Abstract

This article engages with the critical study of contemporary publicity by examining transparency as a strategic project to platformize financial services. The article contributes to understandings of transparency as value cocreation in business-to-business markets. Through field-level discourse analysis, the article shows that transparency is contingent primarily on the nature of the market, in this case, a platformized industry, which valorizes transparency as part of a regime of data sharing and open access. Transparency is further contingent on the market actor: actors with lesser status and market legitimacy are more likely to seek to cocreate transparency with market actors of greater or similar status and legitimacy. The article concludes that in commercial spaces, publicity’s relationship to transparency is not only determined by market logic, but that all market logics are being drawn further toward a technological definition of transparency as “shareveillance,” as more segments of economic life become platformized.

Introduction

For marketers, promoting customer engagement with financial services is a constant challenge. Digital content marketing eases some of this burden through compelling visual storytelling and quick, cost–effective ways of tracking which storytelling techniques work best. Content marketing’s function is to market a product or service by creating and distributing free informational or entertainment content, especially online. It is “storytelling for sales” across multiple genres, through hyperlinked texts (Wall & Spinuzzi, 2018).

Fintech magazine (fintechmagazine.com) is one example of modern content marketing in financial services. Fintech focuses exclusively on the fast-growing segment of financial services known as financial technology or fintech. The monthly magazine is noted for its hyperstylized, image-led design with saturated color filters, back-lit portraits of industry leaders, and stock photography portraying professionals at work. Company stories are typed in extra-large font, with key messages highlighted through lift-out pull quotes. The intangible nature of fintech work is visualized as numerical data streams or glowing nodes and connectors, superimposed over equally glowing backgrounds. Unlike subscription-based finance magazines, Fintech is open-access, enabling prospective customers to click on the magazine’s hyperlinked images to view industry videos, presentations, and sales material hosted on social media platforms.

In this article, I examine business-to-business (B2B) marketing techniques used by fintech players. As Europe’s fintech market matures, the industry has become increasingly platformized, insofar as cloud-based digital platforms have become fintech’s dominant infrastructural and economic model (Helmond, 2015). Platformization is marked by data-sharing regimes or “shareveillance,” a term coined by Birchall in her 2017 book of the same name to define the state in which “any relationship with data is only made possible through a conditional idea of sharing” (p. 1). Birchall (2017, 2011) focuses extensively on transparency as citizen data sharing via Open Government platforms. Elsewhere, Bodle (2011) has examined regimes of consumer data sharing on social media platforms. Here, I explore transparency discourses of industry data sharing inside financial markets, where traditional financial providers have been likewise pressed into “shareveillance” by the European Union’s Payment Services Directive 2 (European Commission, 2020), more commonly known as Open Banking (more on this next). This 2018 legislation requires incumbent financial providers to share customers’ data with third-party companies by opening up their proprietary financial systems to cloud-based platforms, thus enabling other companies to innovate and distribute financial products and services via those platforms (Hendrikse et al., 2018).

I argue that for marketers, digital content marketing presents an ideal transparency–publicity nexus through which to position the fintech industry favorably against the opacity associated with traditional financial services. In the fintech marketplace, transparency has crucial societal context, bound up in a series of events encapsulated by the 2008 global financial crisis, which shook public trust in financial services. Opacity and murky practices were deemed the primary cause, and the financial industry’s enduring weakness, notably in respect of the design, trading, and processing of complex financial instruments, and the offshore vehicles in which these instruments were often held (Gibson & Simpson, 2015). The crisis provided the right conditions in the ensuing decade for fintech companies to accelerate the next wave of digital transformation in financial services, with backing from venture capital investors. Market reorganization was further authorized by regulators, persuaded that new financial technologies could remove the dodgy human element in financial transactions and reduce the need for trust by delivering openness and transparency to an industry known for opaque practices.

Backed by skilled marketing, the burgeoning fintech industry wove a convincing postcrisis narrative framing the solution to lost trust in financial services as “more tech.” The fintech industry grew exponentially (one 2017 study traced 22% growth in U.K. fintech between 2014 and 2016 alone), digitizing money creation, payments, lending, money management, and risk management. Fintech promised more than the appeal of quick and easy financial transactions via app-only banks and pay-as-you-go insurers; it also promised more authentic customer engagement and greater transparency. Fintech brands such as Klarna, Transferwise, N26, Monzo, and Revolut experienced several years of high-speed growth, ranking amongst Europe’s Top 20 fintech brands by value before 2020’s global pandemic and economic downturn (Invyo, 2019). Today, many United Kingdom and European customers aggregate and “see” their different financial products and accounts in one place (e.g., on a single mobile phone app) for greater convenience when moving and managing money.

A decade on from the global financial crisis, new European Union legislation, commonly known as “Open Banking,” is shifting normative understandings of transparency in financial services. Open Banking legislation allows European financial services to become truly platformized by permitting third parties (usually tech firms) to access mountains of customer data sequestered inside banks, insurers, and other financial services providers. Simply put, the 2018 transparency regulation permits technology companies to access banks’ customer data with customers’ permission. The digital key to unlocking transparency in platformized markets is the open API (application programming interface), a software tool which allows data sharing between websites and online services, making it possible for tech companies to have a transparent view of financial providers’ customers (Bodle, 2011; van Dijck et al., 2018). APIs help platform ecosystems grow through economies of scale by attracting more companies offering innovative services, thus attracting more end-users.

