance, R&D expenditures, and industry classification (Berrone and Gomez-Mejia 2009; Sharkey and Bromley 2015; Aragón-Correa, Marcus, and Hurtado-Torres 2016). We ran ordinary least squares (OLS) regression using STATA 15.0 software 2 and calibrated the z-standardized residuals into fuzzy sets. The resulting set membership represents corporations with relatively low environmental impact when compared with industry peers of similar size, financial performance, R&D expenditure, and from the same climate-impact sector (using the inverse z-standardized residuals). Firms with a z-score of −1 or less are considered “fully in” the set of firms with relatively low emissions, z-scores of 1 or more are “fully out,” and a score of 0 (the predicted average emissions level) is the cross-over point.

Our causal conditions include corporate governance characteristics of shareholders, managers, and employees, measuring their time horizon (long- or short-term) and extent of their formal decision-making rights. For shareholders, we examined the time horizon of the legal person holding the largest number of shares. 3 Membership in the set of corporations with long-term shareholders was scored as 1 (fully in) for pension funds, labor funds, families or individuals, foundations, and state agencies, whereas investment managers or companies and investment banks were scored 0 (“fully out”). We also calibrated two intermediate categories: shareholders who are part of other companies and holding companies, which are more long-term than short-term with set memberships of 0.66, while banks are more short-term than long-term on a 0.33 level. Next, we measured the formal decision-making rights of shareholders through the voting rights held by the single largest owner. Following La Porta, Lopez-de-Silanes, and Shleifer (1999), we consider shareholders with more than 20% of voting rights (fully in) as having a large ownership stake, allowing some effective control. Likewise, we deem 10% of voting rights as the 0.5 cross-over point, since this point represents a significant threshold of votes and is mirrored in the rule requiring mandatory disclosure in many countries. The lower anchor point is 5%, which represents dispersed ownership (Holderness 2009).

For managers, we calibrated the set of long-term management time-horizon by measuring the extent to which compensation packages are linked to stock performance (Ortiz-de-Mandojana, Bansal, and Aragón-Correa 2019). Stock-based compensation may persuade CEOs, aiming to satisfy shareholders, to underinvest in long-term assets (Höpner 2001). We used an indicator that reflects whether the CEO’s compensation is or is not linked to total shareholder return (TSR). TSR encourages “managers to view decisions in much the same way a shareholder would” (Edwards 1994: 60), thus being a good measure for the extent of shareholder orientation within management compensation. The set is a crisp set and defined as a corporation with long-term (no TSR) compensation (fully in = 1). Meanwhile, the extent of decision-making rights of managers on the board relates to board independence. In Germany, the two-tier system mandates a strict division between executive board and supervisory board. Thus, we measured whether the person holding the chair of the supervisory board had held the CEO position prior to becoming chair. Research on CEO duality in the Anglo-Saxon context has shown that CEOs have a greater ability to exert their interests if they concurrently have a position on the board (Walls and Berrone 2017). We argue that if a former CEO is chair of the board, managerial power increases and makes external control more challenging. The set is a crisp set with a former CEO as chairman of the board (fully in = 1). Otherwise, companies are fully out (0).

For employees, time horizon relates to stable employment. 4 We investigated this by measuring company-level employee turnover (García-Castro, Aguilera, and Ariño 2013) to indicate long-term relationships between employees and employers (Cotton and Tuttle 1986). Missing values were hand coded with information about employment reductions compared with the previous year. We coded companies with less than 5% turnover as fully in the set of companies with long-term-oriented employment, whereas those with turnover greater than 20% were fully out. Sousa-Poza and Henneberger (2004) showed that, on average, 7.3% of employees in Germany intend to leave the company, suggesting a common turnover around this number. Therefore, we define more than 10% turnover as a conservative cross-over point between companies with secure or insecure employment.

We examine the decision rights of employees by measuring representation in corporate boards. German legislation mandates for employees to hold one-third or one-half of supervisory board seats, but it also leaves room for differences in certain practices related to the extent of representation by union representatives or whether employees have membership in various board committees. Moreover, the German law leaves room to avoid the co-determination rights (e.g., by splitting the company in several separate units under one holding). We used the MB-ix measure developed by Scholz and Vitols (2018) to capture the strength of employee representation in German corporate boards across six structural dimensions: composition of the board, structure of the board, structure of the committees, internationalization, influence of the board, and the role of the Chief Human Resource officer. The extent of employee representation varies on a 0 to 100 scale, ranging from no institutionalized co-determination to cases in which employees are presented on all dimensions. For this study, we calibrated the ranking into four categories: no co-determination (0), little to medium institutionalized representation (primarily companies with one-third codetermination) (0.33), medium to high representation (companies with parity in the supervisory board but with several deficits in, for example, the composition of the committees) (0.67), and full representation (companies with parity in the supervisory board and little to no deficit in, for example, the composition of committees) (1).

Qualitative Comparative Analysis (QCA) of Corporate Governance Configurations

We used fsQCA 3.0 (Ragin and Davey 2016) to examine the consistency of cases with our outcome (low carbon emissions) across all logically possible combinations of causal conditions using a truth table (see Appendix Table C). Established QCA criteria minimized the table: We utilized a conservative consistency threshold of ≥0.8 (Ragin 2008; Fiss 2011; Misangyi and Acharya 2014; Lewellyn and Fainshmidt 2017) and a minimum number of two cases, appropriate for medium-sized samples (Meuer 2014). Moreover, we included only configurations with a PRI (proportional reduction in inconsistency) measure

Going Back to the Cases: Interviewing Employee Representatives

To deepen our understanding of the mechanisms operating in different corporate governance configurations, we zoomed-in on the actual engagement of employee representatives. Specifically, we returned to the companies underlying our QCA analysis (Ragin 2008) to explore how employee representatives use their formal decision-making rights to engage with corporate environmental impact.

