Abstract

Behavioral science has witnessed an explosion in the number of biases identified by behavioral scientists, to more than 200 at present. This article identifies the 10 most important behavioral biases for project management. First, we argue it is a mistake to equate behavioral bias with cognitive bias, as is common. Cognitive bias is half the story; political bias the other half. Second, we list the top 10 behavioral biases in project management: (1) strategic misrepresentation, (2) optimism bias, (3) uniqueness bias, (4) the planning fallacy, (5) overconfidence bias, (6) hindsight bias, (7) availability bias, (8) the base rate fallacy, (9) anchoring, and (10) escalation of commitment. Each bias is defined, and its impacts on project management are explained, with examples. Third, base rate neglect is identified as a primary reason that projects underperform. This is supported by presentation of the most comprehensive set of base rates that exist in project management scholarship, from 2,062 projects. Finally, recent findings of power law outcomes in project performance are identified as a possible first stage in discovering a general theory of project management, with more fundamental and more scientific explanations of project outcomes than found in conventional theory.

Keywords

Introduction

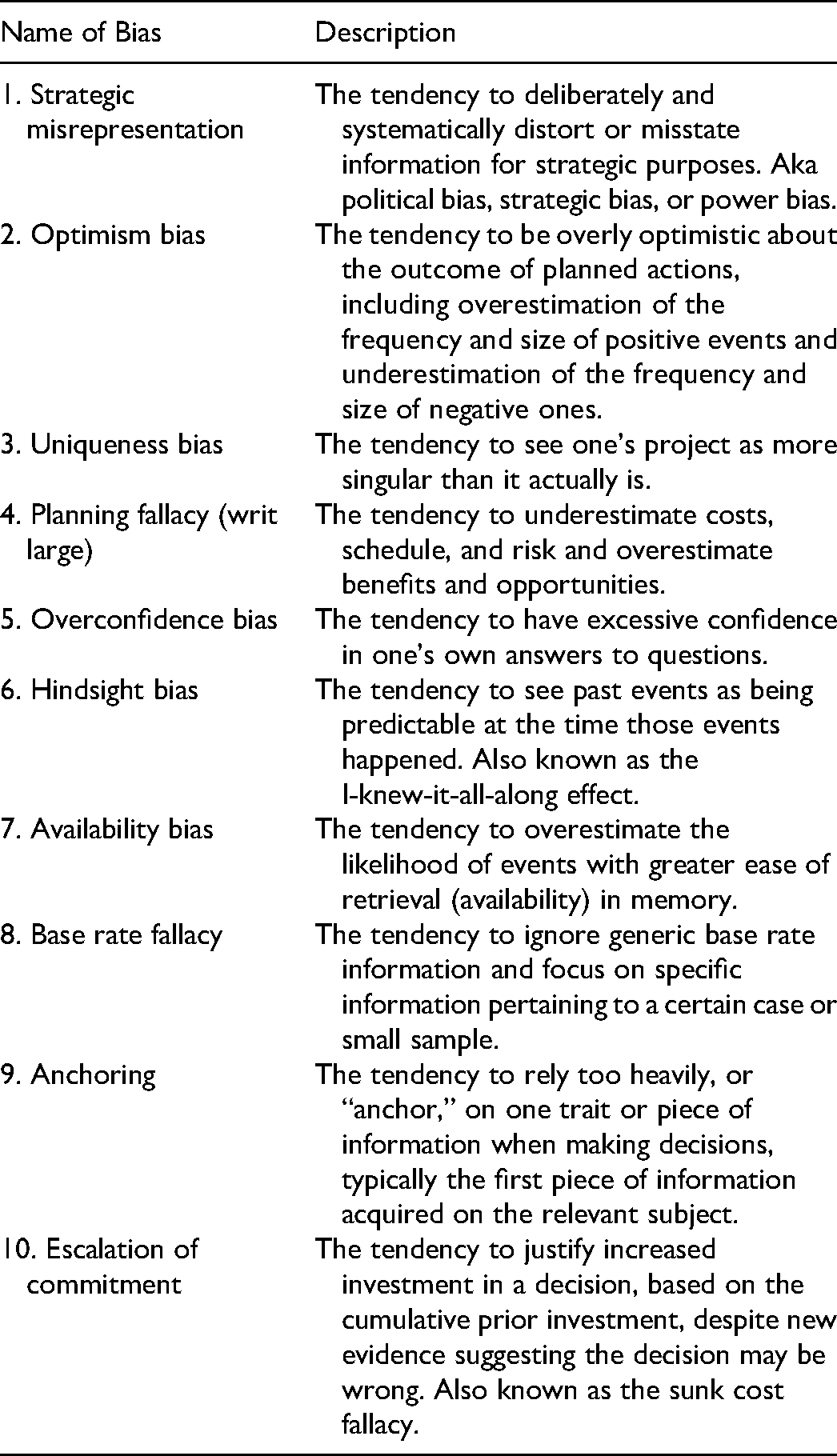

Since the early work of Tversky and Kahneman (1974), the number of biases identified by behavioral scientists has exploded in what has been termed a behavioral revolution in economics, management, and across the social and human sciences. Today, Wikipedia's list of cognitive biases contains more than 200 items (“List of cognitive biases,” 2021). The present article gives an overview of the most important behavioral biases in project planning and management, summarized in Table 1. They are the biases most likely to trip up project planners and managers and negatively impact project outcomes, if the biases are not identified and dealt with up front and during delivery.

Top 10 Behavioral Biases in Project Planning and Management

Many would agree with Kahneman (2011, p. 255) that optimism bias “may well be the most significant of the cognitive biases.” However, behavioral biases are not limited to cognitive biases, though behavioral scientists, and especially behavioral economists, often seem to think so. For instance, in his history of behavioral economics, Nobel laureate Richard Thaler (2015, p. 261) defines what he calls “the real point of behavioral economics” as “to highlight behaviors that are in conflict with the standard rational model.” But, nothing in this definition limits the object of behavioral economics to cognitive bias. Other types of bias, for example, political bias, also conflict with the standard rational model, although you would never know this from reading Thaler's (2015) history of the field. Thaler (2015, p. 357) speaks of “the unrealism of hyperrational models,” and we agree. But, behavioral economics itself suffers from such unrealism, because it ignores that many behavioral phenomena are better explained by political bias than by cognitive bias.

In short, behavioral economics in its present form suffer from an overfocus on cognitive psychology: Economic decisions get overaccounted for in psychological terms, when other perspectives—for instance political, sociological, and organizational—may be more pertinent. If all you have is a hammer, everything looks like a nail. Similarly, if all you have is psychology, everything gets diagnosed as a psychological problem, even when it is not. Behavioral economics suffers from a “psychology bias,” in this sense. Cognitive bias is only half the story in behavioral science. Political bias is the other half.

Political bias—understood as deliberate strategic distortions—arises from power relations, instead of from cognition, and has long been the object of study in political economy. Political bias is particularly important for big, consequential decisions and projects, which are often subject to high political–organizational pressures. In fact, for very large projects—so-called megaprojects—the most significant behavioral bias is arguably political bias, more specifically, strategic misrepresentation (Flyvbjerg et al., 2002; Flyvbjerg et al., 2018; Wachs, 2013). Cognitive bias may account well for outcomes in the simple lab experiments done by behavioral scientists. But for real-world decision-making—in big hierarchical organizations, involving office politics, salesmanship, jockeying for position and funds, including in the C-suite and ministerial offices, with millions and sometimes billions of dollars at stake—political bias is pervasive and must be taken into account. Or so I argue.