Open Banking’s vision of transparency co-opts the technology sector’s definition of transparency, and parallels Birchall’s (2017, 2011) examination of Open Government as a transparency movement, which positions citizen data sharing as a welcome, democratizing process. However, in financial markets, the “Silicon Valley” definition overrides ethical understandings of transparency as openness and honesty in business relationships and practices. Many fintech competitors are raising market visibility and seeking credibility with regulators by promoting transparent data sharing and promising fairer service to consumers. However, many incumbent financial providers have yet to platformize, while many tech companies have yet to innovate financial products. Where the different sides form a strategic alliance, they can engage in relationship transparency—that is, transparency in relevant business processes between vendors and buyers—to demonstrate that a financial incumbent is working toward data sharing with the help of a trustworthy tech partner. These strategic alliances effectively create transparency as value, where transparency becomes, momentarily, a distinctive commercial capability, and competitive advantage (Walters et al., 2002) in Europe’s fintech markets.

Fintech’s transparency narrative requires deeper investigation in the wake of Open Banking. Vast assortments of data—not just financial data—are now visible to fintech companies. However, recent academic research on data sharing in the fintech industry typically focuses on consumer markets (e.g., Bernards, 2019; Westermeier, 2020). Less attention has been paid to a related fintech transparency project taking place behind the scenes as fintech companies and incumbents raise visibility with prospective investors and commercial partners. As one fintech industry pundit puts it: “Transparency is important for comparative shopping between fintech players and for business legitimacy. It shows we are stepping up and maturing as an industry” (Sheedy, 2019). “It’s in our interest to be transparent,” says another fintech professional, “because it is a unique selling point” (Daniel, 2016).

The questions driving this study are as follows: How has the notion of transparency been incorporated into B2B fintech marketing? What strategic purposes does transparency serve in B2B markets, and whose interests does it best serve? I answer these questions through field-level discourse analysis of Fintech, a B2B content marketing magazine published monthly, from the United Kingdom. Across 18 issues of Fintech magazine—February 2019 to May 2020—I examine transparency as a form of value cocreated by Fintech’s diverse contributors—insurers, banks, credit unions, fintech companies, and technology infrastructure companies providing cloud-computing and data governance. I explore the resulting transparency discourses as a form of field-level boundary-work by incumbent financial providers and smaller, or lesser-known fintech companies and suppliers. These aspirants may operate on the outskirts of fintech’s most profitable areas or may be seeking greater brand recognition to attract investors and other stakeholders.

Contributors to Fintech magazine engage in discursive boundary-work through protectionist, hybridized, and expansionary discourses. Protectionist discourses emphasize exclusiveness of one’s knowledge area; hybridizing discourses fragment knowledge into new specialisms; and expansionary discourses expand into knowledge areas claimed by others. These discourses can overlap, and run concurrently (Bourne, 2019). Fintech magazine’s monthly format provides a discursive mechanism for fintech’s players to cocreate transparency by promoting regimes of industry data sharing, and normalizing financial services’ reorganization around platformization as a route to consumer openness, fairness, and transparency (Gillespie, 2010). As professional genre, content marketing supports strategic discourses by a heterogeneous group of market players, collaboratively working to improve their legitimacy and status as bona fide actors in the global fintech market.

By examining transparency as a strategic project to further platformize financial services, the article contributes understandings of transparency as value cocreation in B2B markets. I show that transparency is contingent primarily on the nature of the market: here I examine a platformized industry, which valorizes transparency as regimes of data sharing and open access. Transparency is further contingent on the market actor: actors with lesser status and market legitimacy are more likely to seek to cocreate transparency with market actors of greater or similar status and legitimacy. I conclude that in commercial spaces, publicity’s relationship to transparency is not only determined by market logic, but that all market logics are being drawn further toward a technological definition of transparency as “shareveillance” (Birchall, 2017), and “a single view” of customer data, as more segments of economic life become platformized.

Fintech’s Shifting Boundaries

As a field of expert knowledge, fintech’s boundaries have changed constantly since fintech companies first emerged decades ago. One of the oldest fintech brands is Swift, a cooperative financial messaging system founded in 1973 to send electronic money instructions securely around the world, from one bank to another. The first wave of fintech brands was similar to Swift, supplying back-office services that were largely invisible to the public. Platformization of financial services began in the 1990s when fund supermarkets and stock market trading platforms evolved (Chishti & Barberis, 2016). As with contemporary platforms, 1990s financial platforms had layers of infrastructure, data, and users. They could also scale up rapidly with limited investment in fixed capital or other assets, while finding new ways to extract value from monetizing data (Langley & Leyshon, 2020).

As the term “fintech” has evolved, so too has the relationship between legacy fintech companies, fintech start-ups, and incumbent financial institutions. Fintech is now used “interchangeably to describe both technology-driven innovation across financial services and to pick out a specific group of firms that combine innovative business models with technology to enable, enhance and disrupt the financial sectors” (HM Treasury, 2018, p. 3). This official U.K. government definition of fintech appropriately captures the shifting boundaries between incumbent financial services and newer tech companies, including fintech specialists. Fintech can now refer both to an array of actors and services; older financial technology companies as well as newer startups; a business model, division, or internal company created within an incumbent financial institution; products and platforms-as-a-service offered by tech companies; or the platform ecosystem encapsulating these different kinds of companies.

The reason fintech’s definition remains fluid is that experts from both the tech sector and from financial services are deliberately reshaping the discursive boundaries of what fintech means, enabling new market opportunities, innovation, and expansion. Currently within fintech’s professional boundaries are all those tech firms, fintech specialists, and incumbents which have successfully been platformized, that is to say, their infrastructures have been successfully opened up, by accumulating former data silos on cloud-based platforms and making previously sequestered data readable through APIs. Outside fintech’s discursive boundary are those companies which have yet to embark on this transformation toward platformization.