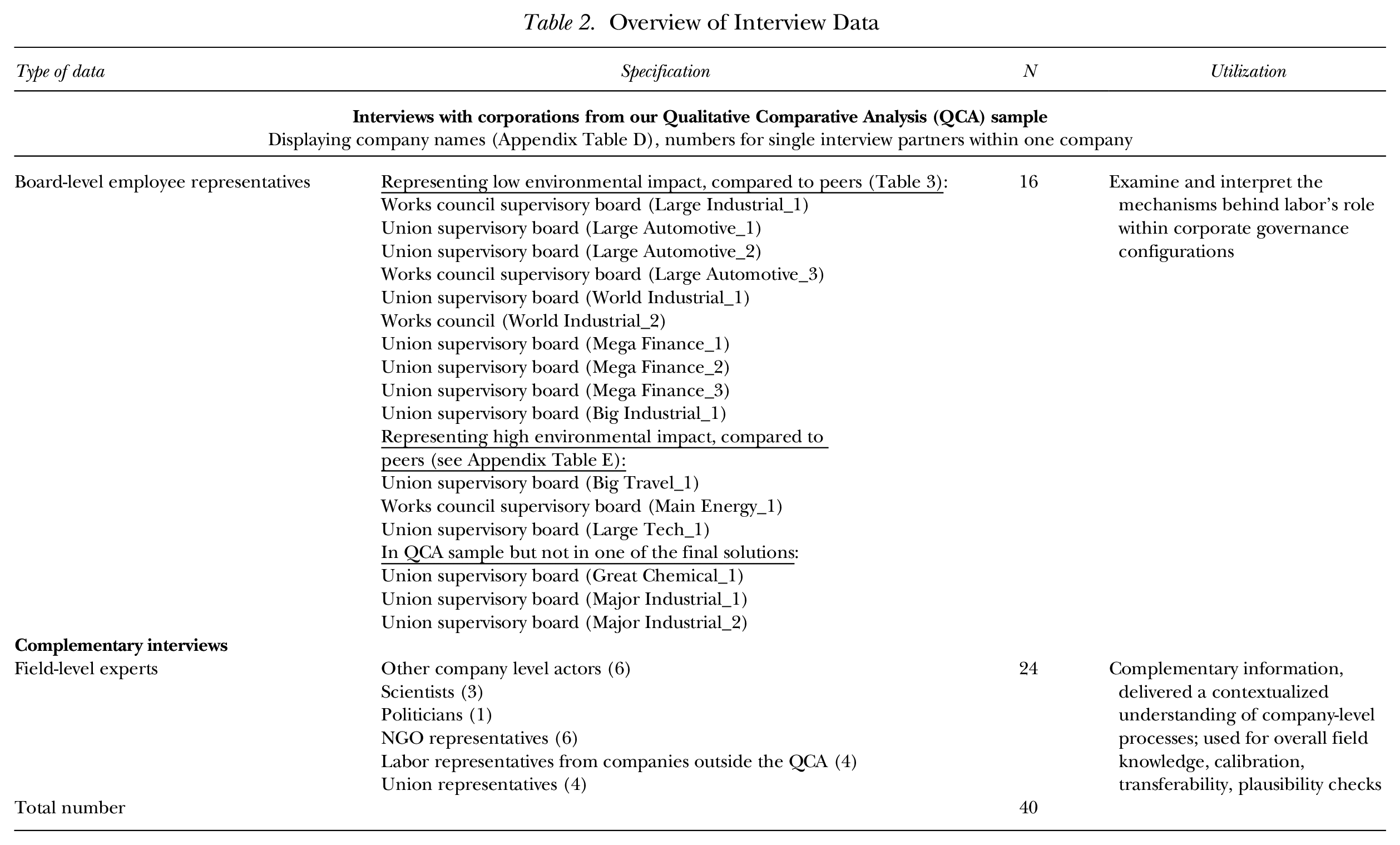

We conducted interviews with board-level employee representatives from the supervisory board of the companies underlying the QCA. To identify interview partners, we used contacts from prior research projects to enter the field and asked our interview partners for further contacts in a snowball-like sampling approach (Biernacki and Waldorf 1981). Since our analysis focuses on configurations for relatively low environmental impact, we aimed for interviewing supervisory board members from at least one company from each pathway in our QCA results (Table 2).

Overview of Interview Data

As a complement, we enriched our understanding through information from field experts (Meuser and Nagel 2002), including NGOs, politicians, scientists, and other company-level actors. These interviews helped to shape our interview questions and informed the calibration of our data in the QCA at the beginning of our research process. Later, the interviews with union representatives and labor representatives from companies outside of our QCA sample were used for plausibility checks and matters of transferability.

The overall data collection led to 40 interviews between 2015 and 2023 (see Table 2): 16 interviews with employee representatives from corporations in our QCA and 24 complementary interviews. The data collection took place at different stages of the research project (see above) but was also slowed down due to COVID and care work responsibilities of the authors (four children were born during the project). The interviews used a set of broad and open-ended questions that developed iteratively during the research process and focused on generating insights on “how” labor representatives engage with corporate environmental policies and impacts. With open-ended questions, we acknowledged that “people’s knowledge, views, understandings, interpretations, experiences, and interactions are meaningful properties of the social reality” (Mason 2002: 63), and actors are knowledgeable agents who self-reflectively make sense and communicate their activities (Giddens 1984). The interview audio was recorded and transcribed verbatim.

