Abstract

In African countries such as Ghana, microentrepreneurs make formal economy goods and services available to base of the pyramid (BOP) consumers. Multinational enterprises (MNEs) co-opt BOP business models when they enter the BOP market. We conducted a case study of six MNEs and 36 microentrepreneurs in three key sectors. In two sectors (fast-moving consumer goods and telecommunications), reverse bridging enables MNEs to capture value from BOP business models, which has a negative impact on both the financial and social capital of microentrepreneurs. In the third sector (finance), microentrepreneurs are buffered from the negative effects of co-optation through a process of integrating, which enhances their social capital but reduces their financial capital. Our research contributes to the BOP literature, first by demonstrating that financial and social capital are intertwined at the BOP level, and second by analyzing how the negative effects of co-optation can be cushioned by enhancing microentrepreneurs’ social capital.

Keywords

Base of the pyramid (BOP) approaches were initially heralded as a way for multinational enterprises (MNEs) to expand their markets by catering profitably to the global poor while also offering poor consumers better goods and services to which they previously had no access (Prahalad, 2009). Early critics highlighted that the poor needed to be involved in such commercial activities not just as consumers but also as producers (Karnani, 2007). In response, proponents of the BOP approach shifted their focus toward co-creation activities involving different stakeholders to increase both the inclusivity and suitability of BOP business models (London & Hart, 2004; Prahalad & Ramaswamy, 2004). Co-creation was seen as addressing the institutional distance that MNEs faced when engaging with BOP consumers (Rivera-Santos et al., 2012; Schuster & Holtbrügge, 2014; Webb et al., 2010). This also highlighted the potential role of domestic BOP entrepreneurs (Rivera-Santos & Rufín, 2010; Webb et al., 2010). Recent research has drawn attention to the fact that co-creation and entrepreneurial BOP activities do not necessarily alleviate poverty. This complicates the BOP premise of commercially engaging the poor for mutual benefit (Banerjee & Jackson, 2017; Hall et al., 2012; Nahi, 2016).

The African continent was initially not well represented in BOP research (Kolk et al., 2013), and more research on the developmental potential of entrepreneurship in Africa is still needed (Vermeire & Bruton, 2016). There are some studies on African entrepreneurship that investigate the impact of institutional constraints (Saka-Helmhout et al., 2020), the role of history (Decker et al., 2020), and responses to poverty and resource constraints at the BOP level (Slade-Shantz et al., 2018; Yessoufou et al., 2018). The continent is home to 54 states that reflect diverse conditions and legacies, but research tends to focus on only a small number of these states (Taylor, 2020). This observation highlights how representation of the continent remains partial.

More research is needed to explore whether the BOP strategies of MNEs are displacing or disrupting African microentrepreneurs, who are essential to marginalized communities (Ansari et al., 2012; Warnholz, 2007). Thus, our line of enquiry focuses on how microentrepreneurs in Ghana make goods and services from the formal economy accessible to poor consumers in the informal economy. This pattern from the formal to the informal economy occurs across the African continent (Webb et al., 2020). We define the informal economy as untaxed and unregulated but not necessarily illegal (Godfrey, 2011; Webb et al., 2010). We use the term “BOP strategies” to describe approaches aimed at penetrating the market in the informal economy, which suffers from poverty and resource constraints. We analyze the BOP business models developed by microentrepreneurs in the West African country of Ghana and co-opted by MNEs to denote how value is created, and how and by whom it is captured (Richardson, 2008).

We focus on the BOP initiatives of MNEs and the microentrepreneurs with which they partner in Ghana, a politically stable democracy that has seen economic growth and an increased inflow of foreign direct investment since the 1990s, but which still has a high poverty rate at 21.4% (World Bank Group, 2016). We interviewed 36 microentrepreneurs across three different sectors: fast-moving consumer goods (FMCG), telecommunications, and finance. We also interviewed 18 managers from six MNEs in these sectors (54 interviews in total). We use a business model approach to understand value creation and capture at the BOP level to answer the research question: Are BOP business models co-opted by MNEs, and if so, how? Our research found that the impact on microentrepreneurs’ financial and social capital varied by sector and business model. We argue that microentrepreneurs made goods and services from the formal economy available to the poor but that co-optation by MNEs mostly creates value at the margins while capturing value at the expense of microentrepreneurs. We outline two processes of business model co-optation in FMCG and telecommunications: bridging and reverse bridging. These first reduce microentrepreneurs’ financial capital and consequently their social capital. Second, we outline the processes of substituting and integrating, which occur in the finance sector. Together they enhance microentrepreneurs’ social capital but reduce their financial capital. Our research contributes to the debates on whether MNEs’ engagement at the BOP level is beneficial to the development of informal entrepreneurship in developing countries (Vermeire & Bruton, 2016), and whether MNE engagement enhances or damages the social capital of BOP microentrepreneurs and their communities (Ansari et al., 2012).

BOP Entrepreneurs and Business Models

Local microentrepreneurs serve as agents that move goods and services in their communities, and this occurs in the informal economy throughout sub-Saharan Africa (Woodward et al., 2014). These activities have recently attracted attention in the literature (Lutz et al., 2021; Slade-Shantz et al., 2018; Webb et al., 2020; Yessoufou et al., 2018). For example, Seelos and Mair (2007) draw attention to the fact that existing capabilities of local BOP businesses can be leveraged to build new markets that cater to the poor and are profitable at the same time (Dolan & Scott, 2009). The contributions of these microentrepreneurs in alleviating poverty and improving living conditions in their communities have become areas of interest to scholars (Arnold & Valentin, 2013; Brix-Asala et al., 2016; Brix-Asala & Seuring, 2020; Dembek et al., 2018; Heuer et al., 2020; Rosca & Bendul, 2019).

Informal microentrepreneurs deliver products to markets underserved by the formal economy (Webb et al., 2020), and they may become distribution networks for MNEs (Rivera-Santos & Rufín, 2010). Vermeire and Bruton (2016) argued that poverty and entrepreneurship in sub-Saharan Africa are under-researched, even though entrepreneurship has the potential to offer local solutions that ameliorate poverty. An early study that focused on BOP entrepreneurs as drivers of innovation (Hall et al., 2012) cautioned that innovation at the BOP level does not necessarily result in positive social impacts (see also Arnould & Mohr, 2005).

Since London (2008) and Prahalad and colleagues (Prahalad, 2004; Prahalad & Hammond, 2002; Prahalad & Hart, 2002) introduced the BOP concept, the debate has shifted toward co-invention as a central component of BOP approaches, with a focus on building local capacity (London & Hart, 2004). Co-invention and co-creation at the BOP level address the issue of significant institutional distance (Schuster & Holtbrügge, 2012; Webb et al., 2010), but it is difficult for MNEs to meaningfully innovate in and for BOP markets, as they often do not understand the specific needs of low-income customers (Subrahmanyan et al., 2008). MNEs also struggle to gain local legitimacy in BOP communities that are highly mistrustful of strangers (Rivera-Santos & Rufín, 2010), especially those communities with a colonial history (Claus et al., 2021; Mason et al., 2017).

Scholars have questioned whether MNEs are indeed suitable partners to address issues of poverty (Sinkovics et al., 2014). Chmielewski et al. (2020) argue social enterprises are better at forming inclusive business structures than are large MNEs because they have a more focused vision and purpose, and they work more effectively with grassroots partners, leading to complex networks of nontraditional partnerships. Other scholars have challenged the notion of co-creation because of the potential exploitation of consumers when the roles of consumer and producer become blurred (Cova et al., 2011). Rivera-Santos and Rufín (2010) have argued that co-creation is likely to make the role of MNEs less central in partnerships at the BOP level. Nahi’s (2016) review of the co-creation literature criticizes that some definitions of co-creation do not even entail interfirm activities, and some highlight that engaging MNEs’ local staff is sufficient to claim co-creation (Berger et al., 2011).

Co-creation activities by MNEs at the BOP level can easily lead to co-optation, given that they are ultimately conceived around innovative business models that address the needs of the poor but in a profitable manner (London & Hart, 2004). Definitions of business models abound, so our research targets how firms create, deliver, and capture value (Richardson, 2008). The BOP literature often focuses on the creation of value through disruptive innovation (Hart & Christensen, 2002), but it also tends to focus less on who creates the value and who captures it. Early BOP research identified MNEs as innovators of BOP business models (Hall et al., 2012; Prahalad, 2009). This line of enquiry has been extended: large domestic firms, nongovernmental organizations, governments, and small and medium enterprises have all been identified as alternative sources of innovation (Altman et al., 2009; Anderson & Markides, 2007; Arnould & Mohr, 2005; Brinkerhoff, 2008; Hahn, 2009; Johnson, 2007; José, 2008).

Recent work has looked at the opportunities and constraints faced by African microentrepreneurs (Decker et al., 2020; Saka-Helmhout et al., 2020). Slade-Shantz and colleagues (2018) describe how the dense and isolated networks of BOP entrepreneurs limit choices for growth and innovation, and Saka-Helmhout and colleagues (2020) describe how microentrepreneurs at the BOP level are essentially copying the incremental innovations they encounter. We acknowledge that individual BOP microentrepreneurs may well only copy or innovate in minor ways, but we also argue that this innovation needs to be considered cumulatively, collectively, and historically. Mason and colleagues (2013, 2017) remind us that we can only understand BOP markets if we understand how their histories inform their practices and that we should view them as spaces of learning. Concepts such as co-creation assume that innovation is linked to the superior knowledge and resources that the MNEs contribute, while microentrepreneurs only assist with opportunity identification.

