Abstract

Health insurance schemes are increasingly recognized as tools to finance health care provision in low-income countries. The main objective of this study was to find out the awareness of and demand for health insurance and to identify those reasons that influence the demand in Jimma town, southwest Ethiopia. We conducted a community-based cross-sectional quantitative study on 741 households from December 1 to December 31, 2012. Data were analyzed using Statistical Package for Social Sciences (SPSS) version 16. Presence of chronic illness in the family was the predictor of the willingness to take part in health insurance. Most of the participants have awareness about insurance, but they did little and/or gave unrelated explanation about health insurance. Only half of the participants (51.5%) wanted to have health insurance. Major reasons for not being willing to participate in health insurance were religious values and beliefs, ability to pay for their health-care cost, and feeling of being unable to pay the premium because of low income.

Introduction

Insurance is a contract that protects the insured from a loss from damage, illness, or death, especially a contract that transfers the risk of a specified loss. 1 American Heritage Concise Dictionary defines it as the equitable transfer of the risk of a loss from one entity to another, in exchange for payment. 2

Health insurance is insurance against the risk of incurring medical expenses among individuals, families, and groups. It protects from the risk of incurring medical expenses by giving chance to participate in several forms of insurance programs. In a country such as Ethiopia where public health care suffers from poor management, poor service quality, and weak finance, development of health insurance is likely to bring improvement in public health care.3–6

If private health insurance covers the service demand of certain percent of population, it will reduce the need for government financing of secondary and tertiary care. This helps a government to have well-targeted health-care financing to serve people who would not have access to private insurance. This in turn helps to address public health priorities such as immunizations that are public goods. 7

Before launching any major health initiative, there ought to be a clear vision of health care for the country, and it should have clear public health policy to realize that vision. Ideally, certain basic health services, including inpatient care, must be available to every member of the society. Patients can pay through insurance if they have health insurance cover or at least have access to health insurance, with government subsidizing insurance premium in full or in part for those who cannot afford it. 8

Health insurance programs are increasingly recognized as tools to finance health care provision in low-income countries. There is high demand from people for quality healthcare services, and there is extreme underutilization of health services in several countries. Therefore, World Health Organization argued that social health insurance may improve access to acceptable quality health care. 9

In 2010, the Federal Ministry of Health of Ethiopia completed the health service financing report to promote healthcare financing and health insurance programs at national, regional, woreda, and health institution levels.10,11

This reform identified health insurance as a technical way to provide another source of revenue and a way to improve the country's low health service use. 12 Cross-sectional studies showed that lack of health insurance compromises access to health service, use of preventive health services, and chronic disease management. 13

Lack of health insurance promotes delay in seeking care and noncompliance with the treatment regime and results in an overall poor health outcome. World Health Organization recommended compulsory health insurance as the best form of health-care financing even though many factors affect clients’ participation.14–16 This study was initiated from personal clinical experience of patients noted being unable to pay for their health care. Similar patients came to the institution for treatment and were seen not being able to pay for medications or admissions. “Self-discharge” because of the inability to afford further treatment costs is seen in the health-care service. The authors believe that health insurance coverage is the main solution for such a barrier to health care. The purpose of this study was to find out how people currently pay for health care services and their familiarity with health insurance. Their demand for health insurance and the reasons contributing to taking part in health insurance among Jimma town community were also the aims of this study.

Methods

Setting

The study was conducted in Jimma town, the capital of Jimma zone in Oromia region, southwest Ethiopia, which is located 346 km from Addis Ababa. The town has 13 kebeles organized under three districts. According to the Ethiopian Census in 2007, there were 30,016 housing units and 120,960 population. 17 The study period was from December 1 to 31, 2012.

Study design

A community-based cross-sectional design with a quantitative method was employed.

Population

The source population was all household heads or spouses who live in Jimma town. The study population was the sampled 741 household heads or spouses of Jimma town who will participate in the study.

Sample size determination and sampling technique

The sample size to be studied was determined using the Open-Epi calculator. Assumptions included the estimated demand for health insurance at 50%. The initial sample size (379) was doubled since we wanted to study both awareness and demand for health insurance. Selecting a sample size of 758 provided a 100% margin of error.

Sampling technique

Systematic sampling technique was used to select households from randomly selected four (30%) kebeles of the town to include in the study.