Our analysis of labor strategies on environmental impact focuses on the interviews at the firms of our QCA results. We followed a theory-developing coding procedure (Strauss and Corbin 1990; Gioia, Corley, and Hamilton 2013) using the MaxQDA software. First, we conducted an open coding of agentic aspects from employee representatives regarding environmental impact. After the contextual embedding of each individual interview and individual actors, we performed a cross-case analysis by comparing across individual interview partners to identify patterns of activities, while formulating categories that remained very close to the interviews. Second, we undertook some aggregation by identifying recursive instances of strategies intended to influence corporate environmental strategies. Through internal discussions, we identified similarities and differences among activities and grouped them into four strategies. Third, by comparing these strategies, we conceptualized their differences in terms of how they make use of institutionalized decision-making rights and leverage types of power resources (see Table F in the Online Appendix for illustrative quotes). Finally, we zoomed-out (Nicolini 2009) to map these strategies back onto the cases from the QCA results and their respective corporate governance configurations. The research team discussed and interpreted the relationships between strategies and corporate governance configurations in light of our original research question (see Table 4 and related discussion below).

Results

Corporate Governance Configurations for Environmental Impact

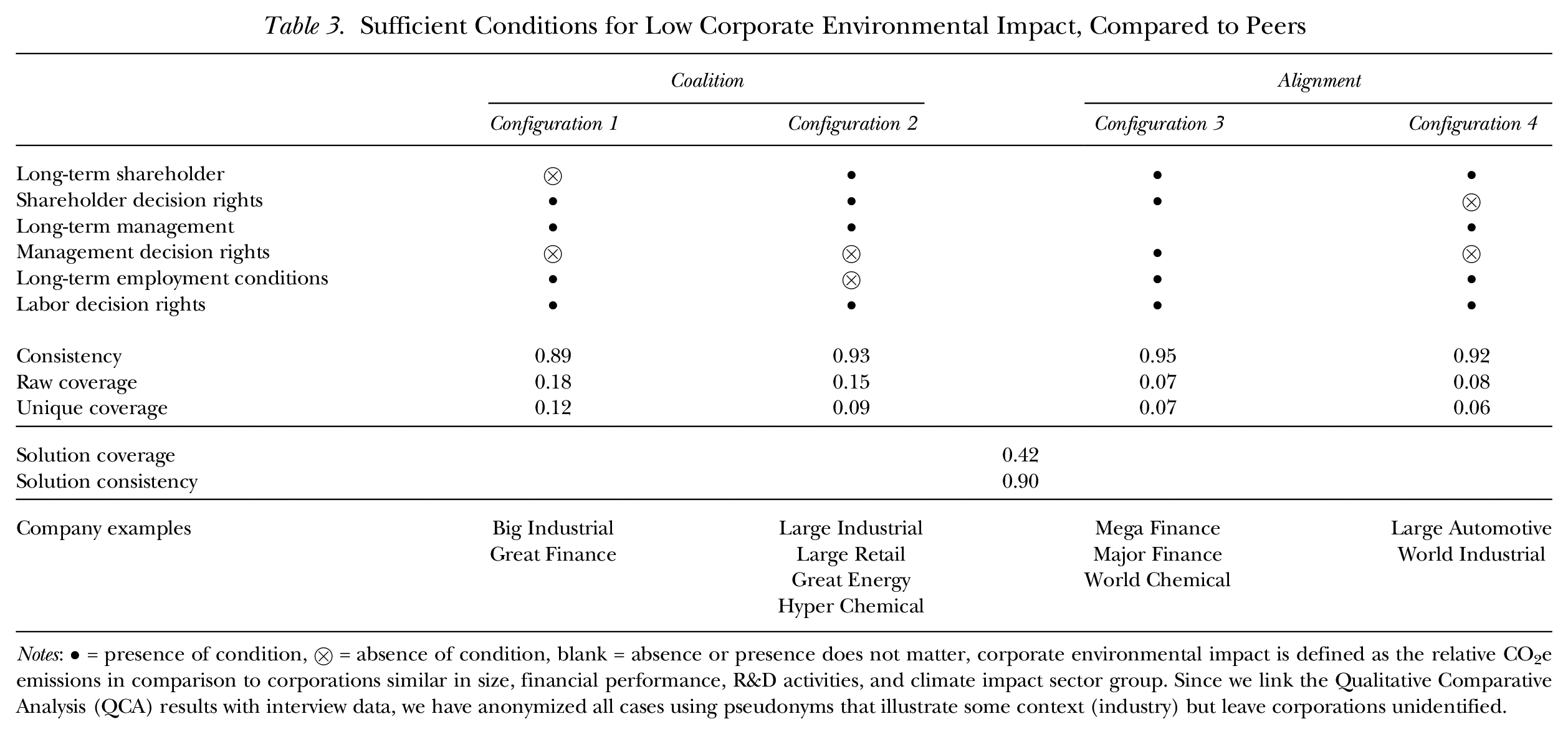

The QCA results identify corporate governance configurations sufficient for low environmental impact. Table 3 summarizes the set-theoretic results, 6 where each column displays a different combination of corporate governance conditions. We denote the presence of a condition with full circles (•) and an absence with barred circles (⨂), while empty cells indicate that this condition bears no relevance (Ragin 2008). We report the consistency and coverage of each configuration plus the overall analysis in which raw coverage includes the overlap between configurations, and unique coverage is the proportion of membership attributed to individual configurations only. Finally, Table 3 reports pseudonyms for the company cases that are empirical examples for each pathway. We stress that corporations with low impact are not necessarily “green” companies but have a low environmental impact relative to peers of similar size, financial performance, R&D expenditure, and from the same climate-impact sector. Moreover, our analysis of necessary conditions showed that no corporate governance condition alone (consistency threshold >0.90) is necessary for low environmental impact.