What matters most for this discussion of transparency and publicity is that the increasing ubiquity, speed, and connectivity of digital platforms all promise to make transparency in financial services—vis-à-vis pricing, fairness, and comparability with other products—at least technically possible for consumers (Gillespie, 2010). Here, successful fintech actors, investors, and regulators have positioned transparency of industry data sharing in a way that supposedly favors the consumer; yet such shareveillance, as indicated by Birchall (2017), simultaneously poses privacy concerns. This is just one barrier that marketers must overcome, thus revealing the tensions and limits of Open Banking and transparency. However, fintech companies’ real interest in transparency is entirely driven by the need to “see” customers as a whole—their financial data plus all their other data—in order to sell customers new financial products and services.

The next section of this article explores literature on transparency in B2B markets and in platform ecosystems. This is followed by a discussion of content marketing as a professional genre (Wall & Spinuzzi, 2018), and the chosen method of field-level discourse analysis (Bourne, 2019). Thereafter, I discuss findings, connecting transparency as a form of value cocreation achieved through texts strategically deployed to respond to protectionist discourses, and to establish discourses of hybridizing knowledge, or expansionary encroachment on other experts’ knowledge areas.

Transparency as Cocreated Value in Fintech Markets

Transparency is generally treated as a good thing in financial marketing literature, a reliable means of making visible the complex, intangible features of financial products, and allowing customers to assess and compare price and fairness (see, e.g., Farquhar & Meidan, 2010; Rankin, 2004). For markets to gain adequate regulatory and public support for activity amidst successive scandals and crises, as well as market innovation and change, transparency has become a cherished, unquestioned business principle. In the case of fintech’s transparency project, transparency is increasingly instrumental in response to Open Banking. I position fintech actors as desiring transparency to build trust with regulators and to attract investors, partners, and suppliers. In the long wake of the 2008 financial crisis, transparency becomes a sign of cultural and moral authority for fintech actors (Birchall, 2011).

So, what is marketing’s role in promoting transparency in fintech markets? Edwards (2020) argues that where transparency is called on to counter criticisms of publicity—particularly in commercial environments—it can only be enacted as visibility management, allowing organizations to ensure their transparency efforts align with operational imperatives and legitimacy claims. Marketing plays an important role in visibility management; in a digital age, this increasingly means search visibility, that is making products, services, and ideas visible via website navigation, search engine optimization, social media promotion, and hyperlinked content (Kingsnorth, 2019). Additionally, marketing’s dominant logic in the 21st century is value cocreation between a company and its stakeholders (Farquhar & Meidan, 2010; Singaraju et al., 2016; Vargo & Lusch, 2004). This view of marketing reflects the increasing service orientation of the global economy, with financial services and fintech part of this trend. A value cocreation approach suggests that it is marketing’s job to find routes through which organizations and sectors can cocreate transparency with customers and key stakeholders.

Cocreating Relationship Transparency in B2B Markets

So how does marketing create transparency as value in B2B markets? In industrial markets, the relational dimension is sensitive and crucial across both customer and supplier networks (Eggert & Helm, 2003; Singaraju et al., 2016). This is especially true of B2B financial services; the market is dynamic, the products complex, and years may be required to convert a prospective customer into a client. Once established, B2B financial relationships can be close and long-term, involving a complex pattern of interaction between and within each company (Athanassopoulou, 2006; Eggert & Helm, 2003). B2B clients often form an integral part of the service offering, providing key information needed to determine the nature of the service, and frequently coproducing the product with the supplier (Athanassopoulou, 2006). For instance, Monzo, the app-only bank, launched Monzo “Nearby Friends” in 2018 so customers could make direct payments to friends via mobile phones. The service works via Google Nearby, Google’s peer-to-peer networking API, and requires Bluetooth to transmit signals to other phones (O’Hear, 2018). As Monzo formed B2B alliances with Google and Bluetooth, the terms “customer” and “supplier” could fall away to become “partnerships,” representing the cocreative process of platformized B2B relationships.

Relationship transparency is therefore the most valued form of transparency in B2B markets, and the guiding principle of B2B financial marketing. Relationship transparency is based on B2B partners’ important characteristics, as well as their quality of information exchange (Eggert & Helm, 2003). For instance, B2B partners might seek transparency about each other’s financial balance sheets, organizational strength, or technical expertise, or they may want information on how stable and reliable a partner is at gauging market prospects, overall decision making, and bill paying. A B2B partner may also seek transparency on whether the relationship is exclusive, or whether the other partner is testing the market for better alternatives (Eggert & Helm, 2003).

The Monzo example outlined earlier illustrates why digitally collaborative markets such as fintech require higher coordination, knowledge sharing, trust, and transparency than traditional B2B market relationships (Ronchi, 2011). Every customer interaction with Monzo’s Nearby Friends is also an interaction with Google Nearby and Bluetooth via other mobile phones. As with traditional market relationships, digital collaboratives seek transparency through visibility of information sharing, planning, and new product development. However, in financial services markets, the increased need to assert fintech credentials has taken on a more purposeful air, to the extent that transparency has become a collective project of value cocreation for certain groups of B2B fintech marketers. Specifically, as financial services become more platformized, a range of heterogeneous tech companies must collaborate with financial incumbents and convince them to advance new technologies for mutual profit. In Europe’s fintech markets therefore, B2B relationship transparency is the catalyst for cocreating a broader financial services’ view of transparency as regimes of industry data sharing on platforms.

Fintech: Field and Hierarchies

In the fast-moving fintech market, the very largest actors—incumbents such as large global and national banks and insurers, other financial brands with household names, as well as fintech “unicorns” (start-up tech firms valued at more than US$1 billion)—all occupy the top of the fintech hierarchy. They are joined by large and powerful venture capital investors, which collectively own stakes in hundreds of fintech firms. The more elite fintech actors may be less likely to seek transparency (at least temporarily) because of their scale, unregulated status, or influence with brand communities and investors. Some of these companies, such as Revolut, claim to do no marketing at all (Braileanu, 2017). As a fintech unicorn, Revolut’s assertion effectively relegates marketing as a necessity for those fintech companies lacking legitimacy and status. B2B marketing efforts to cocreate transparency in the fintech market are therefore more likely to be conducted by companies outside fintech’s elite.

