Abstract

Recent developments in engineering design have resulted in substantial improvements to the seismic performance of new buildings. However, buildings constructed before recent upgrades to the seismic regulations comprise a large portion of the existing building inventory. Buildings with insufficient seismic capacity are susceptible to extensive damage or collapse during an earthquake, contributing to economic losses and casualties. Effective risk mitigation strategies such as seismic retrofitting could potentially address the vulnerability of the existing building stock to earthquake hazards. Yet, seismic retrofit programs suffer from low take-up rates. Thus, identifying barriers for seismic retrofit adoption and strategies to increase take-up rates can help mitigate losses from future events. This study develops an agent-based model to assess homeowner response to multiple seismic retrofit promotion strategies. The simulation framework is applied to a case study of owner-occupied, residential-detached dwellings in Vancouver, British Columbia, Canada, to evaluate the effectiveness of various potential seismic retrofit promotion strategies. These strategies are compared regarding the number of adopters and the reduction in total annual losses to residential building structures and contents in the City of Vancouver. The main barriers to adopting retrofit measures among different income groups are identified, and appropriate interventions to target those barriers are suggested. Modeling the impact of policies allows policymakers to evaluate their effects and fine-tune the policy interventions before their implementation.

Keywords

Introduction

Appropriate risk mitigation strategies such as seismic retrofitting can minimize earthquakes’ social, economic, and socioeconomic consequences. In countries with proactive retrofit policies, including Japan, Italy, and New Zealand, the number of collapses and severely damaged buildings in recent earthquakes was lower than expected (Zhang et al., 2022). Recent studies by the Geological Survey of Canada suggest that seismic retrofits would have similar benefits. According to the National Earthquake Scenario Catalogue, a magnitude 7.0 earthquake beneath the Strait of Georgia in British Columbia could cause $30.3 CAD billion in total losses, heavy damage to 10,626 buildings, and displace 345,774 people. However, across all residential buildings, seismic retrofitting in Vancouver would reduce the economic losses by 25% and the number of heavily damaged buildings by 34% (Hobbs et al., 2021). This suggests that improved seismic design, including retrofits, can have a meaningful impact on building performance during an earthquake.

Although seismic retrofitting can help to protect life and property, many owners are reluctant to adopt retrofit measures due to various reasons (e.g. underestimating the earthquake risk, not believing in retrofitting effectiveness or benefits) (Egbelakin, 2013; Egbelakin et al., 2014; Egbelakin et al., 2011; Kashani et al., 2019). At present, only a few countries (e.g. the United States and New Zealand) have enacted mandatory retrofit requirements for privately owned residential dwellings. However, implementing mandatory policies is often challenging due to high enforcement costs and potential resistance from property owners. Therefore, most countries rely on voluntary retrofitting programs supported by government-sponsored financial and technical assistance (Zhang et al., 2022). Well-designed incentive policies can encourage homeowners to undertake seismic adjustments, thereby reducing earthquake-related risks in their communities (Egbelakin, 2013; Egbelakin et al., 2011). This emphasizes the important role of governments in motivating homeowners to adopt retrofit measures through appropriate policy interventions. A review of international practices reveals that common incentive mechanisms include retrofit grants, tax rebates, and government-backed loans (Zhang et al., 2022). While most retrofit promotion mechanisms focus on financial incentives, retrofit costs are small relative to the building values. For example, in Canada, seismic retrofitting of a single detached dwelling would cost between CAD 4000 and 10,000, while the average price of a detached home in Vancouver is between CAD 1.5 and 2 million (The Canadian Real Estate Association, 2024). Thus, it is arguable that there exist other barriers preventing private residential homeowners from adopting seismic retrofit measures. Understanding these differences would enable policymakers to design targeted interventions that encourage adoption among specific population groups.

To shed light on this topic, this study provides two contributions. First, we develop a computational simulation framework to provide insights into the implementation of seismic retrofit programs. We develop an agent-based approach to simulate the homeowner’s decision processes as they engage with seismic retrofit programs. Homeowners are the primary agents in this model. These agents have attributes (e.g. disposable income, risk perception, education level) and behaviors (e.g. their attitude toward seismic retrofit). Policies are implemented by local authorities to encourage the adoption of seismic retrofit measures (e.g. subsidies or education programs). Homeowner Agents also interact with each other. These interactions might influence their understanding of seismic risks and attitudes toward seismic retrofitting, leading to behavioral changes over time. Second, we apply this framework to a case study of Vancouver, British Columbia, Canada, to compare the effectiveness of different policy interventions to encourage Vancouver-detached homeowners to retrofit their homes. The suggested seismic retrofit promotion policies are evaluated regarding the total number of homeowners adopting the retrofit measures and the reduction in total annual losses to residential building structures and contents in the City of Vancouver. The main barriers to adopting seismic adjustment measures among different income groups are identified, and appropriate policy interventions to target those barriers are suggested. Modeling the impact of policies before their application allows policymakers to evaluate their effects. So they can fine-tune the policy interventions before their implementation. This study provides insight into the efficient design of seismic risk mitigation policies in earthquake-prone communities.

Modeling seismic retrofit decision-making

The process of individuals’ undertaking protective actions has been studied in psychology, sociology, economics, and health sciences mainly through two theories: (i) attitude-behavioral theories and (ii) social and cognitive processes theories. The models originated from the attitude-behavioral theories focus on the relationship between attitudes, intentions, and behaviors. They explain how people’s attitudes toward risks and mitigation strategies influence their decisions and actions (Ajzen, 1991; Rosenstock, 1974). Within the context of the attitude-behavioral theoretical perspective, the models with application in seismic risk mitigation are the Theory of Reasoned Action (TRA) and the Theory of Planned Behavior (TPB) (Ajzen, 1991; Egbelakin, 2013). These theories explain why individuals adopt precautionary actions, such as retrofitting buildings or purchasing insurance, based on their perception of seismic risks and their attitude toward the effectiveness of mitigation measures (Ajzen, 1991; Lindell and Perry, 2000).

The theories incorporating the social and cognitive processes focus on understanding how individuals evaluate risks, resources, and social influences to make decisions about disaster preparedness and mitigation (Mulilis and Lippa, 1990). These theories incorporate cognitive appraisal, social interaction, and behavioral intention to explain preparedness behaviors. Some of the key theories in this category include the Protection Motivation Theory (PMT) (Rogers, 1975), Person-Relative-to-Event Theory (PrE) (Mulilis and Duval, 1995), Protective Action Decision Model (PDAM) (Lindell and Perry, 2003), and Social Cognitive Preparation Model (Paton, 2003). Models based on social and cognitive processes theories recognize that problem-focused coping motivates action but also account for barriers, such as perceived lack of resources, that may inhibit preparedness. These models have been used to study the impact of proposed variables within the context of several natural hazards such as earthquakes, volcanic eruptions, and tsunami (Paton et al., 2008, 2010).

Building upon factors identified by these theoretical models which influence the adoption of precautionary action, Egbelakin (2013) developed a conceptual framework to describe homeowners’ seismic retrofit decision-making. Similar variations of this model have been used by other scholars to study the seismic risk mitigation behavior of homeowners (e.g. Kashani et al., 2019; Taylan, 2015). According to this model, the process of adopting and implementing the seismic adjustment measures comprises three sequential phases: (i) intention formation, (ii) decision formation, and (iii) adoption and implementation of seismic adjustment.

Intention formation phase

The intention formation phase describes an individual’s process of developing the intention to adopt seismic mitigation measures. Intention, as a behavioral attribute, is driven by intrinsic factors or external stimuli (Paton, 2003). Behavioral intention is a critical precursor to protective actions, although it does not translate directly into decisions or behaviors. Several factors have been identified in the earthquake risk management literature to predict behavioral intention (Ajzen, 2002; Egbelakin, 2013; Paton and Johnston, 2017): self-efficacy, defined as the belief in a personal capacity to succeed in a task or achieve a goal; outcome expectancy, which anticipates whether personal actions lead to a desirable outcome (Paton, 2003); perceived responsibility, which reflects the individual’s sense of responsibility for personal and close family safety against earthquake potential impacts (or a potential threat) (Mulilis and Duval, 1995); and risk perception, which refers to the individual’s subjective judgment of the likelihood and consequences of a future adverse event (Sjöberg, 2004). Risk perception is shaped by how individuals interpret and personalize a hazard and its potential impacts, with those who perceive themselves as vulnerable and at risk being more likely to seek actions to mitigate the consequences of a potential disaster (Dash and Gladwin, 2007). Risk perception has been long established as a valid precursor for intention formation in disaster preparedness (Solberg et al., 2010).