Measurements

An adapted English questionnaire was used for data collection. The questionnaire was adapted from the tool developed by Constella Futures. 18 The questionnaire has different subsections including socio-demographic variables, illness episodes, hospitalization, expenses for medical care and treatment, and chronic illness.

Study variables

The independent variables include socio-demographic variables, illness episodes, admission, expense, awareness about health insurance. The dependent variable is demand for health insurance service.

Data collectors

All data collectors and supervisors had bachelor's degree qualification in health-related fields. The total number of data collectors and supervisors was six and three, respectively. Principal investigators gave two-day training for data collectors and supervisors on the objectives of the study and how to interview, how to approach, and how to handle questions.

Data quality control

Data collectors introduced themselves and the purpose of the study to the study participants. The developed questionnaire was adapted from similar studies 18 based on the objective of the study and the context of the study area to assure the content quality of the data. The experts assured the content validity of the questionnaire. Training of data collectors and supervisors and close supervision during data collection were conducted. The questionnaire was also pretested on the pilot area. The quality of the data was also assured through training of data collectors, checking completeness and consistency of filled questionnaire, data clearing, and analysis of the data through proper data analysis methods.

Data analysis

The data were entered into statistical package for social sciences (SPSS) version 16.0. The data were edited and cleaned for inconsistencies and completeness. Descriptive analysis was performed to describe the characteristics of the study participants. Simple logistic regression was done for all variables to find the independent predictors of the demand for health insurance. Multiple logistic regression was done to know the final predictors of the demand from the independent variables. Before using a particular analysis, checking the assumption, nature of the variables, and recoding of the variables were done. Finally, independent variables that had statistically significant association with the dependent variable (P < 0.05) were entered into the final regression model.

Ethical consideration

Ethical clearance was obtained from the ethical clearance committee of College of Public Health and Medical Science of Jimma University. After getting the ethical clearance, written permission was obtained from Jimma town administration, and verbal informed consent was obtained from each study participant.

Results

Seven hundred forty-one households were included in the study, making the response rate 98.02%. In the households, there were 2483 family members having a minimum family size of 1 and a maximum of 10, with a mean family size of 3.4 (Table 1).

Distribution of respondents by their illness episodes and ways of getting health care services, Jimma Town, Southwest Ethiopia, December 2012.

1 US$ = 19.83 birr,

epilepsy, renal problems, bone problems.

Illness episodes and ways of getting health-care services

Three hundred sixty-six (22.79%) family members faced a history of illness episode within the last two years. Among these, 39 of the illness episodes were reported as very serious illnesses (Table 1).

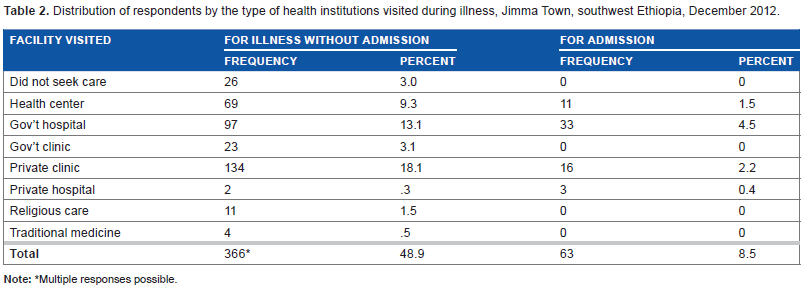

Respondents mostly visited private clinics for treatment during illnesses followed by more visits to government hospitals and health centers (Table 2). Among the 26 individuals who did not seek treatment, 17 (65.4%) did not seek treatment because of having no money to pay for the treatment. Other reasons were inability to obtain permission from work and illness that was not too serious (Table 1).

Distribution of respondents by the type of health institutions visited during illness, Jimma Town, southwest Ethiopia, December 2012.

Multiple responses possible.

Among the study households who faced illness episodes, 52 households (14.2%) practiced self-treatment at home and 68 (18.6%) households got treatment at places other than where they were treated for illnesses without admission. Six (1.6%) of the households prefer other admission health care institutions for health care treatment. The average cost for health service in this study is 441.8 birr with a standard deviation of 1004.3, minimum 10 and maximum of 6850.00 birr. The maximum quantile of health expenses started at an amount of 300 birr. This suggests that more than 80% of the households pay a cost of less than 300 birr for their health care (Table 1). More than two-thirds of the households in the study (68.97%) took treatment for different chronic illnesses. Chronic illnesses in this study include diabetes mellitus, hypertension, heart diseases, tuberculosis, asthma, and other related diseases.

