Abstract

Three years ago Nauru would probably have ranked dead last on a list of “Nations Most Threatening to Global Security.” A tiny (eight-square-mile) island just south of the Marshalls in the Pacific Ocean, Nauru had no military and was of little consequence to anyone but its own 10,000 citizens. It didn't even need development assistance—massive phosphate deposits had made it one of the wealthiest nations in the world on a per capita basis.

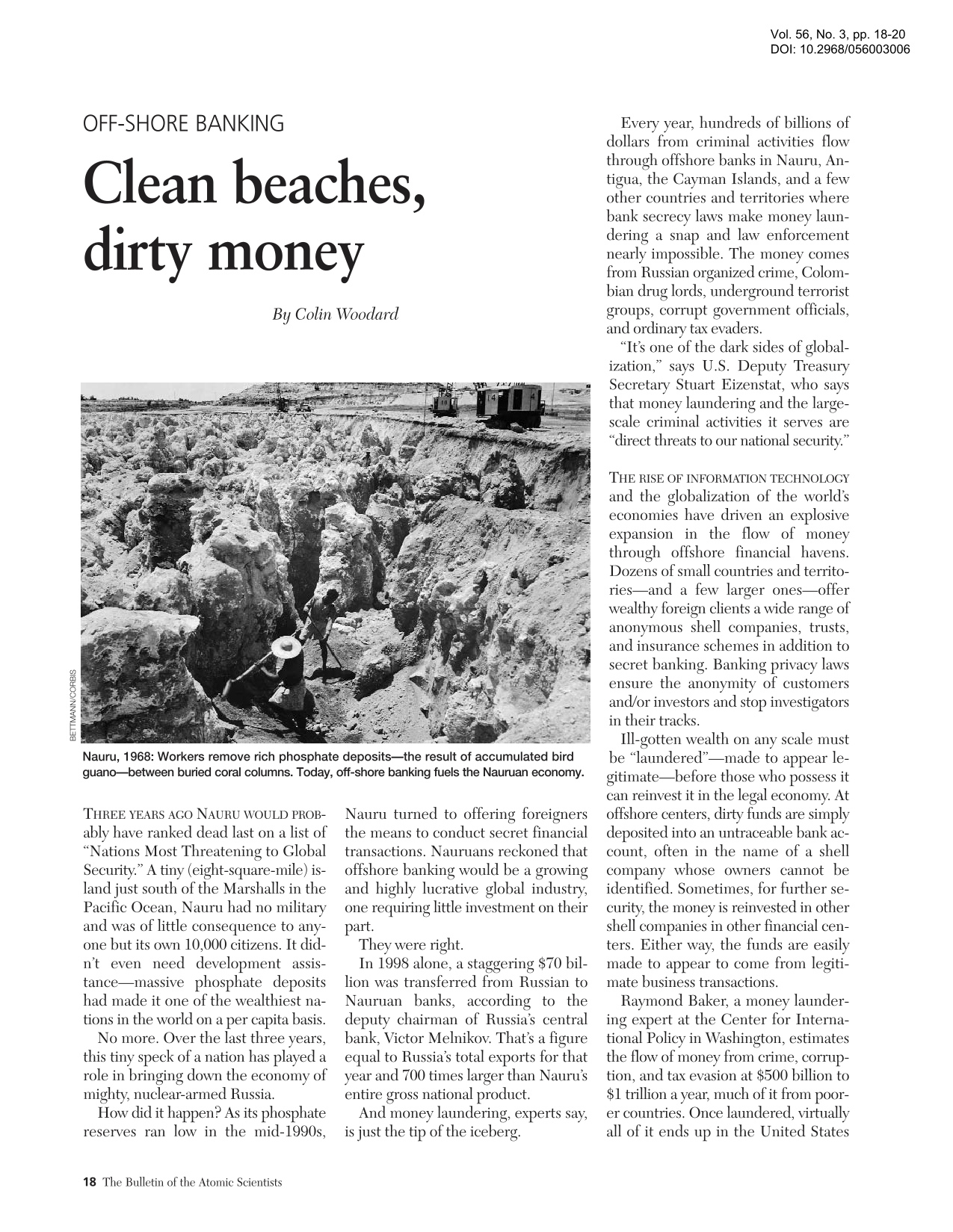

Nauru, 1968: Workers remove rich phosphate deposits—the result of accumulated bird guano—between buried coral columns. Today, off-shore banking fuels the Nauruan economy.

No more. Over the last three years, this tiny speck of a nation has played a role in bringing down the economy of mighty, nuclear-armed Russia.

How did it happen? As its phosphate reserves ran low in the mid-1990s, Nauru turned to offering foreigners the means to conduct secret financial transactions. Nauruans reckoned that offshore banking would be a growing and highly lucrative global industry, one requiring little investment on their part.

They were right.

In 1998 alone, a staggering $70 billion was transferred from Russian to Nauruan banks, according to the deputy chairman of Russia's central bank, Victor Melnikov. That's a figure equal to Russia's total exports for that year and 700 times larger than Nauru's entire gross national product.

And money laundering, experts say, is just the tip of the iceberg.

Every year, hundreds of billions of dollars from criminal activities flow through offshore banks in Nauru, Antigua, the Cayman Islands, and a few other countries and territories where bank secrecy laws make money laundering a snap and law enforcement nearly impossible. The money comes from Russian organized crime, Colombian drug lords, underground terrorist groups, corrupt government officials, and ordinary tax evaders.