Decision formation phase

During the decision formation phase, an individual intending to reduce their seismic risk evaluates the mitigation actions and decides whether to adopt the adjustment measures. The decision is influenced by individual attributes such as the perceived benefit of retrofitting, trust in the stakeholder’s relationship, seismic adjustment efficacy, and resource requirement. Perceived benefit refers to an individual’s judgment of the advantages of adopting seismic adjustments, such as ensuring safety, reducing repair costs, avoiding relocation expenses, and potentially increasing property value or reducing insurance premium (Egbelakin, 2013). Individuals who recognize that the benefits of retrofitting outweigh the costs are more likely to form positive attitudes and decisions toward implementing mitigation measures. However, a lack of understanding of these tangible benefits can deter owners from proceeding with retrofits. Trust in stakeholder relationships influences their acceptance or rejection of information about seismic risk and mitigation measures (Egbelakin, 2013). Information sources’ credibility and perceived trustworthiness, such as government organizations, affect homeowners’ confidence in the information provided, ultimately shaping their decision to adopt seismic mitigation measures (Lindell and Perry, 2003; Paton et al., 2008). Seismic adjustment efficacy refers to an individual’s perception of how effective seismic mitigation measures are in protecting people and property during an earthquake (Lindell and Perry, 2003; Mulilis and Duval, 1995). Seismic adjustment efficacy is measured by mitigation actions that reduce vulnerability to hazard impacts. Both theoretical models and empirical studies in earthquake risk management suggest that seismic adjustment efficacy significantly influences an individual’s decision to adopt hazard mitigation measures (Lindell and Perry, 2003; Mulilis and Duval, 1995). Resource requirements refer to an individual’s belief about having sufficient knowledge, skills, and resources (e.g. Funding, materials, and equipment) necessary to implement seismic mitigation measures (Lindell and Perry, 2003; Paton, 2003). Studies have shown that adequate resources are positively correlated with the decision to adopt hazard mitigation and the actual implementation of these measures. In contrast, a lack of resources often hinders action (Egbelakin, 2013).

Adoption and implementation phase

The final phase involves the adoption and implementation of seismic adjustments. This occurs when factors influencing intention and decision formation in earlier stages are sufficiently high. At this point, individuals who have decided to take a risk reduction action do so by utilizing available resources to implement the necessary adjustments.

External motivators

This section examines external factors that influence different phases of seismic retrofit decision-making. These factors include policies implemented by local governments, such as financial incentives and educational campaigns, which aim to encourage homeowners to adopt retrofit measures. Moreover, social interactions among homeowners can shape opinions about earthquake risk and seismic retrofitting, potentially leading to changes in their decisions.

Financial incentives

The availability of financial incentives can motivate homeowners to adopt and implement seismic adjustments (Egbelakin et al., 2011). Financial incentives can be grants, low-interest loans, or tax deductions distributed to eligible homeowners. Financial incentives can enhance households’ willingness to pay and perceived benefit attributes. One well-documented seismic risk financial incentive program is the Earthquake Brace and Bolt (EBB) retrofit in California (California Residential Mitigation Program, 2024b). The cost of retrofitting a single detached house through the EBB program ranges from USD$3000 to USD$7000, depending on location and retrofit type. The EBB retrofit program offers $3000 grants to all homeowners (California Residential Mitigation Program, 2024a). Moreover, supplemental grants are available for households with less than 80% of the median household income in California to cover up to 100% of the retrofit costs (California Residential Mitigation Program, 2024c).

Educational campaigns

Educational measures highlight the potentially devastating consequences of earthquakes and the effectiveness of seismic adjustment measures in protecting life and property. Education campaigns can include videos on television or social media showcasing the potential damages of a severe earthquake and recommending seismic retrofitting as an effective risk mitigation strategy. Education can enhance homeowners’ perception of risk and the efficacy of mitigation measures. They can also disseminate the earthquake awareness and preparedness message in a community through social interactions. A survey by Egbelakin et al. (2011) showed that 88% of the homeowner participants stated that mass media would largely influence their willingness to prepare for disasters and that repeated exposure to information can strengthen homeowners’ intentions to adopt retrofit measures.

Social influence

Social influence is a fundamental aspect of human interaction that may cause individuals to adapt their opinions or behaviors to align more closely with those they interact with. According to Flache et al. (2017), a large part of the studies on social influence in the literature could be categorized into three classes of models: models of assimilative social influence, models with similarity-biased influence, and models with repulsive influence. The assimilative social influence models propose that when two individuals are connected through an influence relationship, they consistently influence each other to minimize their opinion differences. This framework suggests that societal interactions ultimately lead to consensus but struggle to explain how opinion clustering can endure in densely connected networks without individuals’ fixation on their initial opinions (Flache et al., 2017).

Models with similarity bias abandon the assumption that there is always influence if there is a structural connection between agents (Flache et al., 2017). Instead, these models propose that social influence depends on the similarity between individuals, with greater similarity leading to stronger influence. If opinions differ too greatly, influence may cease altogether, as agents lose “confidence” in the source of influence (Axelrod, 1997; Deffuant et al., 2000; Rainer and Krause, 2002). This similarity-based dynamic creates a feedback loop where agreement reinforces influence, and influence further strengthens agreement among like-minded individuals. As a result, these models can explain the persistence of distinct opinion clusters within a society rather than convergence toward a consensus (Axelrod, 1997; Deffuant et al., 2000; Rainer and Krause, 2002).

Models with repulsive influence assume that as the dissimilarity between individuals’ opinions increases, they evaluate each other more negatively, widening their opinion differences (Rosenbaum, 1986). These dynamics prevent consensus and lead to distinct clusters, which may adopt maximally opposing views, resulting in bipolarization (Flache et al., 2017).