Social Media Platforms and Transparency Discourses

Media technologies are central to collective transparency projects, enabling connected marketers and organizations to see each other and unify messages (Flyverbom, 2015). Social media platforms are therefore a logical site for contemporary marketers to cocreate transparency, since B2B customers and partners can easily integrate resources via social media. Singaraju et al. (2016) identify a specific value cocreation role for social media platforms in B2B marketing: they position social media as multilayered digital technologies delivering specific functions such as identity, conversations, sharing, presence, relationship, reputation, and groups. Using precise digital marketing techniques to share effective transparency storytelling on these platforms can cocreate value for allied fintech partners.

Transparency as Strategic Project: Fintech Magazine

B2B fintech marketing is one of the processes enabling platformization in financial services by determining how value is initially defined, cocreated, and eventually redefined as players enter the fintech field, change field position, or drop out altogether. The regulated nature of financial services, the distributed nature of fintech platforms, and the secrecy of Big Tech platform owners present challenges for both scholarly access to and understanding of fintech (de Reuver et al., 2018). Marketing techniques are not themselves known for transparency, particularly in B2B marketing, which typically takes place away from the public eye. Moreover, many specialist financial publications have high subscription fees, limiting public knowledge of B2B fintech discussions within these pages. For these reasons, de Reuver et al. recommend broader data-driven approaches, including secondary analysis of diverse data sets on platform activities, to be found in publicly available expert blogs, press releases, developer forums, and so on. These sources of opinion and publicity can enable viable methodological approaches since they provide “important additional insights into the process dynamics and evolution of digital platforms” (de Reuver et al., 2018, p. 132).

Content marketing has evolved as an effective B2B lead-generating strategy, and an ideal tool for building relationships in markets where products and services have long sales cycles (Spiller, 2020). Digital content marketing includes communicative text, images, video, audio, slideshows, infographics, and other media. Here “communicative” indicates the structural elements intended to operate with search engine crawlers to keep readers’ attention on the sponsored content. These structural elements include links that connect the article to other sites, and language and design elements intended to steer the audience to click on links (Wall & Spinuzzi, 2018).

As a case study of content marketing, this article’s discursive data set is a glossy, full color, monthly digital magazine called Fintech, produced by BizClik, a specialist B2B content marketer based in the United Kingdom (see https://www.fintechmagazine.com/backIssues). In addition to stories hyperlinked to corporate videos and other content across the web, Fintech magazine issues also contain display advertising, industry rankings, and classified advertising for industry events. According to BizClik’s 2020 Media Kit, the magazine’s readership by sector is as follows: financial services, 30%; technology, 18%; banking, 18%; insurance, 12%; capital markets, 10%; consultancies, 7%, with the final 5% identified as “other.” Readership is international, but concentrated in the United States, Europe, the United Kingdom, and Asia. Fintech magazine’s audience is identified primarily as C-level suite decision makers. BizClik reports 41,800+ monthly online visits, 107,100+ monthly social media views, and an executive level email distribution of 67,400+ 1 (BizClik, 2019). I analyzed 18 issues of Fintech magazine from February 2019 to May 2020. Each issue produced between 100 and 200 pages of content with hyperlinks. My focus was on the fintech actors and their discourses within Fintech’s digital content, as they engaged in cocreating transparency as value with their chosen B2B partners.

As discursive data set, Fintech magazine is valuable for several reasons. First, the magazine provides the opportunity to understand what is happening in the field of fintech by studying one set of relationship networks (Ford et al., 2011). Fintech was designed for the purpose of B2B value cocreation, bringing companies together to support fintech’s progress. The companies featured in the magazine are there because professional marketers strategically incorporated Fintech magazine into companies’ critical business assets (Wall & Spinuzzi, 2018). While a sponsored section of a specialist trade magazine might achieve the same end, across the 18 months of content marketing analyzed, what became apparent is that several Fintech contributors chose to be repeat customers on this content marketing site, either as display advertisers, sponsors of extended feature stories, or cosponsors of another company’s main feature. Fintech magazine, with its international reach, can therefore be seen as a professional genre designed to concentrate and thicken transparency discourses and other forms of value cocreation within the global fintech ecosystem.