Our research challenges such assumptions about the nature of co-creation in BOP business models that connect microentrepreneurs with MNEs. Building on lines of research that conceptualize the BOP as a market (Mason et al., 2017), clusters (Arnould & Mohr, 2005), and network (Rivera-Santos & Rufín, 2010), we argue that microentrepreneurs at the BOP level create value by mediating between the formal and the informal economies (Webb et al., 2020). Rivera and Rufín (2010) highlight the benefits that firms can gain if they “bridge” structural gaps in the network and that such structural gaps are most common at the intersection of formal and the informal economies. MNEs, however, can “muscle in” on the value-creation activities of microenterprises and ultimately hurt small businesses and threaten local jobs and thus household incomes (Warnholz, 2007).

How such economic relationships affect the social capital of poor communities (Ansari et al., 2012) is another aspect of co-creation activities that has not yet seen extensive research. There is evidence that the substitution of traditional relationships by marketized exchange may create or worsen vulnerabilities (Banerjee & Jackson, 2017). Social capital, which confers local benefits such as credit or philanthropy, can accumulate through developing informal support networks in communities (Slade-Shantz et al., 2018), and these networks cannot easily be copied by MNEs seeking to enter BOP markets (Rivera-Santos & Rufín, 2010). This makes collaboration with microentrepreneurs desirable for MNEs but raises the question of whether, from the community’s perspective, co-creation or indeed co-optation by MNEs enhances or destroys their existing social capital (Ansari et al., 2012). Our study offers a better understanding of how microenterprise business models are co-opted by MNEs, and what factors influence this outcome. After investigating three sectors at the BOP level (FMCG, telecommunications, and finance), we identify two business models: bridging and substituting. While both models are co-opted by MNEs, we find that bridging reduces microentrepreneurs’ social capital and substituting maintains or even enhances it.

Research Methods

Research Setting

Our research focuses on the interaction between foreign MNEs and domestic microentrepreneurs operating in the informal economy in Ghana, which has nearly 30 million inhabitants. Ghana has been a democracy since the early 1990s, and a middle-income country since 2007. It has made significant progress against poverty, and now has a lower poverty rate than other sub-Saharan African and middle-income countries (Tanaka, 2019). The MNEs examined in our study are registered and taxed and operate in the formal economy. The microentrepreneurs in our study operate in the informal economy, and none are registered or pay taxes. Ghana’s government has been relatively hostile toward the informal economy (Akuoko et al., 2021), even though the Ghana Statistical Service estimates that about 80% of the population is employed in the informal sector (Koto, 2015). Thus, microenterprises are important sources of household income for Ghanaians who cannot find employment in the formal economy.

Ghana saw significant poverty alleviation in the 1990s and experienced economic growth in the next decade. This meant that by the early 2000s, foreign MNEs operating in Ghana became interested in the BOP level as a new market for their products and services. However, such goods and services were already accessible to poor communities through microentrepreneurs acting as intermediaries between the formal and informal economies. In our study, we focus on how MNEs co-opted microentrepreneur businesses in FMCG, telecommunications, and finance.

Consumer goods have long been accessible in informal markets. For example, instead of supermarkets, many consumers purchase goods from small shops, tabletop sellers, and hawkers (people who sell on the streets with no fixed place of business). This business model has a long history, and it relies on these traders in poor communities to buy goods in bulk and then sell them in smaller and more affordable quantities (Murillo, 2011). Dowuona-Hammond and Atuguba (2008) found that microentrepreneurs in the FMCG sector earn their livelihoods by selling a range of repackaged consumer products made by MNEs—in particular, processed foods, soaps, and detergents.

In the telecommunications sector, access to telephones was difficult for individual households, with few households having phonelines and few public phone boxes available for everyone else. This changed with the advent of mobile telephony in the mid- to late 2000s. In 2012, Ghana still had only 285,000 fixed telephone lines, placing the country 120th in the world, yet it also had 25.6 million mobile phones (placing it 42nd in the world), and more than 80% of Ghanaians had access to mobile phones (The Economist, 2016). In 2010, two fixed-line and six mobile phone companies were authorized to operate in Ghana, but growth and competition have been encouraged in the sector, so mergers and takeovers have reduced this total number to four.

In the finance sector, microfinance is a well-known innovative approach to providing banking services to the poor (Yunus, 2007), and it serves lower-income clients via delivery methods developed in the late 1980s (Christen et al., 2004). Microfinance is, however, predated by more traditional financial practices, such as credit circles run by susu (literally “small” in Twi) collectors in Ghana (Dorado, 2015). Prior to the 2000s, these susu collectors made rounds at markets, local kiosks, and shops, where they collected regular small deposits from traders who could not get to a bank during normal banking hours or whose savings were too small for traditional bank accounts (Aryeetey, 2008). Collected deposits were available to clients after a set period or to borrowers within the scheme for a fee. These traditional financial services are known as Rotating Credit and Savings Associations (RoSCAs) (De Aghion & Morduch, 2000; Mersland, 2011; Roodman, 2012; Rutherford, 2000).

Established banks, domestic and foreign, did not deal with small amounts of money, either for savers or borrowers, so those in poor communities had no access to banking services. In the 2000s, with the advent of global microfinance (Yunus, 2007), some banks in Ghana began to experiment with smaller accounts and to offer services to susu collectors. Banks in Ghana can now legally engage in microfinance by expanding their activities “downwards” (Dorado, 2015), whereas microfinance organizations are registered as nonbanking financial institutions. In the formal banking sector, lending money involves long-term procedures and official documentation, such as land or birth certificates, before loans may be approved (Arp et al., 2016). Interest rates for loans in microfinance and traditional finance are usually higher than at banks but lower than other informal lenders, such as loan sharks (Dorado, 2015). In Ghana, the bank lending rate (the average rate of interest) charged on short-term loans by banks between 2005 and 2017 was 35.5%, reaching an all-time high of 42.84% in July 2016. (There was a record low of 21.24% in March 2008.) Meanwhile, microfinance institutions charge between 48% and 78% per annum (Trading Economics, 2018).

Research Design

Our research examines the FMCG, telecommunications, and microfinance sectors, and our research design followed a multiple-case study approach (Ghauri, 2011; Seawright & Gerring, 2008; Welch et al., 2011; Yin, 2003). This allowed us to recognize both similarities and differences among companies and sectors. We focused on qualitative research to understand better how MNEs and microentrepreneurs developed BOP-level business models, whether co-creation was taking place, and how both parties viewed their businesses development since the MNEs entered the BOP market. Our approach to case studies is contextualist in that we seek to explain BOP strategies in the context of a lower-middle-income African country. Contextualist case studies seek both to explain a particular phenomenon by drawing on the specifics of the setting and to generalize that phenomenon to theory (Welch et al., 2011).

