Abstract

Triggered by the subprime mortgage crisis in the United States (U.S.), a financial tsunami has spread rapidly around the globe, from the U.S. to Europe and the rest of the world, causing the world economy to enter a recession. China is no exception, and has suffered a sharp reduction in the growth of its export and manufacturing sectors. In this paper, we attempt to model and analyze the impact of financial crisis on the manufacturing industry in China using data collected from March 2005 to November 2008 by the China Statistical Databases of the National Bureau of Statistics of China. The results indicate that China's manufacturing industry may have to tolerate a significant negative effect caused by the global financial crisis over a period of time, with its gross industrial output value declining continually throughout 2008 and 2009 before reaching a state of equilibrium. The intervention effect is described in this study as temporary but immediate and abrupt. It is found that the ARIMA-Intervention model is more precise at explaining and analyzing the intervention effects of the financial tsunami.

1. Introduction

When the credit or subprime crisis in the U.S. began in July 2007, it unexpectedly triggered financial turmoil in the U.S. even though the federal government took various actions to prevent the mortgage market from being severely disrupted and to reassure the markets. Soon after the outbreak of this financial crisis, the major financial and monetary authorities in other developed economies joined the fight by discussing and passing massive economic bailout plans and stimulus packages. However, the financial crisis still spread swiftly around the globe, from the U.S. to Europe and then to the rest of the world. The effects on the global economy were even more prominent and evident in September 2008. Stock markets worldwide underwent a dramatic, marked drop in value and continued to plunge with volatility. A number of leading banks were crippled by financial instability and collapsed; in particular, Lehman Brothers went into bankruptcy. As a result of this global financial crisis, dubbed a financial tsunami, the world economy has deteriorated into economic recession. China, an export-driven economy known as the world's factory, has likewise been battered by the global economic slowdown, resulting in weaker domestic demand and decreasing exports. China attempted to stave off the economic downturn initially by cutting interest rates, unchanged since 2002, on September 15, 2008.

According to the International Monetary Fund (2006) and WTO (2007), China's exports grew on average 5.7% in the 1980s, 12.4% in the 1990s, and 21.1% between 2000 and 2006. However, China's exports and imports plunged by 2.2% and 17.9% in November 2008 from a year earlier, and the trade surplus in the first three quarters of 2008 dropped US$4.7 billion compared with the same period in 2007 (National Bureau of Statistics of China, 2008). Specifically, exports to the U.S. declined by 6.1% while those to ASEAN (Association of Southeast Asian nations) countries dropped by 2.4%, a dramatic fall from +21.5% growth in October 2008. It is likely that China's economic growth will continue to slow down, similar to that of trans-Pacific trade and intra-Asian trade in the region as a result of the U.S. and Europe plunging into economic recession. According to figures from China's National Bureau of Statistics, annual Gross Domestic Product (GDP) growth fell from 12.6% in the second quarter of 2007 to 10.6% in the first, 10.1% in the second, and 9% in the third quarter of 2008 (World Bank, 2008). The growth of industrial value-added fell even more steeply to 8.2% in the third quarter of 2008 (World Bank, 2008). The figures for GDP growth and industrial value-added growth are the first single-digit growth rates since its economic reforms in 1978 (which resulted in an average annual growth rate of 10%) and 2001 respectively.

The above statistical data provides convincing evidence that China is not immune to the U.S. financial crisis, especially in terms of its manufacturing economy. This is because its economy, trade and manufacturing activities are closely correlated (Chung et al., 2008). However, previous studies have not investigated the impact of sudden financial crisis on the manufacturing industry. This paper thus attempts to examine and analyze the impact of this global financial crisis. In order to assess the impact of this event, ARIMA intervention analysis will be applied in this study to evaluate the pattern and duration of its effect. This paper consists of six sections. In this section, the global financial crisis and the objective of this paper have been introduced and the structure of the paper presented. Section 2 will discuss the ARIMA model with intervention analysis in terms of the equations involved and the procedures of model estimation. The empirical results and analysis of model estimation using both the ARIMA model and the ARIMA-Intervention model will then be explained in section 3, in which a comparative study will be conducted to assess whether the ARIMA-Intervention model is able to account for the impact of the global financial crisis compared to the ARIMA model. In section 4, major findings will be summarized and highlighted, followed by the conclusion. Lastly, acknowledgements and a list of references will be presented in sections 5 and 6 respectively.

2. The ARIMA Model and Intervention Analysis

A stochastic, time-series ARIMA model will be used to analyze the dynamics of changes, variations and interruptions in the growth of China's manufacturing industry through time-series data. This ARIMA model can help to perceive whether the global financial crisis impacts the growth of China's manufacturing industry and the nature of effect, if any. This will provide firms with insights enabling them to cope with and weather the financial storm. The applications of the ARIMA model with and without intervention analysis have been widely used in different aspects, such as flexible manufacturing system scheduling and simulation (Ip, 1997; Ip et al., 1999), tourism forecasting (Cho, 2001), investigation and forecast of economic factors (Chung et al., 2008), and impact analysis on air travel demand (Lai & Lu, 2005).

