Abstract

The literature on Base of the Pyramid (BoP) strategies emphasizes that creating social value requires collaborative, multi-stakeholder business approaches. However, there is limited understanding of how businesses can successfully coordinate such value creation processes in the developing economies that face significant institutional voids. This study adopts a business model perspective for analyzing social value creation processes that span organizational boundaries. We introduce a novel, theoretically grounded business model framework that helps conceptualize social value by locating the various loci of value creation, and the stakeholders that partake in creating and capturing this value. We subsequently analyze the mechanisms of social value creation in M-Pesa, a renowned boundary-spanning mobile money system that has advanced financial inclusion among tens of millions of users in Kenya. The results show that information and communications technology can help advance social value creation by reducing the cost of coordinating boundary-spanning business models that integrate diverse societal stakeholders. The results further point to uneven distributional outcomes in self-governing social value creation strategies where the focal firm plays a coordinating role.

There is rising academic and practitioner interest on the role of market forces such as business strategy, entrepreneurship, and innovation for addressing society’s grand challenges such as poverty, inequality, and environmental sustainability (George et al., 2012; Porter & Kramer, 2011). The Base of the Pyramid (BoP) literature is one of the pioneering research streams in this field, and has long explored the potential contributions of multinational and local firms for poverty alleviation and social inclusion in lower-income economies (Dembek et al., 2019; Kolk et al., 2014; Prahalad, 2004). BoP strategies aspire to create social value by engendering positive social and environmental outcomes beyond, or in addition to, creating financial profit for shareholders. 1

After an early start that expounded the market potential of low-income consumers in emerging economies, “second generation” BoP strategies have shifted attention to creating social value with and for local stakeholders (Dembek et al., 2019; Nahi, 2016). This approach entails collaborating with civil society organizations and government bodies to create more profound and lasting changes in the lives of BoP constituents. The importance of multi-stakeholder, collaborative approaches for social value creation is also shared by the related research stream in sustainable business models (Freudenreich et al., 2019; Yang et al., 2017), and is justified on normative as well as on pragmatic grounds (Seitanidi & Crane, 2013). Ethically, collaborative approaches of value creation are expected to lead to more inclusive and locally appropriate BoP strategies, thus stymieing potential accusations of exploitation and commercializing poverty (Karnani, 2007). Pragmatically, collaborative approaches of value creation are said to improve the performance of BoP initiatives by helping mobilize a broad spectrum of resources and social network to achieve systemic social impact (London & Hart, 2004; Nahi, 2016). BoP firms can draw benefits by developing new capabilities that integrate their resources with those of external actors, or by pursuing collaborations that open up new sources of innovation and growth (Rivera-Santos et al., 2012; Sanchez & Ricart, 2010). For multinational corporations, working with local actors creates greater understanding of local market and institutional conditions (Rivera-Santos et al., 2012), while also helping bridge their “liability of foreignness” by improving their legitimacy (Dahan et al., 2010; Lashitew & van Tulder, 2019).

Multi-stakeholder value creation strategies, however, tend to be complex, and require intricate governance mechanisms to coordinate activities across stakeholders (Seitanidi & Crane, 2013). These strategies are particularly costly and risky in emerging economies that are characterized by “institutional voids,” which refers to the weakness and, in some cases, complete absence of formal institutions that are needed for devising and enforcing contracts (Mair & Marti, 2009). Inefficient governance and market institutions, such as of insecure property rights and inefficient court systems, increase the cost of negotiating, monitoring, coordination, and enforcing contracts (Mair et al., 2012; Williamson, 1985). In the presence of informational asymmetries, multi-stakeholder social value creation efforts that create economic interdependence with value chain members could also expose the firm to opportunistic behavior by local actors. Research into business strategy among emerging economy firms shows that institutional uncertainties compel firms to shun market exchange in favor of internal coordination mechanisms through vertical and horizontal integration or business group membership (Khanna & Palepu, 2000; Yiu et al., 2007).

If institutional voids have severe adverse effect on traditional businesses (Peng et al., 2005), their effect is likely to be even more pronounced in complex, multi-stakeholder social value creation strategies. This could indeed be a major factor behind the low success rate of BoP firms in creating social value (Dembek et al., 2019). However, in-depth research on social value creation in boundary-spanning BoP initiatives is relatively scant, limiting our understanding of the coordinating and governance challenges in such initiatives. The objective of this research is to provide a coherent conceptualization of social value creation that can improve our understanding of multi-stakeholder (boundary-spanning) social value creation processes.

We draw on the business model perspective for examining the configuration of value creating activities across firm boundaries. We introduce an integrative framework that is suited for analyzing the processes and outcomes of social value creation by building on the activity system perspective of business models (Amit & Zott, 2001; Zott & Amit, 2010). We subsequently conceptualize social value by identifying the loci of social value creation and the primary and secondary stakeholders that partake in creating and capturing this value. The empirical parts of the article exploit the analytical properties of the proposed framework for unpacking the drivers of social value creation in M-Pesa—an innovative, boundary-spanning mobile money service that has extended financial services among tens of millions of in Kenya.

The study responds to calls for “a deeper analysis of the various business models at the BOP” to shed light on the conditions that enable success (Kolk et al., 2014, p. 360). It makes three contributions to BoP and related literatures that examine business-led social value creation strategies. At an analytical level, the study makes a contribution by introducing a new, integrative framework for analyzing the mechanisms of social value creation. Accordingly, we identify three constituent elements of social value: consumer value, producer value, and stakeholder value—which includes value for shareholders, the government, local communities, and the environment at large. Second, the study contributes to the empirical literature by offering novel insights on how BoP businesses overcome the significant coordinating challenges of multi-stakeholder initiatives. Analysis of the M-Pesa case reveals that information and communications technologies (ICT) can enable innovative business models that advance social value by reducing the costs of coordinating boundary-spanning activity systems. Finally, the study contributes to the literature by spelling out the kinds of tensions that arise in multi-stakeholder social value creation strategies. Our results suggest that the same strategies that enhance the total value creation potential of a business model can also end up increasing inequalities among stakeholders.

The remainder of this article is organized as follows. Section 2 recaps the literature on BoP business models to motivate the research goal. Section 3 introduces our business model framework and outlines its relevance for understanding the concept of social value. The next two sections apply the framework for understanding social value creation in M-Pesa: Section 4 introduces our research method and data, and Section 5 presents the key results. Section 6 concludes the article by discussing the implications of our results for future research.

Literature Review: Social Value Creation

Early BoP literature sought to demonstrate the untapped market potential of the BoP market segment, and emphasized the need for devising novel value offerings that meet the unique requirements of low-income consumers (Prahalad, 2004). This approach, also called BoP 1.0, has been criticized for ignoring the fundamental development needs of the poor and inflating their purchasing power (Karnani, 2007). Researchers have questioned the value of BoP strategies such as selling single-serve sachets of commodities, or employing “village ladies” for distributing consumer products in remote areas—strategies employed by large corporations such as Hindustan Unilever (cf. Prahalad, 2004). Such strategies were criticized for overstating the marginal welfare gains for consumers and distributors, and even worse for “commercializing” poverty only to enrich multibillion-dollar corporations (Dembek et al., 2019; Karnani, 2007). A genuine effort to reduce poverty, it was argued, required more sustained interventions to increase the incomes of the poor by improving their employment opportunities, productivity, and market access (Karnani, 2007).

The subsequent literature has introduced the concept of BoP 2.0, which emphasized the need for creating social value through collaborative endeavors of co-creation that actively involve local communities (Dahan et al., 2010; Nahi, 2016; Simanis & Hart, 2009). The emphasis on engaging diverse stakeholders for creating social value is also shared by the related streams of literature on sustainable business models and cross-sector partnerships (Caldwell et al., 2017; Freudenreich et al., 2019; Seitanidi & Crane, 2013; Yang et al., 2017). While enabling greater social impact, collaborative strategies help BoP firms integrate their capabilities with the resources of the ecosystem to create new entrepreneurial and innovation opportunities (Rivera-Santos et al., 2012; Sanchez & Ricart, 2010). For multinational corporations, collaborations with local actors can improve understanding of local market, and institutional conditions (Rivera-Santos et al., 2012), while also giving access to synergetic inputs such as local knowledge, contacts, and social legitimacy (Webb et al., 2010). Moreover, collaborating with local civil society and governmental agencies makes it possible to mobilize a broad spectrum of resources and social networks that are required to achieve systemic social impact (Nahi, 2016).

But collaborative business approaches that engender greater interdependence between the focal firm and its ecosystem are likely to introduce complex coordination challenges. Coordinating value creating activities across diverse societal stakeholders can be costly to initiate and sustain, especially in the emerging and developing economies that face “institutional voids” (Mair et al., 2012). Missing and inefficient formal institutions in the form of insecure property rights, deficient court systems, and poor contract enforcement mechanisms increase transaction costs (Williamson, 1985). Furthermore, lack of market institutions in areas such as grades and standards, corporate governance, and external monitoring increases the costs of negotiating, monitoring, coordinating, and enforcing contracts (Yiu et al., 2007).