From the study, 122 (16.5%) households have at least one family member affected by chronic illnesses, and 80 (10.8%) of them get treatment for it. Thirty three (91.7%) of the 36 respondents gave reasons for not getting treatment for the illnesses as: feel the disease is not too serious, 21; unable to afford, 10; and the service not available, 2. Eighteen of the respondents who got treatment for chronic illnesses did not pay for the service whereas the rest paid money ranging from 100 birr to 4500 birr (Table 1). Two hundred sixty-three (90.7%) of those who seek treatment paid the cost of their health-care service from their own money (Table 3).

Distribution of respondents by their ways of payment for illness and hospitalization costs, Jimma Town, Southwest Ethiopia, December 2012.

Awareness and demand for health insurance service

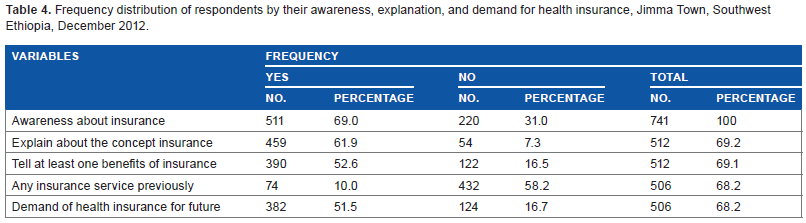

Five hundred eleven participants (68.9%) replied that they have awareness about insurance, and 459 (89.8%) of them tried to explain what insurance is. Three hundred ninety respondents (76.3%) described about the benefits of having health insurance. Seventy four participants (14.5%) responded that they were benefiting from any health insurance services. Three hundred eighty-two participants (51.5%) needed to have health insurance, from which 362 (93.97%) participants wanted health insurance for every health-care service. The rest 20 (6.03%) needed health insurance for only health services during admission (Table 4).

Frequency distribution of respondents by their awareness, explanation, and demand for health insurance, Jimma Town, Southwest Ethiopia, December 2012.

Majority of the respondents (321, 84.03%) who needed the service wanted to pay their premium as a percentage of annual income. The rest 64 (15.97%) wanted to participate by paying a fixed amount of money every time regardless of the annual income. One hundred eight respondents explained why they do not want to have health insurance.

Sex and educational status of the head of the household, expenses for treatment, age of the affected family member, and presence of chronic illnesses in the household were among the independent predictors of demand for health insurance. But only age of the person affected by chronic illness is the final predictor of the demand (AOR = 0.964, 95% CI = [0.924,0.999]) among respondents (Table 5).

Multiple logistic regression result for predictors of demand for health insurance among the community of Jimma Town, Southwest Ethiopia, December 2012.

Reference category; pseudo R2 (Cox & Snell R square = 0.465, Nagelkerke R square = 0.682).

Indicates significance level at P < 0.05.

The thematic areas of reasons for not demanding health insurance were: feeling of being healthy; religious beliefs and values; able to afford any payment for health care; unable to pay “premium”; and little information, not able to trust service, it is difficult to start the service.

The thematic analysis of the reasons for not demanding health insurance showed misunderstanding about health insurance among those who responded as having awareness. For instance, some of the respondents said that they do not need health insurance because they feel healthy and/or there is no ill person in their family.

Other respondents did not want health insurance because they have understanding that getting the service by participation in health insurance is taken as a sin by their religious view. They replied that if they get such service it is considered as taking someone's money for self–-which is forbidden.

A significant number of respondents said that their reason for not demanding health insurance is that they have the ability or financial strength to pay health-care cost for their family. Added reason was the limited ability to pay to get the service.

Discussion

More than two-thirds of the respondents (69%) said that they have awareness about insurance. Nearly 9 out of 10 (89.8%) of those who responded as having awareness gave their own explanation about health insurance. Their explanation suggests that even though more than two-thirds of the participants said that they have awareness about health insurance, their awareness is about insurance for properties like car instead of about covering expenses during illness.