2.1. Transfer Function and Univariate ARIMA Model

The ARIMA model developed by Box and Jenkins (1976) has become popular due to its advantages of power and flexibility (Pankratz, 1983). Put simply, the general transfer function of ARIMA is of the following form:

where Y t and X t are the output and input series respectively, b is the time delay, ω(B)/δ(B) is the polynomial of the transfer function, [θ(B)/φ(B)]ε t is the noise model, and ε t is the residual, i.e. white noise. By simplifying Eqn. (1), Eqn. (2) is obtained below:

where V(B) = δ−1 (B)ω(B)B b , ω(B) = ω 0 –ω1B– … –ω s B s , δ(B) = 1 – δ1B – … – δ r B r , and N t = [θ(B)/φ(B)]ε t .

The univariate ARIMA model combines three components: Autoregressive (AR), Integration (I) and Moving Averages (MA), therefore the general form of a univariate ARIMA model denoted as ARIMA(p,d,q)(P,D,Q) s is defined as Eqn. (3), which is further simplified as Eqn. (4):

where p, d, and q are the order of the AR, I and MA terms respectively; P, D, and Q are the order of the seasonal AR, I and MA terms respectively; ∇ d = (1 – B) d and ∇D s =(1–B s ) D represent the regular and seasonal I operators respectively; φ(B)p and Φ P (B s ) are the nonseasonal and seasonal AR operators respectively; θ q (B) and Θ Q (B s ) are the nonseasonal and seasonal MA operators respectively; and ε t is the disturbance or random error.

2.2. ARIMA Model with Intervention Analysis

As discussed by Box and Jenkins (1976), an intervention model is of the general form:

where I t is an intervention or dummy variable that is defined as:

The present financial crisis is unique in that it was initially triggered in July 2007 and then spread to Europe and the rest of the world, including China evidently, in September 2008, its effect enduring throughout the year 2008. I t = 1 is thus defined for the occurrence of the global financial crisis, and I t = 0 otherwise.

2.3. Procedures of Model Development

In general, the model estimation of ARIMA consists of the following three stages:

Unit root test and identification of the order of difference, i.e. d. This preliminary step is essential to stabilize the time-series data and reduce the residual. The Augmented Dickey-Fuller (ADF) test is often employed for the analysis of the unit root, where the null hypothesis is that the input series has a unit root.

Estimation and diagnosis of the parameters of transfer function, i.e. p and q. The autocorrelation function (ACF), partial autocorrelation function (PACF) and cross-autocorrelation function (CACF) are important to tentatively estimate the parameters of transfer function, while statistical measures naturally provide statistical evidence to support the determination of an appropriate transfer function.

Residual/noise diagnostic check. The correlogram of Q-statistics based on the ACF and PACF of the residual is generally used for residual analysis.

3. Empirical Results and Analysis

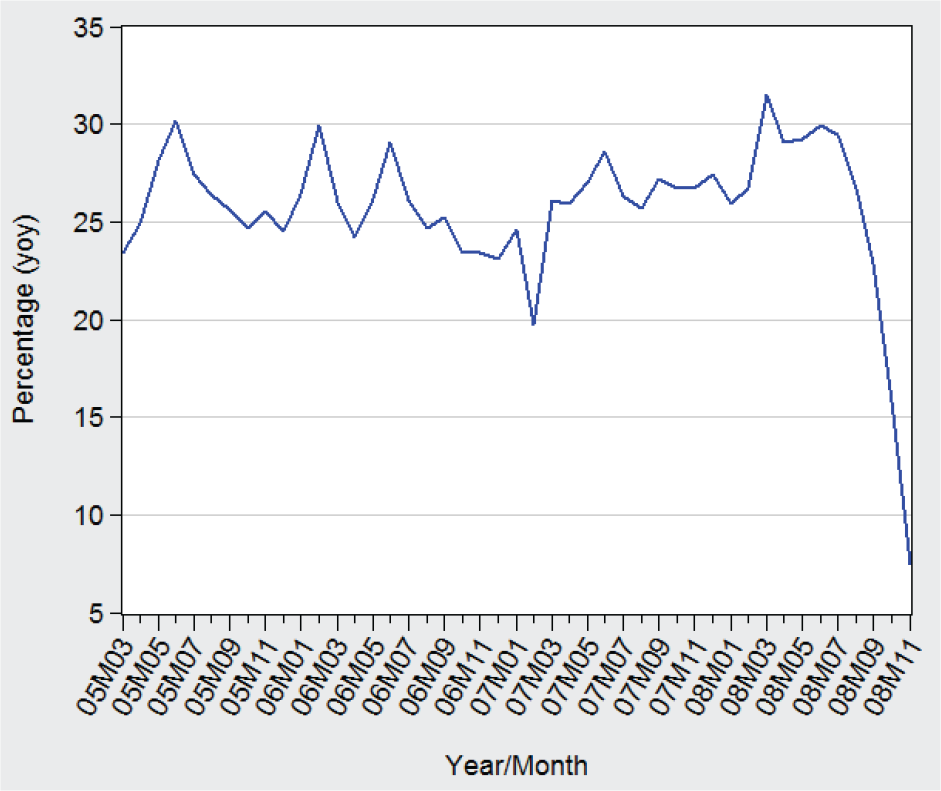

Data for the period between March 2005 and November 2008 provided by the China Statistical Databases authorized by China's National Bureau of Statistics were used for the impact analysis of the financial crisis on China's manufacturing industry. We considered the financial crisis to be the major event affecting the manufacturing industry in China during the period under study. The time-series data for gross industrial output value (ind_output) are exhibited in Fig. 1. The figure shows a dramatic downward trend after August 2008, and seasonality appears to be present in the time-series according to its correlogram.