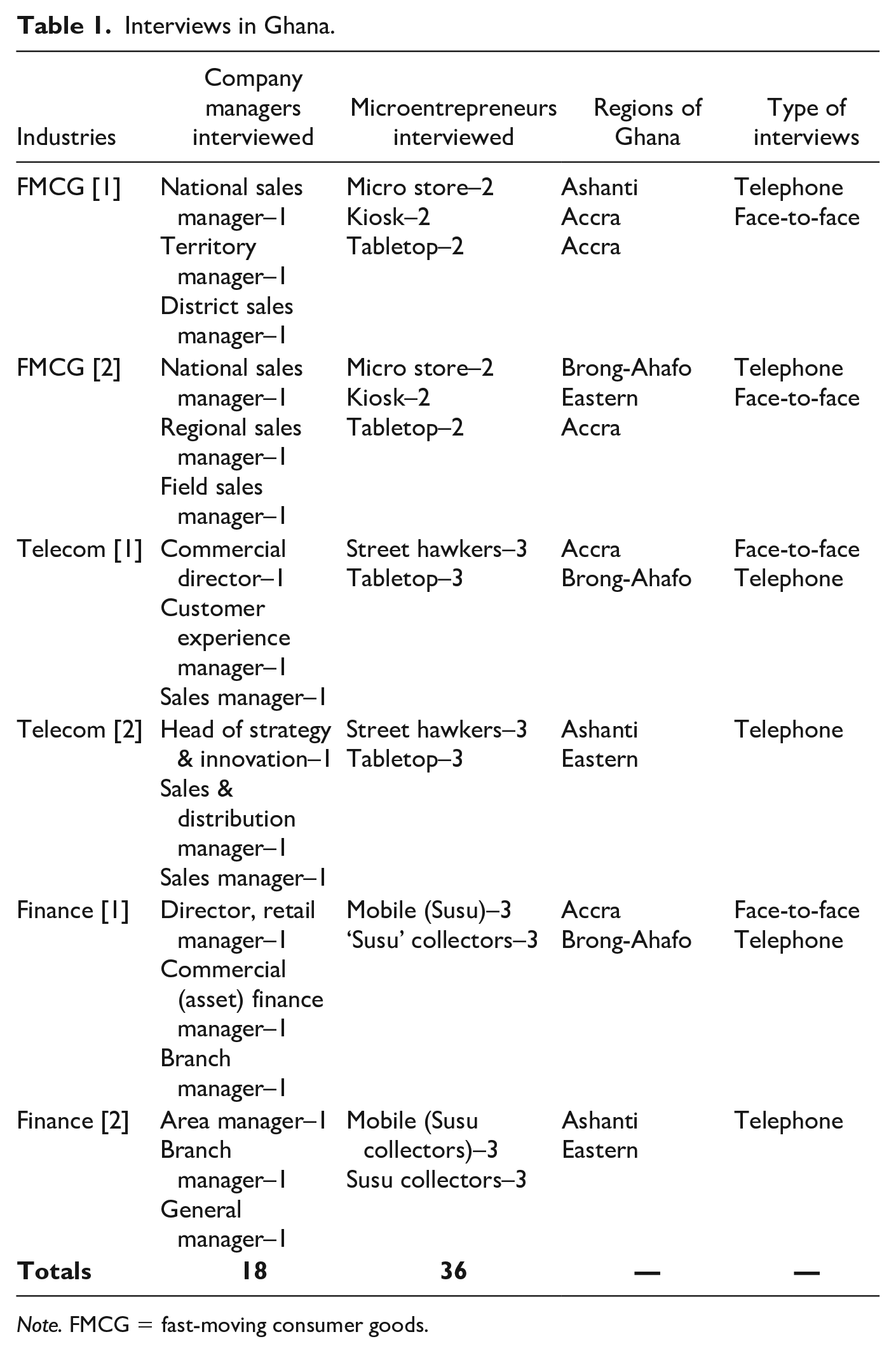

We acknowledge that the phenomenon we investigated evolved over time, which is why we made our approach cross-sectional. We selected these three industries because they have become ubiquitous in informal marketplaces in Ghana. Two MNEs from each industry were selected, for a total of six MNEs. At the time of our research, all of the sampled MNEs engaged in activities in the informal economy, and we refer to their market penetration strategies of reaching consumers in the informal economy as “BOP strategies.” For each MNE, three interviews were conducted with the company’s management. We started with contacts that MNE managers suggested (Eisenhardt, 1989; Heckathorn, 1997; Patton, 2002), and then used snowball sampling to identify informal microentrepreneurs to invite into this study. After contacting an initial set of the microentrepreneurs, we asked them to refer us to other sellers, thus establishing a degree of independence from the initial multinational contacts. We made sure that the microentrepreneurs we interviewed represented the diversity of sellers in the marketplace.

Over a 3-month period, we conducted a total of 54 semistructured interviews with microentrepreneurs and MNE managers in Ghana (Table 1). We asked the microentrepreneurs, for example: What kind of goods and services do they provide? What is their business model? When did the MNEs enter the market? How do they relate to the MNEs? A similar format was used for the managers, who were asked: What kind of work do you do with the microentrepreneurs? How did you develop the business model used with the microentrepreneurs? When, why, and how did their MNE choose to enter the BOP market? Face-to-face interviews were conducted with those participants located in Accra, and telephone interviews were conducted with participants in the other regions of Ghana. Accra is Ghana’s capital and its most commercially vibrant city, but to get a more complete picture, it is important to reflect on the specifics of diverse regional situations across the country.

Interviews in Ghana.

Note. FMCG = fast-moving consumer goods.

Our interviews were conducted in either English or Twi, a widely spoken Ghanaian language. Interviews conducted in Twi were translated into English by the second author. The managers were typically comfortable talking to us in English, because they had formal education and some were not Ghanaian. The second author is a native Twi speaker, and this advantage made it easier for microentrepreneurs to express themselves easily, as most do not have formal education and cannot speak or write in English. The second author asked the questions while a Twi and English-speaking research assistant took notes (Denzin, 2001). Every interview was voice recorded, and most interviews were transcribed by the second author within 72 hours.

Data Analysis

Before analyzing the interview transcripts, we generated open codes guided by the standards of naturalistic enquiry (Lincoln & Guba, 1985). We developed first-order keywords that reflected the terms used by the informants. Each interview was read several times and then coded individually (Van Maanen, 1979). Following Glaser and Strauss (1997), we employed constant comparisons across multiple informants and over time to discern similarities and differences in patterns and themes among the participants. With so much data from the MNEs (Miles & Huberman, 1984), we analyzed each sector in detail before moving on to the next sector, and we then compared companies and interviews. After analyzing each industry, we compared the different sectors.

We used axial coding (Strauss & Corbin, 1998) to find linkages between the first-order concepts. We then grouped these concepts into second-order themes (Gioia & Thomas, 1996). Here, we followed what has become known as the “Gioia method,” and in the findings section, we present a data structure with linked data tables (Gioia & Chittipeddi, 1991; Gioia et al., 2013). We paid particular attention to the linkages and the relationships we identified among the concepts when creating the aggregate dimensions. Finally, we considered the interactions among the different concepts and aggregate dimensions to develop an explanation of the multiple trends and outcomes we were observing.

At first, some of the inductively developed second-order themes remained too descriptive, and this made it difficult to develop aggregate dimensions. We believe this occurred in part because we asked participants about past activities and decisions that were affected by later developments. This led to microentrepreneurs often providing quite brief descriptions of their business models, assuming a significant degree of familiarity from a Twi-speaking, Ghanaian interviewer, and they preferred to discuss their current situation. More detailed descriptions of previous business models occasionally came from MNE managers reflecting on how they analyzed microentrepreneurs and adapted their BOP strategies accordingly. We concluded that prior activities and decisions had been significant in ways that not all market participants were necessarily aware of. Consequently, our development of second-order themes drew on our prior knowledge, and these represent a more holistic perspective (Schaefer & Alvesson, 2020). This interpretive approach is particularly evident in our key concepts of bridging and reverse bridging in the FMCG and telecommunications sectors and substituting and integrating in the finance sector.