Agent-based model for retrofit decision-making

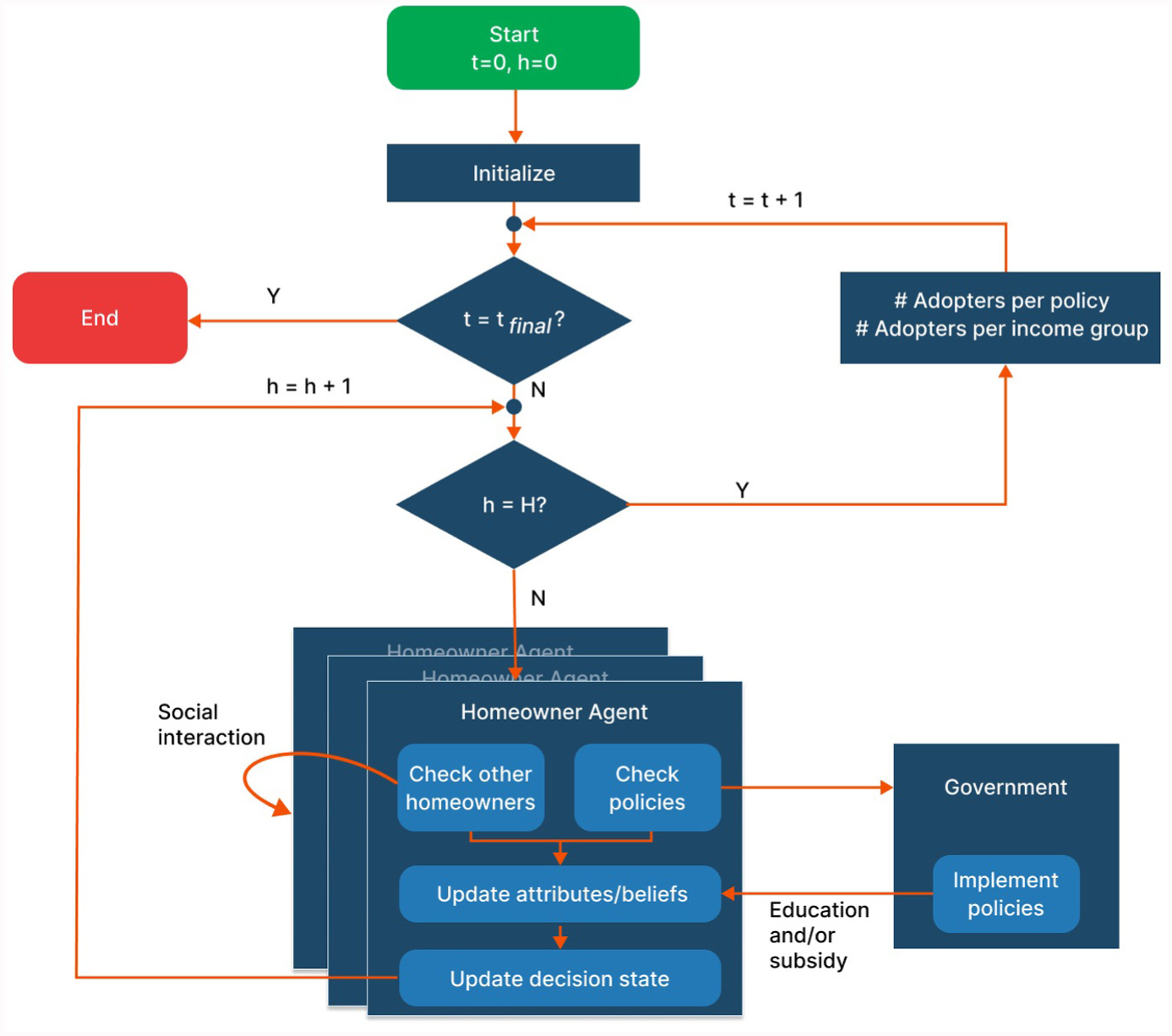

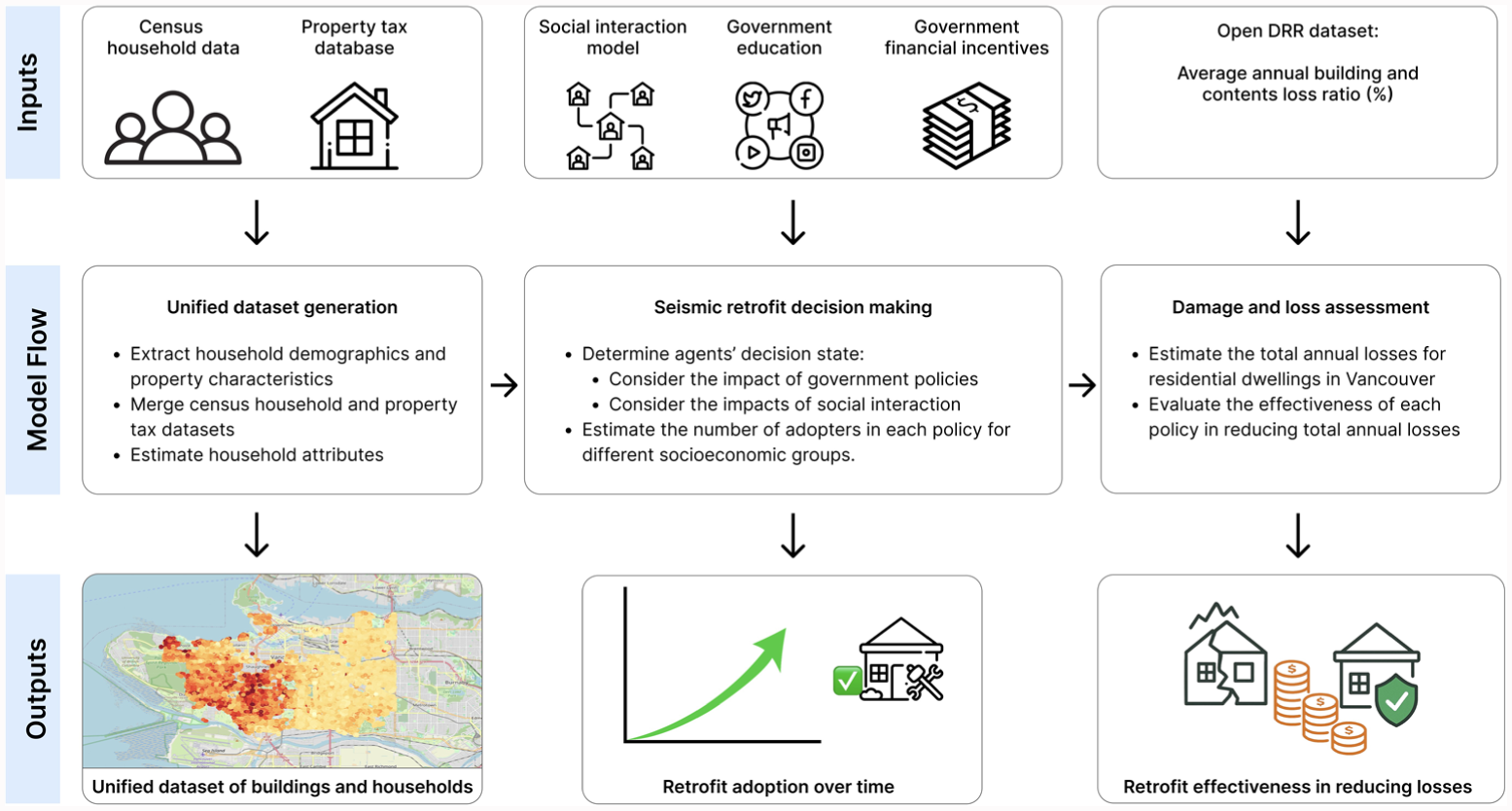

As discussed above, seismic risk mitigation adoption is a complex process influenced by multiple intertwined factors. This study develops an agent-based model to investigate the impact of potential policy interventions to encourage homeowners to adopt seismic retrofit measures. Agent-based models simulate complex processes as a product of multiple interactions between heterogeneous agents. These agents have attributes that define their characteristics and behaviors and determine how they interact with each other. Agents exist in an environment which can impose pressure or constrain the agents’ actions. In our model, households are the primary agents; their attributes represent their demographics, and the main behavior modeled is their attitude toward seismic retrofit (e.g. adopt or not adopt). The environmental pressures represent policies deployed by local authorities that facilitate the adoption of seismic retrofit measures. These retrofit promotion policies may include running educational campaigns to improve knowledge about earthquake risks and consequences, creating value for seismic retrofitting, improving peoples’ beliefs about seismic retrofit efficacy, or providing financial incentives to convince homeowners to retrofit their dwellings. A scenario-based approach is taken to investigate how running seismic retrofit promotion policies would compare to a baseline scenario regarding the total number of agents adopting the seismic retrofit measures and the corresponding reduction in total annual losses to residential dwellings. In the following subsections, we discuss the decision-making process for seismic retrofitting, attributes of Homeowner Agents, the influence mechanisms of government policy interventions, and the dynamic interactions among agents. Figure 1 presents the agent-based model evaluation steps.

Agent-based simulation model flowchart (H = number of homeowners,

Agent’s decision state

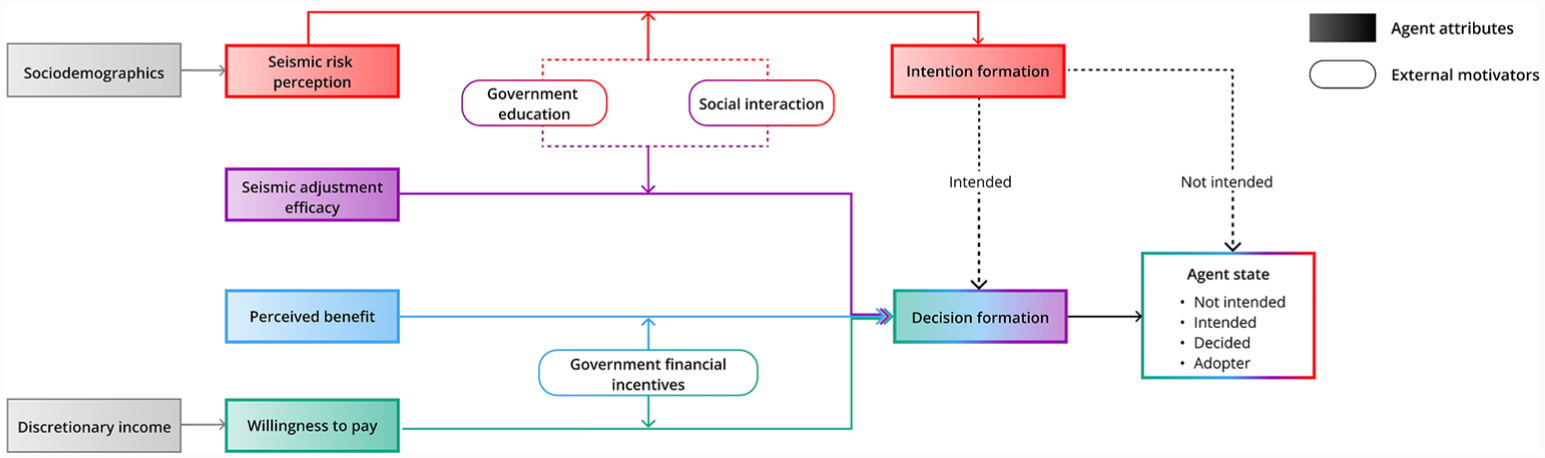

Each Homeowner Agent follows a decision-making process influenced by their attributes and external motivators. Depending on the final levels of these attributes, each agent falls into one of four possible states: (i) Not Intended, (ii) Intended, (iii) Decided, or (iv) Adopter. Agents in Not Intended state are not willing to consider the seismic retrofit measures due to low-risk perception. These agents do not recognize earthquakes as a serious threat to their life and property. Intended agents have a sufficiently high-risk perception but choose not to retrofit due to low perceived benefit and seismic adjustment efficacy attributes. While they understand earthquake risks and potential consequences, they do not believe that seismic retrofitting effectively protects life and property or provides tangible benefits. Agents in Decided state have sufficiently high levels of risk perception to understand the earthquake threat and a high level of either perceived benefit or seismic adjustment efficacy. However, the lack of financial resources prevents them from adopting seismic retrofitting. Finally, Adopter agents have an adequate understanding of seismic risk to consider retrofitting, recognize its effectiveness and benefits, and have sufficient financial resources to implement the retrofit measures. An overview of the decision process for a Homeowner Agent is presented in Figure 2, which explains the details of the steps inside the Homeowner Agent box in Figure 1.