Sufficient Conditions for Low Corporate Environmental Impact, Compared to Peers

Notes: • = presence of condition, ⨂ = absence of condition, blank = absence or presence does not matter, corporate environmental impact is defined as the relative CO2e emissions in comparison to corporations similar in size, financial performance, R&D activities, and climate impact sector group. Since we link the Qualitative Comparative Analysis (QCA) results with interview data, we have anonymized all cases using pseudonyms that illustrate some context (industry) but leave corporations unidentified.

In Table 3, we group our results into two broad types of corporate governance configurations that are sufficient for low environmental impact, which we term coalition and alignment: 1) coalition involves two actor groups sharing a long-term orientation and exerting power over another actor with a short-term orientation; and 2) the alignment of all three corporate governance actors in favor of long-term rather than short-term orientation. While employee voice is insufficient in isolation, it is a necessary part of configurations that are unnecessary but sufficient for our outcome—so-called INUS conditions (Mackie 1965).

Coalition

In a coalition, corporate actors build alliances with other actors to assert their interests (Aguilera and Jackson 2003). Through coalition making, two actors who are not individually powerful may realize their interests and prevail against the interest of another group by together accumulating sufficient formal decision-making power, such as obtaining a voting majority on the board, but also through informal means of agenda setting (e.g., management proposes something aligned with interests of another group) or influencing the preferences and terms of debate (e.g., building momentum around a business case for environmentalism). Configurations 1 and 2 show two different coalitions: management and labor (configuration 1); and shareholders and management (configuration 2).

Configuration 1 is the management–labor coalition, also commonly conceptualized as an insider-driven pattern, which is typical of German corporate governance. Here, we have managers who are long-term oriented yet not so powerful together with long-term oriented and powerful employee representatives. By joining together, this coalition can consistently achieve low environmental impact: Even if the leading shareholder is powerful and short-term oriented, the coalition of long-term management and employees seems to “outnumber” the shareholder. This configuration has a high consistency of 0.89 and a raw coverage of 0.18, thus covering almost one-fifth of cases.

An example is a vignette of the company we have named Great Finance (to maintain anonymity in this study) (see Table 3). In 2013, Great Finance has a very high level of co-determination, as half the members of the supervisory board are employees. The influential supervisory board committees (e.g., election committee, compensation committee) have parity as well, which is true for only a few German companies (Raabe 2010). More than 90% of the employees are hired as permanent staff (per the Great Finance annual report), thus having long-term employment interests. Meanwhile, corporate management has responsibility for sustainability matters, and executive compensation is neither linked to the company’s stock performance nor other short-term performance measures. Long-term orientation is central to Great Finance’s business strategy (Great Finance annual report), unlike high-risk capital market-oriented banking models. Management’s long-term time horizon overlaps with the long-term interests of employees, thus creating a strong internal coalition that stands in contrast to shareholders—here the majority of shares is held by an owner known for short-term oriented returns. This long-term coalition not only enables long-term profits and wages but also has an environmentally friendly impact (e.g., a steep reduction of CO2e per employee in 2013 compared to the previous year; Great Finance annual report).

Configuration 2 represents a management–shareholder coalition. Here the largest shareholder has strong decision rights and is long-term oriented, entering a coalition with managers who have long-term orientation yet lack strong decision rights. This coalition stands in contrast to employee representatives with strong decision rights, but who are not long-term oriented. This configuration has a consistency of 0.93 and covers almost one-sixth of cases (0.15). Closer qualitative examination suggests that the companies fall into two groups: one with lower-skilled jobs and frequent job changes (Large Industrial and Large Retail); the other with well-protected and remunerated jobs (Great Energy and Hyper Chemical), which have nevertheless faced job loss due to broad sectoral-level decline and restructuring. Given these threats to employment stability, employee representatives may acutely feel a tension between preserving jobs versus protecting the environment. Prior research suggests that German supervisory boards have a strong consensus orientation and rarely engage in adversarial voting (Paster 2012). So, while the management–shareholder coalition may exercise decision-making power, our interviews with Large Industrial suggest that powerful employee representatives were unlikely to openly oppose the introduction of lower impact business strategies if they are perceived to also bolster business competitiveness (see more generally Hagen 2020).

Alignment

The concept of alignment describes corporate governance in which actors’ interests are aligned around the long-term. Alignment around long-term rather than short-term interests is widely assumed to be important for low corporate environmental impact (Slawinski and Bansal 2012, 2015; Linnenluecke, Birt, and Griffiths 2015; Slawinski et al. 2017). From our data, configurations 3 and 4 are examples of alignment with no clear line of conflict between corporate governance actors. Specifically, configuration 3 shows alignment between a powerful, long-term shareholder and powerful, long-term employee representatives. For example, World Chemical has a founding family as a majority shareholder who also holds the seat as chair of the supervisory board. For employees, co-determination is strong, and most employees have permanent contracts and long-term orientations (World Chemical annual report). The strong alignment between long-term owners and employees is also typical for Germany’s insider-oriented corporate governance and described in this case as “Chemie-Sozialpartnerschaft” for which corporate governance seeks to generate long-term competitive advantages and protect the company against external threat (e.g., acquisitions). While the management of World Chemical is also long-term, our QCA solution suggests that managers’ time orientation is irrelevant to the solution (an empty cell in QCA) and therefore the aligned long-term orientation of shareholders and employees is sufficient regardless of whether it extends to managers. 7 This configuration has a consistency of 0.95, but a low coverage of 0.07.