Analysis and Findings

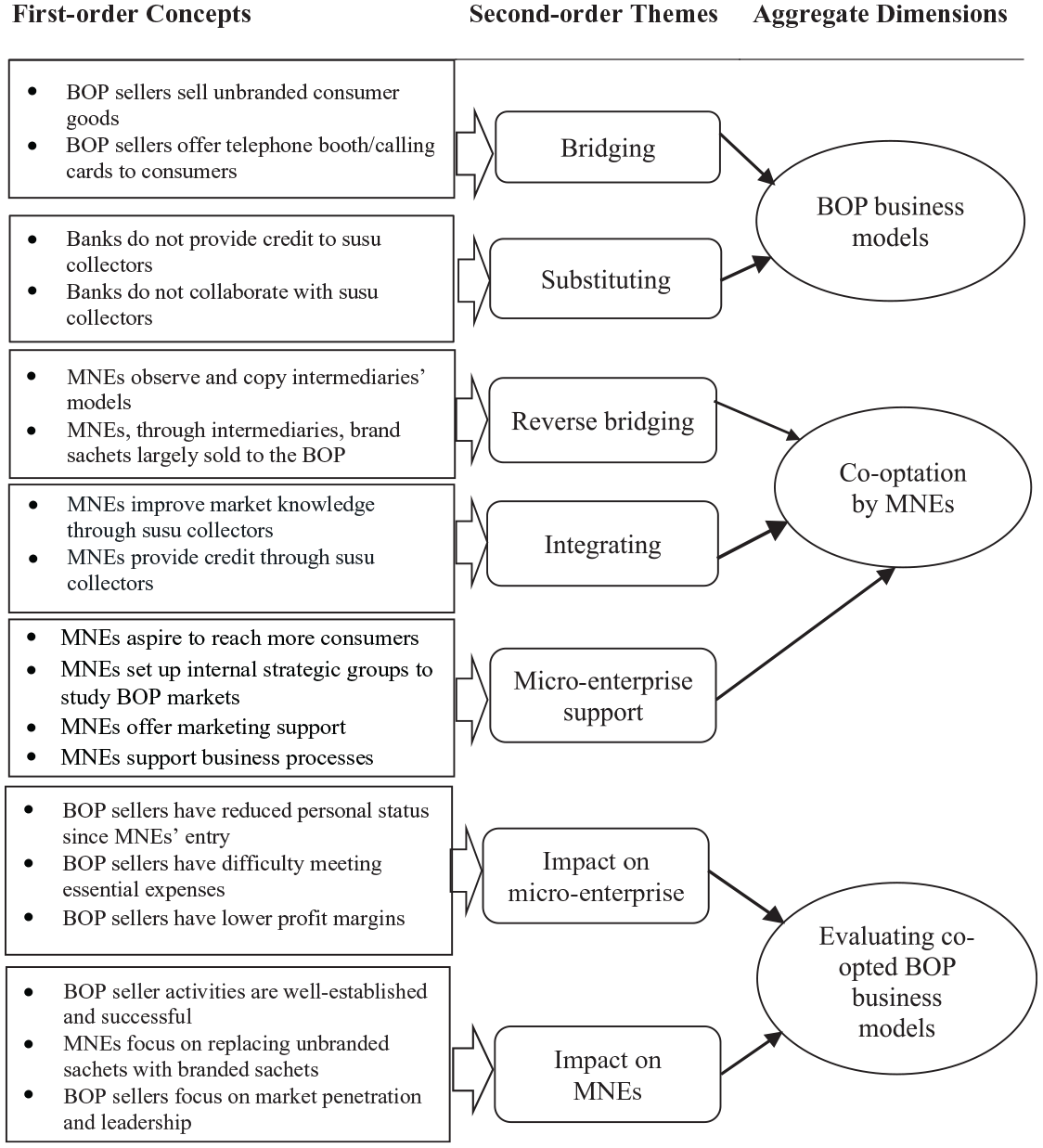

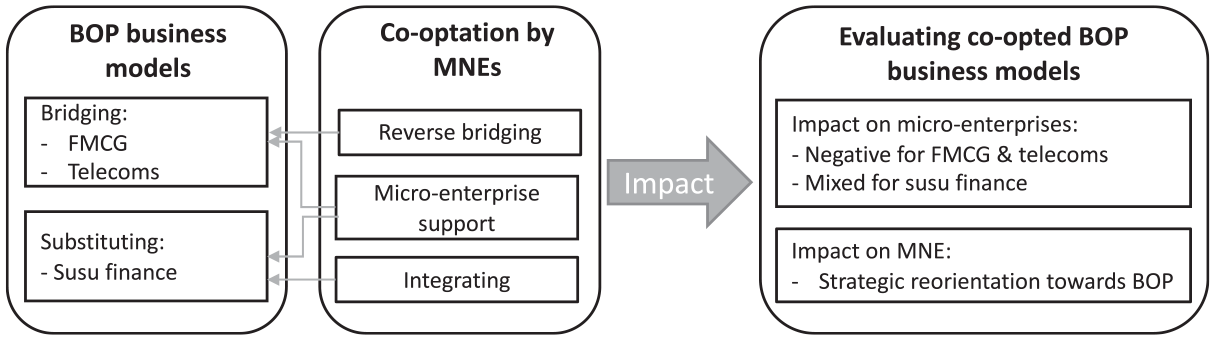

Our research outlines how microentrepreneurs were taking goods and services from the formal economy and making them available to BOP consumers in the informal economy. In this section, we identify two business models: bridging and substituting (Figure 1). Next, we detail how MNEs adapted and co-opted these BOP business models through reverse bridging and integrating, and how they developed commercial relationships through additional microenterprise support. Finally, we discuss the answers participants from both groups gave in evaluating the impact of these changes on their business.

Data structure.

BOP Business Models

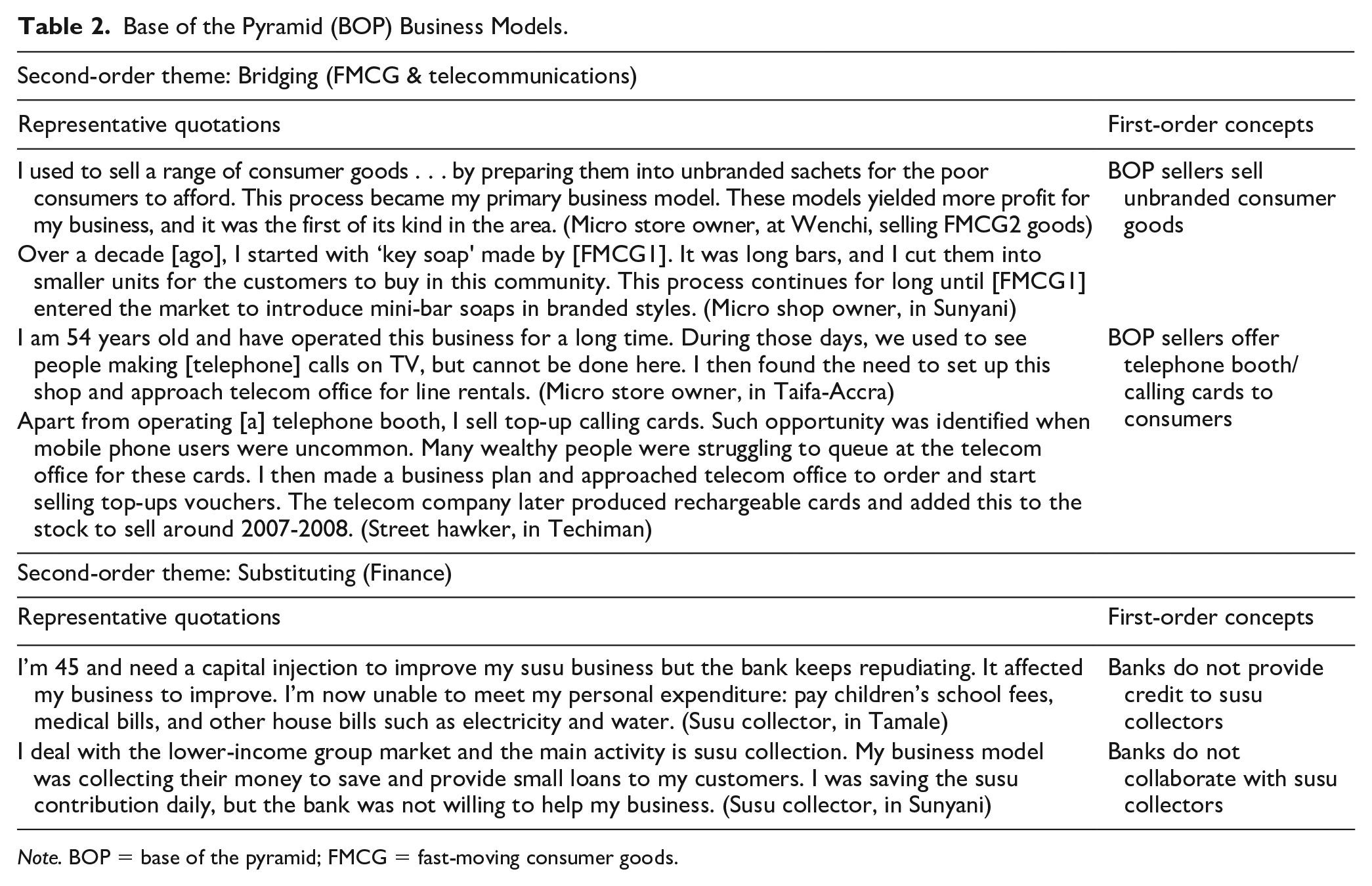

Even a casual visit to Ghana reveals that products and services developed in and for the formal economy are made available in the informal economy. Microentrepreneurs have long employed informal business models to engage in commercial activity, while—until only recently—MNEs focused on serving the formal economy. In the following, we develop the two models that describe how microenterprise BOP businesses operate: by creating value through bridging the gap between the informal and the formal economies or by substituting services for the absence of formal economy services. Table 2 includes the second-order themes that underpin our first-order concepts.

Base of the Pyramid (BOP) Business Models.

Note. BOP = base of the pyramid; FMCG = fast-moving consumer goods.

Bridging the informal and formal economies

Microenterprises in the informal economy in Ghana are owned and operated by members of the communities they serve. Their places of business can be small shops on streets or in stalls in markets or tabletop sellers on roadsides, plus there are hawkers who travel with their goods. The selection of items depends on what these entrepreneurs decide to sell, and prices are are not set but negotiated through haggling. This business model is based on purchasing goods in bulk and repackaging them into smaller and more affordable containers.

Over the last two decades, I established this [business] with the aim of selling provisions in this community. I took the initiative and began to serve them because the environment was safe and the community members were mostly families including children, which suggested that they would require food and other items for their children’s consumption. I began with baby food only, such as cow milk products. . . . I used to prepare sachets with a teaspoon measurement for a baby’s meal for the poor families to buy. (Microentrepreneur, in Kumasi)

In Ghana, FMCG products were sold to BOP consumers in unbranded packages prepared by local store owners. These are bridging activities because the entrepreneurs access goods and services produced in the formal economy and repackage and resell them to consumers in the informal economy. Until the early to mid-2000s, when MNEs moved into the BOP marketplace, bridging was common among BOP microentrepreneurs.

In the telecommunications sector, even before the introduction of mobile phones, bridging occurred frequently. “Space-to-space” shops were small communication centers in which local people could use a phone on a charge-by-call basis, making first landline and then mobile telephony affordable (Acheampong & Esposito, 2014). It was both difficult and expensive to get landlines installed in homes, including significant upfront and fixed costs. Space-to-space shops afforded access to a service in a country where there were few phone booths, allowing people the opportunity to make domestic and international calls to family and friends.

I set up a mobile telephony booth known as space-to-space with sole aim of making business, by charging a small fee. This was made possible as there wasn’t any easy means for people to access telephone (mobile and landline) calls. I managed to make my services affordable and available until the giant telecom company entered the market to make telephone lines available and cheaper for residents. (Tabletop seller, in Sekondi-Takoradi)

Early mobile telephony in Ghana included expensive handsets, costly SIM cards, and high-value recharge vouchers (about US$3 per voucher, higher than the daily income for BOP consumers). These facts highlight that the introduction of these services was aimed at the top, and to some extent the middle, of the economic pyramid. Over time, technology and business models designed for market penetration made mobile phones far more affordable. Today, space-to-space shops no longer exist, having been replaced by tabletop sellers on the roadside offering charge-by-call use of a mobile phone (see Table 2 for illustrative quotes).

Substituting in the informal economy

The picture is more complex for finance than FMCG and telecommunications, because bridging was not feasible. Accessing formal financial services was difficult (if not impossible) for microentrepreneurs and susu collectors, so susu collectors substituted services from the formal banking sector, and these services in turn supported the informal economy.

I identified this place to set up an office as the traders around here were unable to pay [i.e., deposit] their money in at the bank while working. The initial problem was how to build trust. (Susu collector, in Mampong)

In contrast to the FMCG and telecommunications sectors in Ghana, there was no connection between the formal sector and informal markets and practices in the finance sector before the advent of BOP strategies. As a result, we found less evidence of initial bridging activities by susu collectors. This, however, may have been the result of prior refusal by some of the more established banks to extend credit to them or open bank accounts for them, frequent complaints from susu collectors about the past:

I’ve asked the bank to grant my enterprise long-term credit to enable me to give micro credit to my customers, but the bank denied my request. Paperwork and collateral were provided to the bank for consideration, but they just refused. They would rather offer me a six-month loan. This denial negatively affected my business progression. I think the bank should be flexible and confident enough to work together with susu collectors, instead of being negative as it weakens my business prospects. (Susu collector, in Accra)

Thus, bridging and substituting routinely took place at the BOP level at a time when MNEs were focused on the top and middle of the economic pyramid and supported more standard outlets such as bank branches, supermarkets, and larger stores.