Transaction cost theory suggests that the optimal structure between the two alternative governance and coordinating mechanisms, namely markets and organizations (hierarchies), depends on its institutional context (Williamson, 1985). In economies with well-functioning market institutions that support efficient exchange between anonymous buyers and sellers, market-based structures prevail, allowing firms to specialize in a single line of business (Khanna & Palepu, 2000). In contrast, expensive and risky market-based governance and coordination in developing and emerging economies render hierarchies (organizations) preferable to markets. Consequently, firms in developing countries often opt for in-house production of intermediate inputs such as electric power, water supply, and transportation to avoid the risk of opportunism in market-based transactions (Khanna & Palepu, 2000). BoP firms also organize themselves into business groups, either based on joint ownership or other, less structured forms of association. Members of business group then regulate their activities based on internally developed coordination mechanisms, which reduces their dependence on an unreliable market system that would expose them to opportunism and other types of risk (Yiu et al., 2007).

The literature on social value creation suggests that BoP firms can overcome the uncertainties and inefficiencies caused by institutional failures by developing social capital and building a web of trusted connections with a diversity of organizations and institutions (London & Hart, 2004). This suggestion is in line with the theoretical view that networks can offer an alternative governance logic that is distinct from markets and hierarches (Powell, 1990). Social networks are thereby said to increase access to resources and information, leading to the development of “native capabilities” through effective combination of local and global knowledge (Hart & London, 2005). Social networks can also bring about reputational advantages that reduce the potential risk of opportunism such as bribery (Peng et al., 2005) and allow the firm to fly “under the radar” of regulatory regimes that are riddled with corruption and inefficiency (Hart & London, 2005).

Although social networks can help mitigate institutional barriers by supplementing formal contracts (Caldwell et al., 2017), they are unlikely to entirely supplant the need for contractual governance mechanisms. First, social networks are time-taking and expensive to build, and once developed, they lead to relational contracts that are difficult to transfer or replicate in different settings. The strength of formal institutions is precisely in removing the limiting relational element in informal transactions, thus allowing contract-based, arms-length transactions among anonymous actors that do not need costly efforts to build relational profiles. Reliance on relational governance mechanism that are context-specific can thus introduce inefficiencies that limit the ability of BoP ventures to grow by scaling their operations (Lashitew & van Tulder, 2019; Mair et al., 2012). Second, informal coordinating mechanisms could expose the firm to various kinds of risks, especially in developing economies that are pervaded by constraining norms, values and belief systems, such as adherence to patriarchal rules (Webb et al., 2019). Informational asymmetries will also increase the exposure of collaborative businesses to opportunistic behavior by local leaders in the form of adverse selection, moral hazard, cheating, and shirking (Reficco & Márquez, 2012).

Implementing collaborative businesses that blend the diverse competences of societal stakeholders thus requires more than social embeddedness to overcome the limits imposed by institutional voids. The question, therefore, is how BoP businesses that seek to create social value through multi-stakeholder approaches can overcome the coordination and governance challenges posed by institutional voids. To help address this issue, the next section will introduce a new approach for conceptualizing multi-stakeholder social value creation processes, which is subsequently applied to analyzing a real-world case of social value creation.

Theoretical Framework

We adopt a business model perspective to provide a coherent conceptualization of social value, which is poorly defined and understood in the existent literature (Crane et al., 2014; Dembek et al., 2019; Geissdoerfer et al., 2016; Kolk et al., 2014). The business model is a meta-concept that “articulates the logic, the data, and other evidence that support a value proposition for the customer, and a viable structure of revenues and costs for the enterprise delivering that value” (Teece, 2010, p. 179). The concept lies at the intersection of organizational design, entrepreneurial value creation and strategy, and has been used for strategic analysis of issues such as competitive advantage, firm performance, and the management of technological innovations (Amit & Zott, 2015; George & Bock, 2011; Zott et al., 2011). As a multidisciplinary concept, it has been used for examining the interplay between organizational design and strategy, and between the business environment and performance (Teece, 2010). It is hence particularly well-suited to our goal of analyzing the coordination and governance of multi-stakeholder social value creation processes.

This study builds a theoretically grounded framework of business models that is consistent with the conception of business models as mechanisms through which an organization “creates and delivers value to customers, and then converts payments received to profits” (Teece, 2010, p. 173). Specifically, we extend the activity system perspective of business models that was developed by Amit and Zott (2001) and further elaborated in their subsequent works (Amit & Zott, 2001, 2012, 2015). The strength of the activity system perspective is that it is theory-driven and recognizes the boundary-spanning nature of value creating activities. Compared to other approaches, such as the design perspective of Osterwalder (2004) that provide a complete picture of various business model elements but are more suited to expository, diagnostic, and mapping exercises, the activity system perspective has sound theoretical foundations that can support rigorous analysis for establishing causal relationships between business model design and performance (Demil & Lecocq, 2010). Moreover, this perspective takes activities as units of analysis, which allows closeup examination of the coordination of interdependent value creating activities by a network of actors (Zott & Amit, 2010). This approach draws on theoretical insights from value chain analysis, transaction cost economics, the Resource Based View, and strategic networks to characterize value creation processes, which are difficult to comprehend through narrow theorical lenses (Amit & Zott, 2001).

The activity system of business models, however, has certain limitations that need to be addressed before it can be used for our purpose of analyzing the coordination and governance of social value creation activities. Primarily, it is solely concerned with value creation processes and is not integrated with outcomes of value creation. Related to this, there is no explicit identification of relevant stakeholders that are affected by or contribute to value creation. The following subsection discusses our approach for modifying the activity system perspective to address these shortcomings.

Conceptualizing Social Value

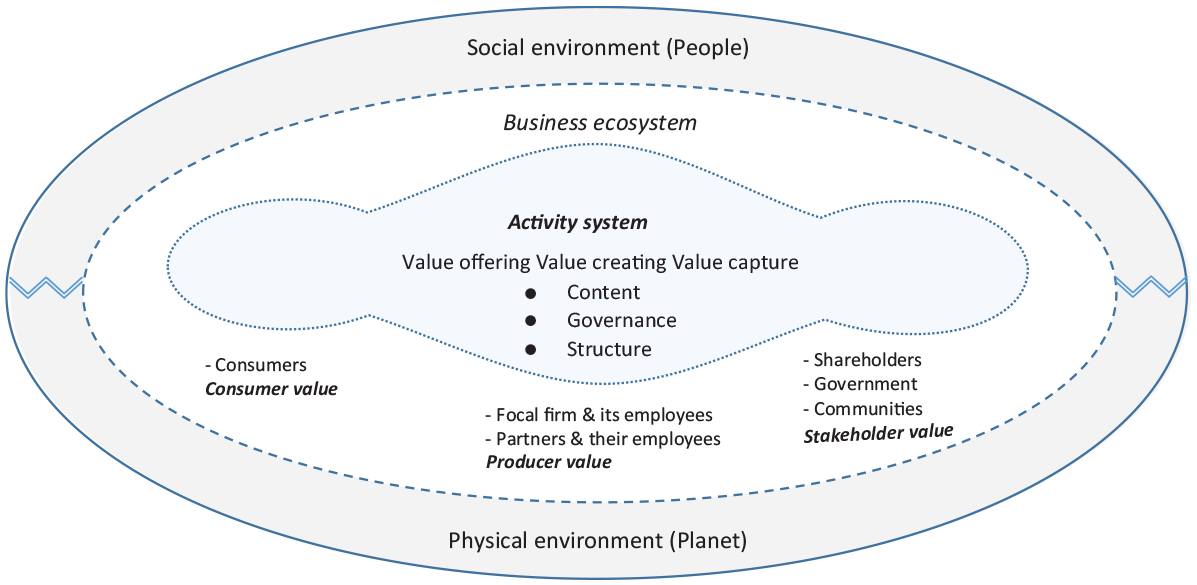

We build on the activity system perspective of business models to develop an integrative framework for conceptualizing social value (Amit & Zott, 2001; Zott & Amit, 2010). First, we extend the existing framework by introducing two additional business model components: (a) value offering and (b) value capture. Figure 1 depicts our business model framework, which situates the value creating activity system within a business ecosystem that comprises its stakeholder network. The activity system is composed of a core of value creating activities, and two extensions related to the value offering/proposition, and value capture/appropriation. In line with the existent literature, this approach characterizes the business model as a set of activities that creates and delivers a value offering to customers and captures part of that value for its stakeholders (Teece, 2010). Second, our modified framework identifies key stakeholders that are related to the business model either because they directly participate in value creating activities, or because they are indirectly affected by them. Finally, we explicitly situate the business model in its social and physical environment, which is crucial for grasping the full extent of positive and negative externalities created by the activity system.

Business Model Components and Relevant Stakeholder Groups.

This framework offers several advantages for understanding the processes and outcomes of social value creation. First, its integrative nature makes it convenient for analyzing the relationship between the firm and its external environment that contains relevant societal stakeholders (Dahan et al., 2010; Zott et al., 2011). In particular, it can be used to capture what type of value an organization creates, how it creates and delivers this value, and how this value is appropriated by societal stakeholders. This makes it useful for assessing the complex interdependence between the focal firm and other actors in multi-stakeholder social value creation efforts (Dahan et al., 2010; Porter & Kramer, 2011).

