Abstract

Since the rise of the knowledge-based economy, many worldwide companies have begun to deal with different frameworks to manage and evaluate the performance of intellectual capital, especially in the area of knowledge management services. This paper presents a novel conceptual model aiming to support management in evaluating and prioritizing their intellectual capital competitive core competences. Based on the analytic hierarchy process, the model analyses interdependences among intellectual capital elements and determines the impacts of core competences on organizational performance. To validate the model, it is empirically applied in the Technology Transfer Unit of the Italian national agency for new technologies, energy and economic development.

1. Introduction

Since the business world has begun to understand the importance of intellectual capital – in relation to both value creation and business performance improvement – the axiom “knowledge is power” has gained ever-greater significance. It is especially pertinent at a time when the global economy is evolving to become more information-intensive [1].

As a result of this change, organizations' intangible assets are becoming the principal factors of success in today's knowledge-based economy; what an organization knows is becoming more important than what an organization owns. This is reflected by today's organizations paying greater attention than ever before to their intellectual capital, patents, trade secrets, processes, management skills, and technologies. The literature proposes a clear relationship between an organization's performance and intangible assets. According to Penrose [2], implementing these intangible resources in an organization's strategies enforces its performance in response to market opportunities. Nevertheless, most organizations still do not understand the importance of their intangible assets [3,4], which leaves the management inside these organizations lacking these competitive value drivers [5]. In this regard, Kim and Kumar [6] refer to the lack of accurate evaluation methods and prioritization of performance drivers, which contributes to identifying the intellectual capital influence on business value. Moreover, Lev [7] highlights the need for an innovative approach towards more efficient assessment of organizations' R&D, far from the traditional accounting and cost-based methods that over-estimate risk perception on R&D investments. These types of performance driver evolution and prioritization models should support organizations' management to define their business gaps and set up their business strategies in alignment with their internal resources to create competence and value [8–11].

Based on these concerns, the authors of this paper present a model called Intellectual Capital Competitiveness Evaluation (ICCE), which aims to support organizations' management in evaluating and prioritizing their organizational intellectual capital competitiveness. Based on analytical hierarchical prioritization of organizations' intellectual capital and its measurement indicators, the ICCE hierarchy model will analyse interdependence between organization performance and its intangible assets. The aim is to determine the impact of intellectual capital on organization performance.

Furthermore, these intellectual capital characteristics will be categorized into three main performance competitiveness drivers (functional and cultural; social and positional; regulatory and operational), giving a set of priorities for intellectual capital competitiveness.

This paper aims to support management in evaluating and prioritizing intellectual capital by considering organizational context; furthermore, it intends to provide organizations with an indicator of strategy gaps, and to support management in implementing strategies and making decisions in response to market opportunities. In addition, an organization's index and the weight and grade of intellectual capital characteristics' contributions to performance will be analysed.

In Section 2 we present a literature review of the relationship between organizations' competencies and intellectual capital, and then demonstrate how the core competencies of these internal resources impact the organizations' performance. In Section 3 we introduce the ICCE conceptual model, along with its evaluation processes. Section 4 presents the empirical screening of the ICCE model application, and Section 5 concludes the paper.

2. Literature Review

2.1 Intellectual capital and competitive capabilities

Organizations' competitive capabilities and process efficiencies are, without doubt, becoming more and more fundamental. In rapidly changing markets, organizations everywhere are striving to succeed and are making tremendous efforts in these domains so as to excel and be unique.

Amit and Schoemaker [12] defined capabilities as “the organization's capacity to deploy resources, usually in combination, using organizational processes” in order to achieve strategic and competitive business performance. Teece et al. [13] defined organizations' capabilities as playing a critical role in sustaining their competitive advantage.

of the literature on Resource-Based View theory (RBV) views capabilities as based on information, tangible or intangible processes, which are firm-specific and are developed over time through complex interactions among the firm's resources [2,14]. These resources include the organization's internal capabilities, such as patents and know-how, which allow it to excel and create competitiveness.

