Abstract

In their recent article, Theissen et al. (2023) re-examined the seminal study of Kim and Bettis (2014) on the positive relationship between firms’ cash holdings and firm value. Theissen et al. (2023) improved on the original Tobin's q measure used to capture firm value and found that—in contrast to the results of Kim and Bettis (2014)–there are not decreasing but increasing returns to holding cash. Separately, Souder et al. (2024) made various methodological improvements and developed a new measure of forward-looking firm value, ultimately finding no relationship between cash holding and value at all. In this article, we combine all methodological refinements made after the original study of Kim and Bettis (2014) into a single analysis. We find that Kim and Bettis’ (2014) original results are correct, despite the numerous limitations of their method.

Keywords

The debate on cash holdings and firm value

Scholars have long debated the effect of firms’ cash holdings on firm value and presented conflicting empirical results. The cash–performance relationship is a theoretical and empirical conundrum (George, 2005). This is because agency theory suggests that large cash holdings give managers the option to use corporate resources in a disciplined fashion, reducing allocative efficiency (Jensen, 1986), and thus firm value. In contrast, the behavioral theory of the firm suggests that large cash holdings may be beneficial because they allow resolving intra-organizational conflicts (Cyert & March, 1963), benefitting firm value. Empirical research has—dependent on various contextual factors—found positive, null, or negative effects of cash holdings on firm value (e.g., Frésard & Salva, 2010; Kalcheva & Lins, 2007).

Kim and Bettis (2014) performed the arguably most influential study, the results of which were confirmed in follow-on studies (e.g., Deb et al., 2017; Nason & Patel, 2016). They measured firm value using Tobin's q and found that there is a positive effect of cash on firm value but that there are diminishing returns to holding cash.

Recently, Theissen et al. (2023) re-examined this seminal study in Journal of Management Scientific Reports and found partially different results. Specifically, the authors improved the measure of firm performance to remove distortions that were introduced by the fact that the cash holding measure (i.e., cash and short-term investments) was also part of the original firm value measure's numerator (i.e., the market value of the firm) and denominator (i.e., total assets). While the positive direct effect of cash on firm value was replicated, the authors surprisingly found increasing rather than decreasing marginal returns to cash.

Recent advances in method and debate

Recently, methods researchers proposed important measurement advances that others brought into the debate on cash holdings. Specifically, Certo et al. (2020) highlighted that the use of scaled variables, i.e., ratios, may be problematic in management research. They argue that ratios are not only theoretically hard to interpret but can also have distorting effects in regression models regardless of whether they are used as independent or dependent variables. Even ratio control variables can affect the parameter estimates and statistical significance of other variables of interest. For the relationship between firms’ cash holdings and firm value, this means that the use of Tobin's q, a ratio dependent variable, is potentially problematic. Similarly, the use of any scaled controls, such as R&D intensity (i.e., R&D expenses divided by net sales; Kim and Bettis, 2014) might be a concern.

Aware of these issues and further motivated by theoretical considerations on financial performance metrics in strategy research, Souder et al. (2024) suggested a novel forward-looking measure for firm value as an alternative to Tobin's q. They built on Certo et al.'s (2020) criticism and developed a new measure of dynamic value as an unscaled alternative. Specifically, they characterized Tobin's q as a variable that gauges (expected) future performance and sought to develop a measure that captures this notion more precisely without being a ratio. To this end, they proposed to partition a firm's market value (less the firm's net current assets) into two separate components. First, a steady-state value, which captures the firm's value if nothing were to change going forward and the firm would simply produce its current cashflows in perpetuity. Second, the dynamic value is then simply the residual and captures what the market expects in future returns from the firm beyond what is already reflected in the firm's current profit levels. The authors argued that dynamic value is superior to Tobin's q not only because it is not a ratio but also because it “provides a stronger signal of expectations about as-yet-unseen future value … because it subtracts out a value derived from the already seen” (Souder et al., 2024, p. 154).

Souder et al. (2024) then used their measure in a simple demonstration in which they attempted to reproduce the main effect of Kim and Bettis (2014). Notably, they made several further changes beyond the new dependent variable. First, they included firm-fixed effects (instead of merely industry fixed effects) to capture purely within-firm variance. Second, they removed the cash flow control variable (which makes no difference to their results). Finally, to be fully consistent with the recommendations of Certo et al. (2020), they also replaced every scaled control variable with an unscaled version (they did not include net sales, the numerator of the formerly scaled variables, as an additional control because the models already included the logarithm of the number of employees as a firm size measure). Table A1 in the online appendix summarizes these changes and the rationales provided by Souder et al (2024).