Workflow of seismic retrofit decision process for Homeowner Agents.

Agent’s attributes

The attributes defined for Homeowner Agents include (i) seismic risk perception, which is the driving factor in the intention formation phase, (ii) perceived benefit, (iii) seismic adjustment efficacy, and (iv) willingness to pay, which are the governing factors in the decision formation phase. The modeling and initiation of each attribute for agents are explained in this section.

Seismic risk perception model

Seismic risk perception is an indicator of community awareness and preparedness. Numerous studies have explored how socioeconomic factors influence risk perception. According to these studies, the key determinants of risk perception include age, gender, education, employment status, income levels, household structure, and building quality (e.g. construction period, land ownership patterns) (Armaş, 2006; Fernandez et al., 2018; Kung and Chen, 2012; Lindell and Whitney, 2000; Lindell et al., 2009, 2016; Mileti and Darlington, 1997; Qureshi et al., 2021; Xue et al., 2021). Other influential factors include previous disaster experience, trust in authorities, financial savings, insurance coverage, risk knowledge and information, and cultural values and worldviews (Niforatos et al., 2024). To simulate the risk perception of our Homeowner Agents, we adopt the survey-based model developed by Niforatos et al., (2024), which estimates seismic risk perception as:

The coefficients of the regression model are presented in table 4 in the Appendix. Each

Perceived benefit

Perceived benefit is a key determinant of homeowners’ decisions to pursue seismic retrofits. Homeowners may not proceed with retrofit measures if they do not understand the tangible benefits of seismic retrofitting. The perceived benefit of Homeowner Agents is set to zero in the baseline scenario, and it responds to external motivators. Homeowner Agents consider the subsidies as a partial return on their investment (retrofit cost), and therefore, the financial incentives enhance homeowners’ perceived benefit. To model the increase in perceived benefit, we assume that if a policy provides 40% partial coverage of retrofit cost, the Homeowner Agent’s perceived benefit increases from 0 to 1 with a probability of 0.4. This modeling assumption reflects survey results conducted by Egbelakin et al. (2011), where 92% of owners stated that they are likely to adopt retrofit measures if the initial cost of implementation could be recovered.

Seismic adjustment efficacy

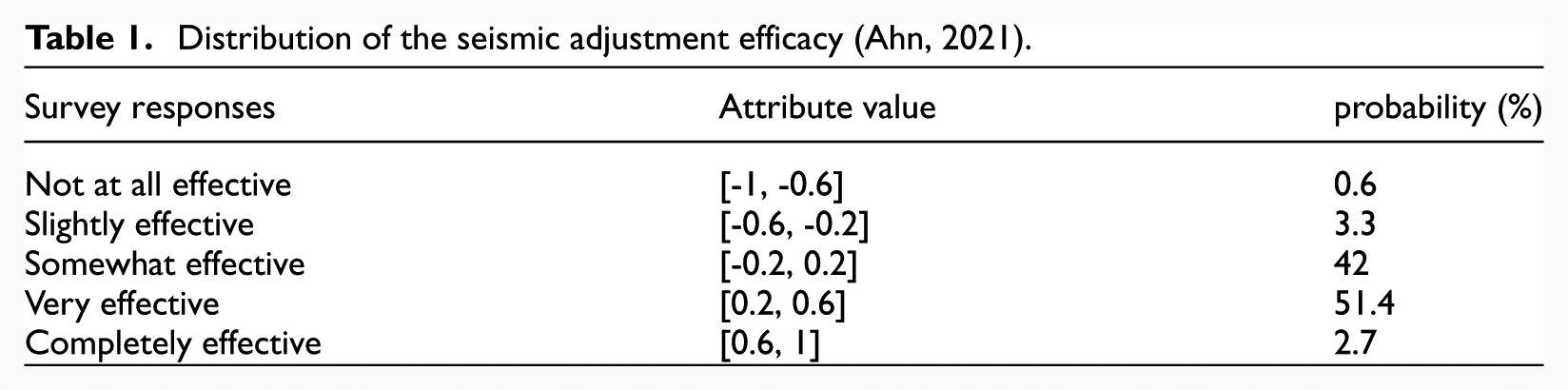

Seismic adjustment efficacy refers to the extent to which people estimate the adequacy of seismic adjustment measures to ensure protection against earthquake impacts and has been shown to influence an individual’s decision to adopt mitigation measures (Mulilis and Duval, 1995). Here, the seismic adjustment efficacy attribute is assigned a value between −1 and 1. A value less than −0.5 represents Homeowner Agents who do not believe in the effectiveness of retrofits in protecting lives and properties. A value larger than 0.5 indicates an agent with a strong positive opinion regarding in effectiveness of retrofits. Similar to seismic risk perception, the Homeowner Agent’s seismic adjustment efficacy attribute values are subjected to change when exposed to government education campaigns or social interaction with other agents. The seismic adjustment efficacy attribute for agents is estimated using the results of a survey conducted in Seattle, USA (Ahn, 2021), as shown in Table 1.

Distribution of the seismic adjustment efficacy (Ahn, 2021).

Willingness to pay

Willingness to pay (WTP) for retrofitting is among the influencing factors in the formation of the decision to adopt the retrofit measures. Willingness to pay is modeled as a function of the household’s discretionary income, the presence of the mortgage, and government subsidies. The willingness to pay attribute takes values between 0 and 1 and is defined as:

This equation specifies that if the Homeowner Agent paid off their mortgage, their willingness to pay for the retrofit measures is maximum (i.e. 1). On the contrary, if the household has a mortgage, the willingness to pay for retrofitting depends on their discretionary income and government contribution in covering the retrofit cost. Therefore, the agent’s willingness to pay increases in the presence of subsidies.

Policy interventions

In this study, the local government implements retrofit promotion policies to convince homeowners to retrofit their dwellings. These policies act as environmental forces on the Homeowner Agents. These policy interventions target specific Homeowner Agents to expedite intention and decision formation phases, affecting their seismic risk perception, seismic adjustment efficacy, perceived benefit, and willingness to pay. Two types of policy interventions are considered: educational measures and financial incentives.

Government education program

Government-led public education campaigns vary in frequency and reach, influenced by objectives, target demographics, and available resources (Humphreys et al., 2024).

In this study, the educational measures are designed in a 5-year time frame with biannual frequency and a probability of exposure equal to 0.5. When exposed to these measures, Homeowner Agents’ risk perception and seismic adjustment efficacy increase at a rate referred to as the policy impact factor

In addition, it is assumed that each subsequent exposure to educational campaigns has a diminishing effect on the increase in households’ risk perception and seismic adjustment efficacy. This reflects that the novelty of the information decreases with repeated exposure. With this, the increase in risk perception and seismic adjustment efficacy is estimated as:

where

Government financial incentives

Financial assistance mimicking the EBB retrofit in California (California Residential Mitigation Program, 2024b) is also simulated as an external motivator. Financial assistance adds to the household’s discretionary income, increasing the Homeowner Agent’s willingness to pay. Also, the agent’s perceived benefit of the retrofit program is set to increase proportionally to the subsidy amount. For example, if a homeowner’s perceived benefit attribute is zero and receives subsidies equal to 40% of the retrofit cost, their perceived benefit increases to 1 with a probability of 0.4. With this added incentive, the household decides whether to adopt the retrofit measures.

One of the challenges that local government may face is that a portion of the population who hold a negative attitude regarding retrofitting would not consider spending the budget on promoting seismic retrofitting and fair use of public resources. To include this in the simulation model, a grievance function is defined such that if a policy involves substantial government subsidies, the opinion of the agents who are not in favor of the retrofitting becomes more negative proportional to the scale of government investment in the program. This group of agents may influence the opinion of the other owners during social interaction within their network. The grievance function acts as the opposite of the education measures, in which a negative wave is created proportional to the budget spent by the government and propagated among agents through social interactions.

