Abstract

It is often maintained that the euro debt crisis showed that the Economic and Monetary Union (EMU) was not sustainable without more fiscal integration. However, important causes of the crisis were extraordinary and are highly unlikely to occur again. While the legacy problems of the crisis have been grave, they can be deemed temporary. Therefore, these problems should be combated pragmatically, but with temporary instruments only. A systematic analysis shows that the root causes have been tackled with a wide variety of reforms, both to the EMU itself and by way of structural reforms of the member states. In particular, evidence is presented that the adjustment capacities of the EMU countries are better than commonly recognised. Additional reforms are suggested, especially in the financial sector. With these reforms in place, future crises would have less serious effects. A reformed EMU should be able to withstand such crises without further fiscal integration.

Keywords

Introduction

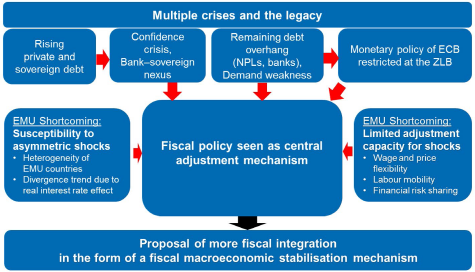

According to a widely accepted view, the recent euro debt crisis has shown that the Economic and Monetary Union (EMU) is not sustainable without fiscal risk sharing. The underlying line of reasoning rests on several arguments, summarised in Fig. 1. Of central importance is the understanding that fiscal policy is a key shock-adjustment mechanism (Fig. 1, central panel). It is claimed that during the euro area crisis, the national fiscal policy of EU members was constrained due to high public deficits and debts (top part, left side of Fig. 1). It is also argued that fiscal policy is of particular importance in the aftermath of the crisis, notably in the context of weak demand and monetary policy at the zero lower bound (top part, right side of Fig. 1). More generally, EMU is considered highly prone to asymmetric shocks (centre left, Fig. 1), while adjustment mechanisms other than fiscal policy are seen to lack effectiveness (centre right, Fig. 1).

Arguments for a fiscal stabilisation mechanism

The debate can be expected to gain new momentum as the European Commission as well as the euro area and EU member countries draw up their positions on deepening the EMU in the process launched by the release of the White Paper on the Future of Europe by the European Commission on 1 March (European Commission

This study contributes to this debate by challenging the above dominant narrative, arguing that more fiscal integration is in fact not needed for the stability of the euro area.

This article is an abbreviated and partly updated version of Matthes and Iara (

For the basic references see Mundell (

Exceptionality of the euro debt crisis

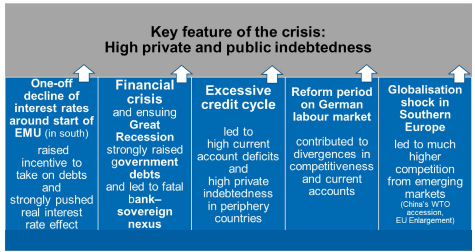

Arguably some of the challenges of the euro area crisis could have been more easily handled had a central fiscal capacity been available to cushion some part of the large shocks to fiscally strained EU members. However, the implication that a fiscal capacity is a necessity for the euro area builds on the understanding that the recent crisis is representative of crises to come. The authors challenge this view, highlighting that this was not the case: the euro area debt crisis can be considered unique, owing to a number of exceptional features. Several extraordinary factors contributed to its severity (Fig. 2), many of which are unlikely to be repeated: the one-off interest rate decrease in the euro area periphery at the onset of EMU; the ensuing extraordinary credit boom; the German labour market reforms in the mid-2000s; the large globalisation shock emanating mainly from China, paralleled by the integration of Eastern European countries into EU value chains; and finally, the context of a severe global financial crisis in 2008. Therefore, some caution is warranted when claims are put forward that the recent crisis is a template of what is to come.

Exceptional circumstances and features of the euro debt crisis

Overall, the root of the crisis was mainly located in the financial sector and the private sector: private debt had grown to very high levels in the run-up to the crisis in many of the stressed countries. Contrary to the popular view, the surge in public debt was much less due to a lax interpretation of the Stability and Growth Pact than to the impact of the global financial crisis on government spending, notably on bank bailouts and fiscal stabilisation (Matthes et al.