Their main results only partially align with those of Kim and Bettis (2014). Specifically, whereas their specification that used Tobin's q but included firm-fixed effects, and the one using (unscaled) market capitalization as a dependent variable showed a positive direct effect of cash holdings on firm value, Souder et al. (2024) did not find a significant effect of firms’ cash holdings on firm value in the form of dynamic value. They thus concluded that it is the removal of the perpetuity value of a firm's current cashflows that drives the null finding because the effect of cash holdings “correlates with investor valuation of current cash flow, which is not captured by dynamic value” (Souder et al., 2024, p. 159). In sum, their findings suggest that the positive relationship between cash holdings and firm value can be found even when using unscaled controls and performance variables (i.e., market capitalization), but not when the unscaled performance variable is dynamic value.

Bringing it all together

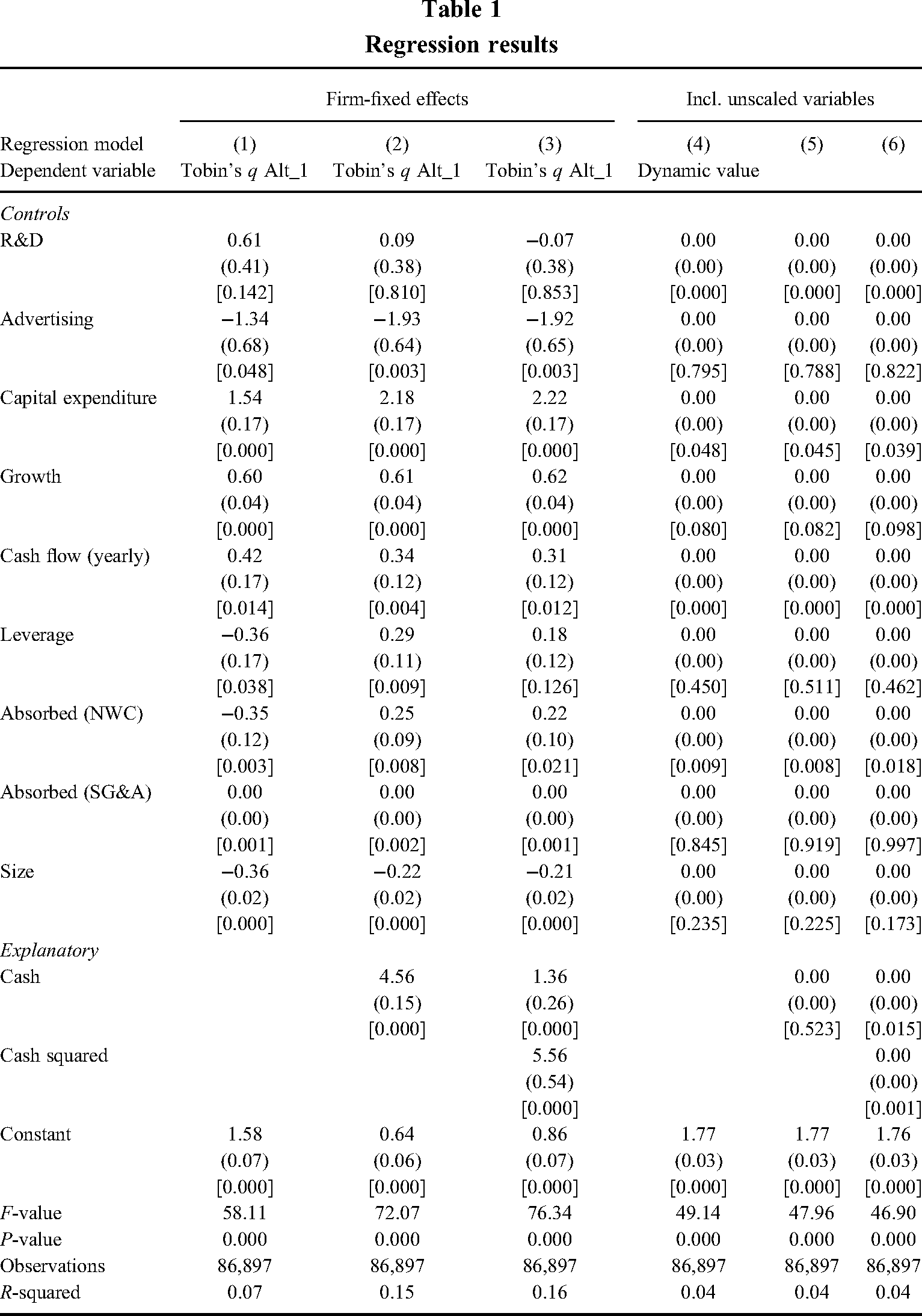

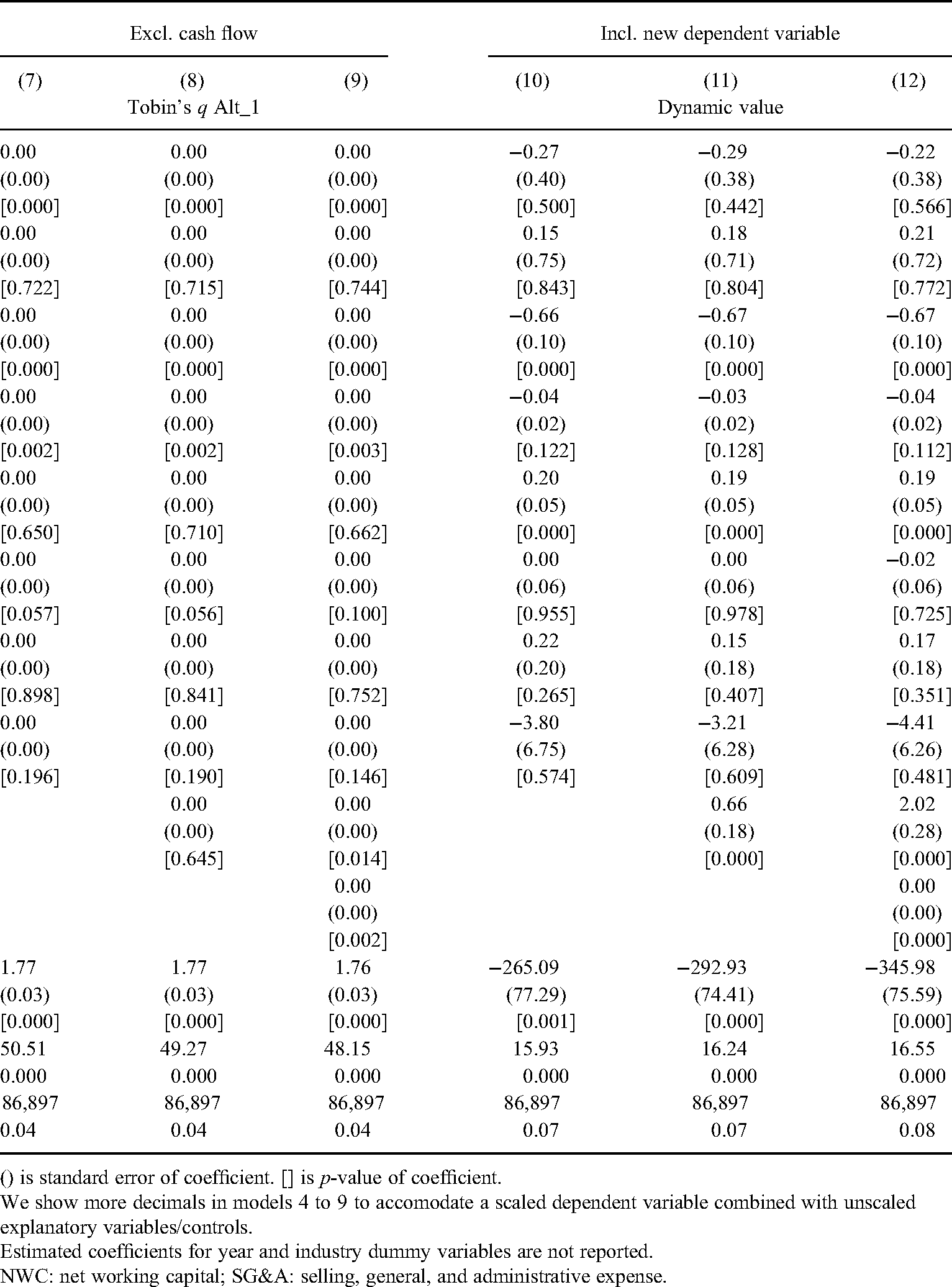

We test the robustness of the findings of both Theissen et al. (2023) and Souder et al. (2024). To this end, we run several regression models. As a starting point, we take Theissen et al.'s (2023) “Step 3” (their Table 4), which is their set of models in which they employed their improved Tobin's q measure and additionally extended their sampling period. We use their sample (but omit some observations to keep the number of observations constant across all our models; this makes no difference to our results) and perform a further re-examination.

In our analyses, we depart from Theissen et al.'s (2023) models in various ways. Specifically, we present four sets of models that incrementally introduce these departures. First, we add firm-fixed effects. We do so because this is in line with Souder et al. (2024) and with the contemporary convention in strategy research to include firm-fixed effects rather than only industry fixed effects to account for unobserved heterogeneity. Using firm-fixed effects also allows us to follow Souder et al. (2024) in not using the Prais–Winsten regression that was employed by Kim and Bettis (2014). Model 1 in Table 1 shows the control model, Model 2 adds cash holdings, and Model 3 introduces the squared term for cash holdings.

Regression results

() is standard error of coefficient. [] is p-value of coefficient.