Many researchers have emphasized the importance of these capabilities and internal resources, presenting them in terms of intellectual capital. Stewart [15] suggested that “every company depends increasingly on knowledge – patents, processes, management skills, and technologies, information about customers and suppliers, and old-fashioned experience”, and that, “added together”, this knowledge is what constitutes intellectual capital [16]. Thus, he defined intellectual capital as a compounding of an organization's internal resources and capabilities, plus the knowledge of its employees.

Other authors refer to the contribution of an organization's internal resources, – its knowledge, skills, capabilities, and commitment to generating intellectual capital. Bohlander and Snell [17] state that intellectual assets such as experience, know-how, innovation and new ideas are crucial value drivers for the organization's performance and competitiveness.

The intellectual capital classification found in the literature refers to a taxonomy which encompasses three types of capital: relational, structural, and human [18–21].

Human capital has been defined as the individual contributions of knowledge, ideas, innovations, patents, and many more, made by employees within the organization bringing value to the organization's intangible assets [22–25]. Other authors include personal values and organizational culture in human capital, as it is difficult to imitate or replace individual contributions to the organizational context [19,21].

Structural capital includes all the organizational processes, policies, functions, procedures and technology, as well as organizational structure [16,19,23]. Bontis [26] suggests that a lack of strong structural capital denotes a lack of effective integration of employee knowledge and skills within an organization, and management of these is a fundamental part of the organization's competitive capabilities.

Relational capital refers to the knowledge and competencies available to organizations through the relational structure with external parties such as customers, suppliers, partners, and business affiliations [23,27,28]. Furthermore, Youndt et al. [18] and Alder and Kwon [1] identified relational capital as “external structure capital” or “external social capital”. These aspects refer to employee interaction with external parties and environments.

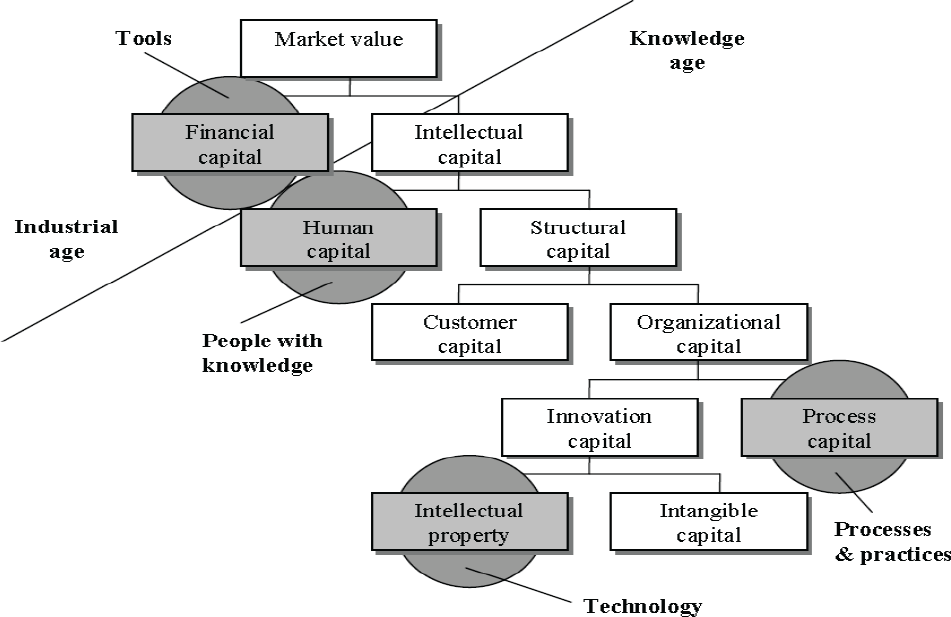

Miller and Morris [29] also highlight the relationship between intellectual capital and organizations' capabilities by mapping it onto the Skandia intellectual capital model, which was introduced by Edvinsson [30]. Figure 1 illustrates how the organizational capability components relate to intellectual capital.