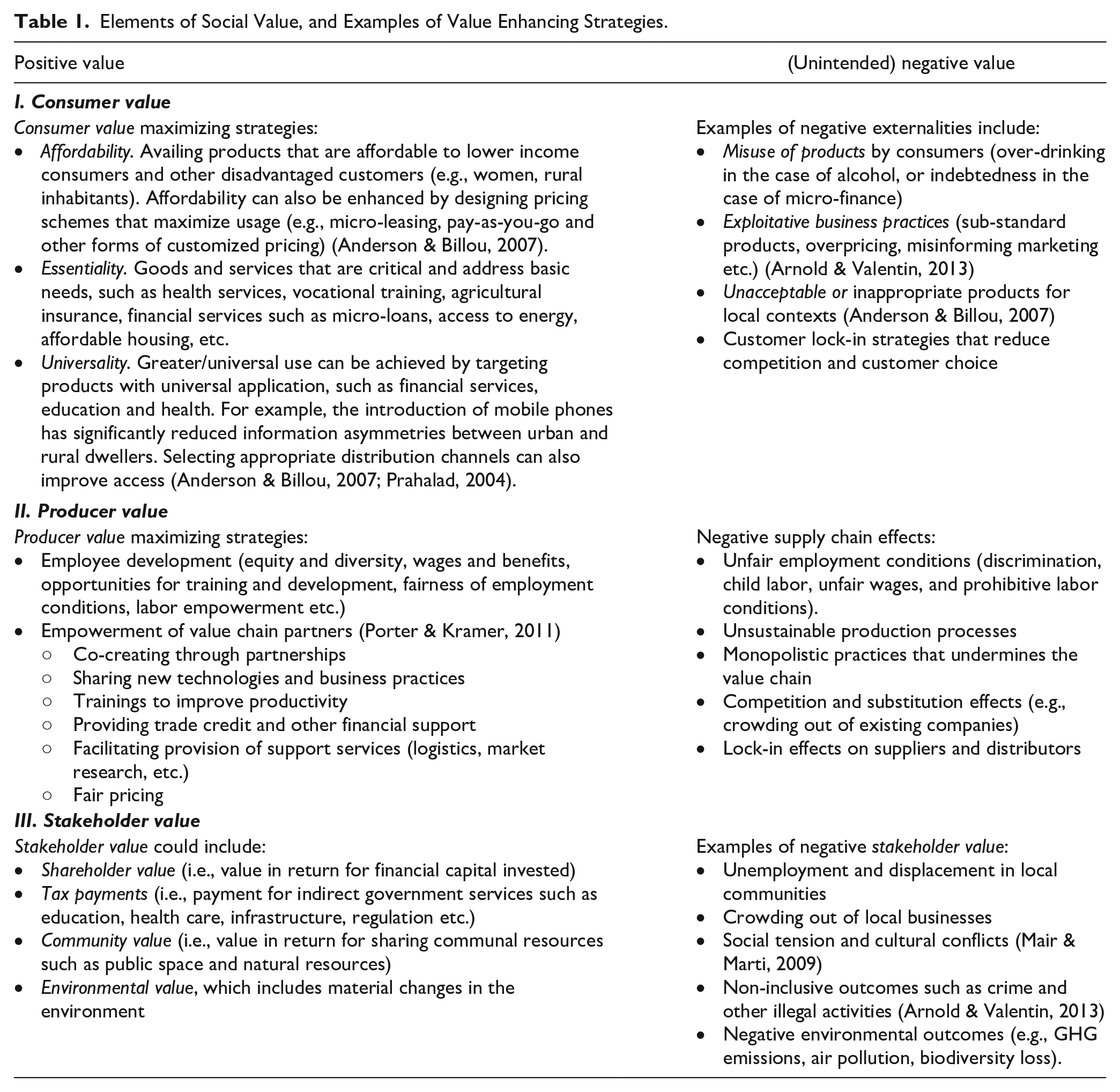

Second, the activity system framework can help unpack the drivers of social value creation through a systematic examination of the configuration of activities in terms of their content, structure, and governance. It is, for example, suitable for analyzing how the use of new technologies such as the internet and mobile phones influences the coordination of activities in a business model (Foss & Saebi, 2017). The business model perspective has been used by previous studies for understanding the dynamics of value creation and capture in changing and new industries (Achtenhagen et al., 2013; Demil & Lecocq, 2010). In our case, the approach can illuminate how information and communication technologies influence the coordination of social value creation activities, and how different systems of governance shape value appropriation (Geissdoerfer et al., 2016). We subsequently provide a brief description of the business model components, and their relationship with social value (Table 1).

Elements of Social Value, and Examples of Value Enhancing Strategies.

The value offering

The value offering is the good or service that is on offer for customers, who either directly consume it or distribute it to other consumers. The value offering can also constitute a bundle of concepts that combines products along with complimentary services. A successful value offering is able to elicit payment from consumers for reasons such as novelty, convenience, simplicity, value for money, aesthetic value, or other functional benefits (Lepak et al., 2007). Creating a successful value offering, therefore, requires an understanding of certain “deep-truths” pertaining to what consumers need and how they can be met (Teece, 2010).

Businesses that aim to enhance social value will need to take additional steps beyond creating a value offering that can elicit payment (Anderson & Markides, 2007). Table 1 identifies some examples of how consumer value can be enhanced or adversely affected by business operations. Welfare economics states that consumer value is the difference between the benefit (utility) that consumers get from using a product or service, and the price they pay for it (Feldman & Serrano, 2006). This value can be increased by providing value offerings that are affordable, essential, and/or universal. 2 Enhancing the affordability of the value offering, for example, through tailored pricing schemes, can benefit relatively low-income consumers that are hurt by small price changes (Anderson & Markides, 2007). Essential value offerings that address fundamental needs such as food, sanitation, health, and education can enhance consumer value since consumers are likely to derive higher benefits (utility) from these services. Finally, businesses can provide universal value offerings that address the latent needs of broad segments of society (e.g., health, education, financial services), and thus can provide benefits for the largest possible number of people.

Creating value

Creating value entails a set of activities, resources and processes that are needed to create the value offering and deliver it to consumers. The process of value creation can be conceptualized in different ways, depending on the purpose of the analysis and the nature of the study. For example, the resource-based view of the firm suggests that value creation can be modeled as a process of bundling resources (Demil & Lecocq, 2010). Our framework builds on the activity systems perspective, which defines value creation as the process of interlinked activities within and across the boundary of the firm (Amit & Zott, 2001; Zott & Amit, 2010). The units of analysis are activities, which are defined as “the engagement of human, physical and/or capital resources . . . to serve a specific purpose” (Zott & Amit, 2010, p. 217). An activity system includes an interdependent set of activities performed by a network of actors that includes the lead firm, its partners, suppliers, and distributors (Zott & Amit, 2010).

Understanding value creation thus involves studying how the activities of the focal firm are interlinked with those of its partners (Zott et al., 2011). Amit and Zott (2001) introduce three design elements of an organization’s activity system that are essential for understanding its value creation process. These are the content, structure, and governance of the activities performed to provide a certain service. The content of an activity system refers to the nature and purpose of the activities, whereas the structure describes the way in which these activities are linked with each other. The structure of the activity system thus reveals the connections between different activities, and their contributions to the value creation process. The governance of an activity system identifies which party performs what activity, and how these responsibilities are enforced (Amit & Zott, 2012; Zott & Amit, 2010). The activity system perspective is thus highly suitable for identifying the drivers of value creation by systematically analyzing the content, structure and governance of an activity system (Amit & Zott, 2001). Table 1 lists the different stakeholders that partake in, or are affected by, the value creation process.

Producer value includes income and other benefits, net of associated costs, for different actors that perform value creating activities throughout the value chain. This includes the value created for the focal firm and its employees, and co-producer value created for business partners, such as distributors and suppliers, that work in tandem with the focal firm to perform various value adding activities, such as the provision of intermediate inputs and services. BoP businesses can advance co-producer value by integrating local producers in their activity system, and taking concomitant measures to boost the value accruing to them through greater formalization, improved productivity and more fair pricing practices (see Table 1).

Value capture/appropriation

Value capture/appropriation refers to aspects of the business model that are related to the capture of economic value by different stakeholders. Traditionally, the ultimate goal of value appropriation is maximizing shareholder value through decisions related to pricing, customer acquisition, market development, cost management, and so on. As a result, value capture by stakeholders that did not (directly) contribute to value creation is referred to as “value slippage” (Lepak et al., 2007) or “value missed” (Yang et al., 2017). Emphasis on social value creation implies a more holistic conception of stakeholders, which also includes the government, members of the business ecosystem, the environment, and local communities. Creating social value, therefore, entails identifying the key societal segments for whom value is created, and developing a governance mechanism that allows them to capture a fair share of the created value. Advancing stakeholder value further requires creating strategies for advancing economic as well as social and environmental value, and assessing performance using appropriate metrics to inform subsequent decisions (see Table 1).

Elements of Social Value

The framework introduced in the previous subsection identifies three broad components of social value: (a) consumer value embedded within the value offering; (b) producer value or value accrued to the focal firm, its partners and their employees; and (c) stakeholder value, which captures effects on stakeholders that are not directly engaged in production but have an interest in (or are affected by) the business, such as capital owners, the government, local communities, and the physical environment. Shareholder value is an important component of stakeholder value, but shareholders are only one among many relevant stakeholder groups that may have interest in the business (Freudenreich et al., 2019). Stakeholder value, therefore, includes values created for diverse stakeholders such as tax payments to the government, social benefits created for local communities, and positive and negative environmental impact (van Tulder et al., 2014).