Agent’s interactions

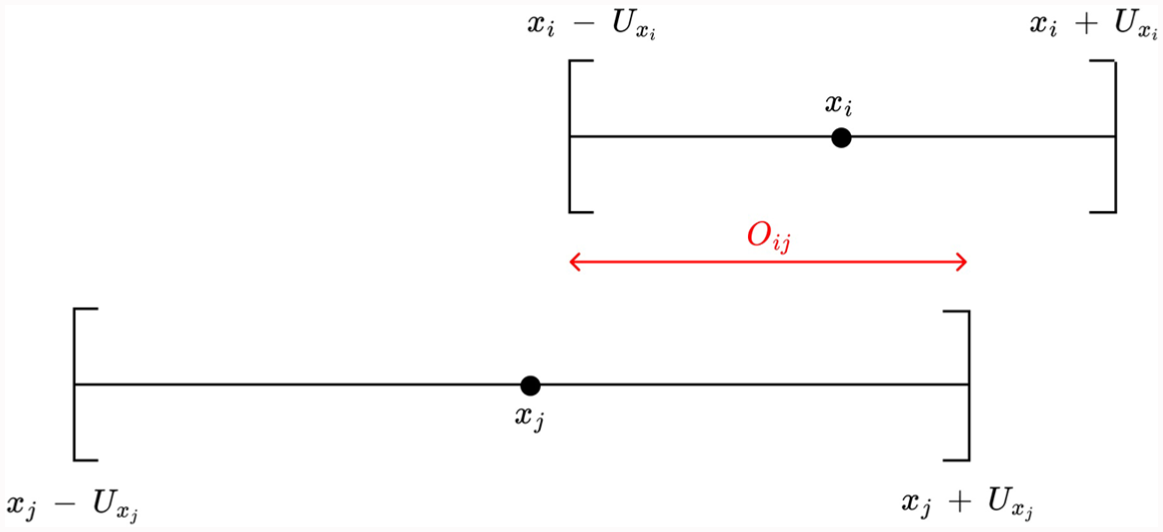

In this study, the relative agreement model (Deffuant et al., 2000, 2002, 2005; Meadows and Cliff, 2012) is used to characterize the change in Homeowner Agents’ opinions about seismic retrofits due to social interaction with other agents. The choice of the similarity-biased model class is consistent with the existing literature that considered the impact of social interaction among agents in different areas such as seismic (Kashani et al., 2019) and flood risk mitigation (Haer et al., 2017; Husby, 2016; Husby and Koks, 2017) and energy technology adoption (Rai and Robinson, 2015; Robinson et al., 2013). The Homeowner Agent’s attributes influenced by the social interaction are seismic risk perception and seismic adjustment efficacy. Consider a population comprised of n agents, and we want to explain the interaction between two agents i and j. Say

where

and their uncertainty level as:

where

Interaction mechanism between agents i and j with attribute x (adapted from Deffuant et al., 2000).

The relative agreement model accounts for the asymmetric influence of individuals with lower uncertainty about their beliefs (Deffuant et al., 2000, 2002; Meadows and Cliff, 2012). These agents, due to their higher confidence, are more persuasive and capable of influencing others’ opinions. Risk perception and seismic adjustment efficacy attributes are subject to change during agents’ social interactions. The corresponding uncertainty level for each attribute is assumed to be proportional to the inverse of the absolute attribute value (Deffuant et al., 2000; Meadows and Cliff, 2012). For the social interaction model, the opinion of an individual is between −1 and 1, where −1 and 1 represent the agents with extreme negative and positive opinion, and its uncertainty is between 0.0 and 2.0 (Meadows and Cliff, 2012). At each time step, each agent interacts with a network of connections. Each network is assumed to consist of 10% local connections who are located within the same neighborhood and 90% non-local connections that might be located anywhere in the city (Rai and Robinson, 2015). The probability of interaction among agents in a social network is defined as the probability that agents exchange opinions about seismic risk and the effectiveness of retrofit measures in every time step. The social interaction among agents influences their attributes and beliefs, which might lead to changes in their behavior or decisions regarding adopting seismic retrofitting over time.

Case study

We apply the developed agent-based model to a case study of Vancouver, British Columbia, Canada, to evaluate homeowners’ response to government-led seismic retrofit promotion policies. The case study is restricted to owner-occupied, detached dwellings built between 1900 and 1972. Dwellings built after 1973 were designed under upgraded seismic regulations in the building code, and dwellings built before 1900 require more advanced seismic retrofitting than common methods (Hobbs et al., 2021). We assume the local government seeks to maximize the number of retrofitted dwellings in Vancouver by running educational campaigns and providing subsidies. The effectiveness of the policy interventions is evaluated in the context of the reduction in total annual earthquake-induced losses to residential dwellings in Vancouver. A scenario-based approach investigates how different seismic retrofit promotion policies compare to a baseline scenario with no policies. An overview of the simulation framework is shown in Figure 4. The Homeowner Agents’ attributes are estimated using Census data. Homeowner Agents may be exposed to government intervention policies, which influence their decision whether to retrofit their dwelling considering the effect of interacting with other Homeowner Agents within their social network to determine the overall retrofit take-up rate upon implementing each policy. Then, the reduction in total annual losses to residential building structures and contents is estimated to evaluate and compare the effectiveness of the retrofit promotion policies.

Overview of the simulation framework.

Data sets used in the study

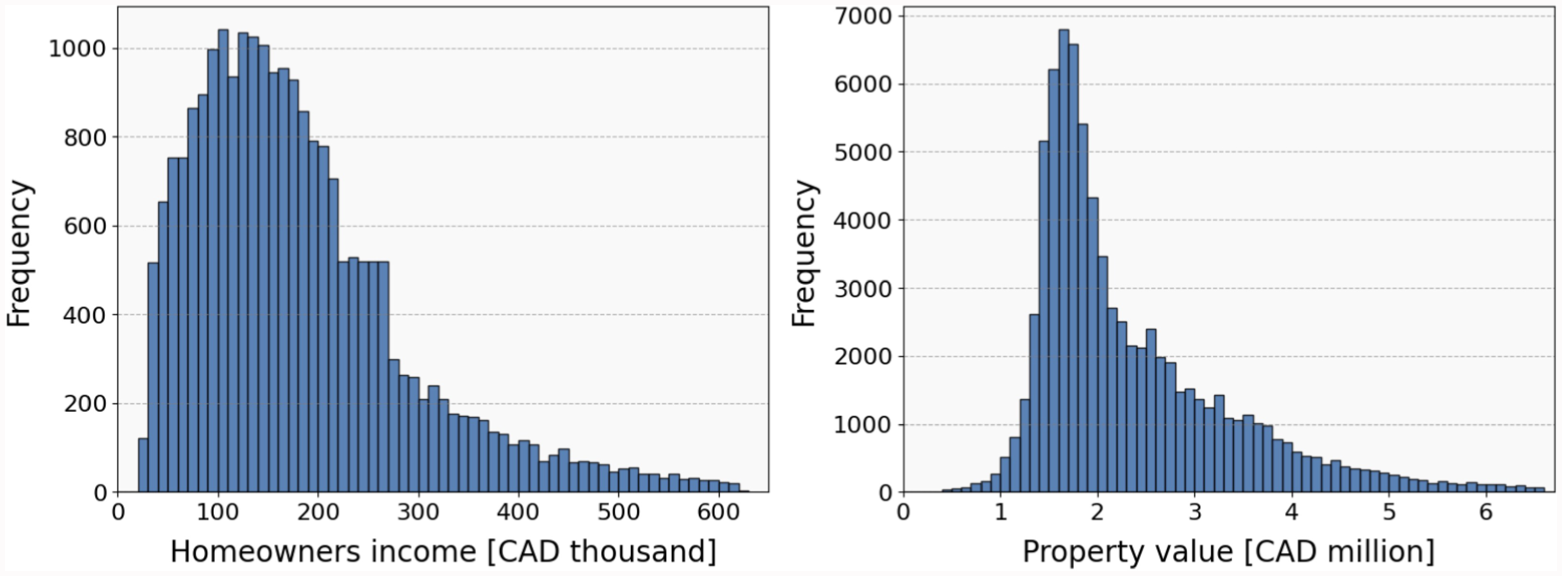

This section describes the datasets used in the study, which include the 2021 Census Public Use Microdata (PUMF) (Statistics Canada, 2021) and the 2022 City of Vancouver property tax database (City of Vancouver, 2022). The 2021 census PUMFs provide access to non-aggregated socioeconomic demographic data covering a sample of the Canadian population. In this tabular data set, each row represents the anonymized responses of one household. We collected PUMFs for the Vancouver Census Metropolitan Area (CMA) code, filtering by tenure status and type of dwelling. We collected data on household income, size, and type, as well as age, gender, and highest level of education of the householder. Households’ incomes were inflated from 2021 to 2022 using consumer price indexes to match the property values from the 2022 property tax database. The median household income of Vancouver-detached homeowners in 2022 dollars was CAD $158,000. Households are separated into three income tiers relative to area median income (AMI): low-income (less than 80% AMI), moderate-income (between 80% and 120% AMI), and high-income (above 120% AMI). The 2022 City of Vancouver property tax database provides land value, improvement value, civic address, and year-built information. The property civic addresses are used to find the geolocations in Vancouver. Figure 5 represents the distribution of single detached homeowners’ income and property values in Vancouver.

Distribution of single detached homeowners’ income and property values in Vancouver.