Relationship between organizational capabilities and intellectual capital (Miller and Morris, 1998)

Furthermore, Figure 1 demonstrates that the intellectual capital of an organization can be further categorized into technology, processes and practices, people with knowledge, and tools, which are all components of organizational capability.

Thus, following on from the pioneering work of the above-mentioned researchers, the authors of this paper defines organizations' competitive capabilities as their capacity to deploy competitive advantages in response to market opportunities and competitors, by exposing and utilizing their human, structural, and relation capabilities to enhance their performance through creativity, innovation, patents, and new products.

2.2 Organizational performance drivers

An organization creates performance competence by linking their internal resources to their activities and processes in accordance with the specific competitive context [31–33]. In this regard, Bessant and Tsekouras [34] wrote that organizational performance competencies are created by abilities, which are outcomes of behavioural habitual procedures. These habitual procedures are created and strengthened over time through organizations' structures, policies and cultures. Furthermore, in [35,36] organizational competencies are seen as specific combinations of behavioural habitual procedures and organizations' activities and processes. The concept of organizational performance competence was introduced by Hamel and Prahalad [37], who highlighted the importance of understanding performance differentials through the organizations' core competencies as “a collective learning in the organization, especially how to coordinate diverse production skills and integrate multiple streams of technologies” with a goal of delivering value to customers. Hamel [38] also described how an organization deploys collaborative learning based on technological processes to utilize their internal production skills and resources, in order to create new competitive advantages for the organization's core activities in response to the market and competitors.

However, Andriessen and Tissen [39] outlined the concept of “weightless wealth”, wherein the ability to do something that provides value to an organization is no longer necessarily connected to production skills. Andriessen [40] pointed to core competence as a source of power and new competitive advantages based on organizations' intangible assets. Furthermore, they defined a core competence taxonomy based on five categories of intangibles that create core competence for organizations in different sectors (Figure 2).

Core competence model (Andriessen and Tissen, 2000)

Andriessen and Tissen [39] emphasized the fact that organizational performance can be imposed through intangible assets such as core competence, which includes: technology and explicit knowledge such as patents, manuals, and procedures; skills and tacit knowledge such as know-how and employee competence, with a role as dynamic knowledge; management processes, which include leadership and control, communication, and management information, and aim to create open channels for knowledge access and flows, as well as designing and implementing value-creating activities; collective values and norms, which include knowledge-screening and control processes and activities, through client focus, reliability, and quality; and finally endowments, which include brand and image, customer base, talent and supplier network, and stakeholders.

The core competencies suggested in [39] identify the capability differentials of organizations' intangible assets, which are considered a source of organizational performance drivers and competitiveness. According to Hall [41], organizations should bring these intangible resources and core competencies into their strategic thinking.

3. The conceptual model of ICCE

Marr et al. [42] wrote: “if organizational performance is measured using a set of measures and no indication of priority is given; individuals are forced to rely on their own judgment as to which is the most important value driver”.

The conceptual ICCE model presented in this paper aims to evaluate and prioritize business performance driven by organizations' intellectual capital core competence. The model identifies a taxonomy of three competitiveness capability drivers (functional and cultural; social and positional; regulatory and operational), which in turn drive the performance and competitive advantage of the organization. These three layers of competitiveness have been defined based on the literature review above, and by considering the relationship between organizations' capabilities and their intellectual capital, which in turn lead to competitive performance, as shown in Table 1.

Organizations' performance competitiveness drivers

These three layers of competitiveness will be used as a prioritization tool for the business performance characteristics within the ICCE model, which aims to support management to understand how their intellectual capital contributes to value creation from an endogenous perspective inside an organization, and from an exogenous perspective outside the organization. According to Ittner and Larcker [43], a better understanding of value creation can then be used as a basis for validation, as well as for decision making.