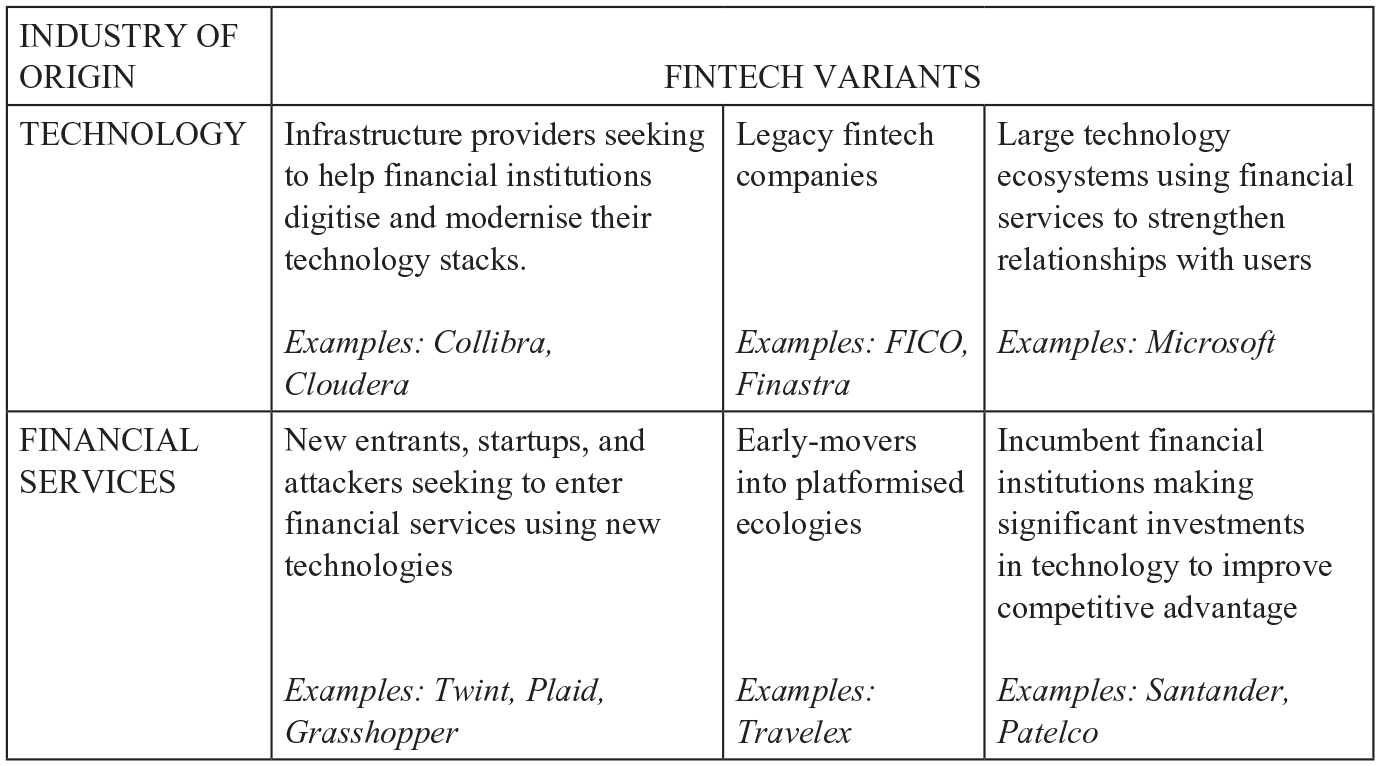

Fintech magazine contributors segmented into six variants.

A second reason for Fintech’s importance as a data set is that the monthly magazine highlights relational interactions between a diverse range of incumbent financial institutions, fintech specialists, tech infrastructure firms, data governance specialists, software developers, and BigTech platforms. Third, the content marketing magazine serves as a useful data set because of the companies not featured within its pages and hyperlinked content. Whereas a financial newspaper or subscription magazine would regularly headline the biggest, trendiest fintech names, Fintech magazine does not. The 18-month data set did not feature any of the fintech companies in Europe’s Top 50, such as Klarna, N26 or Funding Circle. Equally, the U.K.’s largest retail banks—HSBC, RBS, Lloyds, and Barclays—do not feature in Fintech magazine, although Santander, the U.K.’s seventh largest bank, does. Asset managers and mutual funds such as Vanguard, Acorns, and FidelityGo are some of the biggest fintech players, yet this sector is not generally represented in Fintech magazine. Finally, the data set does not include any of the Big Tech GAFA companies—Google, Apple, Facebook, or Amazon—although it does include Microsoft, which remained a secondary player in fintech platformization during the period under review.

Instead, the Fintech data set features companies such as Finastra, a merger of two much older fintech brands, Misys and D&H. Finastra is owned by Vista Equity Partners, a private equity firm, which has a direct interest in Finastra’s sales and marketing strategy, namely to sell financial software to incumbents. The data set also features several credit unions, including California-based Patelco and New York-based Visions FCU. Credit unions’ mutual structure limits their geographical area of operation and prohibits them from taking on debt as other financial incumbents do, so credit unions are generally smaller than banks, and find it tougher to invest in platformization.

The absence of many large, well-known names, and the presence of many aspiring fintech players helps define the field boundaries of the discursive data set. The boundaries, as drawn, suggest that Fintech magazine acts as a strategic transparency project for those companies that need the magazine’s international publicity to cocreate transparency in order to gain legitimacy in global fintech. The companies featured in the magazine are heterogeneous, aiming to join fintech’s “premier league” in different ways. Santander, for example, is a well-known international bank, but platformization could improve Santander’s competitive stance against other global banks. Microsoft is an even bigger global brand than Santander, but the tech company was late to contemporary platformization compared with Google and Facebook. Other Fintech contributors are tech firms hoping to compete with specialist fintech players, and can achieve this through third party endorsement from well-known financial brands, such as insurance company AXA. The strategic partnerships promoted within the magazine’s pages suggest that Fintech is positioned as a professional genre for cocreating transparency through collaborative B2B relationships.

Field-Level Discourse Analysis

B2B content marketing as value creation has received recent attention in scholarship (see, e.g., Hollebeek, 2019; Wang et al., 2019). Yet, as Wall and Spinuzzi (2018) indicate, few studies reveal the complex interdiscursivity of inventing, recording, photographing, writing, and distributing content; or how networks of content connect in a variety of genres, media, and platforms. This B2B research study is unusual in focusing on content marketing produced by a value cocreation network (Fu et al., 2017), rather than by a single organization’s sponsored content. Furthermore, the cocreation network assembled by Fintech magazine is heterogeneous in that contributing companies are based in different countries and sectors. The very heterogeneity in the range of companies contributing to the 18 magazine issues in the data set suggests not only that Fintech contributors may be engaged in a number of marketing tactics beyond the cocreation of transparency, but that contributors may be building transparency in different ways and with different intentions. I aim to capture varied approaches to transparency cocreation drawing on a method of field-level discourse analysis designed to locate and examine field positions and resulting tensions within or between particular sectors of the global fintech industry.