It should be emphasized again that many other behavioral biases exist than those mentioned in Table 1, which are relevant to project planning and management, for example, illusion of control, conservatism bias, normalcy bias, recency bias, probability neglect, the cost–benefit fallacy, the ostrich effect, and more. But, the 10 mentioned here may be considered the most important, and, in this sense, they are deemed to be the most common biases with the most direct impact on project outcomes.

Discussions With Kahneman

My first opportunity to reflect systematically on the relationship between political and cognitive bias was an invitation in 2003 from the editor of Harvard Business Review (HBR) to comment on an article by Lovallo and Kahneman (2003). The year before, Kahneman had won the Nobel Prize in Economics for his path-breaking work with Amos Tversky (who died in 1996) on heuristics and biases in decision-making, including optimism bias, which was the topic of the HBR article. The editor explained to me that he saw Kahneman and me as explaining the same phenomena—cost overruns, delays, and benefit shortfalls in investment decisions—but with fundamentally different theories. As a psychologist, Kahneman explained outcomes in terms of cognitive bias, especially optimism bias and the planning fallacy. As an economic geographer, I explained the same phenomena in terms of political economic bias, specifically strategic misrepresentation. So which of the two theories is right, asked the HBR editor?

The editor's question resulted in a spirited debate in the pages of HBR. I commented on the article by Kahneman and Lovallo (2003) that they,

“underrate one source of bias in forecasting—the deliberate ‘cooking’ of forecasts to get ventures started. My colleagues and I call this the Machiavelli factor. The authors [Kahneman and Lovallo] mention the organizational pressures forecasters face to exaggerate potential business results. But adjusting forecasts because of such pressures can hardly be called optimism or a fallacy; deliberate deception is a more accurate term. Consequently, Lovallo and Kahneman's analysis of the planning fallacy seems valid mainly when political pressures are insignificant. When organizational pressures are significant, both the causes and cures for rosy forecasts will be different from those described by the authors” (Flyvbjerg, 2003, p. 121).

Kahneman and Lovallo (2003, p. 122) responded: “Flyvbjerg and his colleagues reject optimism as a primary cause of cost overruns because of the consistency of the overruns over a significant time period. They assume that people, particularly experts, should learn not only from their mistakes but also from others’ mistakes. This assumption can be challenged on a number of grounds.”

Ultimately, the HBR debate did not so much resolve the question as clarify it and demonstrate its relevance. Kahneman and I therefore continued the discussion offline. Others have commented on Kahneman's generosity in academic interactions. He invited me to visit him at home, first in Paris and later in New York, to develop the thinking on political and cognitive bias and how they may be interrelated. He was more rigorous than anyone I'd discussed bias with before, and I found the discussions highly productive.

In addition to being generous, Kahneman is deeply curious and empirical. Based on our discussions, he decided he wanted to investigate political bias firsthand and asked if I could arrange for him to meet people exposed to such bias. I facilitated an interview with senior officials I knew at the Regional Plan Association of the New York-New Jersey-Connecticut metropolitan (tristate) area, with offices near Kahneman's home in New York. Their work includes forecasting and decision-making for major infrastructure investments in the tristate region, which are among the largest, the most expensive, and most complex in the world. They were the types of projects I studied to develop my theories of strategic misrepresentation. Decision-making on such projects is a far cry from the lab experiments used by Kahneman and other behavioral scientists to document classic cognitive biases like loss aversion, anchoring, optimism, and the planning fallacy.

When Kahneman and I compared notes again, we agreed the balanced position regarding real-world decision-making is that both cognitive and political biases influence outcomes. Sometimes one dominates, sometimes the other, depending on what the stakes are and the degree of political-organizational pressures on individuals. If the stakes are low and political-organizational pressures are absent, which is typical for lab experiments in behavioral science, then cognitive bias will dominate, and such bias will be what you find. But if the stakes and pressures are high—for instance, when deciding whether to spend billions of dollars on a new subway line in Manhattan—political bias and strategic misrepresentation are likely to dominate and will be what you uncover, together with cognitive bias, which is hardwired and therefore present in most, if not all, situations.

Imagine a scale for measuring political-organizational pressures, from weak to strong. At the lower end of the scale, one would expect optimism bias to have more explanatory power of outcomes relative to strategic misrepresentation. But with more political-organizational pressures, outcomes would increasingly be explained in terms of strategic misrepresentation. Optimism bias would not be absent when political-organizational pressures increase, but optimism bias would be supplemented and reinforced by bias caused by strategic misrepresentation. Finally, at the upper end of the scale, with strong political-organizational pressures—for example, the situation where a chief executive officer or minister must have a certain project—one would expect strategic misrepresentation to have more explanatory power relative to optimism bias, again without optimism bias being absent. Big projects, whether in business or government, are typically at the upper end of the scale, with high political-organizational pressures and strategic misrepresentation. The typical project in the typical organization is somewhere in the middle of the scale, exposed to a mix of strategic misrepresentation and optimism bias, where it is not always clear which one is stronger.

The discussions with Kahneman taught me that although I had fully acknowledged the existence of cognitive bias in my initial work on bias (Flyvbjerg et al., 2002), I needed to emphasize cognition more to get the balance right between political and psychological biases in real-life decision-making. This was the object of later publications (Flyvbjerg, 2006; Flyvbjerg, 2013; Flyvbjerg et al., 2004; Flyvbjerg et al., 2009; Flyvbjerg et al., 2016). More importantly, however, in our discussions and in a relatively obscure article by Kahneman and Tversky (1979a), I found an idea for how to eliminate or reduce both cognitive and political biases in decision-making. I developed this into a practical tool called “reference class forecasting” (Flyvbjerg, 2006). In Thinking, Fast and Slow, Kahneman (2011, p. 251) was kind enough to endorse the method as an effective tool for bringing the outside view to bear on projects in order to debias them.

Finally, it has been encouraging to see Kahneman begin to mention political bias in his writings, including in his seminal book, Thinking, Fast and Slow, where he explicitly points out that,

“Errors in the initial budget are not always innocent. The authors of unrealistic plans are often driven by the desire to get the plan approved—whether by their superiors or by a client—supported by the knowledge that projects are rarely abandoned unfinished merely because of overruns in costs or completion times” (Kahneman, 2011, pp. 250–251).

That is clearly not a description of cognitive bias, which is innocent per definition, but of political bias, specifically strategic misrepresentation aimed at getting projects underway. As such, it contrasts with other behavioral economists, for instance, Thaler (2015) who leaves political bias unmentioned in his bestselling history of behavioral economics.

Most likely, none of the above would have happened without the HBR editor's simple question, “Strategic misrepresentation or optimism bias, which is it?” The discussions with Kahneman proved the answer to be: “Both.”

We use this insight below to describe the most important behavioral biases in project planning and management, starting with strategic misrepresentation, followed by optimism bias and eight other biases.

Strategic Misrepresentation

Strategic misrepresentation is the tendency to deliberately and systematically distort or misstate information for strategic purposes (Jones & Euske, 1991; Steinel & De Dreu, 2004). This bias is sometimes also called political bias, strategic bias, power bias, or the Machiavelli factor (Guinote & Vescio, 2010). The bias is a rationalization where the ends justify the means. The strategy (e.g., achieve funding) dictates the bias (e.g., make projects look good on paper). Strategic misrepresentation can be traced to agency problems and political-organizational pressures, for instance, competition for scarce funds or jockeying for position. Strategic misrepresentation is deliberate deception, and as such, it is lying, per definition (Bok, 1999; Carson, 2006; Fallis, 2009).