Co-Optation by MNEs

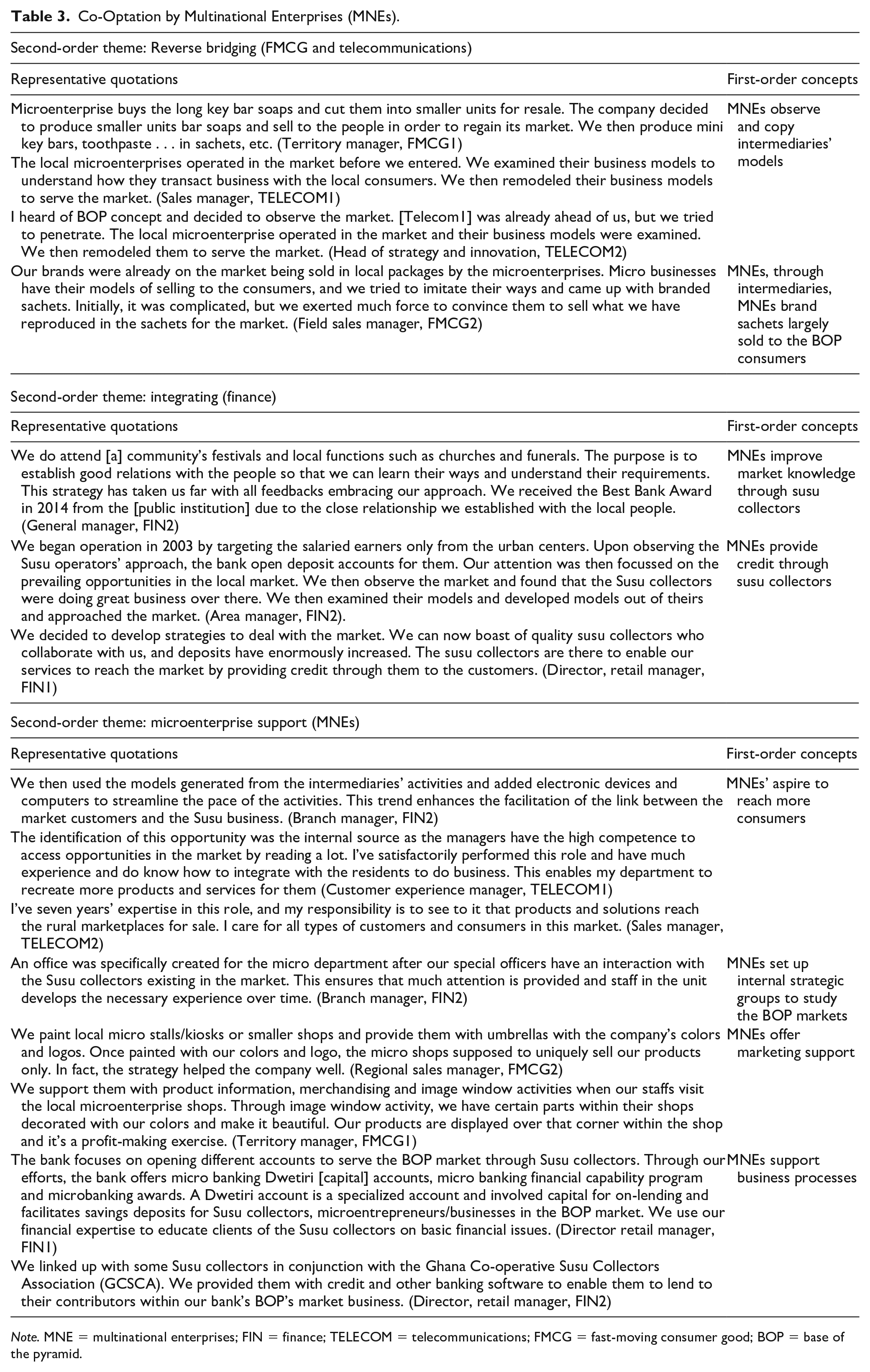

Next, we discuss how MNEs observed BOP business models, adapted them, and—in the process—co-opted microentrepreneurs into business models that allowed MNEs to penetrate BOP markets. These adapted BOP business models were developed by MNEs in the early 2000s and involved reverse bridging into the informal economy, but there is also evidence that integrating was also used (Table 3). While MNEs offered some support to microentrepreneurs, many of the microentrepreneurs that we interviewed, especially those in FMCG and telecommunications, viewed such support critically. Susu collectors, however, were more positive about the support.

Co-Optation by Multinational Enterprises (MNEs).

Note. MNE = multinational enterprises; FIN = finance; TELECOM = telecommunications; FMCG = fast-moving consumer good; BOP = base of the pyramid.

Reverse bridging

In the FMCG sector, MNE managers noticed the consumption of their products at the BOP level in unbranded, repackaged sachets. The difficulty for managers here was to understand how to align their standard approach of doing business with local informal practices. One manager told us:

After entering the market, I was overwhelmed to see how the local micro-enterprise prepared the unbranded sachets with local tools and measurement, which was sold to the final consumers. With active bargaining process by the consumers, they were comfortable buying at different prices. In fact, I was baffled on how to copy the process initially. (Territory manager, at FMCG1)

Cutting down bars of soap into individual pieces and putting instant powders into sachets were established practices in the informal economy, as was negotiating over price. FMCG1 decided to engage directly with the final BOP customer and to turn microenterprises into distribution channels for MNE branded products. In some cases, MNEs changed their products for BOP consumers, as was explained to us by a sales manager:

Having considered and operated in this market, our research staff started thinking about the brands to be made for the next ten years to come. As a result, the company always adjust the function of existing products through repackaging to make it attractive to serve their purposes. For instance, we repackaged a hand washing powder and launched it last year. In fact, it was the same washing powder that was already on the market, but we’ve added certain things to make it more effective for hand washing and other purposes. We’ve been able to renew such products due to how the consumers use them in their various homes. (National sales manager, at FMCG1)

FMCG products adapted for BOP consumers were frequently only changes in packaging. Although the repackaged products were more expensive for consumers, the smaller sizes allowed MNEs to gradually reduce the use of unbranded sachets. These branded packages were safer and more appealing to the eye, even though they also came with a higher consumer price and the environmental cost of significant plastic pollution.

In contrast to the FMCG sector, the entry of telecommunication MNEs into BOP markets in Ghana coincided with significant technological change—that is, the introduction of mobile phones. TELECOM2 first analyzed existing business models before developing their own model, as a manager told us:

When we observed the informal micro-enterprises activities in the market, such as serving the final consumers with space-to-space phone calls with exorbitant charges, we developed strategies to enter the market. Then, we decided to interact with the local micro-enterprises and the consumers to know exactly how they create those models and the benefits associated with it. We then improved our strategies and brought in phone booths and calling cards to enable consumers to access phone calls easily. Some of our existing brands were remodified to enter the market. The company introduced calling cards to be used for mobile phones. (Customer experience manager, at TELECOM1)

This follows a similar strategy used in the FMCG sector: identify existing approaches, make changes to existing products, and turn microentrepreneurs from owners into distributors of redeveloped products. For mobile phone operators, it was less clear how to repackage their products and adapt technological services. A sales manager from TELECOM1 highlighted that they were the first company in the telecom sector to engage in this market, which led to some trial-and-error innovation in the first instance:

We made calling cards, but they were a bit expensive. [. . .] As a result of the influx of mobile phones, the company has produced more calling cards for different kinds of users to choose from. (Sales manager, at TELECOM1)

As noted earlier, existing products and services were adapted through reverse bridging, from the informal economy to the formal: MNEs adapted existing BOP business models to suit their needs and to become business partners of BOP entrepreneurs.

Integrating

Initially, banks and other finance service providers were ambivalent about existing traditional finance models, such as those used by susu collectors. A manager at FIN1 revealed that while the financial company was confident about their market entry, they had to reconsider their approach:

In the early part of 2006, we had about 450 accounts with the bank. Initially, we found it difficult to understand the local models, but we did everything possible to talk to the operators. In fact, we tried and failed in the previous year but have improved all the models and have come down to the level of the customers. We failed because of certain techniques that weren’t applied well, and also the customers did not trust us as we’ve always denied them in the past. However, we realised the customers trusted the existing susu collectors among them. We then encouraged the operators to open accounts with us so that short-term loans can be provided through them to their customers. (Director, retail manager, FIN1)

Susu collectors enjoy a trusted status in their communities, which buffers them against the expansion of other microfinance models. Instead of lending directly to BOP retail entrepreneurs, FIN1 offered loan services to susu collectors, who in turn lent money to their customers. A branch manager at FIN2, which is a relatively recent foreign MNE entrant to Ghana, described a pattern of copying and adapting:

The model of the susu operation within the market was examined by our management team after our entry [into Ghana]. . . . It was based on integrating their models in our strategy and tackling the issue of acceptance by the susu contributors in the market. Knowing that the model has been in existence for several years and the customers might get used to the process, we have to think as to what can be done to attract the consumers. Even though it was not easy as it was the same model, but we just needed to do something by modernising it to suit the market well. (Branch manager, at FIN2)

Entrepreneurs trust susu collectors to provide loans without collateral, because community members and susu operators usually know each other. Entrepreneurs also prefer microfinance loans because little to no documentation is required, they trust their traditional institutions, and they do not fear their request being rejected. This meant that MNEs had to adapt their approach to fit existing susu practices. The importance of trust and social capital inherent in the relationship between entrepreneur and susu collector meant that instead of relying on reverse bridging, financial MNEs had to integrate a new model into their strategies and offer a more attractive service package to susu collectors, which we discuss in the next section.