BoP businesses can maximize social value by increasing any of the three constitutive components of social value without reducing other elements of social value, and without creating unfair distributional outcomes. Furthermore, social value can be enhanced by mitigating the negative externalities that adversely affect different stakeholders (cf. Feldman & Serrano, 2006). Table 1 provides some examples of these (unintended) externalities that can affect consumers, value chain partners, and local communities.

Empirical Application

The following two sections will analyze a real-world case of social value creation using the business model framework introduced in the previous section. The analysis is based on an in-depth study of a multi-stakeholder social value creation initiative in Kenya’s major mobile money service of M-Pesa. Our aim is to apply the framework for understanding the processes of coordination and governance in multi-stakeholder social value creation initiatives in contexts characterized by institutional voids. The analysis will also shed light on the practical challenges, potential trade-offs and tensions that arise in multi-stakeholder initiatives that aim to advance social value for a large number of stakeholders.

Data and Method

We chose the case study method due to its suitability for answering fundamental questions of why and how through an in-depth examination of an emergent phenomenon within its real-life context (Yin, 2014). Case studies are particularly appropriate for analyzing novel phenomena for which existing theory might not apply, and thus there is a need to build or extend theory (Eisenhardt, 1989). The method, therefore, suited our ambition to conduct in-depth data analysis to explain the complex and novel process of social value creation. Our goal is to develop a set of potentially generalizable and testable propositions that can guide future research.

We chose to study M-Pesa because it is generally considered to be a highly successful, multi-stakeholder initiative of social value creation for BoP users. M-Pesa has enhanced consumer value by expanding financial inclusion among tens of millions of poor people in East Africa through an innovative service that is affordable, accessible, and convenient. Moreover, it perfectly matches our goal to study the coordination of multi-stakeholder (boundary-spanning) value creation, since it is delivered collaboratively through an extensive network of actors that includes a telecom firm (Safaricom), hundreds of bank branches, and more than a hundred thousand of small-scale businesses that serve as M-Pesa agents. M-Pesa has received numerous accolades for its social impact from the global association of telecom operators (GSMA) and other international institutions, enabling Safaricom and Vodafone to top Fortune’s “Change The World” list of companies in 2015. Safaricom has subsequently become an active member of global associations that advance sustainable business practices, such as the UN’s Global Compact, the Business and Sustainable Development Commission (BSDC) and is an early adopter and supporter of the Sustainable Development Goals (SDGs).

The success of M-Pesa has spawned a new mobile money industry in Kenya and the East African region at large. 3 Kenya is a world leader in mobile money, with 73% of adults owning a mobile money account in 2017, out of which 81% were users of M-Pesa (Demirguc-Kunt et al., 2018). Several studies have also documented the welfare advantages of M-Pesa, with some reporting that it helped lift 2% of Kenya’s population out of poverty, women-headed households especially benefiting the most form the service (Jack & Suri, 2014; Suri & Jack, 2016). An in-depth case study of M-Pesa, therefore, can shed light on what constitutes social value, and what factors influence the coordination of value creating activities across actors. Given the difficulty of replicating or studying unique cases in multiple settings (Eisenhardt & Graebner, 2007), we follow previous research and adopt a single case study design.

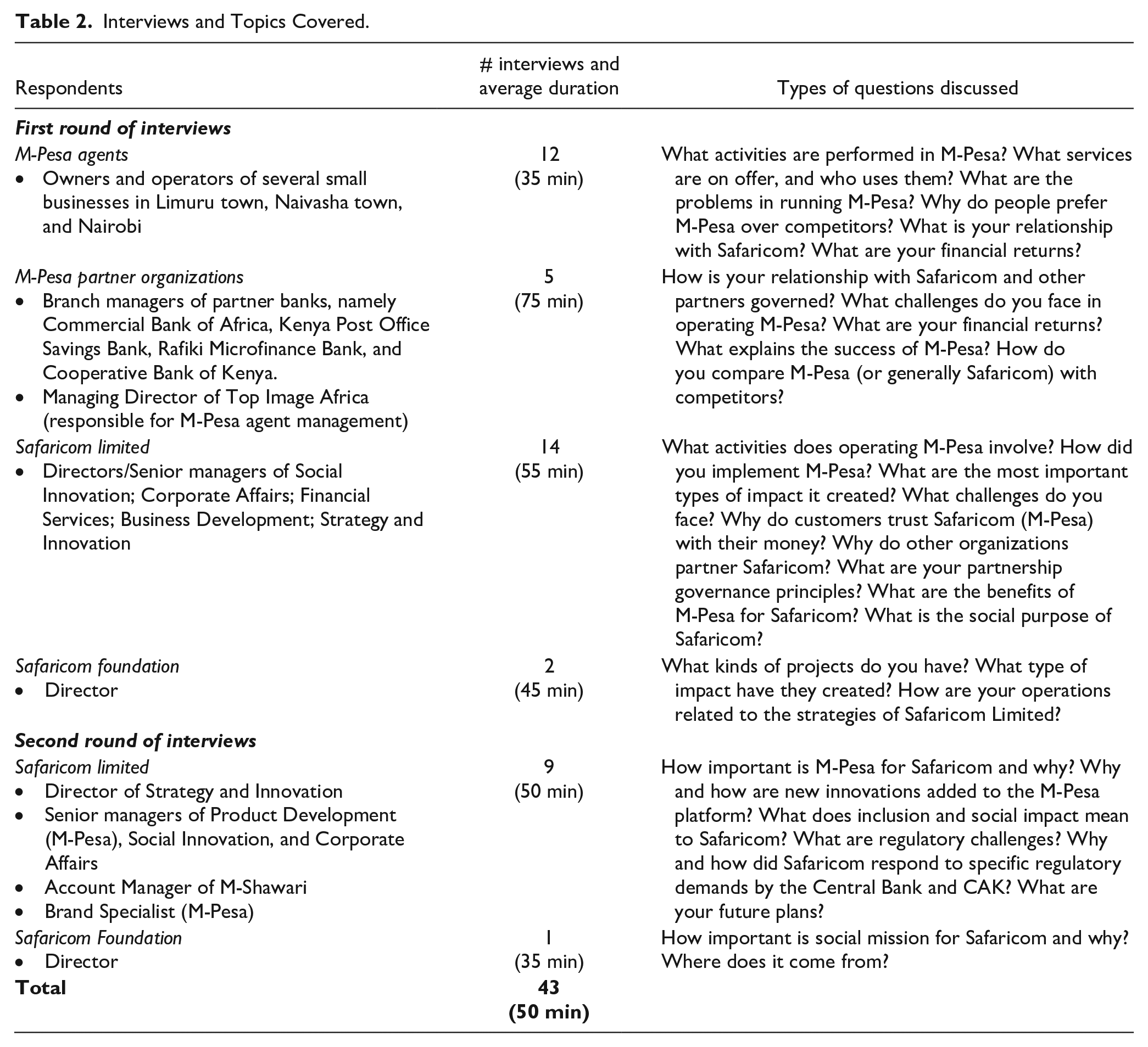

We draw on interview data collected in two rounds of fieldwork and secondary data from multiple sources. The first round of primary data collection took place in a period of 5 weeks in March and April 2016, and the second round took place for a week in February 2017. Prior to data collection, we developed a detailed case study protocol that outlined our research goal (to understand drivers of success in the M-Pesa business model), and our methods for researching it. The protocol included a thick description of the M-Pesa case, and potential research directions that we developed based on insights from our preliminary discussions with two middle-managers of Safaricom, and our reading of archival materials from secondary sources (see Appendix A). It also included a list of respondents, and an extensive set of semi-structured interview questions to guide our data collection. Rather than starting data collection with a clean slate, we approached it with broadly defined, semi-structured questions around specific topics, which we adjusted in subsequent stages in light of emerging insights. Our initial interview questions sought to understand the M-Pesa business model and its ecosystem, and to identify the organizational and business model features that facilitated its diffusion and shaped its social impact (see Table 2). This flexible process made our data collection manageable, and avoided the risk of being overwhelmed by a large volume of data (Eisenhardt, 1989).

Interviews and Topics Covered.

Our interviews covered a wide range of organizations in the M-Pesa ecosystem. The first round of fieldwork resulted in 32 interviews, out of which about half were conducted with medium and senior managers of Safaricom, and the remaining 17 were with external partners (Table 2). We used theoretical sampling procedures (Yin, 2014) in close consultation with our contact persons to choose respondents that were best-positioned to address our questions in terms of their work profile and experience. In a few instances when it was not possible to get access to the selected respondents, we modified our list by choosing among available respondents. All but two interviews were tape-recorded, and for the two cases where transcription was not possible, shorthand notes were taken and verified with the respondents. The duration of the interviews ranged between 30 minutes and 2 hours and averaged about 50 minutes. In addition to conducting the interviews, the researchers visited Safaricom shops to observe how clients used M-Pesa, and personally registered and used M-Pesa to get firsthand experience of using the service.

We also draw on a number of secondary sources to complement our interview data, more particularly for re-constructing a historical account of the development of the service (see Appendix A). This includes a few in-depth retrospective first-person accounts that were written by individuals who played important roles during the initiation of the pilot project. This included Hughes and Lonie (2007), and particularly Vaughan et al. (2013), which was co-authored by Michael Joseph, the former CEO of Safaricom. Likewise, we used archival materials such as annual reports of Safaricom and its partner banks, reports by the Central Bank of Kenya and research reports on M-Pesa. These documents were used to trace the development of the service in terms of important changes in business model features, and for collecting factual data on adoption and development trends. Triangulation of evidence from diverse data sources was useful for identifying key constructs and for cross-checking retrospective accounts from interviews.