Here, a senior Big-Four consultant explains how strategic misrepresentation works in practice: “In the early days of building my transport economics and policy group at [name of company omitted], I carried out a lot of feasibility studies in a subcontractor role to engineers. In virtually all cases it was clear that the engineers simply wanted to justify the project and were looking to the traffic forecasts to help in the process … I once asked an engineer why their cost estimates were invariably underestimated and he simply answered ‘if we gave the true expected outcome costs nothing would be built’” (personal communication, author's archives, italics added).

Signature architecture is notorious for large cost overruns. A leading signature architect, France's Jean Nouvel, winner of the Pritzker Architecture Prize, explains how it works: “I don’t know of buildings that cost less when they were completed than they did at the outset. In France, there is often a theoretical budget that is given because it is the sum that politically has been released to do something. In three out of four cases this sum does not correspond to anything in technical terms. This is a budget that was made because it could be accepted politically. The real price comes later. The politicians make the real price public where they want and when they want” (Nouvel, 2009, p. 4, italics added).

This is strategic misrepresentation. Following its playbook, a strategic cost or schedule estimate will be low, because it is more easily accepted, leading to cost and schedule overruns later. Similarly, a strategic benefit estimate will be high, leading to benefit shortfalls. Strategic misrepresentation therefore produces a systematic bias in outcomes. And, this is precisely what the data show (see Table 2). We see the theory of strategic misrepresentation fits the data well. Explanations of project outcomes in terms of strategic misrepresentation have been set forth by Wachs (1989, 1990, 2013), Kain (1990), Pickrell (1992), Flyvbjerg et al. (2002, 2004, 2005, 2009), and Feynman (2007a, 2007b) among others.

Strategic misrepresentation will be particularly strong where political-organizational pressures are high, as argued above, and such pressures are especially high for big, strategic projects. The bigger and more expensive the project, the more strategic import it is likely to have with more attention from top management and with more opportunities for political-organizational pressures to develop, other things being equal. For project planning and management, the following propositions apply:

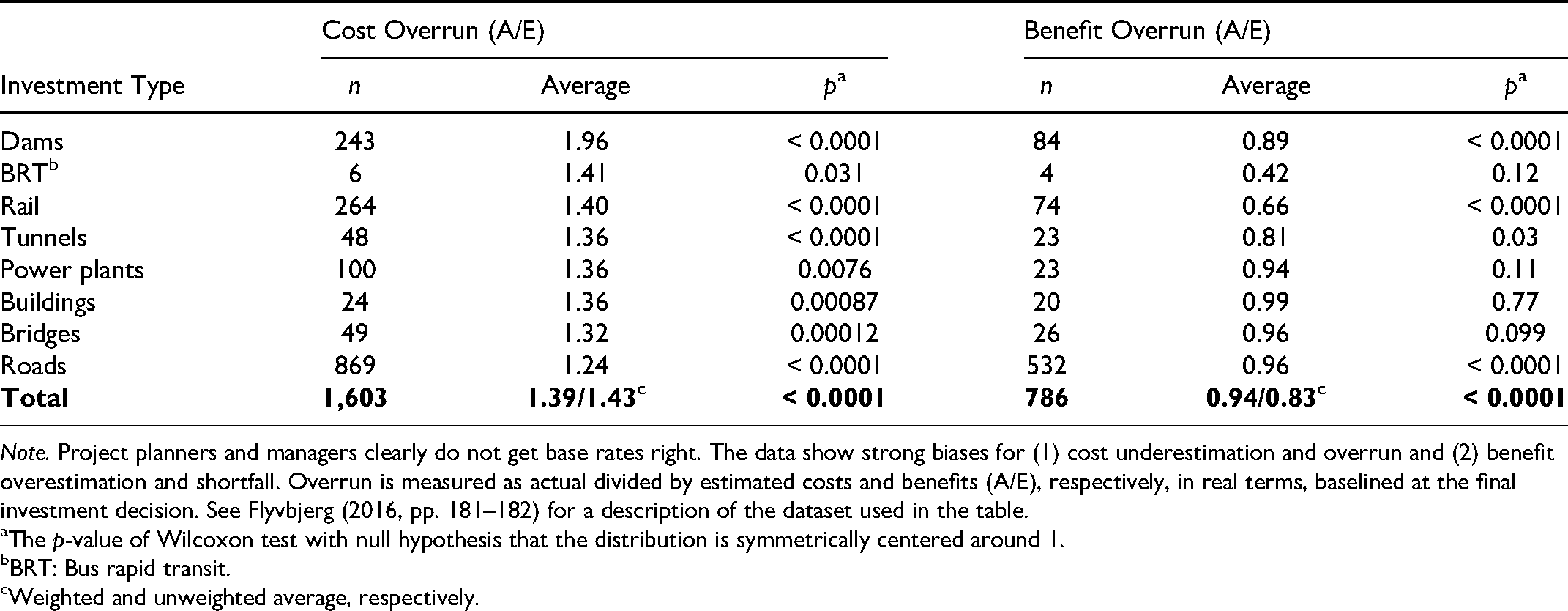

Base Rates for Cost and Benefit Overrun in 2,062 Capital Investment Projects Across Eight Types

Note. Project planners and managers clearly do not get base rates right. The data show strong biases for (1) cost underestimation and overrun and (2) benefit overestimation and shortfall. Overrun is measured as actual divided by estimated costs and benefits (A/E), respectively, in real terms, baselined at the final investment decision. See Flyvbjerg (2016, pp. 181–182) for a description of the dataset used in the table.

The p-value of Wilcoxon test with null hypothesis that the distribution is symmetrically centered around 1.

BRT: Bus rapid transit.

Weighted and unweighted average, respectively.

Proposition 1: For small projects, with low strategic import and no attention from top management, bias, if present, is likely to originate mainly with cognitive bias, for example, optimism bias.

Proposition 2: For big projects, with high strategic import and ample attention from top management, bias, if present, is likely to originate mainly with political bias, for example, strategic misrepresentation, although cognitive bias is also likely to be present.

Strategic misrepresentation has proved especially important in explaining megaproject outcomes. For megaproject management, strategic misrepresentation may be expected to be the dominant bias (Flyvbjerg, 2014).

Professor Martin Wachs of UC Berkeley and UCLA, who pioneered research on strategic misrepresentation in transportation infrastructure forecasting, recently looked back at more than 25 years of scholarship in the area. After carefully weighing the evidence for and against different types of explanations of forecasting inaccuracy, Wachs summarized his findings in the following manner: “While some scholars believe this [misleading forecasting] is a simple technical matter involving the tools and techniques of cost estimation and patronage forecasting, there is growing evidence that the gaps between forecasts and outcomes are the results of deliberate misrepresentation and thus amount to a collective failure of professional ethics … Often … firms making the forecasts stand to benefit if a decision is made to proceed with the project” (Wachs, 2013, p. 112).

Wachs found a general incentive to misrepresent forecasts for infrastructure projects and that this incentive drives forecasting outcomes. Wachs's review and the studies cited above falsify the notion that optimism and other cognitive biases may serve as a stand-alone explanation of cost underestimation and benefit overestimation, which has been the common view in behavioral economics. Explanations in terms of cognitive bias are especially wanting in situations with high political and organizational pressures. In such situations, forecasters, planners, and decision makers intentionally use the following Machiavellian formula to make their projects look good on paper, with a view to securing their approval and funding:

Finally, recent research has found that not only do political and cognitive biases compound each other in the manner described above. Experimental psychologists have shown that political bias directly amplifies cognitive bias in the sense that people who are powerful are affected more strongly by various cognitive biases—for example, availability bias and recency bias—than people who are not (Weick & Guinote, 2008). A heightened sense of power also increases individuals’ optimism in viewing risks and their propensity to engage in risky behavior (Anderson & Galinsky, 2006, p. 529). This is because people in power tend to disregard the rigors of deliberate rationality, which are too slow and cumbersome for their purposes. They prefer—consciously or not—subjective experience and intuitive judgment as the basis for their decisions, as documented by Flyvbjerg (1998, p. 69 ff.), who found that people in power will deliberately exclude experts from meetings when much is at stake, in order to avoid clashes in high-level negotiations between people in power's intuitive decisions and experts’ deliberative rationality. Guinote and Vescio (2010) similarly found that people in power rely on ease of retrieval more than people without power. In consequence, total bias—political plus cognitive—escalates, but not in a simple linear manner where total bias equals the sum of political and cognitive biases but instead in a complex, convex way where political bias amplifies cognitive bias, leading to convex risk. This, undoubtedly, is one reason we find strong convexities in the planning and management of big projects. Decisions about big projects are typically made by highly powerful people, and such individuals are convexity generators, with political bias driving their cognitive biases, which are larger for powerful individuals than for nonpowerful ones.