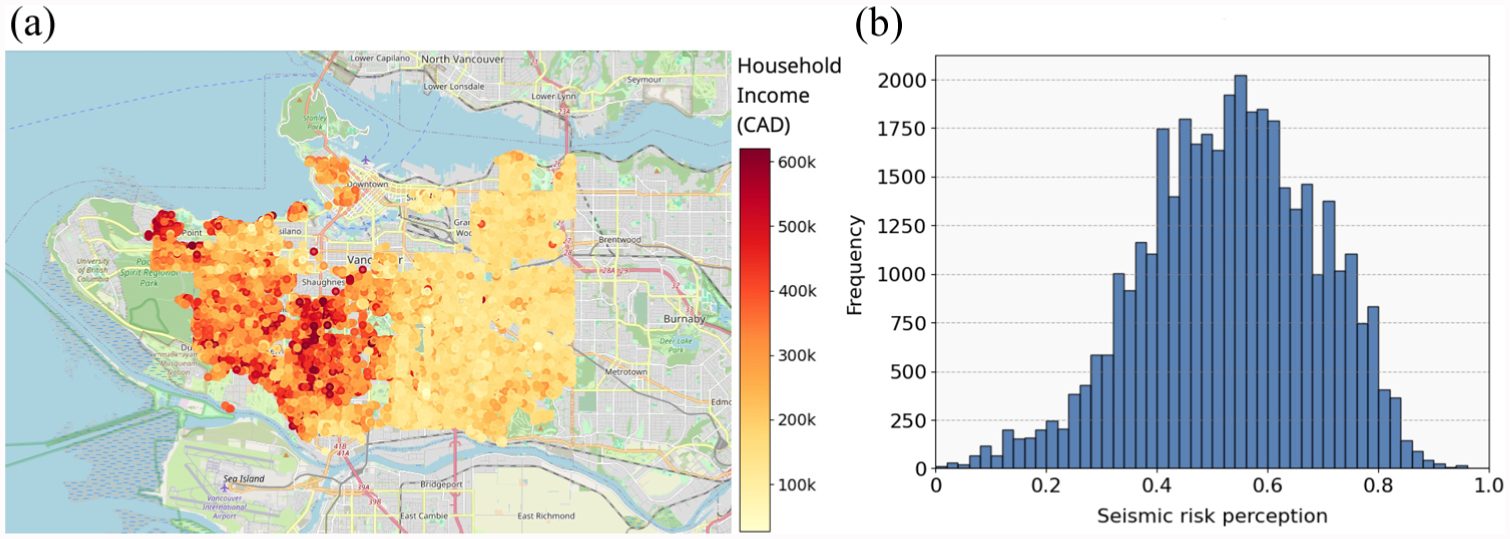

Ideally, we would connect each dwelling in the tax assessor data to one household in the Census PUMFs. However, the PUMFs represent only a subset of all respondents and do not contain location information. To merge the two databases, we assumed a perfect correlation between household income (in the PUMFs) and property values (in the tax assessor data). This method yields a unified data set with household demographics and property characteristics. Although the perfect correlation assumption between property value and household income is not ideal, it allows us to persevere the correlation between household demographics (i.e. income, age, gender, household type and size, and education level). The distributions of household demographics further illustrate this before and after merging with the property tax database in Figures 12–14 in the Appendix. Figure 6a demonstrates the detached dwellings in the City of Vancouver along with the distribution of households’ income, where each dot on the map represents a property and the corresponding household assigned to it.

Detached dwellings in the City of Vancouver and risk perception distribution among homeowners: (a) detached dwellings in the City of Vancouver along with the distribution of households’ income and (b) distribution of seismic risk perception of Vancouver-detached homeowners.

The discretionary income,

where

Policies

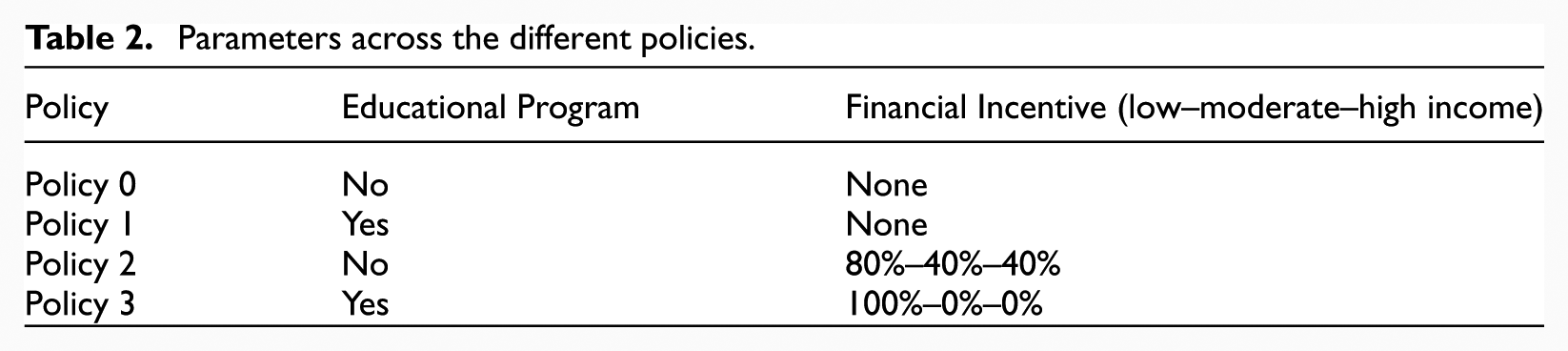

The summary of the policy intervention parameters considered in this study is provided in Table 2. Policy 0 serves as a baseline case with which to compare. Similarly, Policies 1 and 2 were selected to observe the results of the educational campaign and financial incentive programs separately. The EBB initiative inspired the cost coverage ratios in Policy 2 in California, where 40% of the retrofit cost is covered for moderate- and high-income households and 80% for low-income households (California Residential Mitigation Program, 2024c). Policy 3 investigates the effects of joint educational measures and financial support for low-income homeowners (100% retrofit cost coverage) to maximize the retrofit take-up at a lower cost.

Parameters across the different policies.

Results

This section presents the results of the agent-based simulations model across each policy. A sensitivity analysis is presented in Figures 10 and 11 in the Appendix to assess which variables contribute more heavily to the observed simulation results.

Effectiveness of educational campaigns and social interactions on risk perception

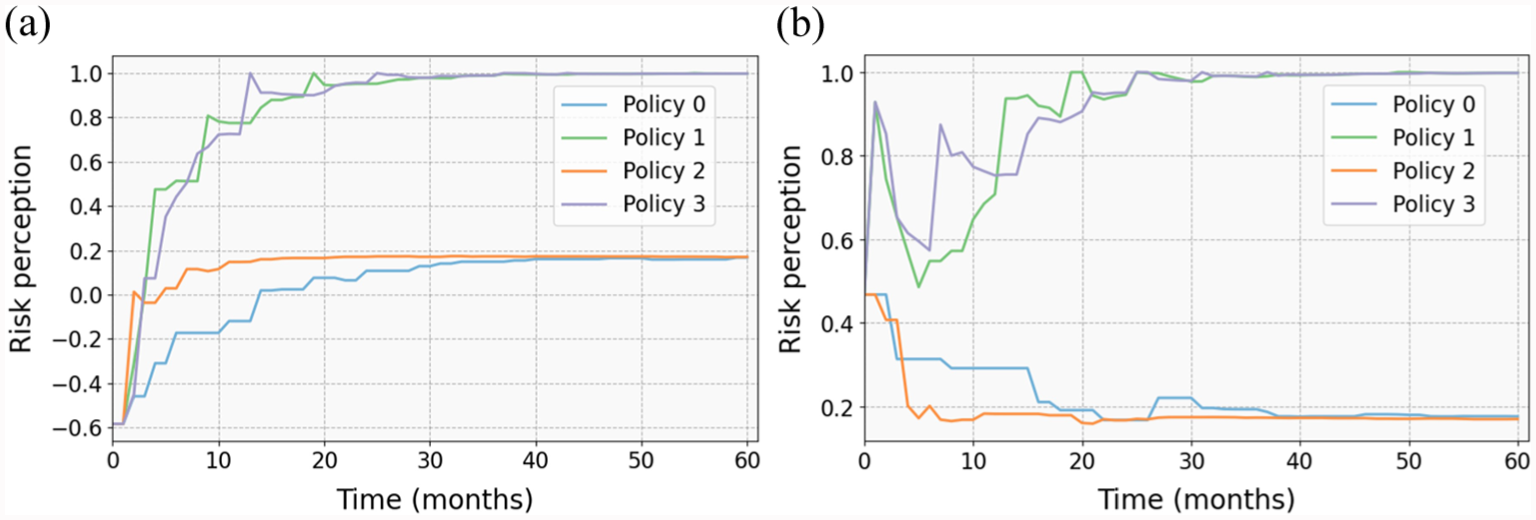

Figure 7 provides context about the model by showing how the risk perception of 2 Homeowner Agents changes within a realization. Figure 7a shows an agent’s initial low-risk perception. Policies 1 and 3, which include an educational component, substantially improve risk perception. Figure 7b shows an agent with an initial risk perception of 0.47, who has a relatively high risk perception but has uncertainty about it. This uncertainty is translated into the fluctuations in risk perception. In policies 0 and 2, the agent’s risk perception reaches a value close to 0.2, while in policies 1 and 3, it maximizes at 1 after 32 months. The reason why risk perception stabilizes at 0.2 for both agents lies in the principles of the relative agreement model, which stipulates during social interaction, agents influence each other toward reducing the differences in their opinions, eventually leading to the formation of multiple clusters of opinions in the entire population (in this case, 0.2 is one of the opinion clusters). A similar pattern exists regarding the influence of educational campaigns on the seismic adjustment efficacy attribute of Homeowner Agents. More details on the distribution of agents’ attributes over time across different policies could be found in Ahmadi (2025).