Configuration 4 shows all corporate governance actors aligned as long-term oriented, but only employees have strong decision rights. Configuration 4 has a high consistency of 0.92 but covers slightly less than 10% of cases (0.08). Like the example of configuration 3, both Large Automotive and World Industrial were founded by industrial families who still have substantial influence today or have been replaced by other long-term investors. Like World Chemical, these cases are well-known examples of the German “Sozialpartnerschaft” central to the Deutschland AG (Beyer 2003). As we show later in the article, the role of employee representation is important here in driving environmental strategy through strategies that engage relatively weak but at least tacitly aligned long-term shareholders and managers.

Back to the Cases: Strategies of Environmental Engagement by Board-Level Employee Representatives

Our qualitative analysis focuses on the mechanisms of how employee voice shapes corporate environmental impact using interviews of employee representatives from the companies underlying the QCA analysis. We identified four strategies of engagement with environmental issues (see Table F in the Online Appendix for an overview) by employee representatives in the supervisory board.

A common feature of all four strategies is a focus on temporality, as highlighted by past research on corporate environmental impact (most prominently Slawinski and Bansal 2012). Engagement centers on the construction of a “more sustainable” future narrative, which Bansal, Reinecke, Suddaby, and Langley (2022: 10) described as the “performative power of projecting desirable futures” (for a broader discussion on future and meaning, see Beckert 2016). “Futurescapes” provide a symbolic framing through which actors exercise softer forms of power by establishing narratives linking corporate sustainability to other future-directed yet consensual issues.

The four strategies differ in how employee representatives mobilize types of power resources. One dimension of formal-legal power is rooted in the legal structure of the corporations and the rights of employee representatives on the supervisory board, which create potential influence on decision-making regarding environmental issues. However, employee representatives never constitute the majority on a board and cannot unilaterally make board-level decisions. Rather, we must consider a wider set of power resources used by employee representatives to set agendas or shape perception of other actors through wider narratives. For instance, employees may seek to mobilize ideational power (Carstensen et al. 2022) to shape the corporate environmental strategy. Moreover, employee representatives also mobilize organizational power resources rooted in their knowledge, experience, and active role in the organizational processes that play a role for the environmental impact of the company. Taken together, the four strategies draw upon one or more different power resources and should not be understood as exhaustive nor mutually exclusive (different strategies can occur simultaneously in one corporation).

Making the Business Case

This strategy involves promoting environmental actions by appealing to the idea of the business case. Employee representatives attempt to justify environmental measures in economic terms by highlighting the opportunities for profit. Compared to the strategy of co-managing (see below), employee representatives are less involved in the implementation of specific environmental policies or programs; instead their cooperation manifests on an ideational level. Employee voice focuses on establishing the idea that environmental protection is good for the viability of the corporation: [Our company] also recognizes quite clearly that we need a transformation to green. Otherwise, we will not be fit for the future, because we would have to pay so much money otherwise, for example for certificate trading, or we will fall behind other competitors. (Union Major Industrial 1)

In making the business case for low environmental impact, employee representatives endorse the logic of management. Sustainability is seen as an ingredient for the jointly desired future economic prosperity in the long-term rather than short-term. Employee representatives appeal to the idea of economic gains: But normally it is so that, if, one must push it . . . over the employee bench and it is always best . . . if one can seize them at the economic screw and say that CSR can pay off for you. And if you point that out, whether it’s in resource consumption or waste minimization, you can get them, and they’ll listen. (Union Big Industrial 1)

Engagement using this strategy commonly stresses the idea of ensuring long-term competitiveness and thus preserving jobs. Employee representatives compare and benchmark the sustainability strategy of their own company to that of other companies. Interestingly, here, information gained through the network connecting employee representatives to the wider trade union movement plays an important role in benchmarking: We said to companies that did not participate in the process [to develop some sustainability related measure], “Here, take a look! They used to do it this way, and that would be something for you, too.” In other words, to use illustrative projects to make clear what is ultimately also possible at other companies that are comparable. (Union Big Industrial 1)

Co-Managing

The second strategy is co-managing, in which employee representatives take on managerial tasks around environmental topics. Co-management practices are widespread in Germany, where labor representatives on the supervisory boards and works councils internalize managerial perspectives and tasks in their cooperation with management (Kotthoff 1981). Such co-operation is underwritten by law, as the Works Constitution Act obliges works councils to act for the good of the company. Since works council representatives are often part of the supervisory board, these cooperative strategies span and connect different levels of the organization. That said, co-managing is also drawing on formal, institutionally granted power resources. Yet, it is not going into opposition to management by the leverage of labor power. Instead, labor representatives in the supervisory board use the formal, institutionally granted power resource for co-operation and thereby attempt to ensure involvement in the strategizing process.

Co-managing diffuses environmental ideas and measures throughout an organization by using the organizational capacities and potential for taking initiative as employees in running the business together with its management. Involvement goes beyond working conditions and relates to a wider gambit of business management. For example, a union representative on a supervisory board reported how labor representatives train employees to develop strategies throughout the organization for increasing efficiency and productivity in ways that bolster sustainability: I talked [with management] about our work and innovation project. We trained works council members to become innovation promoters. [I talked] about the learning factory in Berlin [changed for anonymity reasons], among other places. How can you simply recognize things in sustainability management where a company can become more efficient, more cost-efficient, and thus secure jobs? How can you develop strategies–that’s where the keyword came from–better instead of cheaper? (Union Big Industrial 1)

Here, employee representatives embrace corporate goals but frame them as a desirable future in which environmental goals, business goals, and employment issues such as job security are reconciled.