“It's one of the dark sides of globalization,” says U.S. Deputy Treasury Secretary Stuart Eizenstat, who says that money laundering and the large-scale criminal activities it serves are “direct threats to our national security.”

The rise of information technology and the globalization of the world's economies have driven an explosive expansion in the flow of money through offshore financial havens. Dozens of small countries and territo-ries—and a few larger ones—offer wealthy foreign clients a wide range of anonymous shell companies, trusts, and insurance schemes in addition to secret banking. Banking privacy laws ensure the anonymity of customers and/or investors and stop investigators in their tracks.

Ill-gotten wealth on any scale must be “laundered”—made to appear legitimate—before those who possess it can reinvest it in the legal economy. At offshore centers, dirty funds are simply deposited into an untraceable bank account, often in the name of a shell company whose owners cannot be identified. Sometimes, for further security, the money is reinvested in other shell companies in other financial centers. Either way, the funds are easily made to appear to come from legitimate business transactions.

Raymond Baker, a money laundering expert at the Center for International Policy in Washington, estimates the flow of money from crime, corruption, and tax evasion at $500 billion to $1 trillion a year, much of it from poorer countries. Once laundered, virtually all of it ends up in the United States and Western Europe, whose bankers often turn a blind eye to suspicious money.

“Some bankers say ‘If we don't take it others will,’” Baker says. “I'd like to see us first drive that money from U.S. shores and then from foreign shores after that.”

Russia's economic collapse was assisted in no small part by the theft of an estimated $150 to $350 billion over the past decade. And by facilitating the massive theft of wealth and resources from the developing world as well, offshore financial centers are contributing to international instability. Washington attorney and money laundering expert Jack Blum calls the Russian case “the greatest single theft of a country's resources in the history of the world.”

“All of this has been done by moving money out of the country and through the offshore world,” Blum says.

U.S. banking giants are not completely innocent. In order to compete with offshore centers, many U.S. banks now have “private banking” divisions, which provide customers with a personal banker and strict confidentiality. Minimum opening deposits are typically in the $1 million range.

In November, congressional investigators revealed that Citibank, the largest bank in the United States, helped several corrupt foreign clients hide their ill-gotten fortunes through accounts at its private banking division. Raúl Salinas, the brother of the former president of Mexico—now in prison for murder—moved more than $87 million through Citibank, which allegedly helped conceal his identity. Omar Bongo, the president of Ga-bon—now under investigation for bribery—transferred $130 million through private bank accounts at Citibank; the sons of Nigerian dictator Gen. Sani Abacha moved $110 million.

Citibank earned sizeable commissions for its services—and it may not have broken any laws. Surprisingly, it is not a crime for banks to knowingly accept money that is the result of foreign corruption.

“We can't condemn corruption abroad—be it officials taking bribes or looting their treasuries—and then tolerate American banks making fortunes off that corruption,” says Democratic Sen. Carl Levin of Michigan, who led the investigation. “America can't have it both ways.”

This case, and a multi-billion-dollar scandal involving Russian funds moved through the Bank of New York, are drawing attention to the U.S. side of the problem. Several anti-money laundering bills recently introduced in Congress would require banks to verify the identity and financial background of private banking customers and criminalize the knowing acceptance of corrupt foreign funds. Sources on Capitol Hill expect Congress to take action on the issue this year.

Getting other governments to adopt similar standards will be more difficult. For many small countries, harboring foreign wealth is big business.

The Cayman Islands, a tiny British dependency of 32,000 in the western Caribbean, is now the fifth largest financial center in the world, with money flowing through its banks in volumes similar to those in New York, London, and Frankfurt. Its three tiny islands are home to 590 banks and 30,000 companies, most little more than a brass plate outside a lawyer's office. Their presence has helped give the Caymans a higher standard of living than that of Britain itself.

Facing declining banana and tourism earnings, the eastern Caribbean island of Dominica (population 83,000) has incorporated five offshore banks, 4,600 international business corporations, and five Internet gambling enterprises since 1996. Its government earned at least $3.6 million from financial activities in 1997, according to a State Department report. It also sells “economic citizenship” in exchange for a $50,000 local deposit—an offer seized upon by hundreds of Russians. Similarly, the economy of the Bahamas benefits from the presence of 70,000 international corporations, 400 offshore banks, 97 trust companies, and 62 insurance companies.

But things may be changing. U.S. officials are working with 28 other members of the OECD (Organisation for Economic Cooperation and Development) based Financial Action Task Force Against Money Laundering to standardize financial practices and pressure offshore centers to comply with them. The International Monetary Fund and the World Bank have put corruption and money laundering high on their agendas.

And there are early signs of progress. In December, Bankers Trust and Deutsche Bank, which together operate a key global money transfer system, banned all U.S. dollar payments to banks in Nauru and two other Pacific Ocean countries suspected of money laundering.

Under pressure from London, the Cayman Islands has introduced “know your customer” regulations and increased bank supervision, although companies still do not have to identify their owners or directors. Britain is also considering a tightening of regulations in two other British offshore havens, the Isle of Man and the Channel Islands.

In March, the Clinton administration asked Congress to pass legislation that would give the Treasury Department the power to simply cut offshore centers off from the U.S. banking system.

“There's terrific pressure building on the offshore centers” from the United States and some European countries, says attorney Blum. “If that's coupled with similar kinds of action in other parts of the world, the offshore centers will have no alternative but to change their practices.”