Microenterprise support

Microentrepreneurs receive additional support from MNEs to enhance their activities (Table 4), but these entrepreneurs were often skeptical about whether this support was sufficient. This was particularly true in the FMCG and telecommunications sectors, in which most MNE support is only in terms of marketing. This normally entails MNEs providing product information, painting microenterprise stores, and helping with merchandising.

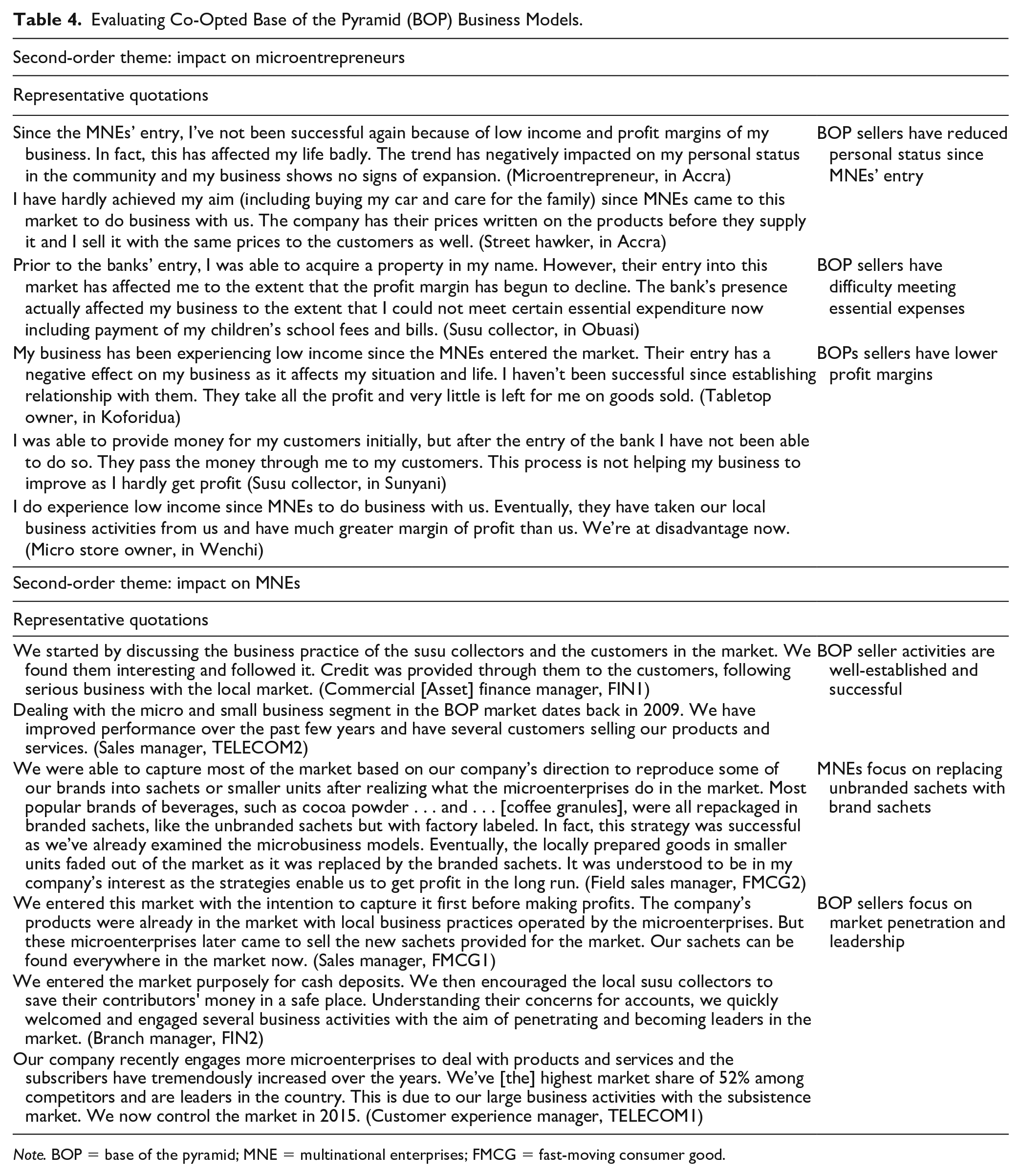

Evaluating Co-Opted Base of the Pyramid (BOP) Business Models.

Note. BOP = base of the pyramid; MNE = multinational enterprises; FMCG = fast-moving consumer good.

Many microentrepreneurs admitted that these steps helped them to develop their businesses to a degree, as one entrepreneur explained:

I do receive support in the form of product information, merchandising and display window activities from [the MNE’s] staff. The display window looks decent where the company beautifies certain corners of the shop purposefully to display their goods. However, [the MNE’s] officials become angry when they come and see competitors’ goods mixed up with theirs on the shelves. To me, this exercise does not primarily seem to contribute to profit making for my business as it is only there for the benefit of the companies. They make me think it will help me, but nothing is gained from this apart from the display window’s beauty. (Microentrepreneur, in Tamale)

A roadside tabletop business owner viewed support from MNEs more as tokenism than as meaningful business development:

I used to receive umbrellas once every year from the company. The umbrella helps by preventing the products I’m selling from deteriorating because of sunshine or rain. Frankly speaking, I’ll be able to purchase these umbrellas when reasonable profit margins are provided by the companies instead of these tokens. All that the [MNE] officials are interested in is the collection of feedback on their products when they visit me. Even last time I made a complaint to them about a robbery, which meant I lost money and goods, but they didn’t show any concern. (Tabletop owner, in Accra)

One MNE manager from FMCG1 presented support for microenterprise in different terms by saying:

We have a project called “village project.” In the villages are some micro-stores and customers whose stores, containers, kiosks, and other sales points are branded by [FMCG1]. The essence of these branding activities in all these points of sales with our products in the villages is to develop their businesses. In the future, we’ll organise training sessions for them, and this is called “retailer huddles.” In this way, we organise sections to educate them on the product information, funds management, records management, customer services, cleanliness, and tidiness of their stores. This is just to bring them up to the state on how we want them to be. This is because the company sees them as a vehicle to get to their destination, so they are critical. (Territory manager, FMCG1)

In the finance sector, MNE support took the form of extending credit and providing technological solutions rather than marketing, according to a manager at FIN2:

The susu collectors are supported with sales devices, and the device is carried to the customer’s place. The special electronic device has a core banking application system on it. So, it is like, the branch office has moved into the pocket and to the customer for transactions. Therefore, when a customer makes a contribution or saves, they can access the customer’s account instantly from the device. The device can issue a receipt to the customer instantly while the amount is deposited. And then an SMS is sent from core banking application on the device to the customer’s mobile phone, acknowledging the transactions. All these make the system less risky as compared to before. (General manager, at FIN2)

Another manager at FIN2 also highlighted that this new collaborative approach was less risky for both parties:

We improved the service of the susu collectors in the market. . . . As a result of improving the service, microcredit was increased and provided to the local market customers, which has a recovery rate of 90% for three years between 2012 and 2014. I feel we’ll continue to improve the service to do business with them because it is becoming less risky. (Branch manager, at FIN2).

Reducing risk and streamlining processes has augmented the operation of traditional credit circles by susu collectors in collaboration with larger financial institutions. Some collectors concurred that outside finance providers lowered their risk, but they were still concerned about their reduced profitability. One susu collector said:

In Ghana, debt recovery exercises have required an outsider to be involved. This is because local consumers may see the stranger as different and would fear getting in trouble with such a person. If they didn’t know the person from the community, then they would remain afraid that legal action could be taken against them should they fail to pay. . . . The local customers are forced to pay any arrears within their midst to avoid problems. I’m able to retrieve money owed me as debts with the bank’s assistance, and this is an excellent way for me to utilise the bank’s support. The greater portion of the monies goes to the bank while I receive little or nothing, and that is the issue. (Susu collector, in Sunyani)

Microentrepreneurs criticized their reduced profit margins, even those who were more positive in their assessment of the overall business relationship. Microentrepreneurs did not view benefits such as marketing support as positively as did MNEs (see Table 3), nor did they consider this benefit sufficient to make up for lower margins, despite higher sales. As customers increasingly prefer the more expensive branded products over the cheaper repackaged sachets, microentrepreneurs are effectively co-opted into BOP business models.

Evaluating Co-Opted BOP Business Models

After MNEs’ reverse bridging or integrating created new BOP business models, these new models were permeated throughout the BOP marketplace. In our interviews, we asked microentrepreneurs to evaluate their current position and to reflect on how this compared to their business model before the MNEs entered the market (see Table 4). The answers to our interview questions are detailed in the following.