The model believes that organizations should focus more on creating competitive value and competences endogenously, with the strategic intent of driving greater value creation for their exogenous environments from customers, alliance, suppliers and partners. Figure 3 presents the conceptual model used in the paper.

The conceptual model

Furthermore, based on AHP [44], the model shows a balanced image of the contribution of intellectual capital to firm performance, as each asset can be allotted a priority that allows measurement of its influence on the organization's competitive capability performance. The definition of these priorities is based on a process which assembles managers' thoughts and experiences through AHP. Figure 3 presents the ICCE conceptual model.

3.1 The model's hierarchical structure

The first level of the hierarchical structure encompasses the organization's goals (organizational performance), and therefore holds the highest degree of significance. This global value includes all of the second-level elements (performance drivers) which specify the content and meaning of the company's goals, including three organizational competitiveness value drivers: functional and cultural; social and positional; regulatory and operational. These are grouped into the elements of the third level (core competence bundle): technology and explicit knowledge; skills and tacit knowledge; collective values and norms; endowments. At the last level, the measurement indicators are provided according to the management's measurement needs.

Organizational performance: organizational performance represents the final results achieved by an organization, based on their core competence bundle. Core competence bundle: located at the second level, the core competence bundle includes technology and explicit knowledge, skills and tacit knowledge, collective values and norms, and endowments. These were identified and categorized in [39] as the main core competencies of the organization. Core competence measurement indicators: the measurement indicators vary from one organization to another, and depend on the typology of the industry and the dimensions of the firm in question. They can be defined according to the organization's sector and its evaluation aims, based on management perceptions.

In this model, managers' opinions and experiences should be taken into consideration for the achievement of desired performance, not only with regard to the actual state of the company's performance, but also its development over time. The choice of intangible assets to be developed by an organization is strictly dependent on its management's capability to make this choice fit the business strategy of the organization [45–47].

3.2 The assessment process

The assessment process begins with establishing the degree of importance (priority) with regard to the totality of the assets in order to achieve the company's prefixed goals.

To do this, the AHP is used to determine the degree of importance of each element of the hierarchical structure and to calculate its overall priority. In order to establish the elements' priorities in the hierarchy, they are pair-wise compared against the element immediately above in the hierarchy.

This comparison is performed using the AHP comparison scale [44], which expresses comparison verbally, and these verbal comparisons are then represented numerically. In particular, the pair-wise comparison process starts at the top of the hierarchy to select the value driver with the highest priority. Then, at the following lower level, the value drivers' priorities are divided by the weighting process between their descendants, and so on. In order to obtain the set of overall priorities, all the pair-wise comparison results need to be synthesized. The overall priority of an element is its degree of importance in relation to all the other elements in the hierarchical structure, and represents its significance with respect to the whole of the company's performance.

Therefore, the overall priority of each measurement indicator is expressed by xijk, where:

i value refers to the value driver j value refers to the five characteristics of each value driver k value refers to the measurement indicators relating to each value driver and to each characteristic, ranging from 1 to the total number of the selected indicators.

In the following step, a qualitative value is calculated, which expresses the numerical value of the performance of each indicator: pijk. In this process, it is necessary to take into account both the temporal variations of indicators and managers' expectations for performance improvement.

To fulfil this objective, it is necessary to apply the AHP again, in a different way from that previously implemented. A pair-wise comparison is made using three elements for each indicator:

The value of the performance calculated for the time period “T” (PT); The value of the performance calculated for the time period immediately preceding the time period “T”, that is “T-1” (P T -1); The desired performance (PDesired).

The three-element matrix of the pair-wise comparison is represented in Figure 5. The three values are derived as follows: P(T-1; T) is the numerical ratio between the value of the indicator performance calculated for the time period “T” (PT) and that calculated for the time period “T-1”; P(T-1; Desired) is inferred from the manager's expectation for the value of such an indicator (PDesired); P(T; Desired) is determined by simply substituting one relation into the other, so as to obtain a numerical value.

