Abstract

Events in recent years have put the European economic integration project and the euro under pressure. The main cause of the euro crisis is loss of competitiveness, particularly on the periphery of the Economic and Monetary Union. To reverse this, Union members must promote structural reforms that increase long-term employment, productivity and external competitiveness. The successful implementation of reforms, however, requires sufficient public support, which in turn presupposes measures that support demand during the implementation of reforms. To that end, important steps include taking an expenditure-based approach to fiscal adjustment and the introduction of the European Deposit Insurance Scheme. And for Greece in particular, the set of necessary steps includes taking ownership of reforms, the downward revision of fiscal targets, and medium- and long-term measures of debt relief conditional upon meeting fiscal/reform targets. Finally, the stability of the euro hinges on the moderation of all fiscal and external imbalances across all member states, regardless of whether these imbalances are apparent or not.

Keywords

Introduction

The European economic integration project is a cornerstone of lasting peace for the European continent. This is sufficient reason to advocate strongly for its continuation. Nevertheless, events in recent years have put it under pressure. The most prominent manifestation of this has been the UK's decision to leave the EU. In other countries, populist and/or extremist anti-EU parties have made electoral advances; and even voters for mainstream pro-EU parties report increasing dissatisfaction with the EU (Oliver

While each country has idiosyncratic features contributing to the increasing prevalence of Euroscepticism, there are two common economic factors. The first is the effects of globalisation on world income distribution (see Milanovic

The second factor is the European debt crisis, which has divided the euro area into two groups. The first includes debtor countries that have been cut off from international bond markets and, as a result, have received official financial assistance conditional upon implementing programmes of economic adjustment. Greece is the most prominent example of this group. The second group includes creditor countries, which have underwritten the assistance programmes provided to the first. In countries such as Greece dissatisfaction with the EU is driven by the adverse effects on welfare of adjustment programmes and a sense of reduced national sovereignty due to the direct involvement of the EU and other international bodies (e.g. the International Monetary Fund) in national economic policy. In creditor countries, dissatisfaction is the result of a sense of the involuntary use of national and private savings to rescue Economic and Monetary Union (EMU) partners that are perceived as imprudent. Starting from opposite reference points, public opinion in both groups converges on a common ground: Euroscepticism.

The two factors explained above are not unrelated. They share a common economic source, namely competitiveness losses in many EMU economies, particularly those on the periphery. These losses will not be reversed if the EMU embarks upon a protectionist course and/or some EMU countries leave the euro. Economic theory and historical experience tell us that free trade promotes production efficiency and welfare standards, and living standards in the long run are determined by an economy's production capacity, that is, its supply side, on which monetary policy has no lasting impact. The only credible answer to Europe's economic and political problems is structural reform, and it is on this that the euro's sustainability ultimately depends.

Having said that, international experience also tells us that a successful programme of reforms requires the support of a critical mass of the population. For this to be in place the latter must perceive reforms to be beneficial and realistic, that is, their adjustment welfare cost should not be regarded as socially untenable. This, in turn, presupposes that until reforms yield positive output effects, economic activity is adequately supported by the demand side. With an emphasis on Greece, this article discusses the reforms necessary in the EMU countries and analyses the demand-supporting conditions that would enable their successful conclusion.

Structural reforms

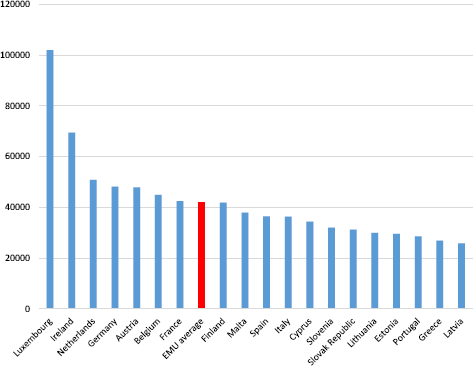

Despite evidence of increased economic convergence among EMU members since 1999, the EMU continues to be divided between a core and a periphery (Campos and Macchiarelli

Gross domestic product based on purchasing-power parity per capita GDP, US dollars in 2015.