Co-managing environmental issues may thus create a visible blurring between the roles of employee representatives and management. One union representative reported: And I was then rather brusquely told by the shareholders that it wasn’t a question of whether it [sustainability] would pay off, so now we’re just swapping roles, but that it was inevitable that [the company] would have to deal with sustainability and become sustainable. (Union Mega Finance 3)

Two aspects are striking. First, long-term orientation is brought in by reconciling profitability and sustainability, which is also key in the strategy of “making the business case.” Second, employee representatives take on managerial tasks and raise strategic questions. Here, co-managing strategies rely on organizational power resources rooted in the competence and knowledge of everyday business operations.

Agenda Setting

The third strategy describes influencing the agenda in board meetings. Employee representatives seek to diffuse sustainability ideas and measures by using their formal-legal power within the institutional setting of board-level co-determination and to raise environmental issues in contexts where they were not present before—if necessary, even against the interests of other actors. This strategy may also involve making the business case, but it goes beyond this by mobilizing their formal decision-making rights to leverage their ideational power more fully. According to one interviewee: We drove them [other board members] forward and sensitized them to [sustainability] issues that previously played no role. (Union Mega Finance 2)

At first glance, this strategy does not lead to specific and binding outcomes, at least in the short term, although it can become performative in the long run. With the help of formal-legal power, employee representatives set an agenda of discourse that can be built upon in the future. It appeals to the ideas and preferences of supervisory board members by stressing a clear time dimension whereby the past is narratively framed as deficient compared to a “desirable future.” Through their engagement, employee representatives raise awareness among board members about sustainability and call on them to be responsible.

Yes, of course, we are also reacting in the same way that society as a whole is reacting to climate change and the corresponding demands for CO2 reduction, but I believe that in my experience we are very much the driver at the corporate level. Simply because, from the point of view of shareholders or management, the focus of their interest is on generating profit. (Union Large Automotive 2)

Dealing

The strategy of dealing describes realizing sustainability measures in exchange for cooperation or concessions on other issues. Here, employee representatives again mobilize their formal-legal power resource but leverage this in actual negotiations in which they can exercise a potential veto. For example, since management compensation is set by the supervisory board, employee representatives argued for the inclusion of sustainability criteria in performance pay targets: The compensation of the Management Board has also been linked to some extent to the issue of sustainability. Because we said that if this issue is kept completely out of the compensation, there is no incentive in the company to do anything about it. . . . That’s why it was important to us that it was included as a certain part of the remuneration, so that it’s also clear that you have to consciously introduce decisions and measures that promote and stabilize sustainability. (Works Council Large Automotive 3)

Dealing thus creates leverage by threatening non-cooperation, but dealing is only possible if employee representatives have something important to “give” in return: So, in order for us to talk to him [the CEO] again about other issues, he agreed to pass certain board resolutions and, for example, to ban flights within Germany. (Union Mega Finance 2)

While research on supervisory boards has documented these strategies in promoting social issues, what is striking here is that employees clearly also “deal” for environmental concerns. Dealing thus combines organizational power resources with formal-legal power in the board itself.