Nine out of ten (90.7%) of those who seek treatment paid the cost of their health-care service from their own money. This shows that most of the study community prefers to get treatment by paying from their own money instead of using alternatives like borrowing from employers, friends, or relatives. About 80% of the participants who paid for the healthcare service of their family paid 300 birr and lower. This shows that if the payment is higher than their capacity to pay, either they may not seek or they may stop continuing their health-care benefit instead of finding other ways of payment (sources). This will have great implication on health-seeking practice and continuity of care for the people.

The result also showed that about 30% of the respondents had no awareness about health insurance. This shows that they are new to the service and benefits.

More than half of the respondents (52.6%) told at least one benefit of health insurance. And like that of their explanation, the benefit most of them described related to replacing lost or damaged property.19–21

Half of the respondents (51.5%) responded that they want to have health insurance. This shows that with having the awareness of insurance related to replacing lost or damaged properties, they feel that health insurance is important. This shows that if the government or any private body starts health insurance service for this study community, more than half of the community will be part of the service. It will be an input to meet one of the health care reform parts that promote health-care financing and improving the low health service utilization.11,12,22

The study showed that nearly half of the study participants either had no awareness about health insurance or they did not want to have health insurance for different reasons. This will drastically affect the health-seeking practice of the population. 23 The study also showed that a few respondents have understanding of participation in health insurance is only during illness. Therefore, giving more information will help the community members to benefit from the service.

The feeling of having the financial strength to pay the health-care cost showed that these respondents had no awareness about one of the main benefits of health insurance, which is sharing of risks. Here, even though people can pay for their health care, if they participate in health insurance, the amount they pay for the service will decrease significantly. On the other hand, inability to pay for the service showed that the insurer should subsidize in full or in part at least for basic health services for the poor part of the community.8,13,16

The way respondents wanted to participate in the service, that is, their preference in the area of coverage for the insurance showed that paying money (premium) proportional to annual or monthly salary is convenient for many potential customers. This is also important for involving different parts of the population with different income levels; members of a community with high income and low income can participate in the service equally. This in turn will help to share the health risk of the community equally.10,24–26 Even though paying money proportional to income is convenient for majority, paying a fixed amount of money is also convenient for some part of the population.

Limitation of the study

Recall bias on money paid for health care and illness episode in the family.

Conclusions

More than two-thirds of the participants reported that they have awareness about insurance, but their explanation about insurance showed that the respondents did not have a clear concept of health insurance and its benefits. Nearly one-fourth reported that they had no awareness about insurance and its benefits. About half of the participants described at least one benefit of insurance. Most of them described its importance about replacing lost or damaged property, not as helping to pay during illness or for any health-care service.

More than 9 out of 10 participants reported that they paid their health-care cost from their own money. Half of the participants wanted to have health insurance, and majority of them wanted to participate by paying their premium as a percentage of their monthly or annual income. Others wanted to get the service by paying a fixed amount of money regularly regardless of their income. Major reasons for not demanding insurance were religious values and beliefs, feeling of being healthy, financial capacity to pay for the health care of family, and feeling of being unable to pay the premium because of poor income.

Awareness creation program about health insurance and its benefits should be given to the community. Health insurance should be taken as a main way of paying for health expenses for the community. Since most participants pay from their own money, if they are unable to pay for the service, they may delay or stop health-seeking practice.

Different types of health insurances with different ways of participation (paying percentages of annual income and fixed amount of money) are based on their preference and their ways of getting their income. For employees, priority can be given to paying a percentage of their salary, whereas for people whose life depends on trade and other businesses, paying a fixed amount of money regularly should be considered. Health insurance services should consider including community members who cannot pay for the service by subsidizing the insurance premium in full or in part.

Further research on how religious values and beliefs affect the demand and utilization of health insurance services should be conducted.

Author Contributions

Produced and designed the research concept and methods: AM, NF. Trained data collectors and supervisors: AM, NF. Performed data analysis: AM, NF. Wrote the final report: AM. Wrote the first draft of the manuscript: AM, NF. Agree with manuscript results and conclusions: AM, NF. Jointly developed the structure and arguments for the paper: AM, NF. Made critical revisions: AM, NF. All authors reviewed and approved of the final manuscript.

Footnotes

Acknowledgments

We would like to thank Jimma University for funding this research, the statistics office and administration of Jimma town for their cooperation in getting information of the total number of households in Jimma town. Finally, we thank the data collectors, supervisors, and study participants for their cooperation.