Optimism Bias

Optimism bias is a cognitive bias, and it is the tendency for individuals to be overly bullish about the outcomes of planned actions (Kahneman, 2011, p. 255). Sharot (2011, p. xv) calls it “one of the greatest deceptions of which the human mind is capable.” Where strategic misrepresentation is deliberate, optimism bias is nondeliberate. In the grip of optimism, people—including experts—are unaware that they are optimistic. They make decisions based on an ideal vision of the future rather than on a rational weighing of realistic gains, losses, and probabilities. They overestimate benefits and underestimate costs. They involuntarily spin scenarios of success and overlook the potential for mistakes and miscalculations. As a result, plans are unlikely to deliver as expected in terms of benefits and costs.

Almost 100 years ago, when Geoffrey Faber founded what would become Faber & Faber, the renowned London publishing house, he was so certain of his project that he bet his mother's, his own, and a few friends’ fortunes on it, concluding, “ “I find it hard to justify my buoyant self-confidence of last year … I ought, I think, to have foreseen trouble and gone more cautiously” (Faber, 2019, pp. 27–28).

That's optimism bias and what it does to individuals. Geoffrey Faber is not the only entrepreneur to have been tripped up like this. It's typical. What's less typical is that Faber & Faber survived to tell the story. Most companies fail and are forgotten.

Optimism bias can be traced to cognitive biases, in other words, systematic deviations from rationality in the way the mind processes information (O'Sullivan, 2015; Sharot et al., 2007; Shepperd et al., 2002). These biases are thought to be ubiquitous. In project planning and management, an optimistic cost or schedule estimate will be low, leading to cost and schedule overruns. An optimistic benefit estimate will be high, leading to benefit shortfalls. Optimism therefore produces a systematic bias in project outcomes, which is what the data show (see Table 2). The theory of optimism bias thus fits the data well, which lends support to its validity.

Interestingly, however, when researchers ask forecasters about causes of inaccuracies in their forecasts, they do not state optimism bias as a main cause, whereas they do mention strategic misrepresentation and the usual suspects: scope changes, complexity, price changes, unexpected underground conditions, bad weather, and so on (Flyvbjerg et al., 2005, pp. 138–140). Psychologists would argue this is because optimism bias is a true cognitive bias. As such it is unreflected by forecasters, including when they participate in surveys of stated causes of forecasting inaccuracy, which is why such surveys cannot be trusted. Psychologists would further argue there is a large body of experimental evidence for the existence of optimism bias (Buehler et al., 1994, 1997; Newby-Clark et al., 2000). However, the experimental data are mostly from simple laboratory experiments with students. This is a problem, because it is an open question to what extent the results apply outside the laboratory, in real-life situations like project planning and management.

Optimism bias can be both a blessing and a curse. Optimism and a “can-do” attitude are obviously necessary to get projects done. Kahneman (2011, p. 255) calls optimism “the engine of capitalism.” I would go further and call it the engine of life. But, optimism can seriously trip us up if we are unaware of its pitfalls and therefore take on risks we would have avoided had we known the real, nonoptimistic, odds. This has been known and reflected since at least the ancient Greeks. More than two millennia ago, the Greek historian Thucydides (2009, p. 220) said about the Athenians that “they expected no reverses” to “their current good fortune”—in other words, they were optimistic, specifically overconfident—and this caused the fall of Athens in the Peloponnesian War, according to Thucydides.

No upside can compensate for the ultimate downside: death. This is a fundamental asymmetry between upside and downside in human existence and is probably why humans are predisposed to loss aversion, as documented by prospect theory (Kahneman & Tversky, 1979b). Quite simply, it is rational in evolutionary terms to be more concerned about downside than upside. “Death” does not have to be of an individual, needless to say. It can be of a nation, a city, a business, or a project.

In my research, I have found that successful leaders have a rare combination of hyperrealism and can-do optimism (Flyvbjerg & Gardner, 2022). I call such individuals “realistic optimists.” Risto Siilasmaa, chairman of Nokia during its recent successful turnaround, goes one step further in highlighting the two disparate dispositions, when he emphasizes “paranoid optimism” as the key to success in leading projects and businesses, always planning for the worst-case scenario: “The more paranoid we are, the harder we will continue to labor to shift the probability curve in our favor and the more optimistic we can afford to be” (Siilasmaa, 2018, p. xvi). If you are looking for someone to successfully lead a project, this is the type of person you want: a realistic optimist, if not a paranoid one. You would never get on a plane if you overheard the pilot say to the copilot, “I’m optimistic about the fuel situation.” Similarly, one should not trust a project leader who is optimistic about the budget or schedule, which is the fuel of projects.

During the Apollo program (1961–1972), the NASA administration criticized its cost engineers for being optimistic with a US$10 billion estimate for the program (approximately US$90 billion in 2021 dollars). The administration told the engineers that their assumption “that everything's going to work” was wrong (Bizony, 2006, p. 41). The engineers then increased their estimate to US$13 billion, which the administration adjusted to US$20 billion and got approved by Congress, to the shock of the engineers. Today, the NASA administration's US$7 billion increase has a technical name: “optimism bias uplift.” NASA jokingly called it the “administrator's discount.” But they were serious when they advised that all senior executives in charge of large, complex projects must apply such a discount to make allowance for the unknown. Whatever the name, it is the single most important reason Apollo has gone down in history as that rare species of multi-billion-dollar project: one delivered on budget. The NASA administration “knew exactly what [it] was doing” for Apollo, as rightly observed by space historian Piers Bizony (ibid.).

Explanations of project outcomes in terms of optimism bias originate with Kahneman and Tversky (1979a) and have been further developed by Kahneman and Lovallo (1993), Lovallo and Kahneman (2003), Flyvbjerg (2009a), and Flyvbjerg et al. (2004, 2009).

We saw above that strategic project planners and managers sometimes underestimate cost and overestimate benefit to achieve approval for their projects. Optimistic planners and managers also do this, albeit unintentionally. The result is the same, however, namely cost overruns and benefit shortfalls. Thus, optimism bias and strategic misrepresentation reinforce each other, when both are present in a project. An interviewee in our research described this strategy as “showing the project at its best” (Flyvbjerg et al., 2004, p. 50). It results in an inverted Darwinism, “survival of the unfittest” (Flyvbjerg, 2009b). It is not the best projects that get implemented like this, but the projects that look best on paper. And, the projects that look best on paper are the projects with the largest cost underestimates and benefit overestimates, other things being equal. But, the larger the cost underestimate on paper, the greater the cost overrun in reality. And, the larger the overestimate of benefits, the greater the benefit shortfall. Therefore, the projects that have been made to look best on paper become the worst, or unfittest, projects in reality.