During the build-up of imbalances that ultimately culminated in the crisis, the increase in private debt grew, alongside large capital flows from the north to the south of the euro area, which were associated with very high current account deficits (Chen et al.

This is why the legacy of the crisis is still severe, particularly in terms of high unemployment and weak investment. However, these problems are temporary, as they mainly relate to the deleveraging process after an immense debt crisis. In the authors’ view, it would be a mistake to build permanent institutions with shortcomings of their own to tackle temporary problems, even if these are grave: the legacy problems of the crisis should be tackled with temporary tools instead. The unconventional policies of the European Central Bank (ECB), as well as the European Fund for Strategic Investment (which needs improving to become more effective) have been useful in this regard.

The contemplation of instruments to tackle the legacy of the crisis also has to start with an acknowledgement that a number of the measures have already been taken. In particular, strengthening banks’ capital base, introducing the Banking Union (with new restructuring and bail-in tools

Additional reforms are needed. The most important two are: (1) ensuring that bail-in-able capital is largely held by professional investors outside of the banking sector, in order to allow for effective bail-ins in case of bank resolutions; (2) phasing out of the preferential treatment of euro area sovereign bonds and notably the disregard for their factual default risk, in order to break the sovereign–bank nexus.

Reforms to mitigate future crises

The repetition of such severe crises can and must be avoided. Several reforms in the euro area—notably in the areas of macroeconomic surveillance, banking supervision, fiscal policy and national regulation, among others—do address the roots of the crisis. However, several additional reforms, mainly in the financial sector, are needed to mitigate the build-up of large financial cycles and private debt increases and to better deal with standard idiosyncratic downturns (see the table in the Appendix for a systematic presentation of reform requirements, reforms already taken and actions that are still required).

The ESM and the ECB's Outright Monetary Transactions programme are important innovations that close a gap in the institutional framework of the EMU. The use of these instruments is essential to avoid the escalation of future sovereign-debt crises. Based on the principle of conditionally,

This principle must not be weakened by a possible integration of the ESM into EU community law or by measures to enhance its democratic accountability: the political independence of the ESM must not be compromised.

To enhance their effectiveness, ESM adjustment programmes need to

show a stronger focus on growth-enhancing structural reforms from the outset, in particular concerning product markets (IMF

consider the possibility of larger fiscal multipliers during deep recessions (Blanchard and Leigh

pay attention to social fairness when designing reforms, strive to minimise negative social outcomes, and specifically consider the sequencing of reforms and seek balance in the distribution of losses (Grüner

A further improved European Semester could constitute a significant contribution to fostering reform progress (Matthes and Iara

What is more, the ESM and ECB (with the Outright Monetary Transactions programme) should be allowed to ring-fence countercyclical national fiscal policies in the event of future crises, even for highly indebted euro area countries. This should only be possible, however, if the affected country implements well-targeted growth-enhancing structural reforms and if it adheres to the fiscal rules of the EU—which provide ample room to counteract standard recessions.

However, fiscal policy needs to be countercyclical not only in recessions but also in economic (and financial) booms. This has proved to be difficult to ensure for political economy reasons, when pressures rise on finance ministers to spend more in view of higher tax revenues. Moreover, measuring the structural fiscal deficit (which is a key guide to the appropriate fiscal stance) has proved difficult, particularly during economic and financial booms when it tends to be underestimated because potential growth is often overestimated. The inclusion of a measure of the financial cycle in the calculation of potential growth and thus of the structural fiscal deficit could possibly limit measurement errors (de Manuel Aramendia and Raciborski

Other recent reforms have made even more important contributions to the mitigation of financial booms in the future: most importantly, the new macroeconomic surveillance framework as part of EU economic governance, and the macro-prudential supervision exercised by the ECB, which has become the Single Supervisory Mechanism in the euro area. Both have filled gaps in the institutional framework of the EMU. It is particularly important that the Single Supervisory Mechanism can overrule national supervisors: this changes their incentives, tackles the notorious inaction bias and makes supervision more effective. However, these instruments have to be actively used.