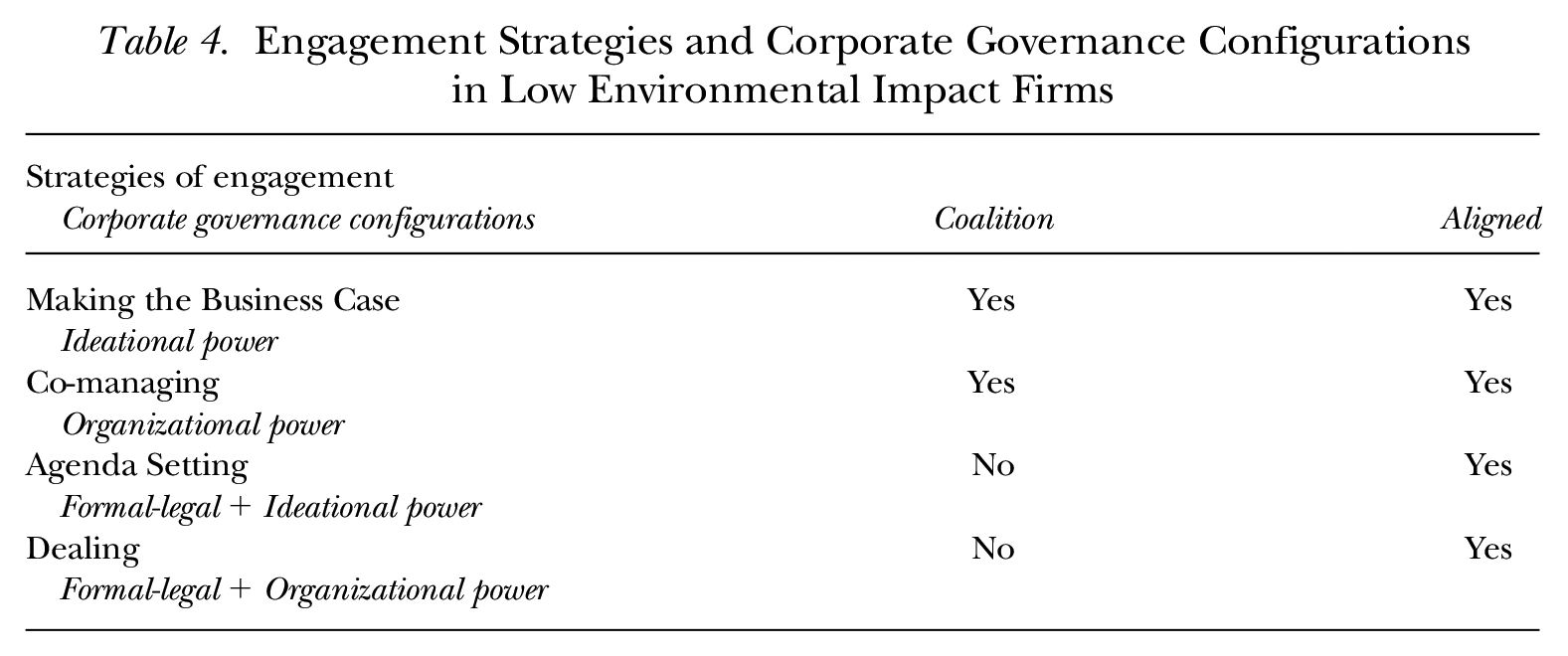

Linking the Strategies and Corporate Governance Configurations

Our findings suggest that various strategies and their related power resources are present within different types of corporate governance configurations. Specifically, we link the findings from our interviews with typical examples from our QCA of corporate governance configurations. While all corporate governance configurations associated with lower environmental impact have strong decision rights for employees, we found that employees enact power resources in ways that differ from one another (and with differing strategies) in the cases of coalition and alignment, as presented in Table 4.

Engagement Strategies and Corporate Governance Configurations in Low Environmental Impact Firms

In corporate governance configurations based on coalitions, at least one actor is opposed to long-term environmental strategies. In this context, we found that employee representatives are limited to strategies of making the business case and co-managing, since these depend less on leveraging formal-legal power resources. Both strategies follow a broad business logic by pursuing the idea of making environmental protection a win for business performance. These strategies thus reflect a pragmatic and incremental approach, in which the environment is “camouflaged” within a context of corporate environmentalism. By making the business case based on the power of the idea itself, employee voice may use persuasion to forge alliances with other long-term actors but simultaneously limit resistance from other short-term actors. One such example is Big Industrial, where long-term employees and management faced a short-term owner (see Table 3). Here, employee representatives relied on organizational resources such as training employees to recognize innovation potential around sustainability management, thereby framing win-win scenarios between environment and business performance. By contrast, employee representatives lacked sufficient power to create deals around pro-environment decisions against the wishes of other actor groups. For example, in the case of Large Industrial, a deal was proposed by the employee side, but it failed.

By contrast, strategies of agenda setting and dealing involve greater mobilization of formal-legal power resources, and they were evident only in configurations of alignment. Our results suggest that leveraging formal-legal power requires not only a strong position for negotiation but also managers and/or owners who are interested in pursuing an environmental agenda. When actors align on a long-term perspective, resistance to sustainability is weaker and decision-making is focused more on what and how to make improvements, rather than on whether to do so at all. For example, at Large Automotive (see Table 3), employee representatives refused to approve a business plan for the coming year because it was not considered sustainable and was insufficient to promote the transformation.

Discussion and Conclusion

In this article we ask how employee voice in corporate governance influences corporate environmental impact and what strategies employee representatives use to engage with environmental issues. The empirical QCA of German corporations shows that strong employee representatives play an integral role in lowering levels of carbon emissions and do so as part of wider corporate governance configurations characterized by either coalition or alignment with managers and shareholders. Our interview data further reveal four distinct strategies for engaging with environmental issues that mobilize different types of power resources.

First, our article contributes to growing research on employment relations and the natural environment. While we know that unions can play a key role in environmental movements (e.g., Räthzel et al. 2010; Barca and Leonardi 2018; Stevis et al. 2018; Räthzel et al. 2021) and individual employees also promote environmental issues in organizations (Markey et al. 2019), less research has focused on whether employee voice in corporate governance may support, impair, or have little impact on corporate environmental performance. This issue is central to understanding how corporations may or may not transform their activities in the face of climate change, as well as the prospects of a “just transition” in the face of short-term risks to job stability during environmental transition (Flanagan and Goods 2022).

Our findings highlight the positive role and scope for agency by employee representatives. Our QCA model had a coverage score of 0.42, thus confirming that corporate governance is an important factor in explaining organizational-level differences in environmental impact. Within the four configurations identified, strong employee representation was a feature of all pathways to lower environmental impact. As such, employee voice can be interpreted as an INUS (insufficient but non-redundant part of an unnecessary but sufficient) condition—employee voice does not impact the environment in isolation, but as a central ingredient within a wider configuration of corporate governance factors. In most cases, employee voice was underpinned by a core of long-term orientated employment, linking future job stability with pro-environmental actions. But even in some cases when employees have relatively short-term employment spells, strong employee representatives engaged for improvements in the corporate environmental performance.

Second, this article extends a small yet growing field of corporate governance literature that takes employee voice seriously (Aguilera et al. 2021). Most research on co-determination has used quantitative data to examine whether employee representation influences shareholder wealth, labor productivity, or other aspects of employment relations (Jäger, Noy, and Schoefer 2022), but the research has tended to examine its impact in isolation from other corporate governance factors. By contrast, we adopt a configurational perspective (e.g., Fiss 2007, 2011; Fiss et al. 2013; Misangyi et al. 2017; Greckhamer et al. 2018) to highlight how employee voice unfolds in conjunction with wider alignment with shareholders and managers on long-term time horizons or unfolds through coalitions with other actors. The role of shareholders and managers alone is not sufficient to explain why a corporation’s impact on the environment is low (Walls, Berrone, and Phan 2012; Walls and Berrone 2017), but in Germany a corporation’s impact depends on the role of employee voice within these configurations. Such conjunctural effects of corporate governance structures may be easily missed in traditional quantitative studies, which focus on the net effects of single variables in isolation.