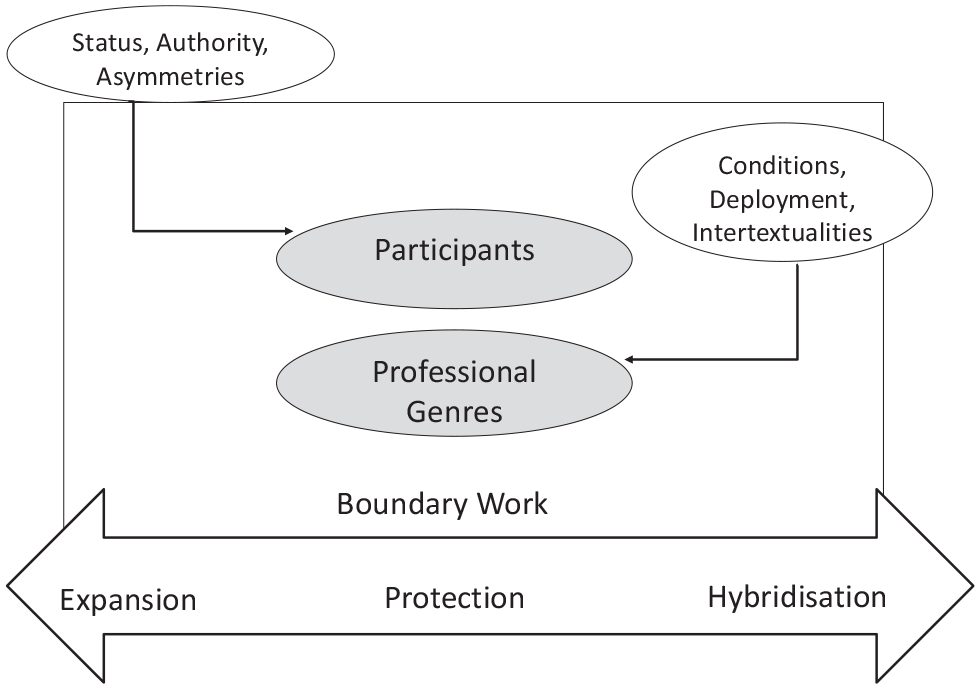

The methodological approach draws on Bourne’s (2019) field-level discourse analytical framework (see Figure 2). This method is designed to deconstruct discursive boundary-work carried out by professionals within an expert field, or between adjacent fields of expertise, in order to reveal how claims to professional knowledge and expertise are successfully deployed, defended, and maintained. In this approach, “boundary-work” refers to discursive efforts to demarcate professional activity and expert knowledge so as to assert distinctive status and centrality within that field. Since boundaries are not fixed, this discursive work is always in motion, revealing tensions between actors claiming or maintaining status (Bourne, 2019). Boundaries define an expert group’s access to material and nonmaterial resources such as power, status, and remuneration (Abbott, 1988). Boundary-work consists of discursive strategies used to establish, obscure, or dissolve distinctions between groups of experts. Professions continually negotiate boundaries in their desire to expand or protect their autonomy (Bucher et al., 2016; Gieryn, 1983). The role and status of Fintech contributors must therefore be understood in relation to other contributors to the magazine, as well as organizations and occupational groups which do not appear, but may play a dominant role in the fintech industry. My main contribution, however, is a clearer understanding of changing hierarchies and associated shifts in power between various expert groups within B2B fintech markets, as certain actors within the field engage in cocreating transparency as value.

Field-level professional discourse analysis.

In the 21st century, “locating how, where and why jurisdictional claims are made” is essential for capturing how marketing and publicity develop in new digital environments (Lewis, 2012). In this study, discursive work is shaped by social media platforms encompassing nonhuman software and systems, linked also to platforms in fintech ecosystems (Flyverbom, 2015; Singaraju et al., 2016). Hence, the article’s further contribution is an understanding of how transparency is cocreated as value via digital environments. Bourne’s (2019) field-level discourse method identifies three primary forms of discursive work designed to produce status in an expert field—discursive work often carried out by fintech market professionals, but also by other actors including regulators, customers, and the media, underscoring the cocreative nature of fintech knowledge claims. The three forms of field-level discursive boundary work are identified as protectionist, hybridized, and expansionary discourses (Bourne, 2019). All three types of field-level boundary work are defined by their strategic intent.

Protectionist discourses encompass efforts, usually by traditional occupants of a field, to defend against encroachment on their knowledge areas. Higher status expert groups may be forced to defend boundaries against incursion by emphasizing the exclusiveness of their abstract knowledge, for example, by constructing newcomers as interlopers—as “mere” digital experts rather than financial specialists. While one might expect marketing and publicity discourse to aim for highly visible images, talk, and text, protectionist discourses may also feature silences. This can happen where higher status experts adopt silence to express “a taken-for-granted assumption of their own technical superiority” (Sanders & Harrison, 2008, p. 297). Silences also occur in mediated discourses, when publicity takes a backseat, allowing market actors to lobby quietly behind the scenes.

Hybridizing discourses are a form of professional boundary work closely associated with entrepreneurial behavior—whether by an innovative start-up, within a single department of an organization, or by financial investors keen on seeing fragmentation of knowledge into new specialisms. Companies engaged in hybridizing boundary work regard monopolistic market behavior as neither desirable nor achievable (Bourne, 2019). Instead, hybridizing discourses laud innovation, entrepreneurship, and active market engagement to carve out brand-new niche specialisms and market identities. It is likely that the rapid growth of fintech ecosystems is accompanied by many hybridizing discourses by newer fintech players, even as platformization leads many financial incumbents to assert innovative, entrepreneurial language.