Agent’s risk perception over time across all policies: (a) agent with an initial risk perception of −0.59 and (b) agent with an initial risk perception of 0.47.

Effectiveness of educational campaigns and financial incentives on retrofit adoption

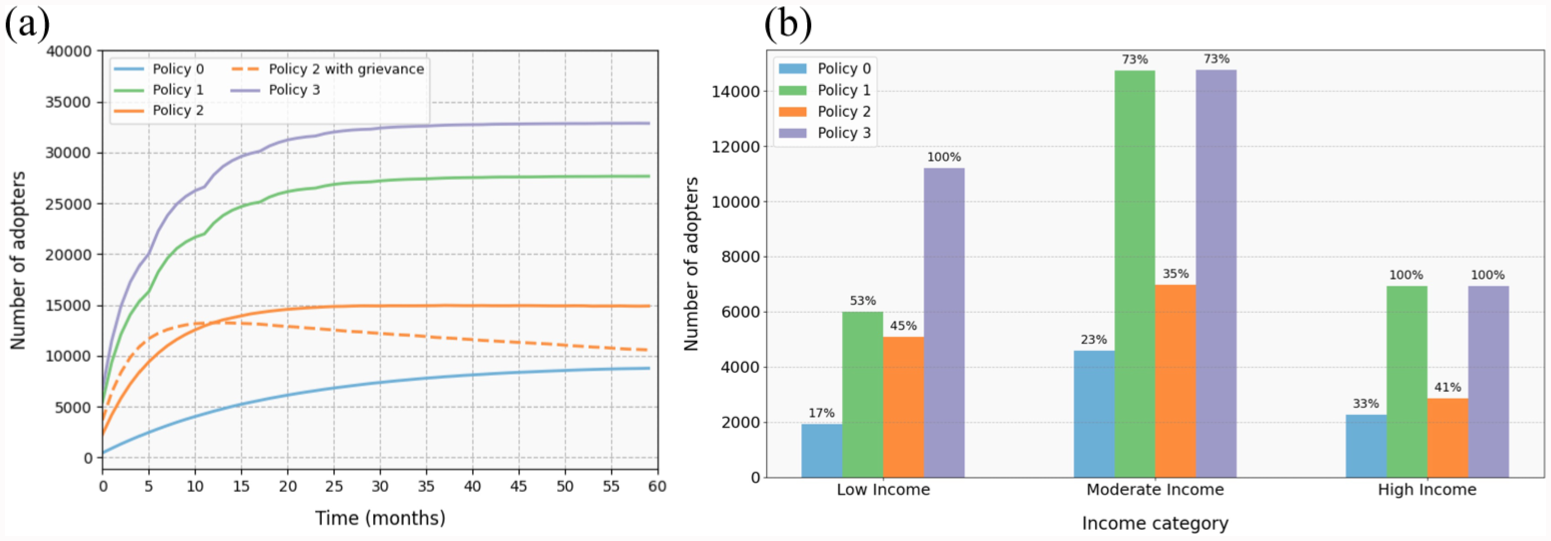

Figure 8a presents the total number of agents in the adopter state across different policies. In Policy 0, the number of adopters reaches 8863 (around 23% of the population), which is in agreement with the findings of Kashani et al. (2019) with a similar proportion of agents in adopter state in the baseline policy within a 5-year time frame. Local governments are often required to update their hazard mitigation plans every 5 years to remain eligible for certain federal assistance programs (Federal Emergency Management Agency, 2025). In Policy 2, where subsidies are introduced, the total number of adopters increases to 14,936 (39% of the population). The effect of the grievance function when implementing Policy 2 is shown with a dashed line. The number of adopters in this case reached 13,000 after 10 months and then reduced to 10,500 after 60 months. This is explained by the negative impact of government investment on the attitude of the Homeowner Agents who are already against the retrofit policy. These agents then influence other agents’ opinions over time to discourage them from adopting retrofit measures. Policy 1, which involves an education campaign, resulted in a total number of 27,679 (72% of the population) adopters after, while Policy 3, which combined education and subsidies, led to the highest overall number of adopters of 32,887 (86% of the population).

Number of agents in adopter state across different policies and different income groups: (a) number of adopter agents in different policies and (b) number of adopter agents in different income groups.

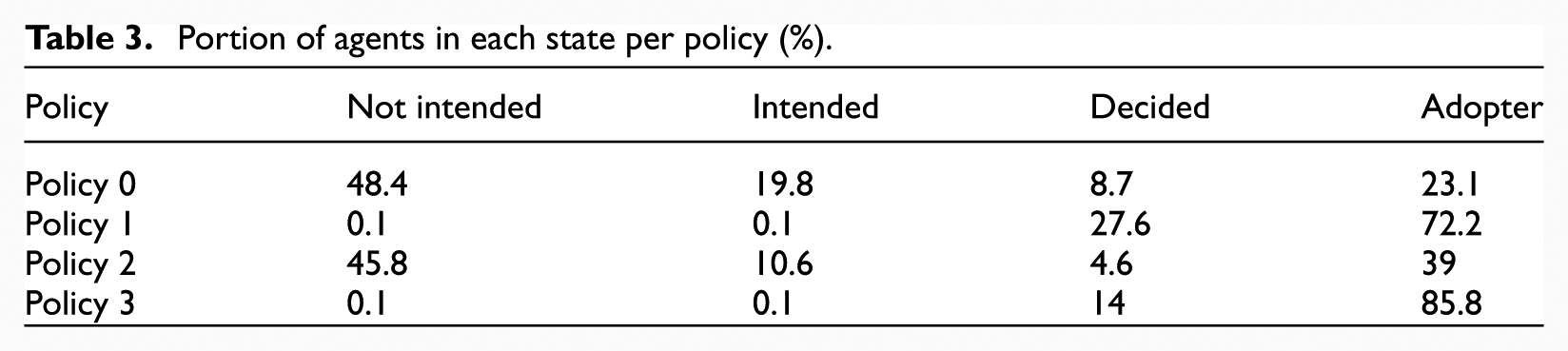

Table 3 presents the number of agents in each decision state per policy. In Policy 0 where government does not implement any retrofit promotion or incentive policy, 77% of the population are in Not Intended, Intended, and Decided states and do not adopt the retrofit measures. These results align with the findings of Zhang et al. (2022) and Egbelakin et al. (2011), stating that without government intervention, most homeowners are reluctant to adopt retrofit measures even though they are aware of their region’s susceptibility to seismic risk.

Portion of agents in each state per policy (%).

Figure 8b provides more insight into the effects of the retrofit promotion policies on the retrofit take-up rates across different income groups. In the baseline policy, retrofit adoption rates increase with income, indicating disparities among low, moderate, and high-income groups. Policy 2, which offers partial retrofit cost coverage, significantly enhances the adoption among low-income homeowners but has a smaller effect on higher-income groups. Educational campaigns in Policy 1 substantially improve adoption across all groups, suggesting that the bottleneck in achieving high retrofit take-up rates is educating homeowners about the seismic risk and devastating potential consequences of earthquakes, particularly among moderate and high-income groups. Policy 3, combining full-cost coverage for low-income households with education, yields the highest adoption rates across all income groups. Providing the full coverage of retrofit costs for low incomes helps homeowners who are in intended or decided states to become adopters. These agents have sufficiently high seismic risk perception, seismic adjustment efficacy, and/or perceived benefit, and the cost of retrofitting measures is the main barrier to adoption. High-income owners are those whose income exceeds CAD$240,000. For these homeowners, the discretionary income calculated using Equation 7 exceeds the cost of the retrofit. Consequently, the only barriers for them adopting seismic retrofits are those related to their perception of earthquake risks and retrofit benefits. Therefore, achieving a 100% adoption rate in Policy 3 demonstrates the impact of education on improving their risk perception/seismic adjustment efficacy attributes. The reason for not achieving a 100% adoption rate among the moderate-income group in Policy 3 is that this group spans a wide income range (CAD 100,000–240,000). Some households on the lower end of this spectrum may still require financial assistance to adopt retrofit measures but are not eligible for subsidies under this policy.