Modern macroeconomics (see Corsetti and Pesenti

Ireland's experience is the most relevant for Greece, the country presenting the biggest potential for supply-side improvements in the EMU area, as suggested by its position in numerous international rankings relating to supply-side performance. On this front, Greece made significant progress in the period 2012–14 (see Arghyrou

Supporting reforms through demand

Structural reforms cause immediate welfare losses to be offset by higher benefits in the future. This is why reforms should be pursued during periods of growth, to moderate their short-term welfare impact. Unfortunately, political considerations often get in the way, resulting in reforms being pursued during recessions when accumulated imbalances make their implementation urgent. The experience of the European periphery is a prime example. But bygones are bygones. European economies must now move on with reforms. In this effort, their prospects for success will improve substantially if demand conditions are as supportive as they can be during the implementation of reforms. To that end, the following factors are important.

Optimal prioritisation

To maximise their effectiveness, reforms should be optimally prioritised. Existing literature (see OECD

Favourable expectations

Demand conditions depend on the regime of expectations under which reforms are implemented. High confidence in the successful conclusion of reforms accelerates positive private responses to reform policies (through investment and consumption), triggering a virtuous circle of mutually enforcing expectations, increased demand and endorsement of reforms. Low confidence causes the opposite dynamics.

Improving expectations depends on two factors. The first of these is the national authorities taking ownership of the reforms. A lack of ownership causes implementation risk, restricting investment and consumption spending, which compromises the endorsement of reforms and reinforces implementation risk. EMU countries whose authorities took ownership of reforms (Ireland, Portugal and Cyprus) have concluded their assistance programmes successfully and returned to positive growth. In Greece, when ownership of the reforms has been absent, between 2009 and 2011 and from 2015 to the present, economic developments have been negative. By contrast, in 2012–14, when authorities assumed ownership of the reforms, the economy made significant progress (see Arghyrou

Second, credible crisis-prevention and crisis-management mechanisms are needed at the EMU level. These are necessary to reassure markets that the probability of major national banking and fiscal crises is limited and that, if they happen, they will not spread to the economy's real sector and/or to other countries. To that end, a number of institutional changes have taken place, including the creation of a new macro-prudential framework, risk-sharing fiscal funds (the European Financial Stability Facility and the European Stability Mechanism), the Outright Monetary Transactions programme and the European Banking Union (EBU), which involves centralised bank supervision and resolution. These are steps in the right direction, both in terms of increasing risk-sharing and reducing moral hazard; however, they are not enough to deliver the necessary improvement in expectations (see Arghyrou

Liquidity and EDIS

The importance of liquidity for business-cycle movements has been well established since the 1960s, documented by the writings of Milton Friedman (

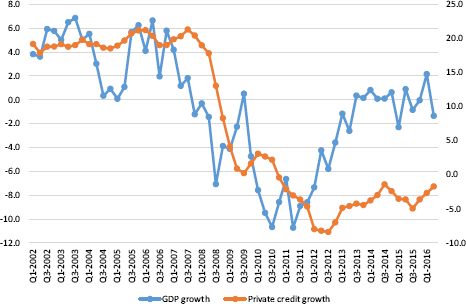

Growth rates for real GDP and bank credit to the private sector in Greece. GDP growth rates are measured on the left vertical axis; bank credit growth rates are measured on the right vertical axis.

The ECB's expansionary monetary policy, however, has three drawbacks. First, it is not uniformly transmitted, as liquidity increases at the core of the EMU have been considerably higher than those at the periphery. This is a reflection of the fact that the ECB has one policy instrument (the Union interest rate or money supply) and numerous policy objectives (national output gaps). As a result, the single monetary policy responds imperfectly to national business cycles, particularly under the financial fragmentation observed during the crisis (ECB

These problems may be ameliorated through the introduction of EDIS. In certain countries EDIS is regarded with legitimate scepticism on moral hazard grounds (see Schuknecht

Fiscal adjustment and debt relief

The EMU crisis has left many countries with excessive public debt levels. This is primarily the result of bank-rescue programmes and, in the case of Greece, fiscal imbalances built up in the run-up to the crisis. Reforms impact on the economy's natural output through the employment and investment responses of the private sector. These responses depend on expectations about future taxation on income and corporate profits. For reforms to be effective, taxation expectations need to be favourable. Therefore, reforms must be accompanied by a credible programme of fiscal adjustment, reducing expected future taxation. This raises two questions. First, how should fiscal adjustment be pursued? Second, how aggressive should it be?