The time-series of ind_output

3.1. Results and Analysis of Univariate ARIMA Model

To make the time-series stable and stationary, the ADF test is applied, which proves that the time-series contains a unit root. Taking one difference, i.e. d = 1, is found to be necessary to reject the null hypothesis and achieve a stationary time-series, as the t-statistic value of ADF (−4.9104) is smaller than the critical values (−2.9314) and (−3.5925) at the 5% and 1% significance level respectively. The ACF, PACF and related statistical measures including the Schwarz criterion (SC), the Akaike info criterion (AIC) and adjusted R-squared (adjusted R2) suggest that the best-fit ARIMA model is of one nonseasonal AR, one nonseasonal MA and two seasonal MA terms with one differencing order, i.e. ARIMA(1,1,1)(0,1,2)12. The ARIMA(1,1,1)(0,1,2)12 model is formulated below.

Diagnostic checks of the estimated ARIMA(1,1,1)(0,1,2)12 model prove that all coefficients are statistically significant with p-value<0.05 under t-statistics, and the estimated model has white noise with insignificant Q-statistics and p-value>0.38 under the residual test. Furthermore, the model projection indicates that the time-series will continually undergo a downward trend until December 2008 before reaching a steady state.

3.2. Results and Analysis of ARIMA-Intervention Model

When we include the financial crisis as an intervention of the time-series, the ARIMA model with intervention analysis is explored. As the global financial crisis extended to China on September 2008 and beyond, the intervention, I t , was initiated on September 2008. The ADF test provides evidence that the time-series in the pre-intervention model has no unit root and is stationary as the t-statistic value of ADF (−3.7577) is smaller than the critical values (−2.935) at the 5% significance level and (−3.601) at the 1% significance level when d = 0. Taking ACF, PACF, SC, AIC and the adjusted R2 into account, the ARIMA model with intervention analysis can be estimated. The pre-intervention model, ARIMA(1,0,0)(2,0,1)12, is determined below.

After the diagnosis of noise and transfer function, the pre-intervention model, ARIMA(1,0,0)(2,0,1)12, is proved to be valid, with significant coefficients and white noise, in which p-value<0.05 under t-statistics and p-value>0.14 under Q-statistics.

The ARIMA model that includes intervention in the global financial crisis is estimated below, where the diagnosis of noise proves that it is a white-noise process and the estimated model is thus valid.

From the results of model estimation and CACF, it is found that the intervention due to the global financial crisis extending to China has had a negative effect on China's manufacturing industry. The intervention effect is calculated as an asymptotic change of 27.74%. The intervention has not only had an immediate effect on China's manufacturing industry, leading to a decrease in its gross industrial output value during September 2008, but also caused a significant decline in the subsequent months. It is further expected that China's manufacturing industry will be seen to have tolerated the destructive effect of the global financial crisis throughout the year of 2008 and into 2009. The intervention analysis further describes the impact of the financial tsunami on China's manufacturing industry as immediate and abrupt.

Key statistical outputs of the ARIMA(1,1,1)(0,1,2)12 and ARIMA-Intervention(1,0,0)(2,0,1)12 models

3.3. Comparative Study

The key statistical outputs of the two models are exhibited in Table 1. They provide evidence that the ARIMA-Intervention model with lower SC and AIC and higher adjusted R2 is more accurate than the ARIMA model without intervention analysis in explaining the trends of China's gross manufacturing output with and without the intervention of the global financial crisis. Hence, it can be seen that employing the ARIMA model with intervention analysis, forecasts and measurement of China's manufacturing industry in the post-intervention periods is more accurate.

4. Conclusion

The U.S. financial crisis was triggered on July 2007; however, it did not affect China's economy and manufacturing industry until later, when it became a disaster and turned into a global economic problem. The intervention effect of the global financial crisis that began in September 2008 on China's manufacturing industry, as measured in this study, is immediate and alarming. This significant negative effect has led to a dramatic decline in China's gross industrial output value since September 2008, which is likely to have continued throughout 2008 and 2009 before reaching a steady state. This study further compares the results of the ARIMA and ARIMA-Intervention models, confirming that the application of intervention analysis is appropriate for explaining the dynamics and impact of interruptions and changes of time-series in a more detailed and precise manner.

Footnotes

5. Acknowledgement

The authors would like to express their sincere thanks to the Hong Kong Polytechnic University for its financial support of this research work under Teaching Company Scheme project number ZW98.