Impact on microentrepreneurs

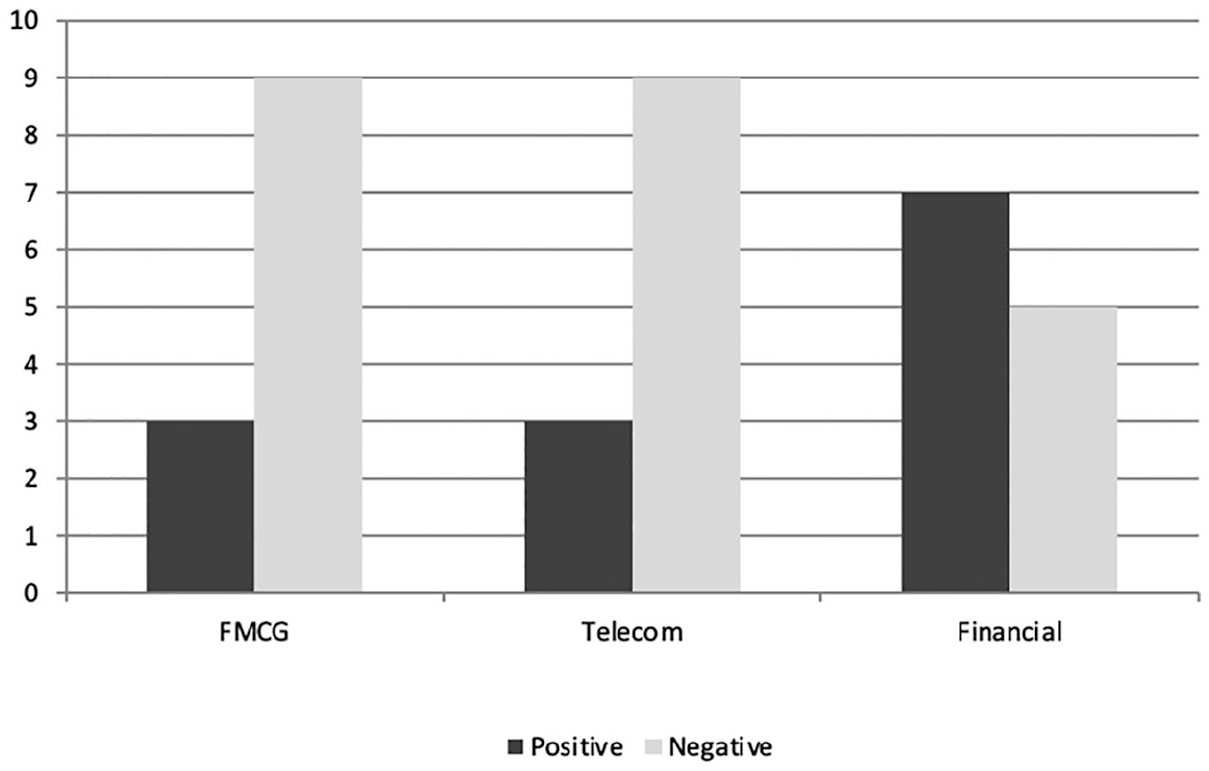

We asked microentrepreneurs to evaluate the impact of the current BOP business model. Nine out of 12 microentrepreneurs in the FMCG, and also the telecom sectors, did not think they benefited from the current arrangement—but they could not afford to not sell MNE products. The responses were a bit less lopsided for finance, where seven out of 12 susu collectors responded that there were benefits to the new model, while five were critical of the new arrangements (Figure 2).

Evaluation of new BOP business models by microentrepreneurs.

We asked about their levels of income and living expenses, their personal status and achievements, information on family size, and present living conditions. Many mentioned that before MNEs entered BOP markets, they could meet their living expenditures (paying bills and school fees, buying food, etc.). Now, many were concerned that their incomes were insufficient to meet their needs. One microentrepreneur complained:

I wasn’t lucky enough to gain a formal education as I dropped out at the early stages of school due to the early death of my parents. I then got [a] little money and invested in this business with no help from anybody. Initially, my business was progressing well and raising my personal status in this community as there were a lot of prospects. Suddenly, [the MNEs] entered, and my business began experiencing a decline, affecting my image as badly as my income. (Microentrepreneur, in Choko)

A susu collector in the Ashanti Region commented in the same vein:

[For] over a decade, I was running a lucrative business before the bank came into the market. I was one of the most respected people with high personal status before the bank’s entry. I was able to acquire a property in my name. Suddenly, the margin of profit and business prospects began to decline after the bank has entered this market. The bank’s presence really affected my business to the extent that I was unable to meet my expenditure such as paying my children’s school fees and bills. The most painful thing is that the bank is gradually grabbing the business from me since I’m losing customers in the market. This situation has really affected my business, my life and family and I blame all on the bank’s entry. (Susu collector, in Kumasi)

A street hawker who sells various calling cards also worried about his lowered income, this time because of TELECOM1:

I’ve got a family of three with the youngest one in class one. My situation was okay some years ago but has changed ever since [MNEs] came into this market. Consequently, I am unable to afford my children’s school fees, food for the family and other living expenditures such as health-related costs for the family. My living condition continues to deteriorate and has affected my personal status. (Street hawker, in Takoradi)

Our respondents considered their businesses successful when they were able to support their families and send their children to school, but also when it enhanced their personal reputation within their communities. They consistently identified lower levels of income (financial capital) and lower personal status (social capital) as central to their concerns. As Figure 3 illustrates, and as stated earlier, susu collectors were slightly more positive than microentrepreneurs in the FMCG and telecom sectors. We address this divergence further in the following sections.

Co-optation of BOP strategies.

Impact on MNEs

Initiating and implementing reverse bridging activities allowed MNEs to develop new management capabilities. The managers interviewed also suggested that the success of these initiatives led MNEs to strategically reorient toward the BOP market. A manager at FMCG1 highlighted the increasing importance of BOP markets for the company:

The company was used to deal[ing] with big retailers in the cities without focusing on the lower-income groups’ market since its establishment in Ghana. Initially, we did not have any interest in this market. In 2002, we realised that micro-entrepreneurs from the local market were approaching us to place orders into their respective stores. They would be found queuing in front of the factory display area to place orders, and this situation went on for a while. Then, I discussed with my MD [managing director] and colleagues to investigate why the micro-entrepreneurs came to us. Then we dispatched marketing representatives to trace their business activities in the local market including how the final consumers patronised the brands. An astonishing thing we found was that the micro store owners were recommending brands to the consumers as to which one was good or bad without proper product information. . . . Subsequently, deliberations were made, and we concluded that we should stop them from approaching us and rather [we] approach them instead. (National sales manager, at FMCG1)

Microentrepreneurs demonstrated a long-standing interest to bridge into the formal economy and form direct relationships with MNEs. MNEs ignored microentrepreneurs—until the early to mid-2000s, when MNEs became aware of them via a mix of business interests and competitor activities. As soon as new BOP business models were established, MNEs used market intelligence and product development to meet specific BOP customer needs. A manager from TELECOM2 described how the firm consistently scanned for information and adjusted products accordingly:

We continue to gather information and have now redeveloped different packages such as monthly, weekly, and daily packages necessary for this market. Other packages also include internet bundles. It enables our customers to top up their primary and secondary internet devices, using a single bundle. They can also top up for themselves and a friend or family member, with single bundle purchase. This market has become our focus, and we’re doing everything to survive. (Director of strategy and innovation, TELECOM2)

The ways in which existing capabilities and business models were co-opted to allow MNEs to tap into BOP business opportunities is perhaps clearest in the financial sector. FMCG firms essentially copied and then improved existing distribution models, and telecom firms adapted new technology to meet BOP customer preferences. For finance, however, traditional formal sector ideas and novel microfinance ideas could not replace the existing relationships between clients and collectors, so MNEs had to find ways to insert new technologies into traditional credit circles. Entering the informal sector through the susu collectors’ business model expanded banks’ notions of retail and microfinance. A director at FIN2 explained:

This company, [FIN2], was originally providing credit to the customers that collect their salaries from their bank and were referred as “payroll type earners. . . . I realised that we lacked something since credit was being given to only the formal employee workers.” I then asked myself, what about the people in the informal sector? Can’t they also get credit? This is because few of them in the local market have been approaching me for help, but they lacked the requisite collateral to access loans. Besides, having realised that, the informal sector has been inaccessible to financial services within the economy, an attempt was made to try them with the support of micro-insurance to protect the loans. . . . We then studied the susu collectors’ model, reduced the risk by introducing technology such as software to enhance the smooth operation of the business. (Director of micro division, FIN2)

The introduction of software and microinsurance schemes allowed banks to reduce the risks associated with the informal economy. This integration, however, was predicated on the willingness of susu collectors and their clients to accept these new technologies and schemes.

Discussion

Our findings show how the formal economy reverse bridged products and services into informal BOP business models and how MNEs strategically copied and refined their products and services to integrate into the BOP marketplace. We next contribute to the debate on poverty alleviation through business initiatives, first by extending knowledge on the effects of co-opted BOP models on social capital, and second by analyzing the effect of co-opted business models on microentrepreneurs.

Social Capital in the BOP Marketplace

Our research contributes to a better understanding of how social capital is maintained, eroded, or enhanced in co-opted BOP business models. Researchers did not initially consider social capital separately and assumed that improved access to products and services would be broadly beneficial. Ansari and colleagues (2012), however, point out that social capital is quite important in BOP models, and we demonstrate that social capital is closely related to how financial capital is generated through such models. When we asked microentrepreneurs to evaluate their collaborations with MNEs, a recurring complaint was their reduced profits because MNEs now captured some or most of the value that they had previously realized. Several authors have argued that essentialist interpretations of poverty are economically reductive and not appropriate for BOP research (Ansari et al., 2012; Mason et al., 2017; Rivera-Santos & Rufín, 2010), but our participants’ responses show that financial capital and social capital are closely intertwined at the BOP level.