Uniqueness Bias

Uniqueness bias was originally identified by psychologists as the tendency of individuals to see themselves as more singular than they actually are, for example, singularly healthy, clever, or attractive (Goethals et al., 1991; Suls et al., 1988; Suls & Wan, 1987). In project planning and management, the term was first used by Flyvbjerg (2014, p. 9), who defined uniqueness bias as the tendency of planners and managers to see their projects as singular. It is a general bias, but it turns out to be particularly rewarding as an object of study in project management, because project planners and managers are systematically primed to see their projects as unique.

The standard definition of a project, according to the biggest professional organization in the field, the U.S.-based Project Management Institute (PMI, 2017, p. 4), directly emphasizes uniqueness as one of two defining features of what a project is: “A project is a temporary endeavor undertaken to create a unique product, service, or result” (italics added). Similarly, the U.K.-based Association for Project Management (APM, 2012) stresses uniqueness as the very first characteristic of what a project is in their official definition: “A project is a unique, transient endeavour, undertaken to achieve planned objectives” (italics added). Academics, too, define projects in terms of uniqueness, here Turner and Müller (2003, p. 7, italics added): “A project is a temporary organization to which resources are assigned to undertake a unique, novel and transient endeavour managing the inherent uncertainty and need for integration in order to deliver beneficial objectives of change.” Similar views of uniqueness as key to the nature of projects may be found in Grün (2004, p. 3, p. 245), Fox and Miller (2006, p. 3, p. 109), and Merrow (2011, p. 161).

We maintain that the understanding of projects as unique is unfortunate, because it contributes to uniqueness bias with project planners and managers. In the grip of uniqueness bias, project managers see their projects as more singular than they actually are. This is reinforced by the fact that new projects often use nonstandard technologies and designs.

Uniqueness bias tends to impede managers’ learning, because they think they have little to learn from other projects as their own project is unique. Uniqueness bias may also feed overconfidence bias (see below) and optimism bias (see above), because planners subject to uniqueness bias tend to underestimate risks. This interpretation is supported by research on IT project management reported in Flyvbjerg and Budzier (2011), Budzier and Flyvbjerg (2013), and Budzier (2014). The research found that managers who see their projects as unique perform significantly worse than other managers. If you are a project leader and you overhear team members speak of your project as unique, you therefore need to react.

It is self-evidently true, of course, that a project may be unique in its own specific geography and time. For instance, California has never built a high-speed rail line before, so in this sense, the California High-Speed Rail Authority is managing a unique project. But, the project is only unique to California and therefore not truly unique. Dozens of similar projects have been built around the world, with data and lessons learned that would be highly valuable to California. In that sense, projects are no different from people. A quote, often ascribed to the anthropologist Margaret Mead, captures the point well: “Always remember that you are absolutely unique. Just like everyone else.” Each person not only is obviously unique but also has a lot in common with other people. The uniqueness of people has not stopped the medical profession from making progress based on what humans have in common. The problem with project management is that uniqueness bias hinders such learning across projects, because project managers and scholars are prone to “localism bias,” which we define as the tendency to see the local as global, due to availability bias for the local. Localism bias explains why local uniqueness is easily and often confused with global uniqueness. In many projects, it does not even occur to project planners and managers to look outside their local project, because “our project is unique,” which is a mantra one hears over and over in projects and that is surprisingly easy to get project managers to admit to.

Uniqueness bias feeds what Kahneman (2011, p. 247) calls the “inside view.” Seeing things from this perspective, planners focus on the specific circumstances and components of the project they are planning and seek evidence in their own experience. Estimates of budget, schedule, and so forth are based on this information, typically built “from the inside and out,” or bottom-up, as in conventional cost engineering. The alternative is the “outside view,” which consists of viewing the project you are planning from the perspective of similar projects that have already been completed, basing your estimates for the planned project on the actual outcomes of these projects. But if your project is truly unique, then similar projects clearly do not exist, and the outside view becomes irrelevant and impossible. This leaves you with the inside view as the only option for planning your project. Even if a project is not truly unique, if the project team thinks it is, then the outside view will be left by the wayside, and the inside view will reign supreme, which is typical. “In the competition with the inside view, the outside view does not stand a chance,” as pithily observed by Kahneman (2011, p. 249). The inside view is the perspective people spontaneously adopt when they plan, reinforced by uniqueness bias for project planners and managers. The inside view is therefore typical of project planning and management. The consequences are dire, because only the outside view effectively takes into account all risks, including the so-called “unknown unknowns.” These are impossible to predict from the inside, because there are too many ways a project can go wrong. However, the unknown unknowns are included in the outside view, because anything that went wrong with the completed projects that constitute the outside view is included in their outcome data (Flyvbjerg, 2006). Using these data for planning and managing a new project therefore leaves you with a measure of all risk, including unknown unknowns. Uniqueness bias makes you blind to unknown unknowns. The outside view is an antidote to uniqueness bias.

Project managers, in addition to being predisposed, like everyone else, to the inside view and uniqueness, have been indoctrinated by their professional organizations to believe projects are unique, as we saw above. Thus it's no surprise it takes substantial experience to cut loose from the conventional view. Patrick O’Connell, an experienced megaproject manager and ex-Practitioner Director of Oxford's BT Centre for Major Programme Management, told me, “The first 20 years as a megaproject manager I saw uniqueness in each project; the next 20 years similarities.” The NASA administration, mentioned above, balked when people insisted the Apollo program, with its aim of landing the first humans on the moon, was unique. How could it not be, as putting people on the moon had never been done before, people argued. The administration would have none of it. They deplored those who saw the program “as so special—as so exceptional,” because such people did not understand the reality of the project. The administration insisted, in contrast, that “the basic knowledge and technology and the human and material resources necessary for the job already existed,” so there was no reason to reinvent the wheel (Webb, 1969, p. 11, p. 61). The NASA-Apollo view of uniqueness bias saw this bias for what it is: a fallacy.

In sum, uniqueness bias feeds the inside view and optimism, which feed underestimation of risk, which makes project teams take on risks they would likely not have accepted had they known the real odds. Good project leaders do not let themselves be fooled like this. They accept that projects may be unique locally, yes. But they understand that to be locally unique is an oxymoron. Local uniqueness is, however, the typical meaning of the term “unique,” when used in project management. It is a misnomer that undermines project performance and thus the project management profession. Truly unique projects are rare. We have lots to learn from other projects. And if we don’t learn, we will not succeed with our projects.

The Planning Fallacy (Writ Large)

The planning fallacy is a subcategory of optimism bias that arises from individuals producing plans and estimates that are unrealistically close to best-case scenarios. The term was originally coined by Kahneman and Tversky (1979a, p. 315) to describe the tendency for people to underestimate task completion times. Buehler et al. (1994, 1997) continued work following this definition. Later, the concept was broadened to cover the tendency for people to, on the one hand, underestimate costs, schedules, and risks for planned actions and, on the other, overestimate benefits and opportunities for those actions. Because the original narrow and later broader concepts are so fundamentally different in the scope they cover, Flyvbjerg and Sunstein (2017) suggested the term “planning fallacy writ large” for the broader concept, to avoid confusing the two.

Flyvbjerg et al. (2003, p. 80) call the tendency to plan according to best-case scenarios the “EGAP principle,” for Everything Goes According to Plan. The planning fallacy and the EGAP principle are similar in the sense that both result in a lack of realism, because of their overreliance on best-case scenarios, as with the NASA cost engineers above. Both lead to base rate neglect, illusion of control, and overconfidence. In this manner, both feed into optimism bias.