After each step of data collection, we used the qualitative data analysis software (NVivo 11) to systematically organize and code our data. We started open coding with the broad aim of identifying business model elements that are likely to characterize the development and diffusion of M-Pesa and its internal coordination mechanisms. As the analysis revealed an increasing number of themes, standard text analysis techniques were used to identify aggregate themes (Braun & Clarke, 2006). Given our aim to understand the coordination mechanisms in business models for social value creation, we closely consulted the business model and BoP literatures to better understand the emerging themes, and to organize them into meaningful constructs (Eisenhardt & Graebner, 2007).

Our subsequent data analysis was iterative and overlapped with data collection as we analyzed our data after each round of fieldwork. In the tradition of abductive research where theory and method are interlinked and inform each other (Van Maanen et al., 2007), we used newly collected data to improve our empirical framework, which in turn pointed to new data needs. This iterative process helped us develop and refine our business model framework, which guided our final analysis on the drivers of social value creation in M-Pesa. We further enhance the generalizability of the results by developing testable propositions to provide sharply defined constructs (Eisenhardt, 1989) that would facilitate subsequent empirical testing (Gioia et al., 2013). To check the validity of the results, preliminary results from the analysis were presented at a research workshop attended by senior management staff of Safaricom who had been involved in the development of M-Pesa from its inception. We made minor changes in our analysis using the feedback from this meeting and other consultations with Safaricom staff, which answered our questions on the M-Pesa business model and the key historical episodes in its development.

The M-Pesa Case

M-Pesa 4 was born out of a pilot project to extend financial services to the poor, with the help of funding from UK’s Department for International Development (DFID), and Vodafone, a minority owner of Safaricom. 5 The initial goal was to develop a product that would allow borrowers of microfinance institutions to repay their loans conveniently using mobile phone devices (Hughes & Lonie, 2007). To pilot the product, Vodafone initiated a partnership that included Safaricom, a local microfinance firm and a local bank called the Commercial Bank of Africa (CBA). Upon the completion of the pilot in 2005, Safaricom and Vodafone recognized a potential for the service as a means of transferring remittances (Hughes & Lonie, 2007). M-Pesa was, therefore, modified into a money transfer service with an interface that made it simple and affordable. The product was nationally launched in Kenya in 2007 in a marketing campaign that targeted domestic remittance senders.

M-Pesa acquired more than 2 million users within a year, which grew to about 10 million within 3 years. As of early 2017, the number of M-Pesa users has reached 27 million, served by a network of more than 130,000 agents spread across the country (Safaricom, 2017). Besides achieving unprecedented levels of financial inclusion that reached nearly 70% of Kenya’s population, M-Pesa provides a much-needed additional income to its vast agent network, which mainly comprises low-income mom-and-pop stores. The value of money transferred through M-Pesa was more than 30% of the country’s gross domestic product (GDP) as of 2011 (Vaughan et al., 2013), which increased to 85% of GDP (Shs 5.29 trillion) by early 2016, making M-Pesa effectively a second currency.

M-Pesa allows customers to conduct financial transactions using a simple SMS-based technology that is available in basic mobile phone devices. To open an M-Pesa account, a customer can register for free at one of the 130,000 agent outlets that are spread across the country. When a customer deposits cash at one of the M-Pesa agents, an equivalent amount of electronic money is transferred to her virtual M-Pesa wallet. The customer can then use her electronic money to make money transfers, buy air time, pay school fees and utility bills, and make payment at tens of thousands of retail and service outlets that have adopted M-Pesa as a payment system. Cash withdrawals and transfers are subject to charges, which depend on the amount of money transferred or withdrawn.

The value offerings provided by M-Pesa have continued to expand in time. Since 2010, M-Pesa has included money deposit and loan services through partnerships with local banks. The most successful of these services is M-Shwari, which was introduced in 2012 in partnership with CBA. M-Shwari provides a paperless bank account that provides several banking products such as interest-bearing deposits and microcredit. The use of microcredits has become popular, and M-Shwari alone had amassed a customer base of more than 12.5 million, and issued more than 50,000 small loans per day with an average value of around 13 USD (Cook & McKay, 2015). M-Pesa now is a platform that bundles diverse services including international remittances, micro-insurance products, and money transfer from regular bank accounts to M-Pesa and vice versa.

Social Value Creation in M-Pesa

The goal of this section is to unpack the activity system of M-Pesa to better understand its underlying processes for creating social value. We start by describing its activity system in terms of the content, structure, and governance of key activities. We will subsequently identify different business model features that shape the coordination and governance of value creation and appropriation processes.