The ICCE model

The pair-wise comparison matrix of each measurement indicator

This particular procedure helps to avoid the inconsistency that could emerge from the fact that one of the three terms of comparison derives from subjective considerations (PDesired), and also that some measurement indicators derive from qualitative data.

By means of the same procedure as was used to find the pair-wise comparison matrix priorities, the normalized values of the priorities for each of PT, PT-1, and PDesired are obtained. The priority of PT is the weight of the measurement indicator performance, calculated for the time period “T” in accordance with its correspondent value for “T-1” and its desired performance.

The repeated application of the aforementioned procedure for each indicator provides an evaluation of performance (pijk), where the indexes i, j, and k are the same as for the value range and connotation of the quantitative value xijk.

For each indicator, the value of pijk is ranged between 0 and 0.5. This follows from the fact that the sum of the three weights of PT, PT-1, and PDesired must be unitary and that the value of P Desired must be higher than those of PT and PT-1, in accordance with managers' expectations. It is demonstrable that PT and PT-1 weights cannot assume values that are either negative or higher than 0.5.

At this point, for each indicator, it is possible to combine the weights of the performance (pijk) with their overall priorities (xijk). The sum of the products of pijk and xijk of each measurement indicator results in a unique index, H.A.I.:

The H.A.I. value ranges between 0 and 0.5, as a consequence of the fact that not every pijk can assume a value which is either negative or higher that 0.5, and that not every xijk can assume a value either negative or higher than 1.

4. Empirical application

This paper presents an empirical study from Italy, where the ICCE model has been applied to a division in an R&D centre. The main aim of this empirical screening is to demonstrate how the ICCE conceptual model can support management in understanding their contribution to business performance, and indicate business performance management gaps.

The ICCE model was applied in the Unit of Training and Technology Transfer (UTT- Learn) within the Italian National Agency for New Technologies, Energy and Sustainable Economic Development (ENEA). This unit aims at creating and ensuring the diffusion of knowledge and the transfer of technology gained within the Agency, by means of both traditional and distance learning courses.

The process of creating and implementing the ICCE model was highly iterative and involved a series of face-to-face interviews with the division managers to understand their core competence activities. It followed the same steps of the ICCE conceptual model (Figure 3). The design starts from defining the UTT-Learn division core competence, depending on its mission, objectives, and vision. The researchers defined32 core competence indicators. Then, the division's managers were asked to choose the most 15 relevant core competence indicators for their division. Table 2 presents the selected 15 core competences.

ENEA UTT-Learn Core Competences

For evaluating the performance contributions of the 15 core competence indicators of the UTT-Learn performance, the researchers applied the AHP model by using the Expert Choice v.11 (EC) software package, which allows the synthesis of values and the understanding of the core competence indicator weights and degree of impact with regard to the UTT-Learn performance.

The AHP questioner model was designed based on these 15 core competence indicators and was sent to the UTT-Learn managers to be answered. Following the ICCE model, the AHP questioner examined the 15 core competences in terms of three layers of performance competitiveness drivers: functional and cultural competitiveness, social and positional competitiveness, regulatory and operational competitiveness.

This analysis has the aim of supporting the management of UTT-Learn to understand the impact of their core competence indicators on the division performance, as well as supporting them with a performance tracing tool, allowing them to identify their strategy gaps and weaknesses, as well as their current strengths (Figure 6).

The UTT-Learn model application

4.1 Obtained Results

This section presents the results obtained for the three performance competitiveness value drivers: regulatory and operational, functional and cultural, social and positional.

4.1.1 Functional and cultural competitiveness

Referring to the obtained results, “functional and cultural” made the highest contribution to UTT-Learn performance. The HAI index obtained a total performance of 0.3450 out of 0.5.

This indicates that the UTT-Learn division gives great attention to deploying competitive advantages through exposing and utilizing their human capital innovative capabilities, skills, experiences, and know-how, especially in order to create and improve an innovative, efficient, effective work environment inside the UTT-Learn division.