Fiscal adjustment is widely regarded as causing short-term contractionary output effects. However, existing evidence (see Alesina et al.

Clearly, a country such as Greece, where the public debt to GDP ratio is currently in the range of 180%, must target primary fiscal surpluses to improve the dynamics of its government's intertemporal budget constraint. But in addition to the primary surplus, the intertemporal budget constraint depends on the stock of debt and the difference between the rates of growth and real interest on debt. In recent years, Greece has benefited from interest rate reductions and extensions of debt maturity. However, as evidenced by Greek long-term government bond yields, these have not been enough to restore confidence in Greece's public debt sustainability. The implementation of reforms will help do so. However, the latter's output effects will appear gradually over the medium term. In the meantime, servicing the Greek debt involves large payments from 2019 onwards. This underlies the 3.5% primary surplus set for Greece's fiscal policy starting from 2018 for an unspecified period of time. However, there are two risks associated with this target.

First, historical evidence suggests that a 3.5% fiscal surplus was relatively rare during the post-war period of 1950–2011, when in 75% of the cases primary balances had values of less than 2.5 and 1.7% for advanced and non-advanced countries respectively (see Mauro et al.

The second risk comes from the level of debt. According to all available projections, the Greek public debt to GDP ratio will remain very high for the foreseeable future. Even if Greece meets its fiscal and reform targets, Greek public debt sustainability will be vulnerable to external shocks causing output losses which, in turn, will threaten credit events. As a result, the risk premiums associated with investments in Greece will remain high, restricting capital inflows, discouraging investment and maintaining high borrowing costs, all of which will restrain growth. It is therefore necessary to further lighten the burden of servicing the Greek public debt, as per the Eurogroup's decision of November 2012, which was confirmed by the agreement on the Greek financial assistance programme in July 2015 and the Eurogroup's decision of May 2016.

See Eurogroup (

To achieve this objective, the Greek authorities must not delay delivering on the commitments undertaken in the context of the third financial assistance programme, and Greece's official lenders, in response, should not delay agreement on measures that reduce the cost of servicing the Greek public debt. These steps, however, may be difficult to conclude due to the presence of a coordination problem. At present, the measures to be taken to reduce the Greek debt burden have not been confirmed; they are only a possibility, to be decided after the conclusion of the third Greek programme in August 2018. As a result, the Greek authorities may be reluctant to take measures involving certain and immediate welfare losses in exchange for uncertain gains following non-guaranteed debt-reduction measures. On the other hand, due to moral-hazard considerations, Greece's partners may be reluctant to commit to debt-reduction measures without evidence of Greece's commitment to fiscal adjustment and reforms.

The solution to this coordination problem may be an agreement postulating gradual, pre-announced, specific and automatic debt reductions, conditional upon Greece meeting targets relating to fiscal policy and reforms (see Arghyrou

Conclusion

This article has discussed the reforms that have to be undertaken in EMU countries to ensure the stability and long-term sustainability of the euro. It has also explained the steps needed to support demand during the implementation of reforms, thus enabling their successful conclusion. It has been argued that structural reforms in the EMU should target increases in long-term employment, productivity and external competitiveness. Demand measures that support reforms include an expenditure-based approach to fiscal adjustment and the introduction of EDIS. And in the case of Greece, they include ownership of reforms, the downward revision of fiscal targets, and medium- and long-term measures of debt relief conditional upon the meeting of fiscal/reforms targets.

Finally, economic adjustment in the euro area requires moderation of all fiscal and external imbalances across all member states. Within a monetary union, both excessive deficits and excessive surpluses can cause negative externalities at the union level. Furthermore, any country's participation in the euro implies that its systemic risk increases by a fraction of its partners’ systemic risk, due to the increased interdependence brought about by monetary and banking integration. Imported systemic risk can be reduced, but it can never be fully eliminated. This is why the euro area needs effective risk-reduction and risk-sharing mechanisms, both of which are equally important in the long run. The stability of the euro will improve substantially if all national economic policies are designed with these facts in mind. European solidarity goes hand in hand with macroeconomic prudence, and leading by example requires national macro-policies involving a mix of national and Union-wide priorities that can be sustained by all of the member nations. Prudence and consideration for Union objectives are the two sides of good European citizenship, without which the euro's long-term stability cannot be guaranteed.

Footnotes