The Activity System

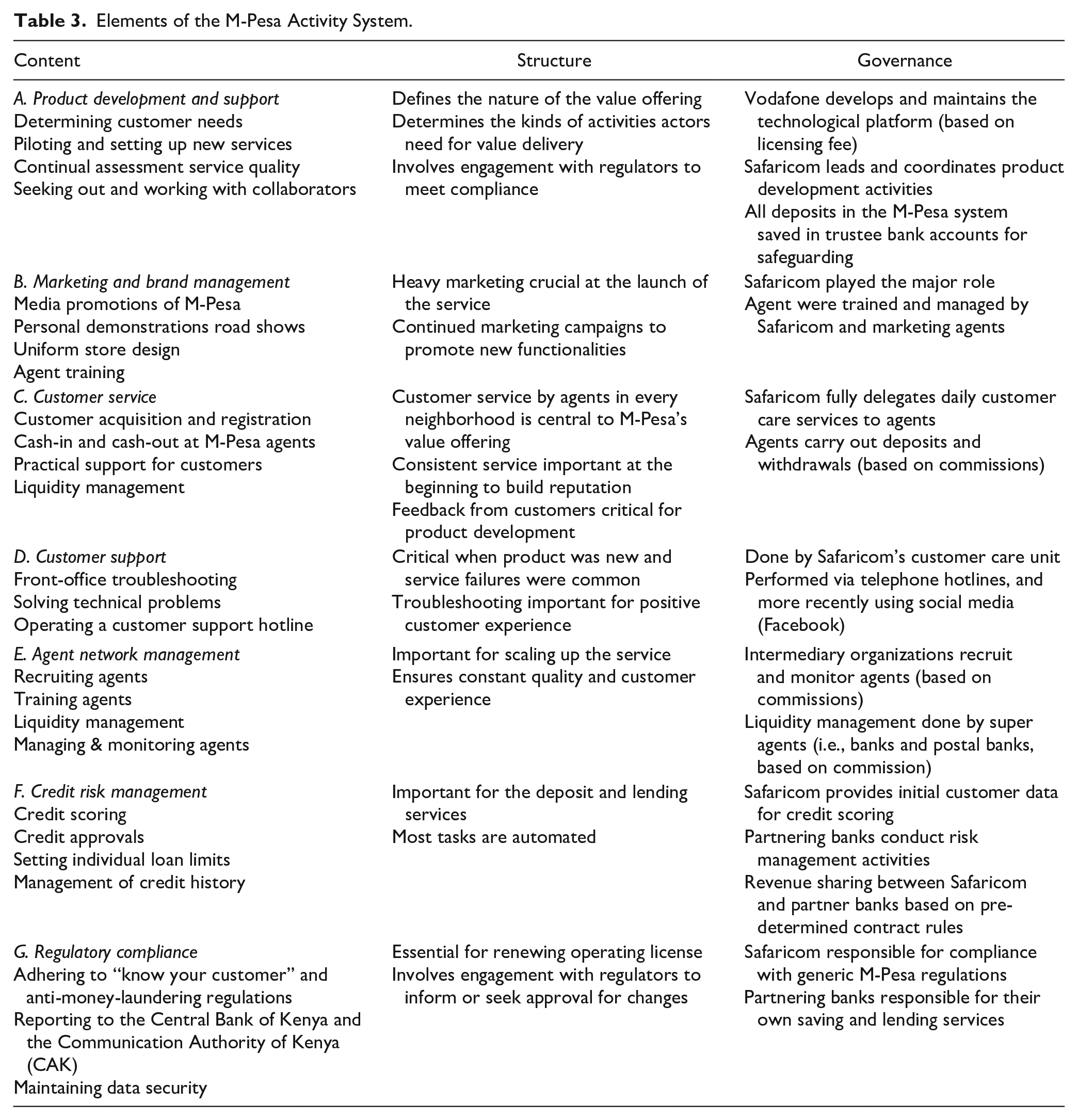

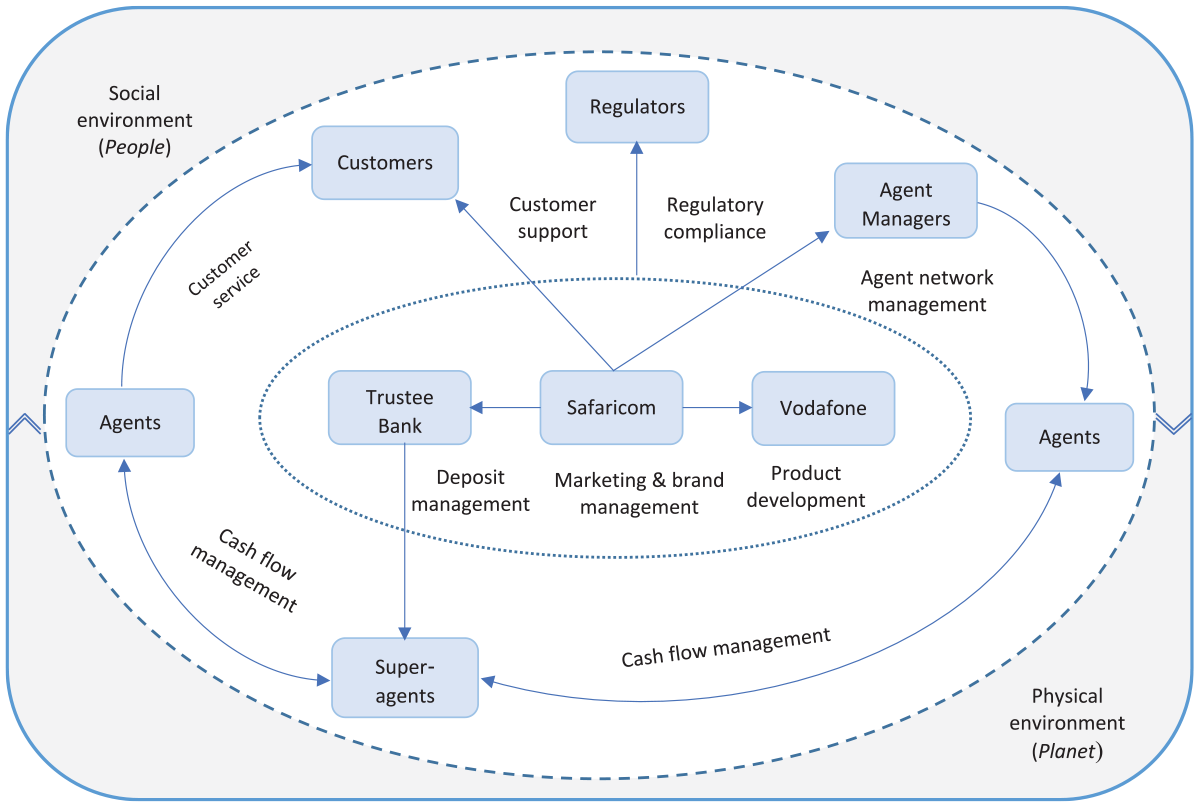

Our data analysis identified a large number of activities performed by Safaricom and other value chain partners to implement M-Pesa. We identified the following seven aggregate themes, which constitute the key elements of the M-Pesa activity system: (a) product development and support, (b) marketing and brand management, (c) customer service, (d) customer support, (e) agent network management, (f) credit risk management, and (g) regulatory compliance. Table 3 summarizes the content, structure, and governance of each of these activity sets, and Figure 2 provides a visual representation of the relationship between these activities.

Elements of the M-Pesa Activity System.

A Depiction of the M-Pesa Business Model.

Product development and support

Product development in M-Pesa involves sustained efforts to determine emerging market needs and devise appropriate value offerings. The technological platform for M-Pesa was custom-built by Vodafone and licensed to Safaricom in exchange for a technology fee, which made it possible to frequently adapt the product’s features in response to customer feedback (Hughes & Lonie, 2007). Safaricom was responsible for operational aspects of product development, including identifying new customer needs, deciding whether or not to initiate new value offerings, and committing the necessary resources. Safaricom’s commitment for social causes was critical for the success of M-Pesa, 6 beginning from ensuring that the service targeted a socially important, unmet market need, to mobilizing resources, and acquiring legitimacy for the new service. At the time of launch of M-Pesa in 2007, Kenya lacked regulatory provisions to govern mobile banking, which necessitated proactive engagement with the Central Bank of Kenya during product development (Cook & McKay, 2015). Product development and support remained important throughout the operation as the M-Pesa platform continuously expanded to include new functionalities such as saving and borrowing services, and integration with ATMs, which were often implemented in collaboration with local banks and other organizations. Based on the experiences from the piloting of M-Pesa, these services were highly informed by customer feedback through market research, but also through direct observation of the ways in which customers used the product.

Marketing and brand management

Safaricom employed mass awareness-raising campaigns that included television and radio advertisements and personal demonstrations in road shows (Mas & Ngweno, 2010). In addition, word-of-mouth marketing was used to facilitate the diffusion of M-Pesa and build trust in the early days of the service. Safaricom also leveraged its recognizable brand name to enhance the appeal of M-Pesa, for example, by adopting uniform displays with a Safaricom logo in all agent shops (Mas & Radcliffe, 2010). Marketing activities are organized and executed mainly by Safaricom, which has extensive marketing experience, strong market presence, and positive brand image in Kenya.

Customer service

Customer service in M-Pesa includes activities such as cash-in and cash-out services, registering new customers, on-site troubleshooting, and cash flow management. The vital task of converting cash to electronic money and vice versa is carried out by an extensive network of agents. The role of Safaricom here is limited as agents are fully responsible for acquiring and registering new M-Pesa customers and introducing them to the service. Since commissions are based on the value of transactions and the number of new customer registrations, agents have strong incentive to attract and maintain customers through high-quality service. Individual agents must maintain sufficient cash stock in their stores to avoid turning down customers that need cash withdrawal. Agents thus regularly visit bank branches and other partners (also called super agents) to replenish their cash stock at the beginning of the day (or whenever they need cash), and to convert it back to electronic money, often at the end of a working day.

Customer support

Customer support for M-Pesa is provided by Safaricom through various channels. In its early days, M-Pesa experienced frequent operational problems including system blackouts and other technical glitches, in addition to customer mistakes due to lack of familiarity with the service. Safaricom responded by establishing a back-office customer support unit and a dedicated hotline that users could call to troubleshoot these problems. In addition, Safaricom provided customer support in its retail centers that are located in all major cities. A reliable customer service was crucial for establishing trust in M-Pesa, especially among new customers that were not familiar with the service (Morawczynski & Miscione, 2008). More recently, technical problems have become less common, so customer support is being given through social networks (Facebook) to reduce the cost of maintaining customer support staff.

Agent network management

M-Pesa’s more than 130,000 agents form the interface between Safaricom and M-Pesa users, making the task of agent network management a vital activity. The task includes recruiting new agents, training and monitoring them regularly, and managing their liquidity. Early investments to ensure high-quality agent network with extensive coverage was vital for the quick success of M-Pesa. Safaricom delegates these activities to external subsidiaries due to the extensive nature of the task and its distance from its core operations. Two intermediary marketing organizations are responsible for recruiting, training, and regularly monitoring agents on behalf of Safaricom. These organizations conduct all agent administration tasks, including handling monthly commission payments for the agents they manage. In addition, Safaricom partners with an extensive network of financial institutions, including bank branches, postal banks, and microfinance institutes, to manage the cash stocks of agents. These institutions are also called “super-agents” and serve as wholesalers for distributing cash and electronic money between Safaricom and its agents. Their main task is dispensing cash to agents for daily use (often at the beginning of the day) and taking deposits from agents (often at the end of the day), which is conducted with the help of the electronic transaction system of M-Pesa. These super-agents also receive commissions from Safaricom based on the value of transactions they handle with the agents.

Credit risk management

Credit risk management is needed for money deposit and lending services through functionalities such as M-Shwari and KCB M-Pesa. Each of these services are offered in partnership with local banks, since lending and other banking services are not permissible to a telecom firm like Safaricom. The banks take the leading role in running credit risk management tasks, including deciding loan limits for clients, processing loan applications, handling interest fees, following up payment, and legal and other recourses in the case of default.

Regulatory compliance

Regulatory compliance in M-Pesa involves meeting multiple financial statutory provisions including “know your customer” regulations, anti-money laundering policies, and compliance with value limits for transfers and loans. Safaricom is required to regularly report key indicators on the performance of M-Pesa to the regulator of the financial sector (Central Bank of Kenya) and to the telecom regulator (Communications Authority of Kenya, or CAK). Most of the regulatory demands related to the general operations of M-Pesa are the responsibility of Safaricom, whereas specific regulations pertaining to deposit and lending activities are the responsibilities of the respective partnering banks.

Figure 2 visually maps out these activities, along with the actors responsible for them and their linkages. In terms of structure, it reveals that product development, deposit management, marketing, and brand management were central activities that were performed by the three core stakeholders in the activity stem. The arrows linking different stakeholders also reveal the way different activities were coordinated and governed. For example, Safaricom was responsible for customer support, agents were responsible for customer service, and Trustee Banks handled deposit management functions through various super-agents. In addition to providing an overview of the flow of value adding activities among stakeholders, these linkages indicate the allocation of responsibility and the associated structure of governance in the activity system.

Drivers of Value Creation

Having described the different elements of the activity system of M-Pesa, we now systematically investigate how their coordination and governance influenced social value creation. Since consumer, producer, and stakeholder value are created jointly in a collaborative activity system, we look at the activity system holistically rather than seeking to establish separate driving factors for each element. Our analysis identified five cross-cutting features of the M-Pesa’s activity system that played an important role in its ability to create social value. Additional evidence, including illustrative quotes from our interviews, to support these results is provided in Appendix B.