Moreover, under functional and cultural competitiveness the management of UTT-Learn recognizes great importance in the performance of the following core competence indicators: client focus, vision planning capability, customer satisfaction, with total obtained performances of 0.0965, 0.0830, and 0.0370, respectively.

This means that the UTT-Learn management accords a high priority to the external environment and the division business strategy through enhancing and adding more competitive advantages to the substantially experienced and knowledgeable employees for the UTT-Learn division.

4.1.2 Social and positional competitiveness

The “social and positional” driver made the second highest contribution to UTT-Learn performance, with a total obtained performance of 0.3247 out of 0.5.

The social and positional competitiveness performance shows high core competence under the following indicators: national and international project funding, codified knowledge diffusion, vision planning capability, with a total performance of 0.0830, 0.0627, and 0.0374, respectively.

The social and positional competitiveness generates the highest performance impact due to the fact that UTT-Learn provided distance learning courses, training and development workshops and seminars for more than 13,000 external customers.

4.1.3 Regulatory and operational competitiveness

The performance driver that contributed least was “regulatory and operational competitiveness”, which showed the third highest competitiveness contribution to UTT-Learn performance. The HAI index obtained a total performance weight of 0.3044 out of 0.5.

The highest impacts of the core competence indicators were driven by the organizational culture, vision planning capability, information technology in service for supporting the research, teaching and industrial cooperative practice, with a total performance of 0.0818, 0.0467, and 0.0444, respectively.

However, the regulatory and operational competitiveness shows the lowest performance impact in comparison to “functional and cultural” and “social and positional”. This means that the management of UTT-Learn need to pay more attention to and focus more on exposing and utilizing their structural capital capabilities, developing effective protocols and organizational routines, encouraging knowledge exchange, and promoting the importance of building external and internal relations with academics and professionals to exchange knowledge, ideas, and innovation.

Figure 7 presents the core competence impacts of the UTT-Learn performance competitiveness drivers. The high growth under “functional and cultural” indicates an efficient human capital; even so, the management should consider giving more attention to the low performance indicators under this value driver.

Core competence impacts of the UTT-Learn performance competitiveness drivers

The same attention should be given to the other low performance indicators under the regulatory and operational, social and positional competitiveness drivers, to sustain a balanced image of performance for UTT-Learn among the relational, human and structural capitals. Figure 8 illustrates the global weights of the core competence indicators under the three performance competitiveness drivers.

The global weights of the core competence indicators

5. Conclusions

We have developed a theoretical Intellectual Capital Competitiveness Evaluation (ICCE) model. The model introduces organizational performance in terms of a firm's internal capabilities and resources with the strategic intention to understand how these internal resources contribute to creating value for the organization's external environments from stakeholders, customers, and markets. Three main categories of competitive performance drivers have been developed on the basis of the literature on organizations' intangible resources: functional and cultural, regulatory and operational, and social and positional competitiveness. These categories support the organization's management in evaluating and understanding their intellectual capital contributions in response to organizational performance.

The main contribution of this conceptual model is the testing of intellectual capital competitiveness within organizations, to investigate business gaps and set up strategies in alignment with their internal resources and capabilities in order to create competence and value in response to exogenous environments.

Moreover, the ICCE model supports managers by providing a set of measures and indications of their intangible assets' priorities, which avoids any dysfunctional consequences of performance measurement based on individual judgments about the “most important” value driver. By applying AHP analysis, the model identifies separate contributions to competitive performance. By obtaining weights expressing the aggregate importance of the organizational elements, the model provides management with a deep analytical tool with which to assess their organization's capabilities.

In the empirical study presented here, 15 core competence measurement indicators have been suggested. However, a point that must be addressed is that these indicators depend on the environment and sector where the ICCE model is applied. Further studies should be carried out to investigate the interrelationship between organizations' intellectual capital capabilities and their performance contributions in different sectors, in order to ensure the validation of the ICCE model.