Further to the reforms already taken and additional measures suggested above, to prevent excessive financial booms, countercyclical capital buffers should be actively used. As the banking sector is more strictly regulated, more efforts are needed to prevent the build-up of financial-stability risks in the shadow banking sector (ECB

Improved functioning of EMU: less heterogeneity and divergence among EMU countries

Further reflections on the future of the euro area must take note of the fact that, in terms of regulatory and adjustment capacities, the optimality characteristics of the EMU have substantially improved in the course of the recent crisis, indeed much more than conventionally recognised.

These improvements also concern the degree of vulnerability of EMU countries to asymmetric shocks as well as to internal forces that could lead to divergence among them (Fig. 1, centre left).

Structural reforms have reduced regulatory heterogeneity

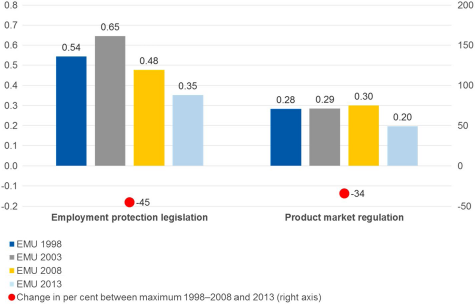

First, euro area members have recently become less dissimilar in important economic dimensions. Traditionally, the EMU has been considered too heterogeneous and therefore susceptible to asymmetric shocks (Pisani-Ferry

Change in heterogeneity of regulation: standard deviation among a sample of EMU countries*

Reduced sample due to lack of data available from 1998 for some countries. Lower standard deviation indicates less heterogeneity. There has been a reduction.

Country-specific macro-prudential measures to mitigate the real interest rate effect

The one-size-does-not-fit-all problem of the single monetary policy and the resulting real interest rate effect are key problems in every currency union and have proved to be important causes of the build-up of macroeconomic imbalances in the EMU (see, e.g. European Commission

To counteract this problem and prevent large asymmetric financial cycles, macro-prudential policy tools can and should be used in a country-specific way.

For similar recommendations see Black (

Improved functioning of the EMU: better adjustment capacities for idiosyncratic shocks

With EMU members not having the ability to devalue their currency or to pursue a national monetary policy tailored to their needs, other effective mechanisms need to be in place to enable their economies to adjust to idiosyncratic shocks. It is commonly held that price and quantity adjustments in labour and product markets respectively are too weak in Europe: this is why fiscal tools are seen as the prime instruments of crisis mitigation. In reality, however, these adjustment capacities are better than commonly recognised and have, to a large degree, further improved due to the various reforms taken during the crisis (Fig. 1, centre right).

Downward wage rigidity is lower than recognised and has been further reduced

Insufficient downward wage flexibility during recessions has long been considered a deep rooted and notorious problem in the euro area, notably among its southern European members (Dickens et al.

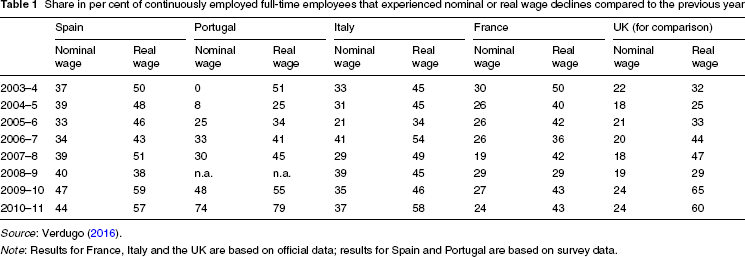

Share in per cent of continuously employed full-time employees that experienced nominal or real wage declines compared to the previous year

Source: Verdugo (

Note: Results for France, Italy and the UK are based on official data; results for Spain and Portugal are based on survey data.