Finally, expansionary discourses expand authority or expertise into domains claimed by other expert groups. Boundary work in expansionary discourses heightens the contrast between rival experts and professions in ways that flatter the aggressor’s side (Gieryn, 1983). Expansionary discourses are therefore evident in talk, text, or images where one expert group opts to go on the offensive. Expansionary discourses in professional fields feature assertive language, and regular pronouncements about moves to occupy or capture new areas of expertise regardless of whether the aggressor actually possesses this expertise (Bourne, 2019).

Macro-level discursive methods reposition fintech’s transparency discourses within field-level contexts. The rise of fintech has, for example, reshaped how expert knowledge is produced in financial services. Open Banking accelerates the urgency for companies to redefine themselves as open and transparent to industry data sharing. Meanwhile, the limited options for investment return in low interest rate jurisdictions drive venture capital investors to pour billions of dollars into backing fintech startups. For this discussion, the most intriguing discursive boundary within the fintech field is the boundary that excludes Fintech’s contributors from the elite group of financial and tech companies which either possess fintech legitimacy or do not need it. This discursive boundary, I argue, is determined by premium value, that is to say, companies possessing the greatest distinctive commercial capabilities (e.g., successful product innovations), brand recognition, and competitive advantage within fintech markets (Walters et al., 2002). Those companies needing to build transparency can do so by publicizing their willingness to undergo digital transformation. This transparency–publicity (see Edwards, 2020) can be achieved through discursive boundary work activated in different ways. In the findings section that follows, I examine how Fintech’s B2B value cocreation network interweaves the three discursive strategies—protection, hybridization, and expansion—to cocreate transparency for various fintech actors.

Findings: Fintech’s Transparency Project

Protectionist Discourse Instigates Fintech’s Transparency Project

One of the strengths of field-level approaches to discourse comes from meaning supplied through a search for discursive context. Understanding why a professional text was deployed at a particular time comes through understanding the text’s external conditions, deployment, and intertextualities (see Figure 2). Fintech’s content marketers may control the magazine’s stylized spaces, but the magazine’s content is shaped by industry realities. Notably, Fintech magazine’s launch in February 2019 followed a year of intense protectionist discourses in mainstream media, engineered by high street banks, leading the Daily Telegraph to ponder “How Britain’s financial giants scuppered the digital banking revolution” (Cook, 2020). This protectionist discourse by large, international incumbents demonstrates how the existing structure of a field can act as a “brake on innovation,” leading some innovators to enlist the support of other companies with which they had no previous relationship (Ford et al., 2011, p. 187).

Fintech contributors repeatedly refer to this protectionist discourse happening outside the magazine’s spaces, citing incumbents’ protectionist narratives as the number one transparency problem hindering the platformization of finance. The material impact of incumbents’ protectionist discourse is captured by two Fintech contributors—Finastra and FICO—both legacy fintech companies (see Figure 2). According to Finastra and FICO, many incumbents had failed to install modern cloud-based platforms and open APIs. According to Finastra, banks were not “very open to sharing this data” (Minnock, 2019b, p. 35). Meanwhile, FICO claimed that siloed practices prevented incumbents from achieving “customer centricity,” that is, the ability to develop a single view of an individual customer (High, 2020, p. 99). Without cloud platforms and open APIs, customers’ financial data remained siloed in banks’ on-premises computer systems, where tech companies could not see it.

Materially speaking, individual fintech companies stand to benefit from open access to data in a number of ways. Some fintech companies want to sell their cloud-based platform-as-a-service to financial incumbents. Other fintechs want to sell ancillary financial products to consumers such as credit cards, mortgages, or investments (High, 2020). Both sets of fintech companies want incumbents to open up their data silos in order to achieve the all-important value of the “network effect,” in which the number of people joining the platform network and the range of new products sold via that platform increases the value that can be extracted through sheer variety and scale. A transparent “whole” view of customers and their product preferences can then lead to more profit. At stake is a delay in expanding Europe’s fintech market and losing out to regions where no such protectionist discourses exist. Fintech contributors therefore cast incumbents’ supposed lack of openness and transparency as a site of struggle which deters other actors from cocreating transparency as value.

Hybridizing Discourse Shapes the “Digital Transformation Journey”

For Fintech contributors, hybridizing discourses are cocreative in generating new market identities, where a tech company generally helps an incumbent financial provider to embark on a “digital transformation journey.” The digital transformation journey is a persistent motif used by Fintech’s content marketers to relate the stories of multiple contributors across consecutive editions of the magazine. In the launch edition, the editor explains that Fintech will “explore the digital transformation journeys of leading global businesses and find out how the experts are navigating this exciting new financial landscape” (Minnock, 2019a, p. 5).

The typical digital transformation journey as told by Fintech’s content marketers begins with having the right corporate mind-set, one that welcomes openness and transparency, and supports the platformizing of financial services. The digital transformation journey takes more than just a mind-set; it requires a company to allow its data silos to be broken down, thus enabling data sharing and collaboration. Italian insurer Generali is one incumbent keen to emphasize its “digitally savvy mind-set.” Since insurance remains one of the more opaque areas of financial services, Generali’s platformization is akin to changing the insurer’s “DNA.” Generali describes the time before its “digital transformation journey,” back when it had enormous amounts of data not leveraged to “its full potential.” Then, Generali devised “a careful digital transformation plan” (Mullan, 2019, pp. 109-110). At the end of its transformation, Generali had rolled out a Corporate Data Warehouse to consolidate existing data and introduced a customer relationship management system from Microsoft Dynamics for collecting new data. The use of the term “journey” suggests that incumbents with the right mind-set are eager to become platformized, eager to transform into a new, hybrid market player.