Utility

Utility here refers to the capacity of a value offering to enhance consumer value by addressing a deeply-needed (essential) and broadly demanded (universal) social issue in a commercially feasible and affordable way (Cf. Table 1). An important factor behind the rapid diffusion of M-Pesa is the functionality of the value offering, which effectively met a universal and essential latent demand for financial services that was not affordably provided by existing financial institutions (Jack & Suri, 2014). Due to the low level of bank penetration in Kenya, people had to either travel in person or use messengers to transfer money across the country. Other alternatives such as postal services were perceived to be too expensive and slow. M-Pesa thus provided a reliable, convenient, and affordable alternative to the existing methods of money transfer that were risky and expensive. The extensive agent network of M-Pesa, its integration with ATM platforms and bank branches, and the widespread availability of mobile phones also enhanced the functional benefits of M-Pesa for sending and receiving money.

The utility of M-Pesa was enhanced through conscious design efforts to create a locally appropriate value offering. From its inception, M-Pesa was intended to be simple enough to be usable by ordinary people with limited technological exposure. The application uses basic SMS technology that is available on every mobile phone, and supports text in the local language (Swahili), which makes it accessible for everyone. The operation of the technological platform and its user interface is straightforward, greatly enhancing its appeal for potential users. The M-Pesa menu is directly installed on the SIM card, and customers can make transactions immediately after opening an account and depositing cash. Such a high level of adaptation to meet the needs of the local Kenyan market was achieved through a deliberate decision to develop the technological platform of M-Pesa in-house by Vodafone.

The value delivery and other support activities of the activity system also improved the utility of the product by enhancing customer experience. For example, the value offering was introduced to customers using a simple marketing campaign to “send money home,” which emphasized a highly demanded function of the product. Once customers were acquainted with the peer-to-peer money transfer service, additional extensions with various functions were gradually introduced. The registration process to open an M-Pesa account is short and free of charge, and the transaction processes are also clearly communicated through visual displays. When a customer transfers money, she receives an instant message confirming payment while at the other end of the line the receiver gets a notification of receipt. The prices charged for sending and receiving services are publicly displayed at the agents’ shops, which creates consistency and transparency, eventually enhancing trust.

Overall, M-Pesa can be characterized as an inclusive value offering that extends a wide range of financial services to millions of previously excluded users, such as rural inhabitants, semi-literate people, and low-income users. Surveys of mobile money usage indicate that more than half of M-Pesa users do not have formal bank accounts (Demirgüç-Kunt & Klapper, 2012), making M-Pesa their only means of accessing financial services. This was achieved by increasing the utility of the value offering and finetuning its delivery system, which expanded its potential to create social value. This leads to our first proposition:

Proposition 1: A careful design of the value offering that ensures local appropriateness, and an effective delivery system enable greater consumer value by increasing the utility of the offering to previously excluded users.

Boundary spanning

M-Pesa is a boundary spanning or multi-stakeholder business model that is implemented through a collaboration of diverse organizations in different industries. At the core of this collaboration are the three leading firms—Safaricom, Vodafone, and CBA—that contribute their competences to create the value offering of M-Pesa (see Figure 2). A second layer of organizations constitutes an extensive network of agents, super-agents, and other intermediaries that made M-Pesa accessible throughout the country. The service, therefore, is offered through an ecosystem of organizations that interact intensively to co-create a unique value offering that would not have been created by any of them individually.

Each of these organizations contribute unique competences. Safaricom, for example, took on marketing and brand management tasks to take advantage of its recognizable brand name, solid marketing expertise, and the technology to reach potential users. Agent network management, on the other hand, was far from Safaricom’s core competences, and was hence outsourced to intermediary marketing organizations through contractual arrangements. The involvement of diverse partners in the ecosystem enabled the service to be embedded into various payment and financial platforms that led to more intensive use of the service. As a result, M-Pesa is now integrated into the payment systems of utility companies, retail and service centers, bank branches, and even tax offices.

Transaction cost theory can be used to explain why M-Pesa is offered neither by a single organization (hierarchies) nor through independent market exchange, but rather through the hybrid form of alliances (Powell, 1990; Williamson, 1975). The assets needed to create value in M-Pesa are unique to the partnering organizations and could not have been easily outsourced. The brand name and organizational resources of Safaricom, the technological expertise of Vodafone, and the operational license and risk management knowhow of partner banks are embedded within the respective organizations, which necessitated a hierarchical organizational form. On the other hand, M-Pesa was built around clearly stipulated contractual arrangements that reduced transaction costs and thus allowed independent, market-based coordination. Moreover, the use of SMS technology for executing and communicating transactions further reduced coordination and monitoring costs. The hybrid or alliance-based organizational form of M-Pesa, therefore, optimizes between the high levels of asset specificity of the resources required for the service, and the low cost of coordinating activities among service providers that was achieved by using ICT.

The use of ICT has thus enabled a boundary-spanning activity system that created co-producer value for more than 130,000 smalls businesses, including informal mom-and-pop store that earned commission income as M-Pesa agents. Effective use of ICT for creating and delivering a more accessible and affordable value offering is also the main reason why M-Pesa is preferred to alternative services such as agency banking and micro-finance. The case, therefore, illustrates how ICT enables new business models that enable unique value offerings through the bundling of diverse competences.

Proposition 2: ICT enables greater social value creation by reducing the cost of coordinating boundary-spanning activity systems, thus allowing the bundling of diverse competences into unique value offerings.

Alignment

In any activity system that encompasses different organizations, success will eventually depend on the alignment of interests, values and resources (Gulati & Singh, 1998). The activity system of M-Pesa was designed in such a way that each partnering party not only contributes unique resources for creating value, but also captures some of the benefits– thus creating an alignment of interests. The financial rewards have been most apparent for Safaricom, for whom revenues from M-Pesa made up 25% of its annual revenues in 2016 (Safaricom, 2017). 7 The service also provided additional commission income for 130,000 small and micro enterprises that served as M-Pesa agents. Revenue sharing on the basis of commissions between Safaricom on the one hand, and agents and super-agents of M-Pesa on the other, was crucial for motivating the latter to give high quality customer service. This was governed by contractually enforced agreements that stipulated the roles, responsibilities and rewards of each party, which enhanced transparency.

Furthermore, banks and other financial institutions benefited from M-Pesa in a number of ways, which reduced initial opposition and gradually won their endorsement (Vaughan et al., 2013). First, M-Pesa encouraged people to save and transact through formal financial institutions rather than saving money at home, which the banks saw as beneficial. Second, most banks in the country started to serve as agents or super-agents, which enabled them to receive commission income in exchange for handling M-Pesa transactions. Finally, M-Pesa streamlined banking services since clients now could manage their savings by transferring money to and from their M-Pesa accounts, either through their mobile phones or through ATM outlets. This reduced the frequency with which clients needed to visit bank branches, improving operational efficiency. 8 The integration of financial institutions in the activity system was thus essential for placating early opposition from incumbent banks that felt threatened by M-Pesa’s radically innovative business model for providing financial services.

Furthermore, the provision of financial services through M-Pesa was aligned with the interests of the Central Bank of Kenya, which aimed to promote financial inclusion. This shared interest eased the regulatory burden for M-Pesa, allowing it to operate outside the extensive regulatory framework that governed financial institutions (Mas & Radcliffe, 2010). The alignment of the interests and incentives among the diverse stakeholders in the M-Pesa activity system was thus essential for acquiring regulatory approval, and subsequently for its integration with the broader economy.

Proposition 3: An activity governance system that aligns the interests of diverse stakeholders advances social value creation by facilitating the integration of new value creating activities within established activity systems.

Centrality

Analysis of the M-Pesa activity system reveals the central position held by Safaricom. Although Safaricom delegated several activities to its agents and partners (Table 2), the company maintained strict control over the most important decisions in the activity system. For example, the payment system is strictly centralized—all commissions are collected by Safaricom after each transaction, to be paid back to agents and super-agents at the end of the month. Likewise, Safaricom remains to be the major party responsible for coordinating the legal framework that governs its relationship with its value chain partners, especially with its agent network. This central position of Safaricom gave it the power to set contractual terms that were beneficial to itself relative to its partners. Until very recently, for example, Safaricom used exclusion clauses to prohibit M-Pesa agents from serving as gents of competing mobile money service providers. However, as a central player, Safaricom is also the thread that holds everything together. The organization’s commitment for the service was crucial in the early days when strong leadership was needed to make risky investments for building the technology and mobilizing an extensive agent network. For example, Safaricom bore the full cost of replacing millions of old SIM cards with new ones in which the M-Pesa application was pre-installed during the introduction of the service. This illustrates that M-Pesa was an outcome of a deliberate organizational effort to advance social value through a novel technology-driven business model.

Proposition 4: The presence of a committed and well-resourced central player in an activity system fosters social value creation by enabling effective coordination and risk taking.

Lock-in

The activity system of M-Pesa has an array of lock-in mechanisms that maintain its current customer base. This is apparent from the fact that, in spite of the entry of more than five competitors, including more affordable ones such as Airtel Money, M-Pesa continues to be by far the largest mobile money service in the country, with a market share of 81% in terms of users as of 2017. 9 We identify three important factors that explain this outcome: (a) network externalities, (b) Safaricom’s strong brand name and reputation, and (c) conscious strategies to attract and maintain customers.