At the most fundamental level, Kahneman and Tversky (1979a) identified the planning fallacy as arising from a tendency with people to neglect distributional information when they plan. People who plan would adopt what Kahneman and Tversky (1979a, p. 315) first called an “internal approach to prediction” and later renamed the “inside view,” under the influence of which people would focus on “the constituents of the specific problem rather than on the distribution of outcomes in similar cases.” Kahneman and Tversky (1979a) emphasized that “The internal approach to the evaluation of plans is likely to produce underestimation [of schedules].” For the planning fallacy writ large, such underestimation applies to costs, schedules, and risk, whereas overestimation applies to benefits and opportunities.

Interestingly, Guinote (2017, pp. 365–366) found in an experiment that subjects who had been made to feel in power were more likely to underestimate the time needed to complete a task than those not in power, demonstrating a higher degree of planning fallacy for people in power. Again, this is an example of how power bias and cognitive bias interact, resulting in amplification and convexity.

The planning fallacy's combination of underestimated costs and overestimated benefits generates risks to the second degree. Instead of cost risk and benefit risk canceling out one another—as other theories predict, for example, Hirschman's (2014) principle of the Hiding Hand—under the planning fallacy, the two types of risk reinforce each other, creating convex (accelerated) risks for projects from the get-go. The planning fallacy goes a long way in explaining the Iron Law of project management: “Over budget, over time, under benefits, over and over again” (Flyvbjerg, 2017). As a project leader, you want to avoid convex risks because such risks are particularly damaging. You want to avoid committing the planning fallacy and especially for people in power.

Overconfidence Bias, Hindsight Bias, and Availability Bias

Overconfidence bias is the tendency to have excessive confidence in one's own answers to questions and to not fully recognize the uncertainty of the world and one's ignorance of it. People have been shown to be prone to what is called the “illusion of certainty” in (a) overestimating how much they understand and (b) underestimating the role of chance events and lack of knowledge, in effect underestimating the variability of events they are exposed to in their lives (Moore & Healy, 2008; Pallier et al., 2002; Proeger & Meub, 2014). Overconfidence bias is found with both laypeople and experts, including project planners and managers (Fabricius & Büttgen, 2015).

Overconfidence bias is fed by illusions of certainty, which are fed by hindsight bias also known as the “I-knew-it-all-along effect.” Availability bias—the tendency to overweigh whatever comes to mind—similarly feeds overconfidence bias. Availability is influenced by the recency of memories and by how unusual or emotionally charged they may be, with more recent, more unusual, and more emotional memories being more easily recalled. Overconfidence bias is a type of optimism, and it feeds overall optimism bias.

A simple way to illustrate overconfidence bias is to ask people to estimate confidence intervals for statistical outcomes. In one experiment, the chief financial officers (CFOs) of large U.S. corporations were asked to estimate the return next year on shares in the relevant Standard & Poor's index (Kahneman, 2011, p. 261). In addition, the CFOs were asked to give their best guess of the 80% confidence interval for the estimated returns by estimating a value for returns they were 90% sure would be too low (the lower decile, or P10) and a second value they were 90% sure would be too high (the upper decile, or P90), with 80% of returns estimated to fall between these two values (and 20% outside). Comparing actual returns with the estimated confidence interval, it was found that 67% of actual returns fell outside the estimated 80% confidence interval, or 3.35 times as many as estimated. The actual variance of outcomes was grossly underestimated by these financial experts, which is the same as saying they grossly underestimated risk. It is a typical finding. The human brain, including the brains of experts, spontaneously underestimates variance. For whatever reason, humans seem hardwired for this.

In project management, overconfidence bias is built into the tools experts use for risk management. The tools, which are typically based on computer models using so-called Monte Carlo simulations, or similar, look scientific and objective but are anything but. Again, this is easy to document. You simply compare assumed variance in a specific, planned project with actual, historic variance for its project type, and you find the same result as for the CFOs above (Batselier & Vanhoucke, 2016). The bias is generated by experts assuming thin-tailed distributions of risk (normal or near-normal), when the real distributions are fat-tailed (lognormal, power law, or similar probability distribution) (Taleb, 2004). The error is not with Monte Carlo models as such, but with erroneous input into the models. Garbage in, garbage out, as always. To eliminate overconfidence bias, you want a more objective method that takes all distributional information into account, not just the distributional information experts can think of, which is subject to availability bias. The method needs to run on historical data from projects that have actually been completed. Flyvbjerg (2006) describes such a method.

In the thrall of overconfidence bias, project planners and decision makers underestimate risk by overrating their level of knowledge and ignoring or underrating the role of chance events in deciding the fate of projects. Hiring experts will generally not help, because experts are just as susceptible to overconfidence bias as laypeople and therefore tend to underestimate risk, too. There is even evidence that the experts who are most in demand are the most overconfident. In other words, people are attracted to, and willing to pay for, confidence, more than expertise (Kahneman, 2011, p. 263; Tetlock, 2005). Risk underestimation feeds the Iron Law of project management and is the most common cause of project downfall. Good project leaders must know how to avoid this.

Individuals produce confidence by storytelling. The more coherent a story we can tell about what we see, the more confident we feel. But, coherence does not necessarily equal validity. People tend to assume “what you see is all there is,” called WYSIATI by Kahneman (2011, pp. 87–88), who gives this concept pride of place in explaining a long list of biases, including overconfidence bias. People spin a story based on what they see. Under the influence of WYSIATI, they spontaneously impose a coherent pattern on reality, while they suppress doubt and ambiguity and fail to allow for missing evidence, says Kahneman. The human brain excels at inferring patterns and generating meaning based on skimpy, or even nonexistent, evidence. But, coherence based on faulty or insufficient data is not true coherence, needless to say. If we are not careful, our brains quickly settle for anything that looks like coherence and uses it as a proxy for validity. This may not be a big problem most of the time, and may even be effective, on average, in evolutionary terms, which could be why the brain works like this. But for big consequential decisions, typical of project planning and management, it is not an advisable strategy. Nevertheless, project leaders and their teams often have a very coherent—and very wrong—story about their project, for instance that the project is unique, as we saw above under uniqueness bias, or that the project may be completed faster and cheaper than the average project or that everything will go according to plan. The antidote is better, more carefully curated stories, based on better data.

Gigerenzer (2018, p. 324) has rightly observed that overconfidence, presented by psychologists as a nondeliberate cognitive bias, is in fact often a deliberate strategic bias used to achieve predefined objectives; in other words, it is strategic misrepresentation. Financial analysts, for instance, “who earn their money by mostly incorrect predictions such as forecasting exchange rates or the stock market had better be overconfident; otherwise few would buy their advice,” argues Gigerenzer, who further observes about this fundamental confusion of one type of bias for a completely different one that, “[c]onceptual clarity is desperately needed” (Gigerenzer, 2018, p. 324).

Finally, regarding the relationship between power bias and cognitive bias mentioned above, powerful individuals have been shown to be more susceptible to availability bias than individuals who are not powerful. The causal mechanism seems to be that powerful individuals are affected more strongly by ease of retrieval than by the content they retrieve, because they are more likely to “go with the flow” and trust their intuition than individuals who are not powerful (Weick & Guinote, 2008). This finding has been largely ignored by behavioral economists, including Thaler (2015) in his history of the field. This is unfortunate, because the finding documents convexity to the second degree for situations with power. By overlooking this, behavioral economists make the same mistake they criticize conventional economists for, namely overlooking and underestimating variance and risk. Conventional economists make the mistake by disregarding cognitive bias; behavioral economists by ignoring power bias and its effect on cognitive bias. Underestimating convexity is a very human mistake, to be sure. We all do it. But, it needs to be accounted for if we want to understand all relevant risks and protect ourselves against them in project planning and management.