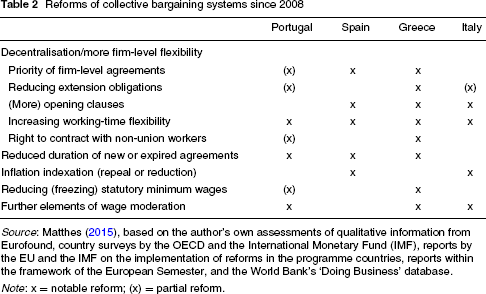

In addition, the recent structural reforms in stressed euro area countries have significantly contributed to further increasing the flexibility of wages and prices (Anderton and Bonthuis

Reforms of collective bargaining systems since 2008

Source: Matthes (

Note: x = notable reform; (x) = partial reform.

Short-term labour mobility as high as in the US during recent crisis

If a country runs into a recession, labour mobility can contribute to reducing unemployment and can help to stabilise incomes. However, labour mobility in the EMU has traditionally been deemed low compared to in the US. In the course of the recent crisis, however, short-term migration flows have been much higher than expected (Huart and Tchakpalla

This positive finding is not only due to a considerable increase in the short-term migration of citizens born in EMU member states (which remains rather limited overall), but importantly also to the emigration of immigrants from non-EMU countries (Eastern Europe and North Africa) who had formerly moved to the respective countries. These latter migration flows also fulfil the function of a pressure valve for quantity adjustment on the labour market. However, the further removal of impediments to labour mobility is still required.

Deepening financial integration, particularly in equity and longer term financing

Financial risk sharing is a key adjustment mechanism for idiosyncratic shocks (see, e.g. Asdrubali et al.

This is not the whole picture, though. In fact, equity and investment fund exposures remained largely intact, as did direct bank loans (SVR

Nevertheless, financial risk-sharing capacities need to improve further in the EMU. The Banking Union and especially the bail-in instrument are important achievements in this respect, and further steps need to be taken to complete implementation of the Banking Union, notably the setting-up of a common European deposit insurance scheme. However, the risk-sharing capacities of such a scheme should only be increased in parallel with the risk reduction in the European banking system, particularly regarding the reduction of non-performing loans and of the exposure of banks’ balance sheets to domestic sovereign bonds. On top of this, further reforms are required: the Capital Markets Union agenda of the European Commission needs to be taken forward, and a clear roadmap must be followed to foster financial integration in the euro area. Regulatory incentives are needed for more diversification among asset classes and investors, more equity (instead of debt) financing and more long-term (instead of short-term) investments.

Finally, one more area has not yet been addressed by the recent reforms: the unambiguous assignment of responsibility for sovereign debt. Strengthening fiscal responsibility and ruling out expectations of bailouts or debt monetisation would necessitate an explicit procedure for sovereign defaults. Otherwise, financial market actors are prone to underestimate the risk involved in sovereign debt and thus demand lower risk premiums than appropriate, thereby limiting the incentive for national governments to pursue a stability-oriented fiscal policy. A reliable sovereign-debt restructuring mechanism should be adopted for newly issued debt with an appropriate phase-in period (Busch and Matthes

Conclusion

This article contributes to the debate on the future of the EMU and challenges the claim that fiscal integration is indispensable for its long-term viability. Specifically it highlights that, due to specific historical preconditions, the character of the recent crisis was unique, and that important institutional reforms have already been made. Therefore, the experience of this crisis is not a valid point of departure for contemplating permanent instruments of fiscal integration in the euro area.

Overall, the reform pressures of the recent crisis have significantly improved the structural functioning of the EMU. On this basis, and with the additional reforms suggested here, it is far from evident that the EMU would be unsustainable without further fiscal integration. The prospect of fiscal integration in the EMU thus needs to be discussed as a political choice and not as an economic necessity.