Effectiveness of policies in reducing earthquake losses

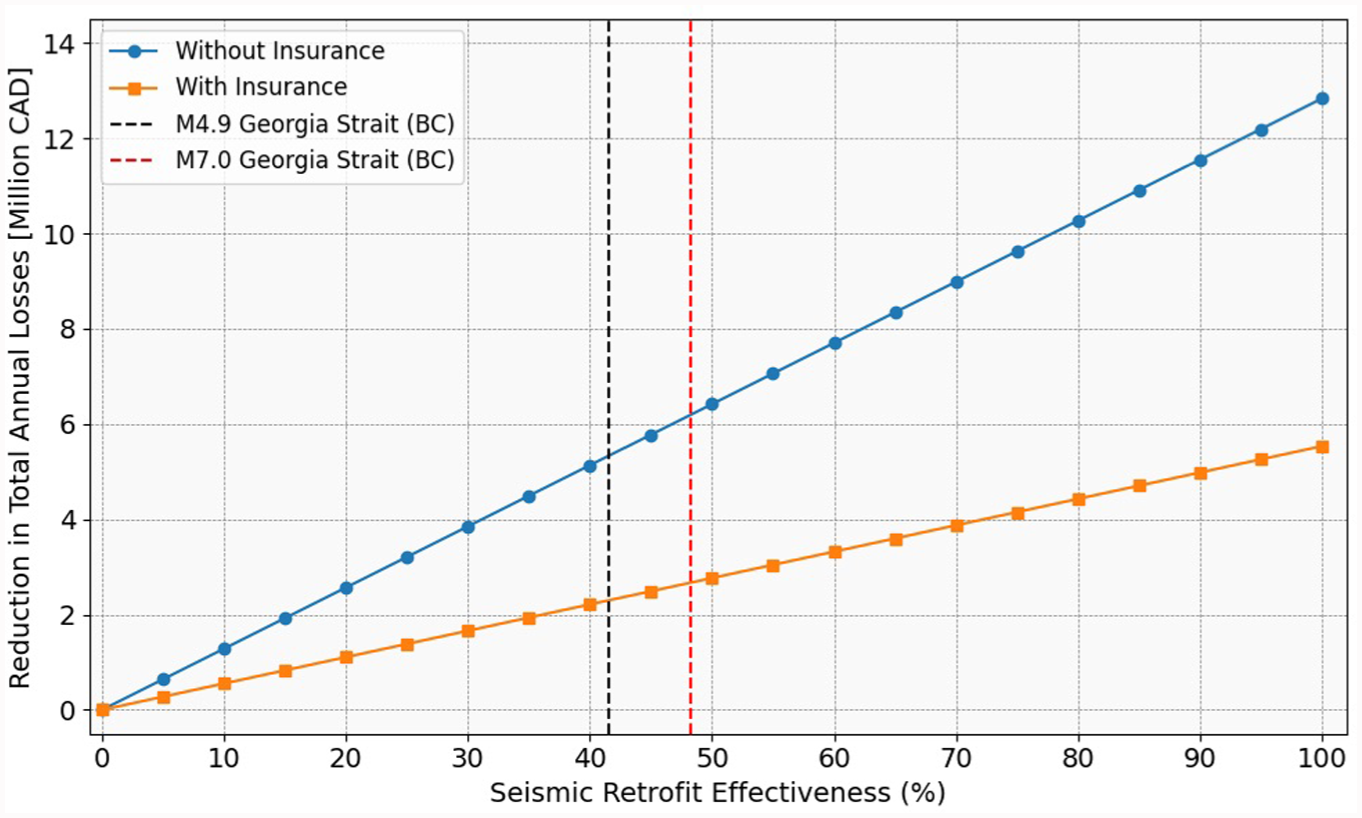

This section provides a simplified assessment of the effectiveness of seismic retrofitting in reducing earthquake-induced losses. Data representing the average annual losses (AALs) to building structures and contents are extracted from the National Canadian Earthquake Risk Profile developed by the Geological Survey of Canada (Risk Profiler, 2025). These loss ratios are multiplied by total exposure to estimate the total annual losses for residential dwellings in the city of Vancouver. This probabilistic risk assessment method accounts for uncertainty in earthquake magnitude, location, frequency, and ground motion propagation. It considers all possible earthquakes that could affect a location, their probabilities, and their potential impacts. Figure 9 illustrates the reduction in total annual losses to the structure and contents of single-family buildings under two scenarios: (i) without insurance and (ii) with insurance. For insured buildings, it is assumed that the insurance will be triggered, and the homeowner will only pay the deductible (12.5% in British Columbia (Goda et al., 2020)). Moreover, retrofitted homes may still experience losses. Data from the Canadian National Earthquake Scenario Catalog (Hobbs et al., 2021) suggest that for hypothetical M7.0 and M4.9 earthquakes in the Strait of Georgia, seismic retrofitting results in 48.2% and 41.5% reductions in losses for wood-framed single-family dwellings with cripple walls in Vancouver. For completeness, Figure 9 shows results for multiple values of retrofit effectiveness. Comparing Policy 1, Policy 2, and Policy 3 under these conditions, we observe a reduction of CAD $1.8, $1.0, and $2.2 million in insured total annual losses for single-family buildings. From a policy perspective, this suggests that government investments in retrofit promotion (e.g. through educational campaigns or subsidies) can be cost-effective, provided the total intervention cost is less than the avoided losses. While this exercise provides initial figures, a more robust assessment of costs and benefits would require collaboration between public agencies and private stakeholders, including the insurance and construction sectors.

Reduction in total annual losses to single-family residential building structures and contents based on retrofit effectiveness in the City of Vancouver.

Discussions and limitations

The problem tackled in this study is complex, and its modeling has limitations. First, our results suggest high retrofit adoption rates for policies incorporating educational campaigns (72% in Policy 1 and 86% in Policy 3). However, a limitation of the agent-based model lies in its assumption of rational behavior among agents. That is, we assume that an individual with the intention and resources to retrofit their home will do so. In reality, human risk-based decision-making might deviate from rational behavior due to cognitive biases, emotional responses, or misinformation (Kahneman, 2011; Slovic, 1987).

Second, educational campaigns and programs are complex interventions with varying effectiveness depending on factors such as content quality, delivery platform, and target population. This study models this effectiveness via a single parameter agnostic to the target population,

Third, the model is comprised of different components that are based on empirical data. For example, the attributes of Homeowner Agents in the agent-based model, including risk perception, seismic adjustment efficacy, perceived benefit, and willingness to pay, are modeled based on available studies in the literature but employed using demographic data from Vancouver homeowners from the Census PUMF and property information from the City of Vancouver tax assessor database. While this approach does not validate the model as a whole, it guarantees that its building blocks are robust. We believe that such a model is better used as a tool to support decisions rather than making them. While the model includes assumptions that may not accurately reflect future realities, these assumptions are consistent across all simulations. Thus, we envision that the relative results between baseline and improved scenarios inform the magnitude of the potential benefits of a policy because such assumptions will have limited influence on the interpretation of the relative results.

We believe that many of the limitations in our current model could be substantially mitigated by a survey of the population of interest (e.g. residents of Vancouver). Surveys are a common method for estimating population attributes within the community under study. In this research, existing models and surveys from the literature were used to estimate the relevant attributes of Vancouver’s detached homeowners for the decision-making model. For example, survey results conducted in Greece and Seattle were used to estimate the seismic risk perception and seismic adjustment efficacy attributes of the Homeowner Agents. However, collecting data through surveys specifically targeting detached homeowners in Vancouver would help better calibrate and validate the model.

Conclusion

We develop an agent-based model to evaluate the impact of potential seismic retrofit promotion policies. In this framework, households are modeled as agents with attributes reflecting their demographics and behaviors related to seismic retrofitting decisions. Policy interventions, such as subsidies and educational programs, are implemented by local authorities to encourage the adoption of seismic retrofit measures. The effectiveness of the government-led seismic retrofit promotion policies is evaluated in terms of the total number of adopter agents and the reduction in total annual losses to residential building structures and contents in the City of Vancouver. Annual building and content losses, with and without retrofits, are obtained from the Canadian National Earthquake Scenario Catalog (Risk Profiler, 2025).

The results suggest that a combination of educational programs and retrofit cost subsidies for low-income households yields the highest adoption rates and the largest reduction in total annual losses to detached residential dwellings. However, our results show focusing only on an educational campaign can achieve similar results in terms of adopters and loss reduction. Educational campaigns target seismic risk perception and seismic adjustment efficacy attributes of the homeowners. The model highlights that risk perception is the main barrier for moderate- and high-income groups, while the combination of risk perception, willingness to pay, and perceived benefits (tangible financial returns) are the factors impeding the adoption of retrofit measures among low-income homeowners. Survey results conducted on detached homeowners in the City of Vancouver can be used to calibrate the model and estimate the agents’ attributes that influence seismic retrofit decision-making.

The analysis on the effectiveness of retrofit promotion policies in reducing earthquake-induced annual losses suggests that government investment in education or subsidies could be cost-effective provided that the implementation costs remain below the projected savings in avoided losses. The model results could be used to inform local government what would be the viable annual budget to be spent on seismic risk reduction strategies. A more comprehensive cost-benefit analysis is needed, involving collaboration between public agencies, insurers, and the construction industry to quantify implementation costs, co-benefits, and risk-sharing mechanisms.

This study contributes both methodologically and quantitatively to the development of effective seismic risk mitigation policies. By modeling policy impacts before implementation, policymakers can better evaluate and refine strategies to minimize damage and losses in future seismic events.

Footnotes

Appendix 1

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The second author received financial support from his Discovery Grant from the Natural Sciences and Engineering Research Council of Canada (RGPIN-2023-03537).