We show more decimals in models 4 to 9 to accomodate a scaled dependent variable combined with unscaled explanatory variables/controls.

Estimated coefficients for year and industry dummy variables are not reported.

NWC: net working capital; SG&A: selling, general, and administrative expense.

Second, to resolve the potential problems brought about by ratio control variables, we follow the recommendation of Certo et al. (2020) and the implementation by Souder et al. (2024) and use unscaled variables (treating the firm size measure as a control for scale; additionally including net sales, the original denominator of the scaled variables, as a control makes no difference to our results). Table 1's Model 4 is the control model, Model 5 adds cash holdings, and Model 6 adds the squared term for cash holdings.

Third, in line with Souder et al. (2024), we remove the cash flow control. Models 7–9 include controls, add cash holdings, and the squared term for cash holdings, respectively.

Finally, we use dynamic value as our dependent variable to capture firm value (Souder et al., 2024). Models 10–12 again mirror the models in the prior step, showing a control model, a model with cash holdings, and one with its squared term.

Coming full circle and looking ahead

For brevity, we focus our discussion on the most important models and findings. As evident from Model 3, the finding of increasing positive marginal returns to cash that was presented by Theissen et al. (2023) is not affected by the inclusion of firm-fixed effects and the necessary change in the estimation approach. This was to be expected, as prior deviations from Kim and Bettis (2014) on this model change found a similar main relationship (e.g., Deb et al., 2017). Importantly, however, the relationship is affected by the inclusion of unscaled independent variables (see Model 6), which yield positive but decreasing marginal returns of cash. This suggests that the results found by Theissen et al. (2023) were indeed impacted by the econometric problems identified by Certo et al. (2020), who suggested that scaled independent or control variables may introduce distortions in effect sizes and significance levels because they violate the assumptions of regression analysis. Our results remain stable when excluding the control for cash flows (see Model 9). These findings are meaningful because they suggest that the initial results of Kim and Bettis (2014), i.e., negative marginal effects of cash holdings on firm value, appear to be valid despite the methodological limitations of their analyses. When using the dynamic value measure to capture firm value, these results are further corroborated (see Model 12), and we again find a positive relationship between cash holdings and firm value, but with decreasing marginal returns.

In sum, using improved methods, we reaffirm the original finding of Kim and Bettis (2014) that there is a positive relationship between cash holding and firm value (both measured as an improved Tobin's q and as dynamic value). We also reaffirm their finding on decreasing marginal effects of cash and thus challenge the newer results of Theissen et al. (2023). Using a larger sample than Souder et al. (2024), we further challenge their finding that there is no relationship between cash holding and firm value as measured as dynamic value.

Our results suggest avenues for future research. For one, prior research has identified various contingencies for the value of cash (e.g., Deb et al., 2017; Nason & Patel, 2016). It is likely worth examining whether these results hold when incorporating the recent methodological advances. For another, cash holdings represent an important type of slack, a notion that has recently been reinstated as a key theoretical construct (Mount et al., 2024). Consequently, we urge future empirical research to evaluate whether previous findings on the performance implications of other types of slack are robust to changes in method and sample.

Replicating in circles?

Our commentary shows that even individual reproducibility and replication studies (Köhler & Cortina, 2023) are not a panacea and may not necessarily lead to progress in the sense of getting closer to the truth. The constructive replication of Theissen et al. (2023) introduced several advancements over Kim and Bettis (2014). What our reproducibility study shows is that the path to knowledge may not necessarily be linear, and that—since no empirical study is ever perfect—there is invariably a chance that even improvements in some aspects may produce results that can be overturned again once yet additional improvements are introduced. In fact, as in our case, sometimes improvements lead back to the results obtained by much earlier research.

Nevertheless, this is not to say in the least that reproducibility and replication studies should not be performed. On the contrary, they are our best shot at getting to the core of empirical phenomena. It is just that we should probably always do one more.

Supplemental Material

sj-docx-1-msr-10.1177_27550311241308263 - Supplemental material for Coming full circle on cash holdings and firm value: A comment on Kim and Bettis (2014), Theissen et al. (2023), and Souder et al. (2024)

Supplemental material, sj-docx-1-msr-10.1177_27550311241308263 for Coming full circle on cash holdings and firm value: A comment on Kim and Bettis (2014), Theissen et al. (2023), and Souder et al. (2024) by Christopher Jung and Lorenz Graf-Vlachy in Journal of Management Scientific Reports

Footnotes

Acknowledgements

The authors gratefully acknowledge helpful guidance by Maria Kraimer and Bill Schulze, as well as helpful discussions with Maximilian Theissen and David Souder.

Availability of data and material

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.

Consent for publication

Not applicable.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethics approval and consent to participate

Not applicable.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.