As Santander puts it: We partner with Cloudera to run our big data platform here in Santander UK. [We were] able to understand through this collaboration that we don’t need to have silos of data going forward . . . if you get rid of silos, you can truly transform the way people across the organization behave. (Minnock, 2019c, pp. 126-127)

To those outside the fintech field, the content marketers’ storytelling of “digital transformation journeys” could seem problematic. After all, the financial services sector first adopted digital platforms back in the 1990s, and many companies have upgraded their digital operations since then. So why do Fintech contributors seek out publicity for these latest digital upgrades? The answer lies in embracing Open Banking’s shareveillance mandate of open APIs. This transformative step of enabling open APIs to unlock financial incumbents’ data silos allows the rest of the fintech market to “see in.” This is fintech transparency, this is fintech’s notion of value cocreated with financial incumbents.

Expansionary Discourse: Data-Hunters Find an “in” Through Partnerships

To free data from silos and make data transparent to tech companies is to complete the digital transformation journey. But this can only be achieved with the “right partner,” which may not necessarily be a specialist fintech firm. Many of the tech companies featured in Fintech magazine are not fintech specialists, but specialists in infrastructure or data governance. These companies moved rapidly on fintech territory with the advent of Open Banking. Tech companies that are not fintech specialists (see Figure 1) are engaged in an expansionary discourse, moving into new territory and asserting fintech expertise in order to profit from the rapid platformization of finance. Travelex, the foreign exchange company, states that partnerships with such tech providers have “brought a tremendous amount of transparency:”

The world we live in now is about integration, the ability to use API to call other services—therefore, it’s fundamental that we have a fresh, open and aligned relationship with our partners. We have a very large distributed network we need to support . . . 9,500 employees dispersed globally across six continents. We rely on partners such as Ultima and CDW for provision of hardware, software and support across a number of systems to enable us to deliver the best services for our customers and employees. (Minnock, 2019d, p. 28)

The transparency cocreated between incumbents and tech firms is ultimately defined by industry data sharing, offering the potential for the single-customer view. For data to be transparent, it must be easily accessed and easy to work with, no matter where the data is located, or what application created the data. Uniting a financial incumbent’s separate databases together on the right cloud-based data platform is fintech’s “holy grail.”

Conclusion: Retaining Ethical Understandings of Transparency

This article has examined links between publicity and transparency as value cocreation in B2B markets. The value cocreation approach suggests that it is marketing’s job to find routes through which organizations and sectors can cocreate transparency with customers and key stakeholders. Social media platforms are a logical site for contemporary marketers to cocreate transparency, since B2B partners can easily integrate resources via social media, enabling connected marketers and organizations to see each other and unify messages. By examining 18 issues of Fintech, a B2B content marketing magazine with cross-border reach, I have shown how content marketing publicity as a professional genre can potentially thicken transparency discourses to support value cocreation in international B2B markets. I have further shown how transparency is intentionally built through discursive boundary work activated in response to or via three discursive strategies—protectionist, hybridizing, and expansionary—to cocreate transparency for diverse fintech actors. The three discursive typologies provide insight into fintech’s transparency–publicity nexus.

In the case of Fintech magazine, transparency was cocreated by heterogeneous fintech actors in response to protectionist discourses deployed by incumbent financial institutions outside of Fintech magazine’s digital spaces. Within Fintech magazine, the value cocreation network of diverse fintech actors constructed transparency in two significant ways. First, financial incumbents emphasized hybridizing discourses to demonstrate their internal transformation into platformized companies and acceptance of new data-sharing regimes. Second, tech companies seeking to capture fintech market share used expansionary discourses to demonstrate services to incumbents constructing platform software or systems to enable a trustworthy shareveillance regime.

A question arising from the data analysis is which actors are empowered by Fintech’s transparency discourses, and what effect such power relations have on field dynamics. The data set may be too limited to answer this comprehensively. However, an enduring problem with financial services is they are easily copied by competitors, making it difficult to gain any lasting competitive advantage (Farquhar & Meidan, 2010). This suggests that transparency is unlikely to remain a competitive advantage in fintech over the long term. Furthermore, studies of value cocreation on platforms indicate that all cocreated value is more beneficial to platform owners than it is to any of the companies accessing platform services (Haile & Altmann, 2016).

Finally, while Fintech magazine does not represent all the fintech industry, the analysis presented suggests that publicity’s relationship to transparency is not only determined by market logic, but that all market logics are being drawn further toward a technological definition of transparency as “a single view” of customer data, as more segments of economic life become platformized. B2B marketing involves influential processes through which companies cocreate value. In platformized markets, such value cocreation typically seeks to normalize technological advances that reap profits. Accelerated by Open Banking, the fintech market’s move toward shareveillance echoes research on Open Government discourses by Birchall (2017, 2011) as well as ongoing scholarship on public data sharing (Bodle, 2011; Gillespie, 2010; van Dijck et al., 2018).

As more fintech market actors embrace technological definitions of transparency, this dilutes ethical understandings of transparency as openness and honesty in business relationships and practices. Yet the fintech industry has not bypassed ethical issues associated with wider financial services. In 2020, Wirecard, a legacy fintech company, collapsed with €1.9 billion (US$4 billion) in losses, representing Europe’s largest accounting fraud of the postwar era. Initial investigations suggest key parts of Wirecard’s digital payment processes were not transparent. Wirecard’s collapse could threaten fintech’s platform ecosystem (Skinner, 2020), and shift fintech’s transparency discourses altogether.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.