Like Benassi (2023) has shown for HR practices, the positive effects of employee voice depend on how employee representatives use their voice and thereby mobilize and enact various types of power resources (Refslund and Arnholtz 2022). But note that employee representatives never hold a structural majority in the board that would enable them to impose decisions unilaterally based on formal-legal power. Rather, we show how they use their position to enact different strategies of engagement with environmental issues, making the business case, co-management, agenda setting, and deal making. Several strategies rely strongly on ideational power (Carstensen et al. 2022) rooted in the idea of a strong business case for environmentalism, which is effective given its alignment with already hegemonic management ideas (Rothstein 2022). More generally, we find that strategies for employee voice are more restricted when owners and managers lack alignment on long-term goals. Here employee representatives must rely on coalitions with other actors by seeking to legitimize environmental action by making a business case or strengthening implementation through co-management. Meanwhile, where greater alignment exists, employee representatives have greater scope to also use formal-legal power resources more directly to further environmental agendas through agenda setting or dealing. Thus, our article shows a potential to further dialogue between power resource theory (Refslund and Arnholtz 2022) and corporate governance research (Aguilera et al. 2021).

Our findings have important practical implications. Employees are not necessarily aligned to organizational change when transition to low carbon activities may threaten jobs or vested interests of employee groups. However, strong employee voice may help align employee representatives as supporters or even crucial drivers of environmentally friendly strategies. Employee representatives, unions, and other actors may also draw insights about the repertoire of strategies for engaging with environmental issues, and the conditions under which these are likely to be successful. Successful positioning on the topic of sustainability is also an opportunity for a union renewal (Farnhill 2018; Allan and Robinson 2022). Furthermore, at the level of public policy, our findings suggest that the agenda of promoting sustainable corporate practices would benefit from revisiting the issue of employee representation on corporate boards as part of good corporate governance (Vitols and Kluge 2011). Nonetheless, our results show a tendency for employee representatives to adopt managerial logic, suggesting that the distinct contribution of employee voice remains circumscribed by the wider context of corporate capitalism (Wright and Nyberg 2017)—within which environmental gains at the corporate level are only relative and still fall far short of addressing the grand challenge of climate change (Giuliani 2018; Dörrenbächer, Geppert, and Bozkurt 2024).

This article has several limitations that suggest the need for future research. First, the QCA analysis is based on German stock market–listed corporations subject to requirements for board-level employee representation. Further research could extend this analysis over time or compare Germany with other countries with board-level employee representation. Our sample is also focused on rather traditional industries whereas many green industries are populated with smaller and younger firms that often fall outside traditional forms of employee representation. Representation by trade unions or works councils appears especially problematic in green industries (Helfen, Nicklich, and Sydow 2019), which are part of a wider decline in co-determination in Germany (e.g., employees covered by a works council) (Townsend, Demarie, and Hendrickson 2016). Such developments would need to be addressed in future research. Second, our conceptualization and measurement of environmental performance capture the relative performance of companies, as is common across most similar studies. “Relatively low environmental impact” describes companies that perform better than others but does not mean that corporations perform well in absolute terms (e.g., being on track to meet global goals on emissions reduction). Given the urgency of climate issues, future research should calibrate concepts and measurement more strongly to public policy targets. Third, our study drew upon interviews with employee representatives. Despite the challenges of access, we see potential for qualitative research to take a more holistic view by interviewing the entire set of corporate governance actors in the same companies, including management and shareholders. This approach could examine more nuanced aspects of corporate governance configurations and extend our understanding of the engagement strategies presented.

Supplemental Material

sj-pdf-1-ilr-10.1177_00197939251351678 – Supplemental material for Employee Voice and Corporate Governance: Power and Engagement for the Environment

Supplemental material, sj-pdf-1-ilr-10.1177_00197939251351678 for Employee Voice and Corporate Governance: Power and Engagement for the Environment by Julia Bartosch, Manuel Nicklich and Gregory Jackson in ILR Review

Footnotes

For general questions as well as for information regarding the data and/or computer programs used to generate the results presented in the article, please contact the lead author, Julia Bartosch, at

1

CDP provides a framework for reporting on CO2 equivalent (CO2e) emissions yet leaves some leeway for companies regarding their actual data collection and estimation methods.

2

All control variables increase the model fit, and together they explain almost 50% of variance in CO2e as emissions (adjusted r-square is 0.45).

3

Secondary data were used to create our own classification. Using the name of the owner with the largest number of shares, we classified this information (investment manager, investment bank, bank, state, holding, pension fund, labor fund, family or individual, foundation, or other company) in ownership types (short-term, more short-term, more long-term, long-term), relying on Banker Thomson One and our own web research. Classifying was done by two researchers independently and double-checked by coder triangulation on a smaller sample.

4

We are aware that a simple reduction in terms of “secure working conditions equal interest in environmental topics” is not reflecting many empirical cases of working-class environmentalism. Therefore, this is a proxy while being fully aware that such use can further manifest this superficial idea (![]() ).

).

5

6

We show the intermediary solution as a standard procedure in QCA research.

7

In cases where managers are short-term, configuration 3 could also be interpreted as a coalition wherein shareholders and employees exert power over managers.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.