Footnotes

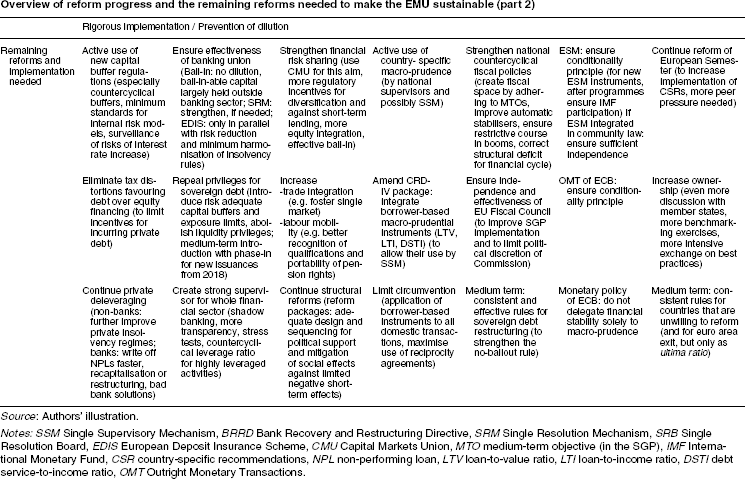

Appendix

Overview of reform progress and the remaining reforms needed to make the EMU sustainable (part 2)

| Rigorous implementation / Prevention of dilution |

|||||||

|---|---|---|---|---|---|---|---|

| Remaining reforms and implementation needed | Active use of new capital buffer regulations (especially countercyclical buffers, minimum standards for internal risk models, surveillance of risks of interest rate increase) | Ensure effectiveness of banking union (Bail-in: no dilution, bail-in-able capital largely held outside banking sector; SRM: strengthen, if needed; EDIS: only in parallel with risk reduction and minimum harmonisation of insolvency rules) | Strengthen financial risk sharing (use CMU for this aim, more regulatory incentives for diversification and against short-term lending, more equity integration, effective bail-in) | Active use of country- specific macro-prudence (by national supervisors and possibly SSM) | Strengthen national countercyclical fiscal policies (create fiscal space by adhering to MTOs, improve automatic stabilisers, ensure restrictive course in booms, correct structural deficit for financial cycle) | ESM: ensure conditionality principle (for new ESM instruments, after programmes ensure IMF participation) If ESM integrated in community law: ensure sufficient independence | Continue reform of European Semester (to increase implementation of CSRs, more peer pressure needed) |

| Eliminate tax distortions favouring debt over equity financing (to limit incentives for incurring private debt) | Repeal privileges for sovereign debt (introduce risk adequate capital buffers and exposure limits, abolish liquidity privileges; medium-term introduction with phase-in for new issuances from 2018) |

Increase trade integration (e.g. foster single market) labour mobility (e.g. better recognition of qualifications and portability of pension rights) |

Amend CRDIV package: integrate borrower-based macro-prudential instruments (LTV, LTI, DSTI) (to allow their use by SSM) | Ensure independence and effectiveness of EU Fiscal Council (to improve SGP implementation and to limit political discretion of Commission) | OMT of ECB: ensure conditionality principle | Increase ownership (even more discussion with member states, more benchmarking exercises, more intensive exchange on best practices) | |

| Continue private deleveraging (non-banks: further improve private insolvency regimes; banks: write off NPLs faster, recapitalisation or restructuring, bad bank solutions) | Create strong supervisor for whole financial sector (shadow banking, more transparency, stress tests, countercyclical leverage ratio for highly leveraged activities) | Continue structural reforms (reform packages: adequate design and sequencing for political support and mitigation of social effects against limited negative short-term effects) | Limit circumvention (application of borrower-based instruments to all domestic transactions, maximise use of reciprocity agreements) | Medium term: consistent and effective rules for sovereign debt restructuring (to strengthen the no-bailout rule) | Monetary policy of ECB: do not delegate financial stability solely to macro-prudence | Medium term: consistent rules for countries that are unwilling to reform (and for euro area exit, but only as ultima ratio) | |

Source: Authors’ illustration.

Notes: SSM Single Supervisory Mechanism, BRRD Bank Recovery and Restructuring Directive, SRM Single Resolution Mechanism, SRB Single Resolution Board, EDIS European Deposit Insurance Scheme, CMU Capital Markets Union, MTO medium-term objective (in the SGP), IMF International Monetary Fund, CSR country-specific recommendations, NPL non-performing loan, LTV loan-to-value ratio, LTI loan-to-income ratio, DSTI debt service-to-income ratio, OMT Outright Monetary Transactions.