According to network theory, the value and attractiveness of a network increases with the number of its users since the possibilities for its users to interact and to use the system also expands, attracting even more users and locking in existing ones (Farrell & Klemperer, 2007). Network externalities constitute an important lock-in mechanism in M-Pesa, which resulted from Safaricom’s first-mover advantage and its dominant position in Kenya’s telecom sector. With a market share of more than 70%, Safaricom started off with millions of subscribers who freely upgraded their SIM cards to become M-Pesa users. The company also owned a large network of distribution shops that were quickly expanded to become M-Pesa agents, while also drawing from its extensive pool of airtime dealers to recruit agents. The large-scale launch of the service and the accompanying aggressive marketing made it an instant success, quickly attracting millions of customers. This initial success allowed agents to earn high commission revenues, which in turn brought in more agents and kept existing ones, thus effectively curtailing the ability of late-coming competitors to make headways.

Customers and agents also had more reasons to continue using M-Pesa, apart from the benefits of belonging to an ever-expanding mobile money network. Through effective marketing, Safaricom had managed to strongly connect M-Pesa to its own brand name to increase customer trust in the new service. Being a major, pioneering mobile telecom company, Safaricom already had a recognizable brand name, which it successfully leveraged to strengthen trust on its new M-Pesa service (Morawczynski & Miscione, 2008).

The last lock-in mechanism in M-Pesa is a number of conscious strategies that were adopted to attract and keep customers. For example, M-Pesa transaction fees were initially more expensive for users who transferred money to non-registered users, which put pressure on regular money recipients to register for the service. Furthermore, subsequent years saw increased customer engagement through ever-expanding sets of functionalities. This included an expanding portfolio of organizations that adopted M-Pasa for bill payments, the ability to withdraw money from ATMs, interest-bearing deposits, micro-loans, and so on.

Proposition 5: Lock-in mechanisms that promote the retention of customers and value chain partners strengthen the competitive position of the dominant service, and its potential to create social value.

Value Appropriation

The five propositions in the previous subsection identified various features of the M-Pesa business model that enhanced overall social value creation. Some of these drivers, however, have uneven distributional effect that tended to increase value captured by certain stakeholders relative to others. For example, lock-in mechanisms increase producer value by cementing the market position of M-Pesa, thus benefiting the focal company and its partners. These beneficiaries include Safaricom, Vodafone, partnering banks, and its chain of agents and super-agents. However, the long-term effect of lock-in strategies on consumer value could be negative if they end up restricting competition and innovation.

Likewise, while the centrality of the focal firm is crucial for total value creation, it increases the lead firm’s power relative to other stakeholders. The focal firm could use its dominance and bargaining power to capture economic rent through beneficial pricing mechanisms, as Safaricom did with its M-Pesa agents through exclusion clauses that prohibited working for competitors. In 2014, for example, the telecom regulator passed a ruling that barred Safaricom from using agent exclusion clauses, effectively forcing it to share M-Pesa agents with other competing services. This shows that market forces (such as network externalities) and value chain governance systems in multi-stakeholder social value creation initiatives can lead to uneven appropriation of value among stakeholders. At the same time, transaction costs could increase, and network effects decrease if agents were allowed to opportunistically switch across operators.

The M-Pesa case indicates that social value creation that increases the level of income of various societal stakeholders could at the same time increase inequalities. This is especially the case when the governance of the activity system is designed exclusively or predominantly by a dominant focal firm, and when market forces such as network externalities create first-mover advantages. In these conditions, the terms of contracts designed by a powerful focal firm are likely to end up cementing its dominant position, as illustrated in the case of M-Pesa. Even when a business model increases consumer, producer, and stakeholder value simultaneously, inherent power asymmetries could thus end up increasing overall inequality. This insight is consistent with the current evidence in the macroeconomic literature, which shows that the same entrepreneurial drivers of economic growth skew the distribution of wealth toward capital owners, because the return to capital tends to be greater than the growth rate of the economy (Piketty, 2014). Our micro-level result suggests that the tension between advancing total value creation and containing inequalities remains salient even when social value creation becomes a dominant focus of entrepreneurial initiatives. Our final conclusion can thus be formulated as follows:

Proposition 6: Business models that increase total social value could nonetheless lead to greater income inequality between societal stakeholders.

Discussion and Conclusion

Recent research into social value creation at the “Base of the Pyramid” underscores the importance of multi-stakeholder strategies that involve intensive collaborative effort (Kolk et al., 2014; Simanis & Hart, 2009). Other related research streams such as sustainable business models and social entrepreneurship also place great emphasis on collaborative social value creation strategies that integrate the capabilities of various societal stakeholders (Freudenreich et al., 2019; Yang et al., 2017). At the same time, there is limited research effort on the mechanisms of coordinating collaborative ventures in emerging economies that are punctuated by institutional voids that inhibit effective coordination of complex value creation networks.

This study has used a business model framework to conceptualize social value creation, and empirically examine the coordination of social value creating activities in a case of multi-stakeholder initiative. Building on the activity perspective of business models (Amit & Zott, 2012; Zott & Amit, 2010), we have introduced an integrative framework that enabled us to identify the loci of value creation and the primary and secondary stakeholders that create and capture this value. We have spelt out three constituent components of social value, namely: (a) consumer value, (b) producer value, and (c) stakeholder value, which includes value for shareholders, the government, and local communities.

Our empirical analysis was based on an in-depth case study of M-Pesa, a boundary-spanning service that helped extend mobile-based financial services to tens of millions of users in Kenya. The results revealed how ICT could support an efficient coordination of complex activity systems that helped advance social value creation. Effective use of technology in M-Pesa enabled an efficient and innovative configuration of activities that drew on the capabilities of diverse stakeholders to create offerings that met the unique needs of the BoP market segment. The use of technology thus helped implement a hybrid business model that sidestepped the need for a market-based approaches, which would have required robust institutional arrangement to facilitate coordination.

At the same time, the analysis has revealed how potentially adverse distributional outcomes could arise in multi-stakeholder social value creation initiatives. This result highlights an intriguing aspect of social value creation: Even when total value is increased and most stakeholders are better off, the question of what constitutes a fair distributional outcome is much less obvious. Exclusive focus on achieving the most efficient coordination mechanism could lead to a highly centralized governance structure that disproportionately benefits the focal firm. Creating social value could thus involve a tender act of managing inevitable trade-offs between enhancing total value and avoiding an unfair process of value appropriation. For researchers, this underscores the importance of paying close attention to potential tensions between economic efficiency or total welfare on the one hand, and distributional fairness on the other. Given institutional arrangements that promote and legitimize the measurement and communication of total value creation outcomes, distributional issues can be very easy overlook. Future research can particularly take on the challenging question of what constitutes a fair or inclusive process of value appropriation, and what kinds of governance mechanisms can help achieve it.

In terms of managerial implications, our analysis revealed the profound potential of ICT to fuel organizational innovations that can overcome institutional inefficiencies in emerging economies. However, the results also suggest that leveraging ICT for creating novel business models requires significant financial investment, and coordination effort by the lead firm. This includes eliciting support from collaborators and competitors alike to alter institutional arrangements, which necessitates solid managerial commitment and strong social networks from the lead firm. The results hence suggest the kinds of capabilities businesses need to effectively play this lead role. As our case study showed, Safaricom used its dominant and extensive telecom network to directly reach millions of potential M-Pesa users, and leveraged its reputation to convince customers to entrust their money with M-Pesa and convince regulators to approve its yet-unknown service. Researchers can further explicate the various contingencies that influence the ability of organizations to successfully deploy new technologies that overcome institutional voids and/or advance social value creation. It would be particularly useful to spell out any ethical or pragmatic responsibilities that should correspond with the exploitation of specific network externalities by focal firms—an issue that is also highly relevant to the debate on the regulation of social network platforms, which likewise have a mixed legacy in terms of advancing social value.

This study has certain limitations that also open avenues for future research. While our business model framework offers building blocks for characterizing the processes and outcomes of social value creation, it may require further refinement to better understand the dynamics of value appropriation. The results on the drivers of social value creation that emerged from our case study can also benefit from further empirical testing to verify their generalizability. Moreover, our research has heavily focused on economic value as it investigated the processes of value creation and appropriation among societal stockholders. Considering that social exclusion, poverty, and inequality are major drivers of environmental degradation, and are in turn reinforced by it, future research should look into the complex relationship between socio-economic challenges and environmental sustainability. Overall, we hope that our conceptual and empirical contributions will inspire new research into the processes through which business organizations can advance social value creation.

Footnotes

Appendix

Illustrative Quotes and Evidence for Key Results.

“We realized very quickly that the “The lady who cleans my house would probably not be able to get a facility at the bank at all, if she needed to. Kenyans and Africans at large have been primarily informal borrowers. If I needed money, I would go to my neighbor or call on someone to help me.” A middle-level manager of Safaricom “The amounts that are borrowed are also on average about fifty dollars. And people tend to pay back over three days. Particularly women who are doing small and micro businesses. They turn it around very quickly so that they can borrow again.” The interviews showed that the focus on customer utility goes back to the early years of Safaricom, for example when billing per second was introduced in 2000. Similar early initiatives included a free “call me back” SMS services for people who run out of airtime credit (2005) and an airtime credit for people who were unable to buy airtime for different reasons (Okoa Jakazi service since 2009). A senior manager of a partner organization characterizes Safaricom’s approach toward customer needs as follows: “If you go to Kibira [a slum in Nairobi], people . . . buy sugar for the day, for five or ten shillings or twenty shillings. Because people are payed either on a weekly or daily basis . . . So Safaricom saw this and they launched the 20 shillings air time, and 50 shillings.” |