The Base Rate Fallacy

The base rate fallacy—sometimes also called base rate bias or base rate neglect—is the tendency to ignore base rate information (general data pertaining to a statistical population or a large sample, e.g., its average) and focus on specific information (data only pertaining to a certain case or a small number of cases) (Bar-Hillel, 1980; Tversky & Kahneman, 1982). If you play poker and assume different odds than those that apply, you are subject to the base rate fallacy and likely to lose. The objective odds are the base rate.

People often think the information they have is more relevant than it actually is or they are blind to relevant information they do not have. Both situations result in the base rate fallacy. “Probability neglect”—a term coined by Sunstein (2002, pp. 62–63) to denote the situation where people overfocus on bad outcomes with small likelihoods, for instance terrorist attacks—is a special case of the base rate fallacy.

The base rate fallacy is fed by other biases, for instance, uniqueness bias, described above, which results in extreme base rate neglect, because the case at hand is believed to be singular, wherefore information about other cases is deemed irrelevant. The inside view, hindsight bias, availability bias, recency bias, WYSIATI bias, overconfidence bias, and framing bias also feed the base rate fallacy. Base rate neglect is particularly pronounced when there is a good, strong story. Big, monumental projects typically have such a story, contributing to extra base rate neglect for those. Finally, we saw above that people, including experts, underestimate variance. In the typical project, base rate neglect therefore combines with variance neglect, following this formula:

Preliminary results from our research indicate that variance neglect receives less attention in project management than base rate neglect, which is unfortunate, because the research also indicates that variance neglect is typically larger and has even more drastic impact on project outcomes than base rate neglect.

The base rate fallacy runs rampant in project planning and management, as documented by the Iron Law described earlier. Table 2 shows the most comprehensive overview that exists of base rates for costs and benefits in project management, based on data from 2,062 projects covering eight project types. Most projects do not get base rates right, as documented by averages that are different from one (1.0 ≈ correct base rate) at a level of statistical significance so high (p < 0.0001) it is rarely found in studies of human behavior. The base rate fallacy is deeply entrenched in project management, as the data show. Flyvbjerg and Bester (2021) argue that base rate neglect results in a new behavioral bias, which they call the “cost–benefit fallacy,” which routinely derail cost–benefit analyses of projects to a degree where such analyses cannot be trusted.

As pointed out by Kahneman (2011, p. 150), “anyone who ignores base rates and the quality of evidence in probability assessments will certainly make mistakes.” The cure for the base rate fallacy, in and out of project management, is to get the base rate right by taking an outside view, for instance through reference class forecasting, carrying out premortems, or doing decision hygiene (Flyvbjerg, 2006; Klein, 2007; Kahneman et al., 2011, 2021, pp. 312–324, 371–372).

If you are a project planner or manager, the easiest and most effective way to get started with curbing behavioral biases in your work is getting your base rates right, for the projects you are working on. Hopefully, most can see that if you do not understand the real odds of a game, you are unlikely to succeed at it. But that is the situation for most project planners and managers: they do not get the odds right for the game they are playing: project management. Table 2 documents this beyond reasonable doubt and establishes realistic base rates for a number of important areas in project management that planners can use as a starting point for getting their projects right. Data for other project types were not included for reasons of space but show similar results.

Anchoring

Anchoring is the tendency to rely too heavily, or “anchor,” on one piece of information when making decisions. Anchoring was originally demonstrated and theorized by Tversky and Kahneman (1974). In their perhaps most famous experiment, subjects were asked to estimate the percentage of African countries in the United Nations. First, a number between 0 and 100 was determined by spinning a wheel of fortune in the subjects’ presence. Second, the subjects were instructed to indicate whether that number was higher or lower than the percentage of African countries in the United Nations. Third, the subjects were asked to estimate this percentage by moving upward or downward from the given number. The median estimate was 25% for subjects who received the number 10 from the wheel of fortune as their starting point, whereas it was 45% for subjects who started with 65. A random anchor significantly influenced the outcome.

Similar results have been found in other experiments for a wide variety of different subjects of estimation (Chapman & Johnson, 1999; Fudenberg et al., 2012). Anchoring is pervasive. The human brain will anchor in most anything, whether random numbers, previous experience, or false information. It has proven difficult to avoid this (Epley & Gilovich, 2006; Simmons et al., 2010; Wilson et al., 1996). The most effective way of dealing with anchoring is therefore to make sure the brain anchors in relevant information before making decisions. An obvious choice would be to anchor in base rates that are pertinent to the decision at hand, as proposed by Flyvbjerg (2006). This advice is similar to recommending that gamblers must know the objective odds of each game they play. It is sound advice but often goes unheeded in project management.

Project planners and managers tend to err by anchoring their decisions in plans that are best-case, instead of most likely, scenarios, as mentioned above. Planners and organizations also frequently anchor in their own limited experience, instead of seeking out a broader scope of histories, which would be more representative of the wider range of possible outcomes that actually apply to the project they are planning.

This happened to Hong Kong's MTR Corporation when they were tasked with building the first high-speed rail line in the territory. MTR anchored in its own experience with urban and conventional rail instead of throwing the net wider and looking at high-speed rail around the world. High-speed rail is significantly more difficult to build than urban and conventional rail, and MTR had never built a high-speed rail line before. Despite—or perhaps because of—MTR's proven competence in building urban and conventional rail, the anchor for the high-speed rail line proved optimistic, resulting in significant cost and schedule overruns for the new venture (Flyvbjerg et al., 2014).

Ansar et al. (2014, p. 48) similarly found that planners of large dams around the world have generally anchored in the North American experience with building dams, for no better reason than North America built their dams first. By choosing this anchor, planners ended up allowing insufficient adjustments to fully reflect local risks, for example, exchange rate risks, corruption, logistics, and the quality of local project management teams. This resulted in optimistic budgets and higher cost overruns for dams built outside North America.

Anchoring is fed by other biases, including availability bias and recency bias, which induce people to anchor in the most available or most recent information, respectively. Anchoring results in base rate neglect, in other words, underestimation of the probabilities, and thus the risks, that face a project (see previous section). Smart project leaders avoid this by anchoring their project in the base rate for similar projects to the one they are planning, for instance, by benchmarking their project against outcomes for a representative class of similar, completed projects. Flyvbjerg (2013) explains how to do this, and Kahneman (2011, p. 154) explicitly identifies anchoring in the base rate as the cure for the WYSIATI bias mentioned above. Anchoring in the base rate is similar to taking an outside view, and the outside view is “an anchor that is meaningful,” as rightly observed by Tetlock and Gardner (2015, pp. 117–120), whereas spontaneous anchors typically are less meaningful and lead to biased decisions with hidden risks.

Escalation of Commitment

Last, but not least, escalation of commitment (sometimes also called commitment bias) is the tendency to justify increased investment in a decision, based on the cumulative prior investment, despite new evidence suggesting the decision may be wrong and additional costs will not be offset by benefits. Consider the example of two friends with tickets for a professional basketball game a long drive from where they live. On the day of the game, there is a big snowstorm. The higher the price the friends paid for the tickets, the more likely they are to brave the blizzard and attempt driving to the game, investing more time, money, and risk (Thaler, 2015, p. 20). That is escalation of commitment. In contrast, the rational approach when deciding whether to invest further in a venture would be to disregard what you have already invested.

Escalation of commitment applies to individuals, groups, and whole organizations. It was first described by Staw (1976) with later work by Brockner (1992), Staw (1997), Sleesman et al. (2012), and Drummond (2014, 2017). Economists use related terms like the “sunk-cost fallacy” (Arkes & Blumer, 1985) and “lock-in” (Cantarelli et al., 2010b) to describe similar phenomena. Escalation of commitment is captured in popular proverbs such as, “Throwing good money after bad” and “In for a penny, in for a pound.”