In our study, we identified two business models (bridging and substituting) that connect informal economy actors with formal economy goods and services, even though BOP microentrepreneurs face structural holes when seeking to access formal economy goods and services (see also Rivera-Santos & Rufín, 2010). In the FMCG and telecommunications sectors, microentrepreneurs are able to bridge this gap with MNEs (see Figure 3). For microentrepreneurs in these fields, their relationships with MNEs are transactional in nature, and they remain subject to the social norms of behavior of their communities. Demonstrating munificence to their customers as well as providing for their families are important for microentrepreneurs to build status in their communities (Slade-Shantz et al., 2018). Hence, lower profits were consistently mentioned as reducing their ability to provide for their families and pay their children’s school fees, thus damaging their personal status. Our research demonstrates that in a country like Ghana, where accumulation, status, and respectability are intimately linked and mutually enhancing, financial capital and social capital should not be considered separately.

The situation was slightly different with substituting, the second business model, which was used when it was not otherwise possible to connect to services in the formal sector. Susu collectors handled banking functions such as saving, lending, and capital accumulation because formal banks did offer services for small amounts of money. A close-knit network of relationships, with daily visits by the collectors to workplaces, replaced collateral. This allowed small-scale, trust-based financial circles to pool resources and provide banking in a resource-constrained setting (Dorado, 2015). While susu collectors or their customers might abscond with funds (Yeboah, 2010), a sense of trust reinforced close contact, personal knowledge, and social control within communities. Here again, social capital was generated through relationship-building and improved financial income.

The Evolution of BOP Business Models

Both types of business models (bridging and substituting) have been largely overlooked in the wider BOP literature in favor of general statements that MNEs suffer from institutional distance when seeking to enter BOP markets (Brix-Asala & Seuring, 2020; Rivera-Santos et al., 2012). Rarely is it acknowledged that goods and services from the formal economy were available at the grassroots level long before the entry of MNEs. Especially for the FMCG sector, there is copious historical evidence that informal microentrepreneurs distributed consumer products throughout the 20th century (Murillo, 2011). In response to the Gold Coast Riots of 1948 (a historical consumer protest), small-scale retail in Ghana was increasingly protected during decolonization, and this continued through local legislation after independence (Decker, 2007; Harneit-Sievers, 1996). Substituting finance business models for RoSCAs is similarly historically embedded (Mason et al., 2017). Closing structural holes between the informal and formal economies provided economic opportunities and livelihoods at the BOP level long before MNEs developed strategies to enter BOP markets.

Prior to the early to mid-2000s, MNEs were not engaged with BOP consumers, BOP entrepreneurs, or BOP business models. BOP community reliance on financial and social capital made it difficult for MNEs to develop a value proposition for the three markets discussed in this article. Co-creation between international and local actors was proposed as a potential solution (José, 2008; London & Hart, 2004; Prahalad & Hart, 2002; Viswanathan et al., 2008). This issue is that co-creation ignores existing BOP business models and their long history. It has also been criticized for its potential exploitation of relationships because co-creation tends to be vague about value capture relationships (Cova et al., 2011). We argue that MNEs’ BOP strategies allowed them to reverse bridge existing informal business models to their benefit and capture a greater share of the BOP marketplace value. MNEs’ improved value capture has not necessarily been offset by greater value generation for the microentrepreneurs, because MNEs often only innovate at the margins.

Co-Optation of BOP Business Models Through “Reverse Bridging”

Our study challenges whether co-creation was also co-optation in the two business models we describe. In FMCG and telecommunications, reverse bridging meant MNEs engaged with microentrepreneurs as distributors for their goods and services. Yet innovations, such as the “single-serve revolution” (Prahalad, 2004, pp. 16–17), were practiced by microentrepreneurs in Ghana at least since the early 20th century. Hence, our concept of reverse bridging challenges the notion that MNEs were sources of innovation and added value to BOP business models. We find that MNEs co-opted the business models of microentrepreneurs to reduce their own institutional distance to BOP consumers, who generally distrusted foreigners in their communities (Claus et al., 2021; Slade-Shantz et al., 2018; Webb et al., 2010). MNEs used reverse bridging to access the social capital of microentrepreneurs, making distribution more efficient.

Especially in the FMCG and telecommunications sectors, the co-optation of BOP business models created value only at the margins for microentrepreneurs but was especially effective at capturing value for MNEs. There was some added value for customers, such as with product safety (e.g., preventing adulteration from repackaging), suitability, and convenience. For example, branded and prepackaged containers were safer than repackaged sachets, but they also were more expensive for customers. At the same time, fixed prices reduced microentrepreneurs’ profit margins and shifting value capture to MNEs.

Business models in telecommunications included technological innovations that further undermined BOP business models. Space-to-space communications centers represented a widespread and, for a time, successful business model bridging formal economy services (landlines and overseas calls) with consumers in the informal economy via a delivering service rather than an “ownership-type business model” (Bocken et al., 2014, p. 48). The introduction of mobile phones spread far more rapidly in Africa than Western observers or telecommunications companies initially expected (The Economist, 2005). With mobile phone handsets becoming increasingly available and affordable, space-to-space phone booth operators could no longer charge high fees. In contrast to the FMCG sector, this technological shift broadly benefited consumers through lower costs, greater convenience, and improved access.

Co-Optation of BOP Finance Business Model Through “Integration”

There is a fundamentally different pattern in the co-opting of the BOP business model in the finance sector. Susu collectors originally substituted for inaccessible formal services. MNEs found it difficult, and likely unprofitable, to displace susu collectors. Thus, they first integrated (rather than reverse bridged) with the susu collectors’ existing customer relationships and then innovated BOP practices. This difference in pattern became clear when microentrepreneurs were interviewed regarding support from MNEs. FMCG and telecom microentrepreneurs found marketing support was only superficial and cosmetic, whereas microentrepreneurs in finance positively evaluated this support because of improvements in technology and credit recovery. This is the result of two factors: differences in the way social capital was generated in substituting rather than bridging and better innovation in integrating than in reverse bridging.

We point out here that the substitution process included significant constraints. Traditionally, susu collectors did not require collateral or formal registration to provide savings and loans services to their customers, and they operated entirely divorced from the formal banking sector. Thus, RoSCAs generally did not provide security or offer opportunities for legal redress in cases of malfeasance. They also had limited ability to raise capital. Process and technology innovations, however, provided significant additional benefits to microentrepreneurs. For example, their lending risks were lowered through the support of larger financial institutions both in terms of process and enforcement. Several of our interviewees mentioned the advantage of having outsiders help collecting debts. Also, microentrepreneurs received process improvements (such as electronic handheld devices to keep records of deposits) that provided greater accountability to all parties.

Banks and microfinance organizations working with susu collectors gained significant benefits from the social capital inherent in the system. Collectors know their customers well and see them every day, retaining the trust of their communities in ways that retail banks and microfinance institutions cannot. This made partnerships with RoSCAs more cost-effective than many standard microfinance approaches. The integration process combined the social capital of the collector as a trusted insider with the ability of MNEs to effectively collect outstanding loans.

In contrast to the lowered social capital (and financial capital) felt by microenterprises in FMCG and telecommunications through reverse bridging, microenterprises in finance appear to have increased social capital from integrating—even though, there too, financial capital fell. We identify several reasons for this discrepancy in effects on social capital. First, finance MNEs cannot easily insert their own brand into this sector, as could MNEs selling consumer goods or telecommunications. Integrating trust-based financial relationships would be impossible without the established social capital of susu collectors. Second, financial integration created a virtuous cycle of MNE co-optation and susu collector social capital. Third, trust-based RoSCAs generate a different kind of social capital than the more transactional relationships in retail and telecommunications. Susu collectors’ social capital was not as tightly linked to their financial capital as those the in FMCG and telecommunications sectors.

Conclusion

Based on in-depth fieldwork and interviews with BOP microentrepreneurs and representatives of MNEs in Ghana across three sectors, our research addresses the question: Are BOP business models co-opted by MNEs, and if so, how? Our research challenges the notion of simple co-creation at the BOP level, and describes two processes by which MNEs co-opt existing business models. First, in FMCG and telecommunications, reverse bridging allows MNEs to insert their own branded products in BOP communities, displacing existing transactional relationships between BOP consumers and BOP entrepreneurs. This practice was found to reduce both the financial capital and the social capital of microentrepreneurs without also meaningfully supporting them. Second, in finance, integrating allows MNEs to incorporate susu collectors into their value chains by (1) taking advantage of collectors’ trust-based relationships with their customers, and (2) offering collectors improvements in process and security and greater access to capital. While susu collectors complained of reduced profits and thus reduced financial capital, they appreciated their enhanced social capital.

Our work contributes to the BOP literature in two ways. First, we highlight that financial capital and social capital are closely intertwined at the BOP level and that cultural norms and expectations bind microentrepreneurs to their communities. Second, we outline two forms of co-optation. The first is reverse bridging, which, according to our FMCG and telecommunication microentrepreneur interviewees, reduced both their financial and social capital. The second form is integration, which, according to our finance microentrepreneur interviewees, increased their social capital but lowered their financial capital. We emphasize that MNEs’ engagement at the BOP level should focus on enhancing the skills and capabilities of their informal sector partners, which could offset the negative impact on the livelihoods and resilience of poor communities after MNEs’ value capture.

Footnotes

Acknowledgements

The authors would like to thank the editor, Sylvia Dorado, and the three anonymous reviewers for their helpful and constructive comments. They also thank the British Academy of Management, which awarded them the Best Paper Prize in the African Studies Track in 2020, as well as the numerous colleagues who have given us food for thought in several research seminars and events, including at the University of Leeds in 2019, the University of Bristol in 2020, The New School in 2021, and the University of Liverpool in 2021.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Author Biographies

![]() .

.

![]() .

.