In its original definition, escalation of commitment is unreflected and nondeliberate. People do not know they are subject to the bias, as with other cognitive biases. However, once you understand the mechanism, it may be used deliberately. In his autobiography, famous Hollywood director Elia Kazan (1997, pp. 412–413) explains how he used sunk costs and escalation of commitment to get his projects going: “Quickly I planned my position on costs … My tactic was one familiar to directors who make films off the common path: to get the work rolling, involve actors contractually, build sets, collect props and costumes, expose negative, and so get the studio in deep. Once money in some significant amount had been spent, it would be difficult for Harry [Cohn, President and co-founder of Columbia Pictures] to do anything except scream and holler. If he suspended a film that had been shooting for a few weeks, he'd be in for an irretrievable loss, not only of money but of ‘face.’ The thing to do was get the film going.”

Kazan here combines strategic misrepresentation with cognitive bias to achieve takeoff for his projects. The misrepresentation consists in initially (a) being “economical with the truth” regarding the real cost of his projects and (b) just “get the film going” to sink in sufficient cost to create a point of no return. After this, Kazan trusts the studio head to fall victim to cognitive bias, specifically sunk cost and escalation of commitment, in the grip of which he will allocate more money to the film instead of halting it, which might have been the rational decision. This is the studio head's version of Thaler’s (2015) “driving into the blizzard,” described above. As argued earlier, such interaction between cognitive and political bias is common in shaping project outcomes. Most project managers will know examples similar to Kazan’s. It is too simple to think of outcomes as being generated solely by either cognitive bias or political bias. Such purity may be constructed in lab experiments. In real life, both are typically at play with complex interactions between the two.

A number of excellent case studies exist that demonstrate the pertinence of escalation of commitment to project planning and management, for example, of Expo 86 (Ross & Staw, 1986), the Shoreham nuclear power plant (Ross & Staw, 1993), and Denver International Airport (Monteagre & Keil, 2000), each of which present their own version of “driving into the blizzard.”

We saw above how optimism bias undermines project performance. Escalation of commitment amplifies this. Consider that once a forecast turns out to have been optimistic, often the wisest thing would be to give up the project. But, escalation of commitment and the sunk cost fallacy keep decision-makers from doing the right thing. Instead, they keep going, throwing good money after bad.

Escalation of commitment often coexists with and is reinforced by what has been called “preferential attachment” or the “Yule process” (Barabási, 2014; Barabási & Albert, 1999; Gabaix, 2009). Preferential attachment is a procedure in which some quantity, for example, money or connections in a network, is distributed among a number of individuals or units according to how much they already have, so that those who have much receive more than those who have little, known also as the “Matthew effect.”

In project planning and management, Flyvbjerg (2009b) argued that the investments that look best on paper get funded and that these are the investments with the largest cost underestimates and therefore the largest need for additional funding during delivery, resulting in preferential attachment of funds to these investments, once they have their initial funding. After an investment has been approved and funded, typically there is lock-in and a point of no return, after which escalation of commitment follows, with more and more funds allocated to the original investment to close the gap between the original cost underestimate and actual outturn cost (Cantarelli et al., 2010b; Drummond, 2017).

Interestingly, preferential attachment has been identified as a causal mechanism that generates outcome distributions with a fat upper tail, specifically power law distributions (Barabási, 2014; Krapivsky & Krioukov, 2008). In the case of cost, this would predict an overincidence (compared with the Gaussian) of extreme cost overruns. So far, we have tested the thesis for cost and cost overrun with the Olympic Games, where the thesis found strong support in the data (Flyvbjerg et al., 2021). Currently, we are further testing the thesis for information technology projects, while tests of other project types are in the pipeline. Should the thesis hold across project types, we may be in the first stages of discovering a general theory of project management, with more fundamental and more scientific explanations of project outcomes than those found in conventional theory.

Discussion

Scientific revolutions rarely happen without friction. So, too, for the behavioral revolution. It has been met with skepticism, including from parts of the project management community (Flyvbjerg et al., 2018). Some members prefer to stick with conventional explanations of project underperformance in terms of errors of scope, complexity, labor and materials prices, archaeology, geology, bad weather, ramp-up problems, demand fluctuations, and so forth (Cantarelli et al., 2010a).

Behavioral scientists would agree with the skeptics that scope changes, complexity, and so forth are relevant for understanding what goes on in projects but would not see them as root causes of outcomes. According to behavioral science, the root cause of, say, cost overrun is the well-documented fact that project planners and managers keep underestimating scope changes, complexity, and so forth in project after project.

From the point of view of behavioral science, the mechanisms of scope changes, complex interfaces, price changes, archaeology, geology, bad weather, and business cycles are not unknown to project planners and managers, just as it is not unknown that such mechanisms may be mitigated. However, project planners and managers often underestimate these mechanisms and mitigation measures, due to optimism bias, overconfidence bias, the planning fallacy, and strategic misrepresentation. In behavioral terms, unaccounted for scope changes are manifestations of such underestimation on the part of project planners, and it is in this sense bias and underestimation are root causes and scope changes are just causes. But because scope changes are more visible than the underlying root causes, they are often mistaken for the cause of outcomes, for example, cost overrun.

In behavioral terms, the causal chain starts with human bias (political and cognitive), which leads to underestimation of scope during planning, which leads to unaccounted for scope changes during delivery, which leads to cost overrun. Scope changes are an intermediate stage in this causal chain through which the root causes manifest themselves. Behavioral science tells project planners and managers, “Your biggest risk is you.” It is not scope changes, complexity, and so forth in themselves that are the main problem; it is how human beings misconceive and underestimate these phenomena, through optimism bias, overconfidence bias, and strategic misrepresentation. This is a profound and proven insight that behavioral science brings to project planning and management. You can disregard it, of course. But if you do, project performance would likely suffer. You would be the gambler not knowing the odds of their game.

Behavioral science is not perfect. We saw above how behavioral economics suffers from a “psychology bias,” in the sense it tends to reduce behavioral biases to cognitive biases, ignoring political bias in the process, thus committing the very sin it accuses conventional economics of, namely theory-induced blindness resulting in limited rationality. Gigerenzer (2018) goes further and criticizes behavioral economics for “bias bias,” and he is right when he calls for conceptual clarification. Not all behavioral biases are well defined, or even well delineated: many and large overlaps exist among different biases that need clarification, including for the 10 described above. Just as seriously, many biases have only been documented in simplified lab experiments but are tacitly assumed to hold in real-life situations outside the lab, without sound demonstration that the assumption holds. Finally, the psychology used by behavioral economists is not considered cutting-edge by psychologists, a fact openly acknowledged by Thaler (2015, p. 180), who further admits it is often difficult to pin down which specific behavioral bias is causing outcomes in a given situation or to rule out alternative explanations (Thaler, 2015, p. 295).

Nevertheless, the behavioral revolution seems to be here to stay, and it entails an important change of perspective for project management: The problem with project cost overruns and benefit shortfalls is not error but bias, and as long as we try to solve the problem as something it is not (error), we will not succeed. Estimates and decisions need to be debiased, which is fundamentally different from eliminating error. Furthermore, the problem is not even cost overruns or benefit shortfalls, it is cost underestimation and benefit overestimation. Overrun, for instance, is mainly a consequence of underestimation, with the latter happening upstream from overrun, for big projects often years before overruns manifest. Again, if we try to solve the problem as something it is not (cost overrun), we will fail. We need to solve the problem of upstream cost underestimation in order to solve the problem of downstream cost overrun. Once we understand these straightforward insights, we understand that we and our projects are better off with an understanding of behavioral science and behavioral bias than without it.